Embed Size (px)

Citation preview

BUSINESS OUTLOOKGLOBAL ELECTRONICS

INDUSTRYWALT CUSTERCUSTER CONSULTING GROUPwww.custerconsulting.comMarch 2012

20120301

BUSINESS CYCLE Components & Capital Equipment

OEMEMSPCBsRaw MaterialsCapital Equipment

0

RecessionExpansionTime

6-9Month Lag

20111205

Global Electronic Supply Chain Forecast 2012 vs 2011

3

5

2

4

-20

Combined GDP

Electronic Equipment

Rigid & Flex PCBs

Semiconductors

Semi Capital Spending

0 5 10-5-10-15-20-25% Change

20120205

Henderson Ventures

Gartner

Henderson Ventures

Custer Consulting Group

Henderson Ventures

Global "Purchasing Managers" Index

JPMorgan

1 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 303 04 05 06 07 08 09 10 11 12

32

34

36

38

40

42

44

46

48

50

52

54

56

58

60DIFFUSION INDEX

0

10

20

30

40

50

60

70

EXPANSIONCONTRACTION

20120301

Global Manufacturing PMIT Summary50 = no change on previous month.

Jan Feb Change SummaryGlobal PMI 51.3 51.1 - Expanding, slower rateOutput 51.9 52.5 + Expanding, faster rateNew Orders 51.7 51.3 - Expanding, slower rateInput Prices 52.6 56.6 + Rising, faster rateEmployment 51.0 51.1 + Rising, faster rate

World Purchasing Managers' Indices

3 6 9123 6 9123 6 9123 6 9123 6 9123 6 9123 6 9123 6 9123 6 9123 6 9123 6 9123 6 912300 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

0.5

0.7

0.9

1.1

1.3

1.5

1.73/12 rate of change

USA "0" Growth ChinaEurope World

Source: Custer Consulting Group

20120301

Electronic Equipment

20050118

BUSINESS

COMMUNICATION

CONSUMER

AUTO

COMPUTER

GOVMILITARY

INDUSTRIAL

INSTRUMENT

1.7%22.9%

13.2%

6.6%29.8%

9.3%

8.6%

8.1%

Electronic Outlook 10/11

20111006

World Electronic Equipment by Type 2011

$2,019 Billion @ 2010 exchange

Electronic Equipment SuppliersComposite of 105 Public Companies

Revenue, Net Income & Inventory

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 400 01 02 03 04 05 06 07 08 09 10 11

0

50

100

150

200

250

300

350

-50

$ Billion

Revenue 139146151159137142135145129133135148137144150168163172169190176184186206192201206226211225234260239252254245212224235264243255269298273286287311Income 12 12 11 8 -1 -5 -12 0 3 -10 0 1 6 5 8 12 12 14 13 16 14 15 14 23 17 12 18 20 19 21 20 22 20 20 19 -2 11 16 19 25 21 24 28 35 29 31 27 37

Inventory 63 65 68 70 72 65 58 53 52 50 48 45 45 46 45 46 48 49 50 49 51 51 52 51 54 57 60 60 59 62 64 65 68 71 71 65 62 62 62 62 63 66 69 72 73 78 79 76

+4%

20120226

Computer 13, Internet 5, Storage 10, Communication 12, SEMI 20, Medical 24, Instruments 11, Military 6

Electronic Equipment SuppliersComposite of 104 Public Companies

Quarterly Revenue Growth

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 401 02 03 04 05 06 07 08 09 10 11

0.0

5.0

10.0

15.0

20.0

25.0

-5.0

-10.0

-15.0

% Growth (quarter vs same quarter in prior year)

20120226

Computer 11, Internet 5, Storage 10, Communication 11, SEMI 13, Medical 24, Instruments 6, Military 6

Global Electronic Equipment Shipment Growth3/12 & 12/12 Rate of Change

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 101 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

0.85

0.9

0.95

1

1.05

1.1

1.15

1.2Rate of Growth (1.0=no growth)

12/12 3/12 Series 3

Custer Consulting Group based upon Industry Sector Composite Data, 104 companies

20120226

Inventory/Sales RatioLarge Component Distributors, Semiconductor, EMS &

OEM Companies

3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 200 01 02 03 04 05 06 07 08 09 10 11 12

CY

0.200.250.300.350.400.450.500.550.600.650.700.750.800.850.90

Quarterly Inventory/Sales ($)

SemiconductorEMSOEMComponent Distrib

20120226

4 Component Distributor, 18 Semiconductor, 12 EMS and 104 OEM Company Composite

EMS

Chips

OEM

Distr

European Computer, Electronic & Optical products Production

Eurostat, C26 category, EU 27 countries

1 4710147101 471014 7101 4710147101 4710147101 4710147101 4710147101 471014710198 99 00 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

70

80

90

100

110

120

130

Index (2005=100), Seasonally Adjusted

20120215

Japan Electronic Equipment Production2000 to Present

JEITA www.jeita.or.jp/

1 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 91100 01 02 03 04 05 06 07 08 09 10 11

CALENDAR YEAR

0

500

1000

1500

2000Yen billion

Consumer Electronic EquipmentElectronic Measuring InstrumentationCommunications EquipmentComputers & Related EquipmentElectronic Business MachinesElec Application Equip

-24% -2%+1%

-23%

20120227

-3%+9%

-13%

+17%-10%

-3%

Taiwan/China Electronic Equipment ProducersComposite of 101 Manufacturers

1 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 911102 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

0

200

400

600

800NT$ (billions)

20120212

Taiwan listed companies, often with significant manufacturing in China

2011/2010 up 5%

US Electronic Equipment Orders & ShipmentsCommunications, Computer, Military, Instruments

http://www.census.gov/indicator/www/m3/

1 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 710198 99 00 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

14

16

18

20

22

24

26

28

30

32

34$B (Monthly Orders - Seasonally Adjusted)

OrdersShipments

20120229

Global Electronic Equipment Shipment Growth

1 4 7 101 4 7 101 4 7 101 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 101 4 7 101 4 7 10100 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

0.6

0.7

0.8

0.9

1

1.1

1.2

1.3

1.4

1.5

1.63/12 rate of growth in local currency

Taiwan/ChinaEuropeJapanUSA0 Growth

20120229

Europe = Eurostat EU27 NACE C26 (computer, electronic & optical products)

World Electronic Equipment Monthly Shipments

Converted @ Constant 2010 Exchange Rates

1357911135791113579111357911135791113579111357911135791113579111357911135791113579111300 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

0

20

40

60

80

100$ Billions

N America W Europe Japan SE Asia ROW

Source: Custer Consulting Group

20120229

World Electronic Equipment Monthly Shipments

Converted @ Constant 2010 Exchange Rates

1 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 911100 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

80

90

100

110

120

130

140

150

160

170

180$ Billions

Source: Custer Consulting Group

20120229

TopicsEconomy

Electronic Equipment

Semiconductors

Other Components

EMS/ODM

PCB

Summary & Forecasts

20091008

Business Conditions2010 through mid-2011 was a period of significant growth. Excess ordering & inventory building occurred.

Electronic supply chain expansion stalled in late 2011 but USA and SE Asia is again growing.

Solar/photovoltaic growth has slowed significantly.

Major Issues:- Europe's tighter fiscal policies, squeezed consumer purchasing power & sovereign-debt tensions- U.S. high unemployment & political wrangling- China's rising costs, labor shortages & real estate bubble.- Japan's strong yen hurting exports & ongoing effects of earthquake & nuclear disaster- Thailand flooding (shifting business to other regions)

2005011820110705

Global Electronic Supply Chain Forecast 2011 vs 2010

3

2

-1

0

14

Combined GDP

Electronic Equipment

Rigid & Flex PCBs

Semiconductors

Semi Capital Spending

0 5 10 15% Change

20120205

Henderson Ventures

Gartner

Henderson Ventures

Custer Consulting Group

Henderson Ventures

Global Economy

20050118

Industrial Production - World% Change vs. One Year Earlier

Economist 2/2012 http://www.economist.com Output, prices and jobs

20120229

Europe- EU27Manufacture of computer, electronic & optical products

3/12 & 12/12 Rate of Change

3 6 9 12 3 6 9 12 3 6 9 12 3 6 9 12 3 6 9 12 3 6 9 12 3 6 9 12 3 6 9 12 3 6 9 12 3 6 9 12 3 6 9 12 3 6 9 12 3 6 9 1299 00 01 02 03 04 05 06 07 08 09 10 11

CALENDAR YEAR

0.75

0.8

0.85

0.9

0.95

1

1.05

1.1

1.15

1.2

1.25Rate of Growth (1.0=no growth)

12/12 3/12 Zero Growth

Eurostat, class C26

20120215

Japan Electronic Equipment Production by Month - 2000 to Present

JEITA www.jeita.or.jp/

1 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 911100 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

0

100

200

300

400

500

600

700

800Yen Billion

Consumer Electronic EquipmentElectronic Measuring InstrumentationCommunications EquipmentComputers & Related EquipmentElectronic Business MachinesElec Application Equip

20120227

U.S. Electronic Equipment - Orders, Shipments &

Inventories

20050118

U.S. Electronic Equipment Book/Bill Ratio3-Month Average

1.0731.01710.9831 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 710196 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

0.85

0.9

0.95

1

1.05

1.1

1.15B/B (3 Month Avg)

http://www.census.gov/indicator/www/m3/

20120229

1-monthB/B =0.96

U.S. Electronic Equipment OrdersAdjusted vs Non Seasonally Adjusted

www.census.gov/indicator/www/m3/

1 7 1 7 1 7 1 7 1 7 1 7 1 7 1 7 1 7 1 7 1 7 1 7 1 7 1 7 1 7 1 7 1 71/1295 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11

CALENDAR YEAR

8

12

16

20

24

28

32

36

40$ B

AdjustedNot Adjusted

20120205

U.S. Electronic Equipment Order & Shipment GrowthComputer, Communications, Measurement & Control and Military

1 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 710195 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

0.6

0.7

0.8

0.9

1

1.1

1.2

1.33/12 rate of growth

Shipments Orders Zero Growth

http://www.census.gov/indicator/www/m3/

20120229

US Electronic Equipment OrdersMonthly Data

http://www.census.gov/indicator/www/m3/

1 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 7101 4 710199 00 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

0

2

4

6

8

10

12

14

$ B (Seasonally Adjusted)Search & NavigationElectromedical, Instruments & ControlsCommunicationComputerDefense

20120229

U.S. Electronic Equipment Orders

http://www.census.gov/indicator/www/m3/

1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 1000 01 02 03 04 05 06 07 08 09 10 11

CALENDAR YEAR

0

5

10

15

20

25

30

35$ Billion

Military-CommunicationsMilitary-Search & NavigationComputer & RelatedCommunications- non MilitarySearch & Navigation - non MilitaryMedical, Measuring & Control

Military

20120205

Instruments

Communication

Computer

U.S. Electronic Equipment Orders

http://www.census.gov/indicator/www/m3/

1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 1000 01 02 03 04 05 06 07 08 09 10 11

CALENDAR YEAR

0%

20%

40%

60%

80%

100%

Military-CommunicationsMilitary-Search & NavigationComputerCommunications- non MilitarySearch & Navigation - non MilitaryMedical, Measuring & Control

Military

20120205

Computer

Communication

Instruments

US Electronic Equipment InventoriesMonthly Data

http://www.census.gov/indicator/www/m3/

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 195 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

0

2

4

6

8

10

12

14

16

18

$ B (Seasonally Adjusted)

SEARCH & NAVIGATIONELECTROMEDICAL, MEASURE & CONTROLCOMMUNICATIONCOMPUTERDEFENSE

20120229

Value of U.S. "Computers & Electronic Products" Inventories by Stage of Fabrication

Decemberber 2011

www.census.gov/indicator/www/m3/hist/naicsinvp.xls

Materials & Supplies39.1%

Work in Process36.7%

Finished Goods24.2%

TOTAL: $47.3 Billion

20120205

Value of U.S. "Computers & Electronic Products" Inventories by Stage of Fabrication

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 192 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

5

10

15

20

25

30$ Billions

Materials & Supplies Work in Process Finished Goods

http://www.census.gov/indicator/www/m3/hist/naicsinvp.xls

20120205

U.S. Electronic Equipment InventoriesInventories vs. Orders

www.census.gov/indicator/www/m3/

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 192 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

1

1.2

1.4

1.6

1.8

2

2.2

2.4

20120229

Market Segments2005011820050118

Volume (Shift to Low Cost Areas)Personal ComputersMobile PhonesOther Consumer ElectronicsDatacom/TelecomAutomotive

"Protected"MilitaryMedicalInstruments & ControlsHigh IP Content

Prototype, Quick Response, Short Run, Need for Local Support

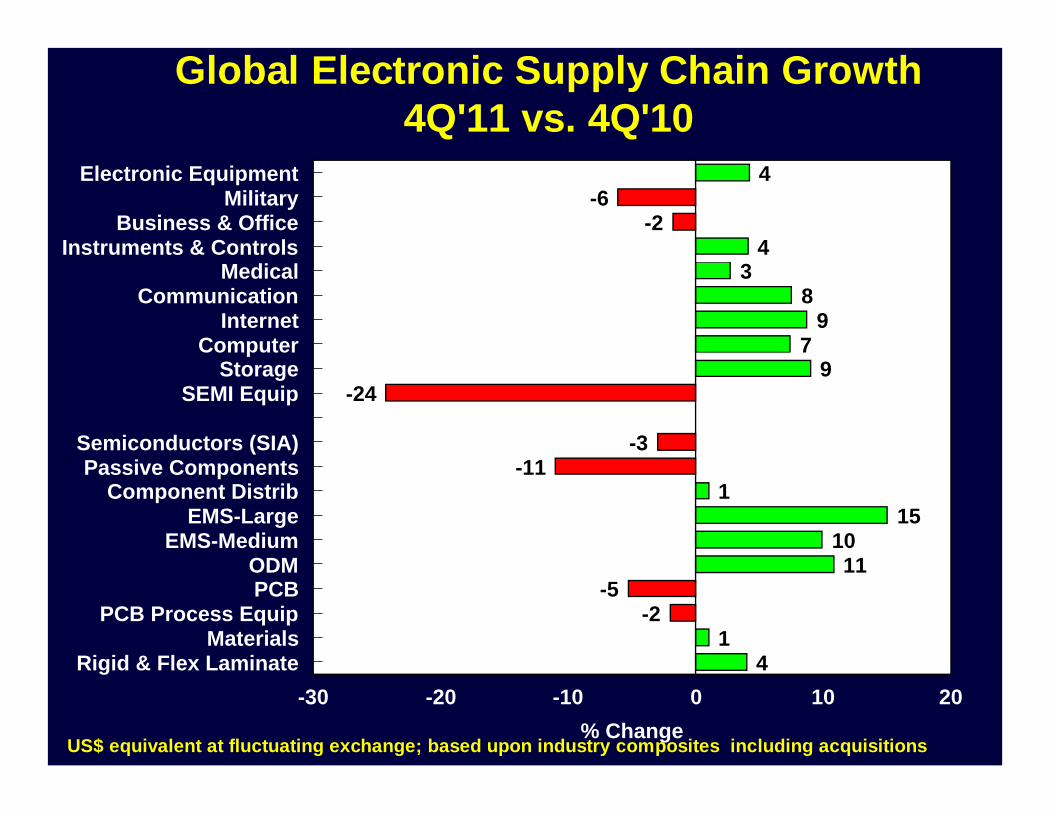

Global Electronic Supply Chain Growth 4Q'11 vs. 4Q'10

4-6

-24

38

97

9-24

-3-11

115

1011

-5-2

14

Electronic EquipmentMilitary

Business & OfficeInstruments & Controls

MedicalCommunication

InternetComputer

StorageSEMI Equip

Semiconductors (SIA)Passive Components

Component DistribEMS-Large

EMS-MediumODMPCB

PCB Process EquipMaterials

Rigid & Flex Laminate0 10 20-10-20-30

% Change

20120226

US$ equivalent at fluctuating exchange; based upon industry composites including acquisitions

Instruments & Control EquipmentComposite of 12 Public Companies

Revenue, Net Income & Inventory

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 400 01 02 03 04 05 06 07 08 09 10 11

0.0

5.0

10.0

15.0

20.0

-5.0

US$ Billions

Revenue 9.2 9.410.29.5 9.6 8.7 7.9 7.4 7.5 7.9 8.1 7.5 7.8 8.08.3 8.3 8.8 9.0 9.3 9.2 9.3 9.8 9.7 9.710.110.710.911.012.313.113.813.414.115.015.113.111.912.112.512.712.813.214.214.114.615.516.014.6Income 0.9 0.9 1.00.8 0.8 0.3 0.3-0.1-0.0 0.2 0.2 0.0 0.2-1.0 0.5 0.5 0.6 0.7 0.8 0.8 0.8 0.8 0.8 3.7 0.9 1.1 1.0 1.2 1.6 1.2 1.4 1.3 1.3 1.4 1.5 0.9 0.6 0.8 0.9 1.0 1.1 1.4 1.6 1.6 1.4 2.1 1.2 1.2

Inventory 6.4 6.5 5.56.2 5.9 5.6 5.2 5.0 4.8 4.7 4.4 4.4 4.4 4.44.1 4.3 4.4 4.3 4.6 4.7 4.7 4.6 4.5 4.5 4.6 4.9 4.8 6.0 5.7 5.9 5.8 6.1 6.4 6.5 6.2 6.3 6.0 5.7 5.4 5.5 5.7 5.9 6.1 6.2 6.7 7.0 6.7 7.0

Agilent, Ametek, Emerson, Itron, Keithly, LeCroy, PerkinElmer, Rockwell Automation, Teledyne, ThermoFisher, Varian, Woodward Govenor

+4%

20120226

4Q'11 estimate based upon partial data

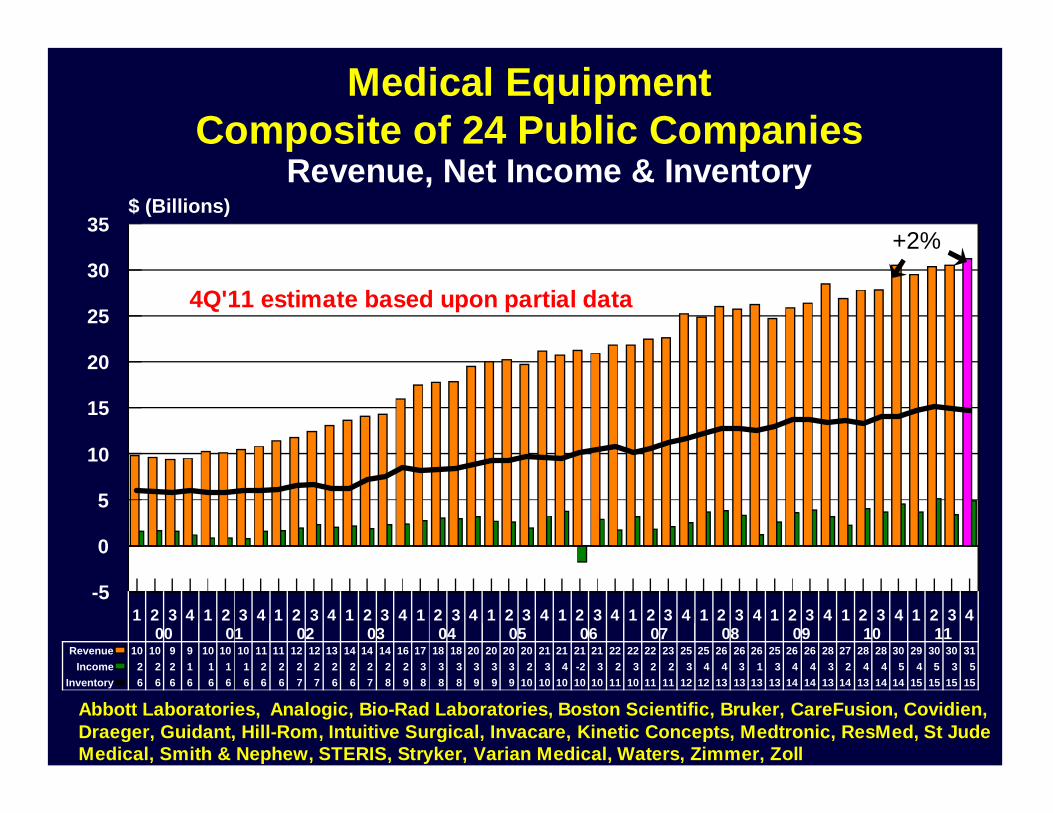

Medical EquipmentComposite of 24 Public Companies

Revenue, Net Income & Inventory

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 400 01 02 03 04 05 06 07 08 09 10 11

0

5

10

15

20

25

30

35

-5

$ (Billions)

Revenue 10 10 9 9 10 10 10 11 11 12 12 13 14 14 14 16 17 18 18 20 20 20 20 21 21 21 21 22 22 22 23 25 25 26 26 26 25 26 26 28 27 28 28 30 29 30 30 31Income 2 2 2 1 1 1 1 2 2 2 2 2 2 2 2 2 3 3 3 3 3 3 2 3 4 -2 3 2 3 2 2 3 4 4 3 1 3 4 4 3 2 4 4 5 4 5 3 5

Inventory 6 6 6 6 6 6 6 6 6 7 7 6 6 7 8 9 8 8 8 9 9 9 10 10 10 10 10 11 10 11 11 12 12 13 13 13 13 14 14 13 14 13 14 14 15 15 15 15

Abbott Laboratories, Analogic, Bio-Rad Laboratories, Boston Scientific, Bruker, CareFusion, Covidien, Draeger, Guidant, Hill-Rom, Intuitive Surgical, Invacare, Kinetic Concepts, Medtronic, ResMed, St Jude Medical, Smith & Nephew, STERIS, Stryker, Varian Medical, Waters, Zimmer, Zoll

+2%

20120226

4Q'11 estimate based upon partial data

Military EquipmentComposite of 6 Public Companies

Revenue, Net Income & Inventory

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 400 01 02 03 04 05 06 07 08 09 10 11

0.0

10.0

20.0

30.0

40.0

50.0

-10.0

$ Billions

Revenue 16.115.915.518.014.317.517.921.218.219.119.322.321.723.924.827.226.332.126.830.227.329.629.131.929.031.230.833.130.032.933.735.632.635.534.636.834.736.135.437.935.236.937.139.433.935.135.537.0Income 0.3 0.6-0.1 0.7 0.4 0.4 0.2-1.0 0.2 0.3 0.7-0.1 0.9 0.9 0.7 1.2 1.0 1.2 1.2 1.4 1.4 1.5 1.5 1.7 1.8 2.2 1.9 2.2 2.2 3.3 2.4 2.7 2.2 2.7 2.7-0.6 2.4 2.2 2.6 2.6 2.4 2.7 2.8 2.8 2.4 2.6 2.7 2.6

Inventory 8.9 8.3 8.7 8.3 8.6 9.6 9.2 8.6 8.7 8.6 7.9 7.8 7.6 7.7 7.4 7.6 7.7 7.5 7.2 6.8 7.0 7.0 7.2 7.0 7.5 7.8 8.1 6.1 6.0 6.1 6.0 6.3 6.4 6.3 6.6 7.0 7.1 7.0 7.3 7.5 7.7 7.4 7.3 7.8 7.7 7.9 7.5 8.0

General Dynamics, Harris, Lockheed, Northrop Grumman, Raytheon, Rockwell Collins

-6%

20120206

U.S. Defense Capital GoodsOrders & Shipments

http://www.census.gov/indicator/www/m3/

147101471014 71014710147101471014710147101471014 7101471014710147101 4710147101471014710147101471014710192 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

1

6

11

16

21

26

$ Billions

OrdersShipments

20120229

Computer, Data Storage, Datacom & Telecom Equipment Suppliers

Composite of 43 Public Companies

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 400 01 02 03 04 05 06 07 08 09 10 11

0

50

100

150

200

250

-50

$ Billion

Revenue 100107111117 99 103 96103 89 90 91 101 91 94 99 112105107109125114119122137125130135153139148156179160169173164138147156179161169181205185195196221Income 8 9 8 5 -3 -7-13 0 1 -13 -3 0 3 3 5 8 7 8 8 11 9 9 10 13 9 9 11 14 11 14 13 14 12 11 11 -2 7 11 12 18 14 15 18 24 19 19 18 28

Inventory 39 41 45 47 48 41 35 31 28 26 26 23 23 23 23 23 24 25 25 25 26 26 27 27 28 30 32 32 32 35 36 36 38 39 39 34 31 30 31 31 31 34 36 38 38 41 43 40

+8%

20120226

Computer 13, Internet 9, Storage 10, Communication 12

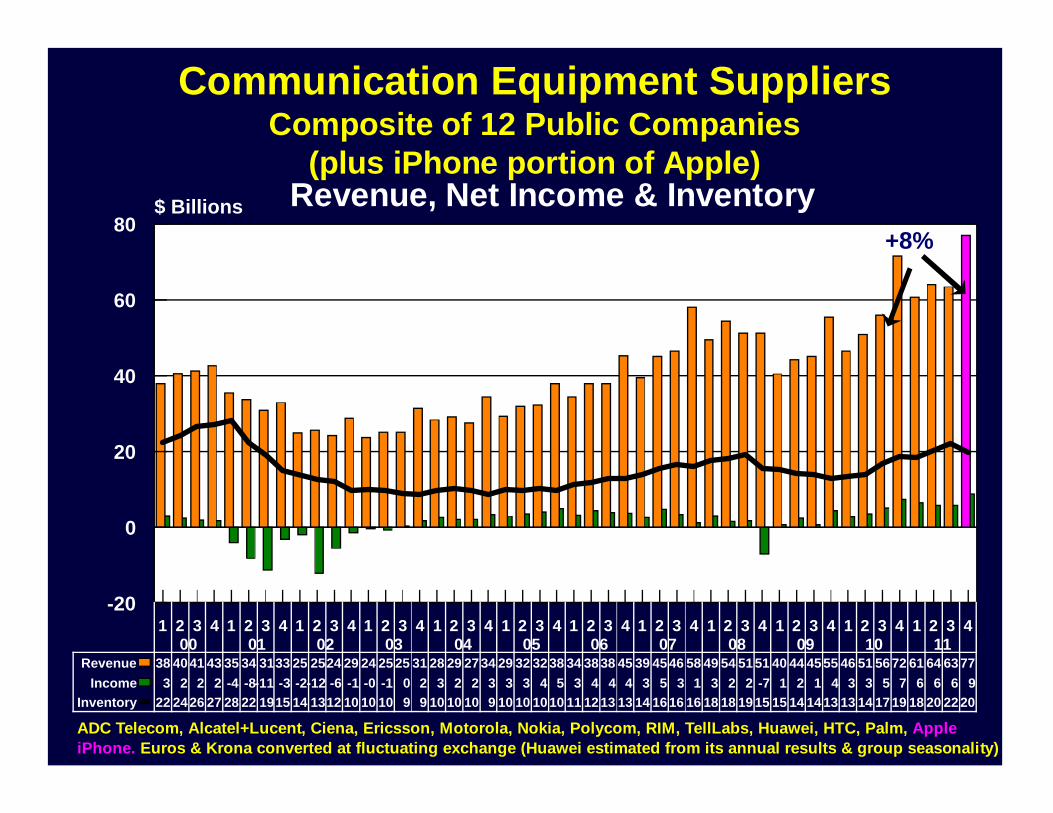

Communication Equipment SuppliersComposite of 12 Public Companies

(plus iPhone portion of Apple)Revenue, Net Income & Inventory

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 400 01 02 03 04 05 06 07 08 09 10 11

0

20

40

60

80

-20

$ Billions

Revenue 38 4041 43 35 34 3133 25 2524 29 24 2525 31 28 29 2734 29 32 3238 34 3838 45 39 4546 58 49 54 5151 40 44 4555 46 51 5672 61 64 6377Income 3 2 2 2 -4 -8-11 -3 -2-12 -6 -1 -0 -1 0 2 3 2 2 3 3 3 4 5 3 4 4 4 3 5 3 1 3 2 2 -7 1 2 1 4 3 3 5 7 6 6 6 9

Inventory 22 2426 27 28 22 1915 14 1312 10 10 10 9 9 10 10 10 9 10 10 1010 11 1213 13 14 1616 16 18 18 1915 15 14 1413 13 14 1719 18 20 2220

ADC Telecom, Alcatel+Lucent, Ciena, Ericsson, Motorola, Nokia, Polycom, RIM, TellLabs, Huawei, HTC, Palm, Apple iPhone. Euros & Krona converted at fluctuating exchange (Huawei estimated from its annual results & group seasonality)

+8%

2007021320120215

World Mobile Phone Unit ShipmentsTotal Sales - Analog & Digital

Gartner Dataquest 2/12, ABI Research (2012 data forecast) 1/12

108172

284413 400 432

520

674817

991

1,1531,2221,211

1,388

1,597

1,775

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 20120

500

1,000

1,500

2,000

20120218

Smartphone Unit Shipments to End UsersWorld

Gartner DataQuest 11/11, IDC 2/12

4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 407 08 09 10 11

0

20

40

60

80

100

120

140

160

180Units (Millions)

20120209

Computer Equipment SuppliersComposite of 13 Public Companies

Revenue, Net Income & Inventory

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 400 01 02 03 04 05 06 07 08 09 10 11

0

20

40

60

80

100

120

-20

$ Billion

Revenue 51 54 57 60 52 58 55 59 54 54 56 61 57 58 62 68 64 65 68 76 70 71 75 82 74 75 79 88 80 83 88 97 88 92 98 92 79 83 89 99 90 9410010899104105116Income 4 5 4 4 2 2 1 3 2 -1 2 0 3 3 3 5 3 4 4 5 4 4 3 6 4 4 5 7 5 6 6 9 6 7 6 8 5 7 8 10 7 8 10 1310 11 9 15

Inventory 14 14 15 15 16 15 12 13 12 11 11 11 11 11 11 11 12 12 13 13 12 13 13 13 13 14 14 15 14 15 15 15 15 16 15 14 12 12 13 13 13 15 14 1414 15 15 15

+7%

20120225

Acer+Gateway, Apple, Creative Tech, Cray, Dell, HP, IBM, Lenovo, Mercury, NCR, Sun Micro, Unisys

Apple iPhone financials reported in Communication sectorMedia tablets included with "Computer Equipment"

Media Tablet ShipmentsEmerging & Mature Markets

DisplaySearch 10/11

20

64

110

163

209

259

311

367

2010 2011 2012 2013 2014 2015 2016 20170

100

200

300

400

Emerging 4 25 40 64 88 119 148 185Mature 17 39 70 99 120 140 163 182

20110925

Semiconductors

20050118

Global Semiconductor Shipments3-Month Growth Rates on $ Basis

Total $ Shipments from All Countries to an AreaSIA website: www.sia-online.org/

1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 184 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

0.4

0.6

0.8

1

1.2

1.4

1.63/12 Rate of Change

1

2 3

4

5

6

7

8

9

10

20120205

11 12

13

World Semiconductor Shipments Monthly US$

SIA

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 183 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

0

5

10

15

20

25

30US$ Billions (3-month average)

20120205

2009 recession much sharper but shorter than 2001

Record high

Monthly Semiconductor Shipments$ Billions (3-month average)

SIA www.sia-online.org/

12/10 12/11 % CH

Americas 4.57 4.36 -4.6%

Europe 3.30 2.78 -15.8%

Japan 3.97 3.59 -9.5%

Asia Pacific 13.31 13.10 -1.6%

Total 25.15 23.83 -5.3%

20120205

CCG Semiconductor Leading Indicator vs. Global Semiconductor Shipments

1 7 1 7 1 7 1 7 1 7 1 7 1 7 1 7 1 7 1 7 1 7 1 7 100 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

0.30.40.50.60.70.80.9

11.11.21.31.41.51.61.7

3/12 rate of growthCCG Semiconductor Leading IndicatorZero GrowthSIA Semiconductor Shipments

http://www.census.gov/indicator/www/m3/

20120301

2-monthlead

Semiconductor Shipments to N. Americavs. U.S Electronic Equipment Production

Total $ Semiconductor Shipments from All Countries to N. America www.sia-online.org/U.S. Electronic Equipment Shipments www.census.gov/indicator/www/m3/

1357911135791113579111357911135791113579111357911135791113579111357911135791113579111357911199 00 01 02 03 04 05 06 07 08 09 10 11 12

0.4

0.6

0.8

1

1.2

1.4

1.6

1.83/12 Rate of Change (US$)

SemiconductorsEquipment

20120229

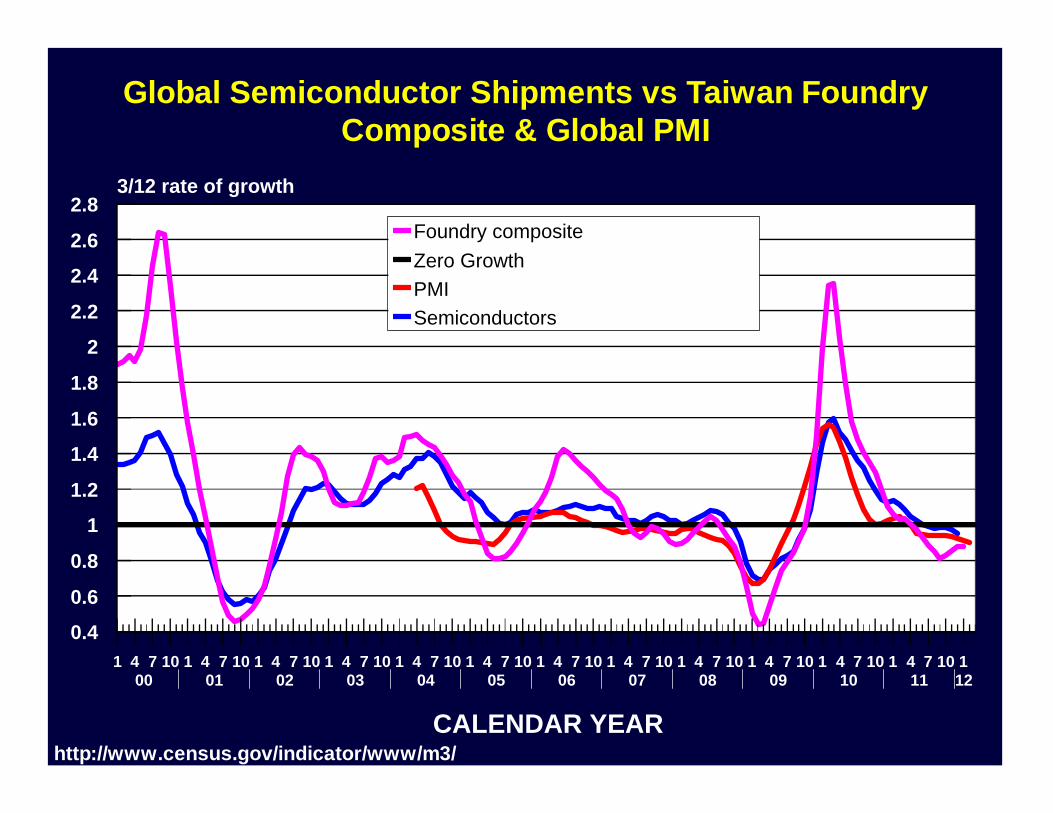

Global Semiconductor Shipments vs Taiwan Foundry Composite & Global PMI

1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 100 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

2.2

2.4

2.6

2.83/12 rate of growth

Foundry compositeZero GrowthPMISemiconductors

http://www.census.gov/indicator/www/m3/

20120301

Semiconductor Fab, Assembly, Packaging,Test & Measurement

Equipment

20050118

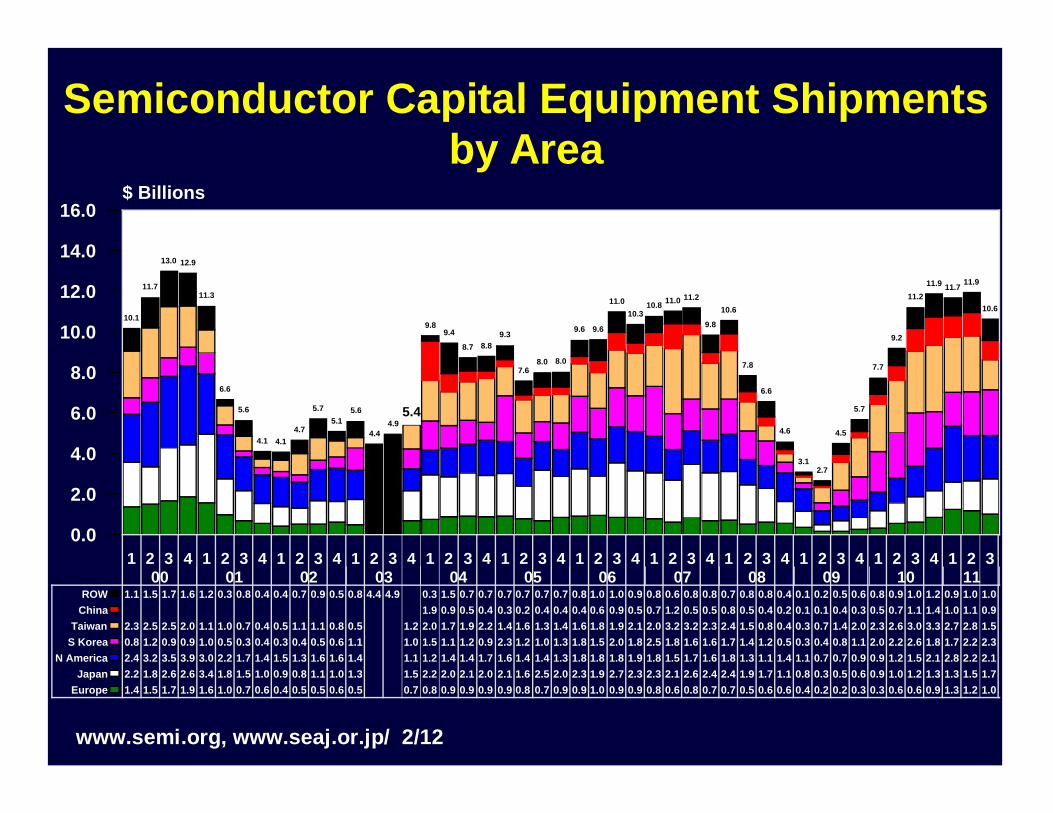

Semiconductor Capital Equipment Shipments by Area

5.4

10.1

11.7

13.0 12.9

11.3

6.6

5.6

4.1 4.14.7

5.75.1

5.6

4.44.9

9.89.4

8.7 8.89.3

7.68.0 8.0

9.6 9.6

11.010.3

10.8 11.0 11.2

9.8

10.6

7.8

6.6

4.6

3.12.7

4.5

5.7

7.7

9.2

11.211.9 11.7 11.9

10.6

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 300 01 02 03 04 05 06 07 08 09 10 11

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0$ Billions

Europe 1.4 1.5 1.7 1.9 1.6 1.0 0.7 0.6 0.4 0.5 0.5 0.6 0.5 0.7 0.8 0.9 0.9 0.9 0.9 0.8 0.7 0.9 0.9 1.0 0.9 0.9 0.8 0.6 0.8 0.7 0.7 0.5 0.6 0.6 0.4 0.2 0.2 0.3 0.3 0.6 0.6 0.9 1.3 1.2 1.0Japan 2.2 1.8 2.6 2.6 3.4 1.8 1.5 1.0 0.9 0.8 1.1 1.0 1.3 1.5 2.2 2.0 2.1 2.0 2.1 1.6 2.5 2.0 2.3 1.9 2.7 2.3 2.3 2.1 2.6 2.4 2.4 1.9 1.7 1.1 0.8 0.3 0.5 0.6 0.9 1.0 1.2 1.3 1.3 1.5 1.7

N America 2.4 3.2 3.5 3.9 3.0 2.2 1.7 1.4 1.5 1.3 1.6 1.6 1.4 1.1 1.2 1.4 1.4 1.7 1.6 1.4 1.4 1.3 1.8 1.8 1.8 1.9 1.8 1.5 1.7 1.6 1.8 1.3 1.1 1.4 1.1 0.7 0.7 0.9 0.9 1.2 1.5 2.1 2.8 2.2 2.1S Korea 0.8 1.2 0.9 0.9 1.0 0.5 0.3 0.4 0.3 0.4 0.5 0.6 1.1 1.0 1.5 1.1 1.2 0.9 2.3 1.2 1.0 1.3 1.8 1.5 2.0 1.8 2.5 1.8 1.6 1.6 1.7 1.4 1.2 0.5 0.3 0.4 0.8 1.1 2.0 2.2 2.6 1.8 1.7 2.2 2.3Taiwan 2.3 2.5 2.5 2.0 1.1 1.0 0.7 0.4 0.5 1.1 1.1 0.8 0.5 1.2 2.0 1.7 1.9 2.2 1.4 1.6 1.3 1.4 1.6 1.8 1.9 2.1 2.0 3.2 3.2 2.3 2.4 1.5 0.8 0.4 0.3 0.7 1.4 2.0 2.3 2.6 3.0 3.3 2.7 2.8 1.5

China 1.9 0.9 0.5 0.4 0.3 0.2 0.4 0.4 0.4 0.6 0.9 0.5 0.7 1.2 0.5 0.5 0.8 0.5 0.4 0.2 0.1 0.1 0.4 0.3 0.5 0.7 1.1 1.4 1.0 1.1 0.9ROW 1.1 1.5 1.7 1.6 1.2 0.3 0.8 0.4 0.4 0.7 0.9 0.5 0.8 4.4 4.9 0.3 1.5 0.7 0.7 0.7 0.7 0.7 0.7 0.8 1.0 1.0 0.9 0.8 0.6 0.8 0.8 0.7 0.8 0.8 0.4 0.1 0.2 0.5 0.6 0.8 0.9 1.0 1.2 0.9 1.0 1.0

www.semi.org, www.seaj.or.jp/ 2/12

20120225

Worldwide Semiconductor Capital Equipment Market by Geography (with forecast)

19.8 22.2

37.132.9

40.5 42.8

29.5

15.9

39.9 41.837.3

40.1

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130.0

10.0

20.0

30.0

40.0

50.0$ Billions

N America 5.9 4.7 5.8 5.7 7.3 6.6 5.6 3.4 5.8 8.8 6.8 7.2Japan 3.9 5.6 8.3 8.2 9.2 9.3 7.0 2.2 4.4 5.8 5.2 5.7

Taiwan 3.5 2.9 7.8 5.7 7.3 10.7 5.0 4.4 11.3 8.1 6.9 8.3Europe 2.1 2.6 3.4 3.3 3.6 2.9 2.5 1.0 2.3 3.9 3.4 3.5

S Korea 1.7 3.2 4.6 5.8 7.0 7.4 4.9 2.6 8.6 8.0 8.6 8.4China 1.2 2.7 1.3 2.3 2.9 1.9 0.9 3.7 3.8 3.5 3.8ROW 2.7 2.1 4.5 2.9 3.7 3.1 2.6 1.4 3.8 3.5 2.9 3.2

SEMI 11/2011 (and prior reports)

20111207

Global Semiconductor & Semiconductor Capital Equipment3-Month Shipment Growth Rates on $ Basis

Sources: SIA; Semiconductor Equipment Association of Japan, www.semi.org

159159159159159159159159159159159159159159159159159159159159159159159159159159159159184 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 1112

0.20.40.60.8

11.21.41.61.8

22.22.42.62.8

33.23.43.6

3/12 Rate of Change

SemiconductorsSEMI Capital EquipSeries 5

Chips

Capital Equipment

20120226

Solar/Photovoltaic

20050118

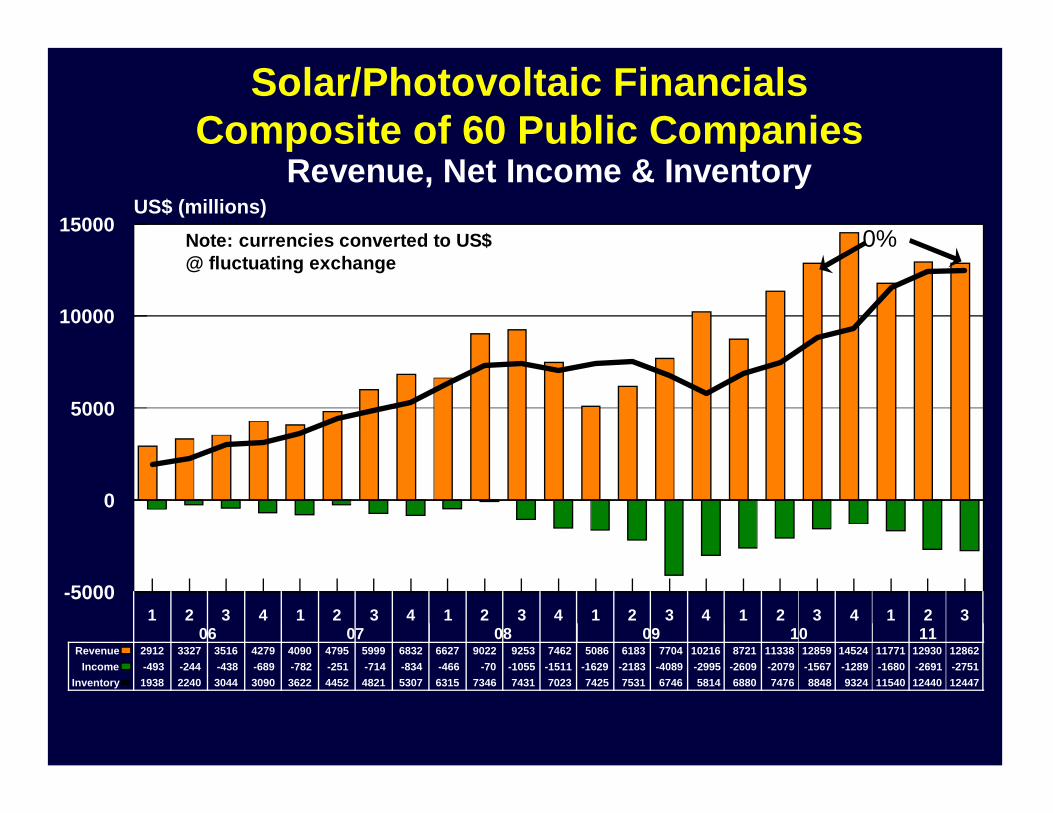

Solar/Photovoltaic FinancialsComposite of 60 Public Companies

Revenue, Net Income & Inventory

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 306 07 08 09 10 11

0

5000

10000

15000

-5000

US$ (millions)

Revenue 2912 3327 3516 4279 4090 4795 5999 6832 6627 9022 9253 7462 5086 6183 7704 10216 8721 11338 12859 14524 11771 12930 12862Income -493 -244 -438 -689 -782 -251 -714 -834 -466 -70 -1055 -1511 -1629 -2183 -4089 -2995 -2609 -2079 -1567 -1289 -1680 -2691 -2751

Inventory 1938 2240 3044 3090 3622 4452 4821 5307 6315 7346 7431 7023 7425 7531 6746 5814 6880 7476 8848 9324 11540 12440 12447

0%

20120102

Note: currencies converted to US$ @ fluctuating exchange

Taiwan Solar/Photovoltaic Panel CompaniesComposite of 17 Manufacturers

135791113579111357911135791113579111357911135791113579111357911135791113579111357911100 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

0

2

4

6

8

10

12

14

16

18

20NT$ billions

20120212

Big Sun Energy Technology, Daxon, DelSolar, e_TON Solar Tec, Eversol, Gintech, Green Energy Technology (GET), Ligitek, Motech, Neo Solar Power, Phoenixtec Power Co (PPC), Precision Silicon, Sino-American Silicon Products, Sonartech, Sysgration, Tyntek, Wafer Works

2011/2010 Revenuedown 18%

Component Distributors

20050118

DMASS European Semiconductor Distribution Industry

DMASS 2/2012 http://dmass.com/

598

434

139 118126 117110 96

203 209199142

4Q 4Q10 11

0

200

400

600

800Euros (millions)

GermanyItalyUKFranceE EuropeNordic

20120215

Only GrowthRegions

Georg Steinberger, chairman of DMASS, commented on the results: "As expected, 2011 remained positive and set another sales record for semiconductor distribution. However, the last quarter displayed very precisely the current market trends of cautious ordering behaviour in some and inventory corrections in some other industry segments. The two halves of 2011 couldn't have been more different, from 23% plus to 7% minus. Predictions under the current climate would be dangerous, but I would not be surprised to see exactly the opposite in 2012 - weak first half and stronger second half."

DMASS

1121

1027983 967

120012201170

1060

1185115310931130

138014001340

1270

1480

13701310

1210

13721340

1220

1075992

869926 960

1345

15001560

1470

1810

1710

1500

1350

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 403 04 05 06 07 08 09 10 11

0

500

1000

1500

2000Euros (millions)

Germany 342 297 274 368 348 342 292 357 342 343 333 439 438 434 393 491 435 434 380 461 437 419 347 329 289 315 314 457 498 551 494 640 603 531 434Italy 161 152 158 171 138 140 175 166 131 144 198 193 159 160 201 182 155 152 183 174 132 117 116 99 91 104 155 166 153 143 200 183 136 118UK 157 144 149 154 154 133 137 138 138 140 149 158 154 142 146 133 127 109 117 116 110 101 86 82 86 83 112 128 138 125 144 138 128 117

France 116 103 122 125 118 118 124 116 105 107 133 130 118 113 129 117 107 102 114 111 96 93 91 78 73 78 111 118 109 112 130 122 104 96Other 346 331 983 693 403 422 418 377 392 391 376 406 461 481 475 462 513 503 487 467 497 502 464 417 370 321 361 381 510 590 609 596 696 664 601 585

20120215

European Semiconductor Distribution Industry

http://dmass.com/

EMS & ODM Companies

20050118

Large Global EMS Providers2010 vs. 2011 Sales ($M)

2010 2011 Growth %Hon Hai (Foxconn) Taiwan 74,341 94,122 +27%Flextronics Singapore 27,761 29,944 +8%Jabil Circuit USA 14,403 16,763 +16%Celestica Canada 6,526 7,213 +11%Sanmina-SCI USA 6,503 6,442 - 1%Benchmark Elec USA 2,402 2,253 -6%Plexus USA 2,149 2,195 +2%Venture Mfg Singapore 1,967 1,935 -2%Sypris USA 267 339 +27%

Total 136,319 161,206 +18%

Sources: Company data Local currency converted at fluctuating exchange

2011/2010

20120226

Large EMS Providers Composite of 9 Public Companies

Revenue, Net Income & Inventory

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 100 01 02 03 04 05 06 07 08 09 10 11 12

0

10

20

30

40

50

-10

US$ Billions @ fluctuating exchange

Revenue 12 15 17 21 18 16 15 15 14 15 15 16 15 15 16 18 17 18 19 20 19 20 20 23 20 22 25 28 23 25 28 31 26 27 32 30 21 22 25 28 27 31 38 41 35 39 40 47 43Income 0 -0 0 0 0 0 -0 0 -0 -0 -3 -0 0 -3 -0 0 0 0 0 -0 -1 0 1 1 0 1 1 1 1 1 -0 0 0 1 0 -7 -1 0 1 1 1 1 1 1 1 1 1 1

Inventory 7 9 11 12 13 11 10 9 8 7 7 6 6 6 7 7 8 8 8 8 8 8 8 9 9 11 12 12 12 12 13 12 11 13 13 10 9 9 9 9 10 11 13 12 13 13 14 14

Benchmark+Pemstar, Celestica, Flextronics+Solectron, Foxconn, Jabil, Plexus, Sanmina-SCI, Sypris, Venture Mfg

+15%

20120226

+23%Q1'12/Q1'11

Guidance

Most of growth due to Foxconn

Large EMS Providers Composite of 8 Public Companies

Quarterly Revenue Growth

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 401 02 03 04 05 06 07 08 09 10 11

0.0

20.0

40.0

60.0

-20.0

-40.0

Benchmark+Pemstar, Celestica, Flextronics+Solectron, Jabil, Plexus, Sanmina-SCI, Sypris,Venture Mfg

20120226

Excludes Foxconn

Large Taiwan ODM Providers 2011 vs. 2010 Sales ($M)

2010 2011 Growth %Foxconn (Hon Hai) 78,705 94,361 20%Quanta Computer 36,184 36,084 0%Compal Electronics 28,734 22,099 -23%Wistron 18,573 19,937 7%Chimei Innolux 17,986 16,516 -8%Inventec 11,887 11,515 -3%Asustek Computer 10,086 10,809 7%Lite On Technology 3,480 3,219 -8%Mitac International 1,689 1,144 - 32%Inventec Appliance 1,490 842 - 44%Total 208,813 216,526 + 4%

Source: Company data, NT$ converted at constant avg 2011 exchange (29.39 NT$ = 1US$)

2011/2010

20120112

Taiwan ODM CompaniesComposite Sales of 10 Large Manufacturers

Company Financial Releases

13579111357911135791113579111357911135791113579111357911135791113579111357911135791113579111357911198 99 00 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

050

100150200250300350400450500550600650700

NT$ (Billions)

Asustek Computer, Chei Mei, Compal Electronics, Foxconn, Chimei Innolux , Inventec, Inventec Appliance, Lite On Technology, Mitac International, Quanta Computer, Wistron, Chei Mei Display replacing Chei Mei & Innolux Display 3/10 & later

20120212

2010/2009+34%

Large ODM Companies Composite of 10 Public Manufacturers

Quarterly Revenue Growth

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 499 00 01 02 03 04 05 06 07 08 09 10 11

0

20

40

60

80

-20

20120113

Asustek Computer, Compal Electronics, Foxconn, Chimei Innolux, Inventec, Inventec Appliance, LiteOn Technology, Mitac International, Quanta Computer, Wistron

Foxconn major cause of growth

PCB Fabrication

20050118

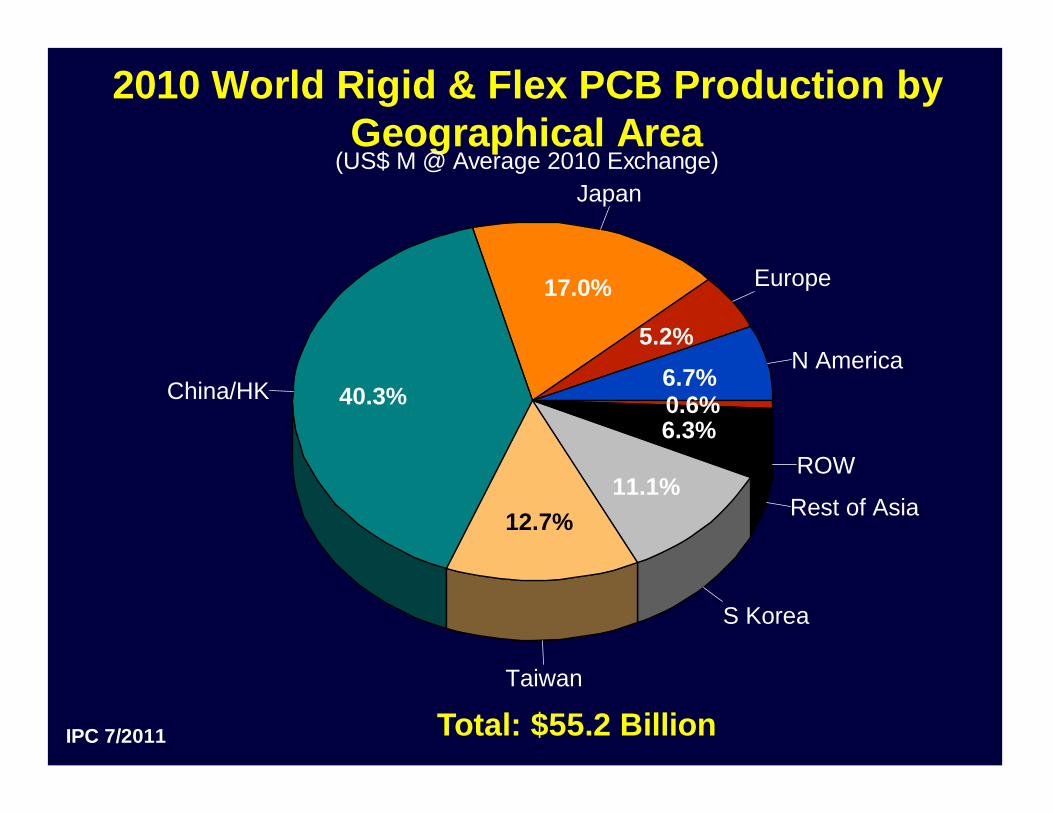

2010 World Rigid & Flex PCB Production by Geographical Area

IPC 7/2011

N America

Europe

Japan

China/HK

Taiwan

S Korea

Rest of Asia

ROW

6.7%5.2%

17.0%

40.3%

12.7%11.1%

6.3%0.6%

Total: $55.2 Billion

20110914

(US$ M @ Average 2010 Exchange)

Japan PCB Shipments

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 182 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

0

20

40

60

80

100Yen (billion)

www.jpca.org/kikaitoukei/kikai2011.xls

20120227

2010/2009+16%

Taiwan Shipments42 Rigid PCB & 8 Laminate Manufacturers

Company Financial Releases

13579111357911135791113579111357911135791113579111357911135791113579111357911101 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

7

10

13

16

19

22

25

28

31

34PCB - NT$ (billions)

0

500

1000

1500

2000

2500

3000

3500Laminate - NT$ (millions)

PCB Laminate

20120212

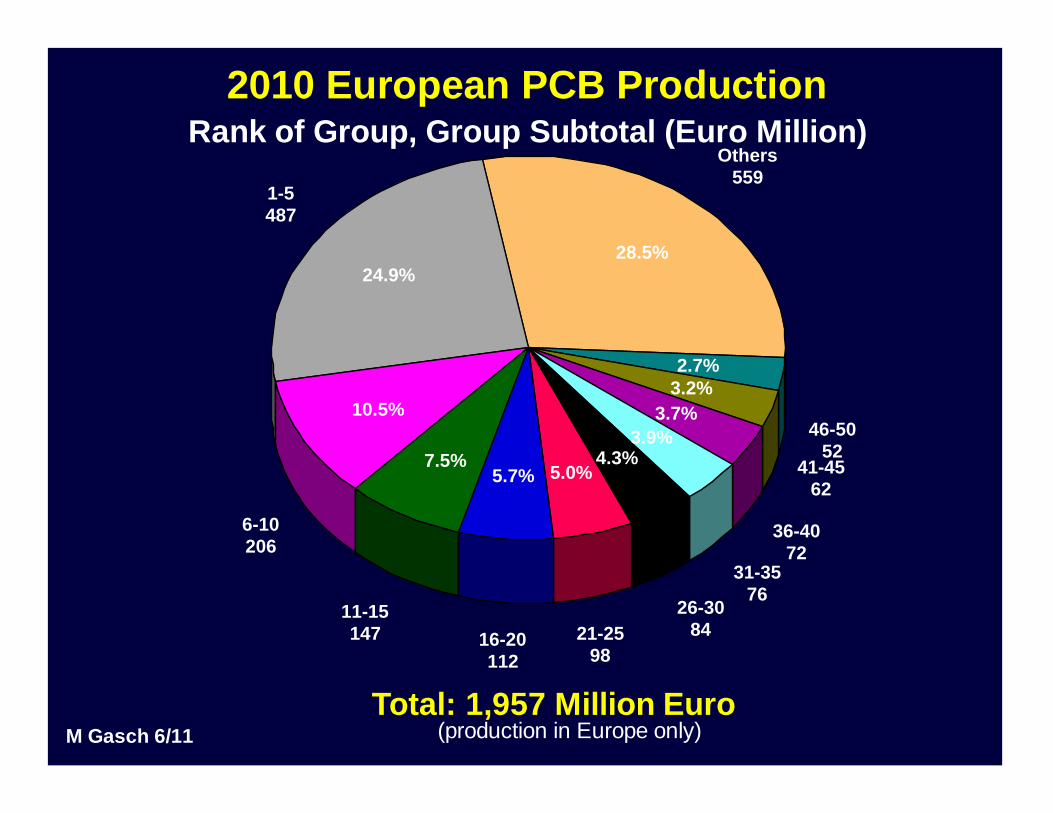

2010 European PCB Companies

M Gasch 6/2011

20100711

Rank Maker Rank Maker1 Wurth 26 Greule2 AT&S 27 Cistel-Laier3 Schweizer Electronic 28 Optiprint4 Multek 29 LPP Pfullingen5 KSG 30 Rohde & Schwarz6 Ruwel Int. 31 Precoplat7 Elvia Group 32 Technoflex8 Mektec Europe 33 ACB9 Cire Group 34 Eltos10 PPC 35 Freudenberg Mechatronic11 Somacis 36 Europrint Eger12 Schoeller 37 Ilfa13 GS Swiss PCB 38 Exception14 Dyconex 39 Ramaer15 Cicor Group 40 Cofidur-Tecchi16 Invotec 41 Graphic17 Hausermann 42 Elekonta Marek18 Flacon Group 43 Cimulec19 Varioprint 44 TW Elektronek20 Polytron Print 45 Jenaer Lp21 Schaltungsdruck Storz 46 Fela22 Elco 47 Pri Dana23 hmp 48 ggp Peters24 Aspocomp 49 Cebisa25 OMR 50 Cipsa

Total 1,957 Million Euros (production in Europe only)

2010 European PCB Production

M Gasch 6/11

1-5487

6-10206

11-15147 16-20

11221-25

98

26-3084

31-3576

36-4072

41-4562

46-5052

Others559

24.9%

10.5%

7.5%5.7% 5.0%

4.3%3.9%

3.7%3.2%2.7%

28.5%

Total: 1,957 Million Euro

20110711

Rank of Group, Group Subtotal (Euro Million)

(production in Europe only)

European PCB Monthly Shipments

1357911135791113579111357911135791113579111357911135791113579111357911135791113579111357911199 00 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

0

100

200

300

400

500

600Euros (fluctuating exchange)

Source: Custer Consulting Group estimate based upon industry data

20120118

N AMERICAN PCB GROWTH INDICATORS% GROWTH - Jan 2012 vs Jan 2011

RIGID PCB $ SHIPMENTSDown 3.1%

RIGID PCB $ BOOKINGSUp 10.9%

RIGID PCB BOOK/BILL RATIO3-MONTH AVG 1.01

1-MONTH 1.07FLEX CIRCUIT $ SHIPMENTS

Down 7.9%FLEX CIRCUIT $ BOOKINGS

Down 29.4%FLEX CIRCUIT BOOK/BILL RATIO

3-MONTH AVG 1.05 1-MONTH 1.09

20120301

N American Rigid PCB Shipments & Orders

IPC

1 2 3 4 5 6 7 8 91011121 2 3 4 5 6 7 8 91011121 2 3 4 5 6 7 8 91011121 2 3 4 5 6 7 8 9101112108 09 10 11 12

CALENDAR YEAR

0

50

100

150

200$M (statistical sample of about 50% of producers)

OrdersShipments

20120301

2011/2010 Rigid PCB Shipment Growth:

-2.3%

Note: IPC survey captures "market" not domestic production. About 15% of the above represents imported boards resold by N American PCB producers in survey.

U.S. Electronic Equipment vs Rigid PCBs$ Order Growth

IPC & U.S. Dept of Census

147101471014710147101471014710147101471014710147101471014710147101471014710147101471014710194 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

0.30.40.50.60.70.80.9

11.11.21.31.41.51.6

3/12 RATE OF CHANGE

EQUIPMENT

PCB

20120301

Inventory builds and excess orders

Inventory/order corrections

Materials&

Process Equipment

20050118

Copper, High Grade (HG, Comex)

http://futures.tradingcharts.com/chart/CP/B9

j 4 7101 4 7 101 4 7 101 4 7 101 4 7 101 4 7101 4 7101 4 7 101 4 7 101 4 7 101 4 7 101 4 7 10100 01 02 03 04 05 06 07 08 09 10 11 12

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

Material Suppliers (excluding laminate)Composite of 13 Companies

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 403 04 05 06 07 08 09 10 11

CY

0

500

1000

1500

2000

2500

3000

3500Thousands

Revenue 153915431617168818991905199320571900190022162139197721972043202921652408239324712699292426431940147118061922193620872348229422852481271225992315

+1%

Momentive, OM Group, Taiwan Glass, Baotech, Glotech, Shenmao, Wahlee,Topoint, Cabot Micro, Chemtura, Cookson Elec, Eternal Chemical , Hexcel, Chang Wah

20120213

NT$ & GBP converted to US$ at fluctuating exchange

4Q'11 estimate based upon partial data

Rigid & Flex Laminate SuppliersComposite of 11 Companies

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 402 03 04 05 06 07 08 09 10 11

CY

0

100

200

300

400$ Millions

Revenue 153 160 162 156 160 165 185 235 246 276 268 257 259 267 284 318 314 333 375 365 316 320 368 326 303 305 323 222 192 222 258 246 286 335 333 302 370 356 371 315

+4%

Arisawa, Elite Materials, Hwa Woei, Iteq, Microcosm,Park Electrochemical, Rogers, Shinemore, Taiflex, Top Union, Uniplus

NT$ converted at fluctuating exchange

20120208

4Q'11 estimate based upon partial data

Process Equipment Related SuppliersComposite of 8 Companies

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 402 03 04 05 06 07 08 09 10 11

CY

0

200

400

600

800

1000$ Millions

Revenue 401 409 440 410 416 406 436 468 552 607 648 588 580 564 619 588 658 673 708 650 656 682 767 713 743 743 710 600 492 514 549 589 721 795 838 811 877 940 937 798

-2%

C-Sun,Tailing Technology, Camtek, ESI, GSI Group, Orbotech,Nordson, Coherent

20120226

PCBFlat Panel DisplaysTouch ScreensPhotovoltaic

4Q'11 estimate based upon partial data

World PCB Model

20050118

2011 World Rigid & Flex PCB Production by Geographical Area

Henderson Ventures 10/11

N America

Europe

Japan

China/HK

Taiwan

S Korea

Rest of Asia

ROW

6.5%5.3%

14.1%

42.3%

13.1%11.7%

6.5%0.6%

Total: $55.7 Billion

20111006

(US$ M @ Average 2010 Exchange)

Regional PCB Shipment Growth

1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 101 4 7 101 4 7 101 4 7 101 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 100 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

0.40.50.60.70.80.9

11.11.21.31.41.51.61.71.81.9

3/12 rate of growth in local currency

Taiwan/ChinaEuropeJapanN America0 Growth

20120227

Sources: IPC, JPCA, Taiwan/China composite; modified SIA chip shipments to approximate Europe

World PCB Monthly ShipmentsConverted @ Constant 2010 Exchange Rates

1357911135791113579111357911135791113579111357911135791113579111357911135791113579111357911199 00 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

0

1

2

3

4Thousands

N America Europe Japan ROA

Source: Custer Consulting Group

20120227

World PCB Shipments (with forecast)Converted @ Constant 2010 Exchange Rates

1 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 911199 00 01 02 03 04 05 06 07 08 09 10 11 12 13

CALENDAR YEAR

20

30

40

50

60$ Billion

Source: Custer Consulting Group - 2010 base year expanded by monthly growth of N. American, European, Japanese & Taiwan/China monthly PCB shipments

20120227

51.742.937.631.729.4

Growth calculations:Europe = composite European SIA & local PCB assoc dataJapan & N. America from JPCA & IPC dataTaiwan/China:46 rigid & flex company compositeRest of Asia growth = Taiwan/China 44 company composite

38.6 31.231.6 54.3 53.2 45.9 54.5

-14%+19%

53.9

-1%

+2%

54.8

World Global PMI, Electronic Equipment, PCB & Semiconductor Shipments

3 6 9123 6 9123 6 9123 6 9123 6 9123 6 9123 6 9123 6 9123 6 9123 6 9123 6 9123 6 912300 01 02 03 04 05 06 07 08 09 10 11 12

CALENDAR YEAR

0.5

0.7

0.9

1.1

1.3

1.5

3/12 rate of change

PCB "0" Growth SIAEl Equip Global PMI

Source: Custer Consulting Group

20120301

Final CommentsGrowth slowed in late 2011

USA & SE Asia are now in early recovery. Europe and Japan have unique challenges and are lagging.

Timely global data sources are available.

Early 2012 will be difficult, but good opportunties will still exist.

Focus on the high growth markets and customers.

Watch the leading indicators.

2012 is the year to take market share from your competitors!

2005011820110622