Embed Size (px)

Citation preview

ro COP Board of Governors of the Federal Reserve System

FR Hi OMB Number 70297 Approval expires December 31 2015 Page 1 of2

Annual Report of Holding Companies-FR Y-6

Report at the close of business as of the end of fiscal Year

This Report is required by law Section 5(c)(1)(A) of the Bank Holding Company Act (12 USC sect 1844 (c)(1)(A)) Section 8(a) of the International Banking Act (12 USC sect 3106(a)) Sections 11(a)(1) 25 and 25A of the Federal Reserve Act (12 USC sectsect 248(a)(1) 602 and 611a) Section 21113(c) of Regulation K (12 CFR sect 21113(c)) and Section 2255(b) of Regulation Y (12 CFR sect 2255(b)) and section 1 O(c)(2)(H) of the Home Owners Loan Act Return to the appropriate Federal Reserve Bank the original and the number of copies specified

NOTE The Annual Report of Holding Companies must be signed by one director of the top-tier holding company This individual should also be a senior official of the top-tier holding company In the event that the top-tier holding company does not have an individual who is a senior official and is also a director the chairshyman of the board must sign the report

1 H Michael Lawson Name of the Holding Company Director and Official

President and Chief Executive Officer Trtle of the Holding Company Director and Official

attest that the Annual Report of Holding Companies (including the supporting attachments) for this report date has been preshypared in conformance with the instructions issued by the Federal Reserve System and are true and correct to the best of my knowledge and belief

With respect to information regarding individuals contained in this report the Reporter certifies that it has the authority to provide this information to the Federal Reserve The Reporter also certifies that it has the authority on behalf of each individual to consent or object to public release of information regarding that individual The Federal Reserve may assume in the absence of a request for confidential treatment submitted in accordance with the Boards Rules Regarding Availability of Information 12 CFR Part 261 that the Reporter and individual consent to public release of all details in the report concerning that individual

kfr--SignaCOfaf1dotticial

03302015 Date of Signature

For holding companies nQ1 registered with the SEC-Indicate status of Annual Report to Shareholders

181 is included with the FR Y-6 report

D will be sent under separate cover

D is not prepared

For Federal Reserve Bank Use Only

RSSDID C77R CI

This report form is to be filed by all top-tier bank holding compashynies and top-tier savings and loan holding companies organized under US law and by any foreign banking organization that does not meet the requirements of and is not treated as a qualifyshying foreign banking organization under Section 21123 of Regulation K (12 CFR sect 21123) (See page one of the general instructions for more detail of who must file) The Federal Reserve may not conduct or sponsor and an organization (or a person) is not required to respond to an information collection unless it displays a currently valid OMB control number

Date of Report (top-tier holding companys fiscal year-end)

December 31 2014 Month I Day I Year

none Reporters Legal Entity Identifier (LEI) (20-Character LEI Code)

Reporters Name Street and Mailing Address

RNB Corp Legal Trtle of Holding Company

P 0 Box 340 (Mailing Address of the Hold ing Company) Street I PO Box

Brazil IN 47834 -------City State Zip Code

1 East National Avenue Physical Location (if different from malling address)

Person to whom questions about this report should be directed Michael E Yeager Controller

------------Name Trtle

812-448-2611-159 Area Code I Phone Number I Extension

812-448-8281 Area Code I FAX Number

michaelyeagerriddellonlinecom E-mail Address

NIA Address (URL) for the Holding Co mpanys web page

Does the reporter request confidential treatment for any portion of this

submission

D Yes Please identify the report items to which this request applies

C8J No

O In accordance with the instructions on pages GEN-2 and 3 a Jetter justifying the request is being provided

O The information for which confidential treatment is sought is being submitted separately labeled Confidential

Public reporting burden for this information collection is estimated lo vary from 13 to 101 hours per response with an average of 525 hours per response including time to gather and maintain data in the required form and to review instructions and complete the infonnation collection Send comments regarding this burden estimate or any other aspect of this collection of information including suggestions for reducing this burden to Secretary Board of Governors of the Federal Reserve System 20th and C Streets NW washington DC 20551 and to the Office of Management and Budget Paperwork Reduction Project (7100-0297) Washington DC 20503

102014

RIDDELL NATIONAL BANK

Todays Banking Yesterdays Values

RNB CORP ANNUAL REPORT

2014

CPAs amp Advisors 201 N Illinois Street Suite 700 II PO Sox 44998 II Indianapolis IN 46244-0198

3173834000 II fax 317 3834200 II bkdcom

To the Shareholders and Board of Directors

RNB CORP Brazil Indiana

Independent Auditors Report

We have audited the accompanying consolidated financial statements ofRNB CORP and its subsidiary which comprise the consolidated balance sheets as of December 3 1 2014 and 2013 and the related consolidated statements of income comprehensive income shareholders equity and cash flows for the years then ended and the related notes to the financial statements

Managements Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America this includes the design implementation and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement whether due to fraud or error

Auditors Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audits We conducted our audits in accordance with auditing standards generally accepted in the United States of America Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements The procedures selected depend on the auditors judgment including the assessment of the risks of material misstatement of the consolidated financial statements whether due to fraud or error In making those risk assessments the auditor considers internal control relevant to the entitys preparation and fair presentation of the consolidated financial statements i n order to design audit procedures that are appropriate in the circumstances but not for the purpose of expressing an opinion on the effectiveness of the entitys internal control Accordingly we express no such opinion An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management as well as evaluating the overall presentation of the consolidated financial statements

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion

PraxitY MEMBEll

Gl08Al ALtlAlfCt Of IHbfPEHDEHT FIRMS

Opinion

In our opinion the consolidated financial statements referred to abov present fairly in all material respects the financial position ofRNB CORP and its subsidiary as of December 31 2014 and 2013 and the results of their operations and their cash flows for the years then ended in accordance with accounting principles generally accepted in the United States of America

Indianapolis Indiana February 27 2015

1 -middot

2

RNB CORP Consolidated Balance Sheets Decem ber 31 201 4 a n d 2013

Assets

Cash and due from banks

Interest-bearing demand deposits

Cash and cash equivalents Investment securities available for sale

Loans held for sale

Loans net of allowance for loan losses of $ 1 757 785 and $1846358 Premises and equipment Federal Reserve and Federal Home Loan Bank membership stock Interest receivable

Other assets

Total assets

Liab ilities

Deposits

N oninterest-bearing

Interest-bearing

Total deposits

Other borrowings Dividends payable Interest payable

Other liabilities Total liabilities

Sharehol d e rs Equity Common stock no par or stated value

Authorized - 500000 shares

Issued and outstanding - 443509 and 440925 shares

Retained earnings

Accumulated other comprehensive loss

Total shareholders equity

Total liabilities and shareholders equity

See Notes to Consolidated Financial Statements

$

$

$

$

2014 2013

4258363 $ 4452428 1 674904 38882 5933267 449 1 310

25867482 27928824 1384691 1 39467

1461 858 12 142120514 2832422 2923074

740100 720200 1 136173 1 1 0 1 443 4735045 44 1 8520

1 88814992 $ 1 83843352

26748695 $ 22834692 1 35027358 131 8 1 6244 1 61 776053 154650936

10228547 1 3239545 554363 551277 1 81061 357864

1 816453 1 27431 9 1 74556477 170073941

945792 865688 14828098 14100530 (1 515375) ( 1 196807) 14258515 1 376941 1

1 88814992 $ 183843352

3

RNB CORP Consolidated Statements of Income

Years Ended December 31 201 4 and 2013

2014

Interest and Dividend Income

Loans receivable $ 7137918

Investment securities

Taxable including dividend income 365404

Tax-exempt 237314

Other interest and dividends 42379

Total interest and dividend income 7783015

Interest Expense

Deposits 1238845

Borrowings 62884

Total interest expense 1301729

Net Interest Income 6481286

Provision for loan losses 480000

Net Interest Income After Provision for Loan Losses 6001286

Other Income

Fiduciary activities 29359

Service charges on deposit accounts 460721

Gain on loans sold 630444

Investment gains (losses) 246906

ATu1 fees 258118

Other operating income 144344

Total other income 1769892

Other Expenses

Salaries and employee benefits 3015717

Net occupancy expenses 408877

Equipment expenses 435637

Director and committee fees 148221

Legal and professional 291894

ATM processing 189723

Advertising and promotion 287110

Federal Deposit Insurance Corporation insurance expense 164694

Other operating expenses 801459

Total other expenses 5743332

Income Before Income Tax 2027846

Income tax expense 688606

Netlncome $ 1339240

Per Share

Net income $ 303

lgteighted-Average Shares Outstanding 441381

See Notes to Consolidated Financial Statements

2013

$ 6892384

290159 288343

51457 7522343

1860113 63923

1924036

5598307 480000

5118307

45549 537402 767662

(8194) 242978 348935

1934332

3203981 401090 507517 146784 274344

199462 268283 169574 623925

5794960

1257679 284078

$ 973601

$ 222

439368

4

RNB CORP Consol idated Statem ents of Comprehensive I n come

Years Ended December 3 1 201 4 a n d 2013

2014

Net Income $ 1 339240

Other Comprehensiye Loss

Change in netl1Ilealized gain (loss) on securities available for sale net of taxes of$184032 and $(219007) for 2014 and2013 respectively middot 280578

Less reclassificati611 adjusfinent for realized gains (losses) ineluded in net income netoftaxes of $97799 and $(3246) for 2014 and 2013 respectively 149107

Change in net accumulated other comprehensive income (loss) for postretirementplan net of taxes of$(295059) and $77215 for 2014 and 2013 respectively (450039)

(3J8568)

Comprehensive Incqme $ 1020672

--

See Notes to Consolidated Financial Statements

2013

$ 973601

(47241 9)

(4948)

1 1 7771 (349700)

$ 623901

5

RNB CORP Consolidated Statements of Shareholders Equity

Years Ended December31 201 4 and 2013

middotAccumulated Common Stock Other

Shares Retained Comprehensive Outstanding Amount Earning Loss

Balances January 1 2013 436189 s 723608 $ 13735406 $ (847107)

Net income 973601

Other comprehensive Joss (349700)

Issuance of stock 4736 142080

Cash dividends ($138 per share) (608477) -

Balances Decenibr 31middot2013 440925 865688 14i00530 (1196807)

Net income 1339240

Other comprehensive loss (318568)

Issuance of stockmiddot 2584 80104

Cash dividends($138 per share) (6ll672)

Balances December 31 2014 443509 $ 945792 $ 14828093 $ (J515375)

See Notes to Consolidated Financial Statements

Total

s 13611907

973601

(349700)

142080

(608477)

13769411

1339240

(318568)

80104

(611672)

$ 14258515

6

RNB CORP Consol idated Statements of Cash Flows

Years Ended December 3 1 201 4 and 2013

2014

Operating Activities Net income $ 1339240 Items not requiring (providing) cash

Provision for loan losses 480000 Depreciation and amortization 278769 Deferred income tax (45899) Securities amortization net 305437 Net realized (gain) loss on available-for-sale securities (246906) Net realized (gain) loss on OREO 33040 Increase in cash surrender value (44619)

Net change in Loans held for sale (1245224) Interest receivable (34730) Interest payable (176803)

Other adjustments 214557 Net cash provided by operating activities 856862

Investing Activilies Purchases of securities available for sale (7547942) Proceeds from maturities and paydowns of securities

available for sale 5996926 Proceeds from the sale of available-for-sale securities 3725621 Redemption of membership stock Net change in loans (52778 17) Purchase of membership stock (19900) Proceeds from the sale of OREO 310687 Purchases of premises and equipment (1881 17)

Net cash used in investing activities (3000542)

Financing Activities Net change in

Noninterest-bearing NOW money market and savings deposits 7818147 Certificates of deposit (693030) Other borrowings (3010998)

Repayments ofborrowings Issuance of stock net 80104 Cash dividends (608586)

Net cash provided by financing activities 3585637

Net Change in Cash and Cash Equivalents 1441957

Cash and Cash Equivalents Beginning of Year 449 1310

Cash and Cash Equivalents End of Year $ 5933267

Additional Cash Flows Information Interest paid $ 1451160 Income tax paid 469000

See Notes to Consolidated Financial Statements

2013

$ 973601

480000 310169

(4468) 379065

8194 (28224) (50150)

235784 29102

1727 249760

2584560

( 1 1 282162)

7873335 368631 1

36100 (1 0057092)

664171 (74649)

(9153986)

18 1 052 1634777 3518925 (300000)

142080 (602850)

4573984

(1995442)

6486752

$ 4491310

$ 1922309 92000

7

N ote 1

RNB CORP N otes to Consolidated F inancial Statements

December 3 1 2014 and 2013 (Table Dollar Amounts in Thousands)

N ature of O perations and S u mmary of Significant Accounting Po licies

The accounting and reporting policies ofRNB CORP (Company) and its wholly owned subsidiary The Riddell National Bank (Bank) and the Banks wholly owned subsidiary RNB Investments Inc which holds services manages and invests a portion of the Banks investment portfolio conform to accounting principles generally accepted in the United States of America and reporting practices followed by the banking industry The more significant of the policies are described below

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting period Actual results could differ from those estimates

Material estimates that are particularly susceptible to significant change relate to the determination of the allowance for loan losses valuation of real estate acquired in connection with foreclosures or in satisfaction ofloans loan servicing rights and fair values of financial instruments

The Company is a bank-holding company whose principal activity is the ownership of the Bank The Bank operates under a national bank charter and provides full banking services including trust services As a national bank the Bank is subject to regulation by the Office of the Comptroller of the Currency and the Federal Deposit Insurance Corporation (FDIC)

The Bank generates commercial mortgage and consumer loans and receives deposits from customers located primarily in Clay and Vigo counties and other surrounding Indiana coulities The Banks loans are generally secured by specific items of collateral including real property consumer assets and business assets

Consolidation - The consolidated financial statements include the accounts of the Company the Bank and RNB Investments Inc after elimination of all material intercompany transactions

Cash and Cash Equivalents - The Company considers all liquid investments with original maturities of three months or less to be cash equivalents As of December 3 1 2014 and 2013 cash and cash equivalents are defined to include cash on hand deposits in other institutions and federal funds sold

At December 3 1 2014 the Companys cash accounts exceeded federally insured limits by approximately $1990000 Additionally the Company had approximately $566000 on deposit with the Federal Reserve Bank and the Federal Home Loan Bank of Indianapolis as of December 3 1 2014 which is not federally insured

8

RNB CORP N otes to Consolidated Financial Statem ents

December 3 1 201 4 a n d 20 1 3 (Table Dol lar Amounts in Thousands)

Investment Securities - Debt securities are classified as held to maturity when the Company has the positive intent and ability to hold the securities to maturity Securities held to maturity are carried at amortized cost Debt securities not classified as held to maturity are classified as available for sale Securities available for sale are carried at fair value with unrealized gains and losses reported separately in accumulated other comprehensive income net of tax

Amortization of premiums and accretion of discounts are recorded as interest income from securities Realized gains and losses are recorded as net security gains (losses) Gains and losses on sales of securities are determined on the specific-identification method

For debt securities with fair value below amortized cost when the Company does not intend to sell a debt security and it is more likely than not the Company will not have to sell the security before recovery of its cost basis it recognizes the credit component of an other-than-temporary impairment of a debt security in earnings and the remaining portion in other comprehensive loss

Loans held for sale are carried at the lower of cost or fair value determined using an aggregate basis Write-downs to fair value are recognized as a charge to earnings at the time the decline in value occurs Forward commitments to sell mortgage loans are acquired to reduce market risk on mortgage loans in the process of origination and mortgage loans held for sale Gains and losses resulting from sales of mortgage loans are recognized when the respective loans are sold to investors Gains and losses are determined by the difference between the selling price and the carrying amount of the loans sold net of discounts collected or paid and considering a normal servicing rate

Loans that management has the intent and ability to hold for the foreseeable future or until maturity or payoffs are reported at their outstanding principal balances adjusted for unearned income charge-offs the allowance for loan losses any unamortized deferred fees or costs on originated loans and unamortized premiums or discounts on purchased loans For all loan classes carried at amortized cost interest income is accrued based on the unpaid principal balance

The accrual of interest for all loan classes is discontinued at the time the loan is 90 days past due unless the credit is well-secured and in process of collection Past-due status is based on contractual terms of the loan In all cases all loan classes are placed on nonaccrual or charged off at an earlier date if collection of principal or interest is considered doubtful

All interest accrued but not collected for loans that are placed on nonaccrual or charged off are reversed against interest income The interest on these loans is accounted for on the cash-basis or cost-recovery method until qualifying for return to accrual Loans are returned to accrual status when all the principal and interest amounts contractually due are brought current and future payments are reasonably assured

9

RNB CORP Notes to Conso l idated F inancial Statements

Decem ber 31 20 1 4 and 201 3 (Table Dollar Amounts in Thousands)

middotwhen cash payments are received on impaired loans in each loan class the Company records the payment as a principal reduction and interest income unless collection of the remaining recorded principal amount is doubtful at which time payments are used to reduce the principal balance of the loan Interest income on troubled debt restructured loans is recognized on an accrual basis at the renegotiated rate if the loan is in compliance with the modified terms no principal reduction has been granted and the loan has demonstrated the ability to perform in accordance with the renegotiated terms for a period of at least six months

Allowance for loan losses - The allowance for loan losses is established as losses are estimated to have occurred through a provision for loan losses charged to income Loan losses are charged against the allowance when management believes the loan balance is uncollectible Subsequent recoveries if any are credited to the allowance

The allowance for loan losses is evaluated on a regular basis by management and is based upon managements periodic review of the collectibility of the loans in light of historical experience the nature and volume of the loan portfolio adverse situations that may affect the borrowers ability to repay estimated value of any underlying collateral and prevailing economic conditions This evaluation is inherently subjective as it requires estimates that are susceptible to significant revision as more information becomes available

The allowance consists of allocated and general components The allocated component relates to loans that are classified as impaired For those loans that are classified as impaired an allowance is established when the discounted cash flows (or collateral value or observable market price) of the impaired loan is lower than the carrying value of that loan The general component covers nonclassified loans and is based on actual historical charge-off experience by loan segment experienced by the Company over the prior three years Management believes the three year historical loss experience methodology is appropriate in the current economic environment Other adjustments may be made to the allowance for pools of loans after an assessment of internal or external influences on credit quality that are not fully reflected in the historical loss or risk rating data

A loan is considered impaired when based on current information and events it is probable that the Company vvill be unable to collect the scheduled payments of principal or interest when due according to the contractual terms of the loan agreement Factors considered by management in determining impairment include payment status collateral value and the probability of collecting scheduled principal and interest payments when due Loans that experience insignificant payment delays and payment shortfalls generally are not classified as impaired Management determines the significance of payment delays and payment shortfalls on a case-by-case basis taking into consideration all known factors affecting the loan and borrower Impainnent is measured on a loan-by-loan basis for nonhomogeneous type loans primarily by the loans obtainable market price or the fair value of the underlying collateral Otherwise the present value of the expected future cash flows discounted at the loans effective interest rate is utilized

10

RNB CORP N otes to Cons o l idated Fin a n cial Statements

Decem ber 31 20 1 4 a n d 20 1 3 (Table Dol lar Amounts in Thousands)

Segments of loans with similar risk characteristics are collectively evaluated for impairment based on the segments historical loss experience adjusted for changes in trends conditions and other relevant factors that affect repayment of the loans Accordingly the Company does not separately identify individual consumer and residential loans for impairment measurements unless such loans are the subject of a restructuring agreement due to financial difficulties of the borrower

Premises and equipment are carried at cost net of accumulated depreciation Depreciation is computed using the straight-line method for premises and the declining-balance method for equipment based on the estimated useful lives of the assets Maintenance and repairs are expensed as incurred while major additions and improvements are capitalized Gains and losses on dispositions are included in cmrent operations

lVIortgage-servicing assets are recognized separately when rights are acquired through sale of fmancial assets Under the servicing assets and liabilities accounting gnidance (ASC 860-50) servicing rights resulting from the sale or securitization of loans originated by the Company are initially measured at fair value at the date of transfer The Company subsequently measures each class of servicing asset using the amortization method Under the amortization method servicing rights are amortized in proportion to and over the period of estimated net servicing income The amortized assets are assessed for impairment or increased obligation based on fair value at each reporting date

The servicing assets are evaluated and measured for impairment Impairment if any would be recognized through a valuation allowance to the extent that fair value is less than the carrying amount of the servicing assets No impairment has been incurred at December 31 2014

Servicing fee income is recorded for fees earned for servicing loans The fees are based on a contractual percentage of the outstanding principal per loan and are recorded as income when earned The amortization of mortgage-servicing rights is netted against loan servicing fee income

Federal Reserve and Federal Home Loan Bank membership stock are required investments for institutions that are members of the Federal Reserve (FRB) and Federal Home Loan Bank (FHLB) system The required investments in the common stock are based on a predetermined formula

Income tax in the consolidated statements of income includes deferred income tax provisions or benefits for all significant temporary differences in recognizing income and expenses for financial reporting and income tax purposes The Company files consolidated tax returns with its subsidiary The Companys tax years still subject to examination by taxing authorities are years subsequent to 20 1 1

Earnings per share have been computed based upon the weighted-average common shares outstanding during each year

Comprehensive income consists of net income and other comprehensive loss net of applicable income taxes Other comprehensive loss includes unrealized gains (losses) on investment securities and changes in the funded status of the defined-benefit plan

11

N ote 2

RNB CORP N otes to Cons o l idated Financial Statem e nts

December 31 20 1 4 and 201 3 (Table Dol lar Amounts in Thousands)

Restriction on Cash and D u e F rom Banks

The Bank is required to maintain reserve funds in cash andor on deposit v1rith the Federal Reserve Bank The reserve required at December 31 2014 was $1194000

N ote 3 I nvestment Secu rities

The amortized cost and approximate fair values together with gross umealized gains and losses of securities are as follows

2014 Gross Gross

Amortized Unrealized Unrealized Fair Cost Gains Losses Value

Available for sale Federal agencies $ 7748 $ 1 6 $ 157 $ 7607 State and municipal 6451 55 75 6431 Mortgage-hacked securities

government-sponsored entities (GSEs) 1 1 754 77 70 11761

Marketable equity securities 14 54 68

Total investment securities $ 25967 $ 202 $ 302 $ 25867

2013 Gross Gross

Amortized Unrealized Unrealized Fair Cost Gains Losses Value

Available for sale Federal agencies $ 10483 $ 1 2 $ 178 $ 10317 State and municipal 8853 56 358 8551 Mortgage-backed securities

GSEs 8836 56 165 8727 Marketable equity securities 27 307 334

Total investment securities $ 28199 $ 431 $ 701 $ 27929

12

I

I I I I I

l t I

r

RNB CORP N otes to Consolidated F i n ancial Statements

Dece m b e r 3 1 201 4 and 20 1 3 (Table Dol lar Amounts in Thousands)

Certain investments in debt and marketable equity securities are reported in the consolidated financial statements at an amount less than their historical cost Total fair value of these investments at December 31 2014 and 2013 was $17630000 and $15891000 which is approximately 681and 569 of the Companys investment portfolio These declines in debt securities primarily resulted from changes in market interest rates

Based on evaluation of available evidence including recent changes in market interest rates credit rating information and information obtained from regulatory filings management believes the declines in fair value for these securities are temporary

Should the impairment of any of these securities become other-than-temporary the cost basis of the investment will be reduced and the resulting loss recognized in net income in the period the othershythan-temporary impairment is identified

The following table shows the Companys investments gross unrealized losses and fair value aggregated by investment class and length of time that individual securities have been in a continuous unrealized loss position at December 31 2014

Less Than 12 Months 12 Months or More Total

Description of Fair U n realized Fair Unrealized Fair Unrealized Securities Value Losses Value Losses Value Losses

Federal agencies $ 4797 $ 114 $ 1817 $ 43 $ 6614 $ 157 State and municipal 3410 75 3410 75 Mortgage-backed securities

GS Es 3568 21 4038 49 7606 70

Total temporarily impaired securities $ 11775 $ 210 $ 5855 $ 92 $ 17630 $ 302

The following table shows the Companys investments gross unrealized losses and fair value aggregated by investment class and length of time that individual securities have been in a continuous unrealized loss position at December 31 2013

Less Than 12 Months 12 Months or More Total

Description of Fair U n realized Fair Unrealized Fair U n realized Securities Value Losses Value Losses Value Losses

Federal agencies $ 4234 $ 151 $ 973 $ 27 $ 5207 $ 178 State and municipal 3392 170 1866 188 5258 358 Mortgage-backed securities

GS Es 3760 106 1666 59 5426 165

Total temporarily impaired securities $ JJ386 $ 427 $ 4505 $ 274 $ 15891 $ 701

13

Federal Agencies

RNB CORP N otes to Consolidated F i n ancial Statements

D ecember 31 2014 and 201 3 (Table Dollar Amounts in Thousands)

The unrealized losses on the Companys investments in direct obligations of US gove=ent agencies were caused by interest rate increases The contractual terms of those investments do not permit the issuer to settle the securities at a price less than the amortized cost bases of the investments Because the Company does not intend to sell the investments and it is not more likely than not the Company 1vill be required to sell the investments before recovery of their amortized cost bases which may be mahffily the Company does not consider those investments to be othershythan-temporarily impaired at December 31 2014

State and Municipal

The unrealized losses on the Companys investments in securities of state and municipal divisions were caused by interest rate increases The contractual terms of those investments do not permit the issuer to settle the securities at a price less than the amortized cost bases of the investments Because the Company does not intend to sell the investments and it is not more likely than not the Company will be required to sell the investments before recovery of their amortized cost bases which may be maturity the Company does not consider those invetments to be other-thanshytemporarily impaired at December 31 2014

Mortgage-Backed Securities - GSEs

The unrealized losses on the Companys investment in residential mortgage-backed securities were caused by interest rate changes The Company expects to recover the amortized cost basis over the term of the securities Because the decline in market value is attributable to changes in interest rates and not credit quality and because the Company does not intend to sell the investments and it is not more likely than not the Company will be required to sell the investments before recovery of their amortized cost bases which may be mah1rity the Company does not consider those investments to be other-than-temporarily impaired at December 31 2014

14

RNB CORP Notes to Consol idated Financial Statements

Decem ber 31 201 4 and 20 1 3 (Table Dol lar Amounts in Thousands)

The am01iized cost and fairmiddotvalue of securities available for sale at December 31 2014 by contractual maturity are shown below Expected maturities will differ from contractual maturities because issuers may have the right to call or prepay obligations with or without call or prepayment penalties

Maturity Distribution at December 31

Available for sale Due in one year or less Due after one through five years Due after five through ten years After ten years

Marketable equity securities Mortgage-backed securities GSEs

Totals

$

$

Amortized

Cost

1223 3854 6718 2404

14199 14

1 1 754

25967

$

$

Fair

Value

1 223 38 19 6632 2364

14038 68

1 1 761

25867

Securities with a carrying value and market value of approximately $17062000 and $13793000 were pledged at December 31 2014 and 2013 to secure certain deposits and for other purposes as permitted or required by law

Proceeds from the sale of securities during 2014 and 2013 totaled approximately $3726000 and $3686000 respectively Gains of approximately $247000 and losses of approximately $8000 were realized on those sales during 2014 and 2013 respectively

N ote 4 Loans and Al lowance and Loan Losses

2014 2013

Corrnnercial and industrial $ 27634 $ 27595 Corrnnercial and farm real estate 34230 29460 Residential real estate 74662 74486 Consumer 1 141 8 12426

Total loans 1 47944 143967

Allowance for loan losses (1 758) (1 846)

Total loans net $ 146186 $ 142121

15

RNB CORP Notes to Consolidated F inancial Statements

D ecember 3 1 2014 and 20 1 3 (Table Dollar Amounts in Thousands)

The risk characteristics of each loan portfolio segment are as follows

Co=ercial and Industrial

Co=ercial and industrial loans are primarily based on the identified cash flows of the borrower and secondarily on the underlying collateral provided by the borrower The cash flows of borrowers however may not be as expected and the collateral securing these loans may fluctuate in value Most co=ercial loans are secured by the assets being fmanced or other business assets such as accounts receivable or inventory and may include a personal guarantee Short-term loans may be made on an unsecured basis In the case ofloans secured by accounts receivable the availability of funds for the repayment of these loans may be substantially dependent on the ability of the borrower to collect amounts due from its customers

Co=ercial and Farm Real Estate including Construction

Co=ercial and farm real estate loans are viewed primarily as cash flow loans and secondarily as loans secured by real estate Co=ercial and farm real estate lending typically involves higher loan principal amounts and the repayment of these loans is generally dependent on the successful operation of the property securing the loan or the business conducted on the property securing the loan Commercial and farm real estate loans may be more adversely affected by conditions in the real estate markets or in the general economy The characteristics of properties securing the Companys commercial and farm real estate portfolio are diverse but with geographic location almost entirely in the Companys market area Management monitors and evaluates co=ercial real estate loans based on collateral geography and risk grade criteria In general the Company avoids financing single purpose projects unless other underwriting factors are present to help mitigate risk

Construction loans are underwritten utilizing feasibility studies independent appraisal reviews and fmancial analysis of the developers and property owners Construction loans are generally based on estimates of costs and value associated with the complete project These estimates may be inaccurate Construction loans often involve the disbursement of funds with repayment substantially dependent on the success of the ultimate project Sources of repayment for these types of loans may be pre-committed permanent loans from approved long-term lenders sales of developed property or an interim loan commitment from the Company until permanent financing is obtained These loans are closely monitored by on-site inspections and are considered to have higher risks than other real estate loans due to their ultimate repayment being sensitive to interest rate changes governmental regulation of real property general economic conditions and the availability oflong-term fmancing

16

RNB CORP N otes to Consolidated Financial Statements

D ecem ber 3 1 20 1 4 a n d 20 1 3 (Table Dollar Amounts in Thousands)

Residential and Consumer

Residential and consumer loans consist ofiwo segments - residential real estate loans and consumer loans For residential mortgage loans that are secured by 1-4 family residences and are generally owner-occupied the Company generally establishes a maximum loan-to-value ratio Home equity loans are typically secured by a subordinate interest in 1-4 family residences for which the Company holds a first lien Consumer personal loans are secured by consumer personal assets such as automobiles or recreational vehicles Some consumer personal loans are unsecured such as small installment loans and certain lines of credit Repayment of these loans is primarily dependent on the personal income of the b01Towers which can be impacted by economic conditions in their market areas such as unemployment levels Repayment can also be impacted by changes in property values on residential properties Risk is mitigated by the fact that the loans are of smaller individual amounts and spread over a large number of borrowers

The following tables present by portfolio segment the activity in the allowance for loan losses for the years ended December 31 2014 and 2013

2014 Commercial

a n d Industrial

Commercial and Farm

Real Estate Residential Real Estate eonsumer Total

Beginning Balance $ 286 $ 263 $ 977 $ 320 $ 1846 Provision (8) 59 406 23 480 Loans charged off (459) (159) (618) Recoveries 50 50

Ending Balance $ 278 $ 322 $ 924 $ 234 $ 1758

2013 Commercial Commercial

a n d and Farm Residential Industrial Real Estate Real Estate Consumer Total

Beginning Balance $ 218 $ 257 $ 1068 $ 216 $ 1759

Provision 80 6 77 317 480

Loans charged off (12) (203) (310) (525)

Recoveries 35 97 132

Ending Balance $ 286 $ 263 $ 977 $ 320 $ 1846

17

RNB CORP N otes to Consol idated F i n an cial Stateme nts

December 31 2014 and 20 1 3 (Table Dollar Amounts i n Thousands)

The following tables present the balance in the allowance for loan losses and the recorded investment in loans based on the portfolio segment and impairment method as of December 31

2014 and2013

2014 Commercial Commercial

and and Farm Residential Industrial Real Estate Real Estate Consumer

Allowance Balances

Individually evaluated

for impairment $ $ 37 $ JO $ $ Collectively evaluated

for impairment 278 285 914 234

Total allowance for loan losses $ 278 $ 322 $ 924 $ 234 $

Loan Balances

Individually evaluated

for impairment $ $ 846 $ 1730 $ $ Collectively evaluated

for impairment 27634 33384 72932 I 1418

Total loan balances $ 27634 $ 34230 $ 74662 $ I 1418 $

2013 Commercial Commercial

and and Farm Residential Industrial Real Estate Real Estate Consumer

Allowance Balances

Individually evaluated

for impairment $ 7 $ 36 $ 126 $ $ Collectively evaluated

for impairment 279 227 851 320

Total allowance for loan losses $ 286 $ 263 $ 977 $ 320 $

Loan Balances

Individually evaluated

for impairment $ 344 $ 682 $ 1876 $ $ Collectively evaluated

for impairment 27251 28778 72610 12426

Total loan balances $ 27595 $ 29460 $ 74486 $ 12426 $

Total

47

1711

1758

2576

145368

147944

Total

169

1677

1846

2902

141065

143967

18

RNB CORP Notes to Consolidated Financial Statements

D ecemb e r 3 1 20 1 4 a n d 20 1 3 (Table Dol lar Amounts i n Thousands)

Internal Risk Categodes

Loan grades are numbered 1 through 5 Grades 1 through 2 are considered satisfactory grades The grade of 3 or WatchSpecial Mention represents loans of lower quality and is considered criticized The grades of 4 or Substandard and 5 or Doubtful refer to assets that are classified The use and application of these grades by the Bank will be uniform and shall conform to the banks policy

Pass (1-2) Loans are of acceptable quality and repayment ability providing a nominal credit risk

VatchSpecial Mention (3) Loans have potential weaknesses that deserve managements close attention If left uncorrected these potential weaknesses may result in deterioration of the repayment prospects for the loan or in the institutions credit position at some future date Special mention loans are not adversely classified and do not expose an institution to sufficient risk to warrant adverse classification Ordinarily special mention credits have characteristics which corrective management action would remedy

Substandard ( 4) Loans are inadequately protected by the current sound worth and paying capacity of the obligor or of the collateral pledged if any Loans so classified must have a well-defined weakness or weaknesses that jeopardize the liquidation of the debt They are characterized by the distinct possibility that the Bank will sustain some loss if the deficiencies are not corrected

Doubtful (5) Loans classified as doubtful have all the weaknesses inherent in those classified Substandard with the added characteristic that the weaknesses make collection or liquidation in full on the basis of current known facts conditions and values highly questionable and improbable

The following tables present the credit risk profile of the Companys loan portfolio based on rating category and payment activity as of December 31 2014 and 2013

2014

Commercial Commercial and and Farm Residential

Industrial Real Estate Real Estate Consumer Total

Grade

Pass (1-2) $ 25805 $ 31866 $ 72308 $ 11386 $ 141365 WatchSpecial mention (3) 1474 1161 31 2666 Substandard ( 4) 317 1203 2323 32 3875 Doubtful ( 5) 38 38

Total $ 27634 $ 34230 $ 74662 $ 11418 $ 147944

19

Grade

Pass (1-2)

RNB CORP Notes to Consol idated F inancial Statements

December 31 2014 and 20 1 3 (Table Dol lar Amounts in Thousands)

2013 Commercial Commercial

and and Farm Residential Industrial Real Estate Real Estate

$ 25450 $ 27159 $ 71 712

WatchSpecial mention (3) 1736 1135 35

Substandard ( 4) 409 1 1 66 2739

Doubtful (5)

Total $ 27595 $ 29460 $ 74486

Consumer Total

$ 12335 $ 136656

44 2950

47 4361

$ 12426 $ 143967

The following tables present the Companys loan portfolio aging analysis as of December 3 1 2014 and 20 13

201 4 Loans

90 Days gt 90 Days 30-59 Days 6089 Days and Total Total and Past Due Past Due Greater Past Due Current Loans Accruing

Commercial and industrial $ 236 $ 8 $ 5 1 $ 295 $ 27339 $ 27634 $ 38 Commercial and farm real estate 5 1 3 526 1 039 33191 34230 Residential real estate 2448 494 1588 4530 70132 74662 1869 Consumer 133 34 3 170 1 1248 1 1 418 3

Total loans $ 3330 $ 536 $ 2168 $ 6034 $ 141910 s 147944 $ 1910

201 3 Loans

90 Days gt 90 Days 30-59 Days 60-89 Days and Total Total and Past Due Past Due Greater Past Due Current Loans Accruing

Commercial and industrial $ 80 s 92 $ 2 1 5 $ 387 s 27208 $ 27595 $ Commercial and farm real estate 548 192 286 1026 28434 29460

Residential real estate 2837 520 2071 5428 69058 74486 1728 Consumer 108 53 26 1 87 12239 12426 26

Total loans s 3573 s 857 $ 2598 $ 7028 $ 136939 $ 143967 $ 1754

20

)

RNB CORP N otes to C onsol i d ated F i n a n cial Statements

D ecember 3 1 2014 and 20 1 3 (Table Dollar Amounts in Thousands)

The following table presents the Companys nonaccrual loans at December 3 1 2014 and 20 1 3

Commercial and industrial Commercial and farm real estate Residential real estate Consumer

Total nonaccrual loans

$

$

2014

145 830

1 294 9

2278

$

$

2013

1 70 886

1797 6

2859

The following tables present impaired loans for the years ended December 3 1 2014 and 20 1 3

Impaired loans vithout a specific

valuation allovance

Commercial and industrial

Commercial and farm real estate

Residential real estate

Consumer

Total impaired loans with no related specific reserve

Impaired loans with a specific

valuation allovance

Commercial and industrial

Commercial and farm real estate

Residential real estate

Consumer

Total impaired loans with

an allowance recorded

Total impaired loans

Recorded

$

$

Balance

379 1193

1572

467 537

1004

2576

Unpaid Principal

$

$

Balance

379 1 193

1572

467 537

1 004

2576

2014

Specific Allowance

$

$

37 10

47

47

Average Investment i n

$

Impaired Loans

218 372

1 264

1854

380 501

881

2735

I nterest Income

Recognized

$

$

14 15

1 1 6

145

21 21

42

187

21

RNB CORP N otes to Consol id ated Financial Statements

December 31 20 1 4 and 20 1 3 (Table Dollar Amounts in Thousands)

201 3 Average

Unpaid I nvestment in

Recorded Principal Specific Impaired Balance Balance Allowance Loans

Impaired loans without a specific

valuation allowance

Commercial and industrial $ 179 $ 179 $ $ 1 99 Commercial and farm real estate 61 94 78 Residential real estate 1367 1367 1 955 Consumer

Total impaired loans with

no related specific reserve 1607 1640 2232

Jmpaired loans with a specific

valuation allovance

Commercial and industrial 165 165 7 92 Commercial and farm real estate 621 621 36 506 Residential -real estate 509 509 126 521 Consumer

Total impaired loans with

an allowance recorded 1 295 1295 169 1 1 1 9

Total impaired loans $ 2902 $ 2935 $ 1 69 $ 3351

The following tables present information regarding troubled debt restructurings by class restructured for the years ended December 31 2014 and 2013

2014 Pre-

Interest

Income Recognized

$ 14

58

72

4 24 22

50

$ 122

Post-Modification Modification

Commercial and industrial Commercial and farm real estate Residential real estate Consumer

Number of Loans

1

$

$

Recorded Balance

83

83

Recorded Balance

$ 83

$ 83

22

RNB CORP N otes to Consol id ated F i nancial Statements

December 31 201 4 and 2013 (Table Dol lar Amounts in Thousands)

2013

Pre-Modification

Number of Recorded Loans Balance

Commercial and industrial 1 $ 104 Commercial and farm real estate 300 Residential real estate Consumer

2 $ 404

Post-M odification

Recorded Balance

$ 104 300

$ 404

The troubled debt restructurings noted above generally consisted of interest rate and maturity date concessions and increased the allowance by $6000 in 2013 The troubled debt restructuring in 2014 did not impact the allowance for loan losses

The Company has not had any troubled debt restructuring subsequently default during 2014 or 2013 Default occurs when a loan or lease is 90 days or more past due or transferred to nonaccrual and is vrithin 12 months of restructuring

middot

N ote 5 P rem ises and E q u ipment

2014

Land $ 785

Buildings 3449

Equipment 2601 Total cost 6835

Accumulated depreciation (4003)

Net $ 2832

N ote 6 Deposits

2014

Demand deposits $ 58870

Savings deposits 27508

Certificates and other time deposits of $ 100000 or more 33962

Other certificates and time deposits 41 436

Total deposits $ 161776

2013

$ 785 3345 2901 7031

(4108)

$ 2923

2013

$ 52861 25699 25030 51061

$ 154651

23

RNB CORP Notes to Consolidated Financial Statements

December 31 201 4 and 2013 (Table Dollar Amounts in Thousands)

Certificates and other time deposits maturing in years ending after December 3 1 2014

2015 $ 33593 2016 25560 2017 5005 201 8 4079 2019 6744 Thereafter 417

$ 75398

Certificates of deposit in excess of $250000 totaled $ 15309000 at December 3 1 2014

Note 7 Other Borrowings

2014 2013

Securities sold under repurchase agreements Note payable 45 unsecured due March 25 2015 FHLB overdraft line of credit

$ 9033 1 196

$ 9128 1196 2915

$ 10229 $ 13239

Securities sold under agreements to repurchase consist of obligations of the Company to other parties The obligations are secured by investment securities and such collateral is held by a safekeeping agent The maximum amount of outstanding agreements at any month-end during 2014 and 2013 totaled approximately $ 1 6795000 and $17886000 and the monthly average of such agreements totaled approximately $10807000 and $ 1 1 524000 respectively The agreements at December 3 1 20 14 matured on January 1 2015

The Bank has an overdraft line of credit with the FHLB in the amount of $8000000 The Company had $0 and approximately $2915000 in borrowings on this line of credit at December 31 2014 and 2013 respectively

Note 8 F H LB Advances

The Company had no advances outstanding from the HILB at December 3 1 2014 and 2013 At December 3 1 2014 the Company also has pledged approximately $57047000 of mortgage loans to collateralize any future advances

24

N ote 9

RNB CORP N otes to Consolidated F i nancial Statements

December 31 201 4 a n d 2013 (Table Dol lar Amounts in Thousands)

Loan Servicing

Loans serviced for others are not included in the accompanying consolidated balance sheets The loans are serviced for the Federal National Mortgage Association and the Federal Home Loan Bank of Indianapolis The unpaid principal balances ofloans serviced for others totaled approximately $94537000 and $93506000 at December 3 1 2014 and 2013 respectively

The Company capitalizes mortgage-servicing rights on these loans The aggregate fair value of capitalized mortgage-servicing rights at December 3 1 2014 and 2013 approximates carrying value

Mortgage-servicing rights B alances beginning of year Servicing rights capitalized Amortization of servicing rights

Balances end of year

N ote 1 0 I n come Tax

Income tax expense (benefit) Currently payable

Federal State

Deferred Federal State

Total income tax expense

Reconciliation of federal statutory to actual tax expense Federal statutory income tax at 34 Tax-exempt interest Effect of state income taxes Other

Actual tax expense

$

$

$

$

$

$

2014

2014

837 109 (96)

850

625 1 1 0

(63) 17

689

699 (132)

83 39

689

$

$

$

$

$

$

2013

764 1 99

( 126)

837

2013

241 47

( 19) 1 5

284

428 (149)

41 (36)

284

25

RNB CORP Notes to Consolidated Financial Statements

December 3 1 2014 and 2013 (Table Dol lar Amounts in Thousands)

A cumulative net deferred tax asset (liability) is included in other assets (liabilities) The components of the asset (liability) are as follows

2014 2013

Assets

Allowance for loan losses Securities available for sale Pension and employee benefits Other

Total assets

Liabilities

State income tax FHLB stock Depreciation Prepaid expenses Loan fees Mortgage-servicing rights

Total liabilities

N ote 1 1 Accu m u l ated Comprehensive Loss

$

$

The components of accumulated other comprehensive loss are as follows

Net unrealized losses on available-for-sale securities net of tax of$(35) and $(129)

Items not yet recognized in net periodic pension benefit cost net of tax of$(925) and $(656)

$

$

406 $ 448 34 75

360 47 201 52

1001 622

(46) (23) (22) (22) (70) (94) (34) (58)

(193) (163) (351) (348) (716) (708)

285 $ (86)

2014 2013

(65) $ (197)

(1450) (1000)

(1515) $ (1197) ========

26

RNB CORP N otes to Consol i dated F i nancial Statem ents

D ecem b e r 3 1 201 4 and 2013 (Table Dol lar Amounts in Thousands)

Amounts reclassified from AOCI and the affected line items in the consolidated statements of income during the years ended December 31 2014 and 2013 were as follows

Unrealized gains on available-for-sale securities

Amortization of defined-benefit pension items

$

From AOC 2014 2013

(247) $ 8 Net realized (gains) losses on securities

____ 9_8_ -----(3) Tax effect

$ (149) $ 5 Net reclassified amount =====

Net loss $ 1373 $ 1 19 Components are included in the computation

(544)

$ 829 $

Total reclassification out of AOC $ 680 $

N ote 1 2 Commitments and Contingent Liabi l ities

of net periodic pension cost and presented

in Note 15 (47) Tax effect

72 Net reclassified amount

77

In the normal course of business there are outstanding commitments and contingent liabilities such as commitments to extend credit and standby letters of credit which are not included in the accompanying consolidated financial statements The B anks exposure to credit loss in the event of nonperformance by the other party to the financial instruments for commitments to extend credit and standby letters of credit is represented by the contractual or notional amount of those instruments The Bank uses the same credit policies in making such commihnents as it does for instruments that are included in the consolidated balance sheets

Financial instruments whose contract amount represents credit risk as of December 31 were as follows

201 4 2013

Commitments to extend credit Standby letters of credit

$ 30898 $ 25776 30

27

RNB CORP N otes to Consolidated Financial Statements

D ecember 31 201 4 and 2013 (Table Dol lar Amounts in Thousands)

Commitments to extend credit are agreements to lend to a customer as long as there is no violation of any condition established in the contract Commitments generally have fixed expiration dates or other termination clauses and may require payment of a fee Since many of the commitments are expected to expire without being drawn upon the total commitment amounts do not necessaiily represent future cash requirements The Bank evaluates each customers creditworthiness on a case-by-case basis The amount of collateral obtained if deemed necessary by the Bank upon extension of credit is based on managements credit evaluation Collateral held vaiies but may include accounts receivable inventory property and equipment and income-producing commercial properties

Standby letters of credit are conditional commitments issued by the Bank to guarantee the performance of a customer to a third party

The Company and Bank are also subject to claims and lawsuits which aiise piimaiily in the ordinary course of business It is the opinion of management that the disposition or ultimate resolution of such claims and lawsuits will not have a material adverse effect on the consolidated financial position of the Company

N ote 13 Restriction on Bank D ividends

Without piior approval of the Comptroller of the Currency the Bank is restiicted by national b anking laws as to the maximum amount of dividends it can pay in any calendar year to the Banks retained net profits (as defined) for that year and the two preceding years As a practical matter the Bank restricts dividends to a lesser amount because of the need to maintain an adequate capital structure

N ote 1 4 Regu latory Capital

The Bank is subject to vaiious regulatory capital requirements administered by the federal banking agencies Failure to meet minimum capital requirements can initiate actions by the regulatory agencies that if undertaken could have a mateiial effect on the Companys consolidated financial statements Under capital adequacy guidelines and the regulatory framework for prompt corrective action the Bank must meet specific capital guidelines that involve quantitative measures of the Banks assets liabilities and certain off-balance-sheet items as calculated under regulato1y accounting practices

The Banks capital amounts and classification are also subject to qualitative judgments by the regulators about components iisk weightings and other factors

At December 3 1 2014 management of the Bank believes that it meets all capital adequacy requirements to which it is subject The most recent notification from the regulatory agency categorized the Bank as well capitalized under the regulatory framework for prompt corrective action There have been no conditions or events since that notification that management believes have changed this categoiization

28

RNB CORP N otes to Consolidated Financial Statements

Decem ber 3 1 20 1 4 a n d 20 1 3 (Table Dollar Amounts in Thousands)

The Banks actual and required capital amounts and ratios are as follows

Required for

Actual Adequate Capital1

Amount Ratio Amount Ratio

As of December 3 1 2014

Total capital1 (to risk-weighted assets) $ 1 8404 129 $ 1 1 380 80 Tier 1 capital1 (to risk-weighted assets) 1 6612 1 1 7 5690 40

Tier 1 capital1 (to average assets) 16612 86 7701 40

As of December 31 2013

Total capital1 (to risk-weighted assets) $ 1 7759 128 $ 1 1 122 80 Tier 1 capital1 (to risk-weighted assets) 15883 1 1 4 5561 40 Tier 1 capital 1 (to average assets) 15883 85 7448 40

1 As defined by regulatory agencies

N ote 1 5 Employee Benefits

To Be Well

Capitalized1

Amount Ratio

$ 14225 100 8535 60

9626 50

$ 13 903 100 8342 60 93 10 50

The Company has a noncontributory defined-benefit pension plan covering all employees who meet the eligibility requirements The Companys funding policy is to make the minimum annual contribution that is required by applicable regulations plus such amounts as the Company may determine to be appropriate from time to time The Company expects to contribute $200000 to the plan in 201 5

middot

The Company uses a December 3 1 measurement date for the plan assumptions are

Significant balances costs and

Benefit obligation Fair value of plan assets

Funded status

Accrued benefit cost recognized in the consolidated balance sheets

$

$

$

Pension Benefits 201 4 201 3

(4066) $ (3329) 3 194 3217

(872) $ (1 12)

(872) $ (1 12)

29

RNB CORP N otes to Consolidated F i n ancial Statements

Decem ber 3 1 2 0 1 4 and 20 1 3 (Table Dol lar Amounts in Thousands)

Amounts recognized in accumulated other comprehepsive loss net of tax not yet recognized as components of net periodic benefit cost consist of

Net loss $

Pension Benefits 201 4 201 3

1450 $ 1 000

The accumulated benefit obligation for the defined-benefit pension plan was approximately $3364000 and $2778000 at December 3 1 2014 and 2013 respectively

Other significant balances and costs are

Benefit cost Employer contributions B enefits paid

$

Pension Benefits 201 4 2013

241 200 251

$ 393 600 406

Other changes in plan assets and benefit obligations recognized in other comprehensive loss

Amounts arising during the period Net gain

Amounts reclassified as a component of net periodic benefit cost of the period Net loss

Weighted-average assumptions used to determine benefit costs

Discount rate Expected return on plan assets Rate of compensation increase

$

$

Pension Benefits 201 4 201 3

(1 10) $ (267)

829 72

719 $ (195)

Pension Benefits 201 4 201 3

450 400 250

375 400 250

30

RNB CORP Notes to Consolidated F i nancial Statements

December 3 1 2 0 1 4 and 2 0 1 3 (Table Dol lar Amounts in Thousands)

Weighted-average assumptions used to determine benefit obligations

Pension Benefits 2014 201 3

Discount rate Rate of compensation increase

350 250

450 250

The estimated net loss for the defmed-benefit pension plan expected to be amortized from accumulated other comprehensive loss into net periodic benefit cost over the next fiscal year is $ 1 64000 The Company has estimated the long-term rate ofreturn on plan assets based primarily on historical returns on plan assets adjusted for changes in target portfolio allocations and recent changes in long-term interest rates based upon publicly available information

The following benefit payments which reflect expected future service as appropriate are expected to be paid as ofDecember 3 1 2014

Pension B e n efits

2015 $ 188 2016 1 138 2017 153 2018 44 2019 52 2020-2024 834

Plan assets are held by a bank-administered trust fund which invests the plan assets in accordance with the provisions of the plan agreement The plan agreement permits investments in common stocks corporate bonds and debentures US Government securities certain insurance contracts real estate and other specified investments

Plan assets are re-balanced periodically At December 3 1 201 4 and 2013 plan assets by category are as follows

Debt securities Equity securities Other

Pension B e nefits 2014 2013

25 5

70

25 5

70

100 100

31

RNB CORP N otes to Consolidated F inancial Statements

D ecember 3 1 2 0 1 4 and 2 0 1 3 (Table Dollar Amounts in Thousands)

Pension Plan Assets

Following is a description of the valuation methodologies llsed for pension plan assets measured at fair value on a recurring basis and recognized in the accompanying consolidated balance sheets as well as the general classification of pension plan assets pursuant to the valuation hierarchy

Where quoted market prices are available in an active market plan assets are classified within Level 1 of the valuation hierarchy Level 1 plan assets include money market funds corporate obligations and common stocks If quoted market prices are not available then fair values are estimated by using pricing models quoted prices of plan assets with similar characteristics or discounted cash flows Level 2 plan assets include certificates of deposit In certain cases where Level 1 or Level 2 inputs are not available plan assets are classified within Level 3 of the hierarchy The plan does not have any Level 3 assets

The fair values of the Companys pension plan assets at December 3 1 2014 and 2013 by asset class are as follows

201 4 Fair Value M easurements Using

Quoted Prices in Active Significant

M arkets for Other Significant Identical Observable Unobservable

Fair Assets Inputs Inputs Value (Level 1 ) (Level 2) (Level 3)

Common stocks $ 154 $ 154 $ $ Corporate obligations 806 806 Money market funds 1304 1304 Certificates of deposit 930 930

$ 3194 $ 2264 $ 930 $

2013 Fair Value Measurements Using

Quoted Prices in Active Significant

M arkets for Other Significant Identical O bservable Unobservable

Fair Assets Inputs Inputs Value (Level 1 ) (Level 2) (Level 3)

Common stocks $ 1 54 $ 154 $ $ Corporate obligations 804 804 Money market funds 939 939 Certificates of deposit 1320 1320

$ 3217 $ 1897 $ 1320 $

32

RNB CORP N otes to Consol idated Financial Statements

December 3 1 201 4 and 2 0 1 3 (Table Dol lar Amounts in Thousands)

The Bank has a retirement savings 401 (k) plan in which substantially all employees may participate The Bank matches employees contributions at the rate of 65 percent for 2014 and 2013 for the first 6 percent of base salary contributed by participants The Banks expense for the plan was approximately $60000 for 2014 and for 2013

N ote 1 6 Related Party Transactions

The Bank has entered into transactions with certain directors executive officers significant stockholders and their affiliates or associates (related parties) Such transactions were made in the ordinary course of business on substantially the same terms and conditions including interest rates and collateral as those prevailing at the same time for comparable transactions with other customers and did not in the opinion of management involve more than normal credit risk or present other unfavorable features

Deposits from related parties held by the Bank at December 3 1 2014 and 2013 totaled approximately $ 1 770000 and $ 1 784000 respectively Loans to related parties held at the Bank at December 3 1 2014 and 2013 totaled approximately $ 1 307000 and $326000 respectively

N ote 1 7 Fai r Val ues of Fi nancial Instru m ents

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measnrement date Fair value measurements must maximize the use of observable inputs and minimize the use of unobservable inputs There is a hierarchy of three levels of inputs that may be used to measnre fair value

Level 1 Quoted prices in active markets for identical assets or liabilities

Level 2 Observable inputs other than Level 1 prices such as quoted prices for similar assets or liabilities quoted prices in markets that are not active or other inputs that are observable or can be corroborated by observable market data for substantially the full term of the assets or liabilities

Level 3 Unobservable inputs supported by little or no market activity and are significant to the fair value of the assets or liabilities

33

RNB CORP Notes to Cons o l i dated Financial Statements

D ecember 3 1 20 1 4 and 20 1 3 (Table Dollar Amounts in Thousands)

Following is a description of the valuation methodologies and inputs used for assets measured at fair value on a recurring basis and recognized in the accompanying consolidated balance sheets as well as the general classification of such assets pursuant to the valuation hierarchy

Available-for-Sale Securities

Vhere quoted market prices are available in an active market securities are classified within Level 1 of the valuation hierarchy Level 1 securities consist of marketable equity securities If quoted market prices are not available then fair values are estimated by using pricing models quoted prices of securities with similar characteristics or discounted cash flovvs The fair value measurements consider observable data that may include broker quotes market spreads cash flows tbe US Treasury yield curve live trading levels trade execution data market consensus prepayment speeds and credit infonnation Level 2 securities include federal agencies mortgageshybacked securities and state and municipal securities The Company does not have any Level 3 securities

The following tables present the fair value measurements of assets recognized in the accompanying consolidated balance sheets measured at fair value on a recmTing basis and the level within the fair value hierarchy in which the fair value measurements fall at December 3 1 2014 and 2013

201 4 Fair Value Measurements Using

Quoted Prices in Active Significant

Markets for Other Significant Identical Observable Unobservable

Fair Assets Inputs In puts Value (Level 1 ) (Level 2) (Level 3)

Federal agencies $ 7607 $ $ 7607 $ State and municipal 643 1 643 1 Mortgage-backed securities GSEs 1 1 761 1 1761 Marketable equity securities 68 68

$ 25867 $ 68 $ 25799 $

34

RNB CORP N otes to Consol idated Financial Statem ents

December 3 1 2 0 1 4 a n d 2 0 1 3 (Table Dol lar Amounts i n Thousands)

2013 Fair Value Measurements Using

Quoted Prices in Active Significant

M arkets for Other Significant Identical Observable Unobservable

Fair Assets Inputs In puts Value (Level 1 ) (Level 2) (Level 3)

Federal agencies $ 1 03 1 7 $ $ 103 1 7 $ State and municipal 85 5 1 8551 Mortgage-backed securities GSEs 8727 8727 Marketable equity securities 334 334

$ 27929 $ 334 $ 27595 $

Following is a description of the valuation methodologies and inputs used for assets measured at fair value on a nomecurring basis and recognized in the accompanying consolidated balance sheets as well as the general classification of such assets pursuant to the valuation hierarchy For assets classified withln Level 3 of the fair value hierarchy the process used to develop the reported fair value is described below

Collateral-Dependent Impaired Loans Net of Allowance

The estimated fair value of collateral-dependent impaired loans is based on the appraised fair value of the collateral less estimated cost to sell Collateral-dependent impaired loans are classified within Level 3 of the fair value hierarchy

The Company considers the appraisal or evaluation as the starting point for determining fair value and then considers other factors and events in the environment that may affect the fair value Appraisals of the collateral underlying collateral-dependent loans are obtained when the loan is determined to be collateral-dependent and subsequently as deemed necessary by the Controllers office Appraisals are reviewed for accuracy and consistency by the Controllers office Appraisers are selected from the list of approved appraisers maintained by management The appraised values are reduced by discounts to consider lack of marketability and estimated cost to sell if repayment or satisfaction of the loan is dependent on the sale of the collateral These discounts and estimates are developed by the Controllers office by comparison to historical results

35

RNB CORP N otes to Consolidated Financial Statements

December 3 1 2 0 1 4 and 2 0 1 3 (Table Dollar Amounts in Thousands)

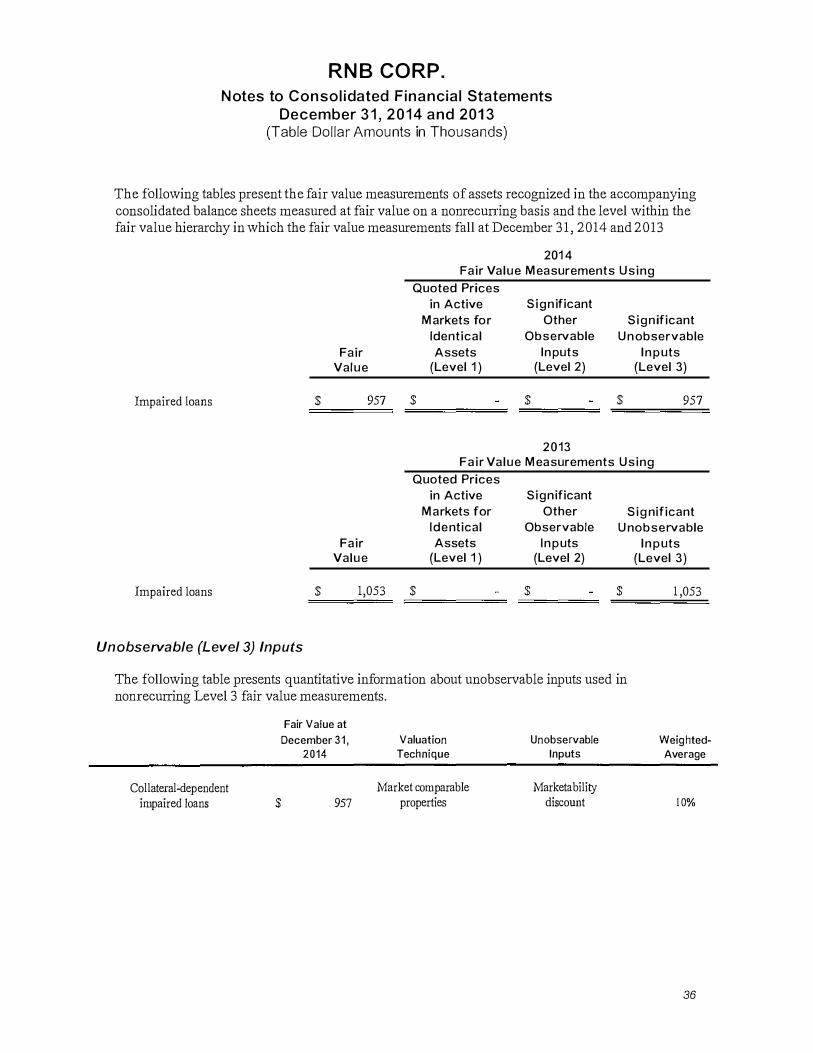

The following tables present the fair value measurements of assets recognized in the accompanying consolidated balance sheets measured at fair value on a nonrecurring basis and the level within the fair value hierarchy in which the fair value measurements fall at December 3 1 2014 and 2013

201 4 Fair Value M easurements Using

Quoted Prices in Active Significant

M arkets for Other Significant Identical Observable Unobservable

Fair Assets Inputs Inputs Value (Level 1 ) (Level 2) (Level 3)

Impaired loans $ 957 $ $ $ 957

2013 Fair Value M easurements Using

Quoted Prices in Active Significant

M arkets for Other Sig nificant Identical Observable U nobservable

Fair Assets Inputs Inputs Value (Level 1 ) (Level 2) (Level 3)

Impaired loans $ 1053 $ $ $ 1 053

Unobservable (Level 3) Inputs

The following table presents quantitative information about unobservable inputs used in nonrecurring Level 3 fair value measurements

Fair Value at

December 3 1 Valuation Unobservable Weig hted-2014 Technique Inputs Average

Collateral-dependent Market comparable Marketability

impaired Joans $ 957 properties discount 1 0

36

RNB CORP N otes to Consolid ated Financial Statements

December 3 1 20 1 4 and 201 3 (Table Dollar Amou nts in Thousands)

Fair Value at

December 3 1 Valuation Unobservable Weighted-

2013 Technique Inputs Average

Collateral-dependent Market comparable Marketability

impaired loans $ 1053 properties discount 10

The following methods and assumptions were used to estimate the fair value of all other financial instruments recognized in the accompanying consolidated balance sheets at amounts other than fair value

Cash and Cash Equivalents - The fair value of cash and cash equivalents approximates carrying value

Loans and Loans Held for Sale - For both short-term loans and variable-rate loans that reprice frequently and with no significant change in credit risk fair values are based on carrying values

The fair values for other loans are estimated using current market quotes or discounted cash flow analyses using interest rates currently being offered for loans with similar terms to borrowers of similar credit quality

FRB and FHLB Membership Stock - Fair value is based on the price at which it may be resold and approximates carrying value

Mortgage-Servicing Rights - The fair value of mortgage-servicing rights approximates carrying value

Interest ReceivablePayable - The fair values of interest receivablepayable approximate carrying values

Deposits - The fair values of noninterest-bearing interest-bearing demand and savings accounts are equal to the amount payable on demand at the balance sheet date Fair values for fixed-rate certificates of deposit are estimated using a discounted cash flow calculation that applies interest rates currently being offered on certificates to a schedule of aggregated expected monthly maturities on such time deposits

Other Borrowings - Other borrowings consist primarily of securities sold under repurchase agreements The fair value of these borrowings approximates carrying value

FHLB Advances - Rates currently available to the Company for debt with similar terms and remaining maturities are used to estimate the fair value of existing debt

37

RNB CORP Notes to Consol idated Financial Statements

December 3 1 2 0 1 4 and 2 0 1 3 (Table Dollar Amounts i n Thousands)

The estimated fair values of the Companys financial instruments are as follows

201 4 Carrying Fair Carrying Amount Value Amo u n t

Assets

Cash and cash equivalents $ 5933 $ 5933 $ 4491 Investment securities available for sale 25867 25867 27929 Loans including loans held for sale net 147571 146771 142260 Stock in FRB and Fl-ILB 740 740 720 Mortgage-servicing rights 850 850 837 Interest receivable 1 136 1 136 1 101

Liabilities

Deposits 1 61776 162233 154651 Other borrowings 1 0229 10229 13240 Interest payable 181 181 358

Note 1 8 Condensed Financial I nformation (Parent Company On ly)

201 3

Fair Value

$ 4491 27929

139969 720 837

1 101

155678 1 3240

358

Presented below is condensed financial information as to financial position results of operations and cash flows of the Company

Condensed Balance Sheets

Assets

Cash on deposit with subsidiary Investment in co=on stock of subsidiary - The

Riddell National Bank Other assets

Total assets

Liabilities

Dividends payable B orrovings Other liabilities

Total liabilities

Shareholders Equity

Total liabilities and shareholders equity

$

$

$

$

201 4

226

15097 691

16014

554 1196

5 1755

14259

16014

$

$

$

$

201 3

196

14688 637

15521

551 1196

5 1752

13769

15521

38

RNB CORP N otes to Consolidated F inancial Statem ents

Dece m ber 3 1 2 0 1 4 and 201 3 (Table Dollar Amounts in Thousands)

Condensed Statements of Income and Comprehensive Income

2014

Income

Dividends from subsidiary $ 660 Dividends from reinsurance company 5

Total income 665

Expenses 57

Income b efore income tax and equity in income of subsidiary 608 Income tax benefit 4

Income before equity in undistributed income of subsidiary 612 Equity in undistributed income of subsidiary 727

Net Income $ 1339

Comprehensive Income $ 1021

Condensed Statements of Cash Flows

2014

Operating Activities

Net income $ 1339 Equity in undistributed income

of subsidiary (727) Other adjustments (26)

Net cash provided by operating activities 586

Investing Activity - paydown ofborrowings (27)

Financing Activities

Cash dividends (609) Stock issuance 80

Net cash used in financing activities (529)