Embed Size (px)

Citation preview

This article was downloaded by: [Umeå University Library]On: 09 October 2014, At: 09:17Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number:1072954 Registered office: Mortimer House, 37-41 Mortimer Street,London W1T 3JH, UK

Development SouthernAfricaPublication details, including instructions forauthors and subscription information:http://www.tandfonline.com/loi/cdsa20

Financing municipal BOOTsin South Africa: Thelenders' perspectiveKaren Breytenbach a & Claudia Manning aa Project Manager, Private Sector InvestmentUnit , Development Bank of SouthernAfrica , MidrandPublished online: 27 Feb 2008.

To cite this article: Karen Breytenbach & Claudia Manning (1999) Financingmunicipal BOOTs in South Africa: The lenders' perspective, DevelopmentSouthern Africa, 16:4, 707-728, DOI: 10.1080/03768359908440109

To link to this article: http://dx.doi.org/10.1080/03768359908440109

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy ofall the information (the “Content”) contained in the publicationson our platform. However, Taylor & Francis, our agents, and ourlicensors make no representations or warranties whatsoever as to theaccuracy, completeness, or suitability for any purpose of the Content.Any opinions and views expressed in this publication are the opinionsand views of the authors, and are not the views of or endorsed byTaylor & Francis. The accuracy of the Content should not be reliedupon and should be independently verified with primary sources ofinformation. Taylor and Francis shall not be liable for any losses,actions, claims, proceedings, demands, costs, expenses, damages,

and other liabilities whatsoever or howsoever caused arising directlyor indirectly in connection with, in relation to or arising out of the useof the Content.

This article may be used for research, teaching, and private studypurposes. Any substantial or systematic reproduction, redistribution,reselling, loan, sub-licensing, systematic supply, or distribution in anyform to anyone is expressly forbidden. Terms & Conditions of accessand use can be found at http://www.tandfonline.com/page/terms-and-conditions

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

Financing Issues

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

Development Southern Africa Vol 16, No 4, Summer 1999

Financing municipal BOOTs in SouthAfrica: the lenders' perspective

Karen Breytenbach & Claudia Manning1

South Africa's first build-own-operate-transfer (BOOT) project for municipal serviceswas signed in late December 1998 by the city of Durban and a private project companyassociated with French conglomerate Vivendi. The project will treat waste water for saleto industrial customers who would otherwise use more expensive potable water in theirmanufacturing processes. The project structure, with its multiple contracts and supportingagreements, guarantees and complex shareholding relationships, represents a sophisti-cated analytical challenge for lenders, whose financing will ultimately be at risk in thedeal. Development finance institutions, such as the Development Bank of Southern Africa(DBSA), must review such projects in even greater detail because of their mandate topromote sustainable infrastructure development in the region. This article presents theDBSA 's analytical perspective on the Durban BOOT project in an effort to capture thecomplex, innovative and strongly developmental character of what, for South Africa, is aground-breaking public-private partnership project.

1. INTRODUCTIONOn 8 December 1998, the first long-term build-own-operate-transfer (BOOT)concession contract for municipal services provision was signed in South Africa.The 22-year contract was awarded to Durban Water Recycling (Pty) Ltd by theDurban Transitional Metropolitan Council. The project involves the rehabilita-tion, operation and maintenance of Durban's secondary treatment works. It in-cludes the design, construction, operation and maintenance of a new tertiarytreatment works that will treat domestic waste water for sale, as a substitute forpotable water, to high-volume water-consuming industries in the South DurbanIndustrial Basin. The rehabilitation and construction work, including the con-struction of a new reticulation system for the reclaimed water, will cost approxi-mately R72,3 million. All assets will be transferred back to the Durban Councilat the end of the concession period.

As a lending institution requested by the private partner to participate in the pro-ject, the Development Bank of Southern Africa (DBSA) has been obliged to re-view the merits of the deal carefully. The structure of the project, with its multi-ple contracts and supporting agreements, guarantees and complex shareholdingrelationships, represents a sophisticated analytical challenge for any lender

1 Both Project Managers, Private Sector Investment Unit, Development Bank of SouthernAfrica, Midrand.

707

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

K Breytenbach & C Manning

whose financing will ultimately be at risk in the deal. The DBSA's perspectiveon deals of this kind is even more detailed than that of commercial lenders orother participants because it is a South African development finance institutioncharged with supporting sustainable infrastructure development in the SouthernAfrican Development Community (SADC). As a result, the DBSA's analyticalchallenges in such a deal are formidable and the need to do full due diligence isparticularly important. This article presents key aspects of the DBSA's analyticalperspective on the Durban BOOT project in an effort to capture the complex,innovative and strongly developmental character of what, for South Africa, is aground-breaking public-private partnership project.

2. BACKGROUNDThe Durban metropolitan area is South Africa's second largest metropolitancomplex, with a population of 2,3 million in 1995, projected to reach 4,8 millionby 2011. During 1997, the area generated approximately R35,6 billion of grossgeographic product (GGP). This figure is 61 per cent of the GGP for KwaZulu-Natal and 6,7 per cent of the national gross domestic product (GDP).

The economic performance of the area is high relative to other metropolitan ar-eas in South Africa. For example, Durban's employment growth was the secondhighest of all South Africa's metropolitan areas in 1998. The diversity in theeconomy is a major strong point for the area and it is expected that the localeconomy will continue to outperform the national economy in the near future.

The industrial sector in this area is, however, along with the rest of South Africanindustry, undergoing severe restructuring in an attempt to become internationallycompetitive. As a result, jobs were shedded in certain manufacturing sectors. It isnevertheless perceived that the economic downswing has reached the bottom ofthe cycle, and the industrial sector is expected to begin showing positive signs inthe near future.

The BOOT project is located in the South Durban Industrial Basin, which is ex-periencing rapid rates of growth as a petrochemical and industrial complex. Anumber of international companies are considering locating in this subregionbecause of the strong profile of the existing industry.

Pursuant to provincial proclamations, the Durban Council has the responsibilityfor providing and operating bulk sewage purification works and disposal pipe-lines for the Durban metropolitan area. In November 1997, the council decidedto introduce private sector investment into the water sector. They invited tendersfor the taking over, modification, operation, management and maintenance of thesecondary treatment works, and the financing, design, construction, operation,management and maintenance of a tertiary treatment works and reticulation sys-tem.

The city pursued an open, competitive tendering process, with four bidders re-sponding with proposals. Omnium de Traitement et de Valorisation Societe

708

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

Financing municipal BOOTs in South Africa: the lenders' perspective

Anonyme (OTV France SA), a limited liability company registered in France anda subsidiary of the reputable international Vivendi Group, was announced aspreferred bidder. OTV France SA, as the project sponsor, registered a South Af-rican company, Durban Water Recycling (Pty) Ltd, which signed the BOOTconcession contract as the concessionaire with the council on 8 December 1998.

3. THE BOOT PROJECT

3.1 Concession contractThe BOOT agreement is a 22-year concession contract between Durban WaterRecycling (DWR) (variously referred to as the private partner, concessionaire orproject company) and the Durban Council (referred to as the public partner orimplementing agent). The core concession contract has two parts: the contractconditions and technical specifications. Incorporated is a conceptual design thattraces the production process from feed water characterisation, through each sub-sidiary process, to the water quality specification required by the principal cus-tomer. The latter is Mondi, a South African paper products manufacturer.

The contract specifies various phases:• The first phase after the signing of the contract allows 194 days for the fulfil-

ment of all suspensive conditions, including preparation of the preliminary de-sign. At the end of this period, the contract becomes fully effective and is for-malised by a commencement date. This period was extended to allow for thefinal negotiations of the many associated contracts.

• The next phase allows 20 months for construction, ending with the commis-sioning date when the concessionaire takes occupation of the redevelopedplant.

• The commissioning period lasts four months. At the end of this period, all testswill have been completed successfully and the plant will be ready to deliverthe quality and quantity of reclaimed water as per the concession contract.

• The first sales date occurs when reclaimed water is first delivered to the buyersand initiates the 20-year concession period.

• The defect liability period — the period during operations in which the con-tractor is liable for any defects in the plant and guarantees the output standardsof the plant - continues for 365 days after the first sales date.

The contract allocates to the concessionaire all the technical and operational risksfor design, construction and operation that are reasonably within its control. Avariety of mechanisms, standard in such contracts, are used to mitigate theserisks:

• The concessionaire provides a construction work performance guarantee ofR3,6 million for a period of one year from the first sales date.

• An operational performance guarantee, to the amount of R 1,8 million, willcome into force on the first sales date and last for not less than two years. Thisguarantee, which will ensure adequate performance of the operations, mainte-

709

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

K Breytenbach & C Manning

nance and management obligations, will then be renewed every two years,with its value increased in accordance with the Consumer Price Index. Theguarantee will be in place until three months after the end of the concessionperiod.

• Project assets will also be insured according to contract provisions, to ensurethat they remain in acceptable condition. Insurance will be to the satisfactionof the lenders. Public liability insurance for a minimum amount of R10 millionfor any one occurrence is required, as well as compliance with all legislation.

• To ensure against the possibility of default by the concessionaire on its loansor other key conditions of the contract, the contract makes provision for lenderstep-in rights, along with the right to appoint a substitute operating entity.

• To ensure against the possibility of a default by the Durban Council, or anysituation where it is impossible to appoint a substitute operating entity, thecontract makes provision for termination with certain financial consequencesthat will have a negative bearing on the party in default. If the contract is ter-minated prematurely, lenders will be paid outstanding debt service amounts(principal, interest and costs) by the Durban Council.

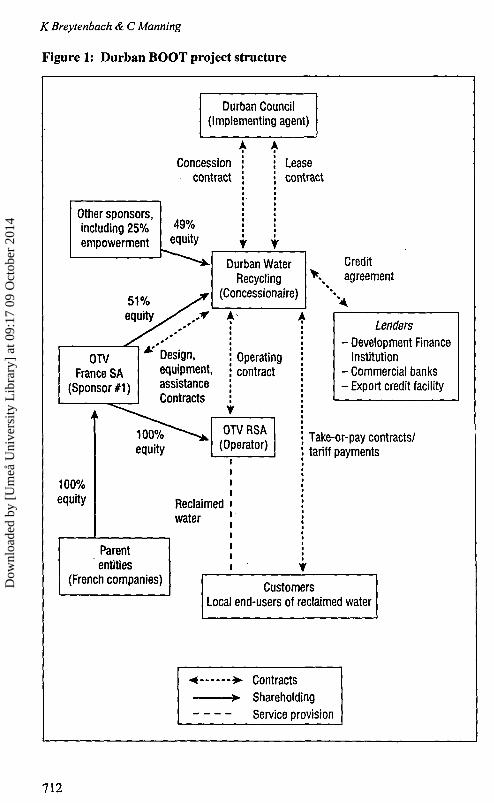

3.2 Supporting agreementsThe overall contract structure with its supporting agreements is complex, buttypical of such projects. The Durban Council has signed a concession contractwith DWR, the concessionaire. The concessionaire will enter into an operation,maintenance and management contract with OTV RSA Environment (Pry) Ltd, a100 per cent owned subsidiary of OTV France SA, which is the preferred bidderand principal project sponsor. The concessionaire will also enter into an engi-neering, procurement and construction contract with OTV RSA. The foreigndesign, equipment and technical assistance will be provided through two addi-tional contractual arrangements with OTV France SA.

The concessionaire will sign 'take-or-pay' water supply agreements with twolocal companies that will be customers for the reclaimed water, as well as withother customers when appropriate. Such contracts obligate payment whether ornot the reclaimed water is needed, or even used. OTV France SA will sign atechnical assistance agreement with their subsidiary, OTV RSA, to support it asthe contractor and operator. OTV France SA will also enter into a managementand technical services agreement with the concessionaire, as required by the con-cession contract. In addition, OTV France SA will enter into a sponsor supportagreement with the various lenders involved to ensure successful project com-pletion.

To summarise, DWR, as the concessionaire, has entered into or will enter into anumber of agreements, including the following:• Concession contract with the Durban Council• Operation, maintenance and management contract with OTV RSA, the opera-

tor

710

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

Financing municipal BOOTs in South Africa: the lenders 'perspective

• Turnkey, engineering, procurement and construction contracts with OTV RSA,the contractor

• Off-shore protocol contract with OTV France SA, the French supplier of for-eign design, equipment and technical assistance

• 'Take-or-pay' water supply agreements with Mondi and other local customersfor the reclaimed water

• Lease agreement with the Durban Council for the use of existing assets and thelease of sites

• Management and technical services agreement and sponsor support agreementwith OTV France SA

• Agreements with lenders to finance the project

Figure 1 illustrates the most significant of these agreements.

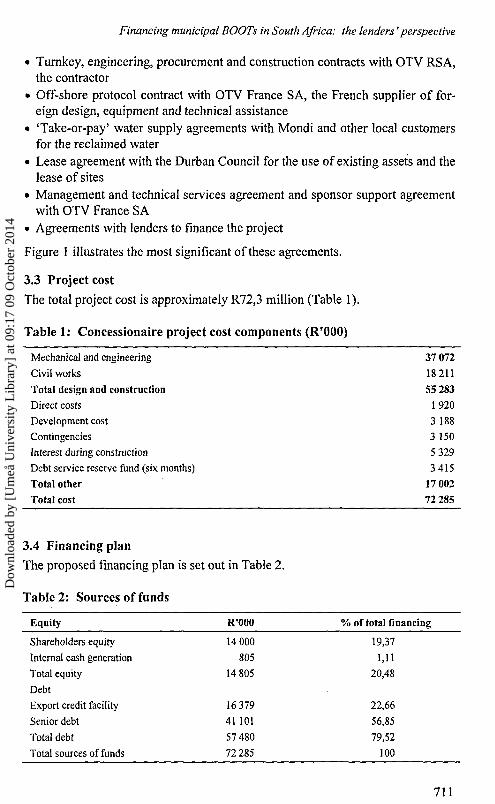

3.3 Project cost

The total project cost is approximately R72,3 million (Table 1).

Table 1: Concessionaire project cost components (R'000)

Mechanical and engineering 37 072

Civil works 18 211

Total design and construction 55 283

Direct costs 1 920

Development cost 3 188

Contingencies 3 150

Interest during construction 5 329

Debt service reserve fund (six months) 3 415

Total other 17 002

Total cost 72 285

3.4 Financing plan

The proposed financing plan is set out in Table 2.

Table 2: Sources of funds

Equity

Shareholders equity

Internal cash generation

Total equity

Debt

Export credit facility

Senior debt

Total debt

Total sources of funds

R'000

14 000

805

14 805

16 379

41 101

57 480

72 285

% of total financing

19,37

1,11

20,48

22,66

56,85

79,52

100

711

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

K Breytenbach & C Manning

Figure 1: Durban BOOT project structure

Durban Council(Implementing agent)

Other sponsors,including 25%empowerment

Concessioncontract

49%equity

Leasecontract

5 1 %equity

Durban WaterRecycling

(Concessionaire)

Creditagreement

OTVFrance SA

(Sponsor #1)

Design,equipment,assistanceContracts

Operatingcontract

100%equity

100%equity

Reclaimedwater

Parententities

(French companies)

Lenders- Development Finance

Institution- Commercial banks- Export credit facility

Take-or-pay contracts/tariff payments

CustomersLocal end-users of reclaimed water

-* *• ContractsShareholdingService provision

712

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

Financing municipal BOOTs in South Africa: the lenders 'perspective

The concessionaire approached the DBSA to provide a portion of the senior debtand to facilitate the extension to the project of an export credit facility madeavailable by the French government, pursuant to a protocol signed between theFrench government and the South African government in October 1995. Thefacility makes concessional funding available for the purchase of goods andservices from a French supplier. The balance of the required financing would beprovided by one or more South African commercial banks.

4. PROJECT APPRAISAL: THE DFI PERSPECTIVE

Durban's BOOT project is a natural candidate for funding from the DBSA, adevelopment finance institution with a mission to support infrastructure devel-opment in southern Africa. The project is consistent with several of the DBSA'smandates: it entails private sector investment in infrastructure through a public-private partnership; it involves investment in the water and waste water sector; itis also consistent with the South African government's policy of encouragingforeign investment and technology transfer.

Participation in such a project by a development finance institution like theDBSA is attractive to the other participants for a number of reasons:• First, the DBSA's relationship with the South African government provides the

foreign sponsor with a considerable degree of comfort, given concerns aboutpolitical and country risk issues.

• Second, the project's structure and integrity would be enhanced considerablythrough the DBSA's involvement. The project structure is complex and theSouth African market's experience with project finance is somewhat limited.The DBSA offers expertise in financing projects at the local government levelin South Africa.

• Third, the DBSA's commitment to the development and implementation ofpublic-private partnerships in municipal services, its strong relationships withSouth African municipalities, as well as its experience in the municipal sector,provide comfort for sponsors and lenders in the market.

These kinds of advantages are not, however, enough to ensure the DBSA's par-ticipation in such a project. As all government transfers to the Bank and guaran-tees on loans ceased in 1995, the DBSA has had to commercialise its operationsto a large extent. In order to exist without government subsidies, the Bank hashad to adopt a cost- and risk-based loan pricing system. This means that theBank's approach to project appraisal is similar to that of a commercial bank, withseveral additional requirements related to the DBSA's mandate to continue sup-porting projects with significant development implications. The elements ofthis appraisal process, as they apply to Durban's BOOT project, are outlinedbelow.

4.1 Assessment of development implications

The Durban BOOT project has a number of strong development implications of

713

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

K Breytenbach & C Manning

the kind that make it an appropriate candidate for the sort of financing providedby the DBSA:• The project will indirectly create additional local income during project con-

struction and operation. By reducing the production costs of industries whichpurchase the reclaimed water, the project will indirectly contribute to the eco-nomic growth of the region. The recycling of waste water will also contributeto the future saving of scarce water resources in South Africa.

• This project is the first investment in South Africa by the French firm,Vivendi, the parent company of the principal project sponsor. If successful, theproject is likely to lead to an expansion of Vivendi's portfolio in the country.

• The BOOT project clearly supports the Growth, Employment and Redistribu-tion (GEAR) strategy of the South African government, which aims to utiliseprivate sector investment to stimulate the economy. Although not a project ofmagnitude, its successful financial closure will send a positive message to theprivate sector and specifically to foreign companies interested in investing inthe water sector.

• Another strength of the project lies in its technology transfer. In terms of theconcession contract, Durban staff will receive annual training in the operationand management of the works, allowing the council to take over operation ofthe works at the end of the concession period, or in the event of termination ofthe concession contract.

• The project also benefits the local engineering community and other local con-sultants working with the sponsor and concessionaire during the design, con-struction and implementation phases.

• The composition of the concession company increases the wealth redistribu-tion impacts of the project. Empowerment companies hold 25 per cent of theshares and the concessionaire has decided to employ an empowerment firm asthe main contractor for the construction phase.

• The concessionaire will provide assisted education for three students from thesurrounding community to study at an approved technikon in a scientific disci-pline associated with the management and treatment of water and waste water.In addition, the concessionaire will offer practical training and experience asrequired by the relevant curriculum.

• The project will create 15 direct jobs during the operational phase. The conces-sionaire has committed itself to sourcing a proportion of these jobs from thelocal community, depending on its skills profile.

• Finally, the project involves strong environmental benefits. By substitutingtreated water for potable water, the project allows potable water to be con-served for alternative uses.

4.2 Assessment of the project sponsorThe sponsor, OTV France SA, is a wholly owned French subsidiary of the inter-national OTV Group, which operates in the water and waste water sector. The

714

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

Financing municipal BOOTs in South Africa: the lenders' perspective

OTV Group is, in turn, a wholly owned subsidiary of Compagnie Générale desEaux, ultimately wholly owned by the French conglomerate, Vivendi. Vivendi isinvolved in water, energy, waste management, transport, communications, con-struction, property and utilities. The OTV Group, as the leading Vivendi subsidi-ary in the field of water treatment engineering, operates worldwide, either di-rectly or through its subsidiaries.

OTV France SA was established in 1933 and has two business interests: the con-struction of water treatment works and the operation of public utilities. In 1997,the OTV Group's total assets amounted to FF4 billion. Operating income forOTV France SA was FF1,7 billion of the OTV holding group's consolidatedincome of FF3,1 billion. This income was split 51:48 between France and the 20other countries in which it conducts business (including Egypt, Turkey, Braziland Malaysia). Over the past ten years, the OTV Group has built or refurbished130 potable water treatment works and 200 waste water treatment facilities inFrance and internationally. In 1996 it was operating 50 waste water treatmentworks in France, serving 11 million people. The 1997 consolidated balance sheetand income statement of Compagnie Generale des Eaux indicate total assets ofFF258,2 billion and a turnover of FF 167,1 billion.

OTV France SA has a 51 per cent shareholding in DWR, the concessionaire, andfully owns OTV RSA, the contractor and operator. OTV France SA will providesponsor support for project completion. OTV RSA will provide the concession-aire with a construction works performance guarantee to the amount of 12,5 percent of the total design and construction costs from a financing institution ac-ceptable to the lenders. An operational performance guarantee, to the amount ofRl,8 million, adjusted annually in line with tariff adjustments, will be availablefrom OTV RSA to the concessionaire. A management and technical assistancesupport agreement and a sponsor support agreement are to be finalised to thesatisfaction of the lenders.

The sponsor support agreement will include the following provisions:• Technical and financial commitment to the successful construction and opera-

tion of the works through performance guarantees• The existence of formal support through a management and technical assis-

tance support agreement for the duration of the contract period• The sponsor support for project completion• The structure of the proposed security package for the loans

4.3 Assessment of the public partner

The implementing agent, or public partner, is the Durban Transitional Metro-politan Council, a local government with an experienced and stable managementteam. The council has a strong financial profile with high liquidity levels. Theexistence of a strong tax base, the relative strength and diversified nature of thelocal economy, and the positive indications of future economic growth and for-

715

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

K Breytenbach & C Manning

eign direct investment, have all contributed to the strong credit ratings given tothe city by a variety of credit rating agencies.

An expected increase in debt levels, however, has contributed to a lowering of itscredit assessment from 7 in 1997 to 6 in 1998 on a 10-point scale used by thecredit rating agency, CA-Ratings (CA-Ratings, 1999). Based on 1998 informa-tion, the credit rating agency Duff and Phelps Credit Rating Company has classi-fied the city as a very strong local authority with a security class short-termcredit rating of D-1 ('very high certainty of timely payment') and a long-termrating of AA- ('very high credit quality') (Duff & Phelps, 1999).

The BOOT project falls under the leadership of the Executive Director of theDurban Council's Water Services and a team of experienced staff who are wellregarded for their efficiency in the municipal water sector. The concession con-tract makes provision for the role of a special council representative who will beresponsible for monitoring the concession contract by, firstly, ensuring that theassets are constructed, maintained and operated in a manner that achieves theobjectives of the concession without interfering in the performance of the worksand, secondly, by ensuring that at the end of the concession period the value ofthe assets to be transferred back to the Durban Council will have been fully re-tained. The council appears to appreciate the benefits of the concession process,as well as the consequences of termination.

4.4 Assessment of the concessionaire

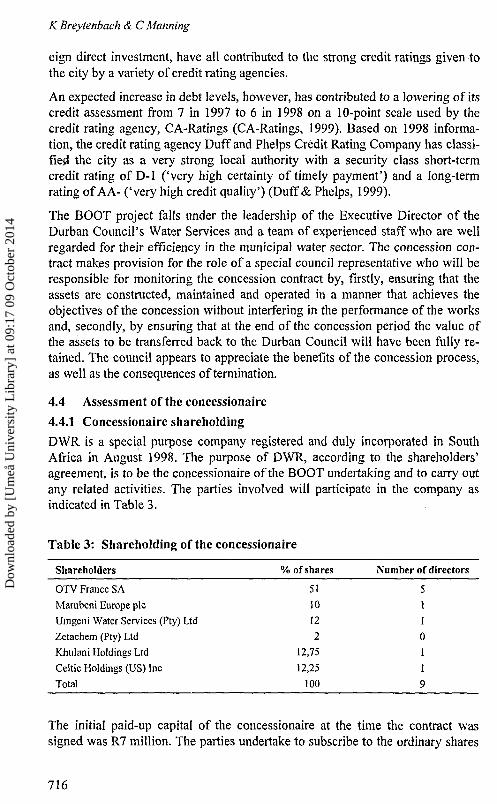

4.4.1 Concessionaire shareholding

DWR is a special purpose company registered and duly incorporated in SouthAfrica in August 1998. The purpose of DWR, according to the shareholders'agreement, is to be the concessionaire of the BOOT undertaking and to carry outany related activities. The parties involved will participate in the company asindicated in Table 3.

Table 3: Shareholding of the concessionaire

Shareholders

OTV France SA

Marubeni Europe plc

Umgeni Water Services (Pty) Ltd

Zetachem (Pty) Ltd

Khulani Holdings Ltd

Celtic Holdings (US) Inc

Total

% of shares

51

10

12

2

12,75

12,25

100

Number of directors

51

1

0

11

9

The initial paid-up capital of the concessionaire at the time the contract wassigned was R7 million. The parties undertake to subscribe to the ordinary shares

716

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

Financing municipal BOOTs in South Africa: the lenders' perspective

in the company in the ratios set out above, before the commencement date, toensure that all equity contributions will be fully paid up by that time. The share-holders' agreement makes provision for an undertaking from all shareholders toprovide a standby equity facility to the amount of R999 999.

4.4.2 Capacity and experience

The concessionaire will not have a large staff complement because the construc-tion and operating functions will be subcontracted to OTV RSA, which will re-ceive the necessary staff, technical and financial support from OTV France SA.The concessionaire will have a managing director whose work record indicatesconsiderable experience in water and sewage treatment concessions, and he orshe will be the company's representative for the various contracts associatedwith the concession. In terms of the management and technical services agree-ment, OTV France SA will provide technical back-up for the concessionaire viathe operator, OTV RSA.

4.5 Market assessment: demand for reclaimed water

The BOOT project is located in an area with high economic growth rates. Thestrength of the project lies in the price of reclaimed water vis-a-vis the price ofpotable water to industry. The price of reclaimed water, based on a sliding scalelinked to consumption, will ensure a saving of at least R0,73/m3. This representsa saving of approximately 28,8 per cent on the price of potable water. The gapbetween the price of water purchased from the concessionaire and that of potablewater is also likely to increase substantially in the future, in the light of the gov-ernment's new national water policy requiring that the real cost of water bepassed on to end-users. The widening of this price gap, along with the conces-sionaire's marketing of the reclaimed water option, is likely to expand the con-cessionaire's customer base significantly.

To ensure demand for most of the reclaimed water to be produced, the conces-sionaire has entered into two take-or-pay water supply agreements with end-usercompanies. The larger agreement is with paper producer Mondi, which is locatedimmediately adjacent to the existing secondary treatment facility. In terms of thisagreement, Mondi will purchase all of its operational water requirements exclu-sively from the concessionaire. Mondi's expected future water requirement isconservatively estimated at 32 megalitres a day. The Mondi take-or-pay watersupply agreement stipulates that it will pay for 30 Ml/day, for the duration of theconcession period, regardless of whether or not it actually needs or takes thisvolume. A similar agreement with another local company is being concluded, interms of which the company will pay for 3,3 Ml/day for 15 years, regardless ofwhether or not it uses that volume. A total of 33,3 Ml/day of the concessionaire'sproduction capacity of 47,5 Ml/day has thus been contractually sold. Other pro-spective customers have also been identified.

717

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

K Breytenbach & C Manning

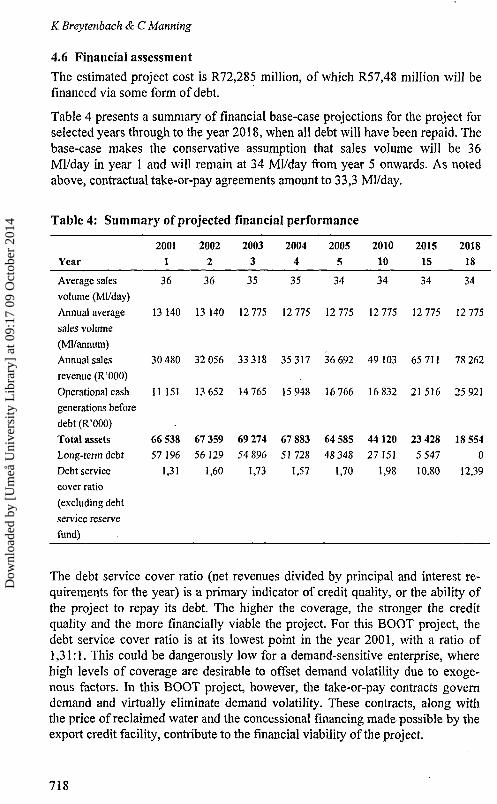

4.6 Financial assessment

The estimated project cost is R72,285 million, of which R57,48 million will befinanced via some form of debt.

Table 4 presents a summary of financial base-case projections for the project forselected years through to the year 2018, when all debt will have been repaid. Thebase-case makes the conservative assumption that sales volume will be 36Ml/day in year 1 and will remain at 34 Ml/day from year 5 onwards. As notedabove, contractual take-or-pay agreements amount to 33,3 Ml/day.

Table 4: Summary of projected financial performance

Year

2001 2002 2003 2004 2005 2010 2015 2018

1 2 3 4 5 10 15 18

Average sales

volume (Ml/day)

Annual average

sales volume

(Ml/annum)

Annual sales

revenue(R'000)

Operational cash

generations before

debt (R'000)

Total assets

Long-term debt

Debt service

cover ratio

(excluding debt

service reserve

fund)

36 36 35 35 34 34 34 34

13 140 13 140 12 775 12 775 12 775 12 775 12 775 12 775

30 480 32 056 33 318 35 317 36 692 49 103 65 711 78 262

11 151 13 652 14 765 15 948 16 766 16 832 21516 25 921

66 538 67 359 69 274 67 883 64 585 44120 23 428 18 554

57 196 56 129 54 896 51728 48 348 27 151 5 547 0

1,31 1,60 1,73 1,57 1,70 1,98 10,80 12,39

The debt service cover ratio (net revenues divided by principal and interest re-quirements for the year) is a primary indicator of credit quality, or the ability ofthe project to repay its debt. The higher the coverage, the stronger the creditquality and the more financially viable the project. For this BOOT project, thedebt service cover ratio is at its lowest point in the year 2001, with a ratio of1,31:1. This could be dangerously low for a demand-sensitive enterprise, wherehigh levels of coverage are desirable to offset demand volatility due to exoge-nous factors. In this BOOT project, however, the take-or-pay contracts governdemand and virtually eliminate demand volatility. These contracts, along withthe price of reclaimed water and the concessional financing made possible by theexport credit facility, contribute to the financial viability of the project.

718

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

Financing municipal BOOTs in South Africa: the lenders 'perspective

To provide a small additional cash cushion against unanticipated, temporaryshortfalls in revenue, the concessionaire is required to maintain a 'debt servicereserve fund' equivalent to six months' worth of debt service costs.

4.7 Technical assessment

4.7.1 Technical overview

The concession contract gives the concessionaire the exclusive right to develop arecycling works for the production of reclaimed water, to be sold to high waterconsuming industries on a take-or-pay basis. This process will involve modifyingan existing secondary treatment facility and building a new tertiary treatmentworks and reticulation system.

The inflow consists of feed water from two city trunk sewers. The effluent passesthrough the primary treatment works where screening, degritting and primarysettling takes place, after which it becomes the influent to the activated sludgetreatment process at the secondary treatment works. A unique process train fol-lows at the tertiary treatment works, dealing with a specific effluent and takinginto account the variations in the feed water and the high quality specificationsfor the reclaimed water. Elements of the treatment process are proprietary toOTV France SA and, although the technology is new to South Africa, it has beentried and tested in numerous works elsewhere in the world.

4.7.2 Quantity of influent

The works will derive influent primarily from the trunk sewer that drains an ad-jacent - mainly residential - area. It can be supplemented by influent from a sec-ond trunk sewer but, because this is primarily industrial sewage, it is of an infe-rior quality for the purposes of reclamation. Some of it can be blended with thedomestic sewage, but the maximum blending ratio has been set at 85:15 to allowthe reclaimed water to meet the specification of the customers. The concessiondocuments present a statistical analysis of the flow records for several years.Using these, the nominal plant capacity has been optimised using a mathematicalmodel of the hydraulics needed to achieve a balance between construction costand standby capacity.

Deficiencies in short-run influent quantities are mitigated by

• the provision of storage in the system• blended use of the industrial influent• blended use of potable water purchased from the city at a discounted price in-

cluded in the concession contract.

Sufficient influent will always be available, but the use of potable water forblending has cost implications. These, in turn, are mitigated by the discountedprice provisions in the concession contract.

719

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

K Breytenbach & C Manning

4.7.3 Quality of influent

The quality of the influent, even from the domestic source, may vary and henceaffect the effectiveness and efficiency of the works in satisfying the specifica-tions for reclaimed water. The concessionaire has studied the influent quality andincorporated the results into the process design. As for quality deficiencies, poorquality influent could be blended with potable water to ensure the continuance ofplant operations. Provision is made for this in the concession contract. The watersupply agreements make provision for proven material increases in variabletreatment costs caused by the deterioration of the quality of feed water to bepassed on to customers in the price of reclaimed water.

4.7.4 Technical capacityThe technical capacity to implement the works resides in OTV France SA. Thesponsor support agreement and terms of the procurement contracts ensure thatthis capacity is available to the concessionaire. Local design work will be doneby a reputable local firm. The civil construction work has been subcontracted ona fixed-price, turnkey basis to a firm with considerable experience in water andwaste water treatment works, including previous work on the project site. Theconceptual designs for the electrical, mechanical and control instrumentationwork were prepared by OTV France SA, and the actual work will be subcon-tracted on a fixed-price, turnkey basis.

4.7.5 Design

The process design incorporates a number of elements that will be used in SouthAfrica for the first time, although they are well established internationally. Froma process point of view, the plant is reasonably flexible and conservatively de-signed. It should be able to meet the reclaimed water specifications, includingany variations that can reasonably be expected, given the substantial knowledgeabout the influent.

4.7.6 Implementation programme

The concession contract includes a preliminary implementation programme,which has subsequently been refined and extended in consultation with the vari-ous contractors, including suppliers of plant elements that will be procured off-shore. The contracts provide financial incentives for early completion and penal-ties for late completion. There are no apparent reasons why the project shouldnot be completed in the 20 months allowed by the programme.

4.7.7 Implementation costs

As the procurement contracts are for a fixed price, cost risks are transferred tothe contractors. Increased payments could be claimed in the events of force ma-jeure, unforeseen circumstances and material variations ordered by the conces-sionaire. The thoroughness of the preparation appears to have kept this risk to aminimum.

720

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

Financing municipal BOOTs in South Africa: the lenders 'perspective

4.8 Environmental assessment

An environmental assessment, which included public participation, was carriedout in accordance with national environmental regulations and the requirementsof the KwaZulu-Natal's Department of Traditional and Environmental Affairs.The provincial department determined, on the basis of a preliminary report, that amore extensive environmental impact assessment report would not be required.

As noted above, the project contains strong environmental benefits. By substi-tuting treated water for potable water, the project allows potable water to be con-served for alternative uses.

4.9 Assessment of social and labour issues

As part of the environmental review, local communities were surveyed regardingtheir reactions to the project. Community support appears to be strong, with theproject being viewed both as a generator of much-needed jobs and a vehicle forthe transfer of skills to local communities.

The concessionaire has committed itself to, firstly, using the workforce of thesurrounding community, secondly, supporting the tertiary education of three stu-dents and, thirdly, carrying out activities that promote affirmative action andempowerment of previously disadvantaged groups. To successfully achieve theseobjectives, the concessionaire has committed itself to establishing a steeringcommittee, comprised of representatives of community organisations, the con-cessionaire and the Durban Council, to address issues of concern to the localcommunity during the life of the project. The DBSA will assist in establishingthis structure, given that it will play an instrumental role in monitoring the con-cessionaire's observance of key social issues. Organised labour has also ex-pressed support for the project.

4.10 Legal and regulatory assessment

4.10.1 Enabling legislation

The Water Services Act (Act 108 of 1997) is the enabling legislation that entitlesthe city to award this concession. The Durban BOOT project avoids some regu-latory problems affecting other municipal public-private partnerships in SouthAfrica because the tariff agreed to as part of this contract is for reference pur-poses only. The industrial customers have independently negotiated the price ofreclaimed water with the concessionaire. The concession contract that serves asthe base document for the concessionaire's undertaking of the project is a legallyvalid document and is fully enforceable.

4.10.2 Project contracts

The concession contract is the primary document from which the concession-aire's rights and obligations flow. The concessionaire is a special-purpose vehi-cle company, duly registered under South African law and consisting of a consor-tium of shareholders. Since the concessionaire does not have all the expertise to

721

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

K Breytenbach & C Manning

carry out its obligations, it has contracted out various specific functions supportedby appropriate performance guarantees from OTV France SA and OTV RSA.

Given the contractual structure, the various project risks appear to have beenallocated to parties best positioned to mitigate them, with appropriate sponsorsupport arrangements where applicable. The structure of the agreements is typi-cal of this type of contractual arrangement and the lenders have satisfied them-selves that the contractual arrangements have been concluded on an arm's-lengthbasis.

4.10.3 Concession agreement

The concession agreement contains customary provisions, as outlined above. It isa 22-year contract that gives the concessionaire the exclusive right to produceand sell reclaimed water. The council is given supervisory powers to monitor thetechnical performance of the concessionaire, who must also provide constructionworks and operational performance guarantees to support its performance un-dertakings. The concessionaire leases the existing assets from the city and un-dertakes to insure all the assets for their full replacement value with annuallyescalated premiums. The tariff will be renegotiated at intervals of five years bytaking into account the full cost of supplying reclaimed water. In order to preparefor the end of the concession and the resumption by the city of the water serv-ices, the concessionaire will procure a non-exclusive licence for the city for theuse of the technology and know-how, and will implement an annual trainingprogramme for designated city employees.

In the event of default by the concessionaire, the lenders have the right to appointa substitute entity or terminate the project. On termination, including a forcemajeure termination, the lenders will be compensated by the city for the full out-standing debt and, in turn, the city will retain ownership of the project assets.Disputes will be settled through arbitration under South African law.

4.10.4 Supporting project agreements

In addition to the agreements cited above, the following supporting projectagreements have been reviewed by lenders and found to be generally acceptable:• Articles and memorandum of association of the concessionaire• Signed shareholders' agreement• Draft operation, management and maintenance agreement between the conces-

sionaire and OTV RSA• Draft take-or-pay water supply agreements to be concluded by the concession-

aire and local customers for reclaimed water• Notarial deed of lease• Intercreditor agreement between the lenders• Engineering procurement construction contract• Foreign design, equipment supply and technical assistance agreements

722

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

Financing municipal BOOTs in South Africa: the lenders' perspective

4.10.5 Project completion

OTV RSA's obligations to construct the plant will be backed by OTV France SAthrough parent company guarantees. The sponsor support agreement undertakenby OTV France SA will provide guaranteed project completion.

5. SUMMARY OF RISKS, RISK ALLOCATION AND MITIGATION

5.1 Participants' riskThe sponsor is a reputable, international company with a strong balance sheetand a commitment to the development of new business opportunities in the Dur-ban area and the region.

The implementing agent, or public partner, is a strong, well-managed localauthority, committed to the successful implementation of public-private partner-ships. The concession has substantial benefits for the Durban Council, as well asfinancial penalties on termination for the party in default.

The sponsor is the majority shareholder in a group of shareholders respected bythe market. The shareholders' agreement stipulates that the full equity contribu-tion from each shareholder will be paid into a special account by the com-mencement date. The participants' risk is regarded as low.

5.2 Design, construction and operating risk

• Design and construction risk: The sponsor carried out detailed research and astatistical analysis as input into the design process. The sponsor guarantees thatthe performance of the equipment will be in accordance with the design speci-fications, so as to meet the obligations of the contractor, as well as to ensurethat the equipment will remain in good working condition until the end of thedefect liability period. Construction completion risk is mitigated by a fixed-price, turnkey contract for the engineering, procurement and constructionworks associated with the project. Sponsor support for project completion willbe available.

• Operating risk: Operating risk is mitigated by a contract with the operator foroperation, management and maintenance. The operator will be responsible forproviding the concessionaire with an operating performance bond. Provisionsfor adequate insurance, as well as liquidated damages, are included in the con-tract.

• Quantity and quality of influent risk: The risks associated with feed waterquantity and quality have been mitigated by a storage facility and the avail-ability of potable water for blending at a discounted price from the DurbanCouncil. The risks of deviation from the required quality and quantity havebeen somewhat mitigated by detailed studies of the influent over time. Theselling price of the reclaimed water will be calculated based on the price ofpotable water to industrial customers. Proven material variations to the treat-ment cost, due to deterioration of influent, will be passed through to the take-

723

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

K Breytenbach & C Manning

or-pay customers. Design, construction and operating risks, including thequality and quantity of influent risk, are regarded as low.

5.3 Technology risk

The technology used by the concessionaire is guaranteed by the sponsor to de-liver the specific quality and quantity standards as required by the concessioncontract. The sponsor is a well-known international operator; the bidding andselection processes used to select the sponsor were competitive and fair. Tech-nology risk is regarded as low.

5.4 Market riskTake-or-pay water supply agreements have been negotiated to the satisfaction ofthe lenders. The available off-take is expected to be higher than the contractualtake-or-pay volumes. Although additional off-take agreements have not beenconcluded, the project is in an area of anticipated economic growth and severalpotential additional local customers have been identified. The expected gap inthe price between the price of potable water to industries, and the price of re-claimed water, will ensure interest from the market. Market risk is regarded aslow.

5.5 Environmental risk

As indicated above, all environmental review procedures have been followed.Government officials charged with reviewing these findings have confirmed thatthe environmental risks associated with the project are regarded as low.

5.6 Termination riskSubstantial benefits will accrue to all parties to the concession agreement. In theevent of termination, the party in default will suffer material financial penalties.If premature termination occurs, lenders will be compensated by the DurbanCouncil, which is regarded as a financially strong local authority. Terminationrisk is regarded as low.

6. LEGAL PROTECTION FOR LENDERSFor the appraisal reviewed above to be meaningful, the overall deal as describedmust be accurately formalised in various agreements. The agreements must in-clude guarantees by the concessionaire, as borrower, that it will do (or not do)various things pursuant to these agreements. Such guarantees are essential toaccessing lender finance.

In one sense, assessing the sort of guarantees that a concessionaire is willing tomake is another aspect of project appraisal, and belongs among the list of ap-praisal categories presented above in Section 4. Because this sort of analysis maybe appropriately thought of as the final step in the process, from a lender's pointof view, these factors are presented here as a concluding section.

724

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

Financing municipal BOOTs in South Africa: the lenders' perspective

Three principal legal mechanisms for ensuring lender protection will be negoti-ated with the borrower on the Durban BOOT project. They are outlined belowand discussed in the following subsections:

• Security packages include assets or property pledged as collateral to be takenover by the lenders in the event of default, or third-party guarantees to makegood on an obligation if the concessionaire defaults.

• Covenants are pledges by the borrower in a loan agreement to do certain thingsand refrain from doing others. Failure to perform accordingly may cause thelender to accelerate the loan repayments or demand full payment of the loan.

• Conditions precedent, as used in the loan agreements associated with this pro-ject, are specific tasks that must be completed before lenders will make actualdisbursements.

For the Durban BOOT project, the following is a selection of the kinds of legalprotection mechanisms that lenders will insist on.

6.1 Security package

The concessionaire, as the borrower, will be required to pledge the followingkinds of security for its bank loans:

• A first-ranking mortgage bond registered on the lease in respect of the proj-ect's immovable property

• A general notarial bond registered over all of the borrower's movable assets• A special notarial bond over plant and equipment• Assignment to the lenders of all the borrower's rights, title and interest in

- the project documents- all insurance taken out by the borrower (other than third-party liability in-

surance)- all other claims (including all leases, licences and operating agreements, as

well as all supply agreements and contracts to which it may be a party) andrevenues of the borrower against its clients and customers, present and fu-ture

- all project accounts• A pledge of the shareholders' shares in the borrower (except for the sponsor's

shares)• A guarantee that repayment to lenders will take priority over repayment of all

shareholders' loans and/or claims to the borrower• A golden share issued by the borrower to the lenders, which will give the lend-

ers voting rights in the event of default

6.2 Key covenants

6.2.1 Positive covenants

The borrower will undertake to do the following:

725

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

K Breytenbach & C Manning

• Comply with all of its obligations described in the project documentation.• Procure the operational performance bond, pursuant to the operation, mainte-

nance and management contract.• Pay all amounts under the project documentation and all taxes.• Obtain and maintain insurance covering risks, on terms approved by the lend-

ers.• Obtain and maintain all necessary consents, licences, etc.• Provide access by the lenders and their advisers to its site, and all books and

records.• Maintain key personnel and an organisational structure to the reasonable satis-

faction of the lenders.• Comply with all applicable laws, environmental regulations and occupational,

health and safety laws.• Prepare an environmental management plan.• Ensure Y2K compliance.• Comply with the employment equity laws.• Participate in the appropriate consultative structures with local stakeholders.

6.2.2 Negative covenants

The borrower will undertake not to do, permit or allow the following without thelender's consent:• Amend or vary any project document.• Terminate, suspend or cancel any of the project documents.• Create any security interest or other encumbrance on any of its undertakings,

business, assets or revenues other than under the security documents.• Dispose of the whole or any part of its property, assets or revenues.• Incur any indebtedness other than under the loan documents.• Carry on any business other than as contemplated by the project documents

and loan documents.• Modify in any material aspect the rights attaching to its share capital or share-

holders' loans, or apply for public listing of its shares.• Enter into any related party transaction unless such transaction is on arm's-

length commercial terms.• Encumber any of its assets.• Pay dividends and/or shareholders' subordinated loan interest, management

fees or capital- until the commissioning date has been reached- unless the debt service reserve account is fully funded- until all capital and interest payments for that period have been made to the

lenders.

726

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

Financing municipal BOOTs in South Africa: the lenders 'perspective

6.3 Conditions precedent for the first disbursement

The lenders will disburse the first tranche of their loan to the concessionaire onlyafter the following conditions have been met:

• All documentation, including all corporate documents, is in full force and ef-fect, and to the satisfaction of the lenders.

• Insurance has been taken out in accordance with a previously agreed-uponschedule of insurance.

• Satisfactory evidence has been produced that all necessary consents, authori-sations, permits, licences and approvals have been granted or issued by thecompetent authorities.

• Satisfactory opinion from the lenders' legal adviser has been obtained.• Satisfactory opinion from the borrower's legal adviser has been obtained.• The annual debt service cover ratio and other financial ratios have been agreed

upon.• Satisfactory proof has been submitted to the lenders as to the organisational

and management structure of the borrower.• A certificate has been received from the borrower's auditors stating that the

borrower has no liabilities or encumbrances immediately prior to financial clo-sure.

• All project accounts are open and proceeds assigned to lenders.• A satisfactory opinion has been received from a tax adviser confirming expec-

tations regarding the tax treatment of the borrower.• The aggregate amount disbursed on the facilities does not cause the project

debt equity ratio to exceed 80:20 as of financial closure.• All fees due to the lenders have been paid.• French export credit facility has been fully approved and is operational.

7. CONCLUSION

Worldwide, the BOOT approach offers a particularly attractive alternative togovernment entities whose financial resources cannot meet their capital con-struction needs. BOOT and its variants provide the means for overcoming thisconstraint while simultaneously encouraging the inflow of technology and ex-pertise, particularly in the operation and maintenance of major capital-intensiveinfrastructure sectors. Today, many countries in the developed and developingworlds promote this form of privately owned and operated infrastructure project,financed on a non-recourse basis under a concession-type arrangement.

The Durban BOOT project is the first major example of this approach in SouthAfrica. It illustrates the complexity of such deals, as well as many of their devel-opmental benefits. This project also illustrates the challenges facing lenders inproviding financing for such deals. The long and detailed appraisal process thatmust be carried out in order to assure lenders that such deals are viable, is new tothe South African banking community, particularly to commercial banks. As

727

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014

K Breytenbach & C Manning

budget constraints continue to impact on local government operations in thecountry, however, these deals are likely to be considered more frequently, alongwith other forms of public-private partnerships. As that happens, the DurbanBOOT should serve as a useful case study of the circumstances and conditionsunder which such arrangements are most appropriate.

REFERENCES

CA-RATINGS, 1999. Assessment of South African local governments. Johan-nesburg: Credit Agency Ratings.DUFF & PHELPS, 1999. Annual Local Government Bulletin. Johannesburg:Duff & Phelps Credit Rating Company of Southern Africa (Pty) Ltd.

728

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

09:

17 0

9 O

ctob

er 2

014