Embed Size (px)

Citation preview

19 November 2019 Global

Sales and Trading personnel at Macquarie are not independent and, therefore, the information herein may be subject to certain conflicts of interest, and may have been shared with other parties prior to publication. Note: To the extent Macquarie Research is referenced, it is identified as such and the associated disclaimers are included in the published research report. Please refer to the important disclosures www.macquarie.com/salesandtradingdisclaimer.

FX AND RATES

Fed's Broad Dollar Index

Source: Bloomberg, Fed, Macquarie Strategy

Strategists

Macquarie Bank Limited Singapore Branch

Gareth Berry +65 6601 0348 [email protected]

Macquarie Futures USA LLC

Thierry Wizman +1 212 231 2082 [email protected]

Macquarie Bank Limited Hong Kong Branch

Trang Thuy Le +852 3922 2113 [email protected]

Macquarie Capital (Europe) Limited

Eimear Daly +44 20 3037 4802 [email protected]

This publication has been prepared by Sales and Trading personnel at Macquarie

and is not a product of the Macquarie Research Department.

Global FX Outlook: Peak USD Topping out

For the US dollar, this is as good as it gets. This is the high-water mark. A “phase

one” US-China trade deal looks possible, which could end the 5-year old US

dollar rally.

The precise timing of any negotiating breakthrough is unknown. But even the

absence of further escalation could encourage a gentle uptick in global growth

and a decline in safe-haven demand.

That should prevent further USD upside and even spark a very gradual decline.

Escalating US political risk much later in 2020 could add to the selling

pressure, especially in USDJPY which could dip to 102 by end-2020.

USDCNY is likely to fall to 6.80 by mid-2020, promoting generalised USD

weakness across Asia-Pacific; KRW and TWD are best placed to benefit.

Any AUDUSD upswing should stop at 0.71 though. The RBA’s easing bias

remains in place and each additional cut from here brings QE potentially closer.

The novelty of unconventional policy, even just the distant threat of it, should help

cap any gains.

The outlook for GBP hinges on the UK general election, scheduled for

December 12th. A stable overall majority for Boris Johnson would trigger a decent

move higher in GBPUSD, towards 1.35 by end-2020. It would also contribute

to a weaker dollar, irrespective of US-China developments.

A recovery in Eurozone PMIs should help EURUSD mount a tentative rebound

towards 1.15 by end-2020, driven by a thaw in trade tensions at home and

abroad. But the threat of US Section 232 auto tariffs is likely to linger.

The potential exists for a more powerful euro upswing, but we’d be surprised

if it happens. Large scale eurozone fiscal stimulus or a hawkish ECB reset both

seem unlikely.

An epic rebalancing out of US stocks and into Eurozone equities is just about

conceivable, given real money positioning is lop-sided. But a spontaneous

recovery in European growth seems very unlikely, so the trigger for such a move

would have to originate inside the US and selectively cripple the US growth

outlook. Outside of extreme US political developments, it’s hard to imagine what

might provide the necessary spark.

The Canadian dollar should be an exception in the developed-market space,

bucking the weaker USD trend. USDCAD could climb to 1.35 by end-Q1 as

poorer data catches policymakers out, and the BoC is finally forced into a long-

awaited easing cycle.

We are constructive on RUB. But ZAR is likely to be left behind in any EM rally,

potentially falling to 15.55 against the USD by end-2020. The Asian high-yielders

(IDR and INR) could also struggle as global bond yields push higher and the Fed

refrains from further cuts. The outlook for BRL, MXN and CLP looks equally

challenging.

90

95

100

105

110

115

120

125

130

135

Jan-95 Jan-03 Jan-11 Jan-19

index

Global FX Outlook: Peak USD

19 November 2019 2

Contents

Forecast Summary ................................................................................ Error! Bookmark not defined. USD: Peak US dollar has arrived .......................................................................................................... 7 CNY: On recovery track ........................................................................................................................ 9 EUR: Basing at last ............................................................................................................................. 12 AUD, NZD: The allure of unconventional measures .......................................................................... 14 GBP: A relief rally ................................................................................................................................ 17 JPY: Rally on hold ............................................................................................................................... 19 CAD: Rates Cuts Will Undermine the Loonie’s Strength ..................................................................... 20 EM FX Asia: A change of fortune ....................................................................................................... 22 EMEA: The risk-reward weighing scales ............................................................................................. 26 Latin America: Will Politics Drive Performance in 2020? ................................................................... 31 Detailed FX Forecasts Table ............................................................................................................... 44

Global FX Outlook: Peak USD

19 November 2019 3

Forecast Summary

Fig 1 Major currency FX forecasts summary

Spot Forecasts*

Currency vs. Latest 19Q4 20Q1 Near-term view

US dollar EUR 1.106 1.090 1.110 Mildly bearish for 2020. A mini-global growth upswing should benefit other more-open economies proportionately more than the US. It should also undermine the dollar’s safe haven appeal. Escalating US political risk could add to the USD selling pressure later in 2020, but we would not want to overstate the case. While the policies of some presidential candidates might not be market-friendly President Trump’s counter-manifesto could keep USD bulls engaged.

by market convention JPY 108.8 109.0 109.0

GBP 1.293 1.300 1.300

AUD 0.682 0.690 0.700

CNY 7.01 6.95 6.85

Euro USD 1.106 1.090 1.110 Getting mildly bullish. EURUSD is well placed to benefit from a gentle global growth upswing, plus an amical Brexit resolution. But FX technical resistance might not be overcome, at the earliest, until the UK’s general election is out of the way on Dec 12th. Escalating US political risk should add to upside pressure later in 2020.

Foreign currency units per euro JPY 120.3 118.8 121.0

GBP 0.856 0.838 0.854

AUD 1.622 1.580 1.586

CNY 7.75 7.58 7.60

Japanese yen USD 108.8 109.0 109.0 Neutral for now. The global economic backdrop looks set to brighten after the recent scare. The Fed seems in no rush to cut again either, which suggests this could be just a mid-cycle adjustment rather than the early stages of a deeper easing campaign. Neither development is good for the yen. But a delayed yen rally still looks likely, as US political risks intensify into the US Presidential Election.

Yen per unit of foreign currency EUR 120.3 118.8 121.0

GBP 140.6 141.7 141.7

AUD 74.2 75.2 76.3

CNY 15.5 15.7 15.9

UK sterling USD 1.293 1.300 1.300 Bullish. ‘Hard Brexit’ risk should recede materially if PM Johnson returns as PM with an overall majority after the upcoming general election. Opinion polls are pointing convincingly in that direction. His new Brexit withdrawal deal could then be ratified, offering a route out of the quicksand. The issue of how to handle the end of the transition period in Dec 2020 would remain unresolved, but at least the tail-risk of a hard no-deal exit would have mostly vanished, ensuring GBP holds on to recent gains and creeps even higher. that depends on Brexit Party and DUP support. There would be very limited room for manoeuvre in that case, raising the risk of a hard no-deal Brexit whenever the clock runs out again, probably sometime in Q1 2020. A thumping overall majority though, however unlikely, would create scope for compromise, in which case.

Foreign currency units per pound EUR 1.169 1.193 1.171

JPY 140.6 141.7 141.7

AUD 1.896 1.884 1.857

CNY 9.06 9.04 8.91

Australian dollar USD 0.682 0.690 0.700 Mildly bullish for now in anticipation of a partial US-China trade deal being struck. This would deliver a shot in the arm for global growth and boost CNY too (dragging AUD along for the ride). But any additional RBA rate cut from here brings closer the day when unconventional measures might be needed. Although we see no imminent risk of this, the market is likely to price in QE well in advance, which — for AUD — should more than neutralise the benefit from any trade resolution.

Foreign currency units per dollar EUR 0.616 0.633 0.631

JPY 74.2 75.2 76.3

GBP 0.527 0.531 0.538

CNY 4.78 4.80 4.80

Chinese renminbi USD 7.01 6.95 6.85 Bullish: Our base case is for a Phase 1 deal to be signed before December 15 to enable 4Q tariff cancelation. A currency agreement in trade deal combined with a step up in China stimulus we forecast by 1Q 2020 and a gentle global growth rebound will support RMB strength in 1H 2020. The PBoC is likely to encourage CNY appreciation post deal via lower USDCNY fixes. A rollback of the September tariffs would be an upside versus our base case, while a delay in Phase-1 deal beyond December represents a downside risk.

RMB per unit of foreign currency EUR 7.75 7.58 7.60

JPY 0.064 0.064 0.063

GBP 9.06 9.04 8.91

AUD 4.78 4.80 4.80

Source: Bloomberg, Macquarie Strategy. *End-of-quarter forecasts.

Global FX Outlook: Peak USD

19 November 2019 4

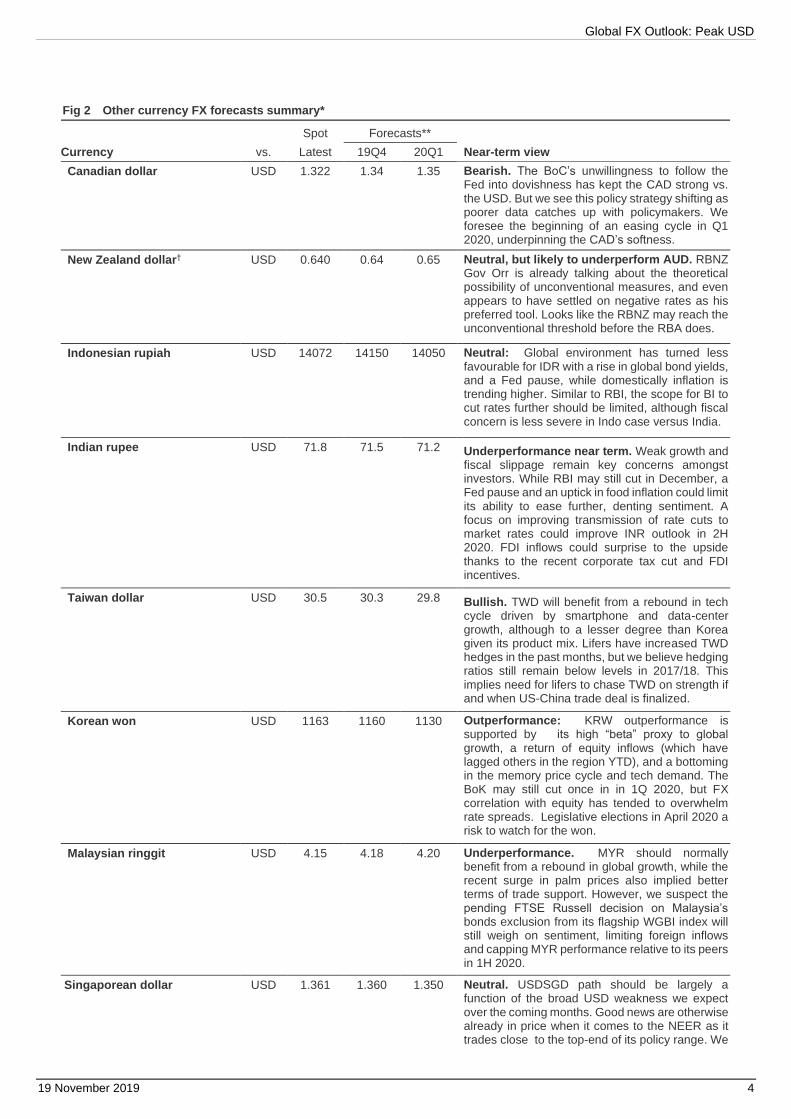

Fig 2 Other currency FX forecasts summary*

Spot Forecasts**

Currency vs. Latest 19Q4 20Q1 Near-term view

Canadian dollar USD 1.322 1.34 1.35 Bearish. The BoC’s unwillingness to follow the Fed into dovishness has kept the CAD strong vs. the USD. But we see this policy strategy shifting as poorer data catches up with policymakers. We foresee the beginning of an easing cycle in Q1 2020, underpinning the CAD’s softness.

New Zealand dollar† USD 0.640 0.64 0.65 Neutral, but likely to underperform AUD. RBNZ Gov Orr is already talking about the theoretical possibility of unconventional measures, and even appears to have settled on negative rates as his preferred tool. Looks like the RBNZ may reach the unconventional threshold before the RBA does.

Indonesian rupiah USD 14072 14150 14050 Neutral: Global environment has turned less favourable for IDR with a rise in global bond yields, and a Fed pause, while domestically inflation is trending higher. Similar to RBI, the scope for BI to cut rates further should be limited, although fiscal concern is less severe in Indo case versus India.

Indian rupee USD 71.8 71.5 71.2 Underperformance near term. Weak growth and fiscal slippage remain key concerns amongst investors. While RBI may still cut in December, a Fed pause and an uptick in food inflation could limit its ability to ease further, denting sentiment. A focus on improving transmission of rate cuts to market rates could improve INR outlook in 2H 2020. FDI inflows could surprise to the upside thanks to the recent corporate tax cut and FDI incentives.

Taiwan dollar USD 30.5 30.3 29.8 Bullish. TWD will benefit from a rebound in tech cycle driven by smartphone and data-center growth, although to a lesser degree than Korea given its product mix. Lifers have increased TWD hedges in the past months, but we believe hedging ratios still remain below levels in 2017/18. This implies need for lifers to chase TWD on strength if and when US-China trade deal is finalized.

Korean won USD 1163 1160 1130 Outperformance: KRW outperformance is

supported by its high “beta” proxy to global growth, a return of equity inflows (which have lagged others in the region YTD), and a bottoming in the memory price cycle and tech demand. The BoK may still cut once in in 1Q 2020, but FX correlation with equity has tended to overwhelm rate spreads. Legislative elections in April 2020 a risk to watch for the won.

Malaysian ringgit USD 4.15 4.18 4.20 Underperformance. MYR should normally benefit from a rebound in global growth, while the recent surge in palm prices also implied better terms of trade support. However, we suspect the pending FTSE Russell decision on Malaysia’s bonds exclusion from its flagship WGBI index will still weigh on sentiment, limiting foreign inflows and capping MYR performance relative to its peers in 1H 2020.

Singaporean dollar USD 1.361 1.360 1.350 Neutral. USDSGD path should be largely a function of the broad USD weakness we expect over the coming months. Good news are otherwise already in price when it comes to the NEER as it trades close to the top-end of its policy range. We

Global FX Outlook: Peak USD

19 November 2019 5

view SGD as a funder for relative value trades in Asia near term.

Philippines peso USD 50.62 50.8 50.0 Neutral. PHP is likely to drop from the top 3 in the EM Asia FX ranking table this year to the middle of the pack in 2020. PHP strength in 2019 was a result of a recovery from an inflation and growth shock in 2018, supportive real rates, and lower current account deficit due to delayed Budget spending. These tailwinds could turn into headwinds in 2020, with the current account deficit likely re-widening while inflation should tick up from a low base.

Argentinian peso USD 59.7 63.0 69.0

Neutral. FX controls have made price discovery in the USD/ARS impossible, but the FX controls are likely to endure for many several quarters, and at least until the new gov’t can conclude its negotiations with bondholders and re-establish access to int’l capital markets. How the new gov’t will treat bondholders will reflect on the coherence of its domestic policies in regard to the needed fiscal adjustment and a resumption of ‘normality’.

Brazilian real USD 4.19 4.25 4.30 Bearish Short-term, More Constructive in 2020. Pressure from the weaker ARS and the BCB’s weak-BRL policy bias will take USD/BRL higher before it stabilizes around 4.25, before reform initiatives help support sentiment and the BRL stabilizes by early 2020.

Chilean peso USD 777 790 810 Relatively Bearish. The prospect that a new constitution will be drafted over the next 9- to 12 months ensures that uncertainty about Chile will remain high throughout 2020. After the BCCh’s measure help stabilize the CLP in the short term, expect depreciation to resume during 2020.

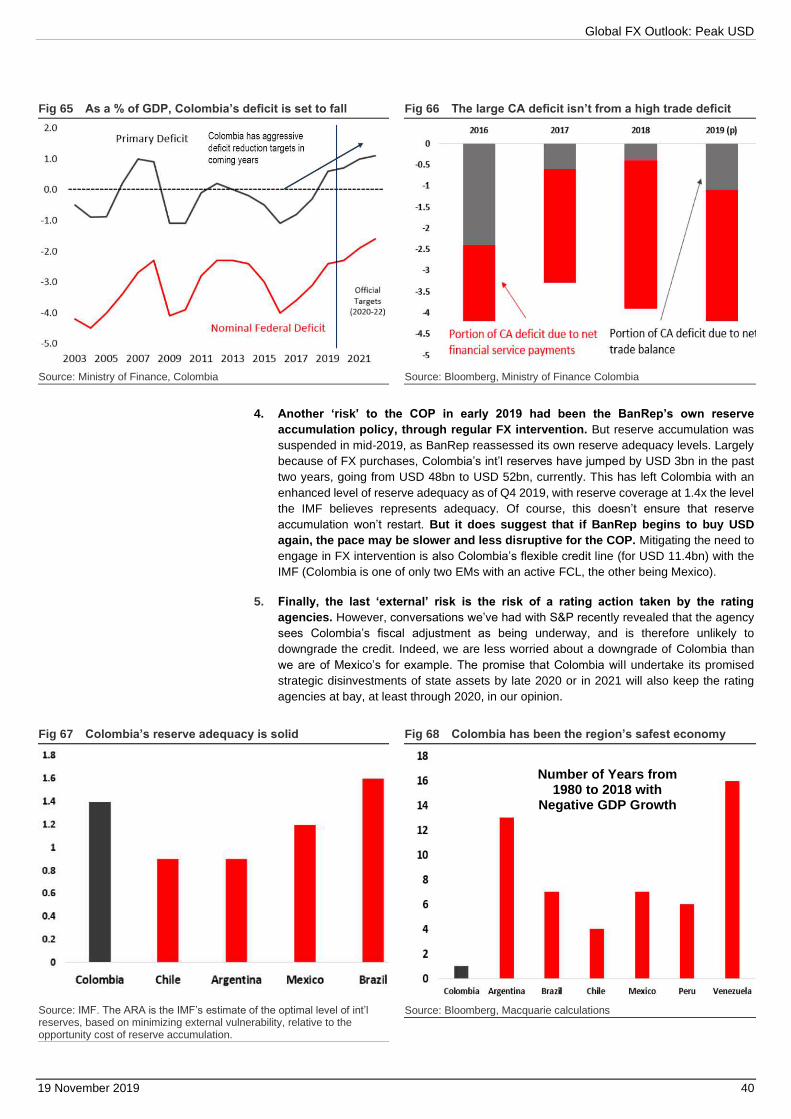

Colombian peso USD 3426 3400 3400 Relatively Bullish. Relative to the region, Colombia has been a growth ‘champ’, although we doubt that strong growth will persist in absolute terms into H2 2019, especially as residential investment slows. Policy rates throughout most of 2020 will still be attractive, and the COP’s diversification properties and its detachment from China will draw organic inflows. The risk comes from labor unrest in the medium term.

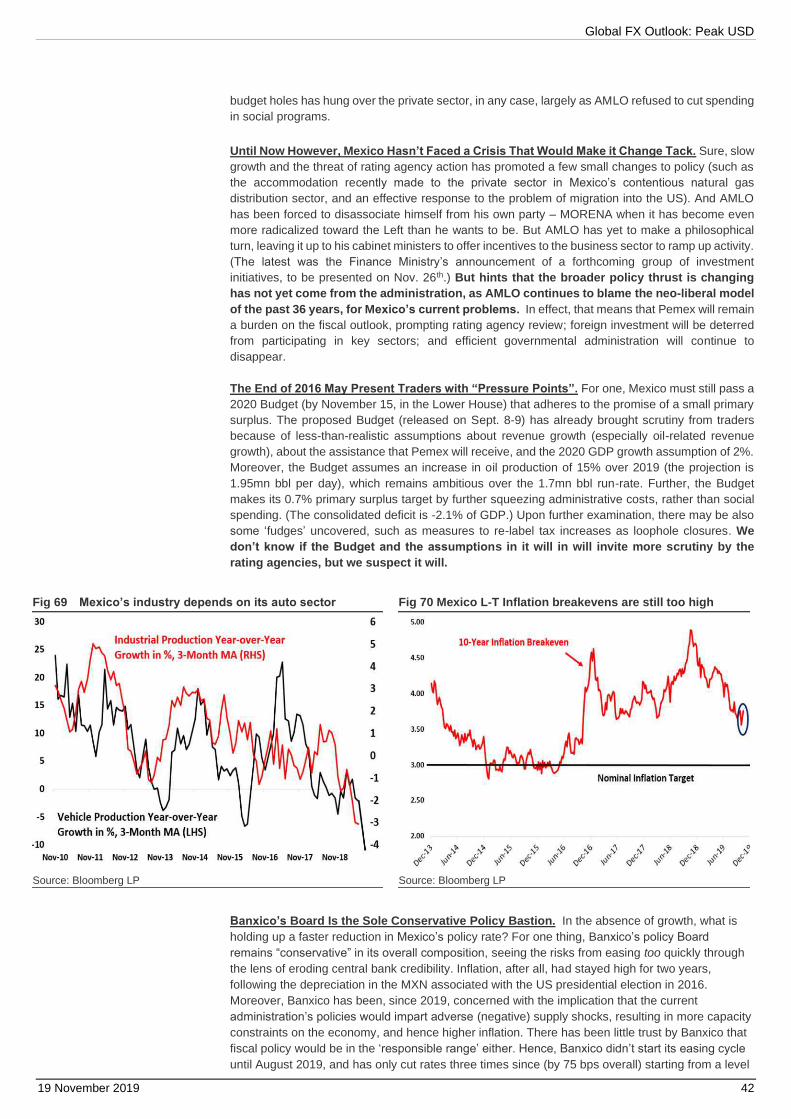

Mexican peso USD 19.2 19.5 20.0 Structurally Bearish. Despite Mexico being in an industrial “slow-growth” trap, we have yet to see an earnest change of policy direction from the AMO administration, leading us to think that the risk is rising that various policy targets go unmet. Banxico remains the last bastion of conservatism, but even it will be gradually cutting the policy rate in 2020.

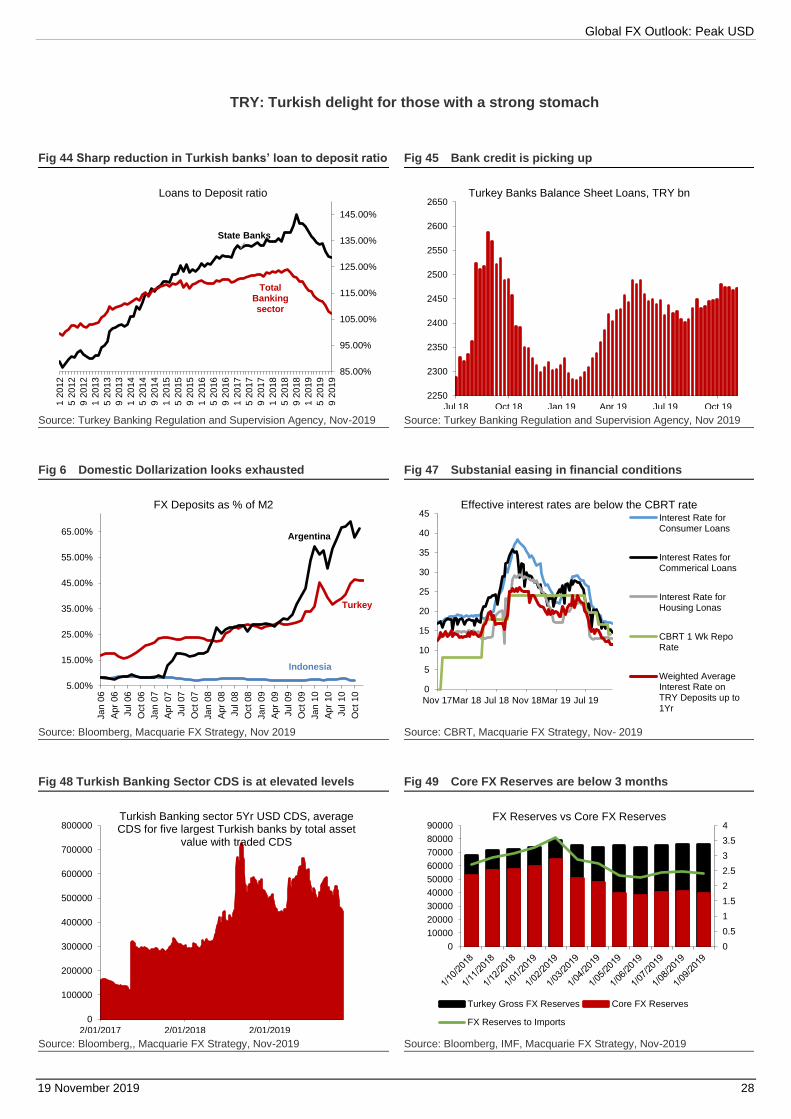

Turkish lira USD 5.72 5.7 5.5 Bullish. A restored positive growth differential and a global reach for yield into 2020 underpin our cautiously constructive view on the TRY. Domestic dollarization also appears to have reached a peak, removing one key driver of TRY weakness. Positioning is also cleaner.

South African rand USD 14.8 14.7 15.8 Relatively Bearish. The combination of low growth, structural barriers to economic reform, high and inexorable rising debt, immediate credit

Global FX Outlook: Peak USD

19 November 2019 6

Fig 3 USD strength prevailing against most FX counterparts into year-end

Source: Bloomberg, Macquarie Strategy.

rating risk and a relatively hawkish central banks means ZAR will be left out of the EM rally in 2020.

Russian ruble USD 63.8 63.0 60.0

Bullish. We are constructive on the RUB due to

our expectation of a stronger EUR into 2020,

fiscal loosening extending the RUB’s relative

growth differential, further CBR rate cuts driving

foreign inflows into OFZ’s and still high real yield

relative to other EMs.

Source: Bloomberg, Macquarie Strategy. *Currencies are quoted as domestic currency per US dollar unless otherwise specified († denotes inverse quotation). **End-of-quarter forecasts.

Global FX Outlook: Peak USD

19 November 2019 7

USD: Peak US dollar has arrived

The dollar’s demise has been frequently foretold ever since its rally began 5 years ago. Perhaps

the soft USD during the BRICs era has left its mark on the psyche. Same goes for the long years

of Fed QE. Both episodes have planted the idea that the dollar’s natural state is one of

weakness.

We have no wish to fall into this trap. But even we must acknowledge that the balance of risks

for 2020 is skewed towards a mildly softer outcome. For the dollar, the situation right now is as

good as it gets. This is the high-water mark.

From here a gentle pickup in global growth seems likely, conditional on a meaningful de-escalation

of US-China trade tensions. That should undermine one veneer of dollar strength: its safe

haven appeal.

It should have other consequences too. US growth would participate in that upswing, but other

more-open economies would benefit proportionately more, especially the Eurozone where the

growth effect would be amplified by relief over the avoidance of a hard Brexit. A EURUSD

upswing could soon be underway.

A trade-truce-inspired CNY surge would also spread USD weakness across the currencies of

Asia-Pacific. Meanwhile, the result of the UK general election has every chance of jolting

GBPUSD into a higher range. Combined, the price action would reinforce the sense that the USD

had turned.

Timing the turnaround will be tricky as much hinges on how long it takes to seal a partial US-

China trade compromise. Suffice it to say that the US political calendar means we are talking

weeks or months, not years.

Fig 4 Equity market performance (USD terms) Fig 5 Foreigners are active in US stocks

Source: Bloomberg, Macquarie Strategy Source: Fed, Macquarie Strategy

The political backdrop

Escalating US political risk could add to the USD selling pressure later in 2020, but we would

not want to overstate the case. While the policies of some presidential candidates might not be

market-friendly (see page 19 here), President Trump’s counter-manifesto could keep USD bulls

engaged. So any adverse impact is likely to be delayed until much closer to the Nov 3rd

Presidential election, or perhaps until after the votes are counted.

Several presidential candidates favour a weaker USD, but this is easier said than done. Ask

President Trump. FX intervention is not as simple as it sounds – if it were, Trump would probably

have done it already.

Admittedly Japan’s government succeeded in weakening the yen, but only after enlisting the help

of the Bank of Japan. We see zero chance that the Federal Reserve, under its current mandate,

would use monetary policy to engineer a weaker USD.

The Fed’s policy framework is currently being reviewed and “make up” strategies to compensate

for past inflation misses are under consideration. But for this to hurt the dollar, the Fed would

25

50

75

100

125

150

175

200

225

Jan-07 Jan-10 Jan-13 Jan-16 Jan-19

ind

ex (

ba

se

= 1

00

)

USEurope excluding UKUKJapan

0

5

10

15

20

Jan-88 Jan-98 Jan-08 Jan-18

as a

sh

are

of to

tal m

kt ca

p (

%)

Foreigner ownership of US stocks

Gareth Berry +65 6601 0348 [email protected] Thierry Wizman +1 212 231 2082 [email protected]

Trang Thuy Le +852 3922 2113 [email protected]

Eimear Daly +44 20 3037 4802 [email protected]

Global FX Outlook: Peak USD

19 November 2019 8

need to pledge to drive the inflation rate above target, beginning soon or even immediately.

A passive tolerance of above-target inflation (if it presents itself) would be no game-changer for the

USD.

The market would also need to have confidence that the Fed could meet this tougher

challenge. Inflation is low now, but not for want of trying. Would trying harder make much

difference?

Political developments could knock the dollar off its perch if a new administration harms

the growth outlook. More specifically, US stocks would be vulnerable if higher corporate taxes

were suddenly imposed, and in theory some dollar weakness could ensue if investors reacted by

trimming their overweight US positions and redeploying into Europe.

Trouble is, we do not recall a sustained period when the USD fell in tandem with US stocks.

Weakness in US equities would likely spread globally, and the USD could actually benefit from

safe-haven demand.

Still, higher foreign participation these days and lop-sided real-money positioning means the

downside risks for the dollar from this are not negligible.

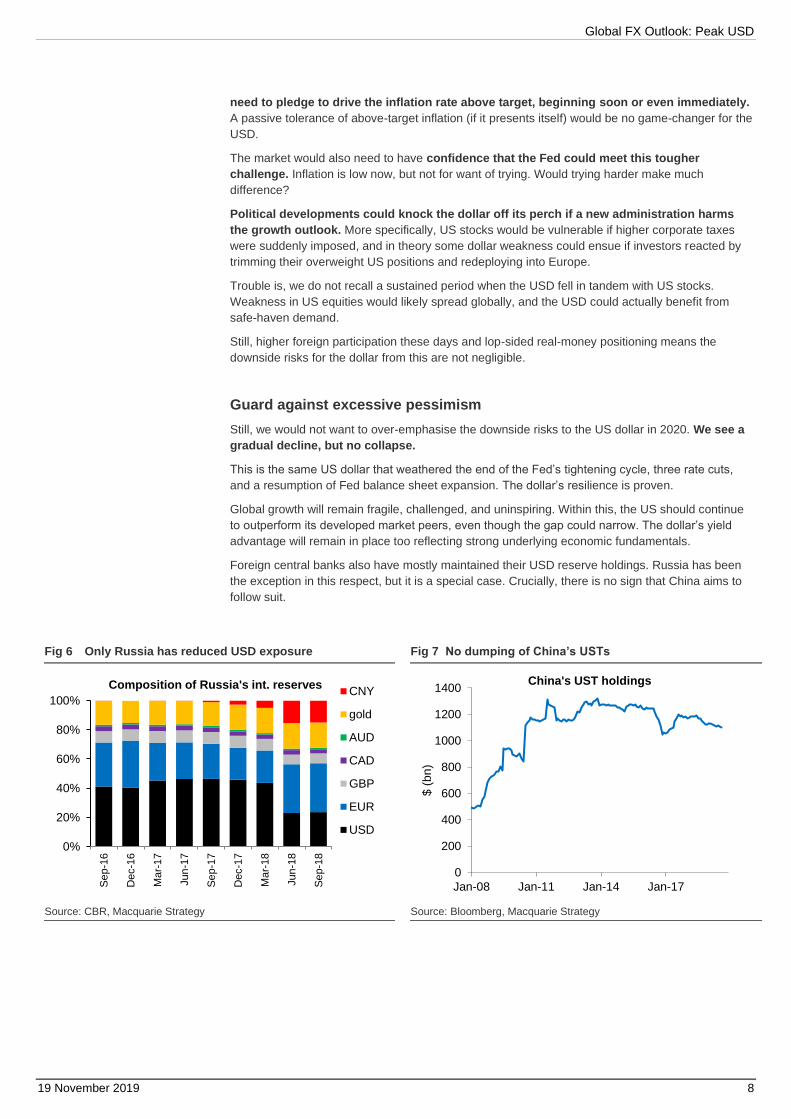

Guard against excessive pessimism

Still, we would not want to over-emphasise the downside risks to the US dollar in 2020. We see a

gradual decline, but no collapse.

This is the same US dollar that weathered the end of the Fed’s tightening cycle, three rate cuts,

and a resumption of Fed balance sheet expansion. The dollar’s resilience is proven.

Global growth will remain fragile, challenged, and uninspiring. Within this, the US should continue

to outperform its developed market peers, even though the gap could narrow. The dollar’s yield

advantage will remain in place too reflecting strong underlying economic fundamentals.

Foreign central banks also have mostly maintained their USD reserve holdings. Russia has been

the exception in this respect, but it is a special case. Crucially, there is no sign that China aims to

follow suit.

Fig 6 Only Russia has reduced USD exposure Fig 7 No dumping of China’s USTs

Source: CBR, Macquarie Strategy Source: Bloomberg, Macquarie Strategy

0%

20%

40%

60%

80%

100%

Se

p-1

6

Dec-1

6

Ma

r-17

Jun

-17

Se

p-1

7

Dec-1

7

Ma

r-18

Jun

-18

Se

p-1

8

Composition of Russia's int. reservesCNY

gold

AUD

CAD

GBP

EUR

USD

0

200

400

600

800

1000

1200

1400

Jan-08 Jan-11 Jan-14 Jan-17

$ (

bn

)

China's UST holdings

Global FX Outlook: Peak USD

19 November 2019 9

CNY: On recovery track

We cut USDCNY forecast to 6.95 by year end and 6.80 by 1H 2020, bringing forward the RMB

gains we had expected through 2020 to the next 6 months.

Despite the uncertainty near term on timing of Phase 1 deal, we think incentives for US and China

to strike an agreement to support their economies are high. A trade truce combined with a rebound

in global growth and a step up in China stimulus we forecast in the next one to two quarters

suggests to us that RMB gains will likely be front-loaded in 1H 2020.

• Our base case is for Phase-1 deal to be signed before December 15 to enable the

cancelation of the December 15 tariffs. If it comes with additional tariff rollback, it would be an

upside versus our forecast. Importantly, we think this trade truce will be more durable than the

previous two (Dec 2018 and Jun 2019), with the US Elections acting as a circuit breaker to

prevent talks breakdown and tariff re-escalation in 2020.

• PBoC’s endorsement of RMB strength could lead the market to price for an implicit

agreement for FX gains in trade deal. We don’t expect a deal to include RMB pledge at a

specific target or range. However, the PBoC will likely encourage RMB strength post deal via

lower USDCNY fixes. The UST may follow through to remove China’s currency manipulator

designation. This should be enough to encourage the market to believe in an implicit agreement

for RMB strength may have been struck.

• China’s policy stimulus should gear up. While timing remains difficult to call, indication may

come from the December Work Conference, where policy makers set their growth and key

economic targets for 2020. We think achieving growth around 6% in 2020 will require a step up

in stimulus.

• A gradual moderation in the USD at a broad level should help add to USDCNY downside.

We expect a gentle global growth rebound, with receding Brexit and US-China trade war risks

also working to lessen the USD’s safe-haven appeal.

Fig 8 Trade war is likely to enter a de-escalation phase after nearly 2 years of escalating

Fig 9 Trade truce combined with a step up in China stimulus should boost RMB prospect in 2020

Source: Bloomberg, Macquarie Strategy Source: Bloomberg, CEIC, Macquarie Strategy

But the path for RMB to get back to below 7 is unlikely to be linear. While not our base case,

the risk of Phase-1 deal being delayed beyond December is high (~30%). The cancelation of the

Chile summit has removed the deadline pressure to have a deal ready by November 16-17 for

signing.

The market can still weather a few months delay as long as trade talks continue, and the

December 15 tariffs are put on hold. However, the uncertainty leading to the December 15

deadline could drive a pullback in risk sentiment and the RMB. Ultimately, we view such rallies in

USDCNY/CNH as opportunities to add to short to position for a better 1H 2020.

6.20

6.40

6.60

6.80

7.00

7.20

7.40

7.60

Jan 18 Apr 18 Jul 18 Oct 18 Jan 19 Apr 19 Jul 19 Oct 19

RMB and US trade tariffs

USDCNH

25% onf irst $34bn

25% on

$50bn

25% on$50bn, 10%

on addtional $200bn

25% on$250bn

25% on$250bn,

15% on additional $110bn

Trump's tarif f threat

Tarrifeffective

dates

6.00

6.20

6.40

6.60

6.80

7.00

7.20

4.0

5.0

6.0

7.0

8.0

9.0

10.0

13 14 15 16 17 18 19

%y oy RMB and macro indicators

USDCNY (RHS,inverted)

China IP grow th, %yoy

Trang Thuy Le +852 3922 2113 [email protected]

Global FX Outlook: Peak USD

19 November 2019 10

A currency agreement forms the basis for yuan stability, and quite likely strength

in 1H 2020

We envisage a Phase 1 deal will include a currency chapter – similar to the USMCA agreement –

with the following strengthened commitments:

• Maintain RMB stable around an equilibrium level

• Foster a market-determined exchange rate regime; refrain from competitive devaluation,

including through intervention in the foreign exchange market;

• Possibly commitment to further liberalize the capital account

• Disclose data on FX intervention on a regular basis, likely within 90 days. Conform to other IMF

requirement on FX reserves and forward disclosure, participation in IMF COFER report (which

China already largely implemented).

• Agree to an enforcement and monitoring mechanism which include regular office-level and

ministerial-level meetings, between the PBoC and US Treasury to monitor FX policy.

What a currency agreement between the US and China is unlikely to include is an explicit pledge

for RMB at a specific target or range, and/or commitment to pursue intervention policies to

achieve such targets (a Plaza Accord like arrangement).

We explained in our Asia FX Strategy: CNY currency clause - from USMCA to Plaza Accord why

such an agreement is not feasible, and its success highly questionable in today’s world.

One key issue is publishing outright FX target/range would lead to speculation and more costly

intervention. Even the Plaza or Lourve Accords did not release FX targets to the public.

Another issue is from the PBoC’s perspective, agreeing to commit to certain RMB target would

essentially mean giving up its FX and potentially monetary policy autonomy – a hard sell to its

domestic audience.

Intervention also has less chance of success absence greater coordination in underlying economic

policy by both US and China.

International criticism, including from the IMF for any such currency arrangement would be high.

But the lack of a specific FX pledge in US-China agreement will not prevent the market to believe

in an “implicit” agreement for RMB appreciation in trade deal. The PBoC is likely to reinforce

such thinking by encouraging faster yuan appreciation post deal, via lower USDCNY fixes.

The US could also signal its approval by removing China’s currency manipulation designation.

In short, any rally in RMB post trade deal will be reinforced by policy, implying scope for it

to extend.

Progress beyond Phase 1 easier said than done – renewed trade uncertainty could

bring back volatility in 2H 2020

As much as we are positive on a Phase 1 US-China trade deal, we find it much harder to see

breakthrough beyond Phase 1. China is unlikely to budge on more structural issues, including its

industrial policy and state subsidy practice. A honeymoon period in 1H for US-China could be

replaced by renewed tensions again in 2H.

Lacking progress in Phase 2 could lead to tariff threat by Trump again - although market may read

them as less credible during the elections.

A scenario where in the final US election race, Trump competes with Elizabeth Warren, who is also

known for being a China hawk and for her restrictive policy on trade, could also lead the market to

pare back optimism on RMB.

Global FX Outlook: Peak USD

19 November 2019 11

Fig 10 CNH vol curves have shifted lower – own protection at the back-end of the curve makes sense early in 2020

Fig 11 China FX vols should be structurally higher as FX regime increasing shift to a more flexible float

At the money implied vols

Source: Bloomberg, Macquarie Strategy Source: Bloomberg, Macquarie Strategy

CNH vol curve has shifted downward in recent months. Long-end vols are at the lower end of their

4-year range, but skews are still well bid for calls. We think owning protection at the back-end of

the vol curve makes sense in early 2020, especially if RMB gains we expect early in the year

further drive down skews and vols from current levels.

China’s effort to open-up its financial market to foreign portfolio investors will make the RMB more

susceptible to hot money flow. This combined with the government’s desire to allow RMB to be

more market determined should lead to a repricing of RMB vols structurally higher - approaching

those of more flexible FX regime, such as KRW.

The evolution of China FX regime is on-going. China vols were well below the basket-managed

SGD vols pre 2015 when CNY FX regime was seen as a managed USD peg. Vols rose structurally

from August 2015 to par with SGD vols after China made an explicit link of the CNY fix to the

CFETS basket.

Since the trade war broke down, China vols have traded above SGD vols. This may reflect a

market premium for trade war, but also a policy realization that a flexible FX regime is best suited

for China in an environment of high external stress.

4.6

4.8

5.0

5.2

5.4

5.6

5.8

1m 2m 3m 6m 9m 1y 2y

% CNH vol curve, %

1m before

Latest

2y median

-1.0

1.0

3.0

5.0

7.0

9.0

11.0

13.0

15.0

14 15 16 17 18 19

% CNY 1y implied vol against FX regime, %

USDCNH1y impl vol

USDSGD1y impl vol

USDKRW1y impl vol

Flexible float regime

Managedbasket regime

Managed USD peg regime

Global FX Outlook: Peak USD

19 November 2019 12

EUR: Basing at last

We keep our rising EURUSD forecast profile, partly in anticipation of some mild USD weakness

later in 2020 courtesy of the US political cycle.

The Eurozone is well positioned to benefit from the mini-global growth upswing too, as the lagged

effect of previous tariff imposition fades, and the prospect of a partial US-China trade deal boosts

sentiment. Even the absence of further escalation represents progress of sorts.

Owing to an open economy, the burden of escalating US-China tensions so far has fallen

disproportionately on the Eurozone, despite the region not being a party to the dispute. The same

logic should also hold in reverse as relations eventually thaw. A headwind could become a

tailwind.

Fig 12 Manufacturing mood needs a boost Fig 13 Sensitivity to the external environment

Source: Bloomberg, Macquarie Strategy Source: World Bank, Macquarie Strategy

So although Eurozone PMIs are subdued now, they could turn soon, helped too by the

avoidance of a hard Brexit. A negotiated EU withdrawal deal means Europe’s hard-pressed

manufacturing sector should continue to enjoy unfettered access to a key export market, and

their complex supply chains will be safeguarded for now at least.

All of this should help EURUSD mount a tentative rebound, although an upswing may be delayed

until the results of the UK general election on December 12th are announced. Until then, the

FX technicals look too challenging.

Also, the FX carry earned by EURUSD shorts is superior to the yield on a 30y UST; in a low yield

world, that’s an important consideration.

The speculative positioning picture does not argue for a sudden euro surge either. There is a

legacy euro net short out there but it’s not substantial. So a cascade of short-covering on any

positive shock could only go so far before the propellant runs out.

From a real-money flow perspective the latest indications suggest a base may be forming in

EURUSD, but nothing more than that for now. Fixed income outflows from the Eurozone have

essentially stopped, but equity inflows from abroad are still nowhere to be seen. The latter is the

missing ingredient, and its absence keeps our euro upside expectations in check.

The market remains overweight US equities though. So anything that triggers an equity

rebalancing out of the US and back into the Eurozone would force us to raise our EURUSD

forecasts. Such a shock would have to originate inside the US though, and selectively cripple the

US growth outlook. Outside of extreme US political developments, it’s hard to imagine what might

realistically provide the spark.

44

46

48

50

52

54

56

58

60

62

Apr-15 Apr-16 Apr-17 Apr-18 Apr-19

ind

ex

Eurozone PMIs

comp

manf

0

10

20

30

40

50

1960 1970 1980 1990 2000 2010

exp

ort

s a

s a

sh

are

of G

DP

(%

)

Exports as a share of GDP

US

China

Eurozone

Gareth Berry +65 6601 0348 [email protected]

Eimear Daly +44 20 3037 4802 [email protected]

更多精品报告,登录东西智库网站(dx2025.com)下载

Global FX Outlook: Peak USD

19 November 2019 13

Fig 14 FX technicals still capping any gains Fig 15 Net positioning in EURUSD FX futures

Source: Bloomberg, Macquarie Strategy Source: Bloomberg, IMM, Macquarie Strategy

There is much talk of two possible wild-card outcomes that could theoretically trigger a sharp

euro upswing, but we’re not convinced:

(1) Eurozone fiscal stimulus would admittedly attract new equity inflows, boost PMIs, and

drive bond yields higher. But even if it happens, it would be small in scale, and not a

game-changer in our view. It is ironic that the countries keenest to launch stimulus (like

Italy) are those with the least scope to do so. Meanwhile, Germany is likely to remain

ideologically opposed to large-scale active stimulus outside of a deep recession scenario.

(2) We don’t hold out much hope for a hawkish policy reset at the ECB either, despite

Lagarde’s arrival as ECB President. Her promised policy review is likely to conclude that

existing accommodative settings should be maintained. Even if the wisdom of negative

interest rates is reconsidered, the same econometric models used to justify their

introduction will probably be consulted again. We see no reason why the models

should recommend a different course of action this time. The conclusion is likely to be

that negative rates are a necessary evil, and must remain in place until inflationary

pressures reappear.

1.00

1.05

1.10

1.15

1.20

1.25

Jan-16 Jan-17 Jan-18 Jan-19

EU

RU

SD

EURUSD

daily close

50dma

100dma

200dma

-250

-200

-150

-100

-50

0

50

100

150

Jan-08 Jan-11 Jan-14 Jan-17

10

00

's o

f co

ntr

acts

EUR speculative positioning

Net long

Net short

Global FX Outlook: Peak USD

19 November 2019 14

AUD, NZD: The allure of unconventional measures

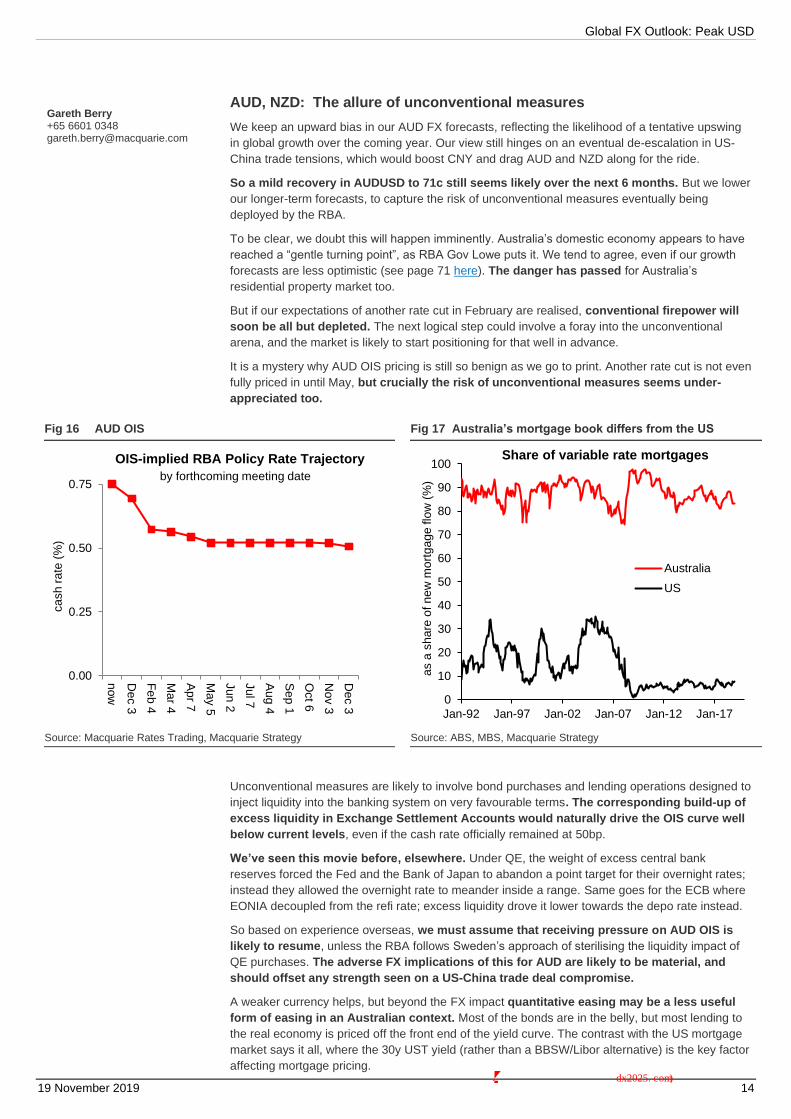

We keep an upward bias in our AUD FX forecasts, reflecting the likelihood of a tentative upswing

in global growth over the coming year. Our view still hinges on an eventual de-escalation in US-

China trade tensions, which would boost CNY and drag AUD and NZD along for the ride.

So a mild recovery in AUDUSD to 71c still seems likely over the next 6 months. But we lower

our longer-term forecasts, to capture the risk of unconventional measures eventually being

deployed by the RBA.

To be clear, we doubt this will happen imminently. Australia’s domestic economy appears to have

reached a “gentle turning point”, as RBA Gov Lowe puts it. We tend to agree, even if our growth

forecasts are less optimistic (see page 71 here). The danger has passed for Australia’s

residential property market too.

But if our expectations of another rate cut in February are realised, conventional firepower will

soon be all but depleted. The next logical step could involve a foray into the unconventional

arena, and the market is likely to start positioning for that well in advance.

It is a mystery why AUD OIS pricing is still so benign as we go to print. Another rate cut is not even

fully priced in until May, but crucially the risk of unconventional measures seems under-

appreciated too.

Fig 16 AUD OIS Fig 17 Australia’s mortgage book differs from the US

Source: Macquarie Rates Trading, Macquarie Strategy Source: ABS, MBS, Macquarie Strategy

Unconventional measures are likely to involve bond purchases and lending operations designed to

inject liquidity into the banking system on very favourable terms. The corresponding build-up of

excess liquidity in Exchange Settlement Accounts would naturally drive the OIS curve well

below current levels, even if the cash rate officially remained at 50bp.

We’ve seen this movie before, elsewhere. Under QE, the weight of excess central bank

reserves forced the Fed and the Bank of Japan to abandon a point target for their overnight rates;

instead they allowed the overnight rate to meander inside a range. Same goes for the ECB where

EONIA decoupled from the refi rate; excess liquidity drove it lower towards the depo rate instead.

So based on experience overseas, we must assume that receiving pressure on AUD OIS is

likely to resume, unless the RBA follows Sweden’s approach of sterilising the liquidity impact of

QE purchases. The adverse FX implications of this for AUD are likely to be material, and

should offset any strength seen on a US-China trade deal compromise.

A weaker currency helps, but beyond the FX impact quantitative easing may be a less useful

form of easing in an Australian context. Most of the bonds are in the belly, but most lending to

the real economy is priced off the front end of the yield curve. The contrast with the US mortgage

market says it all, where the 30y UST yield (rather than a BBSW/Libor alternative) is the key factor

affecting mortgage pricing.

0.00

0.25

0.50

0.75

now

De

c 3

Fe

b 4

Ma

r 4

Ap

r 7

Ma

y 5

Jun

2

Jul 7

Au

g 4

Se

p 1

Oct 6

No

v 3

De

c 3

ca

sh

ra

te (

%)

OIS-implied RBA Policy Rate Trajectory

by forthcoming meeting date

0

10

20

30

40

50

60

70

80

90

100

Jan-92 Jan-97 Jan-02 Jan-07 Jan-12 Jan-17

as a

sh

are

of n

ew

mo

rtg

ag

e flo

w (

%)

Share of variable rate mortgages

Australia

US

Gareth Berry +65 6601 0348 [email protected]

更多精品报告,登录东西智库网站(dx2025.com)下载

Global FX Outlook: Peak USD

19 November 2019 15

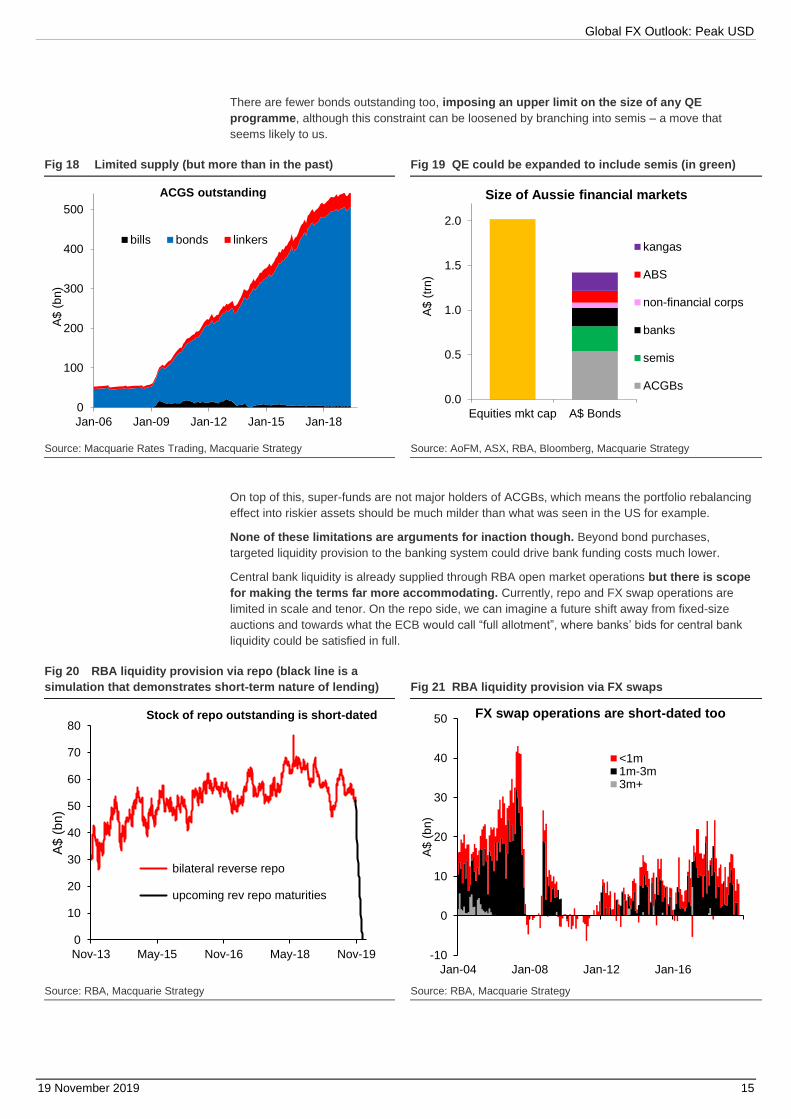

There are fewer bonds outstanding too, imposing an upper limit on the size of any QE

programme, although this constraint can be loosened by branching into semis – a move that

seems likely to us.

Fig 18 Limited supply (but more than in the past) Fig 19 QE could be expanded to include semis (in green)

Source: Macquarie Rates Trading, Macquarie Strategy Source: AoFM, ASX, RBA, Bloomberg, Macquarie Strategy

On top of this, super-funds are not major holders of ACGBs, which means the portfolio rebalancing

effect into riskier assets should be much milder than what was seen in the US for example.

None of these limitations are arguments for inaction though. Beyond bond purchases,

targeted liquidity provision to the banking system could drive bank funding costs much lower.

Central bank liquidity is already supplied through RBA open market operations but there is scope

for making the terms far more accommodating. Currently, repo and FX swap operations are

limited in scale and tenor. On the repo side, we can imagine a future shift away from fixed-size

auctions and towards what the ECB would call “full allotment”, where banks’ bids for central bank

liquidity could be satisfied in full.

Fig 20 RBA liquidity provision via repo (black line is a

simulation that demonstrates short-term nature of lending)

Fig 21 RBA liquidity provision via FX swaps

Source: RBA, Macquarie Strategy Source: RBA, Macquarie Strategy

0

100

200

300

400

500

Jan-06 Jan-09 Jan-12 Jan-15 Jan-18

A$

(b

n)

ACGS outstanding

bills bonds linkers

0.0

0.5

1.0

1.5

2.0

Equities mkt cap A$ BondsA

$ (

trn

)

Size of Aussie financial markets

kangas

ABS

non-financial corps

banks

semis

ACGBs

0

10

20

30

40

50

60

70

80

Nov-13 May-15 Nov-16 May-18 Nov-19

A$ (

bn)

Stock of repo outstanding is short-dated

bilateral reverse repo

upcoming rev repo maturities

-10

0

10

20

30

40

50

Jan-04 Jan-08 Jan-12 Jan-16

A$

(b

n)

FX swap operations are short-dated too

<1m1m-3m3m+

Global FX Outlook: Peak USD

19 November 2019 16

Tenors could be stretched too. Currently roughly 3m money is the maximum available; by

contrast, the ECB, the Bank of Japan, and the Bank of England have all supplied cash to the

banking system for up to 4 years.

Pricing could also be made extra-attractive, especially if banks could demonstrate that the

benefits were being passed on to the real economy.

If these measures are adopted and pushed to the limit, Australia’s mortgage interest rates

could fall another 100bp from current levels. Good for growth, but probably bad for the

currency.

For NZ, the policy trajectory is not dissimilar. Unconventional measures seem likely too eventually,

but an AUDNZD breakout could occur in either direction depending on which central bank

gets there first.

There are two novelties as far as NZ policy is concerned, which could make the adverse FX effect

on NZD more severe. First, Gov. Orr may have already selected negative interest rates his

preferred tool if his televised interview at Jackson Hole is any guide. By contrast the RBA has

described negative rates as “extraordinarily unlikely“, and would lean towards other measures

instead.

Second, foreigners are major holders of NZGBs too, but foreign central banks are less prevalent

than in the case of ACGBs. That means a QE programme in NZ is more likely to see

participation from foreign bond holders, leaving NZD especially exposed as foreigners decide

where to reinvest the proceeds.

更多精品报告,登录东西智库网站(dx2025.com)下载

Global FX Outlook: Peak USD

19 November 2019 17

GBP: A relief rally

We keep our upward-sloping forecast profile for sterling throughout 2020, but we no longer

project a sharp dip around next month’s December 12th general election.

Previously, our fear had been that PM Johnson would fight the election on a hard no-deal Brexit

platform, or at least that his manifesto would keep that option alive. The political incentive for

doing so was clear: it would reduce the risk of losing seats to the Brexit Party, which favours a

clean break with the EU when the UK exits.

If Johnson had failed to broadcast his Brexiteer credentials in this way, enough Brexit Party and

DUP MPs might hold the balance of power afterwards. And the possibility of a negotiated

settlement with Brussels would decline sharply. That was our fear.

But two things have changed. First, after months of fruitless negotiations, a new Brexit

withdrawal agreement has appeared out of the blue; Johnson wasn’t so keen on a hard Brexit after

all, it seems, despite all the rhetoric to the contrary.

Second, the Brexit Party has failed to capitalise on Johnson’s decision to cut a deal. The

deal offers less than a ‘pure’ Brexit, and yet opinion polls indicate that support for the Brexit Party

is dwindling not increasing. In the eyes of voters sympathetic to the Brexit cause, it seems that

Johnson’s deal will do, despite its imperfections.

So the risk of a hard no-deal Brexit has materially receded. Whether sterling can build on

recent gains will depend hugely on the outcome of the forthcoming general election on December

12th. But early signs are encouraging.

Sterling would prefer a stable overall majority for PM Johnson’s Conservative Party. This is also

our base case. Opinion polls show Conservative support is hovering around the magic 40%

which, under the first-past-the-post electoral system, is usually enough to deliver an overall

majority, although does not guarantee it.

Such an outcome would be seen as a public endorsement of the new deal. There would be

no more obstruction by an uncooperative parliament afterwards either. Following parliamentary

ratification, the UK would leave the EU in a legal and political sense on (or even before) Jan 31st,

when the new Article 50 deadline expires.

But unlike the three previous cliff-edges, there would be no risk of an economic shock this

time. Under the terms of the deal, bilateral trade with the EU would remain frictionless at least until

the ‘transition period’ ends on Dec 31st, 2020.

There is in fact no transition; it is a misnomer coined out of political necessity; a ‘standstill

arrangement’ would be a better description. Economically-speaking, everything stays the same

immediately after exit.

Fig 22 Support for the four main parties in opinion polls Fig 23 GBP FX vol is off the highs

Source: Bloomberg, Macquarie Strategy Source: Wikipedia, Macquarie Strategy

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Jun-19 Jul-19 Aug-19 Oct-19

Opinion Polls

Cons LabourLib Dems Brexit Party 6

7

8

9

10

11

12

13

14

May-18 Sep-18 Jan-19 May-19 Sep-19

atm

vo

l (%

)

GBPUSD atm 6m FX vol

First 2 cliff-edges pass without incident

Johnson'snew deal is done

Gareth Berry +65 6601 0348 [email protected]

Eimear Daly +44 20 3037 4802 [email protected]

Global FX Outlook: Peak USD

19 November 2019 18

So if we’re right, the UK could finally move on out of the Brexit quicksand. But more cliff

edges would lie ahead, the first appearing only 11 months later when standstill arrangements

expire.

There is almost zero chance that a full free-trade agreement will be in place before then, so this

deadline will likely be extended too, but probably not without another nervous countdown.

That’s one reason why we see a meaningful, but not explosive, sterling upswing ahead.

The second reason is that corporate investment is likely to remain subdued until the precise terms

of the future trading arrangements have been nailed down. This explains in part why Bank of

England forecasts were downgraded last week, and why the market sees a material risk of a rate

cut over the coming months.

Under the withdrawal deal, Northern Ireland will remain to all intents and purposes inside the EU.

But the island of Great Britain (GB) can let its trade rules diverge from the EU, up to a point. The

degree matters greatly. If GB tries to undercut EU’s regulatory standards, there would be a price

to pay in the form of increased trade frictions with the EU. Border checks would become more

intrusive. The tariff wall would rise.

So for corporate UK, the uncertainty will go on – probably for years. But at least the risk of an

acrimonious hard no-deal Brexit would have almost vanished, and that’s reason enough to

imagine some moderate further sterling upside from here.

Suffice it to say, there are no certainties in democratic elections, especially one as emotive as this

one. It has been so dominated by a single issue that traditional party allegiances cannot be taken

for granted. Even in normal times, opinion polls are not very reliable.

So another hung parliament is a very material risk (40%), though not our base case. We examine

the FX consequences if the hung scenario on page 17-18 here.

更多精品报告,登录东西智库网站(dx2025.com)下载

Global FX Outlook: Peak USD

19 November 2019 19

JPY: Rally on hold

We raise our near-term USDJPY forecasts, to reflect the likelihood of a partial US-China trade deal

over the coming months. Escalating trade tensions had previously driven USDJPY sub-105,

but the selling pressure has now subsided amid signs of progress in negotiations.

Stable US policy settings should relieve some downside pressure on USDJPY too. After three rate

cuts, the Fed has made it clear that further easing is not a foregone conclusion. We expect the US

policy rate to remain unchanged for all of 2020 and 2021 (see page 53 here).

The prospect of a cyclical global mini-upswing should also help support USDJPY, and new highs

by US equities are providing constructive mood music.

Meanwhile bond outflows from Japan-based investors show little sign of stopping, and

equity outflows are now reaccelerating having cooled earlier. These flows should keep

USDJPY supported around current levels, and any dips on temporary setbacks in US-China

negotiations could be seen as buying opportunities.

Fig 24 Japan bond outflows continue unabated

Fig 24 Appetite for foreign equities increasing again too

Source: Bloomberg, Macquarie Strategy Source: Bloomberg, Macquarie Strategy

But a delayed yen rally still looks likely, as US political risks intensify into the Nov 2020

Presidential election. Any resulting USD weakness would be most keenly felt in USDJPY – just

as it was into the previous 2016 election, although the Bank of Japan’s foray into negative rates

territory earlier that year would have amplified that move.

Once the yen rally gets underway, Tokyo should be mostly powerless to stop it. US President

Trump’s has taken a personal interest in the economic policy of trading partners, which means

there is a very high hurdle for Japanese authorities to weaken the yen via FX intervention.

Monetary policy options are very limited too. The Bank of Japan already owns almost half of

the JGB market, and is already the biggest shareholder in a number of single-name equities.

Another rate cut could be counter-productive if used, ultimately boosting the yen instead of

weakening it.

0

10

20

30

40

50

60

70

80

Jan-11 Jan-13 Jan-15 Jan-17 Jan-19

JP

Y (

trn

)

Net Buying of Foreign BondsBy Japanese investors, cumulative

bond outflows abroad

past 12m

initial launchof QQE

negative rates introduced

-20

-10

0

10

20

30

40

Jan-11 Jan-13 Jan-15 Jan-17 Jan-19

JP

Y (

trn

)

Net Buying of Foreign Equities By Japanese investors, cumulative

equities outflows abroad

past 12m

initial launch of QQE

negative rates introduced

Gareth Berry +65 6601 0348 [email protected]

Global FX Outlook: Peak USD

19 November 2019 20

CAD: Rates Cuts Will Undermine the Loonie’s Strength

As we noted back in September’s Global FX Outlook, we haven’t been surprised by the BoC’s

decisions to maintain its neutral tone over during the summer months and well into October.

After all, the data was not deteriorating yet, and Canada was likely going to need to get though

its federal election before the BoC would be comfortable “stepping out” of its comfort zone.

However, we’ve believed that the global rate-cutting cycle would eventually visit the BoC in Ottawa,

even though it might come after it brought glad tidings to all the other major central banks – the Fed,

ECB, RBA, RBNZ, etc. We now believe that the BoC will ease its overnight lending rate (OLR) in

January (our baseline), although we wouldn’t dismiss a cut in the policy rate coming in December,

either. What are the Governing Council’s motivations for an OLR cut (from the current OLR of

1.75%)? In our view, it is not so much that the BoC would be compelled by an upcoming

event, but rather that the bar for a cut is already set low in view of a soft outlook for 2020,

allowing even a drift downward in the data to provide cover for a cut.

Indeed, we believe we’ve seen the BoC already prepare the market for a cut. In its October

Statement, the concluding paragraph removed two key lines that had been construed as hawkish,

i.e., that i) “the economy is operating close to potential and inflation is on target”, and that ii) “the

current degree of monetary stimulus remains appropriate”. Governor Poloz even suggested in his

October press conference that an “insurance rate cut” was discussed by the Governing Council, but

that two factors led to the decision to hold, i) inflation being at the midpoint of the target range, and

ii) strength in housing data suggesting a potential rise in financial vulnerabilities. And consistent with

the more dovish tone, the BoC further downgraded its 2020 real GDP forecast (Q4 on Q4 basis) to

1.6% from 2.0% previously. This downgrade was motivated mainly by a smaller contribution from

business investment and exports, areas that the BoC has proven to be overly optimistic about in the

past.

And yet despite this downgrade, the BoC remains still too optimistic in the view of economist

David Doyle. The BoC’s 2020 growth forecast remains both above the consensus (1.5%) and

David’s own projection for 2020 growth (1.2%). Notwithstanding that, the BoC’s forecast over the

coming 18 months suggests growth that will be below potential growth – even after the BoC cut its

own estimate of potential growth to 1.7% (from 1.9% previously), suggesting a widening output gap.

In our view, this all means that there is very a low bar for cut. That is, if data comes in tad

weaker than the BoC anticipates, or we see any development that would push its growth

forecast toward our own or toward the consensus, the Governing Council will cut in

response. Alternatively, the same response could come out of inflation coming in below projections

in coming months. Core inflation, David believes, has been driven by idiosyncratic categories that

should moderate ahead. Indeed, the BoC seems to know this, insofar as it dropped from its

September policy Statement the line that said “inflation is expected to return sustainably to 2% by

mid-2020”. A reassessment of the convergence theme could be used to justify easier policy. And

finally, we will note that Canada’s yield curve remains (partly) inverted, which has itself provided a

rationale for a cut, in previous cycles. Either way, there’s enough here to suggest that a rate cut

happens by December, or likelier by January.

What about beyond the next few weeks? Well, for one thing, Canada is not escaping the global

manufacturing slowdown, as the structural decline in auto production continues to intensify. Mexico’s

ongoing decline in auto production(see our section on Mexico’s MXN, below) portends a slowdown

in Canada’s too, and passage of the USMCA in the US Congress will not turn things around, but

only cement the status quo, at best. Indeed, the prospect that manufacturing may slow further

underscores our view that the strength seen in Q2’s real GDP growth (3.7% annualized) is

temporary, as the BoC itself had acknowledged.

Nor will Canada escape a slowdown in its housing market, which is among the principal

reasons for growth in 2020 to disappoint. The typical behavior of the Canadian consumer has

been to use the benefit of a lower mortgage rates over several decade to renovate their existing

home, or “move-up” into a more expensive dwelling. This has helped propel home prices higher

relative to incomes and contributed to residential investment’s rise as a share of GDP. But following

the BoC’s rate hikes in 2017-18, the three-decade tailwind behind growth in housing will shift

to headwinds, as mortgage resets begin to take a bite out of household budgets in 2020 and

2021 - unless interest rates revert back to new lows. (The typical fixed-rate period for a Canadian

Thierry Wizman +1 212 231 2082 [email protected]

更多精品报告,登录东西智库网站(dx2025.com)下载

Global FX Outlook: Peak USD

19 November 2019 21

mortgage is five years, and the current five-year Canada yield suggests rates should reset higher in

2020 by roughly 70 bps.)

It is this structure of Canada’s mortgage market that will put the BoC in a difficult position in 2020,

especially if a further rise in US bond yields drags the Canada five-year yield higher, leading to

meaningful increases in mortgage rates upon resets. So although housing data in Canada has

improved in recent months, with yields backing up again there will be ever smaller support

for the economy from the demand for housing and the ancillary wealth-effects that might

bring.

To offset this, David believes that the BoC will be inclined to remain dovish in its rhetoric in

2020 and cut rates by a total of 50 bps in total in 2020, starting in January. Along the way, this

dovishness will be supported by the BoC lowering its own estimate of the “neutral” rate (from 2.25%,

currently) although this may not happen until April’s. Our own view is that the neutral rate is much

lower than the BoC’s estimate, a consequence of elevated housing and corporate debt, an over-

reliance on residential investment, and lower potential output growth in Canada. A policy rate of

1.5%, in our view, is close to ‘neutral.

.

Fig 26 Canada’s forward yield curve will invert further

Fig 27 …and the US vs CA yield spread will widen

Source: Bloomberg LP Source: Bloomberg LP

And what does this all mean for the CAD? Well, up until now, the CAD has been supported nicely

by a Canadian policy rate that has risen relative to the US policy rate, as the US policy rate was

reduced by three times this year, starting in July. But we anticipate that this will switch in 2020, as

Canadian rates decline relative to the US and reverse 2/3rds of the spread compression on the past

six months. (US rates, we expect, will stay unchanged throughout 2020). In conjunction with this, we

expect that the spread between US vs. Canadian government yields – in the tenors that correspond

to the policy horizon - will expand again (see Figure, above). That will also reverse a trend set in

motion in March 2020 as traders began to anticipate the US’s rate easing in March 2019. Canada’s

forward policy-rate curve will invert further, perhaps even as the US’s flattens (see Figure above).

As this happens, the CAD’s footings will be kicked from under it – even as the USD weakens

vs. some non-CAD currencies - and we expect that USD/CAD will begin a slow but long-

anticipated move higher, toward 1.36 and ultimately 1.40 in the longer term. We’ll remind

readers again that among the most important determinants of the USD/CAD pair since the

great financial crisis has been the spread between US and Canada yields in the belly of the

curves.

Global FX Outlook: Peak USD

19 November 2019 22

EM FX Asia: A change of fortune

Our top-down view for receding US-China trade war and Brexit risks, combined with a gentle pick

up in global growth in 1H 2020 suggests for a favourable backdrop for EM FX.

Within Asia, we expect North Asia currency bloc (CNY, KRW and TWD) to outperform in

2020, reversing their misfortunes in 2018 and 2019.

Conditions for CNY, KRW and TWD outperformance are supported by 1/ a more credible de-

escalation phase in US and China trade war in 2020, 2/ A rebound in global growth and step-up in

China stimulus, and 3/ Stabilization in tech demand and core export products.

The turning point is probably already in. The total return gap between an equally weighted

basket of North Asia currencies - CNY, KRW and TWD versus a carry basket – as proxied by INR

and IDR bottomed in early October.

Importantly, we show below that this return gap is highly correlated with the direction of US

10 yield. This makes intuitive sense to us, as a sharp drop in US yields since late 2018 reflected

broader concerns on global growth and escalation in US-China trade war – both detrimental for the

more export-geared North Asian economies. In contrast, the subsequent global chase for yields

benefited INR and IDR disproportionately by boosting inflows into their local currency markets.

Fig 28 USD backdrop should turn more favourable for EM Asia more broadly into 2020

Fig 29 We expect KRW, CNY and TWD to outperform in 2020 following 2 years of underperformance

Source: Bloomberg, Macquarie Strategy Source: Bloomberg, Macquarie Strategy

Fig 30 The gap between North Asia vs. Carry Asia have bottomed in October

Fig 31 A rebound in US 10y a good leading indicator for North Asia outperformance

Total returns index, equally weighted baskets Total returns index, equally weighted baskets

Source: Bloomberg, Macquarie Strategy Source: Bloomberg, Macquarie Strategy

75

80

85

90

95

100

105

110

115

120

08 09 10 11 12 13 14 15 16 17 18 19

Asia FX and DXY, index to Jan 2018

DXY index

USDAsia, equally w eighted basket

-5.0% 0.0% 5.0% 10.0%

THB

IDR

PHP

INR

MYR

SGD

TWD

CNH

KRW

Total returns against USD, %

2018

YTD

89

91

93

95

97

99

101

103

Jan 18 Apr 18 Jul 18 Oct 18 Jan 19 Apr 19 Jul 19 Oct 19

Performance gap between North Asia vs. high yielders complex

High yielding basket (INR, IDR)

North Asia basket (KRW,

CNY, TWD)

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0.88

0.93

0.98

1.03

1.08

1.13

1.18

1.23

12 13 14 15 16 17 18 19

%Performance gap between North Asia vs. high

yielders complex

US 10y yield, % (RHS)

North Asia vs. High Yielders

total return gap

Trang Thuy Le +852 3922 2113 [email protected]

更多精品报告,登录东西智库网站(dx2025.com)下载

Global FX Outlook: Peak USD

19 November 2019 23

KRW, in particular, should benefit from its high “beta” proxy to global growth, a return of equity

inflows (which have lagged others in the region YTD), and a bottoming in the memory price cycle –

a key factor we previously said would turn us more constructive on the won. There are also green

shoots when it comes to Korea’s shipping industry.

Our equity analyst Daniel Kim sees a recovery in DRAM/NAND prices in 2020 with inventory from

key players normalizing, while demand picks up from an acceleration in data-center traffic and 5G-

enabled smartphones. Memory accounts for more than 10% of Korea’s exports, and its price

slump was the key behind Korea’s nominal export and won underperformance in recent years.

That being said, any pick-up in the economy will be gradual, and Korea’s growth in 1H 2020 may

still fall well short of BoK 2.6% forecast and its estimate of growth potential (2.7%-2.8%). This

leaves open the possibility of another rate cut in 1Q 2020 to 1%, an all-time low. However, we are

not too concerned on the effect of an extra rate cut on the won. KRW correlation to equity has

traditionally overwhelmed its correlation to relative interest rate spreads.

Korea’s legislative election (15 April 2020) could be seen as a public referendum for Moon’s

political agenda ahead of the 2022 Presidential Election. A weak economy has been the key

complaint for his administration. Moon currently does not hold a parliament majority, and failure to

make progress could lead to more uncertainty in economic policy in the 2nd half of his 5-year term.

A major shake-up of BoK MPC will also take place in April. 4 out of 7 MPC board members are

expected to depart, including the two most dovish voices – Cho Dongchul and Shin Inseok, but

also the most hawkish member Lee Il Houng. A rate cut, if any, is likely to take place ahead of this

reshuffle.

Fig 325 Terms of trade shock dissipating for Korea

Fig 33 Bottoming of memory price cycle implies better outlook for exports and the won ahead

Macquarie equity team estimate.

Source: Bloomberg, CEIC, Macquarie Strategy Source: CEIC, Macquarie Strategy

TWD will benefit from a rebound in tech cycle driven by smartphone and data-center growth, but

the extent of its tech export rebound should be more modest than Korea. Better product mix

means Taiwan’s tech exports was not hit as badly in 2019 as Korea’s, implying a higher base.

TWD’s resilience in 2019 has also come from a big investment relocation shift – as companies re-

shored and government introduced tax and investment incentives to attract repatriation. But the

momentum here also appears to be slowing into 2H 2019.

TWD’s advantage comes from its huge current account surplus (>10% of GDP) – and an insurance

sector running close to its regulatory cap on foreign assets, implying receding domestic capacity to

recycle the current account balance.

Bond ETF has proven to be a new channel for lifers to bypass regulatory limit, but this is also

facing regulatory scrutiny. Bond ETFs are locally traded and denominated in TWD, although they

are made up primarily of US bonds and US credit. Exhaustion of bond ETF channel will lead to

structural TWD strength, although we will be patient for this theme to play out later in 2020 or

even 2021.

90.0

95.0

100.0

105.0

110.0

115.0

120.0

80.0

85.0

90.0

95.0

100.0

105.0

110.0

10 11 12 13 14 15 16 17 18 19

IndexIndexKRW and terms of trade

KRW effective exchange rate (RHS)

Terms of trade index

-30%

-20%

-10%

0%

10%

20%

30%

Mar 16 Dec 16 Sep 17 Jun 18 Mar 19 Dec 19 Sep 20

US$/1Gb Memory average selling price, %qoq

Forecast

NAND

DRAM

Global FX Outlook: Peak USD

19 November 2019 24

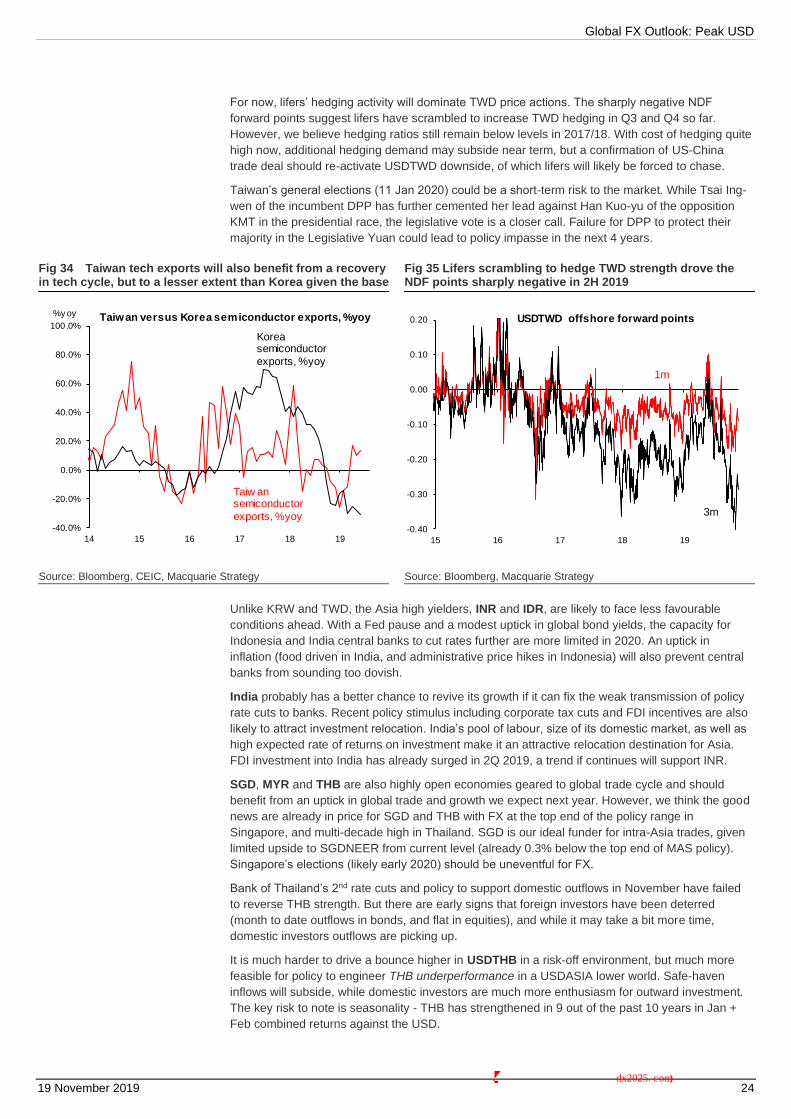

For now, lifers’ hedging activity will dominate TWD price actions. The sharply negative NDF

forward points suggest lifers have scrambled to increase TWD hedging in Q3 and Q4 so far.

However, we believe hedging ratios still remain below levels in 2017/18. With cost of hedging quite

high now, additional hedging demand may subside near term, but a confirmation of US-China

trade deal should re-activate USDTWD downside, of which lifers will likely be forced to chase.

Taiwan’s general elections (11 Jan 2020) could be a short-term risk to the market. While Tsai Ing-

wen of the incumbent DPP has further cemented her lead against Han Kuo-yu of the opposition

KMT in the presidential race, the legislative vote is a closer call. Failure for DPP to protect their

majority in the Legislative Yuan could lead to policy impasse in the next 4 years.

Fig 34 Taiwan tech exports will also benefit from a recovery in tech cycle, but to a lesser extent than Korea given the base

Fig 35 Lifers scrambling to hedge TWD strength drove the NDF points sharply negative in 2H 2019

Source: Bloomberg, CEIC, Macquarie Strategy Source: Bloomberg, Macquarie Strategy

Unlike KRW and TWD, the Asia high yielders, INR and IDR, are likely to face less favourable

conditions ahead. With a Fed pause and a modest uptick in global bond yields, the capacity for

Indonesia and India central banks to cut rates further are more limited in 2020. An uptick in

inflation (food driven in India, and administrative price hikes in Indonesia) will also prevent central

banks from sounding too dovish.

India probably has a better chance to revive its growth if it can fix the weak transmission of policy

rate cuts to banks. Recent policy stimulus including corporate tax cuts and FDI incentives are also

likely to attract investment relocation. India’s pool of labour, size of its domestic market, as well as

high expected rate of returns on investment make it an attractive relocation destination for Asia.

FDI investment into India has already surged in 2Q 2019, a trend if continues will support INR.

SGD, MYR and THB are also highly open economies geared to global trade cycle and should

benefit from an uptick in global trade and growth we expect next year. However, we think the good

news are already in price for SGD and THB with FX at the top end of the policy range in

Singapore, and multi-decade high in Thailand. SGD is our ideal funder for intra-Asia trades, given

limited upside to SGDNEER from current level (already 0.3% below the top end of MAS policy).

Singapore’s elections (likely early 2020) should be uneventful for FX.

Bank of Thailand’s 2nd rate cuts and policy to support domestic outflows in November have failed

to reverse THB strength. But there are early signs that foreign investors have been deterred

(month to date outflows in bonds, and flat in equities), and while it may take a bit more time,

domestic investors outflows are picking up.

It is much harder to drive a bounce higher in USDTHB in a risk-off environment, but much more

feasible for policy to engineer THB underperformance in a USDASIA lower world. Safe-haven

inflows will subside, while domestic investors are much more enthusiasm for outward investment.

The key risk to note is seasonality - THB has strengthened in 9 out of the past 10 years in Jan +

Feb combined returns against the USD.

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

14 15 16 17 18 19

%y oy Taiwan versus Korea semiconductor exports, %yoy

Korea semiconductor

exports, %yoy

Taiw an semiconductor

exports, %yoy-0.40

-0.30

-0.20

-0.10

0.00

0.10

0.20

15 16 17 18 19

USDTWD offshore forward points

1m

3m

更多精品报告,登录东西智库网站(dx2025.com)下载

Global FX Outlook: Peak USD

19 November 2019 25

Fig 36 India should focus on policy transmission of rate cuts to banks in 2020

Fig 37 Ex-China pick-up in FDIs are concentrated in Singapore, India and Indonesia

Source: Macrobond, Macquarie Strategy Source: CEIC, Macquarie Strategy

Relative to SGD and THB, MYR has a better chance to benefit from a rebound in global growth

with its REER largely in line with fundamentals. Palm prices have surged 24% in 3Q, implying

better terms of trade support. However, we suspect the pending FTSE Russell decision on

Malaysia’s bonds exclusion from its flagship WGBI index will still weigh on sentiment, limiting

foreign inflows and capping MYR performance relative to others in 1H 2020.

PHP is likely to drop from the top 3 in the EM Asia FX ranking table this year to the middle of the

pack in 2020. PHP strength in 2019 was a result of a recovery from an inflation and growth shock

in 2018, supportive real rates, and lower current account deficit due to delayed Budget spending.

These tailwinds could turn into headwinds in 2020, with the current account deficit likely re-

widening to above 2% of GDP, while inflation should tick up from a low base in 2019. BSP liquidity

easing could also stimulate capital outflows.

Fig 38 MYR seems more fairly valued, but FTSE pending decision could limit foreign interests into bonds

Fig 39 THB REER at multi-decade high calls for greater policy resistance

Fair value based on crude prices and rolling trend

Source: Bloomberg, CEIC, Macquarie Strategy Source: Bloomberg, Macquarie Strategy

8.0

8.5

9.0

9.5

10.0

10.5

11.0

11.5

12.0

12.5

13.0

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

12 13 14 15 16 17 18 19

%%India Interest Rates

WALR for fresh rupee loans (RHS)**

Repo rate(LHS)

WALR for outstanding rupee loans (RHS)**

*Weighted-average domestic term deposit rate**Weighted-average lending rate

WADTDR for outstanding rupee term deposit (LHS)*

-15 -10 -5 0 5 10

MYR

PHP

TWD

KRW

VND

THB

IDR

INR

SGD

CNY

$bn

Difference in gross FDI versus trend, $bn

(*) Linear trendfrom 2010 to 2017

4q moving average

2Q 2019

78

83

88

93

98

103

108

113

08 09 10 11 12 13 14 15 16 17 18 19

IndexMYR REER valuation

Trend line

MYR REER

+/-2 stdev

70

75

80

85

90

95

100

105

110

115

120

95 98 01 04 07 10 13 16 19

THB REER

Global FX Outlook: Peak USD

19 November 2019 26

EMEA: The risk-reward weighing scales

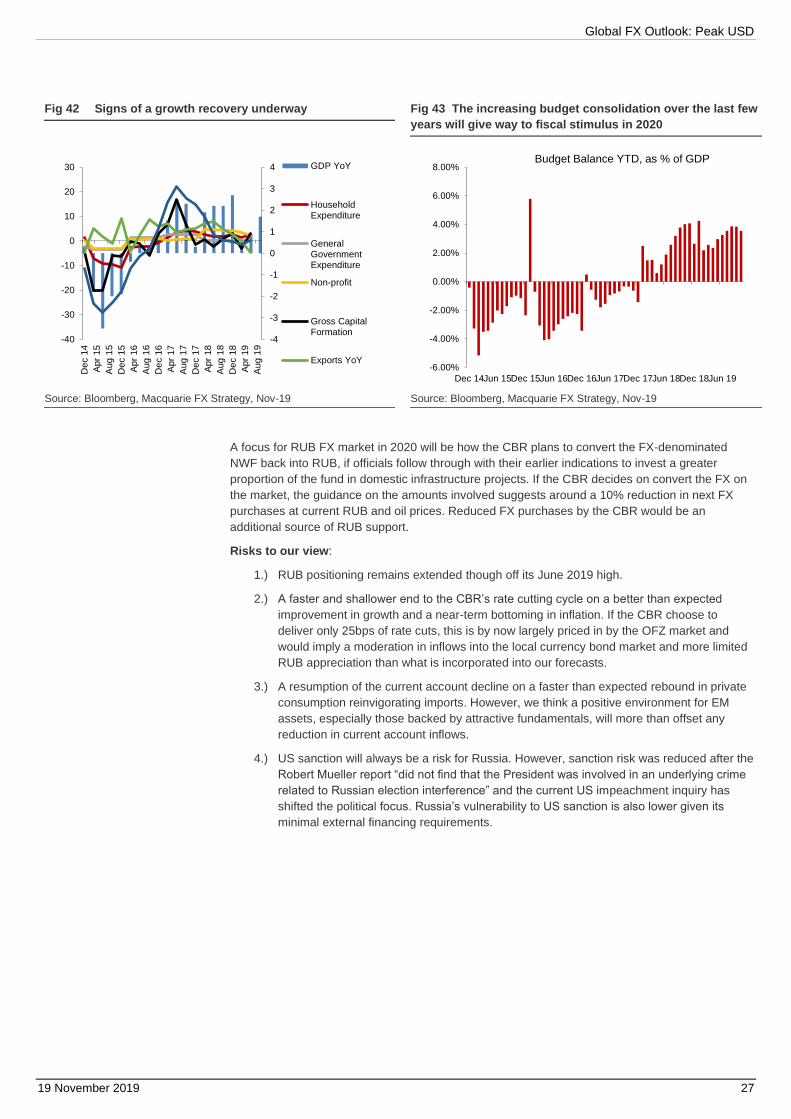

RUB: Ready, steady, rally

We are constructive on the RUB due to our expectation of a stronger EUR into 2020, fiscal

loosening extending the RUB’s relatively growth differential, further Central Bank of Russia rate

cuts driving foreign inflows into OFZ’s and still high real yield relative to other EMs. We forecast

USDRUB at 54 and 55 by end 2020 and 2021, respectively.

1.) We expect the EUR to appreciate modestly against the USD. Macquarie projects the

euro to appreciate to 1.15 versus USD by end-2020 and to 1.17 by end-2021.

2.) A 2020 growth recovery is to be driven by a pick-up government investment and, to