Embed Size (px)

Citation preview

R o b e r t B r ü c k m a n n , e c l a r e o n

D I A C O R E - C E P S P o l i c y Wo r k s h o p

B r u s s e l s 2 1 . 5 . 2 0 1 5

F inanc ing Renewab les : compar i son o f cos t o f cap i ta l in 28 EU MS

Background & methodology of research

Results: comparison of costs of capital

Conclusions

O v e rv ie w

Background & methodology

Main objectives:

Examine the role of risk and its influence on investments in the RES sector;

Compare the cost of capital and show why it matters;

Provide solutions in order to enhance investments in the RES sector;

Scope of research:

What is the range between cost of capital in the 28 EU MS for wind onshore projects and why is there such a range?

Which risks to wind onshore projects have which impact on RES investments?

How do changes in policy design affect costs of capital?

W o rk p a c k a g e : E n h a n c in g RE S in v e s tme n t

Our methodology for comparing costs of capita l and r isks

Model

• Estimation of costs of capital & ranking of wind onshore-investments risks

• Comprehensive literature study

• Application of RE-frame barriers database (more than 900 listed barriers)

• Draft of 28 EU MS country profiles

Evaluation

• Interviews with financial experts (more than 80 interviews in 26 MS)

• Evaluation of underlying assumptions of model & estimated parameters

• Adaptation of model based on input from interviews

Results

• Aggregation of EU-wide data

• Presentation of results and feedback from more than 40 national experts

• Preparation of deliverables: Country profiles, policy toolbox & final report

There are several methods for wind project financing: corporate financing or project financing

Ongoing changing (often falling) interest rates

Constant changes of RES market conditions

Lack of current, significant projects in some EU markets

Trade secrets

B e f o re w e s ta r t : s o me c a v e a ts

Comparison of costs of capital

W ACC e s t ima t io n s o n s h o re w in d – a p p ro x ima t io n b a s e d o n in te rv ie w s

I mp a c t o f c o s ts o f c a p i ta l o n RE S c o s ts in a s y s te m d y n a m ic a p p ro a c h

-

Little supportneeded

Low risk of systemchange

Low deployment

costs +

Much supportneeded

High deployment

costs

High risk of systemchange

Capital costs +

Much supportneeded

High deployment

costs

High risk of systemchange

Cost of capital

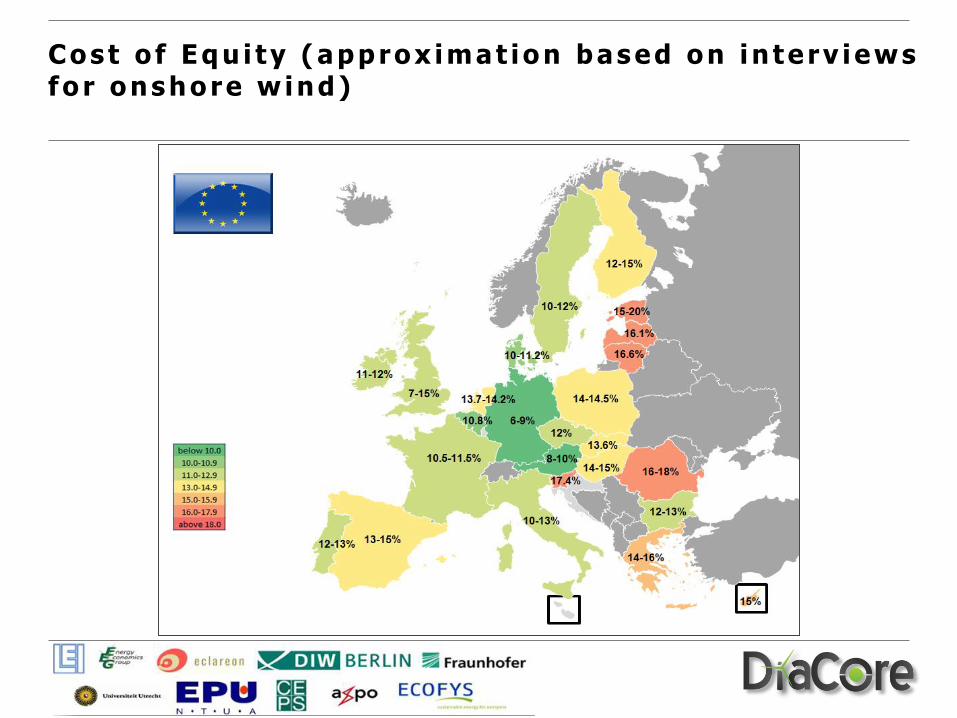

Co s t o f E q u i ty ( a p p ro x ima t io n b a s e d o n in te rv ie w s f o r o n s h o re w in d )

Co s t o f De b t ( a p p ro x ima t io n b a s e d o n in te rv ie w s f o r o n s h o re w in d )

De b t/ E q u i ty R a t i o s ( a p p ro x ima t io n b a s e d o n i n te rv ie w s f o r o n s h o re w in d )

Conclusions

Huge variation in costs of capital for wind onshore projects in EU Member States

High cost of capital lead to increasing wind onshore deployment costs

Difference is in particular due to difference in cost of debt and cost/equity ratio

Factors for differing costs of capital are

RES specific risk premium

Country specific risks

Competition between investors

Co n c lu s io n s

W ACC e s t ima t io n s a n d s u p p o r t s c h e me s f o r o n s h o re w in d

P a u l N o o t h o u t , E c o f y s

D I A C O R E - C E P S P o l i c y Wo r k s h o p

B r u s s e l s 2 1 . 5 . 2 0 1 5

F inanc ing Renewab les : M i t iga t ing r i sks to enhance RES inves tments

What risks are influencing RES investments?

What investment risks are most important?

How can policies mitigate investment risks?

O v e rv ie w

What risks are influencing RES

investments?

0%

2%

4%

6%

8%

10%

12%

Baseline rate Cost of equity RES investment risks

RE S in v e s tme n t r i s k s –H o w r i s k s in f lu e n c e c o s t o f e q u i ty

Ris

ks re

late

d to

RE

S in

vestm

ents

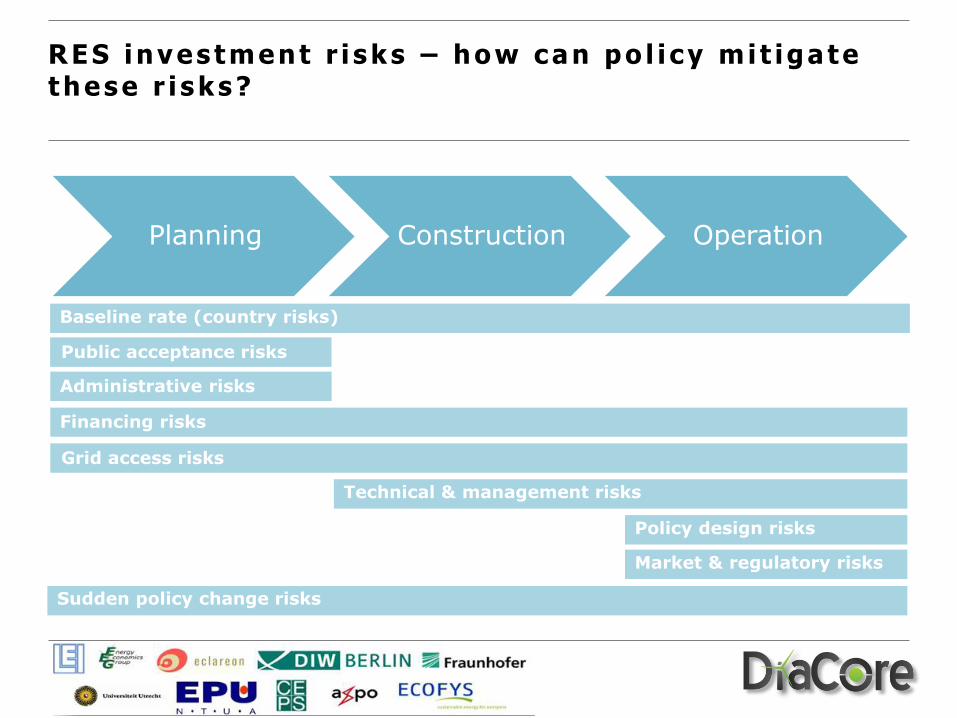

RE S in v e s tme n t r i s k s – Ris k c a te g o r ie s

Planning Construction Operation

Baseline rate (country risks)

Public acceptance risks

Administrative risks

Financing risks

Technical & management risks

Grid access risks

Policy design risks

Market & regulatory risks

Sudden policy change risks

What investment risks are most

important?

Av e ra g e ra n k in g o f r i s k c a te g o r ie s a c ro s s 24 E U M S

Average Ranking of Risks – 24 EU member states

Co mp a r in g r i s k s in N o r th - W e s te rn , E a s te rn a n d S o u th e rn M e m b e r S ta te s

Co mp a r in g r i s k s in M e mb e r S ta te s b y s ta tu s o f w in d p o w e r d e p lo y m e n t

How can policies mitigate

investment risks?

RE S in v e s tme n t r i s k s – h o w c a n p o l i c y mi t ig a te th e s e r i s k s ?

Planning Construction Operation

Baseline rate (country risks)

Public acceptance risks

Administrative risks

Financing risks

Technical & management risks

Grid access risks

Policy design risks

Market & regulatory risks

Sudden policy change risks

Huge variation in capital costs for RES projects in different EU Member States

Significant differences between regions and market development

Across all EU-MS Policy design risks perceived as most pressing;

Not only choice of support scheme essential for reduction of policy risks –specific design of support scheme also very important

Not all risk categories can be mitigated by policy alone, as other factors and stakeholders are also exerting influencing;

Co n c lu s io n s

B a r b a r a B r e i t s c h o p f , F r a u n h o f e r I S I

D I A C O R E - C E P S P o l i c y Wo r k s h o p

B r u s s e l s 2 1 . 5 . 2 0 1 5

F i nanc i ng Renewab l e s : The impac t o f c hanged s uppo r t s c hemes on t he c o s t o f c ap i t a l

Policy Impact Analysis

P o l i c y I mp a c t An a ly s i s : O b j e c t i v e

Objective:

show what the impact of policy design elements ison cost of capital

cost of capital comprises cost of equity and cost ofdebt:

its calculation is based on

interest rate

return on equity

equity share

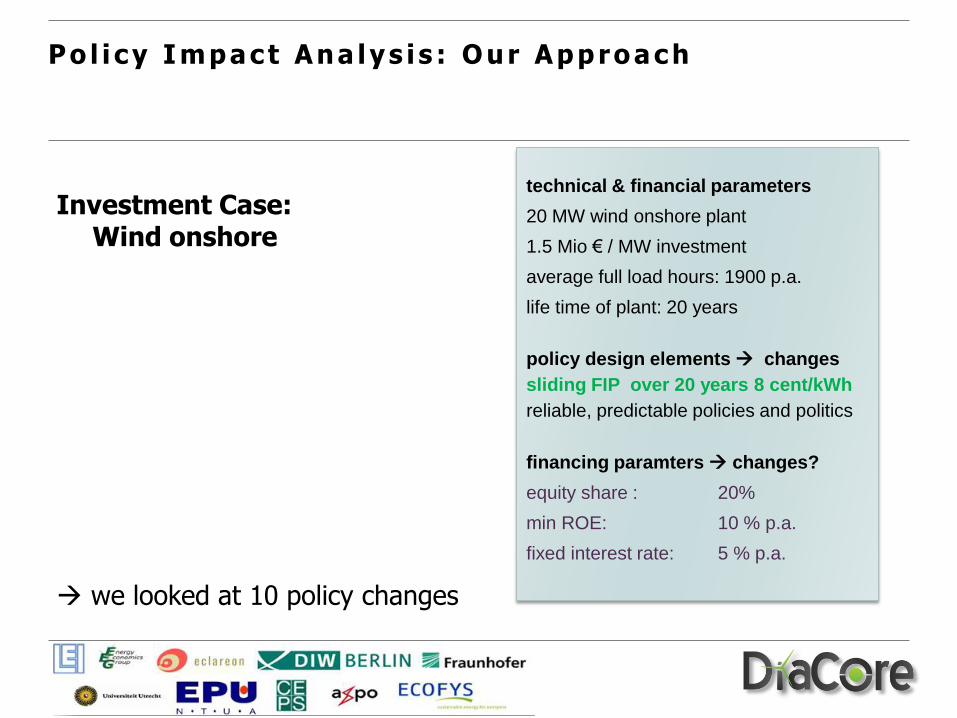

P o l i c y I mp a c t An a ly s i s : O u r Ap p ro a c h

Investment Case: Wind onshore

we looked at 10 policy changes

technical & financial parameters

20 MW wind onshore plant

1.5 Mio € / MW investment

average full load hours: 1900 p.a.

life time of plant: 20 years

policy design elements changes

sliding FIP over 20 years 8 cent/kWh

reliable, predictable policies and politics

financing paramters changes?

equity share : 20%

min ROE: 10 % p.a.

fixed interest rate: 5 % p.a.

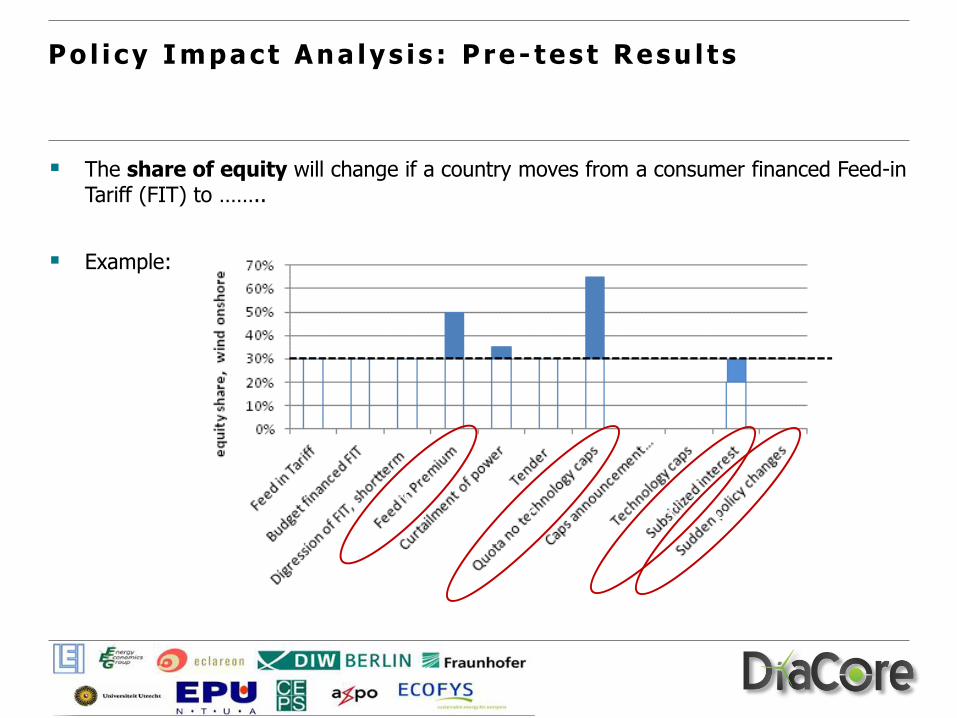

P o l i c y I mp a c t An a ly s i s : P re - te s t Re s u l t s

The share of equity will change if a country moves from a consumer financed Feed-in Tariff (FIT) to ……..

Example:

P o l i c y I mp a c t An a ly s i s : P re - te s t Re s u l t s

The interest rate will change if a country moves from a consumer financed Feed-in Tarif (FIT) to …..

Example:

Changes in policydesign – five„policy cases“:

changes of designfeatures lead touncertainties in

revenues

expenditures

risks

P o l i c y I mp a c t An a ly s i s : Re f in d e d Ap p ro a c h

FIT

risk

policy designs

uncertainty in revenues (price risk)

uncertainty in

expendituresFIT

sliding

FIP

FIP neg penalty due to delayed

/ no operation

expected start of operation

fixed

FIP

policy changeswill be translatedinto risks

risks will betranslated into :

interest rate, return on equity, equity share

or

no financing

P o l i c y I mp a c t An a ly s i s : E x p e c te d O u tc o me

minimum required equity share in %

FIT

sliding

FIP

no sliding

FIP if

negative

prices

fixed FIP

Tender

with

penalties

policy designs

25

20

15

10

30

P o l i c y I mp a c t An a ly s i s : N e x t S te p

our questionnaire

… will be electronically available (DiaCoreWebpage, email)

... and can be filled out by those with a background in financing and project development

Any questions or comments ?

if not, then:

Is there a relevant policy design element/feature that is missing in our approach and that might have a high impact on the (un)certainty of revenues or expenditures ?

Do you agree that the penalty in an auction with sliding feed in premium disposes the highest uncertainty/risk to investors ?

Which other risks do you consider as relevant and are not addressed by our approach ?

P o l i c y I mp a c t An a ly s i s : D i s c u s s io n

http://www.diacore.eu/

More information: Contact Details:Coordinator WP 3:

Lucie Tesnière & Paul Noothout

Ecofys

E-mail: [email protected]

Robert Brückmann & Filip Jirouš

eclareon

E-mail: [email protected]

Barbara Breitschopf & Mario Ragwitz

Fraunhofer ISI

E-mail: [email protected]

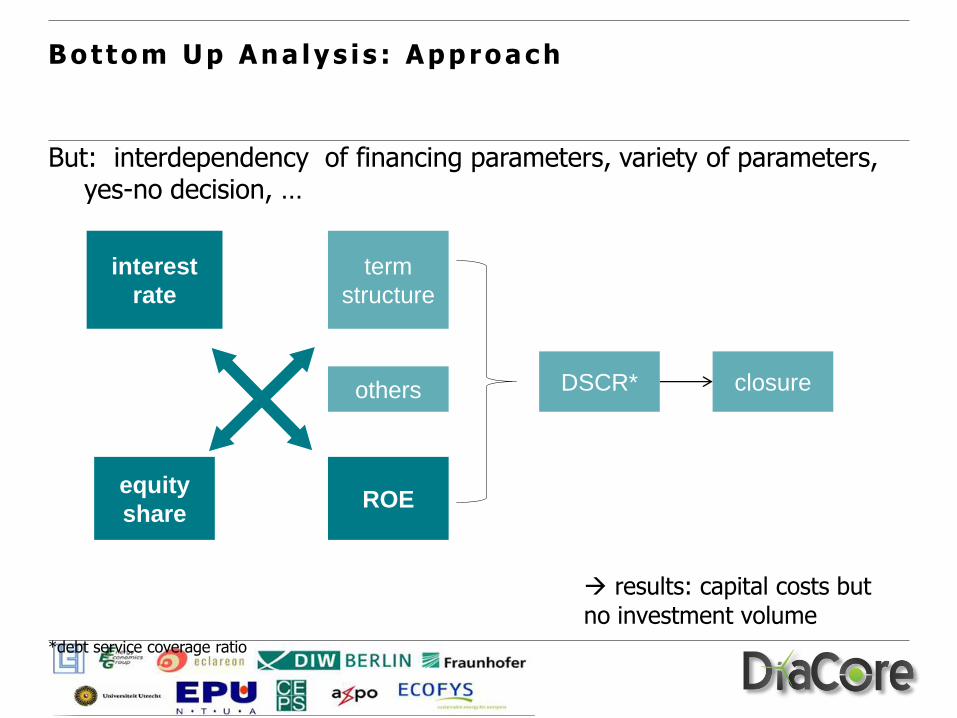

But: interdependency of financing parameters, variety of parameters, yes-no decision, …

results: capital costs but

no investment volume*debt service coverage ratio

B o t to m U p An a ly s i s : Ap p ro a c h

DSCR*

equity

share

term

structure

ROE

interest

rate

closureothers

theoretical model cost of equity and

debt, and risk margins (severity + frequency) under current policy, marketand country situations

top down analysis leads to adjustmentsof theoretical model results country

specific risk ranking and costs but nodirect relation between policy design and risk margins or rankings

bottom-up analysis links policies to risksand financing parameters

Wrap up: Approaches & Resu l t s

country riskprofiles

triple A policy

theoreticaldecomposition of costof equity and debt

significance ofbarriers/risk reflectsrisk margins

most relevant risksare „in“ policy design and changes

policy design changescan be transferredinto changes offinancial parameters

Approach Output Assumption

9