Embed Size (px)

Citation preview

GLOBAL FUND DISTRIBUTION 2017

Distribution snapshots

Number of cross-border funds 11,732Compound annual growth rate over 10 years 7.1%

Number of cross-border registrations 96,548Compound annual growth rate over 10 years 8.3%

Top target market for distribution, AmericasTotal number of new registrations

21Curaçao

Top target market for distribution, EuropeTotal number of new registrations

684United Kingdom

Cross-border distributionDomicile share of authorisationsfor cross-border distribution

63.6% Luxembourg

Top target market for distribution, Asia PacificTotal number of new registrations

169Singapore

Top target market for distribution, Middle EastTotal number of new registrations

6Saudi Arabia

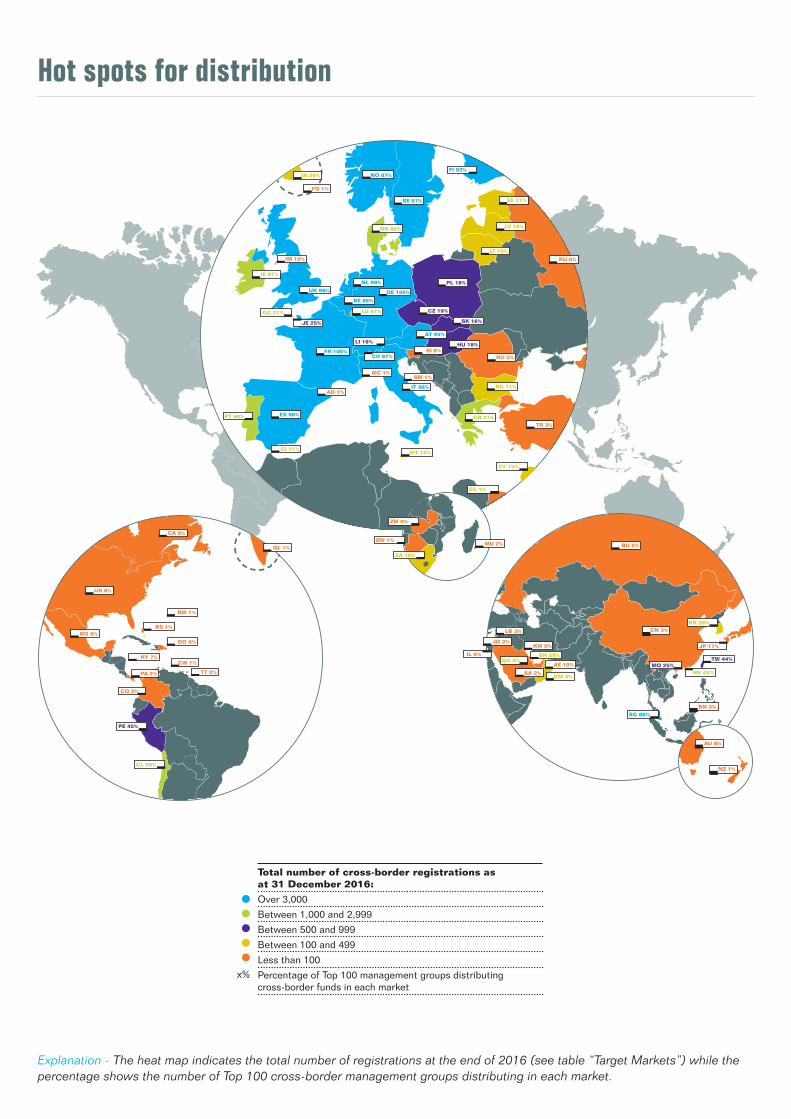

Hot spots for distribution

Total number of cross-border registrations as at 31 December 2016:

Over 3,000

Between 1,000 and 2,999

Between 500 and 999

Between 100 and 499

Less than 100

Percentage of Top 100 management groups distributing cross-border funds in each market

x%

Explanation - The heat map indicates the total number of registrations at the end of 2016 (see table “Target Markets”) while the percentage shows the number of Top 100 cross-border management groups distributing in each market.

TT 2%

CW 1%

MX 6%

US 8%

PA 2%

CO 3%

KY 7%

DO 0%

BS 1%

BM 1%

CL 59%

PE 45%

CA 6%

GL 1%

HK 44%

SG 86%

MO 25%

KR 28%

JP 17%

BH 29%

SA 2%OM 3%

QA 4%

KW 0%

AE 10%

JO 2%

LB 3%

IL 0%TW 44%

RU 0%

AU 8%

BN 3%

NZ 1%

CN 3%

JE 25%

GG 21%

CH 97%

LI 19%

DE 100%

AT 95%

FR 100%

MC 1%SM 1%

NL 99%

UK 99%

ES 98%

GI 11%

IT 98%

SE 97%

DK 80%

FI 93%NO 87%

BE 86%

LU 97%

PT 60%

CZ 19%

SK 16%

GR 27%

IE 81%

PL 18%

EE 11%

LV 10%

RU 0%

LT 10%

IS 20%

HU 18%

MT 15%

IM 10%

FO 1%

BG 11%

RO 5%

TR 3%

SI 8%

MU 2%

AD 1%

ZA 10%

BW 1%

ZM 0%

CY 15%

EG 1%

Evolution of UCITS net sales and AuM

Source: EFAMA and PwC analysis, 31 December 2016

Source: EFAMA and PwC analysis, 31 December 2016

* The large change for France is due to change in EFAMA methodology that took place in Q4 2014. For further details please see EFAMA Quarterly release Q1 2015, segment on UCITs versus AIF.

UCITS funds net sales

Europe

Luxembourg

Ireland

-100

0

100

200

300

400

500

600EUR bn

0

200

400

300

100

500

600

-100

2011 2012 2013 2014 2015 2016

-90

197229

464

573

275

-24

97

153

228

264

736291

56

11296

117

UCITS Assets* - Top European domiciles

Luxembourg

France

Ireland

United Kingdom

2010 2011 2012 2013 2014 2015 2016

1,500

2,500

3,000

3,500

0

500

2,000

1,000 759

1,210

1,760

2,002

2,198

1,881

639 631747

863995

1,083 1,084

2,643

2,9473,116

1,4471,579

1,068 1,116 1,1111,146

763 796

820968 1,044

1,274

+1,235

-414

+820

+445

EUR bn AuM Growth

Evolution of cross-border distribution

Top 5 destinations of leading fund domiciles:

Sources: Lipper LIM and PwC analysis, 31 December 2016 Note: Only true cross-border funds were taken into account - i.e. funds distributed in at least three countries, including their domicile

Number of cross-border funds and registrations

Average registrations per true cross-border fund

5.8 7 7.3 7.6 7.7 7.9 7.9 7.7 7.7 7.8 8 8.1 8.2

Num

ber

of

cross

-bord

er

fund

s

0

20,000

40,000

30,000

10,000

60,000

80,000

70,000

50,000

90,000

100,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 20162004 2005 2006

8,000

10,000

6,000

4,000

2,000

0

12,000

7,9076%7,441

1%

8,5118%

9,43611%

7,36613%

6,52510%

5,90714%

9,8695%

10,4306%

11,2228%

11,7324%

5,1706%

4,8758%

Funds Domicile:

Luxembourg

Ireland

United Kingdom

France

Jersey

Other

Number of true cross-border funds

IrelandRegistrations in:

United Kingdom 2,447

Germany 2,141

France 1,992

Netherlands 1,710

Switzerland 1,689

LuxembourgRegistrations in:

Germany 4,928

Switzerland 4,431

Austria 4,395

France 4,294

United Kingdom 3,651

Funds Domicile:

Luxembourg

Ireland

United Kingdom

France

Jersey

Other

Number of true cross-border funds

Domicile share of authorisations for cross-border distribution

64%

3%

24%

3% 2%

4%

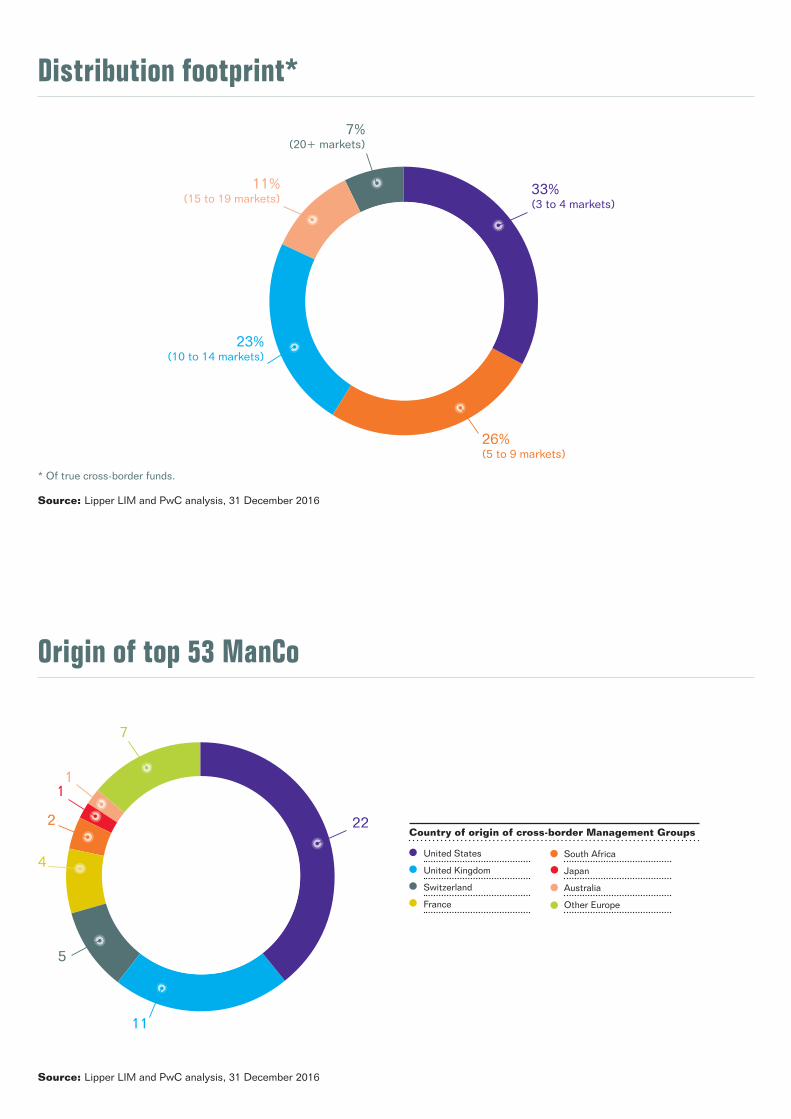

Number of cross-border registrations 96,548

Compound annual growth rate over 10 years 8.3%Number of cross-border funds 11,732

Compound annual growth rate over 10 years 7.1%

Distribution footprint*

* Of true cross-border funds.

Source: Lipper LIM and PwC analysis, 31 December 2016

Origin of top 53 ManCo

Source: Lipper LIM and PwC analysis, 31 December 2016

33% (3 to 4 markets)

7%(20+ markets)

26% (5 to 9 markets)

11%(15 to 19 markets)

23%(10 to 14 markets)

United States

United Kingdom

Switzerland

France

South Africa

Japan

Australia

Other Europe

Country of origin of cross-border Management Groups22

7

11

2

4

5

11

Benchmarking cross-border distribution

Asset classes

Sources: Lipper LIM and PwC analysis, 31 December 2016

Sources: Lipper LIM and PwC analysis, 31 December 2016

Change in number of funds from 2015 to 2016

Breakdown of the number of registrations by investment strategy (top 15 strategies)

0

3000

6000

9000

12000

15000

3,000

0

Number of registrations

Equity Europe

Equity G

lobal

Bond Europe

Equity Specifi

c Secto

r

Equity U

S

Equity Emerging M

arkets

Equity Asia

Pacific

Bond Global

Mixed Asse

t Europe

Bond Emerging Mark

ets

Bond US

Alternati

ve

Equity Jap

an

Absolute Return

Mixed Asse

t US

14,000

12,000

9,000

6,000

2016

2015

Change in number of cross-border funds vs number of funds in 2016 (top 15 strategies)

0

20

40

60

80

100

0

20

40

60

80

100

Equity G

lobal

Equity Europe

Equity U

S

Mixed Asse

t Europe

Alternati

ve

Bond Global

Bond Europe

Absolute Return

Bond US

Target M

aturity

Bond China

Mixed Asse

t US

Bond Emerging Mark

ets

Equity Jap

an

Loan Part

icipati

on Funds

1,515 728 1,141 388 442 612 790 260 1,013 290 201 357 12 86 29Number of funds in 2016

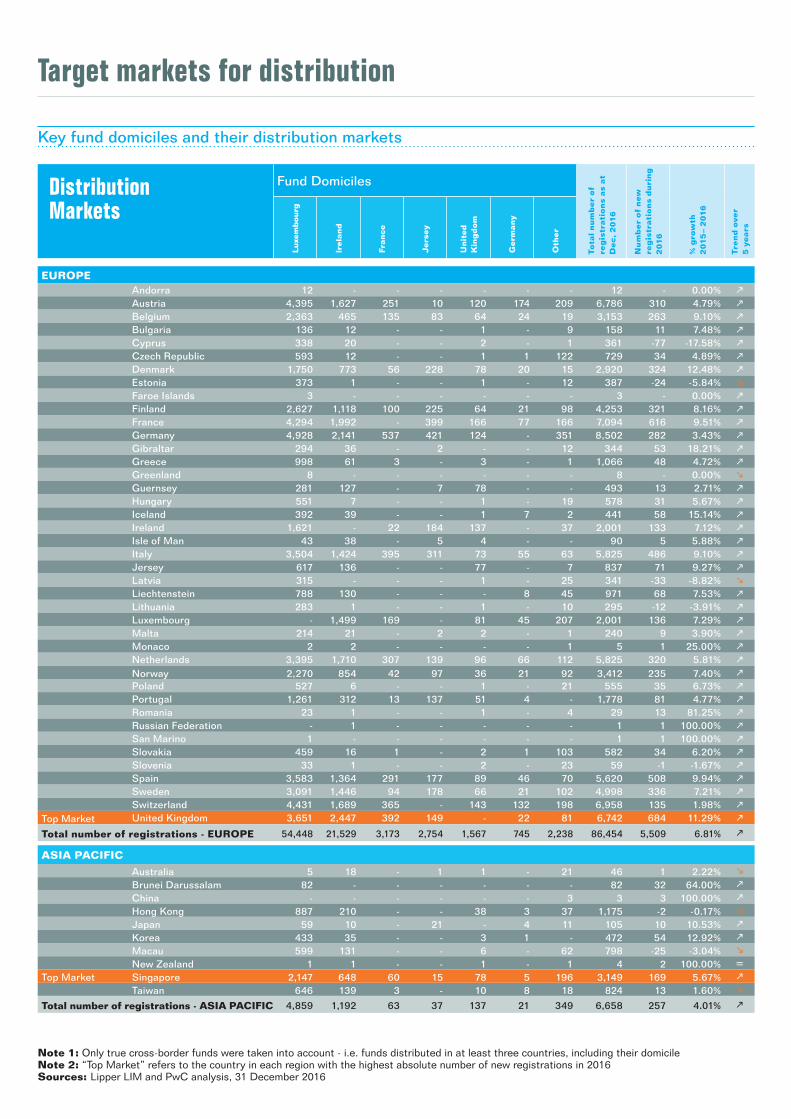

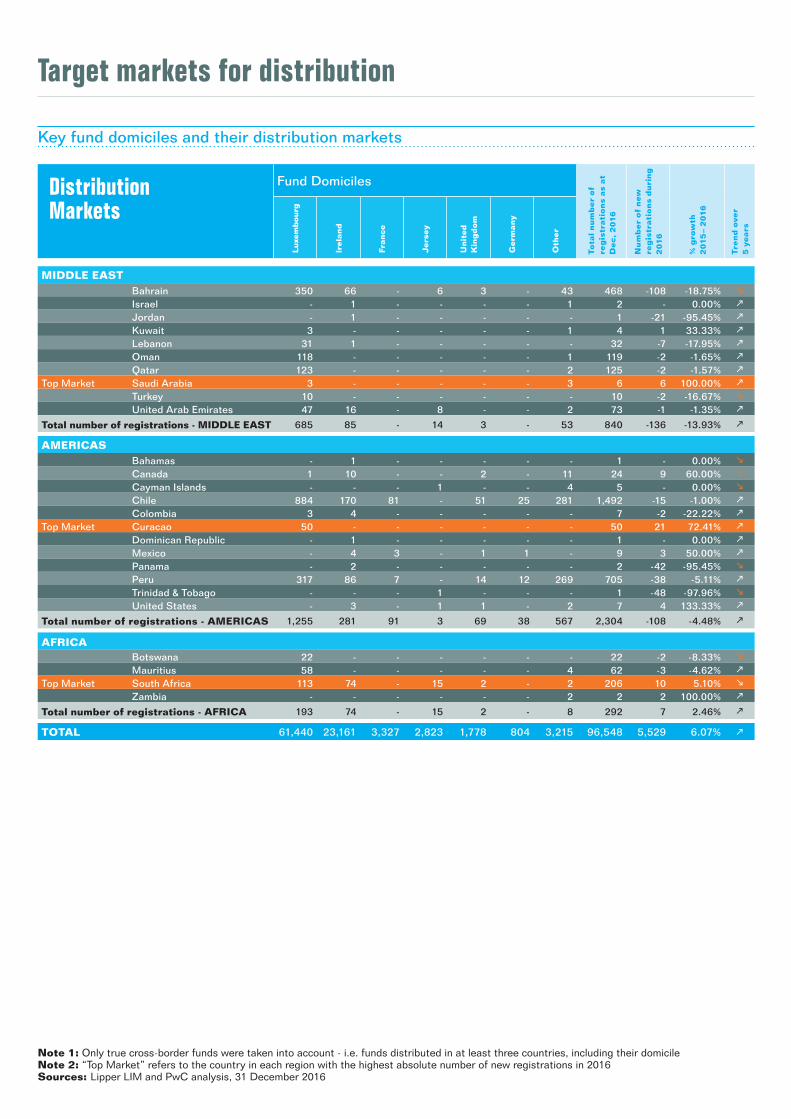

Target markets for distribution

Note 1: Only true cross-border funds were taken into account - i.e. funds distributed in at least three countries, including their domicileNote 2: “Top Market” refers to the country in each region with the highest absolute number of new registrations in 2016Sources: Lipper LIM and PwC analysis, 31 December 2016

Key fund domiciles and their distribution markets

Distribution Markets

Fund Domiciles

Tota

l n

um

ber

of

reg

istr

ati

on

s as

at

Dec, 2

016

Nu

mb

er

of

new

re

gis

trati

on

s d

uri

ng

2

016

% g

row

th

20

15

– 2

016

Tre

nd

ove

r 5

years

Luxe

mbourg

Irela

nd

France

Jers

ey

Unit

ed

K

ing

dom

Germ

any

Oth

er

EUROPEAndorra 12 - - - - - - 12 - 0.00% Austria 4,395 1,627 251 10 120 174 209 6,786 310 4.79% Belgium 2,363 465 135 83 64 24 19 3,153 263 9.10% Bulgaria 136 12 - - 1 - 9 158 11 7.48% Cyprus 338 20 - - 2 - 1 361 -77 -17.58% Czech Republic 593 12 - - 1 1 122 729 34 4.89% Denmark 1,750 773 56 228 78 20 15 2,920 324 12.48% Estonia 373 1 - - 1 - 12 387 -24 -5.84% Faroe Islands 3 - - - - - - 3 - 0.00% Finland 2,627 1,118 100 225 64 21 98 4,253 321 8.16% France 4,294 1,992 - 399 166 77 166 7,094 616 9.51% Germany 4,928 2,141 537 421 124 - 351 8,502 282 3.43% Gibraltar 294 36 - 2 - - 12 344 53 18.21% Greece 998 61 3 - 3 - 1 1,066 48 4.72% Greenland 8 - - - - - - 8 - 0.00% Guernsey 281 127 - 7 78 - - 493 13 2.71% Hungary 551 7 - - 1 - 19 578 31 5.67% Iceland 392 39 - - 1 7 2 441 58 15.14% Ireland 1,621 - 22 184 137 - 37 2,001 133 7.12% Isle of Man 43 38 - 5 4 - - 90 5 5.88% Italy 3,504 1,424 395 311 73 55 63 5,825 486 9.10% Jersey 617 136 - - 77 - 7 837 71 9.27% Latvia 315 - - - 1 - 25 341 -33 -8.82% Liechtenstein 788 130 - - - 8 45 971 68 7.53% Lithuania 283 1 - - 1 - 10 295 -12 -3.91% Luxembourg - 1,499 169 - 81 45 207 2,001 136 7.29% Malta 214 21 - 2 2 - 1 240 9 3.90% Monaco 2 2 - - - - 1 5 1 25.00% Netherlands 3,395 1,710 307 139 96 66 112 5,825 320 5.81% Norway 2,270 854 42 97 36 21 92 3,412 235 7.40% Poland 527 6 - - 1 - 21 555 35 6.73% Portugal 1,261 312 13 137 51 4 - 1,778 81 4.77% Romania 23 1 - - 1 - 4 29 13 81.25% Russian Federation - 1 - - - - - 1 1 100.00% San Marino 1 - - - - - - 1 1 100.00% Slovakia 459 16 1 - 2 1 103 582 34 6.20% Slovenia 33 1 - - 2 - 23 59 -1 -1.67% Spain 3,583 1,364 291 177 89 46 70 5,620 508 9.94% Sweden 3,091 1,446 94 178 66 21 102 4,998 336 7.21% Switzerland 4,431 1,689 365 - 143 132 198 6,958 135 1.98%

Top Market United Kingdom 3,651 2,447 392 149 - 22 81 6,742 684 11.29%

Total number of registrations - EUROPE 54,448 21,529 3,173 2,754 1,567 745 2,238 86,454 5,509 6.81%

ASIA PACIFIC

Australia 5 18 - 1 1 - 21 46 1 2.22% Brunei Darussalam 82 - - - - - - 82 32 64.00% China - - - - - - 3 3 3 100.00% Hong Kong 887 210 - - 38 3 37 1,175 -2 -0.17% Japan 59 10 - 21 - 4 11 105 10 10.53% Korea 433 35 - - 3 1 - 472 54 12.92% Macau 599 131 - - 6 - 62 798 -25 -3.04% New Zealand 1 1 - - 1 - 1 4 2 100.00% =

Top Market Singapore 2,147 648 60 15 78 5 196 3,149 169 5.67% Taiwan 646 139 3 - 10 8 18 824 13 1.60%

Total number of registrations - ASIA PACIFIC 4,859 1,192 63 37 137 21 349 6,658 257 4.01%

Note 1: Only true cross-border funds were taken into account - i.e. funds distributed in at least three countries, including their domicileNote 2: “Top Market” refers to the country in each region with the highest absolute number of new registrations in 2016Sources: Lipper LIM and PwC analysis, 31 December 2016

Target markets for distribution

Key fund domiciles and their distribution markets

Distribution Markets

Fund Domiciles

Tota

l n

um

ber

of

reg

istr

ati

on

s as

at

Dec, 2

016

Nu

mb

er

of

new

re

gis

trati

on

s d

uri

ng

2

016

% g

row

th

20

15

– 2

016

Tre

nd

ove

r 5

years

Luxe

mbourg

Irela

nd

France

Jers

ey

Unit

ed

K

ing

dom

Germ

any

Oth

er

MIDDLE EASTBahrain 350 66 - 6 3 - 43 468 -108 -18.75% Israel - 1 - - - - 1 2 - 0.00% Jordan - 1 - - - - - 1 -21 -95.45% Kuwait 3 - - - - - 1 4 1 33.33% Lebanon 31 1 - - - - - 32 -7 -17.95% Oman 118 - - - - - 1 119 -2 -1.65% Qatar 123 - - - - - 2 125 -2 -1.57%

Top Market Saudi Arabia 3 - - - - - 3 6 6 100.00% Turkey 10 - - - - - - 10 -2 -16.67% United Arab Emirates 47 16 - 8 - - 2 73 -1 -1.35%

Total number of registrations - MIDDLE EAST 685 85 - 14 3 - 53 840 -136 -13.93%

AMERICASBahamas - 1 - - - - - 1 - 0.00% Canada 1 10 - - 2 - 11 24 9 60.00% Cayman Islands - - - 1 - - 4 5 - 0.00% Chile 884 170 81 - 51 25 281 1,492 -15 -1.00% Colombia 3 4 - - - - - 7 -2 -22.22%

Top Market Curacao 50 - - - - - - 50 21 72.41% Dominican Republic - 1 - - - - - 1 - 0.00% Mexico - 4 3 - 1 1 - 9 3 50.00% Panama - 2 - - - - - 2 -42 -95.45% Peru 317 86 7 - 14 12 269 705 -38 -5.11% Trinidad & Tobago - - - 1 - - - 1 -48 -97.96% United States - 3 - 1 1 - 2 7 4 133.33%

Total number of registrations - AMERICAS 1,255 281 91 3 69 38 567 2,304 -108 -4.48%

AFRICABotswana 22 - - - - - - 22 -2 -8.33% Mauritius 58 - - - - - 4 62 -3 -4.62%

Top Market South Africa 113 74 - 15 2 - 2 206 10 5.10% Zambia - - - - - - 2 2 2 100.00%

Total number of registrations - AFRICA 193 74 - 15 2 - 8 292 7 2.46%

TOTAL 61,440 23,161 3,327 2,823 1,778 804 3,215 96,548 5,529 6.07%

Sources: Lipper LIM and PwC analysis, 31 December 2016 Note: Refer to the map for country codes

Top 53 cross-border management groups - Americas

Explanation - Ranking according to the total number of countries of distribution.

Rankin

g

Manag

em

ent

com

pany

Tota

l # o

f co

untr

ies

of d

istr

ibut

ion

at g

roup

lev

el (

incl

udin

g d

omic

ile) MAIN FUND DOMICILES AND

NUMBER OF COUNTRIES OF DISTRIBUTION

AMERICAS

Firs

t do

mic

ile a

nd #

of

coun

trie

s of

dis

trib

utio

n (c

ross

-bor

der)

Sec

ond

dom

icile

and

#

of

coun

trie

s of

di

stri

butio

n(c

ross

-bor

der)

Third

dom

icile

and

# o

f co

untr

ies

of d

istr

ibut

ion

(cro

ss-b

orde

r)

Bah

amas

Ber

mud

a

Can

ada

Cay

man

Isla

nds

Chi

le

Col

ombi

a

Cur

acao

Mex

ico

Pan

ama

Peru

Trin

idad

and

Tob

ago

Uni

ted

Sta

tes

1 FRANKLIN TEMPLETON 52 LU 50 IE 3 US 2 • • • • • •2 HSBC 43 LU 39 IE 18 GG 5 • • •3 BLACKROCK 42 LU 32 IE 24 DE 17 • • • • •4 FIDELITY INTERNATIONAL 37 LU 36 IE 16 UK 10 • •4 JPMORGAN ASSET MANAGEMENT 37 LU 34 HK 6 MU 5 • • •6 BNP PARIBAS 36 LU 34 FR 15 - - • • •7 ALLIANZ GROUP 34 LU 33 IE 15 DE 8 • •7 UBS 34 LU 32 IE 20 DE 3 • • • •9 GAM 33 LU 27 IE 27 UK 4 • •

10 DEUTSCHE BANK 31 LU 23 IE 23 DE 13 • • • •10 INVESCO 31 LU 28 IE 25 KY 2 • •10 PIONEER INVESTMENTS 31 LU 30 AT 2 - - • •10 SCHRODERS 31 LU 30 UK 4 HK 4 • •14 ABERDEEN ASSET MANAGEMNT 30 LU 29 UK 6 - - • •14 CAPITAL GROUP 30 LU 29 - - - - • • •16 COMMONWEALTH BANK OF AUS 29 IE 20 UK 13 - - •16 CREDIT SUISSE GROUP 29 LU 25 IE 10 KY 3 • • • •16 PICTET & CIE 29 LU 28 CH 2 - - • •19 AMUNDI GROUP 28 LU 26 FR 15 IE 6 • • •19 LEGAL & GENERAL GROUP 28 UK 26 LU 11 - -21 BNY MELLON 26 IE 25 UK 10 - - • •21 HENDERSON GROUP 26 LU 25 UK 12 - - • •21 MASSACHUSETTS MUT LIFE 26 IE 25 UK 17 - - • •21 PIMCO 26 IE 25 - - - - •25 LEGG MASON 25 IE 24 - - - - • •25 NN INVESTMENT PARTNERS 25 LU 24 - - - - • •25 PINEBRIDGE 25 IE 24 - - - - • •25 PRUDENTIAL 25 UK 19 LU 14 - - •29 ALLIANCEBERNSTEIN (LUXEMBOURG) S.À R.L. 24 LU 23 - - - - • •29 AXA IM 24 LU 22 IE 21 FR 7 • •29 GOLDMAN SACHS 24 LU 21 IE 15 - - • •29 INVESTEC 24 LU 22 GG 8 UK 2 •29 LYXOR 24 LU 19 FR 16 IE 12 • • •29 T-ROWE PRICE 24 LU 23 - - - - •35 LLOYDS TSB GROUP 23 IE 14 JE 9 UK 235 MORGAN STANLEY 23 LU 22 IE 15 FR 3 • •35 OLD MUTUAL 23 IE 22 UK 6 - - • •35 THREADNEEDLE 23 UK 20 LU 17 - - • •35 VONTOBEL 23 LU 22 - - - - • • •40 AVIVA GROUP 22 LU 21 IE 4 FR 2 •40 JANUS GROUP 22 IE 21 - - - - • • • •40 MFS 22 LU 21 - - - - • •40 NEUBERGER BERMAN 22 IE 21 - - - - •40 NOMURA 22 IE 21 - - - - • • •40 STATE STREET 22 IE 16 LU 14 FR 8 • • •40 VANGUARD GROUP 22 IE 16 US 4 - - • • •47 BARCLAYS 21 IE 16 LU 14 JE 5 •47 BLUEBAY 21 LU 20 - - - - •47 KBC 21 LU 20 BE 8 IE 3 •47 MAN GROUP 21 IE 18 BM 2 - - • •47 NORDEA 21 LU 20 FI 3 - - •47 ROBECO 21 LU 20 NL 10 - - • •47 WELLINGTON MANAGEMENT 21 LU 17 IE 16 US 2 • • • •

TOTAL 1 1 4 6 49 3 1 4 2 38 2 7

Rankin

g

Manag

em

ent

com

pany

Tota

l # o

f co

untr

ies

of d

istr

ibut

ion

at g

roup

lev

el (

incl

udin

g d

omic

ile) MAIN FUND DOMICILES AND

NUMBER OF COUNTRIES OF DISTRIBUTION

EUROPE

Firs

t do

mic

ile a

nd #

of

coun

trie

s of

dis

trib

utio

n (c

ross

-bor

der)

Sec

ond

dom

icile

and

#

of

coun

trie

s of

di

stri

butio

n(c

ross

-bor

der)

Third

dom

icile

and

# o

f co

untr

ies

of d

istr

ibut

ion

(cro

ss-b

orde

r)

And

orra

Aus

tria

Bel

gium

Bul

gari

a

Cyp

rus

Cze

ch R

epub

lic

Den

mar

k

Est

onia

Finl

and

Fran

ce

Ger

man

y

Gib

ralta

r

Gre

ece

Gue

rnse

y

Hun

gary

Icel

and

Irel

and

Isle

of

Man

Ital

y

Jers

ey

Latv

ia

1 FRANKLIN TEMPLETON 52 LU 50 IE 3 US 2 • • • • • • • • • • • • • • • • • •2 HSBC 43 LU 39 IE 18 GG 5 • • • • • • • • • • • • • • •3 BLACKROCK 42 LU 32 IE 24 DE 17 • • • • • • • • • • • • • • • •4 FIDELITY INTERNATIONAL 37 LU 36 IE 16 UK 10 • • • • • • • • • • • • •4 JPMORGAN ASSET MANAGEMENT 37 LU 34 HK 6 MU 5 • • • • • • • • • • • • • •6 BNP PARIBAS 36 LU 34 FR 15 - - • • • • • • • • • • • • •7 ALLIANZ GROUP 34 LU 33 IE 15 DE 8 • • • • • • • • • • • •7 UBS 34 LU 32 IE 20 DE 3 • • • • • • • • • • • • •9 GAM 33 LU 27 IE 27 UK 4 • • • • • • • • • • • • • •

10 DEUTSCHE BANK 31 LU 23 IE 23 DE 13 • • • • • • • • • • •10 INVESCO 31 LU 28 IE 25 KY 2 • • • • • • • • • • • • • •10 PIONEER INVESTMENTS 31 LU 30 AT 2 - - • • • • • • • • • • • • •10 SCHRODERS 31 LU 30 UK 4 HK 4 • • • • • • • • • • • • •14 ABERDEEN ASSET MANAGEMNT 30 LU 29 UK 6 - - • • • • • • • • • • • • •14 CAPITAL GROUP 30 LU 29 - - - - • • • • • • • • • • • •16 COMMONWEALTH BANK OF AUS 29 IE 20 UK 13 - - • • • • • • • • • • • • •16 CREDIT SUISSE GROUP 29 LU 25 IE 10 KY 3 • • • • • • • • • • • • •16 PICTET & CIE 29 LU 28 CH 2 - - • • • • • • • • • •19 AMUNDI GROUP 28 LU 26 FR 15 IE 6 • • • • • • • • • • • •19 LEGAL & GENERAL GROUP 28 UK 26 LU 11 - - • • • • • • • • • • • • • •21 BNY MELLON 26 IE 25 UK 10 - - • • • • • • • • • • • •21 HENDERSON GROUP 26 LU 25 UK 12 - - • • • • • • • • • • •21 MASSACHUSETTS MUT LIFE 26 IE 25 UK 17 - - • • • • • • • • • • •21 PIMCO 26 IE 25 - - - - • • • • • • • • •25 LEGG MASON 25 IE 24 - - - - • • • • • • • • •25 NN INVESTMENT PARTNERS 25 LU 24 - - - - • • • • • • • • • •25 PINEBRIDGE 25 IE 24 - - - - • • • • • • • • •25 PRUDENTIAL 25 UK 19 LU 14 - - • • • • • • • • •29 ALLIANCEBERNSTEIN (LUXEMBOURG) S.À R.L. 24 LU 23 - - - - • • • • • • • •29 AXA IM 24 LU 22 IE 21 FR 7 • • • • • • • • •29 GOLDMAN SACHS 24 LU 21 IE 15 - - • • • • • • • • •29 INVESTEC 24 LU 22 GG 8 UK 2 • • • • • • • • •29 LYXOR 24 LU 19 FR 16 IE 12 • • • • • • • •29 T-ROWE PRICE 24 LU 23 - - - - • • • • • • • • • • •35 LLOYDS TSB GROUP 23 IE 14 JE 9 UK 2 • • • • • • • • • • •35 MORGAN STANLEY 23 LU 22 IE 15 FR 3 • • • • • • • • • •35 OLD MUTUAL 23 IE 22 UK 6 - - • • • • • • • •35 THREADNEEDLE 23 UK 20 LU 17 - - • • • • • • • •35 VONTOBEL 23 LU 22 - - - - • • • • • •40 AVIVA GROUP 22 LU 21 IE 4 FR 2 • • • • • • • • •40 JANUS GROUP 22 IE 21 - - - - • • • • • •40 MFS 22 LU 21 - - - - • • • • • • • •40 NEUBERGER BERMAN 22 IE 21 - - - - • • • • • • • • •40 NOMURA 22 IE 21 - - - - • • • • • • • •40 STATE STREET 22 IE 16 LU 14 FR 8 • • • • • • • • •40 VANGUARD GROUP 22 IE 16 US 4 - - • • • • • • • • •47 BARCLAYS 21 IE 16 LU 14 JE 5 • • • • • • • • • •47 BLUEBAY 21 LU 20 - - - - • • • • • • • • • •47 KBC 21 LU 20 BE 8 IE 3 • • • • • • • • • •47 MAN GROUP 21 IE 18 BM 2 - - • • • • • • • •47 NORDEA 21 LU 20 FI 3 - - • • • • • • • • •47 ROBECO 21 LU 20 NL 10 - - • • • • • • •47 WELLINGTON MANAGEMENT 21 LU 17 IE 16 US 2 • • • • • • • •

TOTAL 1 51 50 8 12 17 47 9 51 53 53 9 23 13 16 18 50 9 53 14 6

Sources: Lipper LIM and PwC analysis, 31 December 2016 Note: Refer to the map for country codes

Top 53 cross-border management groups - Europe

Explanation - Ranking according to the total number of countries of distribution.

Top 53 cross-border management groups - EuropeR

ankin

g

Manag

em

ent

com

pany

Tota

l # o

f co

untr

ies

of d

istr

ibut

ion

at g

roup

lev

el (

incl

udin

g d

omic

ile) MAIN FUND DOMICILES AND

NUMBER OF COUNTRIES OF DISTRIBUTION

EUROPE - continued

Firs

t do

mic

ile a

nd #

of

coun

trie

s of

dis

trib

utio

n (c

ross

-bor

der)

Sec

ond

dom

icile

and

#

of

coun

trie

s of

di

stri

butio

n(c

ross

-bor

der)

Third

dom

icile

and

# o

f co

untr

ies

of d

istr

ibut

ion

(cro

ss-b

orde

r)

Liec

hten

stei

n

Lith

uani

a

Luxe

mbo

urg

Mal

ta

Mon

aco

Net

herl

ands

Nor

way

Pol

and

Por

tuga

l

Rom

ania

San

Mar

ino

Slo

vaki

a

Slo

veni

a

Spa

in

Sw

eden

Sw

itzer

land

Uni

ted

Kin

gdom

1 FRANKLIN TEMPLETON 52 LU 50 IE 3 US 2 • • • • • • • • • • • • •2 HSBC 43 LU 39 IE 18 GG 5 • • • • • • • • • •3 BLACKROCK 42 LU 32 IE 24 DE 17 • • • • • • • • • • •4 FIDELITY INTERNATIONAL 37 LU 36 IE 16 UK 10 • • • • • • • • • • •4 JPMORGAN ASSET MANAGEMENT 37 LU 34 HK 6 MU 5 • • • • • • • • • • •6 BNP PARIBAS 36 LU 34 FR 15 - - • • • • • • • • • • • • •7 ALLIANZ GROUP 34 LU 33 IE 15 DE 8 • • • • • • • • • • •7 UBS 34 LU 32 IE 20 DE 3 • • • • • • • • • •9 GAM 33 LU 27 IE 27 UK 4 • • • • • • • • • •

10 DEUTSCHE BANK 31 LU 23 IE 23 DE 13 • • • • • • • •10 INVESCO 31 LU 28 IE 25 KY 2 • • • • • • • • • •10 PIONEER INVESTMENTS 31 LU 30 AT 2 - - • • • • • • • • • • • •10 SCHRODERS 31 LU 30 UK 4 HK 4 • • • • • • • • • •14 ABERDEEN ASSET MANAGEMNT 30 LU 29 UK 6 - - • • • • • • • • • •14 CAPITAL GROUP 30 LU 29 - - - - • • • • • • • • •16 COMMONWEALTH BANK OF AUS 29 IE 20 UK 13 - - • • • • • • • • • • • • • •16 CREDIT SUISSE GROUP 29 LU 25 IE 10 KY 3 • • • • • • • • •16 PICTET & CIE 29 LU 28 CH 2 - - • • • • • • • • • •19 AMUNDI GROUP 28 LU 26 FR 15 IE 6 • • • • • • • • •19 LEGAL & GENERAL GROUP 28 UK 26 LU 11 - - • • • • • • • • • • • • • •21 BNY MELLON 26 IE 25 UK 10 - - • • • • • • • •21 HENDERSON GROUP 26 LU 25 UK 12 - - • • • • • • • • •21 MASSACHUSETTS MUT LIFE 26 IE 25 UK 17 - - • • • • • • •21 PIMCO 26 IE 25 - - - - • • • • • • • •25 LEGG MASON 25 IE 24 - - - - • • • • • • • • •25 NN INVESTMENT PARTNERS 25 LU 24 - - - - • • • • • • • • • •25 PINEBRIDGE 25 IE 24 - - - - • • • • • • • •25 PRUDENTIAL 25 UK 19 LU 14 - - • • • • • • • •29 ALLIANCEBERNSTEIN (LUXEMBOURG) S.À R.L. 24 LU 23 - - - - • • • • • • • •29 AXA IM 24 LU 22 IE 21 FR 7 • • • • • • • •29 GOLDMAN SACHS 24 LU 21 IE 15 - - • • • • • • • •29 INVESTEC 24 LU 22 GG 8 UK 2 • • • • • • •29 LYXOR 24 LU 19 FR 16 IE 12 • • • • • • • • •29 T-ROWE PRICE 24 LU 23 - - - - • • • • • • • • •35 LLOYDS TSB GROUP 23 IE 14 JE 9 UK 2 • • • • • • • • •35 MORGAN STANLEY 23 LU 22 IE 15 FR 3 • • • • • • • •35 OLD MUTUAL 23 IE 22 UK 6 - - • • • • • • • •35 THREADNEEDLE 23 UK 20 LU 17 - - • • • • • • • •35 VONTOBEL 23 LU 22 - - - - • • • • • • • • •40 AVIVA GROUP 22 LU 21 IE 4 FR 2 • • • • • • • • •40 JANUS GROUP 22 IE 21 - - - - • • • • • • •40 MFS 22 LU 21 - - - - • • • • • • • •40 NEUBERGER BERMAN 22 IE 21 - - - - • • • • • • • • •40 NOMURA 22 IE 21 - - - - • • • • • • • •40 STATE STREET 22 IE 16 LU 14 FR 8 • • • • • • •40 VANGUARD GROUP 22 IE 16 US 4 - - • • • • • • •47 BARCLAYS 21 IE 16 LU 14 JE 5 • • • • • • • •47 BLUEBAY 21 LU 20 - - - - • • • • • • • •47 KBC 21 LU 20 BE 8 IE 3 • • • • • • • • •47 MAN GROUP 21 IE 18 BM 2 - - • • • • • • • • •47 NORDEA 21 LU 20 FI 3 - - • • • • • • • • • •47 ROBECO 21 LU 20 NL 10 - - • • • • • • • •47 WELLINGTON MANAGEMENT 21 LU 17 IE 16 US 2 • • • • • • • •

TOTAL 15 7 53 13 1 53 52 14 45 5 1 12 6 53 52 53 53

Sources: Lipper LIM and PwC analysis, 31 December 2016 Note: Refer to the map for country codes

Explanation - Ranking according to the total number of countries of distribution.

Top 53 cross-border management groups - OthersR

ankin

g

Manag

em

ent

com

pany

Tota

l # o

f co

untr

ies

of d

istr

ibut

ion

at g

roup

lev

el (

incl

udin

g d

omic

ile) MAIN FUND DOMICILES AND

NUMBER OF COUNTRIES OF DISTRIBUTION

ASIA PACIFIC MIDDLE EAST AFRICA

Firs

t do

mic

ile a

nd #

of

coun

trie

s of

dis

trib

utio

n (c

ross

-bor

der)

Sec

ond

dom

icile

and

#

of

coun

trie

s of

di

stri

butio

n(c

ross

-bor

der)

Third

dom

icile

and

# o

f co

untr

ies

of d

istr

ibut

ion

(cro

ss-b

orde

r)

Aus

tral

ia

Bru

nei D

arus

sala

m

Chi

na

Hon

g K

ong

Japa

n

Kor

ea

Mac

au

Sin

gapo

re

Taiw

an

Bah

rain

Jord

an

Leba

non

Om

an

Qat

ar

Sau

di A

rabi

a

Turk

ey

Uni

ted

Ara

b E

mir

ates

Bot

swan

a

Egy

pt

Mau

ritiu

s

Sou

th A

fric

a

1 FRANKLIN TEMPLETON 52 LU 50 IE 3 US 2 • • • • • • • • • • • • • • •2 HSBC 43 LU 39 IE 18 GG 5 • • • • • • • • • • • • • • •3 BLACKROCK 42 LU 32 IE 24 DE 17 • • • • • • • • • •4 FIDELITY INTERNATIONAL 37 LU 36 IE 16 UK 10 • • • • • • • • • • •4 JPMORGAN ASSET MANAGEMENT 37 LU 34 HK 6 MU 5 • • • • • • • • •6 BNP PARIBAS 36 LU 34 FR 15 - - • • • • • • •7 ALLIANZ GROUP 34 LU 33 IE 15 DE 8 • • • • • • • • •7 UBS 34 LU 32 IE 20 DE 3 • • • • • • •9 GAM 33 LU 27 IE 27 UK 4 • • • • • • •

10 DEUTSCHE BANK 31 LU 23 IE 23 DE 13 • • • • • • • •10 INVESCO 31 LU 28 IE 25 KY 2 • • • • •10 PIONEER INVESTMENTS 31 LU 30 AT 2 - - • • • •10 SCHRODERS 31 LU 30 UK 4 HK 4 • • • • • •14 ABERDEEN ASSET MANAGEMNT 30 LU 29 UK 6 - - • • • • •14 CAPITAL GROUP 30 LU 29 - - - - • • • • • •16 COMMONWEALTH BANK OF AUS 29 IE 20 UK 13 - - •16 CREDIT SUISSE GROUP 29 LU 25 IE 10 KY 3 • • •16 PICTET & CIE 29 LU 28 CH 2 - - • • • • • • •19 AMUNDI GROUP 28 LU 26 FR 15 IE 6 • • • •19 LEGAL & GENERAL GROUP 28 UK 26 LU 11 - -21 BNY MELLON 26 IE 25 UK 10 - - • • • •21 HENDERSON GROUP 26 LU 25 UK 12 - - • • • •21 MASSACHUSETTS MUT LIFE 26 IE 25 UK 17 - - • • • • • •21 PIMCO 26 IE 25 - - - - • • • • • • • •25 LEGG MASON 25 IE 24 - - - - • • • • •25 NN INVESTMENT PARTNERS 25 LU 24 - - - - • • •25 PINEBRIDGE 25 IE 24 - - - - • • • • • •25 PRUDENTIAL 25 UK 19 LU 14 - - • • • • • • •29 ALLIANCEBERNSTEIN (LUXEMBOURG) S.À R.L. 24 LU 23 - - - - • • • • • •29 AXA IM 24 LU 22 IE 21 FR 7 • • • • •29 GOLDMAN SACHS 24 LU 21 IE 15 - - • • • • •29 INVESTEC 24 LU 22 GG 8 UK 2 • • • • • • •29 LYXOR 24 LU 19 FR 16 IE 12 • • • •29 T-ROWE PRICE 24 LU 23 - - - - • • •35 LLOYDS TSB GROUP 23 IE 14 JE 9 UK 2 • • •35 MORGAN STANLEY 23 LU 22 IE 15 FR 3 • • •35 OLD MUTUAL 23 IE 22 UK 6 - - • • • • •35 THREADNEEDLE 23 UK 20 LU 17 - - • • • • •35 VONTOBEL 23 LU 22 - - - - • • • • •40 AVIVA GROUP 22 LU 21 IE 4 FR 2 • • •40 JANUS GROUP 22 IE 21 - - - - • • • • •40 MFS 22 LU 21 - - - - • • • •40 NEUBERGER BERMAN 22 IE 21 - - - - • • •40 NOMURA 22 IE 21 - - - - • • •40 STATE STREET 22 IE 16 LU 14 FR 8 • • •40 VANGUARD GROUP 22 IE 16 US 4 - - • • •47 BARCLAYS 21 IE 16 LU 14 JE 5 • •47 BLUEBAY 21 LU 20 - - - - • •47 KBC 21 LU 20 BE 8 IE 3 •47 MAN GROUP 21 IE 18 BM 2 - - • •47 NORDEA 21 LU 20 FI 3 - - •47 ROBECO 21 LU 20 NL 10 - - • • • •47 WELLINGTON MANAGEMENT 21 LU 17 IE 16 US 2 •

TOTAL 5 3 3 38 16 26 25 52 38 25 2 3 3 4 2 3 10 1 1 2 8

Sources: Lipper LIM and PwC analysis, 31 December 2016 Note: Refer to the map for country codes

Explanation - Ranking according to the total number of countries of distribution.

Origin of Luxembourg fund initiators

Companies from all over the world use Luxembourg as their gateway to Europe and the rest of the world. The two countries with the largest market share of assets under management in Luxembourg are the USA and United Kingdom.

Source: CSSF, Figures as of 31 June 2017

Origin of Luxembourg Fund Initiators% of net assets under management per country

25

20

15

10

5

0

US GB DE CH IT FR BE NL LU DK Others

4.2

2.4 2.1 2.0

20.3

17.3

7.1

14.413.4

8.6 8.2

10 REASONS WHY THE FUND INDUSTRY CHOOSES LUXEMBOURG

It has a stable political and social environment and a AAA economy.

It is a founding member of the European Union and is situated at the heart of Europe, with more than 500 million European consumers on its doorstep.

Luxembourg is the largest European fund domicile and the second largest fund centre in the world after the US, with about EUR 3,943 billion in assets under management.

Its fund lawyers, audit firms and tax advisors are highly experienced in cross-border registrations of both UCITS and non-UCITS funds, facilitating fund distribution around the globe.

It has established a competitive framework for UCITS (Undertakings for Collective Investment in Transferable Securities), funds “passported” within the EU, as well as for non-UCITS or alternative investment funds.

It leads the way in investor protection and has a highly experienced and responsive regulator.

It has a unique concentration of investment fund experts specialised in all aspects of product development, administration and distribution.

Luxembourg is endowed with an international and multilingual workforce. English is the language of the financial sector, and French, German and other European languages are also spoken. Its laws provide for so-called umbrella

funds, which have several compartments under a single legal structure, and each compartment can invest in a different asset class.

Luxembourg’s legal and regulatory framework for investment funds is state-of-the-art, and recognised as such by the global asset management community.

About ALFI

The Association of the Luxembourg Fund Industry (ALFI), the representative body forthe Luxembourg investment fund community,was founded in 1988. Today it represents morethan 1 500 Luxembourg-domiciled investmentfunds, asset management companies and a widevariety of service providers including depositarybanks, fund administrators, transfer agents, distributors, law firms, consultants, tax advisers,auditors and accountants, specialist IT providersand communications agencies.Luxembourg is the largest fund domicilein Europe and its investment fund industryis a worldwide leader in cross-border funddistribution. Luxembourg-domiciledinvestment structures are distributed inmore than 70 countries around the globe,with a particular focus on Europe, Asia,Latin America and the Middle East.ALFI defines its mission as to “Lead industryefforts to make Luxembourg the mostattractive international centre”.

Its main objectives are to:

n Help members capitalise on industry trends ALFI’s many technical committees and working

groups constantly review and analyse developments worldwide, as well as legal and regulatory changes in Luxembourg, the EU and beyond, to identify threats and opportunities for the Luxembourg fund industry.

n Shape regulation An up-to-date, innovative legal and fiscal

environment is critical to defend and improve Luxembourg’s competitive position as a centre for the domiciliation, administration and distribution of investment funds. Strong relationships with regulatory authorities, the government and the legislative body enable ALFI to make an effective contribution to decisionmaking through relevant input for changes to the regulatory framework, implementation of European directives and regulation of new products or services.

n Foster dedication to professional standards, integrity and quality

Investor trust is essential for success in

collective investment services and ALFI thus does all it can to promote high professional standards, quality products and services, and integrity. Action in this area includes organising training at all levels, defining codes of conduct, transparency and good corporate governance, and supporting initiatives to combat money laundering.

n Promote the Luxembourg investment fund industry

ALFI actively promotes the Luxembourg

investment fund industry, its products and its services. It represents the sector in financial and in economic missions organised by the Luxembourg government around the world and takes an active part in meetings of the global fund industry.

ALFI is an active member of the European

Fund and Asset Management Association, of the International Investment Funds Association, of Pensions Europe, of the International Association of Pension Funds Administrators and of the Global Impact Investing Network.

For more information, visit our website: www.alfi.lu and follow ALFI on

Tel: +352 22 30 26 - 1Fax: +352 22 30 93

alfi | association of theluxembourg fund industry

12, rue ErasmeL- 1468 Luxembourg

September 2017 © 2017 ALFI. All rights reserved.

ALFI thanks PwC Luxembourg, which produced the content of this document in association with Lipper and Thomson Reuters, for its authorisation to reprint. PwC Luxembourg is a member of ALFI.For further information, please contact us or visit our website www.alfi.lu