Embed Size (px)

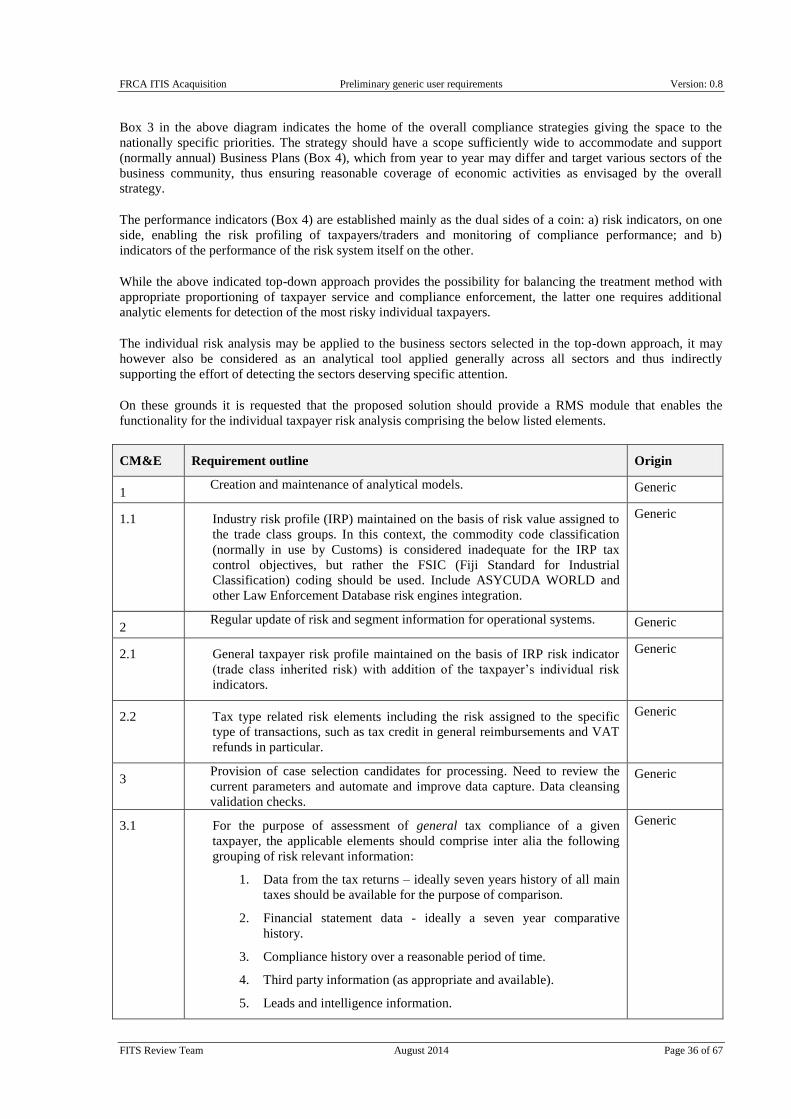

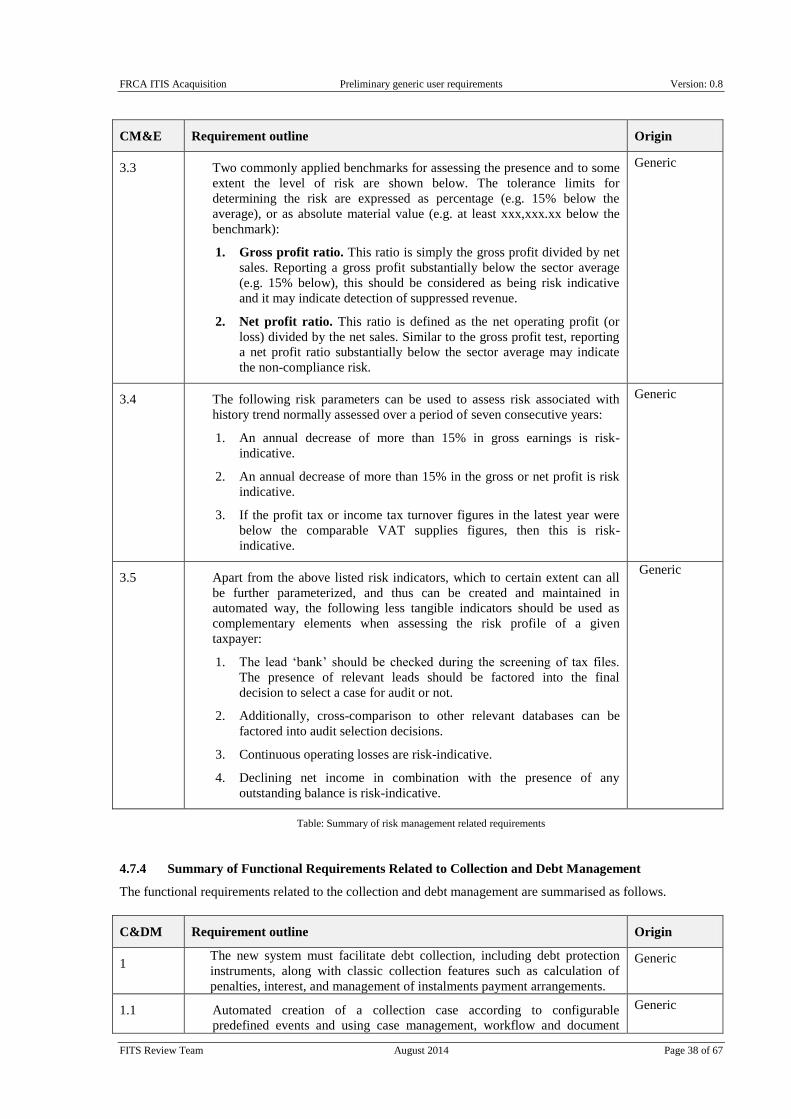

Citation preview

FRCA Implementation of

Integrated Tax System

Requirement Specification Catalogue (RSC)

-- Generic User Requirements --

FITS Review Team August 2014

FRCA ITIS Acquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 2 of 67

Contents

1 TERMS AND ABBREVIATIONS ............................................................................................................. 5

2 INTRODUCTION AND BACKGROUND ................................................................................................ 7

3 CURRENT STATE OF AFFAIRS ............................................................................................................. 7

3.1 GENERAL OUTLINE .................................................................................................................................... 7 3.2 CURRENT FRCA ORGANISATIONAL STRUCTURE ....................................................................................... 9 3.3 FRCA BPS ................................................................................................................................................. 9

4 REQUIREMENTS FOR THE NEW SYSTEM ...................................................................................... 10

4.1 ENVISAGED FUTURE BP STRUCTURE ....................................................................................................... 10 4.1.1 Legislation and Policy ................................................................................................................... 11 4.1.2 Taxpayer Registration ................................................................................................................... 11 4.1.3 Assess Tax ...................................................................................................................................... 11 4.1.4 Debt Management & Collection of Tax ......................................................................................... 12 4.1.5 Make Disbursements ...................................................................................................................... 12 4.1.6 Provide Information Taxpayer Services ........................................................................................ 12

4.2 REQUIREMENT TEMPLATES ...................................................................................................................... 12 4.3 TAXES TO BE COMPUTERISED .................................................................................................................. 14 4.4 GENERAL REQUIREMENTS ....................................................................................................................... 14

4.4.1 Summary of General Requirements ............................................................................................... 15 4.5 SYSTEM ARCHITECTURE AND DESIGN APPROACH ................................................................................... 18

4.5.1 Summary of Requirements Related to the System Architecture and Design .................................. 22 4.5.2 Analysis of Existing IT Components .............................................................................................. 24 4.5.3 Integration Approach..................................................................................................................... 24

4.6 FUNCTIONAL MODEL ............................................................................................................................... 25 4.7 FUNCTIONAL REQUIREMENTS .................................................................................................................. 25

4.7.1 Summary of Functional Requirements Related to the Taxpayer Registration ............................... 26 4.7.2 Summary of Functional Requirements Related to the Assessment and Payments ......................... 28 4.7.3 Summary of Functional Requirements Related to the Compliance Monitoring and Enforcement 33 4.7.4 Summary of Functional Requirements Related to Collection and Debt Management ................... 38 4.7.5 Summary of Functional Requirements Related to Objections and Appeals ................................... 40 4.7.6 Summary of Functional Requirements Related to Taxpayer Services ........................................... 42 4.7.7 Security and Data Privacy Requirements ...................................................................................... 43 4.7.8 IT Operational Requirements ........................................................................................................ 44 4.7.9 Miscellaneous Requirements ......................................................................................................... 45

5 IMPLEMENTATION CONSIDERATIONS .......................................................................................... 46

5.1 OUTLINE .................................................................................................................................................. 47 5.2 CAPABILITY - CHANNEL DELIVERY ......................................................................................................... 47

5.2.1 Abstract .......................................................................................................................................... 47 5.2.2 Details ............................................................................................................................................ 48

5.3 CAPABILITY - CLIENT RELATIONSHIP MANAGEMENT .............................................................................. 49 5.3.1 Abstract .......................................................................................................................................... 49 5.3.2 Details ............................................................................................................................................ 49

5.4 CAPABILITY - REVENUE MANAGEMENT .................................................................................................. 49 5.4.1 Abstract .......................................................................................................................................... 49 5.4.2 Details ............................................................................................................................................ 49

5.5 CAPABILITY - CASE AND WORK MANAGEMENT ...................................................................................... 51 5.5.1 Abstract .......................................................................................................................................... 51 5.5.2 Details ............................................................................................................................................ 51

5.6 CAPABILITY - OUTCOME IMPROVEMENT .................................................................................................. 52 5.6.1 Abstract .......................................................................................................................................... 52 5.6.2 Details ............................................................................................................................................ 52

5.7 CAPABILITY - PLAN AND MANAGE ENTERPRISE ...................................................................................... 53 5.7.1 Abstract .......................................................................................................................................... 53 5.7.2 Details ............................................................................................................................................ 53

FRCA ITIS Acquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 3 of 67

5.8 CAPABILITY - ENABLERS ......................................................................................................................... 54 5.8.1 Abstract .......................................................................................................................................... 54 5.8.2 Details ............................................................................................................................................ 54

6 CHANGE MANAGEMENT ..................................................................................................................... 55

7 INDICATIVE DELIVERY PLAN AND PRELIMINARY SCHEDULE ............................................. 55

7.1 DURATION ............................................................................................................................................... 55 7.2 OVERVIEW ............................................................................................................................................... 55

8 INSTRUCTION TO TENDERERS ......................................................................................................... 56

8.1 GENERAL ................................................................................................................................................. 56 8.1.1 Cost of Tender ............................................................................................................................... 56

8.2 TENDER DOCUMENTS .............................................................................................................................. 56 8.2.1 Tender Procedure .......................................................................................................................... 56 8.2.2 General Responsibility of Tenderer ............................................................................................... 56 8.2.3 Clarification of Tender Documents ............................................................................................... 56 8.2.4 Amendment of Tender Documents ................................................................................................. 57

8.3 PREPARATION OF TENDERS ...................................................................................................................... 57 8.3.1 Language of Tender ....................................................................................................................... 57 8.3.2 Documents Comprising the Tender ............................................................................................... 57 8.3.3 Tender Prices ................................................................................................................................. 57 8.3.4 Tender Currencies ......................................................................................................................... 57 8.3.5 Documents Establishing Good's Conformity to Tender Documents .............................................. 57 8.3.6 Tender Security .............................................................................................................................. 58 8.3.7 Period of Validity of Tenders ......................................................................................................... 58 8.3.8 Format and Signing of Tender ....................................................................................................... 58

8.4 SUBMISSION OF TENDERS ........................................................................................................................ 58 8.4.1 Sealed Envelopes ........................................................................................................................... 58 8.4.2 Number of Proposals ..................................................................................................................... 58 8.4.3 All envelopes shall: ........................................................................................................................ 59 8.4.4 Deadline for Submission of Tenders .............................................................................................. 59 8.4.5 Late Tenders .................................................................................................................................. 59 8.4.6 Modification and Withdrawal of Tenders ...................................................................................... 59 8.4.7 Preliminary Examination ............................................................................................................... 59 8.4.8 Clarification of Tenders ................................................................................................................. 59 8.4.9 Evaluation of Technical Proposals ................................................................................................ 60 8.4.10 Screening of requirements ........................................................................................................ 60 8.4.11 Layout of Technical Proposals ................................................................................................. 60 8.4.12 Presentations ............................................................................................................................ 60 8.4.13 Scoring of Technical Proposals ................................................................................................ 60 8.4.14 Short listed technical proposals ................................................................................................ 60 8.4.15 Demonstrations ......................................................................................................................... 61 8.4.16 Solutions Presentation and Demo ............................................................................................. 61 8.4.17 Final Short-listed Solutions ...................................................................................................... 61 8.4.18 Envelopes containing the financial proposals of Tenderers shall be opened provided that the

technical proposal: ...................................................................................................................................... 61 8.4.19 Financial Evaluation ................................................................................................................ 61

8.5 AWARD OF CONTRACT ............................................................................................................................. 62 8.5.1 Award of Tender ............................................................................................................................ 62 8.5.2 Award Criteria ............................................................................................................................... 62 8.5.3 Purchaser's right to accept any Tender and to reject any or all Tenders ...................................... 62 8.5.4 Notification of Award .................................................................................................................... 62 8.5.5 Signing of Contract ........................................................................................................................ 62 8.5.6 Performance Security .................................................................................................................... 63 8.5.7 Delivery Schedule .......................................................................................................................... 63

Tables TABLE: TERMS AND ABBREVIATIONS ....................................................................................................................... 7

FRCA ITIS Acquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 4 of 67

TABLE: THE CONCEPT OF FUNCTIONAL AND SERVICE REQUIREMENTS ................................................................... 12 TABLE: THE TEMPLATE FOR FUNCTIONAL AND SELECTED MISCELLANEOUS REQUIREMENTS ................................. 13 TABLE: THE TEMPLATE FOR OTHER GROUPS OF REQUIREMENTS ............................................................................ 13 TABLE: MAIN GENERAL REQUIREMENTS ................................................................................................................ 18 TABLE: SUMMARY OF REQUIREMENTS RELATED TO THE COTS ARCHITECTURE AND DESIGN ................................ 24 TABLE: DECLARATIONS AND PAYMENTS VOLUME FOR 2013 .................................................................................. 24 TABLE: SUMMARY TAXPAYER REGISTRATION REQUIREMENTS .............................................................................. 27 TABLE: SELECTED DETAILS OF TAXPAYER REGISTRATION REQUIREMENTS ............................................................ 28 TABLE: SUMMARY TAXPAYER ASSESSMENT AND PAYMENT REQUIREMENTS ......................................................... 29 TABLE: SELECTED DETAILS OF TAXPAYER RETURN MANAGEMENT ........................................................................ 30 TABLE: SELECTED DETAILS OF TAXPAYER PAYMENT PROCESSING ......................................................................... 31 TABLE: SELECTED DETAILS OF TAXPAYER AND REVENUE ACCOUNTING ................................................................ 33 TABLE: SUMMARY OF REQUIREMENTS RELATED TO THE COMPLIANCE MONITORING AND ENFORCEMENT ............. 35 TABLE: SUMMARY OF RISK MANAGEMENT RELATED REQUIREMENTS .................................................................... 38 TABLE: SUMMARY OF REQUIREMENTS RELATED TO THE COLLECTION OF ARREARS AND DEBT MANAGEMENT....... 39 TABLE: SELECTED DETAILS RELATED TO DEBT COLLECTION AND MANAGEMENT .................................................. 40 TABLE: SUMMARY OF REQUIREMENTS RELATED TO THE OBJECTIONS AND APPEALS .............................................. 41 TABLE: FRAMEWORK OF E-SERVICES (SOURCE OECD) .......................................................................................... 42 TABLE: SUMMARY OF SELECTED TAXPAYER SERVICE REQUIREMENTS ................................................................... 43 TABLE: SECURITY AND DATA PRIVACY RELATED REQUIREMENTS .......................................................................... 43 TABLE: SUMMARY OF OPERATIONAL REQUIREMENTS ............................................................................................ 44 TABLE: SUMMARY OF MISCELLANEOUS REQUIREMENTS ........................................................................................ 46 TABLE: DELIVERY CHANNELS ................................................................................................................................ 49 TABLE: CRM ......................................................................................................................................................... 49 TABLE: REVENUE MANAGEMENT ........................................................................................................................... 51 TABLE: CASE AND WORKFLOW MANAGEMENT ....................................................................................................... 52 TABLE: OUTCOME IMPROVEMENT .......................................................................................................................... 53 TABLE: ENTERPRISE PLANNING AND MANAGEMENT .............................................................................................. 53 TABLE: ENABLERS ................................................................................................................................................. 54 TABLE: INDICATIVE DELIVERY PLAN ..................................................................................................................... 56

Diagrams DIAGRAM: FUNCTIONAL GROUPING OF BPS ........................................................................................................... 10 DIAGRAM: CORE BUSINESS OF FRCA TAXATION DIVISION ................................................................................... 11 DIAGRAM: THE LIAM IMPLEMENTATION OF THE TTT PRINCIPLE .......................................................................... 22 DIAGRAM: ENVISAGED GENERAL FUNCTIONAL STRUCTURE AND MAIN INFORMATION FLOW ................................. 25 DIAGRAM: STRATEGIC RISK MANAGEMENT CYCLE MODEL .................................................................................. 35 DIAGRAM: TAX REFERENCE MODEL ...................................................................................................................... 47

FRCA ITIS Acquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 5 of 67

1 TERMS AND ABBREVIATIONS

Terms and abbreviations used in this document and attachments have the meaning as shown in the table below.

Term/abbreviation Meaning

ACCU Amendment Correspondence & Control Unit

ASYCUDA Automated System of Customs Data

BA Business Analyst

BCP Business Continuity Plan

BP Business Process

BR Business Rule

BS Bureau of Statistics

CAAF Civil Aviation Authority of Fiji

CT Corporate Tax

COTS Custom Off The Shelf

CRM Customer Relationship Management

DB Data base

DBMS (DB) Data base management system

DMS Debt Management Services

DoI Department of Immigration

DR Disaster Recovery

EMS Employer Monthly Summary

FAQ Frequently asked questions

FIA Fiji Institute of Accountants

FITS Fiji Integrated Tax System

FNPF Fiji National Provident Fund

FRCA Fiji Revenue & Customs Authority

FSIC Fiji Standard Industrial Classification

GTT Gambling Turnover Tax

HR Human Resources

HR21 Employee & Manager Self Service Kiosk

HW Computer Hardware

ICT Information and Communication Technology

IMF International Monetary Fund

FRCA ITIS Acquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 6 of 67

Term/abbreviation Meaning

IRP Industry Risk Profile

IS Information System

IT Information Technology

ITIS The new Integrated Tax Information System

JID Joint Identification Card

LEU Lodgement Enforcement Unit

LIAM Logical Information Architecture Model

LP Legal person; business entity.

LTA Land Transport Authority

MIS Management Information System

MoF Ministry of Finance

MoJ Ministry of Justice

NGO Non-governmental organization

Nil Return A nil declaration, i.e. the tax period without economic result

NOA Notice of Assessment

NP Natural Person

OECD Organization for European Cooperation and Development

PAYE Final Pay As You Earn As Final Tax

PFTAC Pacific Financial Technical Assistance Centre

PM Project Manager

QA Quality Assurance

RA Revenue Accounting

RBF Reserve Bank of Fiji

REALB Real Estate Licensing Board

Registrar BDM Registrar of Births, Deaths & Marriage

RMS Risk Management System

RSC Requirement Specification Catalogue

SC Steering Committee

SDD Systems design documentation

SOA Service oriented architecture.

SOP Standard Operating Procedures

SPoE Single Point of Entry

SUN SunSystems

FRCA ITIS Acquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 7 of 67

Term/abbreviation Meaning

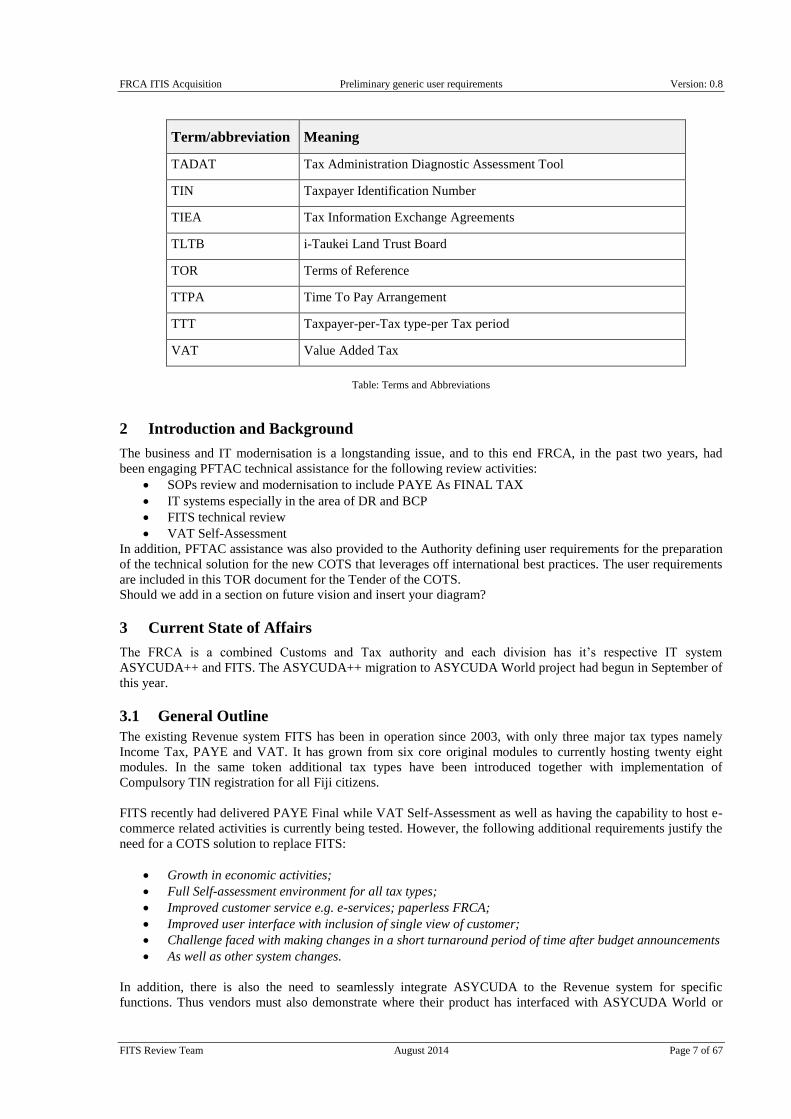

TADAT Tax Administration Diagnostic Assessment Tool

TIN Taxpayer Identification Number

TIEA Tax Information Exchange Agreements

TLTB i-Taukei Land Trust Board

TOR Terms of Reference

TTPA Time To Pay Arrangement

TTT Taxpayer-per-Tax type-per Tax period

VAT Value Added Tax

Table: Terms and Abbreviations

2 Introduction and Background

The business and IT modernisation is a longstanding issue, and to this end FRCA, in the past two years, had

been engaging PFTAC technical assistance for the following review activities:

SOPs review and modernisation to include PAYE As FINAL TAX

IT systems especially in the area of DR and BCP

FITS technical review

VAT Self-Assessment

In addition, PFTAC assistance was also provided to the Authority defining user requirements for the preparation

of the technical solution for the new COTS that leverages off international best practices. The user requirements

are included in this TOR document for the Tender of the COTS.

Should we add in a section on future vision and insert your diagram?

3 Current State of Affairs

The FRCA is a combined Customs and Tax authority and each division has it‘s respective IT system

ASYCUDA++ and FITS. The ASYCUDA++ migration to ASYCUDA World project had begun in September of

this year.

3.1 General Outline

The existing Revenue system FITS has been in operation since 2003, with only three major tax types namely

Income Tax, PAYE and VAT. It has grown from six core original modules to currently hosting twenty eight

modules. In the same token additional tax types have been introduced together with implementation of

Compulsory TIN registration for all Fiji citizens.

FITS recently had delivered PAYE Final while VAT Self-Assessment as well as having the capability to host e-

commerce related activities is currently being tested. However, the following additional requirements justify the

need for a COTS solution to replace FITS:

Growth in economic activities;

Full Self-assessment environment for all tax types;

Improved customer service e.g. e-services; paperless FRCA;

Improved user interface with inclusion of single view of customer;

Challenge faced with making changes in a short turnaround period of time after budget announcements

As well as other system changes.

In addition, there is also the need to seamlessly integrate ASYCUDA to the Revenue system for specific

functions. Thus vendors must also demonstrate where their product has interfaced with ASYCUDA World or

FRCA ITIS Acquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 8 of 67

another customs system as well as successful integration with any other revenue system in the past. The diagram

below depicts the integration needs of the Authority:

ASYCUDA WORLD, EMPLOYERS, FNPF, LOCAL GOVT, REGISTRAR BDM, REGISTRAR COMPANIES, TITLES, BANKS, LTA, TLTB,

INVESTMENT FIJI, IMMIGRATION, LANDS

National Switch

Reserve Bank of Fiji

Commercial Banks

Merchants

EFTPOS Network

Importers/Exporters

International BanksVisa Member Banks

FRCA ITIS Acquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 9 of 67

3.2 Current FRCA Organisational Structure

Diagram: FRCA Organisational Structure

Review the structure – some functions are not in the correct box e.g. TEPU/TIPU are now part of DMS, Benefits no longer a fn of HR

3.3 FRCA BPs

Currently the business processes of FRCA are largely guided by Legislation as well as the various Taxation

functional units. For this reason the provision of the new COTS should include the task of analysis and revision

of all main BPs to ensure the adoption of an end to end process approach and reduce the opportunity for siloed

functional approaches.

It should be determined which processes are obsolete or should be amended, which processes to include with the

view of automation, and which processes should preferably remain manual. In turn, this will serve dual purpose:

a) Easing the understanding of the current FRCA BPs; and

b) Transferring the skills and BP analysis related experience to FRCA.

In addition, the following high-level business rules must be adhered to:

The business requirements must drive IT and are the key to the future IT environment.

Understanding the total cost of a solution from both an implementation and on-going support needs is a

critical requirement for IT decision making.

Maintain a balance between innovation and risk, by carefully assessing risks against potential benefits

when considering the adoption of new technology.

IT decisions are made to provide maximum benefit to the Revenue Administration as a whole.

IT investments are recognized as FRCA corporate assets and are managed accordingly.

Ensure appropriate system security is in place so that information and systems are protected from

unauthorized use and disclosure.

Information is recognized as an asset and must be managed accordingly.

As much as possible there should be ―one version of the truth‖, e.g. collect data once but access it many

times.

IT systems are designed and implemented allowing for reuse by other business processes, e.g. one case

management system for Audit, Debt and Investigations.

Minimize the number of different technologies and products providing the same or similar service.

Capacity must be anticipated and maintained to ensure appropriate responsiveness to end users.

Every IT solution should have disaster recovery addressed as part of the implementation plan.

Hardware and operating systems must operate in an environment where the software is only one version

behind the latest released one.

Commercially developed package software should be purchased whenever possible, rather than build

specific software products just for FRCA.

There must be one central point of taxpayer registration.

Attempt to collect revenue at the original source as much as possible—adopt a full and final approach.

Minimize any customization of the COTS solution—change the business process first before

customizing the COTS.

FRCA ITIS Acquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 10 of 67

End to end business processes must be designed, not functional based siloed processes.

Design these processes by ―being in the shoes of the customer‖—ensure end customers are involved in

business process design, e.g. FIA, groups of taxpayers, etc.

Adopt a ―whole of government ―approach—if another government agency has the taxpayer information

already, how can FRCA access this through system integration?

The current BPs is being updated from an SOP or Operations Manual perspective and it is expected that the use

of these manuals will enable the successful vendor to better understand the current FRCA environment. In

addition, these manuals should be a minimal benchmark of any future Operational Manual(s) /SOP(s) arising

from the new COTS. The successful vendor is required to design a process that will enable FRCA to maintain

these manuals on an on-going basis.

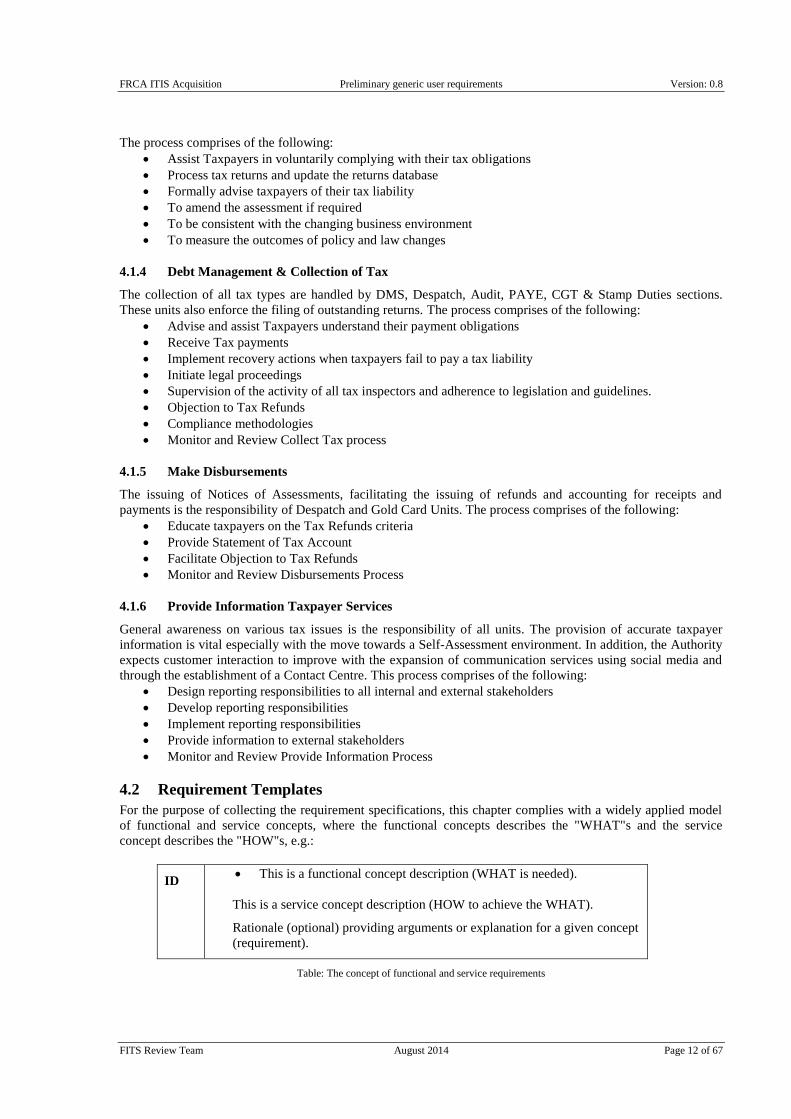

4 Requirements for the New System

4.1 Envisaged Future BP Structure

The FRCA core functions and consequently those of the COTS are closely related to encouraging and servicing

taxpayers to correctly account for their obligations and comply with tax legislation. FRCA is directly responsible

for collecting national taxes, supervising compliance with local taxes, as well as implementing Double Tax

Agreements and TIEA‘s. The main core business processes can be divided into the following groups also

forming the high level business logic of COTS functionality.

1. Legislation and Policy - To ensure better, more effective tax policy development and giving effect to

them through law

2. Taxpayer Registration - To record taxpayer entities in the system.

3. Assess Tax – Determine the correct tax liability

4. Debt Management & Collection of Tax - For taxpayers to file returns and pay taxes due.

5. Make Disbursements - To refund entitlements and issue NOA to taxpayers

6. Provide Information Taxpayer Services - To assist in future planning.

The diagram below depicts major groups of business function within this classification.

Taxation

Core FunctionsManagement of Taxpayers and

Revenue

Organizational Functions

Registration Policy & Law

Collect TaxAssess Tax

Providing Information

Disbursement

Revenue Collection

Audit & Compliance

Functions Customs

Debt Management

Services

Corporate Governance

External

Diagram: Functional grouping of BPs/Review fn grouping e.g. TEPU/TIPU are now part of DMS

FRCA ITIS Acquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 11 of 67

The requirements of this RSC focus largely on the first group of tasks representing the core business of the

Taxation Division illustrated by the next diagram and to applicable extent, other task and processes are dealt

with or referred to; e.g. legal implications, strategic compliance enforcement planning and risk management.

Diagram: Core business of FRCA Taxation Division

4.1.1 Legislation and Policy

The centrally placed Policy & Legal Units are tasked with the responsibility for developing better and more

effective tax policies and giving effect to them through law. The current Low Rate Broad Base Tax policy is

expected to facilitate Fiji‘s economic growth to 3.6% in 2014. The main groups of business processes, most of

which relate to the change management performed by Policy & Legal comprise:

To regulate preferential tax policies

To ensure that the Policy & Law process is fit for purpose

To reflect tax policy and law changes

Implement legal proceedings

Legal support and processing of objections and appeals.

To measure the outcomes of the policy and law changes

To be consistent with changing business environment

4.1.2 Taxpayer Registration

The registrations of all new taxpayers and issue of Joint ID Cards are handled at the Customer Service Centres.

The process comprises of the following:

To improve understanding of the Registration process

To enable taxpayer entities to register for tax purpose

To formally confirm tax registration of taxpayer entities

To update Taxpayer registration database

To deregister the taxpayer following a change in their circumstances

To measure the outcomes of the registration process

To be consistent with the changing business environment

To issue Joint ID Cards to individuals.

4.1.3 Assess Tax

Authority-based assessments are currently being handled by several units including Processing, Technical,

Companies, Gold Card, CGT & Stamp Duties while Self-Assessed returns inclusive of FBT, STT & CCL are

processed by the Data Entry Unit.

On the other hand, the approval process of refunds are currently handled by Processing, Technical, Companies,

Gold Card, with approvers being Chief Assessors, NMRC and GMT.

Monitoring of

economixc

activities

Voluntary

registration

Forced

registration

Deregistration

Tax type

entitlement

Filing

compliance

Declaration

compliance

Payment

compliance

no

Debt

management

IS

Risk

management

FRCA ITIS Acquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 12 of 67

The process comprises of the following:

Assist Taxpayers in voluntarily complying with their tax obligations

Process tax returns and update the returns database

Formally advise taxpayers of their tax liability

To amend the assessment if required

To be consistent with the changing business environment

To measure the outcomes of policy and law changes

4.1.4 Debt Management & Collection of Tax

The collection of all tax types are handled by DMS, Despatch, Audit, PAYE, CGT & Stamp Duties sections.

These units also enforce the filing of outstanding returns. The process comprises of the following:

Advise and assist Taxpayers understand their payment obligations

Receive Tax payments

Implement recovery actions when taxpayers fail to pay a tax liability

Initiate legal proceedings

Supervision of the activity of all tax inspectors and adherence to legislation and guidelines.

Objection to Tax Refunds

Compliance methodologies

Monitor and Review Collect Tax process

4.1.5 Make Disbursements

The issuing of Notices of Assessments, facilitating the issuing of refunds and accounting for receipts and

payments is the responsibility of Despatch and Gold Card Units. The process comprises of the following:

Educate taxpayers on the Tax Refunds criteria

Provide Statement of Tax Account

Facilitate Objection to Tax Refunds

Monitor and Review Disbursements Process

4.1.6 Provide Information Taxpayer Services

General awareness on various tax issues is the responsibility of all units. The provision of accurate taxpayer

information is vital especially with the move towards a Self-Assessment environment. In addition, the Authority

expects customer interaction to improve with the expansion of communication services using social media and

through the establishment of a Contact Centre. This process comprises of the following:

Design reporting responsibilities to all internal and external stakeholders

Develop reporting responsibilities

Implement reporting responsibilities

Provide information to external stakeholders

Monitor and Review Provide Information Process

4.2 Requirement Templates

For the purpose of collecting the requirement specifications, this chapter complies with a widely applied model

of functional and service concepts, where the functional concepts describes the "WHAT"s and the service

concept describes the "HOW"s, e.g.:

ID This is a functional concept description (WHAT is needed).

This is a service concept description (HOW to achieve the WHAT).

Rationale (optional) providing arguments or explanation for a given concept

(requirement).

Table: The concept of functional and service requirements

FRCA ITIS Acquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 13 of 67

At this stage the focus is on functional concepts as most decisions about HOW are not relevant until later. It is

only when the service concept is of importance, or when clear directions are already available, assumed or

strictly recommended, that the service concept is included.

The requirements included in the remainder of the chapter is drafted to the level of granularity and details

expected to be adequate for the inclusion of the envisaged tender dossier to be prepared in the consequent stages

of the COTS acquisition process. For that purpose the requirements are divided into the following groups:

1. Taxes to be computerised.

2. General requirements.

3. Requirements regarding the systems architecture and design approach.

4. Functional model and requirements, sub-divided according to the main functions.

5. Security and data privacy requirements.

6. IT operational requirements.

7. Miscellaneous requirements.

The functional requirements (4) and partial requirements from other groups are structured as shown with three

additional columns indicating the existence of the requirement in existing system, mandatory requirement, and a

proposal based on best practice.

ID This is a functional concept description (WHAT is

needed).

This is a service concept description (HOW to

achieve the WHAT).

Rationale (optional) providing arguments or

explanation for a given concept (requirement).

Existing Mandatory Proposal

Table: The template for functional and selected miscellaneous requirements

Yet other requirements, while following the same functional or service concept are collected with an additional

column showing the origin of a given requirement, which could be either generic (according to acknowledged

international practice) or indicating an authority, organization, a department or an entity as the source of its

origin.

ID This is a functional concept description (WHAT is needed).

This is a service concept description (HOW to achieve the WHAT).

Rationale (optional) providing arguments or explanation for a given

concept (requirement).

Origin

Table: The template for other groups of requirements

As appropriate, the structured and numbered requirements are accompanied by narrative lead-in paragraphs or

explanatory comments.

FRCA ITIS Acquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 14 of 67

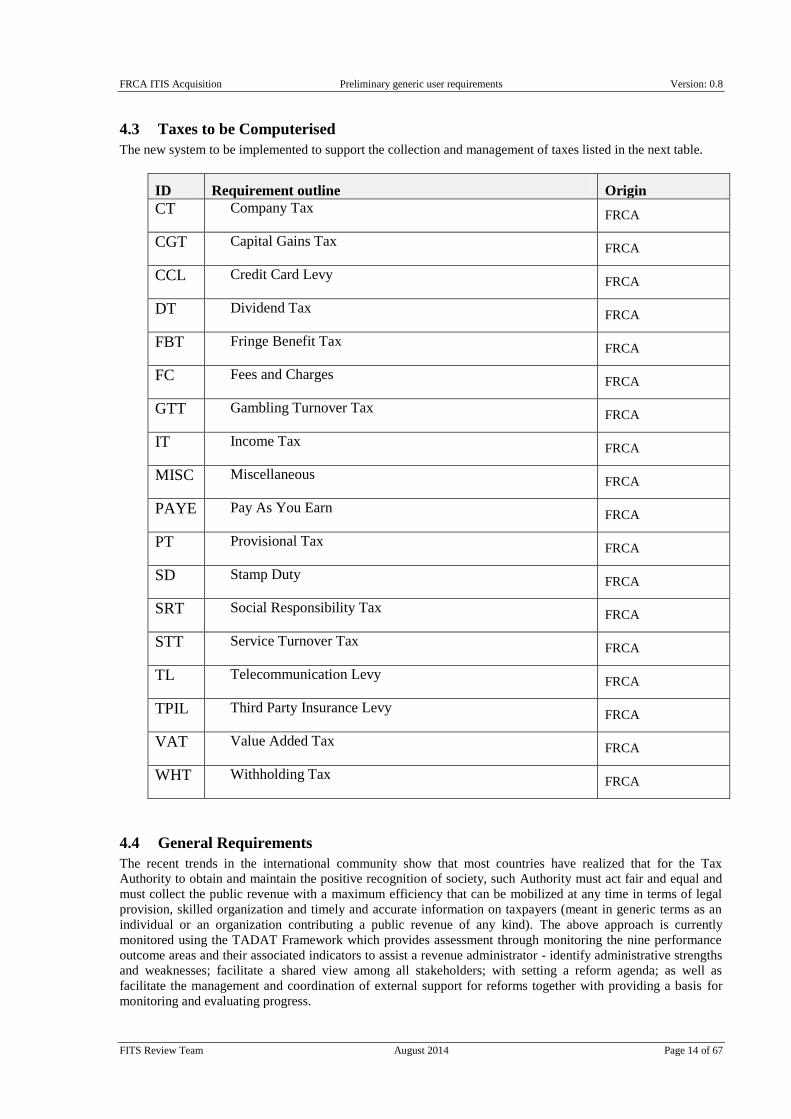

4.3 Taxes to be Computerised

The new system to be implemented to support the collection and management of taxes listed in the next table.

ID Requirement outline Origin

CT Company Tax FRCA

CGT Capital Gains Tax FRCA

CCL Credit Card Levy FRCA

DT Dividend Tax FRCA

FBT Fringe Benefit Tax FRCA

FC Fees and Charges FRCA

GTT Gambling Turnover Tax FRCA

IT Income Tax FRCA

MISC Miscellaneous FRCA

PAYE Pay As You Earn FRCA

PT Provisional Tax FRCA

SD Stamp Duty FRCA

SRT Social Responsibility Tax FRCA

STT Service Turnover Tax FRCA

TL Telecommunication Levy FRCA

TPIL Third Party Insurance Levy FRCA

VAT Value Added Tax FRCA

WHT Withholding Tax FRCA

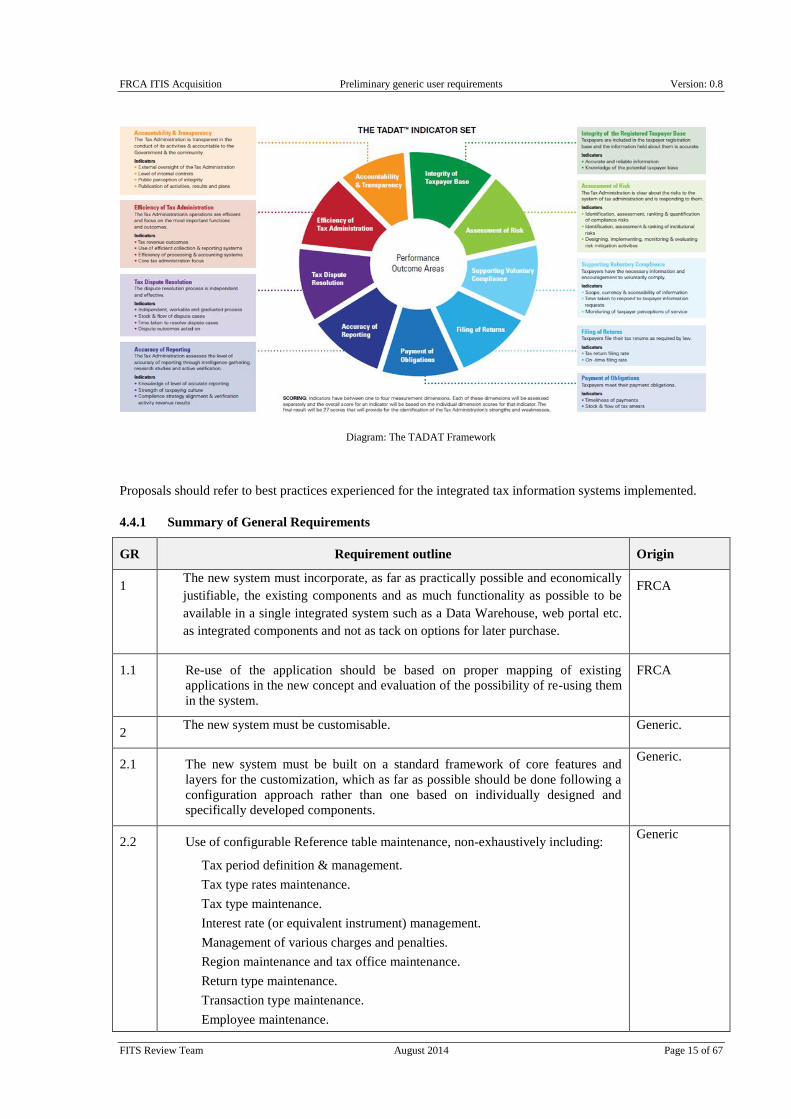

4.4 General Requirements

The recent trends in the international community show that most countries have realized that for the Tax

Authority to obtain and maintain the positive recognition of society, such Authority must act fair and equal and

must collect the public revenue with a maximum efficiency that can be mobilized at any time in terms of legal

provision, skilled organization and timely and accurate information on taxpayers (meant in generic terms as an

individual or an organization contributing a public revenue of any kind). The above approach is currently

monitored using the TADAT Framework which provides assessment through monitoring the nine performance

outcome areas and their associated indicators to assist a revenue administrator - identify administrative strengths

and weaknesses; facilitate a shared view among all stakeholders; with setting a reform agenda; as well as

facilitate the management and coordination of external support for reforms together with providing a basis for

monitoring and evaluating progress.

FRCA ITIS Acquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 15 of 67

Diagram: The TADAT Framework

Proposals should refer to best practices experienced for the integrated tax information systems implemented.

4.4.1 Summary of General Requirements

GR Requirement outline Origin

1 The new system must incorporate, as far as practically possible and economically

justifiable, the existing components and as much functionality as possible to be

available in a single integrated system such as a Data Warehouse, web portal etc.

as integrated components and not as tack on options for later purchase.

FRCA

1.1 Re-use of the application should be based on proper mapping of existing

applications in the new concept and evaluation of the possibility of re-using them

in the system.

FRCA

2 The new system must be customisable. Generic.

2.1 The new system must be built on a standard framework of core features and

layers for the customization, which as far as possible should be done following a

configuration approach rather than one based on individually designed and

specifically developed components.

Generic.

2.2 Use of configurable Reference table maintenance, non-exhaustively including:

Tax period definition & management.

Tax type rates maintenance.

Tax type maintenance.

Interest rate (or equivalent instrument) management.

Management of various charges and penalties.

Region maintenance and tax office maintenance.

Return type maintenance.

Transaction type maintenance.

Employee maintenance.

Generic

FRCA ITIS Acquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 16 of 67

GR Requirement outline Origin

Reasons maintenance.

Adjustment type maintenance.

FSIC code maintenance.

Transaction class maintenance.

Registration status maintenance.

Registration reasons maintenance.

Case type code maintenance.

Criteria type code maintenance.

3 The new system must provide full history of reference data. Generic

FRCA ITIS Acquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 17 of 67

GR Requirement outline Origin

4 The new system must provide a full suite of tax related functionality including a

comprehensive Risk Management System component.

Generic

5 The new system must provide comprehensive data exchange capability for

systematic exchange of relevant data internally (e.g. ASYCUDA World, SUN,

HR21) as well as with other public authorities and private sector 3rd

party

information providers.

Generic

5.1 This involves several external entities: RBF, Investment Fiji, Local Governments,

CAAF, Ministry of Lands, MoF, Bureau of Statistics, MoJ (Registrar of

Company, Registrar of Titles and Birth, Death & Marriage), DoI, LTA, Banks,

REALB and Telecommunication Providers, etc.

FRCA

6 The new system must provide comprehensive Case Management and tracking

capability features.

Generic.

7 The new system must provide comprehensive Document Management. Generic

8 The new system must provide comprehensive MIS, comprising predefined

reports, ad hoc queries and ad hoc report generation.

Generic.

9 The new system must provide support for processing paper based information as

well as electronic processing, i.e. e-filing, e-payments, enquiries, bilateral

exchange of data with taxpayers, etc.

Generic.

10 The new system must provide comprehensive documentation, including system

administration and maintenance literature and user guides. It is required that

online training and all support documentation must be available electronically and

that these must be able to be maintained on an ongoing basis in an effective and

efficient manner.

Generic.

10.1 User manuals must be available as a comprehensive onscreen context sensitive

help system.

Generic.

10.2 System maintenance and operations related manuals to be provided in electronic

form and hard copy.

Generic.

10.3 As a minimum, the following functionalities are generally required for all

overviews and reports:

Screen display.

Appropriate hardcopy printout.

Selected data export.

Mandatory electronic data submission.

Reasonable set up of restrictions and criteria.

Smart search by chosen fields.

Sorting settings.

Saving and selection of prepared settings for shared use.

Generic.

11 The new system must be fully operational by the end of 2016 with migration of its FRCA

FRCA ITIS Acquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 18 of 67

GR Requirement outline Origin

selected components from 2015

12 The new system must be able to import and export data in various formats with

clear data migration plans and a proposed best practise migration model clearly

defined.

Generic.

13 There must be substantial public awareness about the new system. Generic

14 The analysis of tax processes and product optimization regarding the specifics of

the tax process is required.

Generic

14.1 Mapping of current BP presenting "as is" situation. Generic

14.2 Proposing relevant modernization and optimization of all business critical

processes based on the vendor's own reference model and recognized best

practice.

Generic

14.3 Preparing BP model, which includes simulation of automated processes. Generic

15 All user screens, user manuals, and basic technical system support in English

language. The basic configuration ensures that there is no need to create new

program versions for language versions.

FRCA

16 The proposed system should support multi-lingual solution just as all user screens,

user manuals, and basic technical system support must be provided in the English

language.

FRCA

17 The new system must ensure secure, authorised and auditable/traceable access to

taxpayers' data, which in principle and by nature is sensitive and should be

protected accordingly;

Generic

17.1 Vendors may propose use of recognized products for the purposes of

authorization and authentication.

Generic

18 The User Administration module of the new system must use the domain and

privilege of the system administrator, who in turn may assign a subset of his

rights in accordance with security requirements to the so-called advanced users.

Generic

19 Comprehensive risk management is mandatory. Generic

20 The new system should be configured for electronic filing of purchases/sales

books. Generic

21 The new system should be configured for electronic filing of payroll lists and all

related evaluations (business rules applicable). Generic

Table: Main general requirements

4.5 System Architecture and Design Approach

This section provides requirements for selected technical elements related to the new COTS architecture and

design approach. A general view of the new system is based on expectations that it will satisfy all of the

following main demands:

FRCA ITIS Acquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 19 of 67

The new system's architecture will consist of two main layers, i.e. the internal COTS specific

architecture and common services provided by relevant governmental institutions.

The internal COTS specific architecture will be formed by the core tax information system, potentially

a standard or standardized system, integrated at adequate level with the selected components from the

existing IT structure.

The new system must be designed to satisfy the demands for:

1. Multi-tier architecture comprising separate layers for presentation, business logic and database

management.

2. Web based multilingual user interface utilizing a thin web client.

3. Web services provided by loosely coupled components.

4. Business logic layer driven by business rules – a precondition for fulfilling the ambition of national

customization mainly through configuration rather than through (re-)design and (re-)development.

5. Compliance with the Logical Information Architecture Model (LIAM) for integrated revenue

management.

The following diagrams depict a simplified system architecture model; outline the multi-layer system

architecture and present the LIAM built upon the Taxpayer-per-Tax type-per Tax period (TTT)

principle.

The new system architecture should include currently required services and should be able to include

any number of future services within the same service layer. These services should be configurable

based on business rules reflecting the legislative acts.

FRCA ITIS Acquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 20 of 67

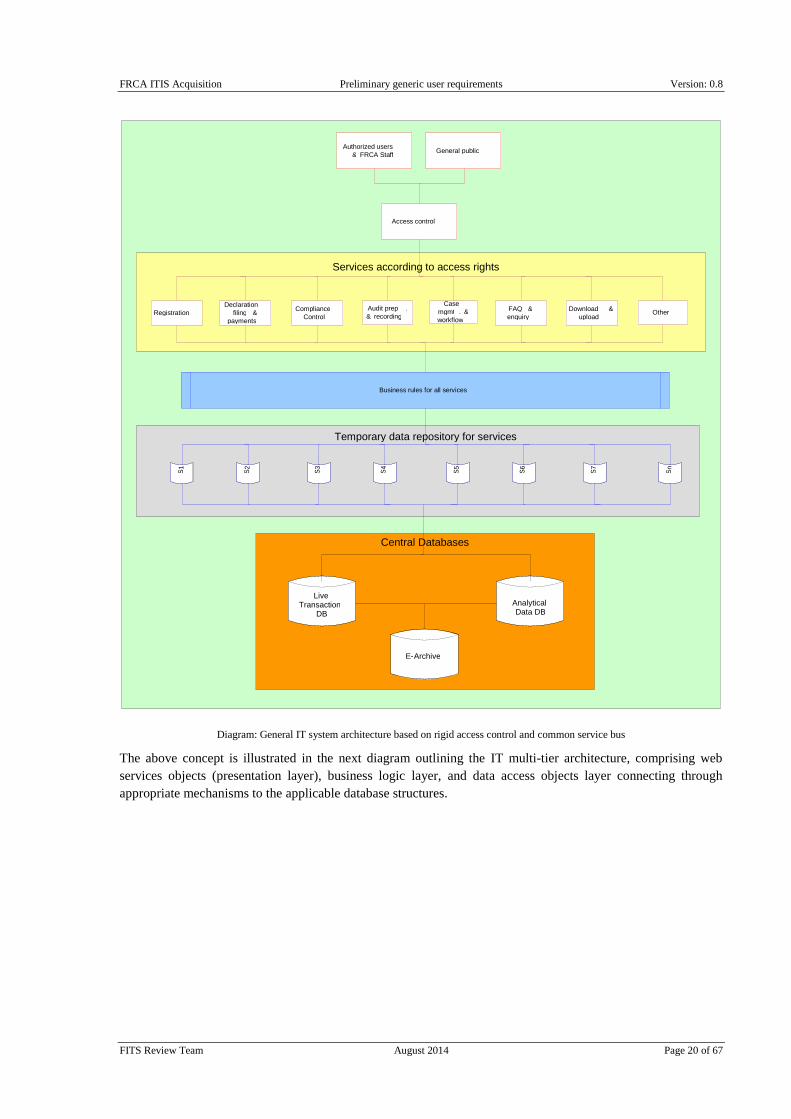

Diagram: General IT system architecture based on rigid access control and common service bus

The above concept is illustrated in the next diagram outlining the IT multi-tier architecture, comprising web

services objects (presentation layer), business logic layer, and data access objects layer connecting through

appropriate mechanisms to the applicable database structures.

Authorized users & FRCA Staff General public

Access control

Registration Declaration

filing & payments

Compliance Control

Audit prep . & recording

Case mgmt . & workflow

FAQ & enquiry

Download & upload Other

S 1

S 2

S 3

S 4

S 5

S 6

S 7

S n

Business rules for all services

Live Transaction

DB Analytical Data DB

E - Archive

Services according to access rights

Temporary data repository for services

Central Databases

FRCA ITIS Acaquisition Preliminary generic user requirements Version: 0.8

P. Menhard 26 March 2014 Page 21 of 67

Diagram: The multi-layer system architecture

DBMS1

DBMS 2

DBMS n

ODBC/JDBCconnection/

command

object (DBMS 1)

Business logic object

(of type: aggregating

data from more DBs)

ODBC/JDBC

connection/

commandobject (DBMS 2)

ODBC/JDBCconnection/

command

object (DBMS 2)

ODBC/JDBCconnection/

command

object (DBMS n)

Business logic

object (of type:

retrieve data from

one DB)

Business logic

object

Business logic

object

Presentation

object

Presentation object

Web services

object

Web services

object

W

E

B

S

E

R

V

E

R

Client WS

Web brow ser

Client WS

Other applications

or other Web

services

http/s request/ response

SOAP request/ response

ODBC/JDBC

compliant DBs

ODBC/JDBC

connection

Data access

objects layer

Business logic

objects layerPresentation objects (& Web

services) layer

Inet/https/

SOAP

A

P

P

L

I

C

A

T

I

O

N

S

E

R

V

E

R

D

B

M

S

S

E

R

V

E

R

Multi-layer System

Architecture

FRCA ITIS Acaquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 22 of 67

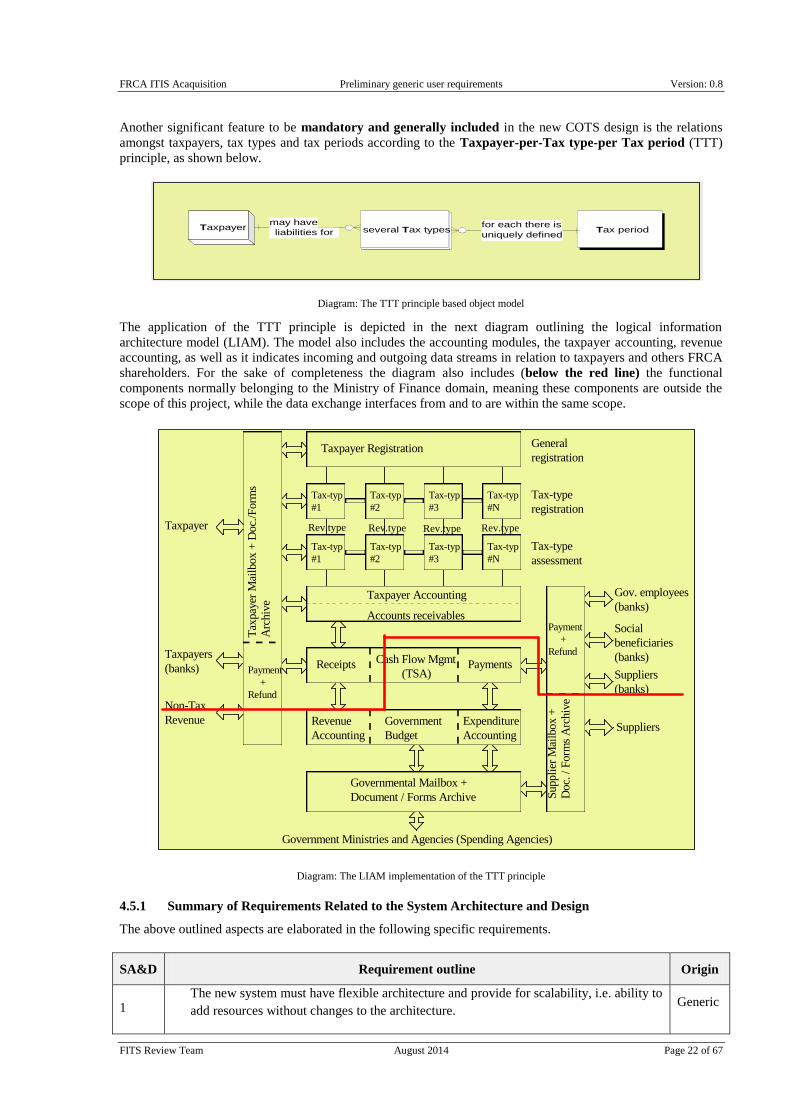

Another significant feature to be mandatory and generally included in the new COTS design is the relations

amongst taxpayers, tax types and tax periods according to the Taxpayer-per-Tax type-per Tax period (TTT)

principle, as shown below.

Diagram: The TTT principle based object model

The application of the TTT principle is depicted in the next diagram outlining the logical information

architecture model (LIAM). The model also includes the accounting modules, the taxpayer accounting, revenue

accounting, as well as it indicates incoming and outgoing data streams in relation to taxpayers and others FRCA

shareholders. For the sake of completeness the diagram also includes (below the red line) the functional

components normally belonging to the Ministry of Finance domain, meaning these components are outside the

scope of this project, while the data exchange interfaces from and to are within the same scope.

Diagram: The LIAM implementation of the TTT principle

4.5.1 Summary of Requirements Related to the System Architecture and Design

The above outlined aspects are elaborated in the following specific requirements.

SA&D Requirement outline Origin

1 The new system must have flexible architecture and provide for scalability, i.e. ability to

add resources without changes to the architecture. Generic

Taxpayer several Tax typesmay have

liabilities for Tax periodfor each there is

uniquely defined

Taxpayer Registration

Taxpayer Accounting

Tax-type

registration

Tax-type

assessment

General

registration

Tax-typ

#1

Tax-typ

#1

Tax-typ

#2

Tax-typ

#2

Tax-typ

#3

Tax-typ

#3

Tax-typ

#N

Tax-typ

#N

Tax

pay

er M

ailb

ox +

Doc.

/Form

s

Arc

hiv

e

Payment

+

Refund

Taxpayer

Taxpayers

(banks) Receipts PaymentsCash Flow Mgmt

(TSA)

Revenue

Accounting

Expenditure

Accounting

Government

Budget

Governmental Mailbox +

Document / Forms Archive Suppli

er M

ailb

ox +

Doc.

/ F

orm

s A

rchiv

e

Government Ministries and Agencies (Spending Agencies)

Suppliers

Payment

+

Refund

Accounts receivables

Suppliers

(banks)

Gov. employees

(banks)

Social

beneficiaries

(banks)

Non-Tax

Revenue

Rev.type Rev.type Rev.type Rev.type

FRCA ITIS Acaquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 23 of 67

SA&D Requirement outline Origin

1.1 As a part of scalability, a maximum virtualization is required, e.g. access to admin tasks

should be granted based on login credentials from any computer in the system, without

the tools used for the purpose being physically present on it.

Generic.

1.2 Preferably, this should include the management of application as well as DB

management.

Generic

1.3 Separate layers for presentation, business logic and DB management. Generic

1.4 Multi-tier system architecture adhering to the SOA principles and standards for

providing a flexible way to combine and use multiple components executed on different

operating systems, technical platform, etc.

Generic

1.5 Web services provided by loosely coupled components and utilizing a thin web client. Generic

1.6 Assuming a web based application, the system should support ―Cascading Style Sheets‖

technical specification for presentation layout of documents.

2

The new tax system must be designed and implemented strictly according to the LIAM,

so as to grant consistent relations between various components (e.g. registration and

accounting) of the system.

Generic.

2.1 In terms of the functional structure, the new system must be designed and implemented

based on modularity principles and depicting the logical flow of information amongst

the functional modules

3 Common (unique) taxpayer identifier is mandatory. Generic.

3.1 Used throughout the system in order to maintain unique identification of tax liabilities

and ease the administration.

Generic.

4 Common double entry book keeping accounting is mandatory. Generic.

4.1 Should be based on the established international accounting standards. Generic.

4.2 Should facilitate daily operations of the authority with respect to the taxpayer

management and tax revenue collection.

Generic.

5

In terms of internal business logic, the new system must be designed and implemented

strictly according to the Taxpayer-per-Tax type-per Tax period (TTT) principle, so as

to grant consistent relations between a taxable body and its obligation for reporting and

paying taxes and non-tax collectibles.

Generic.

5.1 This conformity is required for consistent and direct drill-down to the lowest level of

details kept in the taxpayer ledger and in the associated files, i.e. returns data,

assessment data, payment data, etc.

Generic.

5.2

In terms of the functional structure, the new system must be designed and implemented

based on modularity principles and depicting the logical flow of information amongst

the functional modules.

Generic.

6 Common revenue accounting is mandatory. Generic.

6.1 Provides a complete overview of revenue accounting on the aggregate level and

Generic

FRCA ITIS Acaquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 24 of 67

SA&D Requirement outline Origin

decomposed to the individual tax types and further broken down, as a minimum, to its

main sub-components, i.e. (value of) principal tax, interest, penalty, administrative

charges.

Table: Summary of requirements related to the COTS architecture and design

4.5.2 Analysis of Existing IT Components

Number of

registered

taxpayers

Number of filers Number of filed

declarations

Number of

payment

transactions

700,956 170,824 166,223 121,563

Table: Declarations and payments volume for 2013

4.5.3 Integration Approach

The new system should have an integrated platform for connecting different parts of the system and connecting

with external systems. The next diagram shows the current IT system and sub-systems that need to be fully or

partially replaced. The most appropriate methods of integration with the existing environment must be defined.

Integration must be implemented in the following ways:

- Data level: Data server data server;

- Application level: On the level of application interfaces and web services;

- On user interface level.

Basic guideline for selection of the integration method should be the use of standard technologies and interfaces,

reliability, security and simplicity of the technical solution.

Some of the existing sub-systems will need to be incorporated with the new system in order to offer the single

point of information to all users. Transformed into a high level functional architecture, the next diagram outlines

the functional blocks of the "standard system" with those to be provided through integration, enhancements or

replacements of the existing components.

FRCA ITIS Acaquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 25 of 67

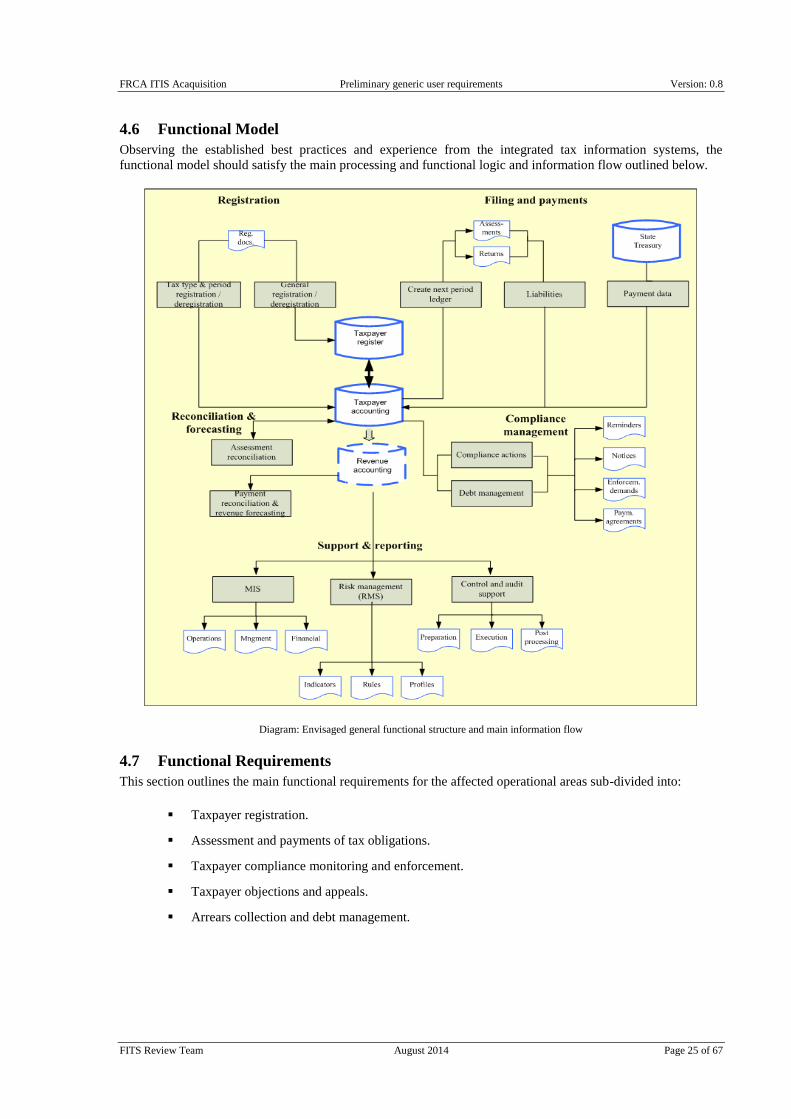

4.6 Functional Model

Observing the established best practices and experience from the integrated tax information systems, the

functional model should satisfy the main processing and functional logic and information flow outlined below.

Diagram: Envisaged general functional structure and main information flow

4.7 Functional Requirements

This section outlines the main functional requirements for the affected operational areas sub-divided into:

Taxpayer registration.

Assessment and payments of tax obligations.

Taxpayer compliance monitoring and enforcement.

Taxpayer objections and appeals.

Arrears collection and debt management.

FRCA ITIS Acaquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 26 of 67

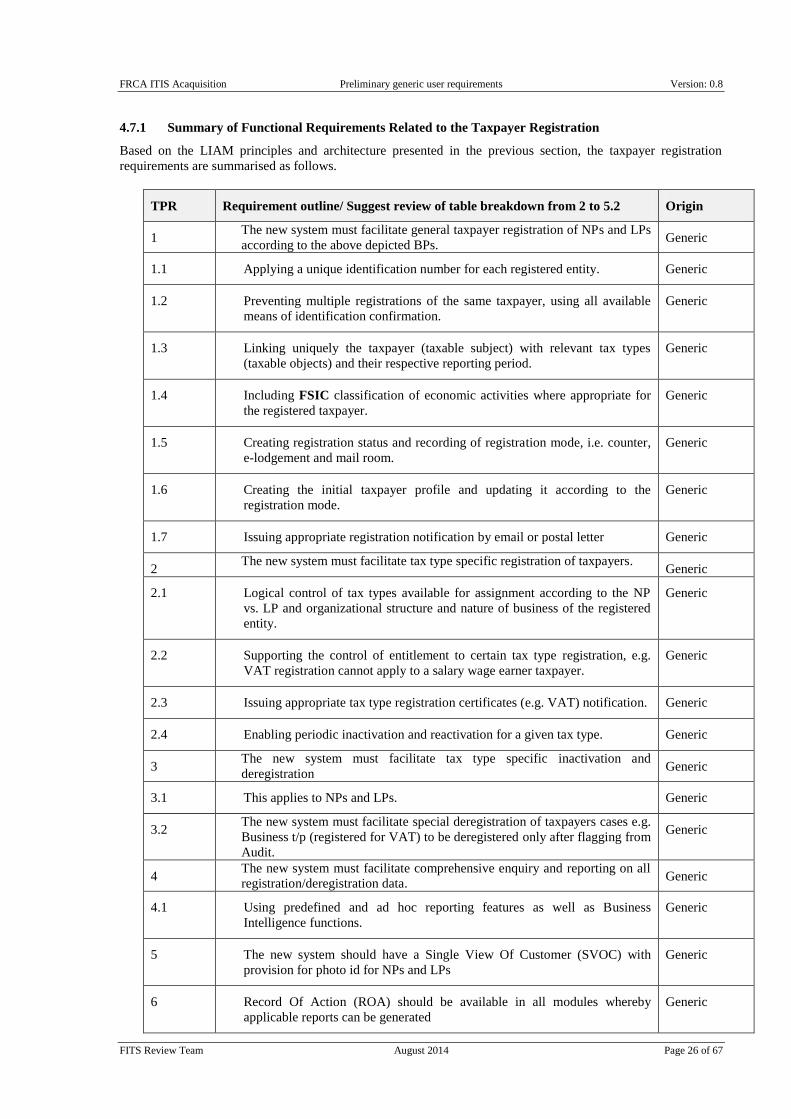

4.7.1 Summary of Functional Requirements Related to the Taxpayer Registration

Based on the LIAM principles and architecture presented in the previous section, the taxpayer registration

requirements are summarised as follows.

TPR Requirement outline/ Suggest review of table breakdown from 2 to 5.2 Origin

1 The new system must facilitate general taxpayer registration of NPs and LPs

according to the above depicted BPs. Generic

1.1 Applying a unique identification number for each registered entity. Generic

1.2 Preventing multiple registrations of the same taxpayer, using all available

means of identification confirmation.

Generic

1.3 Linking uniquely the taxpayer (taxable subject) with relevant tax types

(taxable objects) and their respective reporting period.

Generic

1.4 Including FSIC classification of economic activities where appropriate for

the registered taxpayer.

Generic

1.5 Creating registration status and recording of registration mode, i.e. counter,

e-lodgement and mail room.

Generic

1.6 Creating the initial taxpayer profile and updating it according to the

registration mode.

Generic

1.7 Issuing appropriate registration notification by email or postal letter Generic

2 The new system must facilitate tax type specific registration of taxpayers.

Generic

2.1 Logical control of tax types available for assignment according to the NP

vs. LP and organizational structure and nature of business of the registered

entity.

Generic

2.2 Supporting the control of entitlement to certain tax type registration, e.g.

VAT registration cannot apply to a salary wage earner taxpayer.

Generic

2.3 Issuing appropriate tax type registration certificates (e.g. VAT) notification. Generic

2.4 Enabling periodic inactivation and reactivation for a given tax type. Generic

3 The new system must facilitate tax type specific inactivation and

deregistration Generic

3.1 This applies to NPs and LPs. Generic

3.2 The new system must facilitate special deregistration of taxpayers cases e.g.

Business t/p (registered for VAT) to be deregistered only after flagging from

Audit.

Generic

4 The new system must facilitate comprehensive enquiry and reporting on all

registration/deregistration data. Generic

4.1 Using predefined and ad hoc reporting features as well as Business

Intelligence functions.

Generic

5 The new system should have a Single View Of Customer (SVOC) with

provision for photo id for NPs and LPs

Generic

6 Record Of Action (ROA) should be available in all modules whereby

applicable reports can be generated

Generic

FRCA ITIS Acaquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 27 of 67

TPR Requirement outline/ Suggest review of table breakdown from 2 to 5.2 Origin

7 Ability to maintain the history of contacts and other personal information

for assistance and further analysis including who and when changes were

made.

Generic

8 Electronic signature capturing capability provision Generic

Table: Summary taxpayer registration requirements

4.7.1.1 Taxpayer Registration - Selected Details

TPR-D Required function

Expected provided by / through

Existing Mandatory Proposal

1 Allocate the TIN to a new registrant uniquely identifying

the taxpayer.

Y Y Y

2 Capture and store TIN registration details. Y Y

3 Store FSIC industry code for all TIN registrations with

the possibility of multiple FSIC classification entries.

Y Y Y

4 Capture and store specific registration details for

different tax types.

Y Y Y

5 Maintain and update taxpayer status (active, inactive,

deregistered, etc.)

Y Y Y

6 Allow retrieval of de-registered taxpayer details that has

been archived.

Y Y Y

7 Search taxpayer register by name, trading name, address,

Birth registration number, death registration number,

TIN, and other registration data items.

Y Y Y

8 Produce name and address details for bulk mail-out

exercises according to predetermined criteria for address

labels and pre-printed stationery. This could be for all

taxpayers, individual taxpayers, or selected taxpayers.

Y Y

9 Create and maintain meaningful links to other registered

entities e.g. owners, directors, spouses, related

companies, etc.

Y Y Y

10 Enquire on data or print reports of linked entities. Y Y

11 Cross reference to other official numbers or codes. Y Y

12 Create, maintain and enable viewing of the ‗situation

summary‘ information, indicating on-going audit, open

assessments, suspense items, appeals, bankruptcy,

internal arrangements as a part of the global risk profile.

Y Y

13 Ability to capture, store, and retrieve bank account and

routing information.

Y Y Y

14 Ability to provide maintenance of taxpayer preferred

contacts and agents with effective dating. For bulk

postings, system must include the right or applicable

Y Y

FRCA ITIS Acaquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 28 of 67

TPR-D Required function

Expected provided by / through

Existing Mandatory Proposal

address

15 Ability to support document exporting into PDF, TIFF,

file formats, etc.

Y Y

Table: Selected details of taxpayer registration requirements

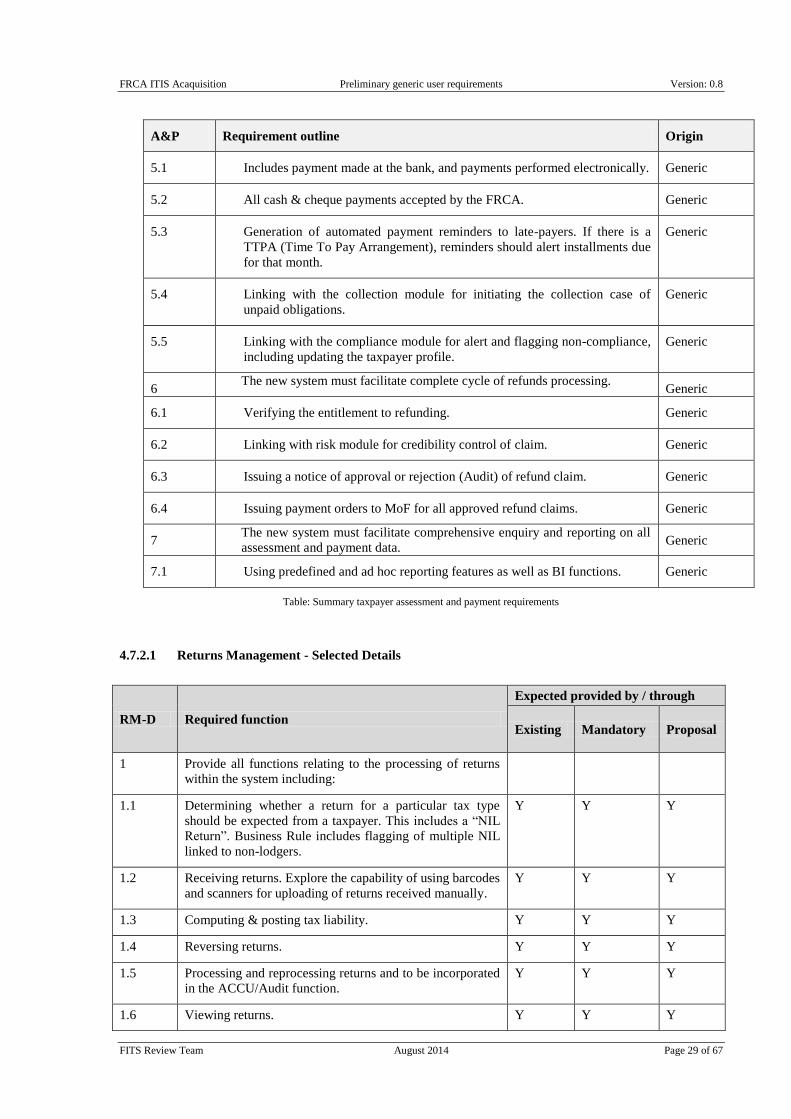

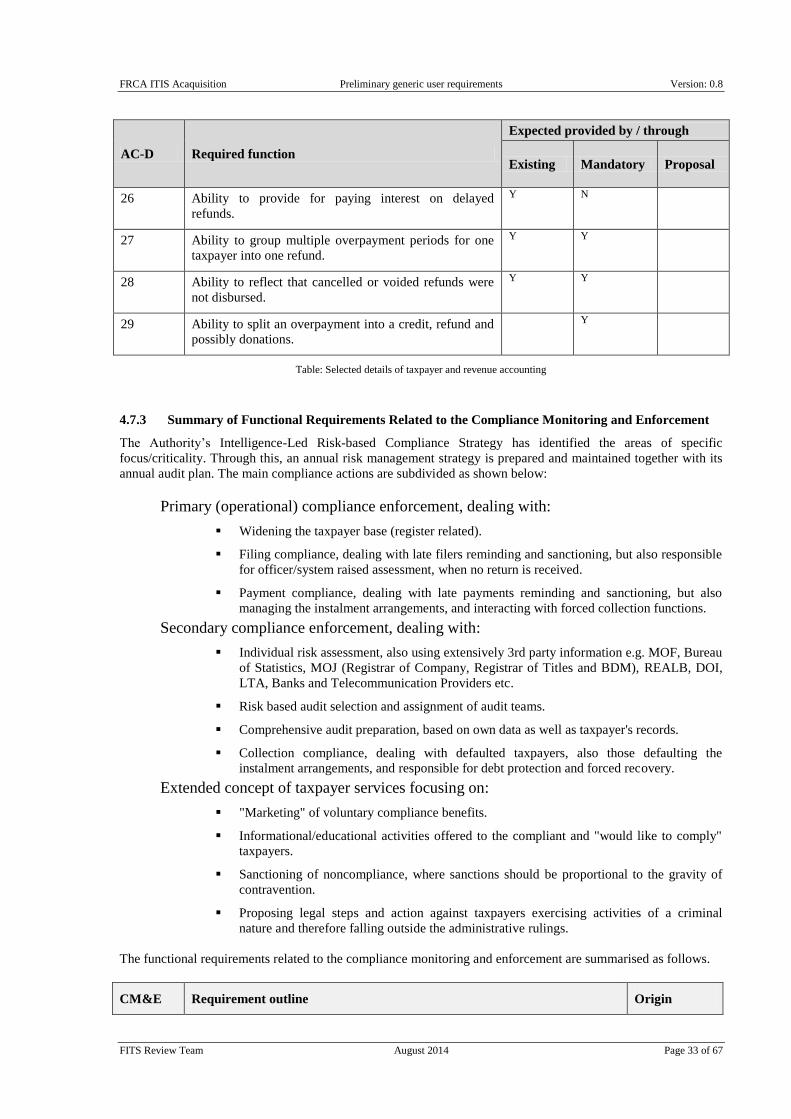

4.7.2 Summary of Functional Requirements Related to the Assessment and Payments

Strictly applying the LIAM principles, the taxpayer assessment and payment requirements are summarised as

follows. Consideration to include electronic stamp facility.

A&P Requirement outline Origin

1 The new system must facilitate recording and management of taxpayers´

liabilities originating from returns, assessment (Self-assessed and FRCA

assessed taxes) and various adjustments. The system should capture all tax

types including Stamp Duty & CGT and integrate with ASYCUDA World.

Generic

1.1 Paper based documents and electronic records received from taxpayers or

generated by the tax officer.

Generic

1.2 All relevant validations, formal, logical, arithmetic and probability check

based on configurable predefined criteria, historic data and other relevant

information sources.

Generic

1.3 Maintaining archive of digital copy of all assessment documents. Generic

1.4 Maintaining analytic data in an appropriate repository. Generic

1.5 Forwarding the aggregated assessment result to the taxpayer accounting

module.

Generic

2 Generation of automated assessment reminders to late-filers. Under current

portfolio management, two reminders of current lodgment & payment dues.

Generic

2.1 Must facilitate an automated system created assessment of late filers /non-

filers as well as an accompanying generated demand letter to be sent based

on configurable predefined criteria, historic data and other relevant

information sources.

Generic

3 An assessment officer is able to adjust or overrule the automated system

before and after assessment especially for self-assessment returns. The

system must allow for electronic & interactive transactions.

Generic

4 The new system must facilitate generation and submission of payment

orders for self-assessed and FRCA assessed taxes with applicable automated

system generated notifications sent for EMS raised; payables due; etc.

Generic

5 The new system must facilitate recording and management of payments

received from taxpayers and refunds made to taxpayers. Generic

FRCA ITIS Acaquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 29 of 67

A&P Requirement outline Origin

5.1 Includes payment made at the bank, and payments performed electronically. Generic

5.2 All cash & cheque payments accepted by the FRCA. Generic

5.3 Generation of automated payment reminders to late-payers. If there is a

TTPA (Time To Pay Arrangement), reminders should alert installments due

for that month.

Generic

5.4 Linking with the collection module for initiating the collection case of

unpaid obligations.

Generic

5.5 Linking with the compliance module for alert and flagging non-compliance,

including updating the taxpayer profile.

Generic

6 The new system must facilitate complete cycle of refunds processing.

Generic

6.1 Verifying the entitlement to refunding. Generic

6.2 Linking with risk module for credibility control of claim. Generic

6.3 Issuing a notice of approval or rejection (Audit) of refund claim. Generic

6.4 Issuing payment orders to MoF for all approved refund claims. Generic

7 The new system must facilitate comprehensive enquiry and reporting on all

assessment and payment data. Generic

7.1 Using predefined and ad hoc reporting features as well as BI functions. Generic

Table: Summary taxpayer assessment and payment requirements

4.7.2.1 Returns Management - Selected Details

RM-D Required function

Expected provided by / through

Existing Mandatory Proposal

1 Provide all functions relating to the processing of returns

within the system including:

1.1 Determining whether a return for a particular tax type

should be expected from a taxpayer. This includes a ―NIL

Return‖. Business Rule includes flagging of multiple NIL

linked to non-lodgers.

Y Y Y

1.2 Receiving returns. Explore the capability of using barcodes

and scanners for uploading of returns received manually.

Y Y Y

1.3 Computing & posting tax liability. Y Y Y

1.4 Reversing returns. Y Y Y

1.5 Processing and reprocessing returns and to be incorporated

in the ACCU/Audit function.

Y Y Y

1.6 Viewing returns. Y Y Y

FRCA ITIS Acaquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 30 of 67

RM-D Required function

Expected provided by / through

Existing Mandatory Proposal

1.7 Viewing filing history. Y Y Y

1.8 Raise a default assessment based on previous returns.

Automatic calculation of liability for a default assessment.

Based on proper rules.

Y Y

1.9 Impose late lodgement penalty, when the lodged return is

overdue or when the default assessment is raised.

Y Y Y

1.10 Ability to view all returns filed at the period level, account

level, or entity level.

Y Y Y

1.11 Ability to allow posting of informational, zero balance,

negative balance and positive balance returns.

Y Y Y

1.12 Provide user modifiable table for validation and posting

rules.

Y Y

1.13 Ability to capture and store return amendments with full

history and linking to the original declaration.

Y Y Y

1.14 Ability to process returns with or without payments.

EMS/PT – cannot process Commissioners Assessment/

Form B & C without PAYE/PT payment.

Y Y Y

1.15 Ability to recognise and prevent duplicate returns. VAT

return lodgement based on taxable period of lodgement.

Y Y Y

1.16 Ability to record the received/postmark date and process

date for all returns.

Y Y Y

1.17 Ability to display taxpayer original and revised (system

calculated) data.

Y Y Y

1.18 Ability to generate electronic receipt for electronic returns. Y Y

1.19 Record and maintain location of paper returns and files. Y Y

1.20 Ability to validate specified lines of a return based on

configurable rules.

Y Y Y

Table: Selected details of taxpayer return management

4.7.2.2 Payment Processing - Selected Details

PP-D Required function

Expected provided by / through

Existing Mandatory Proposal

1 Receive payments by a number of payment method

options.

Y Y Y

2 Capture TIN, tax type, payment date, payment method,

instalment number, payment amount, receipt number,

source document ID.

Y Y Y

FRCA ITIS Acaquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 31 of 67

PP-D Required function

Expected provided by / through

Existing Mandatory Proposal

3 Determine the due date for the payment. Y Y Y

4 Update taxpayer and revenue accounts. Y Y Y

5 Calculate late payment penalties and notify taxpayers of

late payment.

Y Y Y

6 Process unidentified payments (will arise when TTT

payment detail is not present, or is incorrect).

Y Y

All unidentifiable payments can be clearly recognized. Y Y Y

The payment is accounted for in all payment

reconciliations.

Y Y Y

The payment is held on an appropriate suspense account

until full TTT identification.

Y Y Y

Enquire lists for the unidentified payment for manual

resolution.

Y Y Y

Transfer resolved payments to the correct taxpayer

account.

Y Y Y

7 Provide for history of all manipulation to a record (e.g.

Transfer history, Error corrections, etc.).

Y Y Y

8 Provide payment deferral and payment of tax in

instalments for predefined volume and frequency based

on business rules and regulations.

Y Y Y

9 Enable instalment calculation for TTT based on business

rules and regulations.

Y Y Y

10 Facilitate new payment (posting) methods e.g. posting

by third parties such as post offices, banks, e-PAY,

internet, direct bank transfer, etc..

Y Y

Table: Selected details of taxpayer payment processing

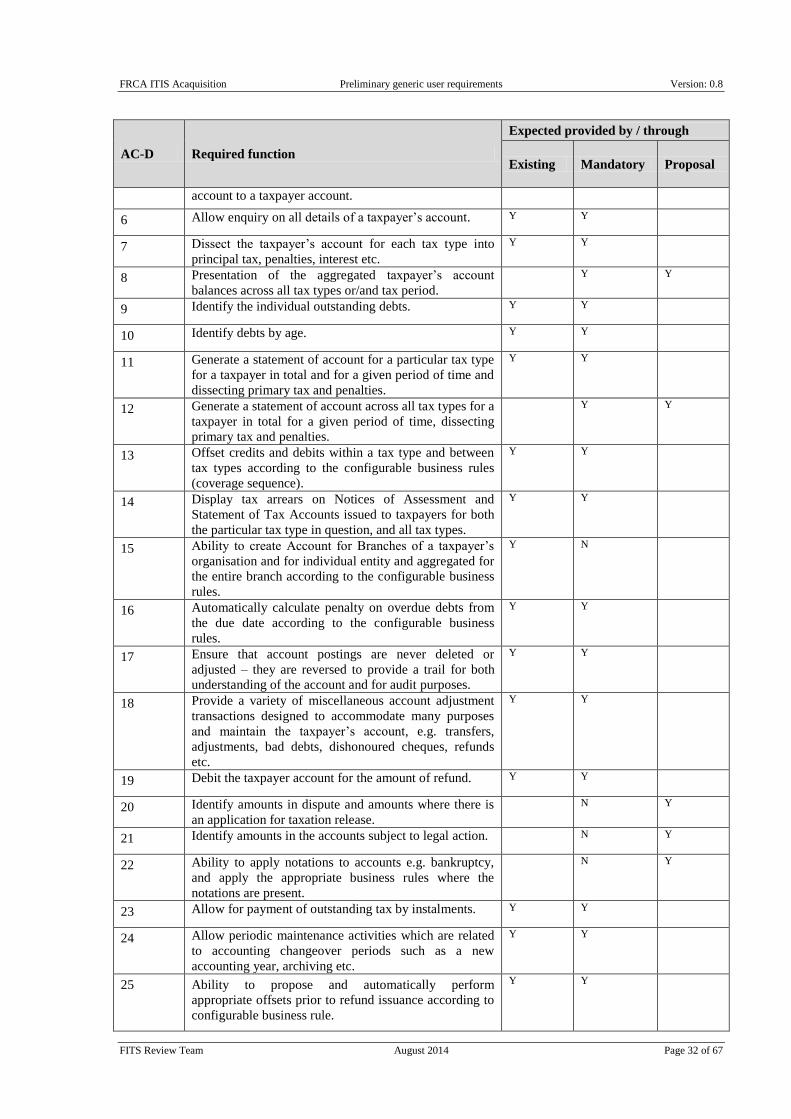

4.7.2.3 Taxpayer and Revenue Accounting - Selected Details

AC-D Required function

Expected provided by / through

Existing Mandatory Proposal

1 Create and maintain a Chart of Accounts Y Y

2 Account for all debits / credits for all taxpayer, tax types

tax period (TTT)

Y Y

3 Maintain a common account posting structure for all

debit and credit transaction types.

Y Y

4 Post debits and credits to taxpayer and revenue accounts

using a common accounting ―engine‖ (double entry

book keeping).

Y Y

5 Enable ―suspense‖ accounts for unidentified payments,

and the ability to transfer payments from the suspense

Y Y

FRCA ITIS Acaquisition Preliminary generic user requirements Version: 0.8

FITS Review Team August 2014 Page 32 of 67

AC-D Required function

Expected provided by / through

Existing Mandatory Proposal

account to a taxpayer account.

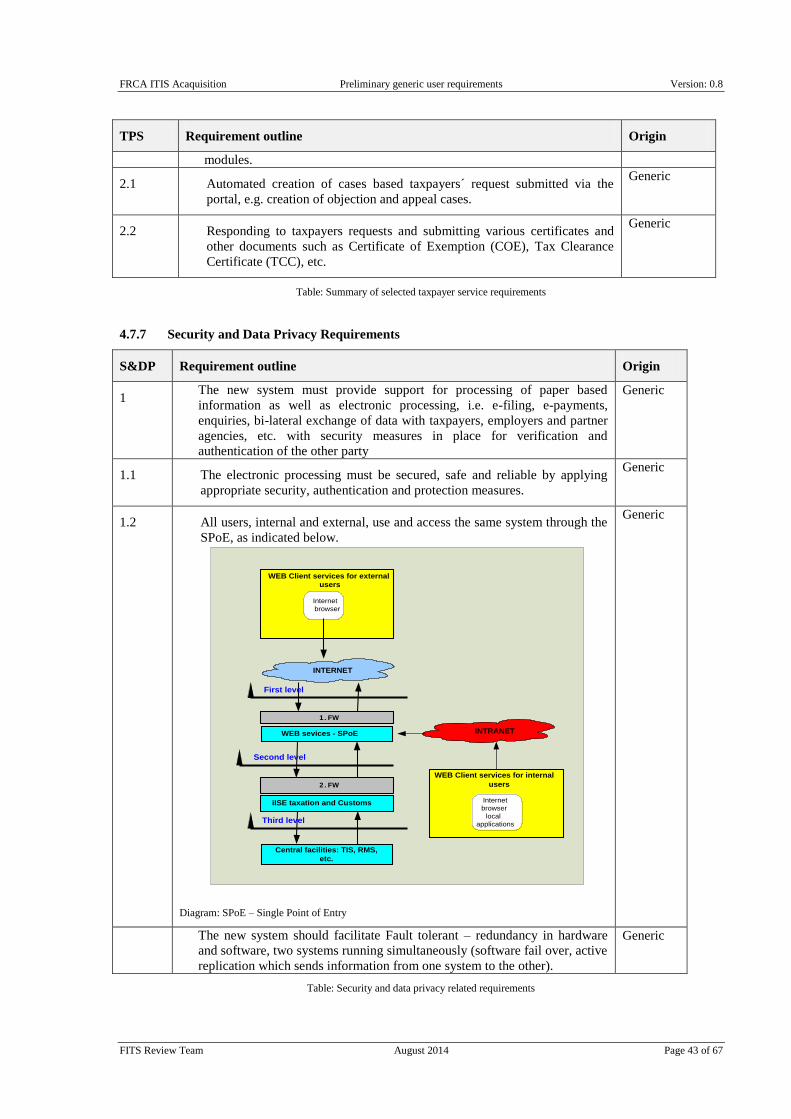

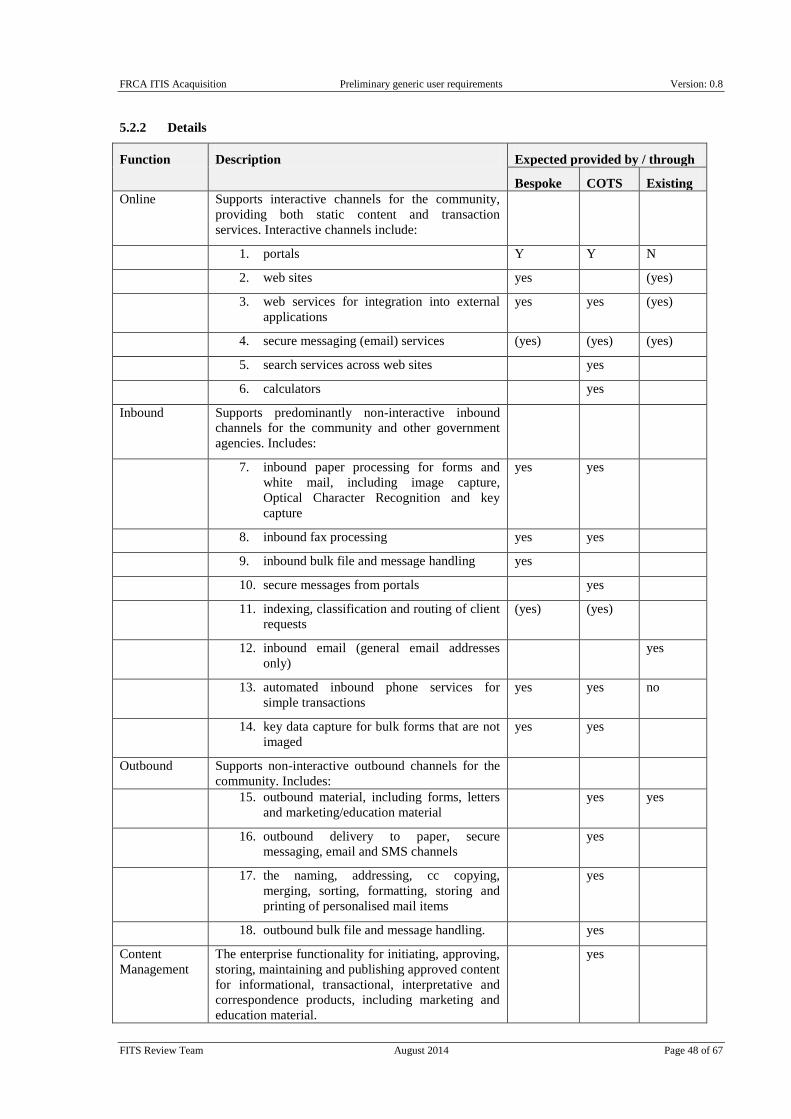

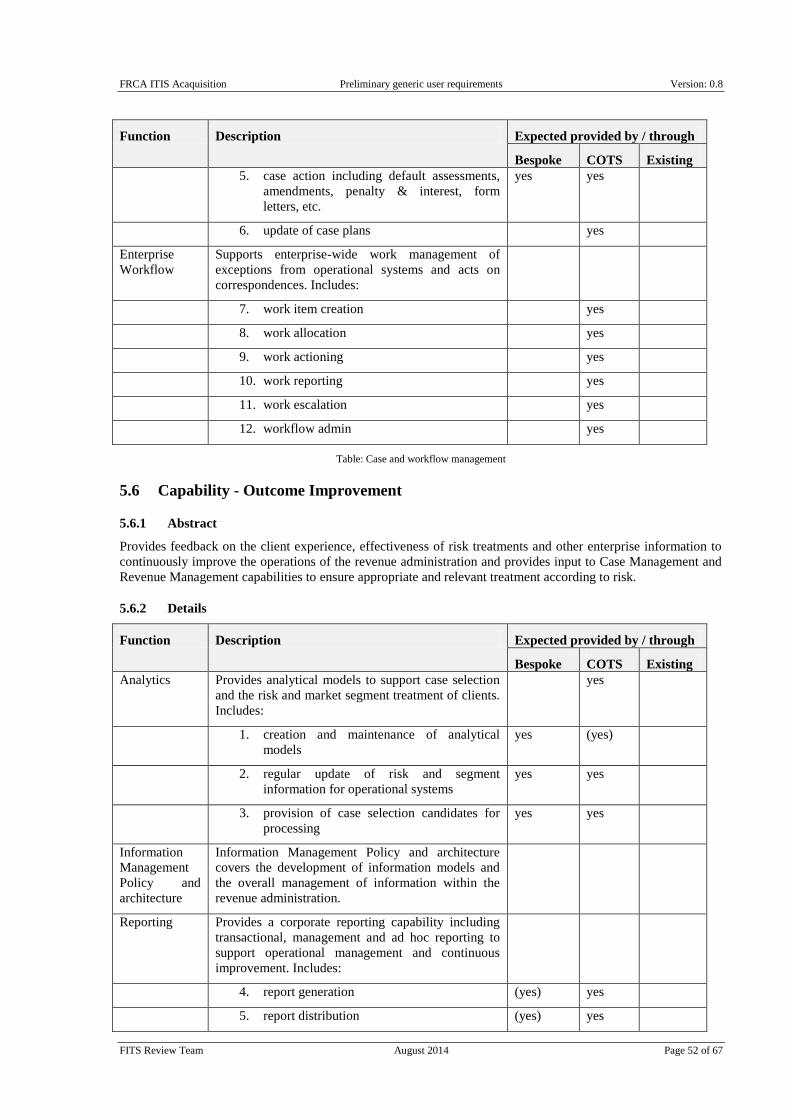

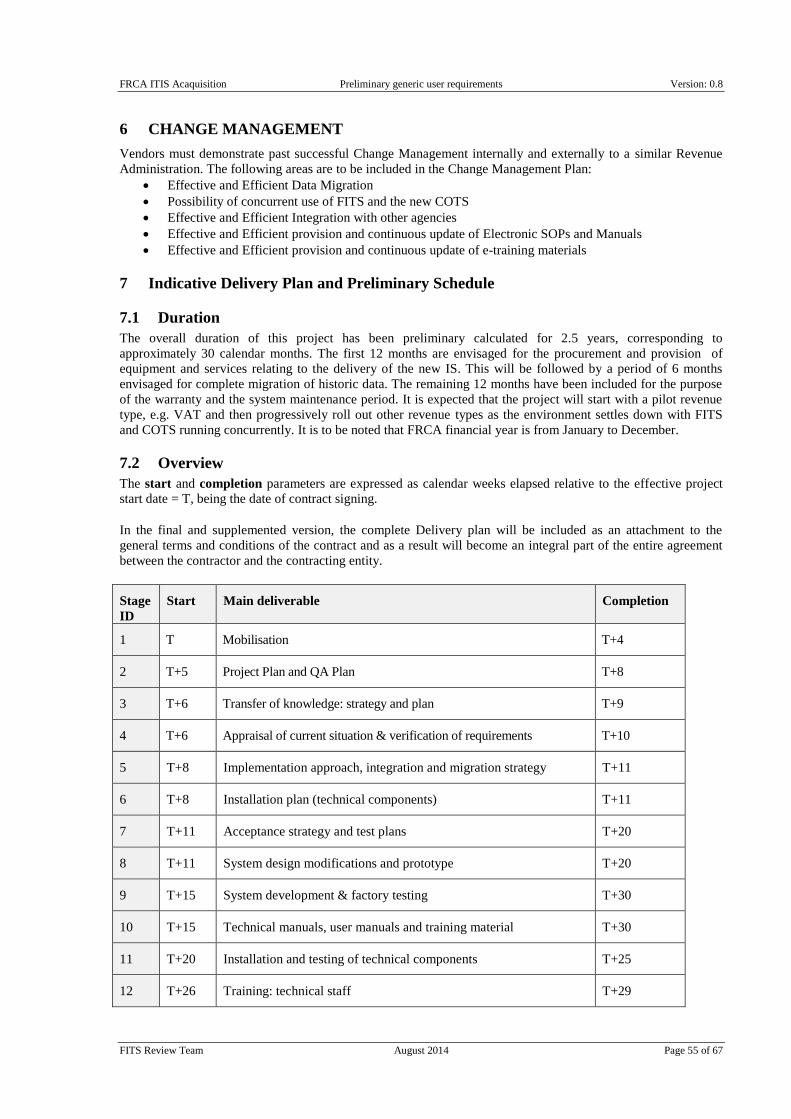

6 Allow enquiry on all details of a taxpayer‘s account. Y Y