Embed Size (px)

Citation preview

UNITED STATES SECURITIES AND EXCHANGE COMMISSIONWashington, D.C. 20549

Form 10-QÈ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2017

or

‘ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIESEXCHANGE ACT OF 1934

For the transition period from to

Commission File Number: 001-14965

The Goldman Sachs Group, Inc.(Exact name of registrant as specified in its charter)

Delaware 13-4019460(State or other jurisdiction of

incorporation or organization)(I.R.S. Employer

Identification No.)

200 West Street, New York, N.Y. 10282(Address of principal executive offices) (Zip Code)

(212) 902-1000(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of theSecurities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was requiredto file such reports), and (2) has been subject to such filing requirements for the past 90 days. È Yes ‘ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, everyInteractive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter)during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).È Yes ‘ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smallerreporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,”“smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer È Accelerated filer ‘

Non-accelerated filer ‘ (Do not check if a smaller reporting company) Smaller reporting company ‘

Emerging growth company ‘

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition periodfor complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the ExchangeAct. ‘

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).‘ Yes È No

APPLICABLE ONLY TO CORPORATE ISSUERS

As of July 21, 2017, there were 386,875,130 shares of the registrant’s common stock outstanding.

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIESQUARTERLY REPORT ON FORM 10-Q FOR THE QUARTER ENDED JUNE 30, 2017

INDEX

Form 10-Q Item Number Page No.

PART I

FINANCIAL INFORMATION 1Item 1

Financial Statements (Unaudited) 1Condensed Consolidated Statements of Earnings 1Condensed Consolidated Statements of

Comprehensive Income 2Condensed Consolidated Statements of Financial

Condition 3Condensed Consolidated Statements of Changes in

Shareholders’ Equity 4Condensed Consolidated Statements of Cash Flows 5Notes to Condensed Consolidated Financial

Statements 6Note 1. Description of Business 6Note 2. Basis of Presentation 6Note 3. Significant Accounting Policies 7Note 4. Financial Instruments Owned and Financial

Instruments Sold, But Not Yet Purchased 14Note 5. Fair Value Measurements 15Note 6. Cash Instruments 16Note 7. Derivatives and Hedging Activities 22Note 8. Fair Value Option 34Note 9. Loans Receivable 41Note 10. Collateralized Agreements and Financings 44Note 11. Securitization Activities 48Note 12. Variable Interest Entities 50Note 13. Other Assets 54Note 14. Deposits 56Note 15. Short-Term Borrowings 57Note 16. Long-Term Borrowings 57Note 17. Other Liabilities and Accrued Expenses 60Note 18. Commitments, Contingencies and

Guarantees 60Note 19. Shareholders’ Equity 64Note 20. Regulation and Capital Adequacy 67Note 21. Earnings Per Common Share 76Note 22. Transactions with Affiliated Funds 76Note 23. Interest Income and Interest Expense 77Note 24. Income Taxes 77Note 25. Business Segments 78Note 26. Credit Concentrations 80Note 27. Legal Proceedings 81

Page No.

Report of Independent Registered PublicAccounting Firm 89

Statistical Disclosures 90Item 2

Management’s Discussion and Analysis of FinancialCondition and Results of Operations 92

Introduction 92Executive Overview 92Business Environment 93Critical Accounting Policies 94Recent Accounting Developments 96Use of Estimates 96Results of Operations 97Balance Sheet and Funding Sources 108Equity Capital Management and Regulatory Capital 113Regulatory Matters and Developments 118Off-Balance-Sheet Arrangements and Contractual

Obligations 121Risk Management 123

Overview and Structure of Risk Management 123Liquidity Risk Management 127Market Risk Management 135Credit Risk Management 140Operational Risk Management 146Model Risk Management 147

Available Information 148Cautionary Statement Pursuant to the U.S. Private

Securities Litigation Reform Act of 1995 149Item 3

Quantitative and Qualitative Disclosures AboutMarket Risk 150

Item 4

Controls and Procedures 150PART II

OTHER INFORMATION 150Item 1

Legal Proceedings 150Item 2

Unregistered Sales of Equity Securities and Use ofProceeds 150

Item 6

Exhibits 151SIGNATURES 151

Goldman Sachs June 2017 Form 10-Q

PART I. FINANCIAL INFORMATIONItem 1. Financial Statements (Unaudited)

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Condensed Consolidated Statements of Earnings(Unaudited)

Three MonthsEnded June

Six MonthsEnded June

in millions, except per share amounts 2017 2016 2017 2016

Revenues

Investment banking $1,730 $1,787 $ 3,433 $ 3,250Investment management 1,433 1,260 2,830 2,522Commissions and fees 794 777 1,565 1,694Market making 1,915 2,490 4,333 4,352Other principal transactions 1,227 864 2,448 815Total non-interest revenues 7,099 7,178 14,609 12,633

Interest income 3,220 2,530 5,966 4,878Interest expense 2,432 1,776 4,662 3,241Net interest income 788 754 1,304 1,637Net revenues, including net interest income 7,887 7,932 15,913 14,270

Operating expenses

Compensation and benefits 3,233 3,331 6,524 5,993

Brokerage, clearing, exchange and distribution fees 663 625 1,278 1,316Market development 141 112 275 234Communications and technology 224 205 447 402Depreciation and amortization 265 245 522 484Occupancy 190 181 366 364Professional fees 229 231 434 451Other expenses 433 539 1,019 987Total non-compensation expenses 2,145 2,138 4,341 4,238Total operating expenses 5,378 5,469 10,865 10,231

Pre-tax earnings 2,509 2,463 5,048 4,039Provision for taxes 678 641 962 1,082Net earnings 1,831 1,822 4,086 2,957Preferred stock dividends 200 188 293 123Net earnings applicable to common shareholders $1,631 $1,634 $ 3,793 $ 2,834

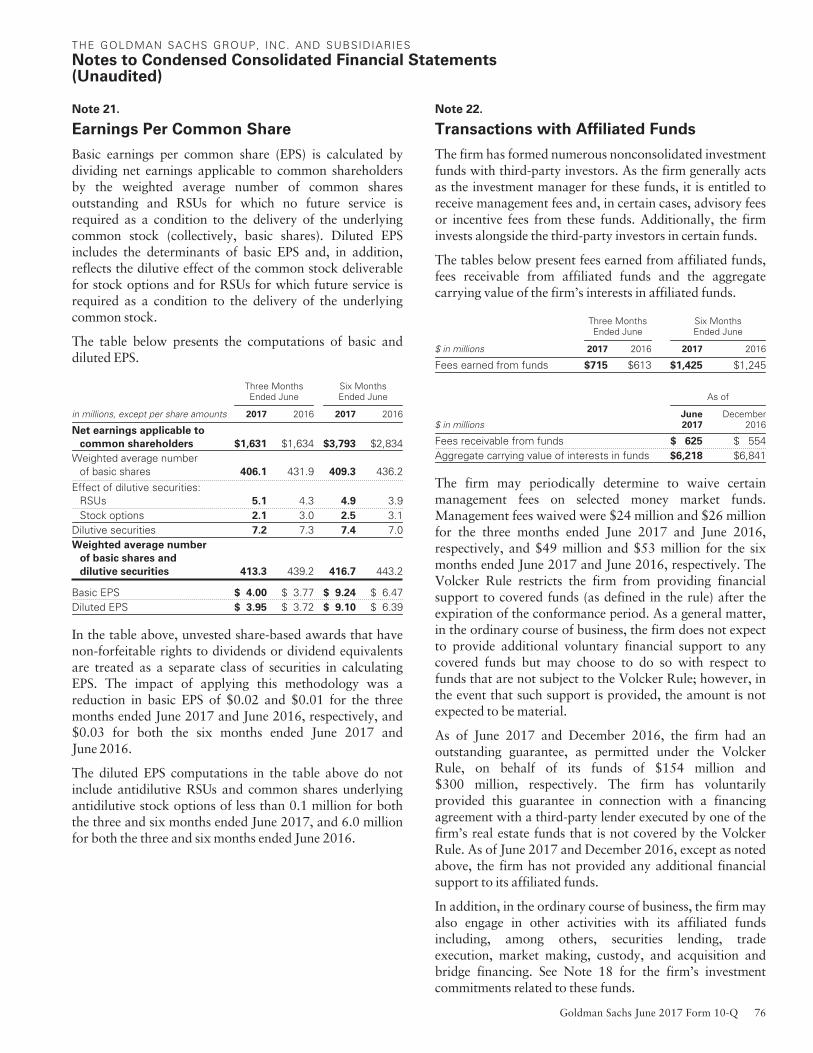

Earnings per common share

Basic $ 4.00 $ 3.77 $ 9.24 $ 6.47Diluted $ 3.95 $ 3.72 $ 9.10 $ 6.39

Dividends declared per common share $ 0.75 $ 0.65 $ 1.40 $ 1.30

Average common shares

Basic 406.1 431.9 409.3 436.2Diluted 413.3 439.2 416.7 443.2

The accompanying notes are an integral part of these condensed consolidated financial statements.

1 Goldman Sachs June 2017 Form 10-Q

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Condensed Consolidated Statements of Comprehensive Income(Unaudited)

Three MonthsEnded June

Six MonthsEnded June

$ in millions 2017 2016 2017 2016

Net earnings $1,831 $1,822 $4,086 $2,957Other comprehensive income/(loss) adjustments, net of tax:

Currency translation 29 (22) 13 (39)Debt valuation adjustment (275) (50) (414) (62)Pension and postretirement liabilities — (1) 1 (37)Available-for-sale securities 1 — 1 —

Other comprehensive loss (245) (73) (399) (138)Comprehensive income $1,586 $1,749 $3,687 $2,819

The accompanying notes are an integral part of these condensed consolidated financial statements.

Goldman Sachs June 2017 Form 10-Q 2

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Condensed Consolidated Statements of Financial Condition(Unaudited)

As of

$ in millions, except per share amountsJune2017

December2016

Assets

Cash and cash equivalents $110,888 $121,711Collateralized agreements:

Securities purchased under agreements to resell and federal funds sold (includes $115,121 and $116,077 at fair value) 115,553 116,925Securities borrowed (includes $70,298 and $82,398 at fair value) 178,301 184,600

Receivables:Brokers, dealers and clearing organizations 32,291 18,044Customers and counterparties (includes $4,895 and $3,266 at fair value) 59,343 47,780Loans receivable 53,952 49,672

Financial instruments owned (at fair value and includes $52,773 and $51,278 pledged as collateral) 327,740 295,952Other assets 28,450 25,481Total assets $906,518 $860,165

Liabilities and shareholders’ equity

Deposits (includes $20,686 and $13,782 at fair value) $125,544 $124,098Collateralized financings:

Securities sold under agreements to repurchase (at fair value) 83,635 71,816Securities loaned (includes $4,753 and $2,647 at fair value) 12,005 7,524Other secured financings (includes $21,967 and $21,073 at fair value) 22,433 21,523

Payables:Brokers, dealers and clearing organizations 10,604 4,386Customers and counterparties 188,958 184,069

Financial instruments sold, but not yet purchased (at fair value) 117,979 117,143Unsecured short-term borrowings (includes $15,945 and $14,792 at fair value) 42,966 39,265Unsecured long-term borrowings (includes $33,760 and $29,410 at fair value) 203,647 189,086Other liabilities and accrued expenses (includes $64 and $621 at fair value) 12,072 14,362Total liabilities 819,843 773,272

Commitments, contingencies and guarantees

Shareholders’ equity

Preferred stock, $0.01 par value; aggregate liquidation preference of $11,203 and $11,203 11,203 11,203Common stock, $0.01 par value; 4,000,000,000 and 4,000,000,000 shares authorized, 881,816,771 and 873,608,100 shares

issued, and 388,213,152 and 392,632,230 shares outstanding 9 9Share-based awards 3,308 3,914Nonvoting common stock, $0.01 par value; 200,000,000 and 200,000,000 shares authorized, no shares issued and outstanding — —Additional paid-in capital 53,187 52,638Retained earnings 92,225 89,039Accumulated other comprehensive loss (1,615) (1,216)Stock held in treasury, at cost, $0.01 par value; 493,603,621 and 480,975,872 shares (71,642) (68,694)Total shareholders’ equity 86,675 86,893Total liabilities and shareholders’ equity $906,518 $860,165

The accompanying notes are an integral part of these condensed consolidated financial statements.

3 Goldman Sachs June 2017 Form 10-Q

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Condensed Consolidated Statements of Changes in Shareholders’ Equity(Unaudited)

$ in millionsSix Months Ended

June 2017Year Ended

December 2016

Preferred stock

Beginning balance $ 11,203 $ 11,200Issued — 1,325Redeemed — (1,322)Ending balance 11,203 11,203Common stock

Beginning balance 9 9Issued — —Ending balance 9 9Share-based awards

Beginning balance, as previously reported 3,914 4,151Cumulative effect of the change in accounting principle related to forfeiture of share-based awards 35 —Beginning balance, adjusted 3,949 4,151Issuance and amortization of share-based awards 1,460 2,143Delivery of common stock underlying share-based awards (1,959) (2,068)Forfeiture of share-based awards (34) (102)Exercise of share-based awards (108) (210)Ending balance 3,308 3,914Additional paid-in capital

Beginning balance 52,638 51,340Delivery of common stock underlying share-based awards 2,056 2,282Cancellation of share-based awards in satisfaction of withholding tax requirements (1,504) (1,121)Preferred stock issuance costs, net — (10)Excess net tax benefit related to share-based awards — 147Cash settlement of share-based awards (3) —Ending balance 53,187 52,638Retained earnings

Beginning balance, as previously reported 89,039 83,386Cumulative effect of the change in accounting principle related to debt valuation adjustment, net of tax — (305)Cumulative effect of the change in accounting principle related to forfeiture of share-based awards, net of tax (24) —Beginning balance, adjusted 89,015 83,081Net earnings 4,086 7,398Dividends and dividend equivalents declared on common stock and share-based awards (583) (1,129)Dividends declared on preferred stock (293) (577)Preferred stock redemption discount — 266Ending balance 92,225 89,039Accumulated other comprehensive loss

Beginning balance, as previously reported (1,216) (718)Cumulative effect of the change in accounting principle related to debt valuation adjustment, net of tax — 305Beginning balance, adjusted (1,216) (413)Other comprehensive loss (399) (803)Ending balance (1,615) (1,216)Stock held in treasury, at cost

Beginning balance (68,694) (62,640)Repurchased (2,966) (6,069)Reissued 28 22Other (10) (7)Ending balance (71,642) (68,694)Total shareholders’ equity $ 86,675 $ 86,893

The accompanying notes are an integral part of these condensed consolidated financial statements.

Goldman Sachs June 2017 Form 10-Q 4

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Condensed Consolidated Statements of Cash Flows(Unaudited)

Six MonthsEnded June

$ in millions 2017 2016

Cash flows from operating activities

Net earnings $ 4,086 $ 2,957Adjustments to reconcile net earnings to net cash provided by/(used for) operating activities:

Depreciation and amortization 522 484Share-based compensation 1,452 1,814Gain related to extinguishment of subordinated borrowings (108) —

Changes in operating assets and liabilities:Receivables and payables (excluding loans receivable), net (14,527) 738Collateralized transactions (excluding other secured financings), net 23,971 (19,350)Financial instruments owned (31,640) 17,274Financial instruments sold, but not yet purchased 472 7,766Other, net 1,919 (4,141)

Net cash provided by/(used for) operating activities (13,853) 7,542Cash flows from investing activities

Purchase of property, leasehold improvements and equipment (1,521) (1,242)Proceeds from sales of property, leasehold improvements and equipment 202 282Net cash acquired in/(used for) business acquisitions (1,086) 15,882Purchase of investments (728) —Proceeds from sales and paydowns of investments 877 818Loans receivable, net (4,686) (2,925)Net cash provided by/(used for) investing activities (6,942) 12,815Cash flows from financing activities

Unsecured short-term borrowings, net (28) 839Other secured financings (short-term), net (881) 1,450Proceeds from issuance of other secured financings (long-term) 4,683 1,995Repayment of other secured financings (long-term), including the current portion (3,151) (3,849)Purchase of APEX, senior guaranteed securities and trust preferred securities (62) (632)Proceeds from issuance of unsecured long-term borrowings 31,654 25,965Repayment of unsecured long-term borrowings, including the current portion (19,343) (22,612)Derivative contracts with a financing element, net 1,002 27Deposits, net 1,446 9,937Common stock repurchased (2,969) (3,294)Settlement of share-based awards in satisfaction of withholding tax requirements (1,507) (902)Dividends and dividend equivalents paid on common stock, preferred stock and share-based awards (876) (860)Proceeds from issuance of preferred stock, net of issuance costs — 655Proceeds from issuance of common stock, including exercise of share-based awards 7 1Cash settlement of share-based awards (3) —Net cash provided by financing activities 9,972 8,720Net increase/(decrease) in cash and cash equivalents (10,823) 29,077Cash and cash equivalents, beginning balance 121,711 93,439Cash and cash equivalents, ending balance $110,888 $122,516

SUPPLEMENTAL DISCLOSURES:

Cash payments for interest, net of capitalized interest, were $6.28 billion and $3.47 billion, and cash payments for income taxes, net of refunds, were $464 millionand $400 million during the six months ended June 2017 and June 2016, respectively.

Cash flows related to common stock repurchased includes common stock repurchased in the prior period for which settlement occurred during the current periodand excludes common stock repurchased during the current period for which settlement occurred in the following period.

Non-cash activities during the six months ended June 2017:

• The firm exchanged $62 million of Trust Preferred Securities and common beneficial interests for $67 million of the firm’s junior subordinated debt.

Non-cash activities during the six months ended June 2016:

• The impact of adoption of ASU No. 2015-02 was a net reduction to both total assets and liabilities of approximately $200 million. See Note 3 for further information.

• The firm sold assets and liabilities of $1.81 billion and $697 million, respectively, that were previously classified as held for sale, in exchange for $1.11 billion offinancial instruments.

• The firm exchanged $505 million of APEX for $666 million of Series E and Series F Preferred Stock. See Note 19 for further information.

The accompanying notes are an integral part of these condensed consolidated financial statements.

5 Goldman Sachs June 2017 Form 10-Q

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements(Unaudited)

Note 1.

Description of Business

The Goldman Sachs Group, Inc. (Group Inc. or parentcompany), a Delaware corporation, together with itsconsolidated subsidiaries (collectively, the firm), is a leadingglobal investment banking, securities and investmentmanagement firm that provides a wide range of financialservices to a substantial and diversified client base thatincludes corporations, financial institutions, governmentsand individuals. Founded in 1869, the firm isheadquartered in New York and maintains offices in allmajor financial centers around the world.

The firm reports its activities in the following four businesssegments:

Investment Banking

The firm provides a broad range of investment bankingservices to a diverse group of corporations, financialinstitutions, investment funds and governments. Servicesinclude strategic advisory assignments with respect tomergers and acquisitions, divestitures, corporate defenseactivities, restructurings, spin-offs and risk management,and debt and equity underwriting of public offerings andprivate placements, including local and cross-bordertransactions and acquisition financing, as well as derivativetransactions directly related to these activities.

Institutional Client Services

The firm facilitates client transactions and makes marketsin fixed income, equity, currency and commodity products,primarily with institutional clients such as corporations,financial institutions, investment funds and governments.The firm also makes markets in and clears clienttransactions on major stock, options and futures exchangesworldwide and provides financing, securities lending andother prime brokerage services to institutional clients.

Investing & Lending

The firm invests in and originates loans to providefinancing to clients. These investments and loans aretypically longer-term in nature. The firm makesinvestments, some of which are consolidated, directly andindirectly through funds that the firm manages, in debtsecurities and loans, public and private equity securities,infrastructure and real estate entities. The firm also makesunsecured loans to individuals through its online platform.

Investment Management

The firm provides investment management services andoffers investment products (primarily through separatelymanaged accounts and commingled vehicles, such asmutual funds and private investment funds) across allmajor asset classes to a diverse set of institutional andindividual clients. The firm also offers wealth advisoryservices, including portfolio management and financialcounseling, and brokerage and other transaction services tohigh-net-worth individuals and families.

Note 2.

Basis of Presentation

These condensed consolidated financial statements areprepared in accordance with accounting principlesgenerally accepted in the United States (U.S. GAAP) andinclude the accounts of Group Inc. and all other entities inwhich the firm has a controlling financial interest.Intercompany transactions and balances have beeneliminated.

These condensed consolidated financial statements areunaudited and should be read in conjunction with theaudited consolidated financial statements included in thefirm’s Annual Report on Form 10-K for the year endedDecember 31, 2016. References to “the 2016 Form 10-K”are to the firm’s Annual Report on Form 10-K for the yearended December 31, 2016. The condensed consolidatedfinancial information as of December 31, 2016 has beenderived from audited consolidated financial statements notincluded herein.

These unaudited condensed consolidated financialstatements reflect all adjustments that are, in the opinion ofmanagement, necessary for a fair statement of the resultsfor the interim periods presented. These adjustments are ofa normal, recurring nature. Interim period operating resultsmay not be indicative of the operating results for a full year.

All references to June 2017, March 2017 and June 2016refer to the firm’s periods ended, or the dates, as the contextrequires, June 30, 2017, March 31, 2017 andJune 30, 2016, respectively. All references toDecember 2016 refer to the date December 31, 2016. Anyreference to a future year refers to a year ending onDecember 31 of that year. Certain reclassifications havebeen made to previously reported amounts to conform tothe current presentation.

Goldman Sachs June 2017 Form 10-Q 6

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements(Unaudited)

Note 3.

Significant Accounting Policies

The firm’s significant accounting policies include when andhow to measure the fair value of assets and liabilities,accounting for goodwill and identifiable intangible assets,and when to consolidate an entity. See Notes 5 through 8for policies on fair value measurements, Note 13 forpolicies on goodwill and identifiable intangible assets, andbelow and Note 12 for policies on consolidationaccounting. All other significant accounting policies areeither described below or included in the followingfootnotes:

Financial Instruments Owned and Financial InstrumentsSold, But Not Yet Purchased Note 4

Fair Value Measurements Note 5

Cash Instruments Note 6

Derivatives and Hedging Activities Note 7

Fair Value Option Note 8

Loans Receivable Note 9

Collateralized Agreements and Financings Note 10

Securitization Activities Note 11

Variable Interest Entities Note 12

Other Assets Note 13

Deposits Note 14

Short-Term Borrowings Note 15

Long-Term Borrowings Note 16

Other Liabilities and Accrued Expenses Note 17

Commitments, Contingencies and Guarantees Note 18

Shareholders’ Equity Note 19

Regulation and Capital Adequacy Note 20

Earnings Per Common Share Note 21

Transactions with Affiliated Funds Note 22

Interest Income and Interest Expense Note 23

Income Taxes Note 24

Business Segments Note 25

Credit Concentrations Note 26

Legal Proceedings Note 27

Consolidation

The firm consolidates entities in which the firm has acontrolling financial interest. The firm determines whetherit has a controlling financial interest in an entity by firstevaluating whether the entity is a voting interest entity or avariable interest entity (VIE).

Voting Interest Entities. Voting interest entities areentities in which (i) the total equity investment at risk issufficient to enable the entity to finance its activitiesindependently and (ii) the equity holders have the power todirect the activities of the entity that most significantlyimpact its economic performance, the obligation to absorbthe losses of the entity and the right to receive the residualreturns of the entity. The usual condition for a controllingfinancial interest in a voting interest entity is ownership of amajority voting interest. If the firm has a controllingmajority voting interest in a voting interest entity, the entityis consolidated.

Variable Interest Entities. A VIE is an entity that lacksone or more of the characteristics of a voting interest entity.The firm has a controlling financial interest in a VIE whenthe firm has a variable interest or interests that provide itwith (i) the power to direct the activities of the VIE thatmost significantly impact the VIE’s economic performanceand (ii) the obligation to absorb losses of the VIE or theright to receive benefits from the VIE that could potentiallybe significant to the VIE. See Note 12 for furtherinformation about VIEs.

Equity-Method Investments. When the firm does nothave a controlling financial interest in an entity but canexert significant influence over the entity’s operating andfinancial policies, the investment is accounted for either(i) under the equity method of accounting or (ii) at fair valueby electing the fair value option available under U.S. GAAP.Significant influence generally exists when the firm owns20% to 50% of the entity’s common stock or in-substancecommon stock.

In general, the firm accounts for investments acquired afterthe fair value option became available, at fair value. Incertain cases, the firm applies the equity method ofaccounting to new investments that are strategic in natureor closely related to the firm’s principal business activities,when the firm has a significant degree of involvement in thecash flows or operations of the investee or when cost-benefit considerations are less significant. See Note 13 forfurther information about equity-method investments.

7 Goldman Sachs June 2017 Form 10-Q

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements(Unaudited)

Investment Funds. The firm has formed numerousinvestment funds with third-party investors. These fundsare typically organized as limited partnerships or limitedliability companies for which the firm acts as generalpartner or manager. Generally, the firm does not hold amajority of the economic interests in these funds. Thesefunds are usually voting interest entities and generally arenot consolidated because third-party investors typicallyhave rights to terminate the funds or to remove the firm asgeneral partner or manager. Investments in these funds aregenerally measured at net asset value (NAV) and areincluded in “Financial instruments owned.” See Notes 6, 18and 22 for further information about investments in funds.

Use of Estimates

Preparation of these condensed consolidated financialstatements requires management to make certain estimatesand assumptions, the most important of which relate to fairvalue measurements, accounting for goodwill andidentifiable intangible assets, discretionary compensationaccruals, the provisions for losses that may arise fromlitigation, regulatory proceedings (including governmentalinvestigations) and tax audits, and the allowance for losseson loans receivable and lending commitments held forinvestment. These estimates and assumptions are based onthe best available information but actual results could bematerially different.

Revenue Recognition

Financial Assets and Financial Liabilities at Fair Value.

Financial instruments owned and Financial instrumentssold, but not yet purchased are recorded at fair value eitherunder the fair value option or in accordance with other U.S.GAAP. In addition, the firm has elected to account forcertain of its other financial assets and financial liabilities atfair value by electing the fair value option. The fair value ofa financial instrument is the amount that would be receivedto sell an asset or paid to transfer a liability in an orderlytransaction between market participants at themeasurement date. Financial assets are marked to bid pricesand financial liabilities are marked to offer prices. Fairvalue measurements do not include transaction costs. Fairvalue gains or losses are generally included in “Marketmaking” for positions in Institutional Client Services and“Other principal transactions” for positions in Investing &Lending. See Notes 5 through 8 for further informationabout fair value measurements.

Investment Banking. Fees from financial advisoryassignments and underwriting revenues are recognized inearnings when the services related to the underlyingtransaction are completed under the terms of theassignment. Expenses associated with such transactions aredeferred until the related revenue is recognized or theassignment is otherwise concluded. Expenses associatedwith financial advisory assignments are recorded asnon-compensation expenses, net of client reimbursements.Underwriting revenues are presented net of relatedexpenses.

Investment Management. The firm earns managementfees and incentive fees for investment management services.Management fees for mutual funds are calculated as apercentage of daily net asset value and are receivedmonthly. Management fees for hedge funds and separatelymanaged accounts are calculated as a percentage ofmonth-end net asset value and are generally receivedquarterly. Management fees for private equity funds arecalculated as a percentage of monthly invested capital orcommitments and are received quarterly, semi-annually orannually, depending on the fund. All management fees arerecognized over the period that the related service isprovided. Incentive fees are calculated as a percentage of afund’s or separately managed account’s return, or excessreturn above a specified benchmark or other performancetarget. Incentive fees are generally based on investmentperformance over a 12-month period or over the life of afund. Fees that are based on performance over a 12-monthperiod are subject to adjustment prior to the end of themeasurement period. For fees that are based on investmentperformance over the life of the fund, future investmentunderperformance may require fees previously distributedto the firm to be returned to the fund. Incentive fees arerecognized only when all material contingencies have beenresolved. Management and incentive fee revenues areincluded in “Investment management” revenues.

The firm makes payments to brokers and advisors relatedto the placement of the firm’s investment funds. Thesepayments are calculated based on either a percentage of themanagement fee or the investment fund’s net asset value.Where the firm is principal to the arrangement, such costsare recorded on a gross basis and included in “Brokerage,clearing, exchange and distribution fees,” and where thefirm is agent to the arrangement, such costs are recorded ona net basis in “Investment management” revenues.

Goldman Sachs June 2017 Form 10-Q 8

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements(Unaudited)

Commissions and Fees. The firm earns “Commissionsand fees” from executing and clearing client transactions onstock, options and futures markets, as well asover-the-counter (OTC) transactions. Commissions andfees are recognized on the day the trade is executed.

Transfers of Financial Assets

Transfers of financial assets are accounted for as sales whenthe firm has relinquished control over the assets transferred.For transfers of financial assets accounted for as sales, anygains or losses are recognized in net revenues. Assets orliabilities that arise from the firm’s continuing involvementwith transferred financial assets are initially recognized atfair value. For transfers of financial assets that are notaccounted for as sales, the assets generally remain in“Financial instruments owned” and the transfer isaccounted for as a collateralized financing, with the relatedinterest expense recognized over the life of the transaction.See Note 10 for further information about transfers offinancial assets accounted for as collateralized financingsand Note 11 for further information about transfers offinancial assets accounted for as sales.

Cash and Cash Equivalents

The firm defines cash equivalents as highly liquid overnightdeposits held in the ordinary course of business. As ofJune 2017 and December 2016, “Cash and cash equivalents”included $15.18 billion and $11.15 billion, respectively, ofcash and due from banks, and $95.71 billion and$110.56 billion, respectively, of interest-bearing depositswith banks. The firm segregates cash for regulatory andother purposes related to client activity. As of June 2017 andDecember 2016, $18.64 billion and $14.65 billion,respectively, of “Cash and cash equivalents” were segregatedfor regulatory and other purposes. See “Recent AccountingDevelopments” for further information.

In addition, the firm segregates securities for regulatory andother purposes related to client activity. See Note 10 forfurther information about segregated securities.

Receivables from and Payables to Brokers, Dealers

and Clearing Organizations

Receivables from and payables to brokers, dealers andclearing organizations are accounted for at cost plusaccrued interest, which generally approximates fair value.While these receivables and payables are carried at amountsthat approximate fair value, they are not accounted for atfair value under the fair value option or at fair value inaccordance with other U.S. GAAP and therefore are notincluded in the firm’s fair value hierarchy in Notes 6through 8. Had these receivables and payables beenincluded in the firm’s fair value hierarchy, substantially allwould have been classified in level 2 as of June 2017 andDecember 2016.

Receivables from Customers and Counterparties

Receivables from customers and counterparties generallyrelate to collateralized transactions. Such receivables areprimarily comprised of customer margin loans, certaintransfers of assets accounted for as secured loans ratherthan purchases at fair value and collateral posted inconnection with certain derivative transactions.Substantially all of these receivables are accounted for atamortized cost net of estimated uncollectible amounts.Certain of the firm’s receivables from customers andcounterparties are accounted for at fair value under the fairvalue option, with changes in fair value generally includedin “Market making” revenues. See Note 8 for furtherinformation about receivables from customers andcounterparties accounted for at fair value under the fairvalue option. In addition, as of June 2017 andDecember 2016, the firm’s receivables from customers andcounterparties included $2.81 billion and $2.60 billion,respectively, of loans held for sale, accounted for at thelower of cost or fair value. See Note 5 for an overview of thefirm’s fair value measurement policies.

As of June 2017 and December 2016, the carrying value ofreceivables not accounted for at fair value generallyapproximated fair value. While these receivables are carriedat amounts that approximate fair value, they are notaccounted for at fair value under the fair value option or atfair value in accordance with other U.S. GAAP andtherefore are not included in the firm’s fair value hierarchyin Notes 6 through 8. Had these receivables been includedin the firm’s fair value hierarchy, substantially all wouldhave been classified in level 2 as of June 2017 andDecember 2016. Interest on receivables from customers andcounterparties is recognized over the life of the transactionand included in “Interest income.”

Payables to Customers and Counterparties

Payables to customers and counterparties primarily consistof customer credit balances related to the firm’s primebrokerage activities. Payables to customers andcounterparties are accounted for at cost plus accruedinterest, which generally approximates fair value. Whilethese payables are carried at amounts that approximate fairvalue, they are not accounted for at fair value under the fairvalue option or at fair value in accordance with other U.S.GAAP and therefore are not included in the firm’s fair valuehierarchy in Notes 6 through 8. Had these payables beenincluded in the firm’s fair value hierarchy, substantially allwould have been classified in level 2 as of June 2017 andDecember 2016. Interest on payables to customers andcounterparties is recognized over the life of the transactionand included in “Interest expense.”

9 Goldman Sachs June 2017 Form 10-Q

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements(Unaudited)

Offsetting Assets and Liabilities

To reduce credit exposures on derivatives and securitiesfinancing transactions, the firm may enter into masternetting agreements or similar arrangements (collectively,netting agreements) with counterparties that permit it tooffset receivables and payables with such counterparties. Anetting agreement is a contract with a counterparty thatpermits net settlement of multiple transactions with thatcounterparty, including upon the exercise of terminationrights by a non-defaulting party. Upon exercise of suchtermination rights, all transactions governed by the nettingagreement are terminated and a net settlement amount iscalculated. In addition, the firm receives and posts cash andsecurities collateral with respect to its derivatives andsecurities financing transactions, subject to the terms of therelated credit support agreements or similar arrangements(collectively, credit support agreements). An enforceablecredit support agreement grants the non-defaulting partyexercising termination rights the right to liquidate thecollateral and apply the proceeds to any amounts owed. Inorder to assess enforceability of the firm’s right of setoffunder netting and credit support agreements, the firmevaluates various factors including applicable bankruptcylaws, local statutes and regulatory provisions in thejurisdiction of the parties to the agreement.

Derivatives are reported on a net-by-counterparty basis(i.e., the net payable or receivable for derivative assets andliabilities for a given counterparty) in the condensedconsolidated statements of financial condition when a legalright of setoff exists under an enforceable nettingagreement. Resale and repurchase agreements andsecurities borrowed and loaned transactions with the sameterm and currency are presented on a net-by-counterpartybasis in the condensed consolidated statements of financialcondition when such transactions meet certain settlementcriteria and are subject to netting agreements.

In the condensed consolidated statements of financialcondition, derivatives are reported net of cash collateralreceived and posted under enforceable credit supportagreements, when transacted under an enforceable nettingagreement. In the condensed consolidated statements offinancial condition, resale and repurchase agreements, andsecurities borrowed and loaned, are not reported net of therelated cash and securities received or posted as collateral.See Note 10 for further information about collateralreceived and pledged, including rights to deliver or repledgecollateral. See Notes 7 and 10 for further information aboutoffsetting.

Share-based Compensation

The cost of employee services received in exchange for ashare-based award is generally measured based on thegrant-date fair value of the award. Share-based awards thatdo not require future service (i.e., vested awards, includingawards granted to retirement-eligible employees) areexpensed immediately. Share-based awards that requirefuture service are amortized over the relevant serviceperiod. Effective January 2017, forfeitures are recordedwhen they occur. Prior to January 2017, expectedforfeitures were estimated and recorded over the vestingperiod. See “Recent Accounting Developments —Improvements to Employee Share-Based PaymentAccounting (ASC 718)” for additional information.

Cash dividend equivalents paid on outstanding restrictedstock units (RSUs) are charged to retained earnings. If RSUsthat require future service are forfeited, the related dividendequivalents originally charged to retained earnings arereclassified to compensation expense in the period in whichforfeiture occurs.

The firm generally issues new shares of common stock upondelivery of share-based awards. In certain cases, primarilyrelated to conflicted employment (as outlined in theapplicable award agreements), the firm may cash settleshare-based compensation awards accounted for as equityinstruments. For these awards, whose terms allow for cashsettlement, additional paid-in capital is adjusted to theextent of the difference between the value of the award atthe time of cash settlement and the grant-date value of theaward.

Foreign Currency Translation

Assets and liabilities denominated in non-U.S. currenciesare translated at rates of exchange prevailing on the date ofthe condensed consolidated statements of financialcondition and revenues and expenses are translated ataverage rates of exchange for the period. Foreign currencyremeasurement gains or losses on transactions innonfunctional currencies are recognized in earnings. Gainsor losses on translation of the financial statements of anon-U.S. operation, when the functional currency is otherthan the U.S. dollar, are included, net of hedges and taxes,in the condensed consolidated statements of comprehensiveincome.

Goldman Sachs June 2017 Form 10-Q 10

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements(Unaudited)

Recent Accounting Developments

Revenue from Contracts with Customers (ASC 606).

In May 2014, the FASB issued ASU No. 2014-09,“Revenue from Contracts with Customers (Topic 606).”This ASU, as amended, provides comprehensive guidanceon the recognition of revenue from customers arising fromthe transfer of goods and services, guidance on accountingfor certain contract costs, and new disclosures.

The ASU is effective for the firm in January 2018 under amodified retrospective approach or retrospectively to allperiods presented. The firm’s implementation effortsinclude identifying revenues and costs within the scope ofthe ASU, reviewing contracts, and analyzing any changes toits existing revenue recognition policies. Based onimplementation work to date, as a result of adopting thisASU, the firm expects that it will, among other things, berequired to recognize certain investment management feesearlier than under the firm’s current revenue recognitionpolicy. The firm will also be required to change the currentpresentation of certain costs from a net presentation withinnet revenues to a gross basis, or vice versa. The firm willadopt this ASU in January 2018 using a modifiedretrospective approach. The firm does not currently expectthat the ASU will have a material impact on its financialcondition, results of operations or cash flows on the date ofadoption.

Measuring the Financial Assets and the Financial

Liabilities of a Consolidated Collateralized Financing

Entity (ASC 810). In August 2014, the FASB issued ASUNo. 2014-13, “Consolidation (Topic 810) — Measuringthe Financial Assets and the Financial Liabilities of aConsolidated Collateralized Financing Entity (CFE).” ThisASU provides an alternative to reflect changes in the fairvalue of the financial assets and the financial liabilities ofthe CFE by measuring either the fair value of the assets orliabilities, whichever is more observable, and provides newdisclosure requirements for those electing this approach.

The firm adopted the ASU in January 2016. Adoption ofthe ASU did not materially affect the firm’s financialcondition, results of operations or cash flows.

Amendments to the Consolidation Analysis

(ASC 810). In February 2015, the FASB issued ASUNo. 2015-02, “Consolidation (Topic 810) — Amendmentsto the Consolidation Analysis.” This ASU eliminates thedeferral of the requirements of ASU No. 2009-17,“Consolidations (Topic 810) — Improvements to FinancialReporting by Enterprises Involved with Variable InterestEntities” for certain interests in investment funds andprovides a scope exception for certain investments inmoney market funds. It also makes several modifications tothe consolidation guidance for VIEs and general partners’investments in limited partnerships, as well asmodifications to the evaluation of whether limitedpartnerships are VIEs or voting interest entities.

The firm adopted the ASU in January 2016, using amodified retrospective approach. The impact of adoptionwas a net reduction to both total assets and total liabilitiesof approximately $200 million, substantially all included in“Financial instruments owned” and in “Other liabilitiesand accrued expenses,” respectively. Adoption of this ASUdid not have an impact on the firm’s results of operations.See Note 12 for further information about the adoption.

Simplifying the Accounting for Measurement-Period

Adjustments (ASC 805). In September 2015, the FASBissued ASU No. 2015-16, “Business Combinations(Topic 805) — Simplifying the Accounting forMeasurement-Period Adjustments.” This ASU eliminatesthe requirement for an acquirer in a business combinationto account for measurement-period adjustmentsretrospectively.

The firm adopted the ASU in January 2016. Adoption ofthe ASU did not materially affect the firm’s financialcondition, results of operations or cash flows.

Recognition and Measurement of Financial Assets

and Financial Liabilities (ASC 825). In January 2016, theFASB issued ASU No. 2016-01, “Financial Instruments(Topic 825) — Recognition and Measurement of FinancialAssets and Financial Liabilities.” This ASU amends certainaspects of recognition, measurement, presentation anddisclosure of financial instruments. It includes arequirement to present separately in other comprehensiveincome changes in fair value attributable to a firm’s owncredit spreads (debt valuation adjustment or DVA), net oftax, on financial liabilities for which the fair value optionwas elected.

11 Goldman Sachs June 2017 Form 10-Q

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements(Unaudited)

The ASU is effective for the firm in January 2018. Earlyadoption is permitted under a modified retrospectiveapproach for the requirements related to DVA. InJanuary 2016, the firm early adopted this ASU for therequirements related to DVA and reclassified thecumulative DVA, a gain of $305 million (net of tax), from“Retained earnings” to “Accumulated other comprehensiveloss.” The firm does not expect the adoption of theremaining provisions of the ASU to have a material impacton its financial condition, results of operations or cashflows.

Leases (ASC 842). In February 2016, the FASB issued ASUNo. 2016-02, “Leases (Topic 842).” This ASU requiresthat, for leases longer than one year, a lessee recognize inthe statements of financial condition a right-of-use asset,representing the right to use the underlying asset for thelease term, and a lease liability, representing the liability tomake lease payments. It also requires that for finance leases,a lessee recognize interest expense on the lease liability,separately from the amortization of the right-of-use asset inthe statements of earnings, while for operating leases, suchamounts should be recognized as a combined expense. Inaddition, this ASU requires expanded disclosures about thenature and terms of lease agreements.

The ASU is effective for the firm in January 2019 under amodified retrospective approach. Early adoption ispermitted. The firm’s implementation efforts includereviewing existing leases and service contracts, which mayinclude embedded leases. The firm expects a gross up on itsconsolidated statements of financial condition uponrecognition of the right-of-use assets and lease liabilities anddoes not expect the amount of the gross up to have amaterial impact on its financial condition.

Improvements to Employee Share-Based Payment

Accounting (ASC 718). In March 2016, the FASB issuedASU No. 2016-09, “Compensation — Stock Compensation(Topic 718) — Improvements to Employee Share-BasedPayment Accounting.” This ASU includes a requirementthat the tax effect related to the settlement of share-basedawards be recorded in income tax benefit or expense in thestatements of earnings rather than directly to additionalpaid-in capital. This change has no impact on totalshareholders’ equity and is required to be adoptedprospectively. The ASU also allows for forfeitures to berecorded when they occur rather than estimated over thevesting period. This change is required to be applied on amodified retrospective basis.

The firm adopted the ASU in January 2017 and the impactof the RSU deliveries and option exercises in the first half of2017 was a reduction to the provision for taxes of$485 million, which was recognized in the condensedconsolidated statements of earnings. The impact will varyin future periods depending upon, among other things, thenumber of RSUs delivered and their change in value sincegrant. Prior to the adoption of this ASU, this amount wouldhave been recorded directly to additional paid-in capital.The firm also elected to account for forfeitures as theyoccur, rather than to estimate forfeitures over the vestingperiod, and the cumulative effect of this election uponadoption was an increase of $35 million to “Share-basedawards” and a decrease of $24 million (net of tax of$11 million) to “Retained earnings” within the condensedconsolidated statements of changes in shareholders’ equity.

In addition, the ASU modifies the classification of certainshare-based payment activities within the statements ofcash flows. As a result, the firm reclassified, on aretrospective basis, a cash outflow of $902 million relatedto the settlement of share-based awards in satisfaction ofwithholding tax requirements from operating activities tofinancing activities and a cash inflow of $78 million ofexcess tax benefits related to share-based awards fromfinancing activities to operating activities within thecondensed consolidated statements of cash flows for the sixmonths ended June 2016.

Measurement of Credit Losses on Financial

Instruments (ASC 326). In June 2016, the FASB issuedASU No. 2016-13, “Financial Instruments — Credit Losses(Topic 326) — Measurement of Credit Losses on FinancialInstruments.” This ASU amends several aspects of themeasurement of credit losses on financial instruments,including replacing the existing incurred credit loss modeland other models with the Current Expected Credit Losses(CECL) model and amending certain aspects of accountingfor purchased financial assets with deterioration in creditquality since origination.

Under CECL, the allowance for losses for financial assetsthat are measured at amortized cost reflects management’sestimate of credit losses over the remaining expected life ofthe financial assets. Expected credit losses for newlyrecognized financial assets, as well as changes to expectedcredit losses during the period, would be recognized inearnings. For certain purchased financial assets withdeterioration in credit quality since origination, an initialallowance would be recorded for expected credit losses andrecognized as an increase to the purchase price rather thanas an expense. Expected credit losses, including losses onoff-balance-sheet exposures such as lending commitments,will be measured based on historical experience, currentconditions and forecasts that affect the collectability of thereported amount.

Goldman Sachs June 2017 Form 10-Q 12

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements(Unaudited)

The ASU is effective for the firm in January 2020 under amodified retrospective approach. Early adoption ispermitted in January 2019. Adoption of the ASU will resultin earlier recognition of credit losses and an increase in therecorded allowance for certain purchased loans withdeterioration in credit quality since origination with acorresponding increase to their gross carrying value. Theimpact of adoption of this ASU on the firm’s financialcondition, results of operations and cash flows will dependon, among other things, the economic environment and thetype of financial assets held by the firm on the date ofadoption.

Classification of Certain Cash Receipts and Cash

Payments (ASC 230). In August 2016, the FASB issuedASU No. 2016-15, “Statement of Cash Flows(Topic 230) — Classification of Certain Cash Receipts andCash Payments.” This ASU provides guidance on thedisclosure and classification of certain items within thestatements of cash flows.

The ASU is effective for the firm in January 2018 under aretrospective approach. Early adoption is permitted. Sincethe ASU only impacts classification in the statements ofcash flows, adoption will not affect the firm’s cash and cashequivalents.

Restricted Cash (ASC 230). In November 2016, the FASBissued ASU No. 2016-18, “Statement of Cash Flows(Topic 230) — Restricted Cash.” This ASU requires thatcash segregated for regulatory and other purposes beincluded in cash and cash equivalents disclosed in thestatements of cash flows and is required to be appliedretrospectively.

The firm early adopted the ASU in December 2016 andreclassified cash segregated for regulatory and otherpurposes into “Cash and cash equivalents” disclosed in theconsolidated statements of cash flows. The impact ofadoption was an increase of $889 million for the sixmonths ended June 2016 to “Net cash used for operatingactivities.” In addition, in December 2016, to be consistentwith the presentation of segregated cash in the consolidatedstatements of cash flows under the ASU, the firmreclassified amounts previously included in “Cash andsecurities segregated for regulatory and other purposes”into “Cash and cash equivalents,” “Securities purchasedunder agreements to resell and federal funds sold,”“Securities borrowed” and “Financial instruments owned”in the consolidated statements of financial condition.Previously reported amounts in the condensed consolidatedstatements of cash flows and notes to the condensedconsolidated financial statements have been conformed tothe current presentation.

Clarifying the Definition of a Business (ASC 805). InJanuary 2017, the FASB issued ASU No. 2017-01,“Business Combinations (Topic 805) — Clarifying theDefinition of a Business.” The ASU amends the definitionof a business and provides a threshold which must beconsidered to determine whether a transaction is anacquisition (or disposal) of an asset or a business.

The ASU is effective for the firm in January 2018 under aprospective approach. Early adoption is permitted. Theimpact of this ASU will depend on the nature of the firm’sactivities after adoption, although the firm expects thatfewer transactions will be treated as acquisitions (ordisposals) of businesses.

Simplifying the Test for Goodwill Impairment

(ASC 350). In January 2017, the FASB issued ASUNo. 2017-04, “Intangibles — Goodwill and Other(Topic 350) — Simplifying the Test for GoodwillImpairment.” The ASU simplifies the quantitative goodwillimpairment test by eliminating the second step of the test.Under this ASU, impairment will be measured bycomparing the estimated fair value of the reporting unitwith its carrying value.

The ASU is effective for the firm in 2020. Early adoption ispermitted. The firm does not expect adoption will have amaterial impact to its goodwill impairment test.

Clarifying the Scope of Asset Derecognition Guidance

and Accounting for Partial Sales of Nonfinancial

Assets (ASC 610-20). In February 2017, the FASB issuedASU No. 2017-05, “Other Income — Gains and Lossesfrom the Derecognition of Nonfinancial Assets (Subtopic610-20) — Clarifying the Scope of Asset DerecognitionGuidance and Accounting for Partial Sales of NonfinancialAssets.” The ASU clarifies the scope of guidance applicableto sales of nonfinancial assets and also provides guidanceon accounting for partial sales of such assets.

The ASU is effective for the firm in January 2018 under aretrospective or modified retrospective approach. The firmwill adopt this ASU using a modified retrospectiveapproach and does not expect adoption of the ASU willhave a material impact on its financial condition, results ofoperations or cash flows.

13 Goldman Sachs June 2017 Form 10-Q

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements(Unaudited)

Note 4.

Financial Instruments Owned and FinancialInstruments Sold, But Not Yet Purchased

Financial instruments owned and financial instrumentssold, but not yet purchased are accounted for at fair valueeither under the fair value option or in accordance withother U.S. GAAP. See Note 8 for further information aboutother financial assets and financial liabilities accounted forat fair value primarily under the fair value option.

The table below presents the firm’s financial instrumentsowned and financial instruments sold, but not yet purchased.

$ in millions

FinancialInstruments

Owned

FinancialInstruments

Sold, ButNot Yet

Purchased

As of June 2017

Money market instruments $ 1,649 $ —

U.S. government and agency obligations 74,238 17,746

Non-U.S. government and agency obligations 35,011 26,754

Loans and securities backed by:Commercial real estate 4,364 5

Residential real estate 9,816 1

Corporate loans and debt securities 33,735 8,654

State and municipal obligations 783 —

Other debt obligations 1,592 1

Equity securities 109,002 25,065

Commodities 3,225 —

Investments in funds at NAV 5,910 —

Subtotal 279,325 78,226

Derivatives 48,415 39,753

Total $327,740 $117,979

As of December 2016Money market instruments $ 1,319 $ —U.S. government and agency obligations 57,657 16,627Non-U.S. government and agency obligations 29,381 20,502Loans and securities backed by:

Commercial real estate 3,842 —Residential real estate 12,195 3

Corporate loans and debt securities 28,659 6,570State and municipal obligations 1,059 —Other debt obligations 1,358 1Equity securities 94,692 25,941Commodities 5,653 —Investments in funds at NAV 6,465 —Subtotal 242,280 69,644Derivatives 53,672 47,499Total $295,952 $117,143

In the table above:

‰ Money market instruments includes commercial paper,certificates of deposit and time deposits, substantially allof which have a maturity of less than one year.

‰ Equity securities includes public and private equities,exchange-traded funds and convertible debentures.

‰ Financial instruments owned included $330 million and$89 million of debt securities accounted for asavailable-for-sale as of June 2017 and December 2016,respectively. As of both June 2017 and December 2016,these securities were primarily comprised of U.S.government and agency obligations and other debtobligations. As of June 2017, substantially all of thesesecurities had maturities of greater than five years (half ofwhich had maturities of greater than ten years). As ofDecember 2016, these securities primarily had maturitiesof greater than ten years. The gross unrealized gains/(losses) included in “Accumulated other comprehensiveloss” related to available-for-sale securities were notmaterial as of both June 2017 and December 2016.

Gains and Losses from Market Making and Other

Principal Transactions

The table below presents “Market making” revenues bymajor product type, as well as “Other principaltransactions” revenues.

Three MonthsEnded June

Six MonthsEnded June

$ in millions 2017 2016 2017 2016

Interest rates $ 2,625 $ (907) $ 3,989 $ 270Credit 382 630 926 1,248Currencies (2,422) 1,618 (2,740) 710Equities 1,293 861 1,871 1,552Commodities 37 288 287 572Market making 1,915 2,490 4,333 4,352Other principal transactions 1,227 864 2,448 815Total $ 3,142 $3,354 $ 6,781 $5,167

In the table above:

‰ Gains/(losses) include both realized and unrealized gainsand losses, and are primarily related to the firm’s financialinstruments owned and financial instruments sold, butnot yet purchased, including both derivative andnon-derivative financial instruments.

‰ Gains/(losses) exclude related interest income and interestexpense. See Note 23 for further information aboutinterest income and interest expense.

‰ Gains/(losses) on other principal transactions areincluded in the firm’s Investing & Lending segment. SeeNote 25 for net revenues, including net interest income,by product type for Investing & Lending, as well as theamount of net interest income included in Investing &Lending.

Goldman Sachs June 2017 Form 10-Q 14

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements(Unaudited)

‰ Gains/(losses) are not representative of the manner inwhich the firm manages its business activities becausemany of the firm’s market-making and client facilitationstrategies utilize financial instruments across variousproduct types. Accordingly, gains or losses in one producttype frequently offset gains or losses in other producttypes. For example, most of the firm’s longer-termderivatives across product types are sensitive to changesin interest rates and may be economically hedged withinterest rate swaps. Similarly, a significant portion of thefirm’s cash instruments and derivatives across producttypes has exposure to foreign currencies and may beeconomically hedged with foreign currency contracts.

Note 5.

Fair Value Measurements

The fair value of a financial instrument is the amount thatwould be received to sell an asset or paid to transfer aliability in an orderly transaction between marketparticipants at the measurement date. Financial assets aremarked to bid prices and financial liabilities are marked tooffer prices. Fair value measurements do not includetransaction costs. The firm measures certain financial assetsand financial liabilities as a portfolio (i.e., based on its netexposure to market and/or credit risks).

The best evidence of fair value is a quoted price in an activemarket. If quoted prices in active markets are not available,fair value is determined by reference to prices for similarinstruments, quoted prices or recent transactions in lessactive markets, or internally developed models thatprimarily use market-based or independently sourcedinputs including, but not limited to, interest rates,volatilities, equity or debt prices, foreign exchange rates,commodity prices, credit spreads and funding spreads (i.e.,the spread or difference between the interest rate at which aborrower could finance a given financial instrument relativeto a benchmark interest rate).

U.S. GAAP has a three-level hierarchy for disclosure of fairvalue measurements. This hierarchy prioritizes inputs to thevaluation techniques used to measure fair value, giving thehighest priority to level 1 inputs and the lowest priority tolevel 3 inputs. A financial instrument’s level in thishierarchy is based on the lowest level of input that issignificant to its fair value measurement. In evaluating thesignificance of a valuation input, the firm considers, amongother factors, a portfolio’s net risk exposure to that input.The fair value hierarchy is as follows:

Level 1. Inputs are unadjusted quoted prices in activemarkets to which the firm had access at the measurementdate for identical, unrestricted assets or liabilities.

Level 2. Inputs to valuation techniques are observable,either directly or indirectly.

Level 3. One or more inputs to valuation techniques aresignificant and unobservable.

The fair values for substantially all of the firm’s financialassets and financial liabilities are based on observable pricesand inputs and are classified in levels 1 and 2 of the fairvalue hierarchy. Certain level 2 and level 3 financial assetsand financial liabilities may require appropriate valuationadjustments that a market participant would require toarrive at fair value for factors such as counterparty and thefirm’s credit quality, funding risk, transfer restrictions,liquidity and bid/offer spreads. Valuation adjustments aregenerally based on market evidence.

See Notes 6 through 8 for further information about fairvalue measurements of cash instruments, derivatives andother financial assets and financial liabilities accounted for atfair value primarily under the fair value option, respectively.

The table below presents financial assets and financialliabilities accounted for at fair value under the fair valueoption or in accordance with other U.S. GAAP.

As of

$ in millionsJune2017

March2017

December2016

Total level 1 financial assets $163,555 $151,691 $135,401Total level 2 financial assets 407,480 406,332 419,585Total level 3 financial assets 20,847 23,288 23,280Investments in funds at NAV 5,910 6,183 6,465Counterparty and cash collateral netting (79,738) (78,540) (87,038)Total financial assets at fair value $518,054 $508,954 $497,693

Total assets $906,518 $894,069 $860,165Total level 3 financial assets divided by:

Total assets 2.3% 2.6% 2.7%Total financial assets at fair value 4.0% 4.6% 4.7%

Total level 1 financial liabilities $ 68,534 $ 67,732 $ 62,504Total level 2 financial liabilities 248,257 246,087 232,027Total level 3 financial liabilities 19,595 21,067 21,448Counterparty and cash collateral netting (37,597) (37,802) (44,695)Total financial liabilities at fair value $298,789 $297,084 $271,284

Total level 3 financial liabilities divided bytotal financial liabilities at fair value 6.6% 7.1% 7.9%

In the table above:

‰ Counterparty netting among positions classified in thesame level is included in that level.

‰ Counterparty and cash collateral netting represents theimpact on derivatives of netting across levels of the fairvalue hierarchy.

‰ Total assets included $878 billion, $867 billion and$835 billion as of June 2017, March 2017 andDecember 2016, respectively, that is carried at fair valueor at amounts that generally approximate fair value.

15 Goldman Sachs June 2017 Form 10-Q

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements(Unaudited)

The table below presents a summary of level 3 financialassets.

As of

$ in millionsJune2017

March2017

December2016

Cash instruments $16,196 $18,324 $18,035Derivatives 4,650 4,950 5,190Other financial assets 1 14 55Total $20,847 $23,288 $23,280

Level 3 financial assets as of June 2017 decreased comparedwith March 2017 and December 2016, primarily reflectinga decrease in level 3 cash instruments. See Notes 6 through8 for further information about level 3 financial assets(including information about unrealized gains and lossesrelated to level 3 financial assets and financial liabilities,and transfers in and out of level 3).

Note 6.

Cash Instruments

Cash instruments include U.S. government and agencyobligations, non-U.S. government and agency obligations,mortgage-backed loans and securities, corporate loans anddebt securities, equity securities, investments in funds atNAV, and other non-derivative financial instrumentsowned and financial instruments sold, but not yetpurchased. See below for the types of cash instrumentsincluded in each level of the fair value hierarchy and thevaluation techniques and significant inputs used todetermine their fair values. See Note 5 for an overview ofthe firm’s fair value measurement policies.

Level 1 Cash Instruments

Level 1 cash instruments include certain money marketinstruments, U.S. government obligations, most non-U.S.government obligations, certain government agencyobligations, certain corporate debt securities and activelytraded listed equities. These instruments are valued usingquoted prices for identical unrestricted instruments inactive markets.

The firm defines active markets for equity instrumentsbased on the average daily trading volume both in absoluteterms and relative to the market capitalization for theinstrument. The firm defines active markets for debtinstruments based on both the average daily trading volumeand the number of days with trading activity.

Level 2 Cash Instruments

Level 2 cash instruments include most money marketinstruments, most government agency obligations, certainnon-U.S. government obligations, most mortgage-backedloans and securities, most corporate loans and debtsecurities, most state and municipal obligations, most otherdebt obligations, restricted or less liquid listed equities,commodities and certain lending commitments.

Valuations of level 2 cash instruments can be verified toquoted prices, recent trading activity for identical or similarinstruments, broker or dealer quotations or alternativepricing sources with reasonable levels of price transparency.Consideration is given to the nature of the quotations (e.g.,indicative or firm) and the relationship of recent marketactivity to the prices provided from alternative pricingsources.

Valuation adjustments are typically made to level 2 cashinstruments (i) if the cash instrument is subject to transferrestrictions and/or (ii) for other premiums and liquiditydiscounts that a market participant would require to arriveat fair value. Valuation adjustments are generally based onmarket evidence.

Level 3 Cash Instruments

Level 3 cash instruments have one or more significantvaluation inputs that are not observable. Absent evidence tothe contrary, level 3 cash instruments are initially valued attransaction price, which is considered to be the best initialestimate of fair value. Subsequently, the firm uses othermethodologies to determine fair value, which vary based onthe type of instrument. Valuation inputs and assumptionsare changed when corroborated by substantive observableevidence, including values realized on sales of financialassets.

Valuation Techniques and Significant Inputs of

Level 3 Cash Instruments

Valuation techniques of level 3 cash instruments vary byinstrument, but are generally based on discounted cash flowtechniques. The valuation techniques and the nature ofsignificant inputs used to determine the fair values of eachtype of level 3 cash instrument are described below:

Loans and Securities Backed by Commercial Real

Estate. Loans and securities backed by commercial realestate are directly or indirectly collateralized by a singlecommercial real estate property or a portfolio of properties,and may include tranches of varying levels ofsubordination. Significant inputs are generally determinedbased on relative value analyses and include:

Goldman Sachs June 2017 Form 10-Q 16

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements(Unaudited)

‰ Transaction prices in both the underlying collateral andinstruments with the same or similar underlyingcollateral;

‰ Market yields implied by transactions of similar or relatedassets and/or current levels and changes in market indicessuch as the CMBX (an index that tracks the performanceof commercial mortgage bonds);

‰ A measure of expected future cash flows in a defaultscenario (recovery rates) implied by the value of theunderlying collateral, which is mainly driven by currentperformance of the underlying collateral, capitalizationrates and multiples. Recovery rates are expressed as apercentage of notional or face value of the instrument andreflect the benefit of credit enhancements on certaininstruments; and

‰ Timing of expected future cash flows (duration) which, incertain cases, may incorporate the impact of otherunobservable inputs (e.g., prepayment speeds).

Loans and Securities Backed by Residential Real

Estate. Loans and securities backed by residential realestate are directly or indirectly collateralized by portfoliosof residential real estate and may include tranches ofvarying levels of subordination. Significant inputs aregenerally determined based on relative value analyses,which incorporate comparisons to instruments with similarcollateral and risk profiles. Significant inputs include:

‰ Transaction prices in both the underlying collateral andinstruments with the same or similar underlyingcollateral;

‰ Market yields implied by transactions of similar or relatedassets;

‰ Cumulative loss expectations, driven by default rates,home price projections, residential property liquidationtimelines, related costs and subsequent recoveries; and

‰ Duration, driven by underlying loan prepayment speedsand residential property liquidation timelines.

Corporate Loans and Debt Securities. Corporate loansand debt securities includes bank loans and bridge loansand corporate debt securities. Significant inputs aregenerally determined based on relative value analyses,which incorporate comparisons both to prices of creditdefault swaps that reference the same or similar underlyinginstrument or entity and to other debt instruments for thesame issuer for which observable prices or brokerquotations are available. Significant inputs include:

‰ Market yields implied by transactions of similar or relatedassets and/or current levels and trends of market indicessuch as CDX and LCDX (indices that track theperformance of corporate credit and loans, respectively);

‰ Current performance and recovery assumptions and,where the firm uses credit default swaps to value therelated cash instrument, the cost of borrowing theunderlying reference obligation; and

‰ Duration.

Equity Securities. Equity securities includes private equitysecurities and convertible debentures. Recent third-partycompleted or pending transactions (e.g., merger proposals,tender offers, debt restructurings) are considered to be thebest evidence for any change in fair value. When these arenot available, the following valuation methodologies areused, as appropriate:

‰ Industry multiples (primarily EBITDA multiples) andpublic comparables;

‰ Transactions in similar instruments;

‰ Discounted cash flow techniques; and

‰ Third-party appraisals.

The firm also considers changes in the outlook for therelevant industry and financial performance of the issuer ascompared to projected performance. Significant inputsinclude:

‰ Market and transaction multiples;

‰ Discount rates and capitalization rates; and

‰ For equity securities with debt-like features, market yieldsimplied by transactions of similar or related assets,current performance and recovery assumptions, andduration.

Other Cash Instruments. Other cash instruments consistsof non-U.S. government and agency obligations, state andmunicipal obligations, and other debt obligations.Significant inputs are generally determined based onrelative value analyses, which incorporate comparisonsboth to prices of credit default swaps that reference thesame or similar underlying instrument or entity and toother debt instruments for the same issuer for whichobservable prices or broker quotations are available.Significant inputs include:

‰ Market yields implied by transactions of similar or relatedassets and/or current levels and trends of market indices;

‰ Current performance and recovery assumptions and,where the firm uses credit default swaps to value therelated cash instrument, the cost of borrowing theunderlying reference obligation; and

‰ Duration.

17 Goldman Sachs June 2017 Form 10-Q

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements(Unaudited)

Fair Value of Cash Instruments by Level

The tables below present cash instrument assets andliabilities at fair value by level within the fair valuehierarchy.

As of June 2017

$ in millions Level 1 Level 2 Level 3 Total

Assets

Money market instruments $ 266 $ 1,383 $ — $ 1,649

U.S. government and agencyobligations 44,431 29,807 — 74,238

Non-U.S. government and agencyobligations 27,787 7,222 2 35,011

Loans and securities backed by:Commercial real estate — 2,964 1,400 4,364

Residential real estate — 9,009 807 9,816

Corporate loans and debtsecurities 702 29,388 3,645 33,735

State and municipal obligations — 684 99 783

Other debt obligations — 1,182 410 1,592

Equity securities 90,264 8,905 9,833 109,002

Commodities — 3,225 — 3,225

Subtotal $163,450 $ 93,769 $16,196 $273,415

Investments in funds at NAV 5,910

Total cash instrument assets $279,325

Liabilities

U.S. government and agencyobligations $ (17,738) $ (8) $ — $ (17,746)

Non-U.S. government and agencyobligations (25,097) (1,657) — (26,754)

Loans and securities backed by:Commercial real estate — (5) — (5)

Residential real estate — (1) — (1)

Corporate loans and debtsecurities (6) (8,616) (32) (8,654)

Other debt obligations — (1) — (1)

Equity securities (24,765) (290) (10) (25,065)

Total cash instrument liabilities $ (67,606) $(10,578) $ (42) $ (78,226)

As of December 2016

$ in millions Level 1 Level 2 Level 3 Total

Assets

Money market instruments $ 188 $ 1,131 $ — $ 1,319U.S. government and agency

obligations 35,254 22,403 — 57,657Non-U.S. government and agency

obligations 22,433 6,933 15 29,381Loans and securities backed by:

Commercial real estate — 2,197 1,645 3,842Residential real estate — 11,350 845 12,195

Corporate loans and debt securities 215 23,804 4,640 28,659State and municipal obligations — 960 99 1,059Other debt obligations — 830 528 1,358Equity securities 77,276 7,153 10,263 94,692Commodities — 5,653 — 5,653Subtotal $135,366 $82,414 $18,035 $235,815Investments in funds at NAV 6,465Total cash instrument assets $242,280

Liabilities

U.S. government and agencyobligations $ (16,615) $ (12) $ — $ (16,627)

Non-U.S. government and agencyobligations (19,137) (1,364) (1) (20,502)

Loans and securities backed byresidential real estate — (3) — (3)

Corporate loans and debt securities (2) (6,524) (44) (6,570)Other debt obligations — (1) — (1)Equity securities (25,768) (156) (17) (25,941)Total cash instrument liabilities $ (61,522) $ (8,060) $ (62) $ (69,644)

In the tables above:

‰ Cash instrument assets and liabilities are included in“Financial instruments owned” and “Financialinstruments sold, but not yet purchased,” respectively.