Embed Size (px)

Citation preview

First Albany CapitalAnnual Growth ConferenceDecember 8, 2004

1

Certain statements contained in this presentation are forward-looking statements. These forward-looking

statements are based upon our current expectations about future events. When used in this presentation, the

words "believe," "anticipate," "intend," "estimate," "expect," “will,” “should,” “may,” and similar expressions, or the

negative of such words and expressions, are intended to identify forward-looking statements, although not all

forward-looking statements contain such words or expressions. These forward-looking statements generally

relate to our plans, objectives and expectations for future operations and are based upon management’s current

estimates and projections of future results or trends. However, these statements are subject to a number of risks

and uncertainties affecting our business. You should read this presentation completely and with the

understanding that actual future results may be materially different from what we expect as a result of these risks

and uncertainties and other factors, which include, but are not limited to: (1) technological, structural and cyclical

changes that could reduce the demand for the services we provide; (2) loss of key customers; (3) the uncertainty

of the outcome of federal energy legislation; (4) the nature of our contracts, particularly our fixed-price contracts;

(5) work hindrance due to inclement weather events; (6) the award of new contracts and the timing of the

performance of those contracts; (7) project delays or cancellations; (8) the failure to meet schedule or

performance requirements of our contracts; (9) the presence of competitors with greater financial resources and

the impact of competitive products, services and pricing; (10) successful integration of the acquisitions into our

business; (11) close out of certain of our projects may or may not occur as anticipated or may be unfavorable to

us; and (12) other factors detailed from time to time in our other reports and filings with the Securities and

Exchange Commission, including the discussion under the heading "Risk Factors" in our Registration Statement

on Form S-1 relating to our initial public offering. Except as required by law, we do not intend to update forward-

looking statements even though our situation may change in the future.

Forward-Looking Statements

2

Introduction to InfraSource

3

Leadership in Infrastructure Services

Vision:

“InfraSource will be the recognized national leader in providing infrastructure services to utility and industrial companies.”

We are leaders in our markets

Favorable trends imply substantial growth opportunities

IFS is well positioned as beneficiary

4

Comprehensive Service Offering

Leading provider of design, engineering and construction services for electric power, natural gas and telecommunications infrastructure

2003 Revenue By End MarketElectric Power

� Transmission lines

� Substations

� Distribution lines

� Industrial services

Natural Gas

� Distribution lines

� Transmission facilities

Telecommunications

� Point-to-point fiber connections in select regional markets

Note: Includes Maslonka in both periods.

Natural Gas28%

Telecom11%

Other3%

Electric Power58%

YTD Sept 2004 Revenue By End Market

Natural Gas31%

Telecom8%

Other3%

Electric Power58%

5

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

1949 1962 1975 1988 2001

Tran

smis

sion

Con

stru

ctio

n S

pend

ing

(in r

eal 2

003

$'s

in m

illio

ns)

0

200

400

600

800

1,000

1,200

Electricity G

eneration Capacity

(in MW

)

Construction Spending Electricity Generation Capacity

0

500

1,000

1,500

2,000

2,500

1998 1999 2000 2001 2002 2003

Num

ber

of T

LRs

Leve

l 2 o

r H

ighe

r

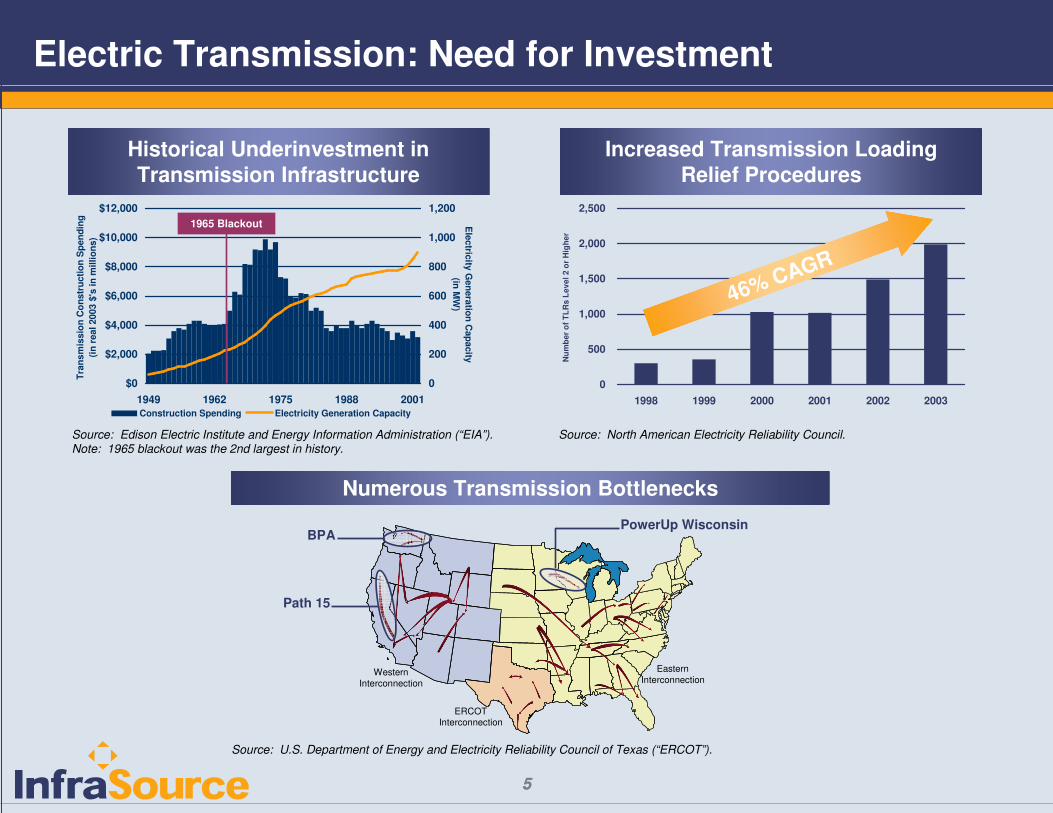

Source: Edison Electric Institute and Energy Information Administration (“EIA”).Note: 1965 blackout was the 2nd largest in history.

Source: North American Electricity Reliability Council.

Source: U.S. Department of Energy and Electricity Reliability Council of Texas (“ERCOT”).

Electric Transmission: Need for Investment

Historical Underinvestment inTransmission Infrastructure

Increased Transmission LoadingRelief Procedures

Numerous Transmission Bottlenecks

1965 Blackout

46% CAGR

5

Path 15

BPAPowerUp Wisconsin

Western Interconnection

ERCOT Interconnection

Eastern Interconnection

6

$3.5

$5.5

$10.0

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

Status Quo Keeping Up Significant Upgrades

An

nu

al T

ran

smis

sio

n S

pen

din

g

Current and Projected Electric Transmission Spending

� Energy Bill not required

� Addressing critical situations

� Backlog of projects is considerable in all regions

� Project planning and approval cycles take time

� Would result in ~ 1% increase in rates

_________________________________________Source: Wall Street research

Materials49%

Internal Labor13%

O utsourced Labor38%

Typical Transmission Spending Breakdown$2 B/yr Increase Likely

($ in billions) Estimates of required incrementalinvestment range from $36B to $100B

Transmission Spending

7

� Utility commissions traditionally regulate rates (bundled)

� Typical ROI 9.5% to 11%

States

� FERC can grant rates for transmission

� Typically less controversial proceedings than with States

� Typical ROI 13%

Federal

� Recently emerging trend:

� Merchant propositions

� Project financing

� Lease-purchase arrangements

Private

Emerging Transmission Funding

� PJM

� NJ utilities expenditure commitments due to reliability issues

� ERCOT (Texas)

� Constraint areas identified

� Multiple relief projects identified in each area

� Rate-making process established

� New England

� 22 near-term projects

� FERC approved regional cost sharing

� $1.4B investment over 5 years

� NU spending of $200m/year on transmission

� Wisconsin

� $2.8B spending over 10 years

� Filed for FERC rate making

� PJM

� Seeking market-based solutions for 30 grid constraints

� Will order utility action if there is no market response

� PMAs

� WAPA, BPA using private financing on recent large projects

Transmission Spending

8

Major Transmission Project Update – 3rd Quarter 2004

Path 15 (WAPA, California):

� Project is complete

� Line turned over to WAPA and testing is in progress

Schultz-Wautoma (BPA, Washington):

� Project is well underway and progressing nicely

Power Up Wisconsin (ATC):

� Work being released in segments

� Substantial mobilization at the end of 3rd quarter on first segment

� Project is progressing; some segments proceeding slowly due to permitting

9

Positioned to Capture Growth in Electric T&D Spending

Electric Transmission/Substation Focus InfraSource Footprint

Focused on specialized, high-margin services for key customers across a broad geographic footprint

Generating Station

InfraSource Primary Focus

InfraSource Capabilities

Substation Step-Up

Transformer

Transmission Line

Transmission Line

Transmission Customer

Substation Step-Down Transformer

Distribution Line

End User

End User

10

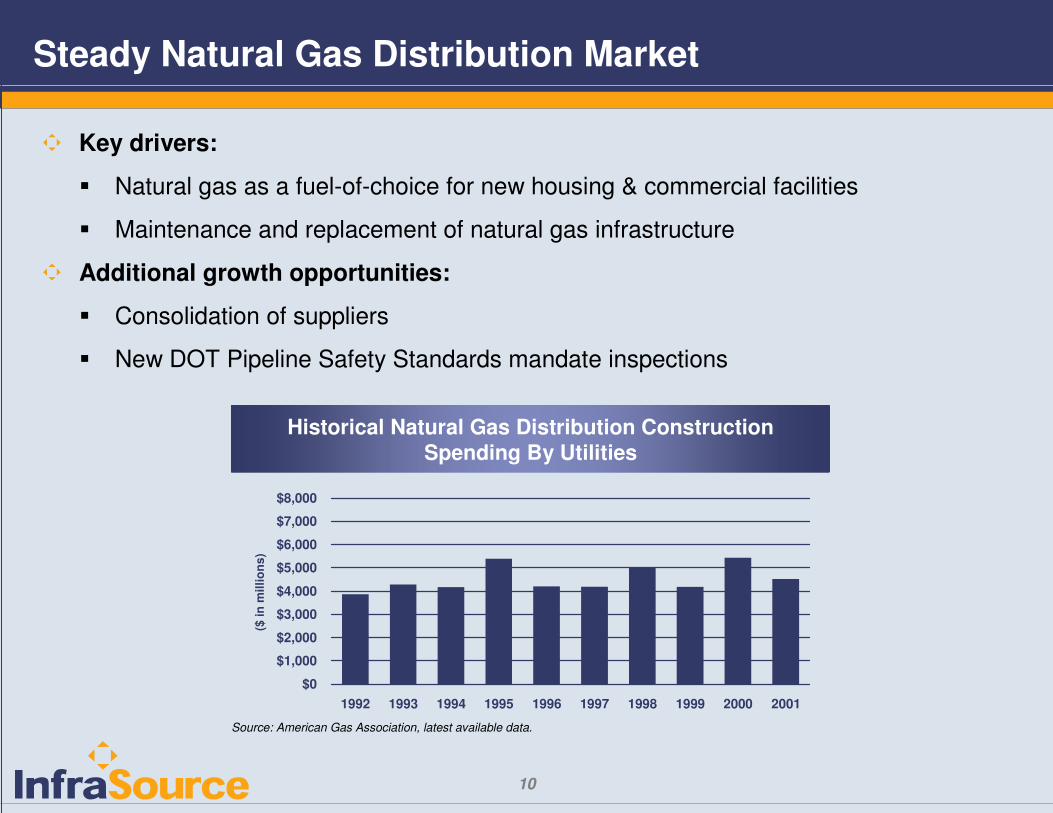

Key drivers:

� Natural gas as a fuel-of-choice for new housing & commercial facilities

� Maintenance and replacement of natural gas infrastructure

Additional growth opportunities:

� Consolidation of suppliers

� New DOT Pipeline Safety Standards mandate inspections

Historical Natural Gas Distribution Construction Spending By Utilities

Source: American Gas Association, latest available data.

Steady Natural Gas Distribution Market

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

($ in

mill

ions

)

11

Leader in Natural Gas Distribution Services

Natural Gas Distribution Focus InfraSource Footprint

Leading natural gas distribution contractor with comprehensive capabilities across a broad geographic footprint

InfraSource Capabilities

City Gate

GateStation

Substation

Substation

InfraSource Primary Focus

12

Strategic Acquisitions

Recent acquisitions:� Acquisition of substantially all the assets and certain liabilities of EnStructure and Utili-Trax

EnStructure, construction services business of SEMCO (NYSE:SEN):� Cash purchase price: $21.3 million� Utility, oil & gas customers in Midwest, South and Southeast� $75 million revenues in 2003� Closing: September 3, 2004

Utili-Trax, construction business of Connexus Energy:� Cash purchase price: $5.3 million� Electric and gas cooperative and municipal utility customers throughout the Midwest� $10 million revenues in 2003� Closing: August 18, 2004

Strategic benefits:� Customer base consolidation in Midwest, including SEMCO and Connexus� Additional geographic reach into South and Southeast� Expanded portfolio of service offerings

Expect positive contribution in 4Q04; integration is progressing smoothly

13

Attractive Telecommunications Niche

Profitable business model with strong cash flows

� Engineering, construction and leasing of point-to-point fiber connections

� Long-term lease contracts

� Virtually no maintenance capex requirements

Key customers include:

14

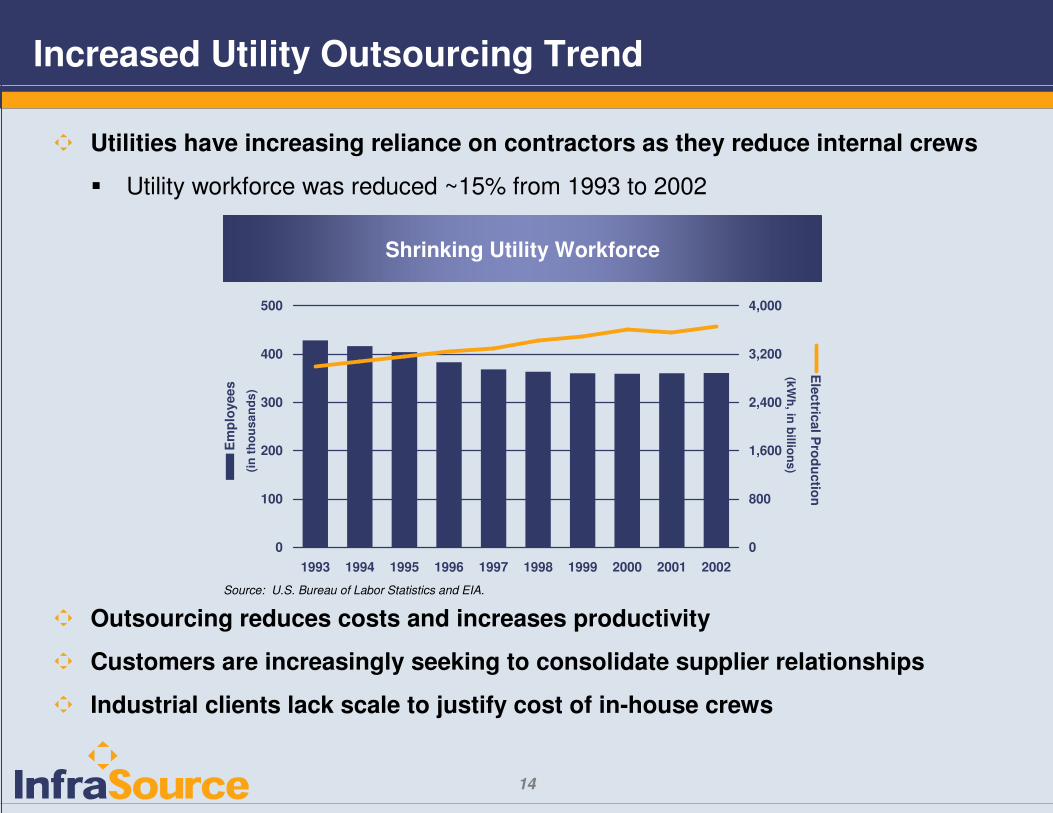

Utilities have increasing reliance on contractors as they reduce internal crews

� Utility workforce was reduced ~15% from 1993 to 2002

Outsourcing reduces costs and increases productivity

Customers are increasingly seeking to consolidate supplier relationships

Industrial clients lack scale to justify cost of in-house crews

Increased Utility Outsourcing Trend

Source: U.S. Bureau of Labor Statistics and EIA.

Shrinking Utility Workforce

0

100

200

300

400

500

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

(in th

ousa

nds)

0

800

1,600

2,400

3,200

4,000

(kWh, in billions)

Electrical P

roductionE

mpl

oyee

s

15

End Market Update – 3rd Quarter 2004

Electric Power:

� Backlog is up 95% or $188 million in 3Q04 versus 3Q03 and up 30% or $88 million versus 2Q04

� Approximately $28 million of the increase versus 2Q04 is due to recent acquisitions

� Awarded three new transmission orders in 3Q04 totaling $23 million

� Continued opportunities in transmission work with key customers on a regional basis

� Sizable increase in backlog of distribution work with awards of $23 million by strategic customers

� Tracking large transmission project opportunities but do not foresee contribution in 1H 2005

Natural Gas:

� Backlog is up 61% or $167 million in 3Q04 versus 3Q03 and up 8% or $34 million versus 2Q04

� Includes $79 million from EnStructure acquisition and represents addition of multi-year blankets

� Addition of these contracts offset the normal seasonal decline in backlog

Telecommunications:

� Backlog is up 42% or $44 million in 3Q04 versus 3Q03 and flat versus 2Q04

� Business is steady and we continue to evaluate and pursue new market opportunities

16

Martin Maslonka19 Years

Paul Daily16 Years

Steve Reiten30 Years

Henry Jackson33 Years

Larry Coleman15 Years

CFOTerence Montgomery

18 Years

Key Subsidiary Presidents

Talented and experienced management team extending deep into theorganization

Average 24 years of industry experience

Experienced Management Team

CEODavid Helwig

30 Years

Sr. VP – Strategic SalesHomer Purcell

30 Years

17

Financial Overview

18

Attractive Financial Model

Positive revenue and earnings momentum:

� Increased backlog and heightened bidding activity

Focus on value added, high margin work

Strong balance sheet with conservative leverage:

� Substantial bonding capacity

� Good liquidity and modest working capital requirements

Balanced approach to use of cash:

� Working capital for growth

� Debt repayment

� Strategic acquisition opportunities

19

Strong Balance Sheet

Note:1. Approximately $30 million of revolver capacity is expected to be used for letters of credit.

3/31/04(Pre-IPO)

6/30/04(Post-IPO)

9/30/04(Post-IPO)

($ in millions)

Cash 16.1$ 19.3$ 6.7$

Debt:Revolver ($85 million) (1) 5.0 - 4.0 Term Loan 139.4 85.1 84.9 Exelon Note 25.2 - - Other Debt 1.1 1.1 1.1

Total Debt 170.7$ 86.2$ 90.0$

Shareholders Equity 172.5 271.3 276.9

Total Capitalization 343.2$ 357.5$ 366.9$

Debt / Equity 99% 32% 33%

20

Reconciliation of Non-GAAP Financial Measures

Adjustment of GAAP measures is beneficial in understanding operating performance without the effect of unusual items including:

� Changes in accounting principle pursuant to SFAS 142

� Discontinued operations

� Amortization of intangibles pursuant to SFAS 141

� Transaction expenses related to the IPO and purchase from Exelon and acquisitions

� Loss on early extinguishment of debt

� Non-recurring gains

Note: see slide 30 for reconciliation of Net Income to EBITDA and EBITDA as Adjusted

($ in millions) 2001 2002 2003 LTM 9/30/04

Revenue 609.3$ 566.5$ 520.6$ 594.5$

Net Income (loss) - GAAP (6.0)$ (175.4)$ (22.2)$ 5.4$

EBITDA 56.5$ 73.2$ 18.1$ 56.6$

EBITDA as Adjusted 52.3$ 67.6$ 46.7$ 68.5$

21

11.5%

9.0%

11.9%

8.6%

$0

$100

$200

$300

$400

$500

$600

$700

2001 2002 2003 LTM0%

3%

6%

9%

12%

15%

18%

21%

Strong Historical Performance

Historical Revenue and EBITDA As Adjusted Margin

Growing core electric power businessPlanned exit from select natural gas contracts with lower margins$75 million decline in telecommunications E&C revenue; minimal exposure in future2002 margin expansion due to increased mix of higher margin IPP work

Rev

enue

($ in

mill

ions

)

EB

ITDA

As A

djusted Margin

$609$566

$521$595

Electric Power Other Natural Gas Telecom

EBITDA margin from continuing operations, before extraordinary items and cumulative effect of a change in accounting principle, net of tax as adjusted

Please refer to our prospectus filed on May 6, 2004 and Form 10-Q filed on November 15, 2004 with the Securities and Exchange Commission for the Company’s financial statements for the periods indicated above.

22

$129

$166

$0

$50

$100

$150

$200

$250

9/23/2003 9/30/2004

($ in

mill

ions

)

Total Backlog

Backlog includes:� Project Work: Signed contracts with authorization to proceed� Master Service Agreements (“MSAs”): Estimate of work to be performed; often 2-3 year terms� Telecommunications Lease Agreements: Signed contracts; typically 5+ years

Backlog is up 69%

Remaining Fiscal Year Backlog

Note: Includes Maslonka in all periods.

$587

$791

$992

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

9/23/2003 12/31/2003 9/30/2004($

in m

illio

ns)

69% Increase

29% Increase

23

10.9%

7.3%

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

9 Mos. 2003 9 Mos. 20040%

3%

6%

9%

12%

15%

18%

21%

YTD September 2004 Performance

Historical Revenue and EBITDA As Adjusted Margin

Increase primarily attributable to: � Additional aerial transmission work including the acquisition of Maslonka & Associates� Underground natural gas work� Offset by declines in other electric and telecommunications work

Rev

enue

($ in

mill

ions

)E

BITD

A A

s Adjusted M

argin

$383

$457

Please refer to our Form 10-Q filed on November 15, 2004 with the Securities and Exchange Commission for the Company’s financial statements for the periods indicated above.

Electric Power Other Natural Gas Telecom

EBITDA margin from continuing operations, before extraordinary items and cumulative effect of a change in accounting principle, net of tax as adjusted

24

4th Quarter 2004 Guidance

Revenues will be 5-7% higher due to effect of recent acquisitions, partially offset by the seasonal nature of our business

Gross margin percentage is expected to increase somewhat as a result of contribution from settlement of several open contract claims:

� Timing of settlements is such that we may not be able to recognize this revenue until 2005 which would result in gross margin percentage lower than the 3rd Quarter if that occurs

SG&A expenses will increase slightly due to our 3rd Quarter acquisitions

Depreciation will increase by approximately 15% due to the acquisitions

Amortization of intangibles assets is expected to be approximately $2.1 million, reflecting continued reduction in acquired backlog

Interest expense will be approximately the same as in the 3rd Quarter:

� Additional benefit of ~$1 million in interest forgiveness from early retirement of the Exelon note

25

Sell Side Coverage

Firm Analyst

D.A. Davidson & Co. John Rogers

First Albany Capital Sanjay Shrestha

Friedman, Billings & Ramsay* Alex Rygiel

Lehman Brothers Tom Ford

Merrill Lynch Lorraine Maikis

Sidoti & Co. Rich Wesolowski

Stifel, Nicolaus & Co. Jeffrey Beach

* - Expected December 2004

26

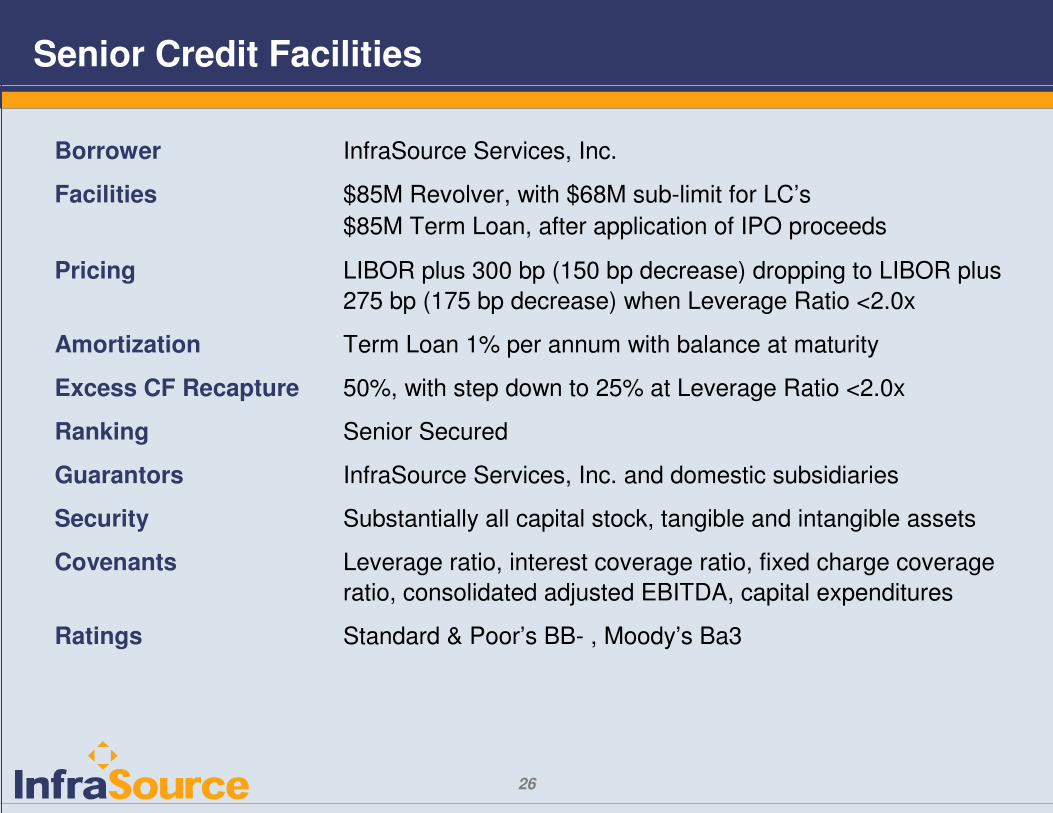

Senior Credit Facilities

Leverage ratio, interest coverage ratio, fixed charge coverage ratio, consolidated adjusted EBITDA, capital expenditures

Covenants

Standard & Poor’s BB- , Moody’s Ba3Ratings

50%, with step down to 25% at Leverage Ratio <2.0xExcess CF Recapture

Term Loan 1% per annum with balance at maturityAmortization

Substantially all capital stock, tangible and intangible assetsSecurity

InfraSource Services, Inc. and domestic subsidiariesGuarantors

Senior SecuredRanking

LIBOR plus 300 bp (150 bp decrease) dropping to LIBOR plus 275 bp (175 bp decrease) when Leverage Ratio <2.0x

Pricing

$85M Revolver, with $68M sub-limit for LC’s$85M Term Loan, after application of IPO proceeds

Facilities

InfraSource Services, Inc.Borrower

27

Leadership in Infrastructure Services

Market leader

� Strong complementary subsidiaries in fragmented markets

� Operational excellence

� Comprehensive capabilities

� Financial strength

� Exceptional safety performance

Growth opportunities

� Upgrade of T&D infrastructure

� Recovery in utility spending

� Trend toward increased outsourcing

� Leverage integrated capabilities to gain market share

� Selective strategic acquisitions

28

Compelling Growth Opportunity

LeadershipPosition

Attractive EndMarkets

Unique GrowthOpportunity

29

Appendices

30

For the For the Period For the PeriodYear Ended January 1 to January 1 to

December 31, September 23, September 23,2001 2002 2003 2003

(in millions)

(Predecessor entity - InfraSource

Incorporated and Subsidiaries)

(Predecessor entity - InfraSource

Incorporated and Subsidiaries)

(Predecessor entity - InfraSource

Incorporated and Subsidiaries)

For the Period May 30 to

December 31, 2003

(Predecessor entity - InfraSource

Incorporated and Subsidiaries)

Nine Months Ended September

30, 2004

Net income (loss) (6.0)$ (175.4)$ (23.5)$ 1.3$ (23.5)$ 4.1$

Cumulative effect of a change in accounting principle, net of tax - 204.1 - - - -

Extraordinary item, net of tax - - - (0.1) - -

Loss (income) on discontinued operations, net of tax 9.4 1.6 12.3 0.3 12.3 (0.4)

Gain on disposition of discontinued operation, net of tax - - - - - (0.6)

Interest expense 1.9 0.4 0.0 4.0 0.0 8.2

Interest income (0.2) (1.4) (1.4) (0.1) (1.4) (0.4)

Income tax expense (benefit) 7.0 14.6 (4.8) 1.1 (5.2) 2.1

Depreciation 28.3 29.5 20.9 5.3 20.9 17.6

Amortization of intangible assets and goodwill 16.0 - - 2.6 - 11.0

EBITDA from continuing operations, before extraordinary items and cumulative effect of a change in accounting principle, net of tax 56.5$ 73.2$ 3.6$ 14.5$ 3.1$ 41.6$

Gain on acquisition purchase price settlement - (5.2) - - - -

Insurance reserve adjustment (4.2) (0.4) 8.6 - 8.7 -

Merger related expenses - - 16.2 - 16.2 (0.3)

Litigation judgment and related costs - - - 3.8 - -

IPO related expenses - - - - - 2.4

Loss on early extinguishment of debt - - - - - 5.5

EnStructure/Utili-Trax severance and personnel expenses - - - - - 0.5

EBITDA from continuing operations, before extraordinary items and cumulative effect of a change in accounting principle, net of tax as adjusted 52.3$ 67.6$ 28.4$ 18.3$ 28.0$ 49.7$

Reconciliation of Non-GAAP Financial Measures

Please refer to our prospectus filed on May 6, 2004 and Form 10-Q filed on November 15, 2004 with the Securities and Exchange Commission for the Company’s financial statements for the periods indicated above.

31

PECo Strategy Review

10/96

PECO/ComEd Merger

Announced

8/99

EXC Merger Closes

10/00

EXC Announces

Intent to Divest

11/01

IFS Agreement

of Sale

6/03

Dashiell Acquisition

6/00

BP/S Acquisition

1/01

Maslonka LOI

8/03

PECo NRCG Pilot

11/96

Underground Acquisition

9/99

MJE Acquisition

12/00

IFS Strategy Review

5/02

IFS Closing

9/03

Maslonka Closing

1/04

PECO T&D GE Nuclear ComEd NGG ComEd NGG ComEd T&D InfraSource

Original InfraSource Acquisitions09/99 – 01/01

EnStructure Utili-Trax

Acquisitions09/04

IFS IPO

5/04

IFS Evolution

![Analyst Day Consolidated Book - RRD.ppt [Read-Only]media.corporate-ir.net/media_files/irol/19/196053/AnalystDay_TDG.pdfCDA InterCorp. Avtech ADS ... Organizational Philosophy Corporate](https://img.dokumen.tips/doc/110x75/5b093fcd7f8b9a51508d07f8/analyst-day-consolidated-book-rrdppt-read-onlymediacorporate-irnetmediafilesirol19196053analystdaytdgpdfcda.jpg)