Embed Size (px)

Citation preview

GENESIS ENERGY

Investor RoadshowMay/June 2017

Marc England, Chief ExecutiveChris Jewell, Chief Financial Officer

For

per

sona

l use

onl

y

Market Overview

For

per

sona

l use

onl

y

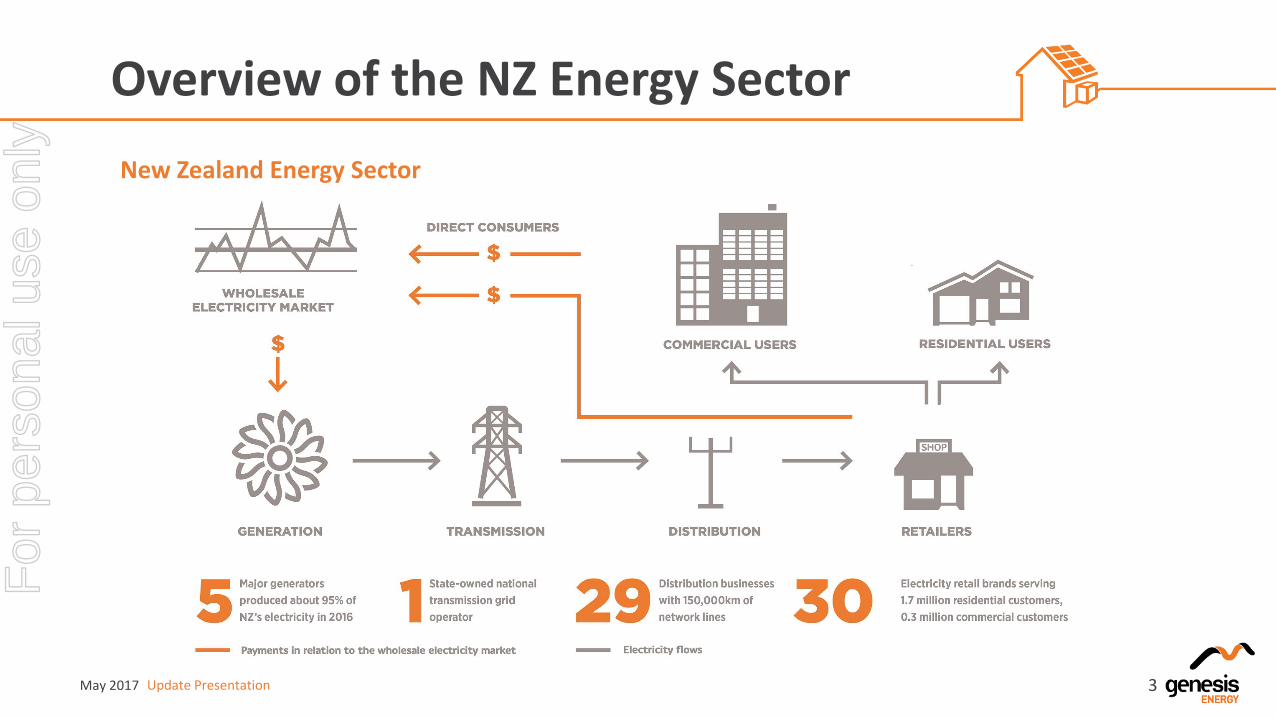

Overview of the NZ Energy Sector

3

New Zealand Energy Sector

May 2017 Update Presentation

For

per

sona

l use

onl

y

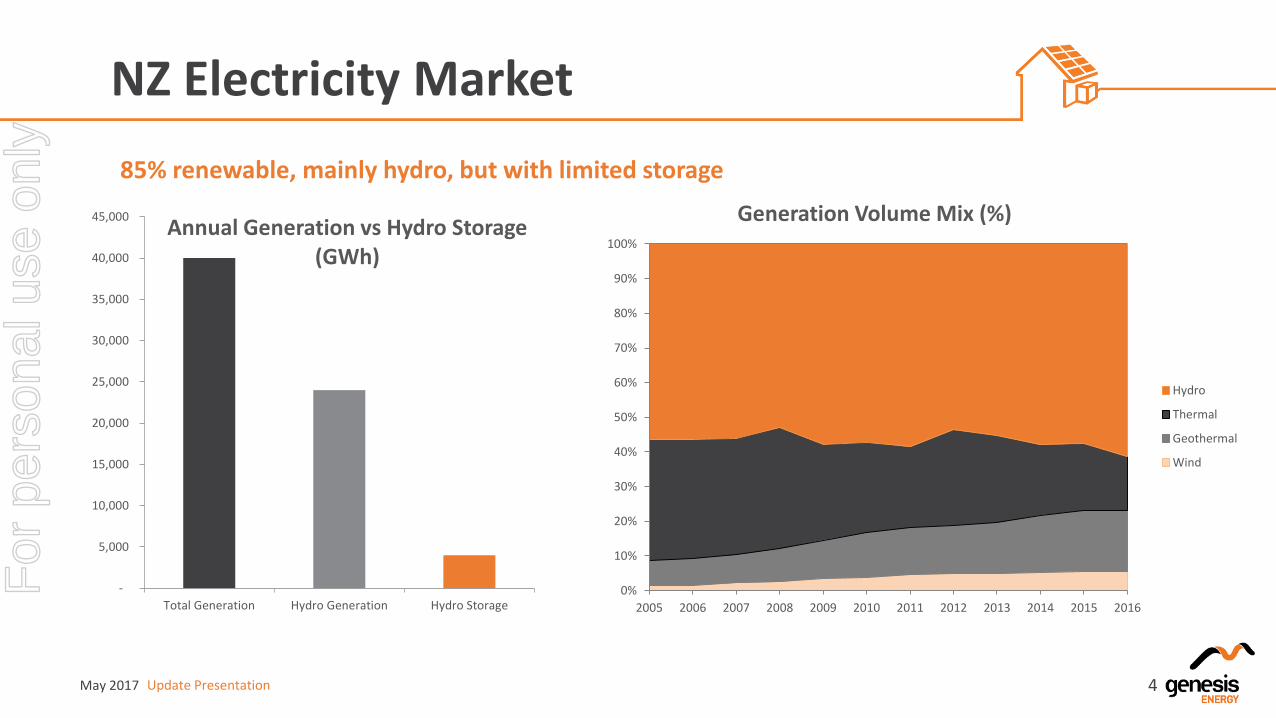

NZ Electricity Market

85% renewable, mainly hydro, but with limited storage

4May 2017 Update Presentation

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Generation Volume Mix (%)

Hydro

Thermal

Geothermal

Wind

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Total Generation Hydro Generation Hydro Storage

Annual Generation vs Hydro Storage (GWh)

For

per

sona

l use

onl

y

NZ Gas Market

Natural gas produced in one region with stable supply

5May 2017 Update Presentation

• Currently 15 producing fields in Taranaki

• The decline in oil price has led to a decline in wells drilled since the 2011 peak

• There is currently an oversupply of gas, but this may become more balanced by 2020 if current levels of exploration continue

• Gas reserves are stable as smaller fields replace Maui’s dwindling production

NET NATURAL GAS PRODUCTION

For

per

sona

l use

onl

y

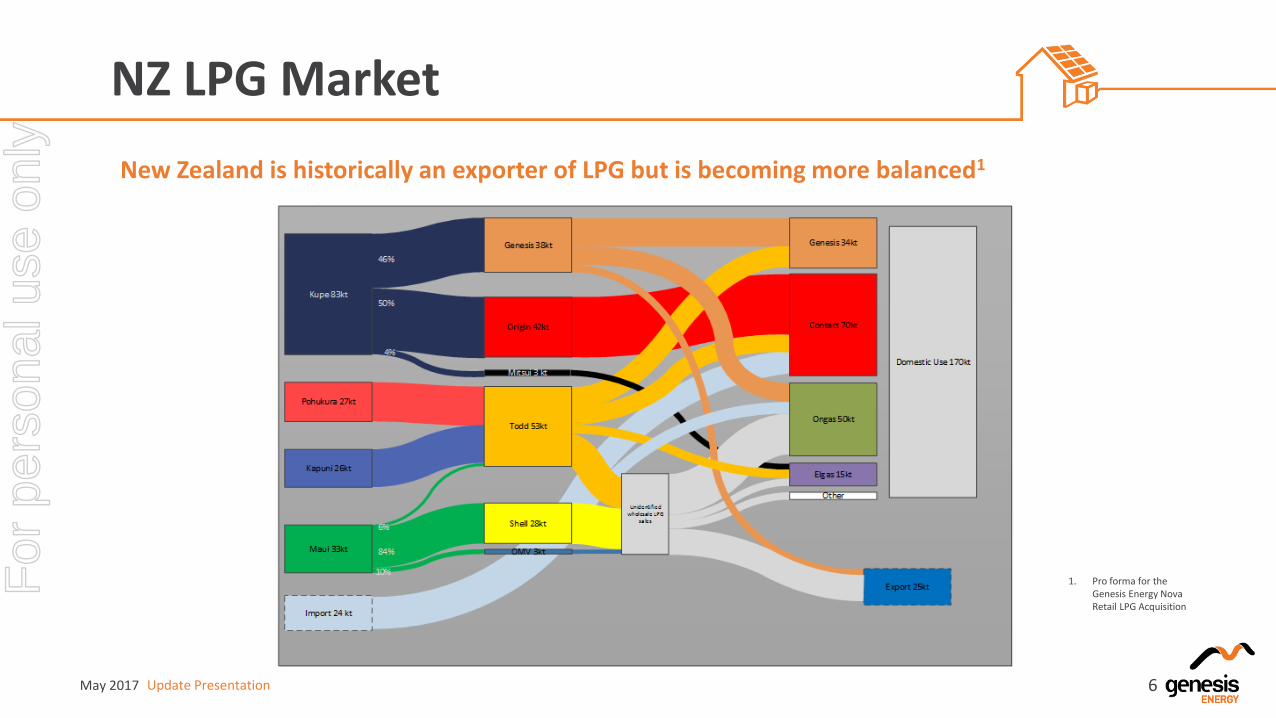

NZ LPG Market

New Zealand is historically an exporter of LPG but is becoming more balanced1

6May 2017 Update Presentation

1. Pro forma for the Genesis Energy Nova Retail LPG Acquisition

For

per

sona

l use

onl

y

Energy Retailing

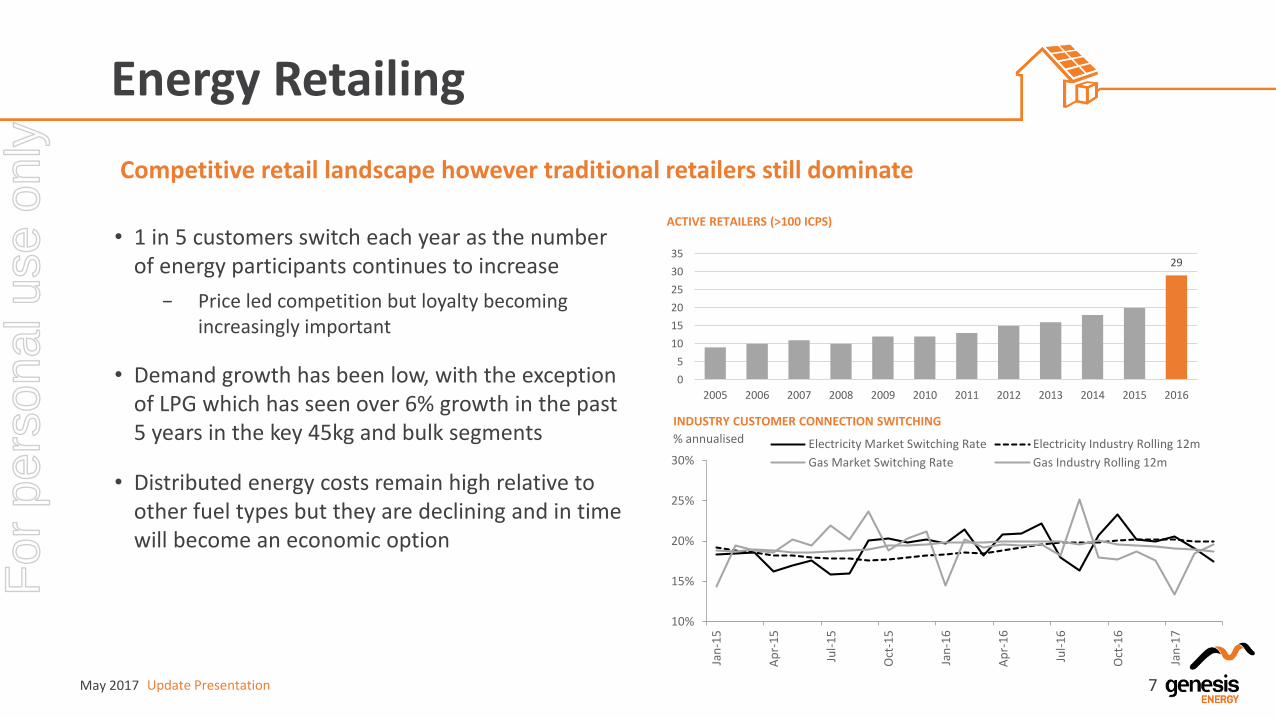

Competitive retail landscape however traditional retailers still dominate

7May 2017 Update Presentation

29

0

5

10

15

20

25

30

35

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

ACTIVE RETAILERS (>100 ICPS)

• 1 in 5 customers switch each year as the number of energy participants continues to increase

− Price led competition but loyalty becoming increasingly important

• Demand growth has been low, with the exception of LPG which has seen over 6% growth in the past 5 years in the key 45kg and bulk segments

• Distributed energy costs remain high relative to other fuel types but they are declining and in time will become an economic option

10%

15%

20%

25%

30%

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

Jan

-17

% annualised

INDUSTRY CUSTOMER CONNECTION SWITCHING

Electricity Market Switching Rate Electricity Industry Rolling 12m

Gas Market Switching Rate Gas Industry Rolling 12m

For

per

sona

l use

onl

y

Genesis Energy Overview

For

per

sona

l use

onl

y

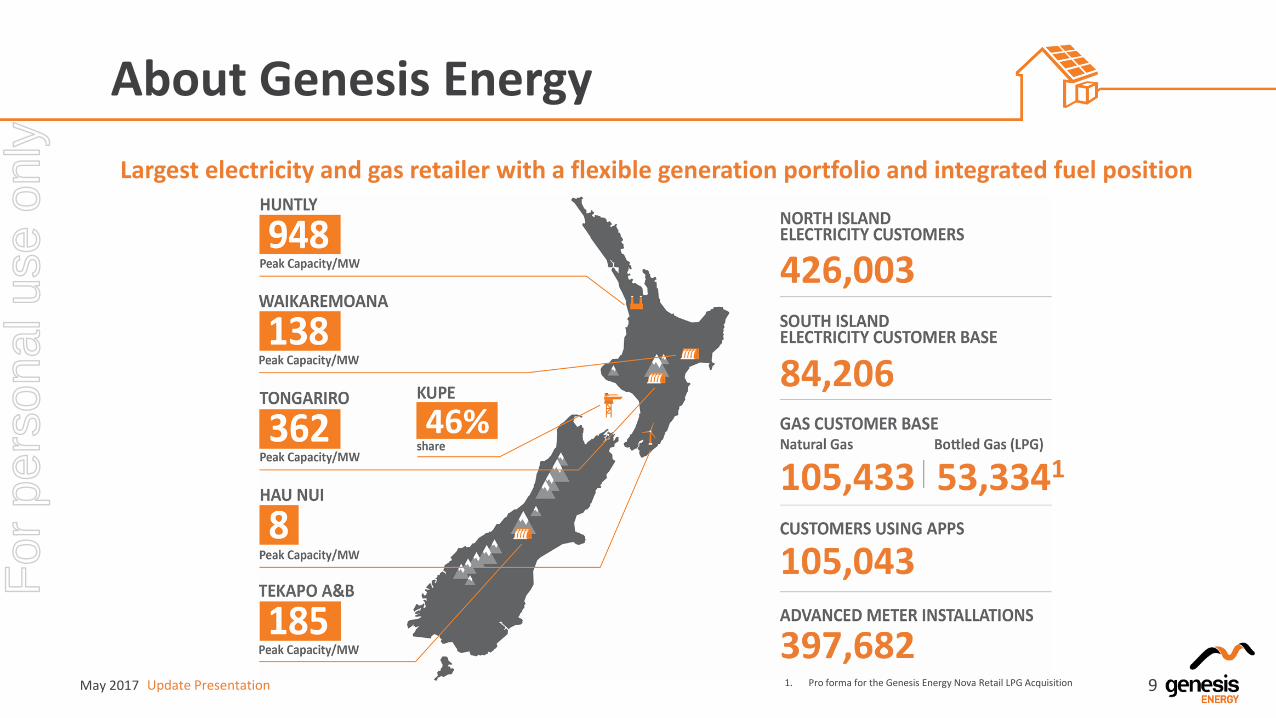

About Genesis Energy

Largest electricity and gas retailer with a flexible generation portfolio and integrated fuel position

9May 2017 Update Presentation 1. Pro forma for the Genesis Energy Nova Retail LPG Acquisition

For

per

sona

l use

onl

y

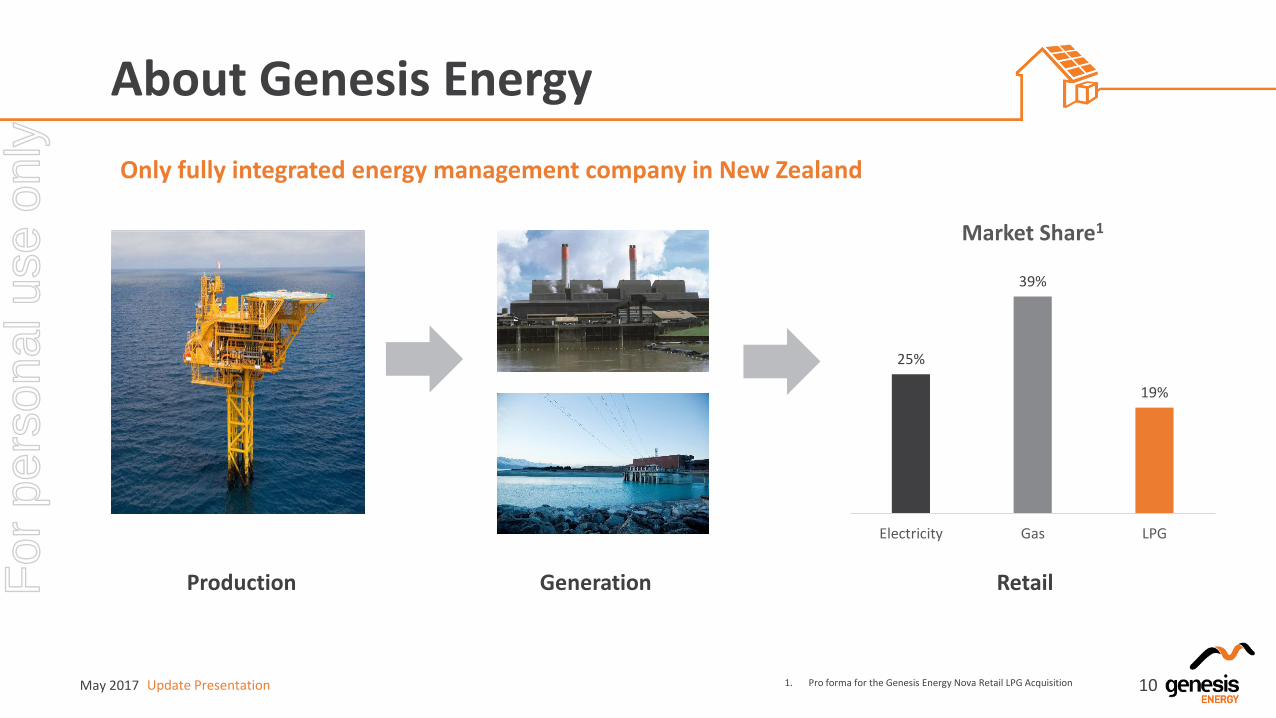

About Genesis Energy

Only fully integrated energy management company in New Zealand

10May 2017 Update Presentation

Production Generation Retail

25%

39%

19%

Electricity Gas LPG

Market Share1

1. Pro forma for the Genesis Energy Nova Retail LPG Acquisition

For

per

sona

l use

onl

y

Financial Overview

A growing dividend stream over time with a BBB+ credit rating

11May 2017 Update Presentation

50

100

150

200

250

FY13 FY14 FY15 FY16

$ MILLION

DIVIDENDS DECLARED AND FREE CASH FLOW

Dividends Free Cash Flow

0

50

100

150

200

250

300

350

FY13 FY14 FY15 FY16 FY17

$ MILLIONEBITDAF1

• $156 million of EBITDAF delivered in first half of FY17 in line with expectations and guidance

• EPS up 4% over the first half

• 8.2cps dividend declared and paid representing a 7.2% cash yield annualised

• Dividend policy to grow over time in real terms

• Committed to BBB+ credit rating

− Genesis Energy continues to target a net debt to EBITDAF ratio of 2.5x to 2.8x over time

− Recently completed successful $225 million hybrid bond raising resulting in pro forma gearing of 33%

1. FY17 based on mid point of guidance

For

per

sona

l use

onl

y

Strategy and Performance UpdateFor

per

sona

l use

onl

y

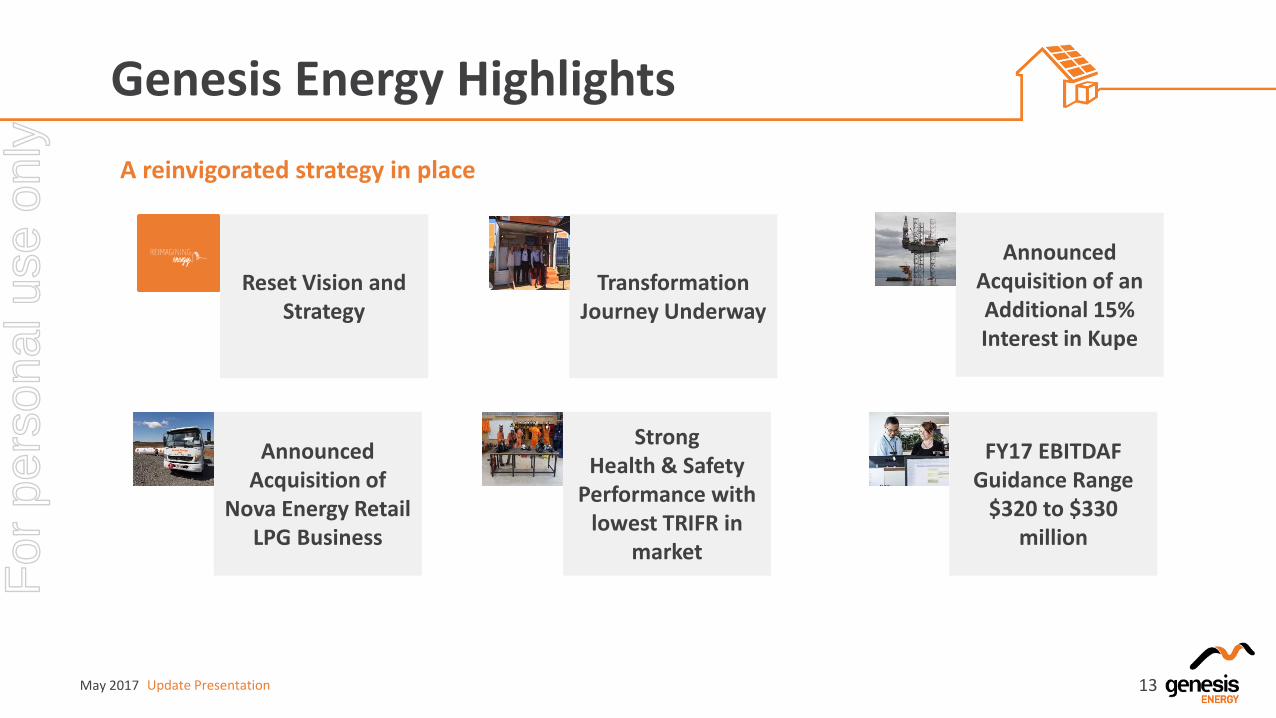

Genesis Energy Highlights

A reinvigorated strategy in place

13

Reset Vision and Strategy

Transformation Journey Underway

Announced Acquisition of an Additional 15% Interest in Kupe

Announced Acquisition of

Nova Energy Retail LPG Business

StrongHealth & Safety

Performance with lowest TRIFR in

market

FY17 EBITDAF Guidance Range

$320 to $330 million

May 2017 Update Presentation

For

per

sona

l use

onl

y

Strategy

Our plan on a page

REIMAGINING ENERGYto be customers’ first choice for energy managementV

isio

n

OPTIMISETo improve short term return

INNOVATEIn long-term value creation

INVESTFor medium term growth

Stra

tegi

c Th

em

es

Lean start up product

development

Cri

tica

l Fu

ture

cap

abili

tie

s Data driven decision making

Field force management

Scaled agile ways of working

Stra

tegi

c P

rio

riti

es

Create enduring customer

relationships

Leverage data, analysis and

insight

Maximise return from

core activities

Deploy technology to

build trust

Enhance experience with

new business models

Commercial relationship

management

Distributed asset management

Software development

Sales capabilities

Organise for best in class

strategic execution

May 2017 Update Presentation 14

For

per

sona

l use

onl

y

Strategic Themes

To Energy Management

May 2017 Update Presentation

1. Optimise generation 2. Optimise “Traditional Retail “

− Deliver best in class cost to serve− Drive loyalty into the customer base− Win and keep valuable customers

3. Seeking corporate efficiency gains

InnovateFor medium term growth

InvestIn long-term value creation

1. Investment into systems and data capabilities, including accelerated foundation investment in retail

2. Develop eco-system platforms that deliver comfort, convenience and control for customers and advantage for Genesis Energy

3. Obtain greater influence of our Kupe business4. Targeted business growth

1. Enable products and services based on new customer data flows2. Become market maker of customer comfort, convenience and control3. Maximise the value of our Bottled Gas resources4. Grow market share in Business to Business segment5. Create an empowered and accountable agile culture and way of working

OptimiseTo improve short term

return

15

For

per

sona

l use

onl

y

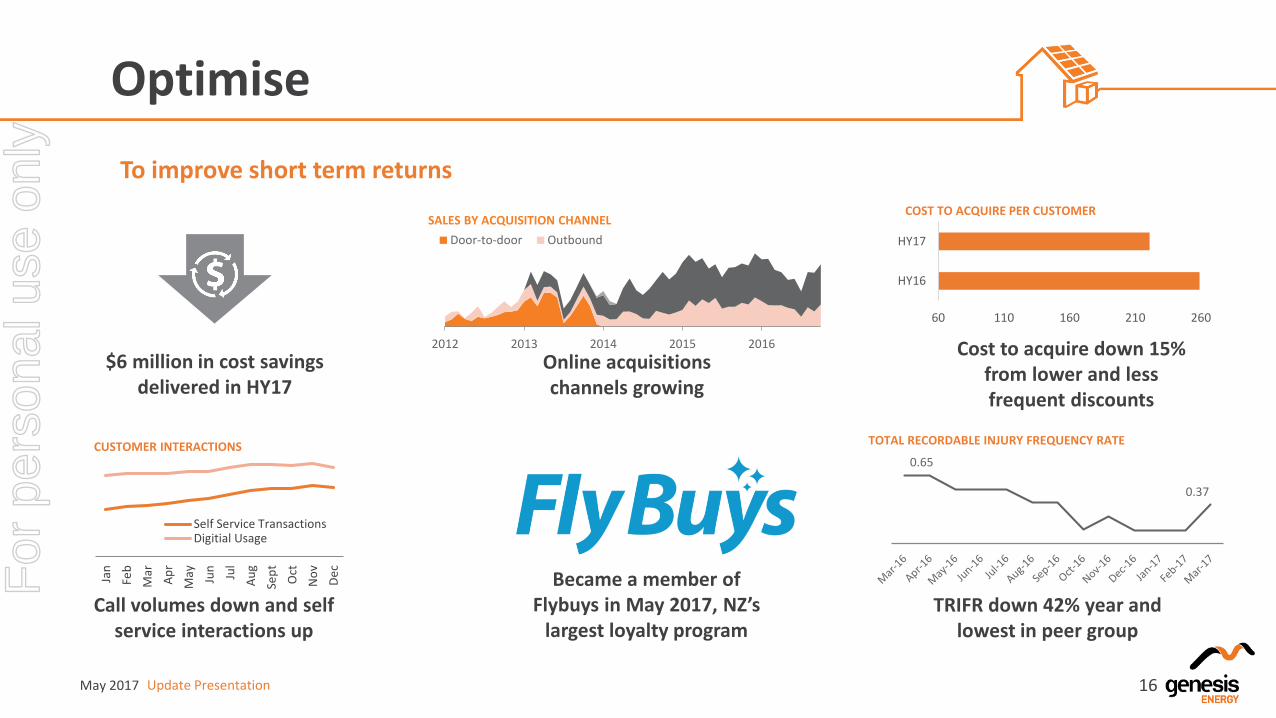

Optimise

To improve short term returns

May 2017 Update Presentation

Cost to acquire down 15% from lower and less frequent discounts

Online acquisitions channels growing

Became a member of Flybuys in May 2017, NZ’s

largest loyalty program

$6 million in cost savings delivered in HY17

TRIFR down 42% year and lowest in peer group

2012 2013 2014 2015 2016

SALES BY ACQUISITION CHANNEL

Door-to-door Outbound

60 110 160 210 260

HY16

HY17

COST TO ACQUIRE PER CUSTOMER

Call volumes down and self service interactions up

Jan

Feb

Mar

Ap

r

May Jun

Jul

Au

g

Sep

t

Oct

No

v

De

c

Self Service TransactionsDigitial Usage

CUSTOMER INTERACTIONS0.65

0.37

TOTAL RECORDABLE INJURY FREQUENCY RATE

16

For

per

sona

l use

onl

y

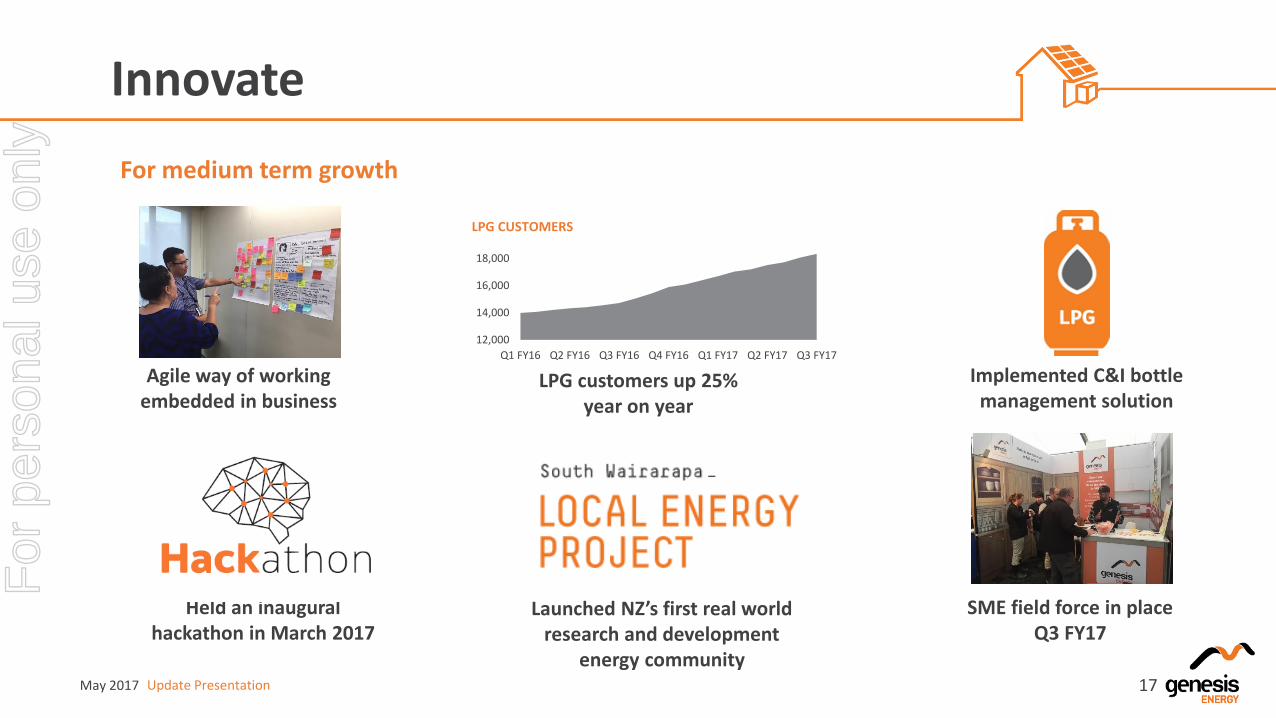

Innovate

For medium term growth

May 2017 Update Presentation

SME field force in place Q3 FY17

LPG customers up 25% year on year

Held an inaugural hackathon in March 2017

Agile way of working embedded in business

Launched NZ’s first real world research and development

energy community

12,000

14,000

16,000

18,000

Q1 FY16 Q2 FY16 Q3 FY16 Q4 FY16 Q1 FY17 Q2 FY17 Q3 FY17

LPG CUSTOMERS

Implemented C&I bottle management solution

17

For

per

sona

l use

onl

y

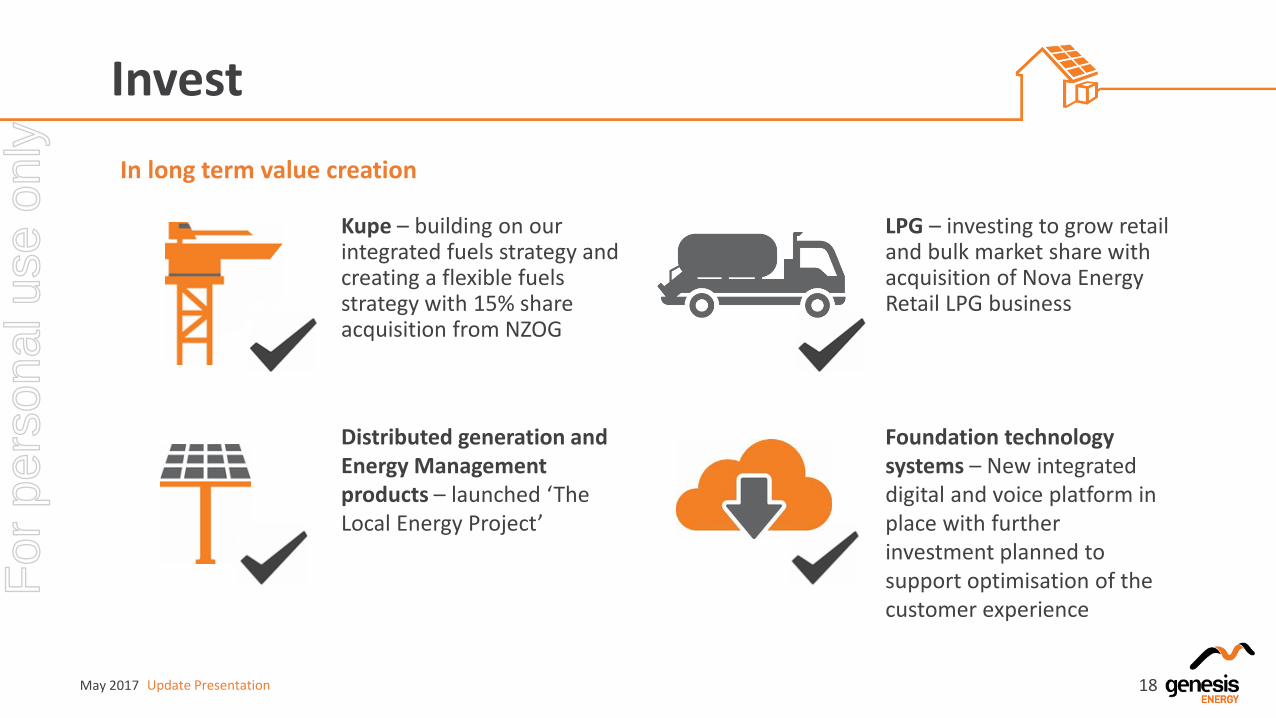

Invest

In long term value creation

Kupe – building on our integrated fuels strategy and creating a flexible fuels strategy with 15% share acquisition from NZOG

LPG – investing to grow retail and bulk market share with acquisition of Nova Energy Retail LPG business

Distributed generation and Energy Management products – launched ‘TheLocal Energy Project’

Foundation technology systems – New integrated digital and voice platform in place with further investment planned to support optimisation of the customer experience

May 2017 Update Presentation 18

For

per

sona

l use

onl

y

Acquisition of 15% stake in Kupe

May 2017 Update Presentation

Greater fuel flexibility and JV influence

1. Enhances ‘Integrated Fuels Strategy’ to create value from production through to generation and retail:

‒ Ownership of more uncontracted gas volumes

‒ Additional LPG volumes, 21% of national production, to boost position in wholesale LPG market

‒ Improved support for retail LPG growth initiative

‒ Attractively priced LPG contract for all of NZOG’s share of LPG

2. Improves level of influence and control within the JV

3. Underpins progressive dividend policy with a more diverse earnings stream

4. Strengthens medium term Balance Sheet metrics

5. Kupe field well understood by Genesis Energy and a strong performing quality asset

19

For

per

sona

l use

onl

y

Nova Energy Retail LPG Acquisition

Significant LPG distribution network covering key demand centres in New Zealand and complementary to Genesis Energy’s existing footprint

Well established customer base across residential, commercial and industrial customers

Distribution chain ideally positioned to capture ongoing growth in New Zealand’s LPG market

Experienced operating team adding to Genesis Energy’s existing capabilities

~$17 million in additional EBITDAF before integration costs and synergies

Option to acquire Nova’s interest in Liquigas

Pivotal moment in customer centric-growth strategy with $192 million acquisition

May 2017 Update Presentation 20

For

per

sona

l use

onl

y

Creating value in our LPG business in an attractive market whilst supporting the strategy of delivering a superior offering of integrated energy management solutions

Nova LPG Benefits for Genesis Energy

Becoming a LPG retailer of scale

in a growth market with

higher margins

Unlocking new customer segments

Scale capability in distribution

with associated margin benefits

Improved customer

loyalty through integrating the

customer experience

Capturing additional

margin from upstream position

Total LPG market share increases from 3% to 19%

in a market with attractive dynamics

Scale allows an improved holistic customer offering

and acceleration of innovation activities

Superior distribution network will allow

Genesis Energy to unlock further growth

Rebalancing upstream and downstream LPG

positions

Leveraging distribution network capabilities to

reduce costs

May 2017 Update Presentation 21

For

per

sona

l use

onl

y

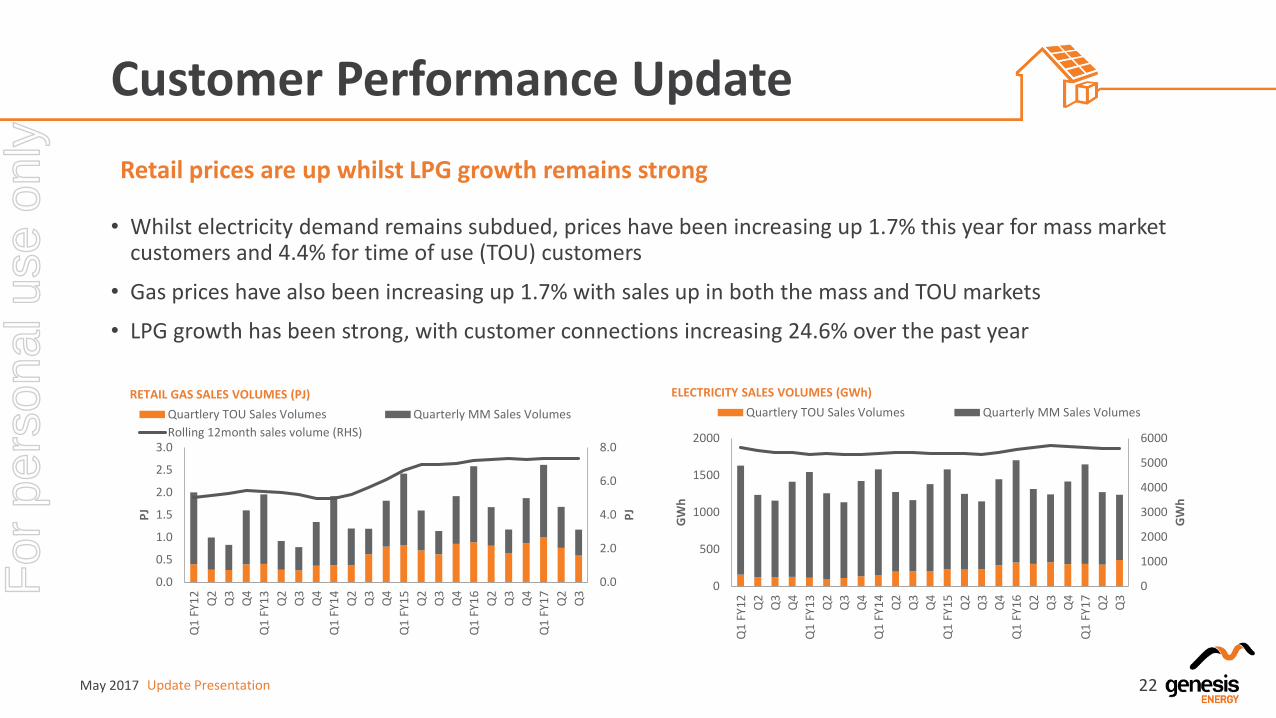

Customer Performance Update

• Whilst electricity demand remains subdued, prices have been increasing up 1.7% this year for mass market customers and 4.4% for time of use (TOU) customers

• Gas prices have also been increasing up 1.7% with sales up in both the mass and TOU markets

• LPG growth has been strong, with customer connections increasing 24.6% over the past year

Retail prices are up whilst LPG growth remains strong

May 2017 Update Presentation

0.0

2.0

4.0

6.0

8.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Q1

FY1

2

Q2

Q3

Q4

Q1

FY1

3

Q2

Q3

Q4

Q1

FY1

4

Q2

Q3

Q4

Q1

FY1

5

Q2

Q3

Q4

Q1

FY1

6

Q2

Q3

Q4

Q1

FY1

7

Q2

Q3

PJ

PJ

RETAIL GAS SALES VOLUMES (PJ)

Quartlery TOU Sales Volumes Quarterly MM Sales Volumes

Rolling 12month sales volume (RHS)

0

1000

2000

3000

4000

5000

6000

0

500

1000

1500

2000

Q1

FY1

2

Q2

Q3

Q4

Q1

FY1

3

Q2

Q3

Q4

Q1

FY1

4

Q2

Q3

Q4

Q1

FY1

5

Q2

Q3

Q4

Q1

FY1

6

Q2

Q3

Q4

Q1

FY1

7

Q2

Q3

GW

h

GW

h

ELECTRICITY SALES VOLUMES (GWh)

Quartlery TOU Sales Volumes Quarterly MM Sales Volumes

22

For

per

sona

l use

onl

y

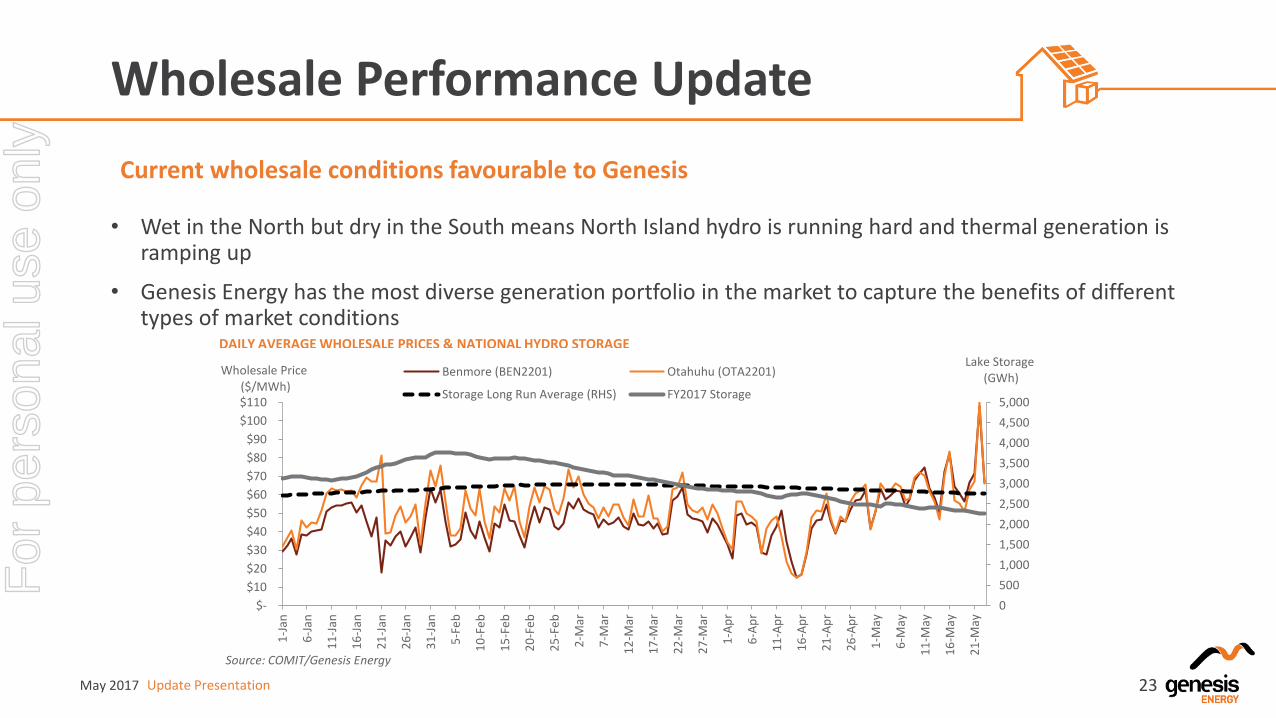

Wholesale Performance Update

• Wet in the North but dry in the South means North Island hydro is running hard and thermal generation is ramping up

• Genesis Energy has the most diverse generation portfolio in the market to capture the benefits of different types of market conditions

Current wholesale conditions favourable to Genesis

May 2017 Update Presentation

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

$-

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

1-J

an

6-J

an

11

-Jan

16

-Jan

21

-Jan

26

-Jan

31

-Jan

5-F

eb

10

-Fe

b

15

-Fe

b

20

-Fe

b

25

-Fe

b

2-M

ar

7-M

ar

12

-Mar

17

-Mar

22

-Mar

27

-Mar

1-A

pr

6-A

pr

11

-Ap

r

16

-Ap

r

21

-Ap

r

26

-Ap

r

1-M

ay

6-M

ay

11

-May

16

-May

21

-May

Lake Storage(GWh)

Wholesale Price($/MWh)

Benmore (BEN2201) Otahuhu (OTA2201)

Storage Long Run Average (RHS) FY2017 Storage

Source: COMIT/Genesis Energy

DAILY AVERAGE WHOLESALE PRICES & NATIONAL HYDRO STORAGE

23

For

per

sona

l use

onl

y

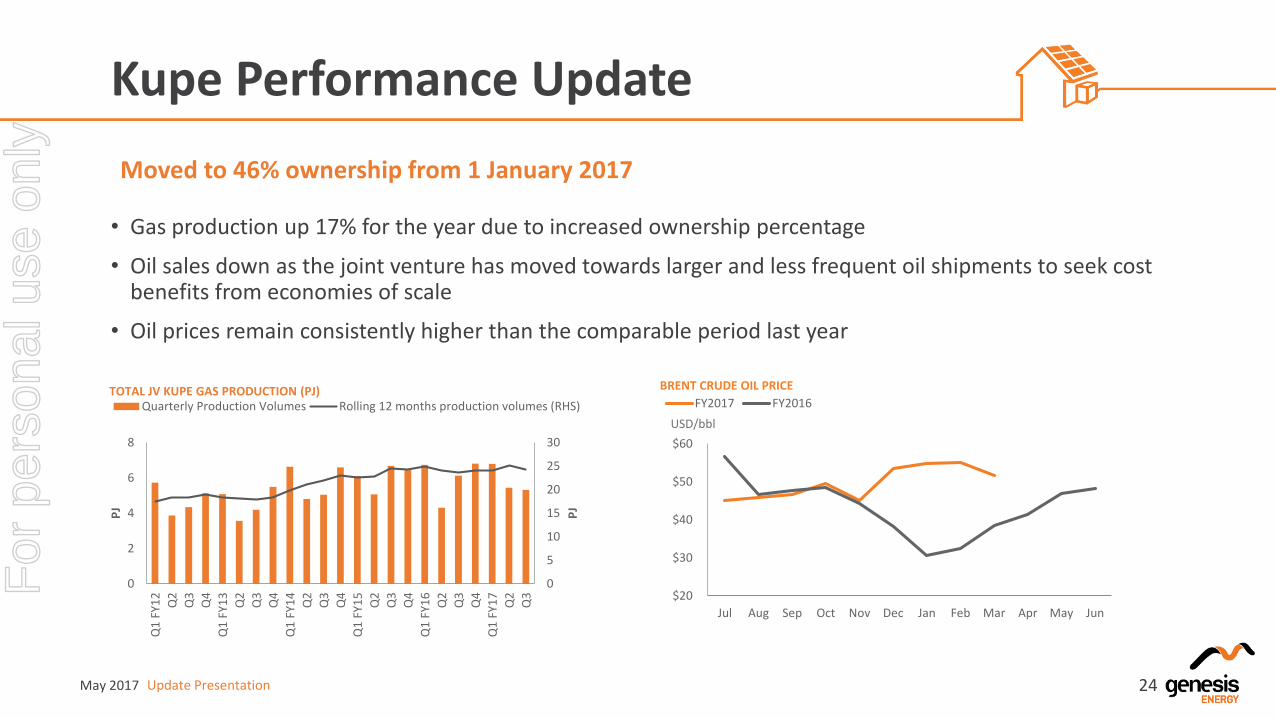

Kupe Performance Update

• Gas production up 17% for the year due to increased ownership percentage

• Oil sales down as the joint venture has moved towards larger and less frequent oil shipments to seek cost benefits from economies of scale

• Oil prices remain consistently higher than the comparable period last year

Moved to 46% ownership from 1 January 2017

May 2017 Update Presentation

$20

$30

$40

$50

$60

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun

USD/bbl

BRENT CRUDE OIL PRICE

FY2017 FY2016

0

5

10

15

20

25

30

0

2

4

6

8

Q1

FY1

2

Q2

Q3

Q4

Q1

FY1

3

Q2

Q3

Q4

Q1

FY1

4

Q2

Q3

Q4

Q1

FY1

5

Q2

Q3

Q4

Q1

FY1

6

Q2

Q3

Q4

Q1

FY1

7

Q2

Q3

PJ

PJ

TOTAL JV KUPE GAS PRODUCTION (PJ)Quarterly Production Volumes Rolling 12 months production volumes (RHS)

24

For

per

sona

l use

onl

y

Outlook

For

per

sona

l use

onl

y

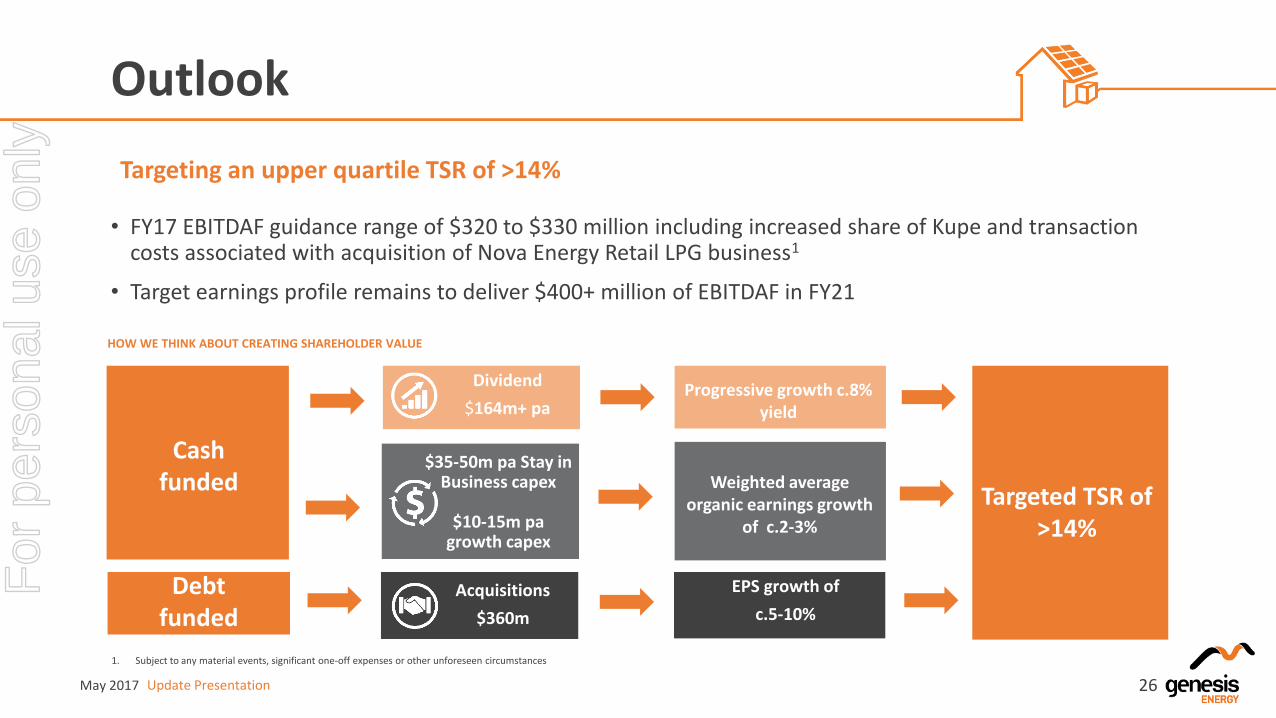

Outlook

• FY17 EBITDAF guidance range of $320 to $330 million including increased share of Kupe and transaction costs associated with acquisition of Nova Energy Retail LPG business1

• Target earnings profile remains to deliver $400+ million of EBITDAF in FY21

Targeting an upper quartile TSR of >14%

1. Subject to any material events, significant one-off expenses or other unforeseen circumstances

May 2017 Update Presentation

Acquisitions

$360m

Dividend

$164m+ pa

$35-50m pa Stay in Business capex

$10-15m pa growth capex

EPS growth of

c.5-10%

Progressive growth c.8% yield

Weighted average organic earnings growth

of c.2-3%

Targeted TSR of >14%

Debt funded

Cash funded

HOW WE THINK ABOUT CREATING SHAREHOLDER VALUE

26

For

per

sona

l use

onl

y

Why Genesis Energy?

Yield plus growth strategy in motion as Genesis Energy transforms

Customer Centric

Generation Flexibility

Integrated Fuel Position

Leading Market Disruption

• Brand strength and largest customer base provides strong platform for growth

• Obsession with customer experience will drive increased loyalty and lower costs

• Leveraging technology to improve the energy experience for customers

• Unique position to flex thermal, renewable and on market activities underpins earnings profile

• Closer integration of maintenance, operations and wholesale activities will optimise asset base

• Large retail market share and long retail South Island position reduces price risks of Tiwai closure

• Flexibility over fuel supply to support generation and retail needs

• Upside opportunity from accelerated production and priority access to uncontracted gas

• Access to increased LPG production provides strong alignment with growth aspirations

• Defining new approaches to energy management

• Accelerating change through agile ways of working

• Embracing unpredictability to develop resilience in rapidly evolving market

May 2017 Update Presentation 27

For

per

sona

l use

onl

y

Thank You

For

per

sona

l use

onl

y