Embed Size (px)

Citation preview

Financing Strategies for the Oil & Gas Industry

ALSO FIND US ON http://www.linkedin.com/companies/216795 http://www.facebook.com/Steptoe.Johnson

© 2013 Steptoe & Johnson PLLC . All Rights Reserved.

Follow Steptoe & Johnson on Twitter: Follow @Steptoe_Johnson

Keynote Speakers

Kristian J. Jamieson Southpointe, PA

Erika R. Groves Southpointe, PA

Financing Strategies for the Oil & Gas Industry

Structuring Bank Financing

• Who is the proposed borrower? • Will the credit require a guarantor? • How are such guarantors affiliated with

your borrower?

• What if your borrower is not the operator? – It is important to know how your borrower is

related to the operator – Knowing how the relationship between the

operator and your borrower works will help determine what collateral you need to secure the loan

– A clear understanding of all entities involved in the process and their ownership of collateral is critical in order to properly structure a loan

Structuring Bank Financing

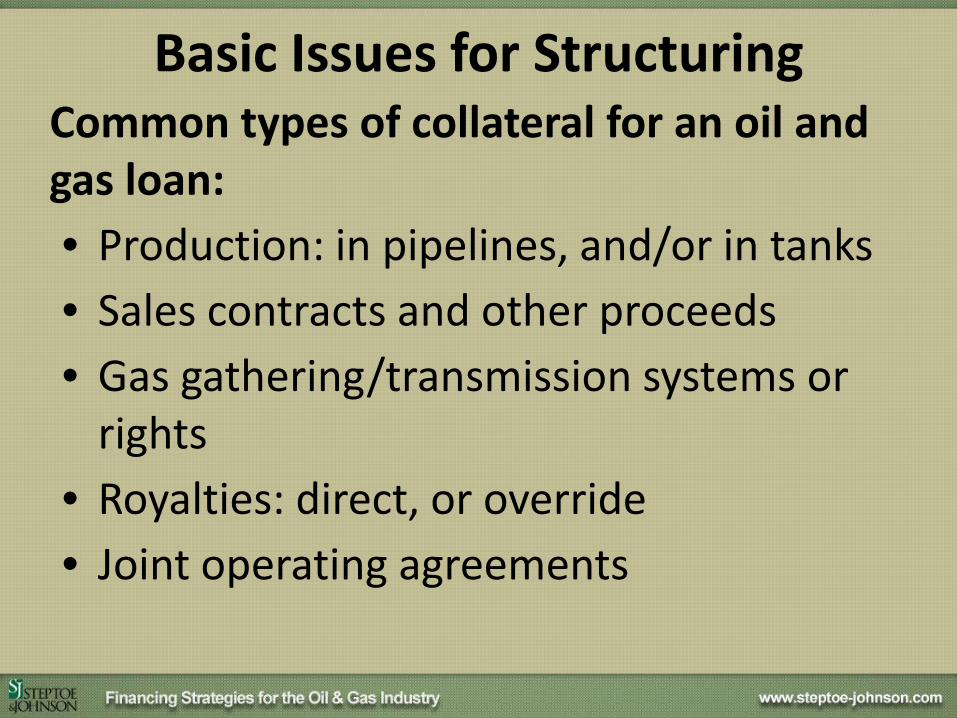

Basic Issues for Structuring Common types of collateral for an oil and gas loan: • Production: in pipelines, and/or in tanks • Sales contracts and other proceeds • Gas gathering/transmission systems or

rights • Royalties: direct, or override • Joint operating agreements

Basic Issues for Structuring Common types of collateral for an oil and gas loan: • Drill sites • Operating equipment • Working, fee or leasehold interests • Fee interests • Severed mineral interests

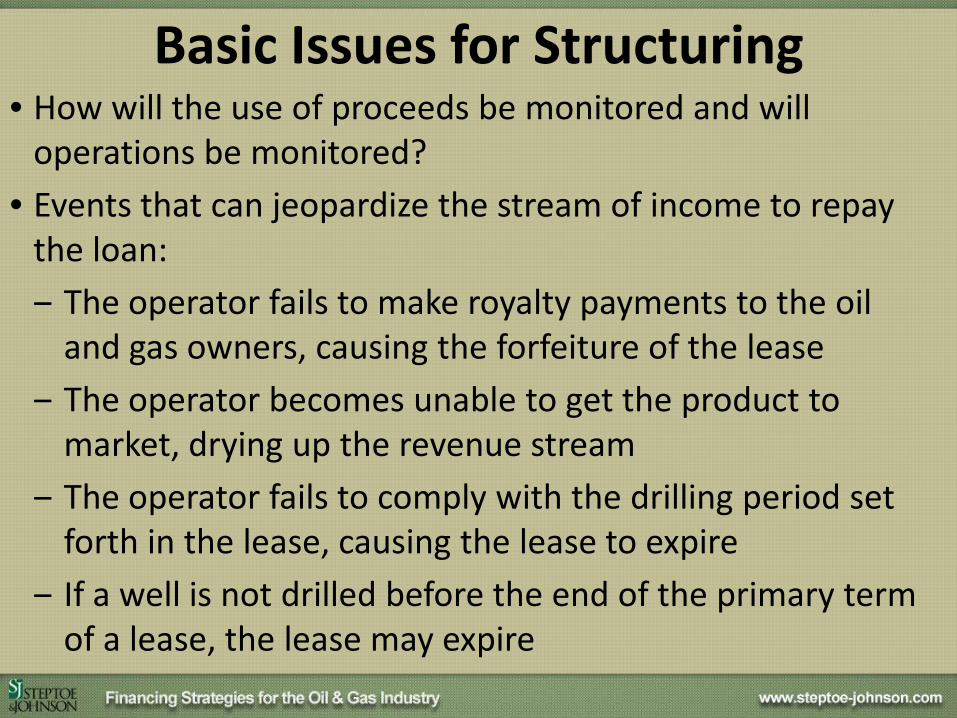

• How will the use of proceeds be monitored and will operations be monitored?

• Events that can jeopardize the stream of income to repay the loan: ‒ The operator fails to make royalty payments to the oil

and gas owners, causing the forfeiture of the lease ‒ The operator becomes unable to get the product to

market, drying up the revenue stream ‒ The operator fails to comply with the drilling period set

forth in the lease, causing the lease to expire ‒ If a well is not drilled before the end of the primary term

of a lease, the lease may expire

Basic Issues for Structuring

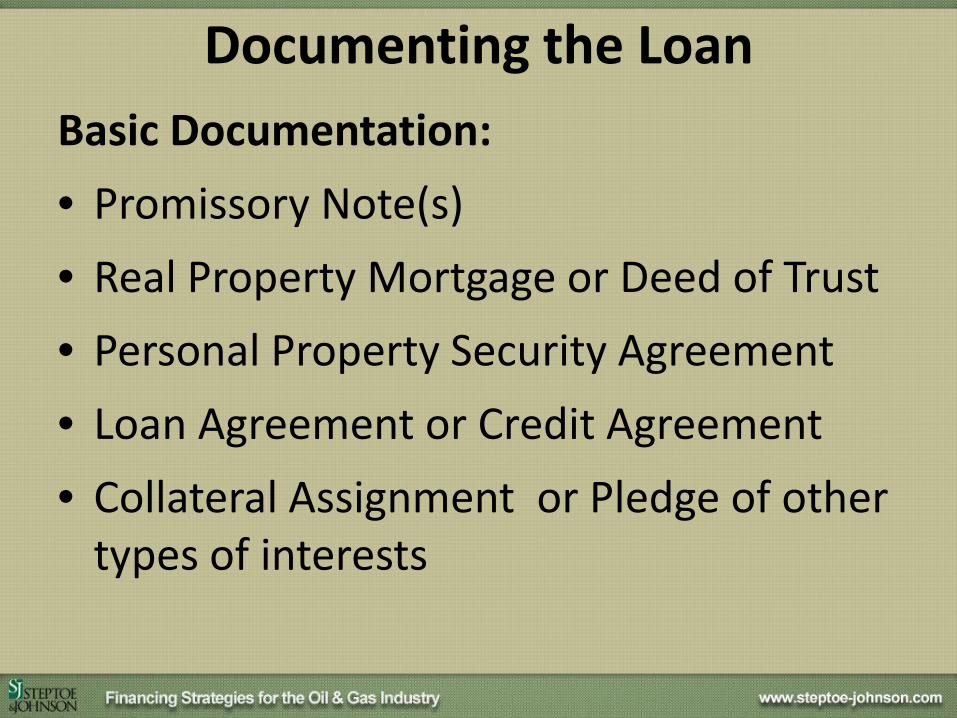

Basic Documentation: • Promissory Note(s) • Real Property Mortgage or Deed of Trust • Personal Property Security Agreement • Loan Agreement or Credit Agreement • Collateral Assignment or Pledge of other

types of interests

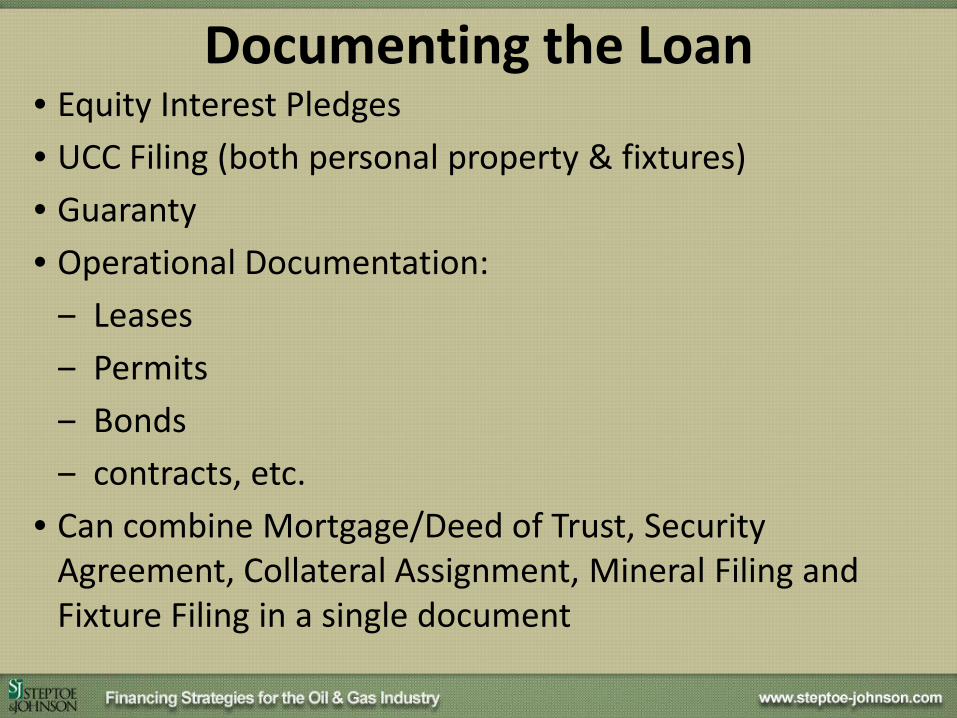

Documenting the Loan

• Equity Interest Pledges • UCC Filing (both personal property & fixtures) • Guaranty • Operational Documentation: ‒ Leases ‒ Permits ‒ Bonds ‒ contracts, etc.

• Can combine Mortgage/Deed of Trust, Security Agreement, Collateral Assignment, Mineral Filing and Fixture Filing in a single document

Documenting the Loan

Lien Perfection: Avoid lien perfection issues by using a document or documents which will cover the collateral regardless of whether the collateral is considered real property or personal proper, i.e., use a mortgage/deed of trust, security agreement and assignment, as well as a mineral filing, fixture filing and UCC financing statements.

Documenting the Loan

Private Equity Financing for the Oil and Gas Industry

How Do Private Equity Funds Invest? • Equity Line of Capital • Platform Investments • Acquisition of Private Company • Minority / Passive Investments • Buyouts • Debt and Debt-like Investment

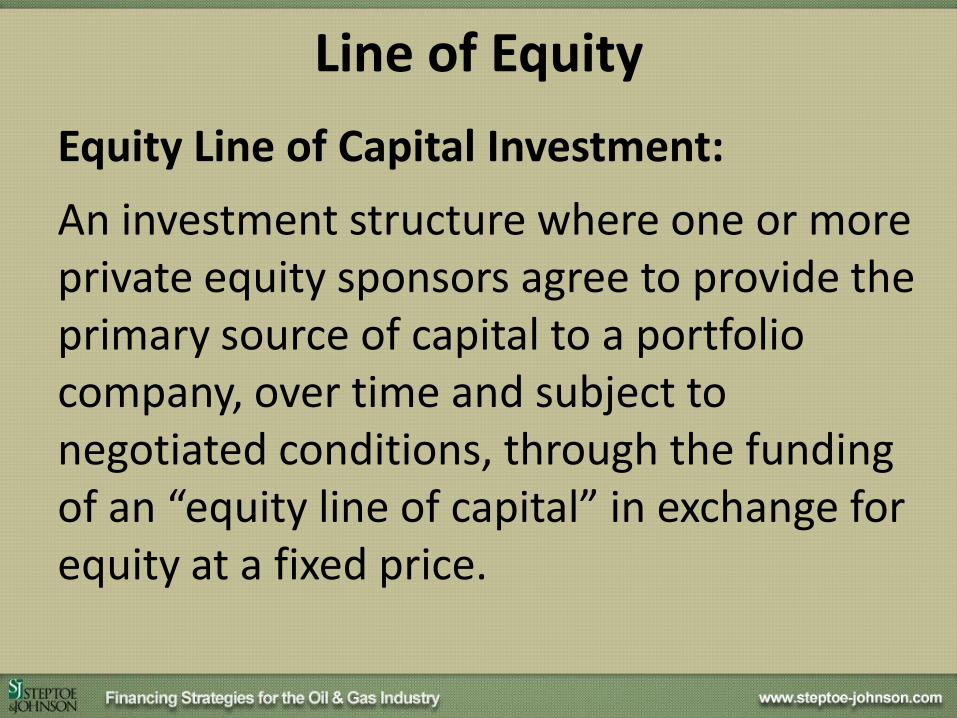

Line of Equity Equity Line of Capital Investment: An investment structure where one or more private equity sponsors agree to provide the primary source of capital to a portfolio company, over time and subject to negotiated conditions, through the funding of an “equity line of capital” in exchange for equity at a fixed price.

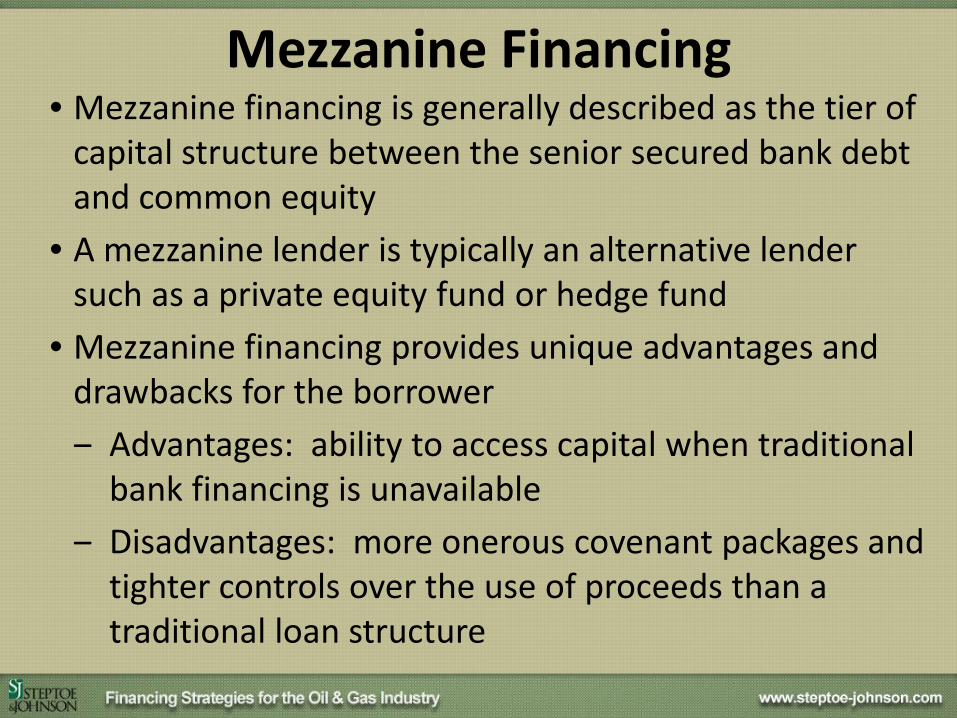

Mezzanine Financing • Mezzanine financing is generally described as the tier of

capital structure between the senior secured bank debt and common equity

• A mezzanine lender is typically an alternative lender such as a private equity fund or hedge fund

• Mezzanine financing provides unique advantages and drawbacks for the borrower ‒ Advantages: ability to access capital when traditional

bank financing is unavailable ‒ Disadvantages: more onerous covenant packages and

tighter controls over the use of proceeds than a traditional loan structure

Mezzanine Financing

Senior Debt

Subordinated Debt

Preferred Equity

Common Equity

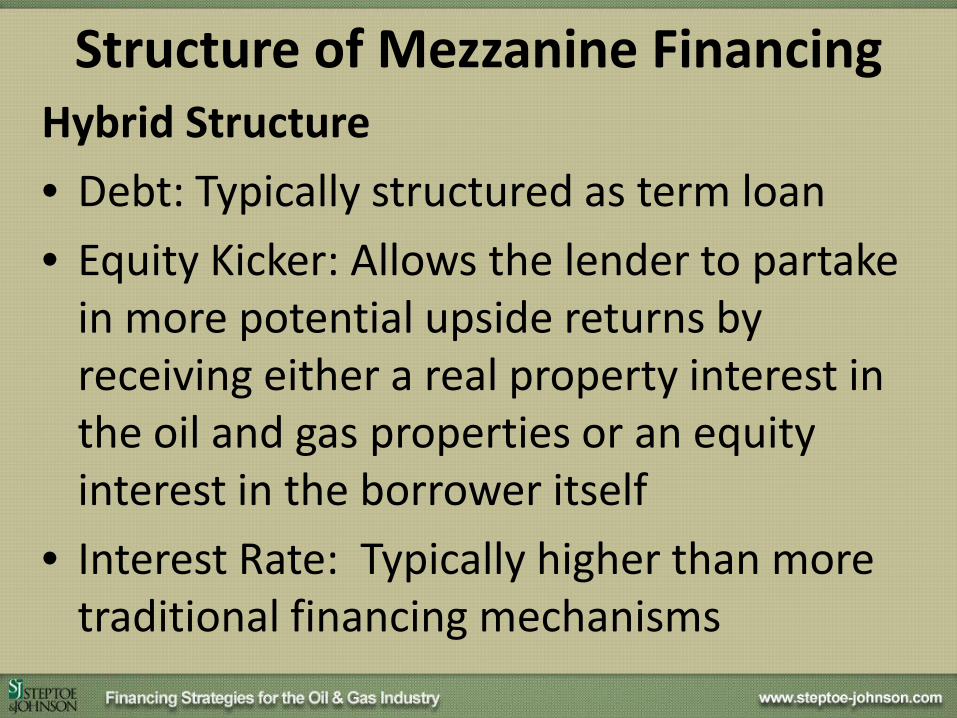

Structure of Mezzanine Financing Hybrid Structure • Debt: Typically structured as term loan • Equity Kicker: Allows the lender to partake

in more potential upside returns by receiving either a real property interest in the oil and gas properties or an equity interest in the borrower itself

• Interest Rate: Typically higher than more traditional financing mechanisms

Points to Takeaway • The energy industry poses a challenge to lenders and

investors due to its unique risks, assets and market factors and counsel from experts in the industry should be sought and utilized when evaluating any potential deal

• Commercial debt financing is available to borrowers but prudent lending practices will generally require senior priority liens on collateral with an established value and credit documents that impose financial covenants and which provide for recourse against the Borrower – Borrower’s must be prepared to endure ongoing monitoring and scrutiny of its assets, operations and financial performance when working with regulated financial institutions

Points to Takeaway • When seeking equity financing, be aware that it

will be more expensive than getting a traditional bank loan, both in terms of interest rate and providing the in-depth information on your company that the equity investors will want to see.

• Also, be prepared for the investor to expect to take a somewhat managerial role, since its return is directly based on the performance of the company.

Thank You!

Kristian J. Jamieson Southpointe, PA

[email protected] 724.873.3127

Erika R. Groves Southpointe, PA

[email protected] 724.873.3177

These materials are public information and have been prepared solely for educational purposes to contribute to the understanding of energy and oil and gas law. These materials reflect only the personal views of the authors and are not individualized legal advice. It is understood that each case is fact-specific, and that the appropriate solution in any case will vary. Therefore, these materials may or may not be relevant to any particular situation. Thus, the authors and Steptoe & Johnson PLLC cannot be bound either philosophically or as representatives of their various present and future clients to the comments expressed in these materials. The presentation of these materials does not establish any form of attorney-client relationship with the authors or Steptoe & Johnson PLLC. While every attempt was made to insure that these materials are accurate, errors or omissions may be contained therein, for which any liability is disclaimed.

Material Disclaimer