Embed Size (px)

Citation preview

FOR INSTITUTIONAL/WHOLESALE/PROFESSIONAL CLIENTS AND QUALIFIED INVESTORS ONLY—NOT FOR RETAIL USE OR DISTRIBUTION

Frequently Asked Questions: European Money Market Fund Reform

J.P. Morgan Global LiquidityJanuary 2017

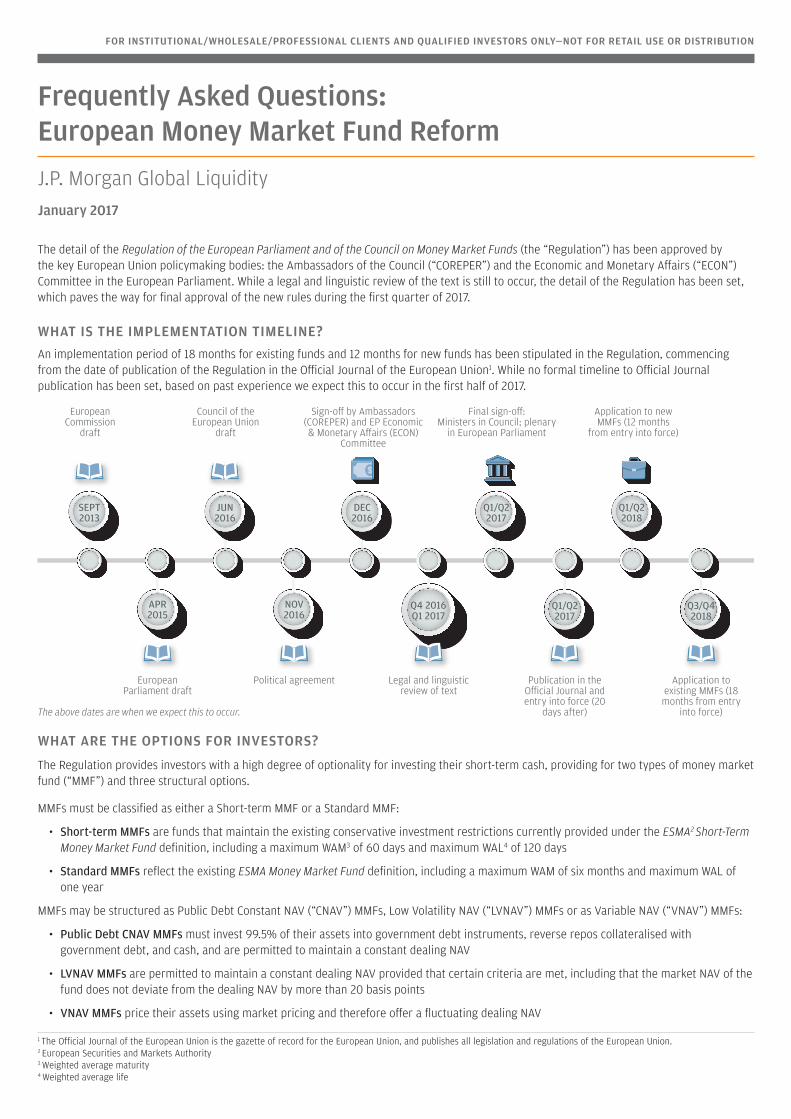

The detail of the Regulation of the European Parliament and of the Council on Money Market Funds (the “Regulation”) has been approved by the key European Union policymaking bodies: the Ambassadors of the Council (“COREPER”) and the Economic and Monetary Affairs (“ECON”) Committee in the European Parliament. While a legal and linguistic review of the text is still to occur, the detail of the Regulation has been set, which paves the way for final approval of the new rules during the first quarter of 2017.

WHAT IS THE IMPLEMENTATION TIMELINE?An implementation period of 18 months for existing funds and 12 months for new funds has been stipulated in the Regulation, commencing from the date of publication of the Regulation in the Official Journal of the European Union1. While no formal timeline to Official Journal publication has been set, based on past experience we expect this to occur in the first half of 2017.

WHAT ARE THE OPTIONS FOR INVESTORS?

The Regulation provides investors with a high degree of optionality for investing their short-term cash, providing for two types of money market fund (“MMF”) and three structural options.

MMFs must be classified as either a Short-term MMF or a Standard MMF:

• Short-term MMFs are funds that maintain the existing conservative investment restrictions currently provided under the ESMA2 Short-Term Money Market Fund definition, including a maximum WAM3 of 60 days and maximum WAL4 of 120 days

• Standard MMFs reflect the existing ESMA Money Market Fund definition, including a maximum WAM of six months and maximum WAL of one year

MMFs may be structured as Public Debt Constant NAV (“CNAV”) MMFs, Low Volatility NAV (“LVNAV”) MMFs or as Variable NAV (“VNAV”) MMFs:

• Public Debt CNAV MMFs must invest 99.5% of their assets into government debt instruments, reverse repos collateralised with government debt, and cash, and are permitted to maintain a constant dealing NAV

• LVNAV MMFs are permitted to maintain a constant dealing NAV provided that certain criteria are met, including that the market NAV of the fund does not deviate from the dealing NAV by more than 20 basis points

• VNAV MMFs price their assets using market pricing and therefore offer a fluctuating dealing NAV

1 The Official Journal of the European Union is the gazette of record for the European Union, and publishes all legislation and regulations of the European Union. 2 European Securities and Markets Authority 3 Weighted average maturity4 Weighted average life

Sign-o� by Ambassadors (COREPER) and EP Economic & Monetary A�airs (ECON)

Committee

Political agreementEuropeanParliament draft

Final sign-o�: Ministers in Council; plenary

in European Parliament

Application to new MMFs (12 months

from entry into force)

Council of the European Union

draft

SEPT2013

European Commission

draft

Legal and linguistic review of text

Publication in the O�cial Journal and entry into force (20

days after)

Application to existing MMFs (18 months from entry

into force)

APR2015

NOV2016

Q4 2016Q1 2017

JUN2016

DEC2016

Q1/Q22017

Q1/Q22018

Q1/Q22017

Q3/Q42018

The above dates are when we expect this to occur.

FOR INSTITUTIONAL/WHOLESALE/PROFESSIONAL CLIENTS AND QUALIFIED INVESTORS ONLY—NOT FOR RETAIL USE OR DISTRIBUTION

ARE ALL THE STRUCTURES AVAILABLE ON BOTH TYPES OF MMF?Short-term MMFs may be structured as Public Debt CNAV, LVNAV or VNAV. Standard MMFs may only be structured as VNAV.

SHORT-TERM MMF STANDARD MMFPublic Debt CNAV ü

LVNAV ü

VNAV ü ü

HOW DOES THE REGULATION COMPARE WITH THE PREVIOUS REQUIREMENTS FOR SHORT-TERM MONEY MARKET FUNDS?

SHORT-TERM MONEY MARKET FUNDSCURRENT NEW

UCITS5/ESMA SHORT-TERM MMF (CNAV)

PUBLIC DEBT CNAV LVNAV VNAV

PORTFOLIO RULESWAM (max) 60 days 60 days 60 days 60 days

WAL (max) 120 days 120 days 120 days 120 days

Maturity (max) 397 days 397 days 397 days 397 days

Credit ratings Instruments must hold one of the two highest short-term credit ratings (A-2/ P-2/F2 or above) from a credit rating agency

Manager must conduct internal credit quality assessment; ratings issued by credit rating agencies may be considered, but may not be solely nor mechanistically relied upon

Manager must conduct internal credit quality assessment; ratings issued by credit rating agencies may be considered, but may not be solely nor mechanistically relied upon

Manager must conduct internal credit quality assessment; ratings issued by credit rating agencies may be considered, but may not be solely nor mechanistically relied upon

LIQUIDITY REQUIREMENTSDaily liquid assets (min)

10%6 10% 10% 7.5%

Weekly liquid assets (min)

30%6 30% 30% 15%

PRICINGDealing NAV Constant NAV (rounded to 2 decimal

places i.e. nearest penny/ cent)Constant NAV (rounded to 2 decimal places i.e. nearest penny/ cent)

Constant NAV (rounded to 2 decimal places i.e. nearest penny/ cent), pro-vided dealing NAV does not deviate from mark-to-market NAV by >20 basis points

Variable (rounded to 4 decimal places)

Valuation Amortised cost Amortised cost Amortised cost for instruments ≤75 days; Mark-to-market for instruments >75 days

Mark-to-market

DIVERSIFICATION REQUIREMENTSMoney market instruments and ABCP

Max 10% in the same body, provided the aggregate of positions over 5% does not exceed 40%

Max 5% in money market instruments & ABCP issued by the same body; aggregate max 15% in ABCP7

Max 10% in money market instruments & ABCP issued by the same body, provided the aggregate of positions over 5% does not exceed 40%; aggregate max 15% in ABCP7

Sovereign instruments

Max 100% per sovereign, agency or European supranational, diversified across a min 6 issues with max 30% per issue

Max 100% per sovereign, agency or European supranational, diversified across a min 6 issues with max 30% per issue

Max 100% per sovereign, agency or European supranational, diversified across a min 6 issues with max 30% per issue

Max 100% per sovereign, agency or European supranational, diversified across a min 6 issues with max 30% per issue

Deposits Max 20% in deposits with the same institution

Max 10% in deposits with the same institution

Max 10% in deposits with the same institution

Max 10% in deposits with the same institution

Reverse repo Max 20% per counterparty8 Max 15% per counterparty Max 15% per counterparty Max 15% per counterparty

Other money market funds

Max 10% Max 5% per MMF Aggregate max 17.5%

Max 5% per MMF Aggregate max 17.5%

Max 5% per MMF Aggregate max 17.5%

Aggregate diversification

Max 20% in transferable securities, money market instruments & depos-its in a single body

N/A Max 15% in money market instruments, ABCP & deposits with a single body

Max 15% in money market instruments, ABCP & deposits with a single body

Concentration Max 10% of debt securities of the same issuer; max 10% of money market instruments of the same issuer

N/A Max 10% of money market instru-ments & ABCP issued by a single body

Max 10% of money market instruments & ABCP issued by a single body

5 Undertaking for Collective Investments in Transferable Securities as defined under Directive 2009/65/EC6 Fitch daily and weekly liquidity requirements7 Following finalisation of the forthcoming European Union Regulation on Simple, Transparent and Standardised (STS) Securitisations, the aggregate of all exposures to securitisations/ABCP shall not exceed 20%, with max 15% in securitisations/ABCP not compliant with the criteria for STS Securitisations.

8 Internal limit

FOR INSTITUTIONAL/WHOLESALE/PROFESSIONAL CLIENTS AND QUALIFIED INVESTORS ONLY—NOT FOR RETAIL USE OR DISTRIBUTION

HOW DOES THE LVNAV MMF WORK?Investors will interact with the LVNAV MMF in much the same way as they interact with the CNAV MMF today. Investors will be able to subscribe and redeem at the two decimal constant NAV (the NAV will be rounded to the nearest cent or penny), provided the fund is managed to certain restrictions:

• Portfolio holdings with a maturity of up to 75 days may be valued using the amortised cost methodology. Longer-dated instruments must be valued using mark-to-market (or mark-to-model) valuations.

• The portfolio level mark-to-market valuation must not deviate from the constant dealing NAV valuation by more than 20 basis points. If the deviation exceeds 20 basis points, investors must subscribe and redeem at the four decimal mark-to-market NAV.

• If the mark-to-market valuation on any instrument in the portfolio deviates from its amortised cost valuation by more than 10 basis points, that instrument must be marked-to-market. The remainder of the portfolio instruments with a maturity of up to 75 days may continue to be valued using the amortised cost methodology, and investors may continue to subscribe and redeem at the two decimal constant dealing NAV.

• The portfolio must hold at least 10% in daily liquid assets and at least 30% in weekly liquid assets.

• If the LVNAV MMF suspends redemptions for more than 15 days in any 90 day period, the LVNAV must convert to a VNAV MMF.

WHAT ASSETS ARE INCLUDED WITHIN THE DAILY LIQUID ASSETS AND WEEKLY LIQUID ASSETS RATIOS?Daily liquid assets comprise cash, and daily maturing assets including overnight reverse repurchase agreements and overnight deposits:

• Short-term Public Debt CNAV MMFs are required to hold at least 10% of their assets in daily liquid assets

• Short-term LVNAV MMFs are required to hold at least 10% of their assets in daily liquid assets

• Short-term VNAV MMFs are required to hold at least 7.5% of their assets in daily liquid assets

• Standard VNAV MMFs are required to hold at least 7.5% of their assets in daily liquid assets

Weekly liquid assets comprise weekly maturing assets including reverse repurchase agreements maturing within five business days, deposits maturing within five business days, and certain government and government-backed assets:

• Short-term Public Debt CNAV MMFs are required to hold at least 30% of their assets in weekly liquid assets, which may include up to 17.5% in highly liquid government and government-backed assets with a residual maturity of up to 190 days

• Short-term LVNAV MMFs are required to hold at least 30% of their assets in weekly liquid assets, which may include up to 17.5% in highly liquid government and government-backed assets with a residual maturity of up to 190 days

• Short-term VNAV MMFs are required to hold at least 15% of their assets in weekly liquid assets, which may include up to 7.5% in money market instruments or shares of other MMFs

• Standard VNAV MMFs are required to hold at least 15% of their assets in in weekly liquid assets, which may include up to 7.5% in money market instruments or shares of other MMFs

The weekly liquid asset ratio includes the daily liquid asset ratio.

WHEN MIGHT A LIQUIDITY FEE OR A REDEMPTION GATE OCCUR?Similar to existing rules and practices in Europe, the Regulation provides for the use of liquidity fees and redemption gates to protect MMFs in times of stress. These apply to public debt CNAV MMFs and LVNAV MMFs only; they do not apply to VNAV MMFs.

EUROPEAN MONEY MARKET FUND REGULATION LIQUIDITY FEE AND REDEMPTION GATE PROVISIONS

If the level of weekly liquid assets falls below 30% and net redemptions from the fund exceed 10% in one day, the MMF board may enact one of the following options:

• Do nothing, or

• Apply a liquidity fee to redeeming investors, equal to the cost of liquidity

• Restrict (“gate”) redemptions to 10% per day for up to 15 days

• Suspend redemptions for up to 15 days

If the level of weekly liquid assets falls below 10%, the MMF board must enact one of the following options:

• Apply a liquidity fee to redeeming investors, equal to the cost of liquidity

• Suspend redemptions for up to 15 days

FOR INSTITUTIONAL/WHOLESALE/PROFESSIONAL CLIENTS AND QUALIFIED INVESTORS ONLY—NOT FOR RETAIL USE OR DISTRIBUTION

WILL THE LIQUIDITY FEE/REDEMPTION GATE TRIGGERS BE THE SAME AS FOR US-DOMICILED MMFS UNDER THE RECENT CHANGES TO THE SEC 2A-79 RULE?The liquidity fee/redemption gate structure under the European Regulation will not be the same as for US-domiciled MMFs.

Under the European regulations, redemption fees/liquidity gates apply to Public Debt CNAVs MMFs and LVNAV MMFs only; they do not apply to VNAVs MMFs.

The recent changes to the SEC 2a-7 Rule for US-domiciled MMFs provide for the use of liquidity fees and redemption gates on institutional prime VNAV MMFs and retail MMFs; government CNAV MMFs are not required to apply liquidity fees/redemption gates, but may opt into them if properly disclosed.

US SEC RULE 2A-7 LIQUIDITY FEE AND REDEMPTION GATE PROVISIONS

Liquidity fees

Fund boards may impose fees up to 2% on all redemptions if:

• The fund’s level of weekly liquid assets falls below 30% of its total assets and the fund’s Board determines that such a fee is in the best interest of the fund

Fund boards must impose a 1% fee on all redemptions if:

• The fund’s weekly liquid assets fall below 10% of its total assets

Exception: The fee does not have to be implemented if the fund’s Board determines that such a fee is not in the best interest of the fund or that a lower or higher (up to 2%) liquidity fee is more appropriate.

Redemption gates

Fund boards may suspend withdrawals from the fund if:

• The fund’s level of weekly liquid assets falls below 30%

• The fund’s Board determines that imposing such a gate is in the fund’s best interest

Gates are limited to no more than 10 business days in any consecutive 90-day period.

HAVE MMFS BEEN PROHIBITED FROM BEING RATED?European policymakers have not prohibited MMFs from soliciting or carrying an external fund rating. MMFs may continue to carry external fund ratings, and the manager must disclose in the prospectus and marketing materials that the rating has been solicited or paid for by the manager.

WHAT DOES THE FIVE-YEAR REVIEW CLAUSE ON THE PUBLIC DEBT CNAV MMF MEAN? European policymakers have included a review clause on the public debt CNAV MMF. Review clauses are not an unusual feature in European regulations.

The Regulation provides that the European Commission must, within five years from the entry into force of the Regulation, present a report on the feasibility of establishing an 80% European Union public debt quota for Public Debt CNAV MMFs. The Commission must examine (i) supply of short term European Union public debt instruments, and (ii) whether the LVNAV MMF might be an appropriate alternative for the Public Debt CNAV MMF.

The Regulation does not presuppose any particular outcome to the review; the results of the review shall be presented to European policymakers, along with any appropriate amendments to the Regulation.

DOES THE REGULATION APPLY ONLY TO MMFS THAT ARE UCITS FUNDS?The Regulation applies to any UCITS or AIF10 that has the objective of offering returns in line with money market rates, or of preserving the value of the investment, and that seek to achieve these objectives by investing in short-term assets such as money market instruments or deposits.

9 On 23 July 2014, the Securities and Exchange Commission (SEC) approved changes to Rule 2a-7 under the Investment Company Act of 1940, which governs the operation of money market funds.

10 Alternative Investment Fund as defined under Directive 2011/61/EU

FOR INSTITUTIONAL/WHOLESALE/PROFESSIONAL CLIENTS AND QUALIFIED INVESTORS ONLY—NOT FOR RETAIL USE OR DISTRIBUTION

* PLEASE NOTE THAT THE SITE IS NOT INTENDED FOR RETAIL PUBLIC IN EUROPE, USA AND ASIA. IT IS INTENDED FOR PROFESSIONAL/INSTITUTIONAL AND QUALIFIED INVESTORS IN EUROPE, INSTITUTIONAL INVESTORS IN SINGAPORE, PROFESSIONAL INVESTORS IN HONG KONG AND INSTITUTIONAL/WHOLESALE INVESTORS IN USA ONLY. PERSONS IN RESPECT OF WHOM PROHIBITIONS APPLY MUST NOT ACCESS THIS SITE. ACCORDINGLY, THE INFORMATION CONTAINED IN THE SITE DOES NOT CONSTITUTE INVESTMENT ADVICE AND IT SHOULD NOT BE TREATED AS AN OFFER TO SELL OR A SOLICITATION OF AN OFFER TO BUY ANY FUND, SECURITY, INVESTMENT PRODUCT OR SERVICE.

NOT FOR RETAIL DISTRIBUTION: This communication has been prepared exclusively for institutional/wholesale/professional clients and qualified investors only as defined by local laws and regulations.

The views contained herein are not to be taken as an advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from J.P. Morgan Asset Management or any of its subsidiaries to participate in any of the transactions mentioned herein. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of writing. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit, and accounting implications and determine, together with their own professional advisers, if any investment mentioned herein is believed to be suitable to their personal goals. Investors should ensure that they obtain all available relevant information before making any investment. It should be noted that investment involves risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Both past performance and yield may not be a reliable guide to future performance.

J.P. Morgan Asset Management is the brand for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. This communication is issued by the following entities: in the United Kingdom by JPMorgan Asset Management (UK) Limited, which is authorized and regulated by the Financial Conduct Authority; in other EEA jurisdictions by JPMorgan Asset Management (Europe) S.à r.l.; in Hong Kong by JF Asset Management Limited, or JPMorgan Funds (Asia) Limited, or JPMorgan Asset Management Real Assets (Asia) Limited; in Singapore by JPMorgan Asset Management (Singapore) Limited (Co. Reg. No. 197601586K), or JPMorgan Asset Management Real Assets (Singapore) Pte Ltd (Co. Reg. No. 201120355E); in Taiwan by JPMorgan Asset Management (Taiwan) Limited; in Japan by JPMorgan Asset Management (Japan) Limited which is a member of the Investment Trusts Association, Japan, the Japan Investment Advisers Association, Type II Financial Instruments Firms Association and the Japan Securities Dealers Association and is regulated by the Financial Services Agency (registration number “Kanto Local Finance Bureau (Financial Instruments Firm) No. 330”); in Korea by JPMorgan Asset Management (Korea) Company Limited; in Australia to wholesale clients only as defined in section 761A and 761G of the Corporations Act 2001 (Cth) by JPMorgan Asset Management (Australia) Limited (ABN 55143832080) (AFSL 376919); in Brazil by Banco J.P. Morgan S.A.; in Canada for institutional clients’ use only by JPMorgan Asset Management (Canada) Inc., and in the United States by JPMorgan Distribution Services Inc. and J.P. Morgan Institutional Investments, Inc., both members of FINRA/SIPC.; and J.P. Morgan Investment Management Inc.

Copyright 2017 JPMorgan Chase & Co. All rights reserved.

LV–JPM34467 | 01/17

693ffe20-d89f-11e6-9dd9-005056960c8a

NEXT STEPSFor further information, please contact your J.P. Morgan Global Liquidity Client Adviser or Client Services Representative at:(352) 3410 3636 in EMEA(852) 2800 2792 in Asia Pacific1 800 766 7722 in USAwww.jpmgloballiquidity.com*