Embed Size (px)

Citation preview

7/29/2019 Fruits of Our Labour

http://slidepdf.com/reader/full/fruits-of-our-labour 1/11

1

Fruits of our Labour:Why the Philippines Needs a Sovereign Wealth Fund and How to Go About

Establishing OneJanuary 2013

Emmanuel C. S. Santos1

Introduction

The Philippines is suffering from a rare form of “Dutch disease”, the negative consequences

of a rapid rise in income normally associated with the export of natural resources. In our

case, the income comes from our export of labour. Remittances from overseas Filipinos

keep rising every year swelling our foreign currency reserves. The peso appreciates as a

result. This diminishes the global competitiveness of our manufacturing and services sectors

with adverse implications for domestic employment.

Meanwhile government keeps borrowing from international markets to finance its chronic

budget deficits. This contributes to the upward pressure on the domestic currency as more

dollars flow in to purchase government securities. To keep its borrowing down and make

credit rating agencies happy, government constrains its spending. It wants to rely on public-

private partnerships (PPP) to provide infrastructure which are both time-consuming to

arrange and limited in scope.

As it postpones development spending credit rating upgrades keep coming. Each time this

happens, fund managers around the world increase the flow of “hot money” into the stock

market, thus contributing to more upward pressure on the peso. Property developers also

cash in as the value of residential and commercial assets appreciates with the rising peso,

which creates even more demand for new development.

The families that receive remittances on the other hand suffer as the purchasing power of

the dollar declines. And due to their dependence on these transfers, the income that families

receive goes mostly to household expenditures. Very little is invested in productive activity;

and when it is, the investment normally goes into retail or transport enterprises, which earn

very marginal returns.

For the rest of the population, finding a job is a struggle. Life is hard as there are not enough

opportunities that come by due to a dearth of fixed private capital expenditures on plant and

equipment let alone research and development. Most of the inflows go to short-term

investments, i.e. the stock market, or to fund property purchases, which results in very little job generation outside the construction industry which demands casual employment due to

the seasonality of its activity.

This in a nutshell is the problem that confounds the Philippines.

1The author is a principal policy officer working in the economic unit of the Department of Premier and

Cabinet, Government of South Australia. This paper first appeared as a series of posts on the ProPinoy blogsite.The views expressed in this paper are his own and do not reflect that of his employer. He can be contacted at

7/29/2019 Fruits of Our Labour

http://slidepdf.com/reader/full/fruits-of-our-labour 2/11

2

Analysis

In 2012, the World Bank projects official remittances to the Philippines to reach just over $24

billion2 (with the Asian Bankers Association estimating an amount of $27 billion as of the end

of October3). This would be just over the Bureau of Internal Revenue’s total tax collections

for 2011 and would have been enough to finance that year’s budget deficit close to five timesover4. This places the Philippines third, just after China and India (each projected to receive

about $65 billion each) and ahead of Mexico (just under $24 billion) in the league table of

remittance-driven economies (see Figure 1).

Figure 1: Monthly remittances inflows (US$ millions)

Source: World Bank

On a monthly basis, the country’s foreign remittance inf lows went from about $600 million in

early 2003 to about $1.5 billion in early 2012. The latter is equal to the annual inflow of

foreign direct investments for 2012. In an economy of roughly PhP10 trillion, remittances

2Bellman, E. 22 November 2012. Wall Street Journal.19 January 2013

http://blogs.wsj.com/searealtime/2012/11/22/philippines-set-to-edge-mexico-for-remittance-olympics-

bronze/. 3Vallecera, Jun. 17 December 2012 “Remittances jump 8.2% to $27.24B.” Business Mirror.19 January 2013

http://businessmirror.com.ph/index.php/news/top-news/5713-remittances-jump-8-2-to-27-24b/. 4“National government full year 2011 fiscal deficit at 2% of GDP.”Bureau of the Treasury 19 January 2013.

http://www.treasury.gov.ph/news/news/Fiscal%20Report-1211.pdf/.

7/29/2019 Fruits of Our Labour

http://slidepdf.com/reader/full/fruits-of-our-labour 3/11

3

contribute about 10% of GDP. Given the multiplier effect that this income creates, it would be

fair to say that remittances contribute about a fifth of the economy.

Unlike Mexico, which is dependent on its northern neighbour the United States for providing

a market for its labour, the Philippine work force has its eggs in many baskets, not only in

different countries, but many occupations, both high- and low-skilled. This made it moreresilient to harsh economic conditions demonstrated by the fact that as the Great Recession

unfolded in the US from September 2008, the growth in remittances to Mexico hit a ceiling,

while that of the Philippines maintained its upward trajectory catching up with its North

American counterpart towards the end of 2011.

As of December 2012, the country’s gross inter national reserves (GIR) stood at $84 billion

exceeding the full year estimate of the BangkoSentral (BSP) of $78 billion5.This was enough

to cover our imports for a full year or to settle all short-term debt obligations 12 times based

on original maturity and 5.7 times based on residual maturity (that is short-term loans based

on original maturity plus principal payments on medium- and long-term loans of both private

and public sectors falling due in the next 12 months).

The GIR of the Philippines is also about 72 per cent larger than the total official reserve

assets of the Reserve Bank of Australia, which was at US$49 billion at the end of December

20126. It is worth asking, what is an economy the size of the Philippines which produces

about $250 billion a year doing with reserves of that amount compared to the resource

exporting Australian economy which is about $ 1 trillion a year ? Do we need to maintain

such a high level of reserves relative to our economy ?

Back in September 2012 when the GIR stood at $82 billion, the country’s external debts

belonging to both the public and private sectors stood at $61.7 billion. That means the BSP

had enough to settle all external obligations and still have roughly $20 billion left over.

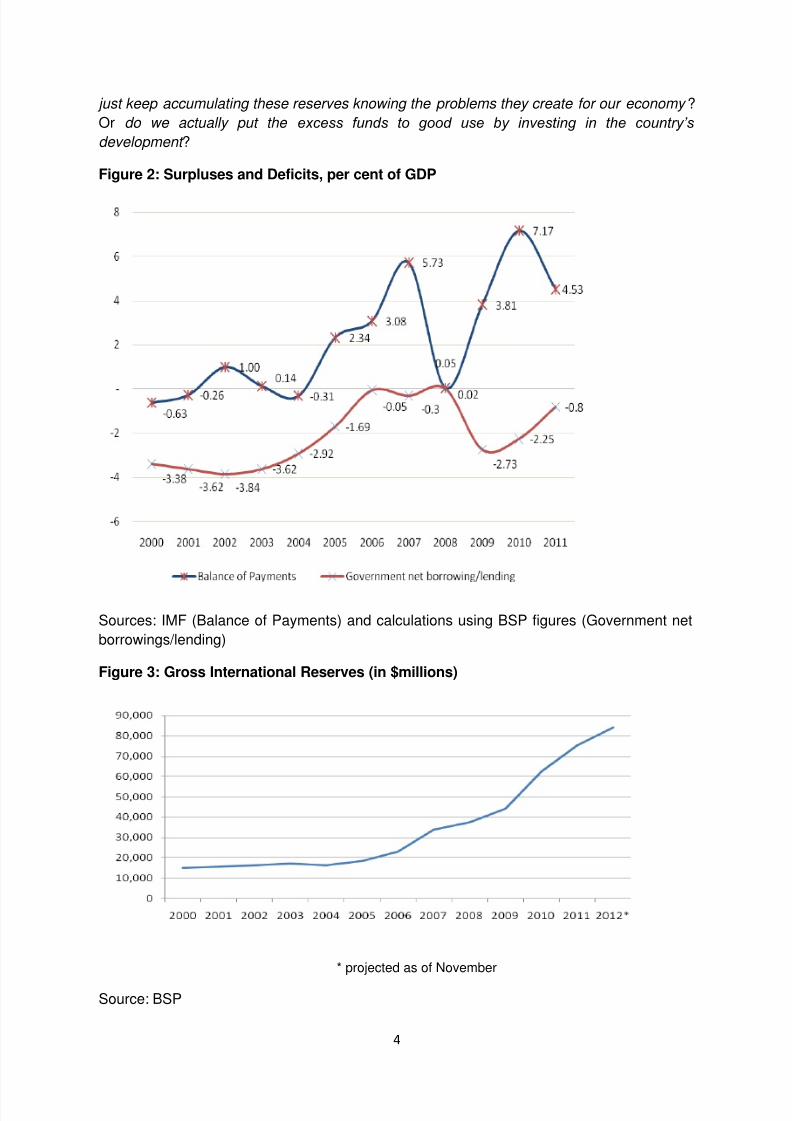

The next two charts show what has happened over the past decade to the finances of the

nation. Figure 2 shows that after a rocky start when the balance of payments (BoP)

fluctuated between surplus and deficit territory from 2000-05, the country has been

producing consistent BoP surpluses averaging about 3.8 per cent of GDP from 2005-11.

A quick rule of thumb is that 1 per cent of GDP is roughly Php100 billion. So on average, the

annual BoP surplus has been about Php380 billion during the past six years. The average

BoP surplus is therefore more than enough to accommodate government’s annual revenue

shortfall which has averaged 2 per cent of GDP per year.

Figure 3 shows the effect these surpluses have had on our GIR. From 2001 to 2011, GIR

have grown on average by 16.7 per cent per annum. Up until 2005, the levels were pretty

flat. Afterwards they rise steeply. This means that a tipping point in the structure of payments

has been reached which has placed our BoP structurally in surplus territory.

No wonder bond markets have had such confidence in the Philippines. As the saying in

business goes, banks will only offer you credit when you don’t need it. The question is do we

5“Gross international reserves.”BangkoSentralngPilipinas. 19 January 2013.

http://www.bsp.gov.ph/statistics/sdds/table12.htm/. 6“Official reserve assets.”9 January 2013. Reserve Bank of Australia. 19 January 2013.

http://www.rba.gov.au/statistics/frequency/reserve-assets.html/.

7/29/2019 Fruits of Our Labour

http://slidepdf.com/reader/full/fruits-of-our-labour 4/11

4

just keep accumulating these reserves knowing the problems they create for our economy ?

Or do we actually put the excess funds to good use by investing in the country’s

development ?

Figure 2: Surpluses and Deficits, per cent of GDP

Sources: IMF (Balance of Payments) and calculations using BSP figures (Government net

borrowings/lending)

Figure 3: Gross International Reserves (in $millions)

* projected as of November

Source: BSP

7/29/2019 Fruits of Our Labour

http://slidepdf.com/reader/full/fruits-of-our-labour 5/11

5

Finally, Figure 4 shows what has happened to the net savings of the Philippines over the

past two decades. From 1989 to 1998, the annual investment rate averaged about 25 per

cent of GDP, while the annual saving rate averaged about 18 per cent, resulting in an annual

net savings of about -7.2 per cent. From 1998 to 2003, the country went through a number of

crises including the Asian flu and a series of uprisings. It came out of this period with the

relationship between investments and savings reversed. From 2003 onwards, the averageannual saving rate (23 per cent of GDP) exceeded the annual investment rate (19.9 per

cent) by about 3.2 per cent of GDP a year.

This is as much due to the drop in the investment rate, as much as it is a rise in savings.

Due to this structural change, the country has become a net saving country since 2003. The

country now suffers not from a lack of capital accumulation, but from a lack of investor

appetite. Despite efforts to raise the competitiveness of the country or to generate

investments through public-private partnerships, the investment rate remains stubbornly low.

We could characterise the country as being stuck in a developmental trap where the only

way to make it more competitive is to improve the productivity of its labour force. The

primary way to do that is through capital deepening. But without a sufficient level of capital

being invested, productivity declines relative to other countries where investments flow. The

nation’s inability to raise productivity deters future investors, and on it goes.

Something has to break the cycle, and this will not occur by simply relying on the “Invisible

Hand of the market”, as private players suffer from the free rider problem—waiting for the

first mover to take action before joining in. It will take some coordinated effort by

government; but given its chronic deficits, it needs to find a new way to jump-start productive

investments.

Figure 4: Net Savings

Source: Asian Development Bank

7/29/2019 Fruits of Our Labour

http://slidepdf.com/reader/full/fruits-of-our-labour 6/11

6

Recommendation

As the title of the paper suggests, we should set up a sovereign wealth fund (SWF) with our

excess reserves. The $20 billion mentioned above could be the seed money. That is enough

to double our infrastructure spending which is currently at 1.5 per cent of GDP every year to

3 per cent, much closer to the recommended 5 per cent, over the next five years. With thatadded spending, the government could easily meet its aspirational stretch target of growing

the economy by 7-8 per cent a year.

Or alternatively, each year, depending on how well our BoP and GIR perform, the

government could just borrow from the BSP to fund its deficits and the SWF. Assuming that

the government’s new revenue measures and fiscal consolidation program reduce its annual

deficit to about 1 per cent of GDP, and that the annual BoP surplus remains at 3.8 per cent

of GDP, there would be enough to fund government’s deficit and set aside another 1 .5 per

cent for the SWF, with the remaining 1 per cent going to GIR.

What is a SWF ?

Let us first define what an SWF is. According to the Sovereign Wealth Fund Institute, it is

a state-owned investment fund or entity that is commonly established from

balance of payments surpluses, official foreign currency operations, the

proceeds of privatisations, governmental transfer payments, fiscal surpluses,

and/or receipts from resource exports 7.

The Institute cites some “interesting facts” about SWFs, namely that some of them “invest

indirectly in domestic industries” and that “they tend to prefer returns over liquidity, thus they

have a higher risk tolerance than traditional foreign exchange reserves. SWFs often receivetheir initial capital through “commodity exports, either taxed or owned by the government” or

through “transfers of assets from official foreign exchange reserves”.

There are about US$5.1 trillion invested in SWFs globally. About three of every five dollars

come from oil and gas exports, the remainder from other sources. The size of funds varies

from as little as US$300 million for Indonesia to as large as US$664 billion for Norway. Of

the 64 SWFs that currently exist, 39 were established since 20008.

How could a SWF be established?

Some have argued that the BSP is restricted by its charter, RA 7653, the Central Bank Act

9

,from investing in instruments other than triple-A rated bonds of foreign governments. At the

time this law was passed, the problem facing the country was chronic BoP deficits. More

transfers out rather than in were being made.

The BSP is tasked under the law with maintaining international monetary stability in the

country. Part of this according to Article II, Section 64 of the law is “to preserve the

7“What is a SWF?” SWF Institute. 19 January 2013 <http://www.swfinstitute.org/sovereign-wealth-fund/>.

8 “Sovereign wealth fund rankings.” SWF Institute. 19 January 2013 <http://www.swfinstitute.org/fund-

rankings/>.9“Republic Act No. 7653.”The LawPhil Project.19 January 2013

http://www.lawphil.net/statutes/repacts/ra1993/ra_7653_1993.html/ .

7/29/2019 Fruits of Our Labour

http://slidepdf.com/reader/full/fruits-of-our-labour 7/11

7

international value of the peso and to maintain its convertibility into other freely convertible

currencies”.

To maintain such stability, Section 65 says that “the Bangko Sentral shall maintain

international reserves adequate to meet any foreseeable net demands on the Bangko

Sentral for foreign currencies”. It would have to judge for itself the adequacy of thesereserves based on “prospective receipts and payments of foreign exchange by the

Philippines”.

Finally, Section 66 lays out the composition of such reserves which it says “may include but

shall not be limited to” gold and other assets that took the form of “documents and

instruments customarily employed for the international transfer of funds; demand and time

deposits in central banks, treasuries and commercial banks abroad; foreign government

securities; and foreign notes and coins”.

Back in September 2011, the central bank governor reportedly offered to purchase

Philippine treasury using its dollar reserves. Although these notes are not triple-A rated, hehad probably realised back then that the BSP already had an adequate supply of reserves to

meet international obligations.

Given that the law says nothing about what to do if the BSP were to have more than a

sufficient level of reserves we can say that the BSP is sailing in unchartered waters. If the

law does not specify what it should do in such a situation, then it should be left to the

discretion of its board to decide how best to deal with it.

To eliminate any doubt, however, and to lay the legal basis for a SWF, existing legislation

should be amended so that the BSP is allowed to transfer funds to the national government

via the purchase of government bonds, the proceeds of which would go to the nationaltreasury and then to the SWF. That should be the prescribed method for transferring funds.

Currently, the return on short-term US treasury notes is between 0 and 0.25 per cent,

negative in real terms, meaning that the BSP is paying the US government to borrow from its

reserves. And the US Federal Reserve has said that it plans to keep interest rates as low as

they are for the foreseeable future until the US unemployment rate goes under 6.5 per cent10

(it is currently at 7.8 per cent). If the BSP lent its excess reserves to the Philippine

government, it would gain a better return and preserve the value of its assets.

What would be the purpose of a Philippine SWF?

The nature and purpose of SWFs are varied, but in the Philippines it might be to do the

following (as adapted from the SWF Institute):

Protect and stabilise the budget and economy from excess volatility in

revenues/exports

Diversify our industry sector to make growth more inclusive and robust

Earn greater returns than on foreign exchange reserves

Assist monetary authorities dissipate unwanted liquidity

Increase savings for future generations

10 “The Fed’s big policy move: what it means.” 12 December 2012. CBS News. 19 January 2013

<http://www.cbsnews.com/8301-505123_162-57558793/the-feds-big-policy-move-what-it-means/ >.

7/29/2019 Fruits of Our Labour

http://slidepdf.com/reader/full/fruits-of-our-labour 8/11

8

Fund social and economic development.

Given the need to boost productivity and improve competitiveness, addressing the

infrastructure backlog would be the most obvious place to start. The PPP projects would be

a good initial source of demand for funding as these projects are designed to earn a market

rate of return for the investor. Another possibility would be for the SWF to enter into joint-ventures with mining firms for the exploration and production of oil and other commodities.

This would ensure that we received a larger share of the benefits from such operations.

A third possibility would be to fund innovation through government procurement, business

incubators, industry clusters, and competitions aimed at the commercialisation of ideas.

Government could serve as a catalyst in the germination of new activity around key areas of

specialisation that the country has already exhibited proficiencies in. The expansion of our

semiconductor and electronics industry into higher value adding activities could be one

priority. The growth of agribusinesses into higher yield crops and value-adding processes

could be another. A fourth priority could be the generation of clean technology and

renewable energy.

How could a SWF be governed and managed?

The Santiago Principles established by 26 countries with SWFs known as the International

Working Group or IWG in 2008 lays out a number of generally accepted principles and

practices or GAPP to ensure that “the SWF arrangements are properly set up and

investments are made on an economic and financial basis”11. One of the main reasons for

this is that as government-owned entities, as SWFs continue to grow in importance to global

capital markets and perform a bigger role in corporate governance, they need to

demonstrate that their investment decisions are not politically motivated.

Traditionally, SWFs took the surplus foreign reserves accumulated within a resource

exporting nation and invested them in long-term projects overseas. This allowed recipient

countries that were often capital constrained and developing to benefit from such investment

flows. The size and relative lack of transparency of some SWFs however caused many

actors in the international community to cast a suspicious eye at these funds.

In the Philippine context, as discussed above, the SWF would be confined to funding

projects within the country given our chronic underinvestment in infrastructure and need to

resuscitate our industrial sector. Given however our historically poor track record at ensuring

that government owned and controlled companies manage their assets in a prudent manner,the main concern in establishing a SWF would be to ring-fence it from the arbitrary and

extractive influence of politics.

The Santiago Principles help to define a set of best practices for us in establishing our own

SWF in the Philippines. The Carnegie Endowment for International Peace talked about what

the effect of signing up to these principles is by saying that

(b)y voluntarily submitting to the Santiago Principles, IWG members ceded

their autonomy to establish governance arrangements in line with their

11“Generally accepted principles and practices – The Santiago Principles.”International Working Group of

Sovereign Wealth Funds. 19 January 2013 <http://www.iwg-swf.org/pubs/gapplist.htm/>.

7/29/2019 Fruits of Our Labour

http://slidepdf.com/reader/full/fruits-of-our-labour 9/11

9

individual needs and preferences. In a way, they made a conscious decision to

limit the reach of their “sovereignty” 12.

One might be tempted after reading that to draw an analogy between the IWG to the World

Trading Organisation or WTO which implements the General Agreement on Trade and

Tariffs or GATT. Unlike that body, the IWG and its successor the International Forum ofSovereign Wealth Funds or IFSWF is purely voluntary and has no powers to sanction its

members. The Carnegie Endowment does draw this distinction. What our Philippine

authorities should do in drawing up the framework for its SWF would be to hard code “the

Principles” into its charter.

As shown in the table below, the Principles may be divided into three distinct parts. These

cover the legal and macroeconomic policy framework of the fund, its institutional and

governance arrangements and structures, and finally its methods for managing investment

decisions and handling risk. I am adapting the Carnegie Endowment’s description of these

parts here.

The policy aims of setting a SWF in the Philippines are clear: to channel excess foreign

reserves in a productive way and to cope with the developmental needs of the country. The

GIR should only be allowed to rise in proportion to external commitments. As the economy

becomes less dependent on foreign borrowing, these external debts will not rise as rapidly

as they have in the past.

Once targeted levels of GIR have been reached, the BSP should be authorised to declare

any additional funds in excess of its requirements. The existing Central Bank Act should be

amended to explicitly state this. The monetary board should be given the task of setting the

appropriate benchmarks for making such declarations and for transferring excess funds to

the SWF via the national bureau of treasury.

The nature of such a transfer, as suggested, should be in the form of a sovereign loan

issued to the national government, which will own the SWF. The SWF must in turn invest in

projects that will have a sufficient return to cover its borrowing and operating costs. This

arrangement would ensure that the value of the BSP ’s assets is preserved.

As to the appointment of its board and officers, the SWF would be subject to the same rules

covering government owned and controlled corporations or GOCCs. The reforms carried out

under the new GOCC law which created a commission to regulate the appointments,

compensation and accountabilities of such officers would apply as well. This would includethe need to provide audited financial statements and management reports and submit to

congressional oversight13.

In terms of the type of projects it would fund, I have suggested four potential areas or

themes. This includes public infrastructure (such as the ones eyed for PPP) aimed at both

social and economic development, joint minerals exploration in partnership or consortium

12Behrendt, S. “Sovereign wealth funds and the Santiago Principles – Where do they stand?” Carnegie Papers

No. 22, May 2010. Carnegie Endowment for International Piece. 19 January 2013

<http://carnegieendowment.org/files/santiago_principles.pdf/>.13 “Republic Act No. 10149.” Official Gazette, Office of the President. 19 January 2013

<http://www.gov.ph/2011/06/06/republic-act-no-10149/ >.

7/29/2019 Fruits of Our Labour

http://slidepdf.com/reader/full/fruits-of-our-labour 10/11

10

with private mining firms, innovation and industry cluster development projects, and clean,

renewable energy projects.

Table 1: Santiago Principles

Section What “the Principles” state there should be GAPP #

Legalframework,objectives, andcoordination withmacroeconomicpolicies

disclosure of legal framework definition and disclosure of policy purpose public disclosure of funding and withdrawal

arrangements

GAPP 1GAPP 2

GAPP 4

Institutionalframework andgovernancestructures

clearly defined roles and responsibilities of theprincipal/owner (the government) and the agent(SWF’s governing body, officers and executives)

a limited role for the principal which is to set the broadobjectives, appointment of governing body or board,

and oversight of operations a clear mandate to the fund’s governing body to set

strategy for achieving its objectives along with beingaccountable for its performance

delegated authority for independently implementingstrategies and handling operations for officers andexecutives under clearly defined roles andresponsibilities

GAPP 6

GAPP 7

GAPP 8

GAPP 9

Investment andriskmanagement

frameworks

disclosure of investment policies information about investment themes, investment

objectives and horizons, and strategic asset

allocation, including:o disclosure of investments that are subject to

non-economic and non-financialconsiderations

o whether they execute ownership rights toprotect the financial value of investments

a framework that identifies, assesses, and managesthe risks of its operations and measures to trackinvestment performance employing relative and/orabsolute benchmarks

GAPP 18

GAPP 19.1

GAPP 21

GAPP 22

*adapted from Behrendt, S. (May 2010). Sovereign Wealth Funds and Santiago Principles: Where do

they stand? Carnegie Papers No. 22, Carnegie Endowment for International Peace.

The allocation of resources across these themes could be based on national priorities. To be

clear, one of the main aims of this SWF would be to support the development priorities of the

nation, and that should be stated unapologetically. But for specific projects, a set of solid

business cases needs to be presented. When entering into joint ventures or consortia with

private players, the SWF should also be allowed to exercise ownership rights over the

project to protect its investments.

Just as with government financial institutions, the SWF should be guided by proper

prudential principles and practices that would manage its risk exposure; but unlike the

conservative treasury management practices of government banks and pension funds, therisk-return equation is different for an equity investor like the SWF. The risk tolerance would

7/29/2019 Fruits of Our Labour

http://slidepdf.com/reader/full/fruits-of-our-labour 11/11

11

be higher while its returns need not necessarily be as large given its lower cost of borrowing.

Its risk adjusted return on capital would thus be lower compared to commercial banks.

Some PPP bidders have expressed concern over political interference in the Philippines

affecting their ability to set rates for services independently of the government. This has

limited their appetite for managing and operating the utilities and transport oriented projectsunder PPP. They have therefore chosen to participate only in building the infrastructure.

Takashi Ishagami of Marubeni Corporation has been quoted as saying that “the Filipino PPP

is far away from our standard”14. It has partnered with a local firm to jointly bid for a $1 billion

railway project in which it would be merely supplying equipment.

If the SWF were to finance such projects with foreign partners, a portion of the excess

foreign reserves would leak out of the country (as intended) through the purchase of foreign

equipment. This will help temper the peso’s rise since these projects will no longer be

financed through overseas assistance or equity from abroad. What could leak in, however, is

foreign technology and know-how because as an equity investor, with a long time frame, the

SWF would also have greater leverage to request that suppliers provide technology transfer

to local partners. This should unapologetically be part of its investment prioritisation

framework.

Conclusion

Under President Benigno “Noynoy” S. Aquino III’s rubric of good governance, the stage is

now set for him to pursue an economic model for the country that was espoused by his late

father, the ex-senator Benigno “Ninoy” Aquino, Jr. In a speech delivered in Los Angeles back

in 1981,the exiled pro-democracy advocate articulated a policy of coordinated investment to

overcome development bottlenecks15. As the Carnegie Endowment for International Peace

found, sound democratic institutions best explain a nation’s compliance with the Santiago

Principles.

With the government now facing the prospect of receiving investment grade status in the

coming year16, it must prepare for any unintended adverse consequences this might have as

more short-term investors flock to the domestic capital market boosting the peso’s value and

putting more of an already unbearable strain on exporters of goods and services. This has

been the impact of previous credit upgrades. This will have perverse consequences for

employment and overall competitiveness.

For good governance to yield economic benefits for the people, it needs to be used toaddress the developmental challenges facing the nation. This presents policy makers with a

once in a generation opportunity to get things right. Setting up a SWF would be the most

appropriate way to free the country from its developmental trap, and it offers the Filipino

people the single best hope of collectively deriving benefit from the fruits of our labour.

14Francisco, R and S. Grudgings. 18 December 2012. “The booming Philippines missing link – foreign

investors.”Reuters. 19 January 2013 <http://www.reuters.com/article/2012/12/19/us-philippines-investment-

idUSBRE8BI01B20121219/>.15

Robles, Raissa. 21 August 2011. “Democracy, according to Ninoy Aquino.”Inside Philippine Politics and

Beyond. 19 January <http://raissarobles.com/2011/08/21/democracy-according-to-ninoy-aquino/>.16Remo, Michelle. 30 October 2012. “Philippines gets credit upgrade from Moody’s”. The Philippine Daily

Inquirer. 19 January 2013 <http://business.inquirer.net/89980/moodys-upgrades-ph-credit-rating/>.