Embed Size (px)

Citation preview

Results for the year ended 31 March 2012

25 June 2012

Gatwick Airport Limited

Operational and financial performance

• Underlying traffic growth from

existing and new carriers, including

long haul carriers to Asian markets

• Continuous improvement in

operational performance, delivering

great customer service

• Strong financial performance

reflecting passenger growth,

increase in allowable aeronautical

yield and tight cost control

• Investment programme continuing to

deliver new and improved facilities

• Financial structure strengthened

through further bond issuance.

Highlights

Traffic growth

- Actual + 6.9%

- Underlying + 3.0%

EBITDA (pre-exceptionals) + 16.9%

Capital expenditure £239.2m

RAB £2,201m

Senior Debt net of cash £1,326m

Senior RAR 0.60x

Senior ICR 3.28x

All figures are for the year ended 31 March 2012 except Senior Debt net of cash and RAB which are shown as at 31 March 2012 2

Our ambition & strategy, consistently applied

3

Improved service and passenger satisfaction

4

Service quality targets met in Q5

Security queuing in Q5

Customer survey score in Q5

On-time departures in peak summer

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

55.0%

60.0%

65.0%

70.0%

75.0%

2007 2008 2009 2010 2011

Peak summer is June, July and August

75%

80%

85%

90%

95%

100%

2009 2010 2011 2012

(Pe

rce

nta

ge)

(Financial years ending 31 March)

North Terminal Average <5 min South Terminal Average <5 min Target

3.9

4.0

4.1

4.2

2009 2010 2011 2012

(Pas

sen

ger

sati

sfac

tio

n)

(Financial years ending 31 March)

Overall QSM Target

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

% Measures Passed % Measures Failed

(Calendar years)

Change of ownership

• New airlines attracted to Gatwick, in competition with other airports

- Asian airlines starting services as an alternative to Heathrow

- AirAsia X latest airline to switch from Stansted to Gatwick (but now ceased all European services)

- Lufthansa and Turkish Airlines providing connectivity beyond home markets

New routes delivering growth and connectivity

• Underlying traffic growth largely from existing carriers making more effective use of peak capacity and available slots:

- Record load factors each month; 88.4% in August 2011

- New routes/frequencies from easyJet, BA, Norwegian

- Some turnover of airlines/routes e.g. Ryanair, Malev, Delta

5

• New long-haul Asian carriers for summer 2012

- Assisting London‟s connectivity to the Far East

Investing in airport transformation

• Delivery of investment programme on schedule

– £239m invested in 2011/12

– £757m invested in Q5-to-date

– Approx. £436m remaining of Q5 programme

(including extension year)

• Projects completed during 2011/12

– South Terminal forecourt (£31m)

– South Terminal security (£45m)

– Pier 2 reconfiguration and upgrade (£38m)

– North Terminal extension (£85m)

• Major projects started in 2011/12

– South Terminal baggage and Pier 1 (£174m)

– Pier 5 reconfiguration (£72m)

– North Terminal baggage (£46m)

– Main runway resurfacing (£44m) 6

Delivering a better retail offering

• Brand new walk-through duty free store

– New walk-through duty and tax-free opens July

2012

– Retail space in the South Terminal departure

lounge being reconfigured

• Innovative bookshop rebranding

– WH Smith stores being rebranded as „London

News Company‟ or „London Book Company‟

– First rebranded store opened March 2012; all

complete in Summer 2012

• Improved catering in the North Terminal

– Two new restaurants opening this year

– First airport in the world to offer a Jamie

Oliver restaurant, opening July 2012

7

8

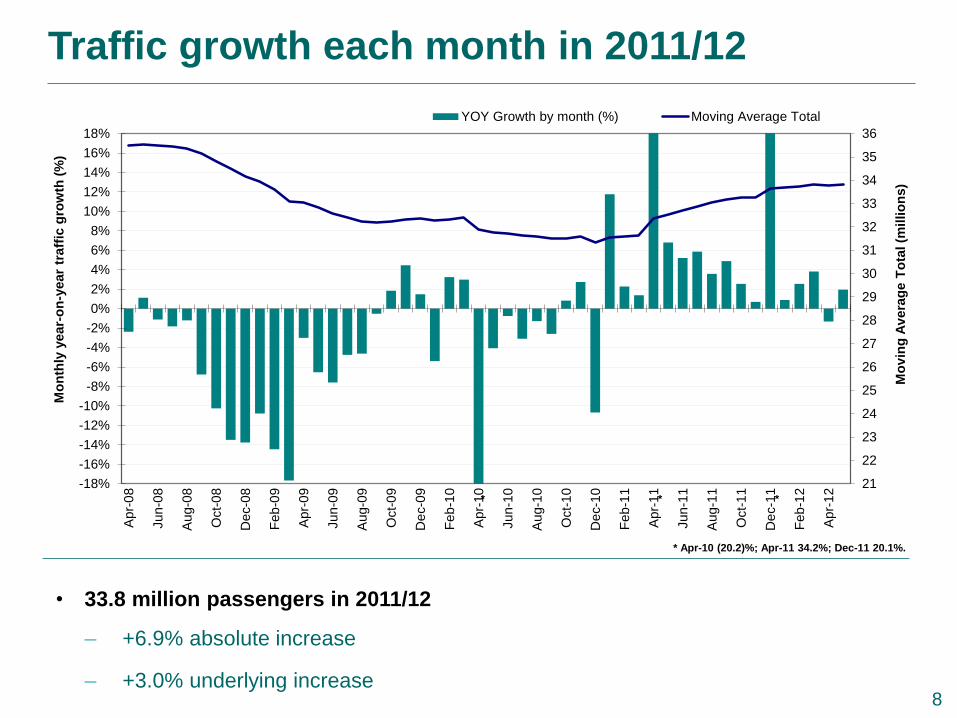

Traffic growth each month in 2011/12

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

-18%

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%A

pr-

08

Jun-0

8

Aug-0

8

Oct-

08

De

c-0

8

Feb

-09

Apr-

09

Jun-0

9

Aug-0

9

Oct-

09

De

c-0

9

Feb

-10

Apr-

10

Jun-1

0

Aug-1

0

Oct-

10

De

c-1

0

Feb

-11

Apr-

11

Jun-1

1

Aug-1

1

Oct-

11

De

c-1

1

Feb

-12

Apr-

12

Mo

vin

g A

vera

ge T

ota

l (m

illio

ns)

Mo

nth

ly y

ear-

on

-year

traff

ic g

row

th (

%)

YOY Growth by month (%) Moving Average Total

* Apr-10 (20.2)%; Apr-11 34.2%; Dec-11 20.1%.

* * *

• 33.8 million passengers in 2011/12

– +6.9% absolute increase

– +3.0% underlying increase

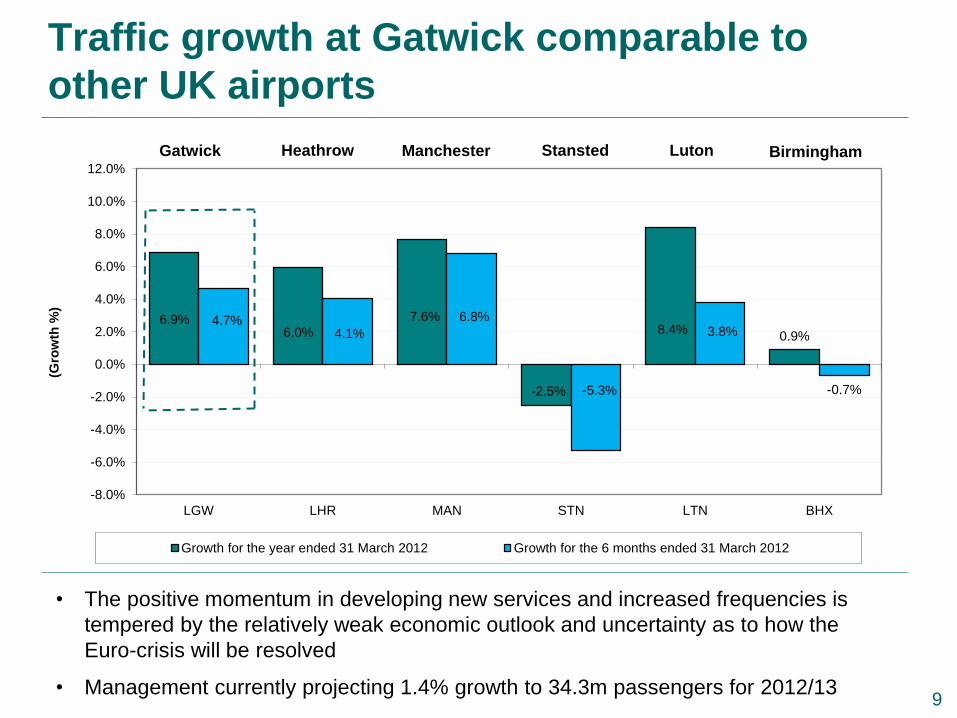

Traffic growth at Gatwick comparable to

other UK airports

9

• The positive momentum in developing new services and increased frequencies is

tempered by the relatively weak economic outlook and uncertainty as to how the

Euro-crisis will be resolved

• Management currently projecting 1.4% growth to 34.3m passengers for 2012/13

6.9% 6.0%

7.6%

-2.5%

8.4% 0.9%

4.7% 4.1%

6.8%

-5.3%

3.8%

-0.7%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

LGW LHR MAN STN LTN BHX

(Gro

wth

%)

Growth for the year ended 31 March 2012 Growth for the 6 months ended 31 March 2012

Stansted Heathrow Luton Manchester Gatwick Birmingham

9

Strong financial performance building on

traffic growth

* Net debt and RAB are shown as at 31 March 2012 and 2011

Figures in £m unless stated Year ended

31 March 2012

Year ended

31 March 2011 Change

Passengers (millions) 33.8 31.6 6.9%

Turnover 517.4 476.3 8.6%

Operating costs (ex D&A and pre-exceptional items)

295.9 286.9 3.1%

EBITDA (pre-exceptional items)

221.5 189.4 16.9%

Net debt * 1,266.5 1,184.3 6.9%

RAB * 2,200.9 1,985.5 10.8%

10

£517.4m +8.6%

Increased turnover reflecting traffic

growth and increase to aeronautical yield • Aeronautical income up +12.2%,

reflecting increases in passengers

(+6.9%) and allowable yield (+5.8%)

• Retail revenue up +4.6%. Net retail

income per passenger declined by

£0.08 to £3.54, reflecting

– greater proportion of EU

passengers

– retail footprint reduced by 6.2%

during terminal redevelopment

– ST retail with new duty and tax-

free store to open in July 2012

• Car park revenue up +5.0%. Net car

park income per passenger higher by

£0.08 at £1.20, reflecting

– more effective pricing and

increased short-stay capacity

– but, lower proportion of UK

originating passengers

274.2 Aeronautical

Retail

Cark

parking

Other

income

Turnover analysis

2010/11 2011/12

244.3

120.9 115.6

51.7 54.3

68.0 64.7 +5.1%

+4.6%

+12.2%

+5.0%

11 £476.3m Total

Increase of 3% in adjusted operating costs*

• Reliance on BAA removed

– IT systems separation

completed in October 2011

– Transitional IT under TSA costs

reduced from £14.4m to £2.4m

• Staff costs increase reflects:

– RPI-linked, 2-year pay deal for

negotiated grades

– Lower operational headcount

– Increased staff costs

associated with the capital

investment and IT programmes

offset by capitalisation

Net staff

costs

General &

other expenses

Rent, rates

& utilities

Maintenance,

IT & TSA

* Operating costs excluding depreciation and amortisation

2010/11 2011/12

Operating costs analysis

40.0 37.6

50.7 57.0

84.6 81.7

111.6 119.6

+7.2%

-3.4%

+12.4%

-6.0%

12 £286.9m Total £295.9m +3.1%

199.3

0.0

242.0

36.4

3.1

1,184.3

1,266.5

1,100.0

1,150.0

1,200.0

1,250.0

1,300.0

1,350.0

1,400.0

1,450.0

1,500.0

Opening Capitalexpenditure

Net interest Cash flowfrom ops

Dividend Other Closing

£m

Net debt 31 March 2011 to 31 March 2012

* Interest capitalised of £11.7m is included within capital expenditure 13

Re-financing risk lowered through further

bond issuance in January 2012

• Debt maturity profile reduces

refinancing risk

– £300m 2041/43 Class A Bond

– £300m 2037/39 Class A Bond

– £300m 2026/28 Class A Bond

– £300m 2024/26 Class A Bond

– £106m Dec-14 Bank Facilities

• Strong liquidity position to fund

investment programme of c.£436m over

next two years from:

– Undrawn bank commitments (£350m

as at 31 March 2012)

– Annual cash flow from operations

(£199m for the year ended 31 March

2012)

• £75m restricted payment planned July

2012

Financial ratio Year ended

31 March

2012

Year ended

31 March

2011

Cash flow

(per covenant) £154.7m £144.8m

Total interest (net) £48.1m £42.0m

Senior ICR 3.28x 3.45x

Trigger <1.50x <1.50x

Senior Debt net of

cash £1,325.8m £1,212.8m

RAB £2,200.9m £1,985.5m

Senior RAR 0.60x 0.61x

Trigger >0.70x >0.70x

14

Regulatory developments

15

• Civil Aviation Bill progressing through Parliament

– General duty on CAA to further interests of passengers

– Provision for derogations for pre-existing financing arrangements

• CAA undertaking assessment of airport market power

– Gatwick‟s analysis indicates it does not have “substantial market power”

– CAA‟s initial views are that each of LGW, LHR & STN have some degree of market

power and thus could be subject to economic regulation beyond the end of Q5

– CAA continuing work on market power and alternatives for economic regulation

• Beyond Q5 preparation

– Constructive Engagement with the airlines underway based on initial business plan

– Outputs of Constructive Engagement to inform the Company‟s business plan to be

submitted to CAA in early 2013

• Q5 extension year

– Gatwick and airlines defining new capital expenditures triggers for 2013/14

Conclusion

• Underlying traffic growth, slowing growth in 2012/13

• Connecting London to Asian markets for Summer 2012

• Continuous improvement in operational performance, delivering great

customer service

• Investment programme on track, transforming facilities

• Strong financial performance in 2011/12, but moderating in 2012/13 with

lower growth in traffic (+1.4%) and aeronautical yield (+1.5%)

Full details of today’s announcement at: www.gatwickairport.com/investor

16

Disclaimer

This material contains certain tables and other statistical analyses (the “Statistical Information”) which have been prepared in reliance on publicly available information and may be

subject to rounding. Numerous assumptions were used in preparing the Statistical Information, which may or may not be reflected herein. Actual events may differ from those

assumed and changes to any assumptions may have a material impact on the position or results shown by the Statistical Information. As such, no assurance can be given as to

the Statistical Information‟s accuracy, appropriateness or completeness in any particular context; nor as to whether the Statistical Information and/or the assumptions upon which it

is based reflect present market conditions or future market performance. The Statistical Information should not be construed as either projections or predictions nor should any

information herein be relied upon as legal, tax, financial or accounting advice. Gatwick Airport Limited (“GAL”) does not make any representation or warranty as to the accuracy or

completeness of the Statistical Information.

These materials contain statements that are not purely historical in nature, but are “forward-looking statements”. These include, among other things, projections, forecasts,

estimates of income, yield and return, and future performance targets. These forward-looking statements are based upon certain assumptions, not all of which are stated. Future

events are difficult to predict and are beyond GAL‟s control. Actual future events may differ from those assumed. All forward-looking statements are based on information available

on the date hereof and neither GAL nor any of its affiliates or advisers assumes any duty to update any forward-looking statements. Accordingly, there can be no assurance that

estimated returns or projections will be realised, that forward-looking statements will materialise or that actual returns or results will not be materially lower that those presented.

This material should not be construed as an offer or solicitation to buy or sell any securities, or any interest in any securities, and nothing herein should be construed as a

recommendation or advice to invest in any securities.

This document has been sent to you in electronic form. You are reminded that documents transmitted via this medium may be altered or changed during the process of electronic

transmission and consequently neither GAL nor any person who controls it (nor any director, officer, employee not agent of it or affiliate or adviser of such person) accepts any

liability or responsibility whatsoever in respect of the difference between the document sent to you in electronic format and the hard copy version available to you upon request

from GAL.

Any reference to “GAL” will include any of its affiliated associated companies and their respective directors, representatives or employees and/or any persons connected with them.

17

Questions