Embed Size (px)

Citation preview

T H E W O R L D B A N K

Global DevelopmentFinanceFinancing the Poorest Countries

2002A N A L Y S I S A N D S U M M A R Y T A B L E S

© 2002 The International Bankfor Reconstruction and Development / The World Bank1818 H Street, NWWashington, DC 20433

All rights reserved.

1 2 3 4 04 03 02

The findings, interpretations, and conclusions expressed here do not necessarily reflect the views of the Board ofExecutive Directors of the World Bank or the governments they represent.

The World Bank cannot guarantee the accuracy of the data included in this work. The boundaries, colors, denominations, and other information shown on any map in this work do not imply onthe part of the World Bank any judgment of the legal status of any territory or the endorsement or acceptance ofsuch boundaries.

Rights and Permissions

The material in this work is copyrighted. No part of this work may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopying, recording, or inclusion in any informationstorage and retrieval system, without the prior written permission of the World Bank. The World Bank encouragesdissemination of its work and will normally grant permission promptly.

For permission to photocopy or reprint, please send a request with complete information to the CopyrightClearance Center, Inc., 222 Rosewood Drive, Danvers, MA 01923, USA, telephone 978-750-8400, fax 978-750-4470, www.copyright.com.

All other queries on rights and licenses, including subsidiary rights, should be addressed to the Office of thePublisher, World Bank, 1818 H Street NW, Washington, DC 20433, USA, fax 202-522-2422, [email protected].

Cover design by W. Drew Fasick, Serif Design GroupCover photo: Curt Carnemark, World Bank Photo Library

ISBN 0-8213-5085-4ISSN 1020-5454

The Report Team vii

Preface viii

Acronyms and Abbreviations ix

Overview 1

Chapter 1 Challenges for Developing Countries during the Coming Global Recovery 5Recession and recovery in the industrial world 7Bust and boom in world trade 13Regional developments 19Risks to the forecast 26Notes 28References 29

Chapter 2 Private Capital Flows to Emerging Markets 31The global slowdown reduced capital market flows to developing countries 31Net resource flows 32Capital market flows 32Trends in FDI 37Emerging market financial crises in 2001 43The prospects for capital market flows and FDI 47Annex 2.1: Forecasts of private flows to developing countries 49Annex 2.2: Measuring resource flows to developing countries 51Notes 51References 52

Chapter 3 The Poor Countries’ International Financial Transactions 55Poor countries have benefited from the growth of global capital flows 55Financial integration in the poor countries 55FDI to the poor countries 59Improved investment climate is associated with rapid growth of FDI 61Effective competition policies are critical 63The participation of foreign banks in poor countries’ financial systems 64Capital outflows 69Annex 3.1: Econometric analysis of foreign bank participation 78Notes 81References 83

iii

.

Table of Contents

iv

Chapter 4 Strengthening Official Financial Support for Developing Countries 89Mixed results from aid have led to a fall in aid 89The policy framework 89Trends in aid 90The macroeconomic impact of aid 96Conditionality and adjustment lending 101Aid and debt relief 104Strengthening the effectiveness of official guarantees 107Annex 4.1 110Notes 111References 113

Appendix 1 Debt Burden Indicators and Country Classifications 119Appendix 2 Commercial Debt Restructuring 133Appendix 3 Official Debt Restructuring 151Appendix 4 Regional Economic Developments and Prospects 165

East Asia and Pacific 166Europe and Central Asia 170Latin America and the Caribbean 174Middle East and North Africa 178South Asia 183Sub-Saharan Africa 186

Appendix 5 Global Commodity Price Prospects 191

Summary tables

Tables1.1 Global conditions affecting growth in developing countries and world GDP growth 71.2 Initiating factors: turning points to downturn and recovery in OECD recessions 101.3 Developing-country forecast summary, 1991–2004 20

2.1 Net long-term resource flows to developing countries, 1991–2001 322.2 Capital market commitments to developing countries, 1991–2001 332.3 Debt ratios during recessions, East Asia and Latin America 332.4 International equity placement and performance of stock markets 342.5 Capital market commitments and spreads for developing countries 382.6 Projected capital market flows to developing countries 472A.1 How representative is the forecasting model? 492A.2 Comparison of forecasts with actual capital market flows to developing countries 502A.3 Statistics for the forecast of FDI 51

3.1 Net external financial flows to developing countries, 1999 563.2 Net long-term capital flows to poor countries, 1986–99 563.3 Annual change in policy performance and FDI as ratio to GDP, 1991–99 613.4 FDI as ratio to GDP and policy performance index in poor countries 613.5 Mining sector performance in three countries, before and after reforms 653.6 Cumulated outflows during 1980–99 703.7 Volatility of capital flows, 1990–99 703.8 Cumulated outflows as a share of GDP, 1999 71

G L O B A L D E V E L O P M E N T F I N A N C E

v

T A B L E O F C O N T E N T S

3A.1 Foreign bank presence and domestic bank performance 783A.2 Panel-VAR results for all developing countries 803A.3 Summary of impulse response functions, all developing countries 803A.4 Results of panel-VAR regression for poor countries 803A.5 Summary of impulse response functions, poor countries 80

4.1 Net official aid to developing countries, by type and source, 1990–2001 934.2 Trends in aid allocation 954.3 Forgiveness of ODA claims, 1970–2000 1054.4 Impact of HIPC Initiative in 24 decision-point cases 1064.5 Export credit commitments to HIPCs, 1990–2000 110

Figures1.1 World and industrial and developing country GDP growth, 1997–2004 61.2 Manufacturing production in the G-3 countries 2000–02 81.3 U.S. manufacturing output, high-tech and non-high-tech industries 91.4 Consumer confidence in the United States, the Euro Area, and Japan 91.5 OECD GDP growth and fiscal balance, 1970–2000 121.6 GDP growth in the industrial countries, 2001–04 121.7 World export growth, 1999–2001 131.8 World industrial production and import volumes 141.9 Shipping cost index (Baltic Dry) 151.10 Real non-oil commodity prices since 1980 181.11 Per capita agricultural production 181.12 Oil prices and OECD oil stocks 191.13 GDP growth in developing regions 211.14 Forecasting the 2001 U.S. slowdown 271.15 Two recessions in the United States, 1990–91 and 2001 27

2.1 Performance of developing-country stock markets by sector 342.2 Bank lending standards and bank credit to developing countries, 1990–2001 352.3 Corporate default rate and risk premiums, 1990–2001 372.4 FDI and M&A in developing countries, 1991–2001 382.5 FDI as ratio to GDP, 1991–2001 402.6 Regional trends of FDI flows, 1991–2001 422.7 North-South and South-South FDI, 1991–1999 42

3.1 Five-year rolling correlation between savings and investment, 1974–1999 573.2 FDI-to-GDP ratios, 1991–2000 593.3 Foreign direct investment in mining exploration and government policies 643.4a Foreign bank presence in poor countries 653.4b Foreign bank presence in Africa 653.5 Effect of greater foreign bank presence on intermediation costs and domestic bank

profitability 663.6 Effect of greater foreign bank presence on international bank lending to poor countries 673.7 Effect of greater foreign bank presence on nonperforming loans 683.8 Capital outflows from developing countries, 1985–99 703.9 Cumulated outflows and minerals exports 733.10 Capital account restrictions 74

vi

G L O B A L D E V E L O P M E N T F I N A N C E

4.1 ODA from donor countries in relation to their GNP, 1990–2000 944.2 Compliance with conditionality and economic performance 1014.3 NPV of external debt of the 24 countries that reached their HIPC decision point 105

Boxes1.1 The Doha Development Agenda 17

2.1 Evidence of changes in the appetite for risk and capital market flows 362.2 The concentration of FDI flows 392.3 Round-tripping of capital flows between China and Hong Kong 412.4 Financial market contagion from the Argentine crisis 442.5 Moral hazard and rescue packages 46

3.1 Improving market access through future-flow securitization 583.2 The investment climate and domestic investment 603.3 Capital outflows from the middle-income countries 723.4 Narrowly focused capital controls in emerging markets 75

4.1 The PRSPs 914.2 The Financing for Development (FfD) process 924.3 The relationship between private and multilateral flows in poor countries 984.4 Official guarantees and the Mozal project 109

vii

THIS REPORT WAS PREPARED BY THE ECO-

nomic Policy and Prospects Group, anddrew on resources throughout the Devel-

opment Economics Vice-Presidency, the EconomicPolicy Sector Board, the World Bank operationalregions, the International Finance Corporation,and the Multilateral Investment Guarantee Asso-ciation. The principal author was William Shaw,with direction by Uri Dadush. Chapter 1 was ledby Hans Timmer, with contributions by JohnBaffes, Betty Dow, Caroline Farah, FernandoMartel Garcia, Bernard Hoekman, Robert Key-fitz, Annette I. De Kleine, Robert Lynn, DonaldMitchell, Mick Riordan, Virendra Singh, ShaneStreifel, Dominique van der Mensbrugghe, andBert Wolfe. Chapters 2–4 were largely prepared bythe international finance team of the EconomicPolicy and Prospects Group, including GholamAzarbayejani, Shweta Bagai, Maria Pia Iannarello,Himmat Kalsi, Eung Ju Kim, Aparna Mathur,Sanket Mohapatra, Shoko Negishi, Bilin Neyapti,Malvina Pollock, Dilip Ratha, and Jeff Ziarko.Additional contributions and background paperswere provided by Dilek Aykut, Punam Chuhan,and Barry Eichengreen (chapter 2); Sara Calvo,Stijn Claessens, Susan Collins, Sebastian Edwards,Simon Evenett, Nagesh Kumar, Jeffrey Lewis,Deepak Mishra, Koh Naito, Claudine Ndayiken-gurutse, Andrew Powell, Jaya Prakash Pradhan,Felix Remy, Tony Thompson, Esen Ulgenerk,Aristomene Varoudakis, and Peter van der Veen(chapter 3); and Paul Collier, David Dollar, RobertKeyfitz, and Dan Morrow (chapter 4). Appendix1 was prepared by Ibrahim Levent, appendix 2 byEung Ju Kim, and appendix 3 by Malvina Pollock.Appendix 4 was prepared by Caroline Farah,Robert Keyfitz, Annette I. De Kleine, Robert Lynn,

Mick Riordan, and Virendra Singh, and benefitedfrom the guidance of the Bank’s regional chiefeconomists. Appendix 5 was prepared by JohnBaffes, Betty Dow, Don Mitchell, and ShaneStreifel. The financial flow and debt estimateswere developed in a collaborative effort by PunamChuhan, Nevin Fahmy, Shelley Fu, Ibrahim Lev-ent, and Gloria Moreno of the Financial DataTeam along with Himmat Kalsi, Eung Ju Kim, andMalvina Pollock of the Economic Policy and Pros-pects Group. The report was prepared under thegeneral direction of Nicholas Stern.

Many others from inside and outside the Bankprovided input, comments, guidance, and supportat various stages of the report’s publication. Ger-ard Caprio, Paula Donovan, Guy Pfeffermann,and Sanjivi Rajasingham were discussants at theBankwide review. Sebastian Edwards, ShahrokhFardoust, Jan Willem Gunning, Jim Hanson, andStephen O’Connell provided extensive reviews ofindividual chapters. Comments were provided byJehan Arulpragasam, Amarendra Bhattacharya,Jaime Biderman, Gerard Caprio, Haydee Celaya,James Emery, Alan Gelb, Ian Goldin, CharleenGust, Daniel Kaufman, Jeni Klugman, Stefan Koe-berle, Jacob Kolster, Richard Newfarmer, JohnPage, Enrique Rueda-Sabater, Sudhir Shetty, PhilipSuttle, Axel van Trotsenburg, and Ulrich Zachau.Comments were also received from the Interna-tional Monetary Fund. Mark Feige edited the re-port to highlight the main messages. AwatifAbuzeid and Katherine Rollins provided assis-tance to the team. Robert King managed dissemi-nation and production activities by the EconomicPolicy and Prospects Group. Book design, editing,production, and dissemination were coordinatedby the World Bank Publications team.

.

The Report Team

viii

GLOBAL DEVELOPMENT FINANCE WAS

formerly published as World Debt Tables.The new name reflects the report’s ex-

panded scope and greater coverage of private fi-nancial flows.

Global Development Finance consists of twovolumes: Analysis and Summary Tables and Coun-try Tables. Analysis and Summary Tables containsanalysis and commentary on recent developmentsin international finance for developing countries.Summary statistical tables are included for selectedregional and analytical groups comprising 148countries.

Country Tables contains statistical tables onthe external debt of the 136 countries that reportpublic and publicly guaranteed debt under theDebtor Reporting System. Also included are tablesof selected debt and resource flow statistics for in-dividual reporting countries, as well as summarytables for regional and income groups.

For the convenience of readers, charts on pagesx to xii summarize graphically the relation between

debt stock and its components; the computation offlows, aggregate net resource flows, and aggregatenet transfers; and the relation between net resourceflows and the balance of payments. Exact defini-tions of these and other terms used in Global De-velopment Finance are found in the Sources andDefinitions section.

The economic aggregates presented in the ta-bles are prepared for the convenience of users;their inclusion is not an endorsement of their valuefor economic analysis. Although debt indicatorscan give useful information about developments indebt-servicing capacity, conclusions drawn fromthem will not be valid unless accompanied by care-ful economic evaluation. The macroeconomic in-formation provided is from standard sources, butmany of them are subject to considerable marginsof error, and the usual care must be taken in inter-preting the indicators. This is particularly true forthe most recent year or two, when figures are pre-liminary or subject to revision.

Preface

.

ix

CIS Commonwealth of Independent StatesCPPR Country Portfolio Performance ReviewDAC Development Assistance Committee

(of the OECD)DCB debt conversion bondDDSR debt and debt service reductionDRS Debtor Reporting System (of the World Bank)EI eligible interest bondEMBI Emerging Market Bond IndexEPZ export processing zoneEU European UnionFDI foreign direct investmentFfD Financing for DevelopmentFLIRB front-loaded interest reduction bondFRN floating-rate noteG-7 Group of Seven (Canada, France,

Germany, Italy, Japan, United Kingdom,United States)

GATS General Agreement on Trade in ServicesGDP gross domestic productGNI gross national incomeHIPC heavily indebted poor countriesHIV human immunodeficiency virusIBRD International Bank for Reconstruction and

Development (of the World Bank Group)ICT information and communications technologyIDA International Development Association

(of the World Bank Group)IFC International Finance CorporationIMF International Monetary FundLIBOR London interbank offered rateLILIC less indebted low-income countryLIMIC less indebted middle-income countryM&A mergers and acquisitions

Mercosur Southern Cone Common Market (Argentina,Brazil, Paraguay, Uruguay; Bolivia andChile are associate members)

MILIC moderately indebted low-income countryMIMIC moderately indebted middle-income countryMUV manufacturing unit valueMYRA multiyear rescheduling agreementNAFTA North American Free Trade AgreementNBC National Bank of Commerce (Tanzania)NGO nongovernmental organizationNIE newly industrialized economyNPV net present valueOA official aidODA official development assistanceOECD Organisation for Economic Co-operation

and DevelopmentOPEC Organization of Petroleum Exporting

CountriesPRSC Poverty Reduction Support CreditPRSP Poverty Reduction Strategy PaperREER real effective exchange rateSDR special drawing right (of the International

Monetary Fund)SILIC severely indebted low-income countrySIMIC severely indebted middle-income countrySMEs small and medium enterprisesU.N. United NationsUNCTAD United Nations Conference on Trade

and DevelopmentURR unremunerated reserve requirementVAR vector autoregressionWTO World Trade OrganizationXGS exports of goods and services

.

Acronyms and Abbreviations

Dollars are current U.S. dollars, unless otherwise specified.

x

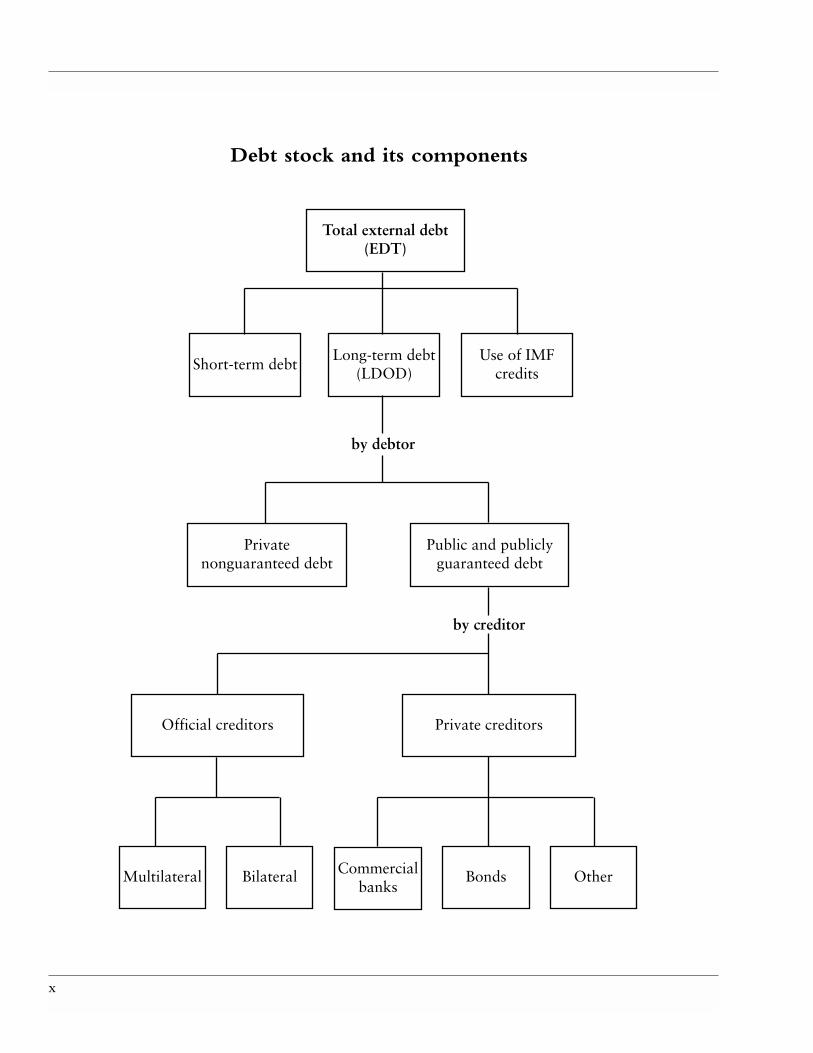

Debt stock and its components

Total external debt(EDT)

Short-term debtLong-term debt

(LDOD)

by debtor

Private nonguaranteed debt

Public and publiclyguaranteed debt

by creditor

Private creditors

Multilateral Bilateral Commercialbanks

Bonds Other

Use of IMF credits

Official creditors

xi

Principal repayments

Aggregate net resource flows and net transfers (long-term) todeveloping countries

Loan disbursements

Foreign direct in-vestment (FDI), portfolio equity

flows, and officialgrants

Net transfers ondebt

Interest payments

minus

equals

minus

equals

Debt service(LTDS)

Aggregate net resource flows

Aggregate nettransfers

Loan interest and FDI profits

minus

equals

Net resource flows on debt

plus equals

Note: Includes only loans with an original maturity of more than one year (long-term loans). Excludes IMF transactions.

xii

Credits Debits

• Exports of goods and services • Imports of goods and services

• Income received • Income paid

• Current transfers • Current transfersIncluding workers’ remittances andprivate grants

• Official unrequited transfers (by foreign • Official unrequited transfers (by national governments) government)

• Official unrequited transfers (by foreign • Official unrequited transfers (by national governments) government)

• Foreign direct investment (by nonresidents) • Foreign direct investment (by residents)(disinvestment shown as negative) (disinvestment shown as negative)

• Portfolio investment (by nonresidents) • Portfolio investment (abroad by (amortizations shown as negative) residents) (amortizations shown as

negative)

• Other long-term capital inflows (by • Other long-term capital outflow (by nonresidents) (amortizations shown residents) (amortizations shown as as negative) negative)

• Short-term capital inflow • Short-term capital outflow

Net changes in reserves

Aggregate net resource flows (long-term) and the balance of payments

Current account

Capital and financial account

Reserve account

Aggregate net resource flows

Net resource flows on debt (long-term)

Overview: International Finance and the Poorest Developing Countries

THE INTEGRATION OF DEVELOPING COUN-

tries into the global economy increasedsharply in the 1990s with improvements in

their economic policies; the massive expansion ofglobal trade and finance driven by technologicalinnovations in communications, transport, anddata management; and the lowering of barriers totrade and financial transactions. Many of the poor-est developing countries1 participated strongly inthis process despite their limited access to capitalmarkets. This report analyzes the interaction be-tween the global expansion of finance and im-provements in domestic policies in the poor coun-tries over the 1990s, and the implications forgrowth and poverty reduction. Three main mes-sages are developed: (a) a strong investment cli-mate is critical to attracting foreign capital andusing it productively; (b) poor countries’ increas-ing integration in the global economy means that they face similar policy challenges as middle-incomecountries, including how to deal with capital mo-bility; and (c) achieving the Millennium Develop-ment Goals will require a substantial rise in aidflows, an increased allocation of aid to countrieswith good policies, and improvements in policiesby both developing countries and donors.

A greater integration of poor countries and private capital—The surge in foreign direct investment (FDI) flowsand the decline in aid have transformed external fi-nance to the poor countries. FDI flows to the poorcountries rose from 0.4 percent of the gross domes-tic product (GDP) in the late 1980s to 2.8 percentin the late 1990s in response to the globalization ofproduction and improvements in domestic policies(see pages 59–61). Aid to these countries fell by 20

1

.

percent in real terms over the same period. Thepoor countries now receive about the same level ofFDI as middle-income countries, relative to the sizeof their economies. In addition, the global expan-sion of international banks coupled with the liber-alization of domestic financial systems in the poorcountries increased the average share of foreignbank assets to more than 40 percent of total assets,more than double the share of 1995 and compara-ble to that of many middle-income countries thathave recently benefited from increased foreignbank participation (see pages 64–66).

—good policies and governance, along withstrong institutions, are critical to using privateflows productivelyA rise in private flows can have a substantial im-pact on investment in the poor countries and, ifproductively used, on growth. However, the policyframework must be right. Improvements in the in-vestment climate (a term that refers to the numer-ous ways in which government affects the produc-tivity of investment, including policies, governance,and the strength of institutions) have boosted theimpact of international financial transactions onproductivity in the poor countries. Domestic firmsin countries with strong investment climates aremore able to absorb the foreign technology andskills that come with FDI (see pages 62–63). Betterpolicies have enabled some poor countries to at-tract more diversified FDI flows—the share ofcountries that export natural resources in the poorcountries’ FDI dropped from half in 1991 to 20percent toward the end of the decade. Countriesthat established the competitive conditions re-quired to attract foreign banks experienced an im-provement in the efficiency of their domestic banks

G L O B A L D E V E L O P M E N T F I N A N C E

and thus a decline in the cost of financial interme-diation (see pages 66–69).

Poor countries face similar challengesfrom globalization as middle-incomecountries

The events of the past year underlined the risksof capital mobility for the middle-income

emerging markets. The current global economicslowdown, exacerbated by the bursting of the high-tech bubble at the end of 2000 and the terrorist at-tacks in September 2001, is exceptionally deep andbroad (see pages 7–11). Capital market flows onceagain proved to be procyclical: the growth slow-down in industrial countries reduced both emerg-ing markets’ export revenues and their access to ex-ternal finance (see pages 32–36). By contrast, thelevel of FDI in 2001 was virtually unchanged fromthe previous year despite adverse global conditions,including a drop in global FDI flows (see pages37–40). The crisis in Argentina illustrates howopen capital accounts can compound the effects ofunsustainable macroeconomic policies and highpublic sector debt, thus seriously complicating sta-bilization efforts (see pages 43–47).

The poor countries are also vulnerable to capi-tal mobility. While most still impose restrictions oncapital account transactions, controls have hadonly limited success in controlling capital outflowsin the context of a weak investment climate, wheredomestic investment opportunities are limited andfears of confiscation or reduction in the value ofassets provide considerable incentive to put moneyabroad (see pages 69–78). Poor countries with bet-ter than average policies (as measured by theWorld Bank) had more success in retaining domes-tic capital: a rough estimate of the stock of theircapital outflows relative to GDP was about one-sixth the size in poor countries with worse than av-erage policies. Capital outflows have been morevolatile in the poor countries than in the middle-in-come countries, while volatility can be more costly(in terms of welfare) in poor countries becausemore people live close to subsistence and have littleprivate insurance or public safety nets. Thus poli-cymakers in poor countries need to recognize thepotential impact of capital mobility on both stabi-lization policies and long-term development.

Good policies and strong governanceare also key to improving aideffectiveness

Earlier empirical studies consistently found aweak relationship between aid and investment,

with even less of an impact of aid on growth. How-ever, more recent research shows that aid makes an effective contribution to growth and poverty re-duction in countries with good economic policies,sound institutions, and strong governance, but haslittle effect in countries with poor policies. A dou-bling of aid flows would help ensure that develop-ing countries achieve the Millennium DevelopmentGoals, provided that this aid is allocated to coun-tries with good policies and large numbers of poorpeople (pages 99–100).

Aid continued to decline in 2001, and the pros-pects for a substantial rise in the medium term arelimited (pages 90–94). Most countries with goodpolicies can continue to absorb additional aid re-sources without seriously impairing the effective-ness of that aid (see pages 96–99). Aid does not, ingeneral, increase the volatility of government re-sources, and appropriate policies can ensure thataid does not contribute to inflationary pressures orcause excessive exchange-rate appreciation. It istrue that even in many countries with good poli-cies, lack of administrative capacity lowers themarginal productivity of aid as aid levels rise.However, recent research indicates that aid levelsto most countries with strong economic programsare well below the threshold where aid becomesineffective.

Better aid policies by donors alsocontribute to poverty reduction

There is evidence that donors have made pro-gress in improving their own policies, through

increasing resources to debt relief for good per-formers, easing complex administrative require-ments that can strain limited government capacity,and reducing the share of tied aid (see pages101–104). Modifications of adjustment assistancehave helped to preserve the use of conditionality inchanneling aid resources to good performers andsupporting the credibility of government policies,while ensuring adequate government flexibilityand domestic stakeholder commitment to the pro-

2

3

O V E R V I E W : I N T E R N A T I O N A L F I N A N C E A N D T H E P O O R E S T D E V E L O P I N G C O U N T R I E S

gram. Here also, recipient government policies arekey: strong leadership and effective administrationby the government can help promote aid coordina-tion and make it easier for donors to adopt moreflexible policies.

Note1. The poor countries are defined to represent developing

countries with relatively low per capita income and almostno access to international capital markets. The group in-cludes all IDA-only countries plus a few blend countries thathave had few IBRD loans over the past few years. The coun-tries included are Afghanistan, Albania, Angola, Armenia,Bangladesh, Benin, Bhutan, Bolivia, Burkina Faso, Burundi,

Cambodia, Cameroon, Cape Verde, Central African Repub-lic, Chad, Comoros, the Democratic Republic of Congo, theRepublic of Congo, Côte d’Ivoire, Djibouti, Eritrea, Ethi-opia, The Gambia, Georgia, Ghana, Guinea, Guinea-Bissau,Guyana, Haiti, Honduras, Kenya, Kiribati, the Kyrgyz Re-public, the Lao People’s Democratic Republic, Lesotho,Liberia, Madagascar, Malawi, Maldives, Mali, Mauritania,Moldova, Mongolia, Mozambique, Myanmar, Nepal,Nicaragua, Niger, Nigeria, Pakistan, Rwanda, Samoa, SãoTomé and Principe, Senegal, Sierra Leone, Solomon Islands,Somalia, Sri Lanka, Sudan, Tajikistan, Tanzania, Togo,Tonga, Uganda, Vanuatu, Vietnam, Republic of Yemen,Zambia, and Zimbabwe. These countries’ average per capitaincome is under $500 per year compared with $2,900 forother developing countries. And most of them are small; onlyPakistan, Bangladesh, Nigeria, Vietnam, Ethiopia, and theDemocratic Republic of Congo have more than 50 millionpeople.

1Challenges for Developing Countries during the Coming Global Recovery

THE CURRENT GLOBAL ECONOMIC SLOW-

down is exceptionally deep and broad.Global growth in 2001, at 1.2 percent, was

2.7 percentage points lower than in 2000 (figure1.1). In the last 40 years the deceleration in grossdomestic product (GDP) was sharper only in1974, during the first oil crisis. The current slow-down is also broad in that the deceleration isequally rapid for industrial countries and develop-ing countries. The slowdown in economic activitycoincides with an unprecedented 14 percentagepoint deceleration of world trade, from recordgrowth of 13 percent in 2000 to a 1 percent de-cline in 2001 (table 1.1). However, contrary tomany earlier downturns, inflationary pressures re-mained very subdued and this allowed monetaryauthorities to loosen their policies substantially.

The bursting of the high-tech bubble at the endof 2000 and the terrorist attacks in September2001 made the deceleration of the global economyso exceptionally sharp. The unpredictable charac-ter of these events made it difficult to anticipate thedepth of the downturn. Nevertheless, after the ter-rorist attacks the expectations—a deeper recessionand a delay of the recovery by one or two quar-ters—appear to be materializing.1 Several of thestrong market reactions to the terrorist attackshave been reversed and signs of a recovery in theUnited States and the high-tech sectors have startedto mount.

Even during this unusually synchronized down-turn, the intensity and character of the economicmalaise differ across countries, sectors, and incomegroups. Especially hard hit are countries dependenton commodity exports, with many commodityprices at historical lows; highly indebted emergingeconomies, because private investors have reduced

5

.

their exposure in emerging markets in reaction toincreased uncertainty, reduced value of portfolios inindustrial countries, and increased default provi-sions; high-tech sectors, with many firms decimatedafter the high-tech bubble burst; and tourism indus-tries, suffering from the aftermath of the terroristattacks. As in every severe downturn, poor peoplepay a high price. Without buffers or safety nets torely upon, their ability to satisfy basic needs is im-mediately at stake when incomes decline.

The current sharp deceleration in economicactivity largely follows a typical investment andinventory cycle, even if it was triggered by otherfactors, such as the bursting of the high-tech bub-ble or the terrorist attacks. Likewise, the standardinvestment cycle is expected to play a major role in recovery. The steep decline in investment andstock building in recent quarters carries seeds for aforceful cyclical recovery. As capital stocks and in-ventories are adjusted downward to reflect lowergrowth expectations, the decline in investment andstock-building tends to become less steep and ac-tivity starts to rebound. The rebound will be fur-ther fueled by aggressive monetary and fiscal stim-ulus, especially in the United States. The currentsynchronism of the cycles in different parts of theworld will likely be reflected in a strong global re-covery, even if recovery in individual countries isnot exceptionally vigorous.

The economic consequences of the terroristattacks probably delayed this rebound by abouttwo quarters, implying strong growth in the sec-ond half of 2002. Weak growth in the second half of 2001 and the first half of 2002 is expectedto keep global growth in 2002 at 1.3 percent,slightly above growth rates for 2001. This outlookimplies a downward adjustment since the publica-

G L O B A L D E V E L O P M E N T F I N A N C E

tion of Global Economic Prospects 2002 (WorldBank 2001), mainly reflecting more pessimisticviews on Japan and Latin America. World tradecould very well decline in 2002 for a second yearin a row. However, an anticipated acceleration inthe second half of 2002 will likely result in a strongrecovery in annual growth for 2003. Althoughglobal GDP growth in 2003 of 3.6 percent wouldfall short of the strong 3.9 percent performance of 2000, advances in world trade are expected tobreach 8 percent.

Not all economies will benefit immediately fromthe robust global rebound. Argentina’s financialstrains have resulted in defaults and devaluation,heralding a protracted period of painful adjustment;but there is also hope that a new base can be cre-ated for resumption of long-term growth. As finan-cial weakness in Japan has worsened during theglobal downturn, a recovery of the external environ-ment can probably not avert, but only alleviate,structural adjustments. Commodity exporters, in-cluding oil producers, have experienced large terms-of-trade losses that will limit their short-term ability to rebound. The speed of recovery toward normaltrends in tourism is uncertain, leaving the prospectscloudy for many of the developing countries that areheavily dependent on this revenue source.

On average, however, developing countries’growth is expected to be robust in 2003 and 2004,reaching 5 percent per year. A strong recovery seems

achievable in the absence of additional adverseshocks to the global economy. Such a recoverywould be supported by modest inflation—medianinflation in the developing world is around 5.5percent, only half the average rate during the1990s—relatively low interest rates after the re-cent easing of U.S. monetary policy, rapidly grow-ing import demand in the industrial countries, anda slight rebound in real commodity prices. Ex-porters of high-tech products are likely to benefitmore than average from this recovery. The mainrisks to this favorable outlook are to be found infinancial markets. The fragile Japanese bankingsector may trigger more adverse developments thanis currently assumed, and the full complement oframifications stemming from financial crises in Ar-gentina and Turkey remains uncertain.

Many developing countries, even those thatcurrently do not have large financial imbalances,face difficult challenges. The global downturn andcountry-based policy responses to slowing growthhave reversed the trend of declining fiscal deficitsin many countries, and deterioration of deficitstend to persist well after economic growth has re-turned to normal levels. Some oil exporters—suchas Nigeria, the República Bolivariana de Vene-zuela, and Indonesia—are particularly vulnerable,as oil prices are expected to continue their down-ward trend. Furthermore, the global downturn im-plies a deterioration of the current account for

6

Percentage change

Figure 1.1 World and industrial and developing country GDP growth, 1997–2004

Source: World Bank Economic Policy and Prospects Group calculations.

0

1

2

3

4

5

6

1997 1998 1999

Forecast

Developingcountries

World

Industrialcountries

2000 2001 2002 2003 2004

C H A L L E N G E S F O R D E V E L O P I N G C O U N T R I E S D U R I N G T H E C O M I N G G L O B A L R E C O V E R Y

many developing countries. Together with limitedavailability of international private capital, thiscould generate new financial strains, which couldimpede further recovery.

Recession and recovery in theindustrial world

The United States, Japan, Germany, and severalsmaller industrial countries in Europe entered

into—or came close to—recession in the course of2001. Aggregate annual growth in the industrialworld decelerated from 3.4 percent in 2000 to 0.9percent in 2001. With almost all recessions havingstarted in the second half of 2001, it is unlikely thataggregate annual growth in 2002 will exceed 2001growth, even with a solid rebound in the secondhalf of the year. Indeed, measured growth is likelyto decline further, to only 0.8 percent. The advancein output in 2003, in contrast, is expected to returnto 3.1 percent, assuming that no major crisis evolves

7

Table 1.1 Global conditions affecting growth in developing countries and world GDP growth(percentage change from previous year, except interest rates and oil prices)

CurrentEstimate Current Forecasts GEP 2002 forecasts

2000 2001 2002 2003 2004 2001 2002 2003

Global conditionsWorld trade (volume) 13.1 –0.8 1.8 8.3 7.3 1.0 4.0 10.2

Inflation (consumer prices) G-7 OECD countriesab 1.9 1.7 0.9 1.6 1.8 1.8 1.4 1.5United States 3.4 2.8 1.5 2.4 2.6 2.8 2.2 2.3

Commodity prices (nominal dollars) Commodity prices, except oil (dollars) –1.3 –9.1 1.3 7.3 6.4 –8.9 1.6 8.1Oil price (dollars, weighted average),dollars a barrel 28.2 24.4 20.0 21.0 19.0 25.0 21.0 20.0

Oil price, percent change 56.2 –13.7 –17.9 5.0 –9.5 –11.3 –16.0 –4.8Manufactures export unit value (dollars)c –2.0 –1.4 –0.5 3.6 3.7 –4.6 4.0 4.4

Interest rates LIBOR, 6 months (dollars, percent)c 6.7 3.3 2.3 4.0 4.6 3.6 2.8 3.0EURIBOR, 6 months (euro, percent)d 4.5 4.0 3.0 4.0 4.2 4.1 3.3 3.3

World GDP (growth) 3.9 1.2 1.3 3.6 3.1 1.3 1.6 3.9High-income countries 3.5 0.8 0.8 3.2 2.6 0.9 1.1 3.5

OECD countries 3.4 0.9 0.8 3.1 2.5 0.9 1.0 3.4United States 4.1 1.1 1.3 3.7 3.1 1.1 1.0 3.9Japan 2.2 –0.8 –1.5 1.7 1.1 –0.8 0.1 2.4Euro Area 3.5 1.4 1.2 3.3 2.7 1.5 1.3 3.6

Non-OECD countries 6.6 –1.0 1.7 4.4 4.0 0.6 3.2 5.7Developing countries 5.4 2.8 3.2 5.0 4.9 2.9 3.7 5.2

East Asia and Pacific 7.4 4.6 5.2 6.9 6.5 4.6 4.9 6.8Europe and Central Asia 6.4 2.2 3.2 4.3 4.0 2.1 3.0 4.2Latin America and the Caribbean 3.8 0.6 0.5 3.8 3.8 0.9 2.5 4.5Middle East and North Africa 4.2 3.1 2.7 3.3 3.3 3.4 2.9 3.6South Asia 4.0 4.3 4.9 5.3 5.2 4.5 5.3 5.5Sub-Saharan Africa 3.1 2.6 2.6 3.6 3.6 2.7 2.7 3.9

Memorandum items East Asian crisis–affected countriese 7.1 2.3 3.5 5.9 5.5 2.3 3.4 5.4Transition countries of ECA 6.2 4.4 3.4 4.0 4.0 4.0 3.1 3.8Developing countries, Excluding the transition countries 5.3 2.6 3.2 5.2 5.0 3.1 3.8 5.5Excluding China and India 5.1 1.8 2.2 4.4 4.2 1.9 2.9 4.5

a. The G-7 countries are Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States.b. Unit value index of manufactures exports for G-5 countries (G-7 minus Canada and Italy) to developing countries, expressed in dollars.c. London interbank offered for dollars.d. Interbank offered rate for euros.e. Indonesia, the Republic of Korea, Malaysia, the Philippines, and Thailand.Source: World Bank Economic Policy and Prospects Group, February 2002 forecast; Global Economic Prospects (GEP) 2002 projections ofOctober 2001.

G L O B A L D E V E L O P M E N T F I N A N C E

from the fragilities in the Japanese banking systemor other sources of tension in the forecast. Growthin 2004 is assumed to fall back to near its long-termtrend of 2.5 percent.

In the fall of 2000 the downturn still hadcharacteristics of a soft landing, with cyclical cor-rections that did not suggest one of the most se-vere decelerations in economic activity in decades.However, in two steps—the first initiated by theburst of the high-tech bubble at the end of 2000,and the second by terrorist attacks in September2001—the global economy decelerated further.

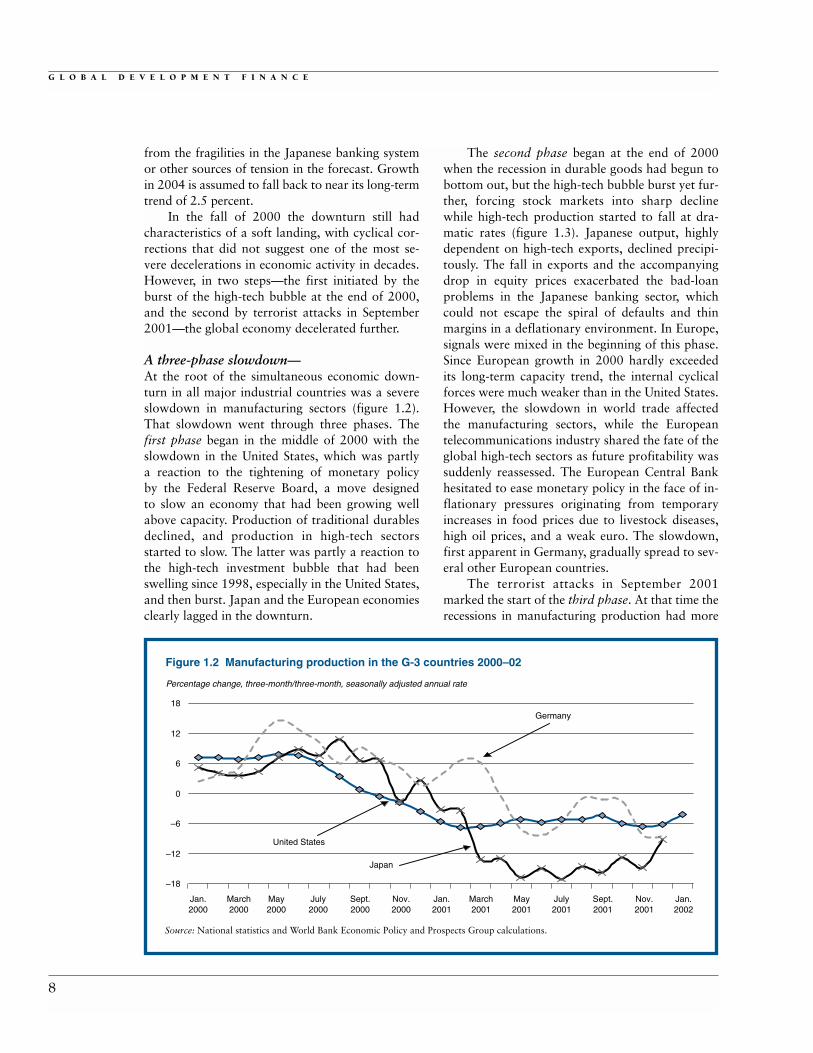

A three-phase slowdown—At the root of the simultaneous economic down-turn in all major industrial countries was a severeslowdown in manufacturing sectors (figure 1.2).That slowdown went through three phases. Thefirst phase began in the middle of 2000 with theslowdown in the United States, which was partly a reaction to the tightening of monetary policy by the Federal Reserve Board, a move designed to slow an economy that had been growing wellabove capacity. Production of traditional durablesdeclined, and production in high-tech sectorsstarted to slow. The latter was partly a reaction tothe high-tech investment bubble that had beenswelling since 1998, especially in the United States,and then burst. Japan and the European economiesclearly lagged in the downturn.

The second phase began at the end of 2000when the recession in durable goods had begun tobottom out, but the high-tech bubble burst yet fur-ther, forcing stock markets into sharp declinewhile high-tech production started to fall at dra-matic rates (figure 1.3). Japanese output, highlydependent on high-tech exports, declined precipi-tously. The fall in exports and the accompanyingdrop in equity prices exacerbated the bad-loanproblems in the Japanese banking sector, whichcould not escape the spiral of defaults and thinmargins in a deflationary environment. In Europe,signals were mixed in the beginning of this phase.Since European growth in 2000 hardly exceededits long-term capacity trend, the internal cyclicalforces were much weaker than in the United States.However, the slowdown in world trade affectedthe manufacturing sectors, while the Europeantelecommunications industry shared the fate of theglobal high-tech sectors as future profitability wassuddenly reassessed. The European Central Bankhesitated to ease monetary policy in the face of in-flationary pressures originating from temporaryincreases in food prices due to livestock diseases,high oil prices, and a weak euro. The slowdown,first apparent in Germany, gradually spread to sev-eral other European countries.

The terrorist attacks in September 2001marked the start of the third phase. At that time therecessions in manufacturing production had more

8

Percentage change, three-month/three-month, seasonally adjusted annual rate

Figure 1.2 Manufacturing production in the G-3 countries 2000–02

Source: National statistics and World Bank Economic Policy and Prospects Group calculations.

–18

Jan.2000

March2000

May2000

July2000

Sept.2000

Germany

United States

Japan

Nov.2000

Jan.2001

March2001

May2001

July2001

Sept.2001

Nov.2001

Jan.2002

–12

–6

0

6

12

18

C H A L L E N G E S F O R D E V E L O P I N G C O U N T R I E S D U R I N G T H E C O M I N G G L O B A L R E C O V E R Y

or less bottomed out, albeit for Japan and theUnited States at still large declining rates. The pe-riod immediately after the terrorist attacks wascharacterized by an extraordinary, but temporary,loss of consumer confidence and deterioration ofbusiness sentiment (figure 1.4). Equity prices plum-meted 15 percent immediately after the attacks,spreads on junk bonds jumped 200 basis points

within weeks, and commodities prices fell 7 percentwithin one month. Industrial production dippedonce again, although it seemed that the high-techcycle was less affected (figure 1.3). While these firstmarket reactions were reversed within one quarter,economic recovery will probably be delayed byabout two quarters as a result of supply disruptionsand shaken confidence.

9

Percentage change, three-month moving average, seasonally adjusted annual rate

Figure 1.3 U.S. manufacturing output, high-tech and non-high-tech industries

Source: Federal Reserve, through Datastream.

10.0

7.5

5.0

2.5

0.0

–2.5

–5.0

–7.5

–10.0

Excluding high-tech(left axis)

High-tech(right axis)

–30

–15

0

15

30

45

60

75

Jan.2000

March2000

May2000

July2000

Sept.2000

Nov.2000

Jan.2001

March2001

May2001

July2001

Sept.2001

Nov.2001

Jan.2002

EC: diffusion Index; U.S. and Japan Indexes, January 2001=100

Figure 1.4 Consumer confidence in the United States, the Euro Area, and Japan

Source: U.S.: Conference Board; Japan: ERISA; Euro Area: European Commission.

65Jan. 2001 March 2001 May 2001 July 2001 Sept. 2001 Nov. 2001 Jan. 2002

Euro Area(right axis)

Japan (left axis)

United States(left axis)

75

85

95

105

115

–12

–10

–8

–6

–4

–2

0

2

Table 1.2 Initiating factors: turning points to downturn and recovery in OECD recessions(changes in contribution to growth, at seasonally adjusted annualized rates)

Downturn Contributions Recovery Contributions

Change in Change in Starting quarter GDP growth Principal sources Ending quarter GDP growth Principal sources

United StatesMid-1970s Q1, 1974 –6.4 S: –4.6 C: –1.6 Q2, 1975 6.0 S: 3.6 I: 1.9Early 1980s Q4, 1981 –9.5 S: –4.8 C: –3.2 Q4, 1982 3.8 I: 1.4 C: 1.3Early 1990s Q4, 1990 –2.8 C: –1.5 I: –1.0 Q1, 1991 2.8 C: 2.1 S: 0.9Current Q3, 2001 –1.3 I: –1.1 C: –0.7 — — — —

JapanMid-1970s Q3, 1973 –6.1 S: –3.3 I: –3.3 Q1, 1975 5.5 C: 2.4 I: 2.3Early 1990s Q2, 1993 –3.5 G: –1.7 S: –0.8 Q3, 1992 1.0 S: 0.9 G: 0.6Asia crisis–present Q2, 1997 –7.3 C: –7.1 I: –1.5 — — — —

EuropeMid-1970s Q4, 1974 –3.6 S: –3.8 C: –1.6 Q3, 1975 3.4 I: 1.4 S: 1.4Early 1980s Q2, 1980 –3.5 C: –2.1 I: –1.4 Q3, 1980 1.2 X: 0.8 I: 0.5Mid-1990s Q2, 1992 –2.4 I: –1.0 C: –0.9 Q2, 1993 2.0 C: 2.1 I: 0.7Current Q2, 2001 –1.7 X: –1.9 C: –0.6 — — — —

— Not available.Notes: GDP growth and contributions by expenditure component are expressed as the change in GDP growth and contributions to growth,measured (1) for “downturn”: average of one or two quarters prior to the turning point, and (2) for “recovery”: turning point to the averageof two quarters following. Principal sources: C=private consumption, G=government expenditures, I=gross fixed investment, S=change instocks, X=net exports of goods and services. Source: World Bank Economic Policy and Prospects Group calculations.

G L O B A L D E V E L O P M E N T F I N A N C E

The prolongation and deepening of the down-turn in the aftermath of the terrorist attacks madethis recession comparable in intensity to the reces-sions of the early 1980s and 1990s, at least for in-dustrial countries. Although the downturn in indi-vidual countries has not necessarily been as deep asduring those two severe recessions, its simultane-ous character made the current slowdown espe-cially sharp for the industrial world as a whole.Experience during the last decades suggests that the turning point to positive growth will probablybe triggered by the investment cycle, and that reces-sions of this magnitude tend to result in a dete-rioration of fiscal balances that typically lasts forthree or more years. The sharp fall in privatespending implies an improvement of the currentaccount in the short run, despite increased fiscaldeficits. The mirror image of the industrial coun-tries’ reduced current account deficit is the ten-dency of current account surpluses to narrow anddeficits to widen in the developing world. The re-mainder of this section will discuss triggers of turn-ing points in economic activity and the behavior ofgovernment balances in the industrial world. In-creased trade linkages have made developing coun-tries more dependent on these turning points in theindustrial countries’ business cycles, and as the cur-

rent account surpluses of developing countries startto decline, a deterioration of government balancescould increase tensions in global capital markets.

—largely driven by investment cyclesThe deep recessions and subsequent recoveries inthe United States during the last three decadeswere primarily the reflection of inventory and in-vestment cycles.2 Table 1.2 summarizes the mainsources of change in GDP growth at the beginningand end of recessions. In the majority of U.S. re-cessions since the 1970s, changes in investment orinventories were the main source of changes inGDP growth, both at the start and close of eachrecession. With the structural decline in invento-ries through the use of new technologies and just-in-time supply systems, the inventory cycle, stilldominant in the 1970s and 1980s, has become lessimportant. The investment cycle was the maincontributing factor in the current recession, andinvestment will likely be the force that brings GDPgrowth out of negative territory. As capital stocksadjust downward, the decline in investment rateswill soften, reversing the downward spiral.

Table 1.2 highlights the fact that net exportshave been a relatively more important factor de-termining the dynamics of recessions in Europe

10

C H A L L E N G E S F O R D E V E L O P I N G C O U N T R I E S D U R I N G T H E C O M I N G G L O B A L R E C O V E R Y

than in the United States. The inventory cycle hasnever been as important in Europe as in the UnitedStates. This could reflect the less pronounced do-mestic business cycles in Europe, which has moreautomatic stabilizers in place, as well as greaterregional diversity in monetary and fiscal policies.Note that the recent downturn in Europe was trig-gered mainly by swings in international trade,rather than by changes in domestic consumption,investment, or inventories. It is thus likely that theinternational trade cycle will also be an importantingredient of the recovery, in which case Europewill lag behind the United States in the rebound.

Japan is the odd one out in this picture. Re-cessions were avoided during the 1980s due tostrong, continuous growth in investment and pro-ductivity. However, investment growth has beendeclining since the early 1990s, when structuralgrowth rates fell, financial bubbles burst, andproblems in the banking sector began to mount.This trend was so strong that it overwhelmed thetendency for investment to experience sharp cycli-cal changes. As a result, investment failed to playthe standard role of initiating a turning point ineconomic activity. This is one reason why Japanstaggered from one recession into another duringthe 1990s, and why it is not easy to identify asource that could reverse the current downturn.

Policy is supportive, but will operate with some delay—Policies will play an important role in the recoveryof the industrial countries. Monetary policy hasnow turned highly expansionary in the UnitedStates, and with some delay, has eased in the EuroArea. In Japan the economy remains in a state ofdeflation (consumer prices have declined for thepast two years), and interest rates can hardly fallany further. Given the lack of headroom for alter-native action, the Bank of Japan initiated a pro-gram of liquidity injections—potentially weakeningthe yen as a way to combat deflation and stimulateexports.

The effects of monetary easing are likely to befelt with some lag, and should provide a neededfillip to demand for consumer durables and hous-ing across the Organisation for Economic Co-operation and Development (OECD) countries.But there is concern that the eventual impact oflower interest rates on business investment may belimited. In particular, investor risk aversion has

risen significantly, depressing investment in high-risk assets, especially in the United States. In Japan,financial markets are burdened by the accumulateddebt of failed businesses, which has reached ¥50trillion ($420 billion) since 1999, of which ¥16trillion accrued during 2001. This has exacerbatedthe “bad loan” problems of the commercial bank-ing system, adding new nonperforming assets al-most as quickly as “old” nonperforming loans arewritten off. Under these circumstances, additionalBank of Japan liquidity is unlikely to greatly in-crease the willingness of Japanese commercialbanks to lend, and signs of a credit crunch for thesmall-business sector may be emerging.

Fiscal policy also offers promise for boostinggrowth, especially in the United States. The U.S.Congress approved more than $40 billion in emer-gency and industry-support funds in the immedi-ate aftermath of September 11. Moreover, tax re-ductions enacted earlier in 2001 will continue tobe implemented over the next few years. In theEuro Area, automatic stabilizers will tend to in-crease public deficits, but the constraints inherentin the Stability and Growth Pact of the EuropeanUnion could limit government support for slowingeconomies.3 In Japan debate continues regardingthe degree and nature of supplemental budget pro-grams, against the background of Prime MinisterJunichiro Koizumi’s stated limits to bond-marketfunding of such efforts. On balance, fiscal stimulusis likely to be a significant additional driving forcefor recovery in the major industrial economies,particularly for the United States.

However useful and needed the fiscal stimulusmay be in the short term, increased deficits couldbecome a burden in the medium run. Historically,deficits that originated in severe downturns tend tolast well beyond the recovery in economic activity(figure 1.5). After the brief and steep recession fol-lowing the first oil crisis in the mid-1970s, the aver-age fiscal deficit (as a share of GDP) in the OECDturned from positive to negative, never again to re-turn to positive territory. After the second oil crisis,it took a decade for the deficits to come back closeto precrisis levels, and after the Gulf War this tookfive years. The stubbornness of deficits is partlydue to the vicious circle of higher debt and increas-ing debt service, and partly due to the temptationto see recessions as unique, temporary phenomenaand a subsequent recovery as a permanent im-provement. While the deterioration of government

11

G L O B A L D E V E L O P M E N T F I N A N C E

deficits is often abrupt, the restoration tends to besmoothed out over time. Of course, many regionaldifferences and different policy decisions deter-mined the trend in the average deficit. Neverthe-less, the historical pattern of persistent deficits isclear, and the main challenge in the current reces-sion is to keep the necessary stimulus confined tothe short run. In the medium run, improvement inthe industrial countries’ fiscal deficits will facilitatea resumption of capital flows toward developingcountries.

—auguring a strong recovery in 2003 Taking into account the likely impact of the inven-tory and investment cycles, and the policy re-sponses, we anticipate that the United States willcome out of the recession in the beginning of 2002and European countries will follow one or twoquarters later, but Japan will hardly reach positivegrowth during the year—resulting in annual 2002growth rates of 1.3, 1.2, and –1.5 percent respec-tively for these countries (figure 1.6). As industrialproduction, investment, and global trade pick uprapidly over the course of the year, 2003 is ex-pected to provide a much rosier picture, with GDPgrowth climbing to 3.7, 3.3, and 1.7 percent in thethree industrial centers. If banking problems inJapan remain unsolved, a relapse into low or nega-tive growth after a temporary export-led recoveryin that country cannot be excluded.

The U.S. current account deficit, which al-ready diminished to $420 billion in 2001 from$445 billion in 2000, as a result of recession andfalling oil prices, is expected to deteriorate onlymodestly over the next two years. The adjustmentin 2002 and coming years is expected to be accom-panied by a gradual weakening of the dollar and awidening of current account deficits in some Euro-

12

GDP percentage change; fiscal balance: percentage of GDP

Figure 1.5 OECD GDP growth and fiscal balance, 1970–2000

Source: OECD.

–6

1970 1973 1976

GDP growth

Fiscal balance

1979 1982 1985 1988 1991 1994 1997 2000

–4

–2

0

2

4

6

Figure 1.6 GDP growth in the industrialcountries, 2001–04

Source: World Bank Economic Policy and ProspectsGroup calculations.

United States Euro Area Japan–2

0

2

4

2001 2002 2003 2004

Percentage change

C H A L L E N G E S F O R D E V E L O P I N G C O U N T R I E S D U R I N G T H E C O M I N G G L O B A L R E C O V E R Y

pean countries. The Japanese current account sur-plus declined substantially in 2001 because thelatest recession in Japan was driven mainly by adecline in exports instead of a deceleration in in-vestment. Because Japanese investment is also notlikely to recover strongly in the near future, thecurrent account surplus is expected to widen againwhen world trade, and Japanese exports, rebound.The current account deficit for the industrial coun-tries as a whole is expected to decline from $280billion in 2000 to $240 billion by 2004, most ofthe improvement being realized in the near term.The mirror image of this development is a reducedcurrent account surplus in the developing coun-tries, partly reflecting declining oil prices and partlyreflecting reduced export opportunities.

Bust and boom in world trade

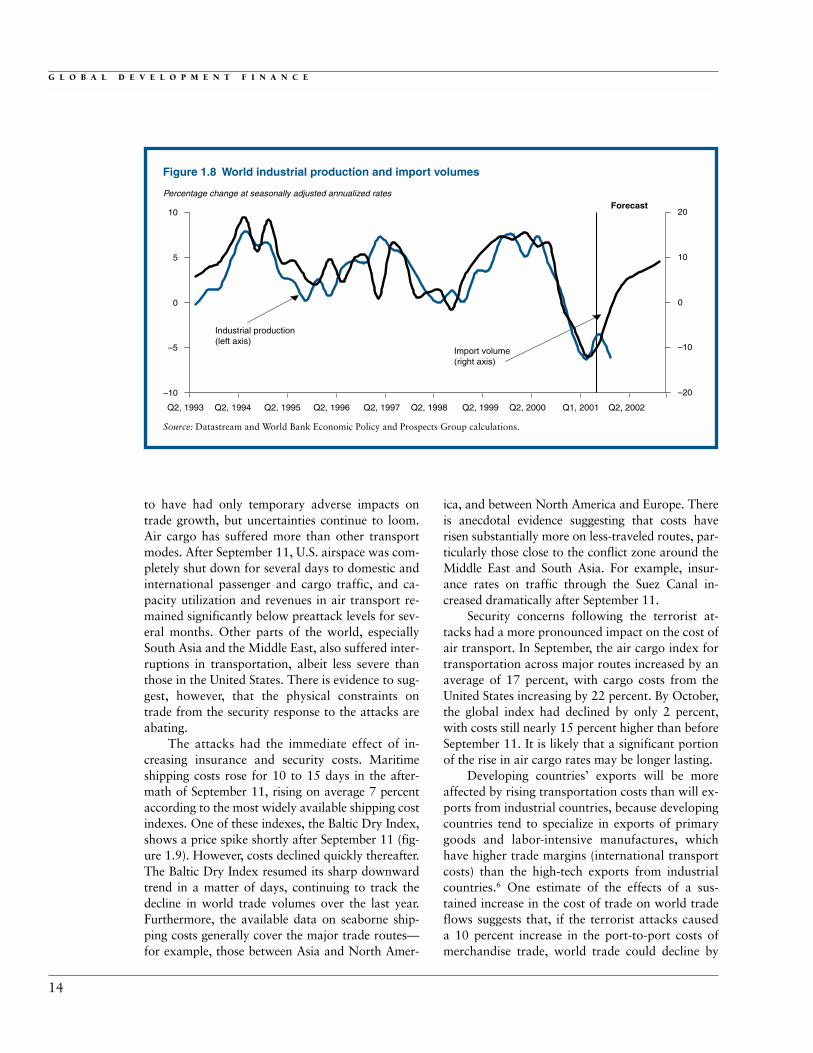

World trade, already undergoing the sharpestdeceleration on record, suffered additional

setbacks following the terrorist attacks of Septem-ber 11. These events delayed the expected recoveryin output, which will in turn delay the rebound inmerchandise trade for one or two quarters. More-over, security concerns disrupted trade flows, as didincreased shipping and insurance costs, althoughmedium-term effects arising from these develop-ments are more uncertain. The attacks also reduceddeveloping countries’ revenues from internationaltourism. However, longer-run prospects for globaltrade have improved after a first important step to-ward a new round of trade negotiations was madeat the World Trade Organization (WTO) minister-ial conference in Doha, Qatar, in November 2001.

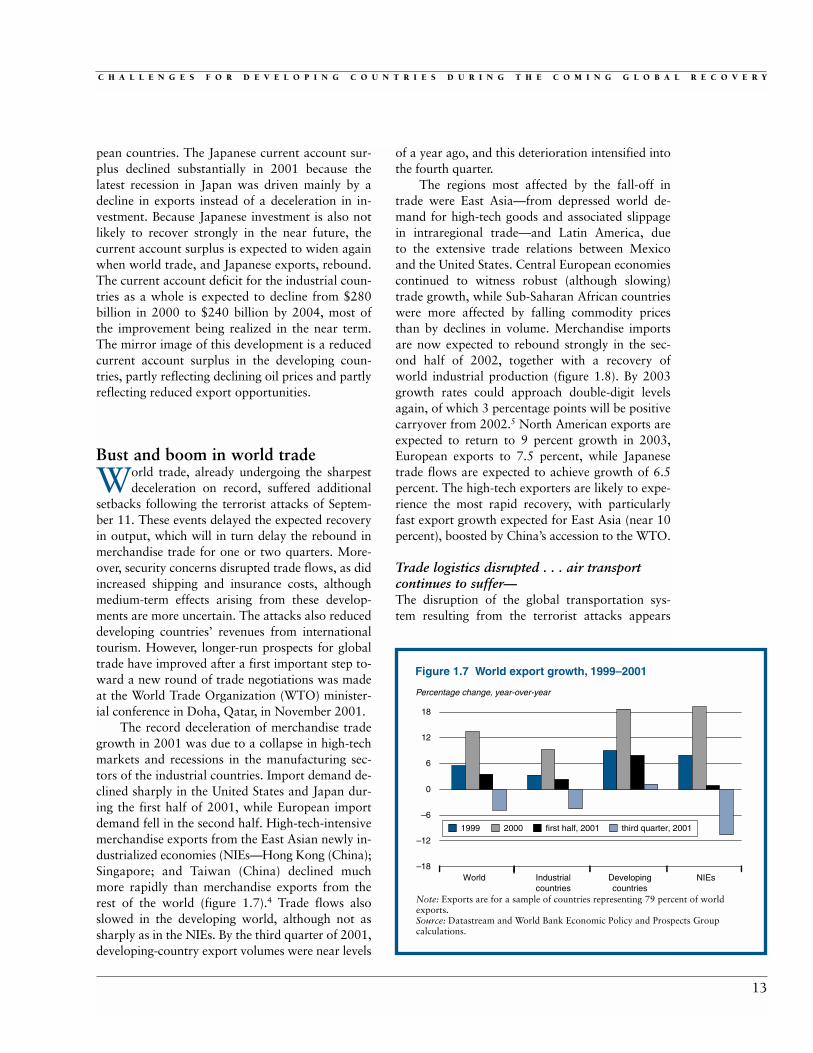

The record deceleration of merchandise tradegrowth in 2001 was due to a collapse in high-techmarkets and recessions in the manufacturing sec-tors of the industrial countries. Import demand de-clined sharply in the United States and Japan dur-ing the first half of 2001, while European importdemand fell in the second half. High-tech-intensivemerchandise exports from the East Asian newly in-dustrialized economies (NIEs—Hong Kong (China);Singapore; and Taiwan (China) declined muchmore rapidly than merchandise exports from therest of the world (figure 1.7).4 Trade flows alsoslowed in the developing world, although not assharply as in the NIEs. By the third quarter of 2001,developing-country export volumes were near levels

of a year ago, and this deterioration intensified intothe fourth quarter.

The regions most affected by the fall-off intrade were East Asia—from depressed world de-mand for high-tech goods and associated slippagein intraregional trade—and Latin America, due to the extensive trade relations between Mexicoand the United States. Central European economiescontinued to witness robust (although slowing)trade growth, while Sub-Saharan African countrieswere more affected by falling commodity pricesthan by declines in volume. Merchandise importsare now expected to rebound strongly in the sec-ond half of 2002, together with a recovery ofworld industrial production (figure 1.8). By 2003growth rates could approach double-digit levelsagain, of which 3 percentage points will be positivecarryover from 2002.5 North American exports areexpected to return to 9 percent growth in 2003,European exports to 7.5 percent, while Japanesetrade flows are expected to achieve growth of 6.5percent. The high-tech exporters are likely to expe-rience the most rapid recovery, with particularlyfast export growth expected for East Asia (near 10percent), boosted by China’s accession to the WTO.

Trade logistics disrupted . . . air transportcontinues to suffer—The disruption of the global transportation sys-tem resulting from the terrorist attacks appears

13

Percentage change, year-over-year

Figure 1.7 World export growth, 1999–2001

Note: Exports are for a sample of countries representing 79 percent of worldexports.Source: Datastream and World Bank Economic Policy and Prospects Groupcalculations.

–18

World Industrialcountries

Developingcountries

NIEs

–12

–6

0

6

12

18

1999 2000 first half, 2001 third quarter, 2001

G L O B A L D E V E L O P M E N T F I N A N C E

to have had only temporary adverse impacts on trade growth, but uncertainties continue to loom.Air cargo has suffered more than other transportmodes. After September 11, U.S. airspace was com-pletely shut down for several days to domestic andinternational passenger and cargo traffic, and ca-pacity utilization and revenues in air transport re-mained significantly below preattack levels for sev-eral months. Other parts of the world, especiallySouth Asia and the Middle East, also suffered inter-ruptions in transportation, albeit less severe thanthose in the United States. There is evidence to sug-gest, however, that the physical constraints ontrade from the security response to the attacks areabating.

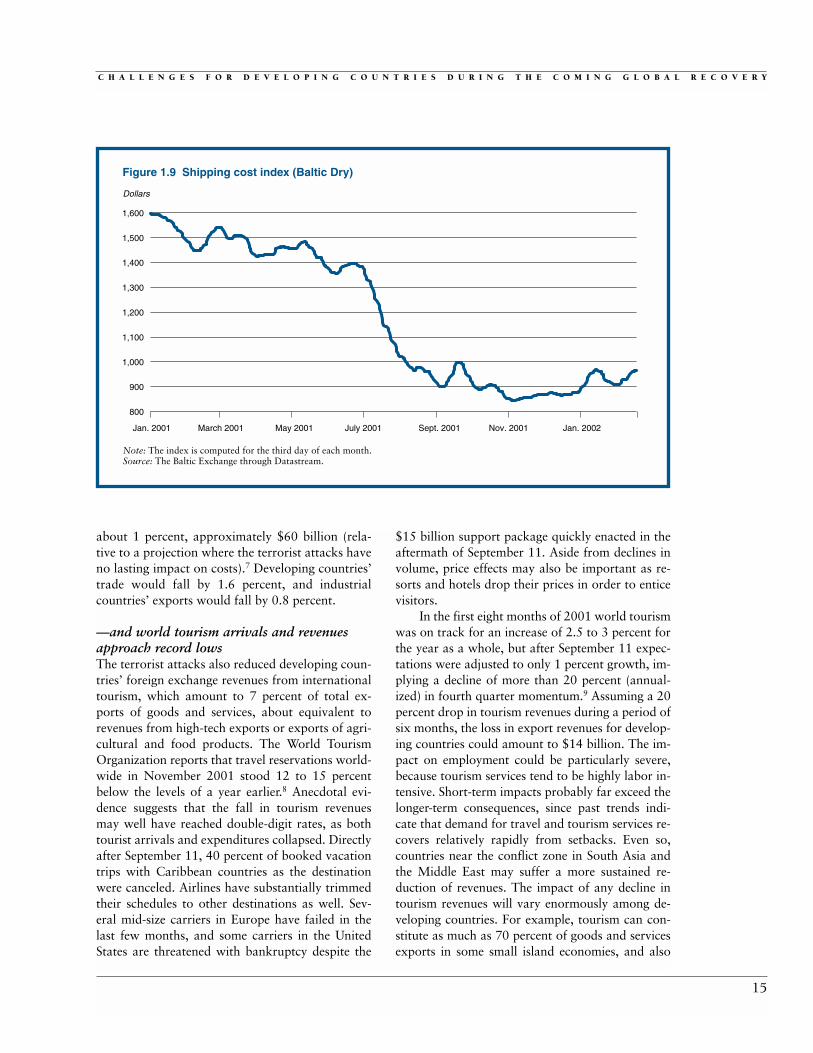

The attacks had the immediate effect of in-creasing insurance and security costs. Maritimeshipping costs rose for 10 to 15 days in the after-math of September 11, rising on average 7 percentaccording to the most widely available shipping costindexes. One of these indexes, the Baltic Dry Index,shows a price spike shortly after September 11 (fig-ure 1.9). However, costs declined quickly thereafter.The Baltic Dry Index resumed its sharp downwardtrend in a matter of days, continuing to track thedecline in world trade volumes over the last year.Furthermore, the available data on seaborne ship-ping costs generally cover the major trade routes—for example, those between Asia and North Amer-

ica, and between North America and Europe. Thereis anecdotal evidence suggesting that costs haverisen substantially more on less-traveled routes, par-ticularly those close to the conflict zone around theMiddle East and South Asia. For example, insur-ance rates on traffic through the Suez Canal in-creased dramatically after September 11.

Security concerns following the terrorist at-tacks had a more pronounced impact on the cost ofair transport. In September, the air cargo index fortransportation across major routes increased by anaverage of 17 percent, with cargo costs from theUnited States increasing by 22 percent. By October,the global index had declined by only 2 percent,with costs still nearly 15 percent higher than beforeSeptember 11. It is likely that a significant portionof the rise in air cargo rates may be longer lasting.

Developing countries’ exports will be moreaffected by rising transportation costs than will ex-ports from industrial countries, because developingcountries tend to specialize in exports of primarygoods and labor-intensive manufactures, whichhave higher trade margins (international transportcosts) than the high-tech exports from industrialcountries.6 One estimate of the effects of a sus-tained increase in the cost of trade on world tradeflows suggests that, if the terrorist attacks caused a 10 percent increase in the port-to-port costs ofmerchandise trade, world trade could decline by

14

Percentage change at seasonally adjusted annualized rates

Figure 1.8 World industrial production and import volumes

Source: Datastream and World Bank Economic Policy and Prospects Group calculations.

–10

Q2, 1993 Q2, 1994 Q2, 1995

Forecast

Industrial production(left axis)

Import volume(right axis)

Q2, 1996 Q2, 1997 Q2, 1998 Q2, 1999 Q2, 2000 Q1, 2001 Q2, 2002

–5

0

5

10

–20

–10

0

10

20

C H A L L E N G E S F O R D E V E L O P I N G C O U N T R I E S D U R I N G T H E C O M I N G G L O B A L R E C O V E R Y

about 1 percent, approximately $60 billion (rela-tive to a projection where the terrorist attacks haveno lasting impact on costs).7 Developing countries’trade would fall by 1.6 percent, and industrialcountries’ exports would fall by 0.8 percent.

—and world tourism arrivals and revenuesapproach record lowsThe terrorist attacks also reduced developing coun-tries’ foreign exchange revenues from internationaltourism, which amount to 7 percent of total ex-ports of goods and services, about equivalent torevenues from high-tech exports or exports of agri-cultural and food products. The World TourismOrganization reports that travel reservations world-wide in November 2001 stood 12 to 15 percentbelow the levels of a year earlier.8 Anecdotal evi-dence suggests that the fall in tourism revenuesmay well have reached double-digit rates, as bothtourist arrivals and expenditures collapsed. Directlyafter September 11, 40 percent of booked vacationtrips with Caribbean countries as the destinationwere canceled. Airlines have substantially trimmedtheir schedules to other destinations as well. Sev-eral mid-size carriers in Europe have failed in thelast few months, and some carriers in the UnitedStates are threatened with bankruptcy despite the

$15 billion support package quickly enacted in theaftermath of September 11. Aside from declines involume, price effects may also be important as re-sorts and hotels drop their prices in order to enticevisitors.

In the first eight months of 2001 world tourismwas on track for an increase of 2.5 to 3 percent forthe year as a whole, but after September 11 expec-tations were adjusted to only 1 percent growth, im-plying a decline of more than 20 percent (annual-ized) in fourth quarter momentum.9 Assuming a 20percent drop in tourism revenues during a period ofsix months, the loss in export revenues for develop-ing countries could amount to $14 billion. The im-pact on employment could be particularly severe,because tourism services tend to be highly labor in-tensive. Short-term impacts probably far exceed thelonger-term consequences, since past trends indi-cate that demand for travel and tourism services re-covers relatively rapidly from setbacks. Even so,countries near the conflict zone in South Asia andthe Middle East may suffer a more sustained re-duction of revenues. The impact of any decline intourism revenues will vary enormously among de-veloping countries. For example, tourism can con-stitute as much as 70 percent of goods and servicesexports in some small island economies, and also

15

Dollars

Figure 1.9 Shipping cost index (Baltic Dry)

Note: The index is computed for the third day of each month.Source: The Baltic Exchange through Datastream.

800

Jan. 2001 March 2001 May 2001 July 2001 Sept. 2001 Nov. 2001 Jan. 2002

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

G L O B A L D E V E L O P M E N T F I N A N C E

has become a key export sector in many Sub-Saharan African countries. Revenues from tourismfor the 14 Sub-Saharan African countries with thehighest dependency on tourism revenues average 22 percent of total export revenues.10 In absoluteterms, Turkey is the largest recipient of tourism rev-enues, and the sharp fall in these receipts since Sep-tember 11 has complicated efforts to overcome thefinancial crisis.

Improved prospects for a development roundof multilateral trade negotiations The Doha Development Agenda—which emergedfrom the WTO Ministerial Conference held inDoha, Qatar, in November 2001—demonstratesthe increased prominence of development con-cerns in WTO deliberations, in turn reflecting in-creased participation by developing countries inthe international trading system. Doha launchednegotiations on market access for manufactures,dispute settlement, WTO rules, environmentalpolicies, and intellectual property protection.These negotiations will complement ongoing talkson market access in agriculture and services, whichare mandated by the Uruguay Round agreements.Negotiations will be launched on four so-calledSingapore issues—competition, investment, tradefacilitation, and transparency in government pro-curement—at the next WTO ministerial meetingin 2003, if consensus can be reached on the modal-ities of such negotiations at that time. Completingnegotiations by January 1, 2005, as envisaged inthe Doha Ministerial Declaration, represents amajor challenge (box 1.1), but success in doing sowould imply large welfare gains for both develop-ing and industrial countries.

Secular declines and cyclical swings incommodities pricesNon-oil commodities. The global economic slow-down, a strong dollar, and large supplies of mostcommodities reduced the average dollar price ofdeveloping countries’ non-oil primary commodityexports by 9 percent in 2001. Demand for metalswas most affected by the economic slowdown,while agricultural commodities continued to facelarge supply increases despite falling prices. Non-oil commodity prices are now one-third belowtheir cyclical high of 1997. Currency depreciationin major commodity exporters in East Asia andLatin America resulted in sharp price declines for

coffee, oilseeds, sugar, and raw materials such asrubber. Continued rapid technological progresscontributed to supply increases in a number ofcommodities,11 and improved policies in some de-veloping countries contributed to large increases inexports.12 Coffee prices were especially hard hit(down 30 percent in 2001 compared with 2000)due to a 20 percent increase in global productionover the past three years with little increase in con-sumption. Cotton prices declined 20 percent in2001 due to large production increases in Chinaand the United States, and rice prices fell 15 per-cent due to the large exports from Thailand andVietnam. Copper prices fell by 12 percent in 2001,and prices would have declined even further ifmajor producers had not cut production by about5 percent in an effort to prevent additional pricedeclines.

The price declines have been especially hardfor exporters in Africa, where non-oil commodi-ties often account for 70 percent or more of ex-port revenues. Ethiopia, for example, derivesnearly two-thirds of total export revenues fromcoffee, and Mali derives about 40 percent of totalexports from cotton. Moreover, the prices of com-modities that account for a large share of Sub-Saharan exports (such as cocoa, coffee, and cop-per) have fallen by more than the prices of com-modities exported by other developing countries(figure 1.10). Since 1980, the index of real non-oilcommodity export prices of Sub-Saharan Africancountries has declined by 10 percent relative to theindex of all developing countries. On top of that,the African index tends to be more volatile overthe price cycle, implying a sharper fall during adownturn. African producers have been unable tomake up for the decline in prices through highervolumes, since African agricultural production hasbeen flat over the past two decades, while agricul-tural production increased rapidly in developingcountries as a whole (figure 1.11). Sub-SaharanAfrica’s non-oil commodity export revenuesdropped at least $3 billion between 1997 and2001—equal to 3.6 percent of non-oil export rev-enues in 1997 and 25 percent of total official de-velopment aid to these countries in 1999.

We expect a recovery of only 15 percent innon-oil commodity prices from current cyclicallows over the interval through 2004. This will leavenon-oil commodity prices 22 percent below their1997 level. The short-term recovery will be driven

16

C H A L L E N G E S F O R D E V E L O P I N G C O U N T R I E S D U R I N G T H E C O M I N G G L O B A L R E C O V E R Y

by a rebound in global economic activity, reducedsupplies and stocks in response to current lowprices, and some weakening of the dollar. There isuncertainty associated with the factors that underliethe recovery of commodities prices, but the impactsof the uncertainties on prices differ markedly. Whilethe timing of the rebound of demand is uncertain,

a recovery that is further delayed will have only alimited negative impact on prices. The potential forunexpected supply increases may be a greater risk.During the 1990s rapid technological progress,combined with improved policies, led to the emer-gence of major producers in a relatively short pe-riod of time, resulting in sharp declines in prices (as

17

The Doha agenda has great potential to be beneficialfrom a development perspective. A great deal of re-

search has documented that there is still a large market-access agenda and that dealing with this agenda willsignificantly increase real incomes and reduce poverty indeveloping countries (World Bank 2001). Research alsosuggests that care is required to determine the develop-ment relevance and payoffs of extending the WTO intoregulatory areas (Hertel, Hoekman, and Martin 2002).The key areas of concern for developing countries in thenew trade round will be market access, regulatory issues,and the magnitude and effectiveness of the technical assis-tance that was promised in Doha.

Improving market access remains a key goal of multi-lateral trade negotiations. Industrial countries will need tomobilize the political will to reduce remaining pockets ofprotection in key sectors such as agriculture, labor-basedservices, and labor-intensive manufactures. Developingcountries also need to be willing to liberalize access totheir markets for goods and services. The relatively highbarriers to trade in goods and services that continue toprevail in many developing countries implies that theyhave a lot to bring to the table in a mercantilist sense.Identifying a set of “concessions” that are of interest topolitically powerful groups in OECD countries and thatare beneficial to developing countries is the major chal-lenge confronting policymakers in the coming years. Theresearch and development communities need to help iden-tify what such issues might be and assist in mobilizing theaffected constituencies.13

As far as multilateral rule-making on regulatory issuesis concerned, better understanding of the issues in develop-ing countries is required, not just by government officialsbut also by the private sector and civil society. Despite fiveyears of studying trade and investment-competition link-ages in WTO working groups set up for that purpose,many low-income countries were fearful in Doha oflaunching negotiations in these areas. There is clearly aneed to provide greater assistance to build capacity andundertake analysis in developing countries to determinethe merits and implications of multilateral disciplines.

Whether it makes sense to rely on negotiation and bindingdispute settlement to address behind-the-border policies inthe WTO is a question that developing countries need toanswer for themselves. The Doha ministerial meeting re-vealed that many countries had an answer to that question,but that many others did not.

The Doha declaration contains numerous commit-ments by high-income WTO members to provide technicalassistance. However, there is no mention of the magnitudeof assistance that will be offered, nor is there discussion of any mechanism to determine what the needs are andhow they should be addressed (that is, what the deliverymechanism might be). Embedding technical assistance in abroader development framework is critical in ensuring thatthe assistance focuses on the priority needs of each countryand is consistent with its development strategy. The sepa-rate section in the Doha declaration on technical coopera-tion and capacity building provides scope to move in thisdirection: Ministers “instruct the Secretariat, in coordina-tion with other relevant agencies, to support domesticefforts for mainstreaming trade into national plans foreconomic development and strategies for poverty reduc-tion” (paragraph 38). A concerted effort will be needed toensure aid is targeted at national priorities, and to ensurethat assistance is provided in an effective manner byagencies with a comparative advantage in an area.

Ensuring that the new round of trade negotiationsachieves a pro-development negotiating outcome is a major challenge. Resistance to liberalization of agricultureand textiles is very strong. Conversely, many low-incomecountries are unwilling to extend the reach of the WTO tocover issues such as competition and investment policies. A major question confronting WTO members is whether adeal should be constructed that involves linking old marketaccess issues to disciplines on new issues such as invest-ment and competition. The feasibility of any such linkagewill depend greatly on what is done in the coming years toaddress developing-country concerns regarding implemen-tation of Uruguay Round agreements and the magnitudeand effectiveness of the technical assistance that waspromised in Doha.

Box 1.1 The Doha Development Agenda

G L O B A L D E V E L O P M E N T F I N A N C E

in the case of coffee). While such supply increasesare difficult to predict, they remain an importantrisk to the forecast. Conversely, abnormal weatherconditions are more likely to lead to higher prices,since bad harvests tend to result in much larger fallsin production than would be the case when goodweather conditions boost production.

Oil prices. The global economic slowdowncontributed to a reduction of oil prices from $28.2a barrel in 2000 to $24.4 in 2001.14 Oil prices

spiked briefly to $31 a barrel immediately follow-ing September 11, but when it became apparentthat there were no immediate threats to oil sup-plies, prices quickly fell, ending the year at $18.5.World oil demand grew little in 2001, and actuallyfell by 1 percent year-on-year in the second half ofthe year as a result of the after-effects of the attacks(such as reduced jet travel, for example), the deep-ening economic slowdown, and mild weather. Withnon-OPEC (Organization of Petroleum ExportingCountries) production growing moderately overall(increases occurred mainly in the Commonwealthof Independent States, or CIS), oil inventories haverisen back to a more comfortable range comparedwith the low levels of 2000 (figure 1.12).

OPEC reduced production three times prior toSeptember 11 to keep the price of its crude basketwithin its target range of $22 to $28 a barrel. But,with the changed political environment after Sep-tember 11 and as the economic slowdown wors-ened, OPEC chose not to activate its “automaticmechanism” that reduces output when the price of oil falls below $22 for 10 consecutive days. In-stead, OPEC countries relied on reducing their pro-duction above quota (estimated at 0.54 millionbarrels a day in November) to help support prices.

With oil prices well below $20 a barrel inNovember, OPEC agreed to reduce quotas by 6.5percent or 1.5 million barrels per day (mb/d) be-ginning January 1, 2002—but only if non-OPECproducers firmly committed to reducing produc-tion by 0.5 mb/d. OPEC threatened a price war ifa deal could not be reached. Non-OPEC producersresponded in part, with major producers Norwayand the Russian Federation each agreeing to cutproduction by 0.15 mb/d. While non-OPEC cutsfell short of the 0.5 mb/d demanded, they werelarge enough for OPEC to follow through on itsproposed cuts, which will last “as long as neces-sary” according to OPEC’s secretary general.