Embed Size (px)

Citation preview

GAO United States Government Accountability Office

Report to the Committee on Small Business and Entrepreneurship, U.S. Senate

HURRICANES KATRINA AND RITA

Federally Funded Programs Have Helped to Address the Needs of Gulf Coast Small Businesses, but Agency Data on Subcontracting Are Incomplete

July 2010

GAO-10-723

What GAO Found

United States Government Accountability Office

Why GAO Did This Study

HighlightsAccountability Integrity Reliability

July 2010 HURRICANES KATRINA AND RITA

Federally Funded Programs Have Helped to Address the Needs of Gulf Coast Small Businesses, but Agency Data on Subcontracting Are Incomplete Highlights of GAO-10-723, a report to the

Committee on Small Business and Entrepreneurship, U.S. Senate

Hurricanes Katrina and Rita wreaked havoc on small businesses in the Gulf Coast, and much federal assistance has been provided to help these businesses. GAO was asked to describe (1) the amount of assistance provided to Gulf Coast small businesses through the Small Business Administration’s (SBA) disaster and Gulf Opportunity (GO) loans, state-administered business assistance programs funded by the Department of Housing and Urban Development’s (HUD) Community Development Block Grants (CDBG), and the Economic Development Administration’s (EDA) Revolving Loan Fund (RLF) program; (2) the extent to which Gulf Coast small businesses received federal contract funds; and (3) the current state of and improvements in the region’s economy. GAO analyzed data on SBA and EDA loans and states’ use of supplemental CDBG appropriations, data on prime and subcontracts awarded for hurricane recovery activities, and economic indicators both before and after the hurricanes.

What GAO Recommends

GAO recommends that the Secretary of Defense should take steps to ensure that contracting officials with the Corps and other DOD departments consistently comply with requirements to monitor the extent to which contractors are meeting subcontracting plan goals. DOD did not concur with the implication that its contracting personnel do not enforce requirements.

Several federal programs provided assistance to Gulf Coast small businesses after the 2005 hurricanes; however, despite this assistance, some small businesses still face recovery challenges. Of the programs we reviewed, SBA provided the greatest amount of assistance to small businesses. SBA approved about $1.4 billion in loans through its Disaster Loan and GO Loan programs to assist with the repair or replacement of damaged property and to address economic losses suffered after the hurricanes. In addition, Louisiana expended about $179 million and Mississippi targeted $3 million in CDBG disaster relief funds for small business assistance grant, loan, and other programs to further assist businesses that in some or all cases, may not have been eligible for SBA loans. EDA did not receive supplemental appropriations after the hurricanes, but Gulf Coast small businesses did receive about $36 million in loans from EDA’s RLF grantees, which provide gap financing to small businesses to start or expand their business. Even with federal assistance, however, some small business owners with whom GAO met have encountered recovery challenges. For example, a few of these small business owners told GAO that they had problems applying for SBA loans because the hurricanes destroyed needed financial records. Other owners face higher expenses, especially the cost of commercial insurance and added debt from these loan programs, which has made recovering difficult. Gulf Coast small businesses received almost $2.9 billion in federal contracts awarded in response to the hurricanes. The Federal Acquisition Regulation

requires that agency contracting officials monitor prime contractors’ performance under subcontracting plans. However, the U.S. Army Corps of Engineers (Corps) and the rest of the Department of Defense (DOD)—two of four agencies that awarded the most in federal contracts for hurricane recovery—could not demonstrate that they were consistently monitoring subcontracting accomplishment data for 13 of the 43 construction contracts for which subcontracting plans were required. Without such monitoring, the Corps and the rest of DOD are limited in their ability to determine the extent to which contractors are following their subcontracting plans. Indicators—including population estimates, number of small businesses, unemployment rates, and housing prices—suggest that the hurricanes’ effects on local economies varied across the Gulf Coast. From 2005 to 2006, some heavily damaged areas experienced steep declines in population and number of small businesses, while less-damaged areas experienced steady increases in these indicators. Since that time, the population and number of small businesses in heavily damaged areas have increased, but they both still remain below prehurricane levels. House prices have shown some steady increases from 2005 to 2008 in heavily damaged metropolitan areas. The impact of the recent oil spill in the Gulf of Mexico on small businesses is uncertain.

View GAO-10-723 or key components. For more information, contact William Shear at (202) 512-8678 or [email protected].

Page i GAO-10-723

Contents

Letter 1

Background 5 Federally Funded Programs Have Helped to Address Different

Needs of Small Businesses, but Some Small Businesses Still Face Challenges, and the Performance of Federally Funded Loans Has Varied 16

Gulf Coast Small Businesses Directly Received Billions of Federal Contracting Dollars, but Reporting of Subcontracting Dollars Awarded Remains Incomplete 30

Economic Conditions Have Varied Across the Gulf Coast Region Following Hurricanes Katrina and Rita and Appear to Be Related in Part to the Level of Damage Sustained in Different Areas 35

Conclusions 55 Recommendation for Executive Action 55 Agency Comments and Our Evaluation 56

Appendix I Objectives, Scope, and Methodology 59

Appendix II Summary of Selected Reports from Research

Organizations Studying the Economic Recovery

of the Gulf Coast Region Following Hurricanes

Katrina and Rita 65

Appendix III Comments from the Department of Defense 68

Appendix IV GAO Contact and Staff Acknowledgments 71

Tables

Table 1: Characteristics of SBA’s Business Disaster Loans 6 Table 2: Amount of CDBG Disaster Relief Funds Provided for

Hurricanes Katrina and Rita, by Selected States 9 Table 3: SBA Disaster Loans Approved for Businesses, Hurricanes

Katrina and Rita, Fiscal Years 2005-2009 17

Federal Assistance to Small Businesses

Table 4: SBA Disaster Loans Approved for Small Businesses in Gulf Coast States, Hurricanes Katrina and Rita, Fiscal Years 2005-2009 17

Table 5: Number and Amount of Approved GO Loans for Small Businesses in Gulf Coast States, Fiscal Years 2005-2009 19

Table 6: Total Amount of RLF and Private Investment, by Selected States 23

Table 7: Status of Subcontracting Accomplishment Information for Hurricanes Katrina- and Rita-Related Construction Contracts Having Subcontracting Plans 33

Table 8: Population and Businesses with 50 or Fewer Employees by Selected States, 2004-2008 36

Table 9: Travel Expenditures and Travel-Generated Employment, 2004-2008 48

Table 10: SBA Statistics on Economic Assistance Provided Following the Deepwater Horizon Oil Spill 51

Figures

Figure 1: Additional Funding Provided to Louisiana’s RLF Grantees for Disaster Recovery Purposes 24

Figure 2: Total Amount of Federal Contract Dollars Provided for Hurricanes Katrina- and Rita-Related Recovery Efforts, Fiscal Years 2005-2009 30

Figure 3: Contract Dollars Awarded Directly to Gulf Coast Small Businesses and Businesses of All Sizes in States Primarily Affected by Hurricanes Katrina and Rita, Fiscal Years 2005-2009 31

Figure 4: Contract Dollars Awarded Directly to Various Types of Small Businesses for Hurricanes Katrina- and Rita-Related Recovery Efforts, Fiscal Years 2005-2009 32

Figure 5: Changes in Population, Louisiana and Mississippi, 2004-2008 37

Figure 6: Changes in Number of Small Businesses, Louisiana and Mississippi, 2004-2007 38

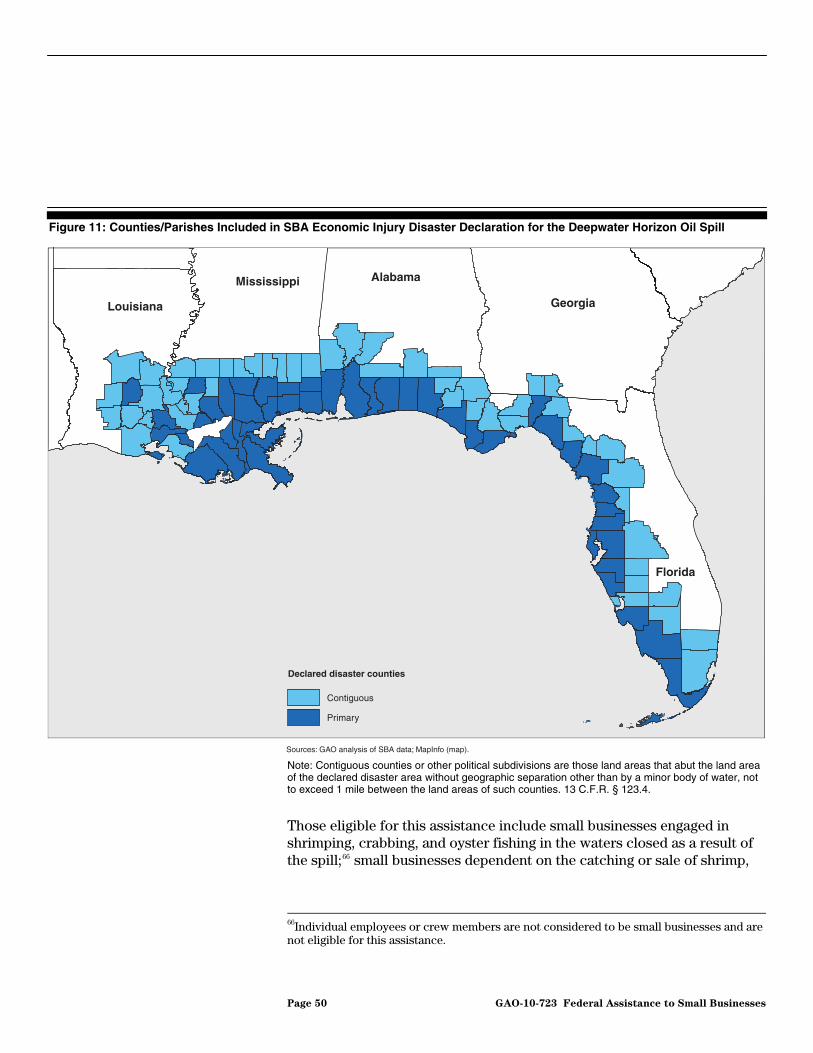

Figure 7: Unemployment Rates by Selected States, 2005-2009 41 Figure 8: Housing Price Index by MSA, 2005-2009 42 Figure 9: Federal Fishery Closure Boundaries as of July 13, 2010 45 Figure 10: U.S. Commercial Landings of Finfish and Shellfish, 2008 47 Figure 11: Counties/Parishes Included in SBA Economic Injury

Disaster Declaration for the Deepwater Horizon Oil Spill 50

Page ii GAO-10-723 Federal Assistance to Small Businesses

Abbreviations

CDBG Community Development Block Grant Corps U.S. Army Corps of Engineers DCMS Disaster Credit Management System DHS Department of Homeland Security DOD Department of Defense EDA Economic Development Administration eSRS Electronic Subcontracting Reporting System FAR Federal Acquisition Regulation FPDS-NG Federal Procurement Data System—Next Generation GO Gulf Opportunity Pilot Loan Program GSA General Services Administration HUBZone Historically Underutilized Business Zone HUD Department of Housing and Urban Development LAS Loan Accounting System MSA Metropolitan Statistical Area NOAA National Oceanic and Atmospheric Administration RLF Revolving Loan Fund SBA Small Business Administration SBDC Small Business Development Center

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

Page iii GAO-10-723 Federal Assistance to Small Businesses

Page 1 GAO-10-723

United States Government Accountability Office

Washington, DC 20548

July 29, 2010

The Honorable Mary L. Landrieu Chair The Honorable Olympia J. Snowe Ranking Member Committee on Small Business and Entrepreneurship United States Senate

Within a 2-month period in 2005, Hurricanes Katrina and Rita struck the Gulf Coast, causing billions of dollars in damage and displacing millions of individuals. Louisiana and Mississippi were the two states most affected, but these hurricanes also caused damage in Alabama, Florida, and Texas. The size and scope of the devastation presented the nation with unprecedented recovery and rebuilding challenges. Small businesses in the region were adversely impacted by the hurricanes and faced many barriers to recovery. Some businesses were completely destroyed, while many others suffered an almost complete loss of inventory, equipment, and records. Additionally, many business owners who employed local residents lost employees when they fled the hurricanes, and businesses that did reopen after the hurricanes faced a smaller customer base because of reduced population levels. The federal government has provided billions of dollars in the form of grants, loans, and contracts to assist in the recovery of the region and its economy. A portion of these funds has been utilized to assist small businesses in rebuilding and reestablishing themselves in a changed marketplace.

Nearly 5 years have passed since the hurricanes, and small businesses in the area are still recovering from the damages they suffered. As part of this committee’s efforts to monitor small business recovery in the Gulf Coast, you asked us to provide information on assistance small businesses in the Gulf Coast received from programs administered by the Small Business Administration (SBA), Department of Housing and Urban Development (HUD), and Economic Development Administration (EDA); on federal contract funds received by small businesses; and on the small business economy in the Gulf Coast region. More specifically, this report describes (1) the amount of assistance small businesses in the Gulf Coast received through SBA’s Disaster and Gulf Opportunity (GO) Pilot Loan programs, state-administered business assistance programs funded by HUD’s Community Development Block Grants (CDBG), and EDA’s Revolving Loan Fund (RLF) Program; the benefits and challenges experienced by

Federal Assistance to Small Businesses

participants in these programs; and the performance of loans extended to small businesses using assistance from these programs; (2) the extent to which Gulf Coast small businesses received federal contract funds for recovery efforts; and (3) the current state of and improvements in the region’s economy, with a focus on the small business economy.

Our work focused on small business recovery efforts in four states impacted by Hurricanes Katrina or Rita: Alabama, Louisiana, Mississippi, and Texas. To address our first objective, we obtained data extracts from SBA’s Disaster Credit Management System (DCMS) and Loan Accounting System and computed descriptive statistics on the number, dollar amount, and performance of disaster and GO loans provided to small businesses, and we interviewed SBA officials knowledgeable about these data. We also performed various tests of the information in the data extracts we obtained to ensure the completeness of the data and concluded that SBA’s data were sufficiently reliable for the purposes of our report. To describe the amount of assistance Gulf Coast small businesses received through state-administered business assistance programs that utilized CDBG disaster relief funds, we reviewed Federal Register notices and interviewed officials from HUD to obtain information on CDBG disaster recovery supplemental appropriations Congress enacted following Hurricanes Katrina and Rita. We also obtained information from state agencies in Alabama, Louisiana, Mississippi, and Texas and interviewed state officials regarding their use of these funds to assist small businesses in recovering from the hurricanes. We determined that information provided by the states was sufficiently reliable for the purposes of our report. To describe the amount of assistance small businesses received through EDA’s RLF Program, we analyzed semiannual reports on loans made by EDA’s RLF grantees in the four states within the scope of our review and interviewed EDA officials who oversee RLF grantees in these states. These data are self-reported by RLF grantees; therefore, in this report we attribute these findings to the RLF grantees. Furthermore, we contacted selected RLF grantees in the areas most impacted by the hurricanes to determine the extent to which loans that they made following the hurricanes were utilized by small businesses for hurricane recovery efforts. We also interviewed officials at Small Business Development Centers (SBDC) and chambers of commerce in areas heavily impacted by the hurricanes in each state to discuss the assistance each provided to small businesses after the hurricanes. Finally, to obtain the perspectives of small business owners regarding the benefits and challenges they experienced in participating in these programs, we conducted focus groups of small business owners in New Orleans, Louisiana, and Gulfport, Mississippi.

Page 2 GAO-10-723 Federal Assistance to Small Businesses

To address our second objective, we obtained data from the Federal Procurement Data System-Next Generation (FPDS-NG), the governmentwide database of contracting activity, to determine the extent to which federal agencies contracted directly with small businesses in Gulf Coast states. Using FPDS-NG data, we identified the top four agencies that awarded the greatest amount of Katrina- and Rita-related contract dollars between fiscal years 2005 and 2009. These agencies were the U.S. Army Corps of Engineers (Corps); Department of Homeland Security (DHS); Department of Defense, excluding the Corps (DOD); and the General Services Administration (GSA).1 Although we could not independently verify the reliability of these data, we reviewed system documentation, conducted electronic data testing for inconsistency errors and completeness, and compared it with supporting documentation when available. On the basis of these efforts, we determined the data on the amount of federal contract dollars received directly for Hurricanes Katrina and Rita recovery efforts to be sufficiently reliable for the purposes of this report.2 We also identified all Corps, DHS, DOD, and GSA construction-related contracts awarded between fiscal years 2005 and 2009 for Katrina- and Rita-related recovery efforts that, according to FPDS-NG, had a subcontracting plan.3 For contracts that had subcontracting plans, we asked the agencies for documentation of prime contractors’ subcontracting award reports in the Electronic Subcontracting Reporting System (eSRS), a governmentwide database for capturing this information, or for copies of the paper subcontracting accomplishment reports. These plans include information on, among other things, goals for the use of small businesses, expressed as a percentage of the total planned subcontracting dollars.4 In addition, we interviewed officials from each of the four agencies to gather additional information relating to subcontracting award reports.

1Throughout this report, unless otherwise noted, we use the acronym DOD to refer to the Department of Defense, excluding the Corps. We are reporting on the Corps and the rest of DOD separately because at least three supplemental appropriations measures for DOD activities relating to Hurricane Katrina relief specifically directed certain funds to the Corps for its disaster relief activities. (Pub. L. No. 109-62, 119 Stat. 1990 (2005); Pub. L. No. 109-148, 119 Stat. 2680 (2005); and Pub. L. No. 109-234, 120 Stat. 418 (2006).)

2FPDS-NG is the only governmentwide system for obtaining information on how federal contract funds are being spent.

3When a prime contract includes a subcontracting plan, the agency awarding the contract indicates this in FPDS-NG.

4These and other aspects of small business subcontracting plan requirements are set forth at FAR Subpart 19.7.

Page 3 GAO-10-723 Federal Assistance to Small Businesses

To address our third objective, we identified the counties most impacted by the hurricanes in each of the four states and also identified various economic indicators that provide a proxy for the state of the small business economy. These indicators include the population, unemployment rate, number of small business establishments, and housing price index. We collected and analyzed data for each indicator, including population estimates from 2000 to 2008, unemployment rates from 2000 to 2009, number of small business establishments from 2000 to 2007, and housing price index estimates from 2000 to 2009. We used these data to identify trends more likely associated with the hurricanes than other economic events within the areas most heavily impacted. In doing so, we also analyzed and compared trends at the state level with trends in the counties most heavily impacted by the hurricanes, where comparable data were available. We determined that the economic indicator data we used were of sufficient reliability for the purposes of our report. To describe the potential impact of the recent Gulf Coast oil spill on the small business economy in the Gulf Coast region, we obtained and analyzed information on the size of the fishing and travel industries; new SBA economic injury disaster loans approved as a result of the oil spill; as well as existing SBA disaster loans in declared areas and the number of deferments SBA has granted on those loans. In addition, we met with Gulf Coast small business owners impacted by the oil spill. We also interviewed organizations assisting these small businesses and organizations studying the economic impacts of the oil spill. Finally, we reviewed assessments by other organizations regarding the posthurricane economic recovery in the Gulf Coast region. Appendix II contains a summary of these organizations’ findings.

We conducted this performance audit from September 2009 to July 2010 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives. See appendix I for more detailed information on the scope and methodology of this report.

Page 4 GAO-10-723 Federal Assistance to Small Businesses

Background

SBA Disaster Assistance The Robert T. Stafford Disaster Relief and Emergency Assistance Act of 1974 (Stafford Act) sets forth requirements for the federal response to presidentially declared disasters.5 A presidential disaster declaration puts into motion long-term federal recovery programs, including SBA’s Disaster Loan Program. While SBA is known primarily for its financial support of small businesses, the agency also plays a critical role in assisting the victims of natural and other declared disasters. SBA’s Disaster Loan Program is the primary federal program for funding long-range recovery for private-sector, nonfarm disaster victims and is the only form of SBA assistance not limited to small businesses. For an SBA disaster loan to be approved, a disaster victim must demonstrate an ability to repay the loan and must provide collateral for loans over a certain value.6 The Small Business Act authorizes SBA to make available the following two types of disaster loans to small businesses:7

• Physical disaster loans: These loans are for permanent rebuilding and replacement of uninsured or underinsured disaster-damaged property. They are available to homeowners, renters, businesses of all sizes, and nonprofit organizations. These loans are intended to repair or replace the disaster victims’ damaged property to its predisaster condition. Almost any business concern or charitable or other nonprofit entity whose property is damaged in a declared disaster area is eligible to apply for a physical disaster loan; however, small businesses in agriculture-related industries—also known as agricultural enterprises—are not eligible.8

• Economic injury disaster loans: These loans provide small businesses that are not able to obtain credit elsewhere with necessary working capital

542 U.S.C. §§ 5121-5207.

6In general, SBA will not require a borrower to pledge collateral to secure a disaster home loan or a physical disaster business loan of $10,000 or less, or an economic injury disaster loan of $5,000 or less. 13 C.F.R. § 123.11.

715 U.S.C. § 636(b).

8An agricultural enterprise is a business primarily engaged in the production of food and fiber, ranching and raising livestock, aquaculture, and all other farming and agriculture-related industries. 13 C.F.R. § 123.201(a). Additional eligibility restrictions can be found at 13 C.F.R. §§ 123.101, 123.201.

Page 5 GAO-10-723 Federal Assistance to Small Businesses

until normal operations resume after a disaster declaration.9 They cover operating expenses the business could have paid had the disaster not occurred. The Small Business Act restricts economic injury disaster loans to small businesses. Agricultural enterprises are also not eligible for economic injury disaster loans.10

Table 1 provides a description of the characteristics of each of these loans.

Table 1: Characteristics of SBA’s Business Disaster Loans

Type of loan Funds use Eligibility Lending limita Interest rateb Loan term

Physical disaster loans

Repair or replace disaster-damaged property owned by the business, including real estate, inventories, supplies, machinery, and equipment.

Businesses of all sizes and private, nonprofit organizations such as charities, churches, and private universities.

$2 million aggregate for the repair or replacement of real estate, inventories, machinery, equipment, and all other physical losses.

Varies, but generally for those who cannot obtain credit elsewhere, interest is capped at 4 percent; for those who can obtain credit elsewhere, interest is capped at 4.5 and 6 percent, respectively, for nonprofits and businesses.

Up to 30 years if no credit available elsewhere. For businesses with credit available elsewhere, maximum loan term is 3 years.

Economic injury disaster loans

Working capital loans to help meet ordinary and necessary financial obligations that cannot be met as a direct result of the disaster.

Small businesses, small agricultural cooperatives, and most private, nonprofit organizations of all sizes.

$2 million aggregate for alleviating economic injury caused by the disaster.

Capped at 4 percent.

Not more than 30 years.

Source: GAO analysis of SBA documents. aThe $2 million limit for business loans applies to the combination of physical and economic injury loans, and it applies to all disaster loans to a business and its affiliates for each disaster. bInterest rates are periodically adjusted and vary for each disaster.

9Credit elsewhere is when SBA believes the business has the availability of credit from nonfederal sources on reasonable terms and conditions because of its cash flow and disposable assets. 13 C.F.R. §§ 123.104, 123.300.

10Certain small nurseries affected by a drought designated by the Secretary of Agriculture, small agricultural cooperatives, and producer cooperatives are eligible for economic injury disaster loans. 13 C.F.R. § 123.300(c).

Page 6 GAO-10-723 Federal Assistance to Small Businesses

SBA procedures generally require small businesses to submit an application for a physical disaster loan no later than 60 days following the disaster declaration and no later than 9 months after this date for an economic injury disaster loan.11 SBA may authorize an extension of the filing period.12 SBA procedures also generally require small businesses to arrange for and obtain all loan funds within 6 months from the date of the loan authorization and agreement.

Due to the overwhelming need for moderate-sized small business loans in severely distressed Gulf Coast communities following Hurricanes Katrina and Rita, SBA implemented the GO Loan Pilot in November 2005 specifically to encourage lenders to lend in these communities and to assist small businesses that could not obtain credit elsewhere with working capital and other general-purpose business loans.13 The pilot program was originally intended to last less than 1 year; however, because of the continuing and substantial needs of small businesses in the area, SBA has extended the program until September 30, 2010. As part of the program, SBA may provide an 85 percent guaranty to qualified lending partners, such as banks, that agree to make expedited loans available under SBA’s 7(a) Loan Program of up to $150,000 to small businesses located in communities affected by the disasters.14 Small businesses apply directly to qualified lenders under the program, who evaluate their creditworthiness and determine whether they require an SBA guaranty to make the loan. SBA agrees to make a decision on whether to apply a

11SBA publishes notice of a disaster declaration in the Federal Register, which generally includes the application deadline and the location for filing a loan application. 13 C.F.R. § 123.3(b).

12Following Hurricanes Katrina and Rita, SBA extended the application filing deadline for physical disaster loans and economic injury disaster loans, which varied by disaster and state. For example, in Louisiana, SBA extended the filing deadline for physical disaster loans until April 10, 2006, and the deadline for economic injury disaster loans until June 28, 2006.

13Eligibility for the GO Loan Pilot is limited to small businesses located in, locating to, or relocating in the parishes/counties that have been presidentially declared as disaster areas resulting from Hurricanes Katrina or Rita, plus any parishes/counties contiguous to those parishes/counties.

14The 7(a) Loan Program is intended to serve small business borrowers who could not otherwise obtain credit under suitable terms and conditions from the private sector without an SBA guaranty. With the exception of loans pursuant to section 506 of the American Recovery and Reinvestment Act of 2009, Pub. L. No. 111-5, 123 Stat. 115 (2009), under the program, SBA provides guaranties of up to 85 percent on loans up to $150,000 made by participating lenders.

Page 7 GAO-10-723 Federal Assistance to Small Businesses

guaranty to a loan within 24 hours. While SBA prescribes the maximum interest rate lenders can charge, the lender and borrower negotiate the actual rate. Lenders can charge a maximum interest rate of 6.5 percentage points over the prime rate for loans of $50,000 or less and a maximum rate of 4.5 percentage points over the prime rate for loans over $50,000.

HUD’s CDBG Disaster Recovery

HUD’s CDBG Program, created in 1974, is the most widely available source of federal assistance to state and local governments for neighborhood revitalization, housing rehabilitation activities, and economic development.15 Eligible activities include housing assistance, historic preservation, real property acquisitions, mitigation, demolition, and economic development. Because of the funding mechanism that the CDBG Program already has in place to provide federal funds to states and localities, the program is widely viewed as a convenient tool for disbursing large amounts of federal funds to address emergency situations. Over the past two decades, CDBG has repeatedly been adapted as a vehicle to respond to federal disasters, such as floods, hurricanes, and terrorist attacks. When the CDBG Program is used to provide disaster relief funds, many of the statutory and regulatory provisions governing the use of CDBG funds may be waived or modified, thereby providing states with even greater flexibility and discretion.

Following Hurricanes Katrina and Rita, Congress enacted three supplemental appropriations between December 2005 and November 2007, under which a total of $19.5 billion was made available in CDBG disaster relief funds to Alabama, Louisiana, Mississippi, and Texas.16 Louisiana received the largest amount of these funds—$13.4 billion (69

15Activities funded with CDBG must address at least one of the following three objectives: (1) principally benefit low- and moderate-income persons, (2) aid in eliminating or preventing slums or blight, or (3) meet principally urgent community development needs.

16Department of Defense, Emergency Supplemental Appropriations to Address Hurricanes in the Gulf of Mexico, and Pandemic Influenza Act, 2006, Pub. L. No. 109-148, 119 Stat. 2680, 2779-2780 (2005); Emergency Supplemental Appropriations Act for Defense, the Global War on Terror, and Hurricane Recovery, 2006, Pub. L. No. 109-234, 120 Stat. 418, 472 (2006); and Department of Defense Appropriations, Pub. L. No. 110-116, 121 Stat. 1295, 1343 (2007). HUD was responsible for allocating the funds from the first two supplemental appropriations among the states in accordance with legal requirements. A third supplemental appropriation passed on November 13, 2007, and provided an additional $3 billion exclusively for Louisiana. These supplemental appropriations also included funds for Florida as a result of Hurricanes Katrina and Wilma. However, Florida is outside the scope of our review, therefore, those amounts are not included in our total.

Page 8 GAO-10-723 Federal Assistance to Small Businesses

percent)—and Mississippi received about $5.5 billion (about 28 percent).17 Alabama and Texas received a combined $599 million—about 3 percent of the total. (See table 2.)

Table 2: Amount of CDBG Disaster Relief Funds Provided for Hurricanes Katrina and Rita, by Selected States

Alabama Louisiana Mississippi Texas Total

1st supplemental CDBG appropriation $74,388,000 $6,210,000,000 $5,058,185,000 $74,523,000 $11,417,096,000

2nd supplemental CDBG appropriation 21,225,574 4,200,000,000 423,036,059 428,671,849 5,072,933,482

3rd supplemental CDBG appropriation - 3,000,000,000 - - 3,000,000,000

Total $95,613,574 $13,410,000,000 $5,481,221,059 $503,194,849 $19,490,029,482

Percentage of total 0.5% 68.8% 28.1% 2.6%

Sources: GAO analysis of Federal Register notices, including 71 Fed. Reg. 7666 (Feb. 13, 2006); 71 Fed. Reg. 63337 (Oct. 30, 2006); 72 Fed. Reg. 70472 (Dec. 11, 2007); and 73 Fed. Reg. 46312 (Aug. 8, 2008).

Note: The third appropriation, an allocation of $3 billion to the State of Louisiana, was solely for the purpose of covering costs associated with the state’s Road Home Program.

Once HUD allocated CDBG disaster relief funds to the affected states, state-level development agencies were responsible for the administration and management of the funds. States are traditionally afforded broad discretion regarding how they decide to allocate CDBG funds to specific projects and programs. In the aftermath of the hurricanes, Congress provided additional flexibility to the states in their use of CDBG disaster relief funds. For example, lawmakers permitted HUD to waive certain regulations and statutes that would otherwise have been applicable, including, among other things, income targeting provisions and public service expenditure caps.18 Specifically, HUD was allowed to waive the threshold outlined in statute that 70 percent of total funds must be allocated to activities that primarily benefit low- and moderate-income persons.19 Instead, only 50 percent of the total funds had to be targeted on this basis, unless the Secretary of HUD found a compelling need to waive the targeting provision altogether. Specific language in the supplemental appropriations acts required states to develop and submit action plans to HUD detailing the proposed use of all funds. Upon submission, HUD

17For more information on how Louisiana and Mississippi allocated their CDBG disaster relief funds, see GAO, Gulf Coast Disaster Recovery: Community Development Block

Grant Program Guidance to States Needs to Be Improved, GAO-09-541 (Washington, D.C.: June 19, 2009).

18Pub. L. No. 109-148, 119 Stat. at 2780; and Pub. L. No. 109-234, 120 Stat. at 472-73.

1942 U.S.C. § 5304(b)(3).

Page 9 GAO-10-723 Federal Assistance to Small Businesses

reviewed the action plans for acceptance. These action plans served as state proposals for how states would use their share of CDBG disaster relief funds and included descriptions of eligibility criteria and how the funds would be used to address both urgent needs and long-term recovery and infrastructure restoration. For example, states can use CDBG disaster relief funds to help businesses retain or create jobs in disaster-impacted areas as an eligible economic development activity.

Following Hurricanes Katrina and Rita, Louisiana and Mississippi implemented small business assistance programs using CDBG disaster relief funds. Louisiana implemented the following three programs:

• Bridge Loan Program: This program provided temporary working capital loans to businesses located in specified areas affected by the hurricanes. The loans generally had 6-month terms, but extensions were granted to some borrowers. They also contained an interest-free period of 180 days under certain circumstances. No new loans were originated after March 2006, as the state implemented the Business Recovery Grant and Loan Program.

• Business Recovery Grant and Loan Program: This program, launched in January 2007, targets assistance to small firms that are deemed to have a chance to survive, contribute to the economy, and maintain and create jobs. Small businesses receive low-cost loans on flexible terms, small grants to reimburse businesses for tangible losses, and technical assistance. Program eligibility has changed over time. For example, when the program was originally structured, only businesses with fewer than 25 employees were eligible; however, according to state officials, the need for these grants and loans was too great, and they increased the employee limit to businesses with fewer than 100 employees. Additionally, state officials told us that they changed the eligibility requirements to allow start-up companies to participate in the program. They explained that this change was made to ensure that entrepreneurial opportunities were encouraged in the state. Small businesses may use grant and loan funds for business operating costs, such as leases; insurance; or debt payment on new equipment, utilities, or inventory. When the program was initially implemented, the interest rate for loans was 0 percent for the term of the loan. Since then, the interest rate has been revised and is 0 percent for the first 2 years of the loan and 4 percent for the remainder of the loan term. Loan terms range from 5 to 7 years.

• Technical Assistance Program: Louisiana developed this program to help small businesses adjust to the posthurricane business environment.

Page 10 GAO-10-723 Federal Assistance to Small Businesses

Through the program, small businesses, including nonprofits, that have been adversely impacted by the hurricanes can receive technical assistance in areas such as business management, strategic planning, accounting, insurance, marketing, and legal matters. Additionally, entrepreneurs or individuals seeking to start a new firm in the impacted area are eligible for the program. State officials told us that the program was designed to complement the Business Recovery Grant and Loan Program, and that it provides assistance to small businesses that received grants or loans to help ensure that the funds are utilized effectively by small businesses.

In 2009, Mississippi implemented one program specifically for small businesses, the Hancock County Job Generation Fund Program, with CDBG disaster relief funds. The program grew out of a grassroots effort by the Hancock County Chamber of Commerce to address the extraordinary needs of small businesses in Hancock County that sustained the most powerful forces of Hurricane Katrina and suffered unprecedented destruction. The program offers loans at a 2 percent interest rate to small businesses that were located in Hancock County 6 months prior to Hurricane Katrina and are committed to remaining there for at least 5 years. Unlike SBA disaster loans or loans made through Louisiana’s Business Recovery Grant and Loan Program, loans made through the Job Generation Fund Program can be converted into forgivable loans if the loan recipient meets certain requirements. For example, a small business owner who purchases and rehabilitates a building in the county to meet current area building codes (if necessary) and maintains business operations in that building for a minimum of 5 years is eligible for a portion of the loan to be forgivable.

EDA Disaster Assistance EDA was established in 1965 within the Department of Commerce to

generate jobs, help retain existing jobs, and stimulate industrial and commercial growth in economically distressed areas of the United States.20 According to EDA, its statutory mandate, as applied to postdisaster

20Public Works and Economic Development Act of 1965, as amended (42 U.S.C. § 3121 et seq.). Upon receipt of an application for investment assistance, EDA measures project eligibility on the basis of (1) an unemployment rate that is, for the most recent 24-month period for which data are available, at least 1 percentage point higher than the national average unemployment rate; (2) per capita income that is, for the most recent period for which data are available, 80 percent or less of the national average per capita income; or (3) a special need circumstance, such as a natural disaster or military base closure, as defined in 13 C.F.R. § 300.3.

Page 11 GAO-10-723 Federal Assistance to Small Businesses

assistance, is to help formulate and implement economic recovery strategies to restore, replace, and expand economic activity in disaster-impacted regions and prioritize projects that will diversify the economic base and lead to a stronger, more globally competitive and disaster-resilient regional economy. In the past, Congress enacted supplemental appropriations for EDA to use in response to natural disasters. For example, following Hurricane Andrew in 1992, Congress appropriated approximately $75 million to EDA under the Supplemental Appropriations, Transfers, and Rescissions Act, 1992.21 In addition, EDA received an initial supplemental appropriation of $100 million for use in regions covered by a major disaster declaration under the Stafford Act, as a result of recent natural disasters, under the Military Construction, Veterans’ Affairs, and Related Agencies Appropriations Act, 2008.22 Congress enacted a second supplemental appropriation for EDA in the amount of $400 million as part of the Consolidated Security, Disaster Assistance, and Continuing Appropriations Act, 2009.23

EDA did not receive a supplemental appropriation for postdisaster recovery assistance following Hurricanes Katrina and Rita. However, the agency used its existing programs, including the RLF Program, to assist with small business recovery efforts in the Gulf Coast region. Under the RLF Program, EDA awards grants on a competitive basis to eligible applicants to establish revolving loan funds. RLF grantees provide loans to small businesses or businesses that cannot otherwise borrow capital from private lending institutions.24 When making loans, RLF grantees must partner with private lending institutions to leverage additional capital for

21Pub. L. No. 102-368, 106 Stat. 1117 (1992).

22Pub. L. No. 110-252, 122 Stat. 2323 (2008).

23Pub. L. No. 110-329, 122 Stat. 3574 (2008).

24States, cities, or other political subdivisions of a state, District Organizations, Indian Tribes, public or private nonprofit organizations, and institutions of higher education may apply for RLF grants. An application for an RLF grant must include or incorporate by reference (if so-approved by EDA) a comprehensive economic development strategy. In addition, grantees must manage RLFs in accordance with an RLF Plan (described in 13 C.F.R. § 307.9) that sets out the RLF’s financing strategy, policy, and portfolio standards. Under the RLF program, EDA does not distinguish between loans made to small businesses and loans made to other businesses. However, EDA officials told us that nearly 100 percent of RLF business lending is to businesses with 500 employees or fewer. Therefore, for our purposes throughout this report, we are assuming that RLF loans were provided to small businesses.

Page 12 GAO-10-723 Federal Assistance to Small Businesses

borrowers.25 Consistent with EDA’s mission to attract private capital investment, RLF grantees generate additional investments for small businesses and entrepreneurial ventures to diversify the regional economy. As borrowers repay loans, RLF grantees use a portion of the interest earned to pay administrative expenses and add the remaining principal and interest repayments to the fund’s capital base to make additional loans. Following the hurricanes, EDA recapitalized four of its RLF grantees in Louisiana for a total of $2 million to make loans to businesses affected by the disasters.26

Contracting by Federal Agencies Following Disasters

In addition to the federal assistance programs that we have previously discussed, many federal agencies carry out emergency response activities through contracts with private businesses, including those for debris removal, reconstruction, and the provision of supplies. Federal agencies’ contracts with private businesses, whether made in the normal course of agency operations or specifically related to a natural disaster declaration, in most cases, are subject to certain goals to increase participation by various types of small businesses. The Small Business Act requires that the President set a governmentwide goal each fiscal year for small business participation for the total value of all prime contracts awarded directly by an agency.27 Additionally, the Small Business Act sets annual prime contract dollar goals for participation by five specific types of small businesses: small businesses, small disadvantaged businesses, businesses

25RLF loans must be used to leverage private investment of at least 2 dollars for every 1 dollar of such RLF loans. This leveraging requirement applies to the RLF portfolio as a whole rather than to individual loans and is effective for the duration of the RLF’s operation. Private investment may include capital invested by the borrower or others, financing from private entities, or the nonguaranteed portion and 90 percent of the guaranteed portions of SBA 7(a) loans and 504 debenture loans. 13 C.F.R. § 307.15(d). According to an EDA official, when working with private lenders, RLF grantees assume the majority of financial risk because should the borrower default on the loan, private lenders recoup their investments first, after which grantees are allowed to recover their investment amount.

26Recapitalization grants are the investments of additional grant funds to increase the capital base of an RLF. 13 C.F.R. § 307.8.

2715 U.S.C. § 644(g). Under this provision, the President must annually establish governmentwide goals for, among other things, procurement contracts awarded to small business concerns. The governmentwide goal for participation by small business concerns must not be less than 23 percent of the total value of all prime contracts awarded for each fiscal year. As stipulated in the Small Business Act, procurement goals are established as a percentage of the total value of all contracts directly awarded by the federal government in a fiscal year.

Page 13 GAO-10-723 Federal Assistance to Small Businesses

owned by women, businesses owned by service-disabled veterans, and businesses located in historically underutilized business zones (HUBZone).28 The Stafford Act also requires federal agencies to give contracting preferences, to the extent feasible and practicable, to organizations, firms, and individuals residing in or doing business primarily in the area affected by a major disaster or emergency.29

The Federal Acquisition Regulation (FAR) implements many federal procurement statutes and provides executive agencies with uniform policies and procedures for acquisition. For example, the FAR generally requires that executive agencies report information about procurements directly to FPDS-NG, a governmentwide contracting database that collects, processes, and disseminates official statistical data on all federal contracting activities that are greater than the micro-purchase threshold (generally $3,000).30 This system automatically obtains from other systems or online resources additional information that is important to the procurement, such as the contractor’s location.

The FAR also requires agencies to measure small business participation in their acquisition programs. A small business may participate via prime contracts—which are contracts awarded directly by a federal agency—or

2815 U.S.C. § 644(g). The Small Business Act defines these businesses as follows: (1) Small businesses are those that are independently owned and operated and are not dominant in their field of operations. (2) Small disadvantaged businesses must be owned and controlled by socially and economically disadvantaged individuals—such as African Americans, Hispanic Americans, Asian Pacific Americans, Subcontinent Asian Americans, or Native Americans. These owners must have at least a 51 percent stake in the business. (3) Women-owned small businesses must have at least 51 percent female ownership. For publicly owned businesses, one or more women must hold at least 51 percent of the stock and control both management and daily business operations. (4) Service-disabled veteran-owned small businesses must be owned—also at least 51 percent—by one or more veterans with a service-related disability. In addition, the management and daily operations of the business must be controlled by one or more veterans with a service-related disability. (5) HUBZone small businesses must have their principal offices physically located in these historically underutilized business zones, which are economically distressed metropolitan or nonmetropolitan areas—that is, areas with low-income levels or high unemployment rates—and must employ some staff who live in these zones. The small business regulations implementing the Small Business Act further define these businesses. 13 C.F.R. §§ 121.401–121.413.

2942 U.S.C. § 5150.

30FAR 4.603(b). In 2006, the FPDS-NG reporting threshold was raised from $2,500 to $3,000. 71 Fed. Reg. 57364 (Sept. 28, 2006). In 2008, the reporting threshold for FPDS-NG was set at the micro-purchase threshold for most types of contract awards. 73 Fed. Reg. 21773 (Apr. 22, 2008) (interim); and 74 Fed. Reg. 2712 (Jan. 15, 2009) (final).

Page 14 GAO-10-723 Federal Assistance to Small Businesses

through subcontracts.31 Any business receiving a contract directly from a federal executive agency for more than the simplified acquisition threshold32 must agree in the contract that small businesses will be given the “maximum practicable opportunity” to participate in the contract “consistent with its efficient performance.”33 Additionally, for acquisitions (or modifications to contracts) that (1) are individually expected to exceed $550,000 ($1 million for construction contracts) and (2) have subcontracting possibilities, the solicitation shall require the apparently successful offeror in a negotiated acquisition to negotiate a subcontracting plan that is acceptable to the contracting officer, and each invitation for bid shall require the bidder selected for award to submit a subcontracting plan to be eligible for award.34 The subcontracting plan must include certain information, such as a description of the types of work the prime contractor believes it is likely to award to subcontractors, as well as goals, expressed as a percentage of total planned subcontracting dollars, for the use of small businesses.35 Generally, contracts that offer subcontracting possibilities and are expected to exceed the monetary thresholds that we have previously mentioned are to include certain clauses.36 These clauses require that for contracts that have individual subcontracting plans, prime contractors generally must semiannually and at project completion report on their progress toward reaching the goals in their subcontracting plans. Generally, contractors that have individual subcontracting plans are required to report on their subcontracting goals and accomplishments twice a year to the federal government through eSRS, which is a governmentwide database for capturing this information. Furthermore, the

31FAR 44.101 defines a subcontractor as “any supplier, distributor, vendor, or firm that furnishes supplies or services to or for a prime contractor or another subcontractor.”

32FAR 2.101 defines “simplified acquisition threshold” to mean $100,000, except when the acquisition of supplies or services is used to support a contingency operation or facilitate against nuclear, biological, chemical, or radiological attack. In those instances, the term means $250,000 for contracts to be awarded and performed inside the United States and $1 million for contracts to be awarded and performed outside of the United States.

33FAR 19.702, 2.101.

34The dollar threshold was changed to $550,000 on September 28, 2006. 71 Fed. Reg. 57363 (Sept. 28, 2006).

35These and other aspects of the small business subcontracting plan requirement are set forth at FAR Subpart 19.7.

36Contracts that are below the simplified acquisition threshold, are personal services contracts, are to be performed entirely outside of the United States, are set aside, or are to be accomplished under the 8(a) program do not require this clause.

Page 15 GAO-10-723 Federal Assistance to Small Businesses

agencies’ administrative contracting officers are responsible for monitoring the prime contractors’ activities and evaluating and documenting contractor performance under any subcontracting plan included in the contract. The contracting officer is tasked with acknowledging receipt of the reports submitted to eSRS.37

Federal funds were used for a number of different small business assistance programs following Hurricanes Katrina and Rita. While the SBA Disaster Loan Program is the primary federal program for funding long-range recovery for the private sector, two states—Louisiana and Mississippi—also developed small business assistance programs using CDBG disaster relief funds that Congress provided in response to the hurricanes. Additionally, although EDA did not receive supplemental disaster appropriations, the agency provided funds to Gulf Coast small businesses for new business start-ups and business expansion through its Revolving Loan Fund Program. However, despite the assistance provided, some small businesses have struggled with recovering from the hurricanes, and loan performance has varied for the various federally funded loan programs.

Federally Funded Programs Have Helped to Address Different Needs of Small Businesses, but Some Small Businesses Still Face Challenges, and the Performance of Federally Funded Loans Has Varied

SBA Provided Gulf Coast Small Businesses with Assistance to Repair Disaster-Damaged Property and Address Economic Losses

SBA provided about $1.4 billion in loans to Gulf Coast businesses of all sizes following Hurricanes Katrina and Rita through its Disaster Loan and GO Loan programs to assist with the repair or replacement of disaster-damaged property, mitigate economic losses that small businesses incurred as a result of the hurricanes, and provide working capital loans to businesses in severely distressed areas. The Disaster Loan Program accounted for about $1.2 billion of the $1.4 billion SBA provided in loans to Gulf Coast businesses. As table 3 shows, SBA approved over 13,400 disaster loans for businesses of all sizes affected by the hurricanes from fiscal years 2005 through 2009, and more than 10,700 of these loans were identified as having assisted small businesses (economic injury disaster loans, and physical and economic injury disaster loans). Also, an

37On July 16, 2010, the FAR was updated to include additional guidance on eSRS, including reporting time frames for subcontracting accomplishment reports and clarification of when a contracting officer shall reject a report as not adequately completed. 75 Fed. Reg. 34260 (June 16, 2010); 73 Fed. Reg. 21779 (Apr. 22, 2008).

Page 16 GAO-10-723 Federal Assistance to Small Businesses

unidentifiable number of small businesses received physical disaster loans. SBA approved about 96 percent of these loans in fiscal year 2006.

Table 3: SBA Disaster Loans Approved for Businesses, Hurricanes Katrina and Rita, Fiscal Years 2005-2009

Dollars in millions

All businesses Small businesses

Disaster loan type Number Amount Number Amount

Physicala 2,743 $347.5 b b

Economic injury 2,491 147.9 2,491 $147.9

Physical and economic injuryc 8,219 747.7 8,219 747.7

Totald 13,453 $1,243.1 10,710 $895.6

Source: GAO analysis of SBA data. aBusinesses of all sizes are eligible for physical disaster loans, but SBA does not maintain data in DCMS on business size for these types of loans. bData are unavailable. cThis category refers to loans that include both a physical and economic injury disaster loan component. Borrowers receiving both of these loans were identified as small businesses because only small businesses are eligible for economic injury loans. dTotals for small businesses may exceed the totals shown because we could not determine the amount and number of physical disaster loans approved specifically for small businesses. These totals exclude 5,921 approved disaster loans, valued at about $686 million, that were later canceled. According to SBA operating procedures, reasons for cancellations include, among others, the verbal or written request of the borrower, the borrower failing to complete and return all loan closing documents by the deadline, and the borrower not satisfying all terms and conditions of the loan agreement.

As table 4 shows, approved SBA disaster loans identified as going to small businesses totaled over $578 million for small businesses in Louisiana and more than $197 million for small businesses in Mississippi.

Table 4: SBA Disaster Loans Approved for Small Businesses in Gulf Coast States, Hurricanes Katrina and Rita, Fiscal Years 2005-2009

Dollars in millions

Alabama Louisiana Mississippi Texas

Disaster loan type Number Amount Number Amount Number Amount Number Amount

Physicala b b b b b b b b

Economic injury 94 $7.4 1,718 $103.0 382 $20.1 297 $17.4

Physical/Economic injuryc 229 32.4 5,237 475.5 1,980 177.2 773 62.7

Totald 323 $39.8 6,955 $578.5 2,362 $197.3 1,070 $80.1

Source: GAO analysis of SBA data.

Page 17 GAO-10-723 Federal Assistance to Small Businesses

aBusinesses of all sizes are eligible for physical disaster loans, but SBA does not maintain data in DCMS on business size for these types of loans. bData are unavailable. cThis category refers to loans that include both a physical and economic injury disaster loan component. Borrowers receiving both of these loans were identified as small businesses because only small businesses are eligible for economic injury loans. dTotals for small businesses may exceed the totals shown in this table because we could not determine the amount and number of physical disaster loans approved specifically for small businesses.

In focus groups that we conducted, several small business owners told us about the benefits associated with receiving SBA disaster loans. For example, one small business owner who operates three grocery stores in New Orleans that sustained severe wind and water damage in Hurricane Katrina noted that the SBA physical and economic injury loans she received gave her a little flexibility in paying her vendors because the vendors were more confident knowing that federal funds were involved and were willing to wait on payments until she received the loan funds. Another small business owner, who operates a Mardi Gras supply store in New Orleans, lost over $1 million in inventory as a result of Hurricane Katrina. She also received both an SBA physical loan and an economic injury loan and said that when she received the loan funds, she was able to pay off her bank line of credit, which prior to receiving the funds, she had not been able to do in 3 years. Another small business owner in New Orleans explained that the SBA physical disaster loan she received allowed her to purchase equipment, and that without the loan her business would be closed today. She added that the loan also made her more aware of the resources that are provided through the local SBDC. Finally, a New Orleans small business owner who operates an automobile service center explained that her center was flooded by 10 feet of water when the levees broke, which destroyed all of the equipment. She said that the SBA physical and economic injury loans she received were the only way she was able to get the business restarted.

SBA also approved about 1,600 GO loans for small businesses in the Gulf Coast states, totaling about $116 million from fiscal years 2005 through 2009 (table 5).

Page 18 GAO-10-723 Federal Assistance to Small Businesses

Table 5: Number and Amount of Approved GO Loans for Small Businesses in Gulf Coast States, Fiscal Years 2005-2009

Dollars in millions

Approved GO loans

State Number Amount

Alabama 85 $4.7

Louisiana 598 54.7

Mississippi 802 49.8

Texas 88 6.9

Totala 1,573 $116.1

Source: GAO analysis of SBA data. aThese totals exclude 221 approved GO loans, valued at $17.6 million that were later canceled. According to SBA operating procedures, reasons for cancellations include, among others, the lender or the applicant indicating that the applicant does not intend to utilize the proceeds or there has been an adverse change.

SBA awarded Mississippi small businesses the greatest number of these loans, but Louisiana small businesses received the greatest amount of funds. According to officials from three local SBA district offices, the GO Loan Program has been popular with lenders and has helped with recovery efforts, as well as offsetting some of the effects of the tightening of the credit markets. Additionally, one local SBDC director stated that he believes the GO Loan Program should be considered a best practice in helping small businesses recover from disasters. Others with whom we spoke also expressed positive views of the program, including lender support for the program and the stability the program helped provide to the region.

Louisiana and Mississippi Used CDBG Disaster Relief Funds to Implement State-Run Programs to Further Assist Gulf Coast Small Businesses

As of December 31, 2009, Louisiana had used about $179 million in CDBG disaster relief funds for three programs to specifically assist small business recovery efforts. Mississippi had developed one program specifically to assist small businesses to which it targeted $3 million in CDBG disaster relief funds; however, as of April 2010, the state was in the process of developing program details and no funds had been spent. The three programs that Louisiana developed are discussed in the following text.

• Bridge Loan Program: Louisiana used about $5.7 million in CDBG disaster relief funds to provide about 800 small businesses with temporary working

Page 19 GAO-10-723 Federal Assistance to Small Businesses

capital loans.38 State officials told us that money was not disbursed for this program after March 2006, and that remaining funds were transferred to the Business Recovery Grant and Loan Program.

• Business Recovery Grant and Loan Program: As of December 31, 2009, Louisiana had used about $164 million in CDBG disaster relief funds and provided over 4,500 Louisiana small businesses grant and loan assistance.39 Under this program, the state has assisted small businesses that applied for conventional or SBA loans but either had not received them or still needed additional assistance. Additionally, state program officials told us that the program helped to provide assistance to certain businesses that were not eligible for SBA disaster loans. For example,state official explained that some fishermen’s boats were completely destroyed during the hurricanes, and that the fishermen did not have the collateral needed to obtain SBA disaster loans. However, because collateral was not needed for this program, these fishermen were eligible. In fact, over 25 percent of the small businesses that are participating in this progra

a

m is in the fishing industry.

• Technical Assistance Program: As of December 31, 2009, Louisiana had used almost $8.9 million in CDBG disaster relief funds to assist about 3,800 small businesses with adjusting to the posthurricane business environment. Over 2,200 of these small businesses were entrepreneurs or start-up companies looking to open businesses in the areas impacted by the hurricanes.

During focus groups that we conducted, Louisiana small business owners also told us about the benefits associated with assistance provided through these programs. For example, one small business owner who operates two retail shoe and accessory stores located in New Orleans explained that her participation in the Business Recovery Grant and Loan Program allowed her to pay down lines of credit that had higher interest rates. Another small business owner who owns a tourist-related gift shop in New Orleans explained that as a result of her small business recovery loan, she was able to purchase merchandise in time for the National Football League Super Bowl in 2010, which helped to boost her sales. She

38According to Louisiana state program officials, the total number of businesses that received loans may be overstated because some businesses received more than one loan.

39Included in this amount were grant assistance of about $67.7 million and loan assistance of about $82 million, according to Louisiana state program officials.

Page 20 GAO-10-723 Federal Assistance to Small Businesses

stated that without the $80,000 loan she received from the program, she would not have been able to stay in business. Another small business owner who operates a bridal shop stated that the assistance she received from the Business Recovery Grant and Loan Program allowed her, among other things, to pay 3 months of operating expenses and reduce the debt owed to some of her manufacturers, which allowed her to buy new product. Finally, one small business owner who prior to Hurricane Katrina was a self-employed consultant to minority business owners stated that the Technical Assistance Program had been extremely helpful. She explained that many small businesses had utilized this program, and that for many of her previous non-English-speaking clients, the program provided the only technical assistance they received after the hurricanes.

According to SBA data we reviewed, the agency determined that 76 small businesses approved for loans under Louisiana’s Business Recovery Grant and Loan Program received duplicate benefits under SBA’s Disaster Loan Program. The Stafford Act prohibits disaster victims from receiving duplicate federal benefits for the same loss.40 SBA and the State of Louisiana developed a process to identify approved Business Recovery Grant and Loan Program applicants who might receive duplicate benefits. A senior-level Louisiana state official told us that having an SBA disaster loan did not necessarily disqualify a small business from the state’s program; rather, the state looked specifically at how the business intended to use the funds and compared that with how the small business used the SBA loan funds. If the intended use of the funds was not the same, then a small business could still receive assistance under both programs. The 76 small businesses determined to have received duplicate benefits for the same loss were required to pay off or pay down their SBA disaster loans with the funds they received under the Business Recovery Grant and Loan Program. These businesses returned about $1.3 million to SBA.

As of April 2010, 42 small businesses located in Hancock County, Mississippi, were approved for loans under the Hancock County Job Generation Fund Program. The state targeted $3 million in CDBG disaster relief funds for this program. However, according to a program official, no loans had been closed because they were working with HUD on remaining program compliance issues. State officials told us that the towns in

4042 U.S.C. § 5155. The receipt of partial benefits does not preclude additional federal assistance for any part of a loss or need for which benefits have not been provided. 42 U.S.C. § 5155(b)(3).

Page 21 GAO-10-723 Federal Assistance to Small Businesses

Hancock County are based around a small business community, and that the bulk of the businesses were located in Hurricane Katrina’s surge area; therefore, there has been a need to provide additional working capital to these businesses until infrastructure repair in the area is complete. During focus groups that we conducted, one Mississippi small business owner who owns a brewery stated that he expects that the funds for which he has been approved will allow him to hire four or five additional employees. He added that he believes that the program is well focused and has the potential for doing a lot of good for the county.

Alabama, Louisiana, and Mississippi also utilized CDBG disaster relief funds for other efforts that benefited small businesses following the hurricanes. For example, while Alabama did not develop programs specifically for small business recovery, state officials noted that small businesses did benefit from the contracts that the state issued for the infrastructure programs funded with CDBG disaster relief funds because the state utilized mostly small and local businesses for such projects. In addition, a senior-level HUD official told us that Louisiana utilized $200 million to subsidize state energy rates, which prevented a large rate increase after the hurricanes and benefited all state residents, including small business owners. Furthermore, Mississippi state officials told us that they used $30 million in CDBG disaster relief funds to subsidize the state’s commercial insurance wind pool between fiscal years 2007 and 2008, which directly benefited small businesses. According to state officials, this subsidy lowered insurance premiums for small businesses, which in turn had increased significantly following the hurricanes. Additionally, state officials noted that the state’s use of CDBG disaster relief funds to repair bridges, roads, and other public infrastructure was critical for small business recovery because this work allowed people to move back to the coastal area, which in turn helped small businesses rebuild their customer base.

Page 22 GAO-10-723 Federal Assistance to Small Businesses

EDA RLF Grantees Have Provided Gulf Coast Small Businesses with Loans to Start New Businesses or Expand Existing Businesses

EDA RLF grantees made approximately $36 million in below-market-rate loans to Gulf Coast small businesses following the hurricanes, primarily for new business start-ups, existing business expansion, and job retention. According to RLF grantee reports we reviewed, these investments generated approximately $196 million in private investment. Table 6 shows the amount EDA invested across the four states in the Gulf Coast region, as well as the total amount of private investments.

Table 6: Total Amount of RLF and Private Investment, by Selected States

Financing, by source Alabama Louisiana Mississippia Texas Total

RLF investment $5,845,752 $8,933,500 $10,529,867 $11,086,482 $36,395,601

Private investment 62,635,470 11,016,627 49,235,276 73,222,743 196,110,116

Total $68,481,222 $19,950,127 $59,765,143 $84,309,225 $232,505,717

Source: GAO analysis of EDA’s RLF grantee data.

Note: The totals only include investments closed after September 1, 2005. aOne RLF grantee’s semiannual report was missing data on the amount of financing provided by the RLF; therefore, the total amount of RLF Investment listed for Mississippi may be understated.

As we have previously noted, EDA awarded $2 million in program funds to recapitalize—or provide additional funding to—four RLF grantees in Louisiana specifically to assist small businesses impacted by the hurricanes (see fig. 1).

Page 23 GAO-10-723 Federal Assistance to Small Businesses

Figure 1: Additional Funding Provided to Louisiana’s RLF Grantees for Disaster Recovery Purposes

Sources: GAO analysis of EDA data; MapInfo (map).

Jefferson Parish Economic Development Commission - $500,000

New Orleans Regional Loan Corporation - $600,000Acadiana

Regional Development District - $600,000

South Central Planning and Development Commission - $300,000

For example, the New Orleans Regional Loan Corporation, an RLF grantee, received $600,000 in additional program funds and made loans to seven small business owners for disaster recovery purposes. One small business owner who operated a restaurant received a loan of $75,000 to help cover uninsured expenses, including new equipment and clean-up costs. In addition, an operator of a service station that sustained flood damage received a loan of $250,000 to purchase new gasoline pumps. Another RLF grantee, the Jefferson Parish Economic Development Commission, received $500,000 in additional program funds; officials told us that they made loans to three small business owners impacted by the hurricanes, including a $340,000 loan to a printing company to purchase new equipment. Finally, the Acadiana Regional Development District used

Page 24 GAO-10-723 Federal Assistance to Small Businesses

their recapitalization amount of $600,000 to make loans to 14 small businesses.

Although EDA did not recapitalize RLF grantees in Alabama, Mississippi, and Texas, RLF grantees in heavily impacted areas of these states told us that they provided other forms of assistance to small businesses for disaster recovery efforts. For example, in Gulfport, Mississippi, an RLF grantee official reported they offered borrowers 2-month loan payment deferments. Similarly, in Beaumont, Texas, an RLF grantee offered 3-month payment deferrals after the hurricanes, but loan borrowers’ accounts continued to accrue interest, and principal was not waived.

Despite Federal Assistance, Small Business Owners Reported Several Challenges to Recovery Efforts

Despite the assistance that federal and state-run programs have provided to small businesses, some small business owners in focus groups that we conducted and others with whom we spoke cited challenges with participating in some of these programs, particularly the SBA Disaster Loan Program.

• Timeliness of assistance received: Several small businesses commented that they did not receive assistance in a timely manner, particularly under SBA’s Disaster Loan Program. One Mississippi small business owner of a storage facility told us it took him 9 months to receive funding from his SBA physical and economic injury disaster loans, during which he had to operate off of $50,000 of his savings and take outside employment to support himself. A wholesale trade small business owner in New Orleans told us that she applied for an SBA disaster loan in the middle of September 2005, received approval in August 2006, and received the final portion of the loan in December 2007. She added that during that period, she invested all income into the business and paid herself a minimum salary. Additionally, SBDC representatives and representatives of local chambers of commerce with whom we spoke stated that the length of time it took to receive SBA Disaster Loans caused difficulties for small businesses trying to sustain in the immediate aftermath of the hurricanes.

In July 2006, we reported that SBA faced an unprecedented demand for disaster loans while also confronting a significant backlog of applications; as a result, hundreds of thousands of loans were not disbursed in a timely

Page 25 GAO-10-723 Federal Assistance to Small Businesses

way.41 We also concluded that SBA had not fully planned for the implementation of its new disaster loan processing system—DCMS—which restricted the number of staff that could access the system and process the large volume of applications. Since then, SBA has taken several steps to reform its Disaster Loan Program, including creating an online loan application, increasing the capacity of DCMS, and developing a Disaster Recovery Plan.42

• Application process and requirements: Two Mississippi small business owners with whom we spoke discussed that they had difficult experiences in applying for SBA disaster loans. They both stated that they had problems with the SBA adjustment process, and that the damage to both of their properties was severely undervalued. Both also said that they had to work with several different SBA case managers throughout the application process, which contributed to their difficult experience because the new case manager was not familiar with actions that had previously occurred on their applications. Another small business owner in New Orleans explained that he needed a lot of financial records to apply for a SBA disaster loan, which presented problems. He said that all of his records sat in over 7 feet of water for 12 weeks and were completely destroyed. Local SBDC officials and officials from chambers of commerce also told us that in some instances, small business owners found the application process so complicated that they decided not to complete it, and that, in some cases, the business owners did not have the proper educational background to complete the application.

Local SBDC officials and officials from state and federal development agencies explained that some small business owners faced difficulty in meeting some of the loan program underwriting requirements for collateral. For example, some small businesses affected by Hurricanes Katrina and Rita were completely destroyed, and all that remained after the storm was the concrete slab on which their business had been located; many of these business owners also lost their homes. In these instances,

41GAO, Small Business Administration: Actions Needed to Provide More Timely Disaster

Assistance, GAO-06-860 (Washington, D.C.: July 28, 2006); and Small Business

Administration: Additional Steps Should Be Taken to Address Reforms to the Disaster

Loan Program and Improve the Application Process for Future Disasters, GAO-09-755 (Washington, D.C.: July 29, 2009).

42For more information on SBA actions to reform the Disaster Loan Program, see GAO, Small Business Administration: Continued Attention Needed to Address Reforms to the

Disaster Loan Program, GAO-10-735T (Washington, D.C.: May 19, 2010).

Page 26 GAO-10-723 Federal Assistance to Small Businesses

some small business owners were unable to meet the collateral requirements for loans.

In addition to the program-related challenges previously listed, many small business owners told us in focus groups that we conducted and others with whom we met reported more general challenges that have hindered small business recovery efforts, including an increased debt load; difficulties in receiving commercial insurance payouts, reduced insurance availability, and increased insurance costs; and difficulty in accessing capital.