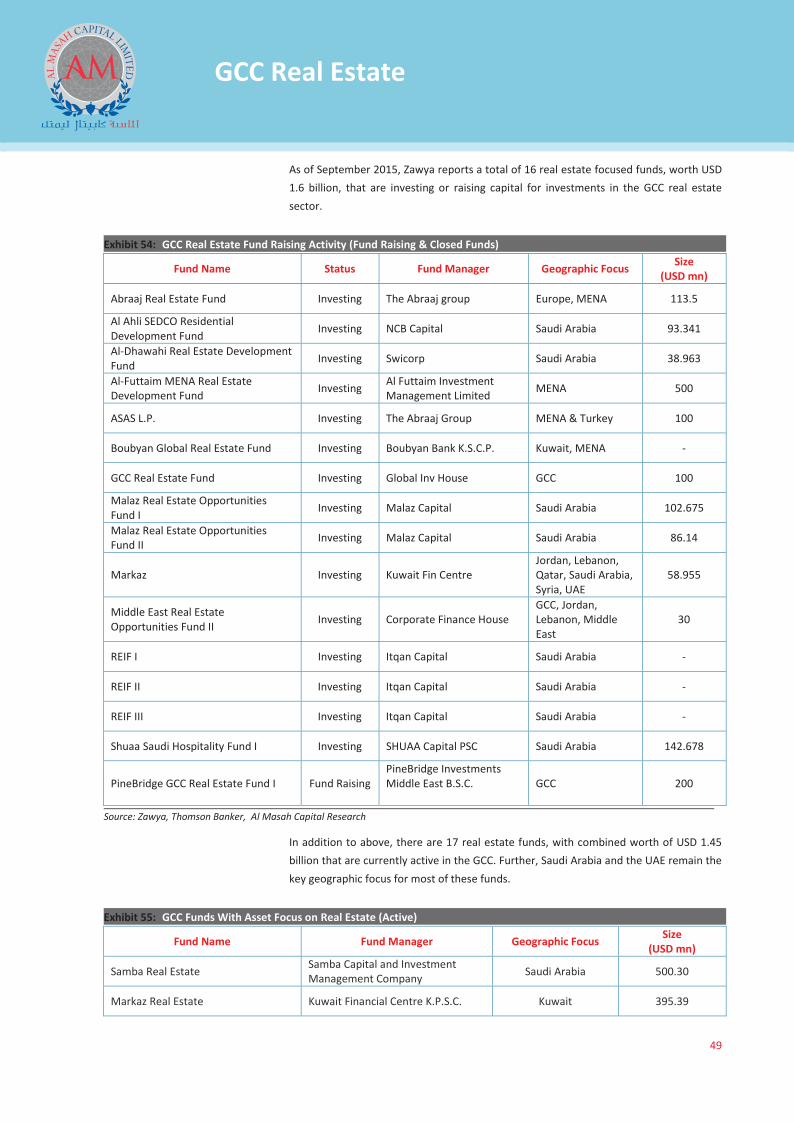

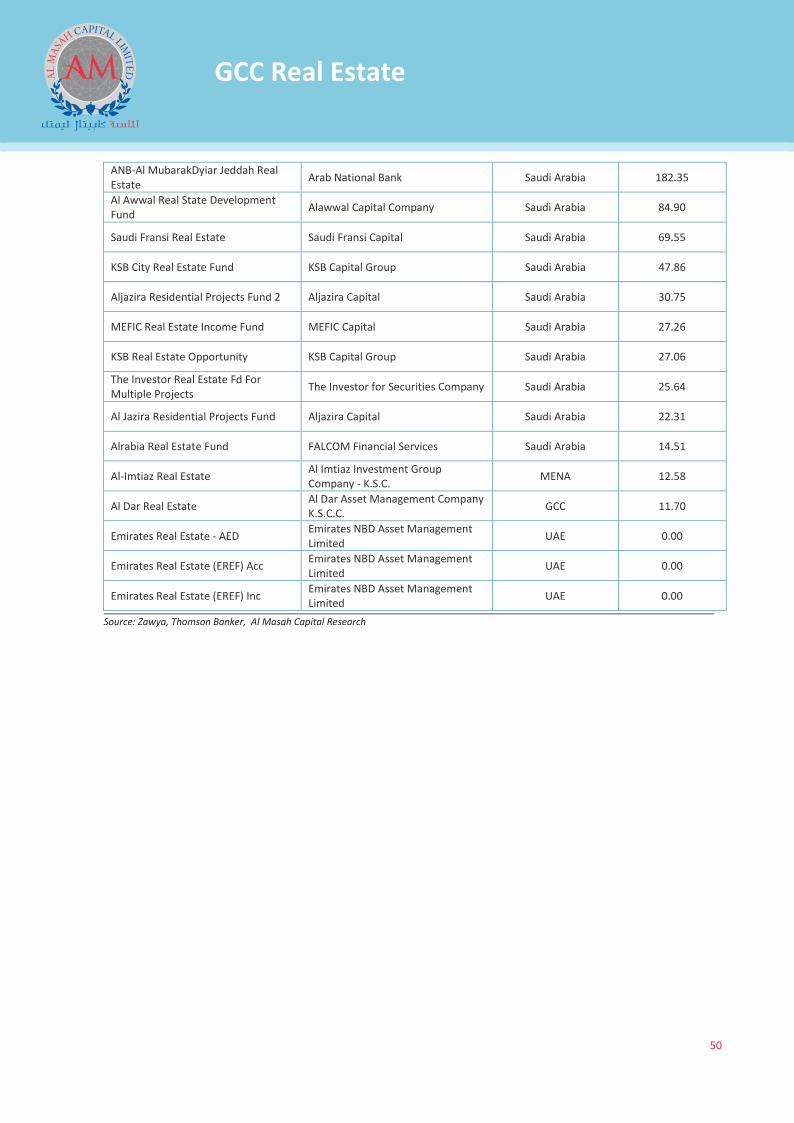

Embed Size (px)

Citation preview

X

51

GCC Real Estate

Al Masah Capital Management Limited

Level 9, Suite 906 & 907 ETA Star - Liberty House Dubai International Financial Centre Dubai-UAE P.O.Box 506838 Tel: +971 4 4531500 Fax: +971 4 4534145 Email: [email protected] Website: www.almasahcapital.com Disclaimer: This report is prepared by Al Masah Capital Management Limited (“AMCML”). AMCML is a company incorporated under the DIFC Companies Law and is regulated by the Dubai Financial Services Authority (“DFSA”). The information contained in this report does not constitute an offer to sell securities or the solicitation of an offer to buy, or recommendation for investment in, any securities in any jurisdiction. The information in this report is not intended as financial advice and is only intended for professionals with appropriate investment knowledge and ones that AMCML is satisfied meet the regulatory criteria to be classified as a ‘Professional Client’ as defined under the Rules & Regulations of the appropriate financial authority. Moreover, none of the report is intended as a prospectus within the meaning of the applicable laws of any jurisdiction and none of the report is directed to any person in any country in which the distribution of such report is unlawful. This report provides general information only. The information and opinions in the report constitute a judgment as at the date indicated and are subject to change without notice. The information may therefore not be accurate or current. The information and opinions contained in this report have been compiled or arrived at from sources believed to be reliable in good faith, but no representation or warranty, express, or implied, is made by AMCML,as to their accuracy, completeness or correctness and AMCML does also not warrant that the information is up to date. Moreover, you should be aware of the fact that investments in undertakings, securities or other financial instruments involve risks. Past results do not guarantee future performance. We accept no liability for any loss arising from the use of material presented in this report. This document has not been reviewed by, approved by or filed with the DFSA. This report or any portion hereof may not be reprinted, sold or redistributed without our prior written consent.

Copyright © 2015 Al Masah Capital Management Limited

Al Masah Capital: GCC Real Estate Sector

December 2015

GCC Real Estate Sector Report_V3 COVER.indd 1 11/10/15 6:59 PM

X

2

GCC Real Estate

GLOBAL REAL ESTATE MARKET

Global real estate market fell back in 2014 due to policy changes in China and other Asia Pacific countries, which led to weakening in land sales. However, sales volumes excluding land sales registered a robust growth courtesy of global liquidity in the markets.

Real estate investment to gain traction in 2015

Global real estate investment fell in 2014 for the first time in 5 years, dropping 6.3% to USD 1.21 trillion from 1.29 trillion in 2013. The slowdown was primarily due to drop in Chinese land purchasing affected by the policy related changes coupled with tightening measured in other APAC markets. Other regions recorded a strong performance with Americas up by 11.4% and Europe, Middle East and Africa (EMEA) up by 11.8% in 2014 as compared to the previous year. Going forward, real estate investment is expected to gain traction in 2015, growing by 11% to reach USD 1.34 trillion driven by increased activity in Americas and EMEA markets.

Exhibit 1: Global Real Estate Investment (2010-15E)

Source: Cushman & Wakefield, Al Masah Capital Research

Offices and hospitality sectors witnessed the strongest investment activity in 2014 followed by retail and industrials. Investments in hospitality sector grew by 16.6% in 2014, accounting for 5.5% of total new investments while office real estate investment accounted for nearly 27% of total new investments in 2014. Multifamily residential sector registered a flat performance on the year with modest US growth offset by falls in Western Europe and parts of Asia.

By fund type, sovereign wealth and private equity funds registered strong growth in real estate investments in 2014. Private equity funds cut spending in Asia and increased their allocation to Southern Europe as well as Western Europe and North America while Sovereign Wealth funds continued to focus in Europe, but investment into North America and Asia grew at a faster pace. Pension funds were also active in 2014 and increased spending in Northern Europe and Australia.

200 220 211 260 291 348 184

272 318 375

417 480 434

437 453

657 502 515

818 928

983

1,292 1,211

1,342

0

200

400

600

800

1,000

1,200

1,400

1,600

2010 2011 2012 2013 2014 2015E

USD bn

Europe, Middle East & Africa Americas Asia Pacific

GCC Real Estate Sector Report_V3.indd 2GCC Real Estate Sector Report_V3.indd 2 11/10/15 6:49 PM11/10/15 6:49 PM

X

3

GCC Real Estate

GCC ECONOMIC OVERVIEW

Booming economy

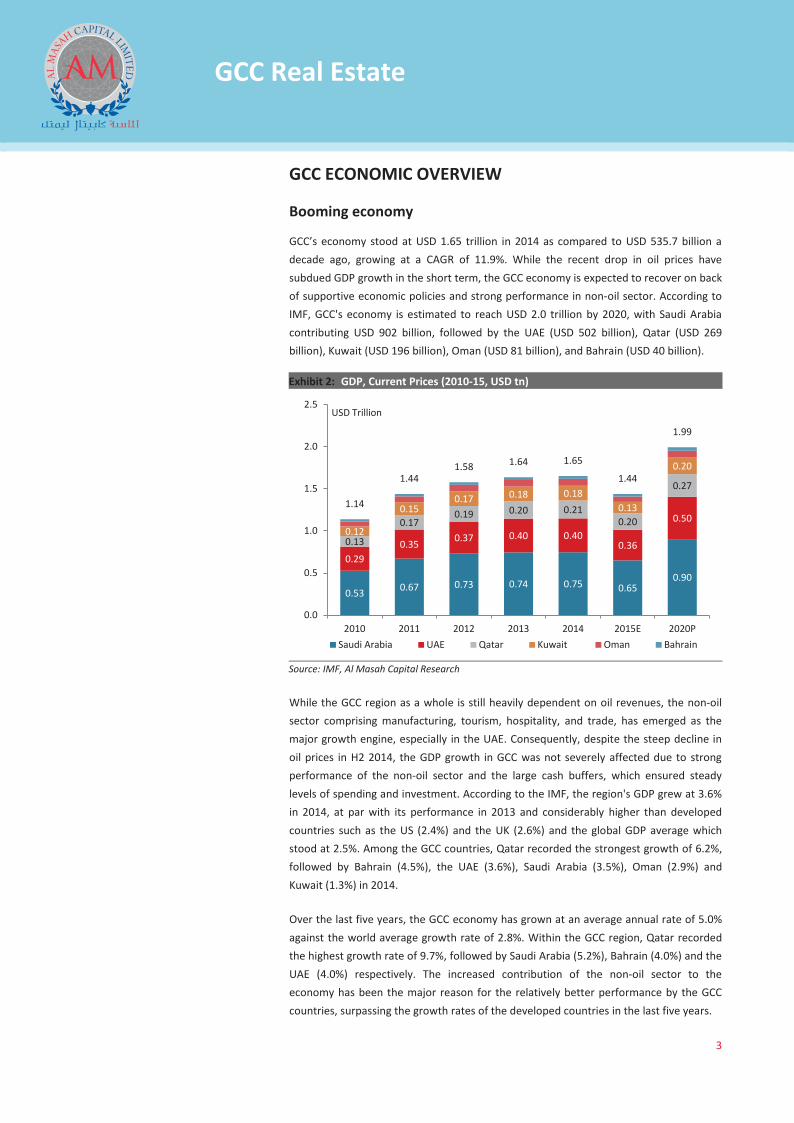

GCC’s economy stood at USD 1.65 trillion in 2014 as compared to USD 535.7 billion a decade ago, growing at a CAGR of 11.9%. While the recent drop in oil prices have subdued GDP growth in the short term, the GCC economy is expected to recover on back of supportive economic policies and strong performance in non-oil sector. According to IMF, GCC's economy is estimated to reach USD 2.0 trillion by 2020, with Saudi Arabia contributing USD 902 billion, followed by the UAE (USD 502 billion), Qatar (USD 269 billion), Kuwait (USD 196 billion), Oman (USD 81 billion), and Bahrain (USD 40 billion).

Exhibit 2: GDP, Current Prices (2010-15, USD tn)

Source: IMF, Al Masah Capital Research

While the GCC region as a whole is still heavily dependent on oil revenues, the non-oil sector comprising manufacturing, tourism, hospitality, and trade, has emerged as the major growth engine, especially in the UAE. Consequently, despite the steep decline in oil prices in H2 2014, the GDP growth in GCC was not severely affected due to strong performance of the non-oil sector and the large cash buffers, which ensured steady levels of spending and investment. According to the IMF, the region's GDP grew at 3.6% in 2014, at par with its performance in 2013 and considerably higher than developed countries such as the US (2.4%) and the UK (2.6%) and the global GDP average which stood at 2.5%. Among the GCC countries, Qatar recorded the strongest growth of 6.2%, followed by Bahrain (4.5%), the UAE (3.6%), Saudi Arabia (3.5%), Oman (2.9%) and Kuwait (1.3%) in 2014.

Over the last five years, the GCC economy has grown at an average annual rate of 5.0% against the world average growth rate of 2.8%. Within the GCC region, Qatar recorded the highest growth rate of 9.7%, followed by Saudi Arabia (5.2%), Bahrain (4.0%) and the UAE (4.0%) respectively. The increased contribution of the non-oil sector to the economy has been the major reason for the relatively better performance by the GCC countries, surpassing the growth rates of the developed countries in the last five years.

0.53 0.67 0.73 0.74 0.75 0.65 0.90

0.29 0.35 0.37 0.40 0.40

0.36

0.50

0.13

0.17 0.19 0.20 0.21

0.20

0.27

0.12

0.15 0.17 0.18 0.18

0.13

0.20

1.14

1.44 1.58 1.64 1.65

1.44

1.99

0.0

0.5

1.0

1.5

2.0

2.5

2010 2011 2012 2013 2014 2015E 2020P

USD Trillion

Saudi Arabia UAE Qatar Kuwait Oman Bahrain

GCC Real Estate Sector Report_V3.indd 3GCC Real Estate Sector Report_V3.indd 3 11/10/15 6:49 PM11/10/15 6:49 PM

X

4

GCC Real Estate

Exhibit 3: Average Annual GDP Growth During the Last Five Years (2010-14)

Source: IMF, Al Masah Capital Research

Continued GDP growth in the region has translated into higher personal income levels. In 2014, GCC’s per capita income grew at 7.6% CAGR to reach USD 33,135 from USD 15,895 in 2004, highlighting the region’s rising affluence levels. The GCC region has a relatively higher per capita income as compared to the world average of around USD 10,804 and MENA average of USD 10,334. Within the GCC region, big differences in per capita income can be observed across the countries. Qatar boasts the highest per capita income of USD 93,397 in the GCC, nearly double of that in the UK (USD 45,603) and the US (USD 54,629). Kuwait has the second largest per capita income in the region of around USD 50,534, followed by the UAE (USD 42,522).

Exhibit 4: Per Capita Income (2014, USD)

Source: IMF, Al Masah Capital Research

9.7%

5.2% 5.0% 4.0% 4.0% 3.5% 3.3% 2.8%

2.2% 1.7%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Qatar SaudiArabia

GCC UAE Bahrain Oman Kuwait WorldAverage

US UK

Average Annual GDP Growth Rate (%)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2004 2009 2014

USD

GCC per Capita Income (USD)

10,334

10,804

20,832

25,409

33,135

42,522

45,603

50,534

54,629

93,397

MENA

World

Oman

Saudi…

GCC

UAE

UK

Kuwait

US

Qatar

Per capita Income (USD)

GCC Real Estate Sector Report_V3.indd 4GCC Real Estate Sector Report_V3.indd 4 11/10/15 6:49 PM11/10/15 6:49 PM

X

5

GCC Real Estate

Favorable Demographics

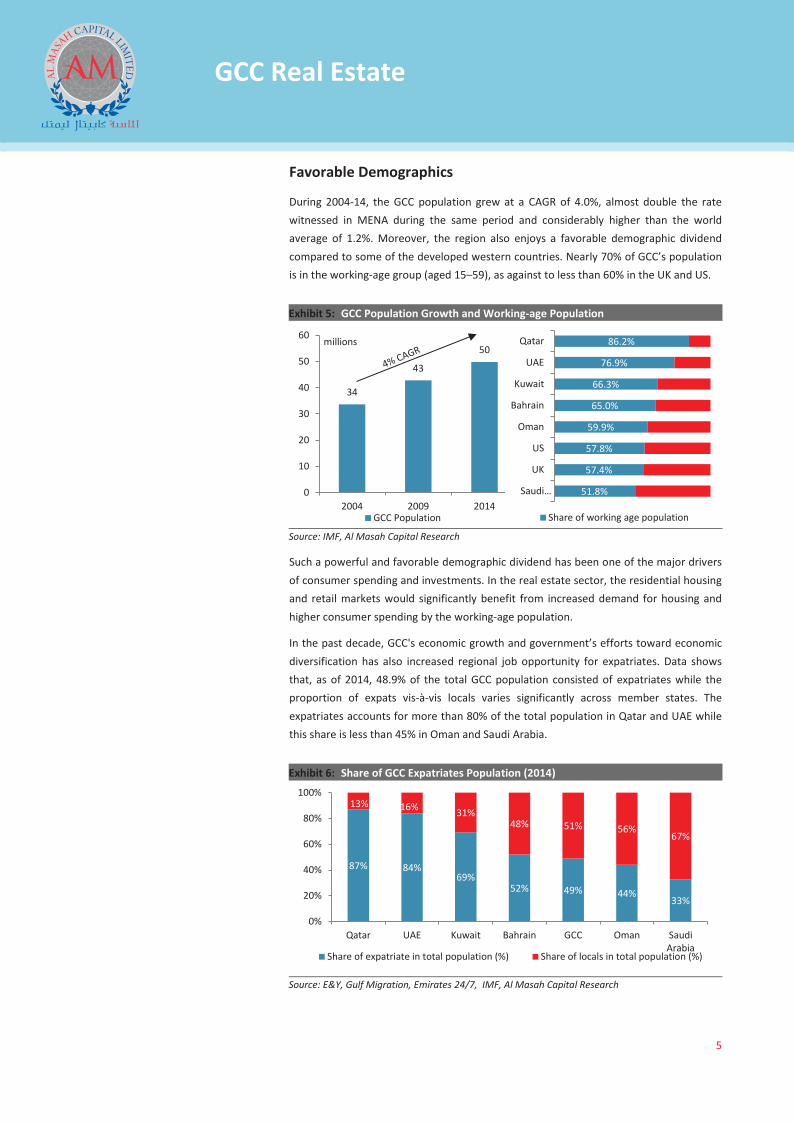

During 2004-14, the GCC population grew at a CAGR of 4.0%, almost double the rate witnessed in MENA during the same period and considerably higher than the world average of 1.2%. Moreover, the region also enjoys a favorable demographic dividend compared to some of the developed western countries. Nearly 70% of GCC’s population is in the working-age group (aged 15–59), as against to less than 60% in the UK and US.

Exhibit 5: GCC Population Growth and Working-age Population

Source: IMF, Al Masah Capital Research

Such a powerful and favorable demographic dividend has been one of the major drivers of consumer spending and investments. In the real estate sector, the residential housing and retail markets would significantly benefit from increased demand for housing and higher consumer spending by the working-age population.

In the past decade, GCC's economic growth and government’s efforts toward economic diversification has also increased regional job opportunity for expatriates. Data shows that, as of 2014, 48.9% of the total GCC population consisted of expatriates while the proportion of expats vis-à-vis locals varies significantly across member states. The expatriates accounts for more than 80% of the total population in Qatar and UAE while this share is less than 45% in Oman and Saudi Arabia.

Exhibit 6: Share of GCC Expatriates Population (2014)

Source: E&Y, Gulf Migration, Emirates 24/7, IMF, Al Masah Capital Research

34

43

50

0

10

20

30

40

50

60

2004 2009 2014

millions

GCC Population

51.8%

57.4%

57.8%

59.9%

65.0%

66.3%

76.9%

86.2%

Saudi…

UK

US

Oman

Bahrain

Kuwait

UAE

Qatar

Share of working age population

87% 84% 69%

52% 49% 44% 33%

13% 16% 31% 48% 51% 56%

67%

0%

20%

40%

60%

80%

100%

Qatar UAE Kuwait Bahrain GCC Oman SaudiArabia

Share of expatriate in total population (%) Share of locals in total population (%)

GCC Real Estate Sector Report_V3.indd 5GCC Real Estate Sector Report_V3.indd 5 11/10/15 6:49 PM11/10/15 6:49 PM

X

6

GCC Real Estate

The expatriate population plays a significant role in the growth of the regional economy with the education and real estate sectors receiving great impetus. The growing expat population has inevitably led to the increase in demand for larger and more luxurious housing which in turn has spurred construction in the premium residential real estate segment. Moreover, the government's decision to allow foreigners to own properties has also surged the real estate demand in the last few years.

Tourism and Upcoming Major Events

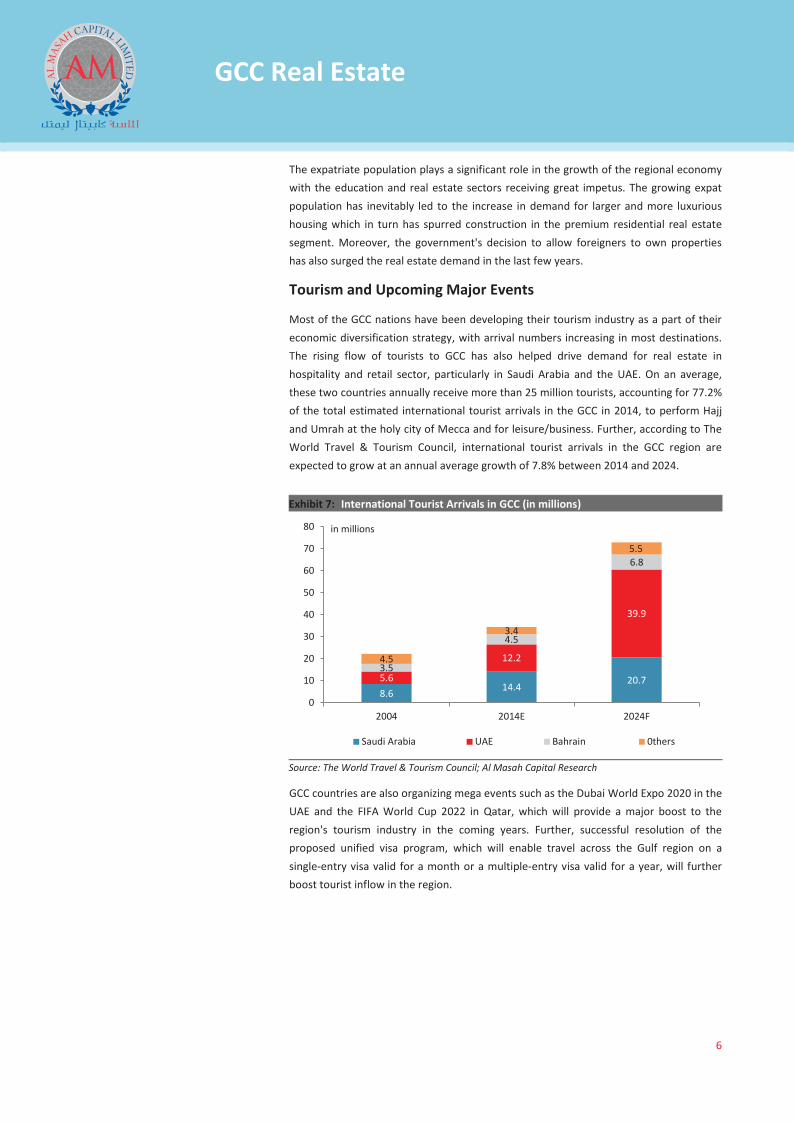

Most of the GCC nations have been developing their tourism industry as a part of their economic diversification strategy, with arrival numbers increasing in most destinations. The rising flow of tourists to GCC has also helped drive demand for real estate in hospitality and retail sector, particularly in Saudi Arabia and the UAE. On an average, these two countries annually receive more than 25 million tourists, accounting for 77.2% of the total estimated international tourist arrivals in the GCC in 2014, to perform Hajj and Umrah at the holy city of Mecca and for leisure/business. Further, according to The World Travel & Tourism Council, international tourist arrivals in the GCC region are expected to grow at an annual average growth of 7.8% between 2014 and 2024.

Exhibit 7: International Tourist Arrivals in GCC (in millions)

Source: The World Travel & Tourism Council; Al Masah Capital Research

GCC countries are also organizing mega events such as the Dubai World Expo 2020 in the UAE and the FIFA World Cup 2022 in Qatar, which will provide a major boost to the region's tourism industry in the coming years. Further, successful resolution of the proposed unified visa program, which will enable travel across the Gulf region on a single-entry visa valid for a month or a multiple-entry visa valid for a year, will further boost tourist inflow in the region.

8.6 14.4 20.7 5.6

12.2

39.9

3.5

4.5

6.8

4.5

3.4

5.5

0

10

20

30

40

50

60

70

80

2004 2014E 2024F

in millions

Saudi Arabia UAE Bahrain 0thers

GCC Real Estate Sector Report_V3.indd 6GCC Real Estate Sector Report_V3.indd 6 11/10/15 6:49 PM11/10/15 6:49 PM

X

7

GCC Real Estate

GCC REAL ESTATE MARKET

Post recession, GCC has emerged as an attractive destination for global investors and the real estate and construction sectors have become key economic barometers for the growth in the region.

REAL ESTATE PROJECTS IN THE GCC

According to Zawya Projects, the total value of ongoing and on-hold real estate projects in the GCC was estimated at USD 1.72 trillion as of September 2015. The UAE led the real estate market accounting for nearly 51% of the total regional projects by value (amounting to USD 0.88 trillion), followed by Saudi Arabia.

Exhibit 8: Value of Real Estate Projects (ongoing and on-hold) in GCC, as of Sept 2015

Source: Zawya Projects, Al Masah Capital Research

In terms of project status, nearly 66% of the GCC projects (by value) are currently ongoing, equating to a total value of USD 1.1 trillion while a substantial portion which equates to USD 0.6 trillion, are on-hold as of September 2015. Going forward, the sluggishness in real estate projects is expected to reduce as both countries have increased their pace in reviving the non-oil sectors, with the real estate industry being the primary benefactor.

Exhibit 9: Real Estate Projects by Status (By Value), as of Sept 2015

Source: Zawya Projects, Al Masah Capital Research

51.1%

26.8%

4.7%

12.6%

2.2%

2.6%

Total Value of Real Estate Projects = USD 1.72 trillion

UAE Saudi Arabia Qatar Kuwait Bahrain Oman

27% 44%

63%

24% 18% 39% 34%

73% 56%

37%

76% 82% 61% 66%

0%

20%

40%

60%

80%

100%

Bahrain Kuwait Oman Qatar Saudi Arabia UAE GCCOn Hold Ongoing

Total Project Value (USD bn)

37.2 217.7 45.2 81.3 460.9 879.4 1721.8

GCC Real Estate Sector Report_V3.indd 7GCC Real Estate Sector Report_V3.indd 7 11/10/15 6:49 PM11/10/15 6:49 PM

X

8

GCC Real Estate

UAE REAL ESTATE SECTOR

Introduction

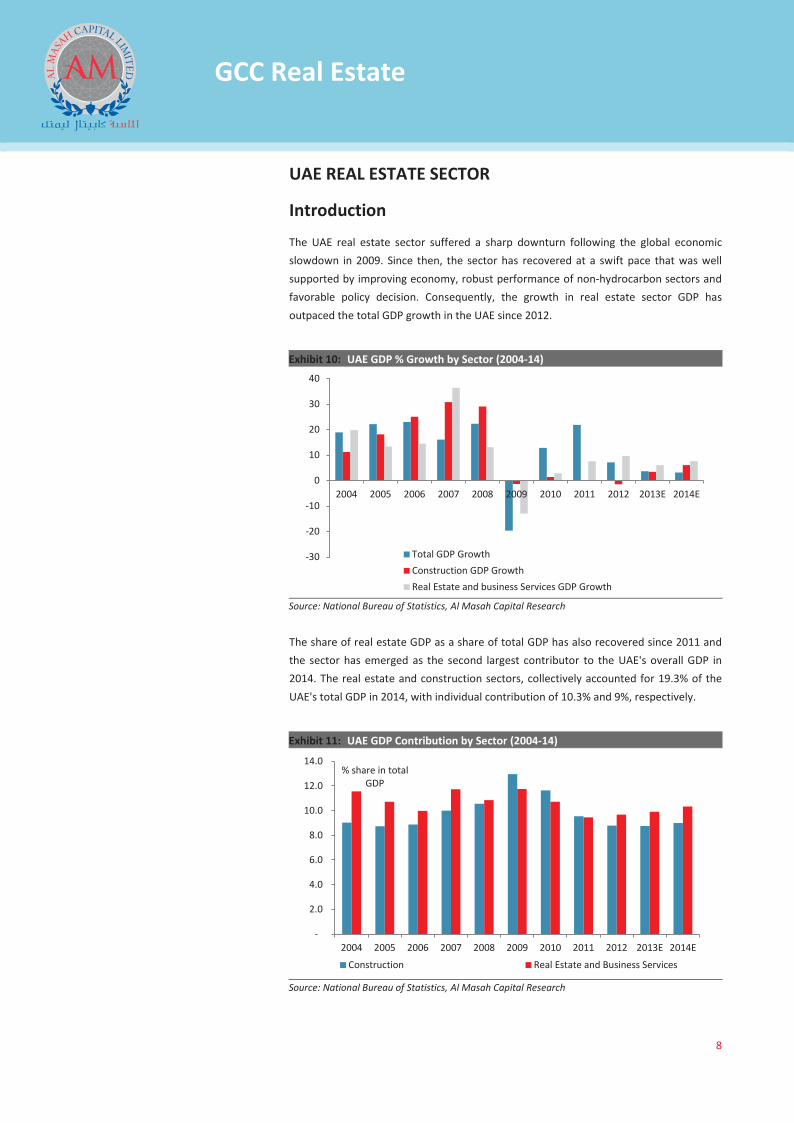

The UAE real estate sector suffered a sharp downturn following the global economic slowdown in 2009. Since then, the sector has recovered at a swift pace that was well supported by improving economy, robust performance of non-hydrocarbon sectors and favorable policy decision. Consequently, the growth in real estate sector GDP has outpaced the total GDP growth in the UAE since 2012.

Exhibit 10: UAE GDP % Growth by Sector (2004-14)

Source: National Bureau of Statistics, Al Masah Capital Research

The share of real estate GDP as a share of total GDP has also recovered since 2011 and the sector has emerged as the second largest contributor to the UAE's overall GDP in 2014. The real estate and construction sectors, collectively accounted for 19.3% of the UAE's total GDP in 2014, with individual contribution of 10.3% and 9%, respectively.

Exhibit 11: UAE GDP Contribution by Sector (2004-14)

Source: National Bureau of Statistics, Al Masah Capital Research

-30

-20

-10

0

10

20

30

40

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014E

Total GDP GrowthConstruction GDP GrowthReal Estate and business Services GDP Growth

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014E

% share in total GDP

Construction Real Estate and Business Services

GCC Real Estate Sector Report_V3.indd 8GCC Real Estate Sector Report_V3.indd 8 11/10/15 6:49 PM11/10/15 6:49 PM

X

9

GCC Real Estate

The recovery in real estate market was also supported by increasing Foreign Direct Investments (FDI) which nearly doubled from AED 30.5 billion in 2007 to AED 71.3 billion in 2014. Foreign portfolio investments (FPI) also recovered from 2009 economic slowdown to reach AED 4 billion in 2012.

Exhibit 12: FDI and FPI in Real Estate Sector (2007-12)

Source: National Bureau of Statistics, Al Masah Capital Research

Impact of Oil Prices

Lower oil prices are leading many in the GCC to wonder about the possible implications for real estate. According to Markit, the seasonally adjusted UAE and Saudi Arabia Purchasing Indices (PMI) remained well above the 50 mark during the last year, suggesting a healthy expansion in the markets’ private non-oil sectors. This is a positive indicator for real estate sector as non-hydrocarbon sector is an important source of demand for property owners in the region.

Exhibit 13: UAE and Saudi Arabia Purchasing Manager Indices (2014-Q2 2015)

Source: Markit, Al Masah Capital Research

Moreover, despite posting huge fiscal deficits, the GCC governments are unlikely to cut back on current levels of spending and will utilize large fiscal reserves to fund infrastructure projects. These large publicly funded, infrastructure-related schemes tend to stimulate hinterland construction activity, and thus support growth in the real estate sector.

30.5

39.8 46.2

54.3 59.9

71.3

2.0 5.6 7.3

3.9 4.3 4.0

0

10

20

30

40

50

60

70

80

2007 2008 2009 2010 2011 2012

in AED Billions

Foreign Direct Investments Foreign Porfolio Investments

51.0

54.0

57.0

60.0

63.0

Jan/

14

Feb/

14

Mar

/14

Apr/

14

May

/14

Jun/

14

Jul/1

4

Aug/

14

Sep/

14

Oct

/14

Nov

/14

Dec/

14

Jan/

15

Feb/

15

Mar

/15

Apr/

15

May

/15

Jun/

15

Jul/1

5

Aug/

15

A figure above 50 suggests economic expansion and below implies contraction. 50 means no change on previous month.

Saudi Arabia PMI UAE PMI

GCC Real Estate Sector Report_V3.indd 9GCC Real Estate Sector Report_V3.indd 9 11/10/15 6:49 PM11/10/15 6:49 PM

X

10

GCC Real Estate

Market Statistics

UAE Office Market

As of 2014, the UAE (including Dubai and Abu Dhabi) holds the largest office stock of 10.7 million sqm of GLA in the GCC. While the office market largely remained oversupplied, the availability of good quality office space in prime locations such as Jumeirah Lake Towers, Business Bay, Tecom regions of Dubai, and Al Reem Island, Muroor, Corniche, and Sowwah Square, among others in Abu Dhabi were scarce in 2014.

Exhibit 14: UAE Office Supply (2010-17F)

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

Abu Dhabi real estate continues to offer a good depth and breadth of opportunities for occupiers, although there is a limited pipeline of new office space which will impact the market in the coming years. The supply of both Grade A and B office stock in Abu Dhabi stood at 3.1 million sqm in 2014, growing at a CAGR of 8.95% from 2.2 million sqm in 2010. Though the overall office segment of Abu Dhabi remained an oversupplied market, the city faced a shortage of Grade A office space in 2014. The city is expected to receive fresh supply of 140,000 sqm of GLA office space in 2015 with the total stock rising to 746,000 sqm between 2015 and 2017. With mixed availability of commercial space across the Abu Dhabi market, potential occupiers remain focused on prime Grade A stock, which is sustaining rents at the top end of the market.

In Dubai, business occupier demand remained focused on high quality office space (Grade A) in prime locations due to limited availability within these offerings. The current market expects an increase in the supply of Grade A office space to meet the demand for quality. Single ownership buildings in the city continue to account for the majority of demand, while strata projects remain less popular. The supply of both Grade A and B office stock in Dubai stood at 7.6 million sqm in 2014, growing at a CAGR of 7.93% from 5.6 million sqm in 2010.The area around the Expo 2020 site is expected to benefit most from the new demand, boosted by established infrastructure facilities such as Al Maktoum International Airport and Jebel Ali Free Zone. Dubai International Financial Centre (DIFC), Jumeirah Lakes Towers, Silicon Oasis and Dubai Investment Park are also expected to see new completions during the period. With significant additions anticipated in the Grade A space, Dubai’s office stock is expected to reach a GLA of 8.5

2,2

00

2,5

30

2,9

00

3,0

00

3,1

00

3,2

00

3,3

40

3,6

55

-

1,000

2,000

3,000

4,000

5,000

2010

2011

2012

2013

2014

2015

E

2016

F

2017

F

Completed Future Supply

Abu Dhabi Office Supply (in '000 sqm)

5,6

00

6,3

00

7,1

00

7,4

00

7,6

00

7,8

00

8,5

00

8,7

00

-

2,000

4,000

6,000

8,000

10,000

2010

2011

2012

2013

2014

2015

E

2016

F

2017

F

Completed Future Supply

Dubai Office Supply (in '000 sqm)

GCC Real Estate Sector Report_V3.indd 10GCC Real Estate Sector Report_V3.indd 10 11/10/15 6:49 PM11/10/15 6:49 PM

X

11

GCC Real Estate

million sqm in 2015 and 8.7 million sqm in 2016. The expected fresh supply of office stock stands at 1.24 million sqm between 2015 and 2017.

Exhibit 15: UAE Office Vacancy & Gross Rental Yield Rates (2010-15)

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

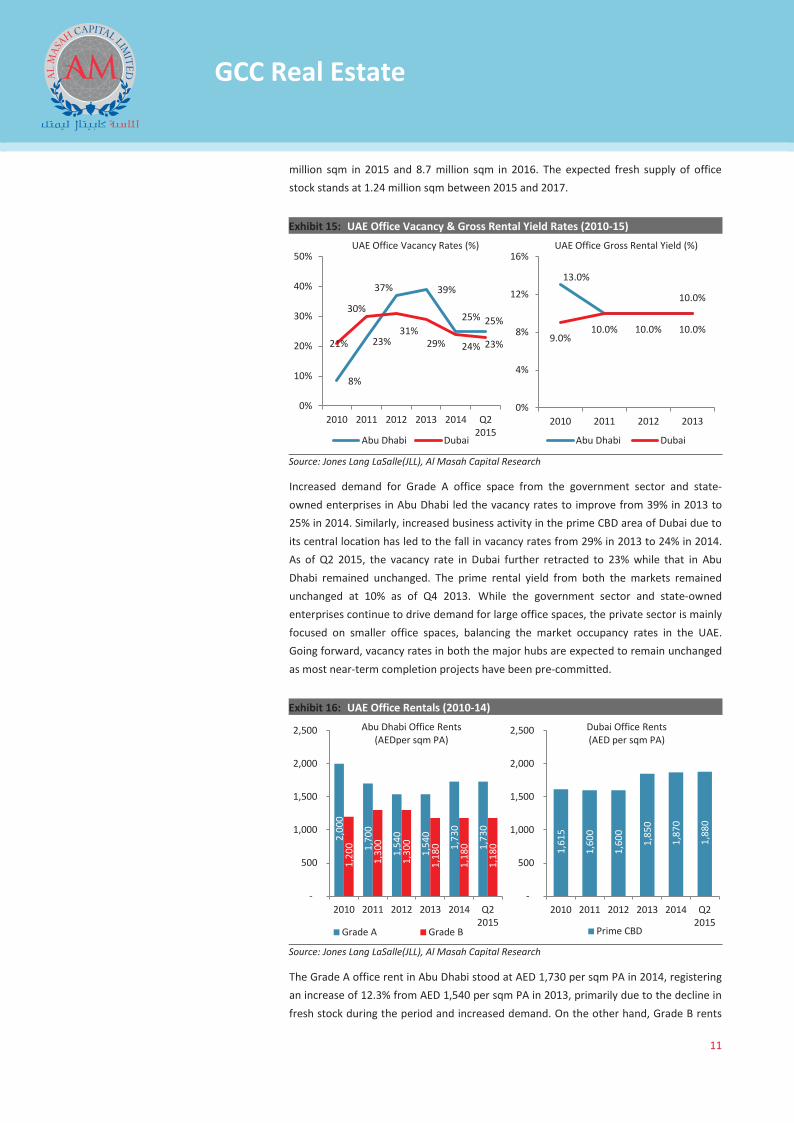

Increased demand for Grade A office space from the government sector and state-owned enterprises in Abu Dhabi led the vacancy rates to improve from 39% in 2013 to 25% in 2014. Similarly, increased business activity in the prime CBD area of Dubai due to its central location has led to the fall in vacancy rates from 29% in 2013 to 24% in 2014. As of Q2 2015, the vacancy rate in Dubai further retracted to 23% while that in Abu Dhabi remained unchanged. The prime rental yield from both the markets remained unchanged at 10% as of Q4 2013. While the government sector and state-owned enterprises continue to drive demand for large office spaces, the private sector is mainly focused on smaller office spaces, balancing the market occupancy rates in the UAE. Going forward, vacancy rates in both the major hubs are expected to remain unchanged as most near-term completion projects have been pre-committed.

Exhibit 16: UAE Office Rentals (2010-14)

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

The Grade A office rent in Abu Dhabi stood at AED 1,730 per sqm PA in 2014, registering an increase of 12.3% from AED 1,540 per sqm PA in 2013, primarily due to the decline in fresh stock during the period and increased demand. On the other hand, Grade B rents

8%

23%

37% 39%

25% 25%

21%

30%

31% 29% 24% 23%

0%

10%

20%

30%

40%

50%

2010 2011 2012 2013 2014 Q22015

Abu Dhabi Dubai

UAE Office Vacancy Rates (%)

13.0%

10.0% 10.0% 10.0% 9.0%

10.0%

0%

4%

8%

12%

16%

2010 2011 2012 2013

Abu Dhabi Dubai

UAE Office Gross Rental Yield (%)

2,0

00

1,7

00

1,5

40

1,5

40

1,7

30

1,7

30

1,2

00

1,3

00

1,3

00

1,1

80

1,1

80

1,1

80

-

500

1,000

1,500

2,000

2,500

2010 2011 2012 2013 2014 Q22015

Grade A Grade B

Abu Dhabi Office Rents (AEDper sqm PA)

1,6

15

1,6

00

1,6

00

1,8

50

1,8

70

1,8

80

-

500

1,000

1,500

2,000

2,500

2010 2011 2012 2013 2014 Q22015

Prime CBD

Dubai Office Rents (AED per sqm PA)

GCC Real Estate Sector Report_V3.indd 11GCC Real Estate Sector Report_V3.indd 11 11/10/15 6:49 PM11/10/15 6:49 PM

X

12

GCC Real Estate

in the city remained muted in 2014 at AED 1,180 per sqm PA, unchanged from previous year. As of Q2 2015, the rentals of Grade A and Grade B offices remained at the same level as in 2014. Going forward, the rents for Grade B offices are expected decline due to limited demand arising from lower oil prices and uncertain economic conditions.

Similar to Abu Dhabi, Dubai faced a shortage of Grade A office space in 2014. As a result, rents for office space in prime CBD area rose 1.1% in 2014 to reach AED 1,870 per sqm PA from AED 1,850 per sqm PA in the preceding year. However, the increase was marginal during the year as compared to 2013 when the rents witnessed a substantial hike of 15.6% due to limited supply and increased demand. Landlords of prime buildings in Dubai are adopting a more mature approach by gradually increasing asking rents as occupancy rates increase. 2014 saw relatively limited new office supply coming to the market in Dubai, driving rental growth in some areas. As of Q2 2015, the market witnessed a marginal hike in rental space of 0.5% with the current rate standing at AED 1,880 sqm PA, as tenants seek to optimize or rationalize their space requirements and consolidate their operations. With over 277,000 jobs estimated to be created by Dubai Expo 2020, more multinationals and start-ups are expected to establish offices in Dubai, providing a further boost to the commercial market in the forthcoming years.

Abu Dhabi Office Market Rental Growth and Pre-crisis levels

0 0 0 6

16

41 45

54 54

41

0

20

40

60

80

Prime Fitted Prime Shell &Core

Good Typical building Low qualitybuilding

% change during 2013-2014 % decline since pre-crisis levels in 2009

Recent Build Old Stock

12

Dubai Office Market Rental Growth and Pre-crisis levels

11

2 7

18

6 3

18

71

0

55

68

60 58

71

0

10

20

30

40

50

60

70

80

Bur Dubai BusinessBay

DIFC DubaiInvestmen

JumeirahLake To

SheikhZayed Ro

Tecom C

% change during 2013-2014 % decline since pre-crisis levels in 2009

GCC Real Estate Sector Report_V3.indd 12GCC Real Estate Sector Report_V3.indd 12 11/10/15 6:49 PM11/10/15 6:49 PM

X

13

GCC Real Estate

According to Reidin, transaction levels in the office sector increased by 16% compared with 2013 with close to 1,500 deals recorded by the Dubai Land Department in 2014. The most transacted areas were Business Bay, Jumeirah Lake Towers and Tecom C, representing close to 80% of all office transactions in 2014 from 90% in 2013. In terms of size, most transactions in 2014 were for mid-sized offices measuring from 1,000 to 2,000 sqft, representing approximately 50% of all transactions, whereas small units of less than 1,000 sqft represented 30%. Although transaction levels improved, sales price growth remained relatively slow, with a yearly increase of only 9% since Q4 2013, and still 50% lower, on average, than at their peak in 2008.

Exhibit 17: Dubai Average Office Sales (AED per sqft PA, 2008-14)

Source: Asteco, Al Masah Capital Research

In 2015, the UAE office rentals are expected remain stable, which is good news for occupiers. However, vacancy rates will remain significant despite a continued gradual improvement in the strata title market, where different investors own one or more floors. Office rental rates in Dubai remained the highest in the UAE. After taking into consideration the cost and quality of living in Dubai & Abu Dhabi, many companies still opted to setup in Dubai rather than the capital. Sharjah and Al Ain predominantly appeal to local companies operating in these cities and, therefore, demand levels remained relatively subdued.

Some of the major ongoing commercial projects in the UAE includes: Dubai World Central (Dubai), Chemicals Industrial City (Abu Dhabi), Expo 2020 Site (Dubai), Dubai World Central - Aviation City (Dubai) and The Opus (Dubai).

0

1,000

2,000

3,000

4,000

5,000

2008 2009 2010 2011 2012 2013 2014

Business Bay DIFC Dubai Investment Park Jumeirah Lake Towers Tecom C

GCC Real Estate Sector Report_V3.indd 13GCC Real Estate Sector Report_V3.indd 13 11/10/15 6:49 PM11/10/15 6:49 PM

X

14

GCC Real Estate

UAE Residential Market

The UAE’s residential sector remained upbeat buoyed by the positive macroeconomic, regulatory and population factors which continue to drive growth across all the regions. The country is also set to commence an AED 5.7 billion (USD 1.6 billion) affordable residential construction project to accommodate as many as 385,000 expatriate workers in a bid to improve the living standards for expatriates, who are increasingly returning to South Asia due to the rising rents. Further, the government has also proposed a new law that mandates developers to allocate about 15%-20% of their projects to the affordable housing category. The implementation of such positive policy decision will drive the residential market in the country.

Exhibit 18: UAE Residential Supply (2010-17F)

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

Although the demand for residential units in Abu Dhabi stood at approximately 290,000 units for 2014, only 244,000 units were available, demonstrating an undersupply condition in the city’s residential market, including its affordable housing segment. Nevertheless, approximately 6,000 residential units are expected to enter the market by the end of 2015, with the numbers further increasing to 6,000 and 13,000 in 2016 and 2017, respectively. With the resuming of government projects such as Louvre, new regulations for claiming housing benefits, and developers planning to push the on-hold and delayed projects coupled with the launch new ones, the total stock of residential units is expected to increase to 250,000 and 256,000 units by the end of 2015 and 2016, respectively.

As per Colliers International, the gap between residential demand and supply is currently 13.0% in Dubai, indicating an oversupplied market. An additional 52,000 housing units are due to enter the market between 2015 and 2017. Going forward, this increase in supply is expected to be absorbed as the economy gains momentum and the city sees an increase in its expatriate workforce due to upcoming events such as Expo 2020. Nearly 50.0% of these additional units are likely to be targeted towards the upper-mid and higher-end of the market, concentrated across the areas of Business Bay, Dubai Marina, Culture Village, Legends, and Palm Jumeirah, among others.

185

194

225

236

244

244

250

256

-

50

100

150

200

250

300

2010

2011

2012

2013

2014

2015

E

2016

F

2017

F

Completed Future Supply

Abu Dhabi Residential Supply (in '000 units)

323

342

356

366

377

379

395

414

-

100

200

300

400

500

2010

2011

2012

2013

2014

2015

E

2016

F

2017

F

Completed Future Supply

Dubai Residential Supply (in '000 units)

GCC Real Estate Sector Report_V3.indd 14GCC Real Estate Sector Report_V3.indd 14 11/10/15 6:49 PM11/10/15 6:49 PM

X

15

GCC Real Estate

Exhibit 19: UAE Residential Rentals (2010-14)

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

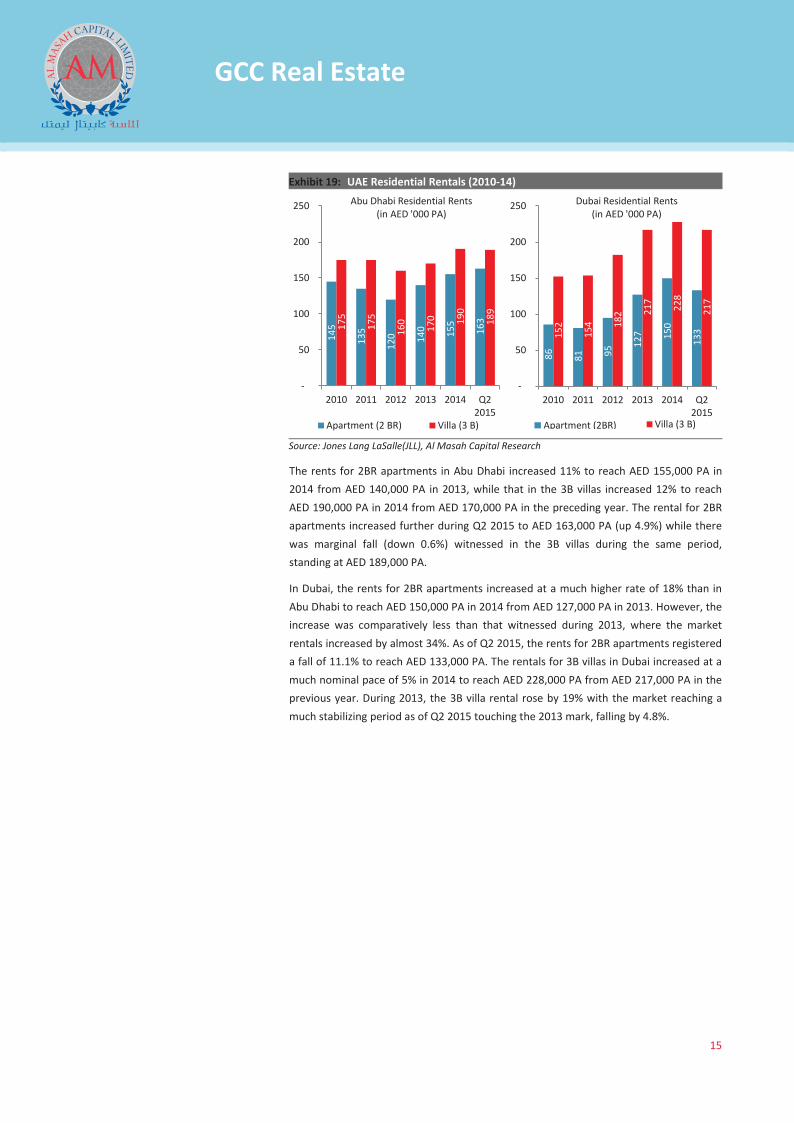

The rents for 2BR apartments in Abu Dhabi increased 11% to reach AED 155,000 PA in 2014 from AED 140,000 PA in 2013, while that in the 3B villas increased 12% to reach AED 190,000 PA in 2014 from AED 170,000 PA in the preceding year. The rental for 2BR apartments increased further during Q2 2015 to AED 163,000 PA (up 4.9%) while there was marginal fall (down 0.6%) witnessed in the 3B villas during the same period, standing at AED 189,000 PA.

In Dubai, the rents for 2BR apartments increased at a much higher rate of 18% than in Abu Dhabi to reach AED 150,000 PA in 2014 from AED 127,000 PA in 2013. However, the increase was comparatively less than that witnessed during 2013, where the market rentals increased by almost 34%. As of Q2 2015, the rents for 2BR apartments registered a fall of 11.1% to reach AED 133,000 PA. The rentals for 3B villas in Dubai increased at a much nominal pace of 5% in 2014 to reach AED 228,000 PA from AED 217,000 PA in the previous year. During 2013, the 3B villa rental rose by 19% with the market reaching a much stabilizing period as of Q2 2015 touching the 2013 mark, falling by 4.8%.

145

135

120

140

155

163

175

175

160

170

190

189

-

50

100

150

200

250

2010 2011 2012 2013 2014 Q22015

Apartment (2 BR) Villa (3 B)

Abu Dhabi Residential Rents (in AED '000 PA)

86

81

95

127

150

133

152

154

182

217

228

217

-

50

100

150

200

250

2010 2011 2012 2013 2014 Q22015

Apartment (3 BR) Villa (3 B)

Dubai Residential Rents (in AED '000 PA)

Apartment (2BR)

GCC Real Estate Sector Report_V3.indd 15GCC Real Estate Sector Report_V3.indd 15 11/10/15 6:49 PM11/10/15 6:49 PM

X

16

GCC Real Estate

Abu Dhabi Residential Rental Growth and Pre-crisis levels

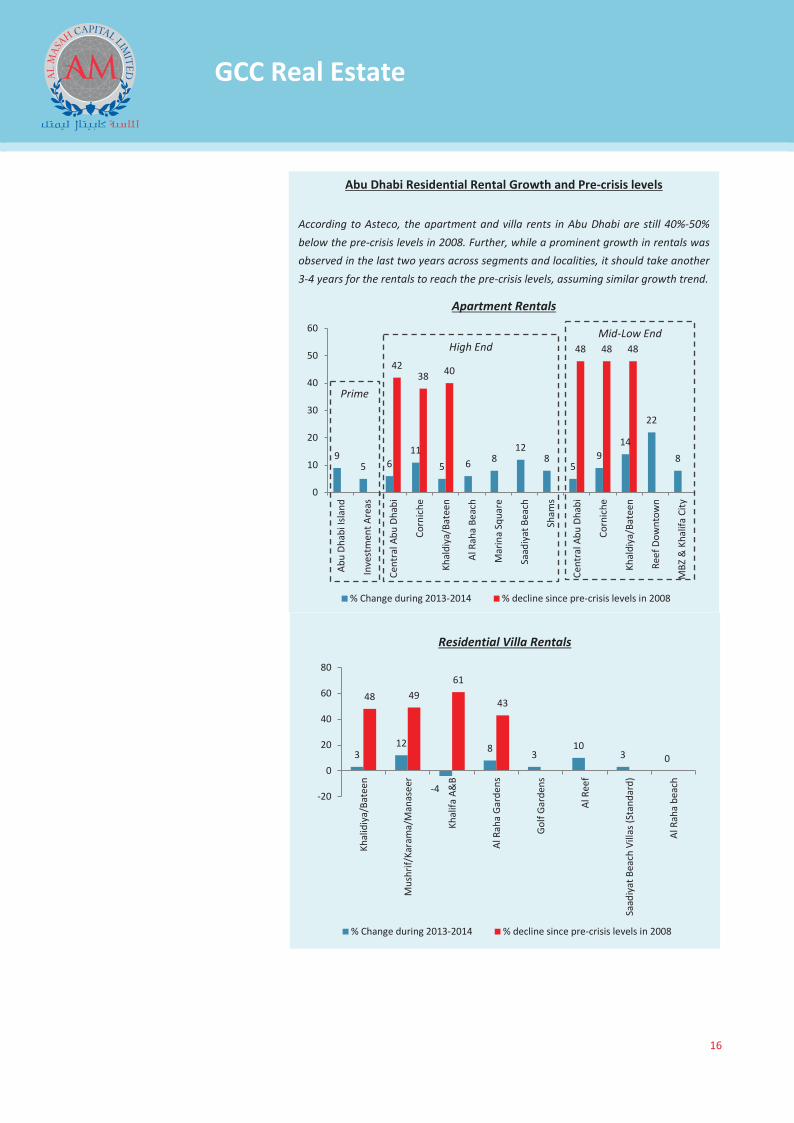

According to Asteco, the apartment and villa rents in Abu Dhabi are still 40%-50% below the pre-crisis levels in 2008. Further, while a prominent growth in rentals was observed in the last two years across segments and localities, it should take another 3-4 years for the rentals to reach the pre-crisis levels, assuming similar growth trend.

Apartment Rentals

9 5 6

11 5 6 8

12 8

5 9

14

22

8

42 38 40

48 48 48

0

10

20

30

40

50

60Ab

u Dh

abi I

sland

Inve

stm

ent A

reas

Cent

ral A

bu D

habi

Corn

iche

Khal

diya

/Bat

een

Al R

aha

Beac

h

Mar

ina

Squa

re

Saad

iyat

Bea

ch

Sham

s

Cent

ral A

bu D

habi

Corn

iche

Khal

diya

/Bat

een

Reef

Dow

ntow

n

MBZ

& K

halif

a Ci

ty

% Change during 2013-2014 % decline since pre-crisis levels in 2008

Prime

High End Mid-Low End

Residential Villa Rentals

3 12

-4

8 3 10

3 0

48 49 61

43

-20

0

20

40

60

80

Khal

idiy

a/Ba

teen

Mus

hrif/

Kara

ma/

Man

asee

r

Khal

ifa A

&B

Al R

aha

Gard

ens

Golf

Gard

ens

Al R

eef

Saad

iyat

Bea

ch V

illas

(Sta

ndar

d)

Al R

aha

beac

h

% Change during 2013-2014 % decline since pre-crisis levels in 2008

GCC Real Estate Sector Report_V3.indd 16GCC Real Estate Sector Report_V3.indd 16 11/10/15 6:49 PM11/10/15 6:49 PM

X

17

GCC Real Estate

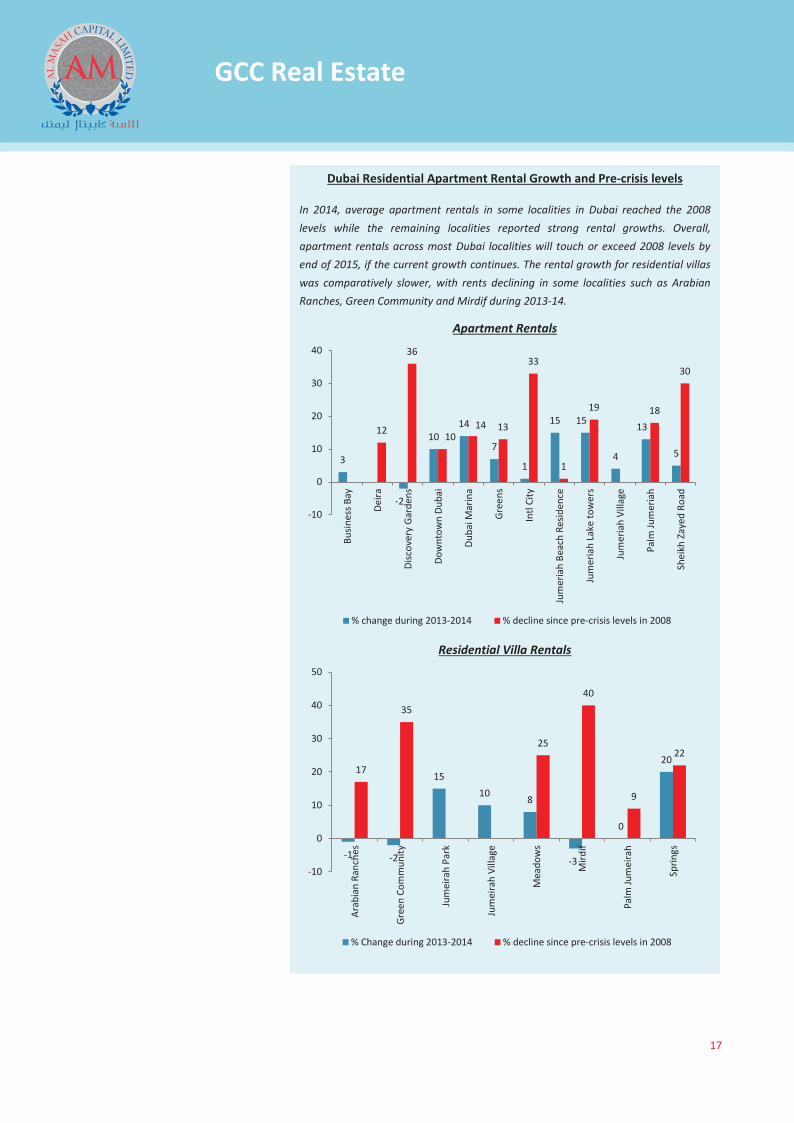

Dubai Residential Apartment Rental Growth and Pre-crisis levels

In 2014, average apartment rentals in some localities in Dubai reached the 2008 levels while the remaining localities reported strong rental growths. Overall, apartment rentals across most Dubai localities will touch or exceed 2008 levels by end of 2015, if the current growth continues. The rental growth for residential villas was comparatively slower, with rents declining in some localities such as Arabian Ranches, Green Community and Mirdif during 2013-14.

Apartment Rentals

3

-2

10 14

7

1

15 15

4

13

5

12

36

10 14 13

33

1

19 18

30

-10

0

10

20

30

40Bu

sines

s Bay

Deira

Disc

over

y Ga

rden

s

Dow

ntow

n Du

bai

Duba

i Mar

ina

Gree

ns

Intl

City

Jum

eria

h Be

ach

Resid

ence

Jum

eria

h La

ke to

wer

s

Jum

eria

h Vi

llage

Palm

Jum

eria

h

Shei

kh Z

ayed

Roa

d

% change during 2013-2014 % decline since pre-crisis levels in 2008

Residential Villa Rentals

-1 -2

15 10 8

-3

0

20 17

35

25

40

9

22

-10

0

10

20

30

40

50

Arab

ian

Ranc

hes

Gree

n Co

mm

unity

Jum

eira

h Pa

rk

Jum

eira

h Vi

llage

Mea

dow

s

Mird

if

Palm

Jum

eira

h

Sprin

gs

% Change during 2013-2014 % decline since pre-crisis levels in 2008

GCC Real Estate Sector Report_V3.indd 17GCC Real Estate Sector Report_V3.indd 17 11/10/15 6:49 PM11/10/15 6:49 PM

X

18

GCC Real Estate

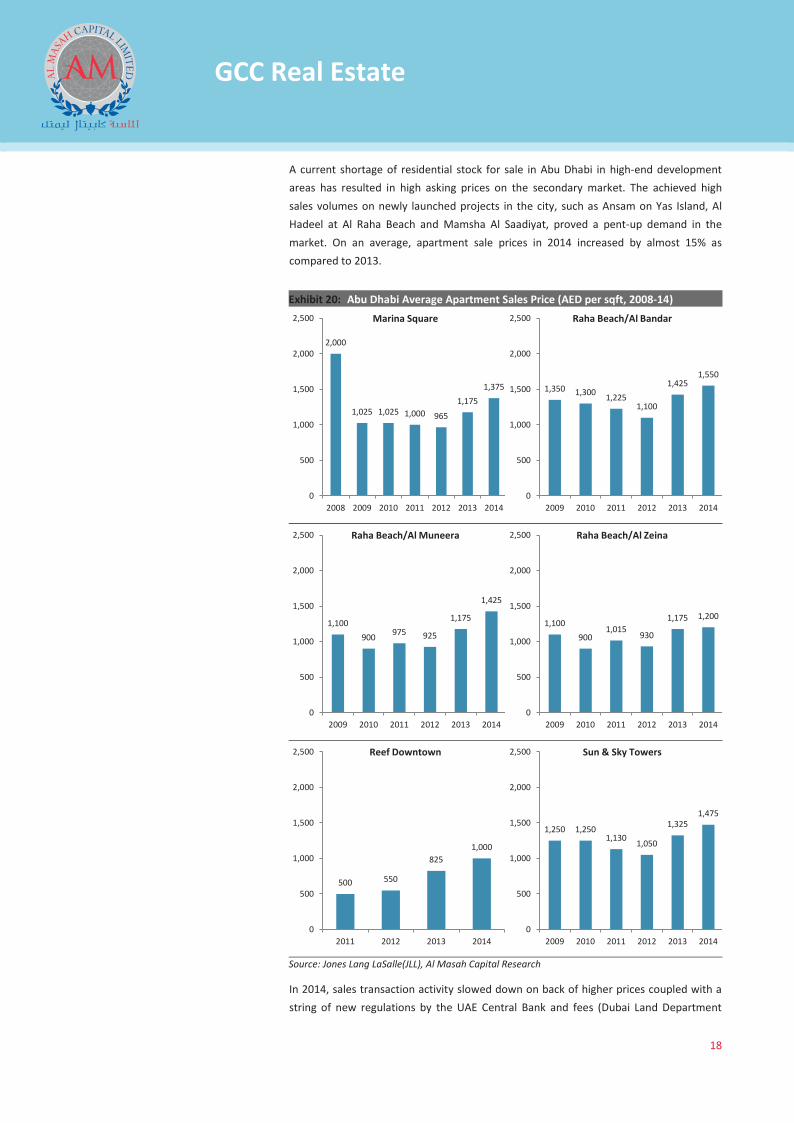

A current shortage of residential stock for sale in Abu Dhabi in high-end development areas has resulted in high asking prices on the secondary market. The achieved high sales volumes on newly launched projects in the city, such as Ansam on Yas Island, Al Hadeel at Al Raha Beach and Mamsha Al Saadiyat, proved a pent-up demand in the market. On an average, apartment sale prices in 2014 increased by almost 15% as compared to 2013.

Exhibit 20: Abu Dhabi Average Apartment Sales Price (AED per sqft, 2008-14)

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

In 2014, sales transaction activity slowed down on back of higher prices coupled with a string of new regulations by the UAE Central Bank and fees (Dubai Land Department

2,000

1,025 1,025 1,000 965

1,175 1,375

0

500

1,000

1,500

2,000

2,500

2008 2009 2010 2011 2012 2013 2014

Marina Square

1,350 1,300 1,225 1,100

1,425 1,550

0

500

1,000

1,500

2,000

2,500

2009 2010 2011 2012 2013 2014

Raha Beach/Al Bandar

1,100 900 975 925

1,175

1,425

0

500

1,000

1,500

2,000

2,500

2009 2010 2011 2012 2013 2014

Raha Beach/Al Muneera

1,100 900

1,015 930

1,175 1,200

0

500

1,000

1,500

2,000

2,500

2009 2010 2011 2012 2013 2014

Raha Beach/Al Zeina

500 550

825 1,000

0

500

1,000

1,500

2,000

2,500

2011 2012 2013 2014

Reef Downtown

1,250 1,250 1,130 1,050

1,325 1,475

0

500

1,000

1,500

2,000

2,500

2009 2010 2011 2012 2013 2014

Sun & Sky Towers

GCC Real Estate Sector Report_V3.indd 18GCC Real Estate Sector Report_V3.indd 18 11/10/15 6:49 PM11/10/15 6:49 PM

X

19

GCC Real Estate

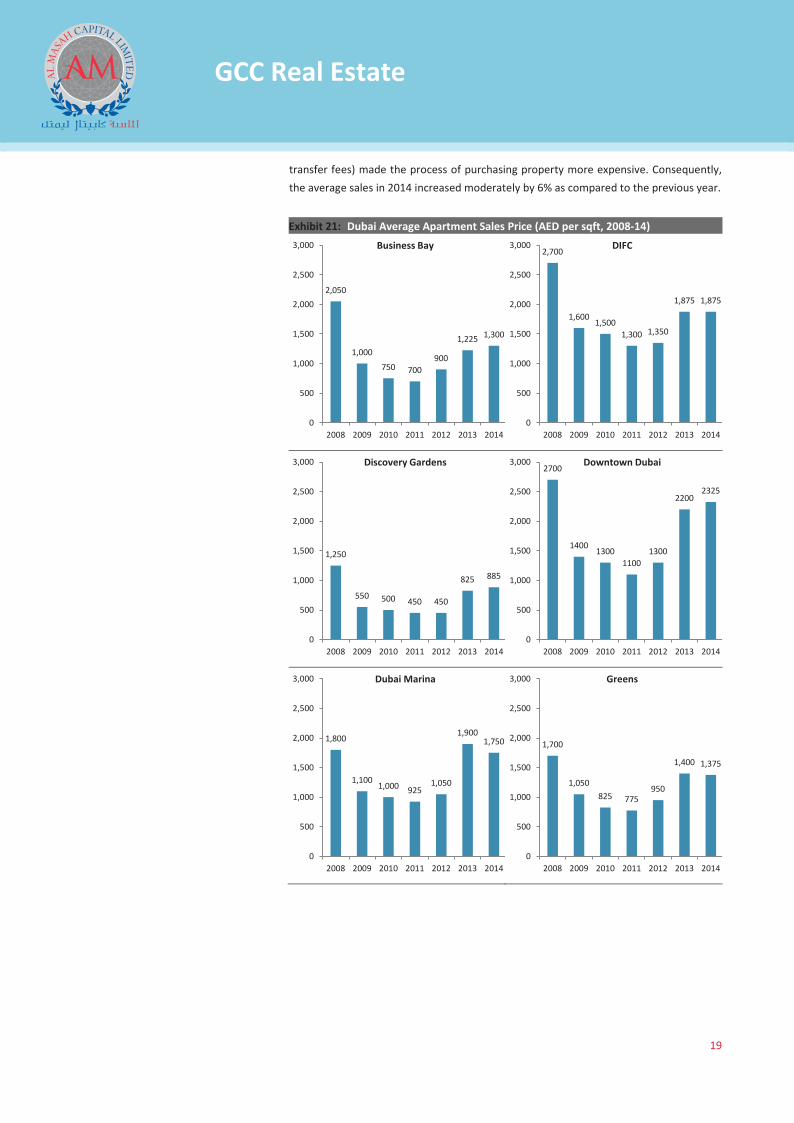

transfer fees) made the process of purchasing property more expensive. Consequently, the average sales in 2014 increased moderately by 6% as compared to the previous year.

Exhibit 21: Dubai Average Apartment Sales Price (AED per sqft, 2008-14)

2,050

1,000

750 700 900

1,225 1,300

0

500

1,000

1,500

2,000

2,500

3,000

2008 2009 2010 2011 2012 2013 2014

Business Bay 2,700

1,600 1,500

1,300 1,350

1,875 1,875

0

500

1,000

1,500

2,000

2,500

3,000

2008 2009 2010 2011 2012 2013 2014

DIFC

1,250

550 500 450 450

825 885

0

500

1,000

1,500

2,000

2,500

3,000

2008 2009 2010 2011 2012 2013 2014

Discovery Gardens 2700

1400 1300

1100 1300

2200 2325

0

500

1,000

1,500

2,000

2,500

3,000

2008 2009 2010 2011 2012 2013 2014

Downtown Dubai

1,800

1,100 1,000 925

1,050

1,900 1,750

0

500

1,000

1,500

2,000

2,500

3,000

2008 2009 2010 2011 2012 2013 2014

Dubai Marina

1,700

1,050 825 775

950

1,400 1,375

0

500

1,000

1,500

2,000

2,500

3,000

2008 2009 2010 2011 2012 2013 2014

Greens

GCC Real Estate Sector Report_V3.indd 19GCC Real Estate Sector Report_V3.indd 19 11/10/15 6:49 PM11/10/15 6:49 PM

X

20

GCC Real Estate

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

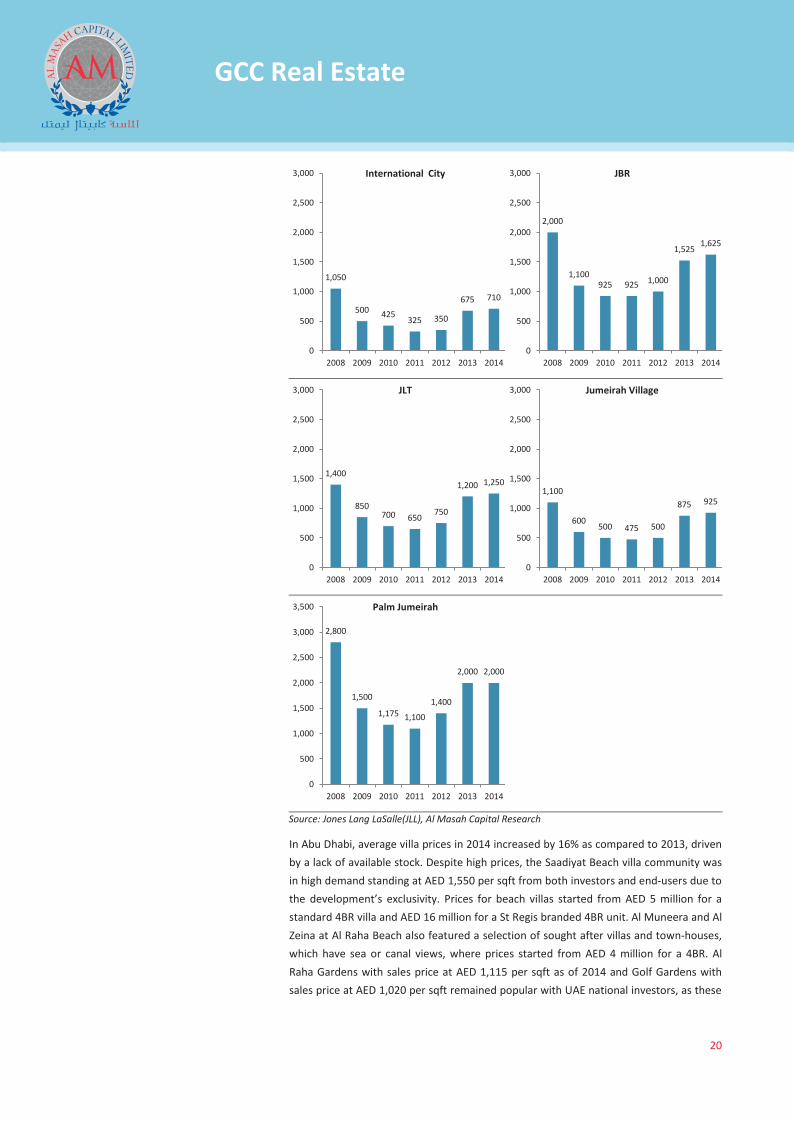

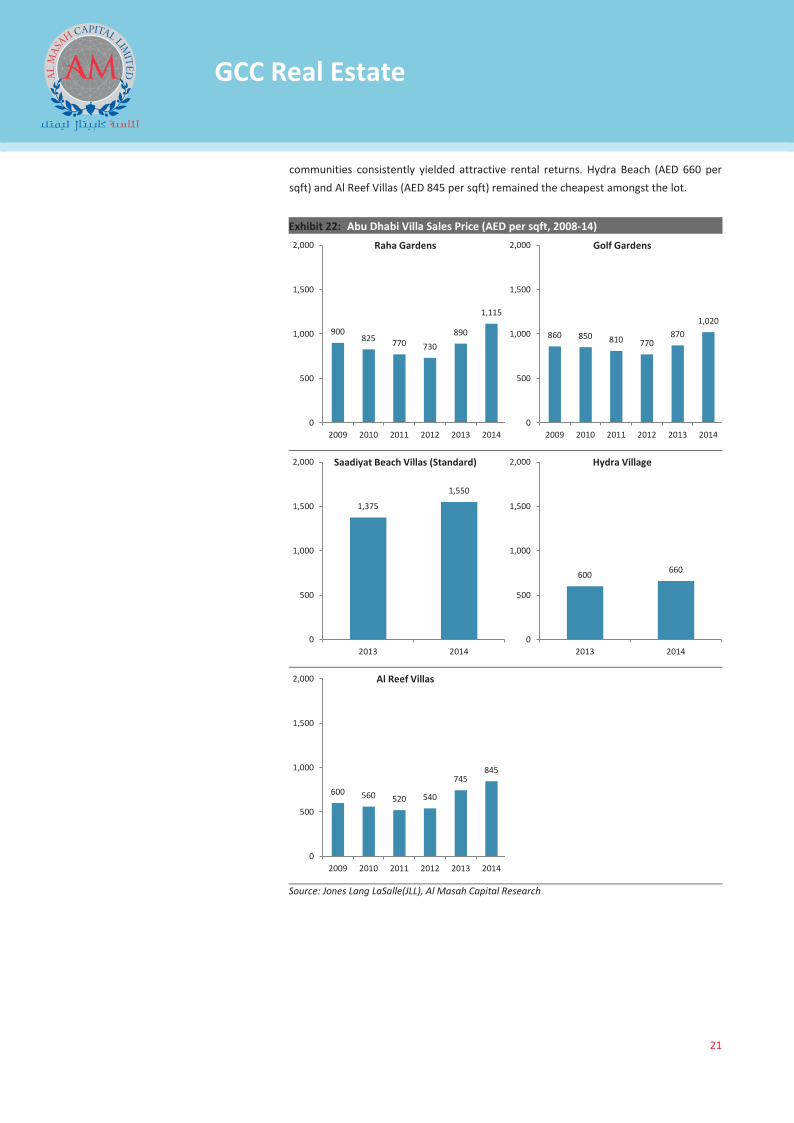

In Abu Dhabi, average villa prices in 2014 increased by 16% as compared to 2013, driven by a lack of available stock. Despite high prices, the Saadiyat Beach villa community was in high demand standing at AED 1,550 per sqft from both investors and end-users due to the development’s exclusivity. Prices for beach villas started from AED 5 million for a standard 4BR villa and AED 16 million for a St Regis branded 4BR unit. Al Muneera and Al Zeina at Al Raha Beach also featured a selection of sought after villas and town-houses, which have sea or canal views, where prices started from AED 4 million for a 4BR. Al Raha Gardens with sales price at AED 1,115 per sqft as of 2014 and Golf Gardens with sales price at AED 1,020 per sqft remained popular with UAE national investors, as these

1,050

500 425 325 350

675 710

0

500

1,000

1,500

2,000

2,500

3,000

2008 2009 2010 2011 2012 2013 2014

International City

2,000

1,100 925 925 1,000

1,525 1,625

0

500

1,000

1,500

2,000

2,500

3,000

2008 2009 2010 2011 2012 2013 2014

JBR

1,400

850 700 650

750

1,200 1,250

0

500

1,000

1,500

2,000

2,500

3,000

2008 2009 2010 2011 2012 2013 2014

JLT

1,100

600 500 475 500

875 925

0

500

1,000

1,500

2,000

2,500

3,000

2008 2009 2010 2011 2012 2013 2014

Jumeirah Village

2,800

1,500

1,175 1,100

1,400

2,000 2,000

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2008 2009 2010 2011 2012 2013 2014

Palm Jumeirah

GCC Real Estate Sector Report_V3.indd 20GCC Real Estate Sector Report_V3.indd 20 11/10/15 6:49 PM11/10/15 6:49 PM

X

21

GCC Real Estate

communities consistently yielded attractive rental returns. Hydra Beach (AED 660 per sqft) and Al Reef Villas (AED 845 per sqft) remained the cheapest amongst the lot.

Exhibit 22: Abu Dhabi Villa Sales Price (AED per sqft, 2008-14)

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

900 825 770 730

890

1,115

0

500

1,000

1,500

2,000

2009 2010 2011 2012 2013 2014

Raha Gardens

860 850 810 770 870

1,020

0

500

1,000

1,500

2,000

2009 2010 2011 2012 2013 2014

Golf Gardens

1,375

1,550

0

500

1,000

1,500

2,000

2013 2014

Saadiyat Beach Villas (Standard)

600 660

0

500

1,000

1,500

2,000

2013 2014

Hydra Village

600 560 520 540

745 845

0

500

1,000

1,500

2,000

2009 2010 2011 2012 2013 2014

Al Reef Villas

GCC Real Estate Sector Report_V3.indd 21GCC Real Estate Sector Report_V3.indd 21 11/10/15 6:49 PM11/10/15 6:49 PM

X

22

GCC Real Estate

In 2014, villa prices in Dubai were stable as compared to 2013. Further, the 2014 average prices were 30% lower than in 2008 levels. For instance, average sale price for Arabian Ranches was AED 2,200 per sqft in 2008 compared to AED 1,150 per sqft in 2014. Palm Jumeirah is the only development that has experienced an increase from its 2008 prices, with rates up by 4%, primarily due to the firm establishment of the Palm as a unique and exclusive villa community, appealing to both local and international buyers.

Exhibit 23: Dubai Average Apartment Sales Price (AED per sqft, 2008-14)

2,200

850 750 750

950

1,225 1,150

0

500

1,000

1,500

2,000

2,500

3,000

2008 2009 2010 2011 2012 2013 2014

Arabian Ranches

1,500

850 750 750

900

1,125 1,250

0

500

1,000

1,500

2,000

2008 2009 2010 2011 2012 2013 2014

Dubai Sport City

1,500

725 650

550

800

1,175 1,175

0

500

1,000

1,500

2,000

2008 2009 2010 2011 2012 2013 2014

Jumeirah Park

1100

600 500 475 500

850

975

0

500

1,000

1,500

2008 2009 2010 2011 2012 2013 2014

Jumeirah Village

2,200

1,000 850 850

1,000

1,300 1,350

0

500

1,000

1,500

2,000

2,500

3,000

2008 2009 2010 2011 2012 2013 2014

Meadows

2,750

1,800 1,550 1,500

1,800

3,000 2,850

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2008 2009 2010 2011 2012 2013 2014

Palm Jumeirah

GCC Real Estate Sector Report_V3.indd 22GCC Real Estate Sector Report_V3.indd 22 11/10/15 6:49 PM11/10/15 6:49 PM

X

23

GCC Real Estate

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

Some of the major ongoing residential projects in the UAE include: The Desert Rose City (Dubai), Al Falah (Abu Dhabi), Habtoor City - Residential Towers (Duabi), North Wathba Development (Abu Dhabi), The Residences at The Marina (Dubai) and DAMAC Towers by Paramount (Duabi).

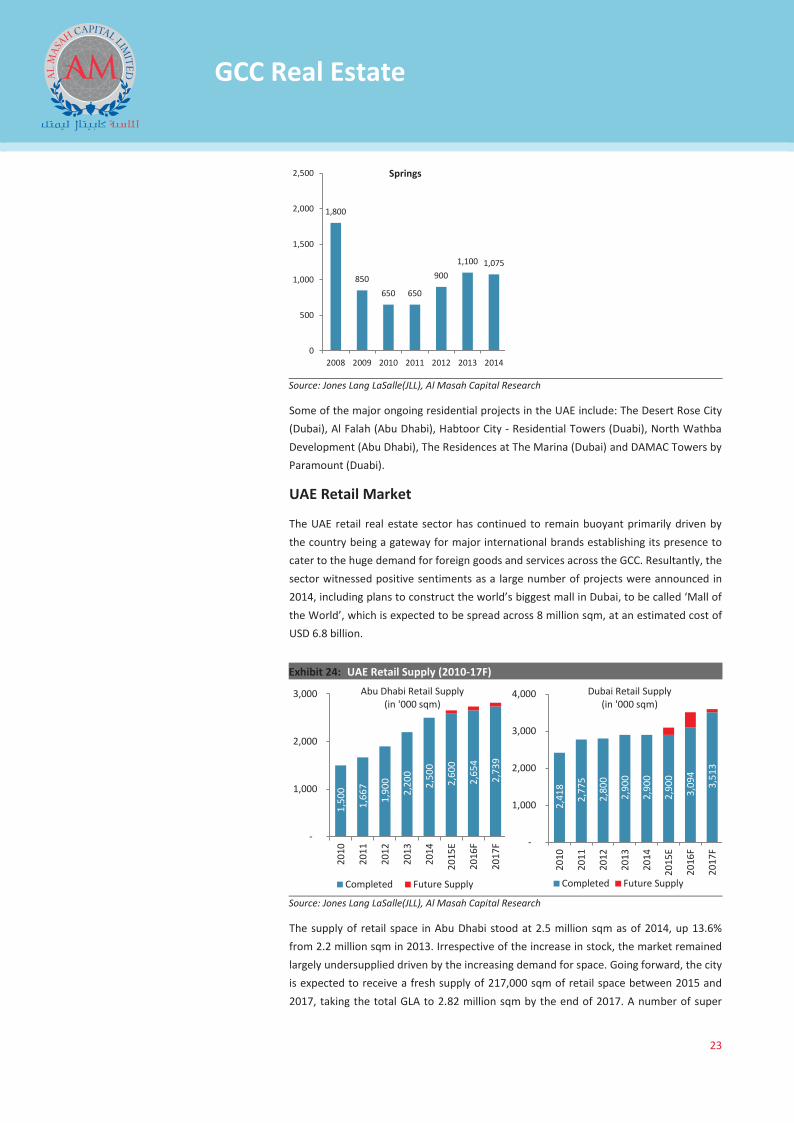

UAE Retail Market

The UAE retail real estate sector has continued to remain buoyant primarily driven by the country being a gateway for major international brands establishing its presence to cater to the huge demand for foreign goods and services across the GCC. Resultantly, the sector witnessed positive sentiments as a large number of projects were announced in 2014, including plans to construct the world’s biggest mall in Dubai, to be called ‘Mall of the World’, which is expected to be spread across 8 million sqm, at an estimated cost of USD 6.8 billion.

Exhibit 24: UAE Retail Supply (2010-17F)

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

The supply of retail space in Abu Dhabi stood at 2.5 million sqm as of 2014, up 13.6% from 2.2 million sqm in 2013. Irrespective of the increase in stock, the market remained largely undersupplied driven by the increasing demand for space. Going forward, the city is expected to receive a fresh supply of 217,000 sqm of retail space between 2015 and 2017, taking the total GLA to 2.82 million sqm by the end of 2017. A number of super

1,800

850 650 650

900 1,100 1,075

0

500

1,000

1,500

2,000

2,500

2008 2009 2010 2011 2012 2013 2014

Springs

1,5

00

1,6

67

1,9

00

2,2

00

2,5

00

2,6

00

2,6

54

2,7

39

-

1,000

2,000

3,000

2010

2011

2012

2013

2014

2015

E

2016

F

2017

F

Completed Future Supply

Abu Dhabi Retail Supply (in '000 sqm)

2,4

18

2,7

75

2,8

00

2,9

00

2,9

00

2,9

00

3,0

94

3,5

13

-

1,000

2,000

3,000

4,000

2010

2011

2012

2013

2014

2015

E

2016

F

2017

F

Completed Future Supply

Dubai Retail Supply (in '000 sqm)

GCC Real Estate Sector Report_V3.indd 23GCC Real Estate Sector Report_V3.indd 23 11/10/15 6:49 PM11/10/15 6:49 PM

X

24

GCC Real Estate

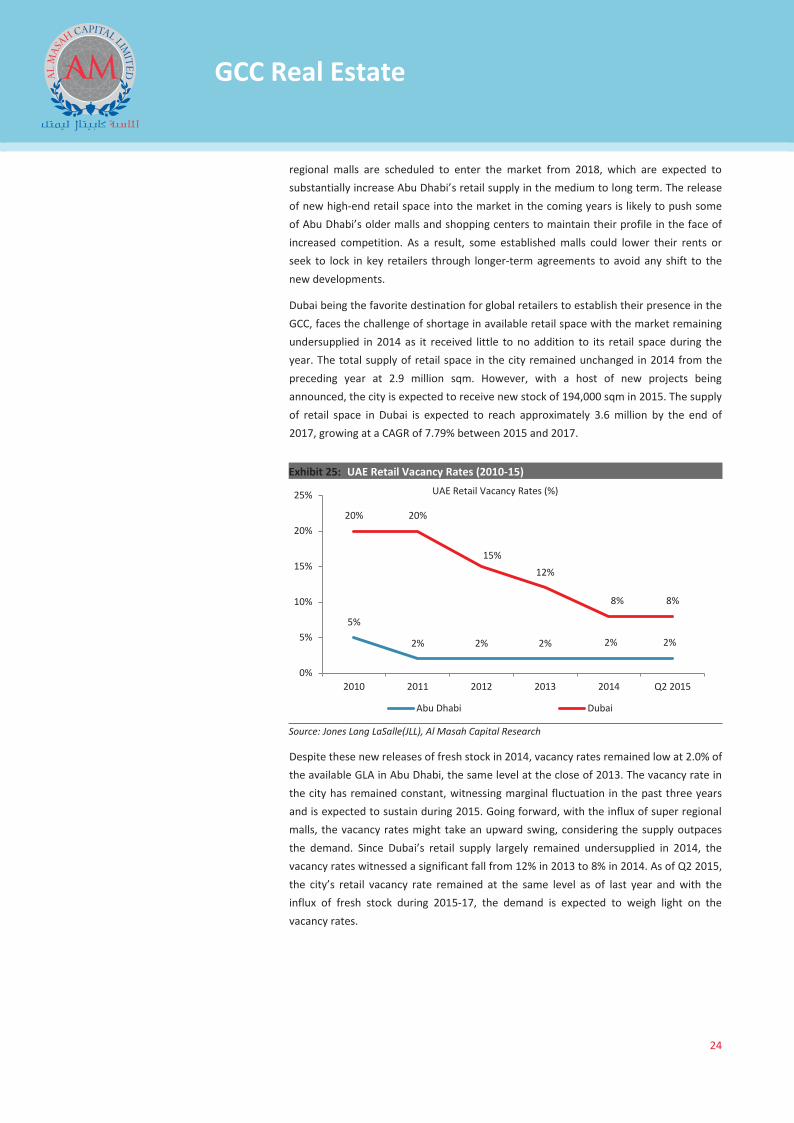

regional malls are scheduled to enter the market from 2018, which are expected to substantially increase Abu Dhabi’s retail supply in the medium to long term. The release of new high-end retail space into the market in the coming years is likely to push some of Abu Dhabi’s older malls and shopping centers to maintain their profile in the face of increased competition. As a result, some established malls could lower their rents or seek to lock in key retailers through longer-term agreements to avoid any shift to the new developments.

Dubai being the favorite destination for global retailers to establish their presence in the GCC, faces the challenge of shortage in available retail space with the market remaining undersupplied in 2014 as it received little to no addition to its retail space during the year. The total supply of retail space in the city remained unchanged in 2014 from the preceding year at 2.9 million sqm. However, with a host of new projects being announced, the city is expected to receive new stock of 194,000 sqm in 2015. The supply of retail space in Dubai is expected to reach approximately 3.6 million by the end of 2017, growing at a CAGR of 7.79% between 2015 and 2017.

Exhibit 25: UAE Retail Vacancy Rates (2010-15)

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

Despite these new releases of fresh stock in 2014, vacancy rates remained low at 2.0% of the available GLA in Abu Dhabi, the same level at the close of 2013. The vacancy rate in the city has remained constant, witnessing marginal fluctuation in the past three years and is expected to sustain during 2015. Going forward, with the influx of super regional malls, the vacancy rates might take an upward swing, considering the supply outpaces the demand. Since Dubai’s retail supply largely remained undersupplied in 2014, the vacancy rates witnessed a significant fall from 12% in 2013 to 8% in 2014. As of Q2 2015, the city’s retail vacancy rate remained at the same level as of last year and with the influx of fresh stock during 2015-17, the demand is expected to weigh light on the vacancy rates.

5%

2% 2% 2% 2% 2%

20% 20%

15%

12%

8% 8%

0%

5%

10%

15%

20%

25%

2010 2011 2012 2013 2014 Q2 2015

Abu Dhabi Dubai

UAE Retail Vacancy Rates (%)

GCC Real Estate Sector Report_V3.indd 24GCC Real Estate Sector Report_V3.indd 24 11/10/15 6:49 PM11/10/15 6:49 PM

X

25

GCC Real Estate

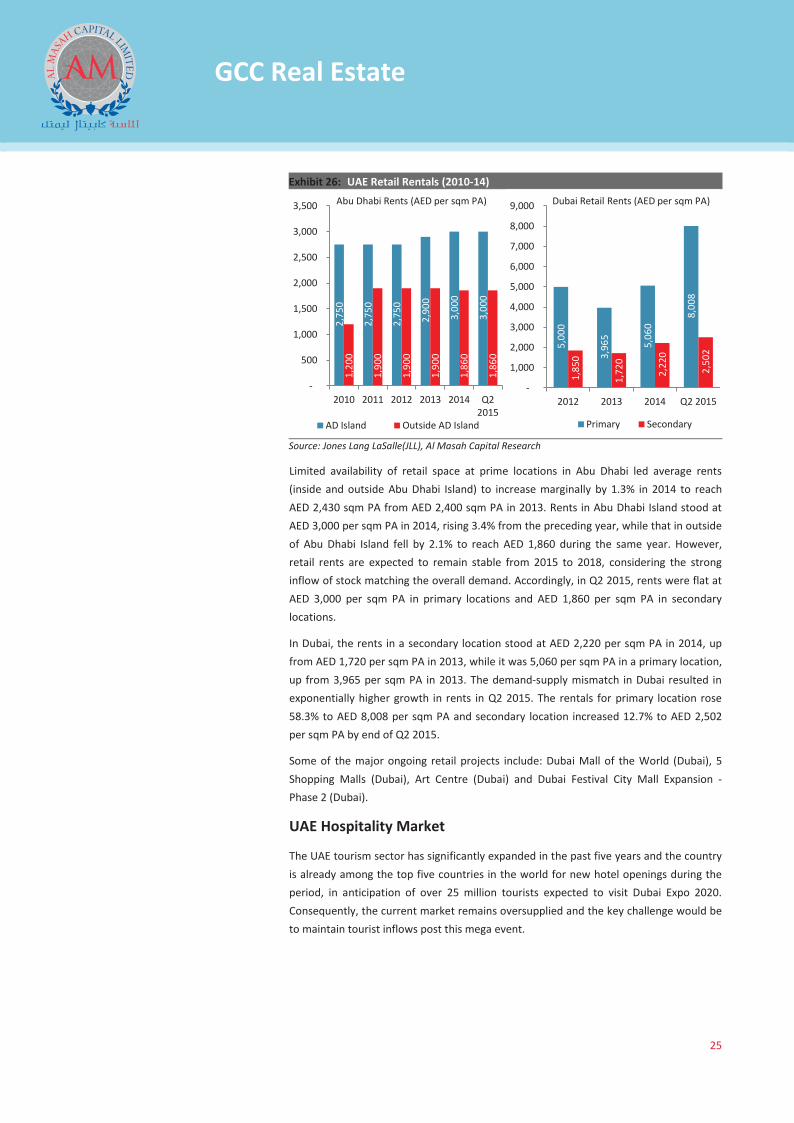

Exhibit 26: UAE Retail Rentals (2010-14)

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

Limited availability of retail space at prime locations in Abu Dhabi led average rents (inside and outside Abu Dhabi Island) to increase marginally by 1.3% in 2014 to reach AED 2,430 sqm PA from AED 2,400 sqm PA in 2013. Rents in Abu Dhabi Island stood at AED 3,000 per sqm PA in 2014, rising 3.4% from the preceding year, while that in outside of Abu Dhabi Island fell by 2.1% to reach AED 1,860 during the same year. However, retail rents are expected to remain stable from 2015 to 2018, considering the strong inflow of stock matching the overall demand. Accordingly, in Q2 2015, rents were flat at AED 3,000 per sqm PA in primary locations and AED 1,860 per sqm PA in secondary locations.

In Dubai, the rents in a secondary location stood at AED 2,220 per sqm PA in 2014, up from AED 1,720 per sqm PA in 2013, while it was 5,060 per sqm PA in a primary location, up from 3,965 per sqm PA in 2013. The demand-supply mismatch in Dubai resulted in exponentially higher growth in rents in Q2 2015. The rentals for primary location rose 58.3% to AED 8,008 per sqm PA and secondary location increased 12.7% to AED 2,502 per sqm PA by end of Q2 2015.

Some of the major ongoing retail projects include: Dubai Mall of the World (Dubai), 5 Shopping Malls (Dubai), Art Centre (Dubai) and Dubai Festival City Mall Expansion - Phase 2 (Dubai).

UAE Hospitality Market

The UAE tourism sector has significantly expanded in the past five years and the country is already among the top five countries in the world for new hotel openings during the period, in anticipation of over 25 million tourists expected to visit Dubai Expo 2020. Consequently, the current market remains oversupplied and the key challenge would be to maintain tourist inflows post this mega event.

2,7

50

2,7

50

2,7

50

2,9

00

3,0

00

3,0

00

1,20

0

1,90

0

1,90

0

1,90

0

1,86

0

1,86

0

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2010 2011 2012 2013 2014 Q22015

AD Island Outside AD Island

Abu Dhabi Rents (AED per sqm PA)

5,0

00

3,9

65

5,0

60 8

,008

1,8

50

1,7

20

2,2

20

2,5

02

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2012 2013 2014 Q2 2015

Primary Secondary

Dubai Retail Rents (AED per sqm PA)

GCC Real Estate Sector Report_V3.indd 25GCC Real Estate Sector Report_V3.indd 25 11/10/15 6:49 PM11/10/15 6:49 PM

X

26

GCC Real Estate

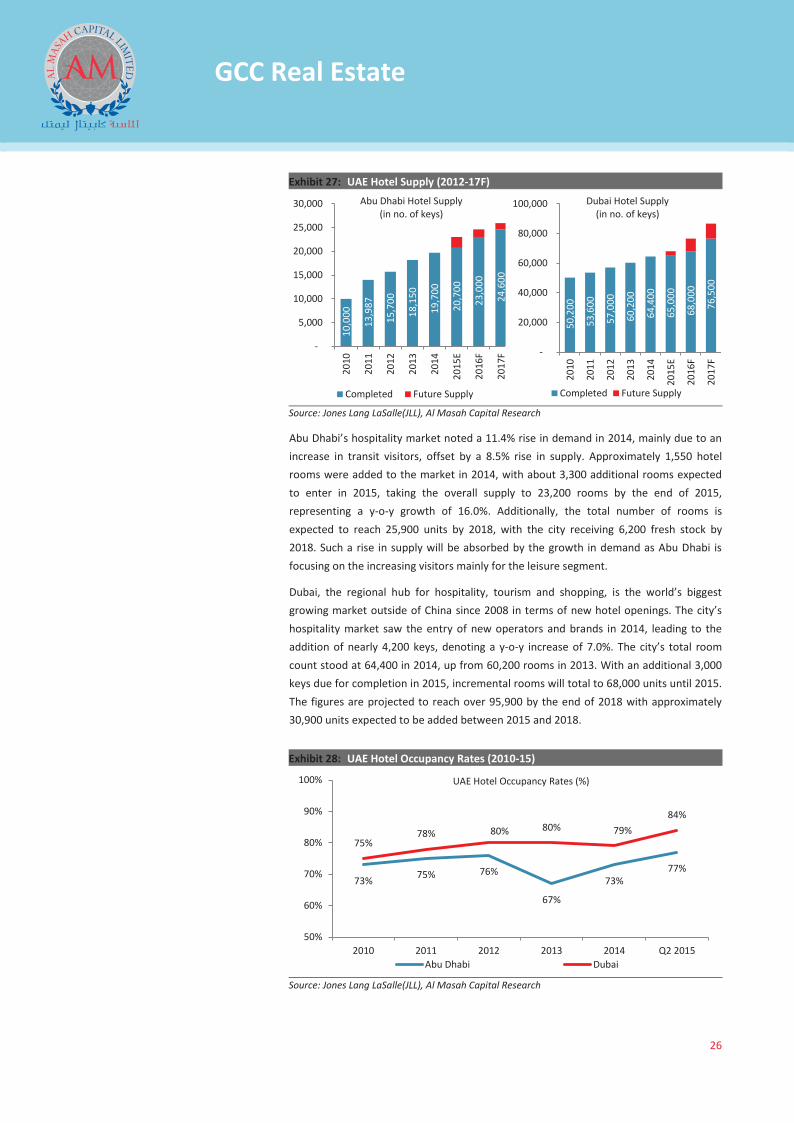

Exhibit 27: UAE Hotel Supply (2012-17F)

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

Abu Dhabi’s hospitality market noted a 11.4% rise in demand in 2014, mainly due to an increase in transit visitors, offset by a 8.5% rise in supply. Approximately 1,550 hotel rooms were added to the market in 2014, with about 3,300 additional rooms expected to enter in 2015, taking the overall supply to 23,200 rooms by the end of 2015, representing a y-o-y growth of 16.0%. Additionally, the total number of rooms is expected to reach 25,900 units by 2018, with the city receiving 6,200 fresh stock by 2018. Such a rise in supply will be absorbed by the growth in demand as Abu Dhabi is focusing on the increasing visitors mainly for the leisure segment.

Dubai, the regional hub for hospitality, tourism and shopping, is the world’s biggest growing market outside of China since 2008 in terms of new hotel openings. The city’s hospitality market saw the entry of new operators and brands in 2014, leading to the addition of nearly 4,200 keys, denoting a y-o-y increase of 7.0%. The city’s total room count stood at 64,400 in 2014, up from 60,200 rooms in 2013. With an additional 3,000 keys due for completion in 2015, incremental rooms will total to 68,000 units until 2015. The figures are projected to reach over 95,900 by the end of 2018 with approximately 30,900 units expected to be added between 2015 and 2018.

Exhibit 28: UAE Hotel Occupancy Rates (2010-15)

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

10,

000

13,

987

15,

700

18,

150

19,

700

20,

700

23,

000

24 ,

600

-

5,000

10,000

15,000

20,000

25,000

30,000

2010

2011

2012

2013

2014

2015

E

2016

F

2017

F

Completed Future Supply

Abu Dhabi Hotel Supply (in no. of keys)

50,

200

53,

600

57,

000

60,

200

64,

400

65,

000

68,

000

76,

500

-

20,000

40,000

60,000

80,000

100,000

2010

2011

2012

2013

2014

2015

E

2016

F

2017

F

Completed Future Supply

Dubai Hotel Supply (in no. of keys)

73% 75% 76%

67%

73% 77%

75% 78% 80% 80% 79%

84%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 Q2 2015Abu Dhabi Dubai

UAE Hotel Occupancy Rates (%)

GCC Real Estate Sector Report_V3.indd 26GCC Real Estate Sector Report_V3.indd 26 11/10/15 6:49 PM11/10/15 6:49 PM

X

27

GCC Real Estate

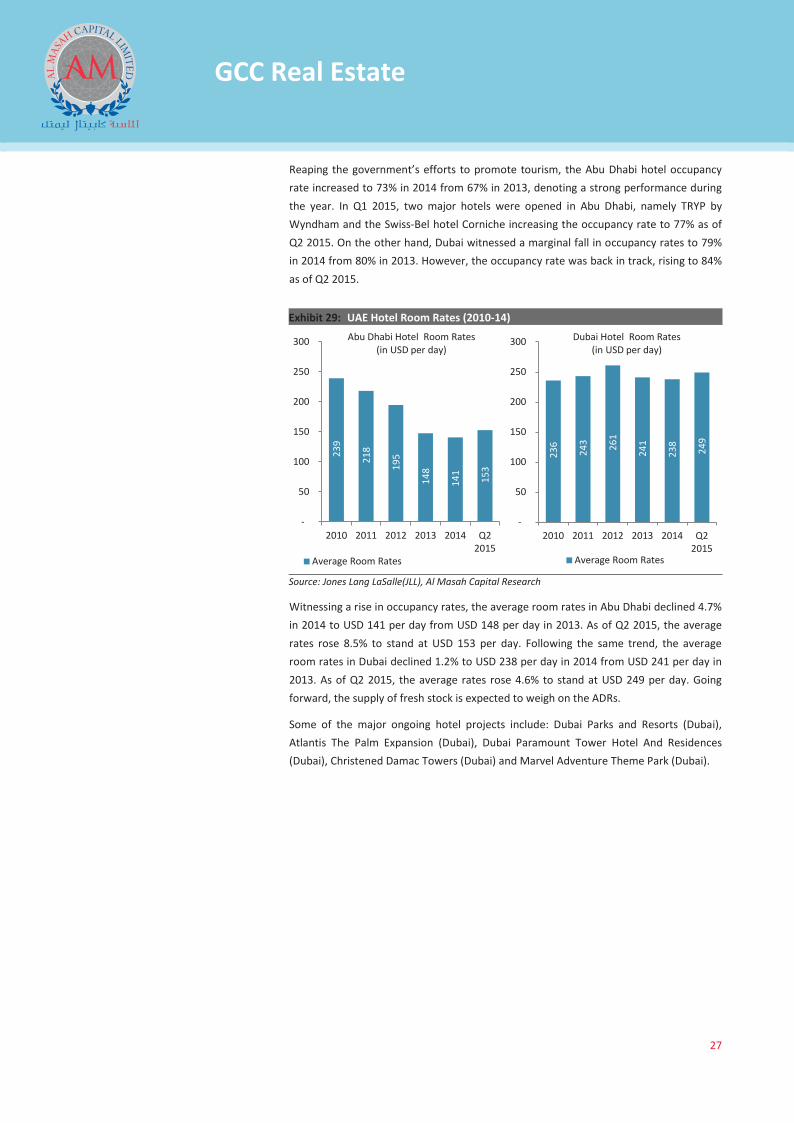

Reaping the government’s efforts to promote tourism, the Abu Dhabi hotel occupancy rate increased to 73% in 2014 from 67% in 2013, denoting a strong performance during the year. In Q1 2015, two major hotels were opened in Abu Dhabi, namely TRYP by Wyndham and the Swiss-Bel hotel Corniche increasing the occupancy rate to 77% as of Q2 2015. On the other hand, Dubai witnessed a marginal fall in occupancy rates to 79% in 2014 from 80% in 2013. However, the occupancy rate was back in track, rising to 84% as of Q2 2015.

Exhibit 29: UAE Hotel Room Rates (2010-14)

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

Witnessing a rise in occupancy rates, the average room rates in Abu Dhabi declined 4.7% in 2014 to USD 141 per day from USD 148 per day in 2013. As of Q2 2015, the average rates rose 8.5% to stand at USD 153 per day. Following the same trend, the average room rates in Dubai declined 1.2% to USD 238 per day in 2014 from USD 241 per day in 2013. As of Q2 2015, the average rates rose 4.6% to stand at USD 249 per day. Going forward, the supply of fresh stock is expected to weigh on the ADRs.

Some of the major ongoing hotel projects include: Dubai Parks and Resorts (Dubai), Atlantis The Palm Expansion (Dubai), Dubai Paramount Tower Hotel And Residences (Dubai), Christened Damac Towers (Dubai) and Marvel Adventure Theme Park (Dubai).

239

218

195

148

141

153

-

50

100

150

200

250

300

2010 2011 2012 2013 2014 Q22015

Average Room Rates

Abu Dhabi Hotel Room Rates (in USD per day)

236

243

261

241

238

249

-

50

100

150

200

250

300

2010 2011 2012 2013 2014 Q22015

Average Room Rates

Dubai Hotel Room Rates (in USD per day)

GCC Real Estate Sector Report_V3.indd 27GCC Real Estate Sector Report_V3.indd 27 11/10/15 6:49 PM11/10/15 6:49 PM

X

28

GCC Real Estate

Real Estate Financing

Despite increase in property prices, real estate lending by UAE banks fell by 1% to reach AED 277 billion in 2014, suggesting that banks’ participation in financing real estate demand was limited during the year. Lending related to completed properties increased 3% to AED 195 billion while lending to properties under construction witnessed a decline of 8% in 2014.

Exhibit 30: Real Estate Lending by UAE Banks (2009-14)

Source: National Bureau of Statistics, Al Masah Capital Research

While the share of individual borrowers in total real estate lending increased from 34% in 2013 to 36% in 2014, overall corporate borrowing for real estate decreased by 2% to reach AED 179 billion in 2014. The major decrease came from developers while hotel related businesses increased their borrowing by more than 20%.

Exhibit 31: Real Estate Lending by Borrower and Property Type (2014)

Source: IMF, Al Masah Capital Research

Most recent changes in banks’ real estate lending reveal limited impact of the current market recovery with bank’s exposure decreasing. Furthermore, bank lending is shifting towards completed properties and as such, becoming less exposed to fluctuations in the residential market and more influenced by general economic conditions.

199

238 241 254 279 277

0

50

100

150

200

250

300

2009 2010 2011 2012 2013 2014

in AED billion

Real Estate Lending by UAE Banks

96 98

183 179

0

50

100

150

200

250

2013 2014

in AED billions

By type of borrower

Individuals Corporates

127 130

83 86

26 32 42 36

0

50

100

150

200

250

2013 2014

in AED billions

By type of property

Residential Non-residential

Hotels Developers

GCC Real Estate Sector Report_V3.indd 28GCC Real Estate Sector Report_V3.indd 28 11/10/15 6:49 PM11/10/15 6:49 PM

X

29

GCC Real Estate

Real Estate Market Sentiments

According to the UAE Real Estate Market Sentiment Survey 2015 conducted by YouGov, the Dubai real estate market will continue the growth momentum over the next 12 months – which is perceived across the board by all respondents including real estate professionals, investors and potential home buyers. Nearly 60% of the investors and 69% of the real estate professionals expressed positive sentiments on the growth of real estate market. Surprisingly among the potential home buyers, younger age categories (18 to 24 years) were more optimistic about growth compared to older age groups (40+ years) - 63% and 49% respectively.

Exhibit 32: Real estate market growth in Dubai (2015 Survey by YouGov)

Source: YouGov, Al Masah Capital Research

From the investors' perspective, the focus on real estate in the portfolio mix is set to continue with a slight increase in real estate investments expected (45%) over the year ahead. As a result, distribution among the rest of investors’ portfolio mix is set to remain comparatively much less, among equities (18%), currencies (16%), commodities (16%), funds/indices (13%) and bonds (13%), according to investors interviewed by YouGov.

Exhibit 33: Investors' Current vs Future Portfolio Mix (2015 Survey by YouGov)

Source: YouGov, Al Masah Capital Research

13%

14%

5%

33%

26%

25%

54%

60%

69%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Potential home buyers

Investors

Real estate professionals

Negative Neutral Positive

13%

13%

16%

16%

18%

45%

11%

13%

14%

15%

19%

43%

0% 10% 20% 30% 40% 5

Bonds

Funds/ Indices

Commodities

Currencies

Equities

Real Estate

Current In the next year

GCC Real Estate Sector Report_V3.indd 29GCC Real Estate Sector Report_V3.indd 29 11/10/15 6:49 PM11/10/15 6:49 PM

X

30

GCC Real Estate

SAUDI ARABIA REAL ESTATE

Saudi Arabia Office Market

Business activities in Saudi Arabia remained buoyant in 2014, with major cities such as Riyadh and Jeddah witnessing a substantial rise in stock and fall in vacancy rates. The average office rents (Grade A and Grade B) in Riyadh witnessed a decline during the year on the back of looming oversupply pressures, while that in Jeddah remained strong increasing substantially from the preceding year.

Exhibit 34: Saudi Arabia Office Supply (2010-17F)

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

The supply of office stock in Riyadh stood at nearly 2.30 million sqm in 2014, growing at a CAGR of 14.25% from 1.35 million sqm in 2010. In view of an increase in supply supplementing the demand, office stock is expected to reach 2.45 million sqm and 2.90 million sqm in 2015 and 2016, respectively. On the other hand, the supply of office stock in Jeddah reached 821,000 sqm in 2014, growing at a CAGR of 23.15% from 357,000 sqm in 2010, imputed by the completion of major projects in the city. Going forward, an additional 104,000 sqm of office space is expected to enter the market in 2015, with further addition of 113,000 sqm in 2016.

Exhibit 35: Saudi Arabia Office Vacancy & Gross Rental Yield Rates (2010-15)

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

1,3

50

1,6

69

1,9

00

2,1

00

2,3

00

2,4

00

2,4

50

2,9

04

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2010

2011

2012

2013

2014

2015

E

2016

F

2017

F

Completed Future Supply

Riyadh Office Supply (in '000 sqm)

357

467

622

715

821

840

944

1,0

57

-

200

400

600

800

1,000

1,200

2010

2011

2012

2013

2014

2015

E

2016

F

2017

F

Completed Future Supply

Jeddah Office Supply (in '000 sqm)

18% 16%

18% 18% 16% 17%

30%

26%

12% 10%

6% 6%

0%

5%

10%

15%

20%

25%

30%

35%

2010 2011 2012 2013 2014 Q22015

Riyadh Jeddah

KSA CBD Office Vacancy Rates (%)

10.3%

10.0% 10.0%

9.5% 9.5%

10.5%

10.0% 10.0%

9%

10%

10%

11%

11%

2010 2011 2012 2013 2014

Riyadh Jeddah

KSA CBD Office Gross Rental Yield (%)

GCC Real Estate Sector Report_V3.indd 30GCC Real Estate Sector Report_V3.indd 30 11/10/15 6:49 PM11/10/15 6:49 PM

X

31

GCC Real Estate

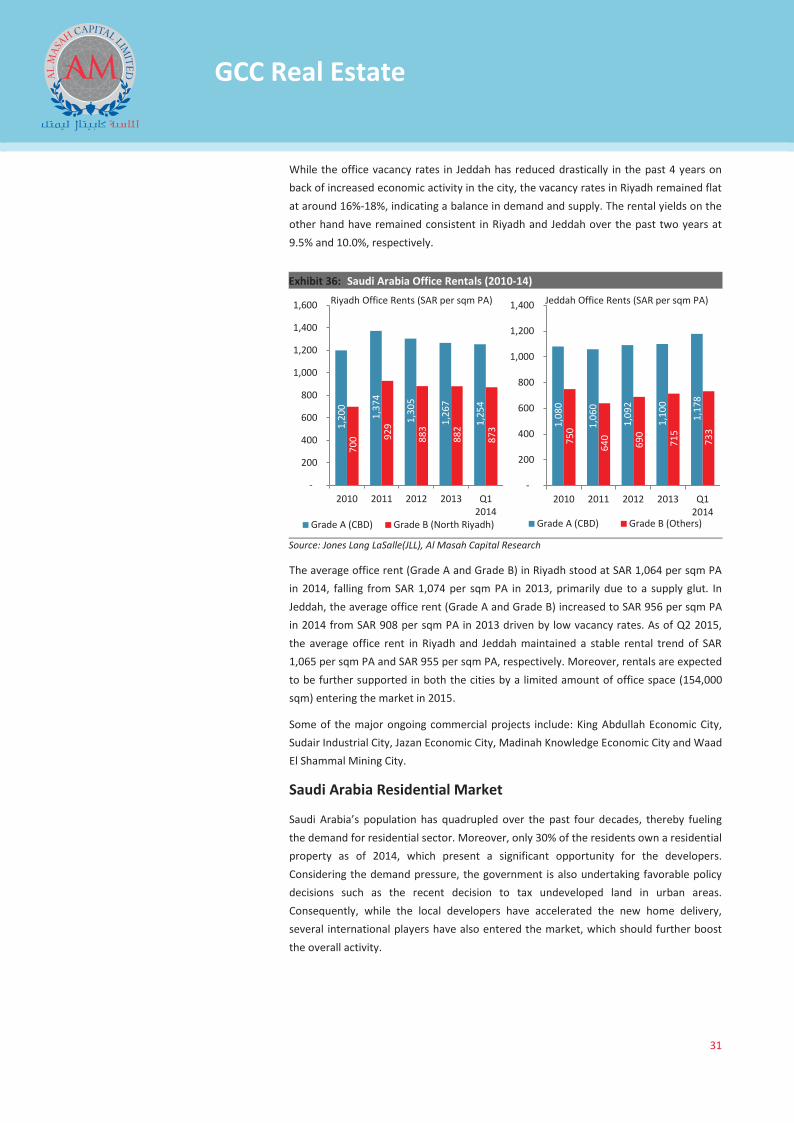

While the office vacancy rates in Jeddah has reduced drastically in the past 4 years on back of increased economic activity in the city, the vacancy rates in Riyadh remained flat at around 16%-18%, indicating a balance in demand and supply. The rental yields on the other hand have remained consistent in Riyadh and Jeddah over the past two years at 9.5% and 10.0%, respectively.

Exhibit 36: Saudi Arabia Office Rentals (2010-14)

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

The average office rent (Grade A and Grade B) in Riyadh stood at SAR 1,064 per sqm PA in 2014, falling from SAR 1,074 per sqm PA in 2013, primarily due to a supply glut. In Jeddah, the average office rent (Grade A and Grade B) increased to SAR 956 per sqm PA in 2014 from SAR 908 per sqm PA in 2013 driven by low vacancy rates. As of Q2 2015, the average office rent in Riyadh and Jeddah maintained a stable rental trend of SAR 1,065 per sqm PA and SAR 955 per sqm PA, respectively. Moreover, rentals are expected to be further supported in both the cities by a limited amount of office space (154,000 sqm) entering the market in 2015.

Some of the major ongoing commercial projects include: King Abdullah Economic City, Sudair Industrial City, Jazan Economic City, Madinah Knowledge Economic City and Waad El Shammal Mining City.

Saudi Arabia Residential Market

Saudi Arabia’s population has quadrupled over the past four decades, thereby fueling the demand for residential sector. Moreover, only 30% of the residents own a residential property as of 2014, which present a significant opportunity for the developers. Considering the demand pressure, the government is also undertaking favorable policy decisions such as the recent decision to tax undeveloped land in urban areas. Consequently, while the local developers have accelerated the new home delivery, several international players have also entered the market, which should further boost the overall activity.

1,2

00

1,3

74

1,3

05

1,2

67

1,2

54

700

929

883

882

873

-

200

400

600

800

1,000

1,200

1,400

1,600

2010 2011 2012 2013 Q12014

Grade A (CBD) Grade B (North Riyadh)

Riyadh Office Rents (SAR per sqm PA)

1,0

80

1,0

60

1,0

92

1,1

00

1,1

78

750

640

690

715

733

-

200

400

600

800

1,000

1,200

1,400

2010 2011 2012 2013 Q12014

Grade A (CBD) Grade B (Others)

Jeddah Office Rents (SAR per sqm PA)

GCC Real Estate Sector Report_V3.indd 31GCC Real Estate Sector Report_V3.indd 31 11/10/15 6:49 PM11/10/15 6:49 PM

X

32

GCC Real Estate

Exhibit 37: Saudi Arabia Residential Supply (2010-17F)

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

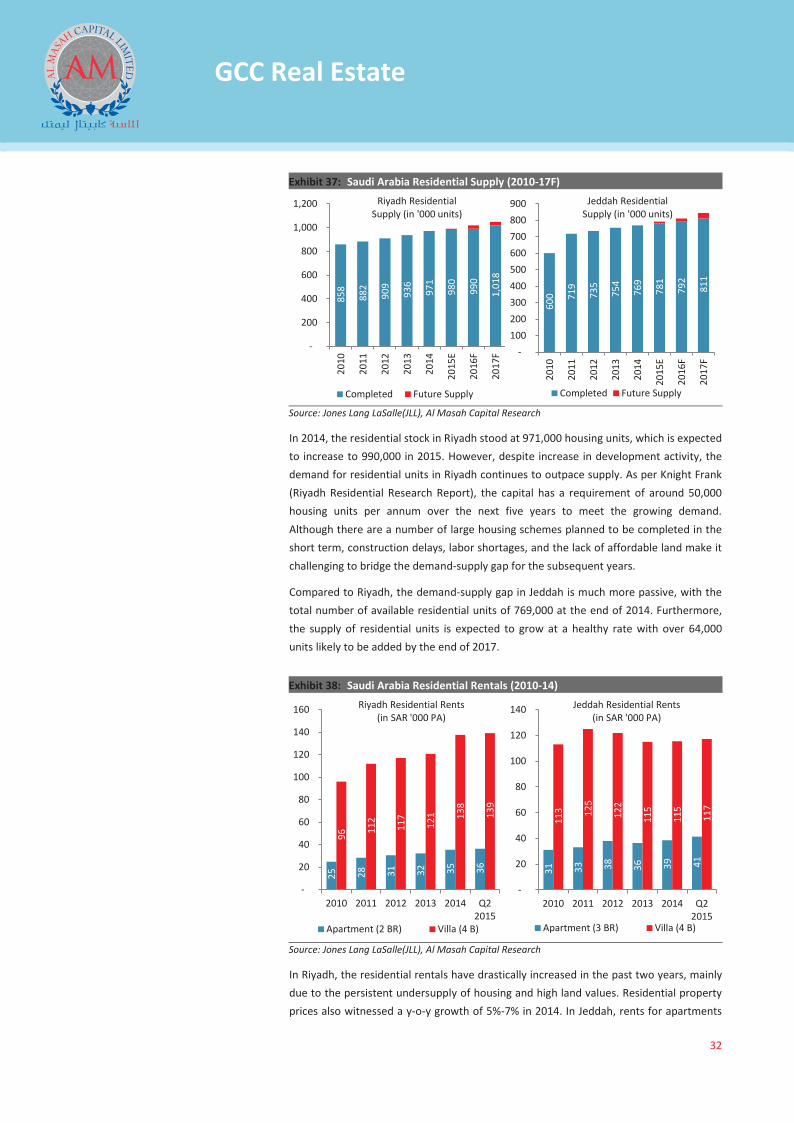

In 2014, the residential stock in Riyadh stood at 971,000 housing units, which is expected to increase to 990,000 in 2015. However, despite increase in development activity, the demand for residential units in Riyadh continues to outpace supply. As per Knight Frank (Riyadh Residential Research Report), the capital has a requirement of around 50,000 housing units per annum over the next five years to meet the growing demand. Although there are a number of large housing schemes planned to be completed in the short term, construction delays, labor shortages, and the lack of affordable land make it challenging to bridge the demand-supply gap for the subsequent years.

Compared to Riyadh, the demand-supply gap in Jeddah is much more passive, with the total number of available residential units of 769,000 at the end of 2014. Furthermore, the supply of residential units is expected to grow at a healthy rate with over 64,000 units likely to be added by the end of 2017.

Exhibit 38: Saudi Arabia Residential Rentals (2010-14)

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

In Riyadh, the residential rentals have drastically increased in the past two years, mainly due to the persistent undersupply of housing and high land values. Residential property prices also witnessed a y-o-y growth of 5%-7% in 2014. In Jeddah, rents for apartments

858

882

909

936

971

980

990

1,0

18

-

200

400

600

800

1,000

1,200

2010

2011

2012

2013

2014

2015

E

2016

F

2017

F

Completed Future Supply

Riyadh Residential Supply (in '000 units)

600

719

735

754

769

781

792

811

- 100 200 300 400 500 600 700 800 900

2010

2011

2012

2013

2014

2015

E

2016

F

2017

F

Completed Future Supply

Jeddah Residential Supply (in '000 units)

25

28

31

32

35

36

96

112

117

121

138

139

-

20

40

60

80

100

120

140

160

2010 2011 2012 2013 2014 Q22015

Apartment (2 BR) Villa (4 B)

Riyadh Residential Rents (in SAR '000 PA)

31

33

38

36

39

41

113

125

122

115

115

117

-

20

40

60

80

100

120

140

2010 2011 2012 2013 2014 Q22015

Apartment (3 BR) Villa (4 B)

Jeddah Residential Rents (in SAR '000 PA)

GCC Real Estate Sector Report_V3.indd 32GCC Real Estate Sector Report_V3.indd 32 11/10/15 6:49 PM11/10/15 6:49 PM

X

33

GCC Real Estate

rose 6.3% and those for villas rose 0.4% in 2014 as compared to a fall 4.4% and 5.7% witnessed in both the segments in 2013, respectively. Further, the western region of Jeddah remained the preferred residential location, recording the highest rental increases.

Going forward, new mortgage law (limiting maximum loan amount to 70% of the property value), which came into effect in November 2014, is likely to discourage residential transactions, especially for the middle income segment that relies heavily on financing, in the short term. However, entry of international developers should boost the construction activity in the long term.

Some of the major ongoing residential projects include: 500,000 Houses Program, Shams Al Arous, Jeddah Housing Project, and Jabal Omar Development Phase 1.

Saudi Arabia Retail Market

Saudi Arabia is one of the largest retail markets in the GCC. Growth in population and personal incomes coupled with increasing consumer preference toward modern retail outlets due to limited entertainment avenues, has boosted the demand of hypermarkets and malls in the country. Consequently, leading retailers such as Panda and Carrefour are on a robust expansion drive. For instance, Panda, the largest retailer in the country, is aiming to expand its outlets from 210 in 2014 to 250 by end of 2015. The growth in retail sector is also well supported by favorable policy decisions such as the recent announcement of Saudi Arabian General Investment Authority (SAGIA) to ease restrictions on foreign investors that will allow them 100% ownership in retail and wholesale businesses as compared to the present level of up to 75%. Going forward, the influx of foreign investment will support the sector growth and will enable the government to improve employment opportunities in the country.

Exhibit 39: Saudi Arabia Retail Supply (2010-17F)

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research

During 2010-14, the retail stock in Riyadh increased by approximately 40% to reach GLA 1.4 million sqm in 2014. While the growth in retail stock in Jeddah was relatively slower during the same period, however the stock is expected to increase drastically in 2016-17 with the expected completion of several large projects. In 2014, the retail stock in Jeddah stood at 923,000 sqm of GLA, with an expected addition of 352,000 sqm GLA by end of 2017.

1,0

43

1,0

73

1,2

00

1,3

00

1,4

00

1,4

00

1,4

95

1,7

18

-

500

1,000

1,500

2,000

2,500

2010

2011

2012

2013

2014

2015

E

2016

F

2017

F

Completed Future Supply

Riyadh Retail Supply (in '000 sqm)

688

770

780

861

923

923

949

1,1

50

-

200

400

600

800

1,000

1,200

1,400

2010

2011

2012

2013

2014

2015

E

2016

F

2017

F

Completed Future Supply

Jeddah Retail Supply (in '000 sqm)

GCC Real Estate Sector Report_V3.indd 33GCC Real Estate Sector Report_V3.indd 33 11/10/15 6:49 PM11/10/15 6:49 PM

X

34

GCC Real Estate

Moreover, the supply of retail stock is also well supported by the demand, which is evident from the declining vacancy rates in both cities. In Riyadh, the vacancy rates fell from 16% in 2010 to 8.0% in Q2 2015 while in Jeddah vacancy rates fell to approximately 7% in Q2 2015 as compared to 13% in 2010.

In Riyadh, the rentals for average mall space surged to SAR 2,788 per sqm PA in 2014 from SAR 2,509 per sqm PA in 2013 (up by 11.1%), primarily driven by the high occupancy rates witnessed during the year. By segments, the rents for super regional malls stood at SAR 2,836 per sqm PA in 2014, up from SAR 2,767 per sqm PA in 2013, while that in community retail centers rose to SAR 2,740 per sqm PA in 2014 from SAR 2,250 per sqm PA in 2013.

Exhibit 40: Saudi Arabia Retail Vacancy Rate (2010-15)

Source: Jones Lang LaSalle(JLL), Al Masah Capital Research