Embed Size (px)

Citation preview

Patrick CavanaghAssociate Economist, Pulp

Boston, MAOctober 2017

Global Fluff Pulp Outlook

© Copyright 2017 RISI, Inc. | Proprietary Information

Market BackgroundFluff Pulp Overview

• What is fluff pulp? Wood pulp produced mainly from softwood fiber Used in the absorbent core of hygiene products E.g., baby diapers, feminine care products, adult incontinence products

Primarily produced in the US South• In 2016, fluff pulp capacity represented nearly 10% of world paper grade market pulp supply

• Demand growth driven by emerging markets• Low market penetration rates• Favorable demographic and economic factors

2© Copyright 2017 RISI, Inc. | Proprietary Information

Fluff Pulp Demand by End UsePercent of Total, 2016 Estimate

3

Disposable Diapers

38%

Adult Incontinence

26%

Feminine Hygiene

24%

Airlaid/Other12%

© Copyright 2017 RISI, Inc. | Proprietary Information

Demand Overview

• World demand growth continues to be steady 2016 global consumption estimated at 5.9 million tonnes Mild slowdown in demand growth in 2015‐2016 (2.7%) due to a pause in global economic conditions

Demand growth is forecast to average 4.7% annually for the next five years

• Emerging markets will account for majority of growth Disposable absorbent hygiene product use grows with income and population

Nearly 85% of total demand growth between 2016 and 2021 will come from emerging markets

• Mature markets will see some consumption growth driven largely by an aging population

4© Copyright 2017 RISI, Inc. | Proprietary Information

Mature Market Demand Growth Relatively Flat

5

* Canada, Japan, Oceania, USA, Western Europe

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Thou

sand

Ton

nes

Eastern EuropeAfrica/Middle EastOther AsiaLatin AmericaChinaMature Markets*

© Copyright 2017 RISI, Inc. | Proprietary Information

Changing Landscape for DemandShare of Fluff Pulp Demand by Region

6

2002 2016

Africa/Middle East5%

North America

26%

Western Europe

29%

China6%

Latin America

10%

Japan7%

Other Asia9%

Eastern Europe

6%

Oceania2%

Africa/Middle East7%

North America

18%

Western Europe

18%

China18%

Latin America

14%

Japan5%

Other Asia11%

Eastern Europe

7%

Oceania2%

© Copyright 2017 RISI, Inc. | Proprietary Information

Demographics and Income Drive Demand• Potential Absorbent Hygiene Product Users (PAHU) fall into three major categories Children age 0‐2.5 (potential diaper consumer) Women age 12‐51 (potential feminine care consumer) Adults age 65 and older (potential AI product consumer)

• Per capita income drives fluff consumption per PAHU As income levels rise, more can be spent on convenience goods such as disposable absorbent hygiene products

As an economy reaches high levels of income, fluff pulp consumption per user levels off

7© Copyright 2017 RISI, Inc. | Proprietary Information

Global Fluff Demand Curve2000‐2016 Real Income per Capita vs Kilograms of Fluff Consumed per Potential Absorbent Hygiene User*

8

*Potential absorbent hygiene users (PAHU) include the populations 0‐2.5 years old, females 12‐51 and 65+ years old.

0.01.02.03.04.05.06.07.08.0

0 10,000 20,000 30,000 40,000 50,000

Kilogram

s

Per Capita Income (2005$)Africa Middle East China Other AsiaBrazil Other Latin America Eastern Europe USACanada Western Europe Nordic JapanOceania

© Copyright 2017 RISI, Inc. | Proprietary Information

Income Levels on the Rise in Emerging MarketsGDP per Capita, 2005 US Dollars at Purchasing Power Parity

9

0

5,000

10,000

15,000

20,000

25,000

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

Eastern Europe China Brazil India Asia ex Japan, China, India

© Copyright 2017 RISI, Inc. | Proprietary Information

Large Consumer Base in Emerging Markets2016 Estimate, Millions

10

0-2.5 Years Old

Females 12-51 Years Old

65+ Years Old

China 43.0 403.9 142.1India 59.1 390.3 76.9Other Asia (excl. Japan) 68.7 436.2 89.7Brazil 7.5 64.5 17.1Other Latin America 19.4 130.3 32.9Africa 98.5 344.7 42.7Eastern Europe 13.2 113.1 56.7Middle East 9.9 46.1 6.1Total 319.3 1,929.1 464.2

© Copyright 2017 RISI, Inc. | Proprietary Information

Supply• Total fluff pulp capacity in 2016 was estimated to be just over 6.6 million tonnes

• Concentrated industry Top three producers by capacity at year‐end 2016 were

International Paper (IP), Georgia‐Pacific (G‐P) and Domtar These three producers account for nearly 78% of the market

• Recent large increases in capacity Riegelwood, Ashdown, Ortiguiera and Suzano collectively adding

over 1 million tonnes of capacity in one year• Hardwood fluff may prove to be disruptive BEK production costs are significantly lower than SBSK If product performance proves good, this could put pressure on

traditional producers in the future

11© Copyright 2017 RISI, Inc. | Proprietary Information

IP/Weyco Deal Increases ConsolidationMarket Share of Top Five Producers by Capacity

12

Before 2016 Acquisition After 2016 Acquisition

Georgia-Pacific

31%

Weyerhaeuser22%

International Paper17%

Domtar8%

Resolute Forest

Products4%

All Other18% Georgia-

Pacific31%

International Paper39%

Domtar8%

Resolute Forest

Products4%

All Other14%

Stora Enso4%

© Copyright 2017 RISI, Inc. | Proprietary Information

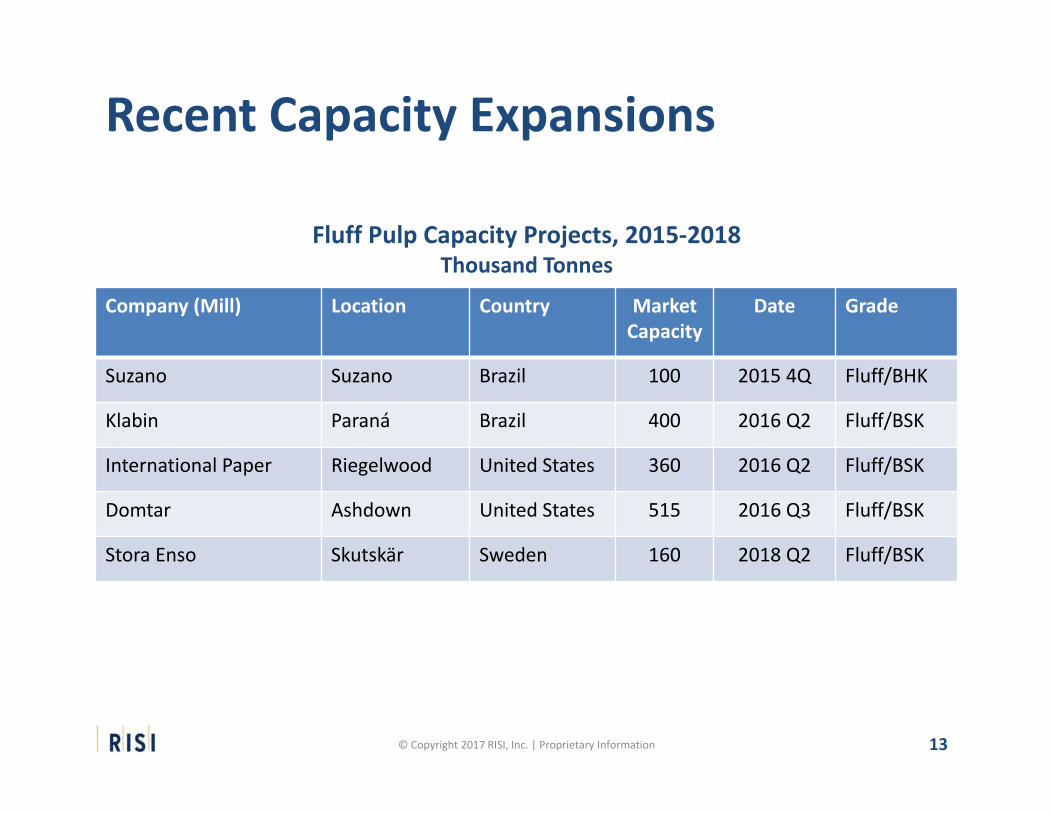

Recent Capacity Expansions

13

Company (Mill) Location Country Market Capacity

Date Grade

Suzano Suzano Brazil 100 2015 4Q Fluff/BHK

Klabin Paraná Brazil 400 2016 Q2 Fluff/BSK

International Paper Riegelwood United States 360 2016 Q2 Fluff/BSK

Domtar Ashdown United States 515 2016 Q3 Fluff/BSK

Stora Enso Skutskär Sweden 160 2018 Q2 Fluff/BSK

Fluff Pulp Capacity Projects, 2015‐2018Thousand Tonnes

© Copyright 2017 RISI, Inc. | Proprietary Information

US South Still Dominating SupplyFluff Pulp Capacity by Major Region

14

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Thou

sand

Ton

nes

Rest of WorldWestern EuropeNorth America

© Copyright 2017 RISI, Inc. | Proprietary Information

Fluff Pulp Price• Strong relationship between paper grade and fluff Large portion of fluff producers can swing between BSK and fluff

Producers swing to fluff pulp as relative profitability of the grade rises in relation to paper grade

• Prices are currently at all‐time highs Third‐quarter 2017 list prices reached $1,120/tonne A reflection of booming demand for paper grade, fluff market consolidation and supportive demographic trends

• New supply should be enough to keep operating rates down through 2020

15© Copyright 2017 RISI, Inc. | Proprietary Information

16

Strong Relationship with Slight LagFluff Pulp and Southern Bleached Softwood Kraft Pulp List Prices

050100150200250300350400450500550600

0100200300400500600700800900

1,0001,1001,200

95 97 99 01 03 05 07 09 11 13 15 17

Fluff‐S

BSK Spread

, US Dollars

Delivered

to USA

, US Dollars per

Tonn

e

FLF‐SBSK (R)Fluff PriceSBSK Price

© Copyright 2017 RISI, Inc. | Proprietary Information

17

Outlook for the World Fluff Pulp Market: Special Market Analysis Studywww.risi.com/fluffpulp16

Thank you for your attention!For more information:

World Pulp & Recovered Paper Forecastwww.risi.com/WPRP5

World Pulp Monthlywww.risi.com/WPM

© Copyright 2017 RISI, Inc. | Proprietary Information