Embed Size (px)

Citation preview

Economic Research & Consulting

December 2010

Global insurance review 2010 and outlook 2011/12

1

Table of contents

Executive summary 2

Moderate growth in developed economies, but robust growth in EMs 6

Non‑life insurance: Two difficult years until the market turns 12

Life insurance: The industry has returned to growth 19

Emerging markets: Booming 25

2

Executive summary

The global economic expansion continues and inflation is not an issue in the short and medium-term

The world economy is expected to continue expanding, led by the emerging market countries. The recovery is very robust in Asian emerging markets and Latin America, while Eastern Europe and the Middle East will soon achieve pre‑crisis growth rates.

In the developed economies, growth will accelerate slightly in the course of 2011 and 2012, but remain close to its long‑run averages of 2.5% to 3.0% in the US, 1.5% in Japan, and approximately 2.0% in Europe. Strong business investment and improving consumer spending will support growth in 2011, while construction will provide a further boost in 2012. Growth will not be strong enough to significantly lower the unemployment rate.

Given this outlook, inflation in the industrialised countries is not expected to rise. However, in several emerging market countries, inflation is rising, and in some cases, is close to 10%. This will require more restrictive monetary policy.

In North America and Europe, economic policy is supporting growth, but the support is increasingly confined to monetary policy. Countries with high budget deficits and public debt are reducing their fiscal stimulus.

Policy rates will remain low through end‑2011. Long‑term rates will gradually increase, along with policy rates and economic activity. Many emerging markets countries and some raw material producing countries have already started to adapt their monetary policy to the improved economic situation.

Capital markets have recovered substantially: stock markets and corporate bond valu‑ations in November substantially exceeded their end‑2009 levels. Nevertheless, as‑set prices are still quite volatile. Several emerging markets have seen a boom in share prices. The improvement in capital markets and the narrowing of credit spreads is expected to continue. Rising interest rates are not expected to derail the market re‑covery because they will be largely driven by economic growth.

Financial market turmoil and political instability could derail the recovery

The economy could be derailed by turmoil in the capital markets. Although the recov‑ery is nearly 18 months old and broadening, the trust of consumers business and investors in its continuation is still weak.

Instability in several important real estate markets – eg the US, Ireland and Spain – have the potential to stress the banking sector.

In Europe, the need of Greece and Ireland for support from the IMF and EU has unsettled financial markets.

Low interest rates in developed economies have created a carry trade in emerging markets, which have higher interest rates. This has pushed up exchange rates in many emerging markets.

Political risks are also a factor. The conflicts in the Middle East – eg Iran – remain un‑solved. The recently intensified conflict between North and South Korea is also a risk.

3

Growth has returned to the insurance industry and capital positions have been restored, but there are challenges

Most insurance companies had restored their capital to pre‑crisis levels by end‑2009 and continued to build a larger capital buffer in 2010. This is true for life insurers and non‑life insurers in the developed and developing economies.

Low interest rates and other after-shocks of the financial crisis pose a challenge to the insurance industry

A key challenge is low interest rates, stemming from expansionary monetary policies. Insurers, pension funds and private savers are paying for the cheap financing of governments and for households and corporations that borrow. The result for non‑life insurers is a modest 6‑8% ROE over the next couple years instead of the average 12% in the period 2003‑2007.

Insurers thus face a serious dilemma. Investment yields will be low if they continue – as they have recently and traditionally – to invest substantially in risk free assets. They could deviate from this conservative path, earning higher returns on riskier assets. However, rating agencies and investors might regard this as highly risky, especially with the ongoing market turmoil. Thus, the best strategy to boost profitability is to strive for higher underwriting standards, which implicitly means a rise in rates and tightening of terms and conditions.

Many regional insurers face the issue of falling credit ratings for government bonds in the periphery countries. The bonds of these OECD member countries, which had been viewed as sound investments, are now considered junk bonds. This may lead to the rethinking of the concept of risk‑free asset, which has been an important pillar for insurance assets in most regulatory jurisdictions.

Given the significance of bank bonds as a highly‑rated asset held by insurers, it is important that bank regulation ensures that banks are safe.

There is also a risk of over-regulation in the insurance industry

Another challenge is the European Solvency II regulatory initiative, which will change the way insurers manage their business, mostly for the better. However, it is also likely to impose higher capital requirements for many insurers if the implementing meas‑ures are not aligned with economic based principles. There is a risk that the regulation will be overly‑burdensome.

The situation of the insurance industry is completely different from that of banks, which will have to increase their capital substantially over the next few years to achieve the higher solvency requirements required by Basel III. Unlike the banking sector, the insurance industry came through this crisis largely unscathed. The overly conservative view of regulators on the insurance sector is not justified.

Systemic risk regulation is another area under discussion. The insurance industry does not dispute that insurance should be involved in macro monitoring since it has a huge stake in the orderly operation of financial markets. However the industry opposes systemic risk supervision of insurance groups because core insurance activi‑ties are not a source of systemic risk, so efforts should be dedicated to enhancing comprehensive group supervision. A very critical point, however, is whether the in‑surance supervisors will classify (re)insurers as a potential source of systemic risk and, if so, which (re)insurers may be classified as systemically important financial institutions (SIFIs). The capital and reporting requirements of SIFIs are still being elaborated, but – most likely – they will be higher.

4

All segments of insurance have recovered

In the P&C primary insurance sector, capital has recovered and a hardening of the market is expected as early as 2012

Along with the economic recovery, demand for P&C insurance will also moderately rise in developed economies (about 3% per annum, after‑inflation). Growth will be quite strong in emerging markets (7%‑8% per annum).

Underwriting results have continued to deteriorate in major European markets (mainly driven by the underwriting losses of the motor business) and in the US. Calendar year combined ratios are expected to be between 100% and 103%, even though they are supported by reserve releases of up to 4% of premiums.

Despite lower profitability, there is no general hardening of rates because: (a) there is positive run‑off, (b) the insured (households and businesses) are more price conscious in the current macro environment, (c) the capital base has largely been restored, so there is plenty of capacity in all insurance segments.

Therefore, for 2011, a further deterioration of profitability is expected. The market may turn in 2012, depending on reserve developments, major losses, and the extent of rate declines in 2011.

Non‑life insurance business growth will likely accelerate in 2011/12 due to robust economic growth. Emerging Asia will continue to outperform, thanks to expected strong economic growth in most regional markets. Business growth will also improve in other emerging regions, due to reviving corporate demand and increasing trade and consumption.

Non-life reinsurance is faring better than the primary sector

The reinsurance industry currently is faring better than the primary insurance industry. For FY 2010, a combined ratio of about 96% is expected. Generally, the reinsurance industry still benefits from the hard market years of 2002/3; releases from prior years’ claims reserves are currently improving the underwriting results by two to three percentage points. Thus, the effective combined ratio of the current business is about 98–100%.

Regarding natural catastrophes and man‑made disasters, the 2010 insured losses are close to the long‑term average for the industry – high losses during the first half year were offset by the benign hurricane season. Price levels in this capital intensive segment are still acceptable in many cases, although greater selection is necessary.

This years’ ROE is expected to be at about 10%, on average, for the industry. Growth expectations will be moderate and profitability is expected to erode as rates decline. In this situation, superior underwriting skills are even more important to successfully pick the right segments and risks.

Executive summary

5

L&H primary insurance will be back on track in 2011

The primary life and health industry is recovering, with global premium income up by 4.3% in 2010. New business is also picking up. The industry will be back on track in 2011.

Investment income will depress published L&H profitability, which to a great extent is driven by investment results.

Increased regulatory capital requirements for riskier assets and products with guar‑antees will affect savings and pension products, the main pillar of earnings for the life industry. Insurers are responding by designing new products and re‑pricing guar‑antees embedded in their products.

The capital situation of life insurers has improved, but some companies will need to further strengthen their balance sheets. The improvement was supported by falling interest rates, but some of this improvement may be reversed once interest rates rise again.

Life insurance business in emerging markets staged a strong rebound in 2010, but growth in 2011/12 is expected to revert to the trend pace. In Latin America and East‑ern Europe, premium growth is projected to accelerate steadily. In emerging Asia, life premiums will increase, but at a slower rate than the 22% recorded in 2010.

L&H reinsurance will grow at a moderate pace

Growth in traditional life reinsurance is constrained by the slow growth of premiums for protection products (eg death and disability). In the industrialised countries, growth will stagnate. However, in emerging markets, premiums will rise approximate‑ly 10% annually.

In the industrialised countries, the growth areas are longevity and large block trans‑actions. The latter will be boosted by consolidation, M&A and spin‑offs.

6

Moderate growth in the developed economies, but robust growth in EMs

Macroeconomic environment

GDP is growing at a modest pace in the industrialised countries and rapidly in the emerging markets. In general, the emerging market countries performed well during the financial crisis of 2007‑09, partially due to strong growth in China, which continued to import raw materials and was only minimally affected by the global downturn. Because the economies of these countries have been growing strongly, inflationary pressures are rising.

It is just the opposite in the developed economies, which still have substantial excess labour and productive capacity. The moderate growth of the developed economies is ex‑pected to continue through 2011 and, most likely, into 2012. Inflation and interest rates are expected to remain low. As a consequence, monetary policy will stay highly accomo‑dative through all of next year. In early 2012, the Fed is likely to begin raising the federal funds rate. However, the European Central Bank and the Bank of England could start tightening monetary policy very slowly as early as the third quarter of 2011. Thus, yields on 10‑year government bonds are not expected to rise close to 5.0% until 2013, con‑straining investment yields at insurance companies in the interim.

2009 2010 2011 2012 2013 2014 2015Real GDP growth, US –2.6 2.7 2.8 3.1 3.0 3.0 3.0annual avg., % Euro area –4.0 1.7 1.7 1.9 1.9 1.9 1.9 UK –4.9 1.8 2.0 2.2 2.5 2.5 2.5 Japan –5.2 2.5 1.5 1.5 1.5 1.5 1.5 China 9.1 9.7 8.7 8.3 7.9 7.8 7.7Inflation, US –0.3 1.6 1.5 1.8 2.0 2.0 2.0all‑items CPI, Euro area 0.3 1.6 1.6 2.0 2.0 2.0 2.0annual avg., % UK 2.2 3.1 3.2 2.2 2.0 2.0 2.0 Japan –1.4 –0.8 –0.2 0.5 1.0 1.1 1.3 China –0.7 3.2 3.2 3.3 3.2 3.1 3.0Policy rate, US 0.25 0.25 0.25 3.00 4.25 4.25 4.25year‑end, % Euro area 1.00 1.00 1.50 3.50 3.75 3.75 3.75 UK 0.50 0.50 1.00 3.50 4.75 4.75 4.75 Japan 0.09 0.10 0.50 1.00 1.50 1.50 1.50Yield, US 3.9 2.9 3.8 4.7 5.0 5.0 5.010‑year govt bond, Euro area 3.4 2.7 3.7 4.0 4.2 4.2 4.2year‑end, % UK 4.0 3.3 4.2 4.8 5.0 5.0 5.0 Japan 1.3 1.2 2.0 2.4 3.0 3.0 3.0

Source: Swiss Re Economic Research & Consulting

A percentage point decline in interest rates lowers P&C insurers’ return on equity by about two percentage points (see Figure 1). Property casualty (P&C) insurers have asset leverage of 2 to 3 times assets, so a decline in rates causes a disproportionate decline in profits. For life insurers (L&H), which have higher leverage, lower investment yields are even more problematic. The aggressive monetary policy in the US has lowered yields globally, reducing yields on corporate bonds. Corporate bond yields – the single best indicator of insurers’ investment yield – are about 80 basis points lower than they were at the end of 2009. Thus, investment returns will constrain the insurance sector’s profita‑bility for the next two to three years.

The developed and emerging markets are growing at very different rates.

In the major economies, monetary policy will remain accommodative and yields on government bonds will be low through next year.

Table 1Real GDP growth, inflation and interest rates in selected regions, 2009 to 2015, %

A percentage point decline in interest rates lowers P&C insurers’ ROE by two percentage points.

7

0%

2%

4%

6%

8%

10%

12%

14%

107%105%103%101%99%97%95%

2009 industry assumptions:Asset leverage: 303%Tax rate1 24%NPW/avg. surplus 86%

2009 ROE was 6.3%; total yield was 3.3%, and CR 101.3%.Adjusted for average cat losses and reserves releases, 2009 CR was about 105%

Sources: A.M. Best, estimates by Economic Research & Consulting.1 based on 10-year average.

4.5%

3.3%

2.5%

Combined Ratio

Source: Swiss Re Economic Research & Consulting

A wide range of risks confront the global economy, cumulatively representing a down‑side risk of about 10% that there could be a sharp disruption to the benign outlook of our baseline forecast. First, the Greek and Irish debt situations could spread to larger European economies, such as Spain. If major restructurings occur, many banks in Europe, which hold the sovereign debt of Greece/Ireland/Portugal/Spain, could become insol‑vent, triggering another financial crisis. Second, the fiscal tightening that has begun in Europe could prove to be too much too soon, and lead to low growth, low inflation and low interest rates for the next few years. Third, the fiscal tightening could prove to be too little too late, especially in the US. If confidence in the dollar declines sharply, interest rates could spike, and slow global economic growth. Fourth, employment growth could stall in Europe and the US, again resulting in a low growth scenario. If a combination of factors pushes the US and Europe into recession at this time, deflation is likely. As Alan Blinder, former Fed Vice Chair, once said, “We are one recession away from deflation.” Under these conditions, a Japanese economic malaise could set in – especially given that most monetary options have already been implemented in an attempt to boost growth. However, that scenario is considerably less likely than 10%.

Figure 1The expected ROE for a given combined ratio for investment yields 2.5%, 3.3% and 4.5% for the US P&C industry in 2009

A wide range of risks confront the global economy at this time.

8

Moderate growth in the developed economies, but robust growth in EMs

The consequences of the Fed’s quantitative easing/low interest rate policies

The desire for more robust growth in the US has led the Federal Reserve Board to imple‑ment more quantitative easing. This policy, along with the Fed’s near‑zero target policy rate, will keep the yield on the 10‑year Treasury note low for a prolonged period. Low interest rates will help restore health to the banking sector and will boost purchases of in‑terest‑sensitive goods, such as housing, business equipment, vehicles and other durable goods. In addition, low interest rates in the US will tend to lower the value of the US dollar relative to other currencies. This is not the mandate of the Fed, but it is a side‑effect of a low interest rate policy. Intended or not, a weak dollar also boosts growth because exports rise and imports fall.

These policies, a low target policy rate and quantitative easing, have other consequences. Low interest rates in the US allow investors to borrow in US dollars and invest in assets in emerging markets where yields are higher. These capital flows have several effects: They put upward pressure on the currencies of the recipient country. China is one

exception to this as its currency is carefully managed by the People’s Bank of China (PBoC). The Chinese central bank has allowed a marginal 3% appreciation of the ren‑minbi since removing the de‑facto peg to the US dollar in June 2010. Also, capital cannot easily flow into China because of its capital control policies. Thus, China’s currency is also relatively weak, which puts a lot of pressure on countries which com‑pete against China to export to other countries.

Inflationary pressures are building in many countries, particularly in Asia, because their economies are close to capacity and they are reluctant to raise interest rates because this will appreciate their currencies further. Inflationary pressures could also rise in Latin America if appropriate monetary policies are not adopted. Some coun‑tries in both regions are imposing capital controls to reduce the inflows of capital and avoid a situation like the Asian crisis of 1997, when the “hot money” quickly flowed out of their countries, causing a liquidity crisis for foreign debt payments.

Many European economies are also unhappy with the policy, particularly if their cur‑rencies are appreciating. However, inflation is unlikely in Europe due to excess labour and productive capacity. The Europeans will instead be at a competitive disadvantage to the US.

Quantitative easing also has additional consequences. Households dependent upon in‑terest income, mostly retirees, will have reduced income if interest rates remain low. In addition, pension plans and insurance companies will also suffer because they depend on investment income to sustain payments to pensioners and policyholders.

Ultimately, the capital flows could fuel an asset bubble, but this is unlikely in the short term. Until the Fed moves to a policy of higher interest rates — which is only likely after growth picks up in the US — currency tensions will continue.

The US Fed has recently decided to purchase more Treasury notes and bills.

Their actions have implications for exchange rates and could lead to inflation.

Some segments – retirees, pension plans and insurers – are harmed by low interest rates.

An asset bubble may form in future years due to capital inflows.

9

0

50

100

150

200

250

300

350

400

450

500

World

Eastern Europe

Latin America

Emerging Asia

Emerging Markets (EM)

20102009200820072006200520042003200220012000

Stock Market Indices (MSCI) January 2000 = 100

Source: MSCI

How emerging markets react to these concerns will hinge on local economic and finan‑cial conditions. For markets that are firmly entrenched on a high growth trajectory and which could overheat, a stronger local currency, combined with monetary and fiscal tightening, is likely to be accepted, thus helping to control inflation. A key consideration is the extent to which China will allow the renminbi to appreciate. Still other markets are ac‑tively considering some forms of capital controls to better manage capital flows. These could take the form of: 1) taxes/limits on short‑term external borrowing; 2) pre‑approvals for foreign portfolio/direct investments; and 3) restrictions on repatriation.

Rather than attempt to cover all possible future scenarios, this section will explore two specific scenarios that would have a significant impact on insurers – the low growth‑low inflation‑low interest‑rate scenario and a scenario in which interest rates rise rapidly, eg 200 basis points, over the next year.

The low growth, low inflation and low interest rate scenario could materialise in a number of ways. First, another recession could push the US and European economies into defla‑tion. From there, monetary policy is less effective and, given large deficits, fiscal policy maneuverability may be limited. Second, the developed economies may simply slow down substantially once inventories have been restored. A return to deflation in the hous‑ing sector would abort any residential building boom, taking away a possible engine of growth, particulary in the US. Third, the lingering effects of the banking crisis could re‑strain credit sufficiently and slow growth to an anemic pace. This would continue to put pressure on prices, keeping inflation and interest rates low. This scenario present prob‑lems for both P&C and L&H insurers. First, investment yields would remain very low. Second, L&H insurers would lose money on products that depend on investment spreads to be profitable, eg interest rate guarantee products. On the positive side, P&C insurers would benefit in their casualty lines from prior year pricing that assumed higher inflation.

Figure 2Equity market performance

Tighter monetary and fiscal policies and appreciated currencies are likely to be used to contain inflation.

Two scenarios will be explored – low growth and an interest rate spike.

Scenario 1: Low growth, low inflation and low interest rates.

10

Moderate growth in the developed economies, but robust growth in EMs

It is also possible that rates rise sharply next year and stay elevated at about 2 percentage points higher. This could occur if inflation and inflationary expectations spike, although this is not likely given the current excess labor and production capacity. This would push up nominal interest rate yields, reducing the value of bonds.

Interest rates could also rise sharply if the global economy is exceptionally more robust next year, as interest rates embody both a real growth and an inflation expectation com‑ponent. Unanticipated growth would also push up yields. A sharp spike in interest rates can have a dramatic impact on insurers’ balance sheets in the short‑run. Under GAAP accounting, the assets would be reduced in value by mark‑to‑market accounting, but there would be no offsetting reduction in liabilities through discounting. The shift could reduce global equity surplus by hundreds of billions of dollars, and potentially trigger a hardening of the market. Nevertheless, in the longer‑term, higher interest rates are bene‑ficial to the insurance industry because investment yields improve.

Economic development in emerging markets, 2010

Emerging economies as a whole weathered the global financial crisis better than the industrialised countries, although with tangible regional disparities. Growth of most emerging regions accelerated in 2010 due to vibrant domestic demand and strengthen‑ing external trade. In particular, emerging Asia has performed well in 2010 (real GDP +8.9%), not only due to the persistent strong performance of China and India, but also accelerated growth in other regional markets. In Latin America (2010: +5.0%), most markets have recovered from the 2009 recession to report modest growth. The Middle East (2010: +5.4%) also staged a convincing rebound. In comparison, the recovery of Central and Eastern Europe (2010: +2.9%) has been more modest because of its de‑pendence on Western Europe and their own fiscal problems.

USD billion

0

5 000

10 000

15 000

20 000

25 000

Central & Eastern EuropeAfrica

Latin America

Middle East

Emerging Asia

20102009200820072006200520042003200220012000

0%

2%

4%

6%

8%

10%

Real GDP growth (all emerging markets)

Real GDP growth

Sources: Oxford Economic Forecasting, Swiss Re Economic Research & Consulting

With solid economic growth in key emerging countries, large capital inflows and robust commodity demand, concerns about accelerating inflationary pressure have resurfaced. Some countries are currently implementing exit strategies from highly expansionary monetary policies to mitigate the risk of inflation. Fiscal consolidation is also rapidly becoming a policy priority in emerging markets, mainly due to increased scrutiny from investors as a result of the sovereign debt crisis in Europe.

Scenario 2: Interest rates rise abruptly by two percentage points.

Current status of emerging markets.

Figure 3GDP by region and emerging markets real growth rate

Monetary policy is now tightening in many countries.

11

The end of the renminbi’s de facto peg to the US dollar

In June 2010, China announced the end of the “crisis‑mode” policy of pegging the ren‑minbi (CNY) to the US dollar. The statement from the People’s Bank of China (PBoC) and subsequent clarifications made it clear that China will not do another one‑off renminbi revaluation against the dollar and that the pace of renminbi appreciation will be very modest. The PBoC is expected to manage the trading range with reference to a basket of currencies of major trading partners, including the US dollar, the euro (EUR), Japanese yen (JPY) and possibly the South Korean won (KRW). Nevertheless, the key currency in the peg is clearly the dollar (the renminbi hardly moves at all when the euro moves against the USD). The CNY/USD spot appreciated 0.56% against the dollar in the first week of the de‑peg and reached around 3% by November. Accelerating inflation and high property prices have prompted policymakers to review their “appropriately accom‑modative” monetary stance. Allowing the currency to appreciate is a de facto monetary tightening. Also, in mid‑October, the central bank temporarily raised the reserve require‑ment ratio of banks by 0.5 percentage points. It further hiked interest rates in later Octo‑ber to signal its concern about excessive loan growth.

Emerging market economic outlook

The outlook for emerging markets in 2011 remains favourable. Supportive government policies, improving labour market conditions and rising consumer sentiment are expected to boost domestic demand in the near term. External trade will also benefit from the rising consumption demand in emerging markets, offsetting sluggish growth in mature economies. Most emerging market currencies are expected to appreciate further in 2011, which will shift the relative competitiveness in favour of the US and China. The near‑term impact of this is, however, not expected to be significant. Some emerging mar‑kets are poised to withdraw fiscal stimulus introduced during the global financial crisis. Given the current robust economic fundamentals, the drive towards fiscal consolidation is not expected to be a significant drag on growth.

Inflation is fast becoming a key concern of policymakers in emerging markets. While most markets are still managing to keep inflation within government targets, the recent acceleration in food and commodity prices is likely to push inflation beyond those targets in the coming months. CPI inflation in China, for example, reached 4.4% in October 2010, much higher than the government’s implicit target of 3%. Inflation will likely rise faster in those emerging markets that are growing at or above trend levels, mainly in the Asia‑Pacific region and the Middle East. Central banks in those markets are likely to react by hiking interest rates and/or allowing faster appreciation of their currencies.

Between 2011 and 2021, the global economy is projected to expand by an annual aver‑age of 3.8%. Emerging markets as a group are projected to continue to grow twice as fast as industrialised economies (5.9% versus 2.4%). Thus, the growth contribution from industrialised countries will decline, especially over the next few years due to their slow recovery from the financial crisis. By 2020, two of the world’s five largest economies will be in emerging Asia. India’s accelerating growth momentum will push its ranking up dramatically from 12th in 2009 to 5th by 2010. While China will remain the second largest economy throughout the next decade, its economy is expected to grow to around two‑thirds of the US by 2020, compared to one‑third in 2009.

The appreciation of the renminbi will be gradual and modest.

Emerging markets will grow rapidly next year.

Inflation pressures are rising in many emerging markets.

In the longer term, emerging markets will grow more than twice as fast as the industrialised economies.

12

Non‑life insurance: Two difficult years until the market turns

The non-life insurance industry returns to growth in 2010

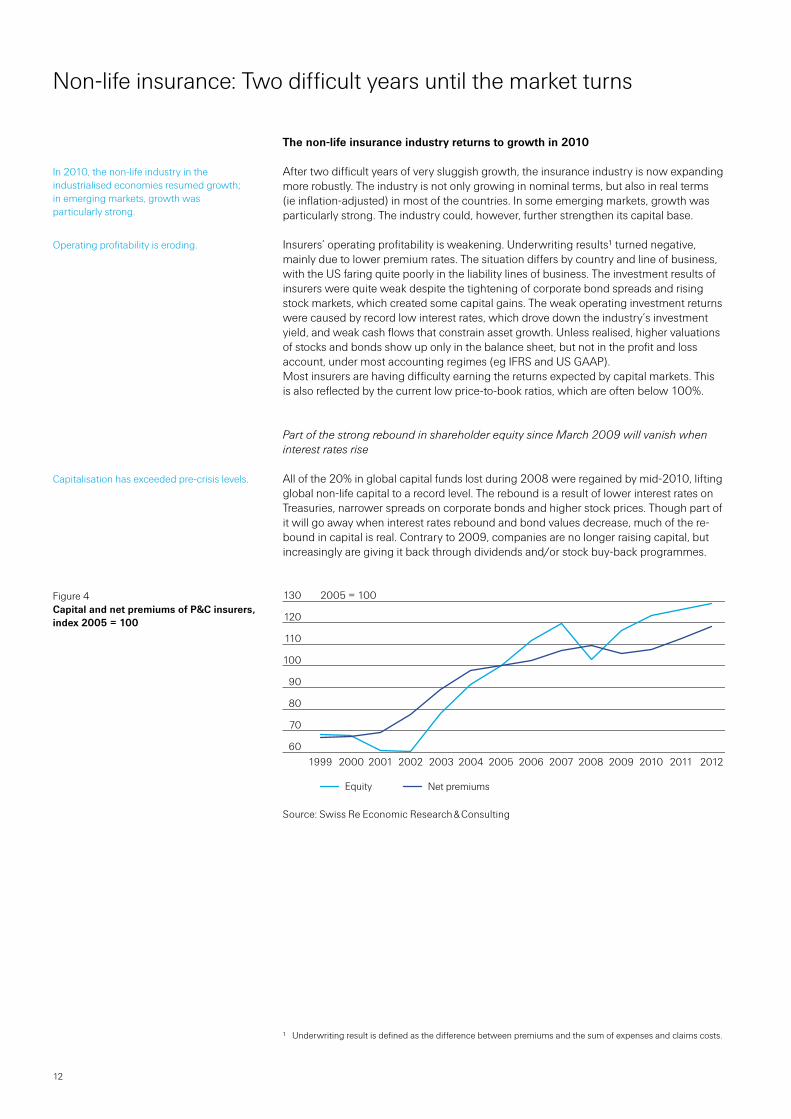

After two difficult years of very sluggish growth, the insurance industry is now expanding more robustly. The industry is not only growing in nominal terms, but also in real terms (ie inflation‑adjusted) in most of the countries. In some emerging markets, growth was particularly strong. The industry could, however, further strengthen its capital base.

Insurers’ operating profitability is weakening. Underwriting results1 turned negative, mainly due to lower premium rates. The situation differs by country and line of business, with the US faring quite poorly in the liability lines of business. The investment results of insurers were quite weak despite the tightening of corporate bond spreads and rising stock markets, which created some capital gains. The weak operating investment returns were caused by record low interest rates, which drove down the industry’s investment yield, and weak cash flows that constrain asset growth. Unless realised, higher valuations of stocks and bonds show up only in the balance sheet, but not in the profit and loss account, under most accounting regimes (eg IFRS and US GAAP).Most insurers are having difficulty earning the returns expected by capital markets. This is also reflected by the current low price‑to‑book ratios, which are often below 100%.

Part of the strong rebound in shareholder equity since March 2009 will vanish when interest rates rise

All of the 20% in global capital funds lost during 2008 were regained by mid‑2010, lifting global non‑life capital to a record level. The rebound is a result of lower interest rates on Treasuries, narrower spreads on corporate bonds and higher stock prices. Though part of it will go away when interest rates rebound and bond values decrease, much of the re‑bound in capital is real. Contrary to 2009, companies are no longer raising capital, but increasingly are giving it back through dividends and/or stock buy‑back programmes.

60

70

80

90

100

110

120

130

Equity Net premiums

20122011201020092008200720062005200420032002200120001999

2005 = 100

Source: Swiss Re Economic Research & Consulting

1 Underwriting result is defined as the difference between premiums and the sum of expenses and claims costs.

In 2010, the non‑life industry in the industrialised economies resumed growth; in emerging markets, growth was particularly strong.

Operating profitability is eroding.

Capitalisation has exceeded pre‑crisis levels.

Figure 4Capital and net premiums of P&C insurers, index 2005 = 100

13

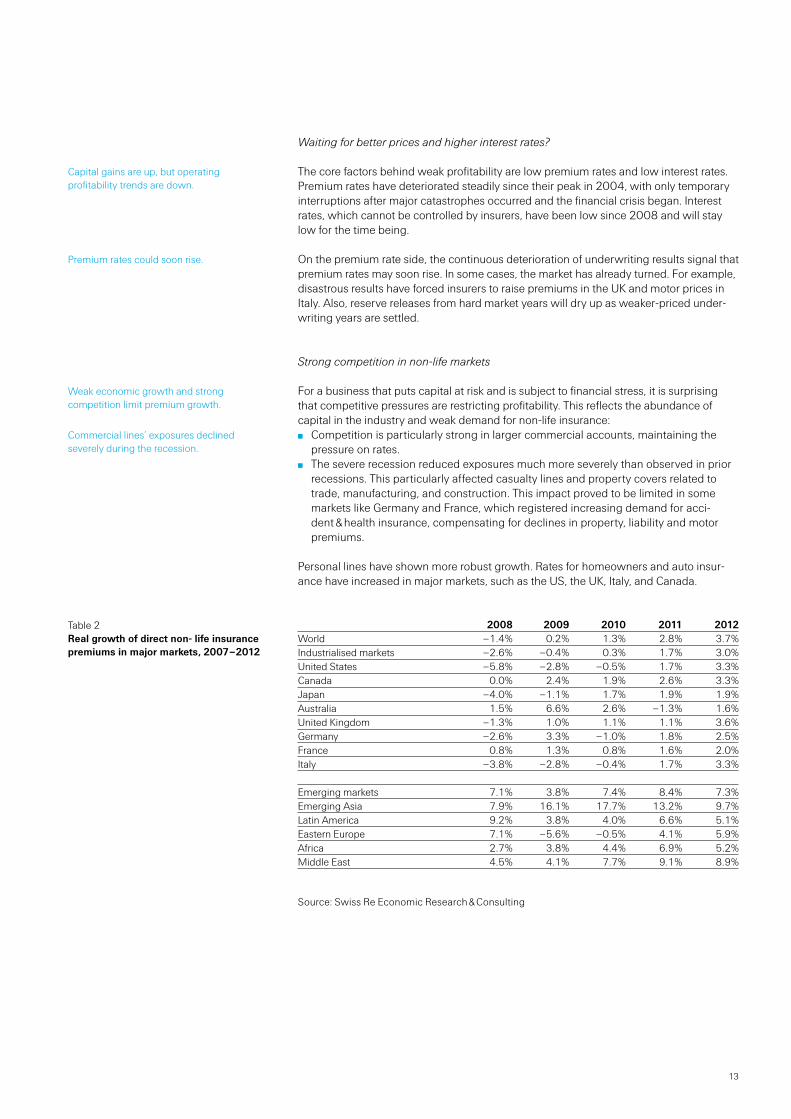

Waiting for better prices and higher interest rates?

The core factors behind weak profitability are low premium rates and low interest rates. Premium rates have deteriorated steadily since their peak in 2004, with only temporary interruptions after major catastrophes occurred and the financial crisis began. Interest rates, which cannot be controlled by insurers, have been low since 2008 and will stay low for the time being.

On the premium rate side, the continuous deterioration of underwriting results signal that premium rates may soon rise. In some cases, the market has already turned. For example, disastrous results have forced insurers to raise premiums in the UK and motor prices in Italy. Also, reserve releases from hard market years will dry up as weaker‑priced under‑writing years are settled.

Strong competition in non-life markets

For a business that puts capital at risk and is subject to financial stress, it is surprising that competitive pressures are restricting profitability. This reflects the abundance of capital in the industry and weak demand for non‑life insurance: Competition is particularly strong in larger commercial accounts, maintaining the

pressure on rates. The severe recession reduced exposures much more severely than observed in prior

recessions. This particularly affected casualty lines and property covers related to trade, manufacturing, and construction. This impact proved to be limited in some markets like Germany and France, which registered increasing demand for acci‑dent & health insurance, compensating for declines in property, liability and motor premiums.

Personal lines have shown more robust growth. Rates for homeowners and auto insur‑ance have increased in major markets, such as the US, the UK, Italy, and Canada.

2008 2009 2010 2011 2012World –1.4% 0.2% 1.3% 2.8% 3.7%Industrialised markets –2.6% –0.4% 0.3% 1.7% 3.0%United States –5.8% –2.8% –0.5% 1.7% 3.3%Canada 0.0% 2.4% 1.9% 2.6% 3.3%Japan –4.0% –1.1% 1.7% 1.9% 1.9%Australia 1.5% 6.6% 2.6% –1.3% 1.6%United Kingdom –1.3% 1.0% 1.1% 1.1% 3.6%Germany –2.6% 3.3% –1.0% 1.8% 2.5%France 0.8% 1.3% 0.8% 1.6% 2.0%Italy –3.8% –2.8% –0.4% 1.7% 3.3%

Emerging markets 7.1% 3.8% 7.4% 8.4% 7.3%Emerging Asia 7.9% 16.1% 17.7% 13.2% 9.7%Latin America 9.2% 3.8% 4.0% 6.6% 5.1%Eastern Europe 7.1% –5.6% –0.5% 4.1% 5.9%Africa 2.7% 3.8% 4.4% 6.9% 5.2%Middle East 4.5% 4.1% 7.7% 9.1% 8.9%

Source: Swiss Re Economic Research & Consulting

Capital gains are up, but operating profitability trends are down.

Premium rates could soon rise.

Weak economic growth and strong competition limit premium growth.

Commercial lines’ exposures declined severely during the recession.

Table 2Real growth of direct non- life insurance premiums in major markets, 2007–2012

14

Non-life insurance: Two difficult years until the market turns

Deteriorating underwriting results show the need for premium rate corrections

The underwriting results in most of the major markets deteriorated further in 2010. The average combined ratio of the G8 markets was 102% in 2010, up from 101% in 2009 and 95% in 2006.

However, profitability in the calendar‑year results for 2009 and 2010 were supported by significant reserves releases. In the US, reserve releases reduced the combined ratio by 4.2 percentage points in 1H2010 and by 2.5 points in 2009. Reserve releases were in a similar range for the large European insurers. The average improvement of the loss ratio in 1H10 was 4.2 points, marginally up from 3.9 points in 1H09.

Points of combined ratio 2007 2008 2009 1H 2010Headline figure, based on calendar year 95.4 104.0 101.3 101.9of which effective cat losses (–) 1.5 6.3 3.4 5.3normal cat losses (+) 4.0 4.0 4.0 4.0Cat adjusted combined ratio 97.9 101.7 101.9 100.6A&E reserves additions (–) 0.4 0.4 0.4 0.4Core reserves releases (+) 1.7 2.2 2.9 4.6Adjusted AY combined ratio 99.2 103.5 104.4 104.8

Sources: A.M. Best, Swiss Re Economic Research & Consulting

Underwriting profitability has deteriorated more in the US than in Europe. Adjusted for average cat losses and reserves releases, the overall combined ratio was about 105% in 1H 2010, about 106% for commercial lines and 104% for personal lines.

In the largest European markets, the underwriting results turned negative. While the largest European markets unanimously suffer from the current dismal performance of the motor business, some markets like the UK and Italy have already registered significant rate improvements this year, which should lead to future improvements in the underwrit‑ing results. Germany and France are expected to follow next year.

Unlike the motor business, other personal lines in Europe usually provide stable and risk‑adequate earnings for non‑life insurers. Also, the commercial insurance segment has generated stable and positive results in Europe, particularly in commercial property, although this line’s profitability has eroded over time. So far in 2010, liability insurance results have been mixed: it was profitable and stable in Germany and improved in France, but deteriorated significantly in Italy and the UK.

Underwriting results are deteriorating.

Reserves releases have improved the reported underwriting results.

Table 3Adjusted US combined ratio, % of net premiums

The motor business is performing poorly in many European markets.

Commercial property performed better, but profitability is deteriorating.

15

Investment results have been supported by one-time effects – overall profitability remains poor

Falling interest rates and, to a lesser extent, spread compression in corporate bonds and asset backed securities (ABS) created substantial realised capital gains, turning the capi‑tal losses of 2009 into capital gains in the first and third quarters of 2010.

Contributions of investment returns to the operating result are expected to have increased from 9.6% of NPE in 2009 to close to 10.9% of NPE in 2010, remaining substantially be‑low the average of 12.5% that was achieved between 1999 and 2009. Operating results and overall profitability improved compared to last year, but remain far below pre‑crisis levels. The ROE remains flat at 6%, falling short of the industry’s cost of capital for the third year in a row.

Outlook 2011/12: Heading for higher growth in 2011 and 2012, but an improvement in profitability requires higher interest and premium rates

The industry is heading for higher growth in 2011 and 2012, but expectations should not be set too high. Growth will be supported by demand for cover as the economy continues to grow. In terms of pricing, the signals are mixed. A broader and stronger turn in the in‑surance pricing is expected for 2012, setting the stage for strong growth and improving profitability.

Motor insurance is expected to drive premium growth. The commercial lines business will continue to be sluggish: increasing demand due to the economic recovery will be eroded by a further softening of rates. In emerging markets, strong economic activity will support solid premium growth.

Underwriting profitability will only react with a lag to price improvements. Therefore, it is likely to deteriorate further in most of the markets and segments in 2011. Casualty rates in the US and Europe will also continue to erode and property rates may soften in regions and markets that avoided large losses in 2009 and 2010.

It is not easy to forecast when prices will turn on a broader scale, but the following are important factors that will eventually turn the market: Reserving may soon prove to be insufficient. It is difficult to estimate this effect and a

wide range exists between individual companies. Reserve releases of previous years will eventually result in the need to strengthen reserves. When this sets in, it will no longer be possible to ignore insufficient pricing and the scene will be set for a hard‑ening of rates.

The expected rise of interest rates (see macro‑economic outlook) may turn out to be another trigger. It will reduce the value of the bond portfolio and shareholders’ equity under GAAP accounting. This could easily amount to 10% of the capital base.2 While this is an accounting ‑ not a real economic ‑ issue, insurers will feel pressure from fi‑nancial analysts to improve profitability.

Last, but not least, stricter solvency regulations and higher capital requirements ex‑pected by rating agencies will help turn the market. Solvency II is still on track to be implemented. As far as rating agencies are concerned, further tightening of their models is expected.

2 Under statutory accounting where asset values are not market‑to‑market, this effect will be significantly lower.

Current investment yields are low.

The ROE remains flat at 6%.

Challenges will persist through 2011; but conditions will improve in 2012.

Premium growth will slowly accelerate in mature markets.

Underwriting profitability is continuing to erode.

Current levels of capitalisation are unlikely to be sustainable.

16

Non-life insurance: Two difficult years until the market turns

Thus, by 2012, the underwriting cycle could turn toward a general hardening if profits deteriorate in 2011, adverse reserve developments occur and mark‑to‑market asset values decline due to rising interest rates.

Declining underwriting results will be partially offset by improving investment results as interest rates rise in 2011 and 2012. Overall, investment results will improve, but will not reach the pre‑crisis levels any time soon. As a result, overall profitability will remain sub‑dued for the next two years.

–15

–10

–5

0

5

10

15

20

Investment result

Underwriting result

20122011201020092008200720062005200420032002200120001999

ROE after tax

Operating result

Source: Swiss Re Economic Research & Consulting

Non-life reinsurance

The reinsurance industry faces many of the same challenges that primary insurers face: weak profitability from low‑yielding investments, reduced premium income, abundant capacity competing for depressed exposure in many lines of business, and high econom‑ic and regulatory uncertainty. Competition remains fierce, particularly in segments and regions that are perceived to diversify risk, such as agro business and the Middle East. Global reinsurance capacity also recovered quickly from the trough of the financial crisis and is at a record level. Reinsurance capital growth outpaced the growth in cedants’ demand.

Growth is also returning to non-life reinsurance

The July 2010 renewals confirmed the trend from the January and April renewals: rein‑surance rates continued a gradual decline across virtually all lines of business and territo‑ries. The high natural catastrophe losses of the first quarter and also the Deepwater Horizon disaster have not triggered an overall turn of the cycle. There were selective rate increases, but these were restricted to loss‑affected market segments, such as Chile property risks and deepwater drilling risks.

Preliminary estimates for premium growth suggest a slight increase of 1% in real terms in 2010. While premiums in industrialised countries probably declined slightly, emerging markets continued to grow. Most of the growth in emerging markets, however, is due to the soaring Chinese insurance market.

A broad hardening of the market is expected by 2012.

Investment results will gradually improve as interest rates rise.

Figure 5Profitability of the 8 major primary markets, 1999-2012

Global reinsurers achieved record capitalisation levels in 2010.

Rates continue to soften despite some major cat losses.

Premium growth was weak in 2010.

17

Underwriting profitability will worsen before it gets better

The industry’s average combined ratio for the nine months through September was 96%, up from 87% in 2009, and slightly up from 94% in 2008 (the year of Hurricane Ike). The good news is that underwriting results were still positive; the bad news is that they con‑tinued to deteriorate.

Reinsurers’ combined ratios suffered from above‑average claims from natural catastrophes mainly due to extraordinarily high losses in the first quarter (eg the Chilean earthquake). Additionally, rates are generally deteriorating.

According to preliminary estimates from Swiss Re, insured losses due to catastrophic events will be close to the 20‑year average.3 High earthquake losses (eg Chile, New Zealand) were offset by unusually modest US hurricane losses. Eight events triggered insurance losses in excess of USD 1 billion. The costliest event in 2010 was the earth‑quake in Chile in February, which cost the insurance industry USD 8 billion, according to preliminary estimates. The earthquake that struck New Zealand in September cost insur‑ers roughly USD 2.7 billion, while winter storm Xynthia in Western Europe led to insured losses of USD 2.8 billion. Property claims from the BP Deepwater Horizon explosion in the Gulf of Mexico are estimated at USD 1 billion. Given the complexity of the claim, this latter estimate is still subject to substantial revision.

Reinsurance rates have generally been softening since the last hard market in 2002/3. This downward trend was slowed by the financial crisis of 2009. The only segment where rates increased was the property cat business in the US, which was underpriced pre‑Katrina. Nevertheless, the underwriting profitability of reinsurance markets held up better than many primary markets.

The industry currently benefits from the hard market years of 2002/3 and the more benign claims trends during the recession. Releases from prior years’ loss reserves are currently helping to improve the underwriting results by two to three percentage points. This will lead to an effective combined ratio of about 98‑100% for 2010.

Investment returns and overall returns – significantly supported by realised capital gains

Reinsurers’ investment returns profited strongly from rebounding capital markets. While current investment yields declined further due to low interest rates, the industry had cap‑ital gains from improving capital markets in the first and third quarter. Reinsurers profit more from improving asset values than primary non‑life insurers due to their higher asset leverage.

Overall, the industry’s average return on equity (ROE) remained at a significantly higher level than the ROE of primary insurers. With an average ROE of 11% for 9M 2010, rein‑surers achieved a solid result for 2010, down from 13% in 2009. However, this was sig‑nificantly up from 2% in 2008 and stronger than the average mature primary market.

3 See press release on Swiss Re’s catastrophe estimates

Combined ratios are trending up.

Cat losses this year were up from 2009, but in line with long‑term averages.

Reinsurance rates have been softening since 2004.

Reserve releases from the hard market years are supporting profitability.

Capital gains are up, while operating profitability is falling.

ROE was 11% in 2010, down from 13% in 2009.

18

Non-life insurance: Two difficult years until the market turns

Outlook 2011/12: More growth and better profitability – broader price increases in 2012?

Premium income, which largely follows the premiums in the primary insurance sector, will be subdued due to the weak growth in industrialised markets. The increasing reinsur‑ance demand in emerging markets, on the other hand, will boost growth for the global reinsurers.

The expected recovery of the global economy will drive an acceleration of exposure growth that will support premium growth. Pricing signals from this year’s reinsurance/ insurance industry conventions in Monte Carlo and Baden‑Baden indicate that the 2011 renewals will be soft to stable at best. Hardening will be limited to lines and segments that have recently experienced high losses.

The reinsurance industry needs to prepare for declining underwriting profitability in 2011. Assuming average catastrophe losses, the combined ratio is expected to approach 100% next year, compared to an average of 90% for the period 2006‑2010. Because of the low interest rate environment in industrialised countries, the overall profitability outlook is eroding. For the reinsurance industry, an average ROE of 8% can be expected.

The outlook for 2012 is more optimistic. With an improving macro‑economic environ‑ment – growth is expected to normalise, pushing interest rates up – reinsurance premium income growth and investment performance will improve. However, the most critical factor will be the turning of the underwriting cycle. Many of the factors that can harden markets will have intensified by the end of 2011, making a change in market sentiment more likely.

Growth will be subdued in mature markets, but strong in emerging markets.

Exposures will outgrow premiums as rates continue to soften.

The average combined ratio is expected to be around 100% in 2011.

Prospects for 2012 look brighter.

19

Life insurance: The industry has returned to growth

Life insurance is growing again

The life insurance industry has returned to positive growth. New business recovered robustly in many countries and global premium income grew by 4.4% in real terms in 2010. In industrialised countries, premium growth was moderate at 2.7%. In emerging markets, premium growth surged 16.7%.

The capital situation has improved substantially, though some of this is due to account-ing methods

The capital situation of the industry has improved substantially, reaching the pre‑crisis level at the end of 2010. The recovery of the stock markets and corporate bond markets, both severely hit in the crisis, contributed significantly to the improved capital situation. A sharp rise in value of government bonds – due to the decline in risk free rates to record low levels in 2010 – also helped improved the capital base of the industry. Insurers also raised capital and, in some cases, lowered dividend payments.

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

Market cap weighted primary

2 Chinese companies

7 European globals

14 US companies

7 UK & Irish companies

3 Canadian companies

2010

Q2

2010

Q1

200

9Q

4

200

9Q

3

200

9Q

2

200

9Q

1

200

8Q

4

200

8Q

3

200

8Q

2

200

8Q

1

2007

Q4

Notes: 1) Missing Q1/Q3 values are interpolated2) AFLAC; Allianz; Assurant Inc; Aviva; AXA; CNP; China Life; Delphi Financial; Generali;

Genworth Financial; Great‑West Lifeco; Hartford; Irish Life & Permanent; Legal & General; Lincoln National; Manulife; Metlife Group; Old Mutual; Phoenix Companies; Ping An; Principal Financial Group; Protective Life; Prudential (UK); Prudential (US); StanCorp Financial Group; Standard Life; St. James Place; Storebrand ASA; Sun Life; Swiss Life; Torchmark; UNUM Group; Zurich FS

Sources: Company reports, Bloomberg, Swiss Re Economic Research & Consulting

While accounting figures in the chart show that capital has reached pre‑crisis levels, some of it is due to accounting issues. The positive interest rate effect on shareholder capital did not have a corresponding negative impact on liabilities because accounting does not adjust liabilities for interest rate movements, whereas assets are mark‑to‑market. When interest rates rise, this capital will disappear.

Nevertheless, the capital situation of life insurers has been considerably improved, even after correcting for accounting issues.

In 2010, primary L&H insurance continued to recover. Inflation‑adjusted premiums grew by 4.4%.

A number of factors have improved the capital situation of the life industry.

Figure 6Shareholders’ equity of 33 mainly life and global companies (IFRS/GAAP data), 2007Q4 =1

As in non‑life, accounting issues in life caused part of the capital improvement.

20

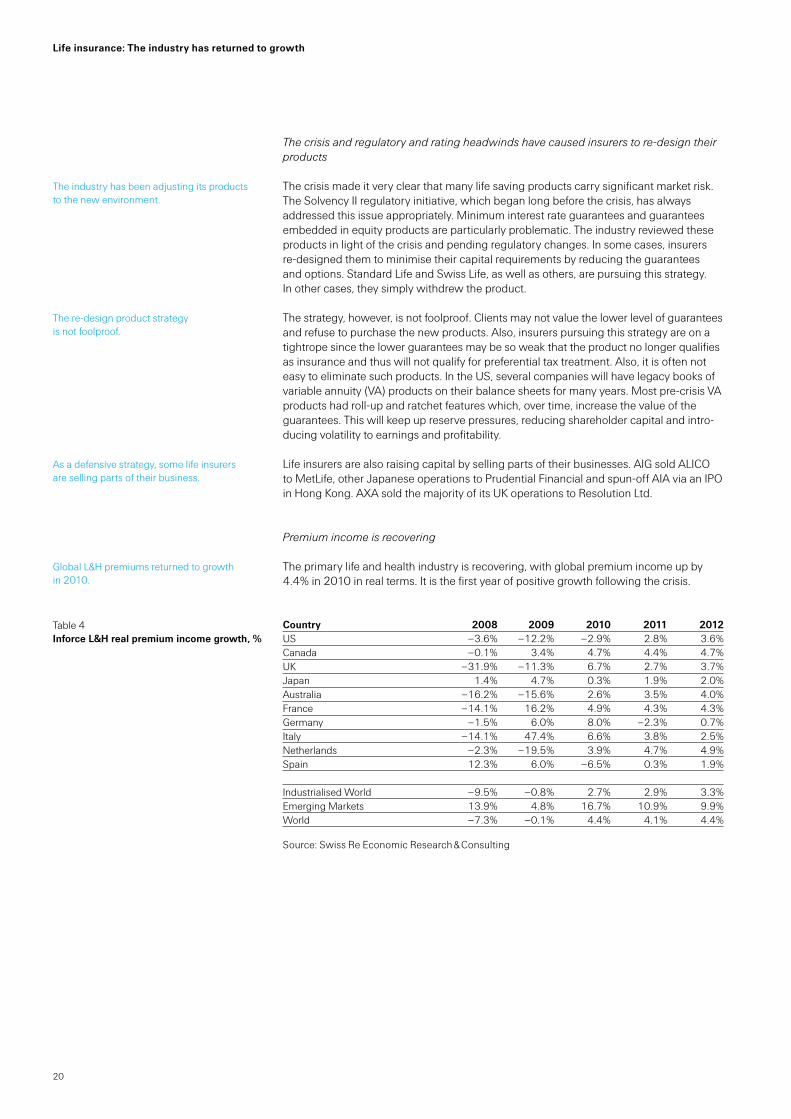

The crisis and regulatory and rating headwinds have caused insurers to re-design their products

The crisis made it very clear that many life saving products carry significant market risk. The Solvency II regulatory initiative, which began long before the crisis, has always addressed this issue appropriately. Minimum interest rate guarantees and guarantees embedded in equity products are particularly problematic. The industry reviewed these products in light of the crisis and pending regulatory changes. In some cases, insurers re‑designed them to minimise their capital requirements by reducing the guarantees and options. Standard Life and Swiss Life, as well as others, are pursuing this strategy. In other cases, they simply withdrew the product.

The strategy, however, is not foolproof. Clients may not value the lower level of guarantees and refuse to purchase the new products. Also, insurers pursuing this strategy are on a tightrope since the lower guarantees may be so weak that the product no longer qualifies as insurance and thus will not qualify for preferential tax treatment. Also, it is often not easy to eliminate such products. In the US, several companies will have legacy books of variable annuity (VA) products on their balance sheets for many years. Most pre‑crisis VA products had roll‑up and ratchet features which, over time, increase the value of the guarantees. This will keep up reserve pressures, reducing shareholder capital and intro‑ducing volatility to earnings and profitability.

Life insurers are also raising capital by selling parts of their businesses. AIG sold ALICO to MetLife, other Japanese operations to Prudential Financial and spun‑off AIA via an IPO in Hong Kong. AXA sold the majority of its UK operations to Resolution Ltd.

Premium income is recovering

The primary life and health industry is recovering, with global premium income up by 4.4% in 2010 in real terms. It is the first year of positive growth following the crisis.

Country 2008 2009 2010 2011 2012US –3.6% –12.2% –2.9% 2.8% 3.6%Canada –0.1% 3.4% 4.7% 4.4% 4.7%UK –31.9% –11.3% 6.7% 2.7% 3.7%Japan 1.4% 4.7% 0.3% 1.9% 2.0%Australia –16.2% –15.6% 2.6% 3.5% 4.0%France –14.1% 16.2% 4.9% 4.3% 4.3%Germany –1.5% 6.0% 8.0% –2.3% 0.7%Italy –14.1% 47.4% 6.6% 3.8% 2.5%Netherlands –2.3% –19.5% 3.9% 4.7% 4.9%Spain 12.3% 6.0% –6.5% 0.3% 1.9%

Industrialised World –9.5% –0.8% 2.7% 2.9% 3.3%Emerging Markets 13.9% 4.8% 16.7% 10.9% 9.9%World –7.3% –0.1% 4.4% 4.1% 4.4%

Source: Swiss Re Economic Research & Consulting

The industry has been adjusting its products to the new environment.

The re‑design product strategy is not foolproof.

As a defensive strategy, some life insurers are selling parts of their business.

Global L&H premiums returned to growth in 2010.

Table 4Inforce L&H real premium income growth, %

Life insurance: The industry has returned to growth

21

New business recovered robustly in many countries in 2010. Major exceptions are the US and Australia. In the US, 2010 sales are expected to decline for a third consecutive year by 7.7% in real terms. In 2008 and 2009, sales fell 4.1% and 15.1% respectively. The decline in 2010 was driven mainly by weak annuity sales since fixed annuities have fallen sharply due to low interest rates. Variable annuities are recovering, but only at a moderate pace.

In other major markets, new business is picking up again or remains strong. In Italy and Germany, where growth has been very high throughout the crisis, growth to some degree stems from single premium deposit‑type insurance contracts that allow policyholders to withdraw money at low or no cost. This money will likely be shifted to banks as soon as they offer attractive returns again. New business growth is likely to slow in these markets unless there is compensating growth in unit‑linked products.

Sales of protection products held up relatively well during the crisis. In 2010, however, term sales are expected to decline in the main markets. In the US, term sales are expected to be down 10% in 2010, partly reflecting price increases and fewer product offerings as well as the economic downturn. In markets like the UK and Ireland, sales continue to be subdued as a result of the weak housing market. By contrast, Canada and Italy, where sales are less dependent on mortgages, posted double‑digit growth.

Country 2008 2009 2010US –4.1% –15.1% –7.7%UK –20.4% –28.9% 4.4%Japan 2.8% 12.0% 5.6%Australia –17.9% –17.8% –10.0%Germany 1.9% 32.7% 25.9%Italy –16.9% 44.3% 13.9%

Sample* –7.9% –4.8% 2.0%

* Inforce premium weighted average of new business growth rates

Source: Swiss Re Economic Research & Consulting

Improving profitability is very difficult in the low interest rate environment

In major markets, net flows (premium income minus claims, benefits and surrenders) improved in 2009 and 2010. This increased assets under management, which supports liquidity and earnings. In addition, it built trust in the L&H industry and improved the in‑dustry’s value proposition.

The operating margins of life companies recovered in the second half of 2009, largely due to the improvement in financial markets and cost containment initiatives. In 2010, however, profitability has stabilised at a level well below the pre‑crisis level.

New business recovered robustly in many countries, but not in the US and Australia.

New business growth is likely to slow in markets where policyholders are simply seeking higher yields than those currently offered by banks.

Sales growth of protection products was mixed in 2010.

Table 5New business real growth

Net flows improved in 2009 and 2010.

Operating profitability has improved, but is still well below the pre‑crisis level.

22

Life insurance: The industry has returned to growth

–10

–5

0

5

10

15

20

25

Market cap weighted primary

2 Chinese companies

7 European globals

15 US companies

7 UK & Irish companies

3 Canadian companies

2010

Q2

2010

Q1

200

9Q

4

200

9Q

3

200

9Q

2

200

9Q

1

200

8Q

4

200

8Q

3

200

8Q

2

200

8Q

1

2007

Q4

Notes: 1) Missing Q1/Q3 values are interpolated2) AFLAC; Allianz; Assurant Inc; Aviva; AXA; CNP; China Life; Delphi Financial; Generali;

Genworth Financial; Great‑West Lifeco; Hartford; Irish Life & Permanent; Legal & General; Lincoln National; Manulife; Metlife Group; Nationwide; Old Mutual; Phoenix Companies; Ping An; Principal Financial Group; Protective Life; Prudential (UK); Prudential (US); StanCorp Financial Group; Standard Life; St. James Place ; Storebrand ASA; Sun Life; Swiss Life; Torchmark; UNUM Group; Zurich FS

Sources: Company reports, Bloomberg, Swiss Re Economic Research & Consulting

Outlook 2011/12: Higher interest rates will help restore profitability, but excessive regulation threatens the business model

Demand for the savings products of the life industry remains robust – there is still a high need to save for retirement – but the newly re‑designed products may dampen it. Also, profitability is an issue due to the higher capital requirements for such products. Nor has the crisis reduced the strong need for traditional life insurance products. Risk products, such as mortality, disability and long‑term care protection, remain in high demand.

Overall, new business growth will be positive in the next few years, driven by an expected recovery of US sales. Therefore, the business case for life insurance remains strong. Unit‑linked products with guarantees will gain ground in line with improving equity markets. However, it will be necessary to re‑design and re‑price these products to better reflect the costs of the embedded risks. Once the economy is back on track, protection products and disability will also pick up again.

From 2011 onwards, premium income is expected to return to its long‑term trend path. In industrialised countries, growth is expected to increase from 2.7% in 2010 to 3.3% in 2012, after adjusting for inflation. In emerging markets, growth is estimated to be much higher, at around 10% in 2011 and 2012.

Figure 7Return on equity of 34 mainly life and global companies (IFRS/GAAP data), %

Ageing populations and the need for protection products sustain demand for life insurance products.

Re‑designed savings products will gain ground along with improving equity markets, while traditional products will grow with the economy.

Premium growth will return to its long‑term trend.

23

The environment will remain challenging through the medium term

Nonetheless, the industry outlook is still clouded. The main issues L&H insurers will face in 2011 are: Low investment yield: Investment income will remain low because of low interest

rates and yields on government and highly‑rated corporate bonds. This will depress L&H profitability, which to a large degree is driven by investment results. Also, policy‑holders may shy away from products with low return guarantees.

More stringent capital requirements: One outcome from the crisis is that capital re‑quirements for asset risk and long‑term guarantees will be more onerous. Under Sol‑vency II insurers will face much more severe stress tests and investments in riskier assets will incur material charges. Companies will need to balance higher expected investment results against higher capital charges. This must be done in conjunction with strategic decisions concerning the level and amount of guarantees they sell.

Need to rebuild capital: The capital situation of life insurers has improved, but some companies will need to further strengthen their balance sheets. For example, in the US, there is still a threat of further asset impairments (eg from commercial mortgages).

Profitability will be stable for now, challenged by volatile financial markets and changes in regulation

Profitability will most likely remain at its current level for the time being. Investment re‑turns are not expected to improve significantly due to low, and only slowly increasing interest rates and volatile equity markets. In most markets, improved sales and relatively low surrenders and withdrawals will support profitability. However, profitability will be pressured by higher hedging costs, higher debt expenses, and potential future asset impairments. In Europe, profitability may be negatively affected by Solvency II, which will, to some extent, discourage insurers from investing in riskier assets. This may not result in much shifting in assets, however, since the allocation to equity is already at a very low level.

Life Reinsurance: Remarkable growth in a difficult environment

The reinsurance industry is benefiting from strong demand for capital relief solutions. Net premiums (for traditional and non‑traditional business) for the top ten reinsurers grew by 9% y‑o‑y in USD terms (+6% in constant currency terms) in the first nine months of 2010.

L&H reinsurance is a highly concentrated business, with the top six players accounting for 75% of the market in 2009. Consolidation is continuing. In January 2010, RGA com‑pleted the acquisition of ING’s group reinsurance business and, in October, Berkshire Hathaway Reinsurance group announced an agreement to acquire Sun Life Financial’s life retrocession business. Aegon is exploring strategic options – including sale – for its life reinsurance business.

Traditional life reinsurance is struggling with low-growth

Traditional life reinsurance continues to be pressured by a challenging protection market and increasing retentions. Global reinsurance premiums declined by 0.3% in real terms in 2010. In industrialised countries, traditional life reinsurance declined by 0.5%, while pre‑miums in emerging markets grew by 4.1%.

The industry still faces the challenges of low investment yields, more stringent capital requirements and further possible asset impairments.

Profitability is likely to be stable for now.

Reinsurers’ are benefiting from the strong demand for capital relief solutions.

Though highly concentrated, L&H industry consolidation continues.

Traditional L&H reinsurance is being challenged by low primary premium growth and declining cession rates.

24

Life insurance: The industry has returned to growth

Finance and capital relief solutions are increasing in importance and demand is higher because of the crisis

Large transactions of various forms – Admin Re, longevity and mortality swaps, and structured life reinsurance solutions – played an important role in recapitalising the life insurance industry. There is still strong demand for these transactions. In 2010, the number of publicly‑disclosed block transactions involving asset transfer – such as Admin Re, bulk purchase annuities and large quota share inforce deals – between (re)insurers is running at about the same level as last year. Fifteen transactions have been completed in 2010 to date, versus seventeen in 2009, with transactions by Resolution Ltd accounting for the bulk of reserves transferred in both years. The number of transactions remains well below the peak from 1998 to 2000, when there were 50–70 transactions per year.

Outlook 2011/12: Financing, supporting growth and helping with the transformation of the life industry are strong value propositions for reinsurance

Traditional life reinsurance growth will be subdued, below 1% in real terms in 2011‑12. In industrialised countries, it will stagnate as a result of declining cession rates in the two major markets US and UK, which account for more than 60% of the global traditional reinsurance business.

In emerging markets, traditional life reinsurance will grow by 7% to 8% annually. Overall, the outlook for non‑traditional life reinsurance remains positive for 2011 and 2012 due to the continuing recapitalisation needs of direct companies, M&A and the demand for longevity solutions.

Although low valuations and an uncertain regulatory environment are an impediment for large scale M&A activity, strategic/forced divestitures by bancassurers and (re)insurers will continue to provide opportunities for block transactions. In Europe, Solvency II will lead to consolidation and run‑offs, mainly for small and medium‑sized companies. Basel III will also likely result in some spin‑offs of insurance companies from banks. In the US, M&A activity has picked up recently and is expected to accelerate due to restructurings, a renewed focus on the core business, and the anticipated impact of Solvency II on European life insurers with US operations.

The market for pure longevity risk transfer continues to have strong momentum. The no‑tional value of publicly‑disclosed swaps rose from USD 1.3bn in 2008 to USD 9.8bn in 2009. The 2010 year‑to‑date notional value is USD 9.0bn. The deals have primarily been in the UK, but there have also been two deals with Australian insurers and one recent deal with a Canadian insurer. Potential demand for longevity reinsurance is significant, particularly by pension funds. In the UK, for example, only 2% of the defined benefit scheme liabilities of GBP 1.4 trillion have been transferred. However, the development of capital market solutions is needed to fully tap market potential. It is estimated that (re)in‑surers in the UK currently only have capacity for around GBP 20bn of deals.

Interest in mortality swaps to transfer extreme mortality risk to reinsurers remains strong as well. Reinsurers provide extreme mortality swaps to banks that offer LoCs for XXX/AXXX reserve funding. The solutions are non‑recourse and transfer solely the extreme mortality risk exposure of the bank. Competition in this space has increased while fees have declined.

Demand is still strong for large reinsurance transactions.

Traditional life reinsurance remains important, but growth will be slow.

The focus of life reinsurers will be on reshaping the industry. Solvency II will generate additional growth for block transactions.

Longevity risk transfer continues to grow at a robust pace, but a capital market solution is needed to significantly spur growth.

Demand for mortality swaps remains strong.

25

Emerging markets: Booming

Emerging market insurance developments, 2010

The market share of emerging regions increased to 16.7%, from 10.5% in 2007, because its strong premium growth is sharply outpacing the relatively stagnant premium growth in industrialised economies. Over the past year, non‑life profitability has benefited from low inflation. Improving investment yields, despite low interest rates, have benefited in‑surance companies, particularly life insurers. The capital of emerging market insurers has returned to, if not surpassed, pre‑crisis levels.

In 2010, non‑life insurance premiums in the emerging markets grew by 7.4% (2009: +2.9%) to USD 243 bn, compared to a long‑term trend rate of 8.9%. Growth is strong in Asia (+17.7%), particularly in China (+22%), Vietnam (+13%) and Indonesia (+8.6%). Two factors, the recovery in external trade and sustained public sector investment in in‑frastructure projects, have been the main drivers of premium growth in Asia, the Middle East (2010: +7.7%) and Latin America (+4%). In comparison, non‑life business stagnated in Central and Eastern Europe (‑0.5%), due to the more fragile economic fundamentals of the region.

Life insurance premiums in emerging markets are estimated to have grown strongly by 16.7% to USD 361 bn in 2010, against a trend growth rate of 13.5% over the past dec‑ade. Strong growth is reported in Asia (+21.7%) due to robust economic fundamentals and a swift rebound in demand for investment‑linked insurance products. Life premiums, for instance, are estimated to have increased 25% in China in 2010. Growth also remained favourable in the Middle East (+7.0%) and Latin America (+8.5%). In Central and Eastern Europe, a particularly severe economic recession significantly affected the life insurance business in 2009, but premiums rebounded to increase by 8.3% in 2010.

Alongside the acceleration in premium growth, most regional insurers also reported im‑proved investment results and higher asset valuations. In the emerging markets, capital returned to its pre‑crisis level due to better investment results/valuation and lower im‑pairment charges. While some international insurers had to restructure their global oper‑ations during the peak of the financial crisis, incumbent domestic insurers in emerging markets used the opportunity to increase their market shares. In Brazil, for example, Itau merged with Unibanco, creating the biggest financial conglomerate in Latin America, and ended its joint ventures with XL and AIG. More M&A activities are happening in emerging markets and the trend is likely to persist into 2011.

The global financial crisis has triggered the renewed focus on insurance solvency and the supervision of group activities. Emerging markets are also rapidly aligning their supervi‑sory standards to international best practices. This is likely to create both major challenges and opportunities for insurers operating in these markets. For example, solvency capital is required to take advantage of growth opportunities arising from increasing demand for insurance cover. Tightening solvency regulations will also test the capital management skills of insurers. In emerging Asia, but also in Latin America, there is a trend towards higher minimum requirements, the adoption of risk‑based‑capital solvency systems, the introduction of dynamic stress tests and the use of scenarios. Eastern Europe has been influenced by Solvency II in the European Union, while Mexico is working to implement a customised version of Solvency II.

Insurers are actively dealing with further regulatory and accounting changes. Regulators are championing better consumer protection through, for example, the establishment of policyholder protection funds and streamlined sales processes. Concurrent changes in insurance accounting standards are also affecting regional insurance markets.

Emerging markets are growing much more rapidly than mature markets in 2010.

Non‑life premium growth has been strong in all regions except in CEE.

Life insurance premium growth has been robust, except in Central and Eastern Europe (CEE).

The investment returns and capital of insurers have improved.

Insurance regulations are tightening in emerging markets.

Insurers will continue to be challenged by the evolving regulatory and accounting developments.

26

Emerging markets: Booming

Emerging markets insurance outlook: Booming

The resilience of the insurance industry in emerging markets during the financial crisis and the positive outlook are helping to increase their attractiveness to international insur‑ers. Many international insurers have explicitly stated that they will actively pursue opportunities in the fast‑growing emerging markets. Insurers are likely to face strong competition from both regional and foreign insurers. It is also probable that banks will increasingly leverage their branch network to further penetrate local insurance markets. Insurers that focused on top line growth will need to shift their focus to profitability.

Life insurance and personal non‑life business lines will benefit in the near term from robust economic and income growth, further urbanisation and the ongoing demograph‑ic change caused by ageing populations. In particular, longevity products – such as an‑nuities – will grow because of the demographic changes in emerging markets. Rising disposable household income will also drive demand for investment‑linked products. In the non‑life sector, the motor business will benefit from further increases in car owner‑ship. Higher incomes will increase demand for property insurance because households will want to protect their rising wealth through insurance. Accident and health covers provided by employers will also benefit from increasing formal employment.

Demand for commercial lines insurance will continue to increase due to government‑sponsored infrastructure projects and recovering trade‑related lines of business. The strong pipeline of infrastructure projects, estimated by the World Bank to be worth USD 900 bn per year, is expected to support growth of engineering and surety lines. Fiscal support for infrastructure spending is, however, expected to gradually fade.

Stronger economic performance and rapid per capita income growth will ensure that in‑surance premium growth in emerging markets outpaces that of industrialised countries. Non‑life insurance premiums in emerging markets are forecasted to grow more than twice as rapidly in industrialised economies over the next decade. In life insurance, pre‑mium growth projections are almost three times the mature market pace, but from a much lower level. As a result, the share of emerging markets in the global life insurance market will increase from 15% in 2010 to 27% by 2020. The share of emerging markets in non‑life is already 16% and will increase to 24%. In absolute terms, however, industr‑ialised countries will still be responsible for a bigger share of the additional premium generated worldwide over the next 10 years.

CAGR 2010–2020 Life Non-lifeEmerging Markets 9.2% 6.8%

Emerging Asia 10.3% 9.7%Middle East 8.3% 7.3%Latin America 8.0% 4.6%Africa 0.0% 4.8%Central & Eastern Europe 7.5% 0.0%

Industrialised countries 3.1% 2.6%World 4.2% 3.3%

Source: Swiss Re Economic Research & Consulting

Emerging Asia is expected to outpace all other emerging regions, both in absolute and relative terms. This is most obvious in life insurance, where the region is expected to ex‑pand by an annual average real rate of 10% within the next 10 years, beating corre‑sponding increases in any other emerging regions. Much of this growth is expected to be generated by further demand for investment‑linked insurance products, while retire‑ment‑related insurance demand is also increasing. In non‑life insurance, Asia will also be the growth leader, but by a smaller margin.

Competition in emerging markets is increasing and will likely lower profitability.

Life and non‑life personal lines will benefit from rising incomes, urbanisation and demographic changes.

Infrastructure investment will boost demand for commercial insurance.

Emerging market premium growth will be twice as fast in P&C and three times as fast in L&H, compared to the industrialised countries.

Table 6Premium growth in life and non-life insurance by regions, forecast 2010–2020

Emerging Asia is expected to grow the fastest over the next decade.

27

28

Published by:

Swiss Reinsurance Company Ltd Canadian Branch 150 King Street West, Suite 1000 Toronto, Ontario M5H 1J9

Telephone +1 416 947 3800 Fax +1 416 364 2449

Swiss Reinsurance Company Ltd Economic Research & Consulting P.O. Box 8022 Zurich Switzerland

Telephone +41 43 285 2551Fax +41 43 282 0075Email: [email protected]

New York Office:55 East 52nd Street, 41st FloorNew York, NY 10055

Telephone +1 212 317 5400Fax +1 212 317 5455

Hong Kong Office:18 Harbour Road, WanchaiCentral Plaza, 61st Floor

Telephone + 852 25 82 5703Fax + 852 25 11 6603

Authors:Thomas HessTelephone +41 43 285 2297

Kurt KarlTelephone +1 212 317 5564

The editorial deadline for this study was 4 December 2010.