Embed Size (px)

Citation preview

First Quarter 2016 GLOBAL ECONOMIC & CAPITAL MARKETS UPDATE

For investment professionals only. Not for further distribution.

2 2

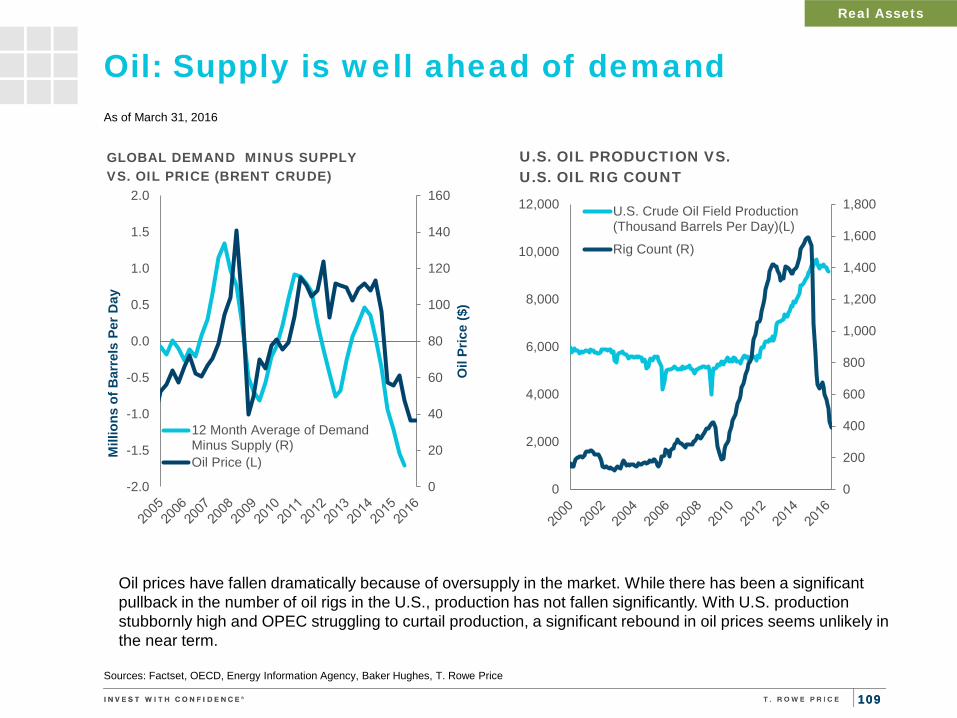

page 86

page 112

page 108

page 87

Table of Contents

Economics page 4

Capital Markets page 46

Equities page 48

Fixed Income

Real Assets

Global Risk Summary

Currency

3 3

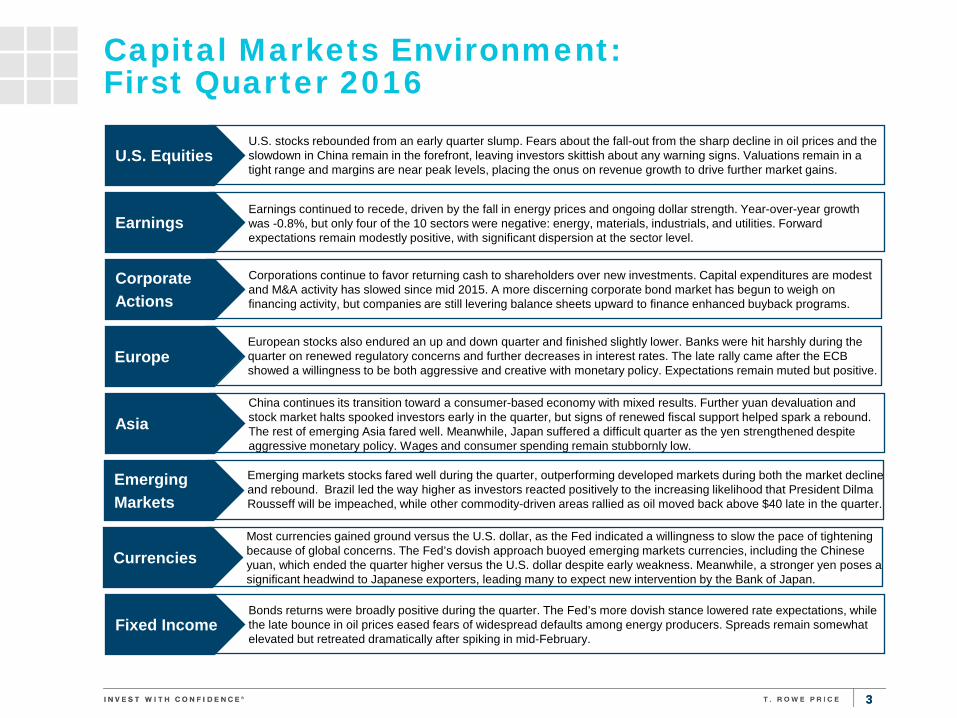

Capital Markets Environment: First Quarter 2016

U.S. Equities U.S. stocks rebounded from an early quarter slump. Fears about the fall-out from the sharp decline in oil prices and the slowdown in China remain in the forefront, leaving investors skittish about any warning signs. Valuations remain in a tight range and margins are near peak levels, placing the onus on revenue growth to drive further market gains.

Earnings Earnings continued to recede, driven by the fall in energy prices and ongoing dollar strength. Year-over-year growth was -0.8%, but only four of the 10 sectors were negative: energy, materials, industrials, and utilities. Forward expectations remain modestly positive, with significant dispersion at the sector level.

Corporate Actions

Corporations continue to favor returning cash to shareholders over new investments. Capital expenditures are modest and M&A activity has slowed since mid 2015. A more discerning corporate bond market has begun to weigh on financing activity, but companies are still levering balance sheets upward to finance enhanced buyback programs.

Asia China continues its transition toward a consumer-based economy with mixed results. Further yuan devaluation and stock market halts spooked investors early in the quarter, but signs of renewed fiscal support helped spark a rebound. The rest of emerging Asia fared well. Meanwhile, Japan suffered a difficult quarter as the yen strengthened despite aggressive monetary policy. Wages and consumer spending remain stubbornly low.

Emerging Markets

Emerging markets stocks fared well during the quarter, outperforming developed markets during both the market decline and rebound. Brazil led the way higher as investors reacted positively to the increasing likelihood that President Dilma Rousseff will be impeached, while other commodity-driven areas rallied as oil moved back above $40 late in the quarter.

Fixed Income Bonds returns were broadly positive during the quarter. The Fed’s more dovish stance lowered rate expectations, while the late bounce in oil prices eased fears of widespread defaults among energy producers. Spreads remain somewhat elevated but retreated dramatically after spiking in mid-February.

Currencies Most currencies gained ground versus the U.S. dollar, as the Fed indicated a willingness to slow the pace of tightening because of global concerns. The Fed’s dovish approach buoyed emerging markets currencies, including the Chinese yuan, which ended the quarter higher versus the U.S. dollar despite early weakness. Meanwhile, a stronger yen poses a significant headwind to Japanese exporters, leading many to expect new intervention by the Bank of Japan.

Europe European stocks also endured an up and down quarter and finished slightly lower. Banks were hit harshly during the quarter on renewed regulatory concerns and further decreases in interest rates. The late rally came after the ECB showed a willingness to be both aggressive and creative with monetary policy. Expectations remain muted but positive.

4 4

U.S. Economy: Measured growth continues

Sources: Factset, Bureau of Economic Analysis, Bureau of Labor Statistics, T. Rowe Price

Solid payroll gains and a falling unemployment rate suggest labor market health.

U.S. economic growth is likely to stay moderate and trend around 2%. We may see quarterly volatility but the year-on-year rate should be between 2.0% and 2.5%.

Economics Economics

-10

-8

-6

-4

-2

0

2

4

6

8

Perc

enta

ge C

hang

e, A

nnua

l Rat

e

REAL GDP GROWTH January 2006 – December 2015

-1,000

-800

-600

-400

-200

0

200

400

600

0

2

4

6

8

10

12

Mon

thly

Cha

nge

(thou

sand

s)

Une

mpl

oym

ent (

%)

UNEMPLOYMENT AND NON-FARM PAYROLLS January 2006– March 2016

Non-Farm Payrolls (R)

Unemployment (L)

5 5

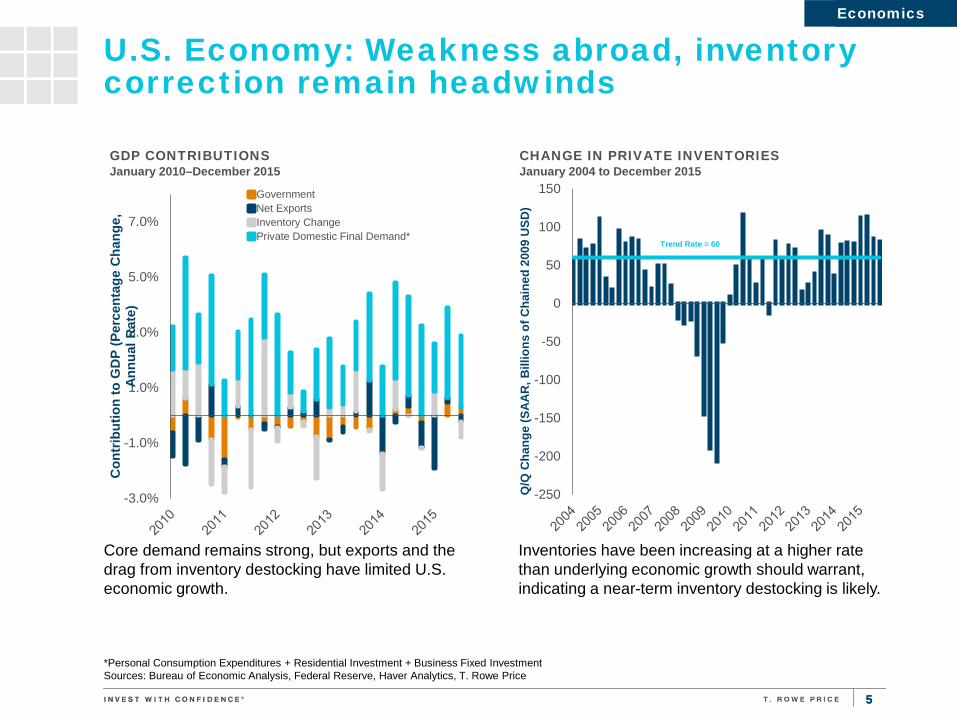

U.S. Economy: Weakness abroad, inventory correction remain headwinds

*Personal Consumption Expenditures + Residential Investment + Business Fixed Investment Sources: Bureau of Economic Analysis, Federal Reserve, Haver Analytics, T. Rowe Price

Inventories have been increasing at a higher rate than underlying economic growth should warrant, indicating a near-term inventory destocking is likely.

Core demand remains strong, but exports and the drag from inventory destocking have limited U.S. economic growth.

Economics Economics

-3.0%

-1.0%

1.0%

3.0%

5.0%

7.0%

Con

trib

utio

n to

GD

P (P

erce

ntag

e C

hang

e,

Annu

al R

ate)

GDP CONTRIBUTIONS January 2010–December 2015

GovernmentNet ExportsInventory ChangePrivate Domestic Final Demand*

Trend Rate = 60

-250

-200

-150

-100

-50

0

50

100

150

Q/Q

Cha

nge

(SA

AR

, Bill

ions

of C

hain

ed 2

009

USD

)

CHANGE IN PRIVATE INVENTORIES January 2004 to December 2015

6 6

Sources: Haver Analytics, Bureau of Economic Analysis, T. Rowe Price

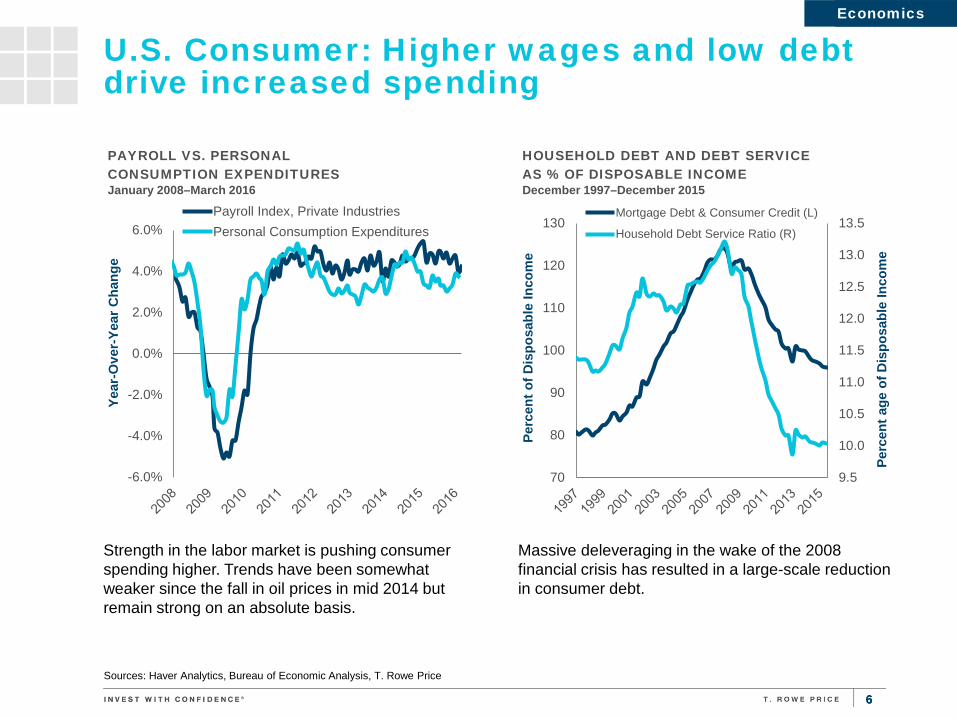

Strength in the labor market is pushing consumer spending higher. Trends have been somewhat weaker since the fall in oil prices in mid 2014 but remain strong on an absolute basis.

Massive deleveraging in the wake of the 2008 financial crisis has resulted in a large-scale reduction in consumer debt.

Economics Economics

U.S. Consumer: Higher wages and low debt drive increased spending

9.5

10.0

10.5

11.0

11.5

12.0

12.5

13.0

13.5

70

80

90

100

110

120

130

Perc

ent a

ge o

f Dis

posa

ble

Inco

me

Perc

ent o

f Dis

posa

ble

Inco

me

HOUSEHOLD DEBT AND DEBT SERVICE AS % OF DISPOSABLE INCOME December 1997–December 2015

Mortgage Debt & Consumer Credit (L)

Household Debt Service Ratio (R)

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

Year

-Ove

r-Ye

ar C

hang

e

PAYROLL VS. PERSONAL CONSUMPTION EXPENDITURES January 2008–March 2016

Payroll Index, Private IndustriesPersonal Consumption Expenditures

7 7

U.S. Economy: Business spending and housing rebound should support growth

Sources: Bureau of Economic Analysis, Bureau of Labor Statistics, Census Bureau, Haver Analytics, T. Rowe Price

Thus far in this cycle, we have not seen housing starts outpace household formation, meaning there is significant room for housing to accelerate.

A cutback in capital expenditures in the oil industry accounts for the decline in investment in structures over the past 4 quarters. This decline has created a significant drag in growth since mid-2014, a drag which may begin to subside in the near term.

Economics Economics

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Con

trib

utio

n to

GD

P

BUSINESS FIXED INVESTMENT January 2010–December 2015

Structures Equipment Intellectual Property

0

500

1000

1500

2000

0

400

800

1200

1600

2000

2400

12 Q

uart

er C

hang

e, A

nnua

lized

Thou

sand

s of

Uni

ts, S

AA

R

HOUSEHOLD FORMATION VS. HOUSING STARTS January 2000–December 2015 Housing Starts (L) Households (R)

8 8

U.S. Fiscal Environment: Government spending is a modest tailwind to growth

Sources: Haver Analytics, Bureau of Economic Analysis, Department of the Treasury, T. Rowe Price

Government finances and employment trends continue to improve. Government spending remains a slight contributor to, rather than a drag on, economic growth.

State and local sectors are making a modest contribution to growth.

Economics Economics

-200

-150

-100

-50

0

50

100

150

-1.0

-0.5

0.0

0.5

1.0

Qua

rter

ly C

hang

e in

Tho

usan

ds

Perc

enta

ge C

hang

e., A

R, 4

Qtr

. Avg

.

GOVERNMENT EXPENDITURES VS. GOVERNMENT EMPLOYMENT January 2007–December 2015

Gov't. Expenditures—Contribution to Real GDP (L)

Gov't. Employment (R)

-8

-6

-4

-2

0

2

4

6

8

10

Perc

enta

ge C

hang

e, Y

ear A

go

REAL GOVERNMENT EXPENDITURES January 2007–December 2015

State and Local Federal

9 9

U.S. Labor Market: Strong but moderating

Employment trends remain broadly positive, however the pace of job creation has moderated since the beginning of 2015.

The unemployment rate is approaching the lows from the prior economic cycle. Meanwhile, the reduction in “under employed” workers has been accelerating since the beginning of 2013, after showing little improvement in the early stages of the recovery.

Economics Economics

0

50

100

150

200

250

300

350

400

450

Cha

nge

in T

hous

ands

PAYROLL EMPLOYMENT January 2011–March 2016

Payroll Employment 12-month average

3

4

5

6

7

8

9

10

11

Perc

ent a

ge o

f Lab

or F

orce

UNEMPLOYMENT RATE VS. PART TIME January 2004–March 2016 Official (U3) Unemployment Rate

Marginally Attached and Involuntary Part TimeWorkers

Sources: Haver Analytics, Bureau of Labor Statistics, T. Rowe Price

10 10

U.S. Inflation: Rising labor costs should begin to affect inflation

PCE = Personal Consumption Expenditures Source: Bureau of Economic Analysis, Bureau of Labor Statistics, Haver Analytics, T. Rowe Price

Economics Economics

-2

-1

0

1

2

3

4

5

Year

-Ove

r-Ye

ar p

erce

ntag

e C

hang

e

PERSONAL CONSUMPTION EXPENDITURES (PCE) PRICE INDEX January 2006–February 2016

PCE Price IndexPCE Price Index Excl. Food & Energy

The increase in labor costs is beginning to have an effect on inflation as low unemployment and a tight labor market put upward pressure on wages.

The collapse in energy prices is keeping core inflation below the Fed’s 2% longer-term target. This effect is likely to fade as energy prices stabilize.

-3

-2

-1

0

1

2

3

4

-3

-2

-1

0

1

2

3

4

Year

-Ove

r-Ye

ar %

Cha

nge

8-Q

uart

er A

nnua

l Per

cent

age

Cha

nge

LABOR COSTS VS. PERSONAL CONSUMPTION EXPENDITURES (PCE) January 2006–December 2015

PCE Price Index Excl. Food & Energy* (R)Unit Labor Costs (L)

11 11

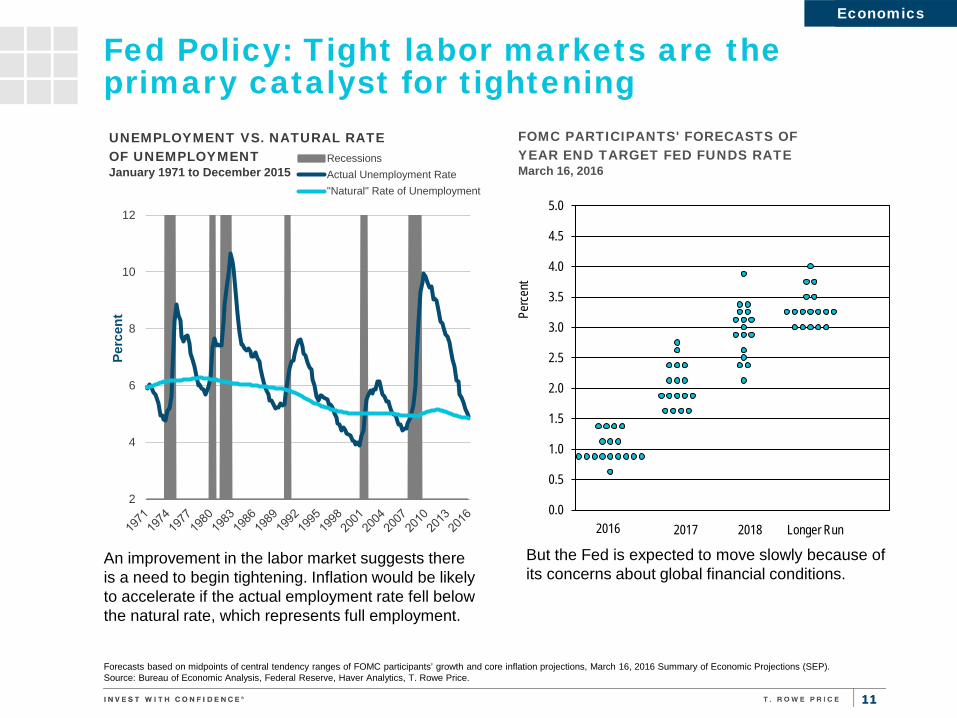

Fed Policy: Tight labor markets are the primary catalyst for tightening

An improvement in the labor market suggests there is a need to begin tightening. Inflation would be likely to accelerate if the actual employment rate fell below the natural rate, which represents full employment.

But the Fed is expected to move slowly because of its concerns about global financial conditions.

Economics Economics

Forecasts based on midpoints of central tendency ranges of FOMC participants’ growth and core inflation projections, March 16, 2016 Summary of Economic Projections (SEP). Source: Bureau of Economic Analysis, Federal Reserve, Haver Analytics, T. Rowe Price.

2

4

6

8

10

12

Perc

ent

UNEMPLOYMENT VS. NATURAL RATE OF UNEMPLOYMENT January 1971 to December 2015

RecessionsActual Unemployment Rate"Natural" Rate of Unemployment

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Perce

nt

FOMC PARTICIPANTS' FORECASTS OF YEAR END TARGET FED FUNDS RATE March 16, 2016

2016 2017 2018 Longer Run

12 12

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Year

-Ove

r-Ye

ar %

Cha

nge

BANK CREDIT GROWTH BY TYPE January 2007–December 2015

Consumer Commercial Real EstateResidential Real Estate Commercial and Industrial

U.S. Credit: Credit growth in industrial sector wavering

* All U.S. domestically chartered commercial banks, break adjusted and seasonally adjusted data Sources: Federal Reserve Board, Haver Analytics, T. Rowe Price

Credit growth in most areas continues to accelerate, with the notable exception of commercial and industrial loans. The uptick in consumer credit growth is a positive sign.

Credit growth has been healthy but volatile. Total credit growth moderated slightly in the second half of 2015, primarily due to a slowdown in corporate bond issuance.

Economics Economics

-15%

-10%

-5%

0%

5%

10%

15%

Year

-Ove

r-Ye

ar %

Cha

nge

CREDIT GROWTH BANK AND NON-BANK FINANCING January 2007–December 2015

Commercial bank loans and leases*

Total credit extended to private nonfinancial sectors

13 13

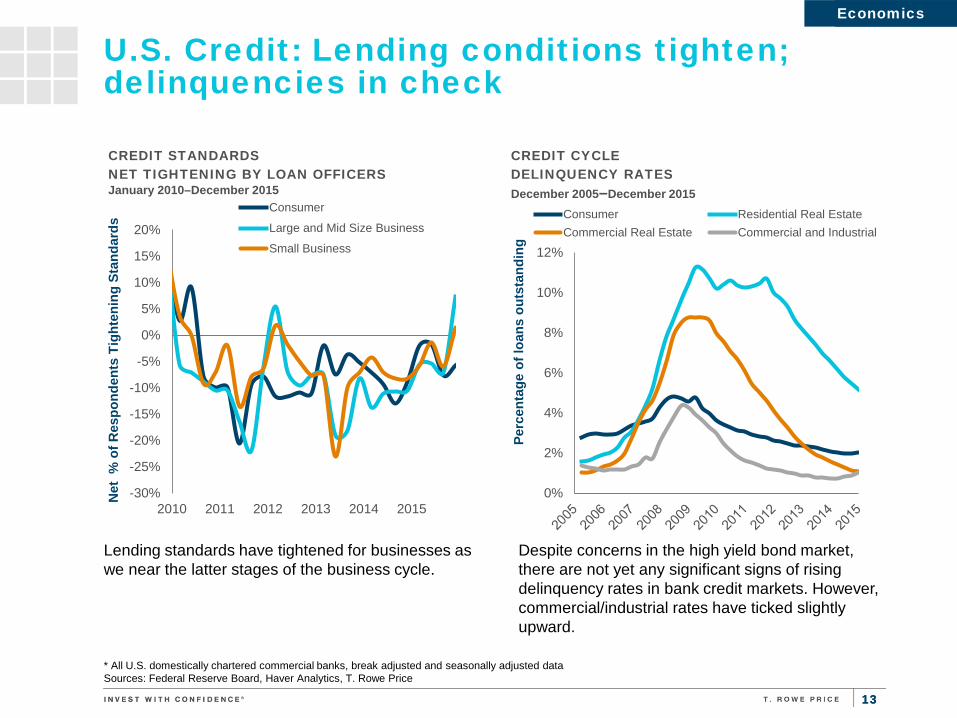

U.S. Credit: Lending conditions tighten; delinquencies in check

* All U.S. domestically chartered commercial banks, break adjusted and seasonally adjusted data Sources: Federal Reserve Board, Haver Analytics, T. Rowe Price

Despite concerns in the high yield bond market, there are not yet any significant signs of rising delinquency rates in bank credit markets. However, commercial/industrial rates have ticked slightly upward.

Lending standards have tightened for businesses as we near the latter stages of the business cycle.

Economics Economics

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

2010 2011 2012 2013 2014 2015

Net

% o

f Res

pond

ents

Tig

hten

ing

Stan

dard

s

CREDIT STANDARDS NET TIGHTENING BY LOAN OFFICERS January 2010–December 2015

Consumer

Large and Mid Size Business

Small Business

0%

2%

4%

6%

8%

10%

12%

Perc

enta

ge o

f loa

ns o

utst

andi

ng

CREDIT CYCLE DELINQUENCY RATES December 2005–December 2015

Consumer Residential Real EstateCommercial Real Estate Commercial and Industrial

14 14

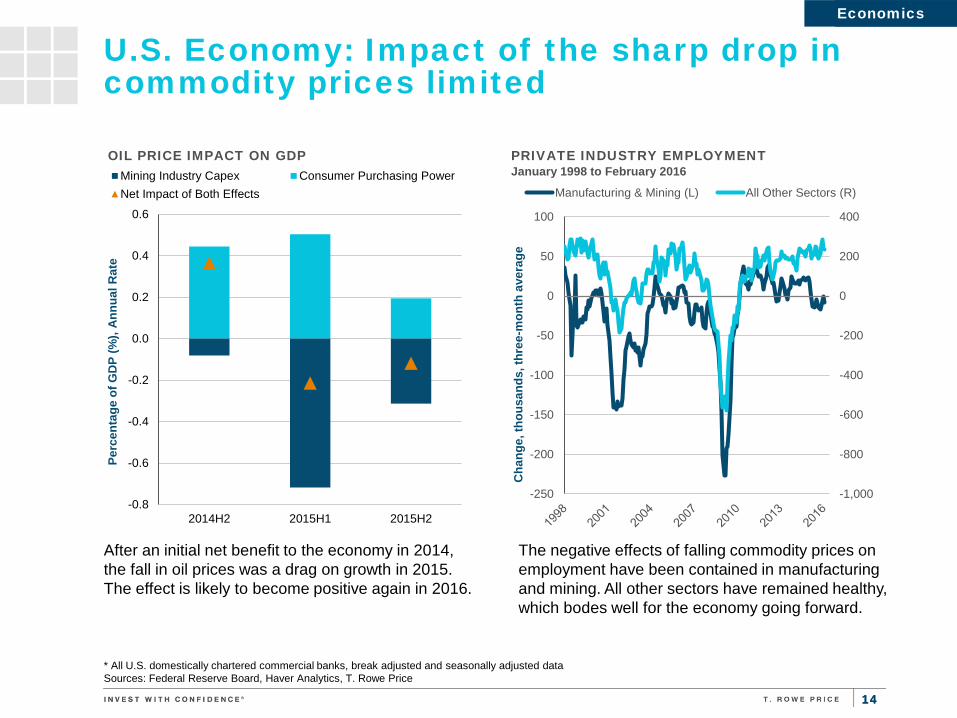

U.S. Economy: Impact of the sharp drop in commodity prices limited

* All U.S. domestically chartered commercial banks, break adjusted and seasonally adjusted data Sources: Federal Reserve Board, Haver Analytics, T. Rowe Price

The negative effects of falling commodity prices on employment have been contained in manufacturing and mining. All other sectors have remained healthy, which bodes well for the economy going forward.

After an initial net benefit to the economy in 2014, the fall in oil prices was a drag on growth in 2015. The effect is likely to become positive again in 2016.

Economics Economics

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

2014H2 2015H1 2015H2

Perc

enta

ge o

f GD

P (%

), A

nnua

l Rat

e

OIL PRICE IMPACT ON GDP Mining Industry Capex Consumer Purchasing PowerNet Impact of Both Effects

-1,000

-800

-600

-400

-200

0

200

400

-250

-200

-150

-100

-50

0

50

100

Cha

nge,

thou

sand

s, th

ree-

mon

th a

vera

ge

PRIVATE INDUSTRY EMPLOYMENT January 1998 to February 2016

Manufacturing & Mining (L) All Other Sectors (R)

15 15

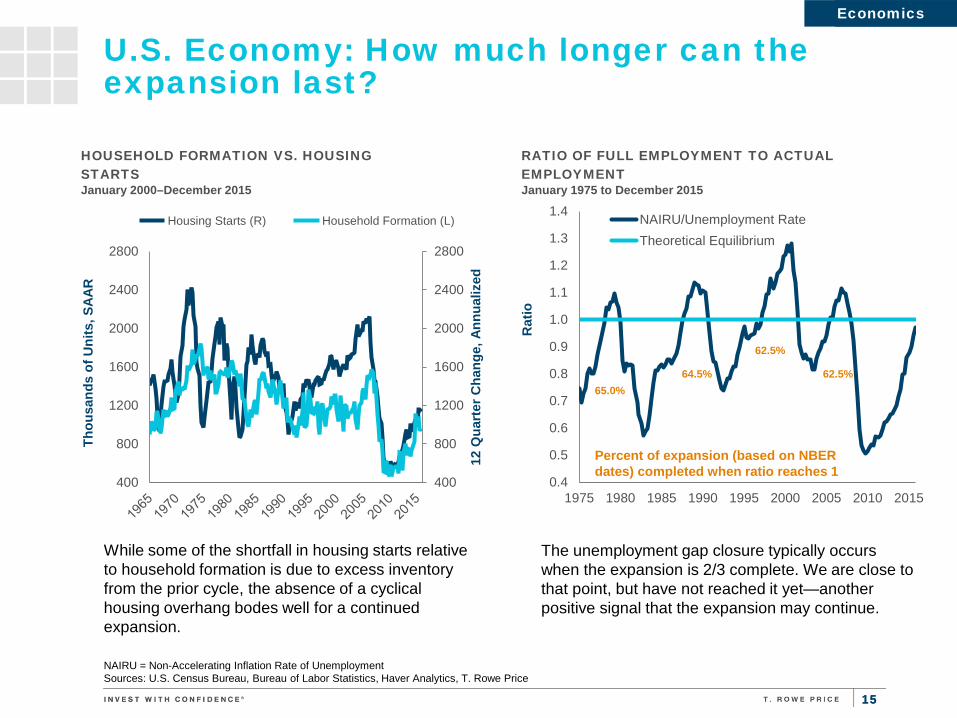

U.S. Economy: How much longer can the expansion last?

NAIRU = Non-Accelerating Inflation Rate of Unemployment Sources: U.S. Census Bureau, Bureau of Labor Statistics, Haver Analytics, T. Rowe Price

The unemployment gap closure typically occurs when the expansion is 2/3 complete. We are close to that point, but have not reached it yet—another positive signal that the expansion may continue.

While some of the shortfall in housing starts relative to household formation is due to excess inventory from the prior cycle, the absence of a cyclical housing overhang bodes well for a continued expansion.

Economics Economics

400

800

1200

1600

2000

2400

2800

400

800

1200

1600

2000

2400

2800

12 Q

uart

er C

hang

e, A

nnua

lized

Thou

sand

s of

Uni

ts, S

AA

R

HOUSEHOLD FORMATION VS. HOUSING STARTS January 2000–December 2015 Housing Starts (R) Household Formation (L)

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1975 1980 1985 1990 1995 2000 2005 2010 2015

Rat

io

RATIO OF FULL EMPLOYMENT TO ACTUAL EMPLOYMENT January 1975 to December 2015

NAIRU/Unemployment RateTheoretical Equilibrium

Percent of expansion (based on NBER dates) completed when ratio reaches 1

65.0% 64.5%

62.5%

62.5%

16 16

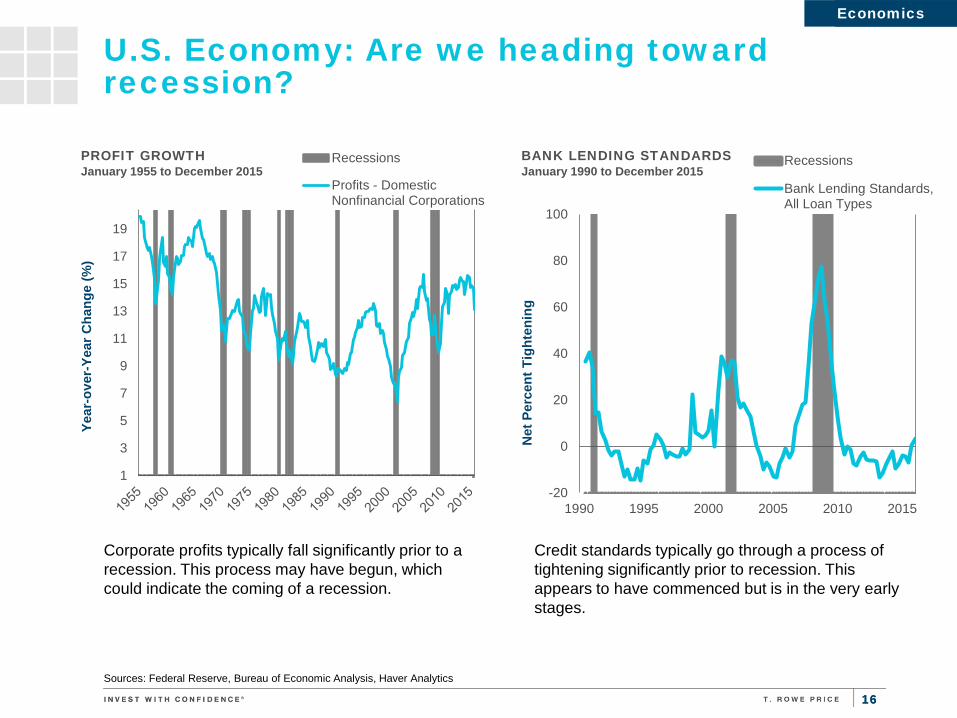

U.S. Economy: Are we heading toward recession?

Sources: Federal Reserve, Bureau of Economic Analysis, Haver Analytics

Credit standards typically go through a process of tightening significantly prior to recession. This appears to have commenced but is in the very early stages.

Corporate profits typically fall significantly prior to a recession. This process may have begun, which could indicate the coming of a recession.

Economics Economics

-20

0

20

40

60

80

100

1990 1995 2000 2005 2010 2015N

et P

erce

nt T

ight

enin

g

BANK LENDING STANDARDS January 1990 to December 2015

Recessions

Bank Lending Standards,All Loan Types

1

3

5

7

9

11

13

15

17

19

Year

-ove

r-Ye

ar C

hang

e (%

)

PROFIT GROWTH January 1955 to December 2015

Recessions

Profits - DomesticNonfinancial Corporations

17 17

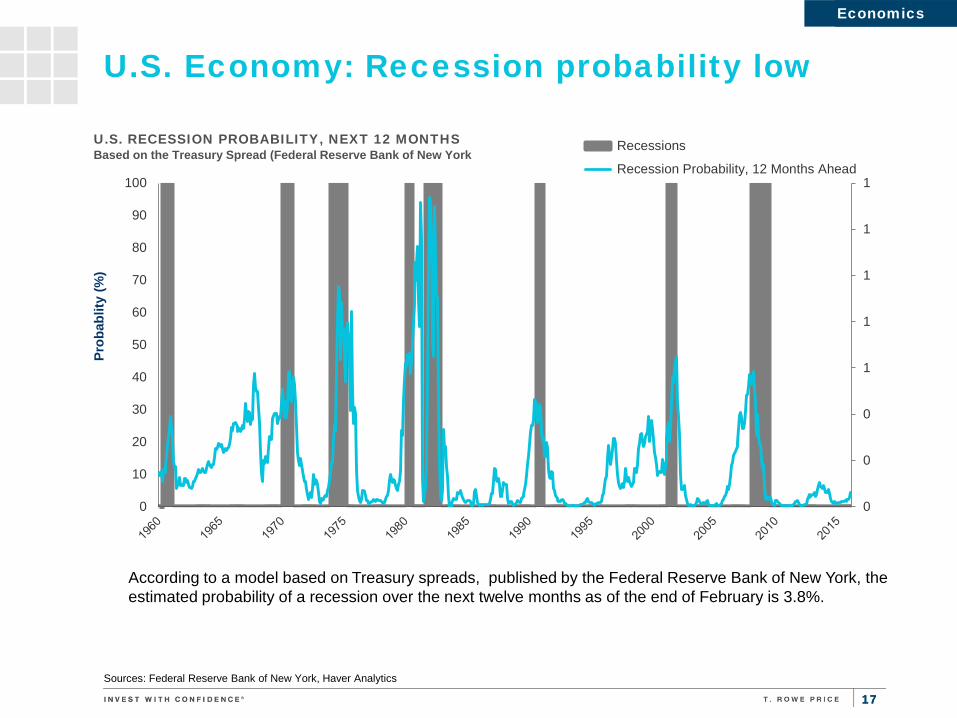

U.S. Economy: Recession probability low

Sources: Federal Reserve Bank of New York, Haver Analytics

According to a model based on Treasury spreads, published by the Federal Reserve Bank of New York, the estimated probability of a recession over the next twelve months as of the end of February is 3.8%.

Economics Economics

0

0

0

1

1

1

1

1

0

10

20

30

40

50

60

70

80

90

100

Prob

ablit

y (%

)

U.S. RECESSION PROBABILITY, NEXT 12 MONTHS Based on the Treasury Spread (Federal Reserve Bank of New York

Recessions

Recession Probability, 12 Months Ahead

18

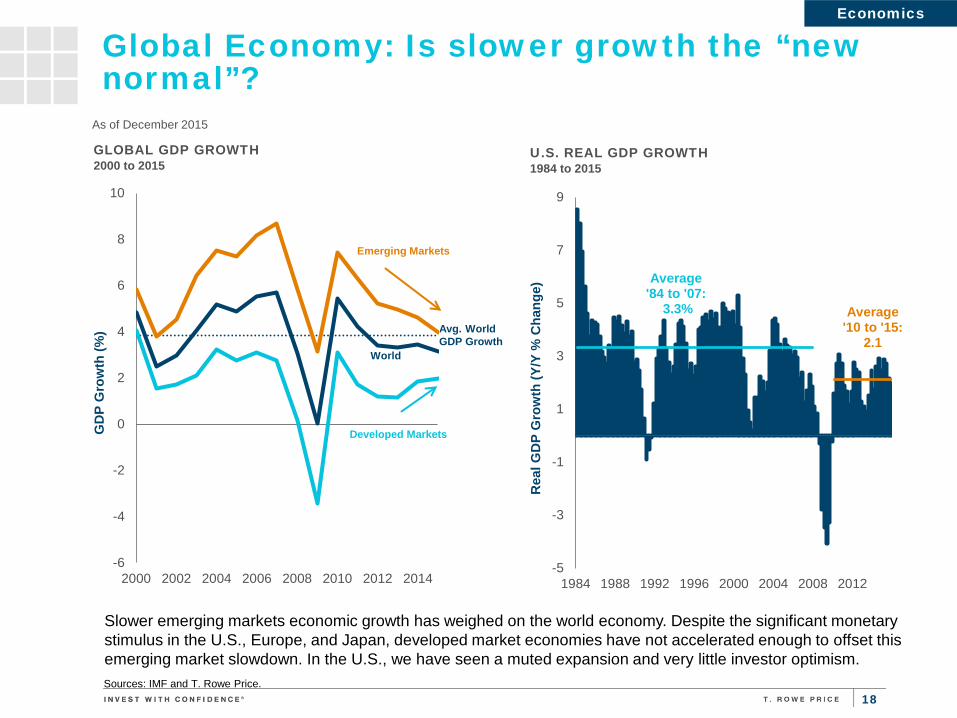

Slower emerging markets economic growth has weighed on the world economy. Despite the significant monetary stimulus in the U.S., Europe, and Japan, developed market economies have not accelerated enough to offset this emerging market slowdown. In the U.S., we have seen a muted expansion and very little investor optimism.

-6

-4

-2

0

2

4

6

8

10

2000 2002 2004 2006 2008 2010 2012 2014

GD

P G

row

th (%

)

GLOBAL GDP GROWTH 2000 to 2015

As of December 2015

Sources: IMF and T. Rowe Price.

Global Economy: Is slower growth the “new normal”?

World

Avg. World GDP Growth

Emerging Markets

Developed Markets

Economics

Average '84 to '07:

3.3% Average '10 to '15:

2.1

-5

-3

-1

1

3

5

7

9

1984 1988 1992 1996 2000 2004 2008 2012

Rea

l GD

P G

row

th (Y

/Y %

Cha

nge)

U.S. REAL GDP GROWTH 1984 to 2015

19 19

Global Economy: Weakness evident among commodity-producing nations

Sources: Haver Analytics, IMF, Markit, T.Rowe Price

GLOBAL MANUFACTURING PMIs As of March 2016

PMI < 50 & Declining m/m PMI < 50 & Increasing m/m PMI > 50 & Declining m/m PMI > 50 & Increasing m/m Scale:

Economics Economics

Mar-16 Feb-16 Jan-16 Dec-15 Nov-15 Oct-15 Sep-15 Aug-15 Jul-15 Jun-15 May-15 Apr-15 Mar-15

Global 50.5 50.0 50.9 50.9 51.2 51.3 50.6 50.7 51.1 51.0 51.3 51.0 51.8

Americas

U.S. 51.5 51.3 52.4 51.2 52.8 54.1 53.1 53.0 53.8 53.6 54.0 54.1 55.7

Canada 51.5 49.4 49.3 47.5 48.6 48.0 48.6 49.4 50.8 51.3 49.8 49.0 48.9

Mexico 53.2 53.1 52.2 52.4 53.0 53.0 52.1 52.4 52.9 52.0 53.3 53.8 53.8

Brazil 46.1 44.5 47.4 45.6 43.8 44.1 47.0 45.8 47.2 46.5 46.0 46.0 46.2

Asia / Pacific

Japan 49.1 50.1 52.3 52.6 52.6 52.4 51.0 51.7 51.2 50.1 50.9 49.9 50.3

Australia 58.1 53.5 51.5 51.9 52.5 50.2 52.1 51.7 50.4 44.2 52.3 48.0 46.3

China 49.7 48.0 48.4 48.3 48.6 48.3 47.2 47.3 47.8 49.4 49.2 48.9 49.6

South Korea 49.5 48.7 49.5 50.7 49.1 49.1 49.2 47.9 47.6 46.1 47.8 48.8 49.2

India 52.4 51.1 51.1 49.1 50.3 50.7 51.2 52.4 52.7 51.3 52.6 51.3 52.1

Indonesia 50.6 48.7 48.9 47.8 46.9 47.8 47.4 48.4 47.3 47.8 47.1 46.7 46.4

Europe / Africa

U.K. 51.0 50.8 52.9 51.9 52.5 55.5 51.5 51.6 51.9 51.4 51.9 51.8 54.3

Euro Area 51.6 51.2 52.3 53.2 52.8 52.3 52.1 52.3 52.4 52.5 52.3 52.0 52.2

Russia 48.3 49.3 49.8 48.7 50.1 50.2 49.1 47.9 48.3 48.7 47.6 48.9 48.1

South Africa 50.5 47.1 43.5 45.5 43.3 48.1 49.0 48.9 51.4 50.0 49.5 47.9 47.9

Turkey 49.2 50.3 50.9 52.2 50.9 49.5 48.8 49.3 50.1 49.0 50.2 48.5 48.0

20 20

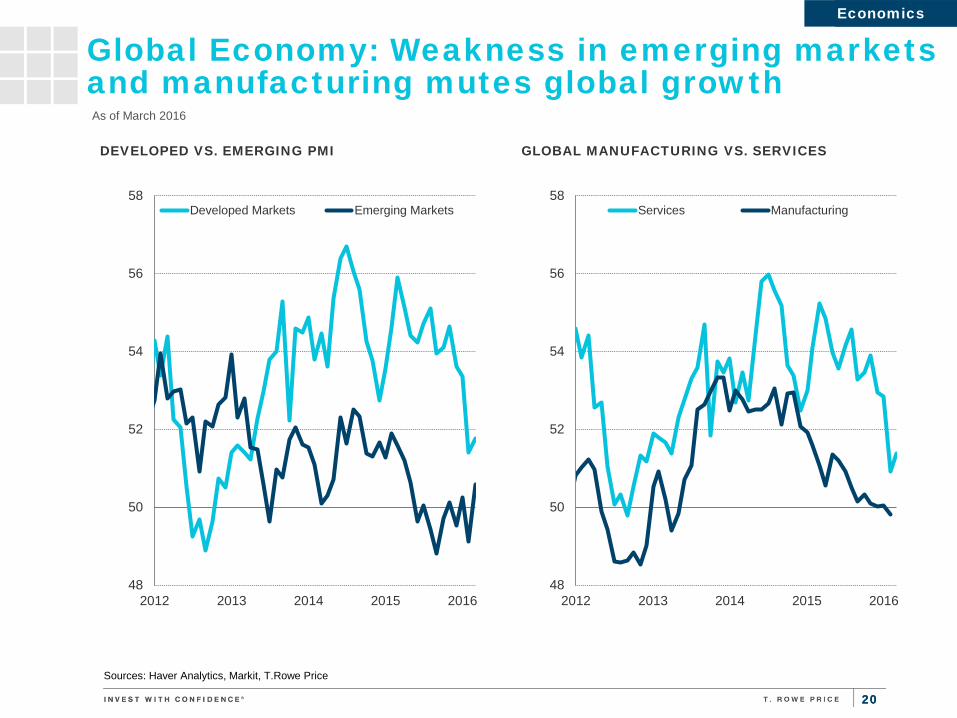

Global Economy: Weakness in emerging markets and manufacturing mutes global growth

Sources: Haver Analytics, Markit, T.Rowe Price

Economics Economics

As of March 2016

48

50

52

54

56

58

2012 2013 2014 2015 2016

DEVELOPED VS. EMERGING PMI

Developed Markets Emerging Markets

48

50

52

54

56

58

2012 2013 2014 2015 2016

GLOBAL MANUFACTURING VS. SERVICES

Services Manufacturing

21 21

Global Economy: Manufacturing weakness is most pronounced in China and the U.S.

Sources: Haver Analytics, Markit, T.Rowe Price

Economics Economics

As of March 2016

44

46

48

50

52

54

56

58

60

2012 2013 2014 2015 2016

GLOBAL PMI

Services Manufacturing

44

46

48

50

52

54

56

58

60

2012 2013 2014 2015 2016

USA PMI

Services Manufacturing

44

46

48

50

52

54

56

58

60

2012 2013 2014 2015 2016

EURO AREA PMI

Services Manufacturing

44

46

48

50

52

54

56

58

60

2012 2013 2014 2015 2016

JAPAN PMI

Services Manufacturing

44

46

48

50

52

54

56

58

60

2012 2013 2014 2015 2016

EMERGING MARKETS PMI

Services Manufacturing

44

46

48

50

52

54

56

58

60

2012 2013 2014 2015 2016

CHINA PMI

Services Manufacturing

22 22

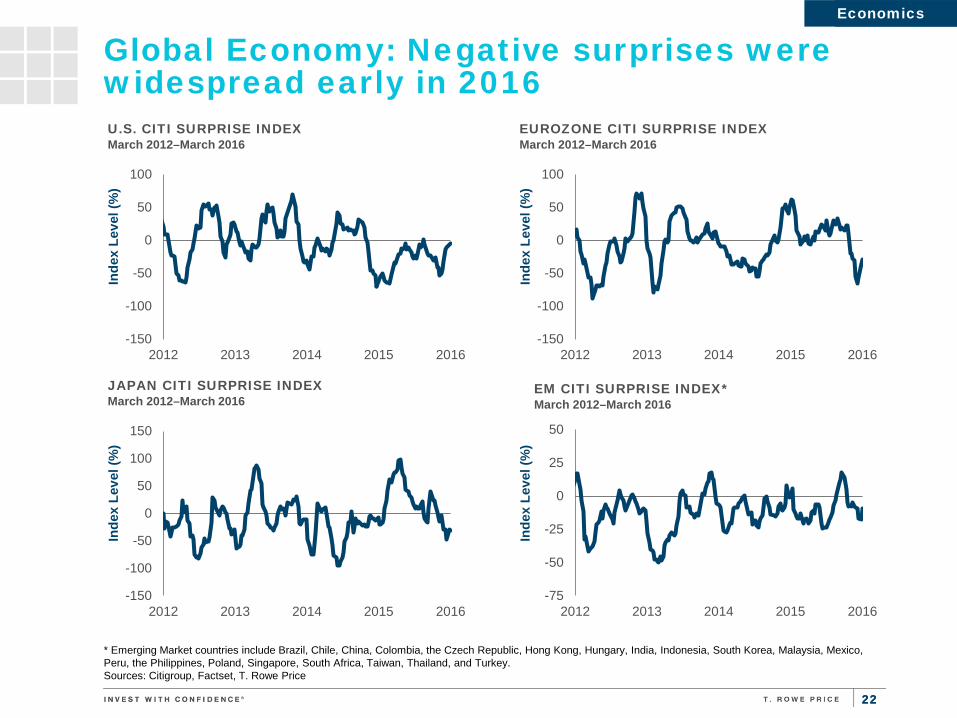

Global Economy: Negative surprises were widespread early in 2016

* Emerging Market countries include Brazil, Chile, China, Colombia, the Czech Republic, Hong Kong, Hungary, India, Indonesia, South Korea, Malaysia, Mexico, Peru, the Philippines, Poland, Singapore, South Africa, Taiwan, Thailand, and Turkey. Sources: Citigroup, Factset, T. Rowe Price

Economics Economics

-150

-100

-50

0

50

100

2012 2013 2014 2015 2016

Inde

x Le

vel (

%)

U.S. CITI SURPRISE INDEX March 2012–March 2016

-150

-100

-50

0

50

100

2012 2013 2014 2015 2016

Inde

x Le

vel (

%)

EUROZONE CITI SURPRISE INDEX March 2012–March 2016

-150

-100

-50

0

50

100

150

2012 2013 2014 2015 2016

Inde

x Le

vel (

%)

JAPAN CITI SURPRISE INDEX March 2012–March 2016

-75

-50

-25

0

25

50

2012 2013 2014 2015 2016

Inde

x Le

vel (

%)

EM CITI SURPRISE INDEX* March 2012–March 2016

23 23

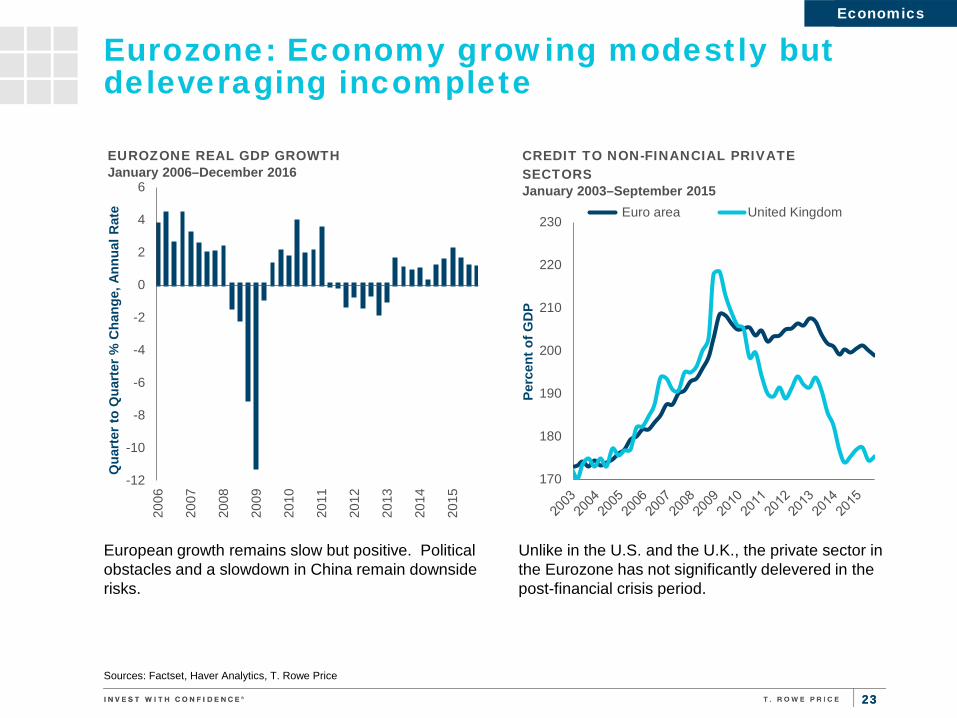

Eurozone: Economy growing modestly but deleveraging incomplete

Sources: Factset, Haver Analytics, T. Rowe Price

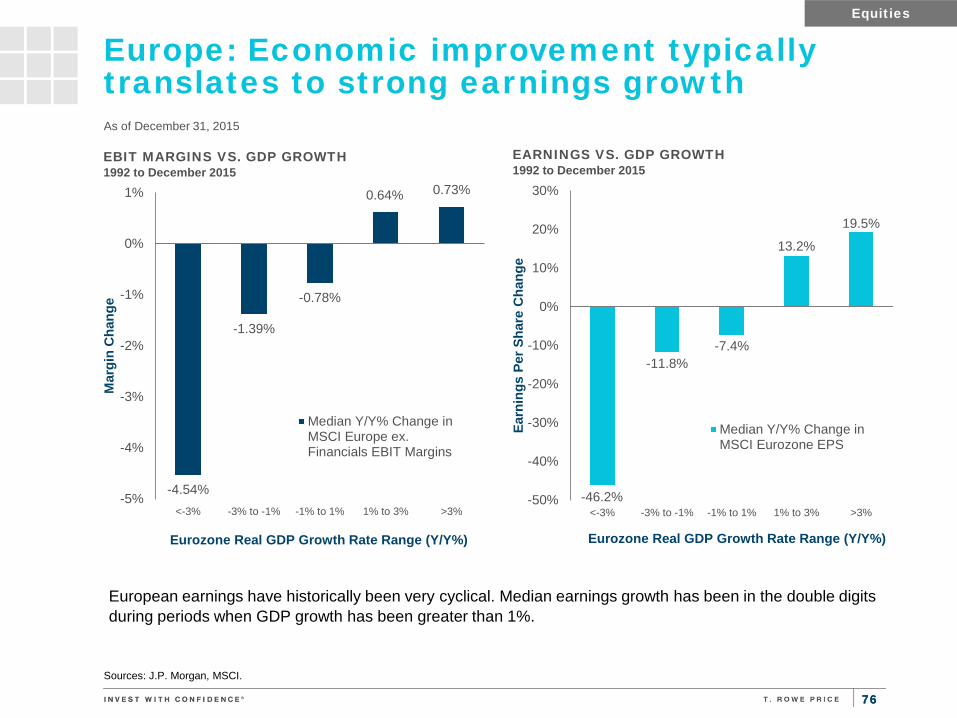

Unlike in the U.S. and the U.K., the private sector in the Eurozone has not significantly delevered in the post-financial crisis period.

European growth remains slow but positive. Political obstacles and a slowdown in China remain downside risks.

Economics Economics

-12

-10

-8

-6

-4

-2

0

2

4

6

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Qua

rter

to Q

uart

er %

Cha

nge,

Ann

ual R

ate

EUROZONE REAL GDP GROWTH January 2006–December 2016

170

180

190

200

210

220

230

Perc

ent o

f GD

P

CREDIT TO NON-FINANCIAL PRIVATE SECTORS January 2003–September 2015

Euro area United Kingdom

24 24

Eurozone: Quantitative easing a success thus far

Sources: Haver Analytics, Markit, European Central Bank, T. Rowe Price

Better financing conditions allow banks to loosen lending standards, while expectations for renewed economic growth boost demand for consumer and business loans. Demand remains strong but supply is wavering as European banks are struggling with low (or negative) rates and increased regulations.

Money supply is growing, spurred by the ECB’s quantitative easing program. Lower financing costs should encourage companies to increase capital expenditures, thereby boosting economic growth.

Economics Economics

0

2

4

6

8

10

12

14

42

44

46

48

50

52

54

56

58

60

2010 2011 2012 2013 2014 2015 2016

M1

Annu

al G

row

th R

ate

(%)

Euro

zone

PM

I

MONEY SUPPLY VS. PMI January 2010– February 2016

Eurozone Flash PMI (12 month lag)

ECB Money Supply: M1: AnnualGrowth Rate

-80

-60

-40

-20

0

20

40

60

80-80

-60

-40

-20

0

20

40

60

80

2006 2008 2010 2012 2014

Cha

nge

in L

endi

ng S

tand

ards

(%) (

Inve

rted

)

Cha

nge

in D

eman

d (%

)

ECB BANK LENDING SURVEY January 2006– March 2016

Business Loan Demand (L)

Household Loan Demand (L)

Lending Standards for Business (R)

Lending Standards for Households (R)

25 25

Eurozone: Periphery conditions improving

Sources: Haver Analytics, European Central Bank, Banca d’Italia, Banco de Espana, Central Statistics Office Ireland, Greece Ministry of Finance, T. Rowe Price

Many of the periphery countries have also made significant progress in balancing their fiscal budgets, although Italy’s progress has been mixed. These improvements should open the way for the pullback in austerity programs going forward.

The current account balances of periphery countries have benefited from a weaker euro.

Economics Economics

-16

-14

-12

-10

-8

-6

-4

-2

0

2

4

6

2009 2010 2011 2012 2013 2014 2015 2016

Perc

ent o

f GD

P

CURRENT ACCOUNT BALANCES 2009 to 2015

Euro Area Portugal ItalyGreece Spain

-30

-25

-20

-15

-10

-5

0

5

2009 2010 2011 2012 2013 2014 2015

Perc

ent o

f GD

P

FISCAL BALANCES 2009 to 2015

Spain Greece Ireland Italy

26 26

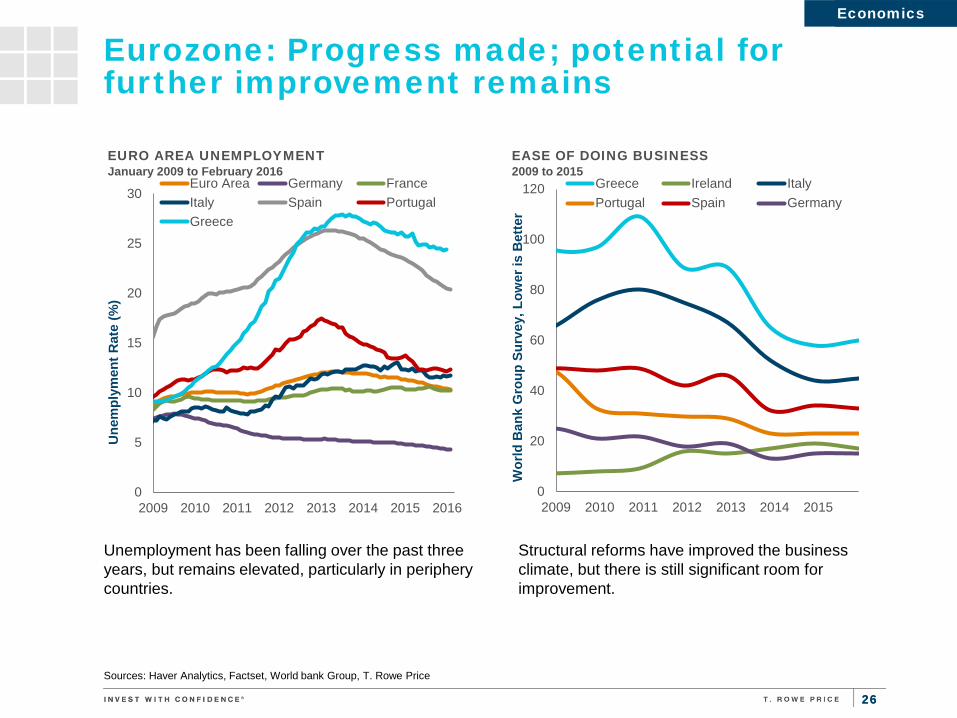

Eurozone: Progress made; potential for further improvement remains

Sources: Haver Analytics, Factset, World bank Group, T. Rowe Price

Structural reforms have improved the business climate, but there is still significant room for improvement.

Unemployment has been falling over the past three years, but remains elevated, particularly in periphery countries.

Economics Economics

0

5

10

15

20

25

30

2009 2010 2011 2012 2013 2014 2015 2016

Une

mpl

ymen

t Rat

e (%

)

EURO AREA UNEMPLOYMENT January 2009 to February 2016

Euro Area Germany FranceItaly Spain PortugalGreece

0

20

40

60

80

100

120

2009 2010 2011 2012 2013 2014 2015W

orld

Ban

k G

roup

Sur

vey,

Low

er is

Bet

ter

EASE OF DOING BUSINESS 2009 to 2015

Greece Ireland ItalyPortugal Spain Germany

27 27

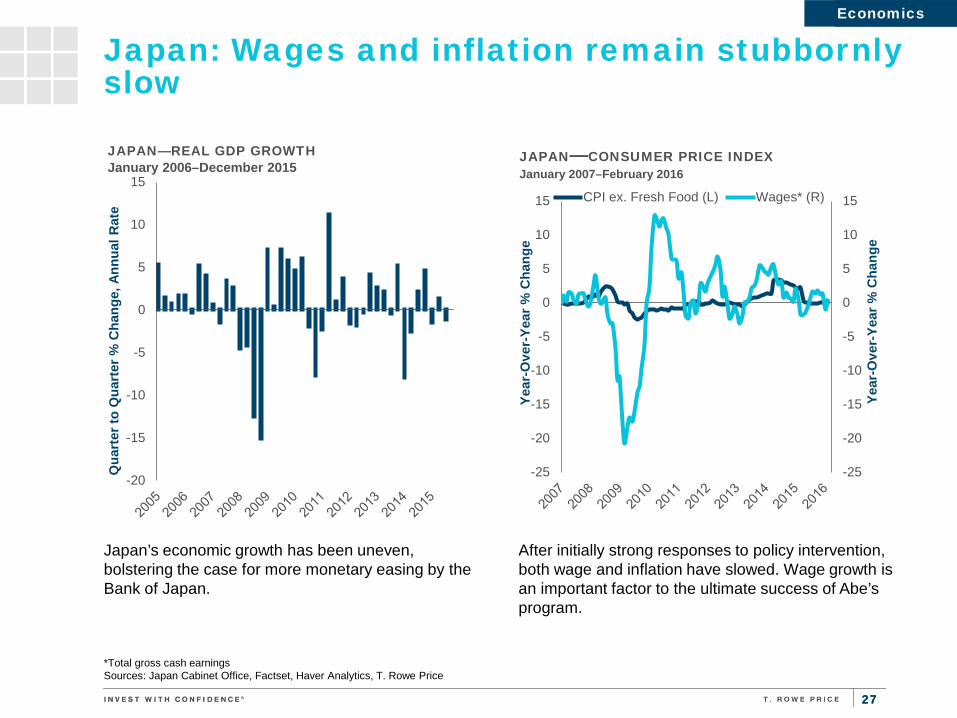

Japan: Wages and inflation remain stubbornly slow

*Total gross cash earnings Sources: Japan Cabinet Office, Factset, Haver Analytics, T. Rowe Price

After initially strong responses to policy intervention, both wage and inflation have slowed. Wage growth is an important factor to the ultimate success of Abe’s program.

Japan’s economic growth has been uneven, bolstering the case for more monetary easing by the Bank of Japan.

Economics Economics

-20

-15

-10

-5

0

5

10

15

Qua

rter

to Q

uart

er %

Cha

nge,

Ann

ual R

ate

JAPAN—REAL GDP GROWTH January 2006–December 2015

-25

-20

-15

-10

-5

0

5

10

15

-25

-20

-15

-10

-5

0

5

10

15

Year

-Ove

r-Ye

ar %

Cha

nge

Year

-Ove

r-Ye

ar %

Cha

nge

JAPAN—CONSUMER PRICE INDEX January 2007–February 2016

CPI ex. Fresh Food (L) Wages* (R)

28 28

Japan: Domestic consumption hampered by tax, demographics

Sources: Cabinet Office of Japan, Japan Ministry of Health, Labour & Welfare, Haver Analytics, T. Rowe Price

Labor force participation has improved in recent years, but the aging of the population remains a significant challenge.

Domestic consumption has stagnated since the consumption tax was increased from 5% to 8% in 2014.

Economics Economics

6,500

6,550

6,600

6,650

6,700

6,750

6,800

6,850

1996 1999 2002 2005 2008 2011 2014Te

n Th

ousa

nd P

erso

ns, S

AA

R

JAPAN - TOTAL LABOR FORCE January 1996 to March 2016

0%

2%

4%

6%

8%

10%

12%

14%

2009 2010 2011 2012 2013 2014 2015 2016

Cum

ulat

ive

Gro

wth

Sin

ce M

arch

200

9

JAPAN - SOURCES OF CONSUMPTION GROWTH 1Q09 to 4Q15 Private Consumption

Government Consumption

29 29

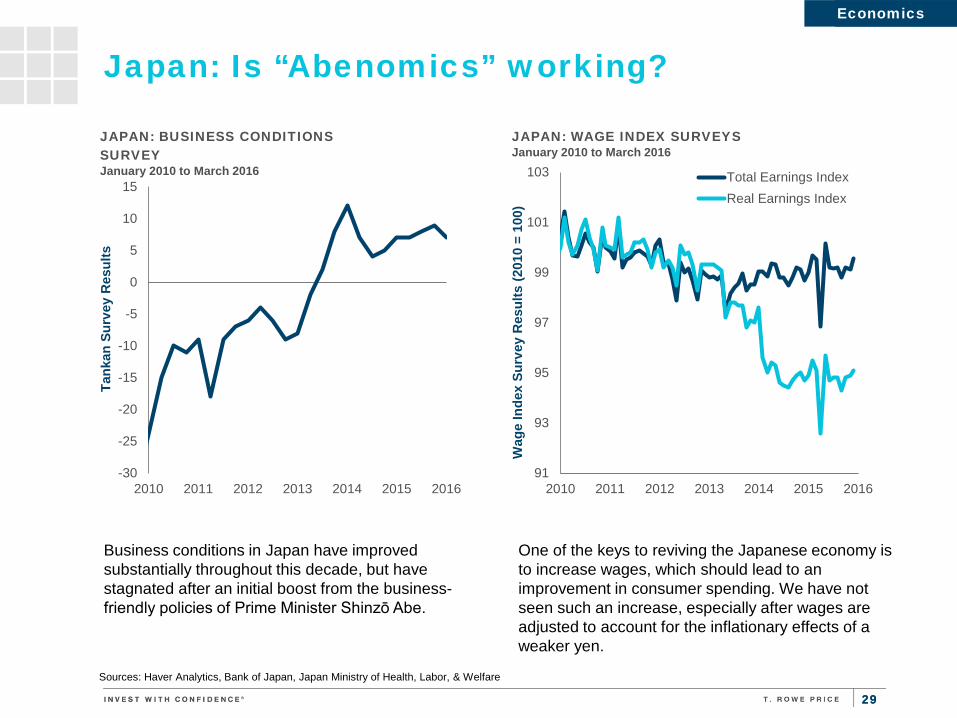

Japan: Is “Abenomics” working?

Sources: Haver Analytics, Bank of Japan, Japan Ministry of Health, Labor, & Welfare

One of the keys to reviving the Japanese economy is to increase wages, which should lead to an improvement in consumer spending. We have not seen such an increase, especially after wages are adjusted to account for the inflationary effects of a weaker yen.

Business conditions in Japan have improved substantially throughout this decade, but have stagnated after an initial boost from the business-friendly policies of Prime Minister Shinzō Abe.

Economics Economics

-30

-25

-20

-15

-10

-5

0

5

10

15

2010 2011 2012 2013 2014 2015 2016

Tank

an S

urve

y R

esul

ts

JAPAN: BUSINESS CONDITIONS SURVEY January 2010 to March 2016

91

93

95

97

99

101

103

2010 2011 2012 2013 2014 2015 2016

Wag

e In

dex

Surv

ey R

esul

ts (2

010

= 10

0)

JAPAN: WAGE INDEX SURVEYS January 2010 to March 2016

Total Earnings IndexReal Earnings Index

30 30

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

2010 2011 2012 2013 2014 2015 2016

Year

-Ove

r-Ye

ar P

erce

ntag

e C

hang

e

EMERGING MARKETS INFLATION January 2010–March 2016

India Brazil China Russia

0

2

4

6

8

10

12

14

16

18

20

2010 2011 2012 2013 2014 2015 Pe

rcen

t (%

)

EMERGING MARKETS CENTRAL BANK RATES January 2010–March 2016

India Brazil China Russia

Emerging Markets: Divergent monetary paths

Sources: Various National Statistical Agencies, Haver Analytics, T. Rowe Price

As growth slows and inflation moderates, many central banks in emerging markets are shifting from tightening to easing monetary policies.

Inflation levels vary significantly across emerging markets. Inflation is accelerating in countries that are most vulnerable to currency devaluation, although this effect has moderated thus far in 2016.

Central Bank policy rate: All Items CPI:

Economics Economics

31 31

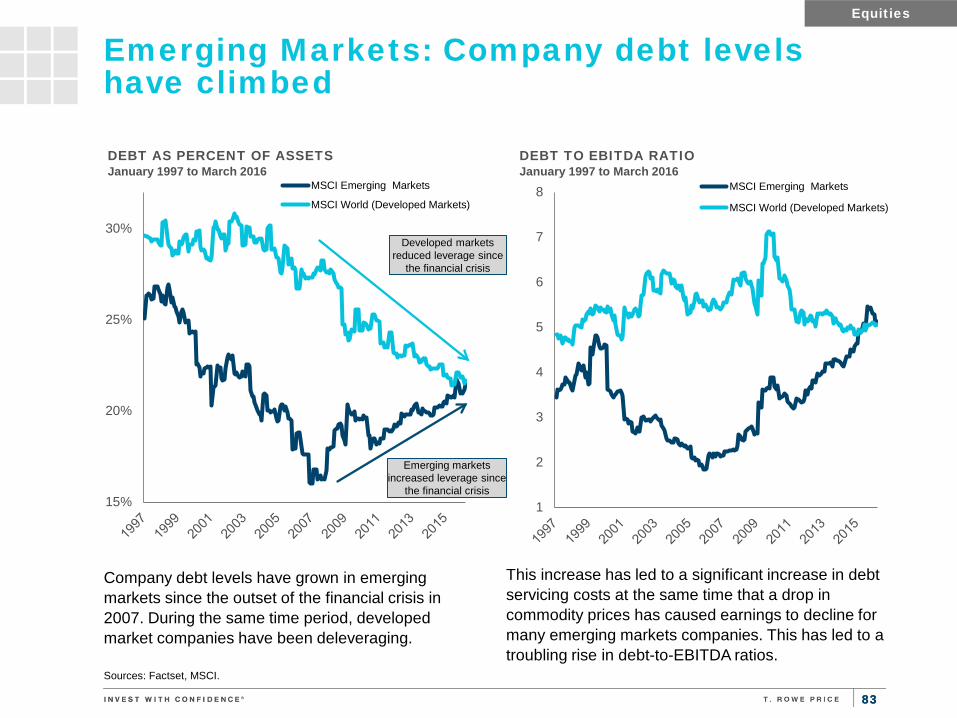

Emerging Markets: Commodity producers face elevated risks

Private credit (non-government) has grown significantly in emerging markets since 2007, but rates vary widely among countries. Most emerging markets have relatively small debt loads relative to developed markets. Markets that have issued new debt to build capacity for commodity production are most at risk, especially if commodity prices remain low.

Economics Economics

Sources: Bank for International Settlements, Haver Analytics, T. Rowe Price

-50

0

50

100

150

200

Priv

ate

Non

-Fin

anci

al C

redi

t as

% o

f GD

P PRIVATE NON-FINANCIAL CREDIT

1997 2007 Current Change since 2007

32 32

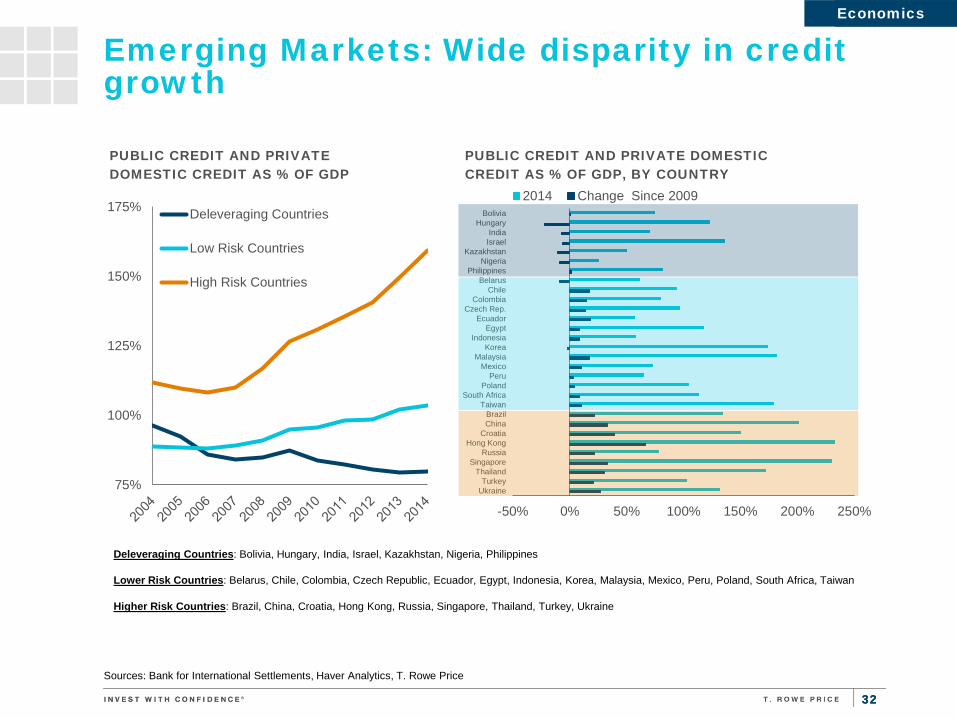

Emerging Markets: Wide disparity in credit growth

Deleveraging Countries: Bolivia, Hungary, India, Israel, Kazakhstan, Nigeria, Philippines

Lower Risk Countries: Belarus, Chile, Colombia, Czech Republic, Ecuador, Egypt, Indonesia, Korea, Malaysia, Mexico, Peru, Poland, South Africa, Taiwan

Higher Risk Countries: Brazil, China, Croatia, Hong Kong, Russia, Singapore, Thailand, Turkey, Ukraine

Economics Economics

Sources: Bank for International Settlements, Haver Analytics, T. Rowe Price

75%

100%

125%

150%

175%

PUBLIC CREDIT AND PRIVATE DOMESTIC CREDIT AS % OF GDP

Deleveraging Countries

Low Risk Countries

High Risk Countries

-50% 0% 50% 100% 150% 200% 250%

BoliviaHungary

IndiaIsrael

KazakhstanNigeria

PhilippinesBelarus

ChileColombia

Czech Rep.Ecuador

EgyptIndonesia

KoreaMalaysia

MexicoPeru

PolandSouth Africa

TaiwanBrazilChina

CroatiaHong Kong

RussiaSingapore

ThailandTurkey

Ukraine

PUBLIC CREDIT AND PRIVATE DOMESTIC CREDIT AS % OF GDP, BY COUNTRY

2014 Change Since 2009

33 33

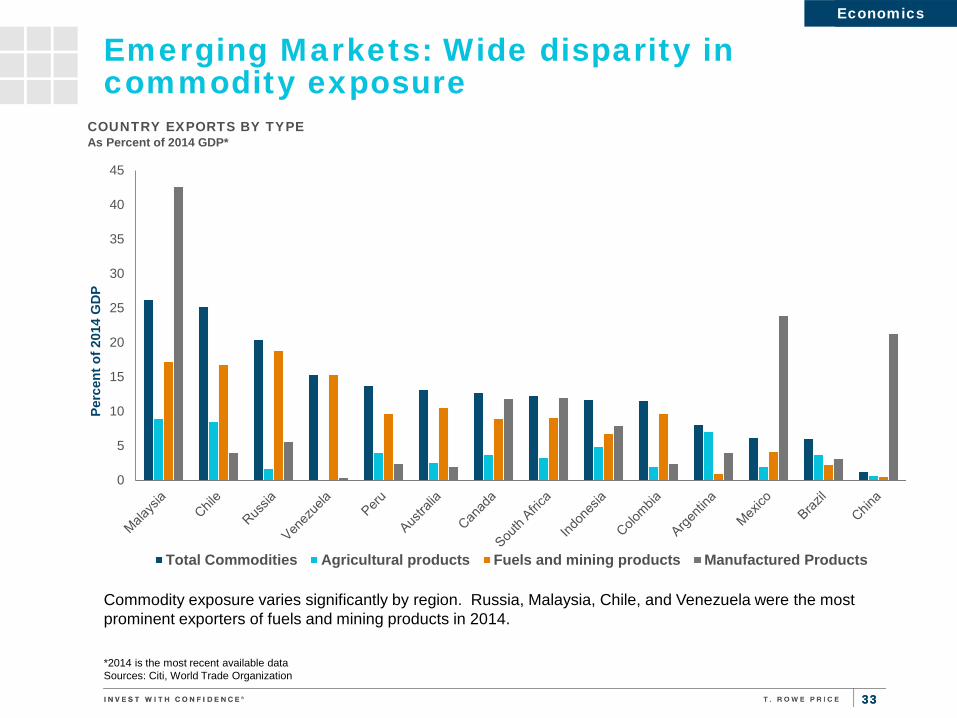

Emerging Markets: Wide disparity in commodity exposure

Economics Economics

*2014 is the most recent available data Sources: Citi, World Trade Organization

0

5

10

15

20

25

30

35

40

45

Perc

ent o

f 201

4 G

DP

COUNTRY EXPORTS BY TYPE As Percent of 2014 GDP*

Total Commodities Agricultural products Fuels and mining products Manufactured Products

Commodity exposure varies significantly by region. Russia, Malaysia, Chile, and Venezuela were the most prominent exporters of fuels and mining products in 2014.

34 34

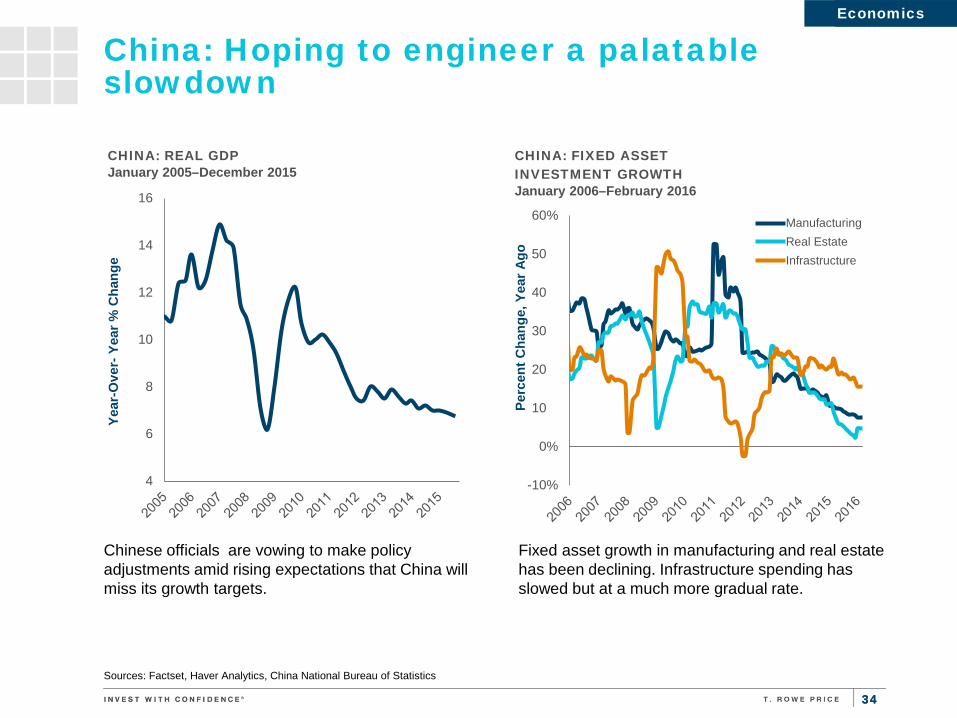

China: Hoping to engineer a palatable slowdown

Sources: Factset, Haver Analytics, China National Bureau of Statistics

Chinese officials are vowing to make policy adjustments amid rising expectations that China will miss its growth targets.

Economics Economics

4

6

8

10

12

14

16

Year

-Ove

r- Y

ear %

Cha

nge

CHINA: REAL GDP January 2005–December 2015

-10%

0%

10%

20%

30%

40%

50%

60%

Perc

ent C

hang

e, Y

ear A

go

CHINA: FIXED ASSET INVESTMENT GROWTH January 2006–February 2016

ManufacturingReal EstateInfrastructure

Fixed asset growth in manufacturing and real estate has been declining. Infrastructure spending has slowed but at a much more gradual rate.

35 35

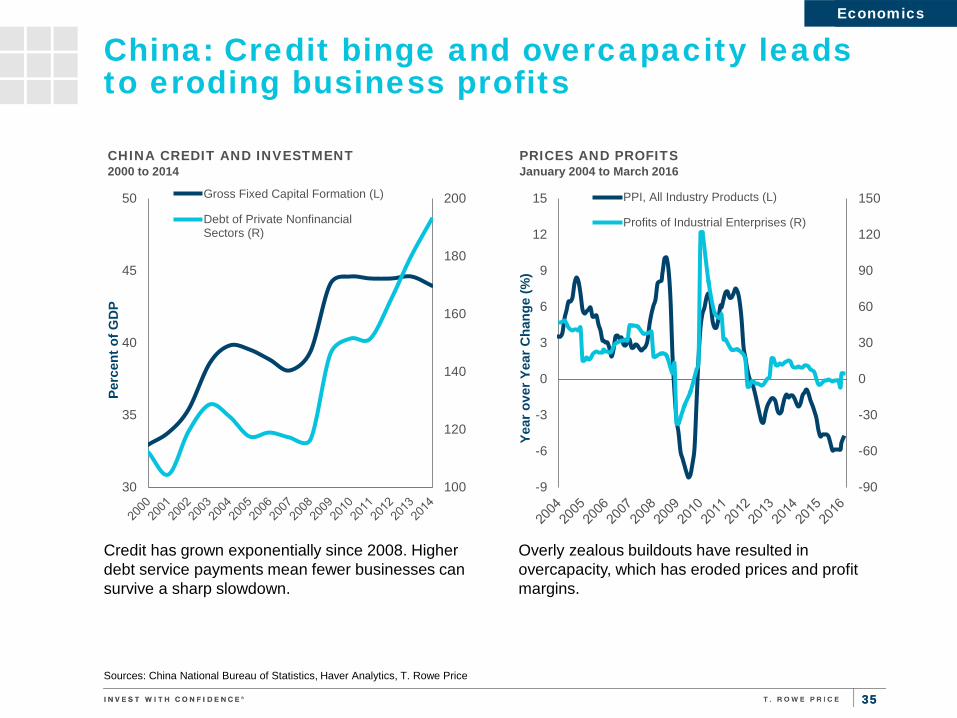

China: Credit binge and overcapacity leads to eroding business profits

Credit has grown exponentially since 2008. Higher debt service payments mean fewer businesses can survive a sharp slowdown.

Economics Economics

Overly zealous buildouts have resulted in overcapacity, which has eroded prices and profit margins.

100

120

140

160

180

200

30

35

40

45

50

Perc

ent o

f GD

P

CHINA CREDIT AND INVESTMENT 2000 to 2014

Gross Fixed Capital Formation (L)

Debt of Private NonfinancialSectors (R)

Sources: China National Bureau of Statistics, Haver Analytics, T. Rowe Price

-90

-60

-30

0

30

60

90

120

150

-9

-6

-3

0

3

6

9

12

15

Year

ove

r Yea

r Cha

nge

(%)

PRICES AND PROFITS January 2004 to March 2016

PPI, All Industry Products (L)

Profits of Industrial Enterprises (R)

36 36

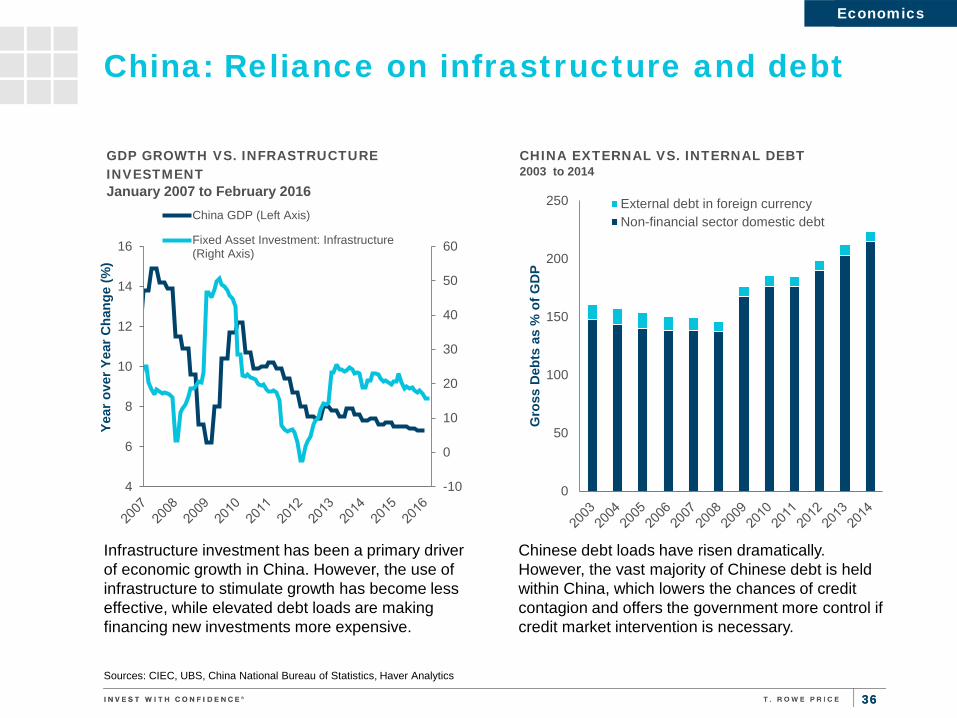

China: Reliance on infrastructure and debt

Sources: CIEC, UBS, China National Bureau of Statistics, Haver Analytics

Infrastructure investment has been a primary driver of economic growth in China. However, the use of infrastructure to stimulate growth has become less effective, while elevated debt loads are making financing new investments more expensive.

Economics Economics

Chinese debt loads have risen dramatically. However, the vast majority of Chinese debt is held within China, which lowers the chances of credit contagion and offers the government more control if credit market intervention is necessary.

0

50

100

150

200

250

Gro

ss D

ebts

as

% o

f GD

P

CHINA EXTERNAL VS. INTERNAL DEBT 2003 to 2014

External debt in foreign currencyNon-financial sector domestic debt

-10

0

10

20

30

40

50

60

4

6

8

10

12

14

16

Year

ove

r Yea

r Cha

nge

(%)

GDP GROWTH VS. INFRASTRUCTURE INVESTMENT January 2007 to February 2016

China GDP (Left Axis)

Fixed Asset Investment: Infrastructure(Right Axis)

37 37

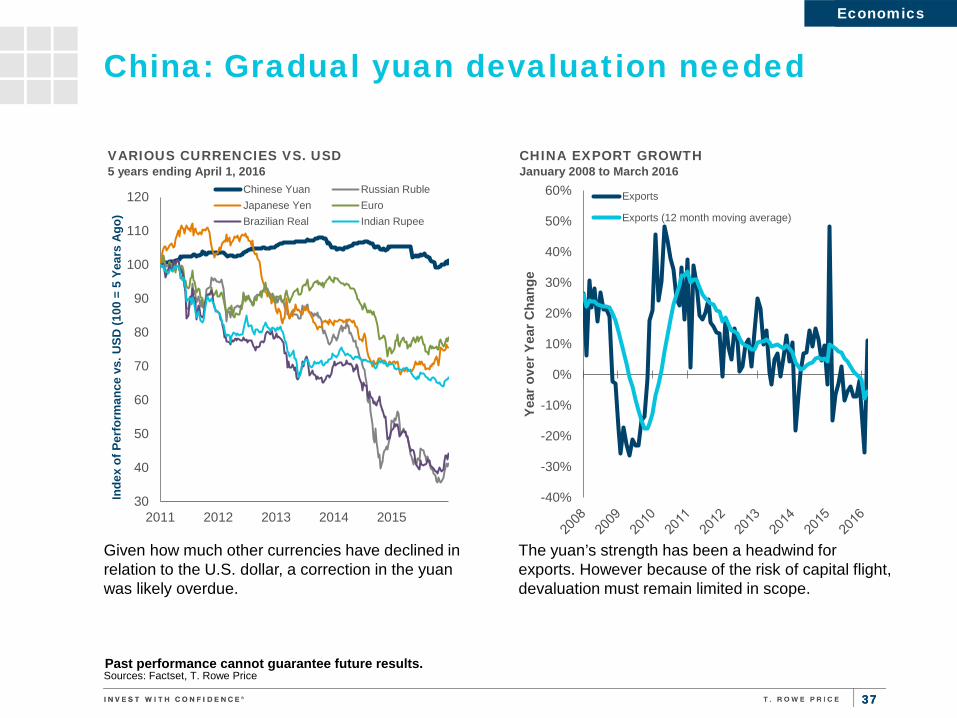

China: Gradual yuan devaluation needed

Given how much other currencies have declined in relation to the U.S. dollar, a correction in the yuan was likely overdue.

Economics Economics

The yuan’s strength has been a headwind for exports. However because of the risk of capital flight, devaluation must remain limited in scope.

Sources: Factset, T. Rowe Price Past performance cannot guarantee future results.

30

40

50

60

70

80

90

100

110

120

2011 2012 2013 2014 2015

Inde

x of

Per

form

ance

vs.

USD

(100

= 5

Yea

rs A

go)

VARIOUS CURRENCIES VS. USD 5 years ending April 1, 2016

Chinese Yuan Russian RubleJapanese Yen EuroBrazilian Real Indian Rupee

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Year

ove

r Yea

r Cha

nge

CHINA EXPORT GROWTH January 2008 to March 2016

Exports

Exports (12 month moving average)

38 38

China: Capital outflow concerns

Initial moves to devalue the yuan/renminbi versus the dollar have caused significant capital outflow, as investors fear further devaluation. This has forced China to spend significant currency reserves stabilizing the currency, but more than $3 trillion in reserves remains.

Economics Economics

However, it is notable that capital flows into China have slowed significantly. This is a stark change in the environment in China, where significant capital inflows have been the norm for many years.

Sources: Haver Analytics, People’s Bank of China, State Administration of Foreign Exchange

-250

-200

-150

-100

-50

0

50

100

150

200

250

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Mill

ions

of U

.S. D

olla

rs

CHINA: FOREIGN CURRENCY RESERVES January 2000 to March 2016

Foreign Currency Reserves (L)Quarterly Change (R)

-1,000

-500

0

500

1,000

1,500

2,000

Mill

ions

of U

.S. D

olla

rs

CHINA: CAPITAL ACCOUNT January 2007 to December 2015

39 39

China: Shifting to a consumption economy?

China’s economy is transitioning toward domestic-led growth model reliant on service-oriented industries and away from an export-driven mode that emphasized external demand.

Economics Economics

Electricity consumption sheds further light on the nature of the shift. Household electricity use grew in 2015, while industry use fell by 5%.

Sources: Haver Analytics, China National Bureau of Statistics, T. Rowe Price

51.3%

30%

35%

40%

45%

50%

55%

Serv

ices

as

% o

f GD

P

CHINA: SERVICES SHARE OF THE ECONOMY 1992 to 4Q15

-5%

0%

5%

10%

15%

20%

25%

All Households IndustryYe

ar o

ver Y

ear C

hang

e (%

)

CHINA: ELECTRICITY CONSUMPTION 2011 2012 2013 2014 2015

40 40

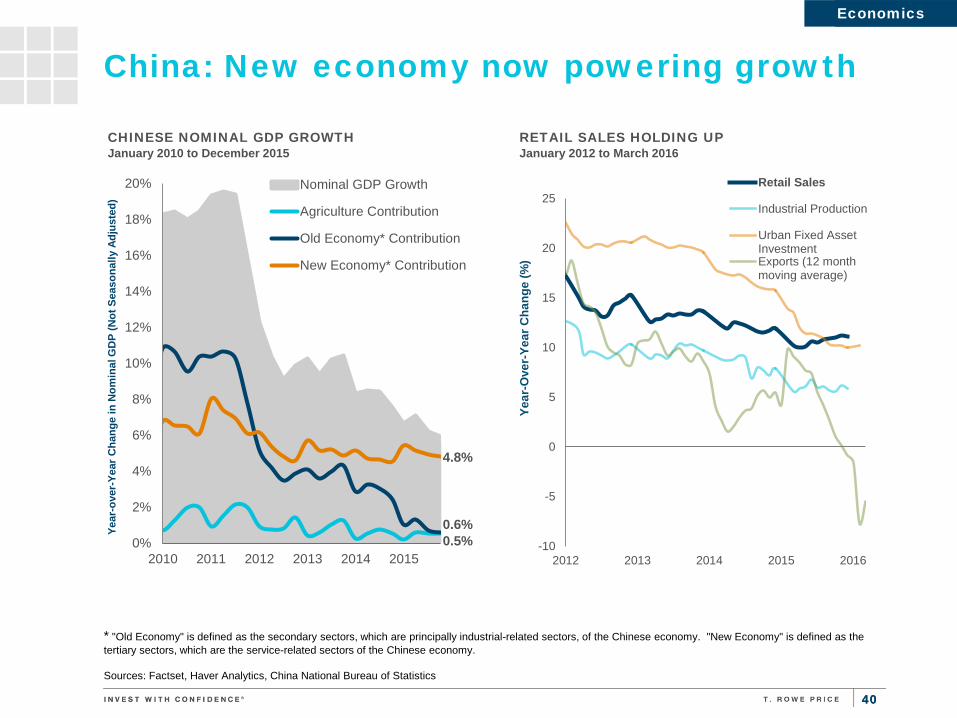

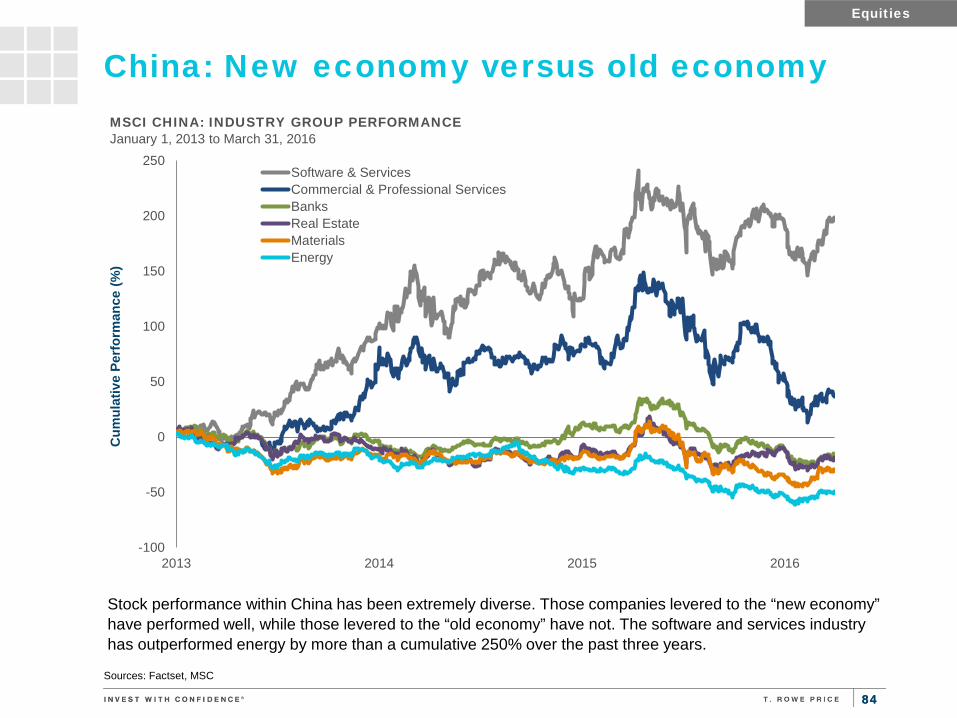

China: New economy now powering growth

* "Old Economy" is defined as the secondary sectors, which are principally industrial-related sectors, of the Chinese economy. "New Economy" is defined as the tertiary sectors, which are the service-related sectors of the Chinese economy. Sources: Factset, Haver Analytics, China National Bureau of Statistics

Economics Economics

-10

-5

0

5

10

15

20

25

2012 2013 2014 2015 2016

Year

-Ove

r-Ye

ar C

hang

e (%

)

RETAIL SALES HOLDING UP January 2012 to March 2016

Retail Sales

Industrial Production

Urban Fixed AssetInvestmentExports (12 monthmoving average)

0.5% 0.6%

4.8%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

2010 2011 2012 2013 2014 2015

Year

-ove

r-Ye

ar C

hang

e in

Nom

inal

GD

P (N

ot S

easo

nally

Adj

uste

d)

CHINESE NOMINAL GDP GROWTH January 2010 to December 2015

Nominal GDP Growth

Agriculture Contribution

Old Economy* Contribution

New Economy* Contribution

41 41

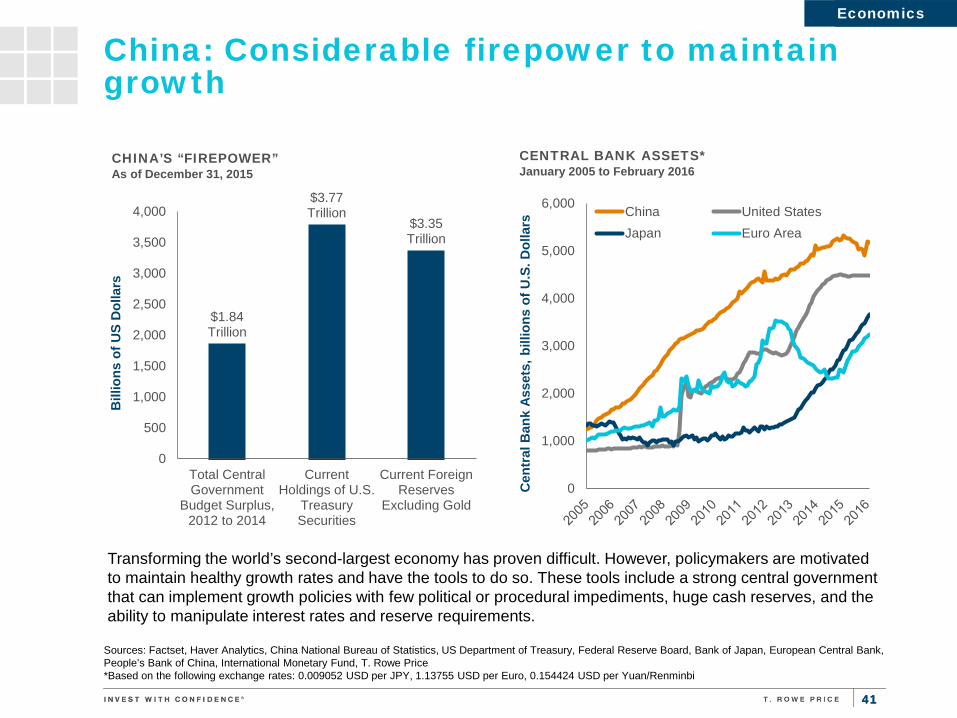

China: Considerable firepower to maintain growth

Economics Economics

Sources: Factset, Haver Analytics, China National Bureau of Statistics, US Department of Treasury, Federal Reserve Board, Bank of Japan, European Central Bank, People’s Bank of China, International Monetary Fund, T. Rowe Price *Based on the following exchange rates: 0.009052 USD per JPY, 1.13755 USD per Euro, 0.154424 USD per Yuan/Renminbi

Transforming the world’s second-largest economy has proven difficult. However, policymakers are motivated to maintain healthy growth rates and have the tools to do so. These tools include a strong central government that can implement growth policies with few political or procedural impediments, huge cash reserves, and the ability to manipulate interest rates and reserve requirements.

$1.84 Trillion

$3.77 Trillion

$3.35 Trillion

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Total CentralGovernment

Budget Surplus,2012 to 2014

CurrentHoldings of U.S.

TreasurySecurities

Current ForeignReserves

Excluding Gold

Bill

ions

of U

S D

olla

rs

CHINA’S “FIREPOWER” As of December 31, 2015

0

1,000

2,000

3,000

4,000

5,000

6,000

Cen

tral

Ban

k As

sets

, bill

ions

of U

.S. D

olla

rs

CENTRAL BANK ASSETS* January 2005 to February 2016

China United StatesJapan Euro Area

42 42

China: Chinese demand has peaked and is dragging commodity prices lower

Global commodity prices have fallen as a result of a decline in Chinese demand. We have seen a clear correlation between Chinese industrial production and global prices of industrial metals.

Economics Economics

Over-investment leads to over-capacity. In South Korea, investment as a percentage of GDP peaked at 42%. In China, this ratio is currently at 46%--a level that appears unsustainable.

Sources: Factset, Haver Analytics, China National Bureau of Statistics, Bank of Korea, T. Rowe Price

20%

25%

30%

35%

40%

45%

50%

Gro

ss F

ixed

Cap

ital I

nves

tmen

t as

Perc

ent o

f GD

P

INVESTMENT AS PERCENT OF GDP 1970 to 2015

Korea China

250

300

350

400

450

500

5%

7%

9%

11%

13%

15%

17%

2011 2012 2013 2014 2015 2016

Inde

x Le

vel

Year

ove

r Yea

r Cha

nge

(%)

CHINA INDUSTRIAL PRODUCTION VS INDUSTRIAL METALS PRICES January 2011 to March 2016

China - Industrial Production (Left)S&P GSCI Industrial Metals Index Price (Right)

43 43

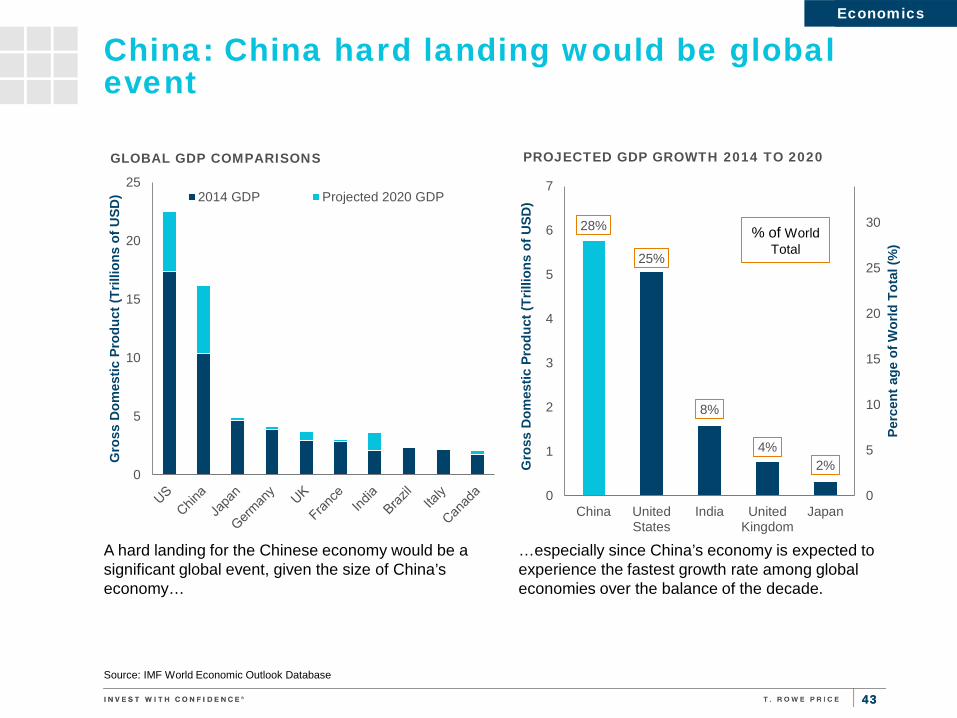

China: China hard landing would be global event

Source: IMF World Economic Outlook Database

A hard landing for the Chinese economy would be a significant global event, given the size of China’s economy…

Economics Economics

…especially since China’s economy is expected to experience the fastest growth rate among global economies over the balance of the decade.

28%

25%

8%

4% 2%

0

5

10

15

20

25

30

0

1

2

3

4

5

6

7

China UnitedStates

India UnitedKingdom

Japan

Perc

ent a

ge o

f Wor

ld T

otal

(%)

Gro

ss D

omes

tic P

rodu

ct (T

rillio

ns o

f USD

)

PROJECTED GDP GROWTH 2014 TO 2020

% of World Total

0

5

10

15

20

25

Gro

ss D

omes

tic P

rodu

ct (T

rillio

ns o

f USD

)

GLOBAL GDP COMPARISONS

2014 GDP Projected 2020 GDP

44 44

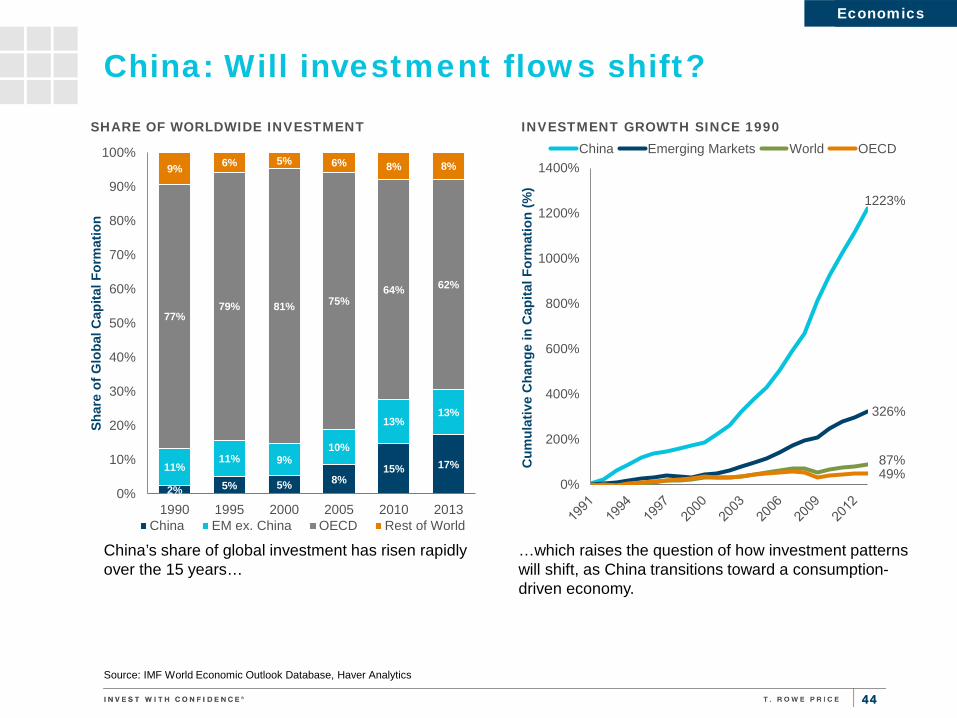

China: Will investment flows shift?

Source: IMF World Economic Outlook Database, Haver Analytics

China’s share of global investment has risen rapidly over the 15 years…

Economics Economics

…which raises the question of how investment patterns will shift, as China transitions toward a consumption-driven economy.

2% 5% 5% 8% 15% 17% 11%

11% 9% 10%

13% 13%

77% 79% 81% 75%

64% 62%

9% 6% 5% 6% 8% 8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1990 1995 2000 2005 2010 2013

Shar

e of

Glo

bal C

apita

l For

mat

ion

SHARE OF WORLDWIDE INVESTMENT

China EM ex. China OECD Rest of World

1223%

326%

87% 49%

0%

200%

400%

600%

800%

1000%

1200%

1400%

Cum

ulat

ive

Cha

nge

in C

apita

l For

mat

ion

(%)

INVESTMENT GROWTH SINCE 1990 China Emerging Markets World OECD

45 45

Global economy: Country comparison As of March 31, 2016

1 As of 6 April 2016 per The Economist 2 As of 14 October 2015 release of IMF World Economic Outlook via Factset 3 As of 6 April 2016 per the CIA World Factbook (2015 est.) Sources: IMF, The Economist, CIA World Factbook, World Bank

Developed Markets Emerging Markets

United States Europe

United Kingdom Japan Australia Canada Brazil Russia India China Mexico

Inflation Rate (CPI)1 1.0% -0.1% 0.3% 0.3% 1.7% 1.4% 10.4% 7.3% 5.2% 2.3% 2.9%

Savings Rate (as a % of GDP)2 17.7% 23.0% 13.4% 24.3% 22.3% 20.8% 12.9% 23.5% 29.% 45.9% 20.5%

Investment Rate (as a % of GDP)2 20.6% 19.3% 17.7% 21.3% 26.4% 22.7% 16.7% 18.1% 30.6% 43.1% 22.5%

Current Account Balance (as a % of 2015 GDP)1 -2.6% 2.8% -4.2% 3.5% -4.0% -2.9% -2.4% 3.9% -1.1% 3.0% -2.7%

Budget Balance (as a % of 2015 GDP)1 -2.5% -1.9% -3.6% -6.2% -2.0% -1.4% -5.4% -2.2% -3.7% -3.0% -3.0%

Gov’t Debt to GDP2 80.7% 69.7% 79.5% 128.1% 18.3% 38.% 42.1% 13.5%3 51.7%3 16.7%3 52.1%

Short-term Rates1 0.63% -0.25% 0.57% 0.00% 2.34% 0.86% 14.11% 12.16% 6.76% 2.85% 4.07%

2014 Real GDP Growth2 2.5% 1.89% 2.20% 0.60% 2.37% 1.2% -3.80% -3.70% 7.30% 6.90% 2.50%

Projected 2015 Real GDP Growth4 2.60% 1.95% 2.20% 1.00% 2.85% 1.70% -3.50% -1.00% 7.50% 6.90% 2.60%

Economics Economics

46 46

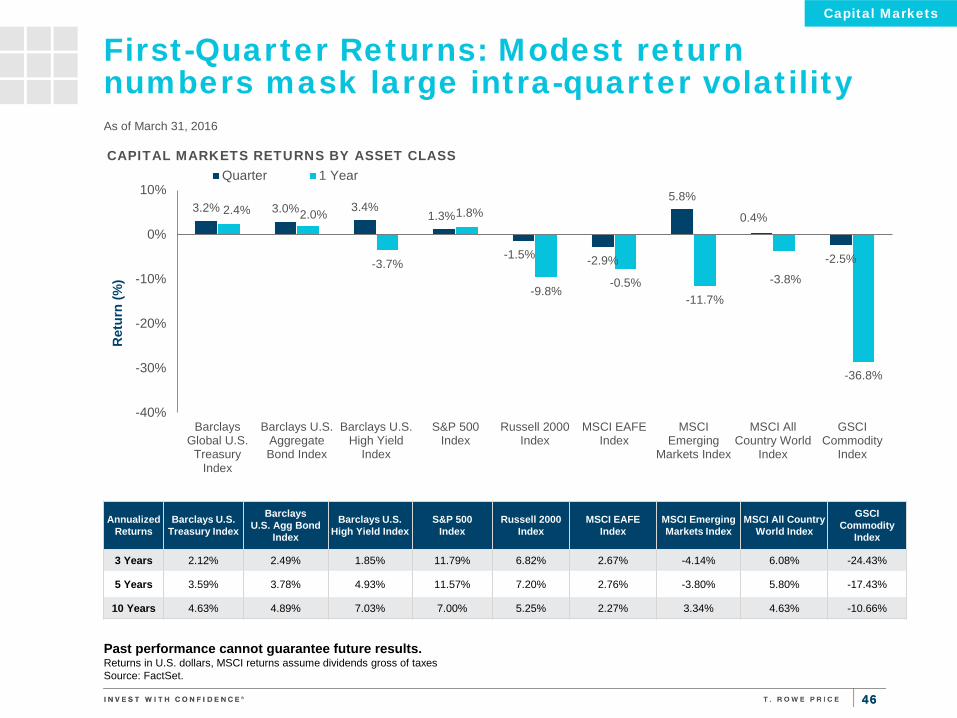

First-Quarter Returns: Modest return numbers mask large intra-quarter volatility As of March 31, 2016

Annualized Returns

Barclays U.S. Treasury Index

Barclays U.S. Agg Bond

Index

Barclays U.S. High Yield Index

S&P 500 Index

Russell 2000 Index

MSCI EAFE Index

MSCI Emerging Markets Index

MSCI All Country World Index

GSCI Commodity

Index

3 Years 2.12% 2.49% 1.85% 11.79% 6.82% 2.67% -4.14% 6.08% -24.43%

5 Years 3.59% 3.78% 4.93% 11.57% 7.20% 2.76% -3.80% 5.80% -17.43%

10 Years 4.63% 4.89% 7.03% 7.00% 5.25% 2.27% 3.34% 4.63% -10.66%

Capital Markets

Past performance cannot guarantee future results. Returns in U.S. dollars, MSCI returns assume dividends gross of taxes Source: FactSet.

3.2% 3.0% 3.4% 1.3%

-1.5% -2.9%

5.8%

0.4%

-2.5%

2.4% 2.0%

-3.7%

1.8%

-9.8% -0.5%

-11.7%

-3.8%

-36.8%

-40%

-30%

-20%

-10%

0%

10%

BarclaysGlobal U.S.

TreasuryIndex

Barclays U.S.AggregateBond Index

Barclays U.S.High Yield

Index

S&P 500Index

Russell 2000Index

MSCI EAFEIndex

MSCIEmerging

Markets Index

MSCI AllCountry World

Index

GSCICommodity

Index

Ret

urn

(%)

CAPITAL MARKETS RETURNS BY ASSET CLASS Quarter 1 Year

47 47

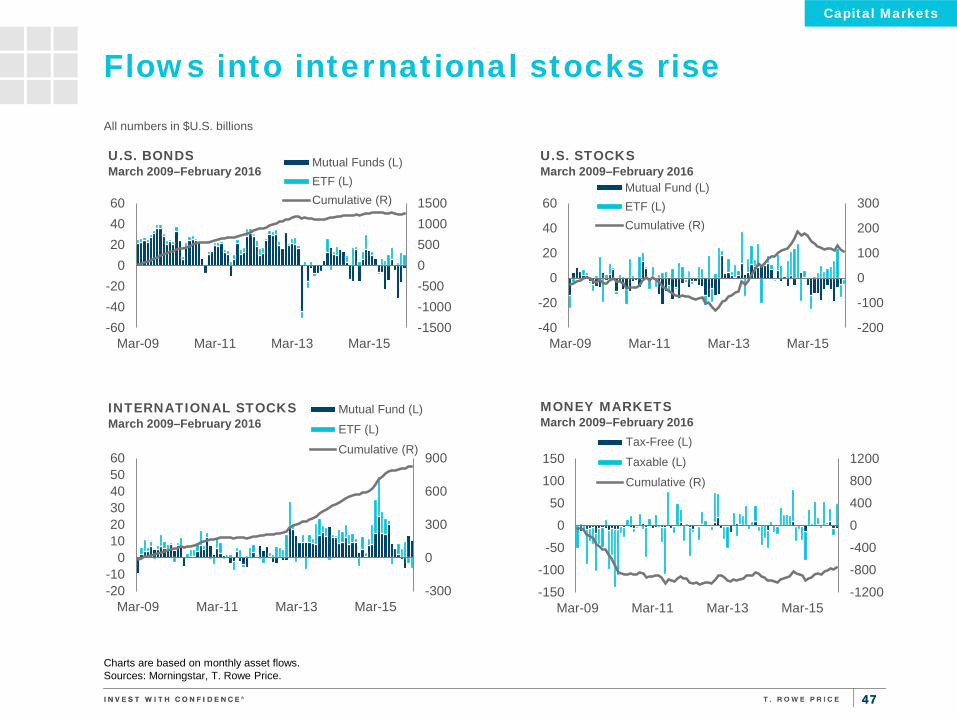

Flows into international stocks rise

-200

-100

0

100

200

300

-40

-20

0

20

40

60

Mar-09 Mar-11 Mar-13 Mar-15

U.S. STOCKS March 2009–February 2016

Mutual Fund (L)ETF (L)Cumulative (R)

All numbers in $U.S. billions

Charts are based on monthly asset flows. Sources: Morningstar, T. Rowe Price.

-1200

-800

-400

0

400

800

1200

-150

-100

-50

0

50

100

150

Mar-09 Mar-11 Mar-13 Mar-15

MONEY MARKETS March 2009–February 2016

Tax-Free (L)

Taxable (L)

Cumulative (R)

-1500-1000-500050010001500

-60-40-20

0204060

Mar-09 Mar-11 Mar-13 Mar-15

U.S. BONDS March 2009–February 2016

Mutual Funds (L)ETF (L)Cumulative (R)

-300

0

300

600

900

-20-10

0102030405060

Mar-09 Mar-11 Mar-13 Mar-15

INTERNATIONAL STOCKS March 2009–February 2016

Mutual Fund (L)

ETF (L)

Cumulative (R)

Capital Markets

48 48

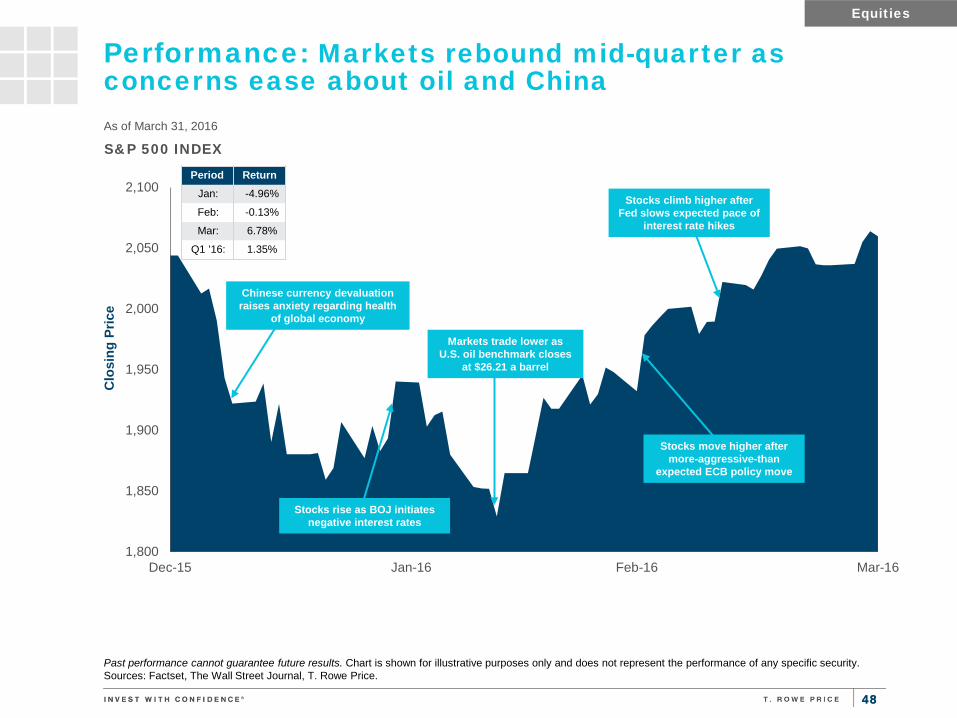

Performance: Markets rebound mid-quarter as concerns ease about oil and China As of March 31, 2016

Past performance cannot guarantee future results. Chart is shown for illustrative purposes only and does not represent the performance of any specific security. Sources: Factset, The Wall Street Journal, T. Rowe Price.

1,800

1,850

1,900

1,950

2,000

2,050

2,100

Dec-15 Jan-16 Feb-16 Mar-16

Clo

sing

Pric

e

S&P 500 INDEX

Stocks climb higher after Fed slows expected pace of

interest rate hikes

Period Return Jan: -4.96%

Feb: -0.13%

Mar: 6.78%

Q1 ’16: 1.35%

Markets trade lower as U.S. oil benchmark closes

at $26.21 a barrel

Chinese currency devaluation raises anxiety regarding health

of global economy

Equities

Stocks rise as BOJ initiates negative interest rates

Stocks move higher after more-aggressive-than

expected ECB policy move

49 49

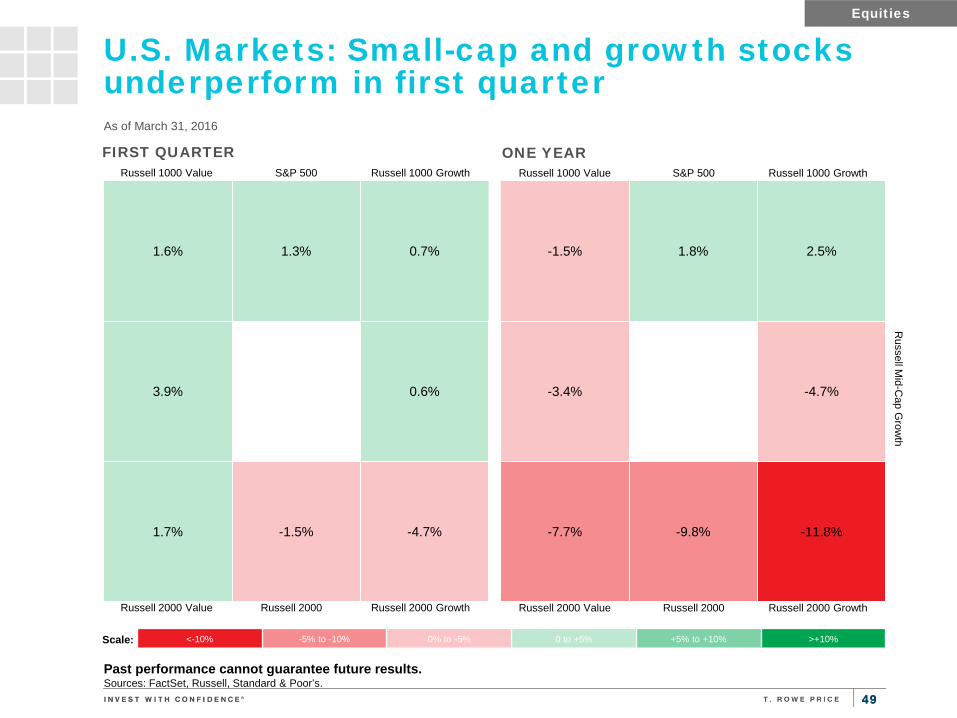

U.S. Markets: Small-cap and growth stocks underperform in first quarter

1.6% 1.3% 0.7%

-1.5% 1.8% 2.5%

3.9%

0.6% -3.4%

-4.7%

1.7% -1.5% -4.7% -7.7% -9.8% -11.8%

As of March 31, 2016

FIRST QUARTER ONE YEAR Russell 1000 Value S&P 500 Russell 1000 Growth Russell 1000 Value S&P 500 Russell 1000 Growth

Russell M

id-Cap G

rowth

Russell 2000 Value Russell 2000 Russell 2000 Growth Russell 2000 Value Russell 2000 Russell 2000 Growth

Equities

<-10% -5% to -10% 0% to -5% 0 to +5% +5% to +10% >+10% Scale:

Past performance cannot guarantee future results. Sources: FactSet, Russell, Standard & Poor’s.

50 50

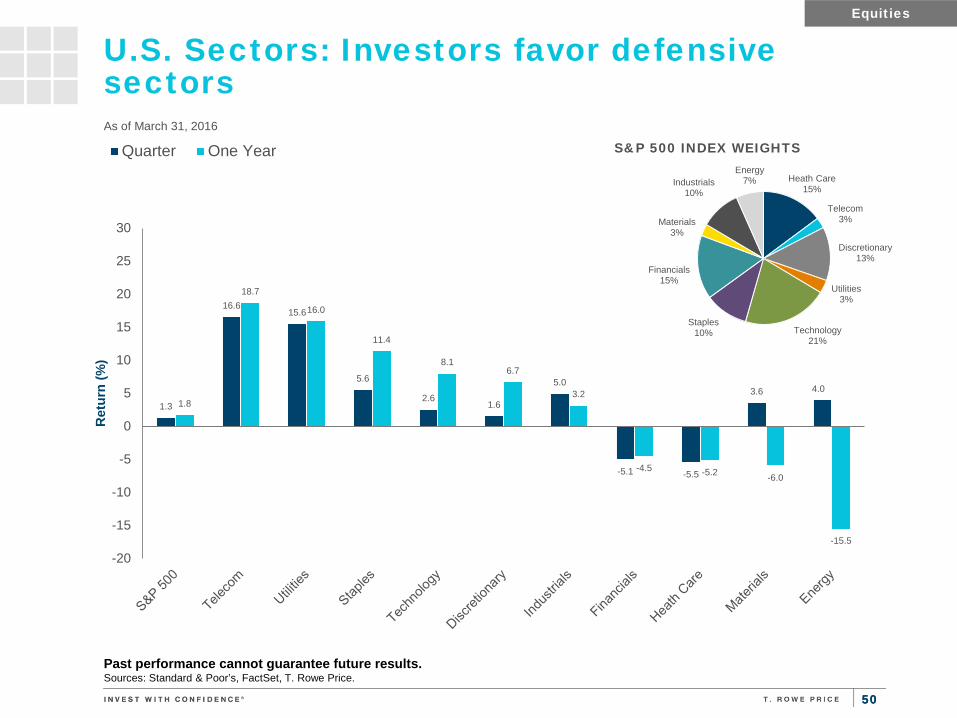

U.S. Sectors: Investors favor defensive sectors As of March 31, 2016

Equities

1.3

16.6 15.6

5.6

2.6 1.6

5.0

-5.1 -5.5

3.6 4.0 1.8

18.7

16.0

11.4

8.1 6.7

3.2

-4.5 -5.2 -6.0

-15.5

-20

-15

-10

-5

0

5

10

15

20

25

30

Ret

urn

(%)

Quarter One YearHeath Care

15%

Telecom 3%

Discretionary 13%

Utilities 3%

Technology 21%

Staples 10%

Financials 15%

Materials 3%

Industrials 10%

Energy 7%

S&P 500 INDEX WEIGHTS

Past performance cannot guarantee future results. Sources: Standard & Poor’s, FactSet, T. Rowe Price.

51 51

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

S&P

500

Div

. Yie

ld M

inus

Ten

Yea

r Tre

asur

y Yi

eld

S&P 500 DIVIDEND YIELD VS. 10 YEAR TREASURY YIELD January 1997–March 2016

10

12

14

16

18

20

22

24

26

28

Pric

e-Ea

rnin

gs M

ultip

le

S&P 500 PRICE TO 12 MONTHS FORWARD EARNINGS January 1997–March 2016

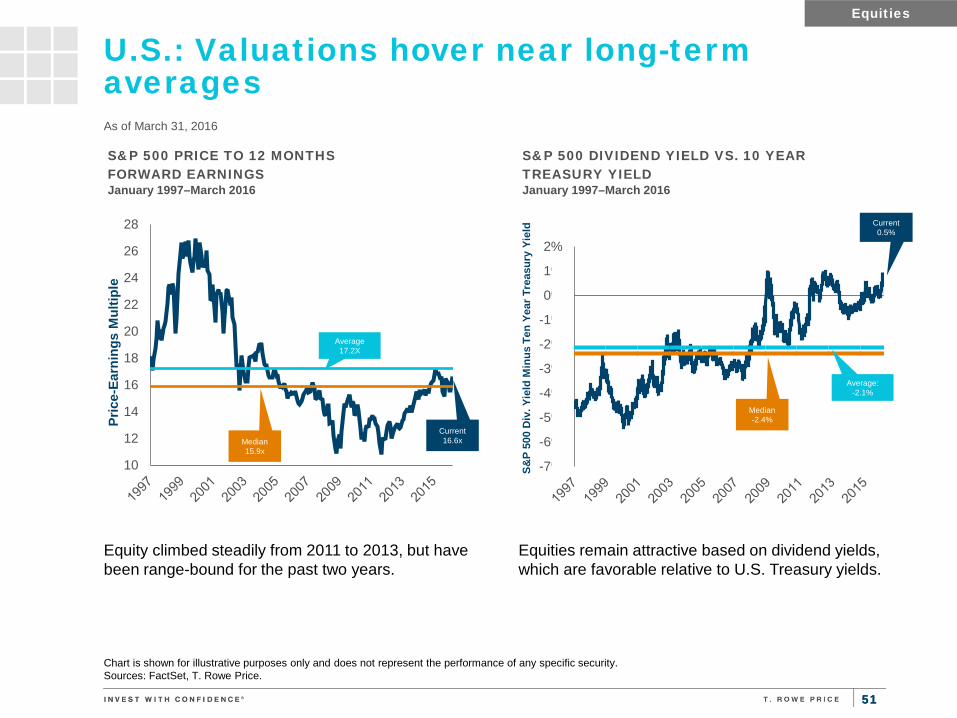

U.S.: Valuations hover near long-term averages As of March 31, 2016

Chart is shown for illustrative purposes only and does not represent the performance of any specific security. Sources: FactSet, T. Rowe Price.

Equities remain attractive based on dividend yields, which are favorable relative to U.S. Treasury yields.

Equity climbed steadily from 2011 to 2013, but have been range-bound for the past two years.

Current 16.6x

Average 17.2X

Average: -2.1%

Current 0.5%

Equities

Median 15.9x

Median -2.4%

52 52

U.S.: Valuations favor growth stocks across market capitalizations

Sources: FactSet, T. Rowe Price.

P/E Ratios (1 Year Forward) by Russell Style Indices

Current (3/31/16) Average High Low

Current Valuation to 20 Year Average

Russell 1000 Value 15.21 14.28 19.90 9.67 6%

Russell 1000 Growth 18.25 21.12 54.50 11.09 -14%

Russell Mid Cap Value 16.28 14.55 17.84 9.24 12%

Russell Mid Cap Growth 19.26 22.10 61.60 10.34 -13%

Russell 2000 Value 15.99 14.69 20.40 10.36 9%

Russell 200 Growth 19.09 21.62 50.80 12.14 -12%

Past 20 Years

Equities

5

10

15

20

25

30

Russell 1000Value

Russell 1000Growth

Russell Mid CapValue

Russell Mid CapGrowth

Russell 2000Value

Russell 2000Growth

Pric

e to

Ear

ning

s M

ultip

le

FORWARD P/E RATIOS March 1996–March 2016

53 53

0.0

0.5

1.0

1.5

2.0

Energy Materials ConsumerDiscretionary

Industrials InformationTechnology

Financials ConsumerStaples

Health Care Telecom. UtilitiesPric

e to

Ear

ning

s M

ultip

le R

elat

ive

to S

&P

500

RELATIVE FORWARD P/E RATIOS March 1996–March 2016

U.S.: Defensive sectors are commanding a premium, energy distorted by impaired earnings

Sources: FactSet, T. Rowe Price.

Past 20 Years

Equities

P/E Ratios (1 Year Forward) by Sector

Current (3/31/16)

Relative to S&P 500 Average High Low

Current Valuation to 20 Year Average

Energy 62.87 3.78 0.94 3.78 0.64 404%

Materials 17.16 1.03 0.98 1.72 0.43 105%

Consumer Discretionary 18.09 1.09 1.13 1.31 0.85 96%

Industrials 16.02 0.96 1.03 1.19 0.80 94%

Information Technology 16.33 0.98 1.27 2.10 0.95 77%

Financials 12.40 0.75 0.78 1.16 0.53 96%

Consumer Staples 20.98 1.26 1.17 1.46 0.74 108%

Health Care 14.90 0.90 1.09 1.47 0.75 83%

Telecom. 13.93 0.84 1.05 1.54 0.74 80%

Utilities 17.71 1.07 0.87 1.25 0.49 123%

54 54

-6

-4

-2

0

2

4

6

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Perc

ent (

%)

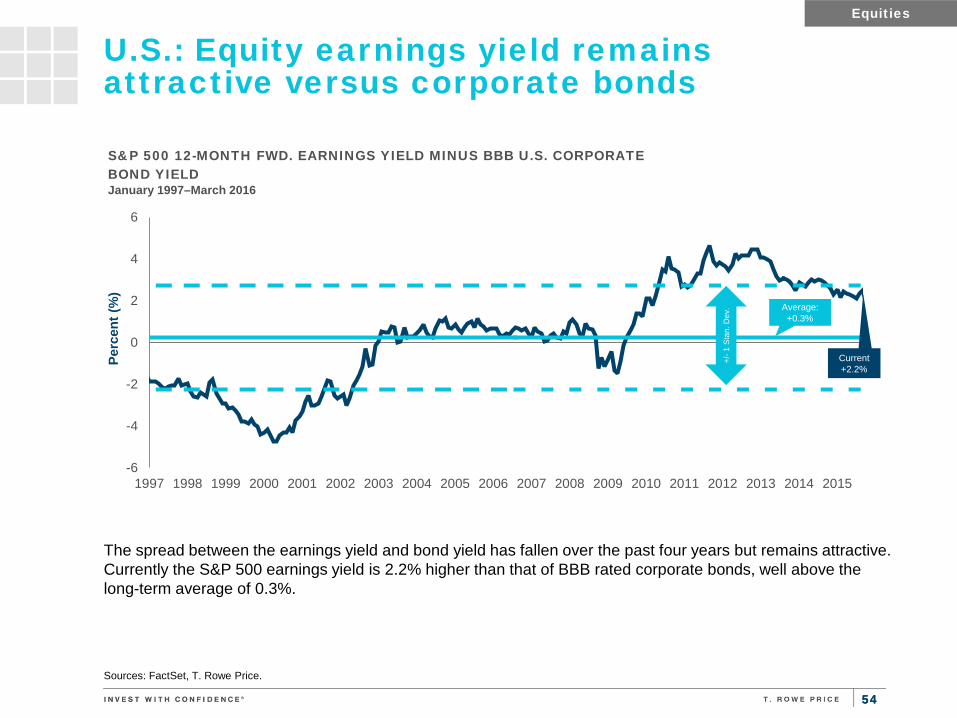

S&P 500 12-MONTH FWD. EARNINGS YIELD MINUS BBB U.S. CORPORATE BOND YIELD January 1997–March 2016

U.S.: Equity earnings yield remains attractive versus corporate bonds

Sources: FactSet, T. Rowe Price.

The spread between the earnings yield and bond yield has fallen over the past four years but remains attractive. Currently the S&P 500 earnings yield is 2.2% higher than that of BBB rated corporate bonds, well above the long-term average of 0.3%.

+/- 1

Sta

n. D

ev.

Equities

Current +2.2%

Average: +0.3%

55 55

0

10

20

30

40

50

60

70

Inde

x Le

vel

CBOE MARKET VOLATILITY INDEX January 1990– March 2016

VIX Average

U.S.: Volatility and correlations fall as macro concerns ease

1 Intra-stock correlations represent the average pair-wise correlation of returns over monthly rolling 90-day periods. Sources: FactSet, T. Rowe Price.

Equities

Volatility has fallen as concerns about China’s slowdown have eased and stock markets have recovered.

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

Cor

rela

tion

INTRA-STOCK CORRELATIONS1 IN THE S&P 500 INDEX December 1990–March 2016

90 Day Correlation Average

Current 14.0

Current 0.18

56 56

U.S.: Weaker energy prices continue to weigh on earnings

Equities

30

40

50

60

70

80

90

100

110

120

130

700

900

1,100

1,300

1,500

1,700

1,900

2,100

2,300

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Earn

ings

Per

Sha

re ($

)

Inde

x Le

vel

S&P 500 INDEX VS EARNINGS PER SHARE January 2000– March 2016

Price (L) Earnings Per Share (R)

Past performance cannot guarantee future results. Source: FactSet.

57 57

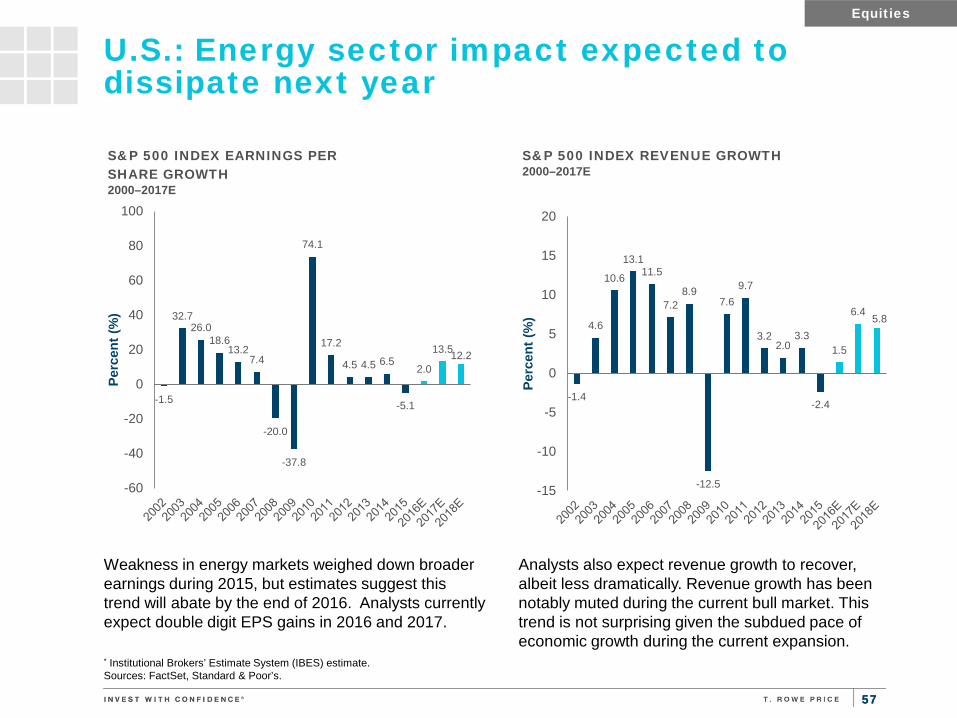

U.S.: Energy sector impact expected to dissipate next year

* Institutional Brokers’ Estimate System (IBES) estimate. Sources: FactSet, Standard & Poor’s.

Analysts also expect revenue growth to recover, albeit less dramatically. Revenue growth has been notably muted during the current bull market. This trend is not surprising given the subdued pace of economic growth during the current expansion.

Weakness in energy markets weighed down broader earnings during 2015, but estimates suggest this trend will abate by the end of 2016. Analysts currently expect double digit EPS gains in 2016 and 2017.

Equities

-1.5

32.7 26.0

18.6 13.2

7.4

-20.0

-37.8

74.1

17.2

4.5 4.5 6.5

-5.1

2.0

13.5 12.2

-60

-40

-20

0

20

40

60

80

100

Perc

ent (

%)

S&P 500 INDEX EARNINGS PER SHARE GROWTH 2000–2017E

-1.4

4.6

10.6

13.1 11.5

7.2 8.9

-12.5

7.6 9.7

3.2 2.0

3.3

-2.4

1.5

6.4 5.8

-15

-10

-5

0

5

10

15

20

Perc

ent (

%)

S&P 500 INDEX REVENUE GROWTH 2000–2017E

58 58

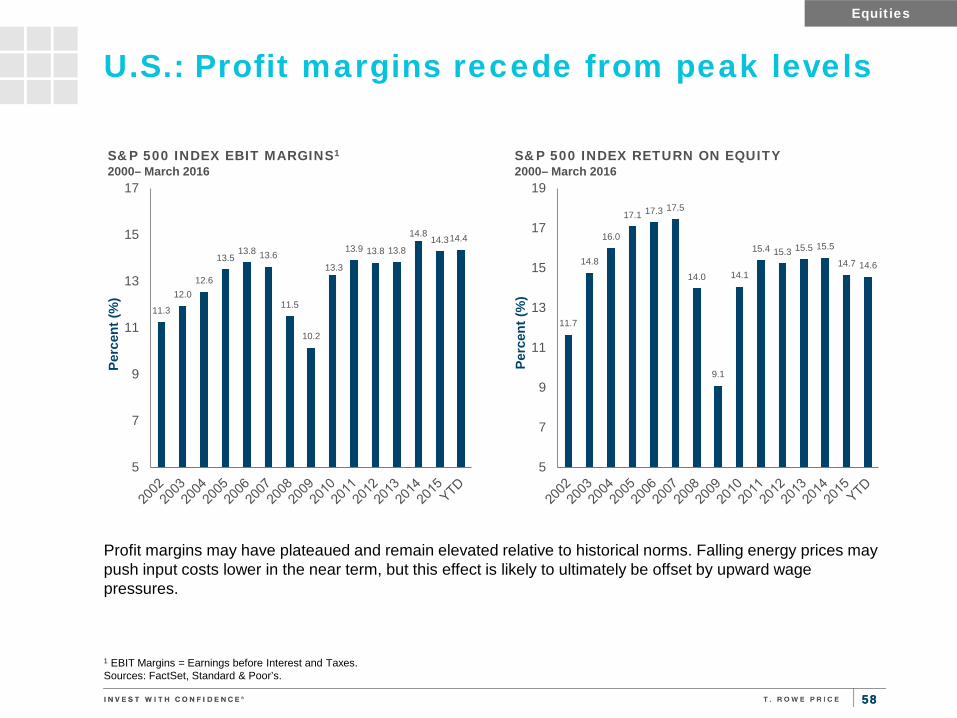

U.S.: Profit margins recede from peak levels

1 EBIT Margins = Earnings before Interest and Taxes. Sources: FactSet, Standard & Poor’s.

Profit margins may have plateaued and remain elevated relative to historical norms. Falling energy prices may push input costs lower in the near term, but this effect is likely to ultimately be offset by upward wage pressures.

Equities

11.3

12.0 12.6

13.5 13.8 13.6

11.5

10.2

13.3

13.9 13.8 13.8

14.8 14.3 14.4

5

7

9

11

13

15

17

Perc

ent (

%)

S&P 500 INDEX EBIT MARGINS1

2000– March 2016

11.7

14.8

16.0

17.1 17.3 17.5

14.0

9.1

14.1

15.4 15.3 15.5 15.5

14.7 14.6

5

7

9

11

13

15

17

19

Perc

ent (

%)

S&P 500 INDEX RETURN ON EQUITY

2000– March 2016

59 59

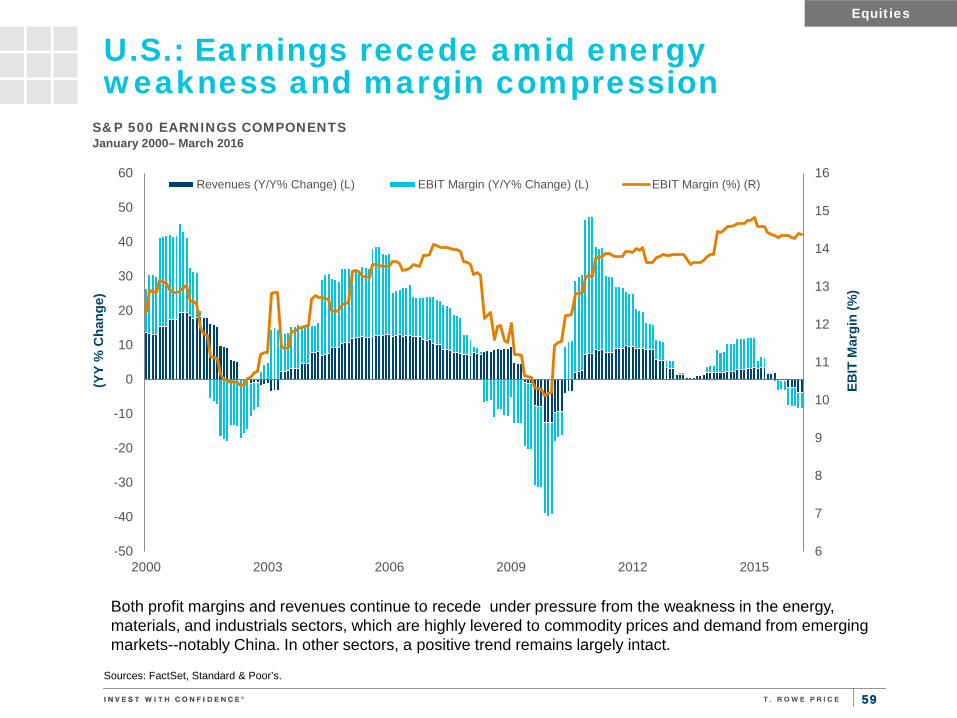

U.S.: Earnings recede amid energy weakness and margin compression

Sources: FactSet, Standard & Poor’s.

Equities

6

7

8

9

10

11

12

13

14

15

16

-50

-40

-30

-20

-10

0

10

20

30

40

50

60

2000 2003 2006 2009 2012 2015

EBIT

Mar

gin

(%)

(YY

% C

hang

e)

S&P 500 EARNINGS COMPONENTS January 2000– March 2016

Revenues (Y/Y% Change) (L) EBIT Margin (Y/Y% Change) (L) EBIT Margin (%) (R)

Both profit margins and revenues continue to recede under pressure from the weakness in the energy, materials, and industrials sectors, which are highly levered to commodity prices and demand from emerging markets--notably China. In other sectors, a positive trend remains largely intact.

60 60

U.S.: Fourth-quarter 2015 earnings and revenues As reported through April 8, 2016

This report is based on trailing 12 month non-GAAP earnings per share and revenues. Sources: FactSet, Standard & Poor’s.

Earnings Growth (YoY) Earnings Surprise

Name YoY Growth Reported (%)

# Pos Growth

# Neg Growth

Surprise (%)

% Pos Surprise

% Neg Surprise

S&P 500 -0.8 289 178 1.2 69.6 19.6 Consumer Discretionary 9.3 58 26 4.8 73.6 17.2 Consumer Staples 0.9 23 14 2.5 65.8 18.4 Energy -61.6 4 33 9.5 67.5 30.0 Financials 5.7 41 24 -0.5 64.0 25.6 Health Care 13.6 48 8 4.5 65.5 18.2 Industrials -4.1 35 27 2.9 72.3 18.5 Information Technology 6.3 42 23 5.5 83.8 7.4 Materials -8.0 14 13 13.8 66.7 18.5 Telecommunication Services 20.4 4 1 1.1 60.0 40.0 Utilities -11.6 20 9 -1.1 55.2 27.6

Revenue Growth (YoY) Revenue Surprise

Name YoY Growth Reported (%)

# Pos Growth

# Neg Growth

Surprise (%)

% Pos Surprise

% Neg Surprise

S&P 500 -2.8 262 238 -0.4 48.4 51.2 Consumer Discretionary 3.5 55 32 0.6 43.7 55.2 Consumer Staples 1.3 19 18 -1.1 42.1 55.3 Energy -35.0 0 37 0.6 61.2 38.8 Financials -0.7 56 34 0.4 44.0 56.0 Health Care 11.2 48 9 0.7 69.1 30.9 Industrials -3.0 26 39 -1.6 40.0 60.0 Information Technology 4.3 40 26 0.4 66.2 33.8 Materials -12.7 7 20 -1.6 25.9 74.1 Telecommunication Services 7.3 4 1 -0.4 40.0 60.0 Utilities -8.6 7 22 -14.3 10.7 89.3

Equities

61 61

Sources: Standard & Poor’s, Factset

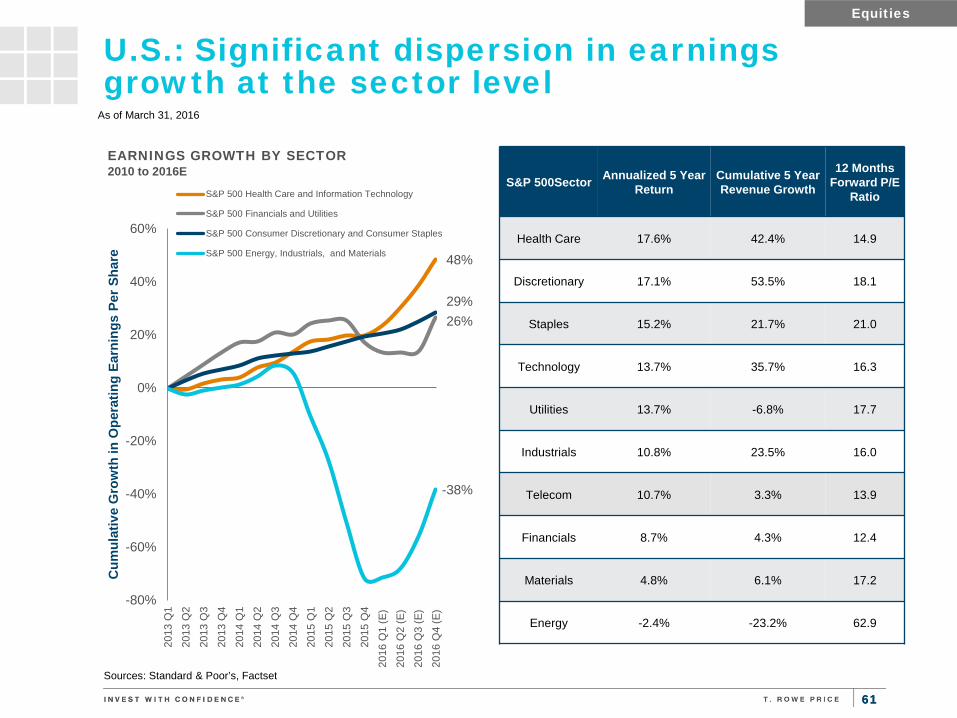

U.S.: Significant dispersion in earnings growth at the sector level

Equities

As of March 31, 2016

48%

26% 29%

-38%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

(E)

2016

Q2

(E)

2016

Q3

(E)

2016

Q4

(E)

Cum

ulat

ive

Gro

wth

in O

pera

ting

Earn

ings

Per

Sha

re

EARNINGS GROWTH BY SECTOR 2010 to 2016E

S&P 500 Health Care and Information Technology

S&P 500 Financials and Utilities

S&P 500 Consumer Discretionary and Consumer Staples

S&P 500 Energy, Industrials, and Materials

S&P 500Sector Annualized 5 Year Return

Cumulative 5 Year Revenue Growth

12 Months Forward P/E

Ratio

Health Care 17.6% 42.4% 14.9

Discretionary 17.1% 53.5% 18.1

Staples 15.2% 21.7% 21.0

Technology 13.7% 35.7% 16.3

Utilities 13.7% -6.8% 17.7

Industrials 10.8% 23.5% 16.0

Telecom 10.7% 3.3% 13.9

Financials 8.7% 4.3% 12.4

Materials 4.8% 6.1% 17.2

Energy -2.4% -23.2% 62.9

62 62

U.S.: Small-cap relative valuations are close to long-term median

Source: The Leuthold Group, LLC.

50%

60%

70%

80%

90%

100%

110%

120%

130%

1983 1987 1991 1995 1999 2003 2007 2011 2015

SMALL-CAP TO LARGE-CAP HISTORICAL P/E RATIO Based on Normalized Earnings, January 1983–March 2016

Small-cap valuations relative to those of large-cap stocks have declined since 2013 and are now just below their long-term median. Currently the P/E ratio of small-caps relative to large-caps is 102%, compared with a long-term median of 103%.

Median: 103%

Equities

Current 102%

63 63

U.S.: Growth vs value disparity has been narrowing

Source: Factset, Russell.

The spread between value and growth reverted significantly towards value during the quarter, as many of the best performers of 2015 (which were concentrated in growth sectors) retrenched.

Equities

Growth Outperforming

Value Outperforming

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

RUSSELL 1000 GROWTH VS. VALUE Rolling 3 year Return Difference

Growth Outperforming

Value Outperforming

-120%

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

RUSSELL 2000 GROWTH VS. VALUE Rolling 3 Year Return Difference

As of March 31, 2016

Past performance cannot guarantee future results.

64 64

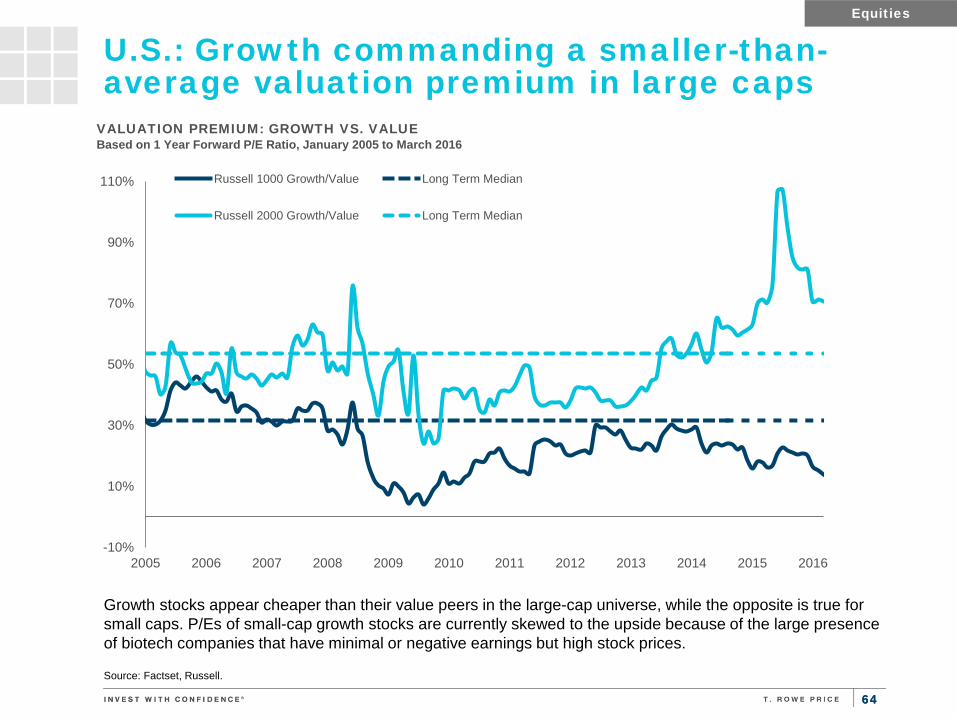

U.S.: Growth commanding a smaller-than-average valuation premium in large caps

Source: Factset, Russell.

Growth stocks appear cheaper than their value peers in the large-cap universe, while the opposite is true for small caps. P/Es of small-cap growth stocks are currently skewed to the upside because of the large presence of biotech companies that have minimal or negative earnings but high stock prices.

Equities

-10%

10%

30%

50%

70%

90%

110%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

VALUATION PREMIUM: GROWTH VS. VALUE Based on 1 Year Forward P/E Ratio, January 2005 to March 2016

Russell 1000 Growth/Value Long Term Median

Russell 2000 Growth/Value Long Term Median

65 65

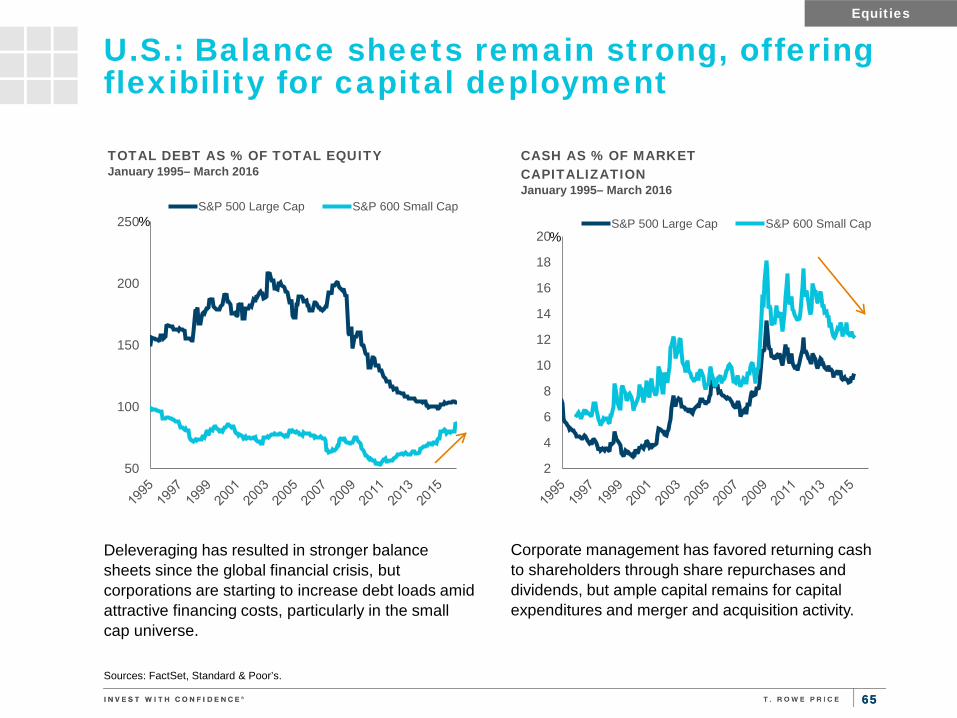

Deleveraging has resulted in stronger balance sheets since the global financial crisis, but corporations are starting to increase debt loads amid attractive financing costs, particularly in the small cap universe.

Sources: FactSet, Standard & Poor’s.

U.S.: Balance sheets remain strong, offering flexibility for capital deployment

Corporate management has favored returning cash to shareholders through share repurchases and dividends, but ample capital remains for capital expenditures and merger and acquisition activity.

%

Equities

%

50

100

150

200

250

TOTAL DEBT AS % OF TOTAL EQUITY January 1995– March 2016

S&P 500 Large Cap S&P 600 Small Cap

2

4

6

8

10

12

14

16

18

20

CASH AS % OF MARKET CAPITALIZATION January 1995– March 2016

S&P 500 Large Cap S&P 600 Small Cap

66 66

* Data based on financial statements released as of 3/31/16. Sources: Citi Research, Factset, Deutsche Bank U.S. Equity Strategy.

U.S.: Shareholder-friendly actions continue; capex spending growth is muted

-100

100

300

500

700

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

U.S

. $, b

illio

ns

S&P 500 CASH DEPLOYMENT 2000–2015* Dividends Buybacks Capex

0

200

400

600

800

1,000

0

50

100

150

200

250

Num

ber of Deals

$ B

illio

ns

Value of Deals (L)Number of Deals (R)

NUMBER AND VALUE OF U.S. M&A DEALS January 2001–March 2016

0

100

200

300

400

500

600

700

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

U.S

. $, b

illio

ns

S&P 500 BUYBACK ANNOUNCEMENTS Rolling 12-month total, January 1996–March 2016

Equities

67 67

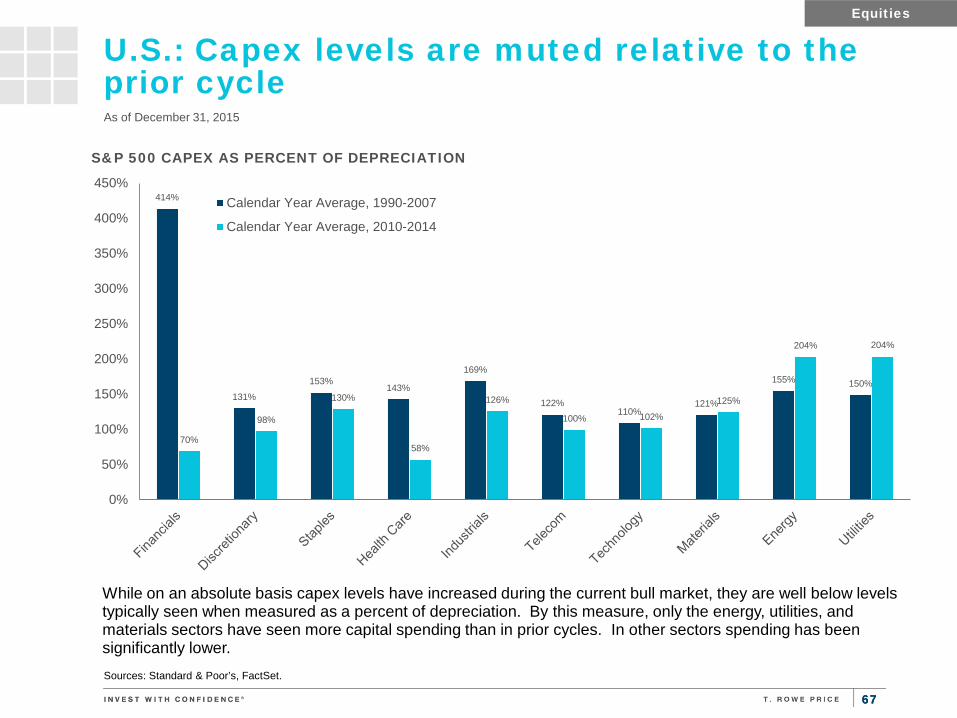

Sources: Standard & Poor’s, FactSet.

U.S.: Capex levels are muted relative to the prior cycle

Equities

414%

131%

153% 143%

169%

122% 110%

121%

155% 150%

70%

98%

130%

58%

126%

100% 102%

125%

204% 204%

0%

50%

100%

150%

200%

250%

300%

350%

400%

450%

S&P 500 CAPEX AS PERCENT OF DEPRECIATION

Calendar Year Average, 1990-2007

Calendar Year Average, 2010-2014

As of December 31, 2015

While on an absolute basis capex levels have increased during the current bull market, they are well below levels typically seen when measured as a percent of depreciation. By this measure, only the energy, utilities, and materials sectors have seen more capital spending than in prior cycles. In other sectors spending has been significantly lower.

68 68

0%

1%

2%

3%

4%

5%

6%

7%

8%

Div

iden

d an

d B

uyba

ck Y

ield

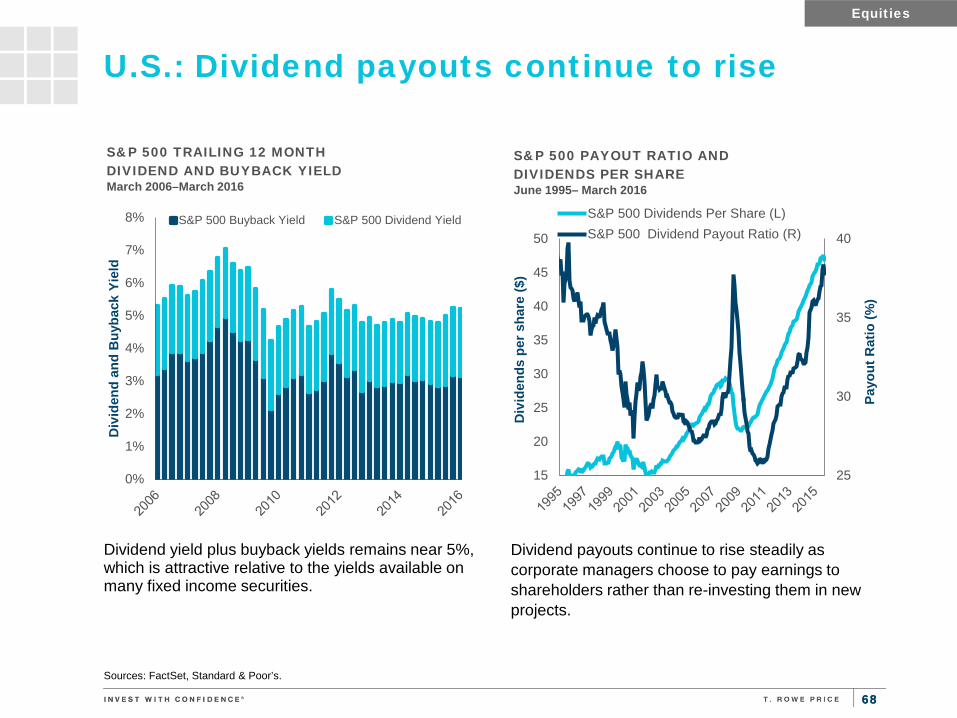

S&P 500 TRAILING 12 MONTH DIVIDEND AND BUYBACK YIELD March 2006–March 2016

S&P 500 Buyback Yield S&P 500 Dividend Yield

Dividend yield plus buyback yields remains near 5%, which is attractive relative to the yields available on many fixed income securities.

Sources: FactSet, Standard & Poor’s.

U.S.: Dividend payouts continue to rise

Dividend payouts continue to rise steadily as corporate managers choose to pay earnings to shareholders rather than re-investing them in new projects.

Equities

25

30

35

40

15

20

25

30

35

40

45

50

Payo

ut R

atio

(%)

Div

iden

ds p

er s

hare

($)

S&P 500 PAYOUT RATIO AND DIVIDENDS PER SHARE June 1995– March 2016

S&P 500 Dividends Per Share (L)S&P 500 Dividend Payout Ratio (R)

69 69

Equity markets typically do not remain range-bound for an extended period of time. However, this has been the case for the S&P 500 since mid-2014.

U.S.: Flat markets are relatively rare

Equities

8%

11% 13%

7%

17%

9% 7%

11%

17%

12%

8% 6%

33%

25%

18%

11%

25%

42%

55%

64%

0%

10%

20%

30%

40%

50%

60%

70%

1 Year Periods 2 Year Periods 3 Year Periods 5 Year Periods

Cum

ulat

ive

Ret

urns

S&P 500 PRICE RETURN Rolling Monthly Periods, January 1927 to March 2016

-20% or worse -5% to -20% -5% to +%5

+5% to +20% +20% or better

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2012 2013 2014 2015 2016

Inde

x Le

vel

S&P 500 INDEX January 2012 to March 2016

Past performance cannot guarantee future results. Sources: FactSet, Standard & Poor’s

70 70

$100

$120

$140

$160

$180

2013 2014 2015 2016Ea

rnin

gs /

Shar

e

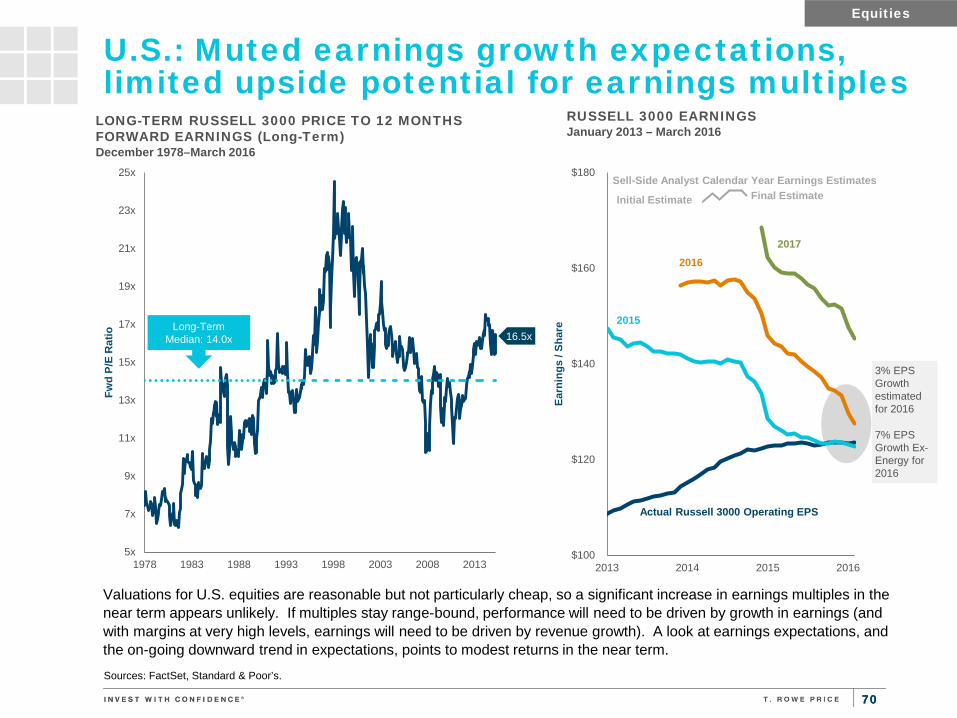

Valuations for U.S. equities are reasonable but not particularly cheap, so a significant increase in earnings multiples in the near term appears unlikely. If multiples stay range-bound, performance will need to be driven by growth in earnings (and with margins at very high levels, earnings will need to be driven by revenue growth). A look at earnings expectations, and the on-going downward trend in expectations, points to modest returns in the near term.

Sources: FactSet, Standard & Poor’s.

U.S.: Muted earnings growth expectations, limited upside potential for earnings multiples

Equities

5x

7x

9x

11x

13x

15x

17x

19x

21x

23x

25x

1978 1983 1988 1993 1998 2003 2008 2013

Fwd

P/E

Rat

io

LONG-TERM RUSSELL 3000 PRICE TO 12 MONTHS FORWARD EARNINGS (Long-Term) December 1978–March 2016

Long-Term Median: 14.0x 16.5x

Initial Estimate Final Estimate

RUSSELL 3000 EARNINGS January 2013 – March 2016

2017 2016

2015

3% EPS Growth estimated for 2016

7% EPS Growth Ex-Energy for 2016

Actual Russell 3000 Operating EPS

Sell-Side Analyst Calendar Year Earnings Estimates

71 71

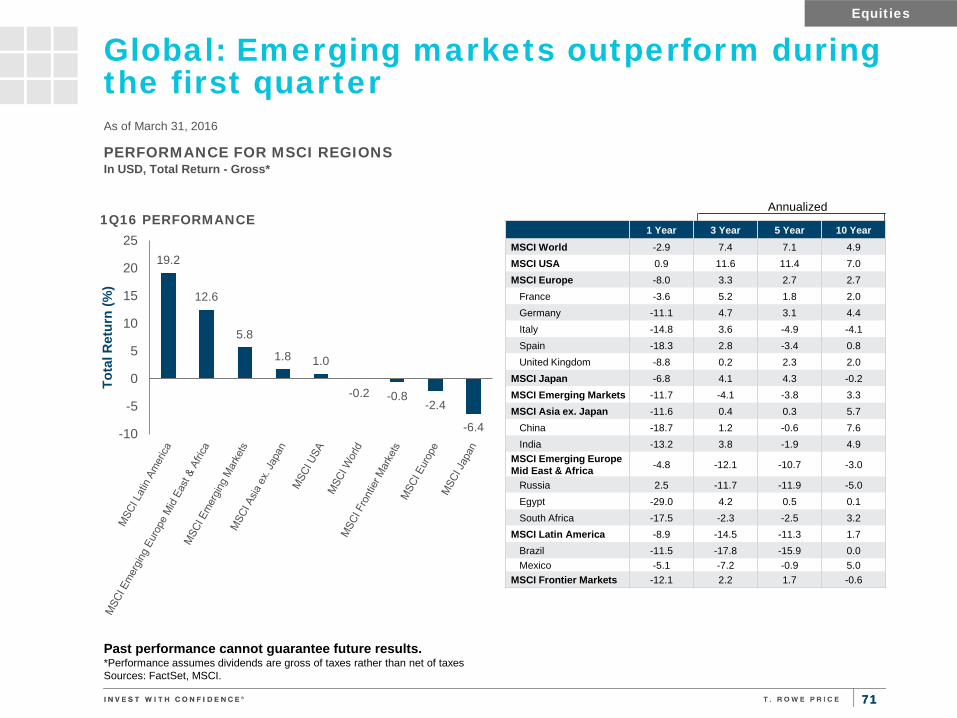

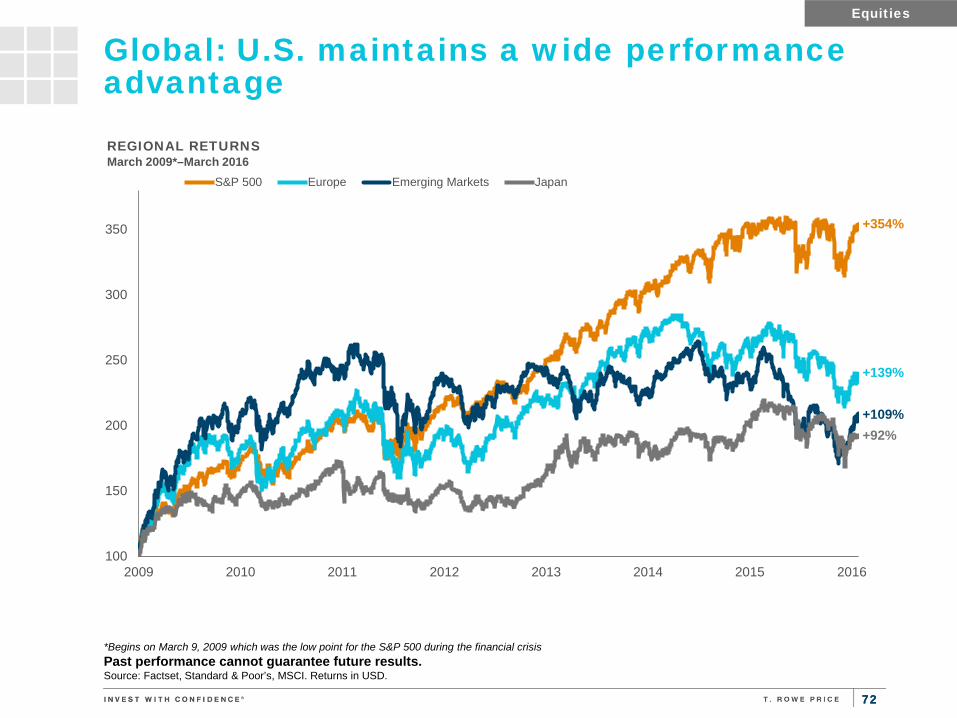

Global: Emerging markets outperform during the first quarter As of March 31, 2016

PERFORMANCE FOR MSCI REGIONS In USD, Total Return - Gross*

1 Year 3 Year 5 Year 10 Year