Embed Size (px)

Citation preview

Electric power special reportApril 2017

Ana-Maria Tolbaru, Editor, European Power DailyLucie Roux, Editor, European Gas Daily Andreas Franke, Senior Writer, European ElectricityFabio Reale, Head of Content, European Gas and Power

French Presidential Elections: Crunch time for the country’s energy mix

www.platts.com/electric-power

April 24 U

PDATE

Special report: Electric power French Presidential Elections: Crunch time for the country’s energy mix

2© 2017 S&P Global Platts, a division of S&P Global, Inc. All rights reserved.

FRENCH CANDIDATES: AT-A-GLANCE ENERGY POSITIONS

MACRON LE PEN

“ It’s not good to have 75% of our energy come from nuclear. I will keep the energy transition program and hence I will keep the 50% cap [by 2025]. ”

“ France needs a new patriotic model of intelligent protectionism. ”

Nuclear Reduce nuclear (supports current policy of 50% share by 2025)

Pro-nuclear (supports lifetime extension program, EDF re-nationalization)

Fessenheim Close Keep open

Renewables Double wind and solar by 2022 in line with current policy path

Moratorium on wind, yes to solar, bioenergy “as long as French”

Security of Supply Battery storage, smart grid to help reduce demand/supply imbalance

Nuclear focus, reduce demand, dependency on external sources

Coal plants Close final coal plants by 2022 No comment

Shale gas Against Against

Carbon tax Pro carbon floor price No comment

EDF ownership - To be re-nationalised 100%

Steel industry Demand supported by Eur50 billion investment plan. ‘Frexit’ to widen steel import deficit with EU

Diesel subsidies End to subsidies, diesel car scrappage subsidies Extension of subsidies

PIRA’s price outlook Structurally bullish if Macron sticks to Hollande’s energy transition path. His agenda would widen France’s structural deficit during the winter peak, through coal and nuclear closures

Mildly bearish in the medium-term, but a moratorium on wind could have a more immediate short-term bullish impact

France is facing its most divisive presidential elections since Jean-Marie Le Pen shocked pollsters in 2002 and booked a surprise place in the second round. Whether Emmanuel Macron will defeat Marine Le Pen in the second round on May 7 with a similar margin as Jacques Chirac defeated her father back in 2002 remains to be seen. But In terms of policy and world view the two candidates again offer an almost antagonistic choice.

This is also true in energy terms with a number of key nuclear issues to be decided under the next president’s watch. Equally, France’s nuclear industry is at the cross-roads – shaken by delays and cost-overruns at Flamanville-3 as well as safety fears at existing reactors that saw power prices spike to record-highs last winter.

The next French president will be the first since Chirac to open a new nuclear power plant. That person will also need to decide the future of France’s oldest reactors, now approaching the end of 40-year life-spans. EDF’s program to extend reactor operation – the ‘Grand Carenage’ – is hugely expensive, but the alternative of closures would hardly be

cheap, with impacts on security of supply, power price, cross-border flows and France’s carbon footprint.

Debates on the need to strengthen carbon prices in the context of the Paris Agreement are therefore to be seen in France’s national interest, but will only work if France can convince its neighbors of shared benefits.

In this special report, S&P Global Platts analyses the range of possible impacts of the two candidates’ views on energy.

A victory for the front-runner, center-left ex-banker and former economy minister Emmanuel Macron, could be structurally bullish for electricity prices and in the long term result in France, Europe’s largest electricity exporter, becoming increasingly dependent on imports.

Macron’s views are also closest to business-as-usual with the candidate set to expand on President Francois Hollande’s energy transition path, while far-right candidate Marine Le Pen favors of a ‘return to glory’ for the French nuclear industry and campaigns for a moratorium on wind power.

Source: Platts, PIRA

Special report: Electric power French Presidential Elections: Crunch time for the country’s energy mix

3© 2017 S&P Global Platts, a division of S&P Global, Inc. All rights reserved.

NUCLEAR AT THE CROSS-ROADS

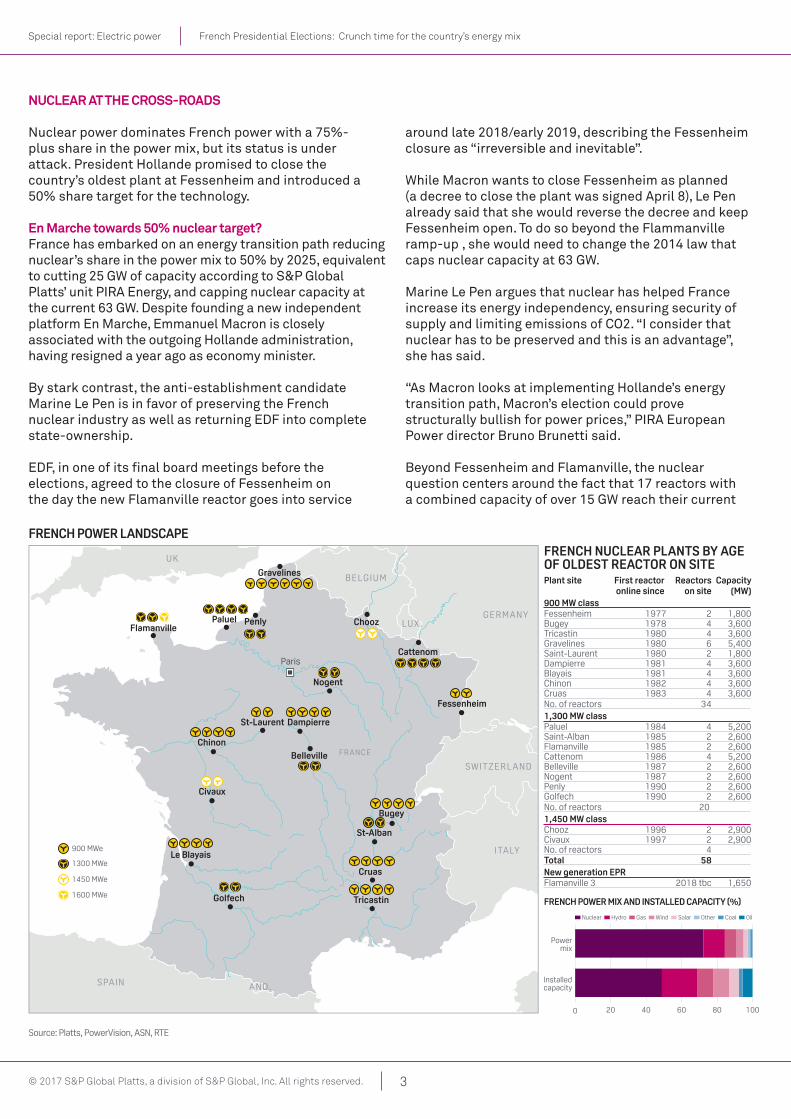

Nuclear power dominates French power with a 75%-plus share in the power mix, but its status is under attack. President Hollande promised to close the country’s oldest plant at Fessenheim and introduced a 50% share target for the technology.

En Marche towards 50% nuclear target?France has embarked on an energy transition path reducing nuclear’s share in the power mix to 50% by 2025, equivalent to cutting 25 GW of capacity according to S&P Global Platts’ unit PIRA Energy, and capping nuclear capacity at the current 63 GW. Despite founding a new independent platform En Marche, Emmanuel Macron is closely associated with the outgoing Hollande administration, having resigned a year ago as economy minister.

By stark contrast, the anti-establishment candidate Marine Le Pen is in favor of preserving the French nuclear industry as well as returning EDF into complete state-ownership.

EDF, in one of its final board meetings before the elections, agreed to the closure of Fessenheim on the day the new Flamanville reactor goes into service

around late 2018/early 2019, describing the Fessenheim closure as “irreversible and inevitable”.

While Macron wants to close Fessenheim as planned (a decree to close the plant was signed April 8), Le Pen already said that she would reverse the decree and keep Fessenheim open. To do so beyond the Flammanville ramp-up , she would need to change the 2014 law that caps nuclear capacity at 63 GW.

Marine Le Pen argues that nuclear has helped France increase its energy independency, ensuring security of supply and limiting emissions of CO2. “I consider that nuclear has to be preserved and this is an advantage”, she has said.

“As Macron looks at implementing Hollande’s energy transition path, Macron’s election could prove structurally bullish for power prices,” PIRA European Power director Bruno Brunetti said.

Beyond Fessenheim and Flamanville, the nuclear question centers around the fact that 17 reactors with a combined capacity of over 15 GW reach their current

Chooz

Cattenom

Penly

Fessenheim

Nogent

Dampierre

Belleville

Chinon

Gravelines

Civaux

Golfech

Le Blayais

Tricastin

Cruas

Bugey

St-Alban

PaluelFlamanville

St-Laurent

FRANCE

SPAIN AND.

SWITZERL AND

ITALY

GERMANY

BELGIUM

UK

LUX .

Paris

FRENCH POWER LANDSCAPE

Source: Platts, PowerVision, ASN, RTE

900 MWe

1300 MWe

1450 MWe

1600 MWe

0 20 40 60 80 100

Installedcapacity

Powermix

Nuclear Hydro Gas Wind Solar Other Coal Oil

FRENCH POWER MIX AND INSTALLED CAPACITY �%�

FRENCH NUCLEAR PLANTS BY AGE OF OLDEST REACTOR ON SITE

Plant site First reactor Reactors Capacity online since on site (MW)900 MW class Fessenheim 1977 2 1,800Bugey 1978 4 3,600Tricastin 1980 4 3,600Gravelines 1980 6 5,400Saint-Laurent 1980 2 1,800Dampierre 1981 4 3,600Blayais 1981 4 3,600Chinon 1982 4 3,600Cruas 1983 4 3,600No. of reactors 34 1,300 MW class Paluel 1984 4 5,200Saint-Alban 1985 2 2,600Flamanville 1985 2 2,600Cattenom 1986 4 5,200Belleville 1987 2 2,600Nogent 1987 2 2,600Penly 1990 2 2,600Golfech 1990 2 2,600No. of reactors 20 1,450 MW class Chooz 1996 2 2,900Civaux 1997 2 2,900No. of reactors 4 Total 58 New generation EPR Flamanville 3 2018 tbc 1,650

Special report: Electric power French Presidential Elections: Crunch time for the country’s energy mix

4© 2017 S&P Global Platts, a division of S&P Global, Inc. All rights reserved.

end-of-lifespan before the next presidential elections in 2022.

While Le Pen supports the program for a life-span extension – the Grand Carenage - Macron’s statements on nuclear suggest his opposition to such a program.

“It’s not good to have 75% of our energy coming from nuclear. I will keep the energy transition program and hence I will keep the 50% cap [by 2025],” Macron said in his manifesto.

However, Macron also said that any strategic decision regarding nuclear would come once French nuclear regulator ASN had published its conclusions on the Grand Carenage towards the end of 2018.

Commentators note that nothing is set in stone in Macron’s views on nuclear beyond Fessenheim and Flamanville, while the goal of reducing nuclear’s share to 50% by 2025 remains challenging .

“An ambitious and brave choice since this will require multiplying by six France’s renewable capacity,” said Philippe Charlez, French energy expert. According to Charlez, France would need 100 GW of renewables to support a reduced nuclear park.

France’s existing renewables target translates to 20 GW of additions over the next eight years. That is too little to offset targeted nuclear closures, according to PIRA.

Platts Analytics’ Eclipse Energy assumes a trajectory towards 70% nuclear as more realistic by 2025, “only hitting the 50% target around 2030.

Around this time we see a switch from net exporter to net importer. This is as much due to significant growth in renewables in France’s neighbouring markets as it is to do with Frances nuclear phase out,” it says.

Any accelerated closure program will bring decommissioning costs into focus – a political can of worms because, as Hollande’s own deputy head of Socialist party PS Barbara Romagnan has said, it is impossible to say what those costs will be. EDF says decommissioning the French nuclear fleet will cost Eur54 billion and plans to set aside Eur23 billion.

This is some way below the per gigawatt decom provisions being made both in Germany and the UK, and has been characterized by a French parliamentary committee as a likely under-estimate.

RENEWABLE ENERGY MOMENTUM BUILDS In France the development of new renewables (wind and solar, not hydro) lag behind not only Germany, but also Spain, Italy and the UK. That started to change under

Grand Carenage

In January 2015, EDF’s board approved an industrial modernization program to extend lifetimes of its 58 operational reactors by at least 10 years to a maximum of 20 years. Known as Grand Carenage, the program is expected to run until 2025. The utility estimates investment of Eur51 billion between 2015 and 2025 to upgrade reactors to ASN’s latest safety standards. In a first step, the program would focus on the PWR 900 MW series with a combined capacity of around 30 GW. Investment corresponds to Eur1.5 million/MW, about twice the capital cost of a new CCGT. The conditions for the 40-year safety review are still in negotiation, with inspections on-going. The objective is to reach an agreement towards the end of 2018. If achieved, ASN would then decide, reactor by reactor, on lifetime extensions. It is ASN and not the president who approves or blocks the extension of reactors beyond 40 years of age based on a review of safety and technical elements.

NUMBER OF FRENCH REACTORS REACHING 40-YEAR-LIFESPAN (cumulative) 2018 2019 2020 2021 2022 2023 2024 2025Reactor units 1 2 5 11 19 19 24 28Capacity (GW) 0.9 1.8 4.5 9.9 17.7 17.1 21.7 25.3Source: Platts analysis on World Nuclear Association data

FRENCH NUCLEAR CAPACITY �40 vs 50 YEAR�LIFE�SPAN

0

20

40

60

80

204020352030202520202015

(GW)

50 years

40 years

Source: RTE

FRENCH YEAR�AHEAD POWER REMAINS BELOW ARENH

20

40

60

80

100

Apr-17Apr-15Apr-13Apr-11Apr-09Apr-07

(Eur/MWh)

Arenh price French year-ahead

Source: Platts

Special report: Electric power French Presidential Elections: Crunch time for the country’s energy mix

5© 2017 S&P Global Platts, a division of S&P Global, Inc. All rights reserved.

France: Macroeconomic Outlook

by Jean-Michel Six, Chief Economist EMEA, S&P Global Ratings

Recent developmentsThe French economy appeared initially as a laggard when growth started to pick up in the Eurozone in 2013, but conditions improved markedly in 2016.

In particular the labor market recorded a fall in the jobless rate as over 210,000 new jobs were created, the biggest jump since the great financial crisis. Overall GDP growth was 1.1% last year thanks in particular to a strong rebound in business investment in the second half of the year.

Rising capacity utilization and an improvement in profit margins, due in particular to targeted government measures (tax credit for competitiveness and employment, reduction in the corporate tax rate under the responsibility pact) have underpinned a recovery in capital spending.

Meanwhile the construction sector, traditionally a key growth engine for the French economy, started to pick up after several years of contraction.

The rebound in inflation was smaller than in the rest of the Eurozone, up 1.2% at the start of 2017, suggesting that it should be less of a drag on household purchasing power than in other countries, such as Spain.

Future trends

France’s GDP grew 0.4% quarter on quarter during Q4 2016 from 0.2% q/q during the third quarter. Short-term indicators suggest growth is likely to stand around 0.3%–0.4% q/q during the first quarter of 2017.

The composite purchasing managers’ index (PMI) reached a 69-month high in March, and consumer confidence reached a nearly 10-year high in February. Consumption of goods, which represents around one-third of total consumption, rose a strong 0.6% in January.

In the short term, the result of the presidential elections, scheduled for late April (first round) and May (second round) is uncertain. Our baseline forecast assumes that a mainstream candidate will be elected. In that case uncertainties around the future of France within the Eurozone will be fully dissipated and 10-year sovereign bond spreads with Germany will shrink again. We recognize that downside risks to this projection exist, however.

Our baseline forecast has consumption remaining the prime driver of overall growth this year and next. A further reduction of slack in the labor market will fully offset the modest rise in headline inflation. We note that despite short term doubts about the outcome of the elections, consumer confidence has remained at its highest level since 2009. A fresh rise after the elections cannot be ruled out that could give consumer spending an additional boost in the second half of the year.

The underlying outlook for business investment remains upbeat. Credit growth has recovered and we expect the European central bank to maintain its current supportive policy through 2018. Interest rates should therefore remain historically low, underpinning capital spending growth. Overall our forecast sees the French economy growing 1.4% this year and 1.4% in the each of the next two years.

That said the French economy faces two major challenges that will need to be addressed over the medium term. One is its lack of competitiveness. Since 2010 imports of goods have grown about three times as fast as the overall GDP suggesting that a considerable part of additional domestic demand “leaks” towards foreign producers. On the global markets French exports have been steadily losing market share and grew last year by a disappointing 1.1% in real terms (versus 3.7% for imports). It would be simplistic to attribute the deteriorated competitiveness to a cost disadvantage only. In fact after the reforms implemented in the past five years French labor costs are at comparable levels with Germany. More fundamentally French exports have a positioning problem in the global value chain, at intermediate levels between Spain and Germany. They find it hard to compete on cost with Spain and to compete on quality and value added with Germany.

The second challenge is that potential growth has steadily declined since the beginning of the great financial crisis. The OECD estimates that French potential growth is currently around 1.2% versus 1.8% on average between 2001 and 2008. In turn the OECD reckons that the output gap, the difference between actual and potential output, is about -2.3%. The implication is that the economy needs to grow above its potential output rate for several years to absorb the slack (labor, capacity utilization) that persists. Economic policies need to set the stage for such a performance to be achieved sustainably over time. In that sense, France is indeed at the crossroads.

FrançoisMitterrand

JacquesChirac

NicolasSarkozy

FrançoisHollande

Next presidentialterm

1981 - 1995 2012 - 2017 2017 - 20221995 - 2007 2007 - 2012

PRESIDENTS AND ENERGY EVENTS TIMELINE

Oil crisis –birth of Frenchnuclear

Fessenheimreactor

comes online

Maastrichtreferendum

Last newFrench reactorsadded

Financialcrisis

Fukushima disaster

Parisclimate

deal

Brexit

Fessenheimclosure/Flamanville 3ramp-up

Eurozonestarts

France brings over40 reactors online

Nuclear hits75% of

power mix

1973 1977 1980s 1990 1992 19991996 2008

French windreaches�rst GW

2006 2011

Eurozonedebt crisis

2012

Energytransition

law

2014 2015 2016

GrandCarenage

review

2018 2019 2020

Source: Platts

EC’sclean energypackage for

2030 targets

Special report: Electric power French Presidential Elections: Crunch time for the country’s energy mix

6© 2017 S&P Global Platts, a division of S&P Global, Inc. All rights reserved.

the Hollande administration, with strong leadership shown by environment and energy minister Segolene Royal in the Paris Agreement on climate change.

As with nuclear, Macron’s views on renewables are again similar to Hollande’s transition energetique, while Le Pen is calling for a moratorium on wind power in France, but is supporting solar.

Macron’s declared target is to double wind and solar capacity by 2022 from a current base of 12 GW wind and 7 GW solar. He is likely to further Royal’s already-financed tenders for 4 GW of solar and 3 GW of onshore wind. Royal’s aim is to lift onshore wind capacity to between 22 GW and 26 GW by 2023, with offshore wind adding 6 GW.

Wind plays a marginal role in the French energy mix with 20 TWh generated in 2016, covering 4% of domestic power demand. French solar amounts to 7 GW installed, with Royal targeting 10 GW by 2018 and 20 GW by 2023. For his part, Macron is on record for saying that he would fund the expansion of renewables by “encouraging” private investment of Eur30 billion.

Le Pen’s manifesto includes a number of specific pledges for a “sustainable France” beyond a moratorium on wind, promising to “massively develop” French solar, biogas and biomass, but with no detail on financing. The Paris Agreement is not mentioned in Le Pen’s Front National manifesto, nor are carbon taxes or the future of France’s remaining coal plants, but there is recognition of energy efficiency gains to be pursued, specifically via subsidies for home insulation, as well as outright support pledged for the country’s nuclear industry – both sustainable, carbon-cutting policy directions.

The price impact of policies lowering peak demand would to be in part offset by a moratorium on wind, according to PIRA.

French solar potential is great, but solar does little to calm winter peaks – when France is vulnerable to tightness caused by electric heating. A moratorium on wind, on the other hand, could limit the system in winter.

PHASING OUT COAL While Le Pen did not provide details on coal plant decommissioning, Macron wants to close the country’s remaining five coal-fired power stations (2.9 GW) by 2022, bringing the current target forward a year, with commentators noting this as a political deadline ahead of the next presidential elections. EDF has retrofitted its three coal units to comply with EU directives and extend their lifetime to 2035, but it is likely Macron will pursue the target regardless. France has reduced its coal fleet by 4 GW in recent years. According to RTE, emissions from the French power sector fell to a historic low of 19

million tonnes in 2014, before rising to over 50 million tonnes in 2016 amid a sharp drop in nuclear output replaced by gas, coal and fuel oil.

FRENCH INSTALLED GENERATION CAPACITY 2016 MW Y-o-Y changeNuclear 63,130 0Fossil fuel* 16,867 -795

Coal* 2,991 0Oil* 5,604 -1,370Gas* 8,273 575

Hydro 25,482 51Wind 11,670 1,345Solar 6,772 576Source: RTE, Platts Powervision*

FRENCH WIND, SOLAR TRAJECTORIESGW 2016 Macron target by 2022 Existing target by 2023Installed solar 6.8 13.6 18.2Installed wind 11.7 23.4 21.8Total 36.9 40.0Source: Platts, RTE, French Multiannual Energy Programme

FRENCH CAPACITY MIX OUTLOOK KEY FUELS�

0

20

40

60

80

20402035203020252020

(GW)

Source: Platts Analytics’ Eclipse Energy

Demand

WindSolarHydroGasNuclearHard coal

SOLAR’S IMPACT ON POWER PRICES

0

5

10

15

20

25

483828188

(GW)

(weeks)

(Eur/MWh)

Source: RTE, Platts Analytics’ Eclipse Energy

0

10

20

30

40

50

Price (right axis)

Solar (left axis)

2013201420152016

201520142013

2016

FOSSIL FUEL CAPACITY UNDER MACRON

0

4

8

12

16

202220212020201920182017

(GW)

Source: Platts

GasCoalFuel oil

Special report: Electric power French Presidential Elections: Crunch time for the country’s energy mix

7© 2017 S&P Global Platts, a division of S&P Global, Inc. All rights reserved.

CARBON TAX REVIVED Proposals for a French carbon floor price emerged in early 2016 when Macron was economy minister. Looming security of supply issues last autumn, however, put paid to the idea and the tax was shelved. Macron brought back this idea and said in his manifesto he would introduce a Eur100/mt carbon tax in 2030, without specifying however any details of the tax – whether it would be a price floor, similar to the UK’s carbon price floor, whether it would be implemented nationally or at EU level.

“We will integrate the ecological cost into the carbon price, increasing the carbon tax to Eur100/mt CO2 in 2030,” Macron’s manifesto reads.

Hollande’s new carbon cost was expected to be Eur30/t in 2017, before the measure was dropped late 2016. A report by RTE published in March 2016 showed that with a Eur30/mt carbon price, the operating hours of the coal fleet would drop below 15 TWh/year, while gas plant run times would increase. The report says: “France sees an overall increase in thermal power generation (and thus in exports) as the carbon price rises: as they become more competitive, gasfired plants are operated instead of coal plants in France, and also find new end-markets in other countries.”

According to Platts Analytics, a Eur10/mt carbon floor price is sufficient for gas plant to start to displace coal for Calendar 2018, while Eur30/mt CO2e would see coal very firmly out of the money.

Le Pen does not mention carbon taxes in her manifesto.

NATURAL GAS UPSIDE ? Under normal conditions France has 4 GW-5 GW spare gas-fired generating capacity of its 8.3 GW total installed capacity according to Platts Power Vision data, enough to offset coal plant closures with remaining flexibility to help in times of nuclear shortfall.

Existing gas capacity was driven hard in winter 2016/17, reducing the surplus to 2 GW on average, down from 4.8 GW in 2015 and 4.4 GW in H1 2016.

Meeting the 50% nuclear target in 2025 would place new pressures on France and necessitate careful planning. As experienced last winter, higher locational spreads would attract imports and potentially support new investment in tandem with the country’s capacity mechanism.

While a carbon price floor would increase the short run marginal cost of gas-fired generation, this would impact run times only to the extent of the availability of cheaper imports and greater domestic renewable energy output.

EFFECT OF CARBON FLOOR PRICE ON COAL�TO�GAS SWITCHINGPrice (Eur/MWh)

Volume (million cu m/d)

Source: Platts Analytics’ Eclipse Energy

14

17

20

23

26

108642

Eur30/mtEur20/mtEur10/mtEur0/mt

Peg N Cal-18Peg N DA

FRENCH GAS vs COAL FIRED GENERATION�WINTER 2016 vs WINTER 2014�

0

2

4

6

8

10

MayAprMarFebJanDec

(GW)

Source: Platts Analytics’ Eclipse Energy

Coal 2016Gas 2016

Gas 2014Coal 2014

FRENCH CCGT RUNNING vs CAPACITY

0

2

4

6

8

Mar-17Mar-16Mar-15Mar-14Mar-13

(GW)

Capacity

Max

AvgUnused

Source: Platts Analytics’ Eclipse Energy

2016 FRENCH GAS IMPORTS Bcm Belgium Germany Norway Spain LNG TotalImports capacity 30.0 19.9 19.7 7.8 34.3 111.6Import flows 18.0 9.3 16.9 0.6 7.3 52.2Spare Capacity 12.1 10.6 2.7 7.1 27.0 59.5Source: Platts analysis, Entsog data

Higher costs would simply be passed on to consumers in the wholesale price as gas increased its price setting role. The equivalent baseload gas fired generation needed to replace the proposed reduction in nuclear output is estimated by Platts at 20 GW-25 GW, corresponding to 28 Bcm-34 Bcm/year of incremental gas demand. Imports and rising renewable energy output would surely make the call on gas less than this.

French gas demand was 63 Bcm in 2016, of which 4.3 Bcm came from the power segment. With no significant domestic production, France is reliant of imports, with

Special report: Electric power French Presidential Elections: Crunch time for the country’s energy mix

8© 2017 S&P Global Platts, a division of S&P Global, Inc. All rights reserved.

85% of its gas needs delivered via pipeline and the balance by LNG imports. Combined pipeline and LNG spare capacity is about 60 Bcm. New demand would not need new import infrastructures.

The gas supply outlook looks healthy on both LNG and pipeline fronts. Global LNG liquefaction capacity is expected to rise by 145 Bcm/yr in the next five years, widening a global supply glut by 30 Bcm/yr by 2022

(relative to 2016’s surplus) according to Platts Analytics. The outlook on pipeline gas supplies is also positive, with Russian gas export to NW Europe forecast to rise from 64 Bcm/yr to 75 Bcm/yr between 2016-2022.

Russian gas data suggest the country has 100 Bcm/yr of spare production capacity along with significant spare transport capacity. This plentiful outlook must be balanced by the importance placed by candidates

Other hydrocarbon sector implications: licensing and subsidies to diesel

by Robert Perkins, Senior Writer, Petroleum News

Emmanuel Macron has fielded one of the strongest green agendas of all French presidential candidates laying out commitments to the environment based on cutting reliance on fossil fuels.

In his ecological transition policy program released in March, Macron promised the start of a “profound break” with France’s existing energy model with regard to fossil fuels.

In addition to maintaining France’s ban on shale fracking and prohibiting shale gas exploration, Macron pledged not to issue any new hydrocarbon exploration licenses.

While France has few conventional domestic oil and gas resources of its own, the move could frustrate hopes for future exploration off French Guyana, the biggest of France’s overseas departments and the EU country’s second largest region. Shell and Tullow raised hopes with the Zaedyus find off the former French South American colony back in 2011, but follow-up drilling failed to provide evidence of commercial volumes and no further wells are planned.

Macron’s promise to end new oil and gas licensing would compromise any future efforts to tap France’s tight oil potential, which the US’ Energy Information Administration estimates as Europe’s biggest resource.

Light on detail, Marine Le Pen has said she would support research and development in a French hydrogen industry in order to reduce dependence on oil. In the past she has promised to reduce energy prices and taxes.

Le Pen’s Front National launched a New Ecology movement in 2014 supporting a platform of “patriotic” defense in the face of international climate deals, and promoting nuclear energy.

Diesel dutiesFrance has already fired the starting gun on fiscal moves to reduce the country’s heavy reliance on diesel in its road fuel mix due to air quality concerns. The final outcome of the French elections could influence the pace of this shift.

France is the region’s biggest diesel market with the EU’s

highest level of diesel penetration across road fuel sales.

As a share of total road fuel sales, French diesel consumption stood at 81% in February according to industry association UFIP, down from an average of 84% in 2015.

Motivated by air quality concerns and the Volkswagen emissions scandal, the French government began cutting tax incentives on diesel in 2015 in a bid to neutralize the price difference with gasoline within the next five to seven years.

At the same time, it introduced a scrappage scheme for diesel cars in polluted areas under its Energy Transition Bill.

Although there is no specific mention of road fuel taxation in her policy manifesto, Le Pen has in the past defended tax advantages for diesel cars, saying that she would maintain these.

By contrast, Macron has promised to continue to bring diesel duties in line with those on gasoline over five years to “drastically” reduce fine particulate pollution.

The former investment banker also plans to back stronger European anti-pollution standards for new vehicles and launch a scrappage scheme for pre-2001 vehicles.

He wants to accelerate the rollout of electric vehicle charging points and maintain France’s tax incentives for low carbon cars.

FRANCE’S DIESEL DOMINANCE � ROAD FUEL SALES

0

10

20

30

40

50

20152012200920062003

(million mt) (%)

Source: UFIP

50

60

70

80

90

100DieselGasoline Diesel

Special report: Electric power French Presidential Elections: Crunch time for the country’s energy mix

9© 2017 S&P Global Platts, a division of S&P Global, Inc. All rights reserved.

on the need to boost France’s energy independence – either by cutting consumption or exploiting indigenous resources.

The current socialist government has set a target to reduce fossil fuel consumption by 30% by 2030.

In terms of domestic resource, France has 3,900 Bcm of technically recoverable shale gas, Europe’s second biggest resource behind Poland. Exploitation of shale gas was banned in 2011 due to environmental concerns and social resistance. Macron says he would continue to ban shale gas exploration. National Front’s position has been one of supporting opposition to shale gas, but Le Pen’s February policy manifesto appears to take a softer approach. She now pledges to ban development of shale gas as long as “satisfactory environmental, safety and health conditions” are not being met.

SECURITY OF SUPPLY ACROSS BORDERS Security of supply will remain a key question at the heart of French energy policy during winter peaks. Key to the French power system is its sensitivity to cold, when each 1 C drop in temperature lifting demand by the output equivalent of two big reactors or around 2.4 GW. Seasonal supply/demand swings are balanced largely by cross-border trade, with net transfer capacity above 15 GW and new lines to come. For how long and to what extent can France depend on its neighbors during winter peaks?

Market-coupling in a European power system While France is known for shunting vast quantities of cheap surplus nuclear across its borders, the recent winter exposed shrinking capacity margins and demonstrated how inflexible its system is when nuclear availability falls. French cross-border transmission capacity is set to rise above 18 GW by 2020 with new cables planned to Italy and the UK providing some comfort in case of fulfilment of Hollande’s nuclear pledge and imposition of a national carbon price, according to PIRA. Capacity is one thing, firm imports another. Dispatchable plant margins are set to fall across Northwest Europe into the 2020s as first the German and then the Belgian nuclear fleets are phased out. RTE simulations of generation availability abroad found that in the event of a cold spell France could import only up to 11 GW, while during oversupplied summer months France could export over 10 GW on a verage.

Platts Analytics expects France to switch from net exporter to net importer on an annualized basis only by 2030. This is in line with its assumption that only by then would the French nuclear fleet have reduced to 50% of the power mix.

“This is as much due to significant growth in renewables in France’s neighbouring markets as it is to do with

ITALYSPAIN

FRANCESWITZERL AND

UNITED KINGDOM

C WE

FRANCE CROSS�BORDER POWER FLOWS 2016

All �gures in TWh.Source: Platts analysis of RTE data

Exports 71.7

Imports 32.6

Balance 39.1

Exports 17.4

Imports 7.3

Exports 13.3

Imports 5.5 Exports 17.7

Imports 1.2

Exports 10.6

Imports 15.9

Exports 12.7

Imports 2.7

FRENCH SPOT POWER PRICE SPIKES IN WINTER 2016 17

-50

0

50

100

150

200

250

Mar-17Feb-17Jan-17Dec-16Nov-16Oct-16

(Eur/MWh)

Source: Platts

SpainUK

FranceGermany

FRENCH CROSS-BORDER POWER FLOW ANALYSIS 2016 average (GW) CWE UK Switzerland Italy Spain TotalAvailable export capacity 4.5 1.8 3.1 2.0 1.5 12.9Available import capacity 3.3 1.8 1.3 1.1 0.7 8.2Export flows 1.2 1.4 2.0 2.0 1.5 8.2Import flows 1.8 0.3 0.8 0.1 0.6 3.7Spare export capacity 3.3 0.4 1.1 0.0 0.0 4.7Spare imports capacity 1.5 1.5 0.5 1.0 0.1 4.5Source: Platts analysis on RTE data

France’s nuclear phase out,” it said. A Macron victory, however, could see adherence to the 2025 nuclear target and a carbon tax helping to support a bullish price outlook. This could in turn inject new impetus into the development of cross border interconnections.

Energy efficiency helps to limit dependence As noted, both candidates support energy efficiency measures. French power demand has been relatively stable since 2010 and stood at 473 TWh in 2016, but there is recognition that reducing peak winter demand is crucial for France’s security of supply. Existing measures are to set to deliver 2 TWh of wintertime

Special report: Electric power French Presidential Elections: Crunch time for the country’s energy mix

10© 2017 S&P Global Platts, a division of S&P Global, Inc. All rights reserved.

savings between now and 2020, RTE reports. Under a high efficiency scenario, load could be reduced by 55 TWh by 2021, while a baseline scenario could see demand fall by 36 TWh by 2021, the TSO says. Macron would offer Eur4 billion for the energy efficient renovation of buildings, while Le Pen has focused on a building insulation program to reduce heating demand.

CONCLUSION

The energy question will not decide the French election, but the outcome of the election will almost certainly have a profound effect on France’s electricity market and those of its neighbors. With front-runners Macron and Le Pen lacking an established party base in the National Assembly, parliamentary elections in June will be crucial in deciding the power of the new President. Without a majority in the National Assembly, material divergence from the current course is unlikely. Equally, union opposition is a potent force in France. Recent strikes and the agonizing over Fessenheim’s closure have served to underline how intransigent the French energy sector can be.

MACRON

In energy terms and for the mid-term future, his views are closest to ‘business as usual’ and haven’t changed much since his time as economy minister under Hollande. Longterm, his goal of reducing nuclear could be structurally bullish, but nothing seems to be set in stone and keeping power prices affordable for households and industry will remain key also under a Macron presidency.

LE PEN

A Le Pen victory in the second round would be another geopolitical earthquake especially in the wake of the surprising Brexit and Trump election outcomes. With Le Pen in the Elysee, most fundamental questions are up for debate with a market reaction to match. In pure terms of the power market, however, a Le Pen victory could potentially mean a continuation of French oversupply during the summer.

Steel Industry: infrastructure investment programs vs Frexit scenariosHenry Cooke, Editor in Chief, Steel Business Briefing

Marine Le Pen has promised to enact some strongly nationalist measures which would have radical but unpredictable effects on metals. The first in her 144-point election program is to hold a referendum on French withdrawal from membership of the European Union, an institution which she has labelled “technocratic, totalitarian and harmful to our freedoms.”

Frexit would have a potentially dramatic impact on the French steel industry, much of which is owned by companies based in other EU countries. The biggest steel producer in France, ArcelorMittal, is headquartered in Luxembourg. Another Luxembourg company owns much of the French stainless steel industry, while Italian and Spanish steelmakers control most of France’s production of construction steels. German, Swiss, British, Indian and Russian steel companies also operate in France. They might respond to any French withdrawal from the EU’s single market by transferring production elsewhere.

Le Pen’s economic program expresses ambitions to strengthen the manufacturing industry. She is suspicious of free trade and globalization, and wants to exit the euro, putting a national currency in place instead. She favors a

degree of trade protectionism, promoting French-made goods over imports where it would be “rational” to do so.

At present, France is a strong net exporter of steel. But its net steel trade with other EU countries is in deficit, so any increased protectionism could be a double-edged sword for the French steel industry.

Emmanuel Macron is promising radical action to tackle France’s endemic mass unemployment. He wants to invest €50 billion over five years in sectors such as information technology, public services and potentially metals-intensive projects in urban renovation, energy, transport and ecology. He is also pledging to reduce company taxation, encourage private investment and to establish a €10 billion national fund to invest in “industries of the future” which he has not clearly identified.

Metals producers could face an increase in their direct and indirect carbon emission costs. With about one-third of French steel produced in electric arc furnaces and the aluminum sector also electricity-intensive, this could have a substantial impact on metals producers’ operating costs.

Special report: Electric power French Presidential Elections: Crunch time for the country’s energy mix

11© 2017 S&P Global Platts, a division of S&P Global, Inc. All rights reserved.

For more information, please visit us online or speak to one of our sales specialists:

www.platts.com | [email protected]

NORTH AMERICA +1-800-PLATTS8 (toll-free) +1-212-904-3070 (direct)

EMEA +44-(0)20-7176-6111

LATIN AMERICA +55-11-3371-5755

ASIA-PACIFIC +65-6530-6430

RUSSIA +7-495-783-4141

The names “S&P Global Platts” and “Platts” and the S&P Global Platts logo

are trademarks of S&P Global Inc. Permission for any commercial use of

the S&P Global Platts logo must be granted in writing by S&P Global Inc.

You may view or otherwise use the information, prices, indices,

assessments and other related information, graphs, tables and images

(“Data”) in this publication only for your personal use or, if you or your

company has a license for the Data from S&P Global Platts and you are

an authorized user, for your company’s internal business use only. You

may not publish, reproduce, extract, distribute, retransmit, resell, create

any derivative work from and/or otherwise provide access to the Data or

any portion thereof to any person (either within or outside your company,

including as part of or via any internal electronic system or intranet), firm

or entity, including any subsidiary, parent, or other entity that is affiliated

with your company, without S&P Global Platts’ prior written consent or

as otherwise authorized under license from S&P Global Platts. Any use

or distribution of the Data beyond the express uses authorized in this

paragraph above is subject to the payment of additional fees to S&P

Global Platts.

S&P Global Platts, its affiliates and all of their third-party licensors

disclaim any and all warranties, express or implied, including, but not

limited to, any warranties of merchantability or fitness for a particular

purpose or use as to the Data, or the results obtained by its use or as to

the performance thereof. Data in this publication includes independent

and verifiable data collected from actual market participants. Any user of

the Data should not rely on any information and/or assessment contained

therein in making any investment, trading, risk management or other

decision. S&P Global Platts, its affiliates and their third-party licensors do

not guarantee the adequacy, accuracy, timeliness and/or completeness

of the Data or any component thereof or any communications (whether

written, oral, electronic or in other format), and shall not be subject to

any damages or liability, including but not limited to any indirect, special,

incidental, punitive or consequential damages (including but not limited to,

loss of profits, trading losses and loss of goodwill).

Permission is granted for those registered with the Copyright Clearance

Center (CCC) to copy material herein for internal reference or personal use

only, provided that appropriate payment is made to the CCC, 222 Rosewood

Drive, Danvers, MA 01923, phone +1-978-750-8400. Reproduction in any

other form, or for any other purpose, is forbidden without the express prior

permission of S&P Global Inc. For article reprints contact: The YGS Group,

phone +1-717-505-9701 x105 (800-501-9571 from the U.S.).

For all other queries or requests pursuant to this notice, please contact

S&P Global Inc. via email at [email protected].

ACKNOWLEDGEMENTS

Key contributions to this report from: Bruno Brunetti (Managing Director, Global Power, PIRA Energy), Henry Cooke (Editor in Chief, Steel Business Briefing), Henry Edwardes-Evans (Associate Editorial Director, Platts Power In Europe), Robert Perkins (Senior Writer, Petroleum News), Glenn Rickson (Head of Power Analysis, Platts Analytics), Jean-Michel Six (Chief Economist EMEA, S&P Global Ratings), Kerry Thacker-Smith (Senior Power Analyst, Platts Analytics)