Embed Size (px)

Citation preview

0

1

Forecasting in a Down Economy: Lessons from VolkswagenJonathan SparksManager of Sales Planning & ForecastingManager of Sales Planning & Forecasting

Agenda• Introductions

• Company Background and Supply Chain Overview

• Industry Outlook in 2008

• How Recessions Affect Forecast Results

• Forecasting Techniques for a Down Economy

2

• Responding to the 2008 Recession

• Results and Next Steps

0

2

Company Overview• Volkswagen Group

• Headquartered in Wolfsburg, Germany• 99 factories in 27 countries• Delivered 8 265 million vehicles in 2011• Delivered 8.265 million vehicles in 2011• 12.3% global market share

Company Overview• Volkswagen of America• HQ in Herndon VA• HQ in Herndon, VA• 13 car product portfolio• 324,000 sales in 2011• 2.5% market share• Jetta #1 selling product• Jetta #1 selling product

0

3

Supply Chain Overview• 6 factories – Portugal, Germany, Mexico, Slovakia, US

• 4 Ports of Entry– Shipping methods :boat, air, rail, truck

5 R i l Offi• 5 Regional Offices– Wholesaling, marketing, incentives, network development

VW Forecast Overview (2008)• Long term forecasts (10 years) – volume and mix

– Lifecycle management– Industry projectionsy p j– Segment projections– Economic factors– Carline growth

• Short term forecasts (1‐2 years) – volume and mix– Statistical modeling from history– Subjective judgment– Regional feedback– Growth targets

6

0

4

2008 Industry Outlook

20

Industry Fcst

16

Sales U

nits (M

illions)

12

8

16.515.815.114.614.416.1

4

0201220112010200920082007

4

2008‐2011 Reality

‐19%‐23%29%

20

ActualIndustry Fcst

23%‐29%‐8% 16.5

12.8

15.8

11.6

15.1

10.4

14.613.2

14.4

16.116.1

Sales U

nits (M

illions)

16

12

8

2012201120102009200820070

4

0

5

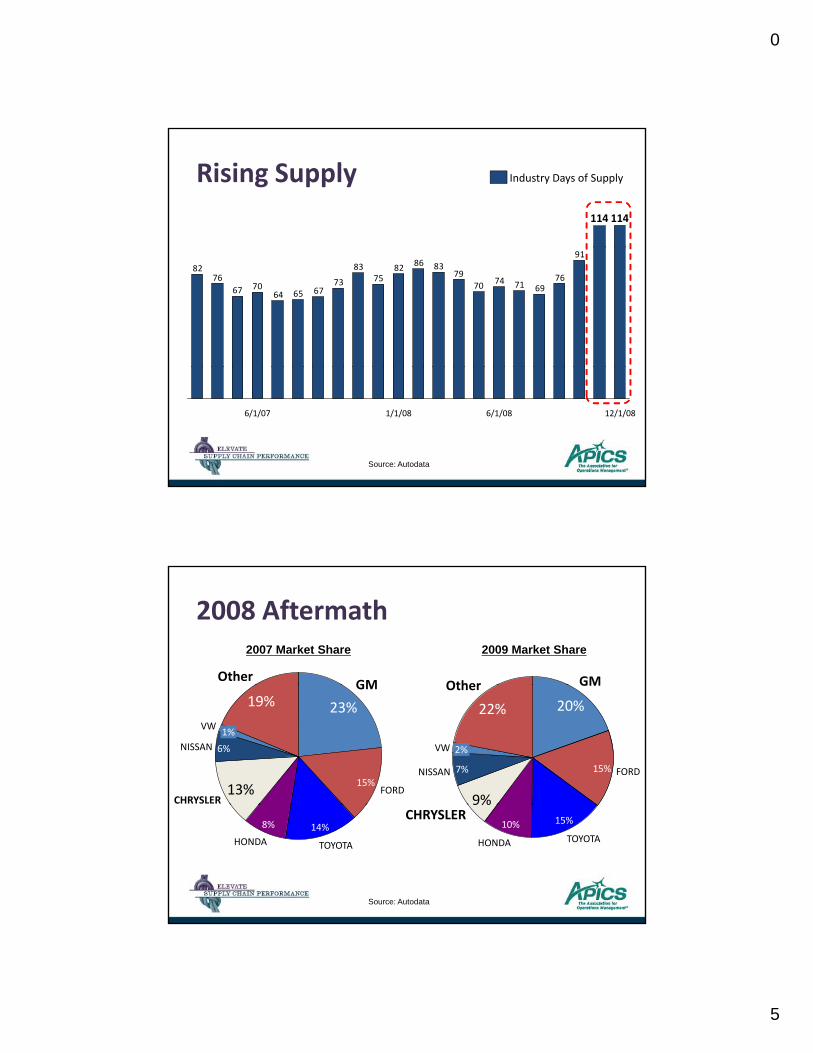

Rising Supply114114

Industry Days of Supply

91

7669717470

79838682

7583

73676564

706776

82

12/1/086/1/081/1/086/1/07

Source: Autodata

2008 Aftermath

GMOtherOther GM

2007 Market Share 2009 Market Share

13% FORD15%

GM

23%19%VW 1%

NISSAN 6%

CHRYSLER 9%

Other

22%

VW 2%

NISSAN 7% FORD15%

GM

20%

14%HONDA

8%

TOYOTA

9%CHRYSLER

HONDA

10%TOYOTA

15%

Source: Autodata

0

6

2008 Aftermath

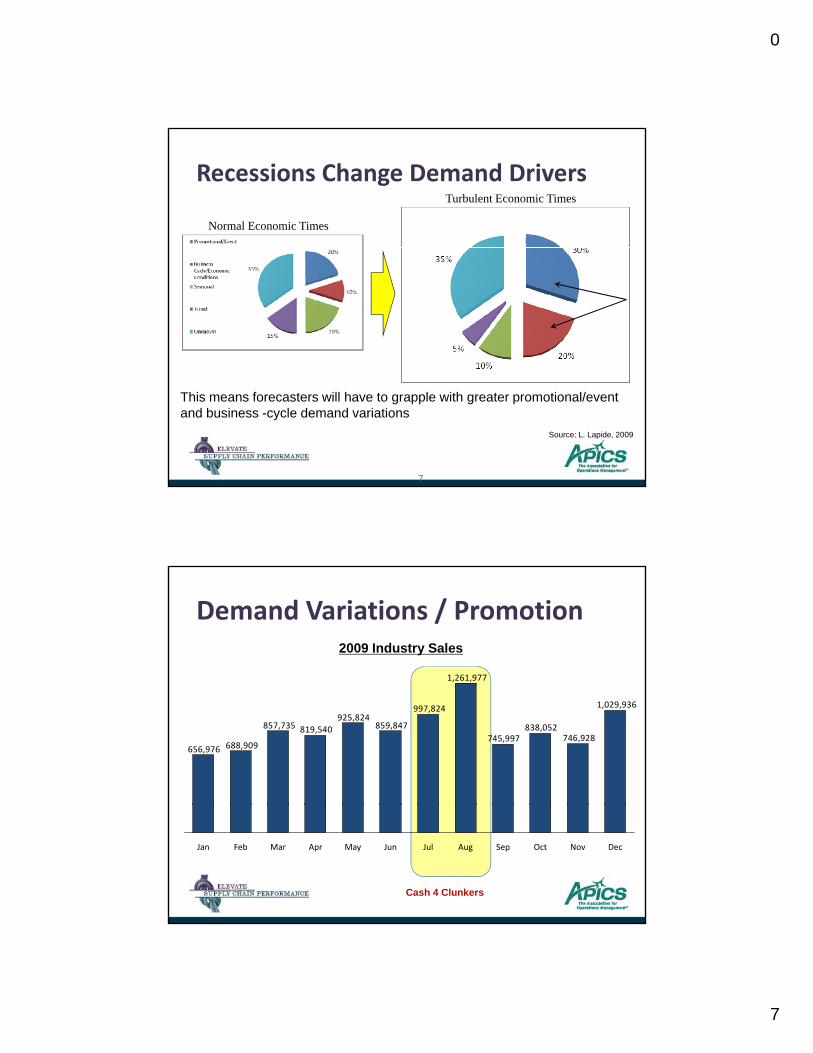

Demand Drivers

Percent of Demand Variation Analysis (Components of Demand Variation ) Source: L. Lapide, 2009

6

0

7

Normal Economic Times

Turbulent Economic Times

Recessions Change Demand Drivers

This means forecasters will have to grapple with greater promotional/event and business -cycle demand variations

Source: L. Lapide, 2009

7

Demand Variations / Promotion

1,261,977

2009 Industry Sales

1,029,936

746,928838,052

745,997

997,824

859,847925,824

819,540857,735

688,909656,976

Jan AugJulJunMayAprMarFeb Sep Oct Nov Dec

Cash 4 Clunkers

0

8

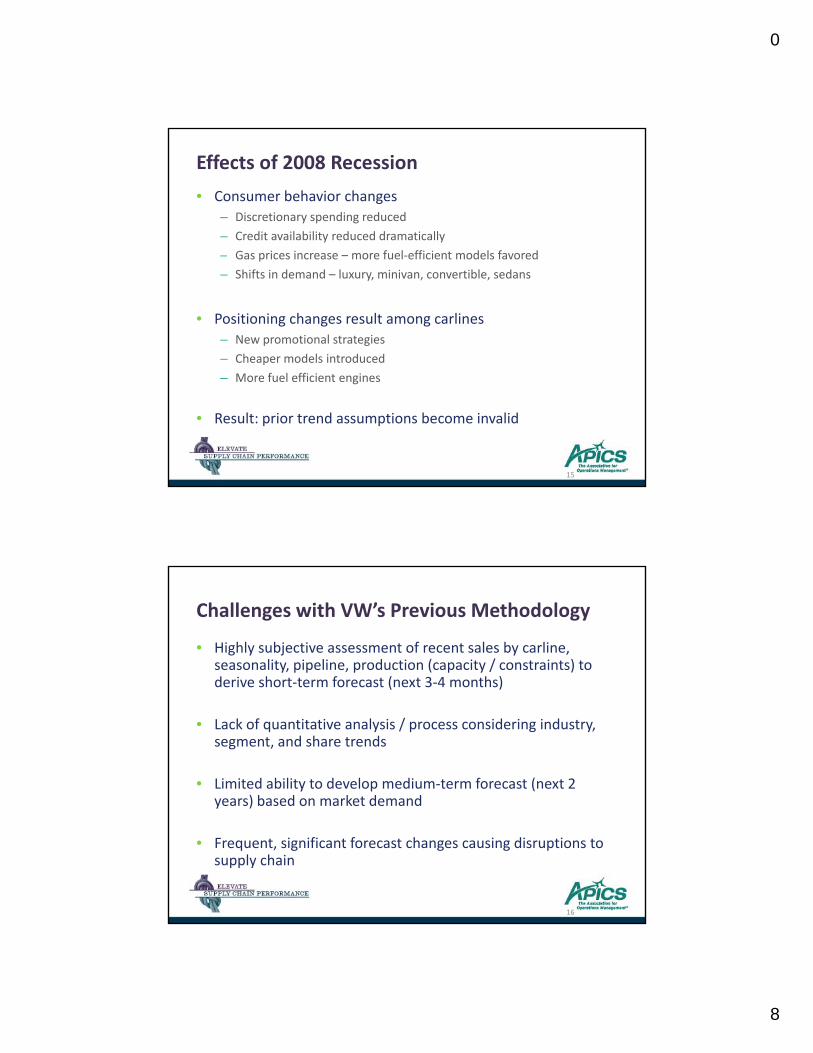

Effects of 2008 Recession• Consumer behavior changes

– Discretionary spending reduced– Credit availability reduced dramatically– Gas prices increase – more fuel‐efficient models favored– Shifts in demand – luxury, minivan, convertible, sedans

• Positioning changes result among carlines– New promotional strategies– Cheaper models introduced– More fuel efficient engines

• Result: prior trend assumptions become invalid

15

Challenges with VW’s Previous Methodology

• Highly subjective assessment of recent sales by carline, seasonality, pipeline, production (capacity / constraints) to derive short‐term forecast (next 3‐4 months)derive short term forecast (next 3 4 months)

• Lack of quantitative analysis / process considering industry, segment, and share trends

• Limited ability to develop medium‐term forecast (next 2 years) based on market demandyears) based on market demand

• Frequent, significant forecast changes causing disruptions to supply chain

16

0

9

Techniques for Turbulent Times1. Stay abreast of what is going on in the market

and organization2008 Situation

Finance IncentivesSales

Forecasting

Marketing

DistributionProduct Planning

Source: L. Lapide, 2009

Sales Forecasting

Techniques for Turbulent Times1. Stay abreast of what is going on in the market

and organization2012 Situation Forecasting

Marketing

Product

Distribution

Product Planning

Finance

Incentives

Source: L. Lapide, 2009

0

10

Techniques for Turbulent Times2. Collect timely downstream data as early

indicators of the performance of promotions and new products (e.g., point of consumption information)

Nissan AltimaHonda AccordFord Fusion

July Aug Sept Oct Nov Dec

27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52

Honda CivicNissan Sentra

Techniques for Turbulent Times3. Stay abreast of changing economic conditions,

listening to internal and external economists

50

100

150

Building Pe

rmits (Tho

usands)

Housing Starts

1

2

3

4

5

Avg. Fue

l Price

Fuel Prices

02007 20092008

02007 20092008

Source: US. Dept. of Commerce Source: US. Dept. of Energy

Source: L. Lapide, 2009

0

11

Techniques for Turbulent Times4. Minimize forecast uncertainty by placing more

focus on high volume and revenue‐generating segments

Source: L. Lapide, 2009

Techniques for Turbulent Times5. Use scenario and range forecasting to model

and represent forecast uncertainties‐Explore multiple forecasting methodsExplore multiple forecasting methods‐Measure effectiveness of each technique

0

12

Techniques for Turbulent Times6. Communicate forecast errors enterprise‐wide to

support risk management strategies in supply (e.g., hedging, buffering, and risk‐pooling)

• Incorporate into scorecard• Hold accountability with stakeholders• Identify largest errors and administer root cause analysis• Discuss with impacted team to mitigate for future

Techniques for Turbulent Times1. Stay on top of industry and departmental actions2. Look ahead for competitor actions that could impact

your business3. Look at economic conditions for leading indicators4. Evaluate your portfolio to focus on core revenue

generators5. Explore alternative forecasting methods and test results5 p o e a te at e o ecast g et ods a d test esu ts6. Communicate forecast errors and discuss root cause

0

13

VW Forecast Overview (2012)• Long term forecasts (10 years) – volume and mix

– Lifecycle management– Industry projectionsy p j– Segment projections

• Competitor launches– Economic factors– Carline growth– Pricing– Marketing– Store growthStore growth

25

VW Forecast Overview (2012)• Short term forecasts (1‐2 years) – volume and mix

– Statistical modeling from history– Subjective judgmentj j g– Regional feedback– Growth targets– Economic factors– Segment growth and share– Competitor marketing and incentives– Web traffic– Industry seasonalityIndustry seasonality

26

0

14

VW Revised Methodology – Statistical

• Baseline forecast produced using alternative statistical methods and consensus agreementmethods and consensus agreement

• Seasonal lift factors are calculated by internal and external sales history

• Remove seasonal lift factors to calculate true trendline

• Overlay seasonal trends with moving average

27

Results

• Increased trend stability due to economic modeling

• Increased collaboration with stakeholders to determine shifts in market conditions

• Promotional programs developed to meet adjusted sales targets

• Marketing strategies adjusted to respond to changes in the market

28

0

15

Results

29

Thank you