Embed Size (px)

Citation preview

Half Year Results Presentation

29 December 2013

For

per

sona

l use

onl

y

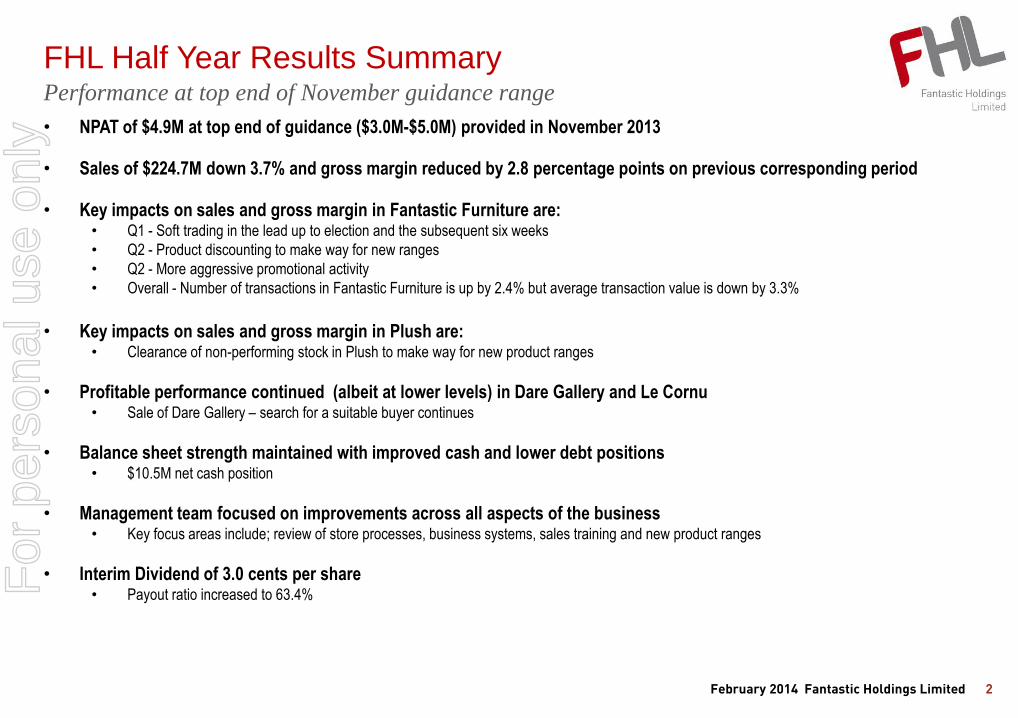

FHL Half Year Results Summary

2 February 2014 Fantastic Holdings Limited

Performance at top end of November guidance range

• NPAT of $4.9M at top end of guidance ($3.0M-$5.0M) provided in November 2013

• Sales of $224.7M down 3.7% and gross margin reduced by 2.8 percentage points on previous corresponding period

• Key impacts on sales and gross margin in Fantastic Furniture are:

• Q1 - Soft trading in the lead up to election and the subsequent six weeks

• Q2 - Product discounting to make way for new ranges

• Q2 - More aggressive promotional activity

• Overall - Number of transactions in Fantastic Furniture is up by 2.4% but average transaction value is down by 3.3%

• Key impacts on sales and gross margin in Plush are: • Clearance of non-performing stock in Plush to make way for new product ranges

• Profitable performance continued (albeit at lower levels) in Dare Gallery and Le Cornu • Sale of Dare Gallery – search for a suitable buyer continues

• Balance sheet strength maintained with improved cash and lower debt positions • $10.5M net cash position

• Management team focused on improvements across all aspects of the business • Key focus areas include; review of store processes, business systems, sales training and new product ranges

• Interim Dividend of 3.0 cents per share • Payout ratio increased to 63.4% F

or p

erso

nal u

se o

nly

Trading Performance – (Delivered Sales) New Stores

Total sales: *$229.3M -3.9%, L4L –6.2%

Fantastic Furniture: Total Sales -0.9%, L4L Sales -3.6%

Plush: Total Sales -18.8%, L4L Sales -21.0%

OMF: Total Sales +8.0%, L4L Sales +8.1%

Dare Gallery: Total Sales -8.5%, L4L Sales -9.4%

Le Cornu: Total Sales -6.8%, L4L Sales -6.8%

Both Fantastic Furniture and Plush had positive L4L written sales in December and January

*Includes only retail sales at company stores and franchisees and is exclusive of GST

Net 2 stores opened since June 2013,

FF: 2 new stores, total stores: 77 (2 franchise)

Plush: nil, total stores: 33

OMF: nil, total stores: 15

Dare Gallery: nil, total stores: 11 (1 franchise)

Le Cornu: nil, total stores: 2

138 stores now in operation (inc 3 franchise stores)

Management Initiatives Financial Management

• The leadership team is progressing on a number of initiatives to strengthen business

foundations and improve stability. Key areas include:

• Company structure - aligning staff to most appropriate roles, store based

operational training, establishment of China manufacturing joint venture,

review of business processes, systems (system rollout), FF business unit

integration

• Reducing the CODB across the business - including project initiatives around

supply chain, back office efficiency and procurement with savings expected to

flow in FY15

• Reviewing product profitability for optimal product returns

• Reviewing product range to provide customers with a more compelling offer

Improved cash balance and lower debt position

• Strong balance sheet with cash position of $28.2 million compared to a debt position of

$17.7 million.

• Return on Equity decline from 11.6% to 4.4% with lower trading profits for the half year

Strategic Review Progress

• Leadership team undertaking a business review across the Group

• Dare Gallery is currently on the market. Search for a suitable buyer continues

Operational Highlights

3 February 2014 Fantastic Holdings Limited

Management initiatives being introduced to improve performance across the business

For

per

sona

l use

onl

y

(1) Includes only retail sales at company owned and franchise stores and is inclusive of GST

(2) Gross margin recorded excludes other income such as franchise fees, property rental and profit on sale of property

All calculations have been computed based on actual numbers.

Financial Summary

4

Delivered performance within guidance range

KEY MESSAGES

• Sales decline largely due to lower average transaction value

in Fantastic Furniture and Plush and reduced number of

transactions in Plush due to incomplete product ranging

• Gross Margin decline due to stock clearance activity and

discounting in Fantastic Furniture and Plush

• CODB increased due to additional property costs associated

with new stores, higher advertising cost, further investments

in international manufacturing as well as increased

depreciation associated with completion of the Dandenong

property development

• Operating cash flows declined reflecting lower sales

• Interim dividend of 3.0 cents per share with payout ratio

increased to 63.4%

Profit After Tax

(2010-2014) Half Year Ended Dec 12 Dec 13 Change

Company and Franchise Sales (1) $ $261.1M $253.8M (2.8%)

LFL Sales % 1.8% (6.2%) (8.0pts)

Statutory Sales $ $233.4M $224.7M (3.7%)

Gross Margin $ $113.0M $102.4M ($10.6M)

Gross Margin % 48.4% 45.6% (2.8pts)

CODB $ $96.6M $99.2M $2.6M

CODB % of sales 41.4% 44.2% 2.8pts

EBITDA $ $21.3M $11.4M ($9.9M)

EBIT $ $17.8M $7.2M (59.5%)

EBIT % of Sales 7.6% 3.2% (4.4pts)

Net Profit After Tax $ $13.5M $4.9M (63.8%)

Net Profit After Tax % of Sales 5.8% 2.2% (3.6pts)

Operating Cash Flow $ $17.2M $8.1M (52.6%)

Store Numbers 134 138 4

EPS (cents) 13.08c 4.73c (63.8%)

Half Year Dividend per Share (cents) 7.50c 3.00c (60.0%)

Return on Equity % 11.6% 4.4% (7.2pts)

$M

February 2014 Fantastic Holdings Limited

12.8

9.8

13.2 13.5

4.9

0.0

3.5

7.0

10.5

14.0

17.5

HY 2010 HY 2011 HY 2012 HY 2013 HY 2014

For

per

sona

l use

onl

y

Business Performance – Sales & Gross Margin

5

Half Year to

Dec 12

Dec 13

Change

Gross Sales*

(inc franchisees) $261.1M $253.8M (2.8%)

Statutory Sales $233.4M $224.7M (3.7%)

LFL Sales % 1.8% (6.2%) (8.0pts)

Margins impacted by discounting to clear non-performing stock

Re

ve

nu

e

($M

)

• Clearance of non performing stock at reduced prices occurred in the six months to Dec13 in both Plush and Fantastic Furniture

• Whilst the number of transactions has increased in Fantastic Furniture, lower average transaction values over the half year resulted in gross margin reduction

KEY MESSAGES

Half Year to

Dec 12

Dec 13

Change

Gross Margin %

48.4%

45.6%

(2.8pts)

Gro

ss M

arg

in

(%)

•Includes only retail sales at company owned and franchise stores and is inclusive of GST

All calculations have been computed based on actual numbers

February 2014 Fantastic Holdings Limited

225 215

221 228

233

150

175

200

225

250

HY 2010 HY 2011 HY 2012 HY 2013 HY 2014

48.3%

46.3% 46.2%

48.4%

45.6%

43.0%

45.0%

47.0%

49.0%

HY 2010 HY 2011 HY 2012 HY 2013 HY 2014

For

per

sona

l use

onl

y

6

Business Performance – Sales Analysis

KEY MESSAGES

• Notwithstanding like for like being down compared to the prior comparative period, Fantastic Furniture and Plush had positive like for like sales in December 2013 and

January 2014

• Fantastic Furniture was impacted by a lower average transaction value and clearance of inventory to make way for new ranges

• Plush sales reflected the incomplete product ranges and the significant clearance and discounting to clear non performing stock

• Le Cornu has been impacted by a slowdown due to difficult market conditions in Adelaide

TOTAL HEADLINE SALES BY PERIOD

$M FY13 FY14 %Variance

1st Half 1st Half HY14 v.s .HY13

FF 165.4 164.0 (0.9%)

Plush 30.8 25.0 (18.8%)

OMF 6.6 7.1 8.0%

Dare 14.4 13.1 (8.5%)

Le Cornu 21.5 20.1 (6.8%)

Total 238.7 229.3 (3.9%)

1st Half FY13 & 1st Half FY14 (L4L Sales Analysis)

% 1H13 1H14 Variance

FF 1.2% (3.6%) (4.8pts)

Plush (6.1%) (21.0%) (14.9pts)

OMF (0.2%) 8.1% 8.3pts

Dare 3.5% (9.4%) (12.9pts)

Le Cornu 11.2% (6.8%) (18.0pts)

Total 1.8% (6.2%) (8.0pts)

Sales for major retail brands have improved in the later part of the half year

•Includes only retail sales at company owned and franchise stores and is exclusive of

GST. This excludes other minor sales not flowing through stores

All calculations have been computed based on actual numbers

February 2014 Fantastic Holdings Limited

For

per

sona

l use

onl

y

Business Performance – Cost of Doing Business

7

HY 2010 HY 2011 HY 2012 HY 2013 HY 2014

Statutory Sales

($M) 214.7 220.6 227.6 233.4 224.7

CODB ($M) 83.8 90.2 93.7 96.6 99.2

CODB / Sales (%) 39.0 40.9 41.2 41.4 44.2

Sales growth has not kept pace with increased costs – a key focus area for management

KEY MESSAGES

• CODB increased due to increased property costs associated with new stores, higher advertising cost, further investments in international manufacturing as well as

increased depreciation associated with completion of the Dandenong property development

• Recurring cost increases include property cost increases CPI, depreciation expenses as a result of IT amortisation costs and Dandenong depreciation

• Costs associated with investment include e-commerce, investment in new stores (Chullora NSW, Burleigh Heads QLD) and set up costs associated with

international manufacturing which are expected to be future revenue generating

• One off costs include stock writedowns of $1.7m and write off of fixed assets of $500k

February 2014 Fantastic Holdings Limited

37%

38%

39%

40%

41%

42%

43%

44%

45%

50.0

60.0

70.0

80.0

90.0

100.0

HY 2010 HY 2011 HY 2012 HY 2013 HY 2014

CO

DB

/ S

ale

s

CO

DB

$M

CODB CODB/Sales

For

per

sona

l use

onl

y

• EBITDA result of $11.4M for the 6 months to Dec 13 down $9.9M on prior comparative period with a multi-pronged approach to recovery in place across:

Sales – New product ranges due to land from Jan 2014 in Fantastic Furniture, which are designed to deliver improved average transaction value outcomes.

Additional sales training is been rolled out across the business

Margin – Integrated margin analysis completed for Fantastic Furniture. Product total returns now being analysed with product ranging strategies. Sales

commission model modified to be based on gross profit margins

CODB – Extensive tender program underway covering procurement contracts / services over $100k pa. Comprehensive supply chain modeling currently being

undertaken. Integration / simplification of the Fantastic Furniture business to deliver an efficient business model is nearing completion

Financial Performance – EBITDA

8

EBITDA impacted by sales decline and margin reductions

KEY MESSAGES

EB

ITD

A (

$M

)

HY 2010 HY 2011 HY 2012 HY 2013 HY 2014

Statutory Sales

($M) 214.7 220.6 227.6 233.4 224.7

EBITDA($M) 20.2 16.3 20.6 21.3 11.4

EBITDA / Sales

(%) 9.4 7.4 9.1 9.1 5.1

* CODB excludes depreciation and amortisation

February 2014 Fantastic Holdings Limited

21.3

11.4

4.3

6.3

2.7 2.0

0.0

5.0

10.0

15.0

20.0

25.0

Dec-12 Margin - Volume

Margin - Mix Increase in Other Income

Increase in CODB

Dec-13

EBITDA

For

per

sona

l use

onl

y

Balance Sheet

9

Balance sheet strengthened with net cash position recorded

KEY MESSAGES

As at Jun 13 Dec 13 Mvt (M) Mvt (%)

Cash ($M) 19.0 28.2 9.2 48.4%

Inventory ($M) 74.5 76.1 1.6 2.1%

Investment Properties ($M) 30.1 24.9 (5.2) (17.2%)

Intangibles ($M) 9.4 8.8 (0.6) (6.3%)

Interest Bearing Loans ($M) 25.3 17.7 (7.6) (30.0%)

Net Assets ($M) (2) 108.1 113.1 5.0 4.6%

Net Debt ($M) (1) (6.3) 10.5 16.8 n/a

Net Debt / Equity (%) 5.9% n/a (1) n/a

Return on Equity (%) 12.5% 4.4% (3) n/a

• Significant progress achieved to reduce the build up of aged and slow moving inventory across major retail brands to provide an efficient working capital base and

increase the stock turns on inventory

• Increase in cash due to settlement of the Campbelltown property for $12M

• Repayment of the Campbelltown property loan of $6.9M and reduction of the Le Cornu debt facility of $0.7M occurred in the period

• FHL owns three properties as at December 2013: Dandenong (VIC), Newcastle (NSW) and Rockhampton (QLD) with a total book value of $28.0M

All calculations have been computed based on actual numbers

February 2014 Fantastic Holdings Limited

(1) Cash at Dec 13 has been positive against the debt position

(2) Includes non-controlling interest

(3) Reflects only six months performance

For

per

sona

l use

onl

y

• Store number movement in the period:

- Fantastic Furniture opened 2 stores; Chullora (NSW) and Burleigh

Heads (QLD)

- Focus of new stores to be on new geographic corridors – without

cannibalisation of existing store networks

Business Performance – Store Network Growth

NSW VIC QLD WA OTHER TOTAL

FF 35 19 10 6 7 77(1)

Plush 13 12 4 - 4 33

OMF 14 - - - 1 15

Dare 2 7 2 - - 11

Le Cornu - - - - 2 2

Total 64 38 16 6 14 138

Network of Stores

(as at 29 December 2013)

Dominating presence in the key markets of NSW and VIC for FF & Plush

10

Number of Stores – split between Company owned and franchise

stores

(as at 29 December 2013)

KEY MESSAGES

• FY14 is a period of consolidation and no new store growth planned for

OMF, Le Cornu and Plush

3 Franchise stores in operation. 2 in Fantastic Furniture and 1 in Dare Gallery

(1) One store in NSW was subsequently closed in Jan 14

February 2014 Fantastic Holdings Limited

69 69 71 71 75

25 29 31 33 33

13 14 15

15 15 8 8 9

10 10

2 2

2 2 2

5 5 4

3 3

0

20

40

60

80

100

120

140

HY 2010 HY 2011 HY 2012 HY 2013 HY 2014

Franchisee

Le Cornu

Dare

OMF

Plush

FF

For

per

sona

l use

onl

y

FHL Group 2HY14 Outlook

11

Cautious outlook on retail sales – focus on efficiency improvements and return to growth

• Sales in January have trended ahead of same period last year for major retail brands (Fantastic Furniture and Plush)

• Performance across individual brands from a L4L sales perspective is a key priority in delivering the turnaround for the

business

• Operational opportunities to improve margin in isolation of sales growth with a key focus on supply chain logistics, cost of

quality and strengthening supplier arrangements

• Re-building the WA brand with investment in advertising

• Offshore manufacturing to begin in the calendar year

• Tough conditions expected to continue during second half:

• competition increasing in key markets

• lower exchange rate to place pressure on pricing, partly offset with local manufacturing capability

• FY14 is a year of rebuilding across the Group with continued focus and effort to reduce the Cost of Doing Business

February 2014 Fantastic Holdings Limited

For

per

sona

l use

onl

y

12

Questions & Answers

February 2014 Fantastic Holdings Limited

For

per

sona

l use

onl

y

Disclaimer

13

• Information in these presentations relating to the price at which relevant investments have been bought or sold in the past or the

yield on such investments cannot be relied upon as a guide to the future performance of such investments

• These presentations do not constitute an offering or recommendation to purchase securities or otherwise constitute an invitation or

inducement to any person to underwrite, subscribe for or otherwise acquire securities in any company within the Fantastic Holdings

Limited group (the “Group”)

• The information is these presentations does not take into account the potential and current individual investment objectives or the

financial situation of investors. Before making or varying any investment in securities in the Group, all investors should consider the

appropriateness of that investment in light of their individual investment objectives and financial situation and should seek their own

independent professional advice

• The presentations contain forward-looking statements which are subject to risks and uncertainties because they relate to future

events, many of which are outside the control of, and are unknown to, Fantastic Holdings Limited. These risks and uncertainties

may cause actual results to differ from any expected future events or events referred to in the forward looking statements. Fantastic

Holdings Limited disclaims any obligation or undertaking to disseminate any updates or revisions to any forward looking statements

in these materials to reflect any change in expectations in relation to any forward looking statements or any change in events,

conditions or circumstances on which any such statement is based

• No representation, warranty or assurance (express or implied) is given or made in relation to any forward looking statement by any

person (including Fantastic Holdings Limited). In particular, no representation, warranty or assurance (express or implied) is given

in relation to any underlying assumption or that any forward looking statement will be achieved

February 2014 Fantastic Holdings Limited

For

per

sona

l use

onl

y