Embed Size (px)

Citation preview

Project Number: 50099-003 Grant Number: August 2018

Lao People’s Democratic Republic: Fourth Greater

Mekong Subregion Corridor Towns Development

Project

Project Administration Manual

ABBREVIATIONS

ADB – Asian Development Bank CTDP – Corridor Towns Development Project DED – detailed engineering design DISC – Design and Implementation Support Consultant DMF – design and monitoring framework DMS – Detailed management survey DONRE – (provincial) department of natural resources and

environment DPWT – (provincial) department pf public works and transport EA – executing agency ECA – environmental compliance audit EGM effective gender mainstreaming EMP – environmental management plan FMA – financial management assessment FY – fiscal year GAP – gender action plan GMS – Greater Mekong Subregion GRM – Grievance Redress Mechanism HH – household IA – implementing agency ICB – international competitive bidding IEE – initial environmental examination MOF – Ministry of Finance MONRE – Ministry of Natural Resources and Environment NCB – national competitive bidding NGO – non-governmental organization O&M – operation and maintenance PAM – project administration manual PCU – project coordination unit PIU – project implementation unit PTRI – Public Works and Transport Research Institute SAO – State Audit Organization SCS – stakeholder communication strategy SOE – Statement of Expenditure SPS – Safeguards Policy Statement SWTP – Small-scale wastewater treatment plants TA – technical assistance TOR – terms of reference UDAA – Urban Development Administration Authority

TABLE OF CONTENTS

I. PROJECT DESCRIPTION 1

A. Summary 1 B. Impact and Outcome 1 C. Outputs 1

II. IMPLEMENTATION PLANS 2 A. Project Readiness Activities 2 B. Overall Project Implementation Plan 2

III. PROJECT MANAGEMENT ARRANGEMENTS 4 A. Project Implementation Organizations: Roles and Responsibilities 4 A. Key Persons Involved in Implementation 7 B. Project Organization Structure 8

IV. COSTS AND FINANCING 9 A. Cost Estimates Preparation and Revisions 9 B. Key Assumptions 9 C. Detailed Cost Estimates by Expenditure Category 10 D. Allocation and Withdrawal of Grant Proceeds 11 E. Detailed Cost Estimates by Financier 12 F. Detailed Cost Estimates by Outputs 13 G. Detailed Cost Estimates by Year 14 H. Contract and Disbursement S-Curve 15 I. Fund Flow Diagram 16

IV. FINANCIAL MANAGEMENT 17 A. Financial Management Assessment 17 B. Disbursement 18 C. Accounting 20 D. Auditing and Public Disclosure 20

VI. PROCUREMENT AND CONSULTING SERVICES 21 A. Advance Contracting and Retroactive Financing 21 B. Procurement of Goods, Works, and Consulting Services 21 C. Procurement Plan 22 D. Consultant's Terms of Reference 22

VII. SAFEGUARDS 22 B. Involuntary Resettlement 24 C. Indigenous Peoples 27

VIII. GENDER AND SOCIAL DIMENSIONS 27 A. Overall Objective and Strategy 27 B. Budget and Implementation Arrangements 27

IX. PERFORMANCE MONITORING, EVALUATION, REPORTING, AND COMMUNICATION 29 A. Project Design and Monitoring Framework 29 B. Monitoring 29 C. Evaluation 30 D. Reporting 30 E. Stakeholder Communication Strategy 32

X. ANTICORRUPTION POLICY 38 XI. ACCOUNTABILITY MECHANISM 38 XII. RECORD OF CHANGES TO THE PROJECT ADMINISTRATION MANUAL 39

ATTTACHMENTS 1. Procurement Plan 2. Terms of Reference of Project Implementation Consultant 3. Financial Management Assessment 4. Outline Quarterly Progress Report 5. Procurement Capacity Assessment TABLES Table 1: Project Implementation Organizations – Lao PDR 4 Table 2: Detailed Cost Estimates by Financier 12 Table 3: Detailed Cost Estimate by Outputs 13 Table 4: Detailed Cost Estimates by Year 14 Table 5: Contract Award 15 Table 6: Disbursement for ADB Grant 15 Table 7: Risk Assessment and Financial Management Action Plan 17

Project Administration Manual Purpose and Process

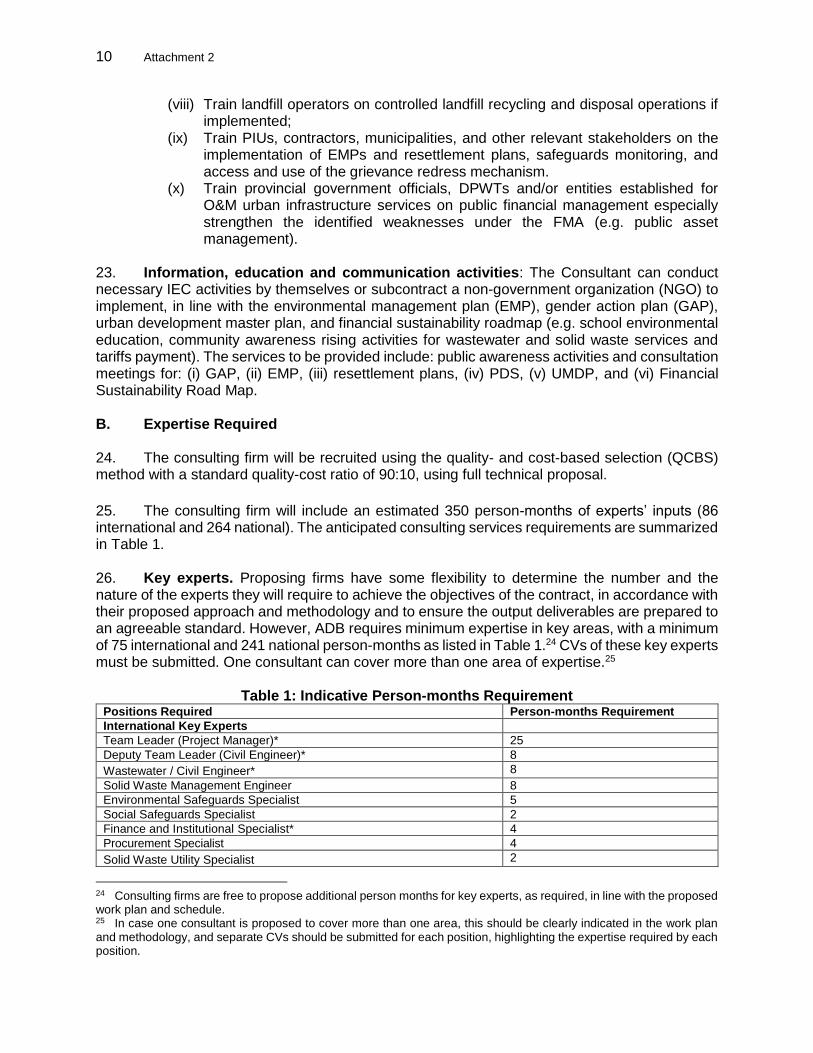

The project administration manual (PAM) describes the essential administrative and management requirements to implement the project on time, within budget, and in accordance with the policies and procedures of the government and Asian Development Bank (ADB). The PAM should include references to all available templates and instructions either through linkages to relevant URLs or directly incorporated in the PAM. The Ministry of Public Works and Transport (MPWT) and Department of Public Works and Transport (DPWT) are wholly responsible for the implementation of ADB-financed projects, as agreed jointly between the recipient and ADB, and in accordance with the policies and procedures of the government and ADB. ADB staff is responsible for supporting implementation including compliance by MPWT and DPWTs of their obligations and responsibilities for project implementation in accordance with ADB’s policies and procedures.

1. At grant negotiations, the recipient and ADB shall agree to the PAM and ensure consistency with the grant agreement. Such agreement shall be reflected in the minutes of the grant negotiations. In the event of any discrepancy or contradiction between the PAM and the grant agreement, the provisions of the grant agreement shall prevail.

2. After ADB Board approval of the project's report and recommendations of the President, changes in implementation arrangements are subject to agreement and approval pursuant to relevant government and ADB administrative procedures (including the Project Administration Instructions) and upon such approval, they will be subsequently incorporated in the PAM.

3.

I. PROJECT DESCRIPTION

A. Summary 1. The project will support the government of the Lao People’s Democratic Republic (Lao PDR) in improving urban environmental services and enhancing regional economic connectivity in the towns of Paksan and Thakhek, which are located along the Greater Mekong Subregion (GMS) Central Corridor. It will finance the: (i) construction of sewerage networks and eight small-scale wastewater treatment plants (SWTP) to improve sanitation; (ii) construction of two controlled landfills and solid waste collection vehicles for municipal waste to improve waste collection and management; (iii) improvement of drainage and riverbank protection; (iv) rehabilitation of the old-town center at Thakhek to promote regional tourism; and (v) preparation of city master plans to promote regional economic connectivity. The project will accelerate urban node development along the GMS Central Corridor in Lao PDR. B. Impact and Outcome 2. Impact: Balanced regional and local development achieved.

3. Outcome: Urban services in Paksan and Thakhek improved.

C. Outputs

4. Output 1: Urban environmental infrastructure improved. The output will include (i) wastewater: four SWTPs with a combined capacity of 900 cubic meters per day (m3/day) for wastewater treatment and 20 kilometer (km) of new sewers in Paksan, and four SWTPs with a combined capacity of 800 m3/day for wastewater treatment and 7 km of new sewers in Thakhek; (ii) drainage: a 23-km and 9-km drainage network in Paksan and Thakhek, respectively; (iii) landfills: 220,000 m3 and 300,000 m3 landfill in Paksan and Thakhek, respectively; (iv) riverbank protection: 1,840 meters (m) and 4,230 m of embankment in Paksan and Thakhek, respectively; and (v) urban renewal and heritage conservation in Thakhek, including an 850-m riverfront promenade, renovation of the old-town square, and restoration and conversion of the post office building into a tourist center to promote sustainable tourism. 5. Output 2: Institutional effectiveness improved. The output will include: (i) training of 25 government staff on urban service delivery, asset management, operation and maintenance (O&M) of urban facilities, and other institutional arrangements for improving urban service delivery; (ii) increasing women’s representation in decision-making and technical positions in the project coordination unit (PCU) and in the project implementation units (PIUs) in Paksan and Thakhek; (iii) preparing urban development strategies and master plans with climate resilience and gender responsive measures for Paksan and Thakhek; and (iv) preparing financial sustainability plans for the Urban Development Administration Authority (UDAA) and Department of Public Works and Transport (DPWT) in Bolikhamxay Province and Khammouan Province, including budgeting, tariff setting for wastewater and solid waste management, and operational effectiveness.

2

II. IMPLEMENTATION PLANS

A. Project Readiness Activities

Table 1: Schedule of Project Readiness Activities

Indicative Activities

2018 2019

Responsible Individual/Unit/

Agency /Government

May Jun Jul Aug Sep Oct Nov Dec Jan

Project implementation arrangement established

MPWT, DPWTs

Advertisement of project management consulting service

ADB, MPWT

ADB Board approval

ADB

Grant signing

ADB, MEF

Government legal opinion provided

MOJ

Grant effectiveness

ADB, MEF

ADB = Asian Development Bank, DPWTs = Provincial Departments of Public Works and Transport, MOF = Ministry of Finance, MOJ = Ministry of Justice, MPWT = Ministry of Public Works and Transport, Sources: Asian Development Bank.

B. Overall Project Implementation Plan

6. The Project is expected to be implemented over a period of five years, beginning in January 2019 with completion by December 2023. The overall project implementation plan is shown in Table 2. The overall project implementation plan will be updated annually by the Ministry of Public Works and Transport (MPWT) and ADB based on actual physical progress.

3

Table 2: Project Implementation Plan Activities 2018 2019 2020 2021 2022 2023 2024

A. Design and Monitoring Framework Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Output 1: Urban environmental infrastructure improved

1.1. Complete BDs for Drainage component

1.2. Complete BDs for SWM component

1.3. Complete BDs for WWT component

1.4. Complete BD for Thakhek Old Town component

1.5. Complete BDs for Riverbank Protection component

1.6. Complete engagement of Drainage contractor(s)

1.7. Complete engagement of SWM contractor(s)

1.8. Complete engagement of WWT contractor(s)

1.9. Complete engagement of Thakhek Old Town contractor(s)

1.10. Complete engagement of Riverbank Protection contractor(s)

1.11. Complete land acquisition and resettlement activities in Thakhek

1.12. Complete land acquisition and resettlement activities in Paksan

1.13. Complete construction of works

Output 2: Institutional effectiveness improved

2.1. Complete procurement of the PIC consulting service

2.2. Begin preparation of urban development strategy and master plans

2.3. Begin preparation of financial sustainability road map

2.4. Finalize urban development strategy and master plans

2.5. Financial sustainability road map developed

2.6. Begin on-the-job training for PCU and PIU staff

2.7. Completion of the PIC consulting service

B. Management Activities

Environment management plan key activities

Resettlement plan key activities

Gender action plan key activities

Communication strategy key activities

Grant reviews and project completion acivities

BD = bidding document; PIC = project implementation consultants; PCU = project coordination unit, PIU = project implementation unit, Q = quarter, SWM = solid waste management, WWT = wastewater treatment Source: Asian Development Bank.

4

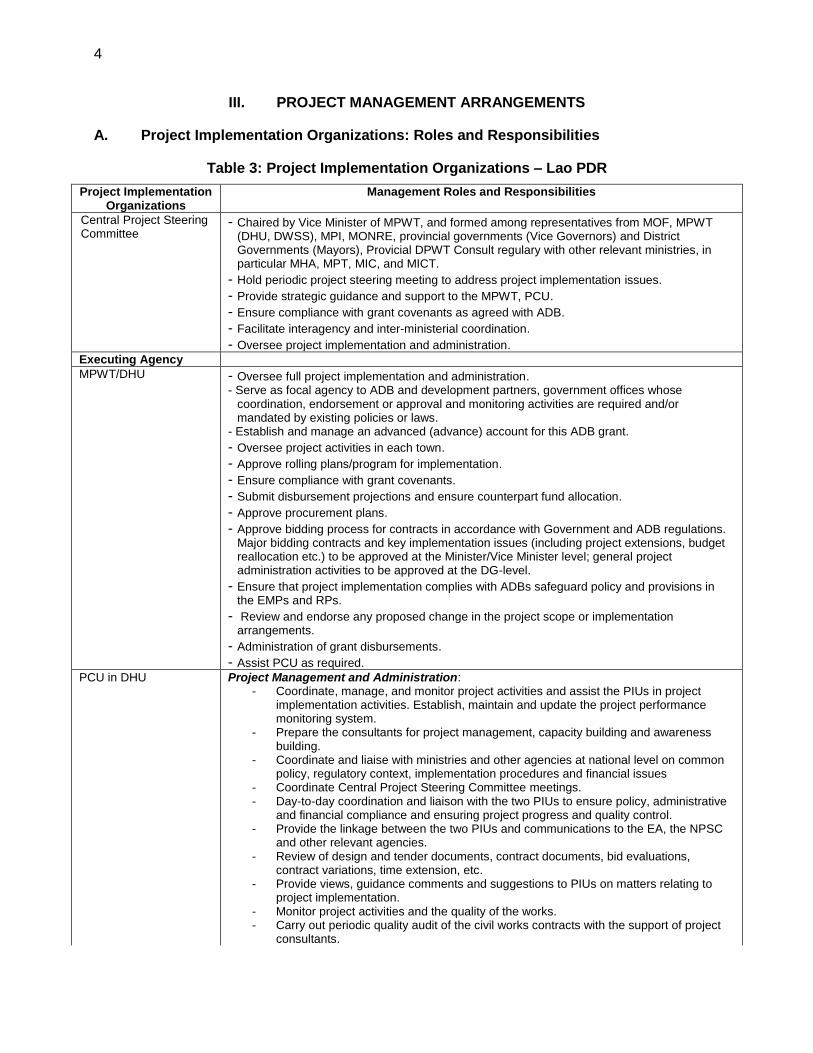

III. PROJECT MANAGEMENT ARRANGEMENTS

A. Project Implementation Organizations: Roles and Responsibilities

Table 3: Project Implementation Organizations – Lao PDR

Project Implementation Organizations

Management Roles and Responsibilities

Central Project Steering Committee

- Chaired by Vice Minister of MPWT, and formed among representatives from MOF, MPWT (DHU, DWSS), MPI, MONRE, provincial governments (Vice Governors) and District Governments (Mayors), Provicial DPWT Consult regulary with other relevant ministries, in particular MHA, MPT, MIC, and MICT.

- Hold periodic project steering meeting to address project implementation issues.

- Provide strategic guidance and support to the MPWT, PCU.

- Ensure compliance with grant covenants as agreed with ADB.

- Facilitate interagency and inter-ministerial coordination.

- Oversee project implementation and administration.

Executing Agency

MPWT/DHU - Oversee full project implementation and administration. - Serve as focal agency to ADB and development partners, government offices whose

coordination, endorsement or approval and monitoring activities are required and/or mandated by existing policies or laws.

- Establish and manage an advanced (advance) account for this ADB grant.

- Oversee project activities in each town.

- Approve rolling plans/program for implementation.

- Ensure compliance with grant covenants.

- Submit disbursement projections and ensure counterpart fund allocation.

- Approve procurement plans.

- Approve bidding process for contracts in accordance with Government and ADB regulations. Major bidding contracts and key implementation issues (including project extensions, budget reallocation etc.) to be approved at the Minister/Vice Minister level; general project administration activities to be approved at the DG-level.

- Ensure that project implementation complies with ADBs safeguard policy and provisions in the EMPs and RPs.

- Review and endorse any proposed change in the project scope or implementation arrangements.

- Administration of grant disbursements.

- Assist PCU as required.

PCU in DHU Project Management and Administration: - Coordinate, manage, and monitor project activities and assist the PIUs in project

implementation activities. Establish, maintain and update the project performance monitoring system.

- Prepare the consultants for project management, capacity building and awareness building.

- Coordinate and liaise with ministries and other agencies at national level on common policy, regulatory context, implementation procedures and financial issues

- Coordinate Central Project Steering Committee meetings. - Day-to-day coordination and liaison with the two PIUs to ensure policy, administrative

and financial compliance and ensuring project progress and quality control. - Provide the linkage between the two PIUs and communications to the EA, the NPSC

and other relevant agencies. - Review of design and tender documents, contract documents, bid evaluations,

contract variations, time extension, etc. - Provide views, guidance comments and suggestions to PIUs on matters relating to

project implementation. - Monitor project activities and the quality of the works. - Carry out periodic quality audit of the civil works contracts with the support of project

consultants.

5

Project Implementation Organizations

Management Roles and Responsibilities

- Provide a quality check of procurement documents and withdrawal applications prior to submission (PCU endorsement required).

- Act as focal point for project agency coordination, and communication with ADB and relevant governmental agencies. Prepare consolidated project reports for submission to MPWT and ADB.

- Organize timely provision of agreed counterpart funds for project activities. - Establish project account. Set up and maintain a strong project financial management

system through Project Accounting Software. - Be responsible for project payments, as required, through the sub- accounts. - Coordinate timely audit of project accounts, and Prepare consolidated project reports

for submission to MPWT and ADB (updated procurement plans (18 month timeframe) in consultation with PIUs and submit to ADB for review and approval, project completion report, reports mandated under the grant agreements and the framework financing agreement to ADB external auditor report, disbursement-related documentation, etc.) and consolidate PIU reports and submit quarterly project progress reports to ADB in agreed format.

- Submit annual contract award and disbursement projections by December of each year.

- Provide support to ADB missions. Procurement

- Review and evaluate all bidding documents and process for further approval. - Send draft bidding documents to ADB for review and approval. - Form and approve a tender evaluation committee for NCB contracts. - Review and approve all bidding and evaluation reports. - Submit evaluation reports to ADB. - Procurement of goods. - Recruitment of consultant teams and manage contracts. - Apply e-procurement when possible. - Recruit and manage consultants under project. - Procurement of project vehicles and equipment of project administration. - Prepare updated procurement plans (18-month timeframe) in consultation with PIUs

and submit to ADB for review and approval. - Provide support and guidance to PIUs during procurement and contract management

process. - Advertise Invitation for Bids of works.

Technical Oversight and Support: - Technical Oversight and Support: Provide technical support and overall guidance to

PIUs, approve subproject proposals against subproject selection criteria, review and approve detailed engineering designs and estimates for NCB, approve any variations during execution of works contracts, and carry out periodic quality audit of the civil works contracts.

Safeguards Compliance: - Safeguards Compliance: Monitor and ensure compliance with ADB’s safeguards

policy and government requirements, obtain statutory clearances, coordinate for obtaining right of way clearances, review monthly PIU monitoring reports and submit consolidated semi-annual safeguards monitoring report to ADB, establish and manage project grievance redress mechanism and ensure project related grievances addressed satisfactorily within timely manner, and provide capacity support to PIUs.

Capacity Building: - Capacity Building Program: Oversee governance improvement and performance,

approve training and capacity building programs conduct training and capacity building programs, oversee public relations, oversee gender action plan and community development.

Implementing Agencies

Implementing Agencies: DPWT of Provinces of Khammouan and Bolikhamxay

- Approve and allocate counterpart budget for the PIUs. - Establish and manage an advanced (advance) account for this ADB grant.

- Assist interdepartmental coordination within the province.

- Communicate with the MPWT/DHU for project implementation progress and activities.

- Provide supports and actions for smooth land acquisition and resettlement activities.

6

Project Implementation Organizations

Management Roles and Responsibilities

Provincial Steering Committees (established in each province)

- Chaired by Vice Governor of the Province, vice-headed by the District’s Mayor (and president of UDAA), and formed among representatives from DPWT, UDAA, DPI, DOF, Provincial Governor and District’s Governor’s offices, and other relevant provincial/districts institutions

- Consult regulary with PIU

- Hold periodic meeting to address project implementation issues in the province

- Provide strategic guidance and support to the DPWT and UDAA

- Ensure compliance with grant covenants as agreed with ADB

- Facilitate interagency coordination and participation of Villages in the activities of the project requiring their commitments

Project Implementation Units (PIU) in Provincial Departments of Public Works and Transport,

Project Management and Administration: - Implement day-to-day project implementation in project towns - Update the RPs and submit to PCU for endorsement prior to submitting to ADB for clearance

prior to implementation. - Update EMPs and validate costs in the project cost table. - Monitor implementation of RPs and submit monitoring reports to the PCU for endorsement

before submitting to EA and ADB. - Ensure environmental protection and mitigation measures (in the EMPs) are incorporated in

detailed designs and contract awards. - Ensure implementation of the EMPs and submit regular monitoring reports through the IAs to

the EAs. - Submit RPs to PCU and ADB for agreement prior to implementation. - Implement GAP, Poverty Reduction and Social Strategy, Stakeholder Participation Plan and

WU capacity building program. - Set up and maintain project financial management system and be responsible for project

payments through sub-project Account. - Liaise with PCU on project implementation. Submit regular (quarterly and annual) project

reports to the PCU. - Open subproject account. Set up and maintain project financial management system and be

responsible for project payments through sub-account. - Submit quarterly reports to PCU in agreed format and as required by PCU. - Maintain subproject and contract level accounting. - Submit claims to PCU. - Coordinate Provincial Project Steering Committee meetings. Procurement of Works: - Prepare detailed designs and procurement documents, bid evaluation and contract awards.

- Advertise Invitation for Bids.

- Manage procurement and conduct all bidding activities including civil works contracts and procurement of vehicles and equipment for SWM.

- Prepare all civil works bidding documents with consultants. - Endorse all civil works bidding documents and send to PCU for review and approval. - Advertise all civil works tenders using e-procurement (if available). - Submit evaluation reports to PCU for civil works contracts. - Sign and manage all civil works civil works contracts (with support from PCU). Technical Support: - Supervise contractors and ensure the quality of works. - Work closely with consultants. - Facilitate collection of data for detailed engineering designs. - Prepare progress report on each contract and include in quarterly reports to PCU and as

required by PCU. Safeguards Compliance: - Implement and monitor safeguards compliance (RPs, EMPs). - Obtain right of way clearances. - Prepare monthly monitoring reports and submit to PCU. Capacity Building: - Implement governance improvement. - Propose training and capacity building programs. - Ensure public outreach. - Implement GAP and community development.

7

Project Implementation Organizations

Management Roles and Responsibilities

Asian Development Bank

- Regular liaison with PCU and EA.

- Review quarterly progress reports submitted by PCU, and follow up on any issues.

- Review auditor reports submitted by PCU.

- Review reports mandated under the grant agreement.

- Conduct annual, mid-term review missions.

- Review draft bidding documents for approval.

- Review bidding evaluation reports for approval.

- Review procurement plans for approval.

- Review recruitment of project implementation consultants.

- Review compliance with safeguards policy.

- Review project performance monitoring and evaluation reports.

- Review progress of capacity building programs. ADB = Asian Development Bank; DG = Director General; DHU = Department of Housing and Urban Planning; DOF = Department of Finance; DWSS = Department of Water Supply and Sanitation; DPWT = Department of Public Works and Transport; EA = executing agency; EMP = environmental management plan; GAP = gender action plan; MIC = Ministry of Industry and Commerce; GAP = gender action plan; MICT = Information Culture and Tourism; MOF = Ministry of Finance; MPI = Ministry of Planning and Investment; MPT = Ministry of Posts and Telecommunications; NSPC = national project steering committee PCU = project coordination unit; PIU = project implementation unit; RP = resettlemt plan; SWM = solid waste management. Sources: Asian Development Bank, Ministry of Public Works and Transport.

B. Key Persons Involved in Implementation

Executing Agency Ministry of Public Works and Transport

Officer's Name : Mr. Khamthavy Thaiphanchanh

Position : Director General – Department of Housing and Urban

Office Address : MPWT, Vientiane

Email address : [email protected]

Telephone No. : +856 21 412283

Asian Development Bank Officer's Name : Mr. Vijay Padmanabhan Position : Director, Urban Development and Water

Division

Office Address : 6 ADB Avenue, Mandaluyong City 1550 Metro Manila, Philippines

Email address : [email protected]

Telephone No. : +63 2 632 6379/5613

Officer's Name : Mr. Sasank Vemuri

Position : Urban Development Specialist

Office Address : 6 ADB Avenue, Mandaluyong City 1550 Metro Manila, Philippines

Email address : [email protected]

Telephone No. : +63 2 632 6153

Project Coordination Unit Officer's Name : Mme. Malychanh Sananikhom, Position : Director of Project Coordination Unit (PCU),

Department of Housing and Urban, MPWT Office Address : MPWT, Vientiane Email address : [email protected], Telephone No. : Tel: +856 21 253114

Project Implementation Unit-Paksan Officer's Name : Position : Email address : Telephone No. :

Project Implementation Unit-Thakhek Officer's Name : Position : Email address : Telephone No. :

8

C. Project Organization Structure

Project Coordination

Unit

Government of the Lao PDR

Ministry of Finance

(Recipient)

ADB

National Level

Provincial/Municipal Level

Central Project Steering

Committee (MPWT, Chair)

Ministry of Public Works and Transport

Department of Housing and Urban

(Executing Agency)

Provincial Department of Public Works and

Transport Project Implementation

Unit-Bolikhamxay Province

Provincial Department of Public Works and

Transport Project Implementation

Unit- Khammouan Province

Provincial Project Steering

Committee (PPSC)

Provincial Project Steering

Committee (PPSC)

Project Implementation

Consultant

9

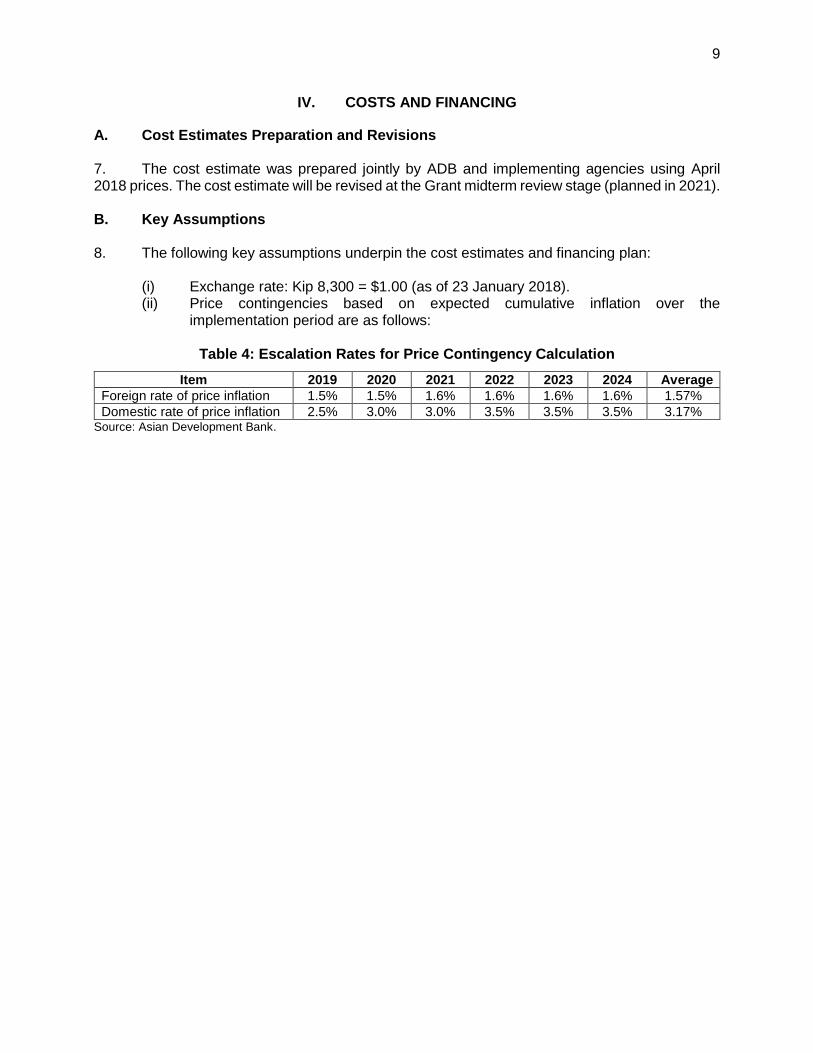

IV. COSTS AND FINANCING

A. Cost Estimates Preparation and Revisions 7. The cost estimate was prepared jointly by ADB and implementing agencies using April 2018 prices. The cost estimate will be revised at the Grant midterm review stage (planned in 2021). B. Key Assumptions 8. The following key assumptions underpin the cost estimates and financing plan:

(i) Exchange rate: Kip 8,300 = $1.00 (as of 23 January 2018). (ii) Price contingencies based on expected cumulative inflation over the

implementation period are as follows:

Table 4: Escalation Rates for Price Contingency Calculation

Item 2019 2020 2021 2022 2023 2024 Average

Foreign rate of price inflation 1.5% 1.5% 1.6% 1.6% 1.6% 1.6% 1.57%

Domestic rate of price inflation 2.5% 3.0% 3.0% 3.5% 3.5% 3.5% 3.17% Source: Asian Development Bank.

10

C. Detailed Cost Estimates by Expenditure Category

Table 5: Detailed Cost Estimates by Expenditure Category

Item

KIP billion $ million % of Total Base Cost Local Foreign Total Local Foreign Total

A. Base Costa,b

1 Civil Works

201.92

134.62

336.54 23.47 15.65 39.12 84.0%

2 Goods and Equipment 8.77 5.85 14.62 1.03 0.68 1.71 3.6%

3 Land Acquisition and Resettlement 10.45 - 10.45 1.24 - 1.24 2.6%

4 Project Implementation Consultant 17.24 11.50 28.74 2.01 1.34 3.34 7.2%

5 Incremental Administration 6.26 4.18 10.44 0.73 0.48 1.21 2.6%

Subtotal (A)

244.65

156.14

400.79 28.47 18.15 46.62 100.0%

B. Contingencies c

1 Physical contingencies 26.48 16.88 43.36 3.08 1.96 5.04 10.8%

2 Price contingencies 14.77 5.80 20.57 1.72 0.67 2.39 5.1%

Subtotal (B) 41.25 22.68 63.93 4.80 2.64 7.44 16.0%

Total (A+B) 285.90 178.82 464.71 33.27 20.79 54.06 116.0% a Includes taxes and duties of $4.13 million. The government will finance value-added taxes and duties through exemption and cash contribution for staff salaries. b In April 2018 prices. c Physical contingency is 11.1%. Price contingency is based on foreign inflation rates of 1.5% in 2018 to 2020, 1.6% from 2021 and onwards; and local inflation rates of 2.0% in 2018, 2.5% in 2019, 3.0% from 2020 to 2021 and 3.5% from 2022 and onwards. Note: Numbers may not sum precisely because of rounding. Source: Asian Development Bank estimates.

11

D. Allocation and Withdrawal of Grant Proceeds

No. Item Amount

Allocated ($)

Percentage and Basis for Withdrawal from Grant Account

1 Works, Good and Consulting Services 40,160,000 100.0% of total amount claimed*

2 Incremental Administration** 1,210,000 100.0% of total amount claimed

3 Unallocated 6,630,000 0.0%

Total 48,000,000 * Exclusive of taxes and duties imposed within the territory of the Recipient. ** Expenses related to support staff and operating costs of the implementing agencies inclusive of office supplies, fuel, and IT equipment. Source: Asian Development Bank estimates.

12

E. Detailed Cost Estimates by Financier

Table 6: Detailed Cost Estimates by Financier ($million)

Item

Grant ADB-ADF Government Total

Amount % Amount %

A. Base Costa,b

1 Civil Works 35.56 90.9% 3.56 9.1% 39.12

2 Goods and Equipment 1.56 90.9% 0.16 9.1% 1.71

3 Land Acquisition and Resettlement - 0.0% 1.24 100.0% 1.24

4 Project Implementation Consultant 3.04 90.9% 0.31 9.1% 3.34

5 Incremental Administration 1.21 100.0% - 0.0% 1.21

Subtotal (A) 41.37 88.7% 5.26 11.3% 46.62

B. Contingenciesc

1 Physical contingencies 4.47 88.7% 0.57 11.3% 5.04

2 Price contingencies 2.16 90.2% 0.24 9.8% 2.39

Subtotal (B) 6.63 89.2% 0.80 10.8% 7.44

Total (A+B) 48.00 88.8% 6.06 11.2% 54.06 a Includes taxes and duties of $4.13 million. The government will finance value-added taxes and duties through exemption and cash

contribution for staff salaries. b In April 2018 prices. c Physical contingency is 11.1%. Price contingency is based on foreign inflation rates of 1.5% in 2018 to 2020, 1.6% from 2021 and

onwards; and local inflation rates of 2.0% in 2018, 2.5% in 2019, 3.0% from 2020 to 2021 and 3.5% from 2022 and onwards. Note: Numbers may not sum precisely because of rounding. Note: Expenses related to support staff and operating costs of the implementing agencies inclusive of office supplies, fuel, IT equipment

and the purchase of six vehicles Source: Asian Development Bank estimates.

13

F. Detailed Cost Estimates by Outputs

Table 7: Detailed Cost Estimates by Outputs ($ million)

No. Item

1a. Paksan Urban Services Improved

1b. Thakhek Urban Services Improved

2. Improved Institutional

Effectiveness

Total Amount % of Cost Category

Amount % of Cost

Category Amount

% of Cost Category

A. Base Costa,b

1 Civil Works 39.12 17.19 44% 21.93 56% - 0%

2 Goods and Equipment 1.71 1.19 69% 0.52 31% - 0%

3 Land Acquisition and Resettlement 1.24 0.41 33% 0.83 67% - 0%

4 Project Implementation Consultant 3.34 - 0% - 0% 3.34 100%

5 Incremental Administration 1.21 - 0% - 0% 1.21 100%

Subtotal (A) 46.62 18.78 40% 23.29 50% 4.56 10%

B. Contingenciesc

1 Physical contingencies 5.04 2.03 40% 2.52 50% 0.49 10%

2 Price contingencies 2.39 0.96 40% 1.20 50% 0.23 10%

Subtotal (B) 7.44 2.99 40% 3.71 50% 0.73 10%

Total (A+B) 54.06 21.8 40% 27.0 50% 5.28 10% a Includes taxes and duties of $4.13 million. The government will finance value-added taxes and duties through exemption and cash contribution for staff salaries. b In April 2018 prices. c Physical contingency is 11.1%. Price contingency is based on foreign inflation rates of 1.5% in 2018 to 2020, 1.6% from 2021 and onwards; and local inflation rates of 2.0% in 2018, 2.5% in 2019, 3.0% from 2020 to 2021 and 3.5% from 2022 and onwards. Source: Asian Development Bank estimates

14

G. Detailed Cost Estimates by Year

Table 8: Detailed Cost Estimates by Year ($ million)

Item 2019 2020 2021 2022 2023 Total

A. Base Costa,b

1 Civil Works - 21.78 16.49 0.85 - 39.12

2 Goods and Equipment - 1.71 - - - 1.71

3 Land Acquisition and Resettlement 1.24 - - - - 1.24

4 Project Implementation Consultant 1.10 0.86 0.78 0.41 0.19 3.34

5 Incremental Administration 0.48 0.18 0.18 0.18 0.18 1.21

Subtotal (A) 2.83 24.54 17.45 1.44 0.37 46.62

B. Contingenciesc

1 Physical contingencies 0.31 2.65 1.89 0.16 0.04 5.04

2 Price contingencies 0.15 1.26 0.90 0.07 0.02 2.39

Subtotal (B) 0.45 3.91 2.78 0.23 0.06 7.44

Total (A+B) 3.28 28.45 20.23 1.67 0.43 54.06 a Includes taxes and duties of $4.13 million. The government will finance value-added taxes and duties through exemption and cash contribution for staff

salaries. b In April 2018 prices. c Physical contingency is 11.1%. Price contingency is based on foreign inflation rates of 1.5% in 2018 to 2020, 1.6% from 2021 and onwards; and local

inflation rates of 2.0% in 2018, 2.5% in 2019, 3.0% from 2020 to 2021 and 3.5% from 2022 and onwards. Source: Asian Development Bank estimates.

15

H. Contract and Disbursement S-curve

Table 9: Contract Award

Q1 Q2 Q3 Q4 Total

2019 3.04 0.31 0.00 7.18 10.53

2020 0.00 0.00 0.00 8.68 8.68

2021 8.23 13.93 0.00 0.00 22.16

2022 0.00 0.00 0.00 0.00 0.00

2023 0.00 0.00 0.00 6.63 6.63

2024 0.00 0.00 0.00 0.00 0.00

TOTAL 48.00

Note: Includes contingencies

Table 10: Disbursement for ADB Grant

Q1 Q2 Q3 Q4 Total

2019 0.25 0.56 0.14 0.14 1.09

2020 0.14 0.47 0.86 0.86 2.33

2021 0.86 1.73 3.86 4.03 10.47

2022 4.03 4.03 4.03 3.70 15.78

2023 3.14 3.14 3.14 2.27 11.70

2024 0.00 0.00 3.31 3.32 6.63

TOTAL 48.00

Note: Includes contingencies

Figure 1: ADB Contract Award and Disbursement

-

10.0

20.0

30.0

40.0

50.0

60.0

Dec/1

8

Ap

r/19

Au

g/1

9

Dec/1

9

Ap

r/20

Au

g/2

0

Dec/2

0

Ap

r/21

Au

g/2

1

Dec/2

1

Ap

r/22

Au

g/2

2

Dec/2

2

Ap

r/23

Au

g/2

3

Dec/2

3

Ap

r/24

Au

g/2

4

Dec/2

4

$ M

illio

n

Award - Plan Disbursement - Plan

16

I. Fund Flow Diagram

Notes: ADB – Asian Development Bank MOF – Ministry of Finance PCU – Project Coordination Unit PIU - Project Implementation Unit

Funds flow Documents flow

PIU-Khammouan

Sub-account

PIU-Bolikhamxay

Sub-account

PCU

Sub-account

MOF

Advance Account

Consultants / Contractors /

Suppliers

ADB

17

V. FINANCIAL MANAGEMENT

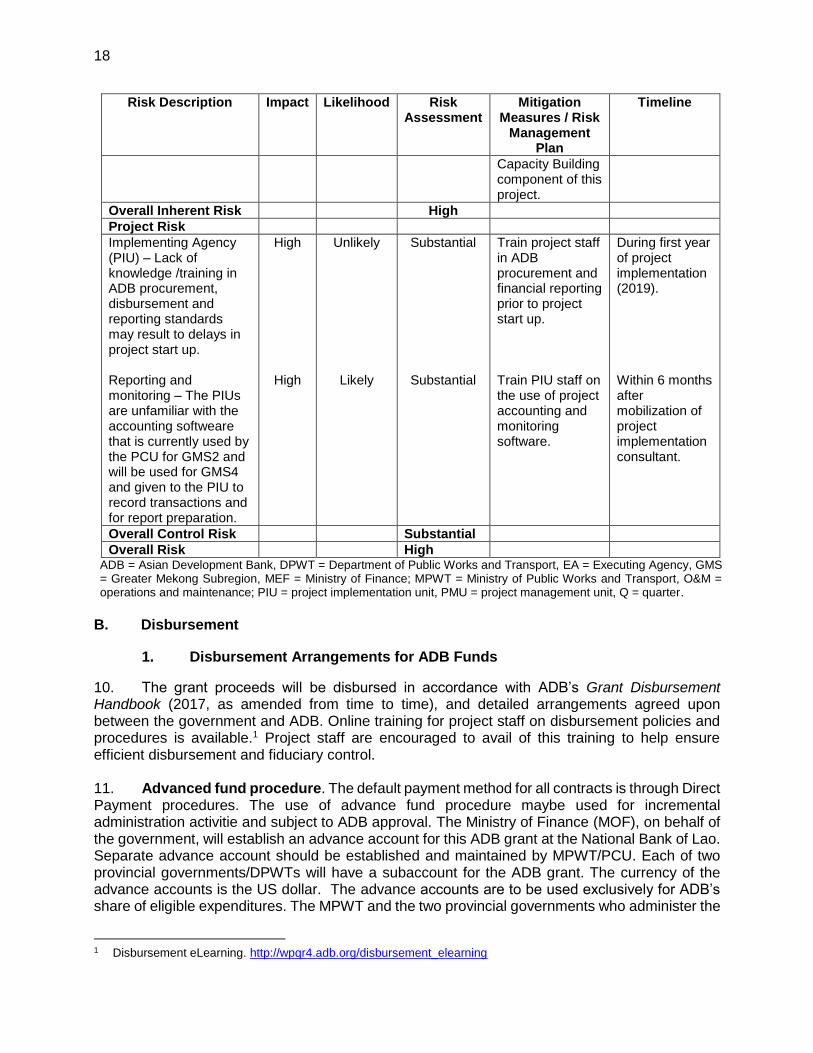

A. Financial Management Assessment 9. The financial management assessment (FMA) was conducted in June to July 2017 in accordance with ADB’s Financial Management Technical Guidance Note (May 2015). Primary data were gathered through the FMA questionnaire from the EAs and IAs, and interviews with the relevant government officials. Secondary data were taken from the FMA reports of previous project. The FMA covered the following aspects: (i) organization and staff capacity, (ii) information management, (iii) funds flow arrangement, (iv) safeguard of assets, (v) strengths and weaknesses, (vi) accounting policies and procedures, (vi) audit, and (vi) project financial reporting system. The summary of risk assessment and financial management action plan is in Table 11.

Table 11: Financial Management, Internal Control and Risk Assessment Risk Description Impact Likelihood Risk

Assessment Mitigation

Measures / Risk Management

Plan

Timeline

Inherent Risk

Country Specific- High dependence on external financing for investment budget with severe shortage of funds for operation and management. Entity Specific- Assets, after procurement / completion of construction, are turned over officially to user government entity and recorded in the Fixed Asset Register of the receiving entity. These assets are not monitored/ inventoried regularly. There is a risk of loss of asset not monitored and maintained properly.

High

High

Likely

Likely

High

High

EA to prepare tariff road map to reduce dependence on national government subsidy for O&M. Update Fixed Asset Register every year during and after project implementation. Train government staff in fixed asset management including linkage to asset preventive maintenance activities.

Within 6 months after mobilization of project implementation consultant. Within 3 months after the completion of construction/ procurement for each grant financed asset.

Entity Specific – Recording of actual revenues and expenditure is weak in the provincial and town levels which may result to lack of accountability.

High Likely High Review compliance of the two provincial and two town governments in the implementation of the Budget Law. Identify deficiencies and include a training program in the

During first year of project implementation (2019).

18

Risk Description Impact Likelihood Risk Assessment

Mitigation Measures / Risk

Management Plan

Timeline

Capacity Building component of this project.

Overall Inherent Risk High

Project Risk

Implementing Agency (PIU) – Lack of knowledge /training in ADB procurement, disbursement and reporting standards may result to delays in project start up. Reporting and monitoring – The PIUs are unfamiliar with the accounting softweare that is currently used by the PCU for GMS2 and will be used for GMS4 and given to the PIU to record transactions and for report preparation.

High

High

Unlikely

Likely

Substantial

Substantial

Train project staff in ADB procurement and financial reporting prior to project start up. Train PIU staff on the use of project accounting and monitoring software.

During first year of project implementation (2019). Within 6 months after mobilization of project implementation consultant.

Overall Control Risk Substantial

Overall Risk High ADB = Asian Development Bank, DPWT = Department of Public Works and Transport, EA = Executing Agency, GMS = Greater Mekong Subregion, MEF = Ministry of Finance; MPWT = Ministry of Public Works and Transport, O&M = operations and maintenance; PIU = project implementation unit, PMU = project management unit, Q = quarter.

B. Disbursement

1. Disbursement Arrangements for ADB Funds

10. The grant proceeds will be disbursed in accordance with ADB’s Grant Disbursement Handbook (2017, as amended from time to time), and detailed arrangements agreed upon between the government and ADB. Online training for project staff on disbursement policies and procedures is available.1 Project staff are encouraged to avail of this training to help ensure efficient disbursement and fiduciary control. 11. Advanced fund procedure. The default payment method for all contracts is through Direct Payment procedures. The use of advance fund procedure maybe used for incremental administration activitie and subject to ADB approval. The Ministry of Finance (MOF), on behalf of the government, will establish an advance account for this ADB grant at the National Bank of Lao. Separate advance account should be established and maintained by MPWT/PCU. Each of two provincial governments/DPWTs will have a subaccount for the ADB grant. The currency of the advance accounts is the US dollar. The advance accounts are to be used exclusively for ADB’s share of eligible expenditures. The MPWT and the two provincial governments who administer the

1 Disbursement eLearning. http://wpqr4.adb.org/disbursement_elearning

19

advance account is accountable and responsible for proper use of advances to the advance account including advances to the sub-accounts. 12. The total outstanding advance to the advance accounts should not exceed the estimate of ADB’s share of expenditures to be paid through the advance accounts for the forthcoming 6 months. The MPWT and the two provincial governments may request for initial and additional advances to the advance accounts based on an Estimate of Expenditure Sheet2 setting out the estimated expenditures to be financed through the accounts for the forthcoming 6 months. Supporting documents should be submitted to ADB or retained by the recipient, the MPWT, and two provincial governments in accordance with ADB’s Grant Disbursement Handbook (2017, as amended from time to time) when liquidating or replenishing the advance accounts. Capable and trained staff must be recruited prior to use the advance fund and SOE procedures.

13. Statement of expenditure procedure (SOE).3 The SOE procedure may be used for reimbursement of eligible expenditures or liquidation of advances to the advance account(s). The ceiling of the SOE procedure is the equivalent of $100,000 per individual payment. Supporting documents and records for the expenditures claimed under the SOE should be maintained and made readily available for review by ADB’s disbursement and review missions, upon ADB’s request for submission of supporting documents on a sampling basis, and for independent audit. Reimbursement and liquidation of individual payments in excess of the SOE ceiling should be supported by full documentation when submitting the withdrawal application to ADB.

14. Before the submission of the first withdrawal application (WA), the recipient should submit to ADB sufficient evidence of the authority of the person(s) who will sign the withdrawal applications on behalf of the government, together with the authenticated specimen signatures of each authorized person. The minimum value per WA is stipulated in the Grant Disbursement Handbook (2017, as amended from time to time). Individual payments below such amount should be paid (i) by the MPWT and subsequently claimed to ADB through reimbursement, or (ii) through the advance fund procedure, unless otherwise accepted by ADB. The recipient should ensure sufficient category and contract balances before requesting disbursements. 15. The MPWT/PCU will be responsible for: (i) preparing disbursement projections; (ii) requesting budgetary allocations for counterpart funds; (iii) collecting supporting documents; and (iv) preparing and sending withdrawal applications to the MOF for onward submission to ADB. The PCU will also be responsible for checking and signing off on all disbursement documents prior to submission to MOF. In case contractual staff salaries are required to be covered by ADB grant proceeds under incremental administration costs, it must be claimed through reimbursements.

2. Disbursement Arrangements for Counterpart Fund 16. The MPWT/PCU will be responsible for the disbursement and liquidation procedures for government funds and will (i) prepare disbursement projections and (ii) request budgetary allocations for counterpart funds. The government will finance value added taxes and duties through exemption and cash contribution for staff salaries. The government will also finance insurance for all cost categories except civil works. Project management staff salaries and

2 Estimate of Expenditure sheet is available in Appendix 8A of ADB’s Grant Disbursement Handbook (2017, as

amended from time to time), 3 SOE forms are available in Appendix 7B and 7D of ADB’s Grant Disbursement Handbook (2017, as amended from

time to time).

20

supplements will also be covered by counterpart funds. Appendixes 3A and 3B of the ADB’s Grant Disbursement Handbook (2017, as amended from time to time) provide further guidance on the proper presentation of local taxes and duties financing in the detailed cost estimate by financier and allocation table in the grant agreement. 17. The MPWT/PCU completes the Government Withdrawal Application Form and attaches a statement of actual expenditure. Supporting expenditure documentation must be maintained by the project team for subsequent review by State Audit Organization (SAO) for audit. The Government Withdrawal Application Form must be signed by the authorized signatories of the MPWT. C. Accounting

18. The MPWT/PCU will maintain, or cause to be maintained, separate books and records by funding source for all expenditures incurred on the project consistent with the Chart of Accounts and Budget Classification of the Government (2007) and Government’s Standard Operating Procedures for Externally-Financed Projects and/or Programs. The MPWT/PCU will prepare project financial statements in accordance with the government’s accounting laws and regulations, which are consistent with international accounting principles and practices. D. Auditing and Public Disclosure

19. The MPWT/PCU will cause the detailed consolidated project financial statements to be audited in accordance with International Standards on Auditing, equivalent national standards adopted by Lao PDR by SAO or an independent auditor acceptable to ADB. The audited project financial statements together with the auditor’s opinion will be presented in the English language to ADB within 6 months from the end of the fiscal year by the executing agency.

20. The audit report for the project financial statements will include a management letter and auditor’s opinions, which cover whether (i) the project financial statements present an accurate and fair view or are presented fairly, in all material respects, in accordance with the applicable financial reporting standards; (ii) the proceeds of the {grant} were used only for the purpose(s) of the project; and (iii) the recipient or executing agency was in compliance with the financial covenants contained in the legal agreements (where applicable).

21. Compliance with financial reporting and auditing requirements will be monitored by review missions and during normal program supervision, and followed up regularly with all concerned, including the external auditor.

22. The government, executing agency, and implementing agency have been made aware of ADB’s approach to delayed submission, and the requirements for satisfactory and acceptable quality of the audited project financial statements.4 ADB reserves the right to require a change in

4 ADB’s approach and procedures regarding delayed submission of audited project financial statements:

(i) When audited project financial statements are not received by the due date, ADB will write to the executing agency advising that (a) the audit documents are overdue; and (b) if they are not received within the next 6 months, requests for new contract awards and disbursement such as new replenishment of advance accounts, processing of new reimbursement, and issuance of new commitment letters will not be processed.

(ii) When audited project financial statements are not received within 6 months after the due date, ADB will withhold processing of requests for new contract awards and disbursement such as new replenishment of advance accounts, processing of new reimbursement, and issuance of new commitment letters. ADB will (a)

21

the auditor (in a manner consistent with the constitution of the recipient), or for additional support to be provided to the auditor, if the audits required are not conducted in a manner satisfactory to ADB, or if the audits are substantially delayed. ADB reserves the right to verify the project’s financial accounts to confirm that the share of ADB’s financing is used in accordance with ADB’s policies and procedures.

23. Public disclosure of the audited project financial statements, including the auditor’s opinion on the project financial statements, will be guided by ADB’s Public Communications Policy 2011.5 After the review, ADB will disclose the audited project financial statements and the opinion of the auditors on the project financial statements no later than 14 days of ADB’s confirmation of their acceptability by posting them on ADB’s website. The management letter, additional auditor’s opinions, and audited entity financial statements will not be disclosed.6

VI. PROCUREMENT AND CONSULTING SERVICES A. Advance Contracting and Retroactive Financing 24. All advance contracting and retroactive financing will be undertaken in conformity with ADB’s Procurement Guidelines (2015, as amended from time to time) and ADB’s Guidelines on the Use of Consultants (2013, as amended from time to time). The issuance of invitations to bid under advance contracting and retroactive financing will be subject to ADB approval. The recipient, MPWT/PCU and two provincial government/DPWTs have been advised that approval of advance contracting and retroactive financing does not commit ADB to finance the project. 25. Advance contracting. The advance contracting packages includes consulting service. The steps to be conducted in advance for recruitment of consultants will include: soliciting and evaluating expressions of interest, shortlisting, and (for firms) preparation of and evaluation of proposals. Contracts for civil works and consultants will only be awarded after the grant becomes effective

B. Procurement of Goods, Works, and Consulting Services

26. All procurement of goods and works will be undertaken in accordance with ADB’s Procurement Guidelines (2015, as amended from time to time). 27. International competitive bidding (ICB) will be used for works contracts estimated to cost $3 million and above. National competitive bidding (NCB) will be used for works contracts estimated to cost over $100,000 equivalent up to below $3 million. For NCB, the first draft English language of the procurement documents (bidding documents, and draft contract) should be submitted for ADB approval regardless of the estimated contract amount. Subsequent procurements are subject to post review. All ICB packages (bidding document, bid evaluation report, and draft contract) are subject to ADB prior review and approval.

inform the executing agency of ADB’s actions; and (b) advise that the grant may be suspended if the audit documents are not received within the next 6 months.

(iii) When audited project financial statements are not received within 12 months after the due date, ADB may suspend the grant.

5 Public Communications Policy: http://www.adb.org/documents/pcp-2011?ref=site/disclosure/publications 6 This type of information would generally fall under public communications policy exceptions to disclosure. ADB. 2011. Public Communications Policy. Paragraph 97(iv) and/or 97(v).

22

28. An 18-month procurement plan indicating threshold and review procedures, goods, works, and consulting service contract packages and national competitive bidding guidelines is in Section C. 29. All consultants and nongovernment organizations (NGOs) will be recruited according to ADB’s Guidelines on the Use of Consultants (2013, as amended from time to time).7 The outline terms of reference (TOR) for project implementation consultants (PIC) are detailed in Section D. The consulting firm will be engaged using the quality- and cost-based selection (QCBS) method with a standard quality–cost ratio of 90:10. C. Procurement Plan 30. The Procurement Plan is included as Attachment 1. D. Consultant’s Terms of Reference 31. Detailed TOR for the Project Implementation Consultants, which will be the sole consulting firm recruited for the project, are included in Attachment 2. E. Procurement Capacity and Risk Assessment 32. The Procurement Capacity Assessment was carried out for the project stakeholders, including the MPWT, DPWTs of Bolikhamxay and Khammouan provinces, and the Paksan and Thakhek UDAA, Municipal Offices, and other provincial departments, identified the infrastructures and facilities that will be included in the Project. A summary of findings from the procurement assessment is included in Attachment 3. The procurement risk is assessed as “high.”

VII. SAFEGUARDS

33. All safeguard documents have been prepared in accordance with ADB’s Safeguards Policy Statement (SPS, 2009). In compliance with ADB’s information disclosure and consultation requirements, the safeguard documents will be posted on ADB’s website. The safeguard categorization for environment and involuntary resettlement is B, and indigenous peoples is C. 34. Relevant safeguard documents include: (i) the initial environmental examination (IEE); (ii) environmental management plans (EMPs), one for each town (Paksan and Thakhek); and (iii) resettlement plans (RPs) for Paksan and Thakhek. Refer to the action plans in the EMPs, and RPs for detailed implementation guidance. 35. Project safeguards grievance redress mechanism (GRM). ADB’s SPS requires that the recipient establish and maintain a GRM to receive and facilitate resolution of affected peoples’ concerns and grievances about the recipient’s social and environmental performance at project level. MPWT shall ensure that: (i) efficient GRMs are in place, functional and relevant focal points are trained to assist the affected persons resolve queries and complaints, if any, in a timely manner; (ii) all complaints are registered, investigated and resolved in a manner consistent with the provisions of GRM reflected in the RP and EMP; iii) complainants/aggrieved persons are kept informed about status of their grievances and remedies available to them; and (iv) adequate staff and resources are available for supervising and monitoring the mechanism.

7 Checklists for actions required to contract consultants by method available in e-Handbook on Project Implementation

at: http://www.adb.org/documents/handbooks/project-implementation/

23

The GRM is described in the RP and IEE. 36. Information disclosure. The draft RPs will be disclosed on ADB website before SRM and the draft IEE before board approval. PCU will disclose on MPWT website. EMPs and RPs will be translated into Lao language and provided to the PIUs to be made available to interested stakeholders on request. PMU shall distribute the Project Information Booklets containing summary of the projects impacts as per final RP, the GRM detailed guidelines with procedures and forms, contacts of the GRC members in local language amongst the Ahs. Project Information Booklets prepared at various stages of the project should include up-to-date information in an understandable language and be widely disseminated to affected persons in a timely manner. The final IEEs and RPs will be updated and disclosed following detailed engineering design (DED). Semi-annual safeguard monitoring reports will be disclosed following review by ADB. 37. Public Consultation. The preliminary project design was informed by consultations carried out with stakeholders and affected persons. Consultation will be ongoing during implementation, as described in the safeguard documents and the Stakeholder Communication Strategy. PCU shall ensure consultations are carried out during update of the safeguards documents following DED. Consultation will include individual and focus group discussions to ensure the affected households are informed about: (a) resettlement impacts, asset valuation/RCS, entitlements and compensation payment modalities with timelines; (b) rehabilitation and income restoration measures suggested for the project affected persons; (c) environmental impacts and mitigation measures; and (d) project GRM. 38. During implementation, there should be regular liaison with affected persons and community, consultation meetings with communities in the project area of influence and with project affected persons, including women and vulnerable groups, to ensure project related information is regularly shared. 39. Prohibited investment activities. Pursuant to ADB’s SPS (2009), ADB funds may not be applied to the activities described on the ADB Prohibited Investment Activities List set forth at Appendix 5 of the SPS (2009). A. Environment

40. The Project is classified as category B for environment according to the ADB’s SPS (2009). The infrastructure components for the towns of Paksan and Thakhek have been screened to check conformity with the safeguard requirements of ADB and the Government of Lao PDR. The identified environmental impacts are largely positive and beneficial on the long-term because of improvements in urban environment, sanitation, and climate resilience of communities. The subprojects are not expected to cause irreversible adverse environmental impacts and any impacts can be mitigated through integration of environmental elements in the engineering design of the subproject components and the implementation of environmental management and monitoring measures during construction and operation.

41. The IEE report with EMP for each town have been prepared based on preliminary engineering designs, survey of the sites, and consultations with the relevant agencies and stakeholders. The EMPs specify the measures to mitigate adverse impacts of the subproject components and identifies the key institutions and indicative costs for implementation. The IEEs also contain a grievance redress mechanism that will facilitate the resolution of complaints during implementation.

24

42. The IEEs and EMPs will be updated and finalized during the DED phase and will form part of the bidding and contract documents. The assimilative capacities of the receiving water bodies of the storm water drainage improvements and decentralized wastewater treatment solutions will be reviewed to ensure that flooding is induced by the project. Local groundwater and human uses surrounding the proposed landfills will be assessed to safeguard communities. Baseline environmental studies that includes assessment of impacts on hydrology, groundwater, surface water, air quality, noise, ecology, and soil quality will be conducted as part of the updated IEEs. Information disclosure and follow-up public consultations will be undertaken with affected stakeholders during detailed design in accordance with ADB’s Public Communications Policy. Concerns raised by stakeholders will be incorporated in the updated IEEs and EMPs. As required by ADB SPS (2009) for existing facilities, an environmental compliance audit (ECA) will be undertaken on the existing dumpsites to determine existence of areas which may cause or is causing environmental risks or impacts and to identify corrective actions to address the environmental issues and ensure that these are avoided or addressed during subproject implementation. The results of the ECA on existing dumpsites and the corrective action plan shall form part of the updated IEEs. The TOR for the conduct of the ECA has been developed.

43. The EA will ensure that each subproject complies with the environmental requirements and standards as stipulated in the Law on Environmental Protection No. 29/NA and other Ministerial Instructions and directives. An Initial Environmental Impact Assessment will be submitted to the Department of Natural Resources (DONRE) for Paksan subproject while a full environmental impact analysis report for the Thakhek subproject will be submitted to Ministry of Natural Resources and Environment (MONRE) to secure the government’s Environmental Compliance Certificate prior to project implementation.

44. A Project Implementation Consultant (PIC) with Environment Specialists (1 international and 1 national) will be commissioned to provide support to MPWT and DPWT. Sufficient budget through the PIC will be allocated for the conduct of baseline studies and ECA, updating of the IEE, preparation of Initial Environmental Impact Assessment and environmental impact analysis for DONRE/MONRE, implementation of the EMP and environmental monitoring plan and post-closure monitoring of existing dumpsites. The PIC will work in close coordination with the Public Works and Transport Research Institute (PTRI) of the MPWT in ensuring the project’s compliance with environmental safeguards identified in the EMP. An Environment Safeguards Officer under the PTRI will be engaged and assigned to the project to sustain the environmental management and monitoring activities of MPWT. Capacity building program on environment safeguards will be undertaken by the PIC through hand-on training for the PTRI, PCUs, PIUs, and other relevant units and agencies.

B. Involuntary Resettlement

45. The safeguard category for Involuntary Resettlement is B. Two resettlement plans (RPs) have been prepared for the sub projects which will trigger land acquisition and resettlement impacts. The RPs are provided for the towns of Paksan and Thakhek.

46. A total of 62,555 m2 will be acquired in Paksan Town and 219 affected households will be affected. Of the 219 affected households (AHs), 61 HHs will be affected by the drainage improvement component, while 107 HHs will be impacted by the riverbank protection component. A further 48 households will be impacted by the waste water and collection systems and 3 HHs by the water treatment plant. The impacts on the livelihoods of AHs are all minor (less than 10% of productive land or structures) and no relocation will be required. The majority of impacts are due to the riverbank protection, but no households are significantly impacted. The cost is estimated

25

to be $499,513 which includes base costs, allowances, and contingencies.

47. A total area of 86,835 m2 will be affected by the subproject components. 27,505 m2 of residential land, agricultural land covering 56,955 m2; government land covering 1,108 m2 and 1,267 m2 of commercial land will be acquired in Thakhek Town. 1000 trees of various species will also be affected. The total number of households affected by land acquisition for the proposed drainage improvements, river bank protection, decentralized wastewater treatment solutions and landfill is 288 AHs. With an average household size of 5 members8 the estimated total number of affected persons is 1,437. Impacts will be minor and/or temporary in nature for 249 households, whereas 39 households are identified as severely affected. The riverbank improvements will have severe impacts on 31 households of which 24 households will be relocated and there are significant impacts with land acquisition affecting over 10% of land for 7 households. The relocation is due to loss of 100% of land parcels and or residential structures. There is also one household that will experience a 20% loss of their commercial land as part of the wastewater network. In addition, there are 7 AHs who will be severely impacted at the solid waste facility. These are waste pickers that are at risk of economic displacement of which 6 of these AHs will require relocation from the proximity of the land fill to a safe distance away but allowing access in order to continue their livelihood activities. There are in total 21 affected people at the solid waste facility. There are a total of 39 severely affected households, (31 HH affected by the riverbank improvements, 7 waste picker HHs and 1 related to the waste water network that will require commercial land acquisition) therefore the number of people that will experience significant impacts is 170. The cost is estimated to be $1,052,932 million, which includes base costs, allowances, external monitoring and contingencies.

48. Project information has been disclosed to affected persons throughout the project preparation and a project information booklet will be updated and distributed during Detailed Measurement Survey (DMS). Resettlement documents have been prepared in consultation with local communities and are in accordance with ADB’s SPS and Lao laws and regulations. The documents have been endorsed, approved and posted on the ADB website. A grievance redress mechanism will help to facilitate resolution of complaints regarding project performance. A rapid appraisal on the severity of impacts shall be conducted in the early stages of DED. The RPs will be updated and disclosed after DED and cleared by ADB prior to contract awards. An independent external monitor will be recruited as early as possible to monitor implementation and in particular, the impacts on severely affected households.

49. The Project will be implemented by MPWT as the executing agency (EA) through the Project Coordination Unit (PCU) in Vientiane and Project Management Unit (PMU) in each town, which will support the EA to undertake overall oversight and management of the Project. It will be supported by implementation consultants to ensure that procedures are followed and that the implementation schedules are kept on track.

50. A PMU has been established at the MPWT to carry out the day to day tasks in the overall implementation of the Project. The PMU will be responsible for the preparation of the RPs with the assistance from the project implementation consultants. The PMU’s task includes the following:

• Allocate a dedicated Social Safeguards officer to oversee the timely implementation of the resettlement plans;

• Submit the RP to MPWT for approval and concurrence by ADB;

8 SES Result conducted by PPTA Consultant and average value is used when HH data is not available

26

• Secure prior approval by MPWT and concurrence from ADB for any variations in approved RP;

• Prepare a data base of the AHs that includes their affected assets gathered during the preparation and updating of the RP;

• Ensure all government requirements are complied with; and

• Monitor and prepare progress reports on RP implementation.

51. The PIC together with the PMU will assist MPWT in preparing and updating the RP through the conduct of the DMS in a participatory and transparent way and consistent with the project resettlement policy. Once approved by DONRE and reviewed and concurred by ADB, the PIC will provide technical advice in the implementation of the approved RP. The PIC will likewise provide capacity-building orientation and skills training, as needed, to concerned personnel of the PMU and other agencies that maybe involved in resettlement implementation.

52. The PIC will provide technical support to the PCU at the EA level to: (i) conduct the rapid appraisal to determine severity of impacts; (ii) ensure that screening and periodic project reviews are carried out; (iii) coordinate the reporting activities of the PCU; and (iv) monitor and coordinate project related procurement to ensure compliance with safeguard requirements; including conducting and documenting consultations and the Grievance Redress Mechanism. The EA/IAs will oversee the implementation of the different subproject components and enforce the implementation of the social safeguard requirements.

53. Together with the PMU, the PIC will supervise civil works activities to ensure that the contractors adhere with the terms of their contract relative to avoiding and/or minimizing resettlement impacts, in addition to ensuring that contractors provide the necessary compensation and/or assistance to the AHs prior to and/or during construction activities. The PIC will assist the PMU in regular monitoring of RP implementation. The PMU is also responsible for responding to complaints from residents or businesses affected by the project works through the Grievance Redress Mechanism.

54. The PCU, in coordination with the DISC is responsible for designing, implementing, and documenting a Grievance and Redress Mechanism for environmental, safety, and social concerns. The mechanism shall be communicated during consultations and made available to affected people. Grievances shall be recorded and addressed in a timely manner.

55. The resettlement plans will be updated following the DED. No economic or physical displacement will occur until compensation and all other entitlements have been paid to the affected hosueholds.

56. A grievance redress mechanism (GRM) has been designed to ensure that the concerns and complaints of the AHs are readily addressed in a timely and satisfactory manner. The AHs will be made fully aware of their rights through verbal and written means during resettlement planning, updating, and implementation. This mechanism will be free to access and have numerous entry points including contractors’ camps and village offices.

57. Temporary resettlement impacts due to the removal and subsequent reconstruction of driveways and road crossing culverts will occur during the construction/improvement of roadside drainage canals located inside the existing road right-of-way (ROW). As part of its contracts, the civil works contractor will carry out the removal and restoration of said driveways and culverts to pre-project conditions.

27

C. Indigenous Peoples

58. The project is classified as category C in accordance with ADB’s Safeguard Policy Statement (2009). ADB’s Indigenous People’s policy requires that under an ADB grant, the recipient will undertake meaningful consultation with affected Indigenous Peoples to ensure their informed participation in (i) designing, implementing, and monitoring measures to avoid adverse impacts on them or, when avoidance is not possible, to minimize, mitigate, and compensate for such effects; and (ii) tailoring project benefits that accrue to them in a culturally appropriate manner. Consultation will be carried out in a manner commensurate with the impacts on affected communities.

VIII. GENDER AND SOCIAL DIMENSIONS

A. Overall Objective and Strategy

59. The project is categorized as Effective Gender Mainstreaming (EGM). In accordance with EGM requirements, the present Gender Action Plan (GAP) has been prepared (Table 12). Identified gender issues include generally lower income of female-headed households (FHHs), comprising 13.7% of HHs in Paksan, 14.1% in Thakhek (weighted average), than male-headed HHs resulting in FHHs paying significantly greater proportion of their income for utilities; limited participation in decision-making and representation in the water and sanitation sector of female staff, limiting more gender responsive urban service delivery; women’s increased responsibilities as caregivers for sick family members, arising from poor environmental sanitation and in household/community clean-up activities during and post flood events; disruptions to school attendance by girls and boys due to flooded and muddy road limited access, arising from inadequate drainage and solid waste services; safety concerns for children and disabled people due to poor road conditions; mobility and income disruption concerns for self-employed traders/vendors (majority female) due to poor road conditions, limited safe and attractive vending locales. In Paksan, self-employment as trader is the most common occupation for women 40% and in Thakhek 37%. In total for both towns 39% of the female income earners are self-employed traders.

60. The project’s gender mainstreaming strategy supports gender equality in the delivery of project benefits and women’s participation in the water and sanitation sector. Key measures include (i) provision of free waste water connections to all households in service areas and to the poor, including FHHs that qualify as poor; (ii) free solid waste collection services for poor HHs, including FHHs that qualify as poor, (iii) female staffing targets in the PCU and PIUs; (iv) targeted capacity development training for female government staff (urban planning and management, project management and M&E, UDAA staff training in O&M, including performance indicators, asset inventory and management); (v) riverbank protection and urban renewal investments include specific design features, which enhance livelihoods of vendors/traders, who are predominantly female; (vi) measures to enhance occupational safety and livelihood security for existing waste pickers (predominantly female); and (vii) collection and monitoring of sex-disaggregated data with gender sensitive indicators will be established in the Project Performance Monitoring System (PPMS).

B. Budget and Implementation Arrangements

61. Cost for free solid waste collection for poor HHs and gender design features for riverbank protection/urban enhancement and landfill management are included in the civil works budget. The GAP budget is $195,000 of which $165,000 is allocated for two Social Development and

28

Gender Specialists (5 PM international and 21 PM national) under the PIC budget. The consultancy also includes additional specialists (capacity development and training) who would support GAP implementation.

62. Ministry of Public Works and Transport, through DHU (EA) and DPWT in Bolikhamxay and Khammouan provinces (IA) will be responsible for GAP implementation, monitoring and reporting. The project will coordinate with LWU to mobilize women’s participation and ensuring project benefits. A qualified Social Development/Gender Officer will be recruited by the PCU. He/she will work full-time the first 2 years and intermittent afterwards to support gender mainstreaming within DHU and across it’s projects. Designated counterpart Social and Gender staff in project implementation units (PIUs), supported by the PIC, will guide overall GAP implementation.

Table 12: Gender Action Plan

Output 1. Urban environmental infrastructure improved Responsible

1a. Wastewater connections to 2,900 HHs, including 320 FHHs and 75 low-income/poor

HHs provided. (2017 baseline: 0). TARGET 1 1b. Free household re-plumbing grants to connect to waste water collection system for poor HHs, including FHHs who qualify as poor. TARGET 2 1c. Free solid waste collection services for poor HHs, including FHHs who qualify as poor. ACTION 1

PCU/PIU UDAA

1d. Riverbank protection and urban renewal investments in Thakhek include specific design features9 to enhance livelihoods of vendors/traders (predominantly female). ACTION 2

1e. Two controlled landfills with capacity volume of at least 530,000 m³ include waste pickers enhanced occupational safety and livelihood security10 (2017 baseline: 37 people, of which 21 are women). TARGET 3

Output 2. Institutional effectiveness improved

2a. 25 government staff (including 10 women) reporting increased knowledge on urban service delivery, O&M of urban facilities and service agreements and other institutional arrangements for improving service delivery (2018 baseline: 0) TARGET 4 2b. Women’s representation in PCU will be 35% (baseline: PCU core staff 50% women) (2013 baseline MPWT: 25% at ministry level); TARGET 5Paksan 2c. Women’s representation in PIUs will be 30% women (baseline: women in technical positions in all provincial departments: 25% in Bolikhamxay, 39% in Khammouan) TARGET 6 2d. Urban development strategy and master plan, with climate resilience and gender responsive measures, developed and approved Paksan and Thakhek (2018 baseline: N/A) ACTION 3 2e. PPMIS include sex-disaggregated data and gender-sensitive monitoring indicators by Q1 2019. TARGET 6

PCU/PIU

FHH= Female-headed households, GAP = Gender Action Plan; LWU= Lao Women Union, M&E = monitoring and evaluation; PCU = Project Coordination Unit; PIU= Project Implementation Unit; PPMIS - Performance Monitoring and Information System; UDAA = Urban Development Administration Authority.

9 Livelihood enhancement design features include street lighting, public toilets for men and women, and platform

constructed along river embankment for vending. 10 Occupational safety and livelihood security measures include formalized employment contracts with Urban

Development Administration authority (UDAA), toilet and washing facilities, covered employee rest area, and safety equipment.

29

IX. PERFORMANCE MONITORING, EVALUATION, REPORTING, AND COMMUNICATION A. Project Design and Monitoring Framework 63. The design and monitoring framework (DMF) is available in the report and recommendation of the President.

B. Monitoring 64. Project performance monitoring. A project performance monitoring system (PPMS) will be established to include the targets, indicators, assumptions, and risks in the DMF. The PPMS will take into account the important monitoring parameters in addition to those included in DMF. The baseline data corresponding to indicators and targets for the DMF targets and PPMS will be collected by the grant consultants. The PIUs with support of consultants will conduct annual surveys and quarterly monitoring of output and outcome indicators, and submit the results in quarterly progress reports to the PMO throughout project implementation. The PMO will consolidate the results and submit quarterly progress reports (QPRs) to ADB. QPRs will include a section on the compliance of contractors with core labor standards in contract preparation and implementation (hiring, construction) periods. These quarterly progress reports will provide information necessary to update ADB's project performance reporting system and include financial information.11 Results of a comprehensive completion survey will be included in the project completion report prepared by the project implementation consultants. Moreover, to help monitor contracts, MPWT with their own existing resources and capacity will input all contracts into their GIS system. 65. Compliance monitoring. The status of compliance with grant covenants, including policy, legal, financial, economic, environmental, and other requirements, will be monitored and reported by the PMO in close coordination with the PIUs, through the quarterly progress reports submitted by the PMO to ADB. All non-compliance issues, if any, will be updated in quarterly progress reports together with remedial and time-bound actions. Each ADB review mission (at least twice a year) will monitor the status of compliance with grant assurances and raise the non-compliance issues with the government and agree on remedial and time-bound actions. 66. Safeguards monitoring. The PCU will submit separate environment and social semi-annual safeguard monitoring reports (EMR and SMR) to ADB, which will be disclosed on ADB’s website. The monitoring reports will be prepared by the PCU safeguards officers, with inputs from the consultants. The status of safeguards implementation, compliance issues, and progress of corrective actions, if any, will be clearly reported to ADB. The status of safeguards implementation will also be discussed at each ADB review mission with necessary issues and agreed actions recorded in aide memoires.