Embed Size (px)

Citation preview

Global Research

August 2008

Sector

GCC Telecom Sector

GCC

Ringing all the way ...

Global Investment House KSCCSharq, Global TowerP.O. Box 28807 Safat13149 KuwaitTel: (965) 295 1000Fax: (965) 295 1005E-mail: [email protected]://www.globalinv.net

Global Investment House stock market indices can be accessedfrom the Bloomberg page GLOHand from Reuters Page GLOB

Omar M. El-Quqa, CFAExecutive Vice [email protected] No:(965) 2951110

Faisal Hasan, CFAHead of [email protected] No:(965) 295 1270

Chandresh BhattAssistant Vice [email protected] No:(965) 295 1282

Abeer GoudaSenior Financial [email protected] No:(965) 295 1272

Vinod ShenoyFinancial [email protected] No:(965) 295 1274

Table of Contents

Investment Summary ---------------------------------------------------------------------------------1

World Telecom Sector Overview -------------------------------------------------------------------5

GCC Telecom Sector Overview --------------------------------------------------------------------7

Fixed Line Services --------------------------------------------------------------------------------7 Cellular Services ------------------------------------------------------------------------------------8

Broadband Services ------------------------------------------------------------------------------ 11

Country-wise Telecom Profile in GCC --------------------------------------------------------- 14

Kuwait --------------------------------------------------------------------------------------------- 14 Qatar ------------------------------------------------------------------------------------------------ 15

Saudi Arabia--------------------------------------------------------------------------------------- 16

UAE ------------------------------------------------------------------------------------------------ 17 Oman ----------------------------------------------------------------------------------------------- 18

Bahrain --------------------------------------------------------------------------------------------- 19

Player Profiles ---------------------------------------------------------------------------------------- 20

Mobile Telecommunications Company (Zain) ----------------------------------------------- 21 National Mobile Telecommunications Company (Wataniya) ------------------------------ 33

Saudi Telecom (STC) ---------------------------------------------------------------------------- 43

Etihad Etisalat Company (Mobily) ------------------------------------------------------------- 58 Emirates Telecommunications Corporation (Etisalat) --------------------------------------- 71

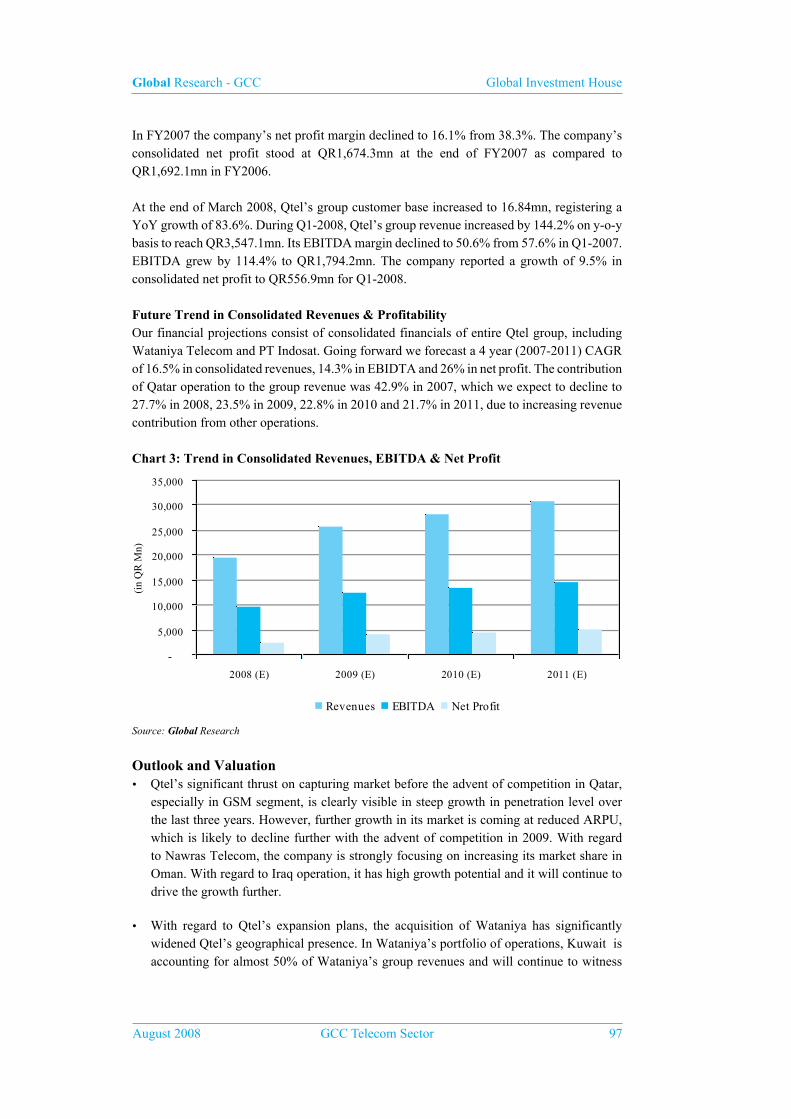

Qatar Telecom (Qtel) ---------------------------------------------------------------------------- 92

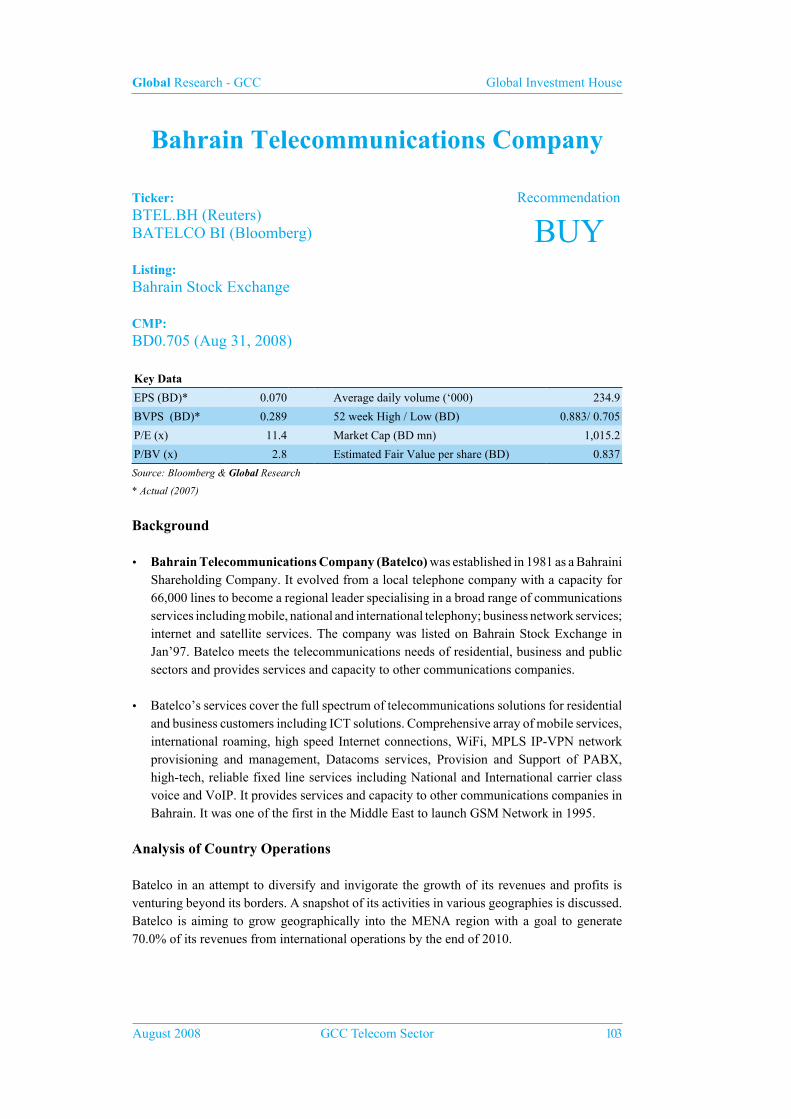

Bahrain Telecommunications Company (Batelco) -----------------------------------------103

Oman Telecommunications Company (OTEL) ---------------------------------------------116

Global Research - GCC Global Investment House

August 2008 GCC Telecom Sector 1

Investment Summary

• In the recent years the GCC telecom players are on an expansion spree following measures from Saudi Arabia, Bahrain, Oman, and UAE to allow additional service providers in the respective countries. This should result in inducing higher competition and further drop in ARPUs in the region and resultant contracting profitability of the players. The service providers should aim to increase their market shares by providing differentiated value added services and providing content based services (like mobile video streaming) to enhance the ARPUs.

• The GCC region registered a decline of 6.9% in fixed line subscribers from 5.8mn subscribers in 2006 to 5.4mn subscribers in 2007 on account of increasing shift of customer base to the more convenient mobile voice services.

• Increasing disposable income and convenience of use is encouraging the cellular penetration in the region. Other important contributing factor to the increased cellular penetration is the relaxation in telecom regulations allowing second or third player in each country apart from the incumbent local carriers (usually the first state run telco service provider in each country). The GCC region registered a 5 year (2002-07) growth in cellular subscribers at a CAGR of 37.6 %. The MENA region has seen the highest worldwide 5 year (2002-07) growth in cellular subscribers at a CAGR of 52.9% against the worldwide increase of 23.3%. With the country wise cellular markets reaching or crossing the 100% penetration levels within the GCC region, all the six member countries registered double digits CAGR during the 5 year (2002-07) period.

• In 2007, Asia and MENA region were the major growth contributors with YoY growth rates of 36.8% and 33.9% respectively. UAE topped the list of high growth contribution with a YoY growth rate of 34.6% with its internet user base increasing from 1.7mn in 2006 to 2.3mn in 2007. The next highest contributor was Saudi Arabia that reported a 31.9% YoY increase in the internet users’ base from 4.7mn in 2006 to 6.2mn in 2007. The high proportion of youth in the demographics, with 55% to 65% of the total population under the age of 30 years is driving the internet usage in the GCC region.

• The higher rate of internet penetration and improved infrastructure services in terms of shift from Dial up to cable is helping increase the broadband subscriber base in the GCC region. The analysis of 5 year (2002-07) CAGR in broadband subscribers worldwide indicates that the GCC region is amongst the top three growth regions in the world. The worldwide broadband subscriber base increased at a 5 year (2002-07) CAGR of 38.9%.

Companies under coverage

As a part of the GCC Telecom coverage we are covering Qatar Telecom (Qtel), Mobile Telecommunications Company (Zain), National Mobile Telecommunications Company (Wataniya), Saudi Telecom (STC), Etihad Etisalat Company (Mobily), Emirates Telecommunications Corporation (Etisalat), Oman Telecommunications Company (OTEL) and Bahrain Telecommunications Company (Batelco) in this report.

Global Research - GCC Global Investment House

2 GCC Telecom Sector August 2008

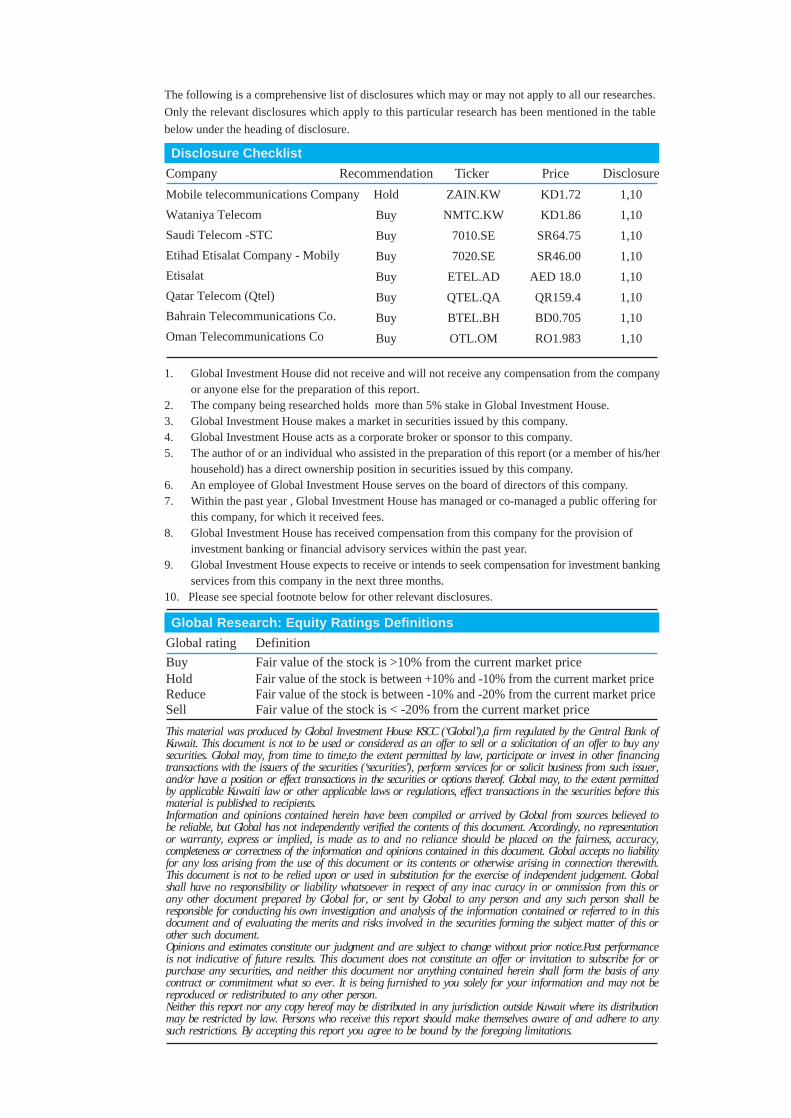

• Mobile Telecommunications Company (Zain) was established in 1983 in Kuwait as the region’s first mobile operator. Since 2003, it has grown significantly becoming the 4th largest telecommunications company in the world in terms of geographic presence with a footprint in 22 countries spread across the Middle East and Africa providing mobile voice and data services to over 50.74mn active customers (as at 30 June 2008). In August 2008 the company is raising its equity capital through rights issue. The company’s paid up capital will be increased by 75% through rights. We have used Sum-Of-The-Parts (SOTP) valuation method for company’s operations in different countries. Based on consolidation of the individual country operations, our SOTP valuation estimates the fair value of Zain’s stock at KD1.77, which is 2.7% higher than the current market price of the stock of KD1.72 per share (as at Aug. 31, 2008). We, therefore, reiterate our “HOLD” recommendation on the stock.

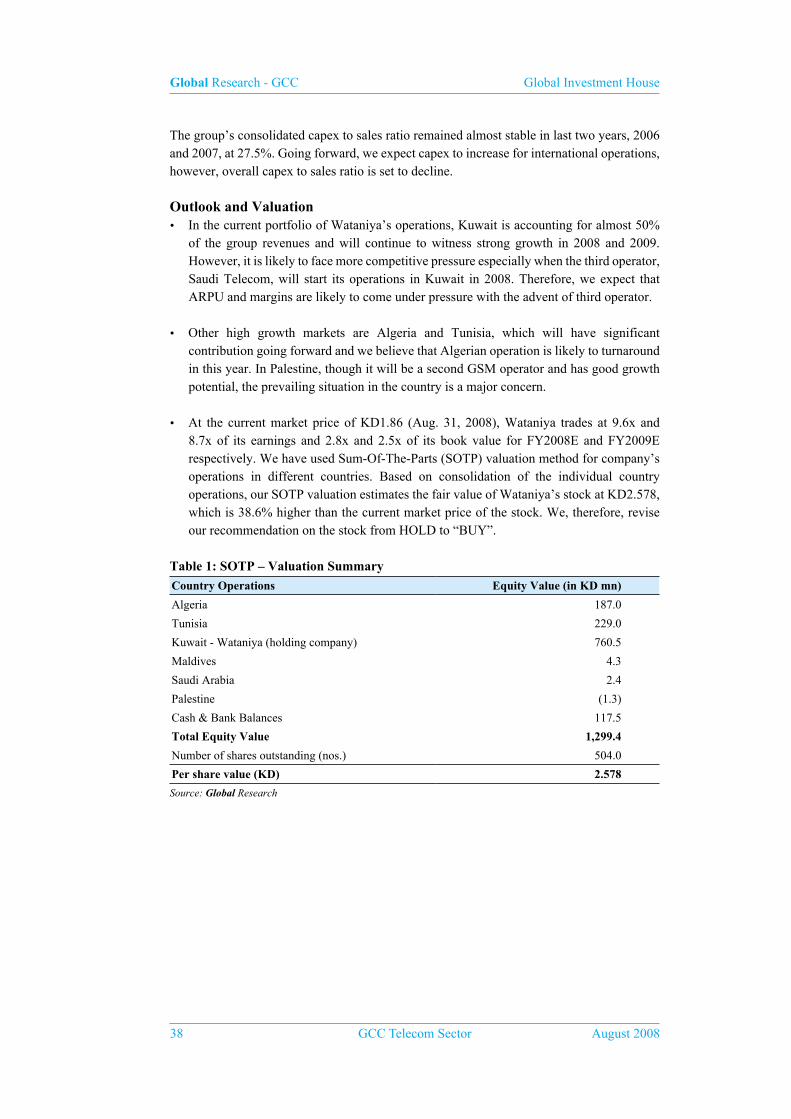

• National Mobile Telecommunications Company (Wataniya) has grown rapidly through acquisitions in the MENA region and Asia. Apart from Kuwait, the company has operations in Maldives (100% stake), Saudi Arabia (55.61% stake), Tunisia (50% stake), Algeria (71% stake) and in 2007 it got a license to launch second mobile services in Palestine (57% stake). In March 2007, Qatar Telecom (Qtel) acquired 51% of Wataniya Telecom shares from Kuwait Projects Company Holding KSC (KIPCO) group for a total cash consideration of US$3.8bn. We have used Sum-Of-The-Parts (SOTP) valuation method for company’s operations in different countries. Based on consolidation of the individual country operations, our SOTP valuation estimates the fair value of Wataniya’s stock at KD2.58, which is 38.6% higher than the current market price of KD1.86 (as at Aug. 31, 2008). We, therefore, revise our recommendation on the stock from HOLD to “BUY”.

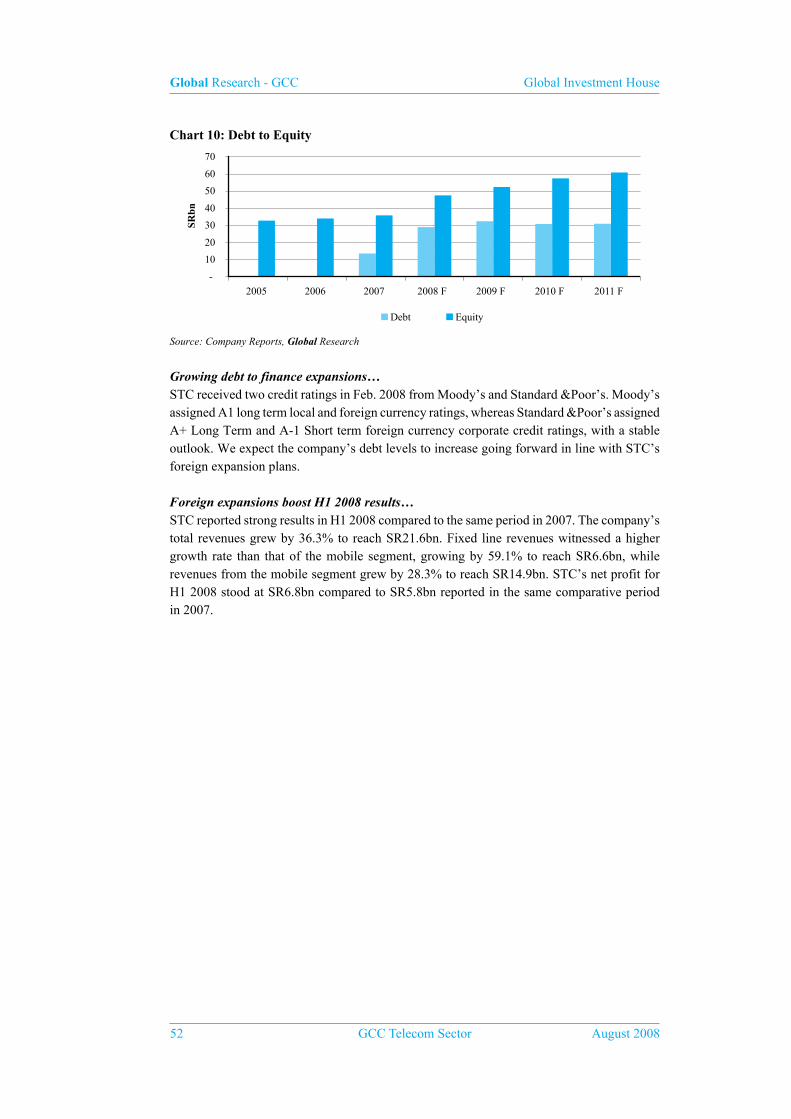

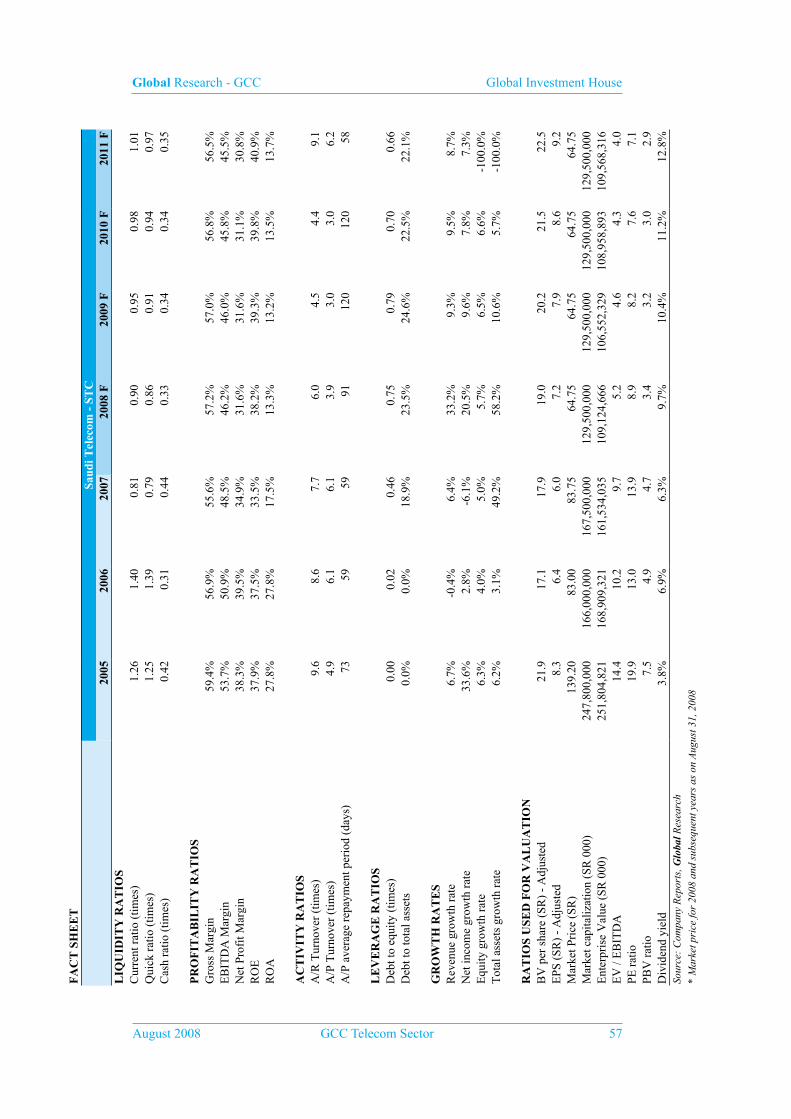

• Saudi Telecom (STC), was the sole provider of telecommunication services in Saudi Arabia until its monopoly in the mobile market ended when the second mobile license was granted in 2004 to Etihad Etisalat Company (Mobily). In March 2007, a consortium led by Zain of Kuwait won the third mobile, and launched its services in 2008. In April 2007, three fixed line licenses were granted in Saudi, ending STC’s monopoly over fixed lines. As a result of increasing competition, the company started expanding outside its home market beginning with the Maxis deal which gave STC foothold in Malaysia, India, and Indonesia, Later, STC won the bid for a 26% stake in Kuwait’s third mobile service operator. Finally, STC acquired a 35% stake in Oger Telecom, which gave STC presence in Turkey and South Africa. We expect STC’s revenues to grow by a CAGR of 9.2% during our forecast period (2008-2011). Our DCF valuation estimates the fair value of STC’s stock at SR78.75, which is 21.6% higher than the current market price of the stock. We therefore reiterate our “BUY” recommendation for STC.

• Etihad Etisalat Company (Mobily), is Saudi’s second mobile operator. Mobily launched its services in May 2005. Within three years of operations, the company managed to grab a market share of 41% by the end of 2007, with 11.1mn subscribers. Mobily has been targeting the data and internet segment aggressively. In 2007, the company acquired a 99.9% stake of the local data provider Bayanat Al-Oula, and set up Mobily InfoTech, a fully owned subsidiary in India, which will provide information technology and consulting services. In addition, Mobily got the approval to acquire 96% of Zagel International Communication Network Company which is specialized in providing internet services in Saudi Arabia. We believe that Mobily’s latest acquisitions will strengthen its position

Global Research - GCC Global Investment House

August 2008 GCC Telecom Sector 3

in the wireless broadband internet segment. Our DCF valuation estimates the fair value of Mobily’s stock at SR68.84, which is 49.6% higher than the current market price of the stock. We therefore reiterate our “BUY” recommendation for Mobily.

• Emirates Telecommunications Corporation (Etisalat) was the sole provider of telecommunication in the UAE until its monopoly was broken when Emirates Integrated Telecommunications Company (EITC) know as “DU” won the second license for fixed line, mobile, and internet services in 2005. The group is present in 15 countries in Africa and Asia. We expect the share of international operations of the group’s top line results to increase from 6% in 2007 to 11% in 2011. We have used Sum-Of-The Parts (SOTP) valuation method for the company’s operations in different countries. Based on the consolidation of the individual company operations, our SOTP valuation estimates the fair value of Etisalat’s stock at AED27, which is 50% higher than the current market price of the stock. We therefore initiate our coverage for Etisalat with a “BUY” recommendation.

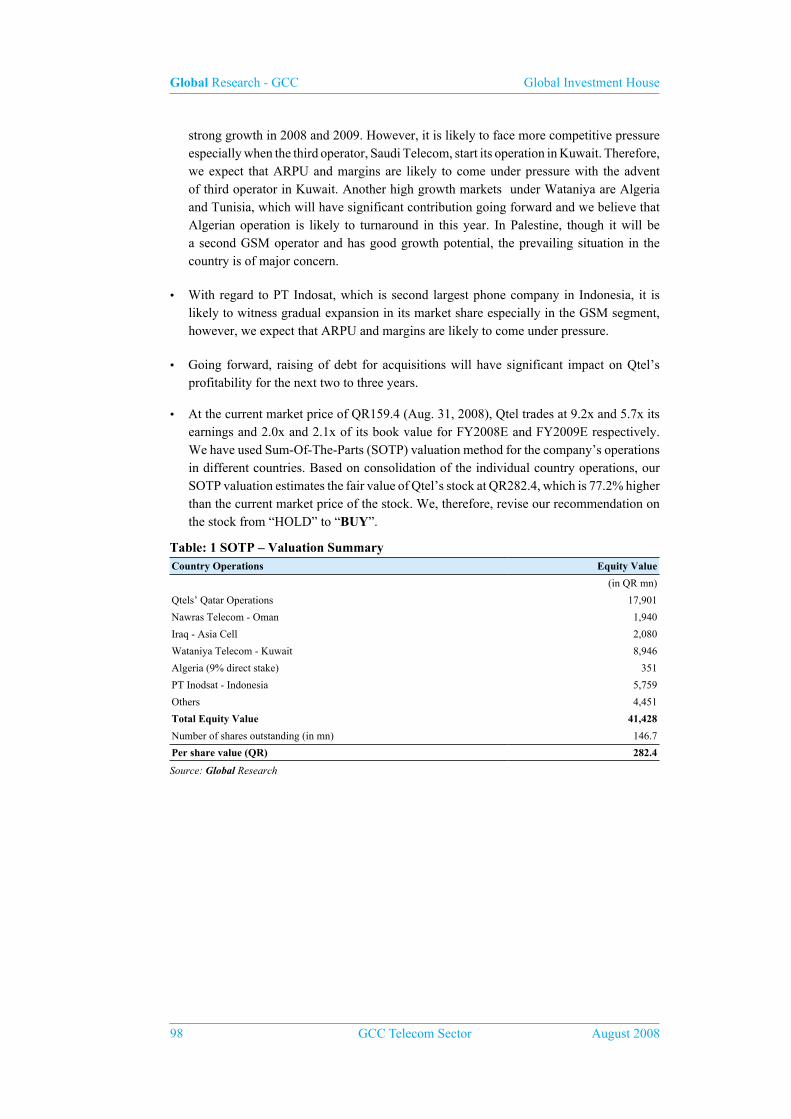

• Qatar Telecom (Qtel) provides domestic and international telecommunication services in Qatar and wireless telecommunication services in the Asia and MENA region through its subsidiaries. The year 2007 was a transformative one for Qtel – characterized by many partnerships and acquisitions in the MENA and Asia regions. These activities have broadened Qtel’s geographic presence to 16 countries (2006 – 2 countries) with the ability to reach over 560mn people. In 2007, the Qtel group’s subscriber base has grown from 1.72mn in 2006 to over 16mn – an increase of over 850%. In March 2007, Qatar Telecom (Qtel) acquired 51% of Wataniya Telecom shares from Kuwait Projects Company Holding KSC (KIPCO) group. In June 2008, Qtel acquired a 40.8% stake in PT Indosat Tbk, Indonesia’s second-largest phone company, from its subsidiary Asia Mobile Holding Pte. Ltd. We have used Sum-Of-The-Parts (SOTP) valuation method for the company’s operations in different countries. Based on consolidation of the individual country operations, our SOTP valuation estimates the fair value of Qtel’s stock at QR282.4, which is 77.2% higher than the current market price of QR159.4er share (as at Aug. 31, 2008). We, therefore, revise our recommendation on the stock from “HOLD” to “BUY”.

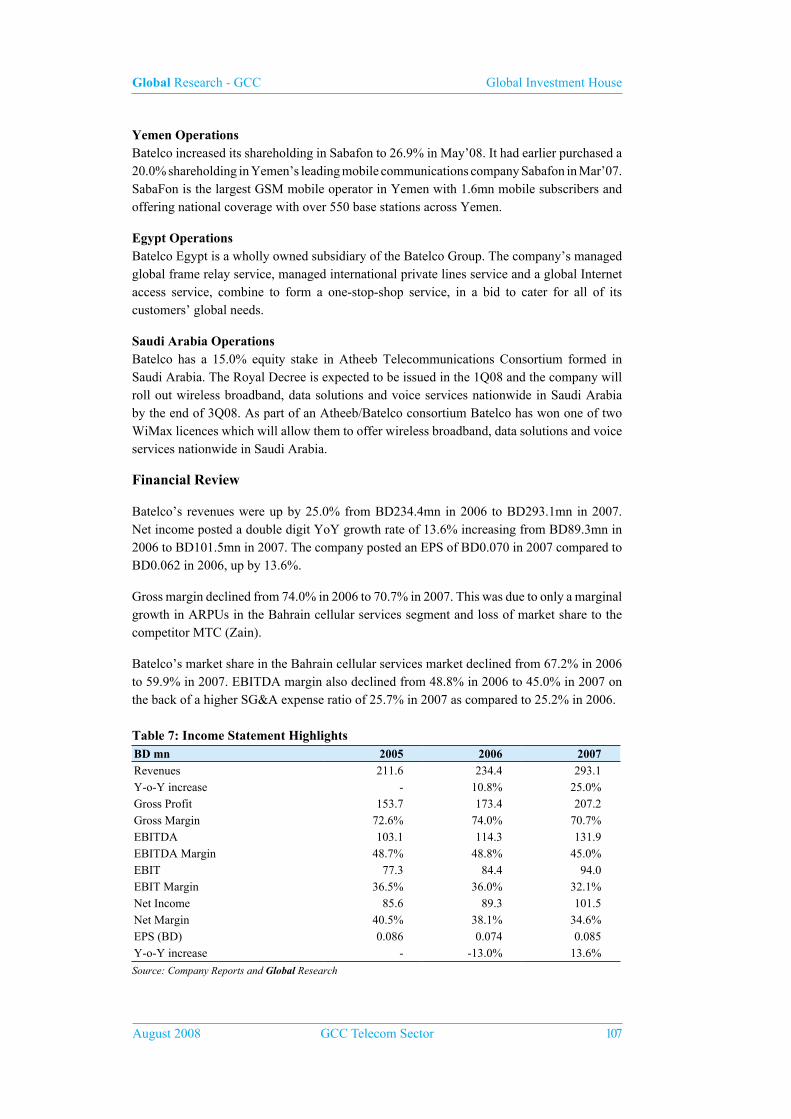

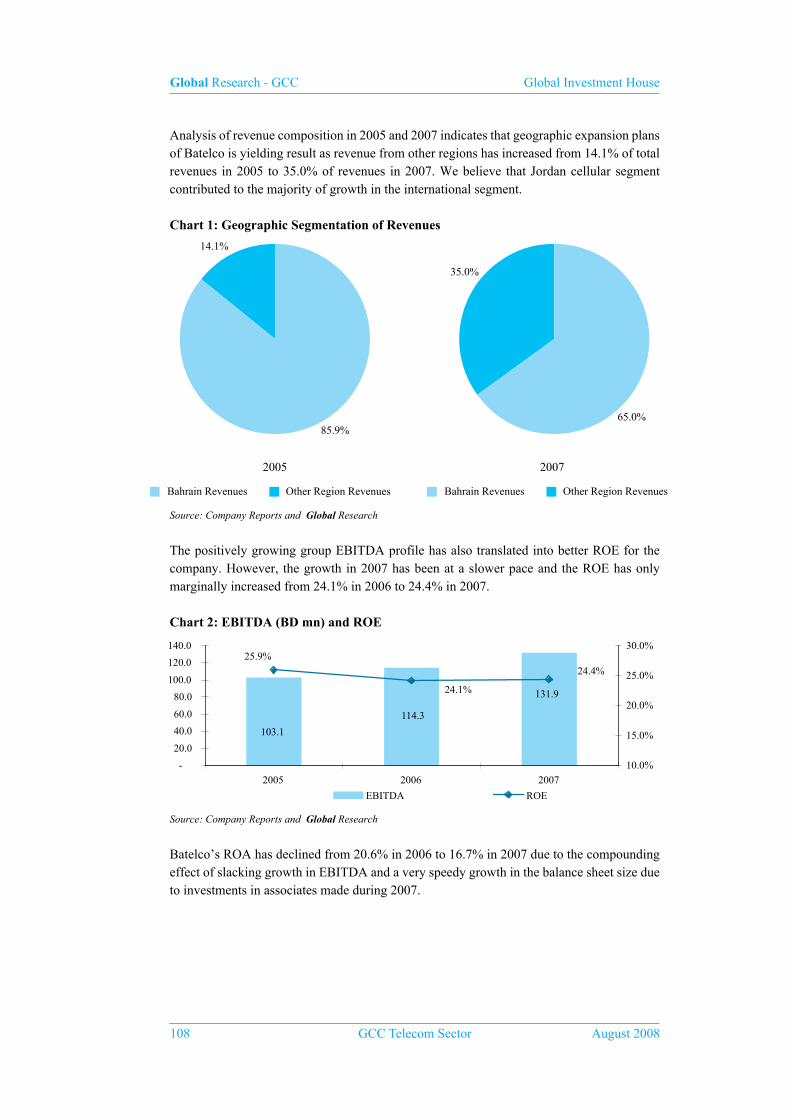

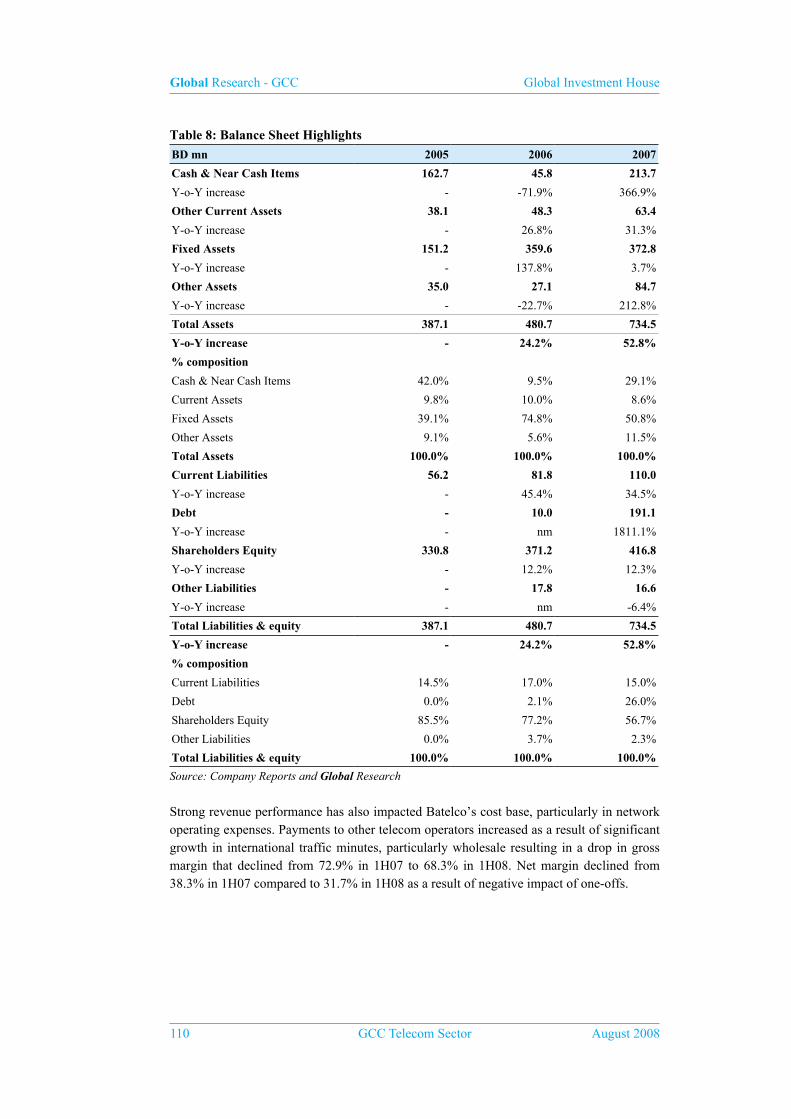

• Bahrain Telecommunications Company (Batelco) is the incumbent telecom operator in Bahrain. The subsidiaries/associates of Batelco are Umniah (Jordan), Qualitynet (Kuwait), Sabafon (Yemen), Batelco Egypt and Atheeb (Saudi Arabia). Batelco posted a double digit YoY net income growth rate of 13.6% increasing from BD89.3mn in 2006 to BD101.5mn in 2007. Batelco has adopted the right strategy of exploring and investing in low penetrated markets both in cellular and broadband space. Its aim to grow geographically into the MENA region with a goal to generate 70.0% of its revenues from international operations by the end of 2010 seems to be achievable given the success they have achieved so far in their investments. The estimated fair value for Batelco works out to BD0.837 per share which offers and upside of 18.7% on the market price of BD0.705 per share (as at Aug. 31, 2008). Hence, we initiate on the stock with a “BUY” recommendation.

• Oman Telecommunications Company (OTEL) is the incumbent telecom service provider in Oman. Nawras is a competitor of OTEL in the cellular segment. OTEL

Global Research - GCC Global Investment House

4 GCC Telecom Sector August 2008

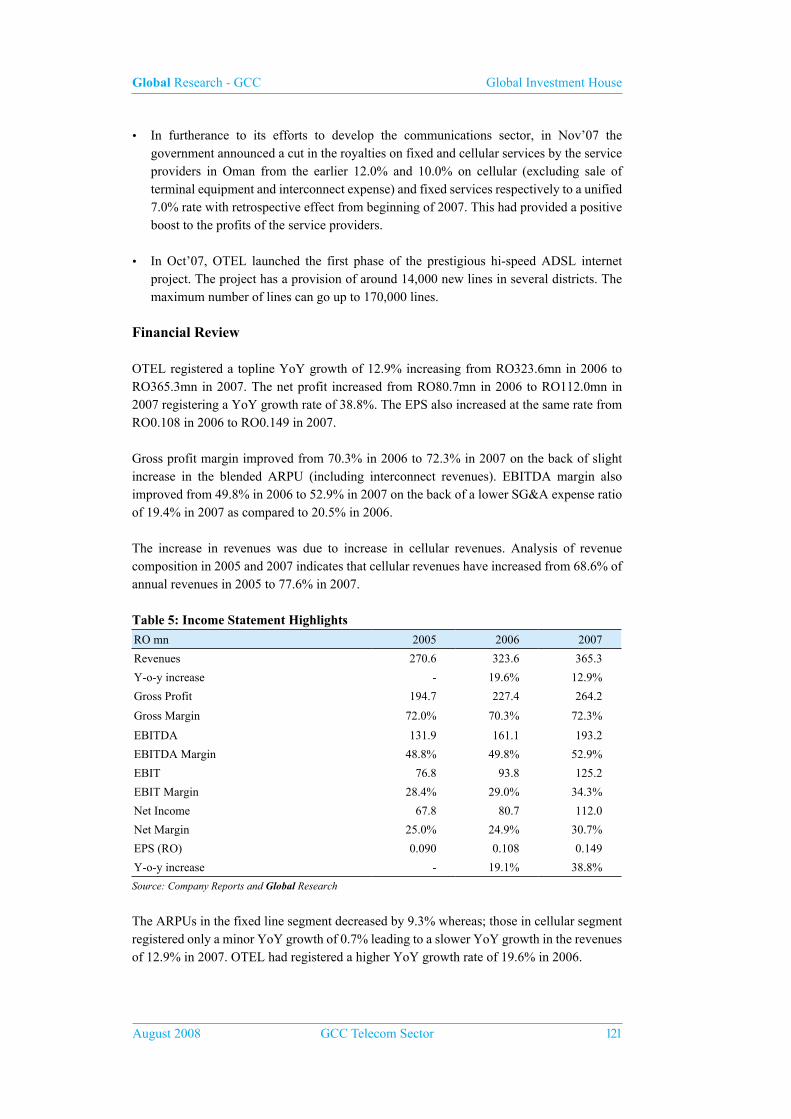

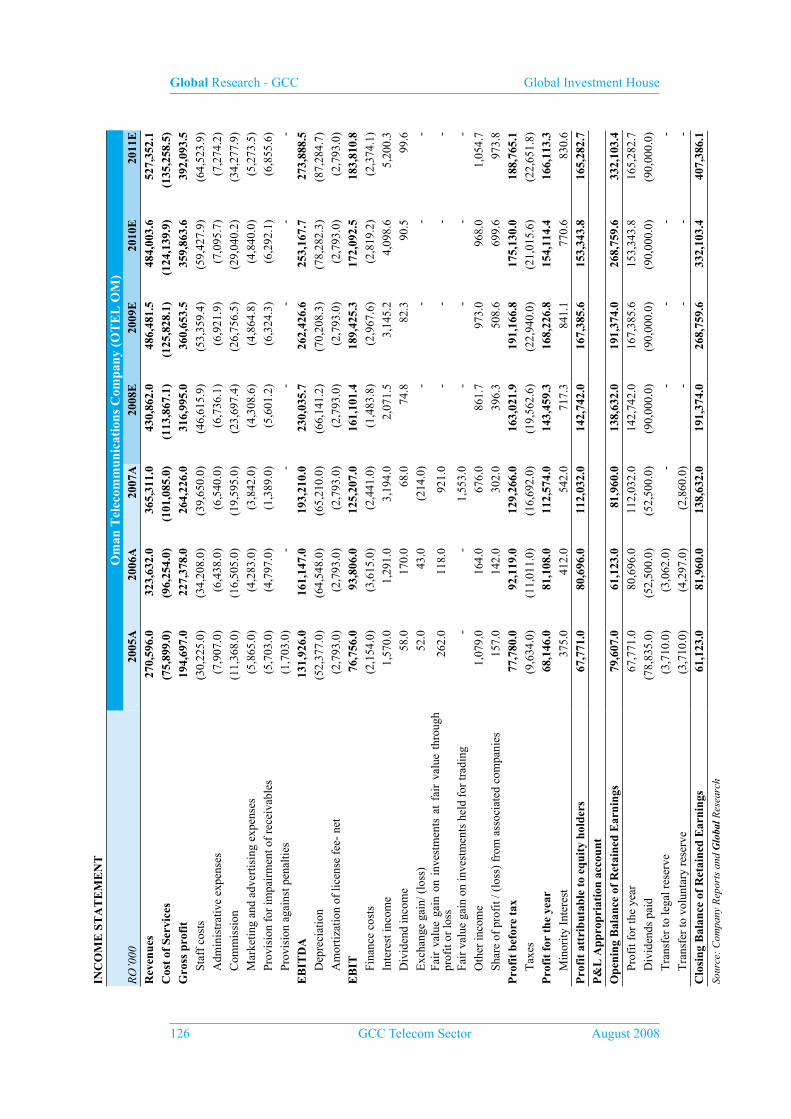

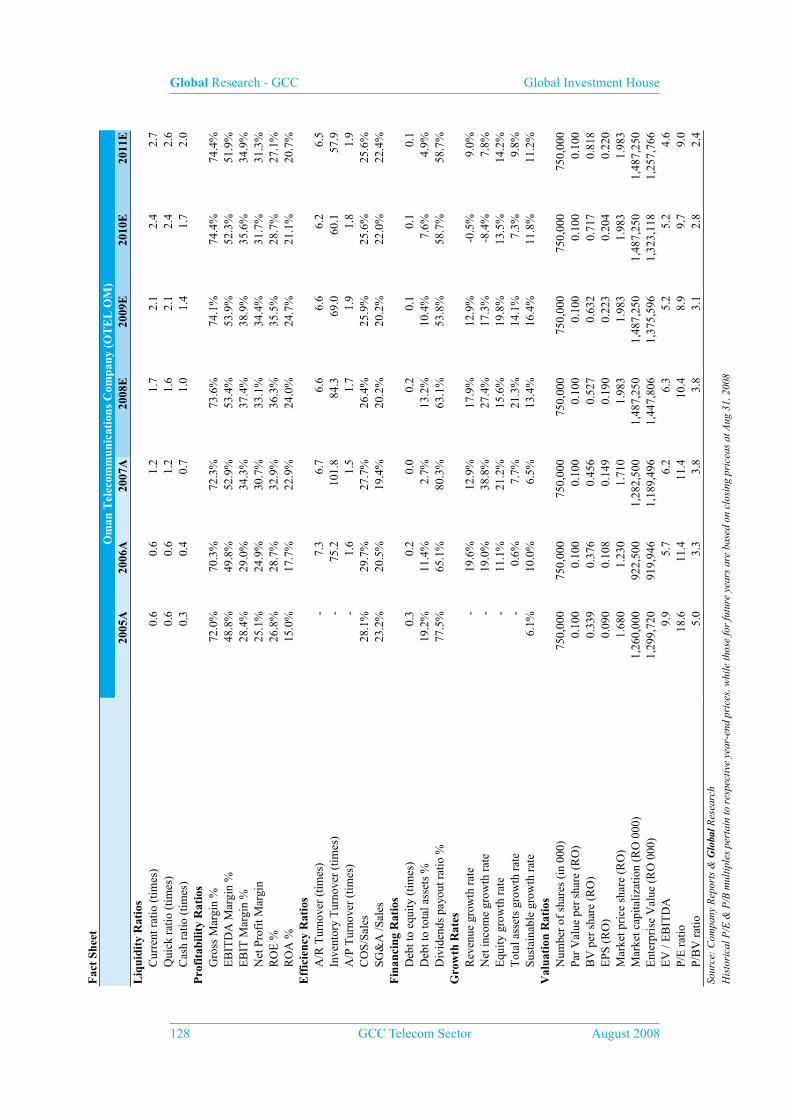

registered a topline YoY growth of 12.9% increasing from RO323.6mn in 2006 to RO365.3mn in 2007. The net profit increased from RO80.7mn in 2006 to RO112.0mn in 2007 registering a YoY growth rate of 38.8%. We believe that the Omani telecom sector is to see unprecedented competition in the coming years attracting cellular players now that TRA is considering a third cellular player. OTEL should continue to retain its market share in this competitive scenario by enhancing revenue growth in Fixed and Mobile segment, while retaining valued customers through loyalty programs. The estimated fair value for OTEL works out to RO2.339 per share which offers and upside of 18.0% on the market price of RO1.983 per share (as at Aug 31, 2008). Hence, we initiate on the stock with a “BUY” recommendation.

Table 1 : “Global” Valuation Matrix

Company Local Currency

Price* Target Reco. Upside / (Downside)

Market Cap.

(US$ bn)

BV** EPS** P/BV (x) P/E (x) EV/EBITDA (x)

M Cap./Sales (x)

2008F 2009F 2008F 2009F 2008F 2009F 2008F 2009F 2008F 2009F 2008 F 2009 F

Zain KD 1.72 1.77 HOLD 2.7% 27.3 0.708 0.751 0.080 0.104 2.4 2.3 21.6 16.6 10.6 9.0 3.8 3.2

Wataniya KD 1.86 2.58 BUY 38.6% 3.5 0.674 0.748 0.193 0.215 2.8 2.5 9.6 8.7 5.3 4.7 1.9 1.7

STC SR 64.75 78.75 BUY 21.6% 34.5 19 20.2 7.200 7.900 3.4 3.2 8.9 8.2 5.2 4.6 2.8 2.6

Mobily SR 46.00 68.84 BUY 49.6% 6.1 15.6 19.7 3.800 4.600 3.0 2.3 12.2 10.1 8.4 7.1 2.2 2.0

Etisalat AED 18.00 27.01 BUY 50.1% 29.3 5.3 6.16 1.660 1.670 3.4 2.9 10.8 10.8 5.4 4.7 3.9 3.4

Qtel QR 159.4 282.4 BUY 77.2% 6.4 78.8 74.2 17.4 27.9 2.0 2.1 9.2 5.7 5.1 3.7 1.2 0.9

Batelco BD 0.705 0.837 BUY 18.7% 2.7 0.345 0.402 0.072 0.076 2.0 1.8 9.8 9.2 7.1 6.3 3.0 2.7

Omantel RO 1.983 2.339 BUY 18.0% 3.9 0.527 0.632 0.190 0.223 3.8 3.1 10.4 8.9 6.3 5.2 3.5 3.1

* Market Price as of August 31, 2008

** In Respective Local Currencies

Source: Global Research

Global Research - GCC Global Investment House

August 2008 GCC Telecom Sector 5

World Telecom Sector Overview

The worldwide communications (Telecoms, Television and Radio) market and the Telecom market in specific are evolving at a very brisk pace. In view of increasing disposable income in the developed and the emerging economies the Telecom sector is now moving from the erstwhile infrastructure driven to more demand driven. Also, the aspect of convergence of voice, data and entertainment are becoming the new trend when the consumption patterns are changing with increasing demand for bundled services.

Telecom sector evolving on the back of “quad play” (including a combination of television, internet, fixed voice and mobile)…

• According to Ofcom UK, Telecoms service revenues increased by 5 year (2001-06) CAGR of 10.0% from US$420.5bn in 2001 to US$676.2bn in 2006 across 12 major developed and developing countries (USA, UK, France, Germany, Italy, Canada, Japan, Sweden, Ireland, Spain, Poland and Netherlands). Mobile is driving most of the growth and accounts for over 50% of total telecoms revenues in all countries except Sweden and Canada. However, with increasing maturity in mobile markets, growth rates have slowed in Europe and Japan.

• Mobile networks capable of delivering high-speed data services are beginning to take off. The number of 3G connections has increased by 200% in most of 12 major developed and developing countries between 2005 and 2006.

• Broadband accounting for 9% of total telecoms revenue across 12 comparator countries

in 2006 (up from less than 2% in 2001) is the fastest growing sector amongst voice.

• Other than the US (which is characterised by regional operators), in terms of market share of the leading operators the UK has the most diversified mobile and broadband markets of the countries analysed. It also has the second most diversified fixed-line market (after Germany) as measured by the market share of the incumbent.

• The decline of fixed-line voice is a characteristic of all the countries. However, there is large variation in measures of fixed to mobile substitution. Approximately 38% of Italian households are mobile only, compared to just 10% in Germany. In terms of call volumes, 49% are made over mobile networks in Spain compared to fewer than 20% in Germany.

• Total broadband connections across the 12 comparator countries increased by 600% between 2001 and 2006. This growth has been driven primarily by DSL broadband which increased its share of connections in every country and is now the largest broadband platform in all countries analysed except the US.

• Likely uneven distribution of high-speed fibre networks is leading to a lower proportion of Japanese consumers (39%) to be satisfied with the speed of their broadband connection than in any other country surveyed. The highest levels of satisfaction with broadband speed were in the US (85%), despite the high proportion of low-speed lines.

• Levels of next-generation access deployments vary significantly according to different market conditions. Japan is the clear leader among the countries analysed with around 30% of broadband connections being delivered via fibre-to-the-home.

Global Research - GCC Global Investment House

6 GCC Telecom Sector August 2008

The convergence has impacted the world wide communications market as follows

• Multi-service communications offerings, which include a combination of television, internet, fixed voice and mobile, are now available in many countries. ‘Quad-play’ bundles, involving all four services, are generally offered by the incumbent telco, but also in some cases by the cable operators.

• The US leads the world in the sale of audio-visual content, which is reflected in the revenues generated by its online TV and video industry. These were 250% higher than the next biggest market, the UK.

• The internet is taking an increasing share of advertising spend across the key comparator countries. The online share is largest in the UK, at 14.4%.

• User-generated content is proliferating, although professional producers appear to provide the most popular content on websites hosting User-generated content. As of the beginning of Nov’07 the three most viewed channels ever on YouTube.com were all contributed by professional American TV and music producers.

• France is the clear market leader in IPTV with 1.5mn subscribers at the end of 2006. IPTV has been a key driver of triple-play offers in France, which have also promoted VoIP take-up to the highest levels in Europe.

• Device convergence in the mobile handset is becoming widespread. For example, between 37% and 82% of internet users across the key comparator countries surveyed by Ofcom use their mobile phone to take photos.

• Over 75% of mobile phone users in the UK, France, Germany and Italy send SMS text messages. This compares with only 17% of mobile users in Japan, who prefer to send email from their mobile phone instead.

• The internet user base in more mature markets tends to include a greater share of younger and older users. The US is the key example of this, where 9% of internet users are over 65 and 20% are 17 or under. The US is the only market among comparator countries where more women than men use the internet.

• A greater proportion of UK internet users (39%) visit social networking sites than in any other key European country surveyed. They also visit these sites more frequently and spend more time on them.

• Search and navigation, and portals, comprise the most-visited types of website in most countries. Google’s lead is greater in Europe than in the US and Japan, where other search engines provide more competition.

Global Research - GCC Global Investment House

August 2008 GCC Telecom Sector 7

GCC Telecom Sector Overview

The trends in US, UK and other major telecom markets are percolating into the GCC region as well, however with some time lag. The increasingly popular mobile services are leading to a decline in fixed line voice subscribers. Though, convergence in this region is far behind its developed international peers with few countries in the region implementing enhanced 3.5G and related data services, the region is pretty much reaching saturation in terms of cellular voice penetration. Value added services and innovation should lead to sustainability of growth in the future.

In the recent years the GCC telecom players are on an expansion spree following measures from Saudi Arabia, Bahrain, Oman, and UAE to allow additional service providers in the respective countries. This should result in inducing higher competition and further drop in ARPUs in the region and resultant contracting profitability of the players. The service providers should aim to increase their market shares by providing differentiated value added services and providing content based services (like mobile video streaming) to enhance the ARPUs.

Though geographic expansion provides an opportunity to grow the customer base, the latest technological developments in the region including Mobile Number Portability (MNP) allows easy churn in customer base and loss of customer to a better service provider. Hence, to maintain profitability the service providers must also aim at optimizing the customer acquisition costs.

Fixed Line ServicesFixed line services are suffering on account of increasing shift of customer base to the more convenient mobile voice services. In 2007, the worldwide fixed line subscribers declined by 0.9% to reach 1,271.2mn from 1,282.5mn in 2006.

Table 1: GCC vs. Worldwide Fixed Line Subscribers

mn 2002 2003 2004 2005 2006 2007

World 1,082.7 1,134.9 1,203.4 1,261.5 1,282.5 1,271.2

Asia 420.5 472.9 535.3 591.9 613.4 606.5

Americas 298.4 295.4 293.5 294.7 287.8 285.7

Europe 320.6 320.9 327.0 326.2 330.1 326.8

Oceania 12.6 12.7 12.6 12.3 12.1 11.8

Rest of Africa 10.8 11.4 10.9 11.9 12.8 12.6

MENA 19.7 21.5 24.1 24.6 26.2 27.8

GCC 4.5 4.6 4.9 5.1 5.8 5.4

Source: ITU and Global Research

This declining trend was also seen in Asia, Americas and Europe where the mobile penetration is on the rise. The Asian market is growing on account of rising volumes backed by increasing disposable income major contributors being India and China who have underwent high economic growth rates of 8 to 11% in the recent years. Also, availability of very cheap handsets in the range of US$20 is encouraging mass consumption of cellular services.

Global Research - GCC Global Investment House

8 GCC Telecom Sector August 2008

MENA sector is the only exception that has shown a 6.1% YoY increase in the fixed line subscribers in 2007. However, the growth in fixed line subscribers is declining as the YoY growth rate decelerated in 2007 at 6.1% compared to 6.7% in 2006. The GCC region however registered a decline of 6.9% from 5.8mn subscribers in 2006 to 5.4mn subscribers in 2007.

However, during the period 2002-2007, the worldwide fixed lines have increased at a 5 year (2002-07) CAGR of 3.3% representing a minor growth rate vis-à-vis a whopping double digit 23.3% growth in cellular subscribers.

Chart 1: Comparative YoY change in 2007 - Fixed Line vs. Cellular Subscribers

-6.9%

19.6%

25.6%

14.7%9.9%

7.7%

33.0%

40.1%

47.7%

-1.1%-0.9% -0.7% -1.0% -2.5% -1.9%

6.1%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

World Asia Americas Europe Oceania Rest of Africa MENA GCC

Fixed line Cellular

Source: ITU and Global Research

The Growth in MENA during the same period was 7.2% on the back of high growth rates in highly populous Morocco and Egypt that registered a 5 year (2002-07) CAGR of 16.3% and 7.7% respectively.

Chart 2: GCC vs. Worldwide - 5 year (2002-07) CAGR of Fixed Line Subscribers

3.3%

7.6%

-0.9% -1.2%

7.2%

3.6%

0.4%

3.1%

-2.0%-1.0%0.0%1.0%2.0%3.0%4.0%5.0%6.0%7.0%8.0%9.0%

World Asia Americas Europe Oceania Rest of Africa MENA GCC

Source: ITU and Global Research

The other growth contributors in these regions were Yemen (12.3%), Syria (10.5%) and Algeria (9.5%). The GCC region however displayed only a modest 5 year (2002-07) CAGR of 3.6% due to an increase in fixed line subscribers in Qatar (6.1%).

Cellular Services

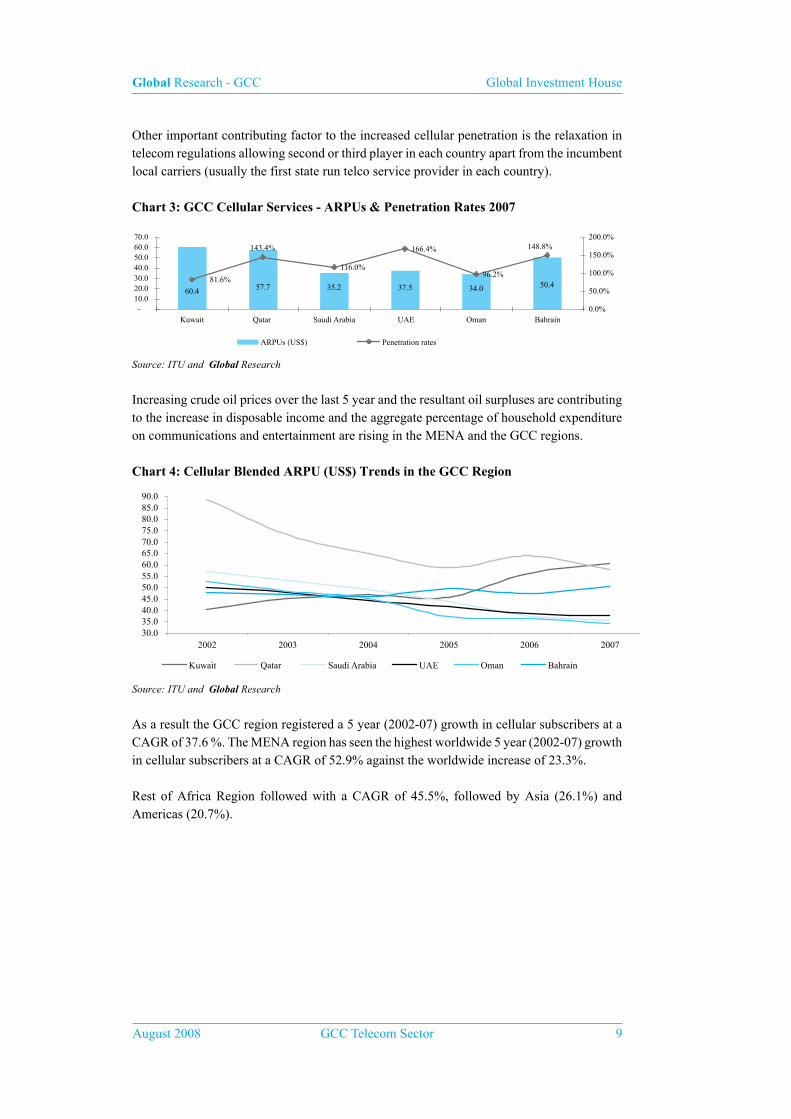

Increasing disposable income and convenience of use is encouraging the cellular penetration in the region.

Global Research - GCC Global Investment House

August 2008 GCC Telecom Sector 9

Other important contributing factor to the increased cellular penetration is the relaxation in telecom regulations allowing second or third player in each country apart from the incumbent local carriers (usually the first state run telco service provider in each country).

Chart 3: GCC Cellular Services - ARPUs & Penetration Rates 2007

50.434.037.535.257.760.4

116.0%

166.4%

96.2%

148.8%143.4%

81.6%

-10.020.030.040.050.060.070.0

Kuwait Qatar Saudi Arabia UAE Oman Bahrain0.0%

50.0%

100.0%

150.0%

200.0%

ARPUs (US$) Penetration rates

Source: ITU and Global Research

Increasing crude oil prices over the last 5 year and the resultant oil surpluses are contributing to the increase in disposable income and the aggregate percentage of household expenditure on communications and entertainment are rising in the MENA and the GCC regions.

Chart 4: Cellular Blended ARPU (US$) Trends in the GCC Region

30.035.040.045.050.055.060.065.070.075.080.085.090.0

2002 2003 2004 2005 2006 2007

Kuwait Qatar Saudi Arabia UAE Oman Bahrain

Source: ITU and Global Research

As a result the GCC region registered a 5 year (2002-07) growth in cellular subscribers at a CAGR of 37.6 %. The MENA region has seen the highest worldwide 5 year (2002-07) growth in cellular subscribers at a CAGR of 52.9% against the worldwide increase of 23.3%.

Rest of Africa Region followed with a CAGR of 45.5%, followed by Asia (26.1%) and Americas (20.7%).

Global Research - GCC Global Investment House

10 GCC Telecom Sector August 2008

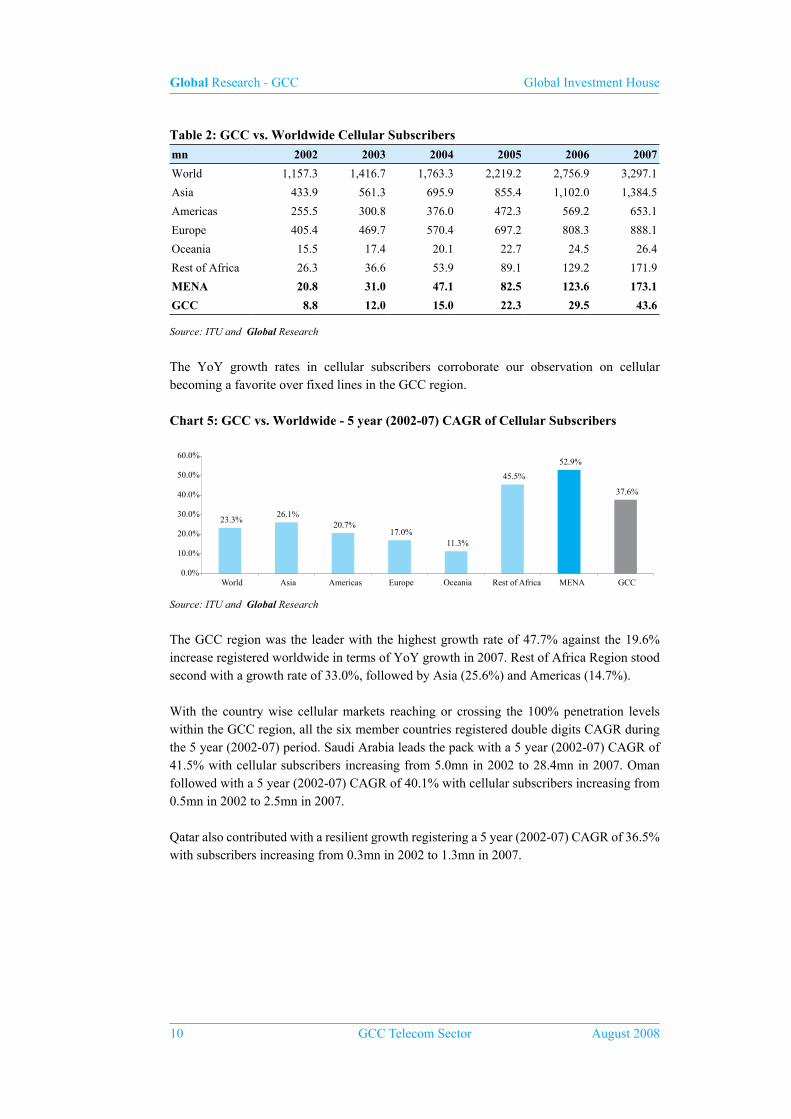

Table 2: GCC vs. Worldwide Cellular Subscribers

mn 2002 2003 2004 2005 2006 2007

World 1,157.3 1,416.7 1,763.3 2,219.2 2,756.9 3,297.1

Asia 433.9 561.3 695.9 855.4 1,102.0 1,384.5

Americas 255.5 300.8 376.0 472.3 569.2 653.1

Europe 405.4 469.7 570.4 697.2 808.3 888.1

Oceania 15.5 17.4 20.1 22.7 24.5 26.4

Rest of Africa 26.3 36.6 53.9 89.1 129.2 171.9

MENA 20.8 31.0 47.1 82.5 123.6 173.1

GCC 8.8 12.0 15.0 22.3 29.5 43.6

Source: ITU and Global Research

The YoY growth rates in cellular subscribers corroborate our observation on cellular becoming a favorite over fixed lines in the GCC region.

Chart 5: GCC vs. Worldwide - 5 year (2002-07) CAGR of Cellular Subscribers

23.3%26.1%

20.7%17.0%

11.3%

45.5%

52.9%

37.6%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

World Asia Americas Europe Oceania Rest of Africa MENA GCC

Source: ITU and Global Research

The GCC region was the leader with the highest growth rate of 47.7% against the 19.6% increase registered worldwide in terms of YoY growth in 2007. Rest of Africa Region stood second with a growth rate of 33.0%, followed by Asia (25.6%) and Americas (14.7%).

With the country wise cellular markets reaching or crossing the 100% penetration levels within the GCC region, all the six member countries registered double digits CAGR during the 5 year (2002-07) period. Saudi Arabia leads the pack with a 5 year (2002-07) CAGR of 41.5% with cellular subscribers increasing from 5.0mn in 2002 to 28.4mn in 2007. Oman followed with a 5 year (2002-07) CAGR of 40.1% with cellular subscribers increasing from 0.5mn in 2002 to 2.5mn in 2007.

Qatar also contributed with a resilient growth registering a 5 year (2002-07) CAGR of 36.5% with subscribers increasing from 0.3mn in 2002 to 1.3mn in 2007.

Global Research - GCC Global Investment House

August 2008 GCC Telecom Sector 11

Chart 6: GCC vs. Worldwide - YoY growth in Cellular Subscribers in 2007

19.6%25.6%

14.7%9.9% 7.7%

33.0%

40.1%

47.7%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

World Asia Americas Europe Oceania Rest of Africa MENA GCC

Source: ITU and Global Research

Broadband Services

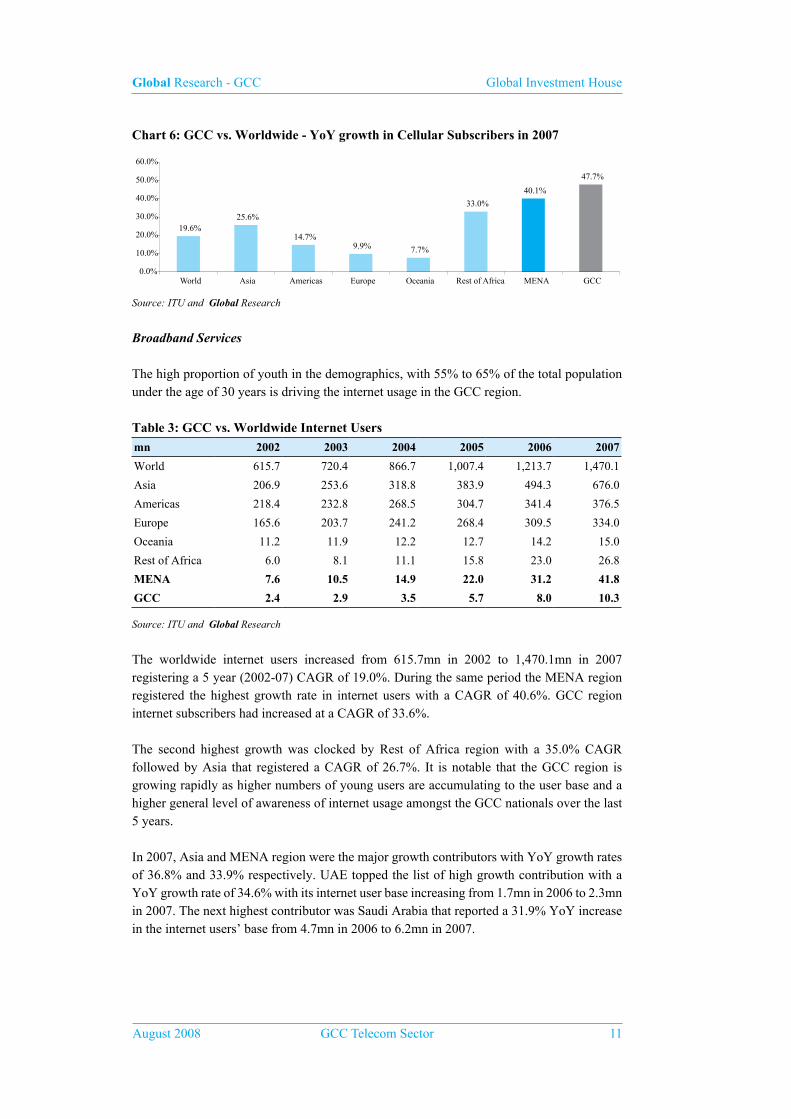

The high proportion of youth in the demographics, with 55% to 65% of the total population under the age of 30 years is driving the internet usage in the GCC region.

Table 3: GCC vs. Worldwide Internet Users

mn 2002 2003 2004 2005 2006 2007

World 615.7 720.4 866.7 1,007.4 1,213.7 1,470.1

Asia 206.9 253.6 318.8 383.9 494.3 676.0

Americas 218.4 232.8 268.5 304.7 341.4 376.5

Europe 165.6 203.7 241.2 268.4 309.5 334.0

Oceania 11.2 11.9 12.2 12.7 14.2 15.0

Rest of Africa 6.0 8.1 11.1 15.8 23.0 26.8

MENA 7.6 10.5 14.9 22.0 31.2 41.8

GCC 2.4 2.9 3.5 5.7 8.0 10.3

Source: ITU and Global Research

The worldwide internet users increased from 615.7mn in 2002 to 1,470.1mn in 2007 registering a 5 year (2002-07) CAGR of 19.0%. During the same period the MENA region registered the highest growth rate in internet users with a CAGR of 40.6%. GCC region internet subscribers had increased at a CAGR of 33.6%.

The second highest growth was clocked by Rest of Africa region with a 35.0% CAGR followed by Asia that registered a CAGR of 26.7%. It is notable that the GCC region is growing rapidly as higher numbers of young users are accumulating to the user base and a higher general level of awareness of internet usage amongst the GCC nationals over the last 5 years.

In 2007, Asia and MENA region were the major growth contributors with YoY growth rates of 36.8% and 33.9% respectively. UAE topped the list of high growth contribution with a YoY growth rate of 34.6% with its internet user base increasing from 1.7mn in 2006 to 2.3mn in 2007. The next highest contributor was Saudi Arabia that reported a 31.9% YoY increase in the internet users’ base from 4.7mn in 2006 to 6.2mn in 2007.

Global Research - GCC Global Investment House

12 GCC Telecom Sector August 2008

Chart 7: GCC vs. Worldwide - 5 year (2002-07) CAGR in Internet Users

19.0%

26.7%

11.5%15.1%

6.1%

35.0%

40.6%

33.6%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

World Asia Americas Europe Oceania Rest of Africa MENA GCC

Source: ITU and Global Research

Qatar also registered an impressive double digit YoY growth rate of 21.1% increasing its internet users’ base from 0.3mn in 2006 to 0.4mn in 2007.

Chart 8: GCC vs. Worldwide - YoY growth in Internet Users in 2007

21.1%

36.8%

10.3%7.9%

5.5%

16.3%

33.9%

28.8%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

World Asia Americas Europe Oceania Rest ofAfrica

MENA GCC

Source: ITU and Global Research

The higher rate of internet penetration and improved infrastructure services in terms of shift from Dial up to cable is helping increase the broadband subscriber base in the GCC region. Table 4: GCC vs. Worldwide Broadband Subscribers

mn 2002 2003 2004 2005 2006 2007

World 66.0 103.7 157.7 216.2 284.4 341.8

Asia 26.9 43.1 64.1 83.3 104.2 127.0

Americas 24.9 34.7 48.9 64.1 82.2 93.5

Europe 13.7 25.0 43.0 65.3 91.3 112.6

Oceania 0.3 0.6 1.2 2.4 4.5 5.6

Rest of Africa 0.0 0.0 0.1 0.2 0.5 0.5

MENA 0.1 0.2 0.4 0.9 1.7 2.7

GCC 0.1 0.1 0.2 0.3 0.6 1.0

Source: ITU and Global Research

The analysis of 5 year (2002-07) CAGR in broadband subscribers worldwide indicates that the GCC region is amongst the top three growth regions in the world. The worldwide broadband subscriber base increased at a 5 year (2002-07) CAGR of 38.9%.

Global Research - GCC Global Investment House

August 2008 GCC Telecom Sector 13

Chart 9: GCC vs. Worldwide - 5 year (2002-07) CAGR in Broadband Subscribers

38.9% 36.4% 30.3%

52.3%

78.8%

132.8%

89.8%71.6%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

World Asia Americas Europe Oceania Rest of Africa MENA GCC

Source: ITU and Global Research

The rest of Africa region was the top growth region with a CAGR of 132.8% during the same period whereas Oceania and the GCC region registered a CAGR of 78.8% and 71.6% respectively.

Chart 10: GCC vs. Worldwide - YoY growth in Broadband Subscribers in 2007

20.2% 21.8%13.8%

23.2% 23.0%

5.2%

57.7%

68.9%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

World Asia Americas Europe Oceania Rest of Africa MENA GCC

Source: ITU and Global Research

In 2007, the GCC region registered the highest growth rate at a YoY rate of 68.9% compared to the worldwide YoY growth rate of 20.2%.

The member countries that contributed to this increase were Saudi Arabia and Qatar. The subscriber base in Saudi Arabia displayed an astronomical YoY growth of 175.0% increasing from 0.2mn subscribers in 2006 to 0.6mn in 2007 on the back of increased spending on IT infrastructure. Qatar followed, growing from 0.05mn subscribers in 2006 to 0.07mn in 2007 registering a YoY growth of 50.2%. We expect the broadband penetration to increase further as a result of the young demographics and increased focus on developing the IT infrastructure in the region.

Global Research - GCC Global Investment House

14 GCC Telecom Sector August 2008

GCC Country-wise Telecom Profile

Kuwait

The Kuwait telecom market is the first to open itself to competition in 1999 in the GCC region for cellular services, though the fixed line market is yet under monopoly government control.

Table 5: Country Telecom Profile – Kuwait

000s 2002 2003 2004 2005 2006 2007

Cellular Subscribers 1,401.8 1,761.4 2,109.7 2,277.0 2,530.0 2,773.7

Cellular Penetration 57.9% 69.2% 76.6% 76.1% 79.5% 81.6%

Pre paid subscribers % 69.0% 76.2% 80.1% 79.5% 79.6% 78.3%

Post paid subscribers % 31.0% 23.8% 19.9% 20.5% 20.4% 21.7%

Blended ARPU (US$) 40.3 45.0 46.8 45.7 56.3 60.4

Fixed Line Subscribers 481.9 486.9 497.0 504.8 516.9 517.0

Fixed Line Penetration % 20.4% 19.6% 19.5% 18.8% 18.7% 18.1%

Broadband Subscribers 10.5 13.0 20.0 25.0 25.0 25.0

Broadband Penetration % 0.4% 0.5% 0.8% 0.9% 0.9% 0.9%Source: ITU and Global Research

Regulatory Environment

Ministry of Communications (MOC) plays the role of the regulator in Kuwait in the absence of an independent Telecom Regulatory Authority (TRA). The fixed line services in Kuwait are completely controlled and operated by the MOC. However, following the trends in the international market and the regional changes with requirement of higher data transfers should lead to a relaxation in this segment and should lead to a higher penetration. The fixed line penetration declined from 20.4% in 2002 to 18.1% in 2007 on account of loss of subscribers to the cellular segment.

Cellular Penetration and ARPUs

Mobile Telecommunications Company and National Mobile Telecommunications Company are the two listed cellular service providers in Kuwait. The MOC opened up the cellular services to competition in 1999, the first country to do that in the GCC region then. This has helped increase the penetration in the region from 57.9% in 2002 to 81.6%. Though the proportion of prepaid subscribers has increased from 69.0% in 2002 to 78.3% in 2007, the ARPUs have increased at a 5 year (2002-07) CAGR of 8.4% from US$40.3 in 2002 to US$60.4 in 2007. We observe that this has occurred due to lower competition on account of only two cellular operators in the country and increasing subscription to high priced value added services.

Global Research - GCC Global Investment House

August 2008 GCC Telecom Sector 15

Qatar

The Telecom market in Qatar is highly monopolized until 2007 and is expected to see growing competition in 2008 or early 2009 onwards with liberalization setting in.

Table 6: Country Telecom Profile – Qatar

000s 2002 2003 2004 2005 2006 2007

Cellular Subscribers 266.7 376.5 490.3 716.8 919.8 1,264.4

Cellular Penetration 43.2% 52.5% 64.9% 90.0% 109.7% 143.4%

Pre paid subscribers % 51.4% 63.5% 72.2% 78.1% 79.9% 83.4%

Post paid subscribers % 48.6% 36.5% 27.8% 21.9% 20.1% 16.6%

Blended ARPU (US$) 88.7 73.1 64.9 58.6 63.8 57.7

Fixed Line Subscribers 176.5 184.5 190.9 205.4 228.3 237.4

Fixed Line Penetration % 26.3% 26.0% 25.8% 26.3% 27.2% 28.3%

Broadband Subscribers 0.2 3.0 10.7 25.1 46.8 70.3

Broadband Penetration % 0.0% 0.4% 1.4% 3.2% 5.6% 8.4%

Source: ITU and Global Research

Regulatory Environment

Supreme Council of Information and Communication Technology (ictQatar) was set up in 2004 as the regulator of telecommunication sector in Qatar. The regulatory environment was highly monopolistic with Qatar Telecom providing both fixed line and cellular services until the decree law No. 34 of 2006 was promulgated to liberalize and open the telecom sector in Qatar.

Cellular Penetration and ARPUs

In continuation to the liberalization decree in 2006 and commercial bidding, Qatar’s second mobile license has been granted to Vodafone in Jun’08. In early 2009, consumers should be able to choose the company that best serves them. Following the years depicting lower cellular penetration since 2002, the penetration level has increased on account of proposed liberalization. The cellular penetration has increased from 43.2% in 2002 to 143.4% in 2007, the third highest in the region after UAE (166.4%) and Bahrain (148.8%).

Global Research - GCC Global Investment House

16 GCC Telecom Sector August 2008

Saudi Arabia

The largest market by size in the GCC region, Saudi Arabian telecom market is growing resiliently in the recent years breaching the 100% penetration mark in the cellular services. However, the level of penetration is low in the fixed line services. The kingdom is characterized by one fixed line and two cellular service providers. A third cellular services provider and a second fixed line services provider are expected to start operations in 2008.

Table 7: Country Telecom Profile – Saudi Arabia

000s 2002 2003 2004 2005 2006 2007

Cellular Subscribers 5,008.0 7,238.2 9,175.8 14,164.2 19,662.6 28,381.0

Cellular Penetration 23.3% 32.9% 40.5% 61.3% 83.0% 116.0%

Pre paid subscribers % 42.0% 52.8% 53.3% 67.4% 76.6% 83.1%

Post paid subscribers % 58.0% 47.2% 46.7% 32.6% 23.4% 16.9%

Blended ARPU (US$) 57.0 53.0 48.9 43.8 37.2 35.2

Fixed Line Subscribers 3,417.0 3,502.6 3,695.1 3,844.0 3,951.0 3,996.0

Fixed Line Penetration % 15.1% 15.0% 15.4% 15.6% 15.7% 16.2%

Broadband Subscribers 34.8 46.0 68.7 67.8 218.2 600.0

Broadband Penetration % 0.2% 0.2% 0.3% 0.3% 0.9% 2.4%

Source: ITU and Global Research

Regulatory Environment

The Independent telecom regulatory authority of Saudi Arabia, the Communications & Information Technology Commission (CITC) was established in 2001. The incumbent fixed line and cellular player Saudi Telecom (STC) established in 1998 is the largest provider followed by Emirates Telecommunications Corporation (ETISALAT) who won the second cellular provider license in 2004. Mobile Telecommunications Company, Kuwait (ZAIN) is expected to commence operations as the third cellular service provider by 2H08 and Bahrain Telecommunications Company (BATELCO) through Atheeb is expected to launch the country’s second fixed line services in 3Q08.

Cellular Penetration and ARPUs

Increasing number of players in the telecom market is driving the penetration and the country’s cellular penetration has breached the 100% levels in 2007 when it clocked an all time high cellular penetration rate of 101.4%. Increasing competition and slashing prices is driving down the ARPUs year after year. The cellular ARPUs have declined from US$57.0 in 2002 to US$35.2 in 2007 thereby declining at a 5 year (2002-07) CAGR of 9.2%. Apart from competition the increasing composition of prepaid subscribers that increased from 50.0% in 2002 to 60.0% in 2007 is also contributing to decline in ARPUs.

Broadband Penetration

The increasing component of youth in the population is driving the internet users in the country and also the broadband subscribers. The broadband penetration has increased from a negligible 0.2% in 2002 to 2.4% in 2007, with subscribers registering a 5 year (2002-07) CAGR of 76.7%.

Global Research - GCC Global Investment House

August 2008 GCC Telecom Sector 17

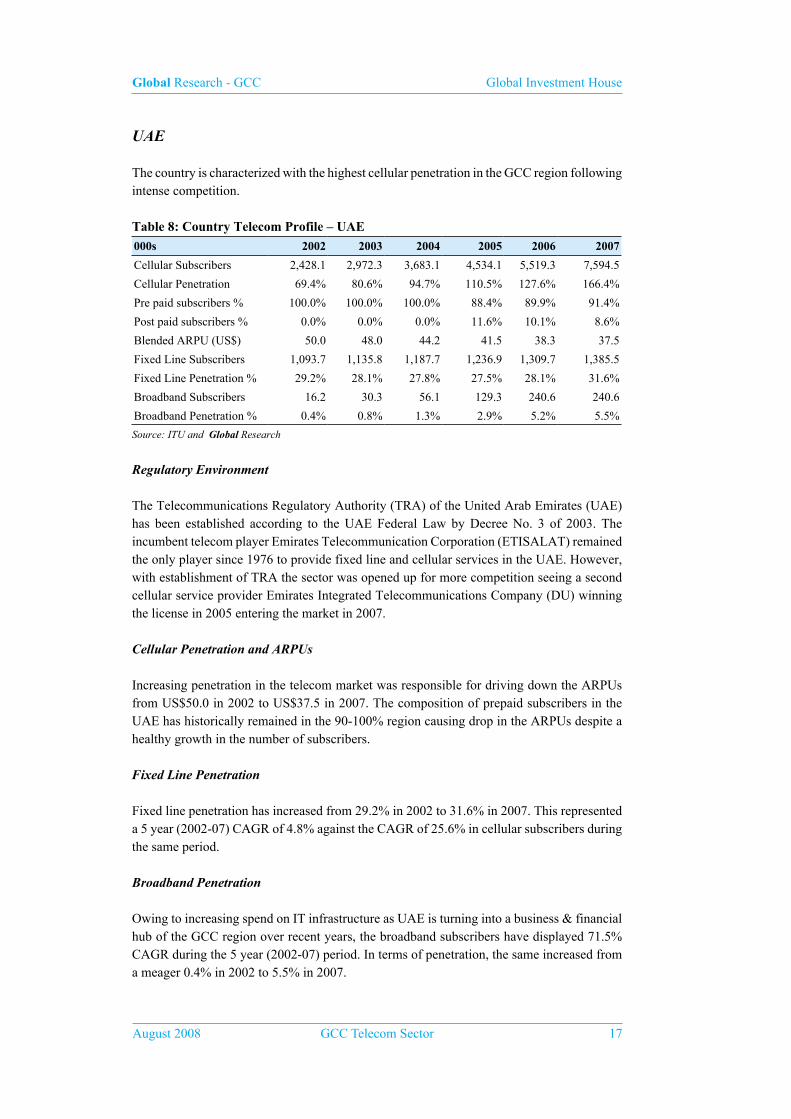

UAE

The country is characterized with the highest cellular penetration in the GCC region following intense competition.

Table 8: Country Telecom Profile – UAE

000s 2002 2003 2004 2005 2006 2007

Cellular Subscribers 2,428.1 2,972.3 3,683.1 4,534.1 5,519.3 7,594.5

Cellular Penetration 69.4% 80.6% 94.7% 110.5% 127.6% 166.4%

Pre paid subscribers % 100.0% 100.0% 100.0% 88.4% 89.9% 91.4%

Post paid subscribers % 0.0% 0.0% 0.0% 11.6% 10.1% 8.6%

Blended ARPU (US$) 50.0 48.0 44.2 41.5 38.3 37.5

Fixed Line Subscribers 1,093.7 1,135.8 1,187.7 1,236.9 1,309.7 1,385.5

Fixed Line Penetration % 29.2% 28.1% 27.8% 27.5% 28.1% 31.6%

Broadband Subscribers 16.2 30.3 56.1 129.3 240.6 240.6

Broadband Penetration % 0.4% 0.8% 1.3% 2.9% 5.2% 5.5%

Source: ITU and Global Research

Regulatory Environment

The Telecommunications Regulatory Authority (TRA) of the United Arab Emirates (UAE) has been established according to the UAE Federal Law by Decree No. 3 of 2003. The incumbent telecom player Emirates Telecommunication Corporation (ETISALAT) remained the only player since 1976 to provide fixed line and cellular services in the UAE. However, with establishment of TRA the sector was opened up for more competition seeing a second cellular service provider Emirates Integrated Telecommunications Company (DU) winning the license in 2005 entering the market in 2007.

Cellular Penetration and ARPUs

Increasing penetration in the telecom market was responsible for driving down the ARPUs from US$50.0 in 2002 to US$37.5 in 2007. The composition of prepaid subscribers in the UAE has historically remained in the 90-100% region causing drop in the ARPUs despite a healthy growth in the number of subscribers.

Fixed Line Penetration

Fixed line penetration has increased from 29.2% in 2002 to 31.6% in 2007. This represented a 5 year (2002-07) CAGR of 4.8% against the CAGR of 25.6% in cellular subscribers during the same period.

Broadband Penetration

Owing to increasing spend on IT infrastructure as UAE is turning into a business & financial hub of the GCC region over recent years, the broadband subscribers have displayed 71.5% CAGR during the 5 year (2002-07) period. In terms of penetration, the same increased from a meager 0.4% in 2002 to 5.5% in 2007.

Global Research - GCC Global Investment House

18 GCC Telecom Sector August 2008

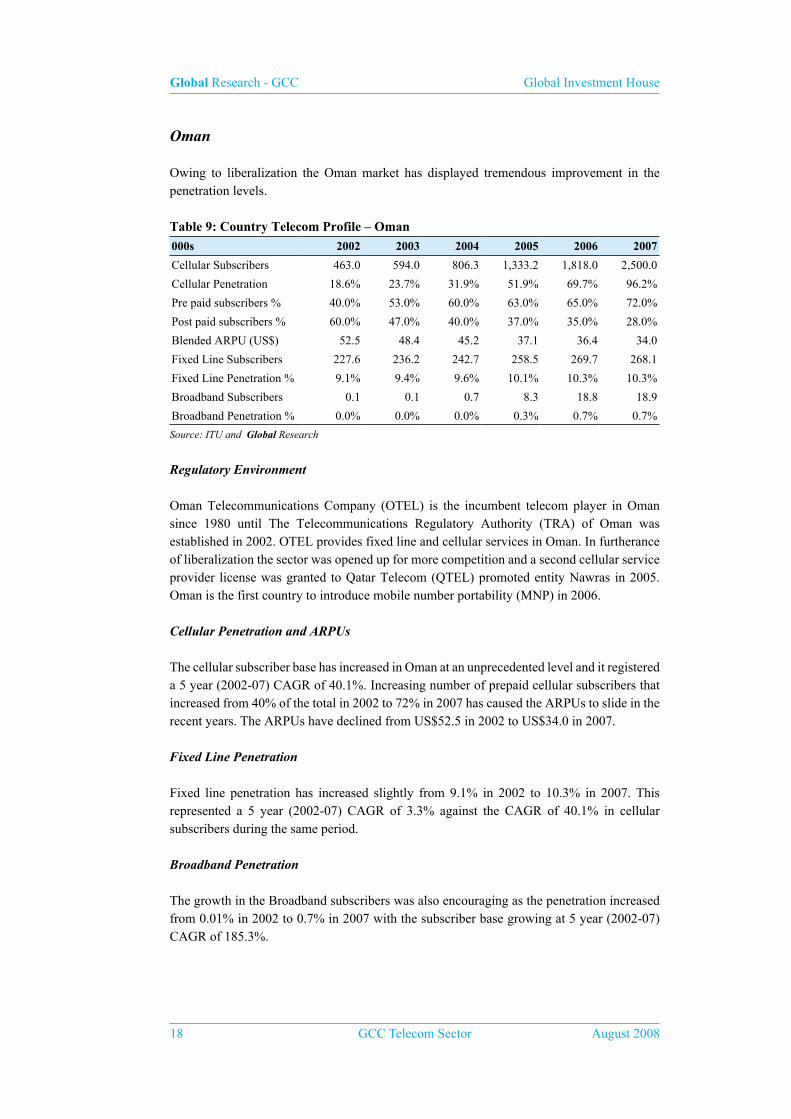

Oman

Owing to liberalization the Oman market has displayed tremendous improvement in the penetration levels.

Table 9: Country Telecom Profile – Oman

000s 2002 2003 2004 2005 2006 2007

Cellular Subscribers 463.0 594.0 806.3 1,333.2 1,818.0 2,500.0

Cellular Penetration 18.6% 23.7% 31.9% 51.9% 69.7% 96.2%

Pre paid subscribers % 40.0% 53.0% 60.0% 63.0% 65.0% 72.0%

Post paid subscribers % 60.0% 47.0% 40.0% 37.0% 35.0% 28.0%

Blended ARPU (US$) 52.5 48.4 45.2 37.1 36.4 34.0

Fixed Line Subscribers 227.6 236.2 242.7 258.5 269.7 268.1

Fixed Line Penetration % 9.1% 9.4% 9.6% 10.1% 10.3% 10.3%

Broadband Subscribers 0.1 0.1 0.7 8.3 18.8 18.9

Broadband Penetration % 0.0% 0.0% 0.0% 0.3% 0.7% 0.7%

Source: ITU and Global Research

Regulatory Environment

Oman Telecommunications Company (OTEL) is the incumbent telecom player in Oman since 1980 until The Telecommunications Regulatory Authority (TRA) of Oman was established in 2002. OTEL provides fixed line and cellular services in Oman. In furtherance of liberalization the sector was opened up for more competition and a second cellular service provider license was granted to Qatar Telecom (QTEL) promoted entity Nawras in 2005. Oman is the first country to introduce mobile number portability (MNP) in 2006.

Cellular Penetration and ARPUs

The cellular subscriber base has increased in Oman at an unprecedented level and it registered a 5 year (2002-07) CAGR of 40.1%. Increasing number of prepaid cellular subscribers that increased from 40% of the total in 2002 to 72% in 2007 has caused the ARPUs to slide in the recent years. The ARPUs have declined from US$52.5 in 2002 to US$34.0 in 2007.

Fixed Line Penetration

Fixed line penetration has increased slightly from 9.1% in 2002 to 10.3% in 2007. This represented a 5 year (2002-07) CAGR of 3.3% against the CAGR of 40.1% in cellular subscribers during the same period.

Broadband Penetration

The growth in the Broadband subscribers was also encouraging as the penetration increased from 0.01% in 2002 to 0.7% in 2007 with the subscriber base growing at 5 year (2002-07) CAGR of 185.3%.

Global Research - GCC Global Investment House

August 2008 GCC Telecom Sector 19

Bahrain

Liberalization has also affected the Bahrain telecom market in a positive manner with higher penetration rates. It has the second highest cellular penetration in the GCC region.

Table 10: Country Telecom Profile – Bahrain

000s 2002 2003 2004 2005 2006 2007

Cellular Subscribers 389.0 443.1 649.8 748.7 907.4 1,116.0

Cellular Penetration 55.6% 62.4% 90.3% 102.6% 122.6% 148.8%

Pre paid subscribers % 76.0% 75.0% 75.0% 75.0% 75.0% 75.0%

Post paid subscribers % 24.0% 25.0% 25.0% 25.0% 25.0% 25.0%

Blended ARPU (US$) 48.0 47.0 46.0 49.4 47.3 50.4

Fixed Line Subscribers 175.4 185.8 191.6 193.5 194.2 194.2

Fixed Line Penetration % 25.1% 26.2% 26.6% 26.5% 26.2% 25.9%

Broadband Subscribers 5.0 9.7 15.0 21.4 38.6 38.6

Broadband Penetration % 0.7% 1.4% 2.1% 2.9% 5.2% 5.1%

Source: ITU and Global Research

Regulatory Environment

The Telecommunications Regulatory Authority (TRA) of Bahrain was established by Legislative Decree No. 48 of 2002 promulgating the Telecommunications Law. Bahrain Telecommunications Company (BATELCO) was established in 1981 as the incumbent telecom player. Following liberalization, Mobile Telecommunications Company (ZAIN) was awarded the second cellular service provider license in 2003. The competition also intensified in the fixed line segment with the licenses for second and third fixed line operators being granted to Lightspeed Communications and Kalaam Telecom respectively.

Cellular Penetration and ARPUs

The cellular penetration has increased from 55.6% in 2002 to a whopping 148.8% in 2007. The entry of new player in the arena gave ample choice to the customers and thus the customer base increased at a 5 year (2002-07) CAGR of 23.5% from 0.4mn in 2002 to 1.1mn in 2007. ARPUs have fluctuated over the 5 year period but remained in the range of US$46.0 to US$50.4 as a result of stable 75% prepaid concentration in the total cellular subscriber base.

Fixed Line Penetration

The competition in the fixed line segment is intensifying with three operators in play; however the penetration is relatively flat at 25.9% in 2007 as compared to 25.1% in 2002 and has not declined as the consumers’ interest was maintained due to provision of internet related facilities through fixed line connections. This was quite different from the declining fixed line penetration trend seen in other countries in the GCC region.

PLAYER PROFILES

Global Research - GCC Global Investment House

August 2008 GCC Telecom Sector 21

Mobile Telecommunications Company(Zain)

TickersZAIN.KW (Reuters)TELE KK (Bloomberg)

Listing:Kuwait Stock Exchange

Current Price: KD1.72 (August 31, 2008)

Key Data

EPS* (fils) 79.5 Avg. daily vol. (‘000) 4,796.7

BVPS* (fils) 708.1 52 week High / Low 2.228 / 1.460

P/E (x) 21.6 Market Cap (KD mn) 7,362

P/BV (x) 2.4 Target Price (KD) 1.766

Source: Global Research

* Projected (2008)

Background• Mobile Telecommunications Company (Zain) was established in 1983 in Kuwait as the

region’s first mobile operator. Since 2003, it has grown significantly becoming the 4th largest telecommunications company in the world in terms of geographic presence with a footprint in 22 countries spread across the Middle East and Africa providing mobile voice and data services to over 50.74mn active customers (as at 30 June 2008).

• In the Middle East the company operates under the Zain brand name in Bahrain, Iraq, Jordan, Kuwait and Sudan. In Lebanon the company operates as mtc-touch. Zain plans to commence operations in the Kingdom of Saudi Arabia during the current year. In Africa, Zain operates under the Celtel brand in 14 sub-Saharan African countries namely: Burkina Faso, Chad, Democratic Republic of the Congo, Republic of the Congo, Gabon, Kenya, Malawi, Madagascar, Niger, Nigeria, Sierra Leone, Tanzania, Uganda and Zambia.

Recent Developments

Launch of Commercial Services in the Kingdom of Saudi ArabiaOn August 26, 2008, Zain announced the launch of commercial services in the Kingdom of Saudi Arabia. With the launch, the Kingdom joins and connects to ‘One Network’, the Group’s renowned, and the world’s first, borderless mobile service offering over 45mn customers in 16 countries favorable rates, free of high roaming charges for cross-border communications. Zain will initially cover 53% of the population in 36 major cities and 14 highways spanning over 4,000 kms. The remaining coverage area will be attained initially through a complimentary countrywide roaming service. Zain will introduce high-speed 3.5G broadband technology to approximately half of the Saudi population offering the latest

HoldRecommendation

Global Research - GCC Global Investment House

22 GCC Telecom Sector August 2008

3.5G services that include television, video-calling, rich multimedia content and even faster internet access. Zain’s network will be further expanded in stages to eventually cover the entire Kingdom. Zain Saudi Arabia is a publicly listed company on the Saudi Stock Exchange ‘Tadawul’.

Expansion of One Network In April 2008, Zain launched borderless ‘One Network’ mobile service to Bahrain, Iraq, Jordan and Sudan. This service will allow Zain’s 15mn customers to communicate in between and to be treated as local customers in terms of pricing while using their home network service. In November 2007, Zain’s subsidiary Celtel International expanded its ‘One Network’, the world’s first borderless mobile network in Africa. This ‘One Network’ in Africa covers 12 countries.

Celtel Re-branded to ZainIn August 2008, Zain announced that it has re-branded its entire African operations from Celtel to Zain. Fourteen country operations across Africa will immediately rebrand to Zain, namely Burkina Faso, Chad, the Republic of Congo, the Democratic Republic of Congo, Gabon, Kenya, Madagascar, Malawi, Niger, Nigeria, Sierra Leone, Tanzania, Uganda and Zambia. Zain also announced the creation of the world’s first cross-continental borderless network, extending and linking its ‘One Network’ service between Africa and the Middle East. The service will be available to 500 million people stretching from the west coast of Africa to the Middle East.

Zain to Increase Equity Capital In August 2008 the company is raising its equity capital through rights issue. The company’s paid up capital will be increased by 75% through rights which is priced at 850 fils per share (premium of 750 fils). The company’s equity capital will increase to KD428.03mn from the current KD189.4mn. The capital increase will allow Zain to finance its future expansion plans as well as meet its financial commitments.

Analysis of Country Operations

Group level PerformanceIn FY2007, total active customers of Zain increased to 42.50mn versus 27.04mn in FY2006, an increase of 57.2%. As of year end 2007, Zain’s African operations – through its subsidiary Celtel International – represented 64% of the company’s customer base while the operations in Middle East countries of Iraq, Sudan, Jordan, Kuwait, Lebanon and Bahrain represented the remaining customers. Zain’s African operations registered a 59% increase in customers in 2007, while the Middle Eastern operations registered a 53% increase over the same period. The company’s customer increase was driven primarily by its high growth African operations including Nigeria, Uganda and Tanzania. In the Middle East, the operations in Iraq, Bahrain and Sudan showed solid growth.

At the end of July 2008, Zain’s group customer base increased to 50.74mn from 42.50mn at the end of 2007, registering a YTD growth of 19.4% and a YoY growth of 57.8%.

Global Research - GCC Global Investment House

August 2008 GCC Telecom Sector 23

Chart 01:Country-wise Customer Segmentation - June 2008

Chart 02:Customer segmentation of African countries– June 2008

Source: Company Reports and Global Research

Middle East Operations

KuwaitIn 2007 Kuwait witnessed a growth of 9.6% in total subscriber base for GSM to reach 2.77mn customers, which indicates penetration rate of 82% on total population and 106% on addressable population. Zain leads the GSM segment in Kuwait with a market share of 57% whereas NMTC accounts for the rest of the market share i.e. 43% as there are only two GSM operators in the country.

In GSM segment, the total customer addition in 2007 was 244,009. In 2007, NMTC gained a larger slice of total market additions with a customer addition of 129,009 which helped it to increase its market share from 42% in 2006 to 43% in 2007. Zain increased its customer strength by 115,000 customers.

In Kuwait, out of the total subscriber base of 2.77mn as of Dec. 2007, 2.17mn customers (78.3%) were prepaid customers while 602,506 (21.7%) customers were postpaid. Zain accounted for 72.5% of the total postpaid customers and 52.5% of total prepaid subscribers while NMTC accounted for 27.5% of total postpaid customers and 47.5% of total prepaid customers.

Saudi Telecom Company (STC), the third operator is likely to start its operation in 2008. In 2007, the government of Kuwait issued a third mobile license to STC for US$907.6mn. MTC’s Kuwait operation had a total of 1.58mn customers by year end 2007, representing an increase of 7.9% over 2006. Out of the total subscriber base, 72.3% were prepaid customers while 27.7% were postpaid customers. For FY2007, Kuwait operations reported revenues of KD359.4mn, contributed 21.4% to total revenues of MTC for the year. EBITDA was at KD194.1mn representing an EBITDA margin of 54%. Net profit from Kuwait operations

Kuwait 3.3%

Jordan 3.9%

Iraq 15.6%

Bahrain1.1%

Lebanon 1.4%

Sudan 9.1%

Africa 65.6%

Burkina Faso 3.5%

Chad 2.3%

Congo Brazzaville 3.5%

DRC 8.1%

Gabon 2.2%

Kenya 5.7%

Madagascar 2.7%

Malawi 2.9%

Niger 2.6%

Nigeria 44.5%

Sierra Leone 1.3%

Tanzania 8.5%

Uganda 5.4%

Zambia 6.9%

Global Research - GCC Global Investment House

24 GCC Telecom Sector August 2008

increased by 53.1% to reach KD216.1mn. In 2007, its Kuwait operations had a high ARPU of US$70, which declined marginally to US$69 at the end of 1H-2008. During 1H-2008, MTC increased its customer base to 1.66mn, a y-t-d increase of 84,000 customers.

JordanZain’s Jordan operation had a total of 1.858mn customers at the end of 2007, representing a 5.2% decline in total customers compared to 2006. In 2007, ARPU for Jordan operations increased to US$19 from US$17 in 2006. Revenues for FY2007 were KD135.3mn, a decline of 4%, compared to KD141mn reported for FY2006. EBITDA was at KD62.5mn representing an EBITDA margin of 46.2%. It reported a decline of 14% in its net profit to reach at KD32.6mn for FY2007.

BahrainBahrain has the highest mobile penetration rate in the region and is leading the way in offering new innovative services such as triple play and Wi-Max. In 2007, Zain’s Bahrain operations increased its total customer base by 92% to 448,000 customers. Its revenues in FY2007 reached to KD42.9mn, registered a growth of 32.4% over FY2006. In 2007, ARPU for Bahrain operations increased to US$42 from US$31 in 2006. Its EBITDA increased by 34% to reach at KD13.5mn. In FY2007, it reported significant growth of 39.2% in net profit to reach at KD4.7mn as compared to KD3.4mn reported in FY2006.

IraqIn Iraq, at the end of 2007 Zain had total customer base of 7.287mn, representing a 128% increase over 2006. Zain’s leading position in the Iraqi market has been further strengthened by the acquisition of Iraqna, one of Iraq’s three mobile operators. Iraq is predominantly a prepaid customer market for the Zain Group as there are only 55,000 postpaid customers and the rest all are prepaid customers. For FY2007, Zain Iraq reported revenues of KD159.1mn representing a growth of 60% for the year. In 2007, ARPU for its Iraq operations declined to US$13 from US$14 in 2006. EBITDA increased by 70.7% to reach KD50.4mn. In FY2007, Iraq operations reported a significant growth of 149% in its bottom-line to reach KD13.2mn from KD5.3mn in FY2006. LebanonZain has a 4-year management contract to operate one of Lebanon’s two GSM operations. In June 2004, MTC won a 4-year management contract to operate one of Lebanon’s two GSM operations. This year, Lebanon is in the midst of privatizing the two state-owned cellular networks, which are currently managed by the Kuwait’s Mobile Telecommunications Company Lebanon (MTC Touch) and the German-Saudi consortium Alfa. MTC has developed the Lebanese operation to full potential in hope that it will be added to the Group’s portfolio as soon as the government undertakes the process of privatization. At the end of 2007, Zain’s Lebanon operation had a total customer base of 630,000 customers which grew by 12.5% over 2006. MTC Touch’s revenues reached KD17.2mn in FY2007, registering an increase of 2% over FY2006. The disclosed revenues are from the management contract and not the total revenues of the operation which are collected by the Government of Lebanon. Its EBITDA and net profit increased by 7.9% and 6.4% to reach at KD3.03mn and KD2.7mn respectively.

Global Research - GCC Global Investment House

August 2008 GCC Telecom Sector 25

SudanIn February 2006, Zain acquired 100% of Mobitel in a deal valued at US$1.33bn. Mobitel, Sudan’s first mobile operator was successfully re-branded to Zain in September 2007. Zain’s Sudan operation had a total of 3.883mn customers at the end of 2007, increasing from 2.754mn in 2006. Its revenues increased by 16% to KD224.8mn in FY2007. EBITDA was KD92.2mn which declined by 21.7% and its net profit declined by 22.1% to reach KD74.7mn in FY2007. In 2007, ARPU for Sudan operations declined to US$20 from US$25 in 2006.

Sub-Saharan Africa (Celtel)As of December 31, 2007, Zain’s African operations, through its subsidiary Celtel International – represented 64% of the company’s customer base and registered a 59% increase in total customers. The company’s customer increase was driven primarily by its high growth African operations including Nigeria, Uganda and Tanzania.

NigeriaAs the competition became intense during the first quarter of 2008, Zain Nigeria (formerly Celtel Nigeria) focused on its key strategic initiatives, controlled 31% market share and was able to sustain its no. 2 position in the mobile telecom market. In addition, Zain Nigeria launched its Blackberry offering into the mass market and was the first operator to offer the Blackberry Red Phone. Adopting the One Network with the neighboring countries has led to increased subscriber acquisition. At the end of 2007, Zain Nigeria had a total customer base of 11.042mn, representing an increase of 73.5%. Zain Nigeria’s operation was accounting for 26% of Zain total customer base in 2007. Its revenues increased by 20.5% to KD332.4mn, EBITDA increased by 5.4% KD111.6mn and its net profit declined by 36.7% to KD23.6mn.

Tanzania Zain’s Tanzania operation had over 2.5mn active customers by year end 2007, representing a 65% increase compared to 2006. Its market share was 39% at the end of the year. The operation’s customers accounted for 6% of Zain total customer base. Its revenues increased by 56% to KD75.2mn, EBITDA increased by 55% KD27.6mn and its net profit grew significantly by 96% to KD14.7mn.

Gabon In Zain’s African operations Gabon is a high APRU market which increased to US$33 in 2007 from US$31 for 2006. Zain Gabon had a total of 666,000 active customers by year end 2007, representing a 30% increase compared to 2006. Its revenues increased by 42% to KD66.1mn, EBITDA increased by 26% KD31.7mn and its net profit grew by 11% to KD14.9mn.

KenyaZain’s Kenya operation had over 2mn active customers by year end 2007, representing an 8% increase over 2006. The operation’s customers accounted for 5% of Zain’s total customer base. In 2007, Zain Kenya’s total revenues grew by 11% to KD55.1mn whereas its EBITDA declined by 38% to KD9mn. It registered an increased net loss of KD6.1mn from KD3.2mn reported for 2006.

Global Research - GCC Global Investment House

26 GCC Telecom Sector August 2008

Other African OperationsIn case of Zain’s Uganda operation the year 2007 was the year of significant achievement as it increased its customer base from 470,000 to over 1.4mn, a growth of 205%. Among Zain’s other major operations in Africa are Democratic republic of Congo which accounted for 5% of the total group revenue. The other major revenue contributors to Zain were Zambia 4.3%, Gabon 3.9%, Tanzania 4.5%, Burkina Faso 1.7%, Niger, Chad and Uganda each contributed 1.6%. Many of these African countries have low penetration rate and offer high growth potential.

Financial Performance In FY2007, Zain reported total revenues of KD1.68bn, EBITDA of KD725.3mn and net profit of KD320.4mn as compared to our projected total revenues of KD1.66bn, EBITDA of KD716.8mn and net profit of KD335.3mn. Zain’s actual performance as compared to our projections for FY2007 showed variations (actual v/s projection) of 1.3% in total revenues, 1.2% in EBITDA, -4.4% in net profit and -4.5% in total assets.

Revenues for the 12-months of FY2007 grew to KD1.68bn, an increase of 29.3% compared to revenues of KD1.3bn reported for FY2006. EBITDA grew to KD725.3mn, an increase of 22.2%, resulting into an EBITDA margin of 43.2%. Its EBITDA margin declined from 45.8% in FY2006 to 43.2% in FY2007. Its finance cost and depreciation & amortization grew by 40.3% and 45.7% to KD123.6mn and KD236.1mn, respectively. Net profit attributable to shareholders of the parent company for FY2007 increased by 8.6% to KD320.4mn as compared to KD295mn reported for FY2006.

In FY2007, the size of consolidated balance sheet of Zain grew by 25.1% to KD4.4bn. Its gross fixed assets increased by 33.3% to reach KD2.3bn. The company’s net intangible assets, represented by goodwill and license fees, increased to KD1.6bn in FY2007 from KD1.5bn for FY2006. The increase in intangibles was mainly due to acquisitions and increase in stake in subsidiaries. In FY2007, the company’s borrowings from banks increased to KD2bn from KD1.4bn in FY2006 which was for its African Celtel operations.

In 1H-2008, Zain Group’s consolidated revenues increased by 17% on y-o-y basis to reach KD936mn. Its EBITDA grew by 10.8% to KD350mn representing an EBITDA margin of 37.4%. Net profit declined from KD149mn reported in 1H-2007 to KD148mn in 1H-2008, witnessing a fall of 0.7%.

Future Trend in Consolidated Revenues & ProfitabilityGoing forward we forecast a 4 year (2007-2011) CAGR of 11.7% in consolidated revenues, 13.7% in EBIDTA and 19.7% in net profit. The contribution of Kuwait operation to the group revenue was 21.4% in 2007, which we expect to decline to 19.7% in 2008, 17.7% in 2009, 16% in 2010 and 14.2% in 2011, due to increasing revenue contribution from other operations.

Global Research - GCC Global Investment House

August 2008 GCC Telecom Sector 27

Chart 3: Trend in Consolidated Revenues, EBITDA and Net Profit

-

500

1,000

1,500

2,000

2,500

3,000

2008 (F) 2009 (F) 2010 (F) 2011 (F)

(in

KD

Mn)

Source: Global Research

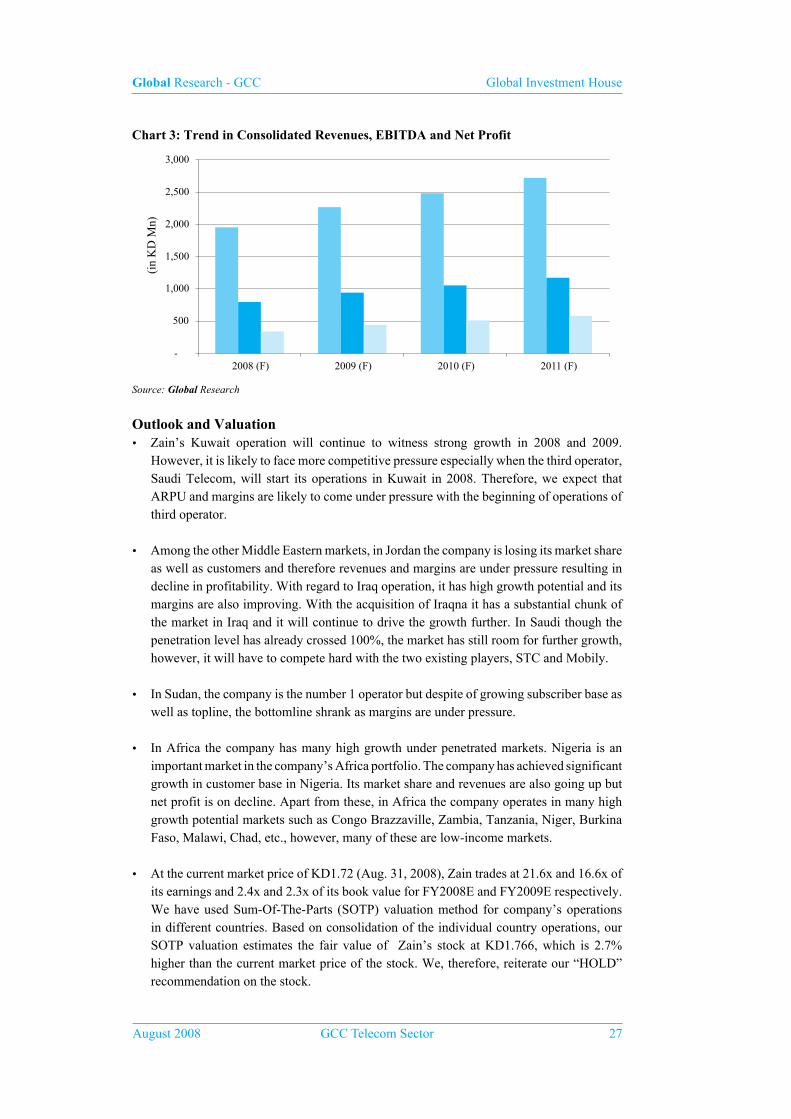

Outlook and Valuation• Zain’s Kuwait operation will continue to witness strong growth in 2008 and 2009.

However, it is likely to face more competitive pressure especially when the third operator, Saudi Telecom, will start its operations in Kuwait in 2008. Therefore, we expect that ARPU and margins are likely to come under pressure with the beginning of operations of third operator.

• Among the other Middle Eastern markets, in Jordan the company is losing its market share as well as customers and therefore revenues and margins are under pressure resulting in decline in profitability. With regard to Iraq operation, it has high growth potential and its margins are also improving. With the acquisition of Iraqna it has a substantial chunk of the market in Iraq and it will continue to drive the growth further. In Saudi though the penetration level has already crossed 100%, the market has still room for further growth, however, it will have to compete hard with the two existing players, STC and Mobily.

• In Sudan, the company is the number 1 operator but despite of growing subscriber base as well as topline, the bottomline shrank as margins are under pressure.

• In Africa the company has many high growth under penetrated markets. Nigeria is an important market in the company’s Africa portfolio. The company has achieved significant growth in customer base in Nigeria. Its market share and revenues are also going up but net profit is on decline. Apart from these, in Africa the company operates in many high growth potential markets such as Congo Brazzaville, Zambia, Tanzania, Niger, Burkina Faso, Malawi, Chad, etc., however, many of these are low-income markets.

• At the current market price of KD1.72 (Aug. 31, 2008), Zain trades at 21.6x and 16.6x of its earnings and 2.4x and 2.3x of its book value for FY2008E and FY2009E respectively. We have used Sum-Of-The-Parts (SOTP) valuation method for company’s operations in different countries. Based on consolidation of the individual country operations, our SOTP valuation estimates the fair value of Zain’s stock at KD1.766, which is 2.7% higher than the current market price of the stock. We, therefore, reiterate our “HOLD” recommendation on the stock.

Global Research - GCC Global Investment House

28 GCC Telecom Sector August 2008

Table 1: SOTP – Valuation Summary

Country Operations Equity Value (in KD mn)

Jordan 454.9

Kuwait 1,798.8

Iraq 305.2

Nigeria 1,071.8

Other African Countries 1,485.4

Sudan 1,164.1

Others 811.8

Cash & Bank Balances 469.0

Total Equity Value 7,561.1

Number of shares outstanding (in mn) 4,280.3

Per share value (KD) 1.766

Source: Global Research

Global Research - GCC Global Investment House

August 2008 GCC Telecom Sector 29

BA

LA

NC

E S

HE

ET

Mob

ile T

elec

omm

unic

atio

ns C

ompa

ny K

SCA

mou

nt in

Kuw

aiti

Din

ar20

05 (

A)

2006

(A

)20

07 (

A)

2008

(F

)20

09 (

F)

2010

(F

)20

11 (

F)

Ass

ets:

B

ank

& c

ash

equi

vale

nts

91,

788,

000

371

,731

,000

1

48,2

26,0

00

325

,938

,789

2

12,9

48,7

85

120

,783

,497

1

25,4

96,6

37

S

hort

-ter

m D

epos

its

201

,091

,000

1

02,5

91,0

00

113

,037

,000

1

80,5

60,1

60

99,

308,

088

101

,790

,790

1

11,9

69,8

69

I

nves

tmen

ts 1

4,56

6,00

0 1

8,45

5,00

0 2

3,00

2,00

0 3

3,58

7,85

2 2

5,19

0,88

9 3

0,22

9,06

7 3

6,27

4,88

0

Tra

de &

bill

ing

rece

ivab

le 6

3,92

1,00

0 1

37,0

96,0

00

170

,718

,000

2

40,5

55,0

89

260

,498

,747

2

91,5

20,6

86

346

,856

,876

Inc

ome

rece

ivab

le 3

,892

,000

4

,760

,000

1

1,66

4,00

0 1

4,65

6,74

6 1

7,00

0,88

6 1

8,61

3,12

9 2

0,42

3,63

9

Oth

er r

ecei

vabl

es 4

9,71

8,00

0 8

1,66

7,00

0 1

06,7

64,0

00

134

,255

,792

1

47,3

41,0

15

161

,313

,783

2

04,2

36,3

90

I

nven

tori

es 7

,025

,000

1

4,79

1,00

0 2

2,04

7,00

0 3

0,44

4,77

8 3

9,59

3,15

0 4

9,65

5,61

2 6

0,81

5,09

4

Pro

visi

on f

or d

oubt

ful d

ebt

(37

,510

,000

) (

39,0

38,0

00)

(42

,870

,000

) (

48,1

63,1

98)

(48

,125

,092

) (

53,2

08,0

50)

(65

,029

,005

)T

otal

Cur

rent

Ass

ets

394

,491

,000

6

92,0

53,0

00

552

,588

,000

9

11,8

36,0

08

753

,756

,468

7

20,6

98,5

12

841

,044

,379

I

nves

tmen

t Sec

uriti

es 1

47,1

11,0

00

134

,842

,000

1

79,4

68,0

00

245

,412

,440

3

06,7

65,5

50

368

,118

,660

4

41,7

42,3

92

I

nves

tmen

ts in

Ass

ocia

tes-

Gro

ss 2

36,3

83,0

00

-

259

,640

,000

3

37,5

32,0

00

421

,915

,000

5

27,3

93,7

50

I

nves

tmen

ts in

Ass

ocia

tes

236

,383

,000

8

,026

,000

2

59,6

40,0

00

337

,532

,000

4

21,9

15,0

00

527

,393

,750

6

59,2

42,1

88

L

oan

to a

n as

soci

ate

170

,875

,000

2

42,8

76,0

00

242

,876

,000

2

42,8

76,0

00

242

,876

,000

Fix

ed a

sset

s 4

99,8

53,0

00

1,1

31,1

89,0

00

1,4

95,6

02,0

00

1,9

43,0

20,1

12

2,2

52,4

96,4

17

2,4

16,6

67,9

78

2,5

42,3

95,3

23

I

ntan

gibl

e A

sset

s 7

56,8

38,0

00

1,4

77,5

57,0

00

1,6

37,2

55,0

00

1,6

75,0

34,6

67

1,6

26,0

29,9

05

1,5

77,2

37,2

44

1,5

34,3

50,7

13

D

efer

red

tax

asse

ts 6

,723

,000

4

0,61

8,00

0 6

4,72

4,00

0 8

7,37

7,40

0 1

13,5

90,6

20

124

,949

,682

1

37,4

44,6

50

O

ther

fin

anci

al a

sset

s 1

4,90

8,00

0 6

,648

,000

6

,850

,000

7

,535

,000

8

,288

,500

9

,117

,350

1

0,02

9,08

5 T

otal

Ass

ets

2,0

56,3

07,0

00

3,4

90,9

33,0

00

4,3

67,0

02,0

00

5,4

50,6

23,6

27

5,7

25,7

18,4

60

5,9

87,0

59,1

76

6,4

09,1

24,7

30

Lia

bilit

ies:

T

rade

pay

able

s 5

8,87

7,00

0 1

02,3

10,0

00

142

,587

,000

1

45,7

59,1

35

175

,491

,761

1

81,6

60,0

89

205

,504

,756

Due

to s

uppl

iers

and

oth

er a

ccru

als

150

,676

,000

2

76,9

94,0

00

337

,690

,000

3

00,6

26,1

07

435

,885

,632

5

17,9

90,4

57

627

,527

,526

Oth

er P

ayab

les

31,

362,

000

48,

092,

000

74,

477,

000

87,

455,

481

118

,575

,514

1

29,7

57,2

07

166

,625

,478

Due

to B

anks

248

,417

,000

4

60,7

21,0

00

453

,747

,000

5

33,3

99,2

45

404

,941

,836

3

93,8

47,4

27

363

,137

,989

Due

to m

inor

ity in

tere

st h

olde

rs 1

31,1

54,0

00

155

,262

,000

1

8,50

9,00

0 1

8,50

9,00

0 1

8,50

9,00

0 1

8,50

9,00

0 1

8,50

9,00

0 T

otal

Cur

rent

Lia

bilit

ies

620

,486

,000

1

,043

,379

,000

1

,027

,010

,000

1

,085

,748

,968

1

,153

,403

,743

1

,241

,764

,179

1

,381

,304

,748

Oth

er n

on-c

urre

nt li

abili

ties

21,

016,

000

16,

023,

000

28,

411,

000

48,

080,

990

50,

485,

039

53,

009,

291

55,

659,

756

Def

erre

d ta

x lia

bilit

ies

5,8

79,0

00

9,9

80,0

00

31,

763,

000

36,

527,

450

42,

006,

568

48,

307,

553

55,

553,

686

Lon

g te

rm D

ebt

190

,342

,000

9

21,1

17,0

00

1,5

31,5

12,0

00

1,0

57,1

29,3

55

1,0

39,0

39,8

24

911

,677

,623

8

48,0

87,5

54

Due

to m

inor

ity in

tere

st h

olde

rs -

-

-

-

-

-

-

T

otal

non

-cur

rent

liab

ilitie

s 2

17,2

37,0

00

947

,120

,000

1

,591

,686

,000

1