Embed Size (px)

Citation preview

GLOBAL IMBALANCES: DO NET CAPITAL FLOWS STILL MATTER? AN INTERNATIONAL MACROECONOMIC PERSPECTIVE

Hélène Rey

London Business School, CEPR and NBER

De Nederlandsche Bank, 2013

Draw on: “Exorbitant Privilege and Exorbitant

Duty”, with Gourinchas and Govillot (2012)

“The Financial Crisis and the Geography of Wealth Transfers”, with Gourinchas and Truempler (2012)

Reforming the International Monetary System with Farhi and Gourinchas (2012)

Chapter for Handbook of International Economics, in preparation, with Gourinchas

Financial Globalization

Large increase in international investment positions especially among advanced economies

Trade in financial assets has outpaced trade in goods and services

Financial globalization has gathered pace since the 1990s.

[Figure]

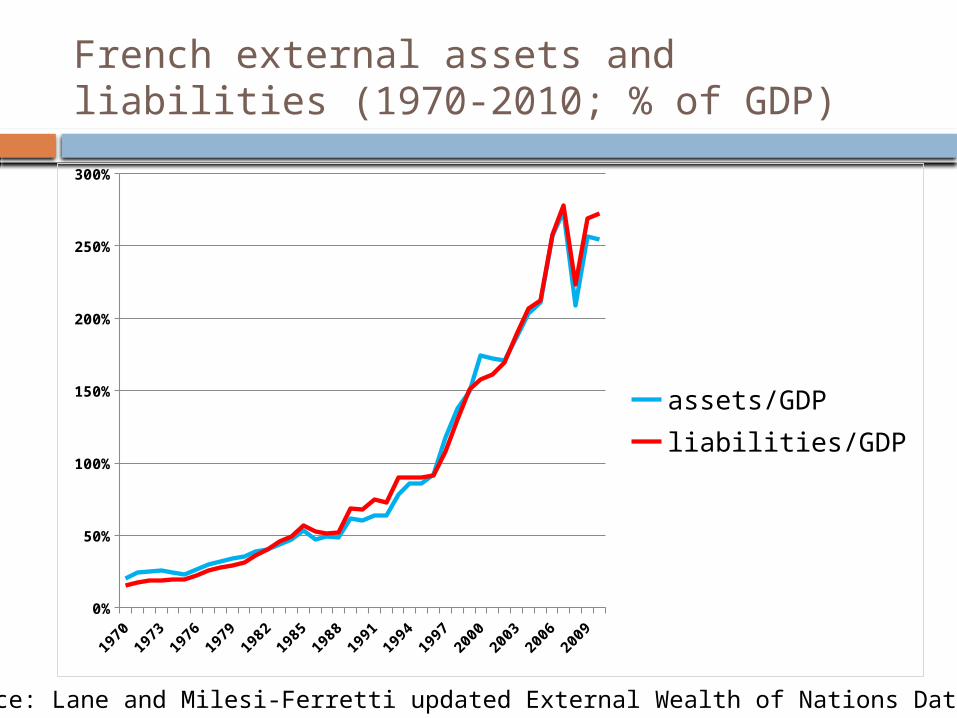

French external assets and liabilities (1970-2010; % of GDP)

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

0%

50%

100%

150%

200%

250%

300%

assets/GDPliabilities/GDP

Source: Lane and Milesi-Ferretti updated External Wealth of Nations Database

Financial crises

International economists traditionally look at current account deficits to predict crises or to forecast consequences of crises.

Financial globalization makes net capital flows less relevant.

Gross capital flows are now key to understand the transmission of international crises.

External balance sheets

Large cross border positions are a vector of both risk sharing and financial contagion

Emerging markets and advanced economies have very different external portfolios

Advanced economies are long in risky assets, emerging markets are long in safer assets (reserves)

Structure of debt portfolio key to understand crisis transmission (Treasuries versus private label AAA assets)

Net external risky assets position (% of GDP)

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

-40%

-30%

-20%

-10%

0%

10%

20%

G7 BRIC

Source: “Exorbitant Privilege and Exorbitant Duty” (Gourinchas, Rey and Govillot (2012))

US external assets

Source: “Exorbitant Privilege and Exorbitant Duty” (Gourinchas, Rey and Govillot (2012))

US external liabilities

The World Banker

The United States is the centre country of the International Monetary System

The United States is the world banker: US issues short-term low-risk assets (T-

bills) US invests in high risk foreign assets

(foreign equity and direct investment) Earns excess returns on its external

position: “exorbitant privilege”.

The United States as a Global Insurer

During latest crisis, US net foreign asset position deteriorated massively:

Between 2007:4 and 2009:1, Net Foreign Assets drop by about USD 2.9 tr.

US liabilities held up well (US issuer of the reserve currency, safe haven) and risky assets plummeted.

A deterioration in the Net Foreign Asset position is a wealth transfer to the rest of the world.

Similar to an insurance payment in crisis time.

Other insurers

Currency gains and losses

Balance sheets matter

Geography of wealth transfers during the crisis Different fortunes depending on portfolio

structure Countries long equity or FDI tend to have

valuation losses Structure of debt portfolio key: government

debt versus corporate debt Correlation of losses with ABCP conduits, ABS

investments, dollar shortage measure and losses on debt portfolio

Future: A New Triffin Dilemma?

In the 1960s currencies could be exchanged at a fixed rate against the dollar whose value was fixed against gold.

Triffin observed that global liquidity demand was outgrowing the United States’ gold reserves (backing the dollars held abroad).

Maintaining the gold value of the dollar was increasingly difficult.

Similarly, fiscal capacity of the dollar is not unlimited Backing of the dollar assets becomes gradually smaller

in a world where relative size of the US shrinks. New Triffin Dilemma

Conclusions

Solving the New Triffin Dilemma (Farhi Gourinchas Rey 2011): develop alternatives to US Treasuries as the dominant reserve asset: multipolar system with the issuance of mutually guaranteed European Bond; open up Chinese financial account, convertibility of the yuan.

More broadly: tracking external balance sheet of countries useful to understand financial vulnerabilities.