Embed Size (px)

Citation preview

109

Fruits and vegetables is one of the most important and fast growing sub-sectors of the food processing

sector, as fruits and vegetables form an indispensable part of healthy diet. China, India, Brazil, USA,

Italy, Spain, Mexico, Iran the Philippines and France are the top ten aggregate fruit producers in the

world.

Asia dominates the world vegetables scene accounting for nearly 60% of global production, with

China and India ranking as 1st and 2nd. European Union and U.S.A follow next. Over the last quarter

of a century (1980-2004), the fruit and vegetable market has been one of the fastest growing of all

agricultural markets.

Global fruit and vegetables consumption increased by an average of 4.5% per annum between 1999

and 2009. This was higher than the world population growth rate, meaning that the global per capita

consumption of fruit and vegetables has also increased.

IntroductionIntroductionIntroductionIntroduction

110

The list of large exporters of fresh fruits and vegetables starts with the USA. Mexico is 2nd, having

overtaken EU in the past decade. Other big exporters are China, Chile, Ecuador and South Africa. In

total, the top 10 exporters account for 66% of the world's fresh fruits and vegetables exports. On the

import side, the EU is the world's largest importer. The US follows closely behind, while other

countries, like Canada, Japan and China have significantly smaller imports. The top 2 importers (EU

and USA) take in 50%.

Fruit and vegetable products (both fresh and processed) accounted for 22% of total agricultural

exports from developing countries. Fruit trade is heavily concentrated in Bananas, Citrus, Grapes and

Apples. Fresh produce comprising citrus, pears, peaches, nectarines, plums and kiwi fruit, and

processed produce comprising tomato based products, fruit juices and concentrates, packed

vegetables as well as tinned and frozen fruits are mostly certified under Protected Geographical

Indication status.

India is the second largest producer of fruits and vegetables in the world, accounting for about 16% of

global vegetable production and 10% of world fruit production. India’s production of fruits and

vegetables, currently, stands at 64 million tonnes and 126 million tonnes, respectively, making up for

around 12% and 14% of world production, in the respective sector. India is a front runner in many

fruits and vegetables with share in world production as follows:

» 41% of mango

» 23% of banana

» 24 % of cashew nut

» 10% of onion

» 30% of cauliflower

» 36% of green peas

Although India’s share in world exports of fruits and vegetables are less than 1.5%, India’s exports of

fruits and vegetables have grown at a CAGR of 20.61% and 7.21% respectively by value between 2004

and 2007. Over 90% of India’s exports in fresh fruits and vegetables mainly go to west Asia and East

European markets. With respect to export value, mango is the main fruit crop, and among vegetables,

onion occupies the first position. In the recent years, potatoes and green vegetables like okra, bitter

gourd, and green chillies are also showing good export potential. Commodity-wise analysis reveals

majority of India’s fruits and vegetables are exported to neighbouring countries followed by Middle

East region.

111

Bangladesh is one of the major trading partners for India for exports of fresh fruits, and onions and

potatoes. However, in the recent years, fruits from India such as grapes, mangoes, and vegetables,

such as eggplant are increasingly gaining market share in the UK, the Netherlands, France and

Germany. India is the fruit and vegetable basket of the world. India produces 54% of world’s mango,

23% banana, 24% cashew nuts, 36% green peas and 10% onion production.

Andhra Pradesh is a major fruit and vegetable producing States of India. A variety of tropical and sub-

tropical fruits and vegetables are grown in the state. The state occupies a distinct place in the national

scenario in respect of some fruits and vegetables as indicated in table.

Production of Major Fruits and Vegetables in Andhra Pradesh [Area: Ha Production: MT]

112

There are 157 fruit and vegetable processing units in the state mainly in the small and medium sector.

Fruit processing activity is largely concentrated in Chittoor district. There are 67 processing units with

an aggregate installed capacity to produce about 2 lakh tonnes of mango and other fruit pulps.

Contract manufacturing for leading exporters and food retail majors is most common. Own account

production is low. 90% of the production by these units is exported in the form of canned pulp or

aseptic concentrate. The remainder finds way to domestic markets in the form of RTS fruit juices and

nectars, jams and jellies and de-hydrated fruit bits.

This report identifies the trade potential and markets for few prominent fruits and vegetables

produced in the state including tomatoes, onion, cabbage, green chilly, mangoes and processed

mangoes (mango sliced dried, mango squash), fresh grapes and raisins and banana.

113

Tomato is one of the largest producing vegetables in the state of Andhra Pradesh amounting to 26.89

% of total vegetable production in 2003-04 to 36.58% in 2006-07. Districts with highest tomato

producing capacity are Prakasam & Vishakhapatnam in coastal region, Karnool & Chittoor region in

Rayalaseema Region; Adilabad & Ranga Reddy in Telangana Region. (Details in the Annexure)

Region-wise Area and Production of Tomato in Andhra Pradesh

(2002-2003 to 2006-2007)

(Area in Hect. & Production in M.Ts.)

2002-03 2003-04 2004-05 2005-06 2006-07 Areas in AP

A P A P A P A P A P

Coastal Area 9833 98330 10335 124020 8686 156348 7583 144077 23306 442814

Rayalaseema Region 44106 441060 39835 478020 38652 695736 33922 644518 26475 503025

Andhra Region 53939 539390 50170 602040 47338 852084 41505 788595 49781 945839

Telangana Region 25500 255000 26904 322848 22164 398952 42782 812858 31288 594472

Andhra Pradesh 79439 794390 77074 924888 69502 1251036 84287 1601453 81069 1540311

However, this high production potential is not reflected in the exports of tomato from the region and

therefore this section will help the tomato exporters from the state to identify the right market for the

exports of tomato.

Trend Analysis for Tomatoes, fresh or chilled (070200)

Table 1 Trend in exports for 070200

2003 2004 2005 2006 2007 2008 CAGR

1473.29 1298.66 2462.526 7522.806 20322.6 35885.69 89.37

The CAGR from the year 2003 to 2008 is 89.37. The overall trend shows a high positive growth rate

during that period. Another trend which can be noticed from the above table is that exports are

growing positively where they have slightly decreased. The CAGR shows that the exports are steadily

increasing.

Tomatoes, fresh or chilled [070200]Tomatoes, fresh or chilled [070200]Tomatoes, fresh or chilled [070200]Tomatoes, fresh or chilled [070200]

114

Figure 1 India’s export to the world

It can be seen from the above graph that India’s export of Tomatoes has been continuously increasing

apart from the year 2004. The growth has been tremendous from 1473.29 US $ mn to 35885 in 2008.

Revealed Comparative Advantage of Tomato

Source: Author’s calculations

India’s export World Export

Year Tomatoes Total Agriculture Tomatoes Total Agriculture RCA

2003 1473.291 324572.077 4293237.753 26636644.7 0.028

2004 1298.66 360681.075 4491324.398 30187384.07 0.024

2005 2462.526 570050.192 5035453.114 32293223.39 0.027

2006 7522.806 622347.956 5637266.856 37184264.96 0.079

2007 20322.595 632880.057 6635987.795 42953816.81 0.202

2008 35885.689 683739.685 5647001.264 40211871.08 0.373

115

Figure 2: RCA for 070200

The RCA values have been quite low starting from .028 in the year 2003 and increasing to .373 in the

year 2008. This shows that India’s strength vis-a-vis world is quite weak.

Major Export Destinations for Tomatoes from the region as per the past trends are Pakistan, United

Arab Emirates, Bangladesh & Maldives.

Importing

Country 2003 2004 2005 2006 2007 2008 Growth

Bangladesh 2.37 0.91 1.18 0.64 0.9 2.41 0.42

Maldives 0.02 0.07 0.02 0.02 0.07 0.09 45.65

Pakistan 0.02 1.55 3.74 31

UAE 0.01 0.01 0.01 0.12 2.47 4.22 353.24

The market fluctuations for these markets are as follows:

2003 2004 2005 2006 2007 2008

Bangladesh Bangladesh Pakistan Pakistan Pakistan Pakistan

Nepal Nepal Bangladesh

United Arab

Emirates

United Arab

Emirates

United Arab

Emirates

Maldives Pakistan

United Arab

Emirates Bangladesh Bangladesh Bangladesh

United

States Maldives Nepal Nepal Nepal Nepal

Italy Japan Maldives Singapore Maldives Maldives

116

From the above we see that Bangladesh which was the best market in 2003 & 2004 had suddenly

declined in subsequent years and had been overpowered by Pakistan and UAE by 2008. Pakistan has

been the topmost market throughout last five years. USA and Japan which are the most desirable

market by the exporters have been unreachable after 2003 and 2004 respectively due to high pesticide

content present in the tomato produced in the region. The details of these SPS issues has been handled

in report II of the project.

Trade Intensity Index for Major export Markets of Tomato

We see that India’s TII with Pakistan has been pretty good at an average around 3 but has reduced to

2.94 in 2008 from a high of 4.62 in 2004. With UAE the TII has been pretty low but has increased

considerably to 0.34 in 2008. With Bangladesh TII has been good at an average of around 2. Maldives

also commands a good TII but has reduced from 4.93 to 2.34 in 2008.

117

Trade Intensity Index of Other Competing Suppliers to identified target Countries

Pakistan TII

India 2.94

UAE 0.02

UAE TII

Jordan 5.52

European Union 0.78

Netherlands 0.82

Ethiopia(excludes Eritrea) 0.59

India 0.35

Bangladesh TII

India 1.93

Thailand 0.45

United Arab Emirates 2.86

Maldives TII

India 3.21

United Arab Emirates 1.07

Sri Lanka 0.16

Lower TII than India Higher TII than India hence the competitor.

⇒ Analyzing the TII of the competitors in the target markets; we see that in Pakistan; UAE is the only

other supplier but India with a TII value difference of 2.92 is in a much comfortable position.

⇒ UAE is the toughest market with tough competition from Jordan, European Union, Netherlands &

Ethiopia since TII values for these markets are higher with UAR as compared to India.

⇒ UAE is also a competitor for India in Bangladesh

⇒ Maldives is a good market to target for tomato exports from the state since India is much better off

that UAE and Srilanka.

118

RELATIVE COMPETITIVE ADVANTAGE

Pakistan Rel. CA

India 1.012

Competitors

UAE 0.005

UAE Rel. CA

India 0.19

Competitors

Jordan 3.03

European Union 0.43

Netherlands 0.44

Ethiopia(excludes Eritrea) 0.32

Bangladesh Rel. CA

India 1.01

Competitors

Thailand 0.23

United Arab Emirates 1.48

Maldives Rel. CA

India 2.37

Competitors

United Arab Emirates 0.79

Sri Lanka 0.12

Relative competitive position for India is better off Tough competition for India

⇒ In Pakistan India has the highest RCE

⇒ In UAE Jordan has the highest RCE

⇒ In Bangladesh UAE has the highest RCE

⇒ In Maldives India has the highest RCE

119

Tariff and Non Tariff barriers for Tomato in Identified Markets

Other Tariff where ever

applicable

Major Markets

Import

tariff

Tariff

description Tariff rate

NTM %

NTM

Customs Duty 35%

Product Characteristics

requirement to protect humans Pakistan

0%

Sales Tax 15%

100%

Labeling requirement to protect

human health

U AE 0% - - 0% none

Maldives 15% - - 0% none

Statutory Rate 100%

Infrastructural

Surcharge 2.5%

VAT 15%

0%

Bangladesh

37.5%

Income Tax on

Imports

0.%

0%

none

The analysis of the table above gives a mixed result. In market where MFN import duties are low like

in case of Pakistan, the non tariff barriers in terms of labeling requirements and human health

requirements are very high and in Markets like Maldives where there are no non tariff barriers, the

MFN duty is high. There is a high Tariff Rate of 35 % in Pakistan and Sales Tax of 15 %. UAE is free of

any Tariffs. Bangladesh involves a variety of tariffs like Infrastructural Surcharge, VAT, Income tax on

Exports, MFN etc. In this scenario, UAE seems to be the best combination where the import duty is 0%

and no non tariff barriers exist. Maldives in the next best option since there is no barrier and the

import duty is relatively lower than other markets.

Presence of Special Safeguard Duty

Country Volume Trigger Price Trigger

Pakistan NO NO

United Arab Amirates NO NO

Bangladesh NO NO

Maldives NO NO

NO NO

There is no special Safeguards duty present in Any Market

120

Tariff Rate Quota Structure of 070200 in major export destinations

Markets

TRQ Quantity (METRIC

TONS)

In quota -

Duty

Out Quota -

Duty

Pakistan No No No

United Arab

Amirates No No No

Bangladesh No No No

Maldives No No No

No No No

Subsidy provided to Tomatoes in Identified markets

Markets Product Specific Non Product Specific Green Box S & D * Currency

Pakistan 3.66 yes none none

UAE none none yes 90,00,000 US$ million

Bangladesh none 40.18 none none (billion Rp)

Maldives none none none 2335.02 RM million

*Special and Differential Treatment – "Development Programs"

Above are the various subsidies available in each market.

Comparative Analysis across Major Export Destinations for Tomatoes

Other Tariff where ever

applicable

NTM

%

NTM Markets Grow

th

Mkt

fluctuatio

n

TII

(Ind versus

competitors)

Import

tariff

Tariff

description Tariff rate

Customs Duty 35%

Product

Characteristics

requirement to

protect humans Pakistan

- Topmost Very good

0% Sales Tax 15%

100%

Labeling

requirement to

protect human

health

UAE 353.2

4

Rising Jordan and

EU 0% - - - -

Bangladesh 0.42 Declining UAE

15% - - - -

Statutory Rate 100%

Infrastructural

Surcharge 2.5%

VAT 15%

Maldives

45.65 Declining Very good

37.5%

Income Tax on

Imports

0.%

- -

121

Trade Intensity Index for Tomatoes across various markets

Markets 2003 2004 2005 2006 2007 2008

Pakistan 0.00 4.62 4.8 6.0 3.56 2.94

UAE 0.00 0.00 0.02 0.24 0.45 0.34

Bangladesh 2.00 1.8 1.5 2.2 3.1 1.9

Maldives 4.2 5.8 6.1 7.0 5.0 2.34

Conclusions

⇒ The exports are growing at a CAGR of 89.37% which is a healthy figure.

⇒ RCA is generally increasing which is a positive sign. Although state of AP needs to

develop an export strategy to improve its competitiveness since the RCA value is very

poor.

⇒ Market Analysis in descending order of priority

Growth Mkt

fluctuation TII with India TII

(Ind versus

competitors)

Tariffs Non Tariffs

(%)

Subsidy

UAE Pakistan Pakistan Maldives

UAE UAE

Bangladesh

Maldives

Pakistan

Maldives UAE

UAE Pakistan

Bangladesh Pakistan Bangladesh

Bangladesh Bangladesh Maldives Bangladesh Pakistan Maldives

Pakistan Maldives Bangladesh UAE Maldives

UAE

A comparative analysis across identified markets highlights the fact that, considering various

parameters, Pakistan stands number one in terms of growth, strength in bilateral trade with India for

indicating high acceptance for Indian tomatoes, less competition and no subsidy. If only Andhra

Pradesh tomato growers and exporters can tackle the non tariff barrier of labeling requirements in

Pakistan, this market is most suggestive. Next best market is UAE, except for the competition from

Jordan and EU.

122

TOMATO PRODUCTION IN ANDHRA PRADESH

Region/District-wise Area and Production of Tomato in Andhra Pradesh

(2002-2003 to 2006-2007)

(Area in Hect. & Production in M.Ts.)

2002-03 2003-04 2004-05 2005-06 2006-07 District

A P A P A P A P A P

Srikakulam 345 3450 526 6312 348 6264 435 8265 348 6612

Vijaya Nagaram 605 6050 643 7716 670 12060 670 12730 585 11115

Vishakhapatnam 1294 12940 1461 17532 1515 27270 2608 49552 2408 45752

East Godavari 681 6810 1423 17076 980 17640 893 16967 962 18278

West Godavari 317 3170 681 8172 196 3528 430 8170 458 8702

Krishna 1322 13220 1004 12048 536 9648 1684 31996 1707 32433

Guntur 1067 10670 315 3780 874 15732 718 13642 778 14782

Prakasam 4048 40480 4238 50856 3526 63468 0 0 16000 304000

Nellore 154 1540 44 528 41 738 145 2755 60 1140

Coastal Area 9833 98330 10335 124020 8686 156348 7583 144077 23306 442814

Chittoor 16838 168380 13296 159552 14588 262584 14678 278882 13529 257051

Cuddapa 2443 24430 2606 31272 4378 78804 4288 81472 1264 24016

Anatapuram 3356 33560 3295 39540 0 0 3906 74214 632 12008

Karnool 21469 214690 20638 247656 19686 354348 11050 209950 11050 209950

Rayalaseema Region 44106 441060 39835 478020 38652 695736 33922 644518 26475 503025

Andhra Region 53939 539390 50170 602040 47338 852084 41505 788595 49781 945839

Mehaboob Nagar 5518 55180 4942 59304 3217 57906 3650 69350 3500 66500

Ranga Reddy 10468 104680 12155 145860 2864 51552 6990 132810 6877 130663

Hyderabad 0 0 0 0 0 0 0 0 0 0

Medak 2207 22070 2474 29688 3722 66996 4081 77539 3790 72010

Nizamabad 1065 10650 2331 27972 1316 23688 2469 46911 2469 46911

Adilabad 1851 18510 1347 16164 7962 143316 21905 416195 11231 213389

Karim Nagar 813 8130 1100 13200 740 13320 1831 34789 1280 24320

Warangal 1688 16880 1085 13020 408 7344 175 3325 432 8208

Khamam 823 8230 647 7764 1375 24750 1381 26239 1400 26600

Nalgonda 1067 10670 823 9876 560 10080 300 5700 309 5871

Telangana Region 25500 255000 26904 322848 22164 398952 42782 812858 31288 594472

Andhra Pradesh 79439 794390 77074 924888 69502 1251036 84287 1601453 81069 1540311

123

The onion is one of the oldest vegetables known to mankind and is used in an array of recipes and

preparations. However, it’s rarely eaten on its own and is usually an accompaniment to the main

course. Depending on the variety, an onion can be tangy and pungent or mild and sweet. World onion

production is estimated at approximately 105 billion pounds each year. The average annual onion

consumption is approximately 13.67 pounds of onions per person across the world. Libya has the

highest consumption of onions with an astounding average per capita consumption of 66.8 pounds. At

least 175 countries grow onions. According to the United Nations Food and Agriculture Organization,

there are an estimated 6.7 million acres of land under onion cultivation in the world, producing 105

billion pounds of onions each year. Approximately 8 percent of this global onion production is traded

internationally. Leading onion production countries are China, India, United States, Turkey and

Pakistan, as can be seen from Table below.

Although onions are consumed in all the countries of the world, they are cultivated only in some

countries. Area under onion cultivation in the world is about 20 lakh hectares. India has the largest

area of about 4 lakh hectares (20 per cent) followed by China at about 3 lakh hectares.

Onions and shallots, fresh or chilled [070310]Onions and shallots, fresh or chilled [070310]Onions and shallots, fresh or chilled [070310]Onions and shallots, fresh or chilled [070310]

124

But the production is the highest in China (48 lakh MT) as against India (44 lakh MT) due to higher

productivity in China (16 MT/ha compared to India’s 14 MT/ha).

Onion production in India

Onion, a major ingredient in Indian food, and a politically-sensitive commodity, is typically cultivated

thrice a year; in monsoon, winter and summer. The onion harvested during October-December is

Kharif crop, during January-March is Rangada crop, and in April-May is called Rabi or Unhal Crop.

All three crops are available for export, with Rabi having the longer shelf life.

In India, of the four lakh hectares of area under onion, the maximum area of about 95,000 hectares

(about 24 per cent) is in Maharashtra. Andhra Pradesh is next important onion producing state facing

domestic competition with rich quality of onions from Karnataka, Orissa, U.P., Rajasthan, M.P., Tamil

Nadu, Bihar and Gujarat.

2 Source: Agricultural Statistics, Indian Horticulture Database, National Horticulture Board, Gurgaon, India 007-08 2006-07

Small onions, known as rose onion, and Krishnapuram onions are grown in Kolar district in

Karnataka and Cudappah district in Andhra Pradesh. Multiplier onion, known as Podisu and Shallots,

are grown in Tamil Nadu, Pondicherry and Andhra Pradesh.

125

District-wise breakup of production of Onion in AP is given in the table below indicating the rise in

the production levels for last five years indicating the importance of onions for the state. This section

handles the market identification for onion export from the state.

District-wise Area and Production of Onion in Andhra Pradesh

(Area in Hect. & Production in M.Ts.)

2004-05 2005-06 2006-07 2007-08 2008-09 District

A P A P A P A P A P

Coastal Area 5163 80078 3179 47685 4288 68608 4849 82433 4825 82025

Rayalaseema

Region 17825 276466 15410 231150 17097 273552 20439 347463 19167 325839

Andhra Region 22988 356544 18589 278835 21385 342160 25288 429896 23992 407864

Telangana

Region 12314 190990 10460 156900 14029 224464 12923 219691 9772 166124

Andhra Pradesh 35302 547534 29049 435735 35414 566624 38211 649587 33764 573988

Export of Onions from India

India’s onion exports have made a gradual growth during the last four-and-a-half decades. Onion is

the pride of India’s agricultural exports and earns valuable foreign exchange for the country. Of the

total fresh vegetable exports, the share of onion is 67 per cent. Onion has now become a cash crop,

which is in demand in export markets as well as in India throughout the year.

2003 2004 2005 2006 2007 2008 CAGR

119.09 231.07 409.22 476.33 293.61 678.96 41.64

The CAGR from the year 2003 to 2008 is 41.64. The overall trend shows a high positive growth rate

during that period. The exports have been consistently increasing apart from 2007 where they fell to

293.61 US $ mn.

126

Figure 3 India’s export to the world

It can be seen from the above graph that India’s exports have been continuously increasing apart from

the year 2007. The growth has been tremendous from 119 US $ mn to 678.96 in 2008.

Revealed Comparative Advantage of Onion

Revealed Comparative Advantage for Indian Onion

India’s Export World's Export

Onion Total agriculture Onion Total agriculture RCA

2003 119.09 296871.65 231566.05 26636644.7 0.046

2004 231.07 364224.70 223174.66 30187384.07 0.085

2005 409.22 537491.59 241927.78 32293223.39 0.101

2006 476.33 609294.18 287299.86 37184264.96 0.101

2007 293.61 632880.05 308438.48 42953816.81 0.064

2008 678.96 683739.68 330276.34 40211871.08 0.120

127

The RCA values have been quite low starting from .04 in the year 2003 and increasing to .12 in the year

2008. This shows that India’s strength vis-a-vis world is quite weak. The strength however has

increased from 2003 to 2008.

Major Export Destination

Onions grown in India are very much in demand in Gulf Countries and Singapore, Malaysia, Sri

Lanka and Bangladesh because of strong pungency. Small onions produced in Andhra Pradesh are

exported from Chennai port to Singapore and Malaysia, and multiplier onions to Singapore, Malaysia,

Sri Lanka etc. The other major export destinations are United Arab Emirates, Canada and Saudi

Arabia.

Importing

Country 2003 2004 2005 2006 2007 2008 Growth

Canada 0.04 0 0 0.01

Saudi Arabia 1.94 2.14 1.32 0.86 1.81 3.55 16.31

UAE 13.79 19.27 16.91 16.61 46.31 35.84 26.97

Market Fluctuations

2003 2004 2005 2006 2007 2008

Iran Iran Iran Iran Kenya UAE

Turkey Turkey Turkey Turkey Turkey Canada

Nigeria UAE Syrian Arab Republic Tanzania UAE Saudi Arabia

UAE Bahamas UAE UAE Uganda Qatar

Kuwait Bangladesh Malaysia Saudi Arabia Spain Bahamas

As we can see the constant markets for last five years have been Iran, UAE and Turkey. Some of the

markets which have recently emerged in last two years are Saudi Arabia, Uganda, Spain and Canada.

But an important observation is that Canada appears only in 2008.

128

INDIA’S TII with Identified Markets for Tomato

United Arab Emirates

Year TII

2003 0.44

2004 1.41

2005 2.15

2006 1.22

2007 1.42

2008 3.55

Canada

Year TII

2003 0

2004 0

2005 0

2006 0

2007 0.002

2008 0.224

Saudi Arabia

Year TII

2003 0.74

2004 0.36

2005 0

2006 0.042

2007 0.015

2008 6.87

As we can see India’s TII in UAE has been consistently increasing, in Canada it is quite low at .224

whereas it is extremely high in Saudi Arabia at 6.87.

129

COMPETETORS TII

Competitor's export to the Market World's Export to the market

UAE Onion Total Agriculture Onion

Total

Agriculture TII

India 410.593 84930.633 625.69 4543.883 0.035

Ethiopia 11.607 23443.105 625.69 4543.883 0.0035

Netherlands 135.569 34194.423 625.69 4543.883 0.028

In UAE each of the competitors has a very low TII

Competitor's export to the Market World's Export to the market

Canada Onion Total Agriculture Onion

Total

Agriculture TII

India 76.191 5585.445 12292.938 12292.938 0.013

United States 11730.297 2048281.608 12292.938 12292.938 0.006

EU 47.137 65022.766 12292.938 12292.938 0.0007

In Canada also every competitor has an extremely low TII

Competitor's export to the Market World's Export to the market

Saudi Arabia Onion Total Agriculture Onion Total Agriculture TII

India 67.72 18302.87 142.98 142.98 0.004

Netherlands 54.52 21907.71 142.98 142.98 0.002

Egypt, Arab 12.51 69642.47 142.98 142.98 0.0002

Again in Saudi Arabia each of the country has an extremely low TII.

TII values lower as compared with India

RELATIVE COMPETITIVE ADVANTAGE

United Arab Emirates India’s Export to the Market World's Export to the market

Onion Total Agriculture Onion Total Agriculture Rel. CA

India 410.593 84930.633 557.769 142568.161 1.23

Competitor's export to UAE World's Export to the market

Competitors Onion Total Agriculture Onion Total Agriculture Rel. CA

Ethiopia 11.607 23443.105 557.769 142568.161 0.12

Netherlands 135.569 34194.423 557.769 142568.161 1.02

130

Canada

India’s Export to the Market World's Export to the market

Onion Total Agriculture Onion Total Agriculture Rel. CA

India 76.19 5585.44 11853.62 2118889.81 2.43

Competitor's export to UAE World's Export to the market

Competitors Onion Total Agriculture Onion Total Agriculture Rel. CA

United States 11730.29 2048281.60 11853.62 2118889.81 1.02

European

Union 47.13 65022.76 11853.62 2118889.81 0.13

Saudi Arabia India’s Export to the Market World's Export to the market

Onion Total Agriculture Onion Total Agriculture Rel. CA

India 67.728 18302.879 134.756 109853.063 3.02

Competitor's export to UAE World's Export to the market

Competitors Onion Total Agriculture Onion Total Agriculture Rel. CA

Netherlands 54.522 21907.713 134.756 109853.063 2.02

Egypt, Arab 12.506 69642.471 134.756 109853.063 0.14

The Trade intensity index analysis substantiated by Relative Competitive Advantage analysis

indicates advantageous position of India vis a vis other competing suppliers in all the identified major

markets.

TARIFFS

Tariff and Non Tariff barriers for Onions in Identified Markets Major Markets Import tariff NTM % NTM

United Arab Emirates 0% 0%

Canada 0% 84.6% Authorization for Plant Health Protection

Saudi Arabia 12.0% 100%

Testing, Inspection and Quarantine

Requirements

Presence of Special Safeguard Duty

Country Volume Trigger Price Trigger

United Arab Emirates NO NO

Canada NO NO

Saudi Arabia NO NO

There is no special Safeguards duty present in Any Market

131

SUBSIDY

Subsidy on Onion in identified markets

Markets Product Specific Non Product Specific Green Box S&D Currency

UAE none none 34,00,000 90,00,000 US$ million

Canada none none US$ million

Saudi Arabia none none none none (billion Rp) Special and Differential Treatment – "Development Programs

Above are the various subsidies available in each market.

Tariff Rate Quota Structure

Tariff Rate Quota Structure of Onion in major export destinations

Markets TRQ Quantity (MT) In quota - Duty Out Quota - Duty

UAE No No No

Canada No No No

Saudi Arabia No No No

There is no Tariff Rate Quota present in any market.

Considering the fact that all the three markets are depicting positive growth in exports and have good

bilateral trade strength as compared with their competitors in the same market, absence of subsidies,

TRQs and special safeguard duty, three prospective markets for Onion export from the state of

Andhra Pradesh could be UAE, Canada and Saudi Arabia.

Strategies to boost Onion Export

Onion Village

The concept of developing the onion villages may help increase the export of onion. The provision of

financial assistance to exporters to complete in the international market may also be looked into.

Export on regular basis not only helps in getting foreign exchange earnings but also allows farmers to

get remunerative price for their produce thereby encouraging them to sustain the production and

availability of onions. Government should in fact have long term export policy and should even

introduce contract production system in suitable pockets.

132

Quality standards for export

The quality standards of onion have been fixed by Agmark although now it is not mandatory to obtain

Agmark certificate for onion export. It is necessary to maintain the quality by observing the standards.

The grades, big, medium, small and mixed are followed for different types of onions which depend on

requirements from importing country. It is observed that Middle East countries demand light red to

dark red colour, European countries and Japan demand yellowish /brown colour onions having mild

pungency, 3-4 cm sized onions are preferred in Bangladesh, 4-6 cm sized are preferred in Middle East

and Far East, while European and Japan prefer 6-7 cm sized onions. Rose onions of 2.5 - 3.5 cm size

and multiplier onions of bigger size with attractive red colour bulblets are preferred for export.

European countries and Japan prefer yellow big-sized onions. The demand in these countries is from

February and up to May and therefore Andhra Pradesh onion exporters should try to fulfill the

demand during this period like in case of onion growers from Nasik area of Maharashtra.

The bulbs selected for export should be reasonably uniform in shape , size, colour and pungency. They

should be mature ,solid, reasonably firm with tough clinging skin, thoroughly cured and dried outer

scales free from dirt and other foreign material. Defective, diseased, damaged bulbs caused by seed

stem, tops, roots, moisture, dry sunscald, sun burn, sprouting, mechanical or other injuries and

staining, free from moulds, soft rot and insect attack should not be used for export. The trained

labourer are thus required for grading and packing of onions for exports. The packing size for export

varies from 8 to 25 kg depending on requirement of onion by importing country. Although jute mesh

bags are used for export, if there is no restriction for their use due to environmental pollution

problems in some countries, plastic-wooven bags since are reusable and attractive, should be

introduced.

India is presently exporting onions to mainly Gulf countries, Far East countries, Bangladesh, and Sri

Lanka where there is not much scope to increase the quantity as some countries have also started their

own production. The scope, however, exists for diversifying the market to European countries and

Japan. These countries do not prefer strong and pungent onions. In these countries, yellow onions

having mild pungency, bigger bulb size with thick fleshy layers are preferred. Similarly, there is a

scope for exporting dehydrated onions as many processing units under export-oriented unit schemes

have been installed in India. These are not presently running to their installed capacity mainly for

want of raw material. Thus, there is a scope for development of varieties suitable for dehydration.

133

Constraints in onion export

There are some constraints seen in onion exports and suggestions to overcome these problems so that

onion export from the state of AP is not only continued but maybe increased :

Suggestions for improvement

• Popularization of improved varieties, quality seed production and distribution, expansion of

area in non- traditional pockets and contract production for export.

• Planning for contract production for export market expansion of area and production of kharif

onion for early harvesting.

• Unawareness of proper post harvest practices and quality. Training of farmers and others

involved in onion production, post-harvest management and marketing.

• Packing material used is not attractive. Introduction of attractive, eco-friendly packages,

consumer packages etc.

• Electrically-ventilated containers for export of yellow onions to Europe . Adequate transport

with reasonable rates, synchronize the rail/road transport with schedule of vessel and

providing insulated wagons.

• Developing more ventilated storage godowns for onions. Providing handling sheds and make

available modified containers with proper ventilation

• To develop market intelligence for different seasons, quality of produce and corresponding

season crop in other competing countries.

STRATEGY FOR INCREASING EXPORT

The strategies suggested to improve the export of onions are :

• Production and distribution of quality seed of improved varieties in adequate quantities by

following seed village concept.

• Development of disease and insect pests resistant, heat / moisture stress tolerant varieties by

taking such work at NRC for Onion and Garlic.

• Development of biological control measures against pests and disease by taking up work with

NRC for Onion and Garlic and NHRDF.

• Development of yellow coloured hybrid and OPs for export to European and Japanese

markets by popularizing the technology for production during late-kharif based on work

undertaken by NHRDF and adopting contract production.

• Development of bigger bulblet varieties in multiplier onion.

• Training of farmers, traders and exporters involved in onion production, handling and

marketing.

• Creation of adequate curing and storage facilities at field level and at ports.

Popularizing various onion products in export markets developing varieties suitable for various

processed products.

134

ONION PRODUCTION IN ANDHRA PRADESH

Region/District-wise Area and Production of Onion in Andhra Pradesh

(2002-2003 to 2006-2007)

(Area in Hect. & Production in M.Ts.)

2002-03 2003-04 2004-05 2005-06 2006-07

District Area

Produ-

ction Area

Produ-

ction Area

Produ-

ction Area

Produ-

ction Area

Produ-

ction

Srikakulam 1541 23901 1129 16935 1620 25920 1831 31127 1620 27540

Vijaya Nagaram 620 9616 395 5925 300 4800 300 5100 855 14535

Vishakhapatnam 540 8375 221 3315 445 7120 470 7990 450 7650

East Godavari 372 5770 303 4545 208 3328 370 6290 550 9350

West Godavari 1 16 0 0 4 64 0 0 0 0

Krishna 223 3459 92 1380 8 128 179 3043 0 0

Guntur 1576 24444 867 13005 843 13488 1699 28883 650 11050

Prakasam 211 3273 95 1425 0 0 0 0 700 11900

Nellore 79 1225 77 1155 860 13760 0 0 0 0

Coastal Area 5163 80078 3179 47685 4288 68608 4849 82433 4825 82025

Chittoor 671 10407 518 7770 601 9616 430 7310 509 8653

Cuddapa 3954 61327 2662 39930 3147 50352 3459 58803 2080 35360

Anatapuram 1545 23963 1381 20715 0 0 500 8500 528 8976

Karnool 11655 180769 10849 162735 13349 213584 16050 272850 16050 272850

Rayalaseema

Region 17825 276466 15410 231150 17097 273552 20439 347463 19167 325839

Andhra Region 22988 356544 18589 278835 21385 342160 25288 429896 23992 407864

Mehaboob

Nagar 3202 49663 2246 33690 3574 57184 3574 60758 2674 45458

Ranga Reddy 2618 40605 2224 33360 358 5728 862 14654 759 12903

Hyderabad 0 0 0 0 0 0 0 0 0 0

Medak 3454 53572 3551 53265 3500 56000 3522 59874 3522 59874

Nizamabad 1524 23637 1042 15630 1820 29120 355 6035 355 6035

Adilabad 599 9290 547 8205 3641 58256 3670 62390 1226 20842

Karim Nagar 688 10671 654 9810 720 11520 806 13702 806 13702

Warangal 213 3304 175 2625 274 4384 0 0 296 5032

Khamam 4 62 3 45 120 1920 134 2278 134 2278

Nalgonda 12 186 18 270 22 352 0 0 0 0

Telangana

Region 12314 190990 10460 156900 14029 224464 12923 219691 9772 166124

Andhra Pradesh 35302 547534 29049 435735 35414 566624 38211 649587 33764 573988

135

Trend Analysis for Salad beetroot, salsif, celeriac, radish & sim edible roots fresh or chilled

Table 2 Trend in exports for 070690

Code 2003 2004 2005 2006 2007 2008

CAGR

070690 117701.1 166504.5 152837 226423.8 263593.9 330584.6 22.94

The CAGR from the year 2003 to 2008 is 22.94. The overall trend shows a high positive growth rate

during that period. The exports have been consistently increasing apart from 2005 where they fell to

15283 US $ mn.

Figure 4 India’s export to the world

It can be seen from the above graph that India’s exports have been continuously increasing apart from

the year 2005. The growth has been tremendous from 117701 US $ mn to 330584.64 in 2008.

Radish [Radish [Radish [Radish [070690]070690]070690]070690]

136

Revealed Comparative Advantage of 070690

RCA for Radish

The RCA values have been quite low starting from .04 in the year 2003 and increasing to .12 in the year

2008. This shows that India’s strength vis-a-vis world is quite weak. The strength however has

increased from 2003 to 2008.

India’s export World export

Radish

Total

Agriculture Radish Total Agriculture RCA

2003 117701.12 296871.65 1271288.62 26636644.7 8.30

2004 166504.49 364224.70 1457308.74 30187384.07 9.46

2005 152836.96 537491.59 1450810.18 32293223.39 6.32

2006 226423.77 609294.18 1766911.72 37184264.96 7.82

2007 263593.91 632880.05 2198338.90 42953816.81 8.13

2008 330584.64 683739.68 2110591.91 40211871.08 9.21

137

Major Export Destination

Major Export Destinations are:

Pakistan

Bangladesh

Malaysia

United Arab Emirates

MARKET FLUCTUATIONS

2003 2004 2005 2006 2007 2008

Bangladesh Bangladesh Bangladesh Bangladesh Bangladesh Bangladesh

Malaysia Malaysia Malaysia Malaysia Malaysia Malaysia

Sri Lanka

United Arab

Emirates Sri Lanka

United Arab

Emirates

United Arab

Emirates

United Arab

Emirates

United Arab

Emirates Sri Lanka

United Arab

Emirates Sri Lanka Sri Lanka Sri Lanka

Nepal Bahamas, The Pakistan Pakistan Pakistan Philippines

INDIA’S TII

Bangladesh

Year

Market's Export

from India of 6

digit

Market's

Export from

India of 2 digit

Market's Export

from World 6

digit

Market's Export

from World 2

digit

TII

2003 42934.665 73682.946 42934.665 169098.842 2.29

2004 76359.206 111562.055 76359.206 203002.386 1.81

2005 61870.719 131809.635 61870.719 209632.394 1.59

2006 71719.077 123763.658 71719.077 262692.466 2.12

2007 88026.852 105162.724 88026.852 339348.18 3.22

2008 133666.527 137560.889 133666.527 265463.202 1.92

Malaysia

Year

Market's Export

from India of 6

digit

Market's

Export from

India of 2 digit

Market's Export

from World 6

digit

Market's Export

from World 2

digit

TII

2003 31546.457 33894.73 50110.925 191542.012 3.55

2004 31644.749 33596.562 55232.94 227554.997 3.88

2005 35465.906 43444.411 64986.826 266132.631 3.34

2006 54865.894 62071.292 81848.591 353317.254 3.81

2007 52359.406 54398.383 94874.985 389454.313 3.95

2008 67818.733 69328.153 91988.354 390391.838 4.15

138

United Arab Emirates

Year

Market's Export

from India of 6

digit

Market's

Export from

India of 2 digit

Market's Export

from World 6

digit

Market's Export

from World 2

digit

TII

2003 13033.242 27077.266 19070.617 172167.992 4.34

2004 21166.311 40922.252 26996.229 179877.944 3.44

2005 15630.118 41197.899 21518.415 257031.925 4.53

2006 34311.771 81988.955 38248.562 363027.674 3.97

2007 46846.066 91305.676 56276.237 426330.857 3.88

2008 39287.293 84930.633 44447.69 460260.239 4.79

Pakistan

Year

Market's Export

from India of 6

digit

Market's

Export from

India of 2 digit

Market's Export

from World 6

digit

Market's Export

from World 2

digit

TII

2003 779.987 52.317 58586.399 0

2004 1.72 2200.907 3.998 73272.47 14.32

2005 6351.49 28304.464 6568.336 139344.475 4.76

2006 16080.538 34635.066 19035.201 219060.309 5.34

2007 5611.22 53127.752 5701.565 186495.373 3.45

2008 4570.244 68818.789 4600.001 202686.982 2.92

COMPETITOR’S TII

Competitor's export to market World's Export to market

Bangladesh Radish Total Agri Radish Total Agri TII

India 133666.527 137560.889 133666.527 265463.202 1.92

Turkey 171.6 305.115 133666.527 265463.202 1.11

Thailand 0.089 499.413 133666.527 265463.202 0.0003

Malaysia Radish Total Agri Radish Total Agri TII

India 67818.733 69328.153 91988.354 390391.838 4.15

Netherlands 10443.261 11966.943 91988.354 390391.838 3.70

China 6740.486 231863.702 91988.354 390391.838 0.12

UAE Radish Total Agri Radish Total Agri TII

India 39287.293 84930.633 44447.69 460260.239 4.79

Pakistan 2482.421 6894.893 44447.69 460260.239 3.72

Egypt 908.335 23847.943 44447.69 460260.239 0.39

Pakistan Radish Total Agri Radish Total Agri TII

India 4570.244 68818.789 4600.001 202686.982 2.92

China 29.757 47682.79 4600.001 202686.982 0.027

India better off than other competing suppliers

139

RELATIVE COMPARATIVE ADVANTAGE

Bangladesh

Country’s export to market World's Export to market

Radish Total Agri Radish Total Agri RCE

India 133666.527 137560.889 133838.216 138365.417 1.004

Turkey 171.6 305.115 133838.216 138365.417 0.58

Thailand 0.089 499.413 133838.216 138365.417 0.00019

Malaysia

India 67818.733 69328.153 85002.48 313158.798 3.60

Netherlands 10443.261 11966.943 85002.48 313158.798 3.21

China 6740.486 231863.702 85002.48 313158.798 0.10

UAE

Country’s export to market World's Export to market

Radish Total Agri Radish Total Agri RCE

India 39287.293 84930.633 42678.049 115673.469 1.25

Pakistan 2482.421 6894.893 42678.049 115673.469 0.97

Egypt 908.335 23847.943 42678.049 115673.469 0.10

Pakistan

India 4570.244 68818.789 4600.001 116501.579 1.68

China 29.757 47682.79 4600.001 116501.579 0.015

Relative competitive advantage of India better off than these other suppliers in identified export

markets.

Tariff and Non Tariff barriers for Radish in Identified Markets

Other Tariff where ever

applicable Major

Markets

Import tariff

Tariff description

Tariff

rate

NTM

%

NTM

Statutory Rate 100%

Instructional

Surcharge 3% Bangladesh

25%

VAT 15%

0%

Malaysia 0% 100%

Testing, Inspection and Quarantine

Requirements

UAE 0% 0% 0% 0% -

Customs Duty 35%

Product Characteristics requirement

to protect humans

Pakistan

0%

Sales Tax

15%

100%

Labeling requirement to protect

human health

140

Presence of Special Safeguard Duty

Country Volume Trigger Price Trigger

Bangladesh NO NO

Malaysia NO NO

United Arab Emirates NO NO

Pakistan NO NO

Tariff Rate Quota Structure for Radish in major export destinations

Markets

TRQ Quantity (METRIC

TONS)

In quota -

Duty

Out Quota -

Duty

Bangladesh No No No

Malaysia No No No

UAE No No No

Pakistan No No No

SUBSIDIES

Markets Product Specific Non Product Specific Green Box S&D* Currency

Bangladesh Not Applicable 40.18 n/a n/a (billion Rp)

Malaysia n/a n/a 756 217 US$ million

United Arab Emirates n/a 34,00,000 90,00,000 US$ million

Pakistan 3.66 n/a n/a n/a * Special and Differential Treatment – Development Programs

Conclusion

Radish Exporters from Andhra Pradesh should majorly concentrate on finding the buyer in the order

of UAE first since the bilateral trade strength of UAE for Indian radish is much higher than that of

Malaysia and Pakistan. Also there is least competition in UAE from other suppliers and import duties

are also zero along with the absence of any type of non tariff barriers. Bangladesh on the other hand

has highest import duty levels along with other type of tariffs like Statutory Rate, Instructional

Surcharge and VAT. Malaysia has 100% SPS on all its 8 digit tariff lines along with ASEAN

preferential duty rates for other competing ASEAN countries and also special and differential

developmental subsidies due to which exporters from India/ AP would loose on the price

competitiveness.

141

Banana is one of the world’s most important food crops. In India, banana crop accounts for 2.8 per

cent of agricultural GDP. It is an important crop for subsistence farmers, and ensures year-round

security for food or income. Edible bananas are of two types—cooking bananas, known as plantations

which can be considered starchy vegetables, and the fruit bananas.

Developed countries are the destination for export of bananas. Around onefifth of globally produced

bananas are exported from the developing countries to the developed countries. Latin America and

Caribbean account for bulk of exports. Philippines is the only Asian country listed among top

exporters of banana in the world. Though India is the largest producer of bananas in the world with a

whopping 23 per cent share, the country’s international banana exports are negligible.

Although one-third of the total fruit production in India constitute banana, its share in the world

banana exports is negligible, largely due to wastage (around 40%), poor handling and lack of proper

post harvest management. However, for banana, besides as a fresh fruit export, potential also lies in

exports in processed forms, and as fibre. Some of the processed food products that are increasingly

gaining importance in the domestic as well as international markets are banana wafers, banana figs,

banana pulp, banana juice and banana flour/powder.

Banana wafers and dehydrated ripe banana, popularly known as banana figs manufactured in the

small and cottage scale sectors are quite prevalent and popular as snack food. Demand for banana

powder and pulp is also increasing. Banana powder and pulp is largely used in the baking and

confectionery, and baby food industries.

Maharashtra accounts for 25% of banana production in India, followed by Tamil Nadu (20%), Gujarat

(15%), Karnataka (10%) and Andhra Pradesh (10%).

Banana [070990]Banana [070990]Banana [070990]Banana [070990]

142

Trend in Exports

There has been an increasing trend in the exports of 070990 with a CAGR of 29% over the period 2003-

08. It can be seen that the growth has been really high 2005-06 region as the export figures zoomed

from US$18.59 to US$44.06 which is a growth of a phenomenal 137%.

Table 1

Trend in Exports for 070990 (US$ mn)

Code 2003 2004 2005 2006 2007 2008 CAGR

70990 13.39 15.61 18.59 44.06 46.90 48.43 29%

RCA

The increasing trend is not just in the absolute values of the exports in this product category. The RCA

values reveal the increasing comparative advantage of Indian exports vis-à-vis World exports in

070990.

Table 2

Comparative Advantage of Banana

Year India's exports India's total exports World's exports World's total exports RCA

2003 13.39 324.57 1687.95 26665.51 0.65

2004 15.61 360.68 1859.40 30182.20 0.70

2005 18.59 570.05 2113.45 32319.23 0.50

2006 44.06 622.35 2596.00 37185.49 1.01

2007 46.90 632.88 2868.64 42938.02 1.11

2008 48.43 683.74 2458.22 39926.02 1.15

143

Major Export Destinations for Banana from AP

The top five destination which can be considered for banana exports are as follows:

• United Arab Emirates

• United Kingdom

• Qatar

• Kuwait

• Saudi Arabia

Table 3

Major Export Destinations for 070990

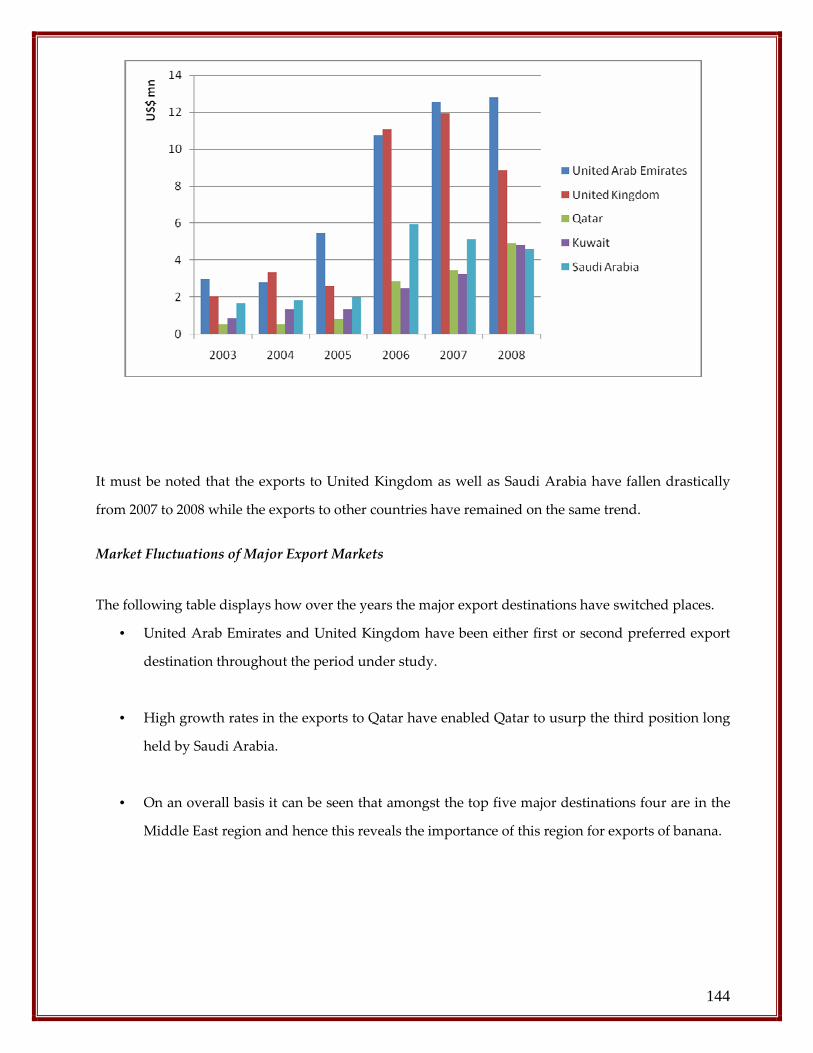

Partner Name 2003 2004 2005 2006 2007 2008 CAGR

United Arab Emirates 2963.438 2773.834 5450.86 10746.321 12550.616 12805.15 34.00

United Kingdom 1994.664 3310.981 2575.985 11045.761 11926.872 8862.032 34.75

Qatar 523.341 528.076 779.656 2850.179 3408.55 4923.197 56.56

Kuwait 830.003 1328.983 1325.037 2453.903 3237.871 4805.445 42.08

Saudi Arabia 1663.925 1795.211 1966.984 5915.536 5116.197 4581.459 22.45

These are the top 5 destinations according to the export figures of 2008 with exports to UAE leading

the pack with US$12.8 mn followed by exports to United Kingdom at US$8.86 mn. However, it must

be noted that over five years the CAGR value stand highest for Qatar at 56.56% where the exports

have grown from US$0.52 mn to US$4.9 mn surpassing Kuwait and Saudi Arabia which have grown

at 42.08% and 22.45% respectively.

144

It must be noted that the exports to United Kingdom as well as Saudi Arabia have fallen drastically

from 2007 to 2008 while the exports to other countries have remained on the same trend.

Market Fluctuations of Major Export Markets

The following table displays how over the years the major export destinations have switched places.

• United Arab Emirates and United Kingdom have been either first or second preferred export

destination throughout the period under study.

• High growth rates in the exports to Qatar have enabled Qatar to usurp the third position long

held by Saudi Arabia.

• On an overall basis it can be seen that amongst the top five major destinations four are in the

Middle East region and hence this reveals the importance of this region for exports of banana.

145

Market Fluctuation

2003 2004 2005 2006 2007 2008

United Arab

Emirates

United

Kingdom

United Arab

Emirates

United

Kingdom

United Arab

Emirates

United Arab

Emirates

United

Kingdom

United Arab

Emirates

United

Kingdom

United Arab

Emirates

United

Kingdom

United

Kingdom

Saudi Arabia Saudi Arabia Saudi Arabia Saudi Arabia Saudi Arabia Qatar

Nepal Kuwait Bahrain Qatar Qatar Kuwait

Kuwait Nepal Kuwait Kuwait Kuwait Saudi Arabia

Trade Intensity Index for banana with respect to Major Export Markets

United Arab Emirates

The trade intensity index with UAE has been fairly stable over the years meeting an average of 1.3. As

can be seen from the figure below the trend has been fairly constant over the last few years.

146

United Kingdom

The trade intensity index with UK has been growing over the years touching a high of 4.19 in the year

2007 and 3.79 in 2008. As can be seen from the figure below the trend has been fairly increasing over

the last three years. Furthermore, if 2005 is regarded as an outlier year then the linear increase seems

to work out in this case.

Saudi Arabia

The trade intensity index with Saudi Arabia has been growing over the years touching a high of 5.80

in the year 2007 and 5.15 in 2008. This TII is highest amongst other market destinations. As can be seen

from the figure below the trend has been fairly increasing over the last few years.

147

Qatar

The trade intensity index with Qatar has been growing over the years with 2008 having a higher TII of

2.83 than 2007 which is contrary to the trends seen in other export destinations. As can be seen from

the figure below the trend has been fairly increasing over the last three years.

Kuwait

The trade intensity index with Kuwait has grown steeply over the last few years with 2008 having a

very high TII of 4.14 which is much more than the average TII of 1.77 seen over the last five years.

148

Competitor Analysis

The following table lists down the five major competitors considered for each of the markets. The

competitors have been chosen according to their vicinity to the Indian export figures to these markets

as we consider these countries more intense rivals to the position of India.

We further saw as to what is the current market share of Indian exports in each of these destinations

(as can be seen from the table below). It can be seen that Indian exports command highest market

share in the Kuwait market at 43% approximately followed by 33% and 34% in Qatar and Saudi

Arabia respectively. It is however in the UK market that it commands a very small 2.41% of market

share showing an immense potential that lies in the UK market which Indian exports can tap.

UAE UK Saudi Arabia Qatar Kuwait

24.21% 2.41% 33.70% 32.88% 42.79%

2004 2005 2006 2007 2008

UAE UK Saudi Arabia Qatar Kuwait

Netherlands Kenya Greece Netherlands Netherlands

Egypt, Arab Rep. France Egypt, Arab Rep. United Arab Emirates Egypt, Arab Rep.

Thailand Netherlands Netherlands France Sri Lanka

France Cyprus Jordan Egypt, Arab Rep. United States

Kenya Panama Sri Lanka Sri Lanka United Arab Emirates

149

Trade Intensity Index of Competitors

United Arab Emirates

Four out of the five major competitors have very high TII values when compared to the TII value that

India holds in respect to the United Arab Emirates. While India has a TII value of 1.3 for the current

year its competitors stand in the range of 5.8 to 7.3 and hence this shows that it would be tough for

India to penetrate the UAE market with these competitors standing in the way.

United Kingdom

For this country, the two competitors having a TII more than India are Kenya and Panama. 85%

of the Kenyan exports to UK in the 07 category are for the product 070990. And hence the very high

value for the TII between Kenya and UK. On the other hand, Panama’s export of Product 070990 to

UK stands comparable to India and thus is the closest competitor.

150

Saudi Arabia

The two major competitors that have a very high TII with Saudi Arabia are Greece and Jordan with the

values of 19.87 and 14.31 respectively which stands much higher than the TII value of 5.15 that India

holds with respect to Saudi Arabia.

Qatar

Three major competitors have TII higher than that of India namely, Netherlands, France and

Sri Lanka that hold the values of 2.95, 3.80 and 4.37 respectively as in comparison to the 2.83 that India

holds in the product category 070990 with respect to Qatar.

151

Kuwait

India stand second highest amongst all its competitors to the export market of Kuwait with the TII

value of 4.14 being slightly behind than that of Netherlands which has a TII value of 4.49. Hence,

clearly India has a steadily strengthened its position in the Kuwait market accompanies with the rising

trend in exports as well as the rising TII values of the years.

Relative Competitive Advantage for 070990 vis-à-vis other Suppliers in Major Markets in 2008

United Arab Emirates

India has one of the least Relative competitive advantage vis-à-vis the other competitors. It has an RCE

value of 0.5 as compared to an average 2.48 RCE value shared by Netherlands, Thailand, France and

Kenya. (See the RCE table attached in the appendix)

United Kingdom

India has an RCE value of 2.73 and stands third in the overall ranking behind Kenya and Panama with

4.96 and 4.26 respectively. It must be noted that both the countries also have higher TII values than

India for this export destination.

152

Saudi Arabia

For this market, India has an RCE value of 2.96 which stand much lower than the value of 11.83 that

Greece.

Qatar

For this market, India has an RCE value of 1.36 as compared to 2.36 that Sri Lanka holds and 2.05 that

France holds.

Kuwait

India has the 2nd highest RCE value of 2.83 in this market after Netherlands which holds an RCE value

of 3.52 and thus is similar to the trend that we say while calculating TII of India’s competitors with

respect to Kuwait.

153

Tariff and Non Tariff barriers for Banana in Identified Markets

Major

Markets

Import

tariff

Other Tariff where ever

applicable

NTM

%

NTM

Tariff

description

Tariff

rate

UAE NA NA NA NA

UK NA NA NA NA

Saudi

Arabia

MFN Rates 12.00% 100% Testing, Inspection or quarantine

requirements

Qatar NA NA NA NA

Kuwait NA NA NA NA

Amongst the five destination markets namely, UAE, UK, Qatar, Saudi Arabia and Kuwait it was seen

that the only country that which has import tariff applicable is that of Saudi Arabia. Saudi Arabia

applies a MFN rate of 12% to the imports under this category of products. It is also the only country

amongst the lot to have 100% Non tariff mechanism which it applies to the “Testing, Inspection or

quarantine requirements”

FTA/PTA

Amongst the five destination markets namely, UAE, UK, Qatar, Saudi Arabia and Kuwait, India does

not hold any Free Trade or Preferential Trade agreement with any of them.

Country FTA/PTA Rate

UAE None -

UK None -

Saudi Arabia None -

Qatar None -

Kuwait None -

154

Tariff Rate Quota Structure in major export destinations

No tariff quotas are applied in any of the export destinations for product 070990.

Tariff Rate Quota Structure of 070990 in major export destinations

Markets TRQ Quantity (METRIC TONS) In quota - Duty Out Quota - Duty

UAE No No No

UK No No No

Saudi Arabia No No No

Qatar No No No

Kuwait No No No

Presence of Special Safeguard Duty

No Special safeguard duty is present in any of the export destinations for product 070990.

Presence of Special Safeguard Duty

Country Volume Trigger

Price

Trigger

UAE NO NO

UK NO NO

Saudi

Arabia NO NO

Qatar NO NO

Kuwait NO NO

Subsidy Structure

While none of the markets have product specific subsidies applicable. It must be noted that UK and

Saudi Arabia have Non Product Specific subsidies existing. In the case of UK, the NPS subsidies have

been taken as applicable to the notifications sent by the EEC.

Markets Non

Product

Specific

Green Box Special and

Differential

Treatment –

"Development

Programs"

Currency Year

UAE 0 3400000 9.000,000 (Dh) 2000/01

UK 728.4 22130.3 21520.8 Mio ECU 1996/97

Saudi Arabia 838.4 674.296 0 (mn SRls) 2006

Qatar 0 0 0 Rial 2004

Kuwait 0 0 0 Dinar -

155

Green Box subsidies are applicable to UAE, UK as well as Saudi Arabia and do not exist in either

Qatar or Kuwait. It must be noted that Kuwait and Qatar are the regions also where Indian exports

have faced highest growth over last 5 years.

Strategy for Promotion of Banana Export from Andhra Pradesh

Of course, the shipping companies are offering service in the form of refrigerated containers for

banana exporters. The specialised containers would enable farmers to transport the produce from

farms to international destinations, while increasing the shelf-life of bananas up to three weeks. Reefer

containers provide a cost-effective logistics solution for fruits and other perishables. Banana

cultivation is facing problems like non-availability of standardised, good-quality planting material and

quality certification of plant material. Though banana is a highly perishable crop, currently no

insurance facility is available for farmers. Air tariffs for banana are also very high. There is an urgent

need for standardisation, certification and rapid multiplication for yielding good-quality material

through tissue culture. Through tissue culture, it would be possible to multiply government

assistance, tissue-culture companies can achieve economies of scale and this can bring down the cost

of planting materials. The insurance facility for farmers is also important. There are centers for

research in banana in Andhra Pradesh which can further be developed for these purposes.

156

Appendix

Table 4: Trade Intensity Index for Banana with respect to Major Export Markets

India's export World Export

Year 070990 07 070990 07 TII

2003 2.96 33.01 12.91 178.11 1.24

2004 2.77 37.20 13.50 176.16 0.97

2005 5.45 44.74 22.64 260.58 1.40

2006 10.75 97.45 32.27 378.46 1.29

2007 12.55 91.31 44.18 426.33 1.33

TII UAE

2008 12.81 84.93 52.90 460.41 1.31

India's export World Export

Year 070990 07 070990 07 TII

2003 1.99 10.79 221.79 2481.69 2.07

2004 3.31 13.84 253.77 2811.19 2.65

2005 2.58 14.17 309.47 3076.26 1.81

2006 11.05 26.90 390.40 3468.52 3.65

2007 11.93 23.47 472.83 3885.75 4.18

TII UK

2008 8.86 18.94 368.17 2979.97 3.79

India's export World Export

Year 070990 07 070990 07 TII

2003 1.66 11.35 10.35 106.38 1.51

2004 1.80 12.28 14.02 130.29 1.36

2005 1.97 14.52 14.16 142.57 1.36

2006 5.92 19.72 17.75 277.54 4.69

2007 5.12 18.13 17.03 349.81 5.80

TII Saudi Arabia

2008 4.58 18.30 13.59 279.75 5.15

India's export World Export

Year 070990 07 070990 07 TII

2003 0.52 2.06 8.45 31.31 0.94

2004 0.53 2.92 4.82 35.15 1.32

2005 0.78 4.30 13.22 45.17 0.62

2006 2.85 7.26 10.71 56.28 2.06

2007 3.41 6.70 16.20 73.89 2.32

TII Qatar

2008 4.92 8.68 14.97 74.40 2.82

India's export World Export

Year 070990 07 070990 07 TII

2003 0.83 5.20 7.89 68.09 1.38

2004 1.33 7.43 7.44 70.03 1.68

2005 1.33 9.62 24.10 91.55 0.52

2006 2.45 12.03 21.92 122.72 1.14

2007 3.24 10.57 23.06 132.19 1.76

TII Kuwait

2008 4.81 12.05 11.23 116.52 4.14

157

TII with other suppliers

UAE Competitor 's

export of 070990

Competitors's

Total Export of 07

World 's export of

070990

World 's export

of 07

TII

Netherlands 22.84 34.19 52.90 457.70 5.78

Egypt, Arab

Rep.

3.53 23.85 52.90 457.70 1.28

Thailand 3.05 4.10 52.90 457.70 6.44

France 2.84 4.05 52.90 457.70 6.06

Kenya 2.51 2.98 52.90 457.70 7.27

UK Competitor 's

export of 070990

Competitors's

Total Export of 07

World 's export of

070990

World 's export

of 07

TII

Kenya 151.81 178.52 368.17 2837.48 6.55

France 58.68 290.27 368.17 2837.48 1.56

Netherlands 29.84 1038.86 368.17 2837.48 0.22

Cyprus 10.40 27.79 368.17 2837.48 2.89

Panama 8.88 12.17 368.17 2837.48 5.62

Saudi

Arabia

Competitor 's

export of 070990

Competitors's

Total Export of 07

World 's export of

070990

World 's export

of 07

TII

Greece 4.08 4.08 13.59 270.04 19.87

Egypt, Arab

Rep.

2.62 69.64 13.59 270.04 0.75

Netherlands 0.76 21.90 13.59 270.04 0.69

Jordan 0.42 0.58 13.59 270.04 14.31

Sri Lanka 0.42 2.00 13.59 270.04 4.14

Qatar Competitor 's

export of 070990

Competitors's

Total Export of 07

World 's export of

070990

World 's export

of 07

TII

Netherlands 6.02 9.06 14.97 66.46 2.95

United Arab

Emirates

1.65 9.36 14.97 66.46 0.78

France 0.67 0.78 14.97 66.46 3.80

Egypt, Arab

Rep.

0.65 6.04 14.97 66.46 0.48

Sri Lanka 0.43 0.44 14.97 66.46 4.37

Kuwait Competitor 's

export of 070990

Competitors's

Total Export of 07

World 's export of

070990

World 's export

of 07

TII

Netherlands 3.44 6.94 11.23 101.77 4.49

Egypt, Arab

Rep.

1.68 18.69 11.23 101.77 0.81

Sri Lanka 0.45 1.21 11.23 101.77 3.40

United

States

0.36 8.29 11.23 101.77 0.39

UAE 0.21 8.48 11.23 101.77 0.22

158

Relative Competitive Advantage for 070990 vis-à-vis other Suppliers in Major Markets in 2008

UAE Competitor 's

export of

070990

Competitors's

Total Export of

07

All Competitor

's Export of

070990

All

Competitor 's

Export of 07

Rel.

Comp.

Adv.

Netherlands 22.84 34.19 47.57 154.10 2.16

India 12.81 84.93 47.57 154.10 0.49

Egypt, Arab

Rep.

3.53 23.85 47.57 154.10 0.48

Thailand 3.05 4.10 47.57 154.10 2.41

France 2.84 4.05 47.57 154.10 2.27

Kenya 2.51 2.98 47.57 154.10 2.72

UK Competitor 's

export of

070990

Competitors's

Total Export of

07

All Competitor

's Export of

070990

All

Competitor 's

Export of 07

Rel.

Comp.

Adv.

Kenya 151.81 178.52 268.48 1566.55 4.96

France 58.68 290.27 268.48 1566.55 1.18

Netherlands 29.84 1038.86 268.48 1566.55 0.17

Cyprus 10.40 27.79 268.48 1566.55 2.18

Panama 8.88 12.17 268.48 1566.55 4.26

India 8.86 18.94 268.48 1566.55 2.73

Saudi

Arabia

Competitor 's

export of

070990

Competitor’s

Total Export of

07

All Competitor

's Export of

070990

All

Competitor 's

Export of 07

Rel.

Comp.

Adv.

India 4.58 18.30 8.30 98.20 2.96

Greece 4.08 4.08 8.30 98.20 11.83

Egypt, Arab

Rep.

2.62 69.64 8.30 98.20 0.45

Netherlands 0.76 21.90 8.30 98.20 0.41

Jordan 0.42 0.58 8.30 98.20 8.52

Sri Lanka 0.42 2.00 8.30 98.20 2.47

Qatar Competitor 's

export of

070990

Competitors's

Total Export of

07

All Competitor

's Export of

070990

All

Competitor 's

Export of 07

Rel.

Comp.

Adv.

Netherlands 6.02 9.06 14.35 34.36 1.59

India 4.92 8.68 14.35 34.36 1.36

United

Arab

Emirates

1.65 9.36 14.35 34.36 0.42

France 0.67 0.78 14.35 34.36 2.05

Egypt, Arab

Rep.

0.65 6.04 14.35 34.36 0.26

Sri Lanka 0.43 0.44 14.35 34.36 2.36

159

Kuwait Competitor 's

export of

070990

Competitors's

Total Export of

07

All Competitor

's Export of

070990

All

Competitor 's

Export of 07

Rel.

Comp.

Adv.

India 4.81 12.05 6.14 43.60 2.83

Netherlands 3.44 6.94 6.14 43.60 3.52

Egypt, Arab

Rep.

1.68 18.69 6.14 43.60 0.64

Sri Lanka 0.45 1.21 6.14 43.60 2.66

United

States

0.36 8.29 6.14 43.60 0.31

United

Arab

Emirates

0.21 8.48 6.14 43.60 0.17

160

GGGGrape cultivation is one of the most remunerative farming enterprises in India. Grapes occupies fifth

position amongst fruit crops with cultivation of over an area of 34,000 hectares and production of 1.08

MT from an area of 0.04 Million ha. Grape is grown under a variety of soil and climatic conditions in

three distinct agro-climatic zones, namely, sub-tropical, hot tropical and mild tropical climatic regions

in India. The major varieties of grapes grown in India are, Thomson Seedless, Sonaka, Anab-e-Shahi,

Perlette, Banglore blue, Pusa seedless, Beauty seedless etc. Maharashtra occupies the first position

with a production of 0.68 MT of grapes, followed by Karnataka. Andhra Pradesh

The Chittoor is the major district in the mid tropical region where the Grapes are grown in Andhra

Pradesh. Besides, in the hot tropical region in Andhra Pradesh, Grapes are grown in around 10,000

acres in the state in the districts of Ranga Reddy, Medak and parts of Mahbubnagar districts as

compared to approximately one lakh acre in Maharashtra. Although Andhra Pradesh falls behind MS

and Karnataka in grape production, but still this is a major fruit for the state in terms of rural

population dependent on it. Though grapes are grown in Chittoor and Anantapur districts also, the

seed variety, Dilkush or Sharad, or seedless Taj Ganesh are mainly meant for domestic consumption.

Therefore this section of the report tries to explore the export prospects of the grapes and raisins from

AP and assists grape exporters to identify right markets for their fresh and processed grapes. The

section also suggests strategies for export development of grapes from the state.

Grapes [080610]Grapes [080610]Grapes [080610]Grapes [080610]

161

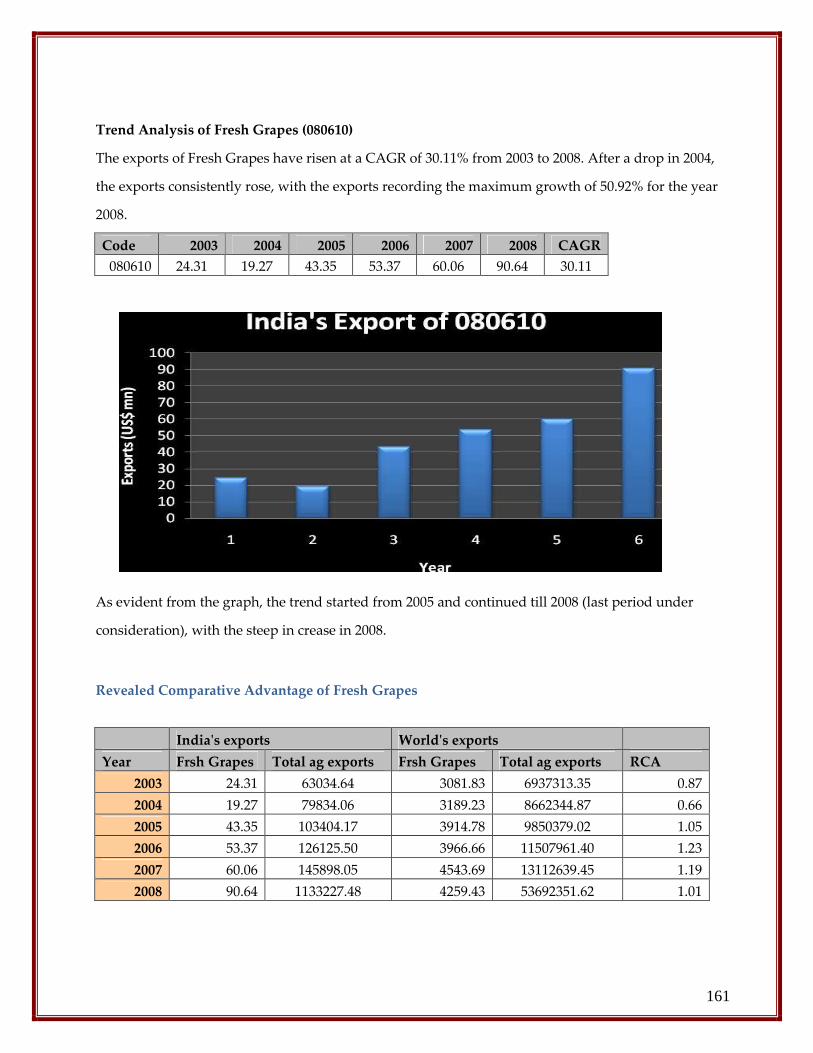

Trend Analysis of Fresh Grapes (080610)

The exports of Fresh Grapes have risen at a CAGR of 30.11% from 2003 to 2008. After a drop in 2004,

the exports consistently rose, with the exports recording the maximum growth of 50.92% for the year

2008.

Code 2003 2004 2005 2006 2007 2008 CAGR

080610 24.31 19.27 43.35 53.37 60.06 90.64 30.11

As evident from the graph, the trend started from 2005 and continued till 2008 (last period under

consideration), with the steep in crease in 2008.

Revealed Comparative Advantage of Fresh Grapes

India's exports World's exports

Year Frsh Grapes Total ag exports Frsh Grapes Total ag exports RCA

2003 24.31 63034.64 3081.83 6937313.35 0.87

2004 19.27 79834.06 3189.23 8662344.87 0.66

2005 43.35 103404.17 3914.78 9850379.02 1.05

2006 53.37 126125.50 3966.66 11507961.40 1.23

2007 60.06 145898.05 4543.69 13112639.45 1.19

2008 90.64 1133227.48 4259.43 53692351.62 1.01

162

Figure 5 RCA for 080610

As for the figures depicted above, India gained competitiveness in the Fresh Grapes market in the

world, post 2005 when its RCA value increased from 0.66 in 2004 to 2005. Since then, India has

displayed revealed comparative advantage in the exports of grapes consistently, with the figure

dropping to 1.01 by the end of 2008.

Major Export Destinations for Fresh Grapes

Approximately, 2.5 percent (22,000 t) of fresh grapes are exported to the Middle East and European

countries as of now. This section will explore the possibilities of export market diversification for

grape and raisin export from Andhra Pradesh.

Partner Name 2003 2004 2005 2006 2007 2008 CAGR

Bangladesh 142.02 606.548 2587.443 4764.899 8652.273 11446.371 140.58

Belgium 250.429 826.032 1070.448 3317.478 2625.527 855.591 27.85

Netherlands 5090.784 3853.734 14486.334 17164.885 18156.255 39639.126 50.75

United Arab

Emirates 4256.413 4679.273 7174.752 7750.402 7302.237 10096.385 18.86

United Kingdom 8828.144 5146.036 13054.562 13388.332 15354.358 18479.821 15.92

163

Of the major Export Destinations as depicted above, the exports to Bangladesh increased the most

over the period under review. In absolute terms, Netherlands is the biggest importer of Indian Fresh

Grapes. Belgium seems to be unattractive considering the low value of exports to it compared to the

other export destinations.

Below is the depiction of the market fluctuation in terms of value of exports of fresh grapes from India

to the markets.

Market Fluctuations of Major Export Markets

2003 2004 2005 2006 2007 2008

United

Kingdom

United

Kingdom Netherlands Netherlands Netherlands Netherlands

Netherlands

United Arab

Emirates

United

Kingdom

United

Kingdom

United

Kingdom

United

Kingdom

United Arab

Emirates Netherlands

United Arab

Emirates

United Arab

Emirates Bangladesh Bangladesh

Belgium Belgium Bangladesh Bangladesh

United Arab

Emirates

United Arab

Emirates

Bangladesh Bangladesh Belgium Belgium Belgium Belgium

United Kingdom slipped from the top export market in 2003 to second most attractive destination in

terms of value of exports. Going by value of exports Netherlands with the CAGR of 50.75% from 2003

to 2008 emerged as the top export destination for Indian Fresh Grapes. As for other destinations,

Bangladesh increased its attractiveness whereas decline in exports to Saudi Arabia pushed it to

number 4 slot in terms of value of exports during 2008.

Trade IntenTrade IntenTrade IntenTrade Intensity Index with Major Marketssity Index with Major Marketssity Index with Major Marketssity Index with Major Markets

Bangladesh India's export World Export

Year Frsh Grapes Total ag exports Frsh Grapes Total ag exports TII

2003 142.02 20338.352 2159.881 41502.423 0.13

2004 606.548 27040.788 3215.784 54362.305 0.38

2005 2587.443 25542.659 5373.14 64872.992 1.22

2006 4764.899 33787.354 7673.077 65795.779 1.21

2007 8652.273 29083.696 11546.96 81721.554 2.11

2008 11446.371 43839.99 15810.397 113599.879 1.88

India’s Trade Intensity Index (TII) with Bangladesh increased consistently peaking in 2007 before

falling to 1.88 in 2008.

164

Belgium

India's export World Export

Year Frsh Grapes

Total ag

exports Frsh Grapes

Total ag

exports TII

2003 250.429 8169.36 107596.499 1285353.66 0.37

2004 826.032 12840.373 118383.583 1526669.706 0.83

2005 1070.448 15715.967 141525.514 1796771.385 0.86

2006 3317.478 14946.813 136124.459 1878577.794 3.06

2007 2625.527 15344.177 135141.98 2012330.922 2.55

2008 855.591 16522.208 147026.894 1944817.771 0.68

India’s TII with Belgium decreased implying that India as a partner in exports of 080610 as compared

to the rest of the world has weakened over the period under review.

Netherlands India's export World Export

Year Frsh Grapes

Total ag

exports Frsh Grapes

Total ag

exports TII

2003 5090.784 58401.15 240595.484 2153122.327 0.78

2004 3853.734 76329.219 284926.349 2568617.022 0.46

2005 14486.334 124295.9 367960.022 3044976.206 0.96

2006 17164.885 132910.994 355062.15 3309568.527 1.20

2007 18156.255 113752.627 413969.945 3830359.157 1.48

2008 39639.126 158211.567 392881.319 3279036.797 2.09