Embed Size (px)

Citation preview

Presenting a live 110‐minute teleconference with interactive Q&A

Form 990‐PF: Latest Compliance Strategies Meeting IRS Demands for Fiscal, Grant and Other Data From Private Foundations

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

WEDNESDAY, FEBRUARY 22, 2012

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Amanda Adams Tax Partner Blazek & Vetterling HoustonAmanda Adams, Tax Partner, Blazek & Vetterling, Houston

Brian Yacker, Partner, YH Advisors, Huntington Beach, Calif.

Milton Cerny, Counsel, McGuire Woods, Washington, D.C.

Candice Meth, Senior Manager, EisnerAmper, New York

For this program, attendees must listen to the audio over the telephone.

Candice Meth, Senior Manager, EisnerAmper, New York

Please refer to the instructions emailed to the registrant for the dial-in information.Attendees can still view the presentation slides online. If you have any questions, pleasecontact Customer Service at1-800-926-7926 ext. 10.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY

Attendees must listen to the audio over the telephone. Attendees can still view the presentation slides online but there is no online audio for this program.

Attendees must stay on the line for at least 100 minutes in order to qualify for a full 2 credits of CPE. Attendance is monitored as required by NASBA.

Please refer to the instructions emailed to the registrant for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.at 1 800 926 7926 ext. 10.

Tips for Optimal Quality

S d Q litSound Quality

For this program, you must listen via the telephone by dialing 1-866-873-1442and entering your PIN when prompted. There will be no sound over the web connection.co ect o .

If you dialed in and have any difficulties during the call, press *0 for assistance. You may also send us a chat or e-mail [email protected] immediately so we can address the problem.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

F PF L t t C li Form 990‐PF: Latest Compliance Strategies Seminar

Feb. 22, 2012

Brian Yacker, YH [email protected]

Amanda Adams, Blazek & [email protected]

Candice Meth, [email protected]

Milton Cerny, McGuire Woods [email protected]

Today’s Program

Form 990-PF Review[Amanda Adams]

Slide 7 – Slide 27

Calculating Minimum Distribution[Brian Yacker]

Slide 28 – Slide 34

Critical Compliance Challenges With Form 990-PF[Amanda Adams, Brian Yacker and Milton Cerny]

Slide 35 – Slide 74

Preparing For Future Form 990-PF Filings: Best Practices[Candice Meth]

Slide 75 – Slide 91

FORM 990 PF REVIEWAmanda Adams, Blazek & Vetterling

FORM 990‐PF REVIEW

Part I: Analysis Of Revenue And Expenses

Column (a) reflects revenue and expenses per books – cash or accrual.

Column (b) reflects revenue and expenses that are subject to the §4940 excise tax on net investment income. More about this calculation to come later.

Column (c) reflects revenue and expenses that are included in the calculation of adjusted net income. For private operating foundations, this column is relevant to determining the spending requirement. For non-operating foundations, this column is generally not completed unless the foundation has income from a charitable activity.

Column (d) reflects expenses which are treated as qualifying distributions. This column is relevant to determining satisfaction of both operating and non-operating foundations’ minimum spending requirements.

8

P II B l ShPart II: Balance Sheets

This section of the return presents the balance sheet of the foundation at the beginning and the end of the year. The FMV of assets held at the end of the year also is reported. A detailed listing of investments held at the end of the year (other than mortgage loans) is required.

Lines 6 and 20 report receivables/payables occurring between the foundation and disqualified persons. Having an entry on either of h li ld b i h i i ibl lf d li h these lines could be a sign that impermissible self-dealing has

occurred.

9

Part III: Analysis Of Changes In NA Or FB

This section of the return demonstrates the components of the change in net assets from the beginning of the year to the end of the year. For many cash-basis foundations, current income is the only change. For foundations that follow the accrual method and report their investments at fair market value, unrealized gains and losses are reported here. Returned grants are also reported in a d losses a e epo ted e e. etu ed g a ts a e also epo ted this section rather than as a reduction of expense or income in Part I.

10

P IV C i l G i A d LPart IV: Capital Gains And Losses

After the passage of the Pension Protection Act of 2006 capital After the passage of the Pension Protection Act of 2006, capital gains and losses from the sale of virtually all capital assets became subject to the §4940 tax on net investment income. Two i t t ti till i timportant exceptions still exist:

1. Capital gains and losses subject to unrelated business income tax are not also subject to §4940 tax.

2. Gains and losses from charitable-use assets held for at least one year are not subject to §4940 tax, if the proceeds from sale are used to purchase similar charitable-use assets similar to the are used to purchase similar charitable use assets similar to the like-kind exchange rules of §1031.

Remember that all sales of publicly traded securities can be t d i gl li D t il l i d f reported on a single line. Details are only required for non-

publicly traded securities.11

Part V: Qualification For Reduced Tax

The normal rate of §4940 tax on net investment income is 2%. This section of the return provides a calculation that may enable the foundation to reduce the tax percentage to 1%. A ratio of qualifying distributions to non-charitable-use assets is calculated based on a five-year history. If current-year qualifying distributions equal or exceed the amount determined by d st but o s equal o e ceed t e a ou t dete ed by multiplying the five-year ratio by the current year’s average of non-charitable-use assets plus 1% of net investment income, then the foundation qualifies for the 1% tax rate for the yearthe foundation qualifies for the 1% tax rate for the year.

Planning tips for reaching the 1% rate will follow later in the presentation.

12

P VI E i TPart VI: Excise Tax

This section reports the tax due on the return as well as any payments made towards the tax. If the foundation was erroneously subject to backup withholding, such amounts can be reported here as credits toward the foundation’s tax liability.

Foundations whose tax liability exceeds $500 for the year must Foundations whose tax liability exceeds $500 for the year must make quarterly tax payments (must deposit electronically). Those whose net investment income has exceeded $1 million in the past h b h i 2 d 4th i three years must base their 2nd – 4th quarter payments using

annualization calculations, which use actual income earned during the year. This can be problematic for those foundations with partnership investments on which they lack timely information.

13

Part VII‐A: Statements Regarding Activities

Although questions 1(political activities) 6 (governing instrument) and 13 Although questions 1(political activities), 6 (governing instrument) and 13 (public inspection) search for possible non-compliance with the requirements of §501(c)(3), the bulk of the questions in this part ask for information that does not necessarily have a negative impact on the information that does not necessarily have a negative impact on the foundation. Changes in activities, organizing documents, new substantial contributors and similar information is required to be reported.

A new question is asked for 2011: Did the foundation make a distribution A new question is asked for 2011: Did the foundation make a distribution to a donor-advised fund over which the foundation or a disqualified person had advisory privileges? If “Yes,” attach a statement.

The statement must report whether the foundation treated the The statement must report whether the foundation treated the distribution as a qualifying distribution and how the distribution will be used for §170(c)(2) purposes.

One wonders whether the IRS plans to restrict grants to DAFs, as they One wonders whether the IRS plans to restrict grants to DAFs, as they have grants to supporting organizations.

14

Part VII‐B: Statements Regarding ActivitiesFor Which Form 4720 May Be Required

Care should be taken in answering the questions in this section, as “Yes” answers may indicate that Form 4720 (a penalty return) is required to be filed. Questions 1-5 seek information to determine if the foundation is subject to one of the Chap. 42 excise taxes on self-dealing, under-distribution, excess business holdings, jeopardizing investments and taxable expenditures. Questions 6 jeopa d g vest e ts a d ta able e pe d tu es. Quest o s 6 and 7 relate to non-Chap. 42 excise taxes.

15

Part VIII: Information About Officers, Etc.

All officers, directors, trustees and foundation managers who served during the year are reported, along with their compensation and average hours per week devoted to the foundation.

The top five highest paid employees compensated >$50 000 are The top five highest-paid employees compensated >$50,000 are reported.

The top five highest-paid independent contractors compensated >$50,000 are reported.

16

Part IX‐A: Summary Of Direct Charitable Activities

Many foundations conduct direct programs in conjunction with, or rather than, making grants to other organizations. Even if the foundation is a non-operating foundation, it has the opportunity to describe its four largest activities and provide the total expenditures related to each. Some foundations are concerned about the appearance of a large percentage of expenses coming about t e appea a ce o a la ge pe ce tage o e pe ses co g from non-grant sources, because it may seem that administrative expenses are too high. Describing direct activities in this part can help indicate when expenses are related to a charitable program help indicate when expenses are related to a charitable program rather than being administrative.

17

Part IX‐B: Summary Of Program‐Related Investments

Program-related investments are made primarily to accomplish a charitable purpose of the foundation, rather than to produce investment income or capital gain from the sale of the investment.

Examples include educational loans to individuals and lowExamples include educational loans to individuals and low-interest loans to other 501(c)(3) organizations.

Only the top two PRIs made during the year are reported, so that ongoing investments are not reported on succeeding returns.

18

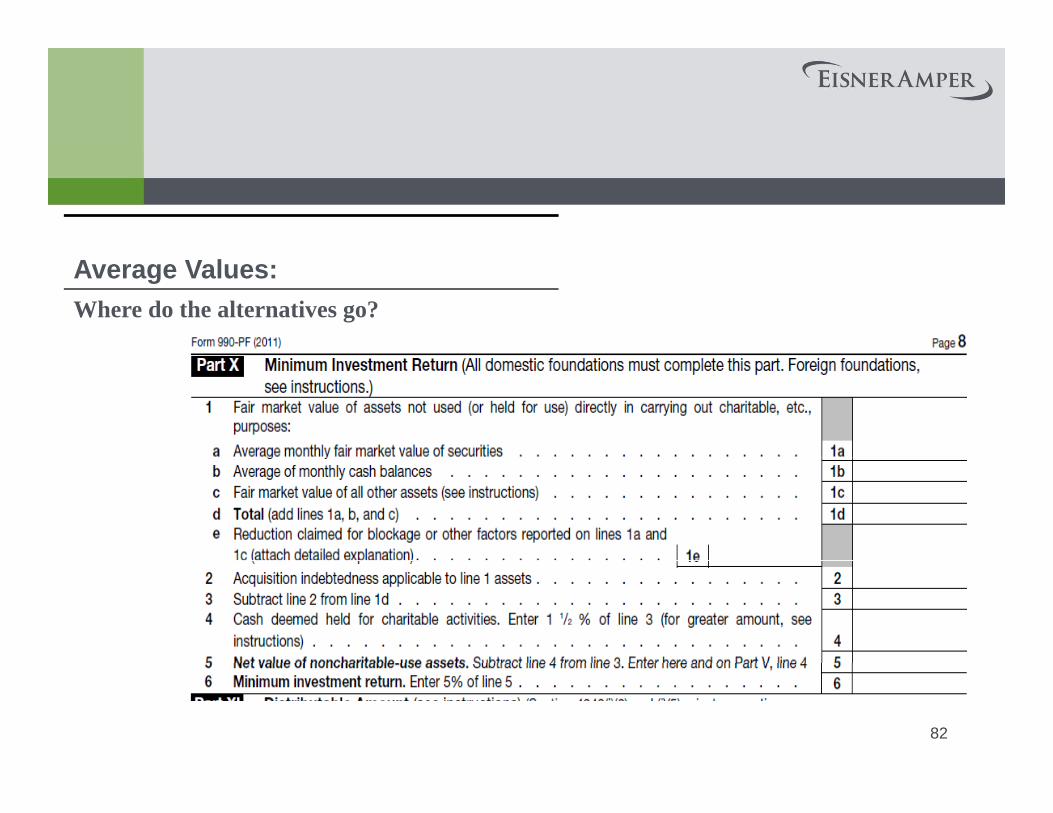

Part X: Minimum Investment Return

This section of the return reports the average fair market value of non-charitable use assets including cash, securities and other assets. This calculation is the first step in determining the amount the foundation is required to spend for charitable purposes. More information on this topic is to follow later.

19

P XI Di ib bl APart XI: Distributable Amount

The minimum investment return (5% of investment assets) is reduced in this section by the excise tax on investment income for the year, as well as the income tax (990-T) for the year. Recoveries of amounts previously treated as qualifying distributions (i.e., returned grants) are added to the MIR to determine the distributable amount.dete e t e d st butable a ou t.

20

P XII Q lif i Di ib iPart XII: Qualifying Distributions

This section calculates the total amount of qualifying distributions for the year by combining the expenses paid from Part I, col. (d) with amounts spent to purchase program-related investments or charitable use assets, and any amounts set-aside for charitable purposes.

Set-asideSet-aside

Type I: Suitability test – straightforward and applicable to foundations of any age; must request in advance and may not

i l il f d dli f b fil dreceive approval until after deadline for return to be filed

Type II: Cash distribution test – generally applicable to foundations in their first few years of existence; complex rules which are difficult to understand; advance approval not required

21

P XIII U di ib d IPart XIII: Undistributed Income

Thi ti ill t t ti f ti f il f ti This section illustrates satisfaction or failure of a non-operating foundation’s payout requirements. It is important to remember that the amount shown on line 6f, col. (d) is not required to be distributed until the tax year after the tax year covered by the return.

Normal ordering of application of distributionsg pp

1. Current-year payout requirement (calculated on prior return)

2. Next year’s payout requirement (calculated on current return)

3. Excess distribution carryover

Elections can be made to divert distributions after Step 1 to satisfy requirements from a prior year (penalty situation) or to y q p y (p y )meet redistribution requirements.

22

Part XIV: Private Operating Foundations

This section illustrates satisfaction of a private operating foundation’s This section illustrates satisfaction of a private operating foundation s payout requirements. The test can be met on an aggregate basis (i.e., total for all four years) or on a three-out-of-four-year basis.

Two-part testTwo-part test

1. Income test (based on lesser of adjusted net income or MIR)

2. One of the following:

I. Asset test (65%+ are charitable-use)

II. Endowment test (spend 2/3 of MIR)

III. Support test (certain required percentages of support from public)

Failure of test means the foundation becomes a non-operating foundation that completes Part XIII.

23

l fPart XV: Supplementary Information

This section provides information about grant programs. A foundation can describe what kinds of organizations/individuals it supports or attempt to forestall submission of unsolicited applications by checking the box.

Details regarding grants paid during the year and those approved Details regarding grants paid during the year and those approved for future payment are presented. Importantly, the public charity status (on the return this is referred to as foundation status) must b d f h [ 509( )(1)]be reported for each grantee [e.g., 509(a)(1)].

24

Part XVI‐A: Analysis Of Income‐Producing Activities

This section analyzes the sources of revenue during the year to show how much revenue was unrelated business income that is taxable, unrelated business income that is not taxable, and related/exempt function income.

25

Part XVI‐B: Relationship Of Activities

For exempt function revenue reported in col. (e) of Part XVI-A, a description is reported in this section explaining how the income-producing activity contributed to the foundation’s exempt purposes.

26

Part XVII: Information Regarding TransfersTo, And Transactions And Relationships , p

With, Non‐Charitable Exempt Organizations

As the title implies, this section reports information about transfers and other transactions with non-charitable exempt organizations as well as relationships with such organizations. It is important to demonstrate that such transactions, etc. do not result in the improper use of charitable funds for non-charitable purposes.pu poses.

27

CALCULATING MINIMUM Brian Yacker, YH Advisors

CALCULATING MINIMUM DISTRIBUTION

Minimum Distribution Requirements (Sect. 4942)

Definitions

o Undistributed income

• Distributable amount exceeds qualifying distributions for any given year.

o Distributable amounto Distributable amount

• Overview

Two years to make qualifying distributions

• Calculation

Essentially, the private foundation’s minimum investment return, with certainadjustments

Private foundation’s grants are returned to the private foundation(§4942(f)(2)(C)(i)).

Amounts received or accrued from the sale of property to the extent that the acquisition of the property was considered a qualifying distribution (§4942(f)(2)(C)(ii))

Any amount set aside for a specific project, to the extent that the y p p j ,amount set aside was not necessary for the purposes for which it was set aside (§4942(f)(2)(C)(iii))

Prepared by YH Advisors, Inc. 29

Minimum Distribution Requirements (Sect. 4942), Cont.

f ( ) Definitions (Cont.)

o Minimum investment return

• 5% of fair market value of non-charitable assets (net total assets less exempt purpose assets)

Examples of exempt-purpose assets

Art owned by private foundation that is displayed in museum Art owned by private foundation that is displayed in museum

Desks in classroom of school operated by private foundation

• Fair market value calculations

Cash

Calculate average monthly cash balances

See regulations (53.4942(a)-2(c)(4)(ii))

Securities

Readily available market quotations

+ NYSE or NASDAQ

+ Any city or regional exchange in which quotations appear on a daily basis

+ Any other exchange (foreign, national, regional) in which quotations appear on a daily basis

+ Regularly traded in a market for which published quotations are available

+ Locally traded in a market for which quotations can be obtained from established brokerage firms

Consistently calculate average monthly fair market value

Marketability discounts permitted (Sect. 4942(e)(2)(B))

See five examples in regulations (53.4942(a)-2(c)(4)(i)(e))

Prepared by YH Advisors, Inc. 30

Minimum Distribution Requirements (Sect. 4942), Cont.

Definitions (Cont.)

o Minimum investment return (Cont.)

• Real estate

Five-year optional reliance, if written appraisal prepared by unrelated (Reg. §53.4942(a)-2(c)(4)(iv))

i ifi d d i d d i l f h f i k l f l Written, certified and independent appraisal of the fair market value of any real estate

Qualified person may not be disqualified person or employee of the private foundation

Commonly accepted valuation methods must be used in making the appraisal

A valuation based upon acceptable methods of valuing property for federal estate tax ill b id d blpurposes will be considered acceptable.

Appraisal must include a closing statement that, in the appraiser’s opinion, the appraised assets were valued according to valuation principles regularly employed in making appraisals of such property, using all reasonable valuation methods.

Private foundation must keep a copy of the independent appraisal for its records.p py p pp

IRS will continue to accept the appraisal for a five-year period even if actual FMV changes.

Planning opportunity: When the FMV of real estate is increasing, the private foundation should utilize the independent appraisal for determining the value of its real estate investments. When it is decreasing, consider obtaining another independent appraisal, even if the five year period has not yet concluded for the original appraisal of the realeven if the five-year period has not yet concluded for the original appraisal of the real estate.

Real estate valuation planning will help the private foundation minimize its minimum distribution requirements, by minimizing the value of total non-charitable assets.

Prepared by YH Advisors, Inc. 31

Minimum Distribution Requirements (Sect. 4942), Cont.

Definitions (Cont.)

o Minimum investment return (Cont.)

• Valuation of other assets

Fair market value consistently determined annually (see Reg. §53.4942(a)-2(c)(4)(iv)(a))

l i b d d b i f d i i id Valuation can be conducted by a private foundation insider.

May be valued as of any day in PF’s tax year, provided that the PF values the asset as ofthat date in all tax years

• Exempt-purpose assets are not considered for the minimum investment return calculation.

Reg §53 4942(a)-2(c)(3): Asset is used directly in carrying out the foundation's exempt purpose only if theReg. §53.4942(a) 2(c)(3): Asset is used directly in carrying out the foundation s exempt purpose only if theasset is actually used by the foundation in the carrying out of the charitable, educational or other similarpurpose that gives rise to the exempt status of the foundation.

Assets held for production of income or for investment are not being used directly incarrying out the foundation's exempt purposes, even though the income from such assets isused to carry out such exempt purposes.

Whether an asset is held for the production of income, rather than used directly to carry out an exempt purpose, is a question of fact.

For example, an office building used for the purpose of providing offices for employees engaged in the management of endowment funds of the foundation is not being used directly by the foundation to carry out its exempt purposes.

When property is used both for exempt and other purposes, if exempt use represents 95% or more of total use, such property shall be considered to be used exclusively for an exempt purpose.

Prepared by YH Advisors, Inc. 32

Minimum Distribution Requirements (Sect. 4942), Cont.

Definitions (Cont.)

o Minimum investment return (Cont.)

• Exempt-purpose assets are not considered for minimum investment returncalculation. (Cont.)

Examples (in the IRS regulations) of assets that are used directly in carrying out exempt purposes:

Administrative assets, such as office equipment and supplies used to the extent they are devoted to and used directly in administration of the foundation's exempt activitiesfoundation's exempt activities

Real estate used by the foundation directly in its exempt activities

Paintings or other works of art owned by the foundation and that are on public display, fixtures and equipment in classrooms, research facilities and

l t d i trelated equipment

Any interest in a functionally related business or in a program-related investment

Property leased by a foundation in carrying out its exempt purposes at no ( i l ) h l f l dcost (or at a nominal rent) to the lessee or for a program-related purpose,

such as the leasing of renovated apartments to low-income tenants at low rent as part of the lessor foundation's program for rehabilitating blighted areas

Prepared by YH Advisors, Inc. 33

Minimum Distribution Requirements (Sect. 4942), Cont.

Definitions (Cont.)

o Minimum investment return (Cont.)

• Reasonable cash balances for administrative expenses (Reg. §53.4942(a)-2(c)(3)(iv))

1.5% of total assets (less exempt-purpose assets)

Exclude 1.5% amount even if greater than average cash balances (seeRev. Rul. 75-392)

May exceed 1 5% amount under certain limited circumstances May exceed 1.5% amount under certain limited circumstances

Attach statement to Form 990-PF

• Short tax years

Minimum investment return percentage is reduced based on the number of days inthe period.

• PLR 9530033

IRS ruled that a private foundation may re-compute its minimum investment returnfor several years, in order to take into account an adjustment to the value of realy , jproperty donated to the foundation.

Prepared by YH Advisors, Inc. 34

Amanda Adams, Blazek & VetterlingBrian Yacker, YH Advisors

CRITICAL COMPLIANCE

Brian Yacker, YH AdvisorsMilton Cerny, McGuire Woods

CHALLENGES WITH FORM 990 PF990‐PF

Disclosing Operational Activities: Part VII‐A, Question 2

Has the foundation engaged in any activities that have not been Has the foundation engaged in any activities that have not been previously reported to the IRS?

1. Generally, any substantially different activities that have not previously been reported (Form 1023 or 990-PF) should be reported here. The foundation will not receive a letter from the IRS approving of such activities as a result. However, it may protect the foundation from retroactive challenges to exempt status by putting the IRS on notice of new activities.

2. Certain new activities require advance approval from the IRS:2. Certain new activities require advance approval from the IRS:

I. Grants to individuals for study, travel, similar purposes

II. Termination of private foundation status through operation as a public charity

36

Disclosing Operational Activities: Part IX‐A – Direct Charitable Activities

The top four programs are reported. Statistical data such as the number of persons served, classes taught, books distributed, etc. enhance the descriptions. The expenses reported include capital expenditures for related assets, but not depreciation. A reasonable and consistent allocation of overhead expenses is permitted.pe tted.

Unless there is significant involvement in the foundation’s grant h i ll d di h i bl programs, they are typically not reported as direct charitable

activities.

This section is critical for private operating foundations.

37

Private Foundation Minimum Qualifying Distributions

Definitions Definitions

o Qualifying distributions (Sect. 4942(g))

• Any amount, including reasonable/necessary administrative expenses, paid toaccomplish charitable purposes; and any amount paid to acquire asset used directlyi i t h it blin carrying out charitable purposes

Expenses incurred directly in carrying out the private foundation’s charitable purposes

Grants and gifts made by the private foundation to qualifying recipients

Exercise expenditure responsibility for grants and gifts made to non-publicExercise expenditure responsibility for grants and gifts made to non publiccharities

NOT including amounts paid to directly or indirectly controlled charitable organizations (seeSect. 4942(g)(1)(A)); or paid to non-functionally integrated, Type III charitable supportorganizations (see also Reg. §53.4942(a)-3(a)(3))

• Acquisition of exempt purpose assets

• Reasonable and necessary administrative expenses (Cont.)

Examples

Expenses attributable to soliciting grants

Expenses related to inspecting determination letter of public charities

NOT expenses related to the management of an investment endowment fund

Prepared by YH Advisors, Inc. 38

Private Foundation Minimum Qualifying Distributions (Cont.)

Definitions (Cont ) Definitions (Cont.)

o Qualifying distributions (Cont.)

• Reasonable and necessary administrative expenses (Cont.)

Internal Revenue Service rulings Internal Revenue Service rulings

Rev. Rul. 75-495: Legal fees paid in a suit to determine the properbeneficiary of part of the private foundation’s income

PLR 9623058: Reasonable legal and accounting expenses incurred by ai t f d ti i bt i i IRS li ith t t t f fprivate foundation in obtaining an IRS ruling with respect to transfer of

assets for purposes of furthering charitable purposes

PLR 9629019: Reasonable and necessary legal, accounting and otherexpenses incurred to implement the transfer of assets from one privatefoundation to another were considered qualifying distributionsfoundation to another were considered qualifying distributions.

Rev. Rul. 74-560: Depreciation expense generally will NOT beconsidered a qualifying distribution.

1988 EO CPE Text

“Other qualifying distributions include expenses attributable tosoliciting grants or contributions to the foundation; preparing Form990-PF … making the return available for public inspection or providingcopies …”

Prepared by YH Advisors, Inc. 39

Private Foundation Minimum Qualifying Distributions (Cont.)

Definitions (Cont.)

o Qualifying distributions (Cont.)

• Reg. §53.4942(a)-3(a)(1)

Amount of a qualifying distribution is equal to the fair market value of the property on the Amount of a qualifying distribution is equal to the fair market value of the property on thedate of distribution.

• Reg. §53.4942(a)-3(a)(8), Example 1

M, a private foundation that uses the calendar year as the taxable year, makes thefollowing payments in 1970: (i) a payment of $44 000 to five employees for conducting afollowing payments in 1970: (i) a payment of $44,000 to five employees for conducting afoundation program of educational grants for research and study; (ii) $20,000 for variousitems of overhead, 10 percent of which is attributable to the activities of the employeesmentioned in payment (i) of this example and the other 90 percent of which is attributableto administrative expenses which were not paid to accomplish any section 170(c)(1) or(2)(B) purpose; and (iii) a $100 000 general purpose grant paid to an educational(2)(B) purpose; and (iii) a $100,000 general purpose grant paid to an educationalinstitution described in section 170(b)(1)(A)(ii) which is not controlled by M or anydisqualified persons with respect to M. Payments (i) and (ii) of this example are qualifyingdistributions to the extent of $46,000 ($44,000 of salaries and 10 percent of the overhead,both of which are reasonable administrative expenses paid to accomplish section 170(c)(1)or (2)(B) purposes) Payment (iii) of this example is also a qualifying distribution since it isor (2)(B) purposes). Payment (iii) of this example is also a qualifying distribution, since it isa contribution for section 170(c)(2)(B) purposes to an organization which is not describedin subparagraph (2)(i)(a) or (b) of this paragraph. The other 90 percent of payment (ii) ofthis example may constitute items of deduction under paragraph (d)(1)(ii) of Section53.4942(a)-2 if such items otherwise qualify.

Prepared by YH Advisors, Inc. 40

Private Foundation Minimum Qualifying Distributions (Cont.)

Definitions (Cont.)

o Qualifying distributions (Cont.)

• PLR 9702040

P i t f d ti ’ dit f t ti f l d t th bli Private foundation’s expenditures for construction of a playground open to the publicfurthered a charitable purpose and thus were qualifying distributions. However,expenditures to install a computer facility whose access was limited to residents of aparticular building did not further charitable purposes.

• PLR 201029040

IRS rules that the fair market value of property to be used by a private foundation (non-operating) to exhibit art and host cooking classes will be a qualifying distribution.

• IRS Information Sheet 2010-0052

Di t ib ti b i t f d ti t i l b LLC t li h h it bl Distribution by a private foundation to a single-member LLC to accomplish charitablepurposes, where the sole member of the LLC is a public charity not controlled by theprivate foundation, is considered to be a qualifying distribution.

• Planning tip

If t di t ib t d i lif i di t ib ti th t f th di t ib ti i th If property distributed is a qualifying distribution, the amount of the distribution is the property's fair market value on the date of distribution. To reduce the excise tax on investment income (e.g. capital gains), the private foundation should make qualifying distributions of appreciated property in lieu of distributing cash.

Prepared by YH Advisors, Inc. 41

Private Foundation Minimum Qualifying Distributions (Cont.)

Short tax years Short tax years

o Rev. Rul. 74-315

• Private foundation that made a valid election to change its accounting period,which resulted in a short taxable year, and that had undistributed income at theend of its prior taxable year must distribute the income before the close of theshort taxable year in order to avoid the taxes imposed by Sect. 4942.

Internal payout ratios Internal payout ratios

o Some larger private foundations look to “smooth” their distributable amounts.

• Coordination with net investment income tax

• Coordination with minimum distribution requirementsCoo d a o u d s u o equ e e s

Prepared by YH Advisors, Inc. 42

Gathering Grant-Making InformationInformation

Grant making requirements under Sect 4945(h) of the IRCGrant-making requirements under Sect. 4945(h) of the IRC• Sect. 4945 prohibits private foundations from making

“taxable expenditures.”• Grants to an individual for travel study, unless it is awarded

on an objective and non-discriminatory basis and approved in advance by the IRSy

• Grants to an organization other than to a public charity or a 509(a)(3), non-functionally integrated ,Type III supporting organization; or an exempt operating foundation described inorganization; or an exempt operating foundation described in Sect. 4940(d)(2)

• Grants to another private foundation, if the foundation i dit ibilit d S t 4945(h)

McGuireWoods LLP | 43CONFIDENTIAL

exercises expenditure responsibility under Sect. 4945(h)

Gathering Grant-Making Information (Cont )(Cont.)

Expenditure responsibility requires:Expenditure responsibility requires:• The grant only be spent for the purpose made.• Foundation receives complete reports on how the funds

t b th twere spent by the grantee.• Conduct of a pre-grant inquiry by the foundation identifying:

• Past history of grantee• Experience of the grantee• Management and activities of the grantee [see

§54.4945(b)(3)]§ ( )( )]• Grants to political subdivisions and certain other

organizations that do not hold a 501(c)(3) status

McGuireWoods LLP | 44CONFIDENTIAL

Gathering Grant-Making Information (Cont )(Cont.)

• Grants to entities under the auto revocation list• Grants to entities under the auto-revocation list• IRS publishes a list of organizations that had federal tax-

exempt status revoked for failure to file annual Form 990 returns for three consecutive yearsreturns for three consecutive years.

• Reinstatement of tax-exempt status • File application for tax exemption

• If it continues to qualify, IRS will issue a new determination letter and indicate on the IRS business master file that it is eligible to receive tax deductible contributions.

• Donors may rely on the new IRS determination and the effective date (usually from the date of the new application). See IRS Notices 2011-43 and 44

McGuireWoods LLP | 45CONFIDENTIAL

Gathering Grant-Making Information (Cont )(Cont.)

International grant-making and expenditure responsibilityC b d t ki• Cross-border grant-making

• Foundation must exercise expenditure responsibility over grants to foreign charities that do not have tax exempt status

bli h it d S t 501( )(3) R R l 74 435as a public charity under Sect. 501(c)(3). Rev. Rul. 74-435. Grants will meet the requirements of Sect. 4945.

Equivalency determinations• Sponsoring organizations of donor-advised funds must

exercise expenditure responsibility over distributions to foreign organizations or be subject to a §4966 excise tax.

• Foundations can make their own equivalency determination, in lieu of obtaining an IRS determination, or by a grantee affidavit or opinion of counsel that grantee meets the

i t f S t 501(C)(3) bli h it SMcGuireWoods LLP | 46

CONFIDENTIAL

requirements of Sect. 501(C)(3) as a public charity. See Rev. Proc. 92-94

Gathering Grant-Making Information (Cont )(Cont.)

Grants from U S private foundations to foreign organizations thatGrants from U.S. private foundations to foreign organizations that do not require expenditure responsibility include:• Good faith efforts by a foundation that the foreign charity is a

Sect 509(a)(1)(2) or (3) type organizationSect. 509(a)(1)(2)- or (3)-type organization• Foreign governments, including instrumentalities and

agencies thereofI t ti l i ti d i t d b ti d• International organizations designated by an executive order under 22 U.S.C. 288. Examples are U.N., UNICEF, UNESCO, World Bank and International Monetary Fund.

McGuireWoods LLP | 47CONFIDENTIAL

Gathering Grant-Making Information (Cont )(Cont.)

Executive Order 13224 prohibits transactions between a foundationExecutive Order 13224 prohibits transactions between a foundation and any foreign organizations or group of individuals, deemed as “terrorist,” listed on the embargoed list of countries by the Treasury Department on foreign asset control.Treasury Department on foreign asset control.

Procedures for making international grants utilizing expenditure responsibility:responsibility:• Pre-grant inquiry• Grant limitations (substantially similar to requirement for

501( )(3) i ti )501(c)(3) organizations)• Grant terms (grantee must agree to submit full and complete

annual reports on how money is spent and comply with grant)

McGuireWoods LLP | 48CONFIDENTIAL

grant)• Grantee reporting capital assets: Two-year rule

Gathering Grant-Making Information (Cont )(Cont.)

• Grantor reporting: Name and address of grantee date• Grantor reporting: Name and address of grantee, date and amount of grant, purpose of the grant, amounts expended by the grantee, whether any portion of grant has been diverted from the purpose of the grant, datehas been diverted from the purpose of the grant, date and verification of grantee reports

• Grantor recordkeeping: Retention of records for IRS• Grantor recordkeeping: Retention of records for IRS review of the agreement, grantor reports, and records of any independent audit or investigation of the grant

McGuireWoods LLP | 49CONFIDENTIAL

T Of S lf D liTypes Of Self‐Dealing

1. Sale between PF (private foundation) and DP (disqualified person)

I. Foundation holds charitable auction and sells item to DP.

II. Foundation makes bad investment; DP wants to buy from ; yfoundation at more than FMV.

III. Foundation manager retires, and PF sells him the car owned by the PF that he used for site visits.y

2. Lease transaction between PF and DP

I. DP leases office space that is larger than needed and sublets space to foundation.space to foundation.

3. Loan between PF and DP

I. Foundation needs $ to make distributions; DP makes loan.

II F d ti l t DP’ b i t bII. Foundation loans money to DP’s business at an above-average interest rate.

50

T Of S lf D li (C )Types Of Self‐Dealing (Cont.)

1. Furnishing of goods, services, or facilities between PF and DP

I. PF provides office space to DP at no charge.

II. DP uses PF’s office supplies.pp

2. Payment of compensation by PF to DP

I. DP receives directors’ fees.

II DP receives payment for serving as PF’s investment managerII. DP receives payment for serving as PF s investment manager.

3. Use of PF’s income or assets by a DP

I. DP uses PF’s deposits in a bank as collateral for a loan.

II. DP uses PF’s accounts with an investment manager to reduce the amount of fees paid on his personal account.

III. PF purchases table at charity gala; DPs and friends attend.

51

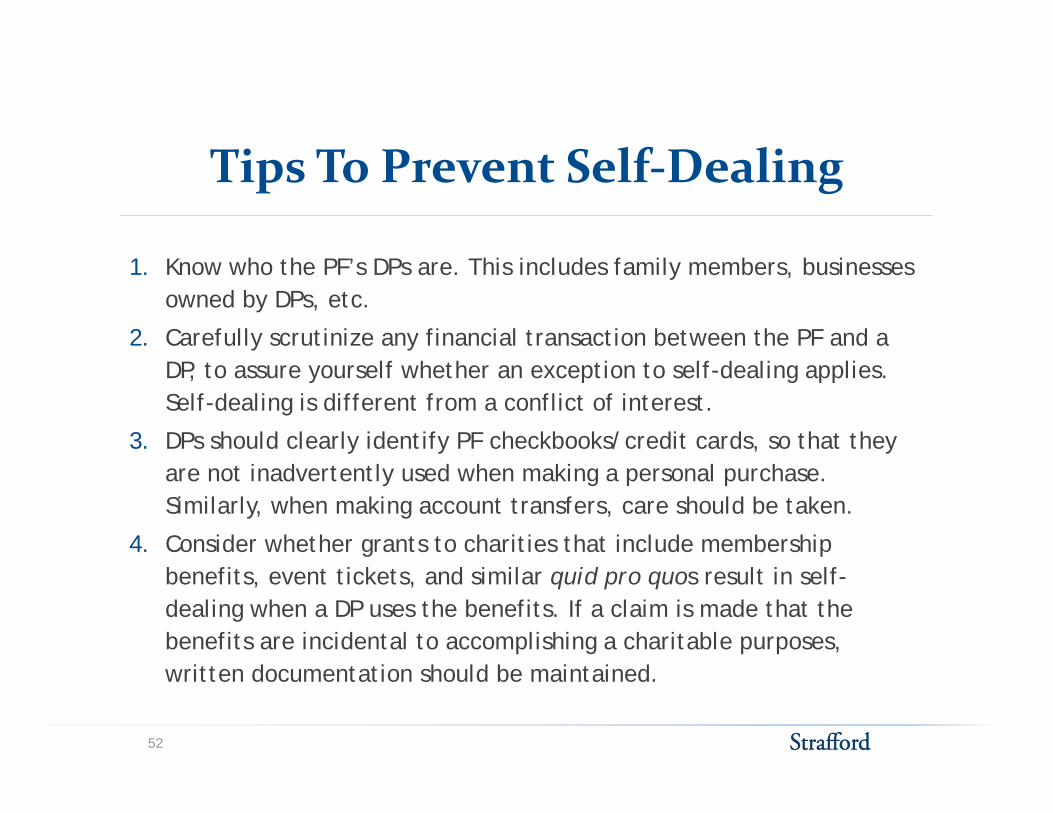

Ti T P S lf D liTips To Prevent Self‐Dealing

1. Know who the PF’s DPs are. This includes family members, businesses owned by DPs, etc.

2. Carefully scrutinize any financial transaction between the PF and a DP, to assure yourself whether an exception to self-dealing applies. Self-dealing is different from a conflict of interest.

3. DPs should clearly identify PF checkbooks/credit cards, so that they are not inadvertently used when making a personal purchase. Similarly, when making account transfers, care should be taken.

4. Consider whether grants to charities that include membership benefits, event tickets, and similar quid pro quos result in self-dealing when a DP uses the benefits. If a claim is made that the benefits are incidental to accomplishing a charitable purposes, written documentation should be maintained.

52

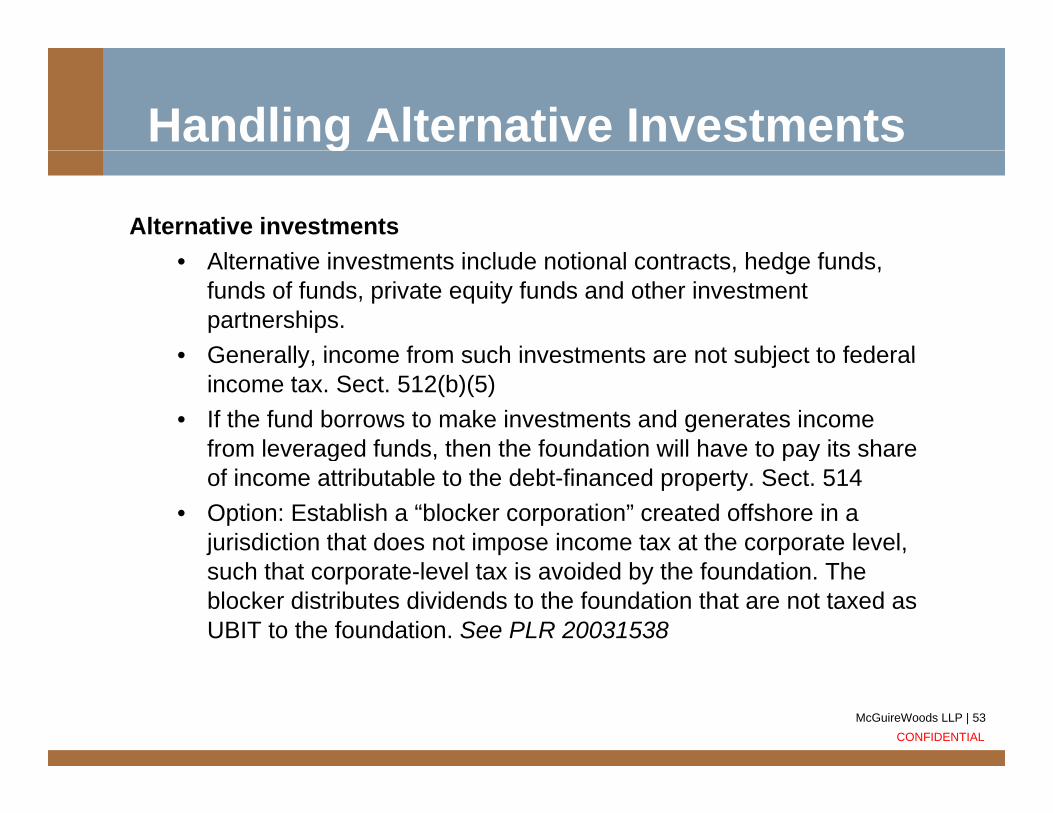

Handling Alternative Investmentsg

Alternative investmentsAlt ti i t t i l d ti l t t h d f d• Alternative investments include notional contracts, hedge funds, funds of funds, private equity funds and other investment partnerships.

• Generally income from such investments are not subject to federal• Generally, income from such investments are not subject to federal income tax. Sect. 512(b)(5)

• If the fund borrows to make investments and generates income from leveraged funds, then the foundation will have to pay its share g , p yof income attributable to the debt-financed property. Sect. 514

• Option: Establish a “blocker corporation” created offshore in a jurisdiction that does not impose income tax at the corporate level, such that corporate-level tax is avoided by the foundation. The blocker distributes dividends to the foundation that are not taxed as UBIT to the foundation. See PLR 20031538

McGuireWoods LLP | 53CONFIDENTIAL

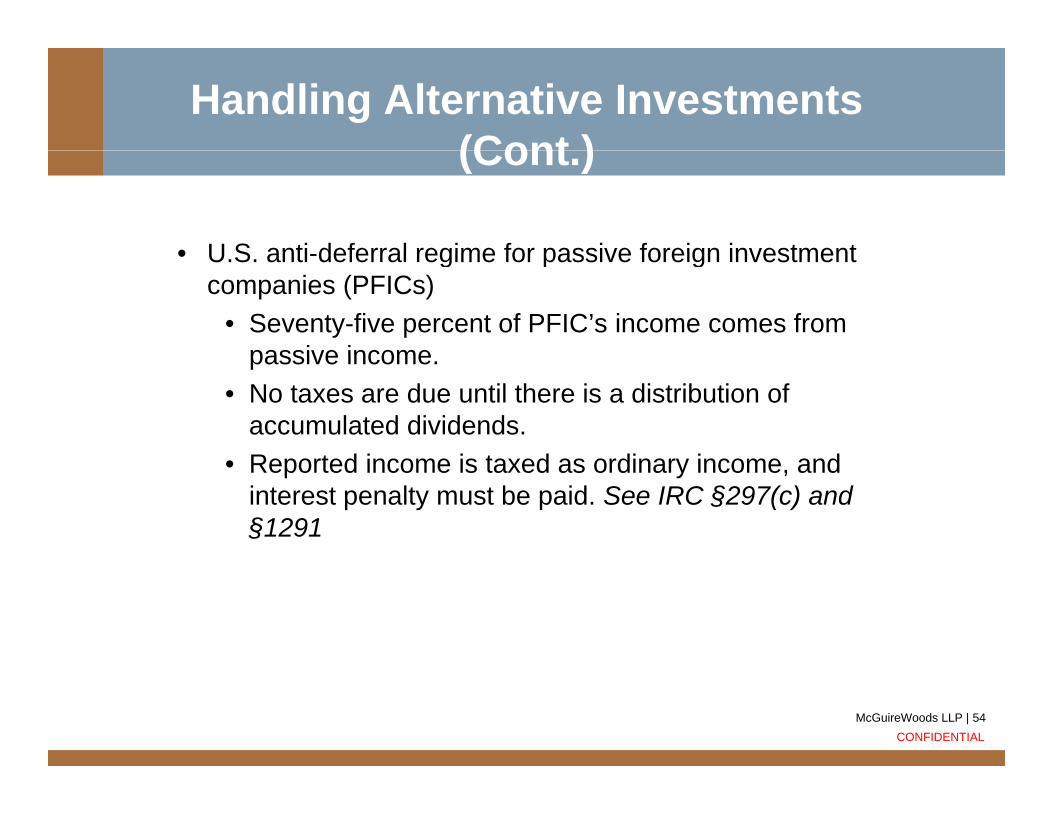

Handling Alternative Investments (Cont )(Cont.)

• U S anti deferral regime for passive foreign investment• U.S. anti-deferral regime for passive foreign investment companies (PFICs)

• Seventy-five percent of PFIC’s income comes from passive incomepassive income.

• No taxes are due until there is a distribution of accumulated dividends.R t d i i t d di i d• Reported income is taxed as ordinary income, and interest penalty must be paid. See IRC §297(c) and §1291

McGuireWoods LLP | 54CONFIDENTIAL

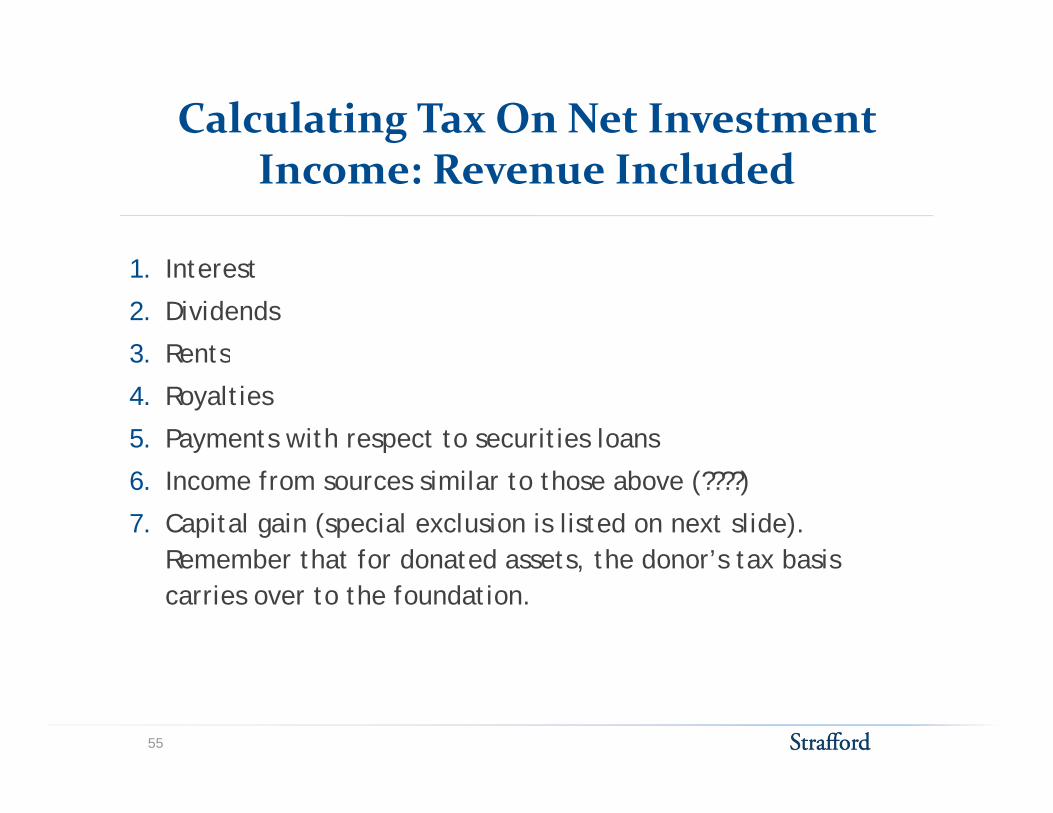

Calculating Tax On Net Investment Income: Revenue Included

1. Interest

2. Dividends

3 Rents3. Rents

4. Royalties

5. Payments with respect to securities loans

6. Income from sources similar to those above (????)

7. Capital gain (special exclusion is listed on next slide). Remember that for donated assets the donor’s tax basis Remember that for donated assets, the donor s tax basis carries over to the foundation.

55

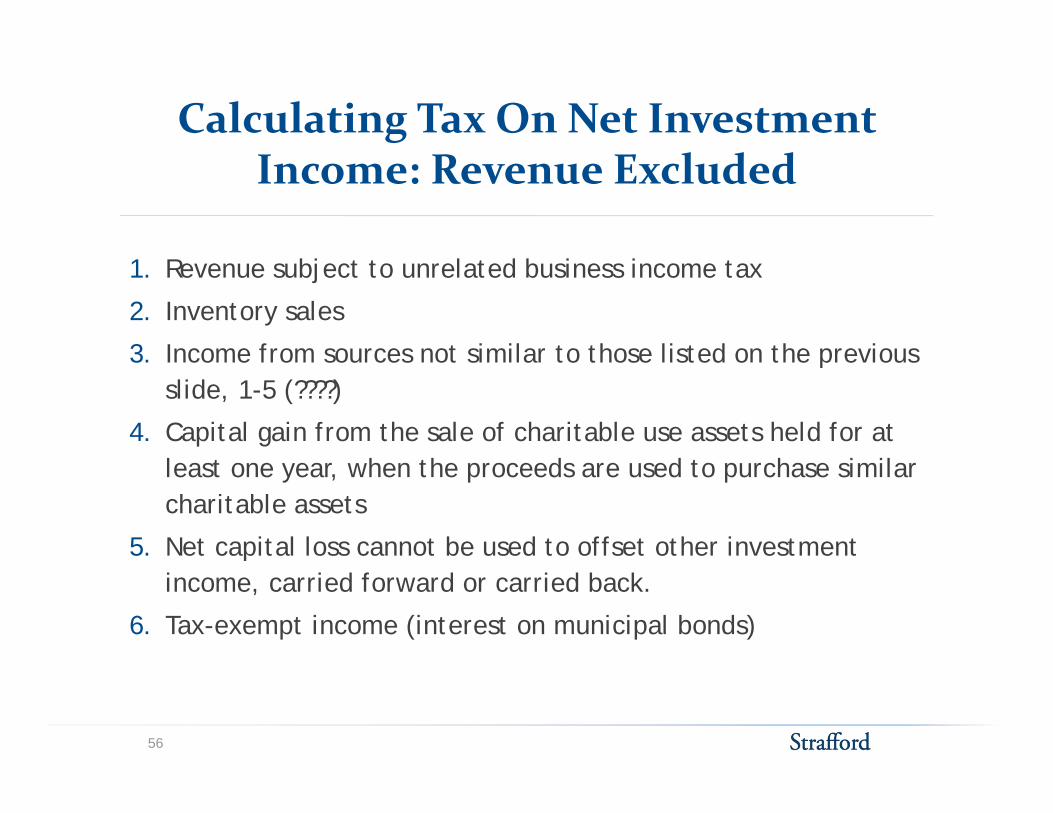

Calculating Tax On Net Investment Income: Revenue Excluded

1. Revenue subject to unrelated business income tax

2. Inventory sales

3 Income from sources not similar to those listed on the previous 3. Income from sources not similar to those listed on the previous slide, 1-5 (????)

4. Capital gain from the sale of charitable use assets held for at l h h d d h i il least one year, when the proceeds are used to purchase similar charitable assets

5. Net capital loss cannot be used to offset other investment pincome, carried forward or carried back.

6. Tax-exempt income (interest on municipal bonds)

56

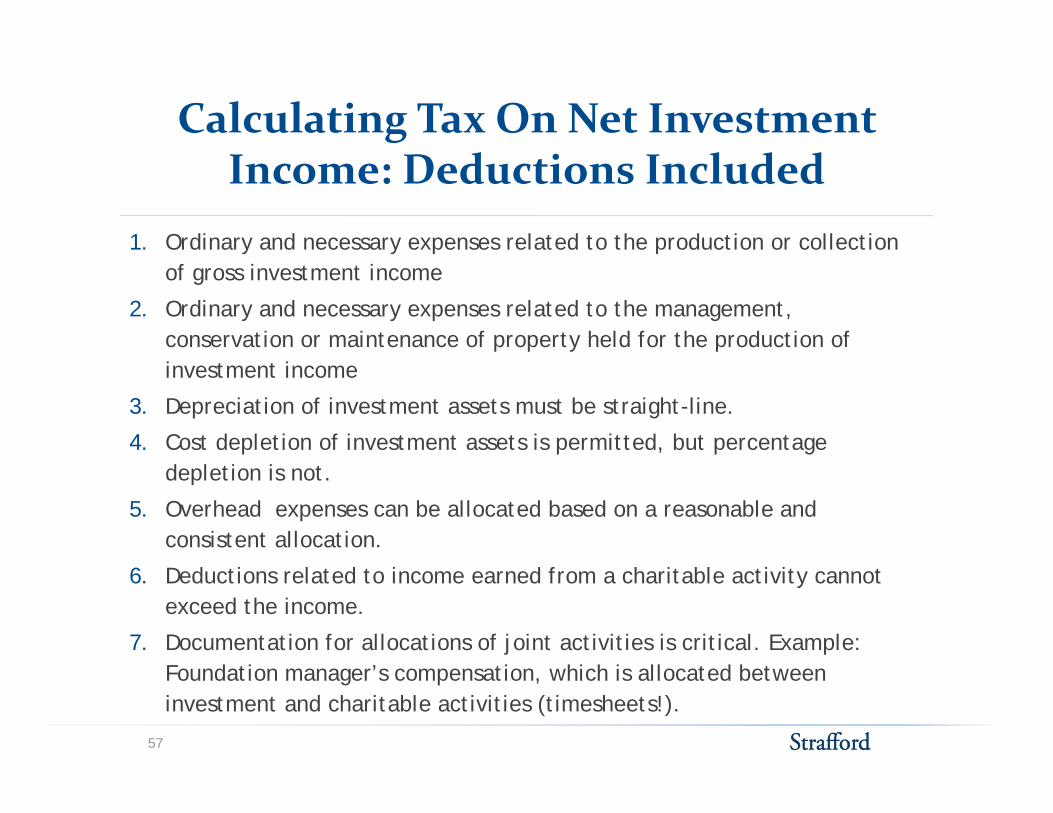

Calculating Tax On Net Investment Income: Deductions Included

1. Ordinary and necessary expenses related to the production or collection y y p pof gross investment income

2. Ordinary and necessary expenses related to the management, conservation or maintenance of property held for the production of investment income

3. Depreciation of investment assets must be straight-line.

4. Cost depletion of investment assets is permitted, but percentage depletion is not.

5. Overhead expenses can be allocated based on a reasonable and consistent allocation.

6. Deductions related to income earned from a charitable activity cannot exceed the income.

7. Documentation for allocations of joint activities is critical. Example: Foundation manager’s compensation, which is allocated between investment and charitable activities (timesheets!).

57

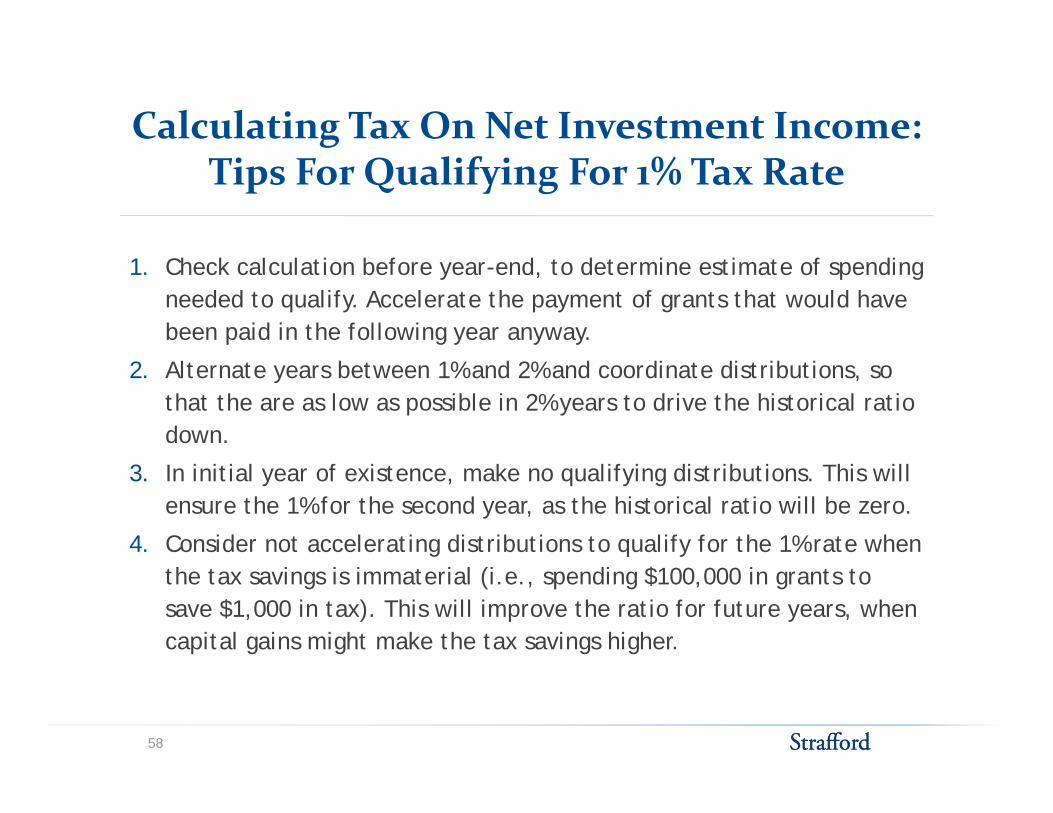

Calculating Tax On Net Investment Income: Tips For Qualifying For 1% Tax Rate

1. Check calculation before year-end, to determine estimate of spending needed to qualify. Accelerate the payment of grants that would have been paid in the following year anyway.

2. Alternate years between 1% and 2% and coordinate distributions, so that the are as low as possible in 2% years to drive the historical ratio down.

3. In initial year of existence, make no qualifying distributions. This will ensure the 1% for the second year, as the historical ratio will be zero.

4. Consider not accelerating distributions to qualify for the 1% rate when the tax savings is immaterial (i.e., spending $100,000 in grants to save $1,000 in tax). This will improve the ratio for future years, when capital gains might make the tax savings higher.

58

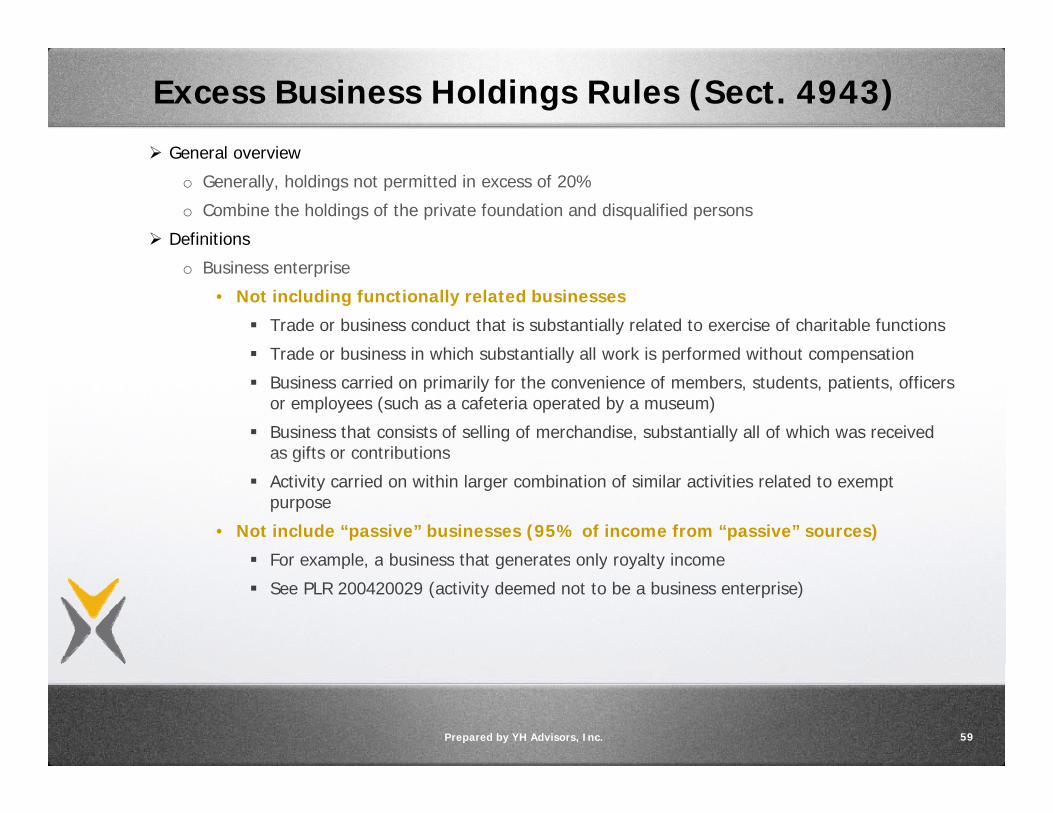

Excess Business Holdings Rules (Sect. 4943)

General overview General overview

o Generally, holdings not permitted in excess of 20%

o Combine the holdings of the private foundation and disqualified persons

Definitions

o Business enterprise

• Not including functionally related businesses

Trade or business conduct that is substantially related to exercise of charitable functions

Trade or business in which substantially all work is performed without compensation Trade or business in which substantially all work is performed without compensation

Business carried on primarily for the convenience of members, students, patients, officers or employees (such as a cafeteria operated by a museum)

Business that consists of selling of merchandise, substantially all of which was received as gifts or contributionsas gifts or contributions

Activity carried on within larger combination of similar activities related to exempt purpose

• Not include “passive” businesses (95% of income from “passive” sources)

For example a business that generates only royalty income For example, a business that generates only royalty income

See PLR 200420029 (activity deemed not to be a business enterprise)

Prepared by YH Advisors, Inc. 59

Excess Business Holdings Rules (Sect. 4943), Cont.

Definitions (Cont.)

o Excess business holdings (Sect. 4943(c)(2))

• General rule: Hold no more than 20% of voting stock

PLR 199124061: Cannot “convert” voting stock to non-voting stock by agreeing not to PLR 199124061: Cannot convert voting stock to non-voting stock by agreeing not tovote the stock

No limit on the amount of non-voting stock that private foundation can own

• Exceptions

Increase to 35% when unrelated owner has effective control (Reg. 53.4943-3(b)(3)(ii))

Effective control is the power to direct the management and policies of abusiness enterprise.

Private foundation can own 2% of voting stock of business enterprise, regardless of whatg p , gis owned by disqualified persons.

Ownership of the stock of a functionally related business (Reg. 53.4943-10(b))

Business related to the exempt purposes of the private foundation

S S t 4942(j)(4) d R 53 4942( ) 2( )(3)(iii) See Sect. 4942(j)(4) and Reg. 53.4942(a)-2(c)(3)(iii)

See PLR 201006032

Private foundation’s program-related investments

Prepared by YH Advisors, Inc. 60

Excess Business Holdings Rules (Sect. 4943), Cont.

Di iti f b i h ldi Disposition of excess business holdings

o 90-day period (knows or reason to know of the excess business holdings)

• Private foundation acquires ownership other than by purchase

For example, disqualified person acquires additional holdings

o Gifts/bequests

• Five-year time period (ability to obtain another five years under certain circumstances)

See Sect. 4943(c)(7)(A)

PLR 200650018: Private foundation received five-year extension when making best efforts to dispose ofinterest in farminterest in farm

PLR 200833018: Private foundation received five-year extension for publicly traded stock (thinvolume/sales restrictions)

PLR 201105053: IRS granted a private foundation an additional five years under Sect. 4943(c)(7) todispose of excess business holding that resulted from an unusually large bequest.

o Consider gifts of “excess” stock/securities, as opposed to just selling

• Potentially reduces capital gain subject to the net investment income excise tax

PLR 201127011

o IRS ruled that a private foundation’s ownership of 100% of the stock of a company would not be classified asexcess business holdings because at least 95% of the company’s gross income came from passive sourcesexcess business holdings, because at least 95% of the company’s gross income came from passive sources.

• See Sect. 4943(d)(3) and Reg. §53.4943-10(c)(1) for the 95% rule

Prepared by YH Advisors, Inc. 61

Jeopardizing Investmentsp g

Jeopardizing investmentsWhat are jeopardizing investments?• What are jeopardizing investments?

• Sect. 4944 provides that if a private foundation invests its assets in such a manner that will jeopardize the accomplishments of its exempt purposes the foundationaccomplishments of its exempt purposes, the foundation and possibly its managers are subject to certain excise taxes.

• Foundation managers failed to exercise ordinary• Foundation managers failed to exercise ordinary business care and prudence under the facts and circumstances at the time of mailing the investment. They knowingly and willing engaged in a transactionThey knowingly and willing engaged in a transaction while aware that it might violate Sect. 4944. The IRS decision is made on an investment-by- investment basis. No category of investments is treated as a “per se”

McGuireWoods LLP | 62CONFIDENTIAL

g y pviolation of Sect. 4944. Transaction may be protected by a reasoned opinion of counsel.

Jeopardizing Investments (Cont.)p g ( )• IRS will closely scrutinize trading in securities on margin,

commodity futures, puts calls and “straddles.”co od ty utu es, puts ca s a d st add es• Program-related investments exempted from jeopardy

investment rules• The primary purpose is to accomplish one or more tax-The primary purpose is to accomplish one or more tax-

exempt purposes, of which no significant purpose can be the production of income or the appreciation of property.

• PRIs are not subject to the excess business holdings rulesPRIs are not subject to the excess business holdings rules under Sect. 4943 and may be treated as qualifying distributions under Sect. 4942.

• An investment can be made to either a charity non-profit orAn investment can be made to either a charity, non profit or commercial business that is carrying out the charitable purposes of the foundation.

• The investment would not have been made but for the

McGuireWoods LLP | 63CONFIDENTIAL

The investment would not have been made but for the investment and the accomplishment of the exempt purpose.

Jeopardizing Investments (Cont.)p g ( )

• Examples• Examples• Low-interest or interest-free loans to needy students• High-risk investments in non-profit/low-income housing• Low-interest loans to small businesses owned by

disadvantaged groups in economically distressed areas where commercial loans are not available

• Investments in businesses in deteriorated urban areas• Investments combating community deterioration• Congress and the IRS are currently considering other g y g

examples.

McGuireWoods LLP | 64CONFIDENTIAL

Jeopardizing Investments (Cont.)p g ( )

• Each program related investment must be made subject to a• Each program-related investment must be made subject to a written commitment that includes:

• An agreement by the recipient to use the funds only for the purposes of the investmentthe purposes of the investment

• Submit at least once a year a full and complete financial report ordinarily required by commercial investorsK d t b k d d• Keep adequate books and records

• Funds must not be used for legislative or political activities

McGuireWoods LLP | 65CONFIDENTIAL

Program-Related Investments

General overview

o Take responsibility for the funds granted to the foreign charity

o Granting private foundation conducts specific oversight and monitoring procedures

• Takes lots of ongoing effort and energyTakes lots of ongoing effort and energy

o Necessary steps

• Pre-grant due diligence that foreign recipient is a bona fide charity

• Ensure that grant is actually spent only for the purpose for which it is made

• Obtain full and complete reports from the foreign grantee organization onhow funds were spent

• Make full and detailed reports on the expenditures to the IRS on Form 990-PF

o Private letter rulings

• See PLR 200813043 for IRS guidance when making grants to foreigncharities

See also PLR 201039047 See also PLR 201039047

• See PLR 200852038 for IRS guidance regarding when expenditureresponsibility should be exercised for grants made to domestic non-charitable entities

Prepared by YH Advisors, Inc. 66

Preparing Form 4720: Reporting Self‐Dealing

1 For self-dealing transactions that involve the use of money (loan) the 1. For self-dealing transactions that involve the use of money (loan), the amount involved is the FMV of the use of the money, not the amount of money borrowed. With today’s interest rates, that amount is usually pretty small.usually pretty small.

2. The self-dealer must file a separate Form 4720 if his tax year is different from the foundation’s (typically, this is an issue if the foundation is on a fiscal year that is other than the calendar year).foundation is on a fiscal year that is other than the calendar year).

3. No abatement of the penalty is permitted.

4. Penalty is 10% of amount involved and is owed by the self-dealer. If penalty is paid by PF this results in another self-dealing transactionpenalty is paid by PF, this results in another self-dealing transaction.

5. Correction involves undoing the transaction to the extent possible, but not putting the PF in a worse position than if it had engaged in the transaction with a non insider If terms are favorable to the PF the transaction with a non-insider. If terms are favorable to the PF and must be rescinded, the DP has to make the PF “whole.”

67

Preparing Form 4720: Reporting A Taxable Expenditure

1. Remember that a taxable expenditure may still be a qualifying distribution. A scholarship grant is a taxable expenditure, because an approved plan is not in place was still made for charitable purposes.

2 Abatement of the penalty can be requested as long as the taxable event was 2. Abatement of the penalty can be requested as long as the taxable event was due to reasonable causes and not willful neglect, and the event was corrected within the prescribed correction period. The correction must be described.

3. Correction is generally accomplished by recovering part or all of the g y p y g pexpenditure, to the extent recovery is possible. Where full recovery is not possible, additional corrective action includes one or more of the following:

Requiring that any unpaid funds due to the grantee be withheld

Requiring that no further grants be made to the particular grantee

Requiring reports regarding the use of the funds

Requiring improved methods of exercising expenditure responsibility

Requiring improved methods of selecting recipients of individual grants.

68

Preparing Form 4720: Foundation Manager Liability

Remember that foundation managers who approve of certain transactions (below) reported on Form 4720 may personally be subject to a penalty. The tax is imposed only when the foundation manager knew that the expenditure was improper and agreed to the making of the expenditure willfully, not under reasonable cause.u de easo able cause.

The following types of penalty transactions could result in FM liability:

S lf d li• Self-dealing

• Taxable expenditure

• Jeopardizing investmentJeopardizing investment

• Political expenditure

69

IRS Compliance Initiativesp

IRS compliance initiatives• The 990-PF is the primary tool used by the IRS to audit• The 990-PF is the primary tool used by the IRS to audit

private foundations.• How does IRS choose which 990-PF to audit?

• Routine examinations: Checklist of records analyzedRoutine examinations: Checklist of records analyzed includes the auditor’s minutes of the meeting, canceled checks and activities.

• Compliance checks recently are emphasizing compensation and benefits of officers and directors.

• Another related organization, individual or substantial contributor under audit can trigger a review of the 990-PFPF.

• Team audits are reserved for larger foundations and include grants both foreign and domestic, compensation and potential excise tax resulting from self-dealing

McGuireWoods LLP | 70CONFIDENTIAL

and potential excise tax resulting from self dealing, jeopardy investments, excess business holdings employment tax and UBIT.

Grants To Donor-Advised Funds

Donor-advised fund advantages over private foundations

o Avoid cost and time of having to prepare Form 990-PF

o Avoid some private foundation excise taxes

o Some say regarding grants and not having to deal with minimum distribution requirements

o Larger AGI charitable contribution deduction limitations

o Increased privacy

• Can be better utilized for anonymous giving

Private foundation grants to donor-advised funds

o Private foundation grants to donor-advised funds can be classified as qualifyingdistributions.

• Donor-advised fund is considered to be a public charity/

• See Reg. §53.4942(a)-3(a)(3) re: definition of ”control”

• See Reg. §53.4942(a)-3(a)(8), Example (5)

h 990 2o New on the Form 990-PF – Part VII-A, Line 12

• Did the foundation make a distribution to a donor-advised fund over which the foundation or a disqualified person had advisory privileges? If “Yes,” attach statement (see instructions).

Prepared by YH Advisors, Inc. 71

Expenditure Responsibility Rules

Necessary steps

o Pre-grant inquiry

• Investigate, based on readily available information, whether the grantee will use the grantedfunds from the private foundation for proper purposes.

• Inquiry should cover the identity, experience and history of grantee and its governing body; andinformation on management activities, finances and practices of the grantee.

• Private foundation must document the purposes of the grant, the assessment of the grantee’sability to achieve goal, and the assessment of grantee’s ability to report on the use of the funds.

• Please e-mail me for examples of pre-grant inquiry formsp p g q y

o Written grant agreement

• Specify the charitable purpose

• Require that the grantee maintain grant funds in separate account

• Require grantee to maintain records of receipts and expenditures and make such recordsq g p pavailable to the private foundation for inspection

• Require the grantee to repay grant funds if they are not utilized for purposes of the grant

• Require the grantee to provide annual reports and a final report on its use of the grant funds

• Prohibit the use of the grant funds for lobbying, political activities, re-granting and non-charitable usescharitable uses

• Must be executed by the private foundation and the grantee

• Please e-mail me for a copy of the sample agreement letter

Prepared by YH Advisors, Inc. 72

Expenditure Responsibility Rules (Cont.)

Necessary steps (Cont.)

o Annual reports (must be received in all years that grant funds expended)

• Detailed breakdown of how grant funds were expended during the relevant period in comparisonto the initial budgets of the grantee

Na ati e desc iption of the g antee’s p og ess in achie ing the p poses of the g ant d ing the• Narrative description of the grantee’s progress in achieving the purposes of the grant during theyear

• Statement of whether the grantee has fully complied with the terms of the grant agreement

• Signature of the authorized officer of the grantee

• Please e-mail for a sample grantee report formease e a o a sa p e g a ee epo o

o Final reports

• Must be received within a reasonable period of time after the close of the grantee’s annualaccounting period in which all the grant funds were expended or the grant was terminated(generally 90 days)

R t t th IRSo Reports to the IRS

• Must annually report to the IRS on every expenditure responsibility grant made

• Please see the example of the Form 990-PF attachment in the course materials

o Investigate problems with grant

P i t f d ti t t k ti if di i f t f d h t k l• Private foundation must take corrective measures if a diversion of grant funds has taken place.

• Take all reasonable and appropriate steps to recover the grant funds

• Withhold further payments to the grantee until receive assurances that further diversions will notoccur

Prepared by YH Advisors, Inc. 73

Expenditure Responsibility Rules (Cont.)

How to fail expenditure responsibility

o Fail to conduct sufficient pre-grant inquiry

o Fail to include required terms in grant agreement

Fail to receive annual or final reportso Fail to receive annual or final reports

o Fail to attach required support documents to the Form 990-PF

Disadvantages of expenditure responsibility Disadvantages of expenditure responsibility

o Tougher to make general support grants under expenditure responsibility

o Required periodic reporting could be tough to obtain from certain countries.

o Probably not the preferred method if the private foundation grantor expects to fund they p p g pforeign charity over a long-term period

Prepared by YH Advisors, Inc. 74

PREPARING FOR FUTURE Candice Meth, EisnerAmper

FORM 990‐PF FILINGS: BEST PRACTICESPRACTICES

Lessons Learned From Self-DealingLessons Learned From Self Dealing

Leases: Don’t pay rent to disqualified person

Special events: A private foundation cannot purchase tickets to a charitable fundraising event and then provide the tickets to di lifi d t thi d ti if d i b fitdisqualified persons or to third parties, if doing so benefits a disqualified person. There is an exception that permits foundation managers to use the tickets if attending the event furthers their duties for the foundation.duties for the foundation.

76

Lessons Learned from Self-Dealing (Cont.)g ( )

Investment management services might be okay.

Loan to disqualified person – bad idea

Using credit cards: If a disqualified person uses a foundation credit card for personal expenses and later reimburses the foundation for the expenses, this is considered a loan and a form of self-dealing, even if the person reimburses the full amount within a month of the transaction.

77

Pro Bono, Please!

As stated in the IRS’ Publication 578 Tax Information for Private Foundations and Foundation Managers “providing goods, services, or g g g

facilities between a private foundation and a disqualified person … is not self-dealing if a disqualified person provides them to the foundation

without charge andthe goods, services, and facilities are used exclusively for purposes

specified in section 501(c)(3) of the Code”.

78

Providing Investment Management ServicesProviding Investment Management Services For A Fee Is Okay

Per Private Letter Ruling 200217056, it was determined that payment for fees by a private foundation for investment services provided

by a disqualified person, as described in Sect 53 4941(d) 3(c)(2)Sect. 53.4941(d)-3(c)(2),

will not be an act of self-dealing.

79

Lessons Learned With Respect pTo Qualifying Distributions

IRS revocation: Keep a record of tax status based on when you made the grant

Foreign grants: Expenditure responsibility or equivalency Foreign grants: Expenditure responsibility or equivalency determination

Giving to donor-advised fund: A good option if you are trying to target the 1% taxto target the 1% tax

Scholarships/honorariums: Might need to create a 1099; special IRS rules!

80

Lessons Learned From Sections On Investments Jeopardizing investments: Foundation manager failed to exercise

“ordinary business care and prudence under the facts and circumstances at the time of mailing the investment.” The manager knowingly and willingly engaged in a transaction that may violateknowingly and willingly engaged in a transaction that may violate Sect. 4944. IRS looks at this on an investment-by-investment basis; there is no specific category known as a “per se” violation of Sect. 4944.

Where to place alternative investments within the average value section: Part X line 1c

You no longer need to give details of realized gains and losses, but You no longer need to give details of realized gains and losses, but you are supposed to list the details of the individual stocks, bonds, etc. that you own at year-end.

Foreign investments: Answer question whether you file Form TD F g q y90-22.1. Beware of offshore hedge fund liquidations at year-end.

81

Average Values:Where do the alternatives go?

82

Minimize Tax Liability While Avoiding Ire Of IRS

Be careful what you allocate to investment expenses: Column “B”

Cost/benefit analysis in terms of targeting the 1% tax –giving money to a donor-advised fund might help!

Remember that Column “B” might be on an accrual basis, g ,whereas Column “D” is always on a cash basis.

Some things don’t get allocated (excise tax expense, depreciation).

If a grant was returned to you from a prior year, you need to report that (Part XI, line 4).

If you took a deduction for a fixed asset (Part XII, line 2) and y ( , )then decided to dispose of it well before its useable life was over, you have implications to consider.

83

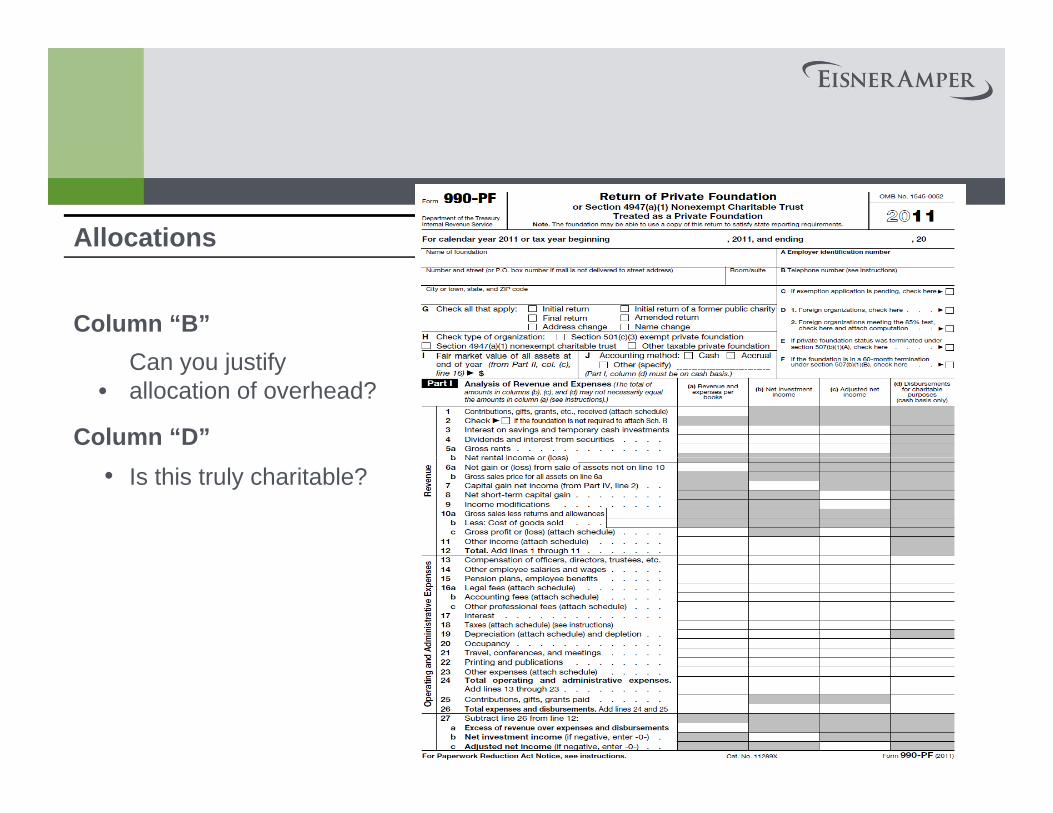

Allocations

Column “B”C j tif

•Can you justify allocation of overhead?

Column “D”• Is this truly charitable?

84

C Ab t C tiConcerns About Compensation Executive compensation is a hot topic in the press.

Are you doing compensation studies? Do you have a compensation-setting committee? Can you show that compensation is reasonable in comparison to that of other foundations?is reasonable in comparison to that of other foundations?

The box for payment to disqualified person should be checked “Y ” (P t VII B Q ti 1( )4) i th ti di t i“Yes” (Part VII-B Question 1(a)4), since the executive director is a disqualified person and he/she gets paid (if no compensation was paid, its possible this box would get checked “No”).

85

C Ab t C ti (C t )Concerns About Compensation (Cont.)

Does it “look bad” if the directors or trustees receive stipends?

A private foundation may pay reasonable compensation to a disqualified person for providing necessary professional services to the foundation. Example: A foundation can pay an accountant who serves on the foundation’s board of directors reasonable fees for accounting services provided to the foundation.

W-2 vs. 1099: An individual receives one or the other, but never both!

86

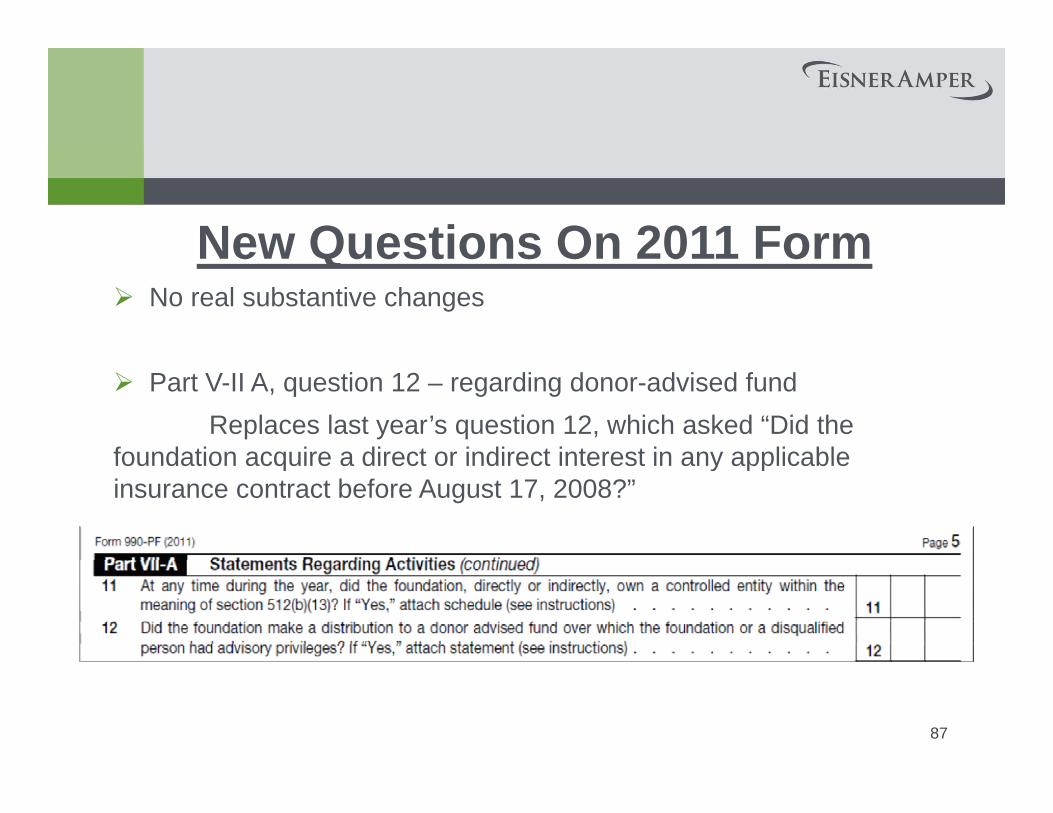

New Questions On 2011 FormNew Questions On 2011 Form No real substantive changes

Part V-II A, question 12 – regarding donor-advised fundReplaces last year’s question 12, which asked “Did the

foundation acquire a direct or indirect interest in any applicablefoundation acquire a direct or indirect interest in any applicable insurance contract before August 17, 2008?”

87

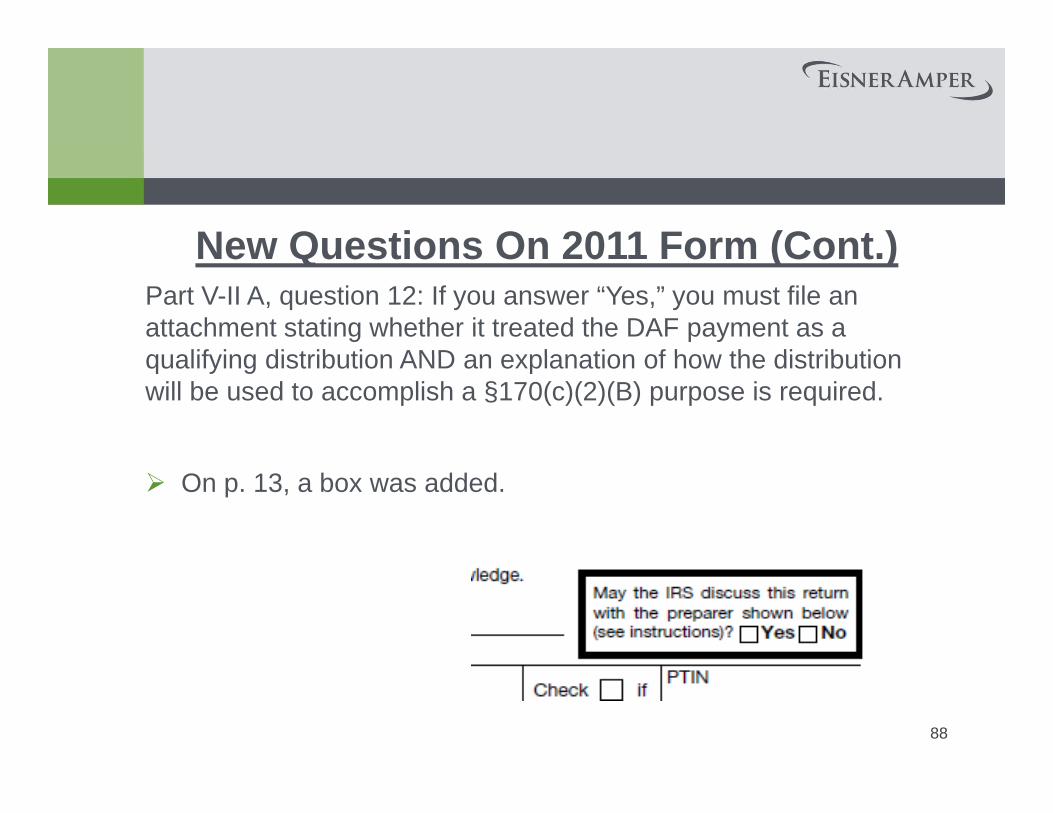

New Questions On 2011 Form (Cont )New Questions On 2011 Form (Cont.)Part V-II A, question 12: If you answer “Yes,” you must file an attachment stating whether it treated the DAF payment as a qualifying distribution AND an explanation of how the distributionqualifying distribution AND an explanation of how the distribution will be used to accomplish a §170(c)(2)(B) purpose is required.

On p. 13, a box was added.

88

2012 IRS Work PlanPrivate foundationsPrivate foundations “Many private foundations hold substantial assets, and private foundations generally are subject to more restrictive rules than other charities. Based on information reported on pthe Form 990-PF, EO is examining a selection of the largest private foundations.”

89

Flat Tax for Private Foundations – Proposed Bills

Proposed fillpOn March 16, 2011, Sen. Charles Schumer, D-NY, introduced a private foundation excise tax bill (S. 593). On June 23, 2011, representatives Erik Paulsen, R-MN, and Danny Davis, D-IL, introduced a companion bill in the House. Both proposals would amend the Internal Revenue Code of 1986 to modify and simplify the excisewould amend the Internal Revenue Code of 1986 to modify and simplify the excise tax on the investment income that private foundations pay. S.593 and H.R. 2311 would remove the current two-tiered excise tax imposed on private foundations and replace it with one flat rate. The proposals set the excise tax rate at 1.39%, deemed to be revenue-neutral by the Joint Committee on Taxation in the 111th Congress. S.593 and H.R. 2311 would be applicable to tax years beginning after the date the bill is enacted.

Updates …90

Future Of Flat Tax For Private Foundations

Administration’s Fiscal Year 2013 Budget Proposal g pOn Feb. 13, 2012, the Administration released its fiscal year 2013 budget proposal. The budget included a provision calling for a single, 1.35% excise tax rate on investment income of private foundations, rather than the revenue-neutral 1.39% that Congress has been advocating The proposed change would be effective forthat Congress has been advocating. The proposed change would be effective for taxable years beginning after the date of enactment. The Administration estimated that permanently setting the rate at 1.35% would result in a tax revenue loss of $54 million over 10 years.

Updates …

91

![Index 09 [] … · 2009 Index of Statements Attached to Return of Private Foundation (Form 990-PF) 1 Form 990-PF, Part I, Line 11, Other Income 2 Form 990-PF, Part I, Line 16a, Legal](https://img.dokumen.tips/doc/110x75/5f7cbd3218dd844229317342/index-09-2009-index-of-statements-attached-to-return-of-private-foundation.jpg)