Embed Size (px)

Citation preview

A Football Business Report

on

Blackburn Rovers Football Club

2004-2013

LUBS 2250 – The Football Business

By

Student Number: 200610820

Word Count: 3,000

Grade Achieved: 74/90 (1st)

`

200610820

1

TABLE OF CONTENTS

ACW TASK 1 2

KEY FINDINGS 2 EVIDENCE 3 TECHNICAL DETAILS 5

ACW TASK 2 6

KEY FINDINGS 6 EVIDENCE 6 TECHNICAL DETAILS 9

ACW TASK 3 10

KEY FINDINGS 10 EVIDENCE 10 TECHNICAL DETAILS 13

ACW TASK 4 14

KEY FINDINGS 14 EVIDENCE 14 TECHNICAL DETAILS 16

`

200610820

2

ACW TASK 1

Analyse the relationship between gate attendances, revenues and league performance for

your selected club over the last 10 years for which financial data is available. Determine

whether or not changes in league performance have had a significant influence on your

club’s gate attendances and revenues.

KEY FINDINGS

Blackburn’s average gate attendances over the past 10 years point to a positive

correlation between league performance and attendance with the highest average

attendance being in the 2009/10 season where they finished 10th in the Premier League,

their third highest position in the last 10 years.

The main anomaly over the past 10 years was in the 2005/06 season where their average

gate attendance was down at 21,015, the second lowest over the past 10 years. This was

despite a strong performance in the league where they finished 6 th, their highest position

over the last 10 years.

Blackburn’s stadium utilization rate has been fairly low over the last 10 seasons when

compared with the average in the Premier League. For example in the 2004/05 season,

Blackburn’s stadium utilization rate was only 72%, compared with the Premier League

average of 94.2% (Deloitte & Touche Annual Review of Football Finance, June 2005).

The 2007/08 season seems to be a turning point for Blackburn Rovers as their strong

performance in the league (finished 7th) was mirrored by a large increase in total revenue

from £43.3 million in 2006/07 to £56.4 million, an increase of 30.3%.

Blackburn’s relegation to the Championship at the end of 2012/13 season saw a drop in

total revenue from £54.2m the season before to £26.9m. Their average gate attendance

also dropped down to 14,997, a decrease of 33.5%.

`

200610820

3

EVIDENCE

From the evidence it is clear that there is a positive link between league performance and

average gate attendances. Over the past 10 years there has been a positive co-movement

between the two factors on 6 occasions. The main anomaly in this analysis is the 2005/06

season where Blackburn’s league position rose from 15th the year before to 6th, however,

average gate attendances fell from 22,315 to 21,015. A possible explanation for this is the sale of

both Andy Cole and Dwight Yorke who had fallen out of favour with the manager at the time,

Graeme Souness. Blackburn’s poor performances the previous season also may have led to the

uncertainty of the outcome of Blackburn’s matches decreasing as fans felt that there team was

likely to lose most games on previous form. This uncertainty of outcome has been seen as a key

aspect determining attendance demand (Gerrard, 2000). In Blackburn’s company accounts report

for the year ending June 2006, the Chairman of the Board admitted “falling attendances remain a

big issue for Rovers”. He stated that this was down to a number of factors including price, kick-off

times, predictable results and television coverage but concluded by saying that the Board were

agreed that prices for matchday tickets at Ewood Park need to be lowered, despite being one of

the lowest in the league already. This reflects the competition for fans that Blackburn faces from

other local clubs such as Burnley, Blackpool and Bolton.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Average Gate

Attendance 24,376 22,315 21,015 21,275 23,944 23,479 25,428 25,000 22,551 14,997

League Position 15 15 6 10 7 15 10 15 19 37

0

2

4

6

8

10

12

14

16

18

2015,000

17,000

19,000

21,000

23,000

25,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Leag

ue P

osit

ion

Ave

rag

e G

ate

Year

Blackburn Rovers Average Gate v League Performance

2003/04 - 2012/13

Average Gate Attendance

League Position

`

200610820

4

It is no surprise that Total Revenue follows a very similar line to that of average gate attendance

as in Blackburn’s case, matchday income has accounted for on average 14.2% of total revenue.

However, as can be seen in the table on the next page, Blackburn have become less reliant on

matchday income over the years; it’s percentage share of total revenue has fallen from 20.8% in

2007 down to 10.0% in 2012. The main reason for this is that media income has grown in

Season Average

League Gate

League

Position

Change in

Gate (HIGHER /LOWER)

Change in League

Position (HIGHER/SAME/LOWER)

Co-

Movement? (YES/NO)

2003/04 24,376 15 - - -

2004/05 22,315 15 LOWER SAME NO

2005/06 21,015 6 LOWER HIGHER NO

2006/07 21,275 10 HIGHER LOWER NO

2007/08 23,944 7 HIGHER HIGHER YES

2008/09 23,479 15 LOWER LOWER YES

2009/10 25,428 10

HIGHER HIGHER YES

2010/11 25,000 15 LOWER LOWER YES

2011/12 22,551 19 LOWER LOWER YES

2012/13 14,997 37 LOWER LOWER YES

0

2

4

6

8

10

12

14

16

18

2020.0

25.0

30.0

35.0

40.0

45.0

50.0

55.0

60.0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013L

eag

ue P

osit

ion

Tota

l R

eve

nu

e £

m

Year

Blackburn Rovers Total Revenue v League Position

2003/04 - 2012/13

Total Revenue League Position

`

200610820

5

significance over the past 10 years. During the 2003/04 season media income accounted for

£21.8m out of total revenue of £40.8m (53.3%) compared with the 2011/12 season (their last in

the Premier League) where media income was £41.1m out of £54.1m (75%). A key driver of this

increase in media revenue has been the lucrative television agreements, especially for the

Premier League where each new deal has historically risen in value by over 50% on the previous

deal.

TECHNICAL DETAILS

Task Summary: - There is evidence to suggest that as league performance increases, gate

attendances increase, however, Blackburn still has an extremely low stadium utilisation rate for

the Premier League. They have also become increasingly reliant to media revenue, which means

staying in the Premier League was a must for Blackburn, their relegation has led to financial

disaster.

Definitions:

Stadium Utilisation – percentage of stadium that is full.

Sources Used:

Blackburn Company Accounts 2004-2013. Available from ICC Financial Database

Workshop 1 and 2

http://www.european-football-statistics.co.uk/attn.htm

http://www.soccerbase.com

Reading 4 – Gate Attendance Demand for Football. Bill Gerrard (2000)

Average Gate

Previous Season

Average Gate

Current Season Difference % Change

Promotion Effect

2001/02 20,740 25,976 5,236 25.25%

Relegation Effect

2012/13 22,551 14,997 -7,554 -33.50%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Matchday Income (£m) 6.8 7.4 7.1 9.0 6.1 6.8 6.2 5.5 5.4 4.3

Revenue (£m) 40.8 41.3 43.4 43.3 56.4 50.9 57.8 57.6 54.2 26.9

MI as % of Revenue 16.6 17.9 16.4 20.8 10.8 13.4 10.7 9.5 10.0 16.0

`

200610820

6

ACW TASK 2

Analyse the relationship between sporting performance and player costs of your selected

club over the last 10 years for which financial data is available. Determine whether or not

your club has operated efficiently in achieving its sporting performance.

KEY FINDINGS

Blackburn’s wage costs have consistently risen over the past 10 years from £27.5m back

in 2004 to £50m in 2012.

During the last 4 years of Blackburn’s run in the Premier League, 2008/09 – 2011/2012,

they have had a consistently high percentage of their total revenue spent on wages,

ranging from 82% in 2009/10 season to 92.2% in their last season in the Premier League.

Drawing comparison with Blackburn’s performances against a club of a similar stature

such as Wigan only reinforces how inefficient they have been over their time in the

Premier League. During the 2011/12 season Wigan had the lowest total revenue in the

League of £53m but their wages expressed as a percentage of revenue was only 72%,

significantly better than Blackburn’s 92.2%. Despite these figures Wigan managed a very

creditable 15th in the League and survived for another season where as Blackburn were

relegated in 19th, 12 points behind Wigan.

EVIDENCE

The trends of the above graph showing Blackburn’s Total Wage expenditure against their league

position paints a basic picture of sporting inefficiency over the last 10 years as a steadily rising

wage bill does not seem to have reflected in better performance results ultimately culminating in

0

5

10

15

20

25

3020.0

25.0

30.0

35.0

40.0

45.0

50.0

55.0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Leag

ue P

osit

ion

Wag

es (

£m

)

Year

Wages vs League Performance - Sporting Performance

Blackburn Rovers 2003/04 - 2012/13

Wage Costs League Position

`

200610820

7

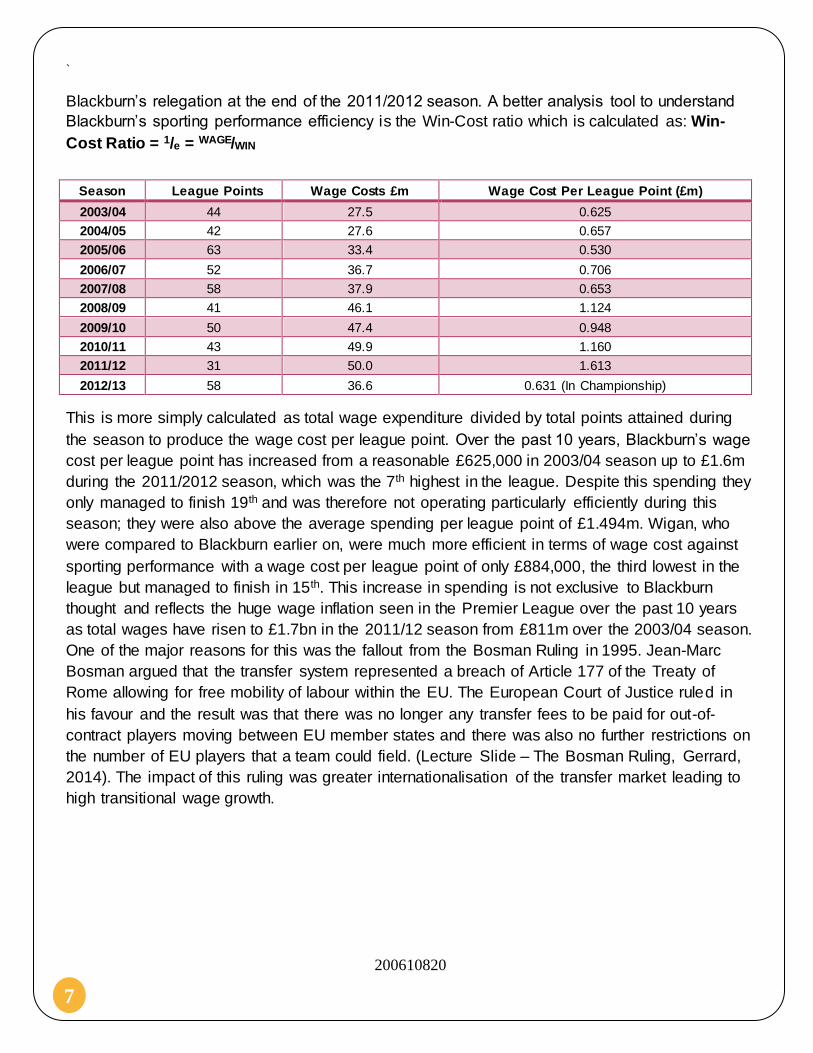

Blackburn’s relegation at the end of the 2011/2012 season. A better analysis tool to understand

Blackburn’s sporting performance efficiency is the Win-Cost ratio which is calculated as: Win-

Cost Ratio = 1/e = WAGE/WIN

This is more simply calculated as total wage expenditure divided by total points attained during

the season to produce the wage cost per league point. Over the past 10 years, Blackburn’s wage

cost per league point has increased from a reasonable £625,000 in 2003/04 season up to £1.6m

during the 2011/2012 season, which was the 7th highest in the league. Despite this spending they

only managed to finish 19th and was therefore not operating particularly efficiently during this

season; they were also above the average spending per league point of £1.494m. Wigan, who

were compared to Blackburn earlier on, were much more efficient in terms of wage cost against

sporting performance with a wage cost per league point of only £884,000, the third lowest in the

league but managed to finish in 15th. This increase in spending is not exclusive to Blackburn

thought and reflects the huge wage inflation seen in the Premier League over the past 10 years

as total wages have risen to £1.7bn in the 2011/12 season from £811m over the 2003/04 season.

One of the major reasons for this was the fallout from the Bosman Ruling in 1995. Jean-Marc

Bosman argued that the transfer system represented a breach of Article 177 of the Treaty of

Rome allowing for free mobility of labour within the EU. The European Court of Justice ruled in

his favour and the result was that there was no longer any transfer fees to be paid for out-of-

contract players moving between EU member states and there was also no further restrictions on

the number of EU players that a team could field. (Lecture Slide – The Bosman Ruling, Gerrard,

2014). The impact of this ruling was greater internationalisation of the transfer market leading to

high transitional wage growth.

Season League Points Wage Costs £m Wage Cost Per League Point (£m)

2003/04 44 27.5 0.625

2004/05 42 27.6 0.657

2005/06 63 33.4 0.530

2006/07 52 36.7 0.706

2007/08 58 37.9 0.653

2008/09 41 46.1 1.124

2009/10 50 47.4 0.948

2010/11 43 49.9 1.160

2011/12 31 50.0 1.613

2012/13 58 36.6 0.631 (In Championship)

`

200610820

8

Another tool of analysis for looking at player costs is the % of Turnover that was being directly

spent on wages. Looking over the last 10 years, Blackburn spent a higher percentage of their

revenue on wages than the average for the Premier League in every single season; in 2013 they

were in the Championship and Deloitte has not yet released figures for the season. Their was a

large jump in the 2006/07 season from 77% the previous season to 84.8% and this can be largely

attributed to the signing of Benny McCarthy at the start of the season who became Blackburn’s

joint highest earner on £35,000 a week. During their last season in the Premier League,

Blackburn spent a huge proportion of their revenue on wages, 92.2%, which was the highest in

Season 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

League Position 15 15 6 10 7 15 10 15 19 37

Total Revenue (£m) 40.8 41.3 43.4 43.3 56.4 50.9 57.8 57.6 54.2 26.9

Wages (£m) 27.5 27.6 33.4 36.7 37.9 46.1 47.4 49.9 50.0 36.6

Wages/League Position

Correlation - NO YES NO YES NO YES NO NO -

Wages as % of

Turnover 67.4% 66.8% 77.0% 84.8% 67.2% 90.1% 82.0% 86.6% 92.2% 136.1%

League Average 61% 59% 62% 63% 62% 67% 68% 70% 70% N/A

0

0.5

1

1.5

2

2.5

3

FA Premier League Wage Cost per League Point 2011/12

Wage Cost per League Point

`

200610820

9

the league. A study of Blackburn’s wage spending over the past 10 years reflects what has

seemed to be a policy of trying to buy their way out of trouble in the Premier League. They have

largely relied on big signings for a club of their size, such as Andy Cole for £10m in 2001, Craig

Bellamy for £6.6m in 2005 and Barry Ferguson for £8.5m in 2004. These players, coming from

clubs such as Manchester United, Newcastle and Rangers demand big wages, which has put

huge pressure on Blackburn’s wage bill. This ultimately did not pay off for Blackburn; as their

wage bill spiraled upwards to 92.2% in 2011/2012, performance in the league did not reflect this

spending and their lowly 19th place finish at the end of the season left them facing relegation,

leading to a huge drop in revenue and ultimately the club making a significant loss the next year,

having to spend 136.1% of their revenue on wages.

There is some evidence to suggest that an increase in wage spending can lead to an increase in

performance; Blackburn’s total wage bill increased by 21% in 2005/06 from the season before

and this lead to Blackburn finishing 9 places higher in the league at 6 th. However this is largely an

irregular occurrence in Blackburn’s history and is immediately countered by figures from the

2008/09 season where wage spending increased from £37.9m to £46.1m but Blackburn

struggled in the league and only finished 15th, 5 places lower than the previous season.

TECHNICAL DETAILS

Task Summary – Blackburn’s extremely high wage bill has left them in a dire position after

relegation into the Championship. It is clear that Blackburn are not always particularly efficient in

converting high wage spending into sporting performance. What is impressive however, is how

Blackburn have survived so long operating a very risky financial portfolio. Their trip to the

Championship will be extremely difficult but they may be helped by the increase in parachute

payments for teams relegated to the Championship to £48m.

Definitions:

Parachute Payments – Payments distributed to teams relegated to soften financial blow of

missing out on Premier League media and sponsorship revenue.

Sources Used:

Blackburn Company Accounts 2004-2013. Available from ICC Financial Database

Class 2 Solutions

Lecture Slides – Bosman http://www.guardian.co.uk/football/2013/apr/18/premier- league-finances-club-by-club

`

200610820

10

ACW TASK 3

Analyse the financial performance of your club over the last five years for which financial

data is available. Determine whether or not your club has performed well financially

KEY FINDINGS

Over the past 10 years Blackburn’s total revenue has been consistently low for a Premier

League club, hovering around the £50m mark.

Their operating costs have exceeded their total revenue for each of the last 10 years and

this has left them in a precarious position.

Blackburn have operated a largely successful trading policy where they top up their low

revenue’s by buying and selling players as needed to fulfill this deficit.

This transfer policy has allowed to Blackburn to operate with an extremely high

Wages/Revenue ratio, the highest in the league on a number of occasions. This is

ultimately what has left them in financial ruin as their successful model was reliant on

remaining in the Premier League to benefit from the sizeable media revenue that the

Premier League brings.

EVIDENCE

BLACKBURN 2013 2012 2011 2010 2009

Revenue £26,900,000 £54,200,000 £57,600,000 £57,800,000 £50,900,000

Staff Costs £36,600,000 £50,000,000 £49,900,000 £47,400,000 £46,100,000

Other Operating Costs £14,600,000 £13,800,000 £11,900,000 £12,100,000 £11,300,000

PBIT -£36,036,146 £4,462,692 -£17,980,620 -£1,298,905 £4,423,370

Operating Profit/Loss -£33,992,972 -£18,446,281 -£12,083,821 -£12,052,356 -£14,536,425

PBITDA -£24,850,095 £14,662,479 -£8,668,750 £10,442,309 £13,886,146

Depreciation -£1,483,562 -£1,386,612 -£1,468,872 -£1,440,613 -£1,414,950

Amortisation -£9,702,489 -£8,813,175 -£7,842,998 -£10,300,601 -£8,047,826

Player Trading -£11,745,663 £14,095,798 -£13,739,797 £452,850 £10,911,969

`

200610820

11

As is pretty evident from the above figures, Blackburn suffered a disastrous year during the

2012/2013 season after their relegation to the Championship. Blackburn had been operating on a

tight rope with a consistently high wage/revenue ratio throughout their stay in the Premier

League. Their strategy was to reinvest any profits made back into the team, either as capital

expenditure or through wages as they believed in order to be competitive they needed to pay

high salaries to attract the players they required. This left Blackburn high and dry when they

began their campaign in the Championship as revenue plummeted from £54.2m to £26.9m,

mostly down to a reduction in media revenue from £41.1m to £17.9m.

Prior to Blackburn’s relegation, their total revenue had remained fairly constant at around £50-

£57m which is very low for a club that was performing reasonably well in the league, finishing in

the top 10 on 4 occasions since 2006. Blackburn have essentially become a trading club,

balancing sales and purchases and where necessary, selling players to fund higher wage bills for

current players. An example of this was in the 2009/10 season where Blackburn were faced with

reducing wages by 10% or finding £4m from player sales. They opted for the latter, not wanting to

cut wages, and sold Stephen Warnock to Aston Villa for £7m replacing him with Pascal

Chimbonda from Tottenham for £3m. This is the way Blackburn have survived over the past 10

years, buying and selling players to balance their books and allow them to keep their wage

packet high. Crucial to this strategy however was the revenue they gained from TV deals in the

Premier League and this is why they have been so badly affected in their first season in the

Championship with Profit before Interest and Tax amounting to -£36,036,146.

Comparatively with Wigan, Blackburn’s performance does not look impressive and we can see

the vast difference in their returns on assets, capital employed and equity in 2012. What is also

extremely noticeable is the price Blackburn paid for relegation; in 2013 they had an ROA of

-59.57% compared with Premier League Wigan’s 4.76%.

BLACKBURN 2013 2012 2011 2010 2009

Rates of Return

ROA -59.57% 7.12% -31.10% -1.93% 6.05%

ROCE -132.65% 9.31% -39.76% -2.67% 8.85%

ROE -238.40% 18.60% -98.64% -6.87% 12.12%

WIGAN 2013 2012 2011 2010 2009

Rates of Return

ROA 4.76% 17.94% -23.19% -13.01% -11.61%

ROCE 10.29% 37.21% -9.45% -5.42% -7.89%

ROE 6.81% 33% -1.98% -6.89% -10.81%

`

200610820

12

Analysing Blackburn’s rates of returns, their financial performance does not seem to have much

stability over the past 5 years. They were operating reasonably steadily through the 2008 and

2009 seasons making PAT of around £3m but in 2011 Blackburn couldn’t balance their operating

losses against sales of players as they made a loss through player transfers of £13m. This

pushed profit after tax down to -£18,615,134, which had a substantial impact on the clubs rates of

return. A promising financial performance in 2012 was again mainly down to the transfer policy of

Blackburn, with Phil Jones and Chris Samba leaving the club, netting Blackburn over £25m for

the pair. This is reflected in the Player Trading/Revenue ratio in the table below, which rose from

-23.85% in 2011 to 26.01%. Unfortunately, Blackburn could not convert this great financial

performance into league performance as they slipped to 19 th by the end of the season with a

Wage/League Points ratio of £1,612,903, their highest of the last 10 years.

Blackburn’s operating margin has been poor throughout the last 10 years, as their operating

costs have always exceeded their total revenue. Once again it is important to state that the only

way they survive operating like this is because of their fluid transfer policy, constantly shipping

players in and out and looking for a profit on them and this explains the vast difference between

their profit margin and their operating margins. The below graph illustrates the vast difference

between their total revenue and operating profit/loss.

2013 2012 2011 2010 2009

Profit Margin -133.96% 8.23% -31.22% -2.25% 8.69%

Operating Margin -126.37% -34.03% -20.98% -20.85% -28.56%

Player Trading/Revenue -43.66% 26.01% -23.85% 0.78% 21.44%

Wage/Revenue Ratio 136.06% 92.25% 86.63% 82.01% 90.57%

Wage/League Points Ratio £631,034 £1,612,903 £1,160,465 £948,000 £1,124,390

-150.00%

-100.00%

-50.00%

0.00%

50.00%

100.00%

-£40,000,000

-£20,000,000

£0

£20,000,000

£40,000,000

£60,000,000

£80,000,000

2009 2010 2011 2012 2013

Blackburn Rovers Operating Profit/Revenue

Revenue Operating Profit/Loss Operating Margin

`

200610820

13

TECHNICAL DETAILS

Task Summary – Blackburn’s financial performance has been extremely inconsistent over the

past 5 years and their overall performance tends to rely mainly on the success or otherwise of

their transfers. They are set to face a difficult struggle to stay afloat after making huge losses in

their first season in the Championship and having to face possible sanctions from the Financial

Fair Play rules.

Definitions:

ROA – Return on Assets

ROCE – Return on Capital Employed

ROE – Return on equity

Sources Used:

Blackburn Company Accounts 2004 – 2013. Available from ICC Financial Database

Lecture Slides

`

200610820

14

ACW TASK 4

Analyse the cash flows for your club over the last five years for which financial data is

available. Determine how your club has financed its investment expenditures.

KEY FINDINGS

Blackburn’s net cash flows have been negative in 4 out of the last 5 years with 2011/2012

being the only exception

Blackburn have continued to take out large loans from the bank in order to finance their

high operating costs and keep wages high.

Blackburn’s net debt has risen from £20m back in 2009 to £54m in 2013.

Blackburn cannot to afford to continue running the club as it is currently running as they

will face hefty punishments under the new Financial Fair Play rules which allow only an

£8m loss in a year for teams in the Championship.

EVIDENCE

Blackburn Rovers 2013 2012 2011 2010 2009

Capital Expenditure and Financial Investment

Payments to acquire intangible

fixed assets -£9,843,694 -£12,269,523 -£10,845958 -£19,297,057 -£2,310,425

Payments to acquire tangible fixed

assets -£1,201,594 -£132,101 -£565,847 -£1,573,029 -£688,906

Receipts from sales of intangible

fixed assets £5,507,934 £24,092,197 £675,002 £21,486,076 £7,069,743

Receipts from sales of tangible

fixed assets £1,147 £2,279 £2,000 £243 £4,320

Net cash inflow/outflow -£5,536,207 £11,692,852 -£10,734,803 £616,233 £4,074,732

Financing

Repayment of Bank Loan 0 0 -£2,625,000 -£875,000 -£875,000

New Loans £20,200,000 £19,150,000 £15,185,848 0 0

Repayment of Loans -£121,452 -£3,196,452 -£5,027,137 -£1,000,000 0

New hire purchase borrowing 0 0 £130,861 £65,356 0

Repayment of hire purchase

borrowing -£23,095 -£53,282 -£59,206 -£29,836 -£1,007

`

200610820

15

Movement in loan from parent

company 0 0 0 0 £3,000,000

Net cash inflow/outflow £20,055,453 £15,900,266 £7,605,366 -£1,839,480 £2,123,993

Returns on investment and servicing of finance

Interest received £694 £8,067 £7,511 £64,361 £21,439

Bank and other interest paid -£462,244 -£211,026 -£639,543 -£661,002 -£860,261

Hire purchase interest paid -£2,522 -£2,522 -£2,522 0 -£230

Net cash inflow/outflow -£464,072 -£205,481 -£634,514 -£596,641 -£839,052

Blackburn’s net cash flow has largely been negative over the past 5 years with the 2011/2012

season being the only positive figure as they recorded an inflow of £17,730,209. This is attributed

to a strong performance in their capital expenditure as the selling of Phil Jones to Manchester

United for £16.5m and Christopher Samba to Anzhi for £11m contributed towards a high receipt

from the sales of intangible fixed assets of £24,092,197. Blackburn have consistently made cash

losses from their operating activities and thus their net cash flows performance has largely come

down to two things, their fluent transfer policy and taking out new loans. From 2011 - 2013,

Blackburn have taken out new loans to the value of £15m, £19m and £20m respectively to help

cover their operating activities deficit and allow them to maintain high wages for their players.

This is inspite of Barclays demands back in 2011 that Venky’s shrink the debt they owe as

agreed when they took control at Ewood Park. This has left the club in £54m worth of debt at the

end of the 2012/13 season and with Financial Fair Play punishments looming thanks to their total

loss for the 2012/13 season amounting to £36m - £24m more than is permitted under the new

regulations – the outlook is bleak for Blackburn Football Club.

Cash Flow Statement 2013 2012 2011 2010 2009

Operating activities -£24,028,650 -£9,657,428 -£3,940,444 -£672,502 -£6,665,966

Investment returns & servicing

finance -£464,072 -£205,481 -£634,514 -£596,641 -£839,052

Taxation £31,978 0 0 0 0

Capital expenditure & financial

investment -£5,536,207 £11,692,852

-

£10,734,803 £616,233 £4,074,732

Financing activites £20,055,453 £15,900,266 £7,605,366 -£1,839,480 £2,123,993

Net Cash Flow -£9,941,498 £17,730,209 -£7,704,395 -£2,492,390 -£1,306,293

Net Debt £54,478,274 £24,481,323 £26,311,266 £21,001,505 £20,348,595

`

200610820

16

TECHNICAL DETAILS

Task Summary – Blackburn’s cash flows have been consistently negative as they take out more

and more loans to cover their high operating costs. They now face an uphill task to begin to pay

off their debts whilst surviving on lower revenue from the Championship.

Definitions:

Financial Fair Play – Restrictions put in place by UEFA to prevent clubs going bankrupt

and increase competition in European Football.

Sources Used:

Blackburn Company Accounts 2004 – 2013. Available from ICC Financial Database

Lecture Slides – Bill Gerrard

http://www.guardian.co.uk/football/david-conn- inside-sport-blog/2012/may/08/blackburn-rovers-nightmare-scenario

Class 4 Solutions