Embed Size (px)

Citation preview

GATX CORPORATIONRailcar Leasing:A Historical Perspective

2

Forward Looking Statement

Forward-looking statements in this presentation that are not historical facts are “forward-looking statements” within the meaning of the Private

Securities Litigation Reform Act of 1995. These include statements that reflect our current views with respect to, among other things, future

events, financial performance and market conditions. In some cases, forward-looking statements can be identified by the use of words such as

“may,” “could,” “expect,” “intend,” “plan,” “seek,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” “continue,” “likely,” “will,” “would,”

and variations of these terms and similar expressions, or the negative of these terms or similar expressions. Specific risks and uncertainties

include, but are not limited to, (1) inability to maintain our assets on lease at satisfactory rates; (2) weak economic conditions, financial market

volatility, and other factors that may decrease demand for our assets and services; (3) decreased demand for portions of our railcar fleet due to

adverse changes in commodity prices, including, but not limited to, sustained low crude oil prices; (4) events having an adverse impact on assets,

customers, or regions where we have a large investment; (5) operational disruption and increased costs associated with increased railcar

assignments following non-renewal of leases, compliance maintenance programs, and other maintenance initiatives; (6) financial and operational

risks associated with long-term railcar purchase commitments; (7) reduced opportunities to generate asset remarketing income; (8) changes in

railroad efficiency that could decrease demand for railcars; (9) operational and financial risks related to our affiliate investments, including the

RRPF affiliates; (10) fluctuations in foreign exchange rates; (11) failure to successfully negotiate collective bargaining agreements with the unions

representing a substantial portion of our employees; (12) the impact of new regulatory requirements for tank cars carrying crude, ethanol, and

other flammable liquids; (13) deterioration of conditions in the capital markets, reductions in our credit ratings, or increases in our financing

costs; (14) asset impairment charges we may be required to recognize; (15) competitive factors in our primary markets; (16) risks related to

international operations and expansion into new geographic markets; (17) exposure to damages, fines, and civil and criminal penalties arising

from a negative outcome in our pending or threatened litigation; (18) changes in or failure to comply with laws, rules, and regulations; (19)

inability to obtain cost-effective insurance; (20) environmental remediation costs; (21) inadequate allowances to cover credit losses in our

portfolio, and (22) other risks discussed in our filings with the US Securities and Exchange Commission (SEC), including our Form 10-K for the year

ended December 31, 2015, and our subsequently filed Form 10-Q reports, all of which are available on the SEC’s website (www.sec.gov).

Investors should not place undue reliance on forward-looking statements, which speak only as of the date they are made, and are not guarantees

of future performance. The Company undertakes no obligation to publicly update or revise these forward-looking statements.

Investor, corporate, financial, historical financial, photographic and news release information may be found at www.gatx.com.

3

Introduction: The Railcar Market Today

Why do railcars exist?

Why do railcar operating lessors exist?

–Capital

–Services

–Risk

4

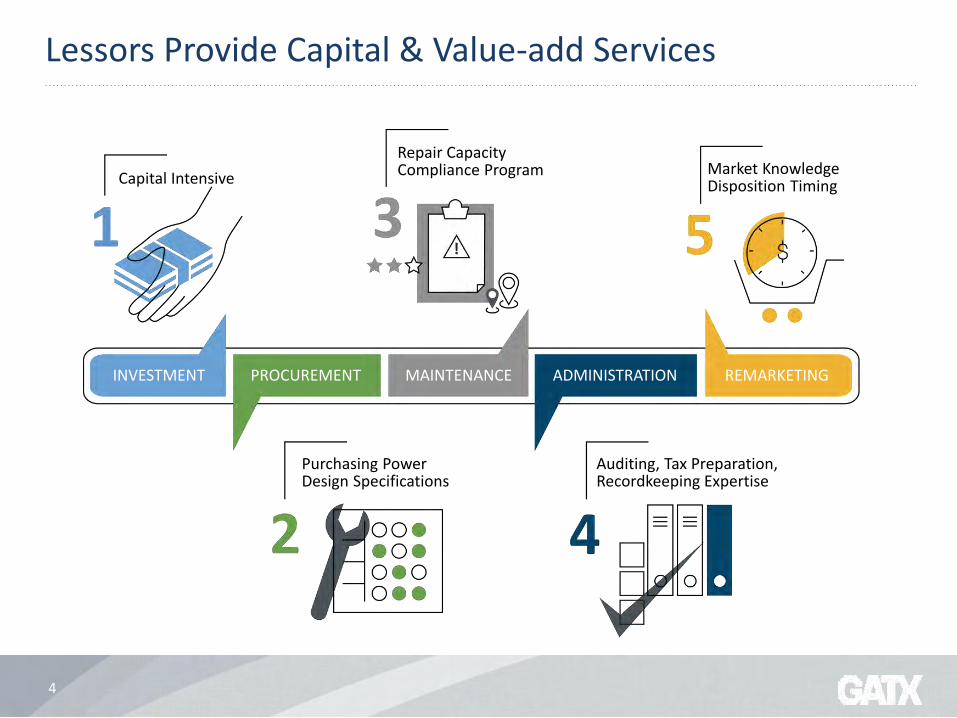

Lessors Provide Capital & Value-add Services

Capital Intensive

Repair CapacityCompliance Program

Purchasing PowerDesign Specifications

Market KnowledgeDisposition Timing

Auditing, Tax Preparation,Recordkeeping Expertise

INVESTMENT PROCUREMENT MAINTENANCE ADMINISTRATION REMARKETING

5

Lessors Assume Operating Risks & Associated Costs

ADMINISTRATIONMaintenance management, car taxes, insurance, engineering, recordkeeping costs

MAINTENANCEExpense incurred to maintain asset – bad order, compliance, other cleaning and repair needs

LEASE OR PURCHASEFinancing or leasing expense

EXPECTED COSTS

NEW COMPLIANCEREQUIREMENTSCost of makingmodificationsto remain compliant

CHANGINGBUSINESS NEEDSImbalanced demandand supply resulting in surplus equipment

OBSOLESCENCEObsolete cardesign resultingin distressed fleet

ADDITIONAL UNEXPECTED COSTS

6

Increasing Regulatory and Maintenance Risks

NUMBER OF REGULATORY AND MAINTENANCE PROGRAMS PER YEAR (BY EFFECTIVE DATE)

SOUTHERN WHEELS

MEXICAN BOLSTERS

TANK CAR QUALIFICATIONS

REFLECTORIZATION FLAMMABLE LIQUIDS

SLACK ADJUSTERS

MCKENZIE VALVES

COMPLIANCE / MAINTENANCE PROGRAM EXAMPLES

Source: DOT, AAR, FRA

WHAT ROLE DO OPERATING LESSORS PLAY IN TODAY’S MARKET?

8

Lessors Own More Than Half the North American Fleet

Source: UMLERApproximately 1.6 million railcars as of 2016

Lessor51%

Railroad21%

Shipper19%

TTX9%

FLEET BY OWNERSHIP

40%

45%

50%

55%

60%

2008 2009 2010 2011 2012 2013 2014 2015 2016

% o

f To

tal F

leet

OWNERSHIP OVER TIME

Lessor Other

9

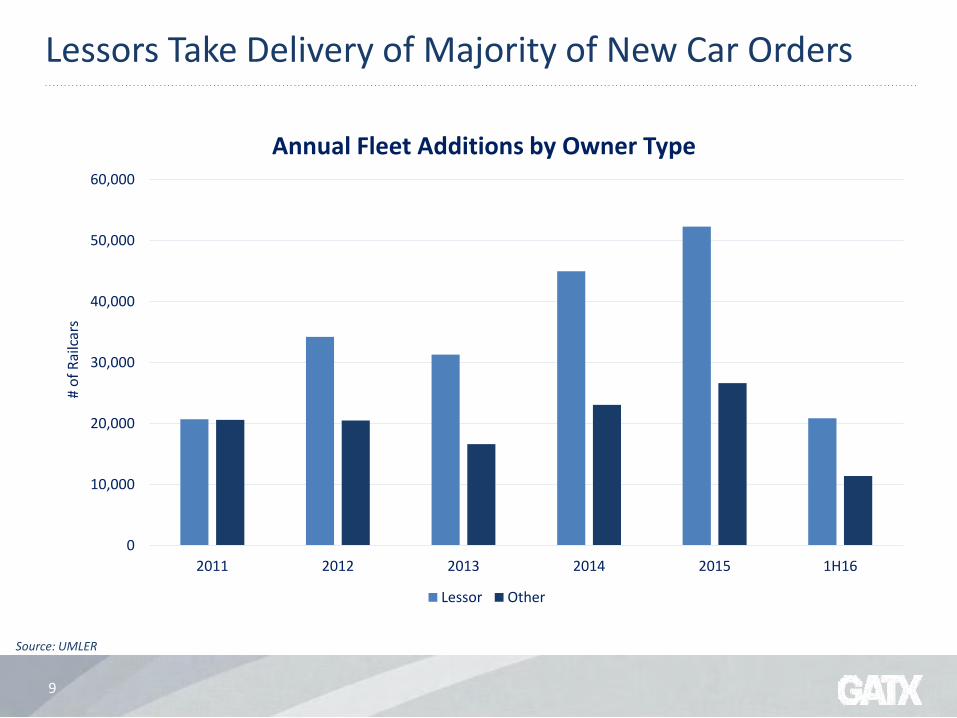

Lessors Take Delivery of Majority of New Car Orders

0

10,000

20,000

30,000

40,000

50,000

60,000

2011 2012 2013 2014 2015 1H16

# o

f R

ailc

ars

Annual Fleet Additions by Owner Type

Lessor Other

Source: UMLER

10

Is today’s railcar market healthy?

Excess new car capacity

Excess existing car supply

Increased railroad velocity

Lower rail freight demand

11

North American New Car Backlog Shows Cyclicality

Source: Railway Supply Institute

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

# o

f R

ailc

ars

‘99 ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15 ‘16

Tank Car Backlog Freight Car Backlog

12

Recent Upturn Featured Speculation and Lack of Diversity

Small Cube

CH20%

Tank41%

All Other39%

New Car Deliveries 2011-2015

Approx. 309K Railcars

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015 3Q16YTD

% o

f To

tal N

ew C

ars

Del

iver

ed

New Car Deliveries 2011-2015

Tank Cars Small Cube CH Other

Source: Railway Supply Institute

CAN A HISTORICAL PERSPECTIVE HELP US UNDERSTAND HOW WE GOT HERE?

14

The world before 1887

As historians have observed, railroads were to the 19th century as internet companies were to the late 20th

– Capital virtually unlimited

– Volatility high

– Era of the “robber barons”

– Essentially no economic regulation

Railroads buy virtually all of their own rolling stock

– Fledgling “private car companies” focus on specialty cars

15

Regulation and Growth: 1887-1945

ICC imposes economic regulation

–Railroad dominance remains

due to lack of alternatives

–Capital availability robust

Subsidized competition emerges

WWII the last heyday of railroad dominance

Railroads continue to own rolling stock

–Private car companies remain roughly the same

16

Decline and the Emergence of Modern Leasing: 1945-1980

Rise of trucking

Regulation limits competitive response

Railroads consolidate and/or encounter financial difficulty

Network shrinks

Railroad capital availability constrained

Alternatives for rolling stock began to emerge

– 1960s: Utility coal trains and leveraged leasing

– 1970s: “Incentive per diem” boxcars and expansion of leasing market

17

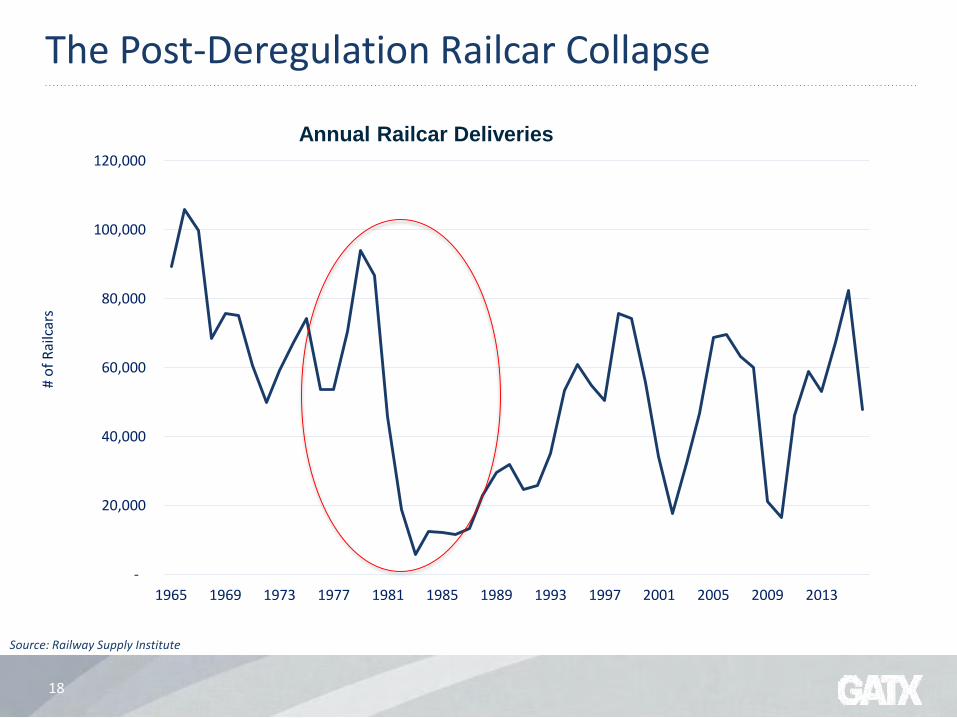

1980-2000: Deregulation and Rationalization

Staggers act of 1980

Uncertainty wipes out many carbuilders

– Decade-and-a-half railcar slump

“Railroad renaissance” begins in 1990s

– Railroads begin to focus capital on fixed plant

– Rise of new generation of operating lessors

– Re-casting of traditional private car companies

– New 286K standard drives fleet replacement

18

The Post-Deregulation Railcar Collapse

-

20,000

40,000

60,000

80,000

100,000

120,000

1965 1969 1973 1977 1981 1985 1989 1993 1997 2001 2005 2009 2013

# o

f R

ailc

ars

Annual Railcar Deliveries

Source: Railway Supply Institute

19

2000-Present: Railroad Renaissance, Railcar Boom and Bust

Railroads capture pricing power and drive returns

– Fixed plant reinvestment in full swing

New (and newer) rail commodities drive huge lessor investment

– PRB coal, ethanol, frac sand, crude oil, NGLs

Railcar cycle becomes exaggerated and volatility reigns

– Rise and fall of PRB coal and CBR

– Severe recessions

– Cheap money

– Aggressive new entrants

– Accidents and regulatory responses

20

The Railroad Renaissance in Graphical Form

$60

$70

$80

$90

$100

$110

$120

$130

$140

$150

$160

$ R

eve

nu

e /

Ton

-Mile

Class I RR Avg. Revenue Per Ton-mile(1990=100)

Source: US DOT Bureau of Transportation Statistics; ABH Consulting

Class I RR Capital Expenditure (billions)

21

The Exaggerated Cyclicality of the Modern Market

-

20,000

40,000

60,000

80,000

100,000

120,000

1965 1969 1973 1977 1981 1985 1989 1993 1997 2001 2005 2009 2013

# o

f R

ailc

ars

Annual Railcar Deliveries

Source: Railway Supply Institute

22

The Extremes of Rail-Hauled Energy Products

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

Petr

ole

um

Pro

du

ct C

arlo

ads

Co

al C

arlo

ads

Boom and Bust in Rail Commodity Carloads

Coal (right axis) Petroleum Products

Source: AAR

23

2017: Where are we now?

Reaping the effects of volatile energy markets and excessive speculation

– Excess capacity, especially for energy-related railcars

– Utilization pressure

– Builder retrenchment

The operating lesson model remains relevant

– Recent developments reinforce the model

– Regulatory actions further underscore leasing value, especially for tank cars

Despite the negatives, money in search of yield can’t seem to stay away from railcars

24

Idle assets are moderating, but still high

0%

5%

10%

15%

20%

25%

30%

35%

5/1/2009 6/1/2010 7/1/2011 8/1/2012 9/1/2013 10/1/2014 11/1/2015 12/1/2016

% Id

le

North American Idle Fleet

Source: AAR

25

Whither goes the future?

The current market has not finished wreaking havoc

–Poorly positioned fleets

–Regulatory complexity

GATX continues to believe that disciplined, diversified, large-scale, full-service operating lessors are well-positioned to withstand the downturn and thrive long-term

QUESTIONS?