Embed Size (px)

Citation preview

FROM NATURE TO YOU

H1 2017 RESULTS14 September 2017

Paris

2

Agenda

H1 highlightsA first-half focused on simplification and execution

H1 2017 resultsIn line with our roadmap

Developments and outlookActivating growth drivers

1.

2.

3.

3

On track for delivering Bright2020 CARE - EXECUTE - GROW

Focus and disciplineGovernance

2015

First levers for profitability

2016

Focus on the product portfolio and the business

project portfolio

2017

4

H1 2017 financial highlights

Acceleration ofsimplification measures

€207.5mSales

€34.5m16.6%EBITDA(% of sales)

Emergingmarkets

40.5%

NPD6%

Inventory-to-salesratio

22.2%

5

H1 HIGHLIGHTS

A first-half focused on simplification and execution

6

Progress in our priority lines of actionCare: People & Pathfinder

Focus on safety

Managing talent

Promoting the adoption of our culture

Increasing ownership of the Pathfinder programme

Improving our environmental footprint

CAREPeople & Culture Sustainable Development

Strongengagement

Performancedriver

Creatingvalue

7

Progress in our priority lines of actionExecute: Simplification and efficacy

Reducing complexity

Lean Management

Global management of indirect procurement

Improving Working Capital Requirements

EXECUTE

Reductionin the number

of SKUs

Improvingprocesses

and internal flows

Implementingan S&OP strategy

8SteerVision Center™ is a registered trademark of Ka Maté Strategy

La SteerVision Center™Steering the Bright2020 strategy

Steering theBright2020

strategy

Decision-making and

implementation of these

decisions

Monitoringand control

of the operations

Involvement of all Directions

9

Analysis of causes and estimates of forecasts

WARNING: Red Graph ESTIMATED FORECASTS: Orange Graph

Action planbased on the Root Causes

TEAM WORKAnalysis of the Root Causes

of Pareto

10

Analysis of causes and estimates of forecasts

WARNING: Red Graph

Action planbased on the Root Causes

TEAM WORKAnalysis of the Root Causes

of Pareto

11

Stronger foundations

The roadmap has been charted

The execution plans have been implemented

12

H1 2017RESULTS

In line with our roadmap

13

H1 2017 financial highlights

€207.5m

REVENUE

(current exch. rates)-0.3%

EBITDA*

NET INCOME

€10.7m5.1%(% of sales)

ACCOUNTSRECEIVABLE

53DSO

INVENTORY-TO-SALESRATIO

40.5%

* Recurring operating EBITDA

16.6%(% of sales)

€34.5m

(current exchange rates)

14

H12017

Revenue 207.5 208.0 -0.3%

Gross margin on COGS 59.4 57.8 +2.8%

Gross margin on COGS (%) 28.7% 27.8%

Recurring operating EBITDA 34.5 33.2 +3.8%

Recurring operating EBITDA margin (%) 16.6% 16.0%

Current operating income 18.1 18.6 -2.6%

Current operating margin (%) 8.7% 8.9%

Net operating income 17.5 19.1 -8.3%

Operating margin (%) 8.4% 9.2%

Net income attributableto Naturex shareholders 10.7 12.2 -12.7%

Net margin (%) 5.1% 5.9%

H12016

Change %

Income statement highlights

IFRSIn €m

REVENUEH1 2017

OPTIMISATION OF THE PRODUCT MIX

16

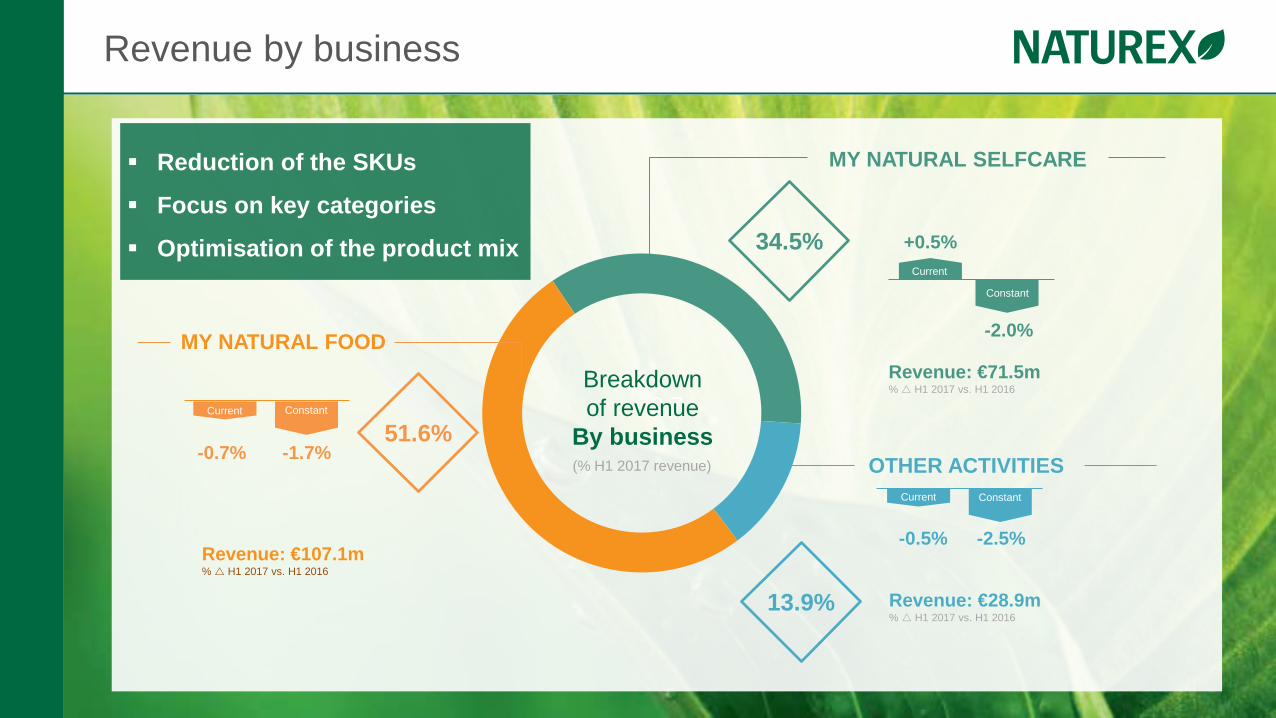

Revenue by business

0.7

MY NATURAL FOOD

MY NATURAL SELFCARE

Revenue: €107.1m% H1 2017 vs. H1 2016

Revenue: €71.5m% H1 2017 vs. H1 2016

OTHER ACTIVITIES

Revenue: €28.9m% H1 2017 vs. H1 2016

Breakdownof revenue

By business(% H1 2017 revenue)

51.6%

34.5%

13.9%

Reduction of the SKUs

Focus on key categories

Optimisation of the product mix

Current

-0.5% -2.5%

Constant

Current

+0.5%

-2.0%

Constant

-1.7%-0.7%

Current Constant

17

NorthAmerica

€91.4m

AsiaPacific

€31.6m

EuropeAfrica

Middle East

€69.8m

+25.1%

15.2%(% of sales)

-10.3%

33.7%(% of sales)

+0.5%

44.1%(% of sales)

Latin America

€14.6m

+4.1%

7.0%(% of sales)

Revenue by regionOur strong original organisation is impacted by the disparities and volatility of our markets

H1 2017 revenue Changes at current exchange ratesCurrency effect: €3.4m (Positive impact: USD and AUD. Negative impact: GBP)

OPERATING PROFITABILITY

Activating ourperformance drivers

19

Expenses by functionEffective cost-containment measures and the allocation of our resources

5.9

15.2

18.4

7.4

14.916.5

Research and Development Marketing and Sales General and Administrative

of sales2.8% 3.6%

of sales7.3%of sales

7.2%of sales

8.8%of sales

7.9%of sales

Accelerating innovation

Deployinga regional salesforce

Rationalisingthe support functions

Reductionin operating expenses

CHANGE IN EXPENSES BY FUNCTION(€m)

H1 2016 H1 2017

FINANCIALPOSITION

Focus and disciplinefor an improvedmanagement of our flows

21

Working capital requirementsImpact of the inventory categorisation process

DSO53 days

Inventories40.5%

of sales (favourable currency effect)

CHANGE IN WORKING CAPITAL REQUIREMENTS(€m)

186.1196.4

182.4

30.06.2016 31.12.2016 30.06.2017

46%of sales

45%of sales

49%of sales

22

HealthSafetyQualityEnvironment

15%

ExtensionGrowth33%

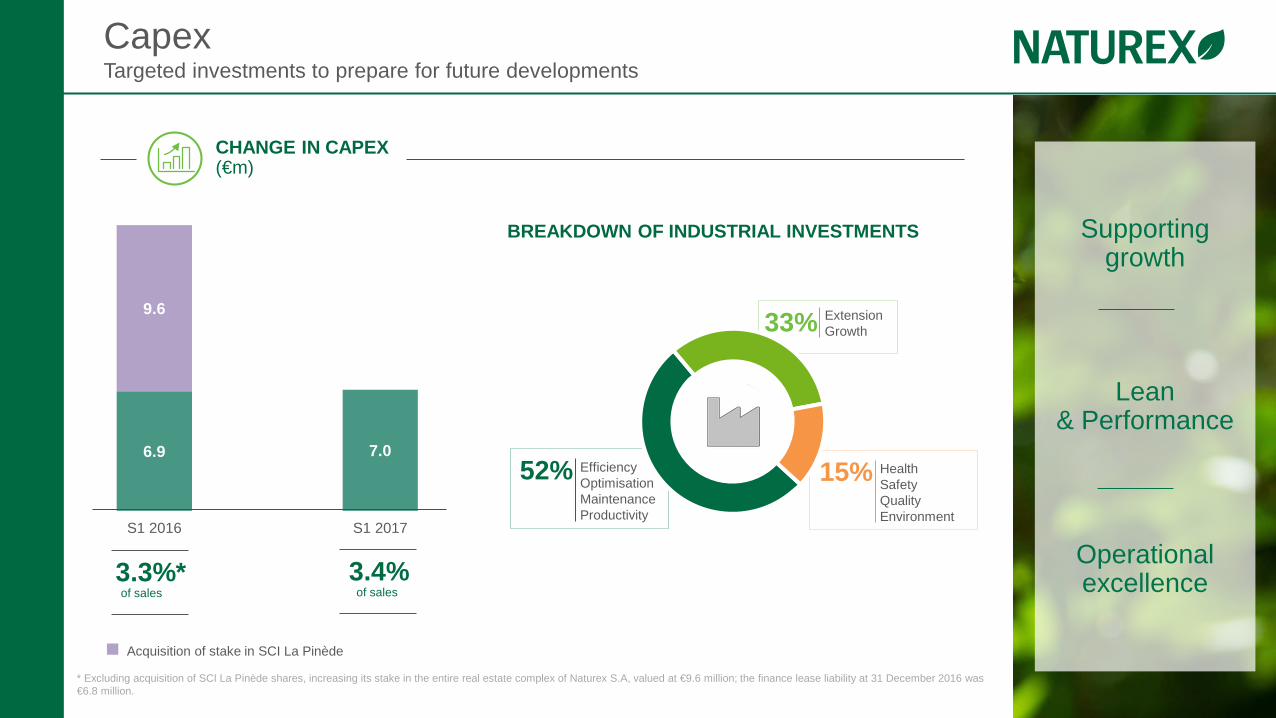

CapexTargeted investments to prepare for future developments

Supporting growth

Lean& Performance

Operational excellence

CHANGE IN CAPEX(€m)

6.9 7.0

9.6

S1 2016 S1 2017

Acquisition of stake in SCI La Pinède

BREAKDOWN OF INDUSTRIAL INVESTMENTS

* Excluding acquisition of SCI La Pinède shares, increasing its stake in the entire real estate complex of Naturex S.A, valued at €9.6 million; the finance lease liability at 31 December 2016 was €6.8 million.

3.3%*of sales

3.4%of sales

EfficiencyOptimisationMaintenanceProductivity

52%

23

CHANGE IN NET FINANCIAL DEBT(€m)

Net financial debt A new structured credit facility providing greater flexibility

173.9

147.0

31.12.2016 30.06.2017

Cost of the structured credit facility: 2.48%

Financial leverage: 2.34

vs. 2.83 at 31/12/2016

Gearing40.3%

vs. 46.7% at 31/12/2016

Bank covenants are respected

Maximum capacity€280m

Full amount repayable on

maturity

Maturityextendedto 2022

Increaseflexibility

24

An improving financial position

Controlled cost structureand well-managed WCR

Negotiation of financial capacitiesto prepare our future developments

25

DEVELOPMENTSAND OUTLOOK

Activatingthe growth engines

26

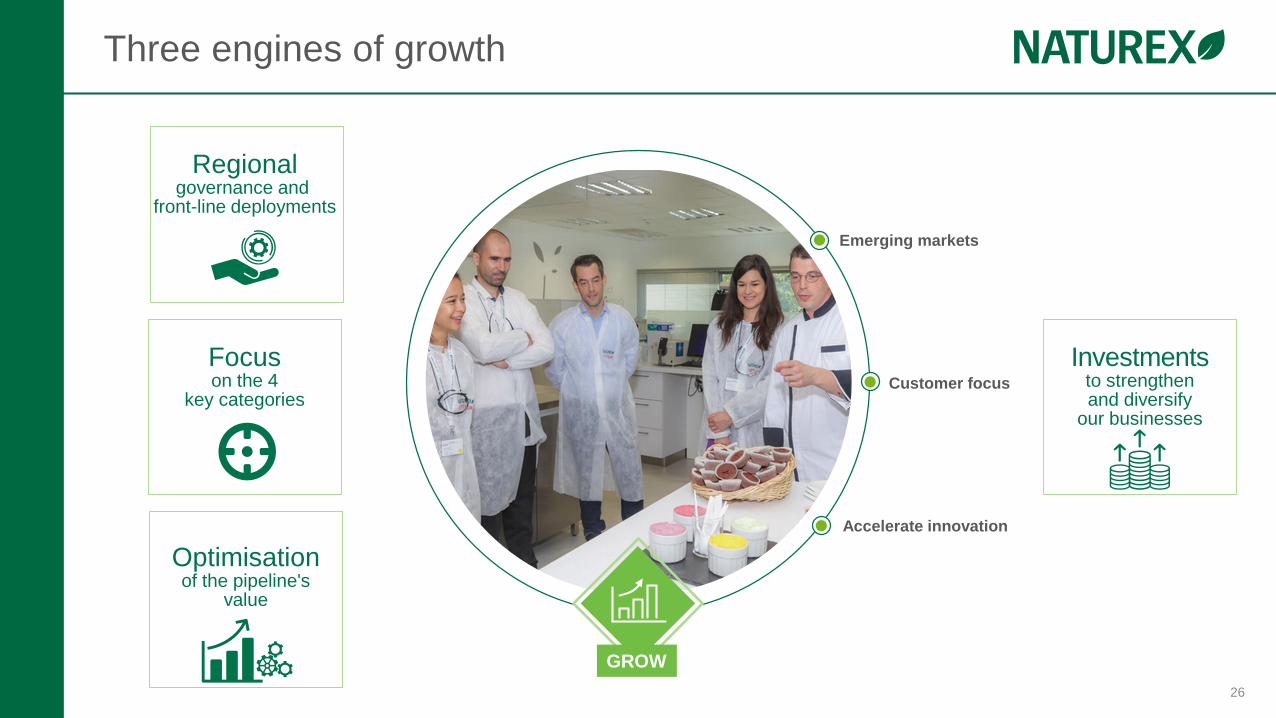

Three engines of growth

Emerging markets

Customer focus

Accelerate innovation

GROW

Regionalgovernance and

front-line deployments

Focuson the 4

key categories

Optimisationof the pipeline's

value

Investmentsto strengthenand diversify

our businesses

27

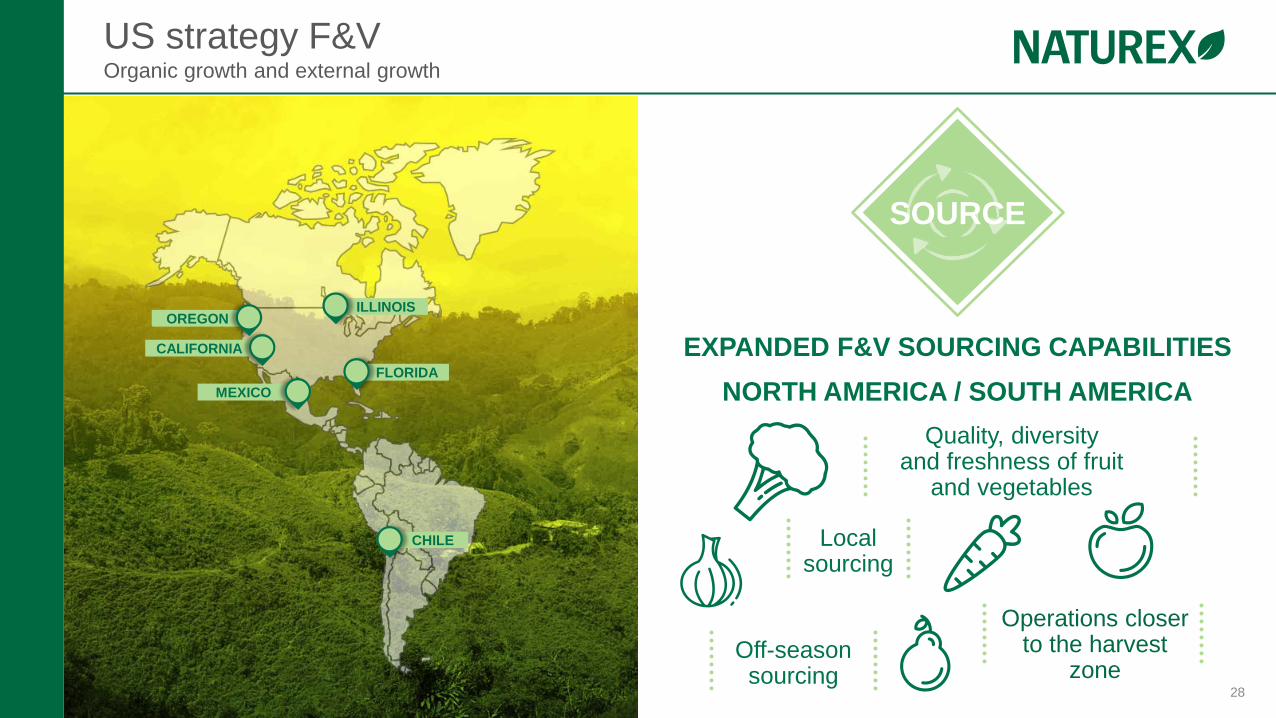

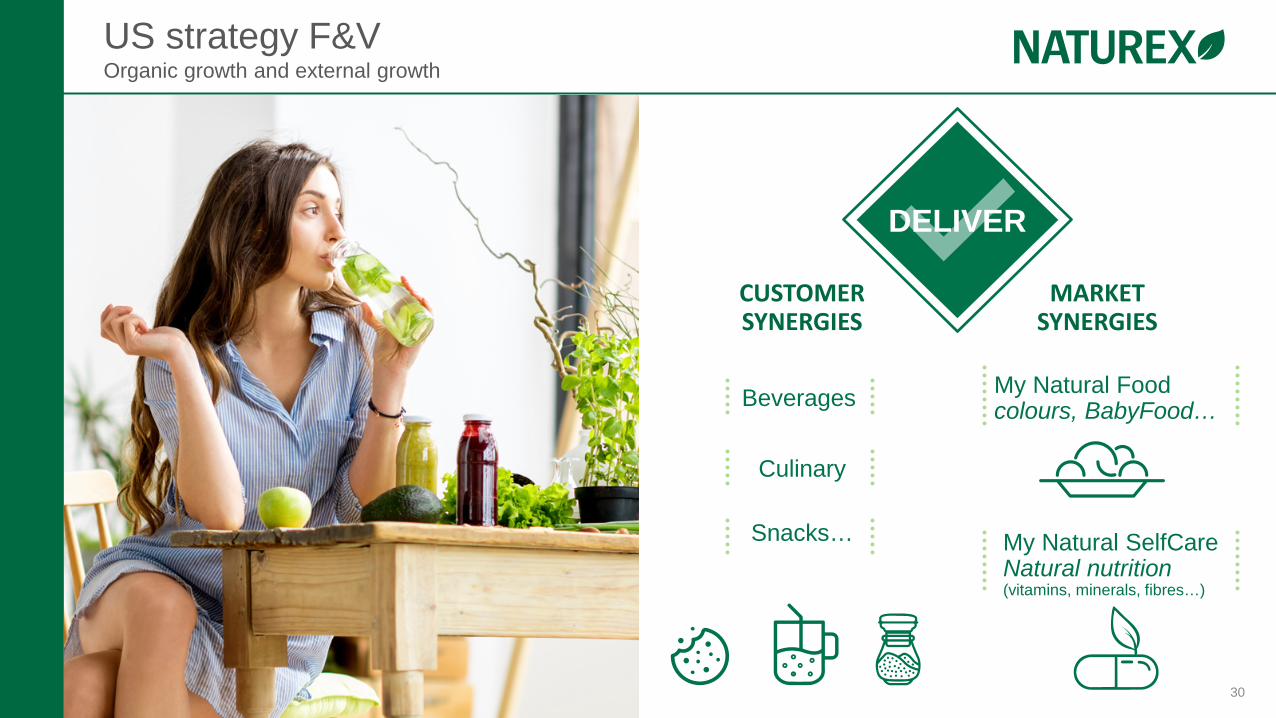

US strategy F&VOrganic growth and external growth

Acquisition of the selected industrial technologies and operations of Haliburton Intl Foods

Acquisition of new technologies Natural vegetable-based solutions

(purees, sauces, roasted veggies) Acquiring a new industrial footprint Exclusive negotiations to acquire business

and manufacturing operations in the US Natural fruit-based specialties

Drum dryer capabilities (VJI) Additional technology to transform

vegetable and fruit-based juices and purees into powder

Buyout of Chile Botanics' minority shareholders

Agreement to buy out their stake F&V off-season sourcing synergies

and development of application solutions

ORGANIC GROWTH EXTERNAL GROWTH

28

SOURCE

US strategy F&VOrganic growth and external growth

EXPANDED F&V SOURCING CAPABILITIESNORTH AMERICA / SOUTH AMERICA

CHILE

MEXICO

CALIFORNIA

OREGONILLINOIS

FLORIDA

Localsourcing

Quality, diversityand freshness of fruit

and vegetables

Off-seasonsourcing

Operations closerto the harvest

zone

29

CONVERT

Drum Dryer - India

US strategy F&VOrganic growth and external growth

3 TECHNOLOGIES

WetUnpasteurized Premium

Juice (UPJ) > liquid

RoastedRoasting

> roasted veggies

DryDryer

> powder

30

DELIVER

CUSTOMERSYNERGIES

My Natural SelfCareNatural nutrition(vitamins, minerals, fibres…)

US strategy F&VOrganic growth and external growth

MARKETSYNERGIES

My Natural Foodcolours, BabyFood…Beverages

Culinary

Snacks…

31

NEW NATURAL ANTIMICROBIAL SOLUTION FOR SAFETY AND CLEAN LABELS IN MEAT

Natural preservatives strategyOrganic growth

RosemaryAtlas Mountains, Morocco

Innovation de rupture

STRONG MARKET TRENDS IN FAVOROF NATURAL PRESERVATIVES

Naturalness Clean label Regulations

PROMOTING THE SHIFT FROM SYNTHETIC TO NATURAL Aligning our industrial capabilities with market

growth on rosemary Completing our range with antimicrobials Fostering breakthrough innovations

AcerolaAlternative to synthetic ascorbic acid

32

ChicagoIllinois - USA Birmingham

UK

AvignonFRANCE

Sao PauloBRAZIL Sydney

AUSTRALIA

MumbaiINDIA

MoscowRUSSIA

ShanghaiCHINA

FOOD & BEVERAGEPERSONAL CARE

Mexico CityMEXICO

Singapore

SpringlabsDriver of performance and differentiation

SUPPORTING THE SALE AND DEVLOPMENTOF THE PIPELINE OF SOLD BUSINESS PROJECTS Customer support and market expertise

Accelerating innovation and improving time-to-market

Promoting our technical expertise in natural ingredients Supporting the development of specific solutions

11 APPLICATION LABORATORIESTHROUGHOUT THE WORLD

Latest openings: Chicago (expansion), Mexico, Singapore Springlab Chicago

33

Diversifying our portfolio to expandand strengthen our presence in our markets

Bolster the commercial pipeline to create value

Investments to fueland accelerate our organic growth

34

Solid foundationsfor the compositionof the organic portfolio

Structural efforts appliedto the running operations

Regional organisationfor greater agility and better allocation of resources

Optimising our financing capacities in preparationfor future developments

Supporting momentum of key categories F&V: Organic growth + M&A

AOX: Organic growth

• Replicating the same strategic review process Colours and Phytoactives

• Focus on innovationand Open innovation

Growth dynamics

P H A S E 1 . P H A S E 2 .

SIMPLIFICATIONCOMPLETED

ENERGISING THECOMMERCIAL PIPELINE

Fully focused on executingour Bright2020 roadmap

Focus on the product portfolio and business pipeline

For a gradual returnto growth in H2 2017

FY 2017

THANK YOU

Q&A