Embed Size (px)

Citation preview

1

Preparing for tough times?

Kelvin Sam, CFA

DnB NOR Asian Investor Conference

September 12, 2011

FPSO outlook

Copyright © 2011 IHS Inc. All Rights Reserved.

ODS-Petrodata tracks 198 FPSOs and 130 potential awards

in FPSbase

2

Copyright © 2011 IHS Inc. All Rights Reserved.

Agenda

1. Overview

2. Lessons from past downturns

3. Capacity

4. Demand

5. Conclusion

3

Copyright © 2011 IHS Inc. All Rights Reserved.

What is an FPSO?

• FPSO (Floating, Production, Storage,

Offloading)

• Ship-shaped structure which receive,

process and stores oil

• Widely used in the Asia-Pacific, Brazil,

Africa and Europe

• 60 per cent of the global fleet is leased

while 40 per cent is owned by oil

companies

4

Copyright © 2011 IHS Inc. All Rights Reserved.

Introduction

5

FPSO contract awards

Newbuilds

Normally owned

USD 0.8 – 2 billion capex

3-4 years construction

Conversions

Normally leased

USD 250 –800 million

capex

2-3 years construction

Redeployments

Normally leased

At least USD 15 million

capex

3-12 months upgrade

Copyright © 2011 IHS Inc. All Rights Reserved.

New leasers arriving with 16 leasers actively bidding globally

6

Asia-Pacific Leasers

• Petrofac

• Ramunia

• Aker FP

• Berlian Laju Tanker

• Bluewater

• Bumi Armada

• BW Offshore

• EOC

• M3nergy

• Maersk FPSO

• MISC

• Mitra Rajasa

• MODEC

• Premuda

• Rubicon/Sea Prod.

• SBM

• Tanker Pacific

Brazil Leasers

• BW Offshore

• Maersk FPSO

• MODEC

• OSX

• Petroserv

• Saipem

• SBM

• Sevan Marine

• Teekay Petrojarl

Africa Leasers

• Bumi Armada

• BW Offshore

• Fred Olsen

• MODEC

• Saipem

• SBM

Europe Leasers

• Bluewater

• BW Offshore

• Maersk FPSO

• Saipem

• Sevan Marine

• Teekay Petrojarl

Expect more consolidation involving smaller players (< 6 units each)

Copyright © 2011 IHS Inc. All Rights Reserved.

0

1

2

3

4

5

6

7

8

9

10

Hyu

nd

ai H

I

Sa

msu

ng

HI

En

ge

vix

DS

ME

Da

lia

n

sh

ipya

rd

Sh

an

gh

ai

Wa

iga

oq

iao

Fe

ne

Sh

ipya

rd IHI

Qin

gd

ao

Be

ha

i

Hu

lls

FPSO hull newbuilds

2003-2011

Delivered

Under construction

Protected by Copyright (c) 1986-2011 ODS-Petrodata Ltd

Market share for hull yards is less fragmented

• Only a few yards are capable of hull construction globally

• COSCO Dalian emerging as a popular choice for owners with its lower cost

structure and improving capabilities

7

0

5

10

15

20

25

30

35

Ke

pp

el O

&M

Se

mb

co

rp M

ari

ne

Dry

do

cks W

orl

d

CO

SC

O D

alia

n

MM

HE

Ya

nta

i Ra

ffle

s

ST

Ma

rin

e

CO

OE

C

Oth

ers

Hu

lls

FPSO hull conversions

2003-2011

Delivered

Under construction

Protected by Copyright (c) 1986-2011 ODS-Petrodata Ltd Sevan 300 hulls counted as conversions

Copyright © 2011 IHS Inc. All Rights Reserved.

FPSO awards staying high in 2011

8

• Both redeployments and new orders contributing to high activity in 2010/2011.

• OGX emerging as a major buyer after ordering four FPSOs in 2011.

• Expect at least 15 awards for 2011.

0

5

10

15

20

25

2003 2004 2005 2006 2007 2008 2009 2010 2011 YTD

Aw

ard

s

FPSO contract awards

8 Petrobras newbuilds

Redeployments

New orders

Protected by Copyright (c) 1986-2011 ODS-Petrodata Ltd Source:ODS-Petrodata

Copyright © 2011 IHS Inc. All Rights Reserved.

FPSOs ordered for many regions since Jan 2010

9

9

Tiro/Sidon

OSX-1

OSX-2

OSX-3

OSX-4

OSX-5

Guara Norte

Kitan

Balnaves

Athena

Huntington

Quad 204

Ardmore

Cendor

TSB

Pagerungan

Berentai

D-1CLOV

Sangos

Goliat

Knarr

• 2010 awards

• 2011 awards

P-66

P-67

P68

P-69

P-70

P-71

P-72

P-73

Guara Pilot

Lula Nordeste

P-58

P-62

Copyright © 2011 IHS Inc. All Rights Reserved.

Growing risks of a global economic slowdown – “Vortex”

10

• IHS uses three oil price scenarios

• “Global Redesign” is our base case scenario where oil prices stay high

• Growing risks of a global recession

• “Vortex arrives earlier” shows the impact of an earlier than expected recession

58

69 75

8997

121

115

5544

5968

75 76 78

77

86

105117

141153 151153 154156 155 157

160162

128134135136138

139130

107

95

117

108109 109 111 113116 115

120

9586 82

7565

55 52 48 45

55

0

20

40

60

80

100

120

140

160

180

Qu

art

erl

y a

ve

rag

e (

US

D/b

arr

el)

Brent oil price scenarios

Historical

Meta (morphosis)

Vortex

Global Redesign

Vortex arrives earlier

Source: IHS CERA and Platts (historical)

Vortex arrives earlier

Copyright © 2011 IHS Inc. All Rights Reserved.

Agenda

1. Overview

2. Lessons from past downturns

3. Capacity

4. Demand

5. Conclusion

11

Copyright © 2011 IHS Inc. All Rights Reserved.

#1 FPSO awards vulnerable in a recession

12

0

5

10

15

20

25

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

FP

SO

s

FPSO contract awards

Protected by Copyright (c) 1986-2011 ODS-Petrodata Ltd Source:ODS-Petrodata

FPSO awards are cyclical

Copyright © 2011 IHS Inc. All Rights Reserved.

#2: Big projects still go ahead in a downturn

13

• Medium to large projects (at least 50,000 b/d) still sanctioned in a recession:

• Longer field life

• Operators of bigger fields tend to have stronger balance sheets.

• Major leasers with strong balance sheets should still grow in a recession.

0

20

40

60

80

100

120

0

5

10

15

20

25

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 YTD

Avera

ge o

il p

rice (

Bre

nt)

Aw

ard

s

FPSO contract awards by oil processing capacity

>100,000 b/d

50-100,000 b/d

<50,000 b/d

Avg Brent oil price

Protected by Copyright (c) 1986-2011 ODS-Petrodata Ltd Source:ODS-Petrodata

Copyright © 2011 IHS Inc. All Rights Reserved.

#2 …while smaller projects are cancelled

14

• Marginal developments at greatest risk in a recession

• Shorter field life

• Usually operated by smaller independents so higher funding risk

Cancelled FPSO contract

Oil

Processing

(b/d) Leaser

Year

cancelled Operator

Contract duration

(years)

East Orovinyare 60,000 Fred Olsen Prod. 2006 BowLeven 5

Bilabri 40,000 BW Offshore 2007 Peak Petroleum 3

Basker-Manta-Gummy 28,000 BW Offshore 2008 Roc Oil 5

Camago Malampaya N/A Nexus FP 2009 BGEC 7

Puffin Southwest 32,500 MODEC 2009 AED Oil 3

Puffin Northeast 40,000 Sea Production 2009 AED Oil 3

Source: ODS-Petrodata

Copyright © 2011 IHS Inc. All Rights Reserved.

#3 FPSOs are sold and not bought

15

• FPSO = a pair of spectacles?

• Difficult to raise cash from selling FPSOs

• FPSOs normally sold below cost

• Main exception was Montara Venture which was sold to the field operator

FPSO Year sold Seller Buyer Sale Price (USD m) Cost (USD m)

Crystal Sea 2007 Seadrill BW Offshore 80 N/A

Nexus 1 2009 Nexus FP OSX 400 700

Montara Venture 2011 Tanker Pacific PTTEP 445 320

DeeP Producer 1 2011 Drydocks World Ramunia 83 335

Jasmine Venture 2011 MODECPetrofac 70

N/A

Cossack Pioneer 2011 NWS JV N/A

Source: ODS-Petrodata

Copyright © 2011 IHS Inc. All Rights Reserved.

Agenda

1. Overview

2. Lessons from past downturns

3. Capacity

4. Demand

5. Conclusion

16

Copyright © 2011 IHS Inc. All Rights Reserved.

Equipment lead times increasing again

17

• Lead times increasing from 2010 lows

• Some turret suppliers eg. SBM Offshore busy (five FPSOs and two complex

turrets)

0

5

10

15

20

25

2006 Jan 2007 Jan 2008 Jan 2009 Jan 2010 Jan 2011 Jan 2011 Sep

Mo

nth

s

Gas Compressor

Gas Turbine

Heat Exchanger

Turret and swivel

Proteced by Copyright (c) 1986-2011 ODS-Petrodata Ltd.

Estimated lead times: Selected FPSO equipment

Source: ODS-Petrodata

Copyright © 2011 IHS Inc. All Rights Reserved.

FPSO costs approaching last peak

18

• Cost model refers to a newbuild FPSO (180,000 b/d)

• Expect costs to increase by 13.6 per cent in 2011

• Salaries increasing by 7-8 per cent in 2011

0

50

100

150

200

250

300

-30%

-20%

-10%

0%

10%

20%

30%

2003 2004 2005 2006 2007 2008 2009 2010 2011f 2012f 2013f 2014f 2015f

No

min

al In

de

x (2

00

3 =

10

0)

Ye

ar o

n Y

ea

r C

ha

ng

e

Cost Model - FPSO

Y-O-Y Change [USD based]

Cost Index (2003=100) [USD based]

Source: ODS-Petrodata, Date: August 15, 2011Protected by Copyright (c) 1986-2011 ODS-Petrodata Ltd.

Copyright © 2011 IHS Inc. All Rights Reserved.

FPSO orders exceeding deliveries

19

• FPSO backlog is a good indicator of capacity bottlenecks

• Units under construction at the highest level in three years even after

excluding the Petrobras newbuilds

0

5

10

15

20

25

30

35

40

45

50

Dec 2

003

Dec 2

004

Dec 2

005

Dec 2

006

Dec 2

007

Dec 2

008

Dec 2

009

Dec 2

010

Sep 2

011

FP

SO

s

FPSOs under construction

Petrobras newbuilds

Conversion

Newbuild

Protected by Copyright (c) 1986-2011 ODS-Petrodata LtdFPSO construction requires 2-4 years

Source:ODS-Petrodata

Copyright © 2011 IHS Inc. All Rights Reserved.

Rig orders leading to higher backlogs and tighter capacity

20

• Backlog includes non-FPS work such as rigbuilding and shipbuilding

• South Korean yards such as Hyundai HI have record backlogs

• “Window of opportunity” to secure capacity is gone?

-

50

100

150

200

250

300

1Q06 3Q06 1Q07 3Q07 1Q08 3Q08 1Q09 3Q09 1Q10 3Q10 1Q11

Ind

ex 1

Q0

6 =

10

0

Shipyard total backlogs in local currencies

Samsung HI DSME Hyundai HI Keppel O&M Sembcorp Marine

Protected by Copyright (c) 1986-2011 ODS-Petrodata Ltd Source: company reports

Copyright © 2011 IHS Inc. All Rights Reserved.

Agenda

1. Overview

2. Lessons from past downturns

3. Capacity

4. Demand

5. Conclusion

21

Copyright © 2011 IHS Inc. All Rights Reserved.

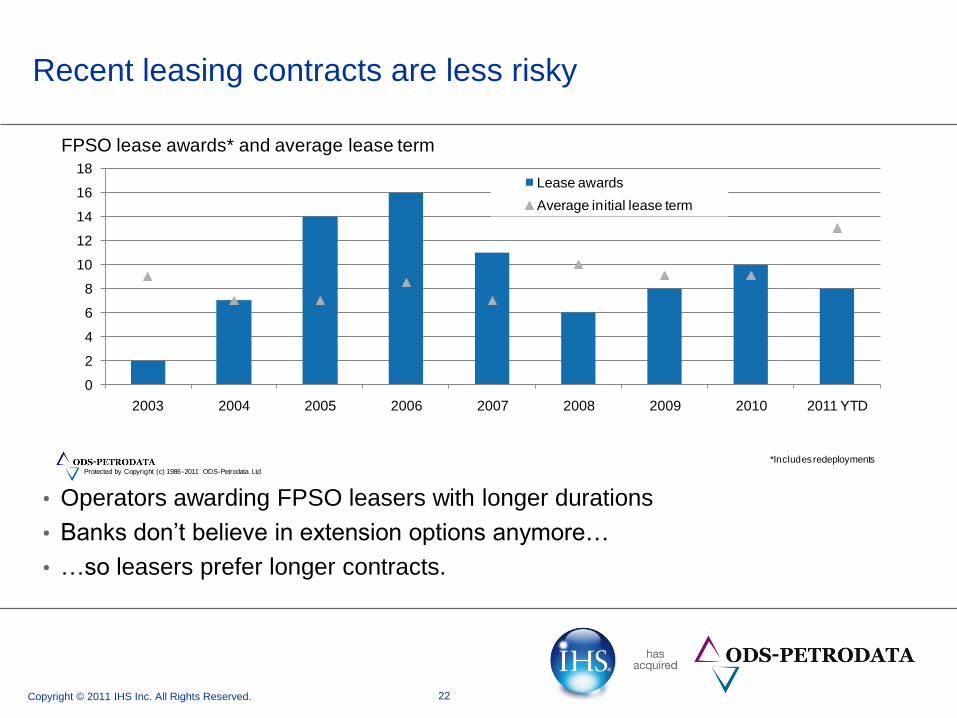

Recent leasing contracts are less risky

22

0

2

4

6

8

10

12

14

16

18

2003 2004 2005 2006 2007 2008 2009 2010 2011 YTD

FPSO lease awards* and average lease term

Lease awards

Average initial lease term

Protected by Copyright (c) 1986-2011 ODS-Petrodata Ltd

*Includes redeployments

• Operators awarding FPSO leasers with longer durations

• Banks don’t believe in extension options anymore…

• …so leasers prefer longer contracts.

Copyright © 2011 IHS Inc. All Rights Reserved.

0

2

4

6

8

10

12

14

16

18

Bra

zil

Asia

-Pa

cif

ic

Afr

ica

Eu

rop

e

Me

d. &

Mid

dle

E

ast

FP

SO

Visible 2012 FPSO demand

Redeployment

Newbuild

Conversion

Protected by Copyright (c) 1986-20101ODS-Petrodata Ltd

We expect 10-15 FPSO awards in 2012

23

Forecast 2012 FPSO awards by operator

Field Region Operator Ownership

Palas Africa BP Own

Gehem Asia-Pacific Chevron Own

Gendalo Asia-Pacific Chevron Own

Chissonga Africa Maersk Oil Lease

OSX FPSO Brazil OGX Lease

OSX FPSO Brazil OGX Lease

Aruana Brazil Petrobras Lease

Transfer of Rights Brazil Petrobras Own

Transfer of Rights Brazil Petrobras Own

Transfer of Rights Brazil Petrobras Own

Franco EWT Brazil Petrobras Lease

Maromba Brazil Petrobras Lease

Bukit Tua Asia-Pacific PETRONAS Lease

Egina Africa Total Own

Tweneboa Africa Tullow Oil Lease

Source: ODS-Petrodata

• Normally expect at least 15 awards

• Less optimistic in 2012

• Recession risk, high costs and tight capacity

Copyright © 2011 IHS Inc. All Rights Reserved.

Expect more redeployment awards in 2012

24

• Several idle FPSOs

• 3-4 FPSOs with no extension options coming off charter annually

• Many FPSOs potentially available in Asia-Pacific and Africa.

0

2

4

6

8

10

12

Idle 2011 2012 2013 2014 2015

FP

SO

Idle/Available FPSOs by region

South America

Europe

Africa

Asia-Pacif ic

Protected by Copyright (c) 1986-2011 ODS-Petrodata LtdSource: ODS-Petrodata

Copyright © 2011 IHS Inc. All Rights Reserved.

More FPSO deliveries if oil prices unchanged

25

We forecast deliveries to peak again by 2014/2015

Asia-Pacific to be the second largest source of demand

Yards in this region should benefit from growing FPSO demand.

0

5

10

15

20

25

30

35

40

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

De

plo

ym

en

ts

Visible/Forecast FPSO Deployments

South America

North America

Med. & Middle East

Europe

Central America

Asia-Pacific

Africa

Forecast

Protected by Copyright (c) 1986-2011 ODS-Petrodata Ltd. Source:ODS-Petrodata

Copyright © 2011 IHS Inc. All Rights Reserved.

There is enough capacity for newbuilds…

26

Newbuild demand to increase by 2015, absorbing spare capacity in Korea.

Buyers have few choices besides the three South Korea yards.

0

1

2

3

4

5

6

7

8

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Hu

ll d

elive

rie

s

Yard capacity* and demand for FPSO newbuild hullsWorld demand (ex Brazil) South Korean yard capacity** World yard capacity (ex Brazil)

Protected by Copyright (c) 1986-2011 ODS-Petrodata Ltd

*South Korean yard capacity falls in 2012-2013 since the yards are busy with rig orders**Includes only Hyundai HI, DSME and Samsung HI

Source: ODS-Petrodata

Copyright © 2011 IHS Inc. All Rights Reserved.

… and conversions

27

Singapore capacity highlighted due to market leadership in conversions.

Excess capacity for conversions.

Capacity to increase due to facilities expansion by incumbents and

growing capabilities of Chinese yards.

0

5

10

15

20

25

30

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Hu

ll d

elive

rie

s

Yard capacity and demand for FPSO conversion hullsWorld demand Singapore yard capacity* World yard capacity

Protected by Copyright (c) 1986-2011 ODS-Petrodata Ltd*Includes only KeppeI O&M and Sembcorp Marine

Source: ODS-Petrodata

Copyright © 2011 IHS Inc. All Rights Reserved.

Conclusion – FPSO outlook for 2012

28

Robust demand( no Vortex). More redeployment awards More leaser consolidation

Some risk of cost overruns as... ...lead times and costs increasing… ...while yards are busier now.

Copyright © 2011 IHS Inc. All Rights Reserved.

Contact us

29

Should you have any questions or need additional information,

please contact us at one of our regional offices or visit us online:

DUBAIHOUSTON

3200 Wilcrest Dr.

Suite 170

Houston, Texas 77042

USA

T +1 832 463 3000

ABERDEEN

2nd Floor

The Exchange No. 1

Market Street

Aberdeen AB11 5PJ

Scotland

T +44 1224 597800

OSLO

Tjuvholmen allé 3, 6th Floor

NO-0252 Oslo

Norway

T +47 21 05 90 00

Crown Plaza 19th Floor

Sheikh Zayed Road

Dubai

United Arab Emirates

T +971 4 3117118

SINGAPORE

04-29 Nordic European Centre

3 International Business Park

Singapore 609927

T +65 6890 1616

www.ods-petrodata.com

Copyright © 2011 IHS Inc. All Rights Reserved.

Oil price scenarios

Global Redesign - Shared interest among major powers to expand trade and

encourage strong economic growth.

Meta – accelerated move towards a lower carbon energy economy. High oil prices

spark reactions that slow down the pace of GHG emissions

Vortex – Volatile economic growth returns. Recession hits Asia, North America

and Europe. Global cooperation suffers

30

![[Unchanged] FPSO: Current status & outlook · Petrobras placed 45 FPSO orders between 2003 and 2014, with the last order placed in Dec 2014 when it awarded Modec a 20-year lease for](https://img.dokumen.tips/doc/110x75/5c4d969b93f3c3245e294604/unchanged-fpso-current-status-outlook-petrobras-placed-45-fpso-orders-between.jpg)