Embed Size (px)

Citation preview

Welcome to: FNSBKG404

Carry Out Business Activity and Instalment Activity Statement Tasks

Lisa Genna [email protected]

Monday – Room H G.0-9 - 6:00 pm to 8:30 pm

1

Lesson 6

FNSBKG404 Carry Out Business Activity and Instalment

Activity Statement Tasks

2

Overview 1. Methods for calculating GST liability

1. The accounts method 2. The GST calculation method

2. Correcting errors made 3. Payments and refunds

3

1.

Methods for calcula1ng GST owed by an en1ty to the ATO

4

There are two (2) methods that you can use to

account for GST owed to the ATO:

1. The accounts method

2. The GST calculation method

Methods for calcula3ng GST owed by an en3ty to the ATO

5

The business completes its Activity Statement directly from its accounting

records e.g. Income Statement

The accounts method

6

This method uses a step-by-step

calculation worksheet.

There are twenty boxes on the

GST Calculation Worksheet

that may need to be completed

to determine the correct amount

of GST payable or receivable.

The GST calcula3on method

7

8

1.1

The accounts method

9

To use the accounts method, the business’s accounting records must be able to: 1. Readily identify GST amounts for its: � Sales � Purchases � Importations 2. Separately record any purchases or importations that were for either: � Private use � Making input taxed sales

3. Identify any GST-free or input-taxed sales.

The accounts method

10

Record Keeping Whichever method is used, the taxpayer is required to keep a copy of the Activity Statement and the records used to prepare it for 5 years after it is prepared, obtained or the transactions have been completed (whichever is later).

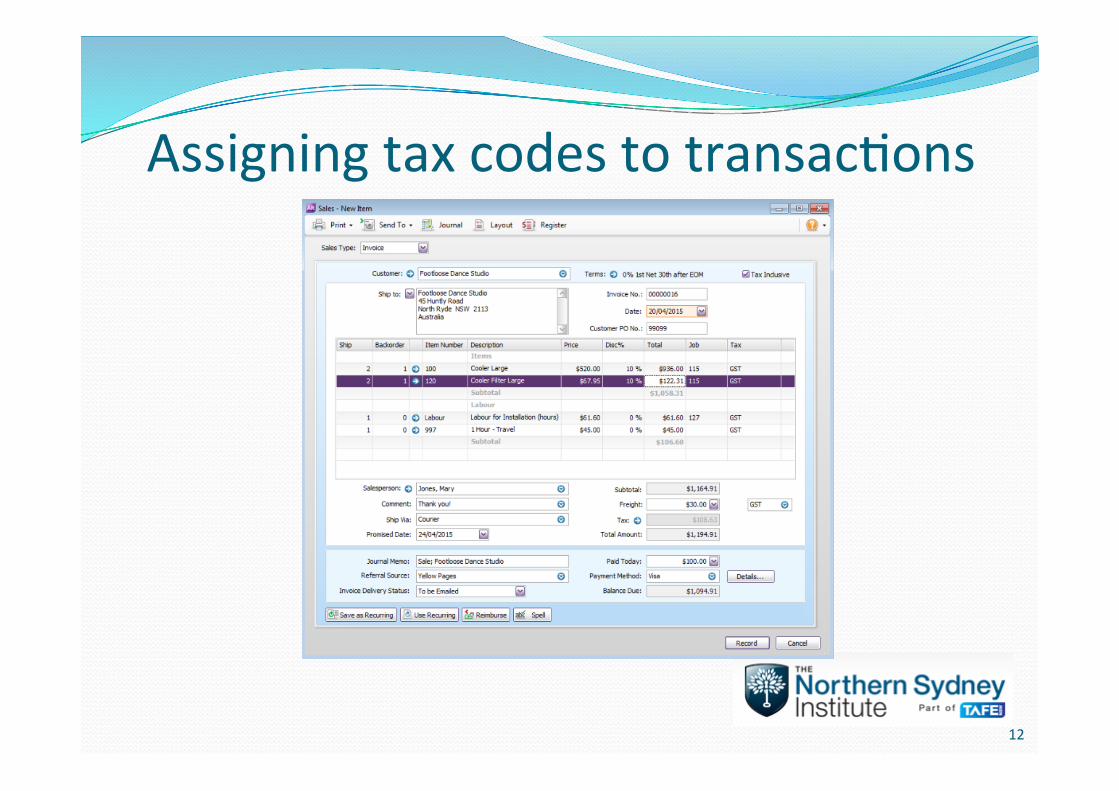

Tax Codes Businesses using computerised accounting systems (e.g. MYOB or Xero) may elect to use the accounts method to complete their Activity Statements. Most of the information needed can be obtained from a report from the system.

In order to generate these reports, the tax treatment of each transaction must be recorded by assigning a tax code to each line item of the transaction.

The accounts method

11

Assigning tax codes to transac3ons

12

1.2

The GST calcula1on method

13

The GST Calcula3on Worksheet GST on Sales

14

The calculation of GST for the amount payable from sales is contained in G1 to G9 on the worksheet.

15

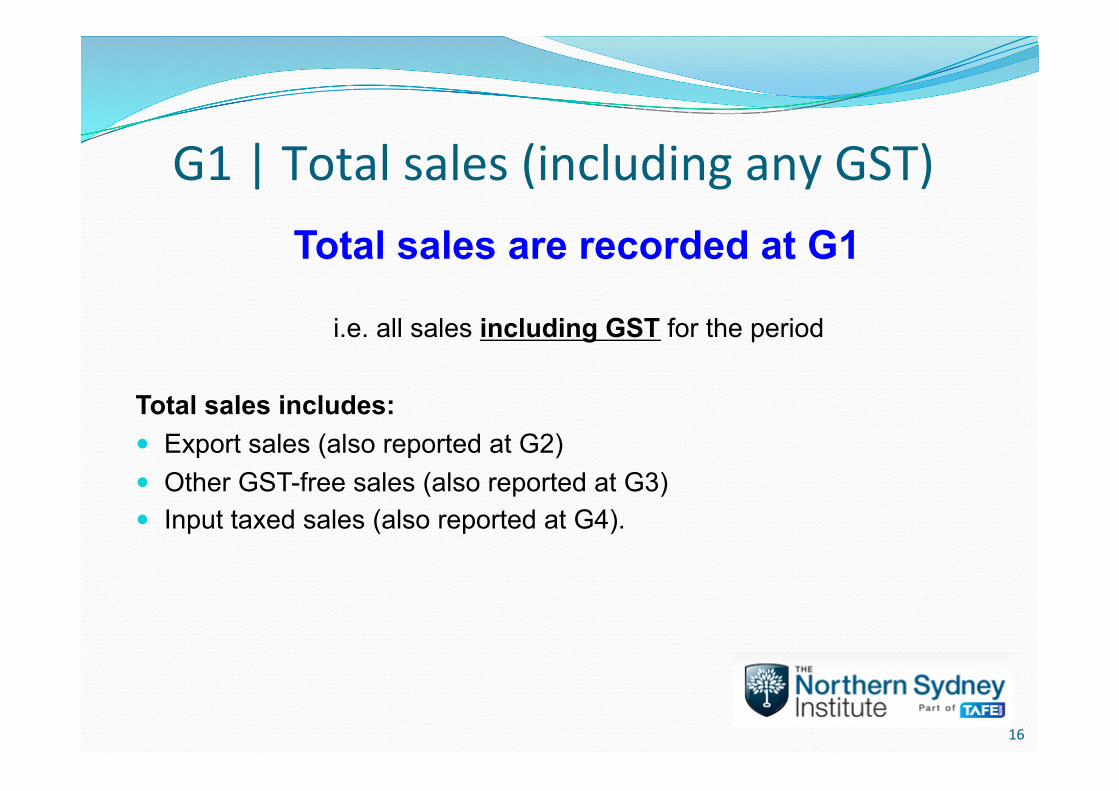

Total sales are recorded at G1

i.e. all sales including GST for the period Total sales includes: � Export sales (also reported at G2) � Other GST-free sales (also reported at G3) � Input taxed sales (also reported at G4).

G1 | Total sales (including any GST)

16

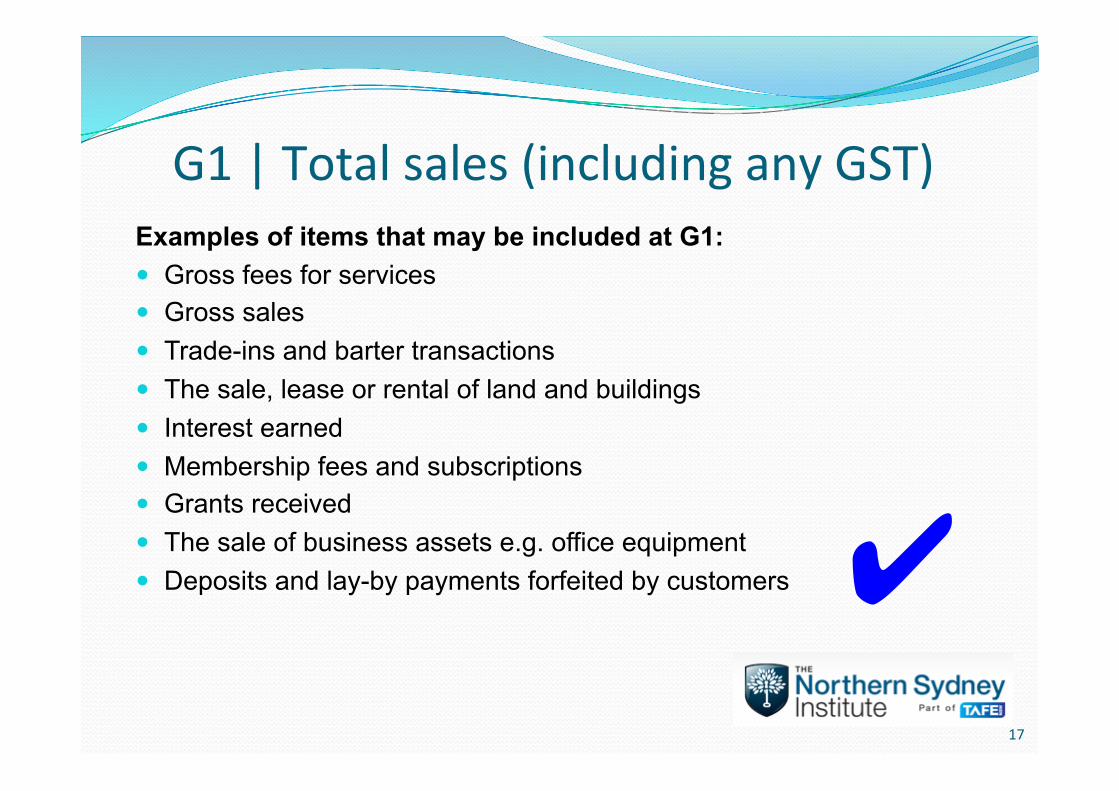

Examples of items that may be included at G1: � Gross fees for services � Gross sales � Trade-ins and barter transactions � The sale, lease or rental of land and buildings � Interest earned � Membership fees and subscriptions � Grants received � The sale of business assets e.g. office equipment � Deposits and lay-by payments forfeited by customers

G1 | Total sales (including any GST)

✔ 17

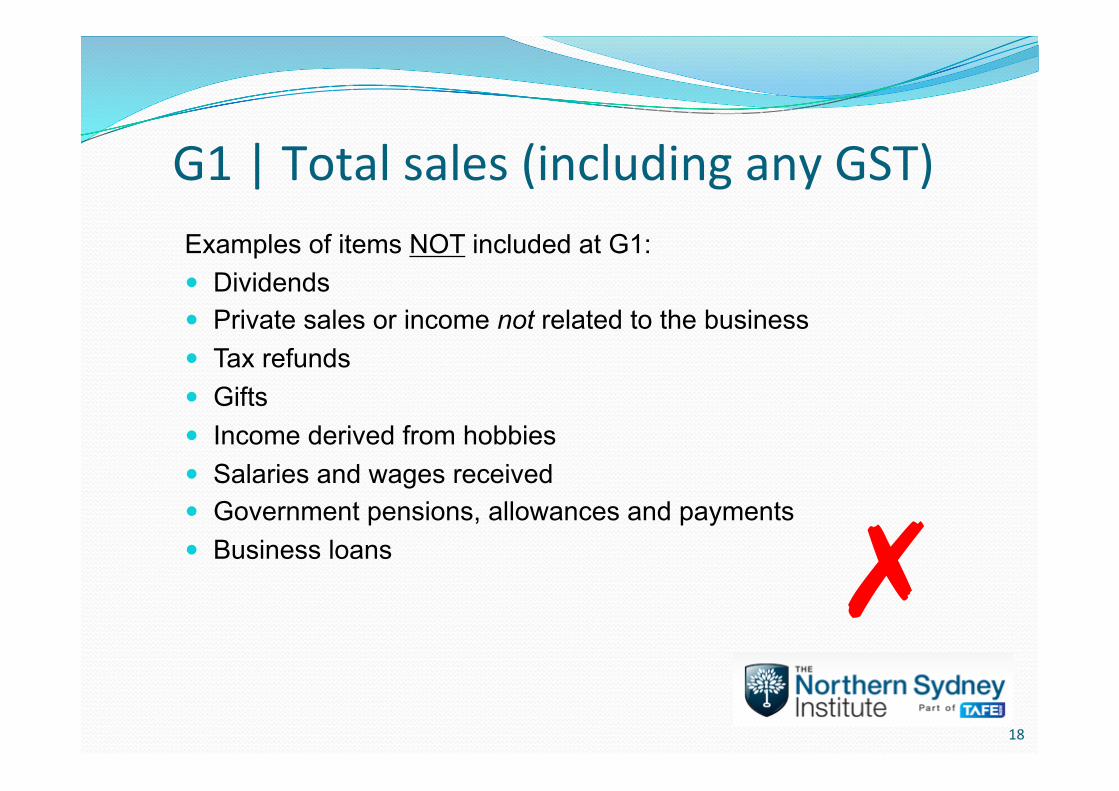

Examples of items NOT included at G1: � Dividends � Private sales or income not related to the business � Tax refunds � Gifts � Income derived from hobbies � Salaries and wages received � Government pensions, allowances and payments � Business loans

G1 | Total sales (including any GST)

✗ 18

The amount to include at G2 is the total amount of export sales This amount is made up of: � The free-on-board value (i.e. the value used for customs purposes

which is the value of the goods in AU$ (country of origin) excluding insurance and freight costs) of exported goods that meet the GST-free export rules, plus charges for freight and insurance for transport of the goods to the point of departure from Australia.

� Payments received for the repairs of goods from overseas that are to be exported.

� Payments received for goods used in the repair of goods from overseas that are to be exported.

G2 | Export sales

19

The 60-day rule:

Exported goods are GST-free if they are exported from

Australia within 60 days of the first of the following two

events:

1. the supplier receives any payment for the goods

2. the supplier issues an invoice for the goods

G2 | Export sales

20

All amounts reported at G2 should also be reported at G1

Do not report any of the following at G2: � GST-free services as these amounts will be reported at G3,

unless the amount relates to the repair, renovation, modification or treatment of goods from overseas whose destination is outside Australia.

� Freight and insurance for the transport of goods outside Australia or other charges imposed outside Australia that are included in the free-on-board value.

� The international transport of goods or passengers. If any of these items are GST-free, they should all be

reported at G3.

G2 | Export sales ✗

21

GST-free sales includes supplies such as: � Most basic food for human consumption � Most health and education services � Eligible childcare services

G3 | Other GST-‐free sales

×All amounts reported at G3 should also be reported at G1

22

You do not report the following at G3: � Exports à these are shown at G2 � Basic food, including food for human consumption, that is:

� – for consumption on the premises from which it is sold (e.g. cafes and restaurants)

� – hot takeaway food � – a food type listed in Schedule 1 of A New Tax System (Goods and

Services Tax) Act 1999 or foods that are a combination of foods where at least one food type in the combination is listed in Schedule 1

� Note; sales of water that are provided in, or transferred into, containers with a capacity of < 100 litres are also not GST-free.

G3 | Other GST-‐free sales ✗

23

Examples of some common items listed in Schedule 1 i.e. items subject to GST:

� certain prepared foods � confectionery � savoury snacks � bakery products � ice cream foods � alcohol � soft drinks � biscuits

G3 | Other GST-‐free sales

24

For input taxed supplies it is the supplier, rather than the end consumer,

who bears the cost of the GST.

The two most common input taxed sales for small businesses are:

1. Financial supplies; and

2. The selling or renting of residential premises.

G4 | Input taxed supplies

All amounts reported at G4 should also be reported at G1

25

Input taxed financial supplies may refer to: � the lending or borrowing of money � giving credit to a customer � the buying or selling of shares � the creation, transfer, assignment or

receiving of an interest in, or a right under, a superannuation fund

G4 | Input taxed supplies

26

“It’s totally debatable” (part 1) What about interest earned by an entity where the amount in question is

only incidental to the taxpayer’s business?

In practice, some entities report these amounts at G3 (other GST-free sales)

based on the argument that there is nothing to report against these amounts

at G13 (purchases for making input taxed sales).

Other entities report these amounts at G4 (input taxed supplies) based on

the argument that interest (income or expense) is a type of financial supply.

What do you think?

G4 | Interest earned

27

� G5 is the total of all sales which are not subject to GST, being export sales, other GST-free sales and input taxed sales.

� Add G2, G3 and G4 together to complete item G5.

G5 | G2 + G3 + G4

28

� G6 is the total of all sales which are subject to GST. � This is calculated as G1 minus G5.

G6 | G1 – G5

29

Businesses may need to make adjustments that change the net amount of GST they are liable to pay for a reporting period. � Increasing adjustments - increase the net amount of GST a

business is liable for. � Decreasing adjustments - decrease the net amount of GST a

business is liable for.

� Only net increasing adjustments should be included at G7. Net decreasing adjustments should be included at G18.

G7 | Adjustments (net increasing)

30

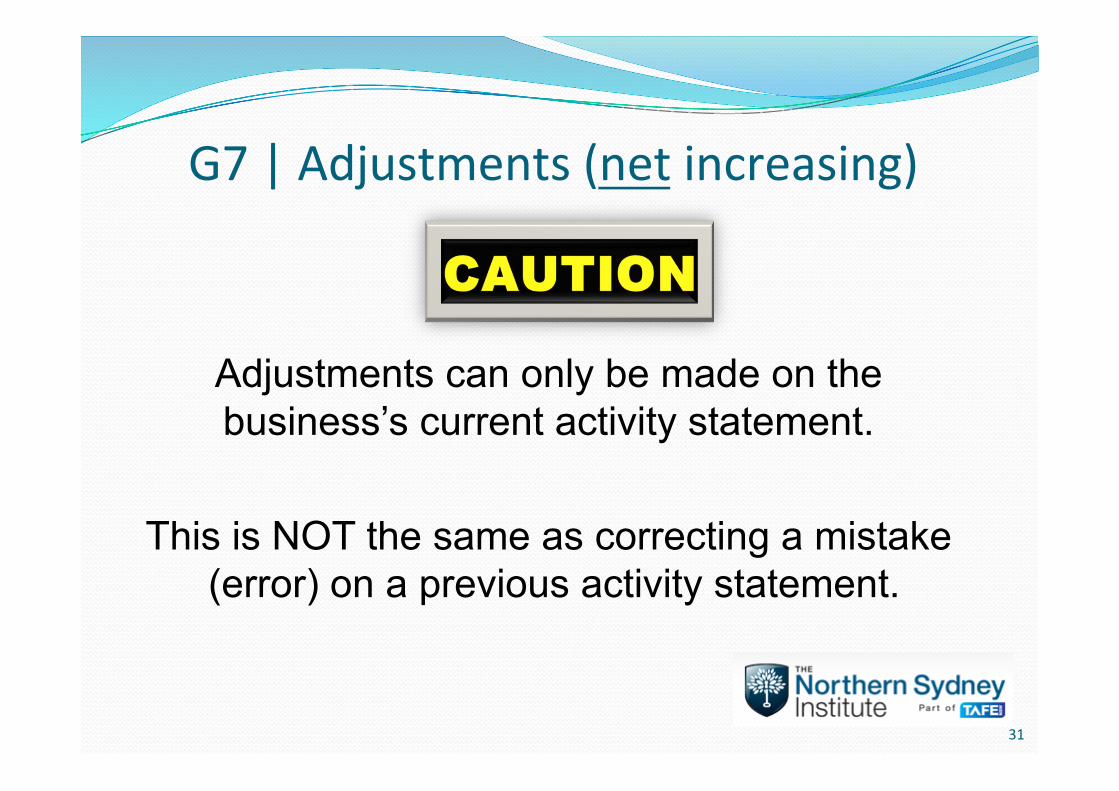

Adjustments can only be made on the business’s current activity statement.

This is NOT the same as correcting a mistake

(error) on a previous activity statement.

G7 | Adjustments (net increasing)

31

Examples of events that may give rise to either increasing and decreasing adjustments:

G7 and G18 | Adjustments

Increasing adjustment Decreasing adjustment Discounts received from suppliers

Discounts provided to customers

Goods returned to a supplier Goods returned by a customer

A bad debt is recovered A bad debt is written off An item purchased for business use is now used for personal use (or increase in personal use %)

An item purchased for personal use is now used for business use (or decrease in personal use %)

32

G8 is the sum of all taxable supplies made during the period. Any net increasing adjustments at G7 are added to G6 to determine the total sales subject to GST (G6 + G7). If there are no adjustments, simply copy the amount from G6 to G8. This will form the basis for calculating the GST amounts owed to the ATO from sales during the period.

G8 | Total sales subject to GST aTer adjustments

33

G8 ÷ 11 To calculate the total GST owing to the ATO relating to taxable supplies made, the amount at G8 is divided by 11. This amount is to be transferred to label 1A on the BAS.

G9 | GST on sales

34

The GST Calcula3on Worksheet GST on Purchases

35

The calculation for the amount of GST paid from purchases is contained in G10 to G20 on the worksheet.

36

Capital purchases are purchases to acquire business assets that have a useful life of > 1 year*. Examples includes � Land and buildings � Equipment and machinery � Motor vehicles � Point of sale terminals � Computers

* non-current assets

G10 | Capital purchases

37

Non-capital purchases include trading stock and normal running expenses (excluding wages and salaries and any superannuation contributions), such as: � Advertising � Printing and stationery � Repairs and maintenance � Equipment rentals � Leases

G11 | Non-‐capital purchases

38

G10 and G11 require the business to separately report its capital and non-capital purchases. If the business already keeps a separate record of these purchases then it can use this record to complete labels G10 and G11. If it does not and its GST turnover is expected to be < $1 million, then the following applies: � The business only needs to record capital items

costing > $1,000 at G10. � Capital items costing $1,000 or less can be recorded at

G11.

G11 | Non-‐capital purchases

39

G12 is the total of all purchases made by the taxpayer during the reporting period, and is calculated by adding capital and non-capital

purchases together.

G12 | G10 + G11

40

At G13, you will include any purchases you made that relate to any of your input taxed sales. e.g. Mali Jones is a landlord who rents out a number of residential properties. Rent received from tenants for the quarter totalled $10,000. During the quarter, she incurred $1,000 to get some faulty electrical wiring repaired in some of the older properties. Mali will report $10,000 at G1 and G4 on her BAS. She will also report $1,000 at G11 and G13 on her BAS.

G13 | Purchases for making input taxed sales

All amounts reported at G13 should also be reported at either G10 or G11

41

Input taxed sales are not subject to GST. What are the implications of this?

� The purchaser cannot claim a credit for GST on purchases used to make input taxed sales.

� The business providing the input taxed supply bears the cost of the GST paid on those purchases (rather than the end consumer).

There is no requirement to report G13 on the Activity Statement, but the business does need to keep a separate record of it.

G13 | Purchases for making input taxed sales

All amounts reported at G13 should also be reported at either G10 or G11

42

If a taxpayer receives anything from an associate for no payment (i.e. for free) or if a taxpayer pays less than the full GST-inclusive market value, it must: STEP 1: Work out what portion of the amount relates to sales that are input taxed; and STEP 2: Report this amount at G13 on the GST calculation worksheet. (refer to ‘Exercise 19’)

G13 | Purchases for making input taxed sales

This has the effect of ensuring that the ATO collects the market value of GST on these supplies and discourages businesses from

attempting to avoid paying tax. 43

At G14, you have to report all purchases not subject to GST including purchases from overseas, donations, interest paid, council rates

and other non-taxable importations.

G14 | Purchases without GST in the price

All amounts reported at G14 should also be reported at either G10 or G11

44

“It’s totally debatable” (part 2) The recommended text suggests that council rates are GST-free and

should therefore be reported at G14 on the GST calculation worksheet.

However, it has been suggested that council rates should be treated as

being ‘out-of-scope’ when it comes to the preparation of a BAS and

therefore should not be reported anywhere on an entity’s BAS (refer to

additional reading: “Council rates and BAS treatment” - TaxEd).

What do you think?

G14 | Council rates

45

Purchases and importations that do not have GST included in the price may include those that are: � GST-free or input taxed � Made by an entity not registered for GST � Not connected with Australia (and therefore not taxable) � Non-taxable importations � Intangible supplies purchased offshore that are not subject to a

GST reverse charge � Payments of Australian taxes, fees and charges where GST was not

included in the price.

There is no requirement to report G14 on the Activity Statement, but the business does need to keep a separate record of it.

G14 | Purchases without GST in the price

46

An intangible supply refers to a ‘good’ that does not have a physical nature as opposed to a physical good i.e. an object. Digital goods such as downloadable music, mobile apps or virtual goods used in virtual economies are all examples of intangible goods. In an increasingly digitised world, intangible goods play an important role in the economy. Virtually anything that is in a digital form and deliverable on the Internet can be considered an intangible good. An intangible good must not be confused with a service. A good is an object whereas a service is an activity. For example, a haircut is an example of a service, not an intangible good.

What is an intangible supply?

47

� If you buy in certain services from outside Australia, you will be required to apply a GST reverse charge. This is intended to take away any GST advantage of buying those services from outside Australia.

� Under the reverse charge, you are required, as the recipient, to account for GST on your activity statement, but only if you are not entitled to full input tax credits.

� The reverse charge applies to the acquisition of all supplies of anything other than goods or real property, if the supply is not connected with Australia.

What is a GST reverse charge?

48

Amounts for purchases and importations that are of a private or domestic nature are required to be reported at G15.

If a purchase or importation was only partly of a private or domestic nature, the taxpayer must work out what amount of the purchase or importation was of a private or domestic nature, and report that amount at G15.

G15 | Es3mated purchases for private use or not income tax deduc3ble

All amounts reported at G15 should also be reported at either G10 or G11

49

Purchases or importations that are not tax deductible are also required to be reported and include: � Expenses for maintaining the taxpayer’s family e.g. school fees � Penalties and fines � Entertainment expenses* � Travel expenses for relatives* � Recreational club expenses* � Expenses for leisure facilities or boats* � Expenses incurred under an agreement for providing non-deductible non-cash business benefits � Expenses incurred when providing meal entertainment if, for FBT purposes, the 50/50 split method or 12-week register method is used to calculate the taxable value of the fringe benefit � Entertainment facility leasing expenses if, for FBT purposes, the 50/50 split method is used to calculate the taxable value of the fringe benefit

* except where the expenses are incurred in providing a fringe benefit

G15 | Es3mated purchases for private use or not income tax deduc3ble

50

If the business: � has a turnover of < $2 million � has not chosen to pay GST by instalments or report GST annually then it can estimate the intended private use portion of a purchase when claiming a GST credit. � In practice, the business claims a GST credit for the total amount of GST

included in the price of the purchase and then, at the end of the income year, makes an adjustment to account for the private portion of all these purchases.

� This adjustment has to be reported at G15.

G15 | Es3mated purchases for private use or not income tax deduc3ble

51

“It’s totally debatable” (part 3) The recommended text suggests that penalties and fines should be

reported at G15 based on the argument that fines are a non-deductible

expense of the taxpayer. If you agree with this argument, then you

should also include the amount in question at G11.

However, it could be argued that penalties and fines should not be

included at G11 because no supply has been made i.e. the item is ‘out-

of-scope’. If you agree with this argument, then you should not include

the amount in question at G15 either.

What do you think?

G15 | Penal3es and fines

52

The following are common items considered ‘out of

scope’ for the purposes of calculating a taxpayer’s GST

liability:

� Depreciation

� Superannuation contributions

� Wages and salaries

� PAYG withholding amounts

‘Out-‐of-‐scope’ items

53

G16 is the total of all purchases from which a taxpayer may not claim an input tax credit.

It is the sum of purchases for making input taxed sales,

purchases without GST in the price, and estimated purchases for private use or not income tax deductible.

G16 | G13 + G14 + G15

54

Total purchases subject to GST

By deducting the amount at G16 (non-creditable purchases) from the amount at G12 (total purchases), the taxpayer can calculate the purchases from which

they are entitled to claim a GST input tax credit.

G17 |G12 – G16

55

Businesses may need to make adjustments that change the net amount of GST they are liable to pay for a reporting period. � Increasing adjustments - increase the net amount of GST a

business is liable for. � Decreasing adjustments - decrease the net amount of GST a

business is liable for.

� Only net decreasing adjustments should be included at G18. Net increasing adjustments should be included at G7.

G18 | Adjustments (net decreasing)

56

Adjustments can only be made on the business’s current activity statement.

This is NOT the same as correcting a mistake

(error) on a previous activity statement.

G18 | Adjustments (net decreasing)

57

Examples of events that may give rise to either increasing and decreasing adjustments:

G7 and G18 | Adjustments

Increasing adjustment Decreasing adjustment Discounts received from suppliers

Discounts provided to customers

Goods returned to a supplier Goods returned by a customer

A bad debt is recovered A bad debt is written off An item purchased for business use is now used for personal use (or increase in personal use %)

An item purchased for personal use is now used for business use (or decrease in personal use %)

58

G19 is the sum of all GST-creditable purchases made during the period. Any net decreasing adjustments at G18 are added to G17 to determine the total purchases subject to GST (G17 + G18). If there are no adjustments, simply copy the amount from G17 to G19. This will form the basis for determining the GST credits that can be claimed.

G19 | Total purchases subject to GST aTer adjustments

59

G19 ÷ 11 To calculate the total credits the taxpayer can claim from the ATO, the amount at G19 is divided by 11. This amount is to be transferred to label 1B on the BAS.

G20 | GST on purchases

60

2.

Correc1ng errors made

61

Errors can be made in completing the BAS. The ATO has made provisions for this.

Errors

62

� If an error on a previous BAS has the effect of decreasing the

taxpayer’s tax liability, then a GST credit may be included on a later

BAS.

� The taxpayer may make the adjustment up to 4 years later (no

value limit applicable).

Errors of this nature may include:

� Finding a tax invoice that was previously lost or overlooked.

� A GST-free sale was incorrectly recorded or classified as being

taxable (i.e. subject to GST)

Errors

63

If an error on a previous BAS has the effect of increasing the

taxpayer’s tax liability, it may be able to make the correction on a later

BAS.

The adjustment is subject to timing and value limits.

Errors may occur in the following circumstances:

� If there was a clerical error, for example, the preparer double-counted

some creditable purchases or did not include some taxable sales.

� A taxable sale was incorrectly recorded or classified as being GST-

free on an earlier Activity Statement.

Errors

64

Error 3me and value limits (for errors that have the effect of increasing a taxpayer’s liability)

65

Refer to additional reading (“ATO determination on correcting GST

mistakes”) for more information on the application of these time and

value limits.

If the taxpayer makes an honest mistake that results in a shortfall in tax payable, the ATO will only require that the taxpayer adjust the Activity Statement to pay the correct amount plus a General Interest Charge (GIC).

Penal3es for errors

66

GIC rates

67

If the taxpayer makes a false or misleading statement that results in a shortfall in tax paid, in addition to being required to pay the shortfall plus a GIC, they may also have to pay a penalty (fine).

The base penalty is a % of the tax shortfall as follows:

� 25% where the mistake is caused by the taxpayer not taking reasonable care.

� 50% where the mistake is caused by the taxpayer being reckless.

� 75% where the mistake is caused by the taxpayer intentionally disregarding the law.

Penal3es for errors

68

3.

Payments and refunds

69

If a taxpayer chooses to mail the completed BAS/IAS to the ATO, a cheque may be attached for any required payment.

Alternatively, other acceptable payment options available include: � BPAY® � Credit card (conditions apply) � Direct credit � Direct debit � Cash, cheque or card at Australia Post outlets

Methods of payment

70

When a taxpayer is in a net payable position à owes money to the ATO � Where the taxpayer has a net tax liability on its Activity Statement,

payment is due on the same date lodgement of the Activity Statement is due.

When a taxpayer is in a net refund position à is owed money by the ATO � Where the taxpayer is in a net refund position, the ATO will issue a

refund once the Activity Statement has been processed. � If all the required information has been provided, refunds should be

processed within 14 working days after lodgement.

Timing of payment or refund

71

Throughout the tax period, the taxpayer should be

recording a liability for their tax obligations as they are

incurred.

e.g. when a sale is made, the GST payable on that sale

should be recorded as a liability in the accounting

records.

Recognising tax liabili3es in the accoun3ng records

72

GST collected is shown as a liability

on the Balance Sheet. GST paid

is shown as a contra-liability on

the Balance Sheet. As at 30 June 2016, Ruff

Cut owes the ATO $609.22 which it

will pay to the ATO when it lodges its

next BAS.

73

This week’s homework � Read the relevant chapter(s) (ref. DELIVERY

& ASSESSMENT GUIDE) � Complete all assigned activities.

74

You are now ready to start the next lesson on:

LCT, WET, FTC (and FBT)

75