Embed Size (px)

Citation preview

For Review O

nly

Corporate Derivatives and Foreign Exchange Risk Management: A Case Study of Non-financial Firms of

Pakistan

Journal: Journal of Risk Finance

Manuscript ID: JRF-Apr-2010-0018.R3

Manuscript Type: Applied Research Paper

Keywords: Foreign Exchange Derivatives, Hedging, Foreign Exchange Exposure, Non-financial Firms, Pakistan

Journal of Risk Finance

For Review O

nly

Corporate Derivatives and Foreign Exchange Risk Management: A Case

Study of Non-financial Firms of Pakistan

Abstract

Purpose: The study aims to identify the factors affecting firms’ decision to use foreign

exchange derivative instruments by using the data of 86 non-financial firms listed on Karachi

Stock Exchange for the period 2004-2007.

Design/Methodology/ Approach: Required data is collected from annual reports of listed

firms of Karachi Stock Exchange. Non-parametric test is used to examine the mean

difference between users and non-users operating characteristics. Logit model is applied to

analyze the impact of firm’s financial distress costs, underinvestment problem, tax convexity,

profitability, managerial ownership and foreign exchange exposure on firms’ decision to use

FX derivative instruments for hedging.

Findings: Results explain that firms having higher foreign sales are more likely to use FX

derivative instruments to reduce exchange rate exposure. Moreover, financially distressed

large size firms with financial constraints and fewer managerial holdings are more likely to

use FX derivatives.

Research Limitations: Incomplete financial instrument disclosure requirements restricted

researchers to use binary variable as a dependent variable instead of notional value or fair

value of derivative usage.

Practical Implications: Study shows that in the presence of amateur derivative market,

Pakistani corporations possessing higher agency costs of debt, agency costs of equity, and

Page 1 of 22 Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

financial constraints will benefit more by defining hedging policies coherent with the firm’s

investment and financing policies in order to enhance firm value.

Originality/Value: In the presence of volatile exchange rates, until now no earlier

empirical study focused on the determinants of firm’s hedging policies in Pakistan. Current

study, therefore, attempts to identify the factors which affect the firm’s decision to use

derivative instruments for hedging foreign exchange exposure of non-financial firms of

Pakistan.

Keywords: Foreign Exchange Derivatives, Hedging, Foreign Exchange Exposure, Non-

financial Firms, Pakistan

Paper type: Research Paper

1. Introduction:

Growing globalization has encouraged many corporations to extend their businesses beyond

the geographical boundaries in order to benefit from competitive advantage and economies of

scale. Penetration into new markets has increased the firm’s profitability, on one hand, and

on the other it has also increased the variability in net income because of various financial

risks. Therefore, the managers of the multinational firms are focusing on the importance of

risk management techniques to reduce variability of their cash flows from foreign operations

due to the fluctuations in foreign exchange rates.

It is generally believed that the higher exchange rate movements and the unpredictability of

foreign sales affect the firms’ level of profitability. Therefore, managers dealing in

international operations are of the view that different trade agreements and removal of

restrictions on capital flows have increased firms’ exchange rate exposure. Additionally,

Page 2 of 22Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

majority of the countries are following floating exchange rate or variations of floating

exchange rate system, due to which estimated cash flows from their international operations

are exposed to higher exchange rate risk and thus highlights the importance of employing

different risk management techniques for hedging firms’ uncovered positions.

Asian crises in 1998 had increased the foreign exchange exposure of the countries having

large number of multinational firms, in general, and Asian countries in particular.

Depreciating currency and unstable economic and political environment in Asian countries

have increased the countries’ risk level, although lower cost of the factors of production and

untapped markets have provided many new opportunities for multinational companies.

During the past five years, Pakistani stock markets have shown higher stock price volatility

and can be characterized as among the top unstable markets. Like many other emerging

economies, in order to hedge the firm’s future cash flows, Pakistan has developed an

exchange traded derivative market for future contracts in 2006 but due to lower trading and

liquidity, corporations are reluctant to invest in derivative instruments. (SECP, 2006).

A significant increase in export and import volume of 36% and 61% respectively, has been

reported by the State bank of Pakistan, during the last five years (SBP, 2009). This increase

in foreign trade volume has shown an increasing exposure faced by corporations due to

exchange rate fluctuations. Corporations also realize that it is difficult to manage exchange

rate risk at the early stages of economic development. Thus, a growing need for employment

of different risk management techniques exists in Pakistani firms to reduce the foreign

exchange exposure. Till now, no exchange traded derivative market exists in Pakistan,

therefore, corporations are using Over the Counter market (OTC) derivative instruments to

hedge their risk exposure. In this context, derivatives, defined as off-balance sheet financial

Page 3 of 22 Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

instruments whose values are hypothetically derived from other financial assets, are widely

used by the firms to hedge their foreign exchange risk.

Existing empirical evidence has focused on examining the factors, both internal and external,

which affect the firms’ decision to hedge foreign exchange exposure (Mian, 1996; Jalivand,

1999; Haushalter, 2000; Guay and Kothari, 2003; Foo and Yu, 2005; Schiozer and Saito,

2009). However, this issue is not well-explored yet in developing and third world countries,

especially, in Pakistan. Therefore, the current study focuses on the Pakistani market to extend

the existing literature by identifying the factors affecting FX derivative usage of firms to

reduce exchange rate exposure by using sample data of 86 listed non-financial firms, for the

period of 2004-2007.

The remaining paper is organized as follows: next section discusses empirical literature,

whereas the data and methodology are presented in the third section. Empirical findings are

discussed in fourth section while the last section concludes the discussion.

2. Literature Review:

It is generally believed that shareholders are able to reduce risk by constructing a well

diversified portfolio. However, existing literature on risk management shows that

corporations are using derivative instruments to minimize firms risk exposure. According to

Modigliani and Miller (1958) under perfect capital market conditions, it is useless for a firm

to reduce risk by using derivatives. Whereas, theoretical evidence provided by Stulz (1984)

and Smith & Stulz (1985) had shown that, under certain market frictions, corporations having

specific operating characteristics like, higher financial distress costs, tax convexity, growth

opportunities, managerial holdings and liquidity constraints, have an opportunity to enhance

firm value by optimally utilizing hedging techniques.

Page 4 of 22Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

By considering investment and financing decisions in accordance with firms’ hedging

policies, Froot et al. (1993) had proved mathematically that derivatives will be beneficial for

firms in two different situations: firstly, when external financing cost exceeds opportunity

cost of internal financing and secondly, when correlation between investment expenditures

and firms’ cash flows were negative. These results were further tested by Gay and Nam

(2002) on 486 non-financial firms of U.S over the period of 1993 to1995 and empirical

findings were consistent with Froot et al. (1993).

A different justification for corporate risk management had been provided by Bessembinder

(1991) that hedging provides an incentive for the firm to decrease financial distress costs by

reducing the opportunistic behavior of equity holders. Purnanandam (2008) had empirically

tested the relationship between financial distressed firms and corporate risk management

activities on 2000 non-financial U.S firms and found that firms’ decision to use derivatives

was positively influenced by leverage whereas highly leveraged firms had lower tendency

towards derivative usage. In order to test the relationship between firms’ endogenous

policies, Lin et al. (2008) had simultaneously examined the relationship between firms

endogenous polices- leverage, growth opportunities and hedging policies, along with other

control variables, with a sample data of 495 S&P firms. They observed that highly leveraged

firms were more likely to use derivatives and highly growth oriented firms, with low debt

ratio, were also more inclined towards the derivative usage.

Graham and Rogers (2002) by taking sample data of 442 U.S non-financial firms had

calculated two tax based incentives for hedging by using derivative instruments and found

that debt tax benefit from hedging is four times more than advantage acquired from tax

convexity. In addition, study had analyzed the simultaneous effect of debt and leverage on

each other and reported a significantly positive effect on each other. Similarly, with another

Page 5 of 22 Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

sample data, Borokhovich (2004) also documented a positive and significant effect of debt

and derivative usage on each other. Borokhovich et al. (2004) had attempted to test the

relationship between board composition and derivative usage on 284 U.S non-financial firms.

By considering other control variables, they suggested that firms having larger outsiders’

holdings were more likely to use derivatives. Coefficient of size and financial constraints

were consistent with the theory whereas results depicted no relationship with

underinvestment problem.

Researchers had also explored the determinants of firms’ derivative usage. By using different

sample size of U.S non-financial firms, Mian (1996), Horang and Wei (1999) and Haushalter

(2000) had found positive effect of leverage on firms’ derivative usage for hedging purpose

whereas many studies exhibited negative relationship of debt (Nance et al., 1993; Fok et al.

1997; Geczy et al., 1997). Nance et al. (1993) and Haushalter (2000) depicted positive

coefficient for size, growth opportunities and tax convexity. Whereas, Mian (1996), Horang

and Wei (1999) observed mixed evidence for size and growth variables and tax convexity.

Mixed results for hedging substitutes and managerial ownership were reported by the

empirically studies of Nance et al. (1993), Fok et al. 1997; Horang and Wei (1999) and

Haushalter (2000).

Based on the same sample data of Australian Non-financial firms, Nguyen and Faff (2002) &

(2003) found that derivative usage was an increasing function of leverage and size, while

managerial ownership is negatively related to firms’ decision to use derivatives. Mixed

evidence was reported for growth options and hedging substitutes. By analyzing 77 non-

financial Canadian firms, Jalivand (1999) depicted a positive relationship between financial

distress hypothesis, dividend payout, convertible debt and firm’s decision to use derivative.

Page 6 of 22Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

Existing empirical evidence is mainly based on developed countries whereas a few empirical

investigations had been undertaken in Asian countries to identify the factors effecting the

firms hedging polices like Muller and Vershoor (2007) and Fizullah (2008). Former

examined the relationship of firms’ operating characteristics with the foreign exchange

exposure on 3,436 Asian firms and estimated a positive influence of size and dividend payout

on foreign exchange risk while leverage and liquidity showed a negative impact. Whereas,

the later one empirically tested 101 Malaysian firms using derivatives and found a positive

relationship between debt, tax convexity, size and firms’ decision to use derivative

techniques, whereas market to book value and dividend yield depicted a negative impact on

derivative usage.

In case of Pakistan, although researchers have tried to determine factors affecting exchange

rate of Pakistani rupee, yet no study had explored the factors, both endogenous and

exogenous, affecting the firms’ decision to use FX derivative instruments for hedging firms’

foreign exchange rate risk in Pakistan. Current paper aims to fill this gap by investigating the

factors influencing firm’s decision to use FX derivatives by using the data of 86 listed non-

financial firms of Pakistan for the period 2004-2007. Moreover, it is also expected that

present study may help in providing additional guidelines to decision makers in managing the

firm’s foreign exchange risk exposure by simultaneously planning firm’s investment and

financing policies with firm’s hedging policies.

3. Data and Methodology:

Following Nguyen & Faff (2002), the study aims to identify the impact of financial distress

costs, underinvestment costs, tax convexity, managerial incentives and other control variables

on firm’s decision to use FX derivative to reduce foreign exchange rate risk. It is assumed

that firms use derivatives to hedge foreign exchange exposure, hence, in order to test whether

Page 7 of 22 Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

firms use FX derivatives to hedge risk exposure or not, Logit model is used with a value

‘one’ for users and ‘zero’ for non-users.

In order to test empirically the factors affecting the firm’s decision to use FX derivatives

instruments, a sample data of 86 non-financial firms are taken for the period of 2004-2007.

Data is collected from annual reports of non-financial firms listed on Karachi Stock

Exchange and prices data is gathered from official website of Karachi Stock Exchange.

According to International Accounting Standards (IAS) 32 and 39, it is mandatory for firms

to disclose their usage of hedging instruments and their respective fair value in the notes of

annual reports in a uniform manner. Almost 60% of the sample firms declared their usage of

foreign currency derivatives. Financial sector has been excluded from the sample data since

their business activities require derivatives to be used for trading purpose or speculative

motive.

For detailed comparison between operating characteristics of firms that consider hedging as a

value enhancing activities to those firms whose operating distinctiveness does not consider

derivative usage as a feasible activity, sample data has been divided into two sub-groups. One

group is classified as users and other as non-users. Non-parametric Univariate test is used to

test the mean difference between the operating characteristics of users and non-users. In order

to identify the determinants of firm’s hedging policies, Logit Model is used. Model 1 depicts

that derivative usage is a function of financial distress costs, tax convexity, asset growth cash

flow, profitability, managerial ownership and foreign sales.

DERIVit = α + β1FDCit + β2INCit + β3SIZEit + β4AGCFit + β5 ROAit +

β6MNGRLit + β7 TAXit + β8 LFSit + eit ….……. (1)

Where,

Page 8 of 22Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

DERIV = dummy one if firm is a FX derivative user and zero otherwise.

FDC = ratio of tangible assets over total assets, representing financial distress costs.

INCOV = ratio of earning before interest and taxes by interest expense, representing

interest coverage ratio.

SIZE = log of total assets, representing size.

AGCF = ratio of addition of change in tangible assets plus depreciation to net income

plus depreciation, representing firm’s ability to convert growth options into assets in

place.

ROA = ratio of earning after interest and taxes by total assets, representing

profitability.

MNGRL = log of managerial holdings, representing managers ownership in firm.

TAX = binary value 1 for unused tax losses and 0 otherwise, representing tax

convexity.

LFS= log of foreign sales, representing foreign exchange exposure.

Whereas, model 2 observed the interaction between firm’s FX derivative usage and its

investment and financing policies following Mian (1996), Lin et al. (2008) and Bartam et al.

(2009).

DERIVit = α + β1LEVit + β2MTBit + β3DPit + β4QRit + eit ………. (2)

Where,

Page 9 of 22 Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

LEV = ratio of total debt to total assets, representing leverage.

MTB = ratio of market value of firm to book value of firm, representing growth

options.

DP = ratio of dividend per share to earning per share, representing dividend payout

ratio.

QR = ratio of subtraction of current assets minus inventory to current liabilities,

representing liquidity.

4. Findings and Analysis:

i. Univariate Analysis:

Table 1 shows descriptive statistics of users and non-users of FX derivatives; standard

deviation is in parenthesis. Univarite analysis explains that users have significantly higher

financial distress costs with mean value of 0.4780 as compared to non-users. Leverage,

calculated by taking ratio of total debt over total assets, is lower for the users though mean

difference is not statistically significant. Users, on average have 0.5804 leverage ratio,

whereas non-users demonstrate mean value of 0.6244. Inconsistent with the theory of

financial distress costs, derivative users are characterized as low debited firms, though they

are able to pay their finance costs but still the additional debt will lead a firm to higher

financial distress costs and it may be costly for a firm to adopt risk management techniques in

such situations. Another measure of firms’ financial distress cost is its interest coverage ratio,

ability of a firm to pay its finance costs, parallel with the theory, users are less competent to

pay its interest costs due to financial constraints and hence employ derivatives as hedging

instruments. Aligned with the Pakistan’s derivative market situation and economies of scale

Page 10 of 22Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

hypothesis, users are identified as large size firms with a value of 6.3332 in comparison with

non-users that document an average size of 6.2800. Mann-Whitney U test show that users and

non-users are statistically different from each other in terms of size.

Firm’s growth opportunities are observed by taking ratio of market value of firm to book

value of firm. Contradictory to theory, users show on average less growth opportunities,

having a mean value of 1.1540, which is lower than average value of non-users; 1.2864.

According to pecking order theory, if firms encounter positive NPV projects then they are

more likely to finance their tasks through internally generated funds. Therefore, corporations

having growth opportunities are more probable to issue debt and thus tend less towards using

FX derivative instruments due to of high transactions costs. Moreover, less growth oriented

firms have little foreign exchange exposure thus less likely to use foreign currency hedging

instruments.

Theory predicts that firms’ ability to finance its growth opportunities provides them an

incentive to use hedging instruments. Consistent with theory, by taking ratio of change in net

tangible assets plus depreciation to net income plus depreciation, reveals that users are less

able to finance its growth opportunities with a mean value of 0.9654 in comparison with non-

users which are on average only 0.4490 incapable in financing their growth opportunities.

Mean difference test of asset growth over cash flow shows that users and non-users are

significantly different from each other.

Page 11 of 22 Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

Table 1 : Univariate Analysis

Variables

Mean

Non-User (140)

Mean

User (204)

Mann-Whitney U test

FDC

.5921

(.4317)

.4780

(.2137)

-3.335

(.001)**

LEV

.6244

(.5139)

.5804

(.2125)

-.870

(.384)

INC

4.7916

(3.7856)

4.0418

(3.2221)

-.853

(.394)

SIZE

6.2800

(.6690)

6.3332

(.9391)

-2.340

(.019)**

MTB

1.2846

(.7931)

1.154

(.5812)

-1.979

(.048)**

AGCF

.4490

(.7169)

.9654

(1.3995)

-3.660

(.000)***

ROA

6.9357E-02

(.1213)

5.1372E-02

(7.11E-02)

-.222

(.824)

DP .5487 .1925 -.709

Page 12 of 22Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

(2.4462) (1.2714) (.478)

QR

4.1415

(3.3618)

2.6851

(2.3274)

-5.577

(.000)***

MNGRL

.5256

(.2991)

.7101

(.2174)

-1.381

(.167)

TAX

.4500

(.4992)

.3970

(.4904)

-.976

(.329)

LFS

1.4888

(2.3763)

3.5456

(2.7339)

-.6727

(.000)***

***,**,* are 1%, 5% and 10% respectively

Similarly, coherent with the expected coefficients for liquidity and profitability, it is found

that users have lower level of profitability and liquidity. Users are identified on average

5.13% profitable, whereas non-users are more profitable firms with the mean value of 6.93%.

Nevertheless, mean difference of users and non-users are not statistically significant.

Moreover, users are identified as liquidity constrained firms with the mean value of 2.6851 in

comparison with non-users, having an average value of 4.1451. In this case, Mann-Whitney

U test shows that users and non-users are significantly different in terms of liquidity.

Contradictory to the theory of substitutes of hedging, firms with lower dividend payout ratio

are characterized as user of hedging instruments. Supporting financial distress hypothesis,

Page 13 of 22 Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

users report that non-users have higher dividend payout ratio of 54.87%, whereas users have

19.25% dividend payout ratio, as lower dividend payout firms perceive themselves riskier

because of highly invariable cash flows, hence, they use hedging instruments to reduce

financial distress costs by minimizing cash flow unpredictability. However, mean difference

test demonstrate statistically insignificant difference between dividend payout ratio of both

the groups.

According to agency cost of equity, managers having higher equity stake are more probable

to use derivative in best interest of firm as it will ultimately affect firm value. Hence,

consistent with the theory, users have higher managerial ownership with the mean value of

0.7101 while non-users document an average value of 0.5256, nevertheless, the mean

difference for both groups is not statistically significant. A dummy variable is used to

measure tax convexity. Contradictory to expectations, non-users show higher tax losses with

the mean value of 0.45 in contrast with users which have 39.7% tax losses. This might be due

to the infant status of Pakistani derivative market. Main (1996) considering sample data of

3022 firms observed hedgers as having lower tax losses.

It is expected that firms’ need to hedge risk exposure is directly proportional to its foreign

exchange exposure which is supported by our findings. Users of hedging instruments are

found to be having more foreign currency exposure with the mean value of 3.5456, whereas,

non-users report an average value of 1.4888 of foreign sales. Mean difference results show

that users are significantly different from non-users in terms of foreign exchange exposure.

Generally, users are identified as a financially distressed large size firms with the lower debt

ratio and growth opportunities. In addition, financially constrained firms having high foreign

Page 14 of 22Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

exchange exposure and larger managerial ownership are characterized as the user of

derivative instruments for hedging purpose.

Correlations coefficients are presented in Table 2. Firms’ operating characteristics are divided

into two groups. Correlation results of Group A, excluding all investment and financing

variables, explain that profitable firms are large in size, have higher interest coverage ratio,

more ability to convert its growth options into assets in place and lower managerial

ownership; which is consistent with the theory. In addition, firms having higher financial

distress costs have lower interest coverage ratio as it is difficult for them to fulfill their

obligations. Group B reports correlation coefficients for firms’ endogenous polices which

supports the theory that financially constrained firms are more likely to take debt for their

investments.

Table 2: Correlation Matrix

Group A

FDC INC SIZE AGCF ROA MNGRL TAX LFS

FDC 1.00

INC -0.24 1.00

SIZE 0.07 0.05 1.00

AGCF 0.07 -0.07 0.03 1.00

ROA 0.08 0.35 0.23 -0.06 1.00

MNGRL 0.11 -0.15 -0.19 0.10 -0.18 1.00

TAX 0.28 -0.27 0.10 0.11 -0.18 0.01 1.00

LFS 0.01 -0.13 0.11 0.09 -0.07 -0.04 0.13 1.00

Page 15 of 22 Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

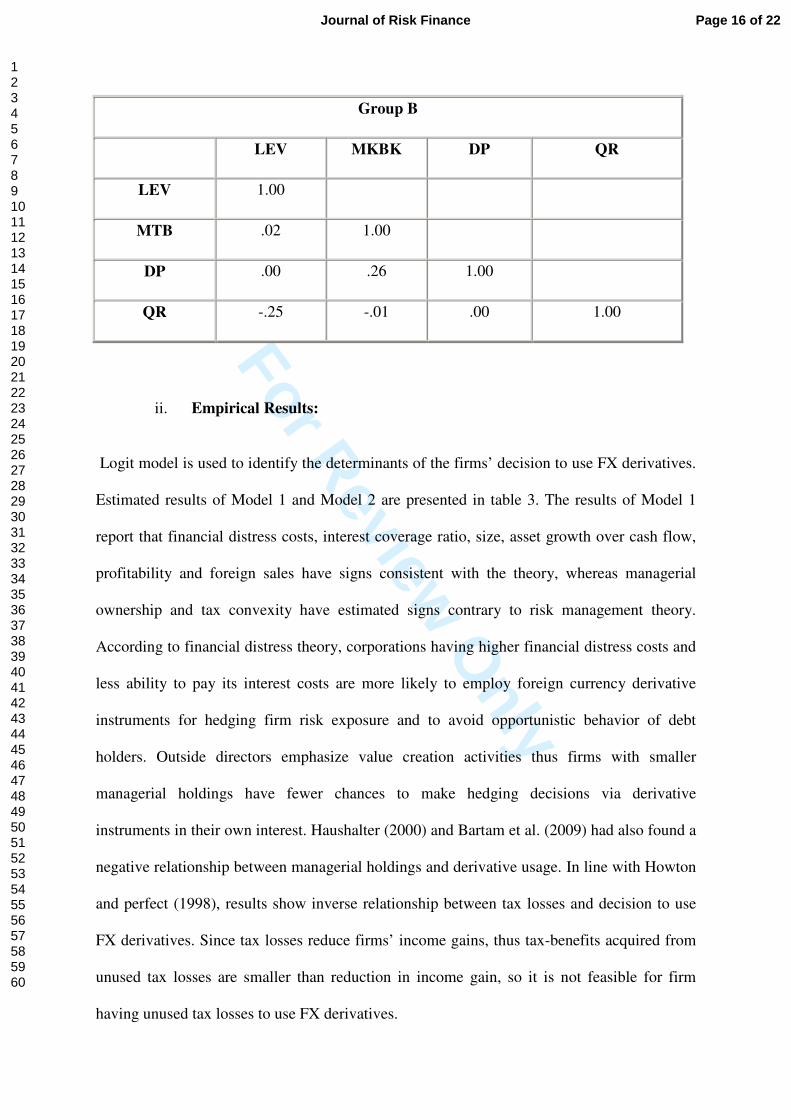

Group B

LEV MKBK DP QR

LEV 1.00

MTB .02 1.00

DP .00 .26 1.00

QR -.25 -.01 .00 1.00

ii. Empirical Results:

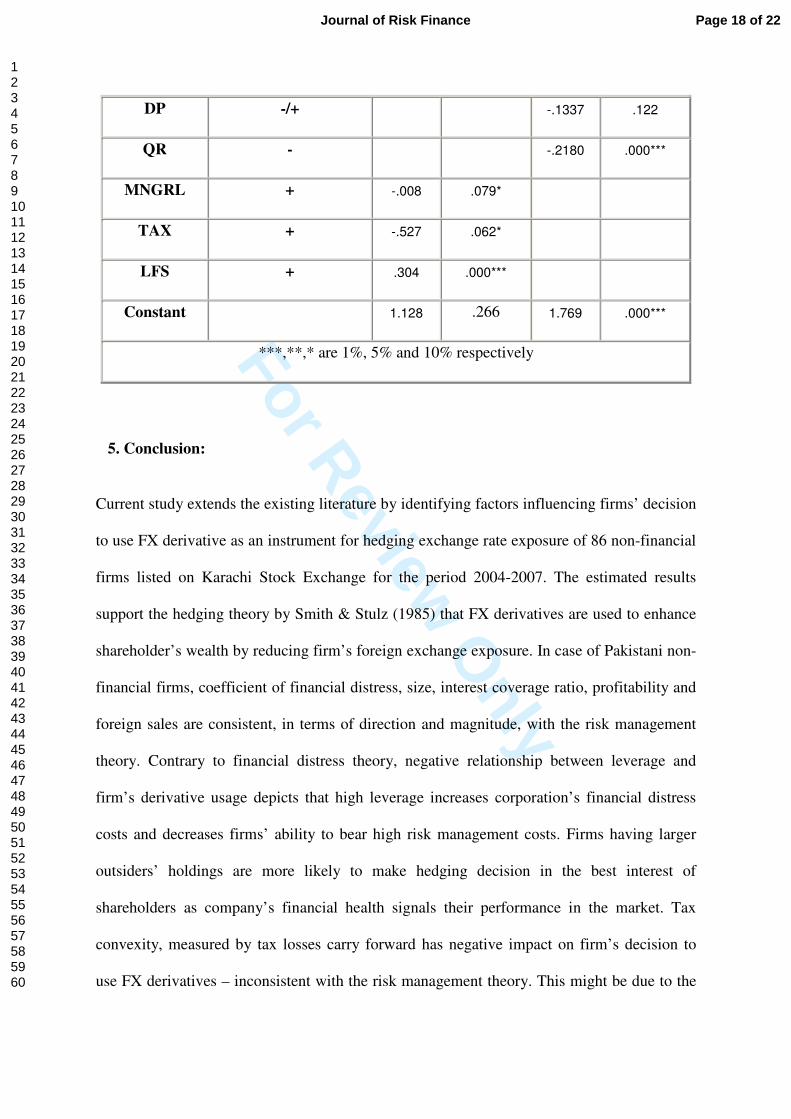

Logit model is used to identify the determinants of the firms’ decision to use FX derivatives.

Estimated results of Model 1 and Model 2 are presented in table 3. The results of Model 1

report that financial distress costs, interest coverage ratio, size, asset growth over cash flow,

profitability and foreign sales have signs consistent with the theory, whereas managerial

ownership and tax convexity have estimated signs contrary to risk management theory.

According to financial distress theory, corporations having higher financial distress costs and

less ability to pay its interest costs are more likely to employ foreign currency derivative

instruments for hedging firm risk exposure and to avoid opportunistic behavior of debt

holders. Outside directors emphasize value creation activities thus firms with smaller

managerial holdings have fewer chances to make hedging decisions via derivative

instruments in their own interest. Haushalter (2000) and Bartam et al. (2009) had also found a

negative relationship between managerial holdings and derivative usage. In line with Howton

and perfect (1998), results show inverse relationship between tax losses and decision to use

FX derivatives. Since tax losses reduce firms’ income gains, thus tax-benefits acquired from

unused tax losses are smaller than reduction in income gain, so it is not feasible for firm

having unused tax losses to use FX derivatives.

Page 16 of 22Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

Empirical results of model 2 support our earlier results of univariate analysis. Similar to

Nance et al. (1993), Fok et al. (1997) and Geczy et al. (1997), leverage depicts a significant

negative effect on firms’ likelihood of derivative usage. Hence, proving that high debt leads

firm to more financial distress and increases its cost of hedging, therefore making it difficult

for a leveraged firm to bear higher risk management costs. Dividend payout ratio shows a

negative effect on firms’ derivative usage, supporting signaling theory. Firms having

volatility in cash flows are more likely to cut dividend amounts in advance so that at the end

of fiscal year lower dividend payout ratio signals a weak financial position of firm; consistent

with Haushalter (2000). Generally, large size financially distressed firms, having lower

leverage, dividend payout ratio, liquidity, managerial ownership, profitability and tax

convexity are more likely to use derivative instruments for hedging purpose.

Table 3: Logit Regression

Variables Predicted signs Model 1 Model 2

Coeff. P-Value Coeff. P-Value

FDC - -2.743 .000***

LEV + -.933 .036**

INC - -.011 .026**

SIZE -/+ .123 .427

MTB + -.0235 .519

AGCF + .087 .023**

ROA - -3.122 .066*

Page 17 of 22 Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

DP -/+ -.1337 .122

QR - -.2180 .000***

MNGRL + -.008 .079*

TAX + -.527 .062*

LFS + .304 .000***

Constant 1.128 .266 1.769 .000***

***,**,* are 1%, 5% and 10% respectively

5. Conclusion:

Current study extends the existing literature by identifying factors influencing firms’ decision

to use FX derivative as an instrument for hedging exchange rate exposure of 86 non-financial

firms listed on Karachi Stock Exchange for the period 2004-2007. The estimated results

support the hedging theory by Smith & Stulz (1985) that FX derivatives are used to enhance

shareholder’s wealth by reducing firm’s foreign exchange exposure. In case of Pakistani non-

financial firms, coefficient of financial distress, size, interest coverage ratio, profitability and

foreign sales are consistent, in terms of direction and magnitude, with the risk management

theory. Contrary to financial distress theory, negative relationship between leverage and

firm’s derivative usage depicts that high leverage increases corporation’s financial distress

costs and decreases firms’ ability to bear high risk management costs. Firms having larger

outsiders’ holdings are more likely to make hedging decision in the best interest of

shareholders as company’s financial health signals their performance in the market. Tax

convexity, measured by tax losses carry forward has negative impact on firm’s decision to

use FX derivatives – inconsistent with the risk management theory. This might be due to the

Page 18 of 22Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

inappropriate measure for tax convexity and the fact that cost of risk management exceeds the

tax deductible benefit of unused tax losses. Unexpected coefficient of dividend payout though

inconsistent with the hedging theory but still supports the signaling theory. Growth options

though shows positive effect on firm’s hedging policies, have insignificant effect on firm’s

derivative usage to hedge exchange rate risk. Study also attempts to examine the relationship

between corporate FX derivative usage and firm’s foreign exchange exposure, and a

significant positive relationship between firm’s foreign sales and their decision to use FX

derivatives to hedge FX exposure is reported, despite of illiquid and amateur Pakistani

derivative market.

The estimated results provide the policy guidelines to the Pakistani firms having foreign

exchange transactions, that the optimal usage of FX derivative instruments may enable them

to smooth their future cash flows by reducing opportunistic behavior of shareholders and

managers, hence, minimizing the agency costs of debt and equity. The findings of current

empirical investigation also suggest that the policy makers should develop a well-organized

exchange traded derivative market in Pakistan for the benefit of financially constrained firms

with highly variable cash flows and foreign sales. The study also highlights that effective

usage of derivative instruments may enable corporations to define their hedging policies that

are compatible with firm’s internal investment and financing policies. Therefore, properly

planned and implemented investment, financing and hedging policies, will not only facilitate

firms in achieving their primary goal of shareholders’ wealth maximization, but may also

enhance economic stability. The current study has identified the factors affecting the firm’s

decision to use FX derivative instruments; however, future research could be focused on

determining the factors influencing the usage of interest rate derivative instruments and

extent of such derivative usage.

Page 19 of 22 Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

References:

Bartram, S.M, and G.W, Brown and F.R, Fehle. (2009), “Interantional Evidence on Financial

Derivative Usage”, Financial Management, pp.185-206.

Berkman, H and M E, Bradbury. (1996), “Empirical Evidence on the Corporate Use of Derivatives”

Financial Management, Vol. 25, No. 2, pp.5-13.

Bessembinder, Hendrik. (1991), “Forward Contracts and Firm Value: Investment Incentive and

Contracting Effects”, The Journal of Financial and Quantitative Analysis, Vol. 26, No.4, pp.519-532.

Borokhovich, K.A, and K.R, Brunarski, and Crutchley, C.E and Simkins, B.J. (2004), “Board

Composition and Corporate Use Of Interest Rate derivatives”, The Journal of Financial Research, Vol.

XXVII, No. (2), pp. 199-216.

Faziullah, M and N.A, Azizan and T.S, Hui. (2008), “The Relationship between Hedging Through

Forwards, Futures & Swaps and Corporate Capital Structure in Malaysia”, Presented at Second

Singapore International Conference on Finance (SSIF), Organized by Saw Center for Financial Studies

and Department of Finance NUS on 17-18 July, Singapore.

Fok, R, C-W and C, Carroll and m C, Chiou. (1997), “Determinants of Corporate Hedging and

Derivatives: A Revisit”, Journal of Economics and Business, Vol. 49, pp. 569-585.

Froot, Kenneth A. and Scharfstein, David S. and Stein, Jeremy C. (1993), “Risk Management:

Coordinating Corporate Investment and Financing Policies”, The Journal of Finance, Vol. 4, No.5, pp.

1629-1658.

Gay, G.D and J, Nam. (1998), “The Underinvestment Problem and Corporate Derivatives Use”,

Financial Management, Vol. 27, No. 4, pp. 53-69.

Geczy, C and B A Minton and C Schrand. (1997), “Why Firms Use Currency Derivatives”, The

Journal of Finance, Vol. 52, No. 4, pp. 1323-1354.

Page 20 of 22Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

Graham, J.R and D.A, Rogers. (2002), “Do Firms Hedge in Response to Tax Incentives?”, The Journal

of Finance, Vol. 57, No. 2, pp.815-839.

Guay, W and S.P, Kothari. (2003), “How much do firms hedge with derivatives?”, Journal of

Financial Economics, Vol. 70, pp. 423-461.

Haushalter, G.D. (2000), “Financing Policy, Basis Risk, and Corporate Hedging: Evidence from Oil

and Gas Producers”, The Journal of Finance, Vol. 55, No. 1, pp. 107-152.

Horng, Y-S and P, Wei. (1999), “An empirical study of the derivative use in the REITs industry”, Real

Estate Economics, Vol. 27, No. 3, pp. 561-587.

Howten, S and S Perfect. (1998), “Currency and Interest rate Derivatives use in U.S Firms”, Financial

Management, Vol. 27, No. 4, pp. 111-121.

Jalilvand, A. (1999), “Why Firms Use Derivatives: Evidence from Canada”, Canadian Journal of

Administrative Science, Vol. 16, No. 3, pp. 213-228.

Lin, C.M and Richard, D.P and Stephen, D.S. (2008), “Hedging, financing, and investment decisions:

Theory and empirical tests”, Journal of Banking & Finance, Vol. 32, pp. 1566-1582.

Mian, S.L. (1996), “Evidence on Corporate hedging policy”, Journal of Financial and Quantitative

Analysis, Vol. 31, No. 3, pp. 419-439

Modigliani, Franco and Miller, Marton H. (1958), “The Cost of Capital, Corporation Finance and The

Theory of Investment”, American Economic Review, Vol. XLVIII, No. 3, pp. 261-297.

Muller, A and W, F.C, Verschoor. (2007), “Asian foreign exchange risk exposure”, J. Japanese Int.

Economies, Vol. 21, pp. 16-37.

Nance, D.R and Smith, C.W and Smithson, C.W. (1993), “On the Determinants of Corporate

Hedging”, The Journal of Finance, Vol. XLVIII, No. 1, pp. 267-284.

Nguyen, H and R Faff. June(2002), “On the Determinants of Derivative Usage by Australian

Companies”, Australian Journal of Management, Vol. 27, No. 1, pp. 1-24

Page 21 of 22 Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

For Review O

nly

Nguyen, H and R Faff. (2003), “Further Evidence on the Corporate Use of Derivatives in Australia:

The Case of Foreign Currency and Interest Rate Instruments”, Australian Journal of Management, Vol.

28, No. 3, pp. 307-318

Purnanandam, Amiyatosh. (2008), “Financial distress and Corporate risk management: Theory and

evidence”, Journal of Financial Economics, Vol. 87, pp. 706-739

SBP. (2009), “Balance of Payment- Imports”, available at: http://www.sbp.org.pk/Ecodata/BOP-

Services/GoodsImport.pdf (accessed 25th

septermber 2009).

SBP. (2009), “Balance of Payment- Exports”, available at: http://www.sbp.org.pk/Ecodata/BOP-

Services/goodsExport.pdf (accessed 25th

septermber 2009).

SECP. (2006), “Report on the Feasibility of Exchange Traded Derivatives Market in Pakistan”,

available at: http://www.secp.gov.pk/Reports/FinalReport_TradedDerivatives.pdf, (accessed 25th

septermber 2009).

Schiozer, R.F and R, Saito. (2009), “The Determinants of Currency Risk Management in Latin

American Non-financial Firms”, Emerging Markets Finance & Trade, Vol. 45, No. 1, pp. 49-71.

Smith, Clifford W and Stulz, Rene M. (1985), “The Determinants of Firms’ Hedging Policies”, Journal

of Financial and Quantitative Analysis, Vol. 20, No. 4, pp. 391-405.

Stulz, Rene. M. (1984), “Optimal Hedging policies”, Journal of Financial and Quantitative policies,

Vol. 19, No. 2, pp. 127-140.

Warner, Jerold. (1977), “Bankruptcy Costs: Some Evidence”, Journal of Finance, Vol. 32, pp. 337-

348.

Page 22 of 22Journal of Risk Finance

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960