Embed Size (px)

DESCRIPTION

sasasa

Citation preview

P2. Formula Sheets

Bionic Turtle FRM Formula Sheets

By David Harper, CFA FRM CIPM www.bionicturtle.com

Note: If you are unable to view the content within this document we recommend the following: MAC Users: The built-in pdf reader will not display our non-standard fonts. Please use adobe’s pdf reader. PC Users: We recommend you use the foxit pdf reader or adobe’s pdf reader. Mobile and Tablet users: We recommend you use the foxit pdf reader app or the adobe pdf reader app. All of these products are free. We apologize for any inconvenience. If you have any additional problems, please email Suzanne.

2

HULL, CHAPTER 19: VOLATILITY SMILES: EXPLAIN HOW PUT-CALL PARITY INDICATES THAT THE IMPLIED

VOLATILITY USED TO PRICE CALL OPTIONS IS THE SAME USED TO PRICE PUT OPTIONS. ...................................... 6 CALCULATE THE EXPECTED DISCOUNTED VALUE OF A ZERO-COUPON SECURITY USING A BINOMIAL TREE. ........... 7 CONSTRUCT AND APPLY AN ARBITRAGE ARGUMENT TO PRICE A CALL OPTION ON A ZERO-COUPON SECURITY USING

REPLICATING PORTFOLIOS. ...................................................................................................................... 8 CALCULATE THE CONVEXITY EFFECT USING JENSEN’S INEQUALITY. ............................................................... 9 TUCKMAN, CHAPTER 9: THE ART OF TERM STRUCTURE MODELS: DRIFT. DESCRIBE THE PROCESS AND

EFFECTIVENESS OF THE FOLLOWING MODELS, AND CONSTRUCT TREE FOR A SHORT-TERM RATE USING THE

FOLLOWING MODELS: A MODEL WITH NORMALLY DISTRIBUTED RATES AND NO DRIFT (MODEL 1) ...................... 9 DESCRIBE … A MODEL INCORPORATING DRIFT (MODEL 2) ......................................................................... 10 CALCULATE THE SHORT-TERM RATE CHANGE AND STANDARD DEVIATION OF THE CHANGE OF THE RATE USING A

MODEL WITH NORMALLY DISTRIBUTED RATES [ASSUMING BOTH DRIFT] AND NO DRIFT. .................................. 11 DESCRIBE THE PROCESS OF AND CONSTRUCT A TREE FOR A SHORT-TERM RATE UNDER THE HO-LEE MODEL WITH

TIME DEPENDENT DRIFT. ....................................................................................................................... 12 DESCRIBE THE PROCESS OF AND CONSTRUCT A SIMPLE AND RECOMBINING TREE FOR A SHORT-TERM RATE UNDER

THE VASICEK MODEL WITH MEAN REVERSION. ......................................................................................... 12 CALCULATE THE VASICEK MODEL RATE CHANGE, STANDARD DEVIATION OF THE CHANGE OF THE RATE, EXPECTED

RATE IN T YEARS, AND HALF-LIFE. .......................................................................................................... 13 TUCKMAN, CHAPTER 10: THE ART OF TSM: VOLATILITY & DISTRIBUTION. DESCRIBE THE SHORT-TERM RATE

PROCESS UNDER A MODEL WITH TIME-DEPENDENT VOLATILITY (MODEL 3). ................................................. 14 CALCULATE THE SHORT-TERM RATE CHANGE AND DESCRIBE THE BEHAVIOR OF THE STANDARD DEVIATION OF THE

CHANGE OF THE RATE USING A MODEL WITH TIME DEPENDENT VOLATILITY. .................................................. 14 DESCRIBE THE SHORT-TERM RATE PROCESS UNDER THE COX-INGERSOLL-ROSS (CIR) AND LOGNORMAL

MODELS. ............................................................................................................................................. 15 DESCRIBE THE IMPACT ON A MBS OF THE WEIGHTED AVERAGE MATURITY, THE WEIGHTED AVERAGE COUPON, AND THE SPEED OF PREPAYMENTS OF THE MORTGAGES UNDERLYING THE MBS. ........................................... 16 IDENTIFY, DESCRIBE, AND CONTRAST DIFFERENT STANDARD PREPAYMENT MEASURES. .................................. 16 DESCRIBE THE EFFECTIVE DURATION AND EFFECTIVE CONVEXITY OF STANDARD MBS INSTRUMENTS AND THE

FACTORS THAT AFFECT THEM. ................................................................................................................ 18 DOWD, MEASURING, CHAPTER 3: ESTIMATING MARKET RISK MEASURES. CALCULATE VAR USING A HISTORICAL

SIMULATION APPROACH ........................................................................................................................ 18 CALCULATE VAR USING A PARAMETRIC ESTIMATION APPROACH ASSUMING THAT THE RETURN DISTRIBUTION IS

EITHER NORMAL OR LOGNORMAL. .......................................................................................................... 19 CALCULATE EXPECTED SHORTFALL GIVEN P/L OR RETURN DATA. ............................................................... 20 DEFINE COHERENT RISK MEASURES. ....................................................................................................... 20 DESCRIBE THE METHOD OF ESTIMATING COHERENT RISK MEASURES BY ESTIMATING QUANTILES. .................... 22 DESCRIBE THE FOLLOWING WEIGHTED HISTORIC SIMULATION APPROACHES: AGE-WEIGHTED HISTORIC

SIMULATION ........................................................................................................................................ 23 DESCRIBE THE FOLLOWING WEIGHTED HISTORIC SIMULATION APPROACHES: VOLATILITY-WEIGHTED HISTORIC

SIMULATION ........................................................................................................................................ 24 DOWD, CHAPTER 5 APPENDIX: MODELING DEPENDENCE: CORRELATIONS AND COPULAS. EXPLAIN THE

DRAWBACKS OF USING CORRELATION TO MEASURE DEPENDENCE. .............................................................. 25 DESCRIBE HOW COPULAS PROVIDE AN ALTERNATIVE MEASURE OF DEPENDENCE. ......................................... 25 IDENTIFY BASIC EXAMPLES OF COPULAS. ................................................................................................. 26 EXPLAIN HOW TAIL DEPENDENCE CAN BE INVESTIGATED USING COPULAS. ................................................... 27 DOWD, CHAPTER 7: PARAMETRIC APPROACHES (II): EXTREME VALUE. COMPARE GENERALIZED EXTREME VALUE

AND POT. DESCRIBE THE PARAMETERS OF A GENERALIZED PARETO (GP) DISTRIBUTION. ............................. 27

3

COMPUTE VAR AND EXPECTED SHORTFALL USING THE POT APPROACH, GIVEN VARIOUS PARAMETER VALUES. . 28 DESCRIBE AND CALCULATE THE MORTGAGE PAYMENT FACTOR. .................................................................. 29 CALCULATE THE STATIC CASH FLOW YIELD OF A MBS USING BOND EQUIVALENT YIELD (BEY) AND DETERMINE

THE ASSOCIATED NOMINAL SPREAD. ....................................................................................................... 29 DESCRIBE THE STEPS FOR VALUING A MORTGAGE SECURITY USING MONTE CARLO METHODOLOGY. ................. 31 DEFINE AND INTERPRET OPTION-ADJUSTED SPREAD (OAS), ZERO-VOLATILITY OAS, AND OPTION COST. .......... 33 EXPLAIN HOW TO SELECT THE NUMBER OF INTEREST RATE PATHS IN MONTE CARLO ANALYSIS. ....................... 34 DESCRIBE TOTAL RETURN ANALYSIS, CALCULATE TOTAL RETURN, AND UNDERSTAND FACTORS PRESENT IN MORE

SOPHISTICATED MODELS. ...................................................................................................................... 35 SERVIGNY, CHAPTER 3: DEFAULT RISK: QUANTITATIVE METHODOLOGIES. DESCRIBE THE MERTON MODEL FOR

CORPORATE SECURITY PRICING, INCLUDING ITS ASSUMPTIONS, STRENGTHS AND WEAKNESSES. ....................... 36 USING THE MERTON MODEL, CALCULATE THE VALUE OF A FIRM'S DEBT AND EQUITY AND THE VOLATILITY OF FIRM

VALUE. ............................................................................................................................................... 37 DEFINE THE FOLLOWING TERMS RELATED TO DEFAULT AND RECOVERY: DEFAULT EVENTS, PROBABILITY OF

DEFAULT, CREDIT EXPOSURE, AND LOSS GIVEN DEFAULT. .......................................................................... 42 CALCULATE EXPECTED LOSS FROM RECOVERY RATES, THE LOSS GIVEN DEFAULT, AND THE PROBABILITY OF

DEFAULT. ............................................................................................................................................ 44 DESCRIBE THE MERTON MODEL, AND USE IT TO CALCULATE THE VALUE OF A FIRM, THE VALUES OF A FIRM’S DEBT

AND EQUITY, AND DEFAULT PROBABILITIES. ............................................................................................. 45 DESCRIBE CREDIT FACTOR MODELS AND EVALUATE AN EXAMPLE OF A SINGLE-FACTOR MODEL. ...................... 47 DEFINE CREDIT VAR (VALUE-AT-RISK). .................................................................................................. 48 MALZ, CHAPTER 7: SPREAD RISK AND DEFAULT INTENSITY MODELS. DEFINE THE DIFFERENT WAYS OF

REPRESENTING SPREADS. COMPARE AND DIFFERENTIATE BETWEEN THE DIFFERENT SPREAD CONVENTIONS AND

COMPUTE ONE SPREAD GIVEN OTHERS WHEN POSSIBLE. ............................................................................ 50 EXPLAIN HOW DEFAULT RISK FOR A SINGLE COMPANY CAN BE MODELED AS A BERNOULLI TRIAL. .................... 51 DEFINE THE HAZARD RATE AND USE IT TO DEFINE PROBABILITY FUNCTIONS FOR DEFAULT TIME AND CONDITIONAL

DEFAULT PROBABILITIES. ...................................................................................................................... 51 CALCULATE RISK-NEUTRAL DEFAULT RATES FROM SPREADS. ..................................................................... 52 DEFINE DEFAULT CORRELATION FOR CREDIT PORTFOLIOS. ......................................................................... 53 DESCRIBE HOW A SINGLE FACTOR MODEL CAN BE USED TO MEASURE CONDITIONAL DEFAULT PROBABILITIES

GIVEN ECONOMIC HEALTH. .................................................................................................................... 53 COMPUTE VARIANCE OF THE CONDITIONAL DEFAULT DISTRIBUTION AND CONDITIONAL PROBABILITY OF DEFAULT

USING SINGLE-FACTOR MODEL. .............................................................................................................. 54 EXPLAIN HOW CREDIT VAR OF A PORTFOLIO IS CALCULATED USING THE SINGLE-FACTOR MODEL, AND HOW

CORRELATION AFFECTS THE DISTRIBUTION OF LOSS SEVERITY FOR INTERMEDIATE VALUES BETWEEN 0 AND 1. .. 55 GREGORY, CHAPTER 2: DEFINING COUNTERPARTY CREDIT RISK ................................................................ 55 DEFINE THE FOLLOWING METRICS FOR CREDIT EXPOSURE: EXPECTED MARK-TO-MARKET, EXPECTED EXPOSURE, POTENTIAL FUTURE EXPOSURE, EXPECTED POSITIVE EXPOSURE, EFFECTIVE EXPOSURE, AND MAXIMUM

EXPOSURE. ......................................................................................................................................... 56 DESCRIBE THE PARAMETERS USED IN SIMPLE SINGLE-FACTOR MODELS … .................................................... 58 DESCRIBE HOW NETTING IS MODELED. .................................................................................................... 60 DEFINE AND CALCULATE THE NETTING FACTOR......................................................................................... 61 DEFINE AND CALCULATE MARGINAL EXPECTED EXPOSURE AND THE EFFECT OF CORRELATION ON TOTAL

EXPOSURE. ......................................................................................................................................... 61 GREGORY, CHAPTER 5: QUANTIFYING COUNTERPARTY CREDIT EXPOSURE, II: THE IMPACT OF COLLATERAL. CALCULATE THE EXPECTED EXPOSURE AND POTENTIAL FUTURE EXPOSURE OVER THE REMARGINING PERIOD

GIVEN NORMAL DISTRIBUTION ASSUMPTIONS. .......................................................................................... 61

4

DEFINE AND CALCULATE CREDIT VALUE ADJUSTMENT (CVA) WHEN NO WRONG-WAY RISK IS PRESENT. ........... 62 DESCRIBE THE PROCESS OF APPROXIMATING THE CVA SPREAD. ................................................................. 63 DEFINE AND CALCULATE THE INCREMENTAL CVA AND THE MARGINAL CVA. ................................................ 63 DEFINE AND CALCULATE CVA AND CVA SPREAD IN THE PRESENCE OF A BILATERAL CONTRACT. ..................... 64 CROUHY CHAPTER 14: DESCRIBE RAROC (RISK-ADJUSTED RETURN ON CAPITAL) METHODOLOGY .................. 65 COMPUTE AND INTERPRET THE RAROC FOR A LOAN OR LOAN PORTFOLIO, AND USE RAROC TO COMPARE

BUSINESS UNIT PERFORMANCE. ............................................................................................................. 66 EXPLAIN HOW THE SECOND-GENERATION RAROC APPROACHES IMPROVE ECONOMIC CAPITAL ALLOCATION

DECISIONS .......................................................................................................................................... 67 COMPUTE THE ADJUSTED RAROC FOR A PROJECT TO DETERMINE ITS VIABILITY. ........................................... 68 DESCRIBE AND CALCULATE LVAR USING THE CONSTANT SPREAD APPROACH AND THE EXOGENOUS SPREAD

APPROACH. ......................................................................................................................................... 74 DESCRIBE ENDOGENOUS PRICE APPROACHES TO LVAR, ITS MOTIVATION AND LIMITATIONS. .......................... 75 CALCULATE A FIRM’S LEVERAGE RATIO, DESCRIBE THE FORMULA FOR THE LEVERAGE EFFECT, AND EXPLAIN THE

RELATIONSHIP BETWEEN LEVERAGE AND A FIRM’S RETURN ON EQUITY. ....................................................... 75 CALCULATE THE EXPECTED TRANSACTIONS COST AND THE 99 PERCENT SPREAD RISK FACTOR FOR A

TRANSACTION. ..................................................................................................................................... 76 CALCULATE THE LIQUIDITY-ADJUSTED VAR FOR A POSITION TO BE LIQUIDATED OVER A NUMBER OF TRADING

DAYS. ................................................................................................................................................. 77 DEFINE CHARACTERISTICS USED TO MEASURE MARKET LIQUIDITY, INCLUDING TIGHTNESS, DEPTH AND

RESILIENCY. ........................................................................................................................................ 78 BASEL II: REVISED FRAMEWORK: DESCRIBE THE KEY ELEMENTS OF THE THREE PILLARS OF BASEL II: MINIMUM

CAPITAL REQUIREMENTS ....................................................................................................................... 79 DESCRIBE AND CONTRAST THE MAJOR ELEMENTS OF THE THREE OPTIONS AVAILABLE FOR THE CALCULATION OF

CREDIT RISK: STANDARDIZED APPROACH, FOUNDATION IRB APPROACH, ADVANCED IRB APPROACH ............ 79 DESCRIBE AND CONTRAST THE MAJOR ELEMENTS OF THE THREE OPTIONS AVAILABLE FOR THE CALCULATION OF

OPERATIONAL RISK: BASIC INDICATOR APPROACH .................................................................................... 80 DESCRIBE AND CONTRAST THE MAJOR ELEMENTS OF THE THREE OPTIONS AVAILABLE FOR THE CALCULATION OF

OPERATIONAL RISK: STANDARDIZED APPROACH ...................................................................................... 81 DESCRIBE AND CONTRAST THE MAJOR ELEMENTS - INCLUDING A DESCRIPTION OF THE RISKS COVERED – OF THE

TWO OPTIONS AVAILABLE FOR THE CALCULATION OF MARKET RISK: STANDARDIZED MEASUREMENT METHOD .. 82 DESCRIBE AND CONTRAST THE MAJOR ELEMENTS - INCLUDING A DESCRIPTION OF THE RISKS COVERED – OF THE

TWO OPTIONS AVAILABLE FOR THE CALCULATION OF MARKET RISK: INTERNAL MODELS APPROACH ................. 83 DEFINE IN THE CONTEXT OF BASEL II AND CALCULATE WHERE APPROPRIATE: RISK WEIGHTS AND RISK-WEIGHTED

ASSETS ............................................................................................................................................... 84 DEFINE IN THE CONTEXT OF BASEL II AND CALCULATE WHERE APPROPRIATE: TIER 1, TIER 2 AND TIER 3 CAPITAL

AND ITS COMPONENTS .......................................................................................................................... 84 BASEL III: GLOBAL REGULATORY FRAMEWORK FOR MORE RESILIENT BANKS AND BANKING SYSTEMS. DESCRIBE

CHANGES TO THE REGULATORY CAPITAL FRAMEWORK, INCLUDING CHANGES TO: THE USE OF LEVERAGE RATIOS 85 DEFINE AND DESCRIBE THE MINIMUM LIQUIDITY COVERAGE RATIO. ............................................................. 86 DEFINE AND DESCRIBE THE NET STABLE FUNDING RATIO. .......................................................................... 88 DEFINE AND DESCRIBE PRACTICAL APPLICATIONS OF PRESCRIBED LIQUIDITY MONITORING TOOLS, INCLUDING: CONCENTRATION OF FUNDING ............................................................................................................... 90 REVISIONS TO THE BASEL II MARKET RISK FRAMEWORK. EXPLAIN AND CALCULATE THE STRESSED VALUE-AT-RISK MEASURE AND THE FREQUENCY AT WHICH IT MUST BE CALCULATED. .................................................... 90

5

GRINOLD, CHAPTER 14: PORTFOLIO CONSTRUCTIO. EXPLAIN PRACTICAL ISSUES IN PORTFOLIO CONSTRUCTION

SUCH AS DETERMINATION OF RISK AVERSION, INCORPORATION OF SPECIFIC RISK AVERSION, AND PROPER ALPHA

COVERAGE. ......................................................................................................................................... 92 DESCRIBE PORTFOLIO REVISIONS AND REBALANCING AND THE TRADEOFFS BETWEEN ALPHA, RISK, TRANSACTION

COSTS AND TIME HORIZON..................................................................................................................... 93 JORION, CHAPTER 7: PORTFOLIO RISK: ANALYTICAL METHODS. DEFINE AND DISTINGUISH BETWEEN INDIVIDUAL

VAR, INCREMENTAL VAR AND DIVERSIFIED PORTFOLIO VAR. ..................................................................... 93 EXPLAIN THE ROLE CORRELATION HAS ON PORTFOLIO RISK. ....................................................................... 95 DEFINE, COMPUTE, AND EXPLAIN THE USES OF MARGINAL VAR, INCREMENTAL VAR, AND COMPONENT VAR. .. 95 DEMONSTRATE HOW ONE CAN USE MARGINAL VAR TO GUIDE DECISIONS ABOUT PORTFOLIO VAR. .................. 97 EXPLAIN THE DIFFERENCE BETWEEN RISK MANAGEMENT AND PORTFOLIO MANAGEMENT, AND DEMONSTRATE

HOW TO USE MARGINAL VAR IN PORTFOLIO MANAGEMENT. ....................................................................... 97 DEFINE AND DESCRIBE THE FOLLOWING TYPES OF RISK: FUNDING RISK ....................................................... 98 RISK MONITORING & PERFORMANCE MEASUREMENT: LITTERMAN, CH17. DEFINE, COMPARE AND CONTRAST

VAR AND TRACKING ERROR AS RISK MEASURES. ....................................................................................... 99 BODIE, CHAPTER 13: EMPIRICAL EVIDENCE ON SECURITY RETURNS. INTERPRET THE EXPECTED RETURN-BETA

RELATIONSHIP IMPLIED IN THE CAPM, AND DESCRIBE THE METHODOLOGIES FOR ESTIMATING THE SECURITY

CHARACTERISTIC LINE AND THE SECURITY MARKET LINE FROM A PROPER DATASET. ....................................... 99 DESCRIBE AND INTERPRET THE FAMA-FRENCH THREE-FACTOR MODEL, AND EXPLAIN HISTORICAL TEST RESULTS

RELATED TO THIS MODEL ..................................................................................................................... 100 BODIE, CHAPTER 24: PORTFOLIO PERFORMANCE EVALUATION. DIFFERENTIATE BETWEEN THE TIME-WEIGHTED

AND DOLLAR-WEIGHTED RETURNS OF A PORTFOLIO AND THEIR APPROPRIATE USES. .................................... 103 DESCRIBE THE DIFFERENT RISK-ADJUSTED PERFORMANCE MEASURES ...................................................... 104 DESCRIBE THE DIFFERENT RISK-ADJUSTED PERFORMANCE MEASURES, SUCH AS: SHARPE’S MEASURE .......... 104 DESCRIBE THE DIFFERENT RISK-ADJUSTED PERFORMANCE MEASURES, SUCH AS: TREYNOR’S MEASURE ........ 105 DESCRIBE THE DIFFERENT RISK-ADJUSTED PERFORMANCE MEASURES, SUCH AS: JENSEN’S MEASURE .......... 105 DESCRIBE THE DIFFERENT RISK-ADJUSTED PERFORMANCE MEASURES, SUCH AS: INFORMATION RATIO.......... 106 DESCRIBE THE USES FOR THE MODIGLIANI-SQUARED AND TREYNOR’S MEASURE IN COMPARING TWO

PORTFOLIOS, AND THE GRAPHICAL REPRESENTATION OF THESE MEASURES. ............................................... 106 DESCRIBE TECHNIQUES TO MEASURE THE MARKET TIMING ABILITY OF FUND MANAGERS WITH: REGRESSION .. 108 DESCRIBE THE DATA SET, MEASUREMENTS, FLAGS, AND MULTIPLE REGRESSION MODELS USED IN THE STUDY. 110 CALCULATE THE MAXIMUM DRAWDOWN, CONCENTRATION RATIO, AND THE VOLUME AND QUOTE HERFINDAHL

INDEX. .............................................................................................................................................. 110

6

Hull, Chapter 19: Volatility smiles: Explain how put-call parity indicates that the implied volatility used to price call options is the same used to price put options.

Put-call parity applies to both model-based relationship and the market-based (observed) relationship:

Black-Scholes Black-Scholes 0

market market 0

rT

rT

c Ke p S

c Ke p S

Such that the pricing error observed when using the Black-Scholes to price a call option should be exactly the same as observed when pricing a put option:

Black-Scholes market Black-Scholes marketc c p p

“This shows that the dollar pricing error when the Black-Scholes model is used to price a European put option should be exactly the same as the dollar pricing error when it is used to price a European call option with the same strike price and time to maturity” – Hull

7

Calculate the expected discounted value of a zero-coupon security using a binomial tree.

Assume the six-month spot rate is 5.00% with semi-annual compounding. Further assume that six months from now the six-month rate will be either 4.50% or 5.50% with equal probability. These assumptions are illustrated with a binomial interest rate tree (“binomial” implies that only two future values are possible). Consider the simple case of a one-year $1,000 par zero-coupon bond:

The expected discounted value is given by:

1 1$973.24 $978.00

2 2 $951.825%1

2

8

Construct and apply an arbitrage argument to price a call option on a zero-coupon security using replicating portfolios.

The payoff of a call option (which pays either $0 or $3) can be replicated by a portfolio:

Long a one-year bond plus Short a six-month bond.

The value of the option must equal the cost of the replicating portfolio:

9

The example (above), which is directly from Tuckman, takes three basic steps:

1. Specify the interest rate assumptions (I.) which includes both an interest rate tree (50% probability of an up-jump from current 5.0% to 5.5% and 50% probability of down-jump to 4.5%) and a one-year rate of 5.15%.

2. Assume the derivative instrument: in this case, a call option with a strike price of $975 (on a bond with face value of $1,000). Find the replicating portfolio (II.). This is the combination of long position in a one-year bond plus a short position in a six-month bond that produces a payoff identical to the derivative. The cost of the portfolio is $0.58, which therefore must be the price of the derivative.

3. Compare the expected discounted value of $1.46, which discounts with the true (or real-world) probabilities (p = 50% and 1-p = 50%), to the arbitrage price of $0.58, which discounts with the risk-neutral probabilities (p = 80.09% and 1-p = 19.91%).

Calculate the convexity effect using Jensen’s inequality.

The convexity effect arises from a special case of Jensen’s Inequality:

1 1 1

1 1 1E

r E r r

Tuckman, Chapter 9: The Art of Term Structure Models: Drift. Describe the process and effectiveness of the following models, and construct tree for a short-term rate using the following models: A model with normally distributed rates and no drift (Model 1)

In regard to notation:

dr denotes the change in the rate over a small time interval, dt, measured in years; σ denotes the annual basis-point volatility of rate changes; dw denotes a normally distributed random variable with mean of zero and standard

deviation of SQRT(dt). Note that dw is only a standard random normal when dt = 1.0; otherwise, dw already scales for time by applying the square root rule.

In the following examples, please take care to note the difference between the rate tree (which only

maps two paths assuming sigma is 1.0) and a simulated process (which is variously rendered due to the various outcomes of the random normal).

10

Model 1: Constant volatility and no drift

dr dw

As the expected value of (dw) is zero, the expected change in the rate (a.k.a., the drift) is zero.

Model 1: Rate Tree

In Model 1, since drift is zero, rate recombines to current rate, r0, at node [2,2]:

�� + ��√�� �� + �√��

�� �� �� − �√�� �� − ��√��

Describe … A model incorporating drift (Model 2)

Model 2: Constant volatility with drift (λ)

dr dt dw

Model 2: Rate Tree

Model 2 is essentially similar to Model 1 except it adds a non-random drift term.

�� + ����+ ��√�� �� + ���+ �√��

�� �� + ���� �� + ���+ −�√�� �� + ����+ ��√��

11

Calculate the short-term rate change and standard deviation of the change of the rate using a model with normally distributed rates [assuming both drift] and no drift.

Rate change under Model 1 (no drift and normally distributed rate)

dr dw

To illustrate, let us assume monthly time steps, dt = 1/12 and

Current or initial rate, r(0) = 3.00% Annual basis point volatility = 200 basis points Assume our uniform random variable happens to be 0.40 such that the random

standard normal = -0.2533 = NORM.S.INV(40%). Each step accepts a different random normal.

The short-term rate then evolves, in the first month: dr = 3.0% + 2.0%*-0.2533*SQRT(1/12) = -0.14627%, and r(1/12) = 3.00% -0.14627% = 2.85373%

Rate change under Model 2 (drift and normally distributed rate)

dr dt dw

To illustrate, let us assume monthly time steps, dt = 1/12 and:

Current or initial rate, r(0) = 4.00% Annual basis point volatility = 250 basis points Annual drift = +100 basis points Assume our uniform random variable happens to be 0.79 such that the random

standard normal = +0.80642 = NORM.S.INV(79%). Each step accepts a different random normal.

The short-term rate then evolves, in the first month: dr = 4.0% + 1.0%*1/12 + 2.5%*0.80642*SQRT(1/12) = +0.6653%, and r(1/12) = 4.00% +0.6653% = 5.665%

Please note: the drift is multiplied by dt, but volatility is by multiplied by SQRT(1/12); i.e., dw is already time-scaled per the square root rule.

12

Describe the process of and construct a tree for a short-term rate under the Ho-Lee Model with time dependent drift.

The dynamics of the risk-neutral process in the Ho-Lee model are given by:

tdr dt dw

This Ho-Lee Model is similar to Model 2, but with a difference:

Model 2 assumes that the drift (lambda) is constant from step to step along the tree; However, this Ho-Lee Model assumes that drift changes over time

Tuckman: “In contrast to Model 2, the drift [in the Ho-Lee Model] depends on time. In other words, the drift of the process may change from date to date. It might be an annualized drift of −20 basis points over the first month, of 20 basis points over the second month, and so on. A drift that varies with time is called a time-dependent drift. Just as with a constant drift, the time-dependent drift over each time period represents some combination of the risk premium and of expected changes in the short-term rate. The flexibility of the Ho-Lee model is easily seen from its corresponding tree: The free parameters and may be used to match the prices of securities with fixed cash flows.”

Describe the process of and construct a simple and recombining tree for a short-term rate under the Vasicek Model with mean reversion.

The Vasicek Model introduces mean reversion into the rate model, which is a common assumption for the level of interest rates. The Vasicek Model is given by:

dr k r dt dw

Where Theta, �, denotes the long-run value or central tendency of the short-term rate in the risk-neutral process and the positive constant, k, denotes the speed of mean reversion.

13

Calculate the Vasicek Model rate change, standard deviation of the change of the rate, expected rate in T years, and half-life.

Rate change under Vasicek Model

dr k r dt dw

Let us assume:

Initial rate, r(0) = 6.0% Strength of mean reversion, k = 0.50 Long-run (equilibrium) rate, θ = 4.0% Annual basis-point volatility = 300 basis points

Consider various realizations of dw under a monthly time-step; i.e., dw = NORM.S.INV((RAND())*SQRT(1/12)

If dw = -0.038, then dr = 0.50*(4.0% - 6.0%)*1/12 + (3.0% * -0.038) = -0.20%, and r(1/12) = 5.80%

If dw = 0.230, then dr = 0.50*(4.0%-6.0%)*1/12 + (3.0% * 0.230) = 0.61%, and r(1/12) = 6.61%

Expected rate in T years

The expectation of the rate in the Vasicek model after (T) years is a weighted average of the current short rate and its long-run value, where the weight on the current short rate decays exponentially at a speed determined by the mean-reverting parameter:

0 1kT kTr e e

Half-life

The mean-reverting parameter (k) does not intuitively describe the pace of mean-reversion. Instead, the “half-life” is defined as the time it takes the factor to progress half the distance toward its goal. The half-life is given by:

ln(2)years

k

If, for example, k = 0.0250, then the half-life (τ) = ln(2)/0.0250 ~= 27.7 years.

14

Tuckman, Chapter 10: The Art of TSM: Volatility & Distribution. Describe the short-term rate process under a model with time-dependent volatility (Model 3).

In the previous chapters, the model of the short-term rate involved either:

No (zero) drift and constant volatility (Model 1) Constant drift and constant volatility (Model 2) Time-dependent drift and constant volatility (Ho-Lee Model) Mean-reverting drift and constant volatility (Vasicek Model)

In this reading, Tuckman introduces so-called Model 3 which assumes time-dependent volatility. The special case is given by:

( ) tdr t dt e dw

Calculate the short-term rate change and describe the behavior of the standard deviation of the change of the rate using a model with time dependent volatility.

( ) tdr t dt e dw

In Model 3 (with time-dependent volatility), let us assume for illustration’s sake:

Annual volatility (sigma) = 126 basis points = 1.26% Alpha factor = 0.080 Drift, λ(t), happens to be constant at +20 basis points (however, please note that

drift could also be time-dependent)

Initially, at time zero (t = 0), the volatility of the short-rate starts at sigma, but over time, declines exponentially toward zero. For example:

At time zero, t = 0, EXP(-0.080 * 0) = 1.0, such that the volatility term = 1.26%*1.0*dw

At t = 5, EXP(-0.080 * 5) = 0.67, such that the volatility term = 1.26%*0.67*dw At t= 10, EXP(-0.080 * 10) = 0.45, such that the volatility term = 1.26%*0.45*dw

Please note that, following Tuckman, the (dw) is already time-scaled; e.g., if the time step is monthly, then (dw) has a standard deviation of SQRT(dt) = SQRT(1/12).

15

If we are given simulated random normals, dw, we can simulate the short-term rate change. For example, let us continue to follow Tuckman and assume the time-step is monthly (dt = 1/12):

On the first month, when t = 1/12, if the random normal, dw = 0.0176, then as EXP(-0.08*1/12) = 0.99, the rate change (dr) = 0.20%*(1/12) + 1.26%*0.99*0.0176 ~= 0.039%, and r(1/12) = 3.000% + 0.039% = 3.039% Note: for convenience EXP(-0.08*1/12) is used, to maintain calculations on the same row, instead of EXP(-0.08*0/12), which is more correct; with minimal impact.

Similarly, on the fifth year (month = 60), assume the prior rate is 3.169%. If the simulated random normal, dw = -0.3700, then as EXP(-0.080*5.0) = 0.67, the rate change (dr) = 0.20%*(1/12) + 1.26%*0.67*-0.3700 = -0.296%, and r(5.0) = 3.169% - 0.296% = 2.873%

Describe the short-term rate process under the Cox-Ingersoll-Ross (CIR) and Lognormal models.

The previous models assume that the basis-point volatility of the short rate is independent of the level of the short rate. However, this is unlikely to be true at extreme levels of the short rate:

When the short-term interest rate is especially high (e.g., during periods of high inflation), the short-term rate in inherently unstable; on the other hand,

When the short-term rate is very low, basis-point volatility is limited by the constraint that interest rates cannot decline much below zero.

The Cox-Ingersoll-Ross (CIR) model assumes a relationship (dependency) between the basis-point volatility and the level of the short rate. The CIR model is given by:

dr k r dt rdw

In addition to the mean reversion (i.e., the tendency of the short-term rate to move toward the equilibrium rate denoted by theta, θ) exhibited in the Vasicek, the Cox-Ingersoll-Ross (CIR) model multiplies volatility by the square root of the level of the interest rate.

Lognormal (Model4)

In the lognormal model, basis-point volatility is proportional to the level of the rate:

dr ardt rdw

16

A variation can be expressed as follows:

ln( ) ( )d r a t dt dw

ln ( ) ln ( ) ln ( )d r k t t r dt t dw

In this case, the natural logarithm of the short rate is normally distributed

Describe the impact on a MBS of the weighted average maturity, the weighted average coupon, and the speed of prepayments of the mortgages underlying the MBS.

The following three factors play an important role in calculating the value of mortgage-backed securities (MBS):

1. Weighted Average Maturity (WAM) of the underlying mortgage pool: WAM is calculated by taking the weighted average of time until maturity of all mortgages in the mortgage pool.

2. Weighted Average Coupon (WAC) of the underlying mortgage pool: WAC is calculated by taking the weighted average of coupons of all mortgages in the mortgage pool.

3. Speed of prepayments: Prepayment speed refers to the speed at which the mortgages are paid off ahead of their schedule. Prepayment speed affects the value of MBS. If no prepayments are expected, then we can expect cash flows quite far in future. However, as the prepayment rates increase, the cash flows are expected sooner than farther in future.

Identify, describe, and contrast different standard prepayment measures.

Constant Maturity Mortality (CMM)

This measure assumes that there is a constant probability that the mortgage will be prepaid after the next coupon. This measure is expressed monthly, as mortgage payments are made monthly. The monthly prepayment rate is also called single monthly mortality (SMM). Assume p is the constant probability, then:

������� �������� ��� = �

������� �������� ��� = (1− �)�

������� �������� ��� = (1− �)��

17

When the monthly prepayment rate is annualized it is called Conditional Prepayment Rate (CPR). We can convert the monthly prepayment rate (p) into annualized conditional prepayment rate using the following formula:

CPR = 1 − (1 − p)12

Alternatively, to calculate monthly rate (p) from the annualized CPR, we can rearrange the formula as follows:

p = 1 − (1 − CPR)����

PSA Prepayment Model

This is a prepayment model established by the Public Securities Association (PSA). The standard model refers to a 100% PSA. 100 PSA assumes the following:

1. The prepayment rate (CPR) will be 0.2% in the first month.

2. It will increase by 0.2% per month for the first 30 months.

3. After 30th month, it will peak at 6% and remain constant till maturity.

This is a convention used by the industry to express prepayment speed. The CPR can be scaled up or down to obtain faster or slower prepayment speeds. For example, 150%PSA will mean a monthly increment by 0.3% and peak at 9%. 200% PSA will mean a monthly increment of 0.4% and peak at 12%.

The following graph plots 100 PSA, 150 PSA, and 200 PSA.

PSA is a multiple of CPR, not the single monthly mortality (SMM). For months 31 and beyond, 50% PSA = 50% * 6.0% CPR = 3.0% CPR. For months 31 and beyond, 200% PSA = 200% * 6.0% CPR = 12.0% CRP.

0

5

10

15

3 8 13

18

23

28

CPR

(%

)

Years

100 PSA

150 PSA

200 PSA

18

Describe the effective duration and effective convexity of standard MBS instruments and the factors that affect them.

Effective Duration (D)

� ≈ −�

�

�(+����)− �(−����)

� × ����

P = current price of MBS, and P(+x bps) and P(-x bps) = Prices of same security when interest rates move up or down by x bps.

Effective Convexity ©

� ≈�

�

�(+����)+ �(−����)− � × �

(����)�

P = current price of MBS, and P(+x bps) and P(-x bps) = Prices of same security when interest rates move up or down by x bps.

Dowd, Measuring, Chapter 3: Estimating Market Risk Measures. Calculate VaR using a historical simulation approach

The simplest way to estimate VaR is by means of historical simulation (HS). The HS approach estimates VaR by means of ordered loss observations. Suppose, for example, 1000 loss observations and are interested in the VaR at the 95% confidence level. Since the confidence level implies a 5%tail, we know that there are 50 observations in the tail, and we can take the VaR to be the 51st highest loss observation.

19

In the case of 200 observations, we would order the loss observations and (where the losses are given by a positive number), the 99% VaR would equal a worst expected loss of $2,524; i.e., the 1% tail contains the worst two losses out of 200.

Ordered Obs Portfolio Portfolio %ile No. P/L P/L or CL VaR

1 1946 5985 0.005 -5985 2 -2524 5807 0.010 -5807

195 4287 -2043 0.975 2043 196 -77 -2466 0.980 2466 197 3654 -2503 0.985 2503 198 2223 -2524 0.990 2524 199 2620 -2988 0.995 2988 200 1588 -3039 1.000 3039

Calculate VaR using a parametric estimation approach assuming that the return distribution is either normal or lognormal.

Under the assumption that profit/loss is normally distributed, the VaR at confidence level alpha (�; please note Dowd uses alpha to denote confidence whereas elsewhere we typically use alpha to denote significance!) is given by:

/ / P L P LVaR z

For example, given a mean of 10% and volatility of 20%, the 95% normal VaR is given by:

Mean 10% Std Dev 20% CL 95% Normal deviate 1.645 95% VaR 22.90%

20

The lognormal VaR is given by:

1 1 exp t R RVaR P z

For example, given a mean of 10% and volatility of 20%, the 95% lognormal VaR is given by:

Mean 10% Std Dev 20% CL 95% Normal deviate 1.645 95% VaR 20.46%

Calculate expected shortfall given P/L or return data.

The expected shortfall (ES) is the probability-weighted average of tail losses. Put another way, the ES is the expected loss conditional on the loss exceeding VaR. The fact that the ES is a probability-weighted average of tail losses implies that we can estimate ES as an average of ‘tail VaRs’. The easiest way to implement this approach is to slice the tail into a large number n of slices, each of which has the same probability mass, estimate the VaR associated with each slice, and take the ES as the average of these VaRs.

Ordered Obs Port. Port. %ile No. P/L P/L or CL VaR ES 1 1946 5985 0.005 -5985 -2253 2 -2524 5807 0.010 -5807 -2234

195 4287 -2043 0.975 2043 3113 196 -77 -2466 0.980 2466 3380 197 3654 -2503 0.985 2503 3685 198 2223 -2524 0.990 2524 4276 199 2620 -2988 0.995 2988 6027 200 1588 -3039 1.000 3039

Define coherent risk measures.

A coherent risk measure must meet the following four conditions:

Sub-additivity Monotonicity Positive homogeneity

21

Translation invariance

Value at risk (VaR) is not sub-additive. Therefore, despite the fact that VaR meets the other three conditions, VaR is not a coherent risk measure.

Sub-additivity

•(X+Y) ≤ (X) + (Y)•“The portfolio’s risk should not be greater than the sum of its parts”

Monotonicity

•If X ≤ Y → (Y) ≤ (X)

•If expected value of Y is greater than X, risk of Y is less than X

Positive homogeneity

•For 0, (X) = (Y)•“Double portfolio, double risk” (leverage)

Translation invariance

•For constant = c, (X+c)=(X)-c

•“Like adding cash”

22

Describe the method of estimating coherent risk measures by estimating quantiles.

Coherent risk measure is a weighted average of the quantiles.

1

0

( ) pM q d pp

In this (Dowd’s) example, there is a weighting function. The particulars of the weighting function are not important: it assigns progressively greater weight to higher confidence levels (quantiles). The quantile is multiplied by the weight, and the summation gives the approximate risk measure:

gamma 0.05

Normal Deviate Weight

CL (A) (B) (A)*(B) 10% (1.282) 0.0000 (0.00) 20% (0.842) 0.0000 (0.00) 30% (0.524) 0.0000 (0.00) 40% (0.253) 0.0001 (0.00) 50% (0.000) 0.0009 (0.00) 60% 0.253 0.0067 0.00 70% 0.524 0.0496 0.03 80% 0.842 0.3663 0.31 90% 1.282 2.7067 3.47

Risk Measure 0.4227

23

1(1 )( )

1

i

nw i

Describe the following weighted historic simulation approaches: Age-weighted historic simulation

Identical to Linda Allen’s truncated hybrid volatility (hybrid of EWMA & HS)

The ratio of consecutive weights is constant at lambda (λ). For example, given n=10 & lambda = 90%

o Weight (2) = 90%*10%/(1-90%^10) = 13.82% o Weight (3) = 90%^2*10%/(1-90%^10) = 12.44% o Ratio of Weight(3)/Weight(2) = λ

The age-weighted historical simulation approach gives four advantages:

It generalizes standard historical simulation (HS) because “we can regard traditional HS as a special case with zero decay, or � →1. If HS is like driving along a road looking only at the rear-view mirror, then traditional equal-weighted HS is only safe if the road is straight, and the age-weighted approach is safe if the road bends gently.”

A suitable choice of lambda (�) can make the VaR (or ES) estimates more responsive to large loss observations: a large loss event will receive a higher weight than under traditional HS, and the resulting next-day VaR would be higher than it would otherwise have been. This not only means that age-weighted VaR estimates are more responsive to large losses, but also makes them better at handling clusters of large losses.

Age-weighting helps to reduce distortions caused by events that are unlikely to recur, and helps to reduce ghost effects. As an observation ages, its probability weight gradually falls and its influence diminishes gradually over time. Furthermore, when it finally falls out of the sample period, its weight will fall a small weighting to zero, instead of abruptly from (1/n) to zero.

We can modify age-weighting in a way that makes our risk estimates more efficient and effectively eliminates any remaining ghost effects. Since age-weighting allows the impact of past extreme events to decline as past events recede in time, it gives us the option of letting our sample size grow over time.

24

Describe the following weighted historic simulation approaches: Volatility-weighted historic simulation

Volatility-weighted historic simulation weight returns by relative volatility

,*, ,

,

T i

t i t i

t i

r r

Benefits

Directly accounts for volatility changes Allows us to incorporate GARCH forecasts Can obtain VaR or ES estimates that can exceed maximum loss in actual datasets Authors give empirical evidence to support superiority of estimates

Dowd on volatility-weighted Historical Simulation: The [HW approach to Volatility-weighted historical simulation] has a number of advantages relative to the traditional equal-weighted and/or the BRW age-weighted approaches:

It takes account of volatility changes in a natural and direct way, whereas equal-weighted HS ignores volatility changes and the age-weighted approach treats volatility changes in a rather arbitrary and restrictive way.

It produces risk estimates that are appropriately sensitive to current volatility estimates, and so enables us to incorporate information from GARCH forecasts into HS VaR and ES estimation.

It allows us to obtain VaR and ES estimates that can exceed the maximum loss in our historical data set: in periods of high volatility, historical returns are scaled upwards, and the HS P/L series used in the HW procedure will have values that exceed actual historical losses. This is a major advantage over traditional HS, which prevents the VaR or ES from being any bigger than the losses in our historical data set.

Empirical evidence presented by HW indicates that their approach produces superior VaR estimates to the BRW one.

25

The HW approach is also capable of various extensions. For instance, we can combine it with the age-weighted approach if we wished to increase the sensitivity of risk estimates to large losses, and to reduce the potential for distortions and ghost effects. We can also combine the HW approach with OS or bootstrap methods to estimate confidence intervals for our VaR or ES – that is, we would work with order statistics or resample with replacement from the HW-adjusted P/L, rather than from the traditional HS P/L.”

Dowd, Chapter 5 Appendix: Modeling Dependence: Correlations and Copulas. Explain the drawbacks of using correlation to measure dependence.

Correlation is a good measure of dependence when random variables are distributed as multivariate elliptical (e.g., normal, student’s)

XY

X Y

If risks are independent → zero correlation, however zero correlation does not imply

independence

Not good for non-elliptical distributions: Correlation “runs into more serious problems once we go outside elliptical distributions.”

Correlation is only defined if variance is finite (Levy can have infinite variance)

Describe how copulas provide an alternative measure of dependence.

If F(x,y) is a joint distribution function with continuous marginals Fx (x) = u and Fy (y) = v, then F(x,y) can be written in terms of a unique function C(u,v)

( , ) ( , )F x y C u v

Copula enables us to construct joint distribution functions from marginal distribution functions in a way that takes account of the dependence structure of our random variables.

26

Dowd on the Basics of Copula Theory: “We need an alternative dependence measure, and the answer is to be found in the theory of copulas. The term ‘copula’ comes from the Latin. It refers to connecting or joining together, and is closely related to more familiar English words such as ‘couple’. However, the ‘copulas’ we are speaking of here are statistical concepts that refer to the way in which random variables relate to each other: more precisely, a copula is a function that joins a multivariate distribution function to a collection of univariate marginal distribution functions. We take the marginal distributions – each of which describes the way in which a random variable moves ‘on its own’ – and the copula function tells us how they ‘come together’ to determine the multivariate distribution. Copulas enable us to extract the dependence structure from the joint distribution function, and so separate out the dependence structure from the marginal distribution functions.

The key result is a theorem due to Sklar (1959). Again suppose for convenience that we are concerned with only two random variables, X and Y .If F(x,y) is a joint distribution function with continuous marginal Fx(x)=u and Fy(y)=v, then F(x,y) can be written in terms of a unique function C(u,v):

F(x,y)=C(u,v)

Where C(u,v) is known as the copula of F(x,y). The copula function describes how the multivariate function F(x,y) is derived from or coupled with the marginal distribution functions Fx(x) and Fy(y), and we can interpret the copula as giving the dependence structure of F(x,y).

This result is important because it enables us to construct joint distribution functions from marginal distribution functions in a way that takes account of the dependence structure of our random variables. To model the joint distribution function, all we need to do is specify our marginal distributions, choose a copula to represent the dependence structure, estimate the parameters involved, and then apply the copula function to our marginals. Once we can model the joint distribution function, we can then in principle use it to estimate any risk measures.”

Identify basic examples of copulas.

Simple copulas

( , ) independence copula

( , ) min[ , ] minimum copula

( , ) max[ 1,0] maximum copula

ind

ind

ind

C u v uv

C u v u v

C u v u v

27

Explain how tail dependence can be investigated using copulas.

Tail dependence is an important issue because extreme events are often related (i.e., disasters often come in pairs or more), and models that fail to accommodate their dependence can literally lead a firm to disaster.

If marginal distributions are continuous, we can define a coefficient of (upper) tail dependence of X and Y as the limit, as α → 1 from below, of

1 1Pr[ ( )| ( )]y xY F Y F

Dowd, Chapter 7: Parametric Approaches (II): Extreme Value. Compare generalized extreme value and POT. Describe the parameters of a generalized Pareto (GP) distribution.

GPD (distribution) characterizes the peaks over threshold (POTS) approach

1

,

1 (1 ) 0

( )

1 exp( ) 0

x

G xx

GPD. Peaks over threshold (POTS). Modern

Two parameters: positive scale () and shape/tail (ξ)

Plus select threshold (u)

28

GEV (distribution) characterizes the block maxima approach

1

, ,

exp (1 ) 0( )

exp( ) 0z

zH z

e

( )/z x

Compute VaR and expected shortfall using the POT approach, given various parameter values.

Value at risk (VaR) and expected shortfall (ES) under the POT approach, which implies a GPD distribution:

Value at Risk (VaR) using POT

1 1n

VaRN

Expected Shortfall is equal to VaR plus the mean-excess loss over VaR

1 1

VaRES

Block Maxima. Classical.

Three params: location (μ), scale (σ) and shape/tail (ξ)

Plus select threshold (u)

29

Describe and calculate the mortgage payment factor.

The mortgage payment factor is given by:

interest rate (1+interest rate)payment factor =

(1+interest rate) 1

LoanTerm

LoanTerm

For example, if the rate is 6.0% and the loan has a 30 year term, the mortgage payment factor is given by:

360

360

6% 6%(1+ )12 12 0.005996

6%(1+ ) 112

And we multiply the mortgage payment factor by the original loan balance to get the monthly payment. For example, if the original loan balance is $100,000 then the monthly payment, in this case, is $599.55.

Mortgage Payment Factor Loan Balance $100,000 Rate (per annum) 6.0% Rate (per month) 0.5% Loan Term (Yrs) 30 Loan Term (Months) 360 Payment factor 0.5996% Monthly Payment $599.55 Excel = PMT() $599.55

Calculate the static cash flow yield of a MBS using bond equivalent yield (BEY) and determine the associated nominal spread.

The yield on a mortgage-backed security (MBS) is called cash flow yield.

The main problem in calculating the cash flow yield is that cash flows are uncertain because of prepayments. Therefore, the calculation of cash flow yield assumes a prepayment rate.

30

Nominal Spread

Conventionally, the yield of a mortgage-backed security is compared to that of a Treasury coupon security.

1. Calculate to MBS’s bond equivalent yield (BEY)

The following formula annualizes the monthly cash flow yield (mortgage yield) for an MBS.

6

2 1 112

miBEY

Note that in case of a Treasury coupon security, the BEY is calculated by doubling the semi-annual yield. However, in case of the MBS, the cash flows typically occur monthly. Using BEY makes the yield of an MBS comparable.

2. Calculate the nominal spread

The second step is to compare the computed cash flow yield to a comparable Treasury security. Comparable can be defined as a Treasury security that has maturity equivalent to the average maturity of the MBS. The nominal spread will be the difference between the two yields.

Nominal Spread = Cash flow yield of MBS – Yield of comparable Treasury security.

Nominal spreads are the most commonly used convention to quote mortgage-backed securities.

One problem is that the nominal spread does not substantially account for the prepayment risk in tranches. Therefore, it is difficult for an investor to evaluate an MBS solely on the basis of nominal spread.

Z-spread

An alternative to nominal spread is the Z-spread.

Z-spread is a more accurate measure because it measures the spread that an investor would realize over the entire Treasury spot curve rather than off one point on the Treasury curve.

However, both nominal spread and Z-spread have the weakness that they don’t appropriately account for prepayment risk.

31

Describe the steps for valuing a mortgage security using Monte Carlo methodology.

The valuation of MBS using Monte Carlo simulation involves generating a set of cash flows based on the simulated mortgage rates. This also requires creating payment vectors for each interest rate path.

Let’s look at the steps involved in valuing MBS using Monte Carlo simulation:

Step 1: Simulate short-term interest rate and refinancing rate paths

The first step is to simulate interest rates (monthly) over the remaining life of the mortgage security. So for a new security with 30 years of life, the interest rates will be simulated for 360 months.

A large number of interest paths (N paths) will be generated depending on the requirement of the model. Each path is called a trial.

A typical model uses the term structure of interest rates to simulate interest rates. Some models use Libor curve instead of Treasury curve.

The model also makes an assumption about the volatility. Volatility determines how dispersed are the future interest rates.

These short-term interest rate paths are used: o To generate the prepayment path or vector, and therefore the cash flows. This

is determined by the refinancing rate available at each point in time. If refinancing rate is higher than the coupon, there is less incentive to refinance, and vice verse.

o To discount the future cash flows of the mortgage security to calculate its present value.

An assumption is made about the relationship between the refinancing rate and the short-term interest rates.

Step 2: Project the cash flow on each interest rate path

Once we have the interest rate paths, the next step is to generate the cash flows for each path.

Cash flow per month = Scheduled principal + Net interest + Pre-payments

Scheduled principal and interest payments: Calculated based on the projected mortgage balance in the prior month.

Prepayments: The prepayments for each month are determined using a prepayment model. In theory, there is a prepayment rate associate with each month for each interest rate path. Assuming a constant prepayment rate is incorrect.

32

Once we have the cash flows for the deal’s collateral are generated, the cash flows for the tranches in the MBS deal can be generated based on the payment rules of the structure.

Step 3: Determine the present value of cash flows on each path

The third step is to calculate the present value of these cash flows on each interest rate path.

The discount rate used is the simulated spot rate on each interest rate path plus a spread. These spot rates can be calculated using the future 1-month interest rates.

��(�)= {[1+ ��(�)][1+ ��(�)]⋯ [1+ ��(�)]}��� − 1

Where,

��(�)= Simulated spot rate for month T on path n

��(�)= Simulated future 1-month rate for month I on path n

Using this formula, the interest rate path for future 1-month rates can be converted into the path for monthly spot rates.

The present value of each cash flow on a path can be calculated using the following formula:

��[��(�)]=��(�)

[1+ ��(�)+ �]�

Where,

��[��(�)]= PV of cash flow for month T on path n

��(�)= Cash flow for month T on path n

��(�)=Sport rate for month T on path n

� =Spread

The present value for a full path will be the sum of present values of all cash flows on the path.

��[���ℎ(�)]= ��[��(�)+ ��(�)+ ⋯ + ����(�)]

33

Step 4: Calculate the theoretical value of mortgage security.

Once we have the present values of cash flows for each path, the value of the mortgage security will be the average of these present values for all interest rate paths.

����� =��[���ℎ(1)]+ ��[���ℎ(2)]+ ⋯ + ��[���ℎ(�)]

�

Where n is the number of interest rate paths.

Define and interpret option-adjusted spread (OAS), zero-volatility OAS, and option cost.

Option-adjusted Spread

While calculating the present value of cash flows for each month, we added the spread K to the spot rate for the month. This is the option-adjusted spread (OAS) if it makes the present values of paths equal to the observed market price. OAS satisfies the following condition

����������� =��[���ℎ(1)]+ ��[���ℎ(2)]+ ⋯ + ��[���ℎ(�)]

�

Interpreting OAS

OAS helps investors by helping them identify securities that have greater value than their price.

Investors can use the OAS of a similar security to calculate the theoretical value of the bond, and compare it to the market price of the security to know if it’s trading cheaper.

Alternatively, investors can use the OAS generated from the market price and compare it to a benchmark or similar security to judge whether it’s a worthwhile investment.

Note that OAS is measuring the average spread over the Treasury forward curve, not the Treasury yield curve.

OAS is a superior measure compared to nominal spread and Z-spread as it considers the borrower’s option to prepay.

Zero-volatility OAS

Zero-volatility OAS is obtained in the same way as the OAS except that it assumes zero volatility. So, only the base case interest rate path is used to calculate the OAS. This is used to determine the implied cost of the option embedded in the MBS.

34

Option Cost

Option cost is a measure of the prepayment risk in an MBS. It is calculated using the following formula:

OptionCost=Zero-volatilityOAS − OAS

Option cost can be used as a proxy for the annual cost of hedging the optionality. The cost is directly related to volatility, if volatility reduces, the option cost declines.

Explain how to select the number of interest rate paths in Monte Carlo analysis.

A typical model might involve generating 256 to 1024 interest rate paths. The number of interest rate paths used determines how good an estimate is. However it is not computationally possible to generate a very large number of paths. What we need is an optimal number of paths that provide us a good estimate will minimum variance.

Variance Reduction Techniques

Most models employ variance reduction techniques that help in cutting down the number of sample paths necessary to get a good statistical sample.

Using a variance reduction technique, one can obtain prices estimate within one tick. What this means is that even the model generates more scenarios the price estimates will not differ by more than one tick.

Principal Component Analysis

Some vendor firms have developed procedures that drastically cut down the number of paths but still provide quite accurate results.

One such procedure is to reduce the number of paths by specifying representative paths that represent similar paths.

For example, using Principal Component Analysis, 1024 sample paths can be represented by, say, just 16 different paths. Each of these representative paths will have a different weight depending on how many sample paths it represents. The value of the security will then be the weighted average of these 16 paths.

35

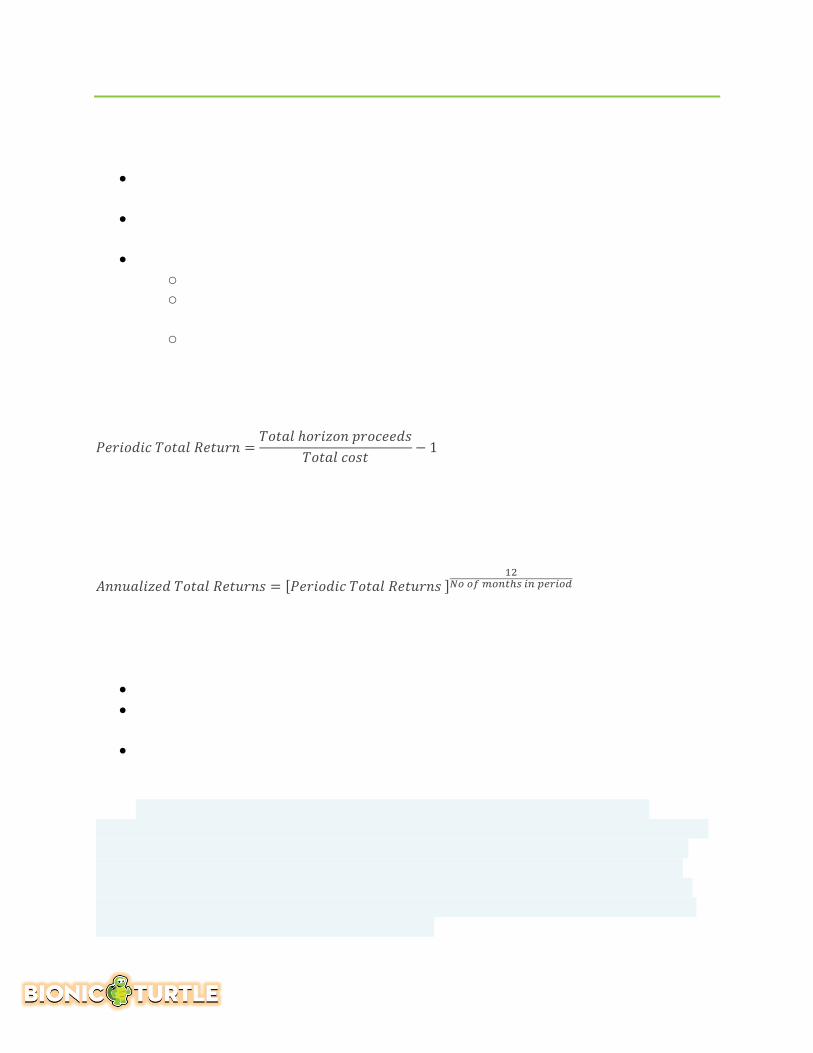

Describe total return analysis, calculate total return, and understand factors present in more sophisticated models.

Monte Carlo simulation and OAS assume that the investor holds the security until maturity. But this may not always be true, as investors have their own horizon.

Total Return Analysis allows investors to evaluate the returns on a security for different investment horizons and interest rate scenarios.

The total returns from an MBS are characterized by the following parameters: o Cost of security at the time of purchase o Security’s projected cash flows (schedules principal payments, interest,

prepayments, and reinvestment income) o Security’s projected value at the horizon date

Example

The total return over a 6-month horizon is calculated using the following formula:

������������������� =�����ℎ��������������

���������− 1

Since these returns are for a 6-month period, the annual returns will be calculated by multiplying them by 2.

Generalized

���������������������� = [��������������������]��

������������������

Factors present in more sophisticated models

In reality, the total return analysis models are highly sophisticated and incorporate many factors:

Models allow returns can be generated in multiple interest rate scenarios. Models allow greater flexibility in generating the inputs. For example, valuation and

prepayment models are utilized to generate horizon price and prepayment rates. The models allow the users to specify when the rate shift happens (immediately, at

horizon, or gradually over time). Culp: “A typical single-name CDS functions almost exactly the same way as credit insurance or a financial guarantee. The credit protection purchaser makes a fixed payment (or a series of fixed payments over time) to the credit protection seller in exchange for a contingent payment upon the occurrence of an event of default by a specific obligation called the reference asset. If the triggering event of default occurs, the credit protection seller makes a cash payment to the protection buyer equal to the par/notional amount of the reference asset minus the expected recovery.”

36

Servigny, Chapter 3: Default Risk: Quantitative Methodologies. Describe the Merton model for corporate security pricing,

including its assumptions, strengths and weaknesses.

Notation:

F = value of debt (as in Face value) S = value of equity (as in Stock) V = value of firm

Under simple (two-class) capital structure, Value of the firm (V) = Value of the debt (F) plus (+) Value of the equity (S) The key insight of Merton model is that equity (shareholders’ claims) is a call option on the firm’s assets. Merton treats the equity claim as a call option on the firm. If the equity holders payoff the debt (i.e., the debt is the exercise price), then they have “exercised” their option and they own the entire firm. But if firm’s assets fall below the value of the debt (or strike price), shareholders essentially hold an “underwater option.”

The value of equity = value of firm’s assets (V) – value of risky debt The value of risky debt = Riskfree debt – put option on firm

The Merton Model’s restrictive assumptions

Simple capital structure: one class of equity + one zero-coupon bond

Value of firm can be observed Value follows a lognormal diffusion

process

Default only occurs at maturity Riskless interest rates are constant Debt is not renegotiated No liquidity adjustment

Capital Structure

Debt(priorclaim)

Equity(residual)

37

Using the Merton model, calculate the value of a firm's debt and equity and the volatility of firm value.

The Merton model for credit treats equity as a call option on the firm’s assets. Under this approach, the value of the equity at date (t) is a function of the value of the firm (V), the face value of the debt (K) and the volatility of the value of the firm ():

( )

2

V N k T t ( )

1log

2

r T tt t V

t V

V

S Ke N k

V K r T t

kT t

Please note this is the same Black-Scholes Merton option pricing model that is reviewed in the Hull assignment; merely the notation is different. Specifically, k = d2.

The Merton model for credit risk has two steps:

(The following breakdown of Merton first appeared in David’s Notebook on our forum at: http://www.bionicturtle.com/forum/threads/merton-model-a-summary-of-the-issues.5646/)

1. Use the Black-Scholes-Merton option-pricing model (BSM OPM) to estimate the price (value) of the firm's equity

2. Using the firm's equity value to assume the firm's asset value and asset volatility, estimate the probability of default (PD) under an assumption that the firm's asset price will follow a lognormal distribution

What’s the role of Black-Sholes-Merton (BSM), here in Merton for credit risk?

The Black-Scholes OPM solves for a European call option = S(0)*N(d1) - K*exp(-rT)*N(d2).

1. BSM OPM is directly applied only in the first step, to get the firm's equity value (and maybe to get the firm's debt)

2. In the second step, N(-d2) is used to estimate PD. It is the same d2, but with one key difference: The riskfree rate (r) in BSM is replaced with a real/physical firm drift (mu). This step uses a component of BSM, so it looks like BSM, but this step is NOT option-pricing at all. It is a simple statistical calculation. Again, N(-d2) is the analog to PD, except real asset drift replaces riskfree rate.

38

What are the two steps, in more detail?

Step 1 (derivatives valuation): price firm equity like a call option

The first step above employs the BSM OPM precisely because its central insight is to treat the firm's equity as a call option on the firm's assets. In this way:

S(0) is replaced by today's firm asset value, V(0), where V(0) = D(0) + E(0); i.e., S(0) in BSM replaced by --> V(0) in Merton

The face value of all debt (not "default threshold" here, that's step 2) replaces the strike price; it's total face value of debt because that is the "strike" that must be paid to retire debt and own the firm's assets. i.e., K or X in BSM replaced by --> F(t) in Merton

We retain the risk-free rate (r) in this step, we do not use the firm's (asset's) expected return. This is theoretically significant: by employing BSM to price equity as a call option, we rely on the brilliant risk-neutral valuation idea, which requires the risk-free rate as the option payoff can be synthesized with riskless certainty. i.e., riskfree rate (r) in BSM is retained in Merton

Summary Step 1:

The Familiar BSM OPM which prices a call option on asset: c(0) = S(0)*N(d1) - K*exp(-rT)*N(d2), is re-purposed to:

Price the firm's equity as if it were an option (strike = debt face value) on firm's assets: E(0) = V(0)*N(d1) - F(t)*exp(-rT)*N(d2)

Two details associated with the first step, that can be skipped

1b. Less important, for FRM exam purposes, is that we solve for both equity value (which informs asset value) and firm asset volatility. The full first step is a simultaneous solution of two equations in two unknowns which produces an assumption for the capital structure (MV of debt + MV of equity = MV of assets) for the firm and the firm's asset volatility. This will not matter in the FRM, it is too tedious. You will instead just be given the assumptions for firm (asset) value and firm (asset) volatility.

1c. More important is that a similar option-based insight can be used to price the value of the firm's debt: the value of the firm's "risky" debt = risk-free debt - put option on firm's assets with strike equal to same face value of debt, where risk-free debt is face value of debt discounted at the risk-free rate.

39

Step 2 (risk measurement): PD = N(-DD)

An FRM P2 candidate should try to understand the relatively simple intuition of this step, which is not option pricing, it is just statistics. Using de Servigny's numbers.

From left-to-right:

Assume current price of assets (i.e., firm value), V(0) = $12.75 Assume assets drift at a rate of mu = +5% per annum At the end of the period, firm will have an expected future value higher than today,

due to positive drift. In this case, V(t) = ~ $13.34 Assume a future distribution, same assumption we use for equities: log returns are

normal --> future prices are lognormal If we are going to make a normal/lognormal assumption, we can treat either, but it

is easier to treat the normal log returns. Our expected future firm value is +28.8% standard deviations above the default threshold = LN(13.34/10) = 28.8%. As our asset volatility is 9.6%, the implies our expected future firm value will be +3 sigma above the default threshold of $10. This final step merely produces a standard normal (Z) variable: LN(13.34/10)/9.6% sigma = Z of ~ 3.0 where 3.0 is the (standardized) distance to default

Under this series of unrealistic assumptions, future insolvency is characterized by a future firm value that is lower than the default threshold of $10; i.e., the area in the tail: PD = N(-DD) = N(-3.0) ~= 0.13%

40

That's Step 2 and the Merton model. Two related ideas:

Risk-free rate (r) vs. asset drift (mu): In BSM, N(d2) = risk-neutral Prob[option expires ITM] and in Merton N(-DD) = risk-neutral Prob[Insolvency; i.e., Asset expires OTM]. BSM risk-neutral d2 = (LN[S(0)/K] + [r - sigma^2/2]*T)/[sigma*SQRT(T)], but Merton's step 2 wants real-world DD = (LN[V(0)/F(t)] + [mu - sigma^2/2]*T)/[sigma*SQRT(T)]

The usage of risk-free rate (r) in the first step and asset drift (mu) in the second step nicely illustrates Jorion's introductory (Chapter 1) distinction between derivatives pricing versus risk measurement. The 1st step above is derivatives pricing. The 2nd step is risk measurement, which he contrasts in five dimensions: 1. distribution of future values, 2. focused on the tail of the distribution [instead of the center, as in step one], 3. Future value horizon, 4. Requires LESS PRECISION (i.e., approximation), and 5. utilizing an ACTUAL (physical) distribution, rather than a risk-neutral

Variation #1: lognormal prices instead of the more familiar normal log returns

The more typical approach, above, derives a standard normal Z deviate by assuming log returns are normally distributed: if LN(S2/S1) is normal then S2 is lognormal. As such, the more typical distance-to-default above produced a standardized normal return-based DD of 3.0 = 28.8% continuous return / 9.6% per annum volatility. In BSM, the numerator of d2 is a continuous return, standardized by dividing by the annualized volatility in the denominator, to give a unitless standard normal deviate.

Alternatively, the distance of default can be expressed as a function of the dollar difference between the future firm asset value and the threshold, in this case: $13.34 - $10 = $3.34. And then standardize that by dividing by the volatility to get the alternative distance to default:

Lognormal price-based Distance to default (DD) = [V(t) - Default]/[sigma*V(t)] = ($13.34 - $10) / (9.6% * $13.34) = 2.607 This price-based lognormal DD of 2.607 is equivalent to the return-based normal DD of 3.0 (normal log returns --> lognormal prices). See row 31 of XLS 6.c.1. for dynamic translation/proof.

41

With respect to the exam (I can't judge the testability of any of this, GARP has been uneven here, overall testability may well be low):

The historical/sample FRM questions tend to query the lognormal price-based DD maybe because it's a shorter formula: [$V(t) - $DefaultPoint]/[sigma*$V(t)]. You'll notice you can't easily retrieve the inverse lognormal CDF, so naturally this sort of questions only asks you the DD and stops short of asking for the PD.

You can confirm with an understanding of the above that this formula wants: Expected future asset value (end of period equity + debt), and The dollar volatility of V(t) is more correct than dollar volatility today [i.e.,

sigma*V(0)] but either is okay. In the simple two-class Merton, MV equity + MV debt = MV of firm assets, V(0) or V(t)

... and debt directly informs the default threshold ... but, otherwise, this DD is entirely a function of firm assets, not equity: asset value today, V(0), drifting at the asset return (mu) to the future expected asset value, V(t), subject to asset volatility, sigma(asset).

Variation #2: KMV (Merton but with two adjustments)

The two steps above illustrate the Merton as (i) assuming the firm will default upon insolvency, asset(t) < face value of all debt(t) and (ii) inferring the area in insolvency tail as a function of a normal return (lognormal price) asset distribution. The KMV method, who I consulted to years ago, recognizes and addresses these two unrealistic assumptions:

1. First, debt consists of short-term obligations (including the short-term portion of long-term debt) and long-term debt. A firm has more time to recover with respect to the long-term debt. KMV's research led it to conclude that the default threshold point is really somewhere in between the short-term debt and the total debt. So, if LT/ST < 1.5, the default threshold = short-term debt + 0.5 * long-term debt.

2. Second, as discussed above, the use of PD = N(-DD) assumes the asset log returns are normally distributed. Let me restate that in, I think, a more meaningful way: by using only the asset volatility, the Merton model tacitly assumes a lognormal distribution of the asset value. As always, this is probably incredibly unrealistic. So, rather than derivate the PD parametrically (i.e., inferring PD as the area under a parametric [lognormal] distribution), KMV resorts to history. Their historical database contains actual firms and their default rates; by back-computing the historical distance-to-defaults, they have a historical correspondence (mapping) of DDs and the actual default rates. For example, whereas parametric normal/lognormal tells us (above) that + 3.0 DD = 0.13% PD (area in the tail), maybe their database shows that +3.0 DD corresponds more nearly to a 0.42% default rate. So, this is a historical empirical translation of DD into PD.

42

In summary, KMV applies Merton (is Merton-based) through 1.5 of the two steps, but abandons the PD = N(-DD) in favor of PD = historical default rate corresponding to DD. Also, KMV tweaks the default threshold from total face value of debt (Merton) to all short-term plus some fraction of long-term debt.

Define the following terms related to default and recovery: default events, probability of default, credit exposure, and loss given default.

Default

Default is failure to pay a financial obligation. Default events include distressed exchanges, in which the creditor receives securities with lower value or an amount of cash less than par in exchange for the original debt. An alternative definition of default is a Merton-type (structural) view of the firm’s

balance sheet: default occurs when the value of the assets drops below the value of the debt, such that equity is reduced to zero or below zero.

Impairment is a weaker accounting concept from the lender’s point of view; a credit can be impaired without default, in which case it is permissible to write down its value and reduce reported earnings by that amount.

According to Malz, “In practice, firms generally file for bankruptcy protection well before their equity is reduced to zero. During bankruptcy, the creditors are prevented from suing the bankrupt debtor to collect what is owed them, and the obligor is allowed to continue business. At the end of the bankruptcy process, the debt is extinguished or discharged. There are a very few exceptions.”

43

Probability of Default

The probability of default is defined over a given time horizon (�); e.g., one year. Each credit has a random default time (t*). The probability of default (p) is the probability of the event (t*) occurs on or before (t); i.e., t* ≤ �. We distinguish three points of time:

The time (t) from which we are viewing default, which is typically “now” or “current” or “initial time;” that is, when t = 0. However, in some cases, we want to think about default probabilities viewed from a future date.

The time interval over which default probabilities are measured: If the perspective time is t = 0, this interval begins at the present time and ends at some future date T, with t = T - 0 = T the length of the time interval. But it may also be a future time interval, with a beginning time T1 and ending time T2,so t = T1 - T2. The probability of default will depend on the length of the time horizon as well as on the perspective time.

The time (t*) at which default occurs. In modeling, this is a random variable, rather than a parameter that we choose.

Credit Exposure

The exposure at default is the amount of money the lender can potentially lose in a default. Exposure can be straightforward (e.g., par or market value of a bond) or a more difficult to ascertain (e.g., the net present value, NPV, of an interest-rate swap contract).

Loss Given Default

When default occurs, in general the creditor does not lose the entire amount of the exposure. The firm’s assets probably have some non-zero value. The firm may be unwound, and the assets sold off, or the firm may be reorganized, so that its assets continue to operate. The loss given default (LGD) is the amount the creditor loses in the event of a default. Exposure is the sum of recovery and loss given default (LGD):

Exposure = Recovery + LGD Recovery is usually expressed as a recovery rate R, a decimal value on [0, 1]:

recoveryrecovery rate(%) =R= 1

exposure exposure

LGD

44

In principle, loss given default (LGD) and recovery are random variables (“random quantities”). As random variables, LGD and recovery (r) create two problems:

1. The uncertainty about LGD makes it more difficult to estimate credit risk 2. The LGD is likely to be correlated with the default probability (PD; aka, EDF) which

adds “an additional layer of modeling difficulty.” In many cases, expected loss (EL) is given as the product of default probability and LGD, but this assumes that LGD is independent of PD.

Recovery rate

The recovery rate can be defined as:

A percent (%) of the current value of an equivalent risk-free bond (recovery of Treasury),

A percent (%) of the market value (recovery of market), or A percent of the face value (recovery of face) of the obligation.