Embed Size (px)

Citation preview

Economics and Strategy

Geopolitical Briefing

February 16, 2021

Taiwan’s semiconductor sector on the front line of great power rivalry By Angelo Katsoras

Taiwan has long been a major point of friction between the United States and China. This dates back to 1949 when the U.S.-backed nationalists lost the civil war to the Communists. The defeated side was forced to flee the mainland for Taiwan. China to this day regards the island as a breakaway province, which it has vowed to take back by force if necessary.

In 1979, the United States agreed to recognize the Communist Party as the sole legal government of China without, however, clarifying its position on Taiwan’s sovereignty. To counter accusations that it was abandoning its ally, the United States passed the Taiwan Relations Act, which mandated continued close economic relations, including with respect to weapon sales. Maintaining a policy of strategic ambiguity, the United States has long refused to say what it would do if China attempted to invade Taiwan.

Taiwan’s emergence over the past few decades as the leading manufacturer of advanced semiconductors (commonly known as chips) has further increased the island’s strategic importance in the eyes of both the United States and China. One Taiwanese company alone, Taiwan Semiconductor Manufacturing Company (TSMC), accounts for about one fifth of all the world’s chip manufacturing and half the production of the most advanced chips on the market today.1

An overview of the semiconductor sector Simply put, semiconductors are the brains behind all IT products from smartphones to advanced defence systems to automobiles. About a trillion chips are currently being produced annually.2

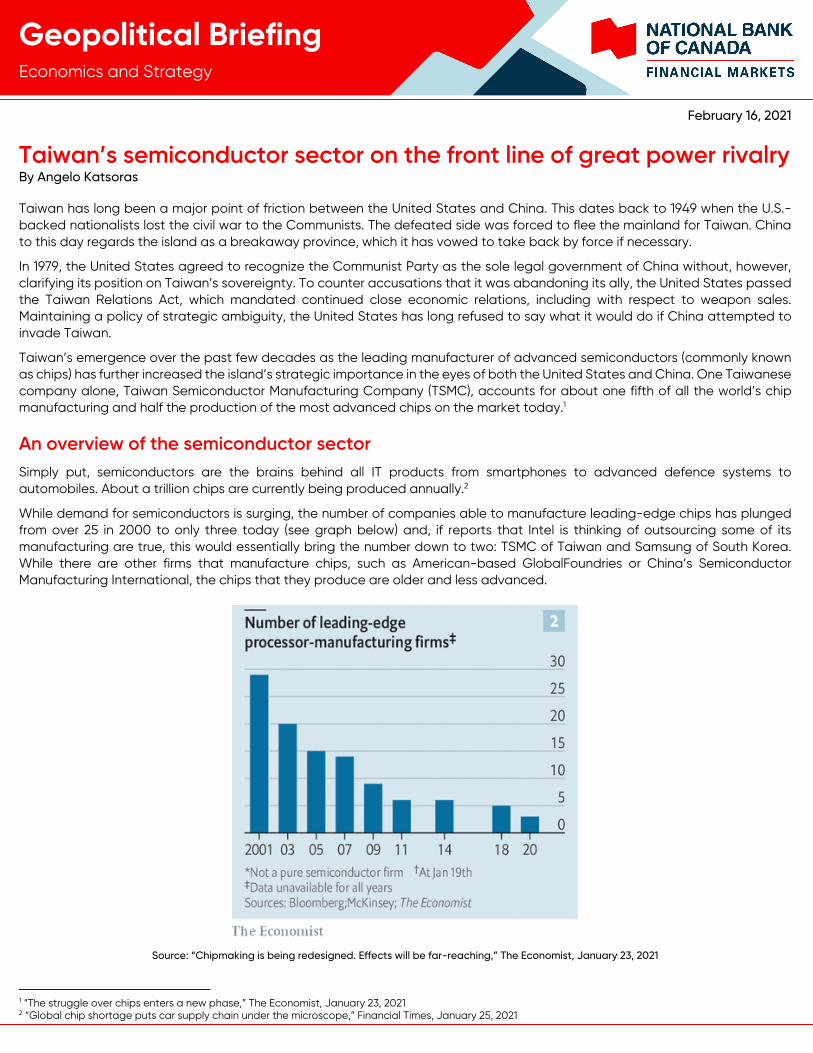

While demand for semiconductors is surging, the number of companies able to manufacture leading-edge chips has plunged from over 25 in 2000 to only three today (see graph below) and, if reports that Intel is thinking of outsourcing some of its manufacturing are true, this would essentially bring the number down to two: TSMC of Taiwan and Samsung of South Korea. While there are other firms that manufacture chips, such as American-based GlobalFoundries or China’s Semiconductor Manufacturing International, the chips that they produce are older and less advanced.

Source: “Chipmaking is being redesigned. Effects will be far-reaching,” The Economist, January 23, 2021

1 “The struggle over chips enters a new phase,” The Economist, January 23, 2021 2 “Global chip shortage puts car supply chain under the microscope,” Financial Times, January 25, 2021

2

Economics and Strategy

Geopolitical Briefing

For the most part, this consolidation is due to the astronomical cost of building a chip factory. TSMC recently built a plant capable of manufacturing 3-nanometre semiconductors, its most advanced chips, for a cost of $19.5 billion.3 Advances in semiconductors are measured in nanometres, or billionths of a metre, with ever-smaller transistors being placed on the newest models.

China’s reliance on imported semiconductors After being heavily criticized for its initial handling of COVID-19, China has emerged from the pandemic in a relatively strong position. It became one of the first countries to get the pandemic largely under control and was the only major world economy to grow in 2020.

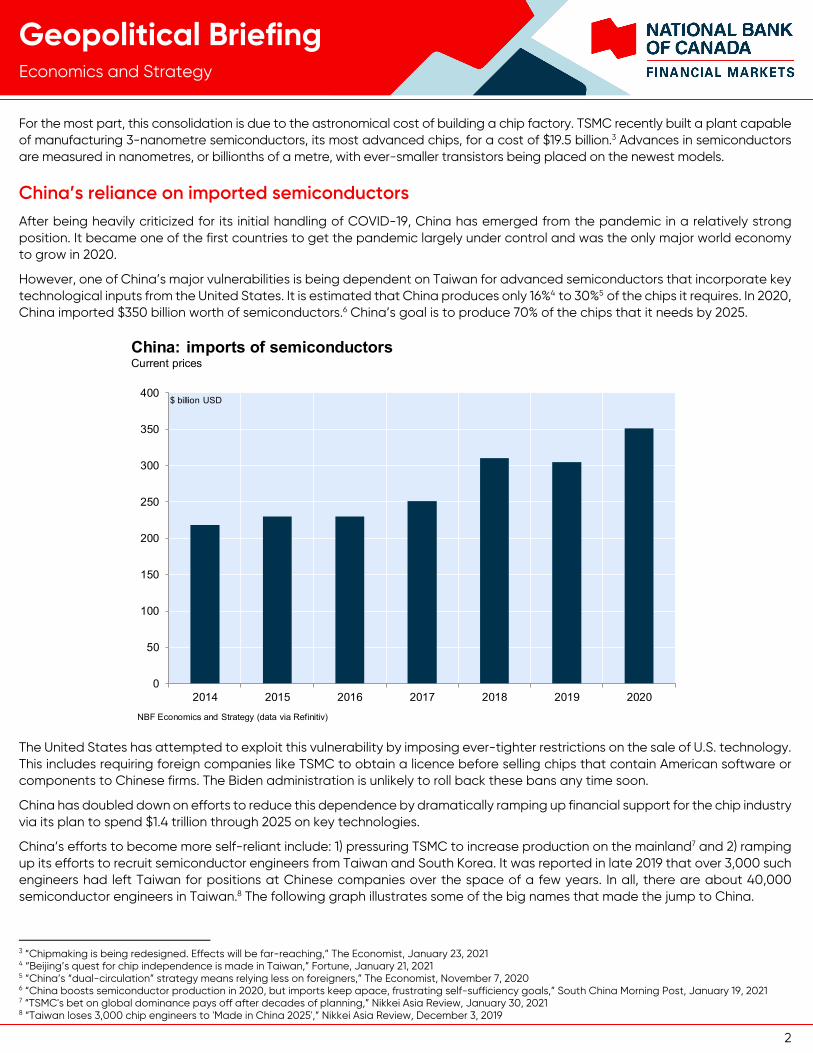

However, one of China’s major vulnerabilities is being dependent on Taiwan for advanced semiconductors that incorporate key technological inputs from the United States. It is estimated that China produces only 16%4 to 30%5 of the chips it requires. In 2020, China imported $350 billion worth of semiconductors.6 China’s goal is to produce 70% of the chips that it needs by 2025.

The United States has attempted to exploit this vulnerability by imposing ever-tighter restrictions on the sale of U.S. technology. This includes requiring foreign companies like TSMC to obtain a licence before selling chips that contain American software or components to Chinese firms. The Biden administration is unlikely to roll back these bans any time soon.

China has doubled down on efforts to reduce this dependence by dramatically ramping up financial support for the chip industry via its plan to spend $1.4 trillion through 2025 on key technologies.

China’s efforts to become more self-reliant include: 1) pressuring TSMC to increase production on the mainland7 and 2) ramping up its efforts to recruit semiconductor engineers from Taiwan and South Korea. It was reported in late 2019 that over 3,000 such engineers had left Taiwan for positions at Chinese companies over the space of a few years. In all, there are about 40,000 semiconductor engineers in Taiwan.8 The following graph illustrates some of the big names that made the jump to China.

3 “Chipmaking is being redesigned. Effects will be far-reaching,” The Economist, January 23, 2021 4 “Beijing’s quest for chip independence is made in Taiwan,” Fortune, January 21, 2021 5 “China’s “dual-circulation” strategy means relying less on foreigners,” The Economist, November 7, 2020 6 “China boosts semiconductor production in 2020, but imports keep apace, frustrating self-sufficiency goals,” South China Morning Post, January 19, 2021 7 “TSMC's bet on global dominance pays off after decades of planning,” Nikkei Asia Review, January 30, 2021 8 “Taiwan loses 3,000 chip engineers to 'Made in China 2025',” Nikkei Asia Review, December 3, 2019

0

50

100

150

200

250

300

350

400

2014 2015 2016 2017 2018 2019 2020

China: imports of semiconductors Current prices

$ billion USD

NBF Economics and Strategy (data via Refinitiv)

3

Economics and Strategy

Geopolitical Briefing

Source: “Taiwan loses 3,000 chip engineers to 'Made in China 2025',” Nikkei Asia Review, December 3, 2019

The United States is also facing its own semiconductor-related challenges At first glance, the position of U.S.-based semiconductor companies appears to be on solid footing, with about 47% of the global market share. However, only about 12% of the world’s semiconductors are currently produced in the United States, down from well over 30% in 1990. Most U.S. chip companies have contracted out their production to Asian producers such as TSMC.9

9 “Why Fewer Chips Say ‘Made in the U.S.A.’,” Wall Street Journal, November 12, 2020

4

Economics and Strategy

Geopolitical Briefing

Share of global chip manufacturing capacity

Source: “Why Fewer Chips Say, ‘Made in the U.S.A.’,” Wall Street Journal, November 12, 2020

While U.S. companies still hold dominant positions in the chip-manufacturing software and equipment market, there is a growing risk companies that have perfected the manufacturing process will inevitably move into these segments as well.

Reshoring Like China, the United States has become increasingly uneasy about being overly dependent on imports of advanced semiconductors. As a result, there is a growing push for companies to build plants on American soil, which includes offering them increased financial incentives.

Last November, TSMC announced that it would build, with the help of generous U.S. subsidies, a $12-billion chip plant in Arizona. More recently Samsung announced that it was considering building a $17-billion factory in the United States. A key factor in its final decision will be the size of government incentives.

On the legislative front, a bill called the “CHIPS for America Act’ was introduced in 2020 with bipartisan support that would secure $25 billion in federal funds and tax incentives.

5

Economics and Strategy

Geopolitical Briefing

Convergence of factors leading to a global chip shortage The geopolitical tensions surrounding semiconductors, in conjunction with the repercussions of the COVID-19 pandemic, have led to a global shortage of chips. The exact reasons for this are the following:

The fact that people have been forced to work and study from home has led to a surge in demand for personal computers and other electronic items, all of which are powered by semiconductors.

At the onset of the pandemic, automakers slashed orders for chips, wrongly assuming that a long-term plunge in sales was imminent. Semiconductor manufacturers responded by shifting production toward electronic products, thus leaving insufficient capacity to meet the car companies’ renewed demand for more chips. Electronic components, which rely on chips to power them, accounted for about 40% of the cost of a new automobile in 2017, up from 20% in 2007.10

Geopolitics have played a role as well. When SMIC, China’s main chip producer, was barred from buying U.S. technology, many of its customers switched to other companies. The problem is that many of these companies were already running at near full capacity.

Before the full force of U.S. trade restrictions went into effect last September, Chinese companies like Huawei rushed to build up huge stockpiles of chips.

Because it can take six to nine months to realign production, the shortage of chips is expected to last well into 2021.11 TSMC raised its prices 10% to 15% last fall and is considering another round of price hikes.12 Going forward, many companies will be tempted to stockpile semiconductors to avoid the risk of being hit by shortages again.

Would China invade Taiwan? As the chart below illustrates, China has an enormous military advantage over Taiwan.

Source: “Defending Taiwan is growing costlier and deadlier,” The Economist, October 10, 2020

Despite this advantage and the fact that China has turned up the pressure on Taiwan of late by conducting intensive military exercises, we do not feel that an invasion is imminent.

So long as Taiwan does not declare independence, China’s strategy of ratcheting up pressure will likely be limited in the near term to selectively applying regulations to Taiwanese business operations on the mainland, intercepting or delaying Taiwanese cargo ships for supposed regulatory infractions, and continued military exercises.

10 “Semiconductors – the next wave,” Deloitte, April 2019 11 “Lack of Tiny Parts Disrupts Auto Factories Worldwide,” New York Times, January 13, 2021 12 “TSMC and Taiwan chip peers weigh new price hikes for autos,” Nikkei Asia Review, January 26, 2021

6

Economics and Strategy

Geopolitical Briefing

China realizes that a major outbreak of hostilities would turn international public opinion against it and have negative economic and social consequences, particularly given its close economic ties with the island. Trade between Taiwan and China reached $150.5 billion in 2018, up from $35 billion in 1999,13 Taiwanese companies have invested $190 billion in Chinese operations over the past three decades, and as many as 1.2 million Taiwanese, or 5% of Taiwan’s population, live on the Chinese mainland.14 Finally, Chinese leaders are no doubt worried that a protracted war could turn public opinion against the government.

However, over the longer term, some analysts worry as China’s economic and military advantages over Taiwan continue to widen, the risk of a military conflict will increase. Under this scenario, China’s opening moves could involve seizing the Taiwanese-controlled Islands closest to the mainland, cutting Taiwan’s underseas internet cables and/or blockading the delivery of oil.

Source: “China’s War on Taiwan Won’t Start in Taiwan,” Geopolitical Futures, August 21, 2020

13 “China-Taiwan Relations,” Council on Foreign Relations, January 22, 2021 14 “Why commercial ties between Taiwan and China are beginning to fray,” The Economist, November 19, 2020

7

Economics and Strategy

Geopolitical Briefing

Would United States fight to defend Taiwan?

In the unlikely event of a full-blown Chinese invasion, the United States would find itself in an almost untenable geopolitical position. On the one hand, it would be very costly to defend Taiwan militarily in terms of both blood and treasure. This is particularly the case given China’s growing military power and its ability to concentrate its forces while America’s military might is spread out around the globe. The higher the level of casualties, the greater the risk of a political backlash at home, as Americans would be wondering why they are involved in a conflict so far from their shores.

On the other hand, deciding not to defend Taiwan would cause a huge loss of global geopolitical prestige and other countries, particularly in the Asian region, would think twice before basing their security on an American-led alliance.

In such a situation, America’s dilemma would be made more difficult by the likelihood that control over Taiwan and its plants would place China on the path to technological supremacy in the semiconductor sector (provided that the plants in question were not significantly damaged).

Further, both great powers are aware that even a minor outbreak in hostilities between the two would shake the global economy and financial markets.

Conclusion While we do not feel that increased tensions over Taiwan will lead to an outbreak of hostilities anytime soon, it will over the longer-term lead to the reconfiguration of semiconductor supply chains. This means that both China and the United States will require, for reasons of national security, that more semiconductors be produced domestically even if this translates into higher costs.

More specifically, Taiwan Semiconductor Manufacturing Company will ultimately be forced by the United States and China to set up production lines in their respective countries, with each country requiring its supply chain to exclude the other’s technology.

Other major countries, such as Japan and Germany, will also try to develop their own domestic capacities.

Bottom line: While all these moves might help ensure security of supply in times of crisis, producing semiconductors in a multitude of locations will reduce economies of scale and significantly add to costs. This makes further hikes in the price of semiconductors and related electronic products likely.

This is in addition to efforts by the United States and other countries to develop their own capacities, regardless of the higher costs involved, in the areas of health care equipment/medicines and rare earth minerals. For further details on cost pressures impacting rare earth mineral production refer to our report entitled: “Superpowers competing for control of minerals and supply chains to fuel the next industrial revolution.”

Finally, while it would level the playing field for companies based in countries with stricter climate regulations, proposals by the United States and the EU to implement carbon border taxes on imports from countries with lesser environmental standards would also increase costs.

Economics and Strategy

Geopolitical Briefing

Economics and Strategy

Montreal Office Toronto Office 514-879-2529 416-869-8598

Stéfane Marion Matthieu Arseneau Warren Lovely Chief Economist and Strategist Deputy Chief Economist Chief Rates and Public Sector Strategist [email protected] [email protected] [email protected]

Paul-André Pinsonnault Angelo Katsoras Kyle Dahms Taylor Schleich Senior Economist Geopolitical Analyst Economist Rates Strategist [email protected] [email protected] [email protected] [email protected]

Daren King Jocelyn Paquet Camille Baillargeon Economist Economist Intern Economist [email protected] [email protected] [email protected]

General

This Report was prepared by National Bank Financial, Inc. (NBF), (a Canadian investment dealer, member of IIROC), an indirect wholly owned subsidiary of National Bank of Canada. National Bank of Canada is a public company listed on the Toronto Stock Exchange.

The particulars contained herein were obtained from sources which we believe to be reliable but are not guaranteed by us and may be incomplete and may be subject to change without notice. The information is current as of the date of this document. Neither the author nor NBF assumes any obligation to update the information or advise on further developments relating to the topics or securities discussed. The opinions expressed are based upon the author(s) analysis and interpretation of these particulars and are not to be construed as a solicitation or offer to buy or sell the securities mentioned herein, and nothing in this Report constitutes a representation that any investment strategy or recommendation contained herein is suitable or appropriate to a recipient’s individual circumstances. In all cases, investors should conduct their own investigation and analysis of such information before taking or omitting to take any action in relation to securities or markets that are analyzed in this Report. The Report alone is not intended to form the basis for an investment decision, or to replace any due diligence or analytical work required by you in making an investment decision.

This Report is for distribution only under such circumstances as may be permitted by applicable law. This Report is not directed at you if NBF or any affiliate distributing this Report is prohibited or restricted by any legislation or regulation in any jurisdiction from making it available to you. You should satisfy yourself before reading it that NBF is permitted to provide this Report to you under relevant legislation and regulations.

National Bank of Canada Financial Markets is a trade name used by National Bank Financial and National Bank of Canada Financial Inc.

Canadian Residents

NBF or its affiliates may engage in any trading strategies described herein for their own account or on a discretionary basis on behalf of certain clients and as market conditions change, may amend or change investment strategy including full and complete divestment. The trading interests of NBF and its affiliates may also be contrary to any opinions expressed in this Report.

NBF or its affiliates often act as financial advisor, agent or underwriter for certain issuers mentioned herein and may receive remuneration for its services. As well NBF and its affiliates and/or their officers, directors, representatives, associates, may have a position in the securities mentioned herein and may make purchases and/or sales of these securities from time to time in the open market or otherwise. NBF and its affiliates may make a market in securities mentioned in this Report. This Report may not be independent of the proprietary interests of NBF and its affiliates.

This Report is not considered a research product under Canadian law and regulation, and consequently is not governed by Canadian rules applicable to the publication and distribution of research Reports, including relevant restrictions or disclosures required to be included in research Reports.

Economics and Strategy

Geopolitical Briefing

UK Residents

This Report is a marketing document. This Report has not been prepared in accordance with EU legal requirements designed to promote the independence of investment research and it is not subject to any prohibition on dealing ahead of the dissemination of investment research. In respect of the distribution of this Report to UK residents, NBF has approved the contents (including, where necessary, for the purposes of Section 21(1) of the Financial Services and Markets Act 2000). This Report is for information purposes only and does not constitute a personal recommendation, or investment, legal or tax advice. NBF and/or its parent and/or any companies within or affiliates of the National Bank of Canada group and/or any of their directors, officers and employees may have or may have had interests or long or short positions in, and may at any time make purchases and/or sales as principal or agent, or may act or may have acted as market maker in the relevant investments or related investments discussed in this Report, or may act or have acted as investment and/or commercial banker with respect hereto. The value of investments, and the income derived from them, can go down as well as up and you may not get back the amount invested. Past performance is not a guide to future performance. If an investment is denominated in a foreign currency, rates of exchange may have an adverse effect on the value of the investment. Investments which are illiquid may be difficult to sell or realise; it may also be difficult to obtain reliable information about their value or the extent of the risks to which they are exposed. Certain transactions, including those involving futures, swaps, and other derivatives, give rise to substantial risk and are not suitable for all investors. The investments contained in this Report are not available to retail customers and this Report is not for distribution to retail clients (within the meaning of the rules of the Financial Conduct Authority). Persons who are retail clients should not act or rely upon the information in this Report. This Report does not constitute or form part of any offer for sale or subscription of or solicitation of any offer to buy or subscribe for the securities described herein nor shall it or any part of it form the basis of or be relied on in connection with any contract or commitment whatsoever.

This information is only for distribution to Eligible Counterparties and Professional Clients in the United Kingdom within the meaning of the rules of the Financial Conduct Authority. NBF is authorised and regulated by the Financial Conduct Authority and has its registered office at 71 Fenchurch Street, London, EC3M 4HD.

NBF is not authorised by the Prudential Regulation Authority and the Financial Conduct Authority to accept deposits in the United Kingdom.

U.S. Residents

With respect to the distribution of this report in the United States of America, National Bank of Canada Financial Inc. (“NBCFI”) which is regulated by the Financial Industry Regulatory Authority (FINRA) and a member of the Securities Investor Protection Corporation (SIPC), an affiliate of NBF, accepts responsibility for its contents, subject to any terms set out above. To make further inquiry related to this report, or to effect any transaction, United States residents should contact their NBCFI registered representative.

This report is not a research report and is intended for Major U.S. Institutional Investors only.

This report is not subject to U.S. independence and disclosure standards applicable to research reports.

HK Residents

With respect to the distribution of this report in Hong Kong by NBC Financial Markets Asia Limited (“NBCFMA”)which is licensed by the Securities and Futures Commission (“SFC”) to conduct Type 1 (dealing in securities) and Type 3 (leveraged foreign exchange trading) regulated activities, the contents of this report are solely for informational purposes. It has not been approved by, reviewed by, verified by or filed with any regulator in Hong Kong. Nothing herein is a recommendation, advice, offer or solicitation to buy or sell a product or service, nor an official confirmation of any transaction. None of the products issuers, NBCFMA or its affiliates or other persons or entities named herein are obliged to notify you of changes to any information and none of the foregoing assume any loss suffered by you in reliance of such information.

The content of this report may contain information about investment products which are not authorized by SFC for offering to the public in Hong Kong and such information will only be available to, those persons who are Professional Investors (as defined in the Securities and Futures Ordinance of Hong Kong (“SFO”)). If you are in any doubt as to your status you should consult a financial adviser or contact us. This material is not meant to be marketing materials and is not intended for public distribution. Please note that neither this material nor the product referred to is authorized for sale by SFC. Please refer to product prospectus for full details.

There may be conflicts of interest relating to NBCFMA or its affiliates’ businesses. These activities and interests include potential multiple advisory, transactional and financial and other interests in securities and instruments that may be purchased or sold by NBCFMA or its affiliates, or in other investment vehicles which are managed by NBCFMA or its affiliates that may purchase or sell such securities and instruments.

No other entity within the National Bank of Canada group, including National Bank of Canada and National Bank Financial Inc, is licensed or registered with the SFC. Accordingly, such entities and their employees are not permitted and do not intend to: (i) carry on a business in any regulated activity in Hong Kong; (ii) hold themselves out as carrying on a business in any regulated activity in Hong Kong; or (iii) actively market their services to the Hong Kong public.

Copyright

This Report may not be reproduced in whole or in part, or further distributed or published or referred to in any manner whatsoever, nor may the information, opinions or conclusions contained in it be referred to without in each case the prior express written consent of NBF.