Embed Size (px)

Citation preview

Functionality of Banks and Hedge Funds and

Contagion Between Financial Institutions: A System Dynamics Approach

Wednesday, March 13

Mila Getmansky

Andrew W. Lo

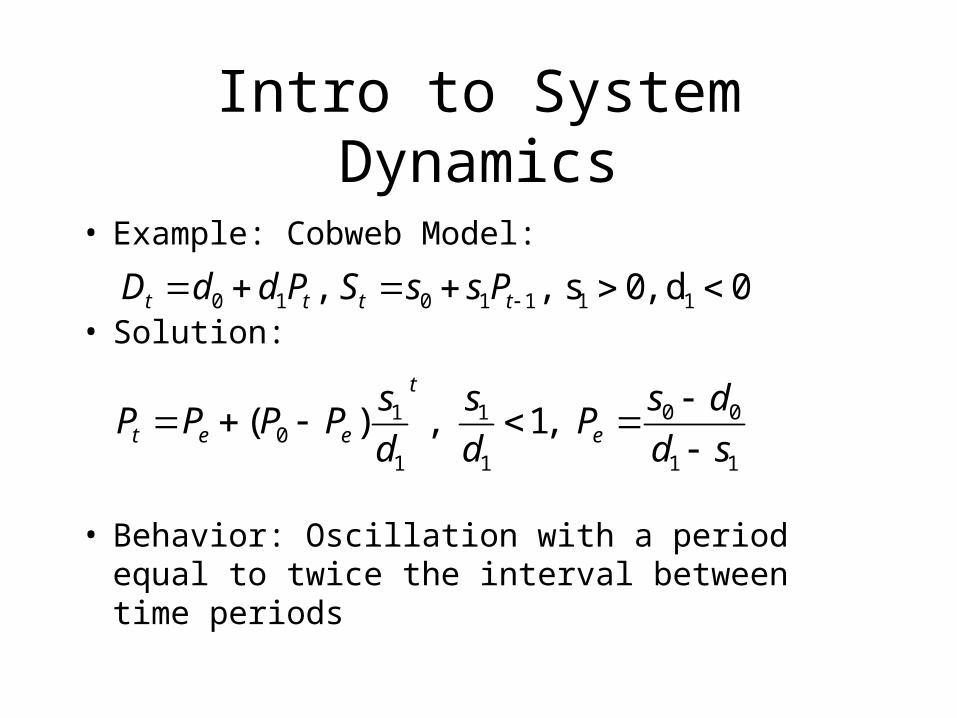

Intro to System Dynamics

• Example: Cobweb Model:

• Solution:

• Behavior: Oscillation with a period equal to twice the interval between time periods

0 1 0 1 1 1 1, , s 0, d 0t t t tD d d P S s s P

0 01 10

1 1 1 1

( ) , 1, t

t e e e

s ds sP P P P P

d d d s

Extensions

• Do not represent stock and flow structure of real markets (inventories, work in process, and production capacity)

• Formulated in discrete time• The interval between periods is assumed to

correspond to the time required to produce the commodity. However, the observed periods of commodity cycles are much greater than twice the production delays. (The construction time for commercial buildings is about 3 years, but the real estate cycle ranges from 10 to 20 years).

Extensions

• The model does not distinguish between production capacity and capacity utilization and so cannot explain the multiple oscillatory periods observed in many industries.

• Behavioral decision processes of the market are not modeled.

Corporate Growth Model

• Explain differences in: – Growth patterns– Stability– Market share– Profitability

• Different patterns found:– Within the same industry– Occurring in same time frame

• Not explained by:– Product– Quality

Model

• Size– 60 Levels (Integrations)– 250 Variables

• Top management power structure– 90% intangible variables

• Connect major sectors• Goals and traditions are the basis for decisions• Information channels (between market and

company)

SD Versus Traditional Approach

• Not an equilibrium model (unless at steady-state); Focus is Dynamics

• Objective: understand dynamics of underlying structure of a system such as hedge fund, contagion, etc.; model the impact of different scenarios and decisions versus finding an optimal point estimate

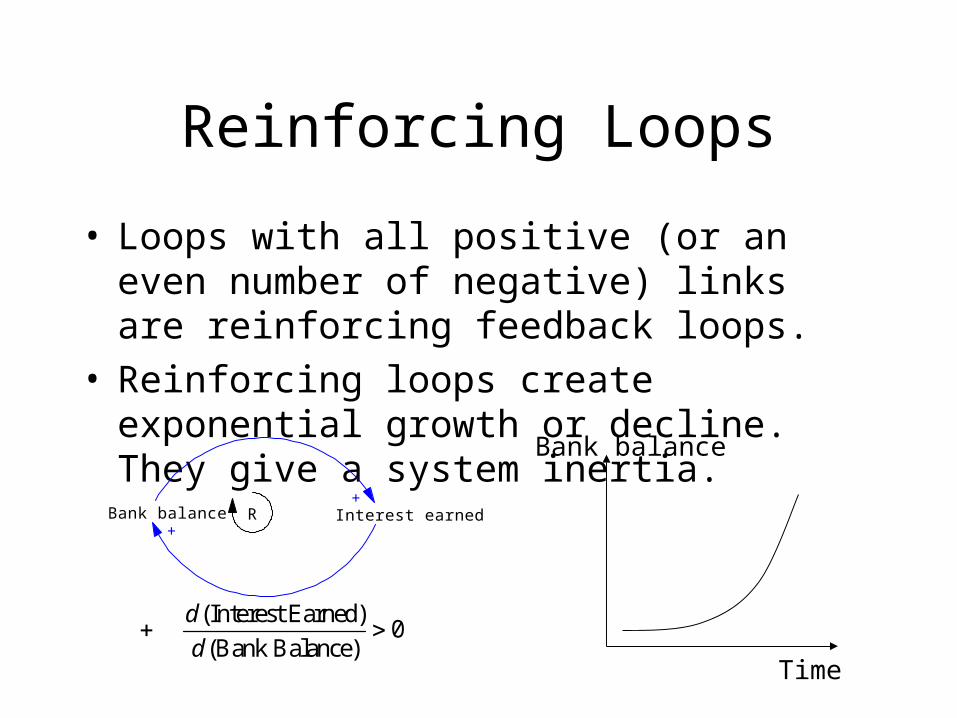

Reinforcing Loops

• Loops with all positive (or an even number of negative) links are reinforcing feedback loops.

• Reinforcing loops create exponential growth or decline. They give a system inertia.

Bank balance Interest earned+

+R

Time

Bank balance

(Interest Earned) 0

(Bank Balance)

d

d

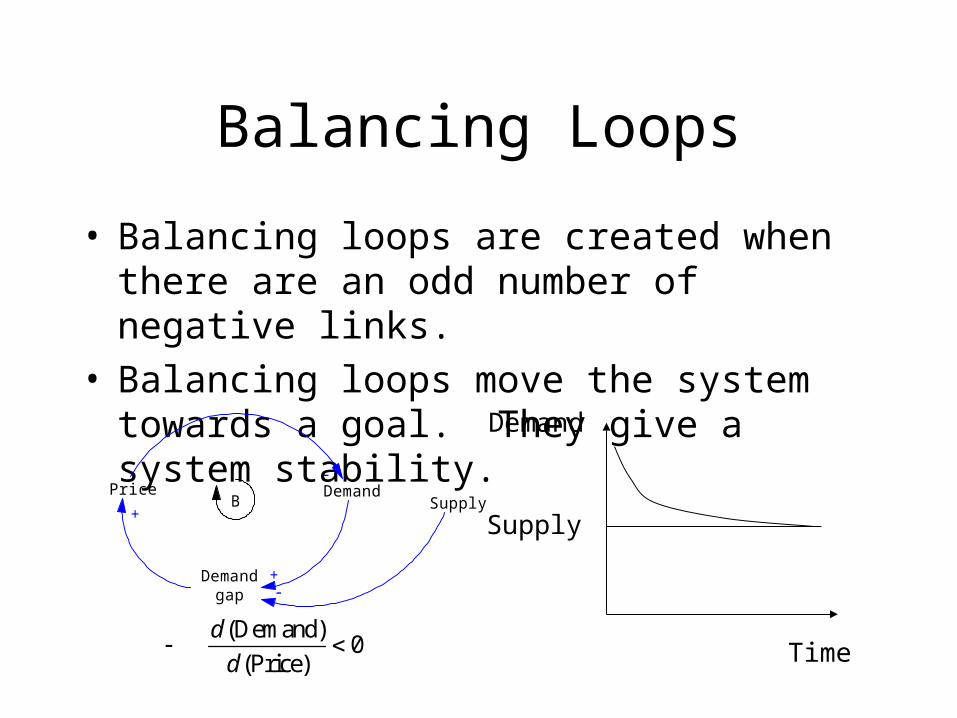

Balancing Loops

• Balancing loops are created when there are an odd number of negative links.

• Balancing loops move the system towards a goal. They give a system stability.

Price Demand-

B

Demandgap

+

+Supply

-

Time

Demand

Supply

(Demand) 0

(Price)

d

d

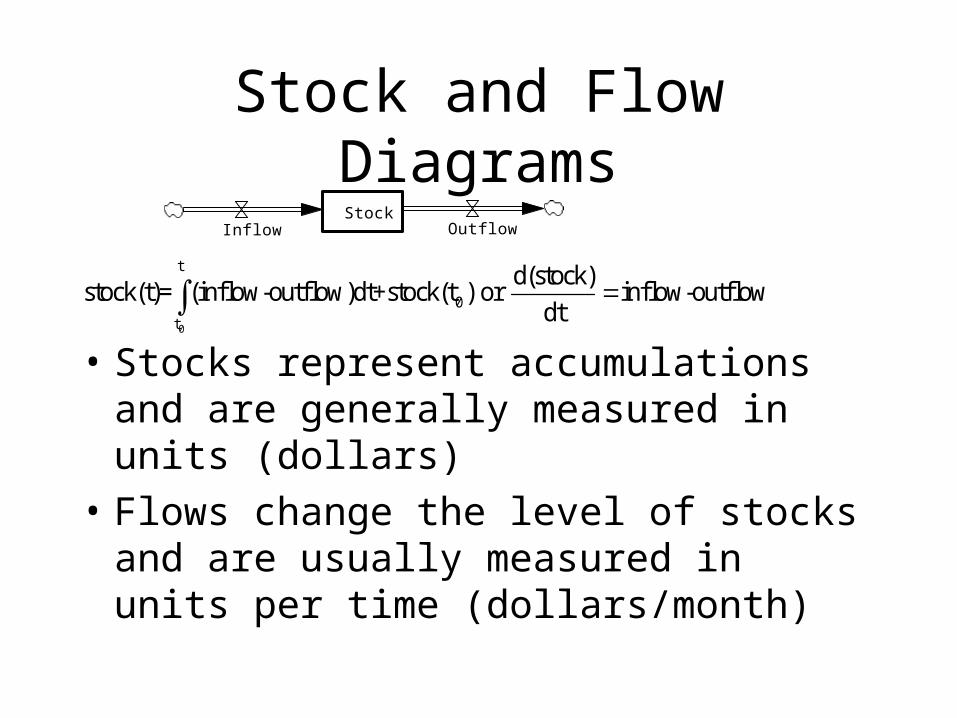

Stock and Flow Diagrams

• Stocks represent accumulations and are generally measured in units (dollars)

• Flows change the level of stocks and are usually measured in units per time (dollars/month)

0

t

0

t

d(stock)stock(t)= (inflow-outflow)dt+stock(t ) or inflow-outflow

dt

StockInflow Outflow

Hedge Funds – An Overview

• What are hedge funds?– Unregulated investment partnerships available

to wealthy individuals and institutions (“sophisticated accredited investors”)

– Seek above-average returns using aggressive, high-risk strategies unavailable to mutual funds and other traditional money managers

More on Hedge Funds

• Investing strategies include, but are not limited, to:– Short selling

– Leverage

– Arbitrage

– Derivatives

• Compensation structure is as follows:– Percentage of assets under management (usually 1%)

– Percentage of profits (usually 20%)

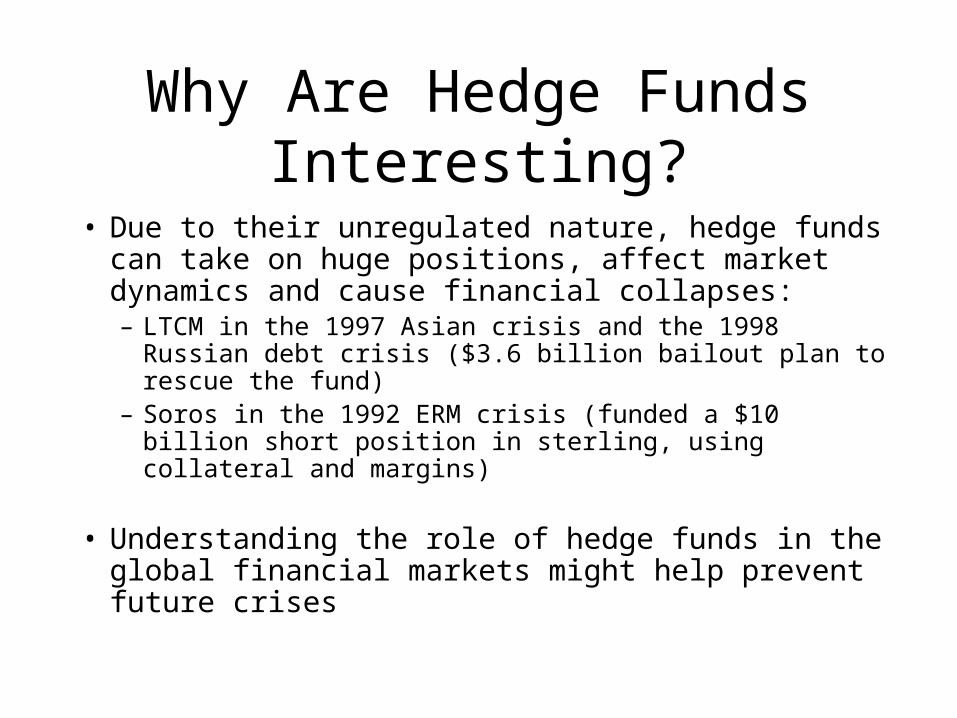

Why Are Hedge Funds Interesting?

• Due to their unregulated nature, hedge funds can take on huge positions, affect market dynamics and cause financial collapses:– LTCM in the 1997 Asian crisis and the 1998 Russian

debt crisis ($3.6 billion bailout plan to rescue the fund)– Soros in the 1992 ERM crisis (funded a $10 billion short

position in sterling, using collateral and margins)

• Understanding the role of hedge funds in the global financial markets might help prevent future crises

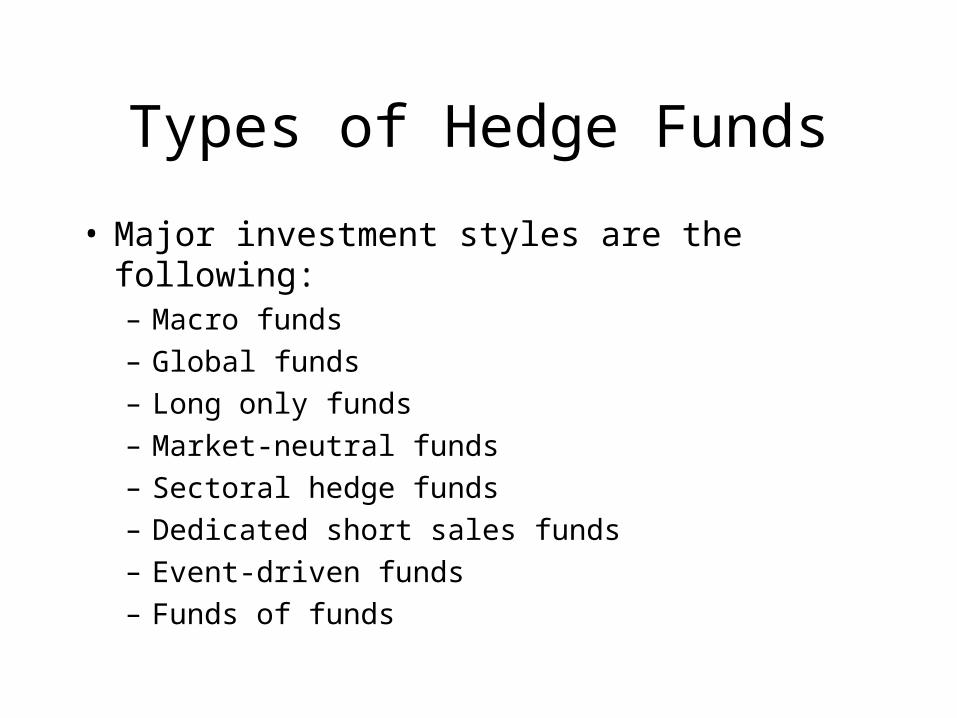

Types of Hedge Funds

• Major investment styles are the following:– Macro funds

– Global funds

– Long only funds

– Market-neutral funds

– Sectoral hedge funds

– Dedicated short sales funds

– Event-driven funds

– Funds of funds

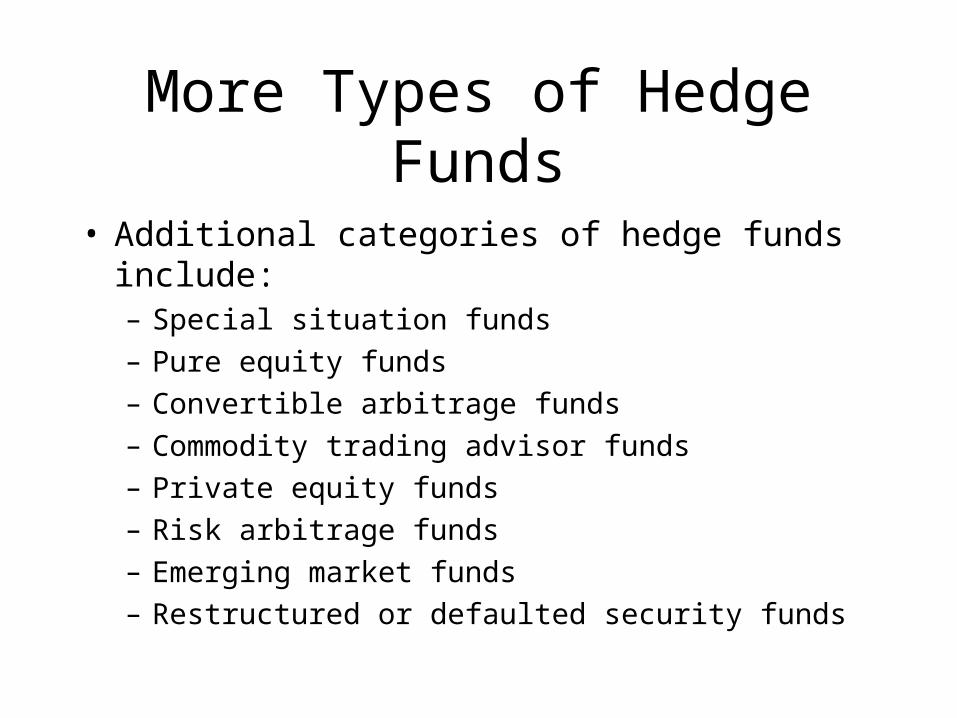

More Types of Hedge Funds

• Additional categories of hedge funds include:– Special situation funds

– Pure equity funds

– Convertible arbitrage funds

– Commodity trading advisor funds

– Private equity funds

– Risk arbitrage funds

– Emerging market funds

– Restructured or defaulted security funds

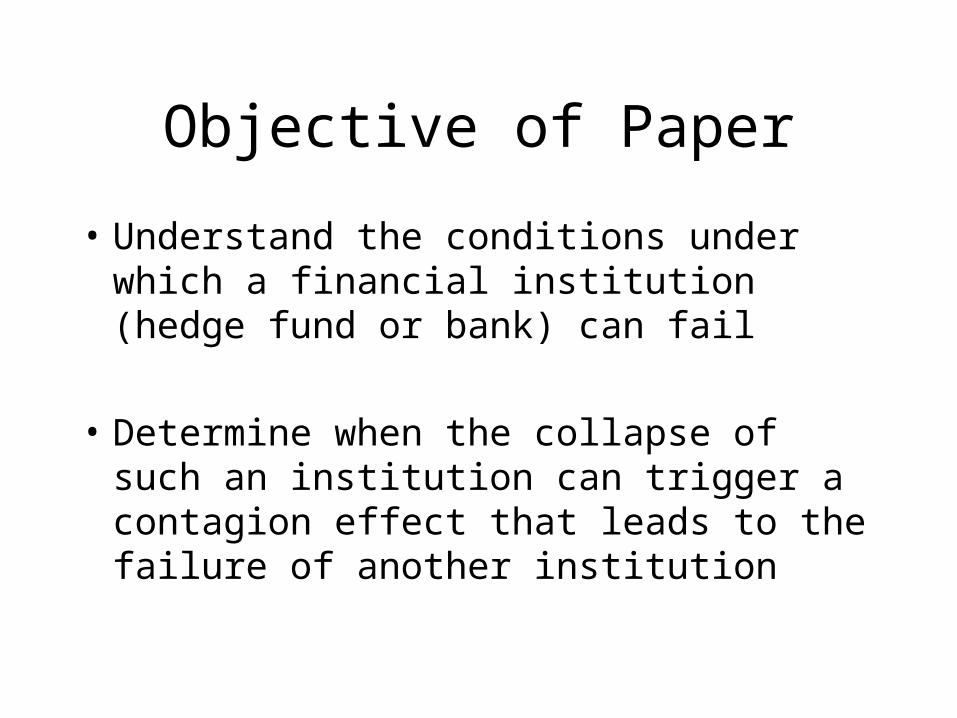

Objective of Paper

• Understand the conditions under which a financial institution (hedge fund or bank) can fail

• Determine when the collapse of such an institution can trigger a contagion effect that leads to the failure of another institution

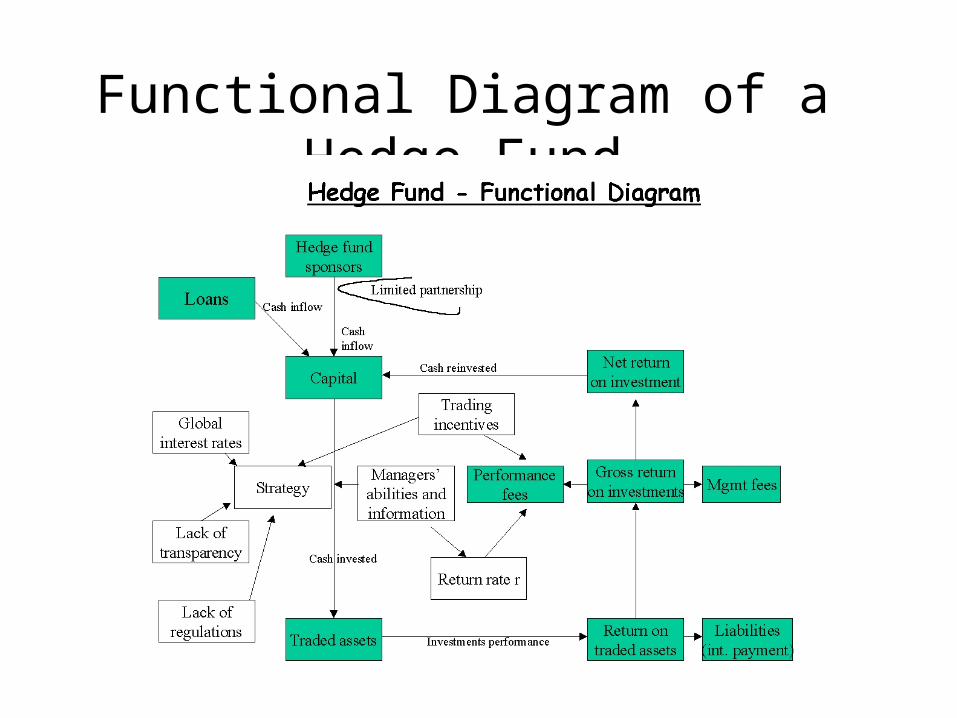

Functional Diagram of a Hedge Fund

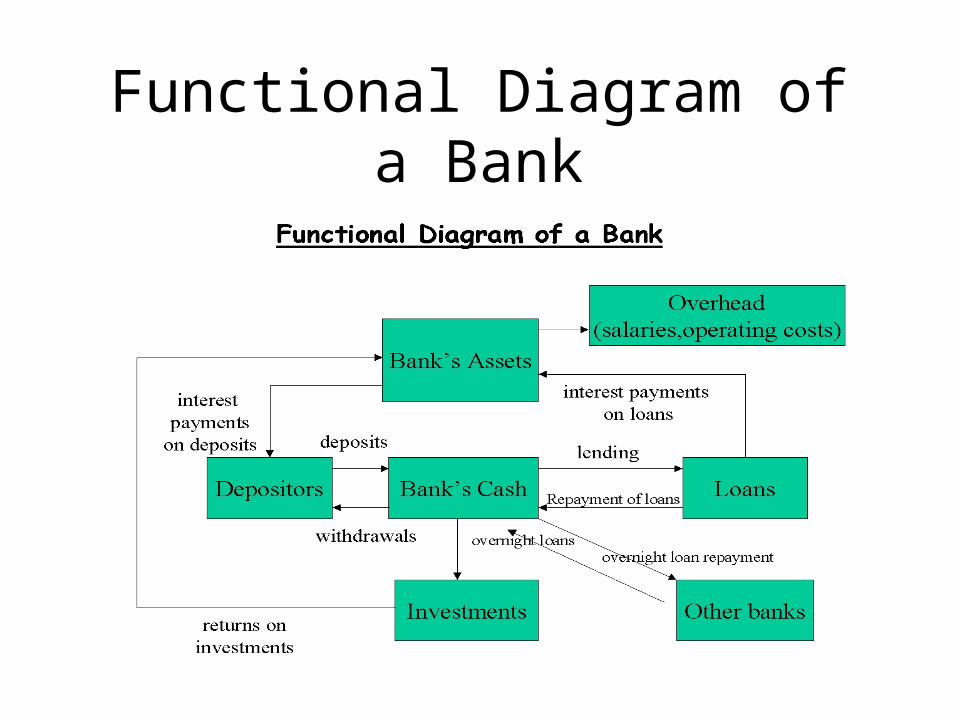

Functional Diagram of a Bank

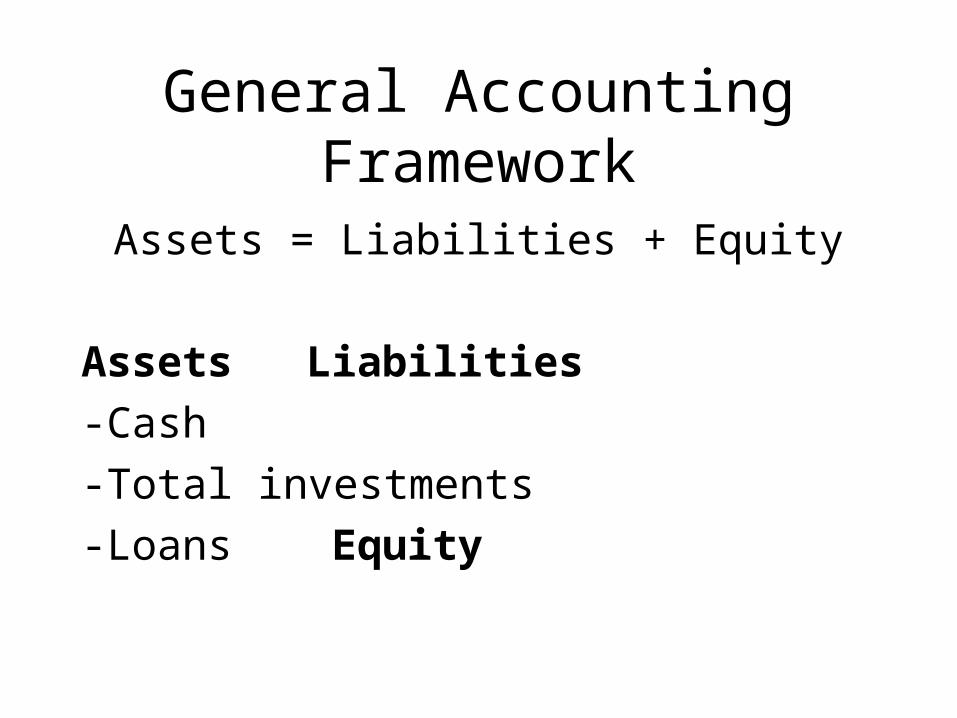

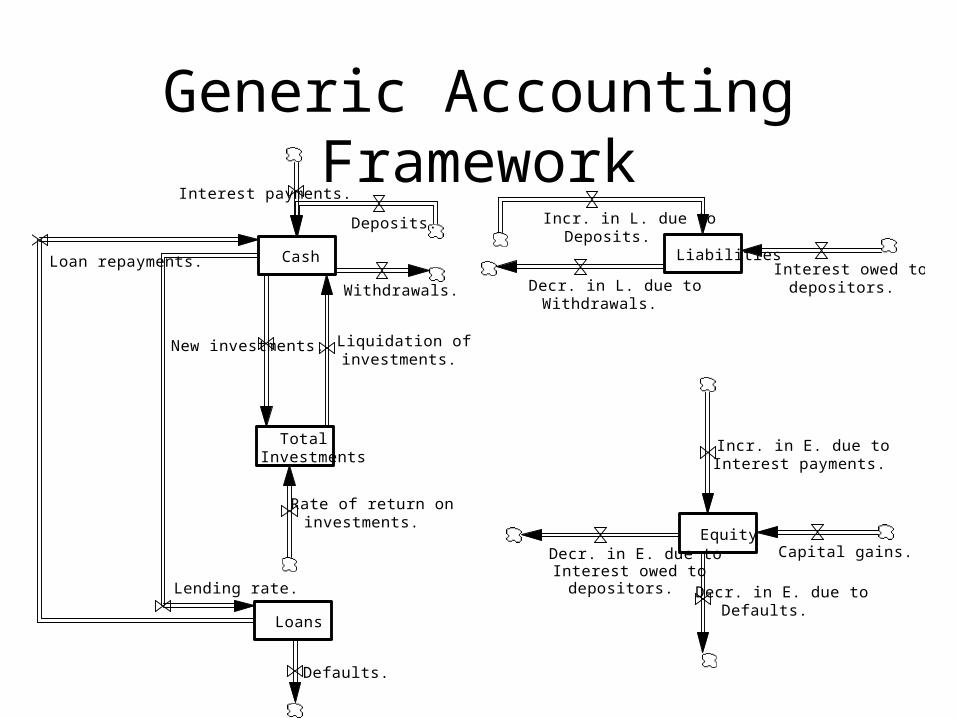

General Accounting Framework

Assets = Liabilities + Equity

Assets Liabilities

-Cash

-Total investments

-Loans Equity

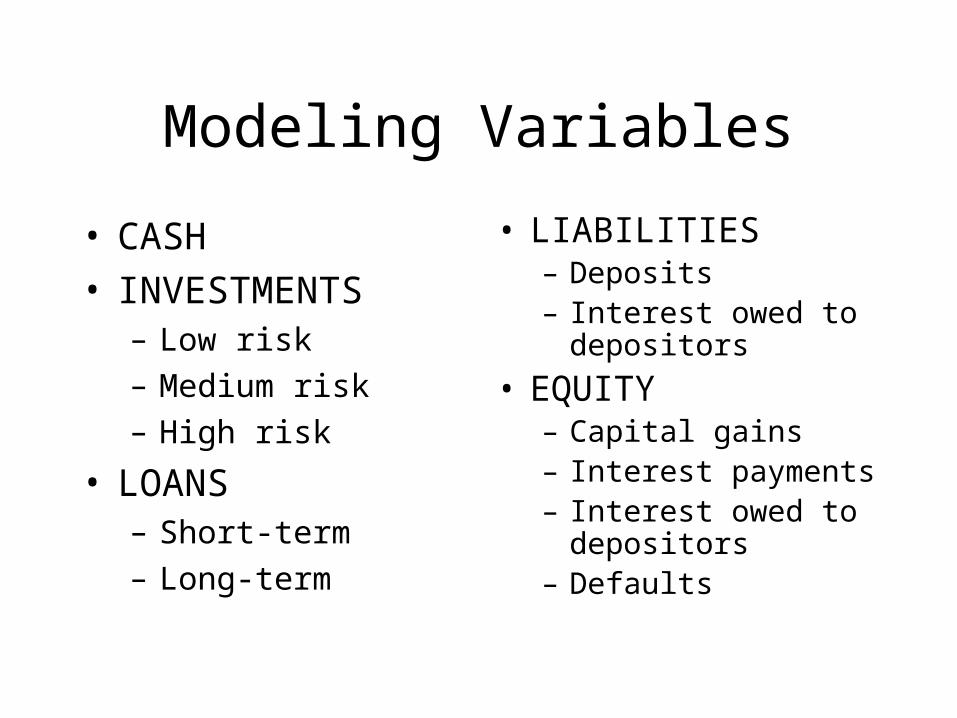

Modeling Variables

• CASH• INVESTMENTS

– Low risk

– Medium risk

– High risk

• LOANS– Short-term

– Long-term

• LIABILITIES– Deposits– Interest owed to

depositors

• EQUITY– Capital gains– Interest payments– Interest owed to

depositors– Defaults

Generic Accounting Framework

Cash

TotalInvestments

Loans

Liabilities

Equity

Lending rate.

Loan repayments.

Liquidation ofinvestments.

New investments.

Interest payments.

Rate of return oninvestments.

Defaults.

Decr. in E. due toDefaults.

Capital gains.

Interest owed todepositors.

Incr. in E. due toInterest payments.

Withdrawals.

Incr. in L. due toDeposits.

Decr. in L. due toWithdrawals.

Deposits.

Decr. in E. due toInterest owed to

depositors.

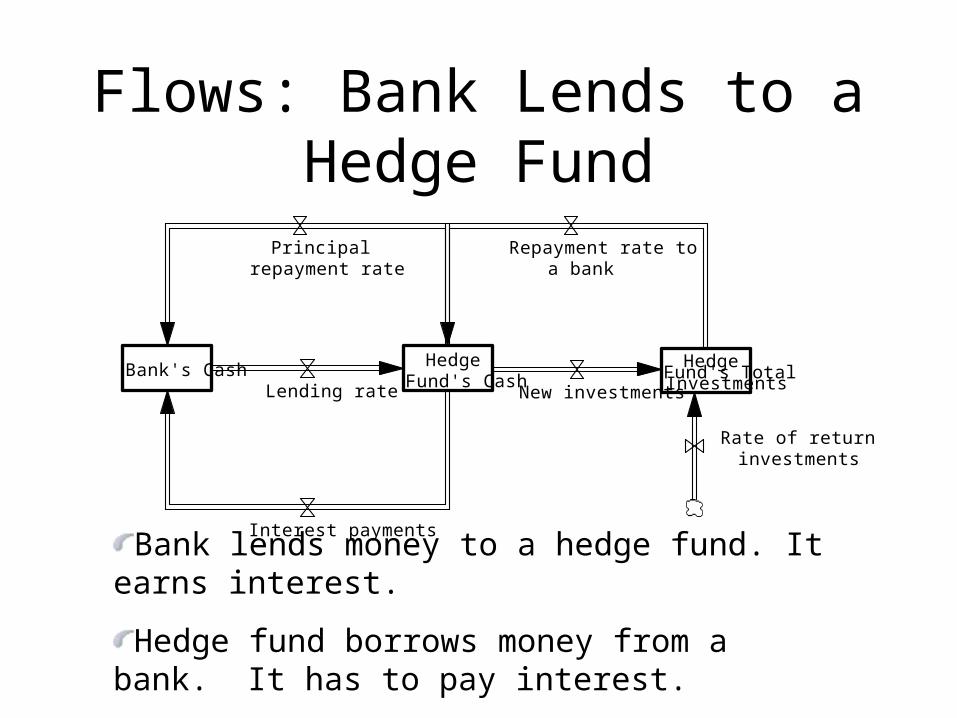

Flows: Bank Lends to a Hedge Fund

Bank's CashHedge

Fund's CashHedge

Fund's TotalInvestmentsNew investmentsLending rate

Interest payments

Principalrepayment rate

Repayment rate toa bank

Rate of return oninvestments

Bank lends money to a hedge fund. It earns interest.

Hedge fund borrows money from a bank. It has to pay interest.

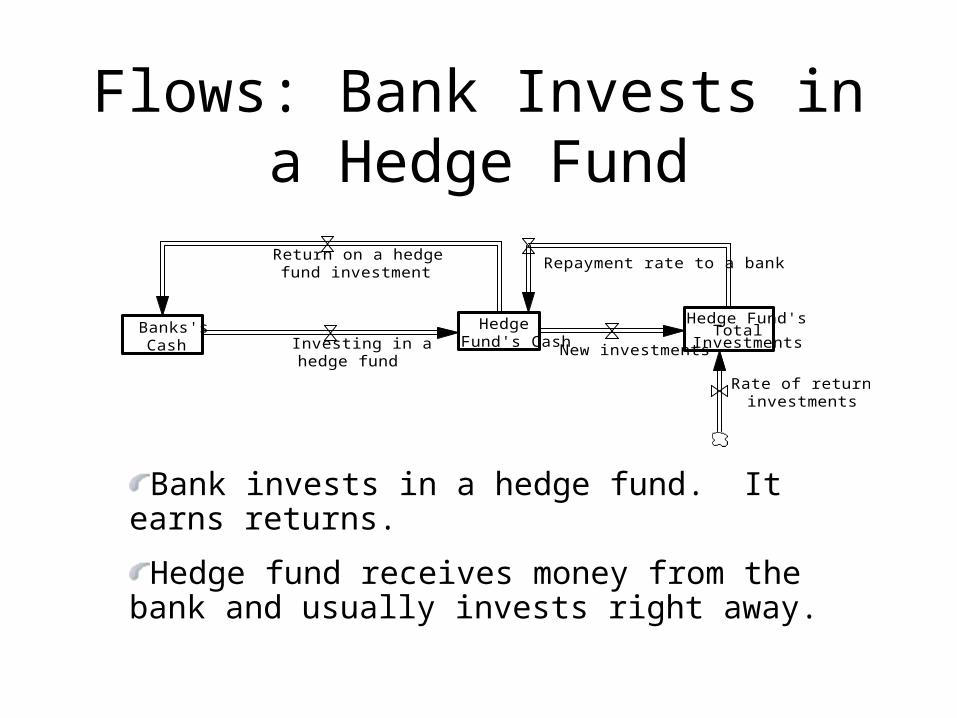

Flows: Bank Invests in a Hedge Fund

Banks'sCash

HedgeFund's Cash

Return on a hedgefund investment

Investing in ahedge fund

Hedge Fund'sTotal

InvestmentsNew investments

Rate of return oninvestments

Repayment rate to a bank

Bank invests in a hedge fund. It earns returns.

Hedge fund receives money from the bank and usually invests right away.

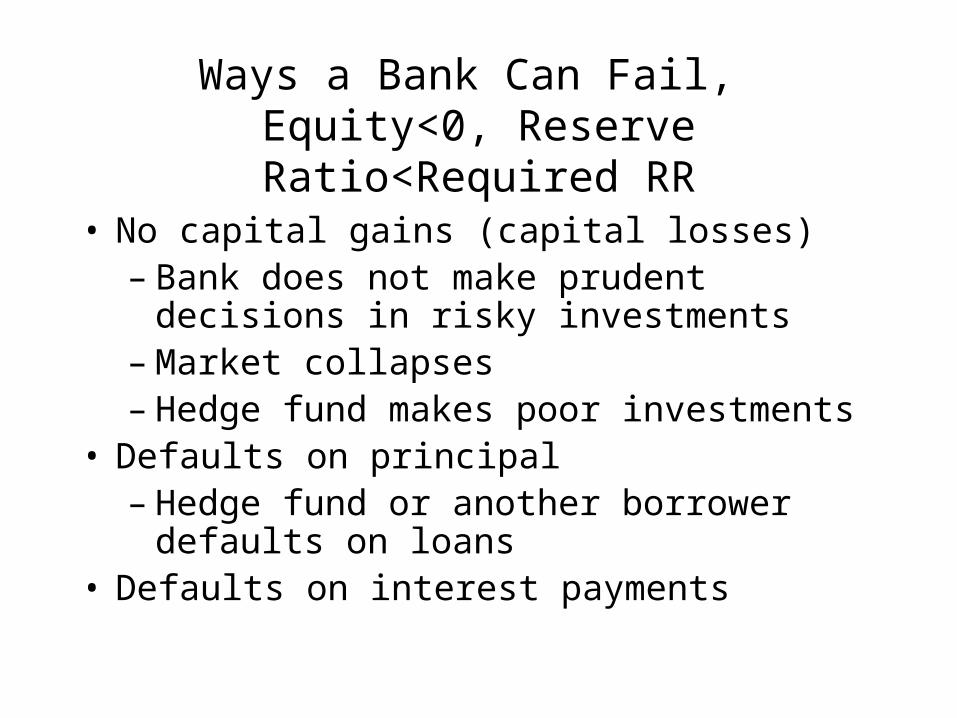

Ways a Bank Can Fail, Equity<0, Reserve Ratio<Required RR

• No capital gains (capital losses)– Bank does not make prudent decisions in risky

investments– Market collapses– Hedge fund makes poor investments

• Defaults on principal– Hedge fund or another borrower defaults on

loans• Defaults on interest payments

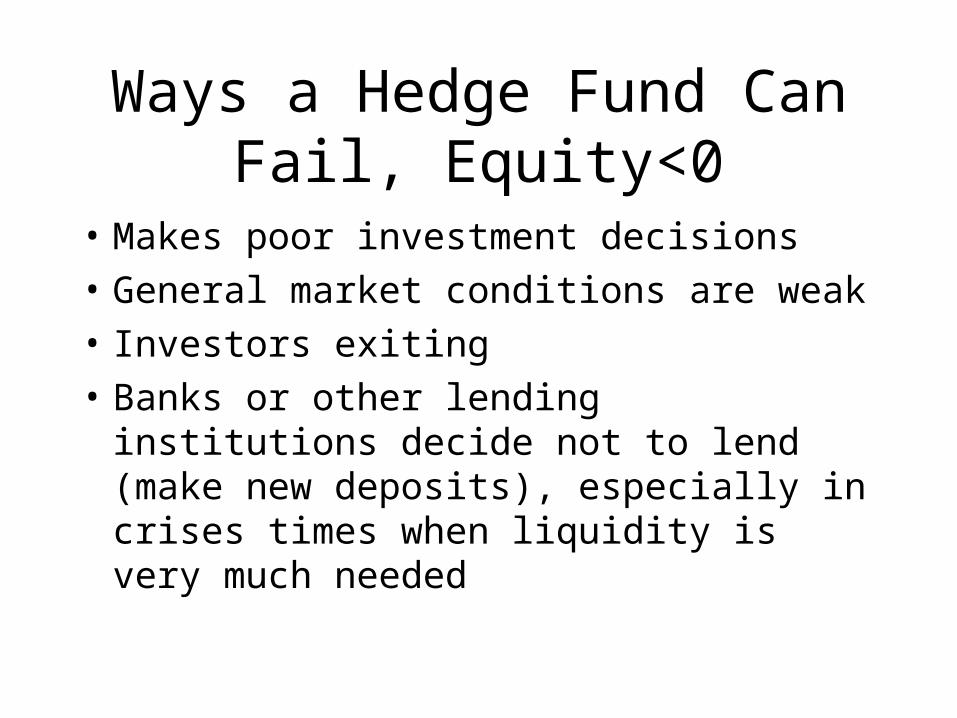

Ways a Hedge Fund Can Fail, Equity<0

• Makes poor investment decisions

• General market conditions are weak

• Investors exiting

• Banks or other lending institutions decide not to lend (make new deposits), especially in crises times when liquidity is very much needed

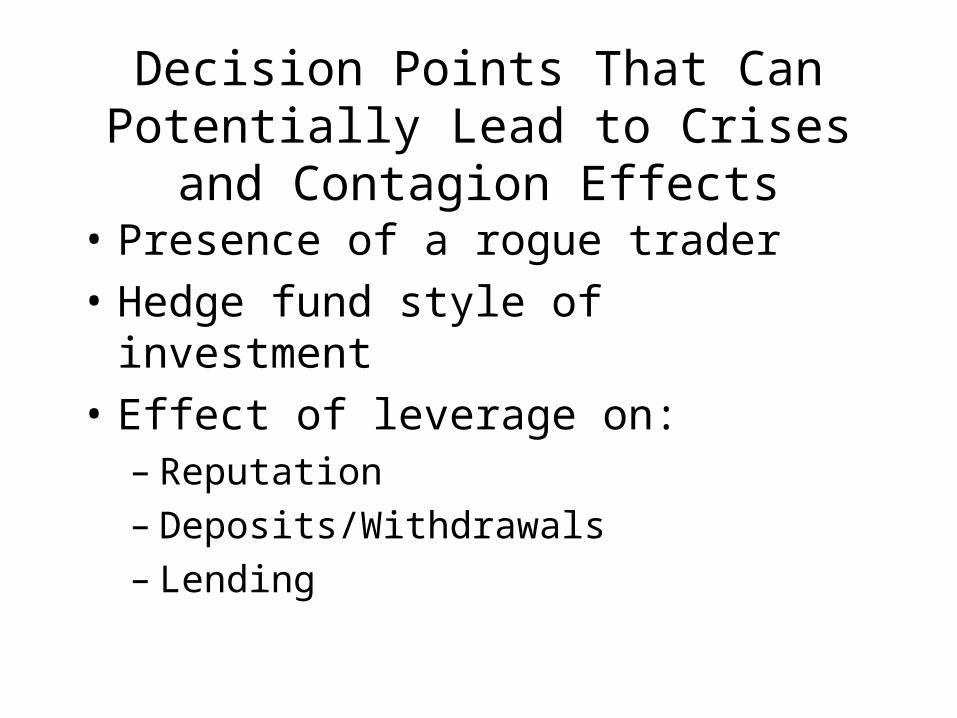

Decision Points That Can Potentially Lead to Crises and Contagion Effects

• Presence of a rogue trader

• Hedge fund style of investment

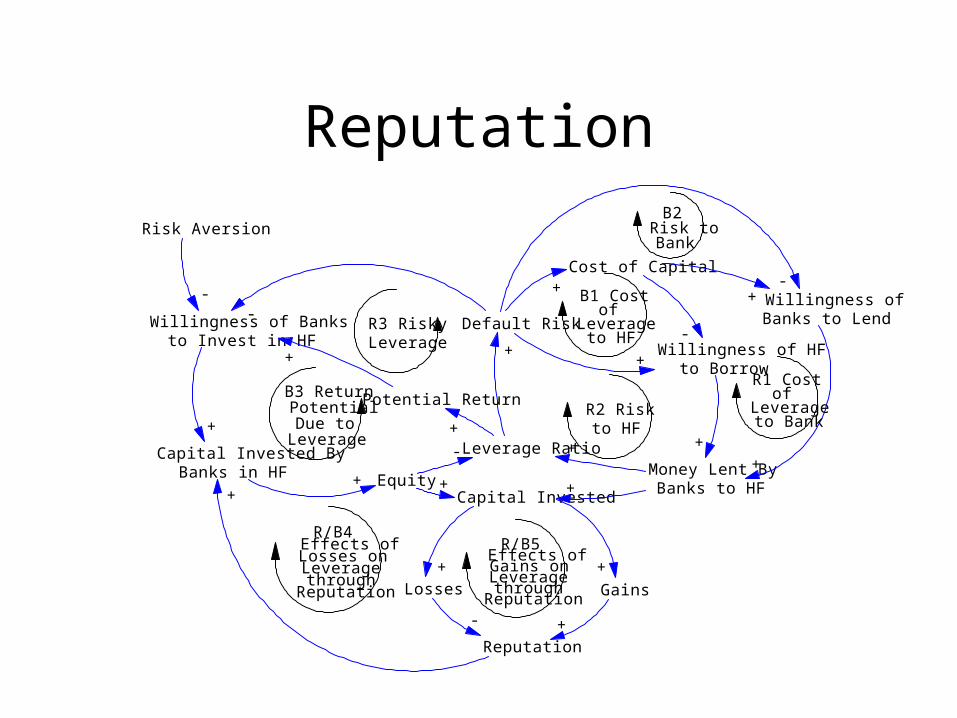

• Effect of leverage on: – Reputation– Deposits/Withdrawals– Lending

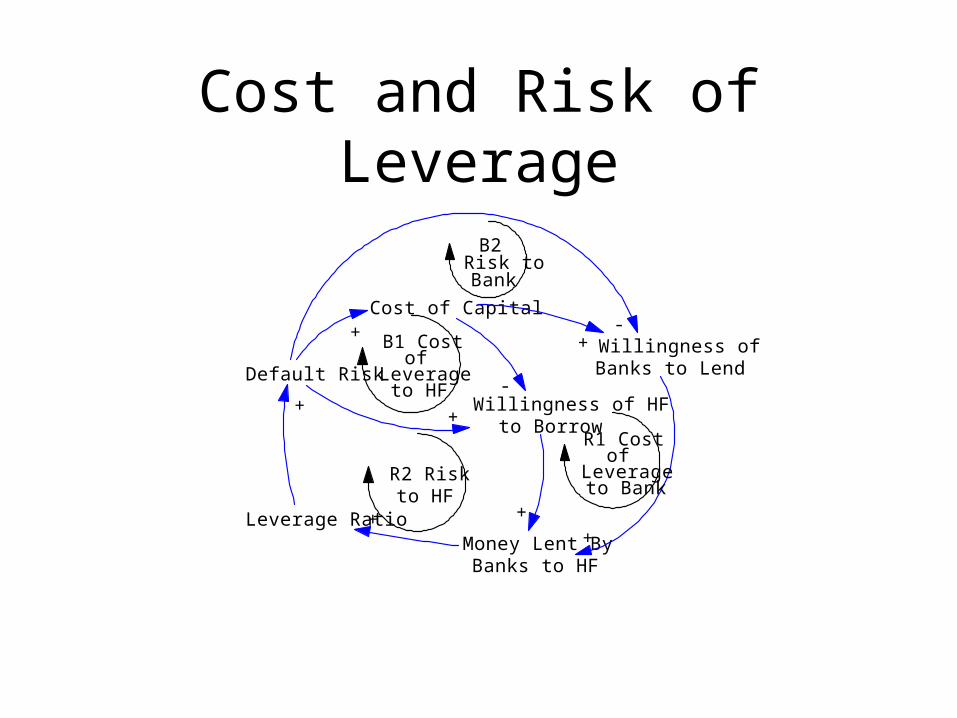

Cost and Risk of Leverage

Leverage Ratio

Default Risk

Cost of Capital+

Money Lent ByBanks to HF

Willingness of HFto Borrow

-

++

B1 Costof

Leverageto HF

+

Willingness ofBanks to Lend

+

+

R1 Costof

Leverageto Bank

+

-

R2 Riskto HF

B2Risk toBank

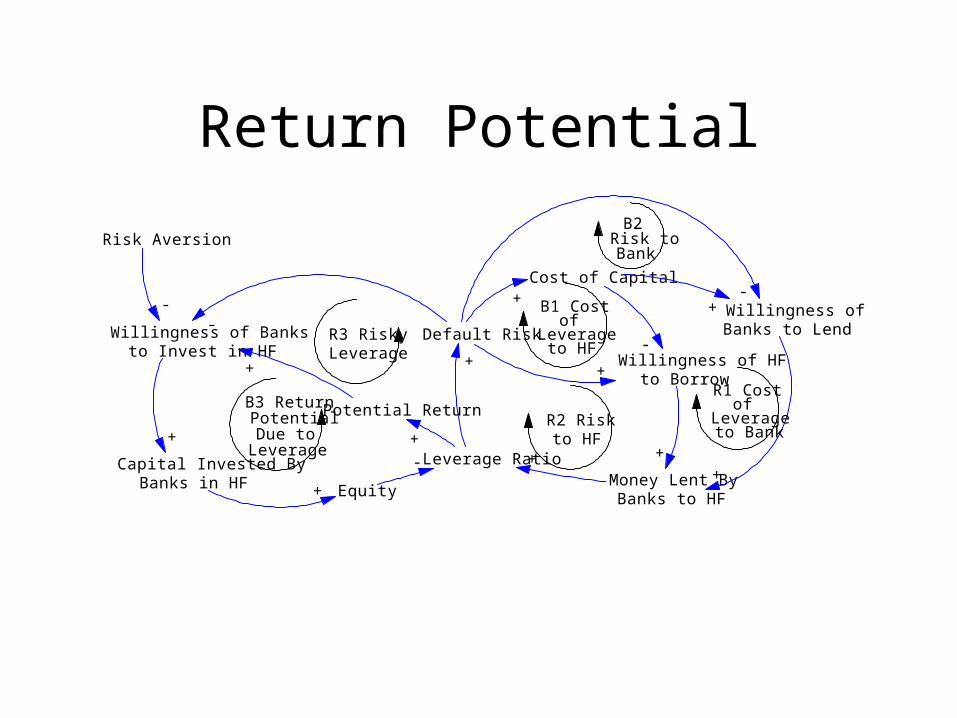

Return Potential

Capital Invested ByBanks in HF

Leverage Ratio

Default Risk

Cost of Capital+

Money Lent ByBanks to HF

Willingness of HFto Borrow

-

++

B1 Costof

Leverageto HF

Willingness of Banksto Invest in HF

-

+

Equity+

-

R3 RiskyLeverage +

Potential Return

+

+

B3 ReturnPotentialDue to

Leverage

Risk Aversion

- Willingness ofBanks to Lend

+

+

R1 Costof

Leverageto Bank

+

-

R2 Riskto HF

B2Risk toBank

Reputation

Capital Invested ByBanks in HF

Leverage Ratio

Default Risk

Cost of Capital+

Money Lent ByBanks to HF

Willingness of HFto Borrow

-

++

B1 Costof

Leverageto HF

Willingness of Banksto Invest in HF

-

+

Equity+

-

R3 RiskyLeverage +

Losses Gains

Reputation

- +

+

R/B5Effects ofGains onLeveragethrough

Reputation

R/B4Effects ofLosses onLeveragethrough

Reputation

Potential Return

+

+

B3 ReturnPotentialDue to

Leverage

Risk Aversion

- Willingness ofBanks to Lend

+

+

R1 Costof

Leverageto Bank

Capital Invested+ +

++

+

-

R2 Riskto HF

B2Risk toBank

Rogue Trader

• Losses

• Bets

• Probability of a rogue trader

• Skill

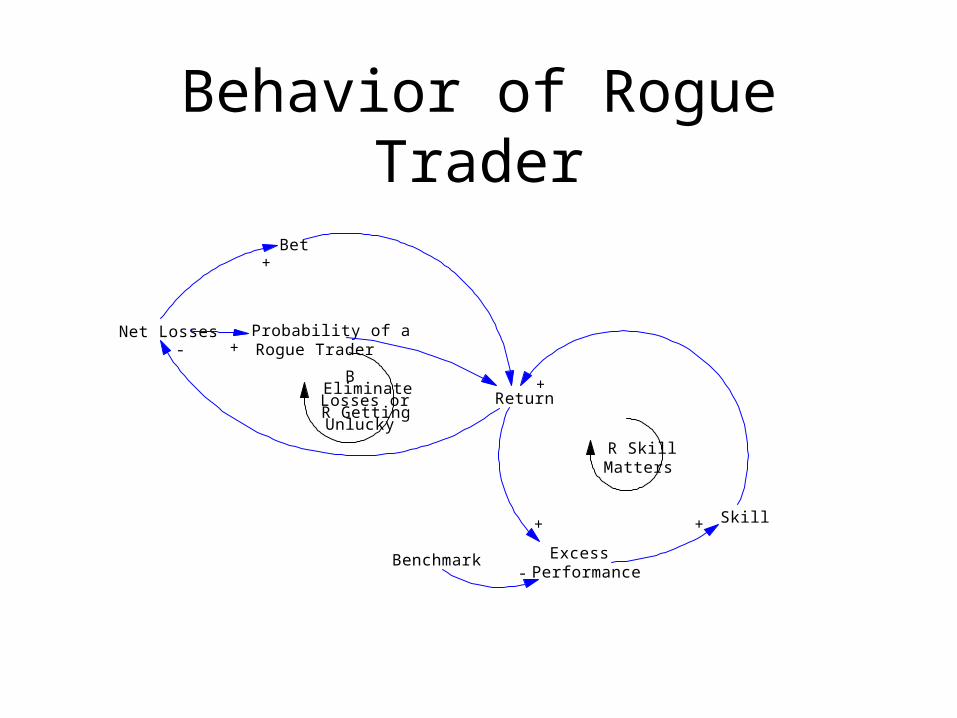

Behavior of Rogue Trader

Net Losses

Bet

Return

Skill

ExcessPerformance

Benchmark

+

+

+

-

Probability of aRogue Trader

+

+-

R SkillMatters

BEliminateLosses orR GettingUnlucky

Summary and Conclusions

• Dynamics Are Critical

• Effects Are Highly Nonlinear

• Implications for:– Credit– Liquidity– Volatility– Regulatory Environment