Embed Size (px)

Citation preview

Financing Entrepreneurial Ventures

William D. BygraveBabson College

GEM2004 ConferenceLondon Business School

January 20, 2005

Copyright © 2005 Babson College & London Business School

Sources of startup financing

• Entrepreneurs themselves

• Informal investors

• Venture capitalists

Prevalence Rate of Informal Investors, Adults 18-99 years old

0.00

5.00

10.00

15.00

20.00

25.00Br

azil

Cro

atia

Japa

nPo

rtuga

lN

ethe

rland

sU

KBe

lgiu

mFr

ance

Pola

ndH

unga

rySl

oven

iaSw

eden

Gre

ece

Italy

Sing

apor

eSp

ain

Hon

g Ko

ngIre

land

Isra

elAu

stra

liaD

enm

ark

Arge

ntin

aFi

nlan

dC

anad

aG

erm

any

Sout

h Af

rica

Nor

way

USA

New

Zea

land

Icel

and

Ecua

dor

Peru

Uga

nda

Jord

an

Pre

vale

nce

rate

, pe

rcen

t of

adu

lts

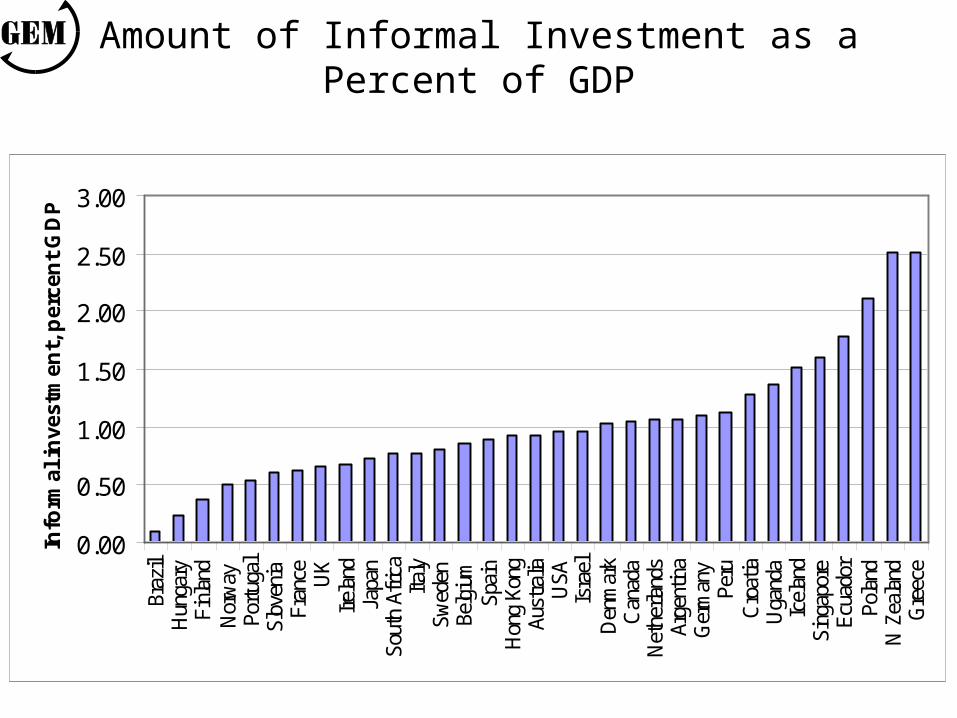

Amount of Informal Investment as a Percent of GDP

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Braz

ilH

unga

ryFi

nlan

dN

orw

ayPo

rtuga

lSl

oven

iaFr

ance UK

Irela

ndJa

pan

Sout

h Af

rica

Italy

Swed

enBe

lgiu

mSp

ain

Hon

g Ko

ngAu

stra

liaU

SAIs

rael

Den

mar

kC

anad

aN

ethe

rland

sAr

gent

ina

Ger

man

yPe

ruC

roat

iaU

gand

aIc

elan

dSi

ngap

ore

Ecua

dor

Pola

ndN

Zea

land

Gre

ece

Info

rmal

inve

stm

ent,

per

cen

t G

DP

Annual Amount per Informal Investor vs GDP per Capita, US$

y = 0.3558x1.0234

R2 = 0.7785

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

0 10,000 20,000 30,000 40,000 50,000 60,000GDP per Capita, US$

An

nu

al a

mo

un

t p

er i

nfo

rmal

in

vest

or,

US

$

NO

USA

DK

IE

JPNL

IS

SE

UK

BE

FI

FRDE

CA

IT

AU

HK

NZ

SG

GR

ILPT ES

SI

HR

PL

HU

JO

SAAR

BRPEUG

EC

R2 is the proportion of the variation that is explained by the trend line. An R2 of .7785 indicates that 77.85% of the variation in annual amount per informal investor is explained by GDP per capita.

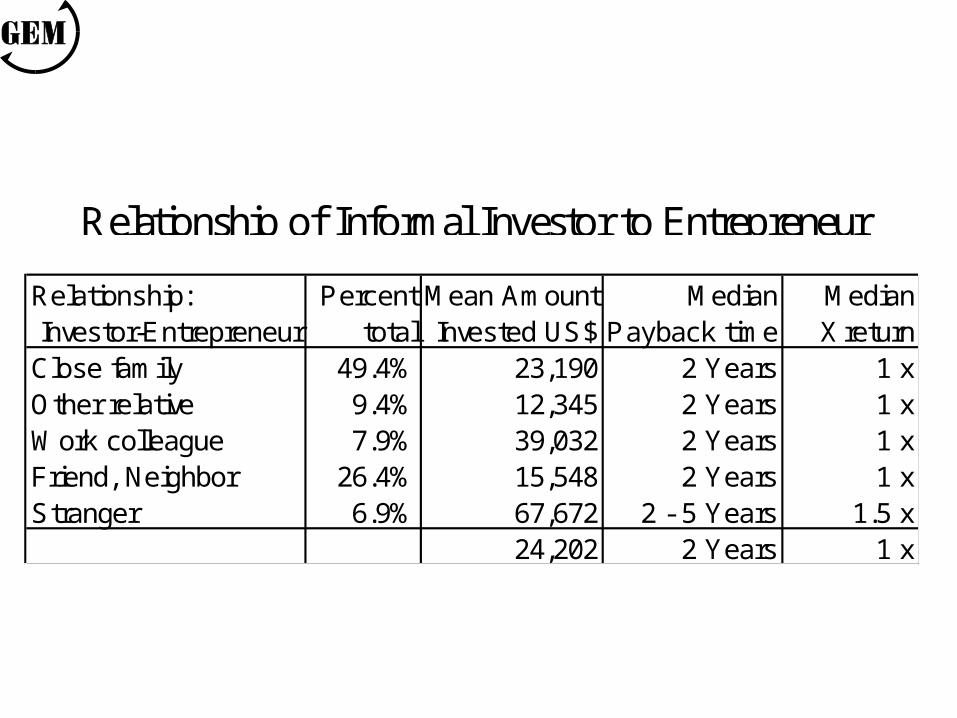

Relationship: Percent Mean Amount Median MedianInvestor-Entrepreneur total Invested US$ Payback time X return

Close family 49.4% 23,190 2 Years 1 xOther relative 9.4% 12,345 2 Years 1 xWork colleague 7.9% 39,032 2 Years 1 xFriend, Neighbor 26.4% 15,548 2 Years 1 xStranger 6.9% 67,672 2 - 5 Years 1.5 x

24,202 2 Years 1 x

Relationship of Informal Investor to Entrepreneur

Self-Funding by Entrepreneurs

• Entrepreneurs themselves provide 65.8% of the capital for their new ventures.

• Total capital needed to start a new venture is $53,673.

• Entrepreneurs provide $35,317.

• External informal investors provide $18,356.

Expected IRR forInformal Investors

0%

10%

20%

30%

40%

50%

60%

≤0% 0 - 10% 10 - 20% 20 - 40% 40 - 100% ≥100%

Expected IRR

Per

cen

t o

f E

ntr

epre

neu

rs &

Info

rmal

Inve

sto

rs

Entrepreneurs

Informal Investors

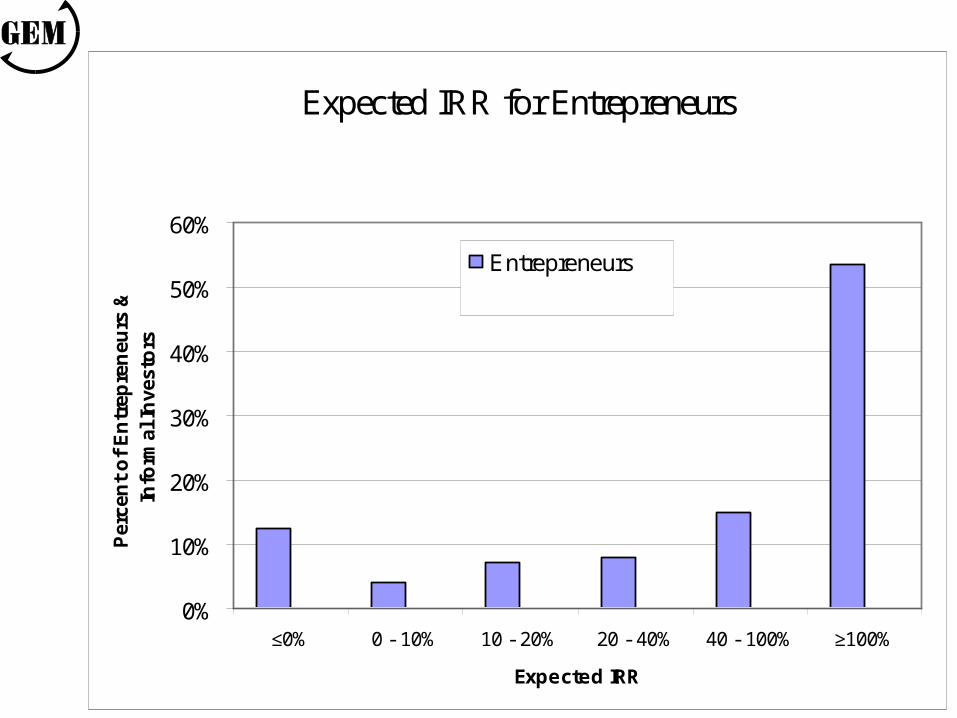

Expected IRR for Entrepreneurs

0%

10%

20%

30%

40%

50%

60%

≤0% 0 - 10% 10 - 20% 20 - 40% 40 - 100% ≥100%

Expected IRR

Per

cen

t o

f E

ntr

epre

neu

rs &

Info

rmal

Inve

sto

rs

Entrepreneurs

Informal Investors

Expected IRR for Entrepreneurs &Informal Investors

0%

10%

20%

30%

40%

50%

60%

≤0% 0 - 10% 10 - 20% 20 - 40% 40 - 100% ≥100%

Expected IRR

Per

cen

t o

f E

ntr

epre

neu

rs &

Info

rmal

Inve

sto

rs

Entrepreneurs

Informal Investors

Startup Funding per Company vs GDP per Capita

y = 5.1083x0.9644

R2 = 0.8571

0

50,000

100,000

150,000

200,000

250,000

0 10,000 20,000 30,000 40,000 50,000 60,000

GDP per Capita, US$

Sta

rtu

p f

un

din

g/c

om

pan

y, U

S$

NO

DK

IE

USA

SE

NL

IT

FRDE

UKBE

AU

CA

SGES

NZGR

ILHUPL

SAARBRPE

ECUG

R2 is the proportion of the variation that is explained by the trend line. An R2 of 0.8571 indicates that 85.71% of the variation in startup funding is explained by GDP per capita.

Startup Funding per Company vs GDP per Capita

y = 5.1083x0.9644

R2 = 0.8571

0

50,000

100,000

150,000

200,000

250,000

0 10,000 20,000 30,000 40,000 50,000 60,000

GDP per Capita, US$

Sta

rtu

p f

un

din

g/c

om

pan

y, U

S$

NO

DK

IE

USA

SE

NL

IT

FRDE

UKBE

AU

CA

SGES

NZGR

ILHUPL

SAARBRPE

ECUG

R2 is the proportion of the variation that is explained by the trend line. An R2 of 0.8571 indicates that 85.71% of the variation in startup funding is explained by GDP per capita.

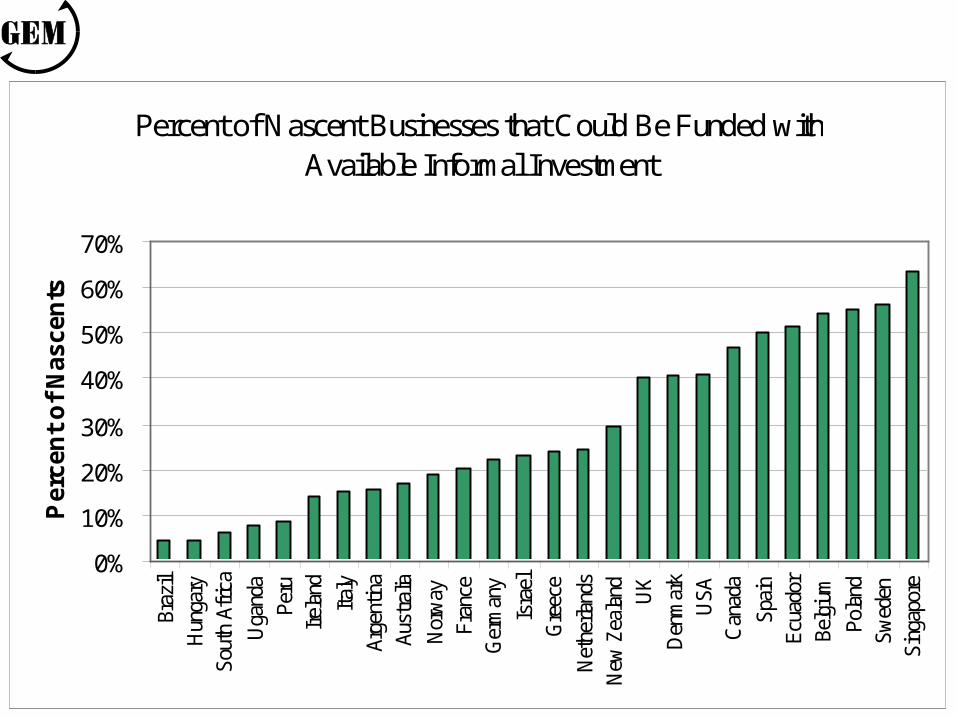

Percent of Nascent Businesses that Could Be Funded with Available Informal Investment

0%

10%

20%

30%

40%

50%

60%

70%

Braz

ilH

unga

rySo

uth

Afric

aU

gand

aPe

ruIre

land

Italy

Arge

ntin

aAu

stra

liaN

orw

ayFr

ance

Ger

man

yIs

rael

Gre

ece

Net

herla

nds

New

Zea

land UK

Den

mar

kU

SAC

anad

aSp

ain

Ecua

dor

Belg

ium

Pola

ndSw

eden

Sing

apor

e

Per

cen

t o

f N

asce

nts

Percent of Nascent Businesses that Could Be Funded with Available Informal Investment

0%

10%

20%

30%

40%

50%

60%

70%

Braz

ilH

unga

rySo

uth

Afric

aU

gand

aPe

ruIre

land

Italy

Arge

ntin

aAu

stra

liaN

orw

ayFr

ance

Ger

man

yIs

rael

Gre

ece

Net

herla

nds

New

Zea

land UK

Den

mar

kU

SAC

anad

aSp

ain

Ecua

dor

Belg

ium

Pola

ndSw

eden

Sing

apor

e

Per

cen

t o

f N

asce

nts

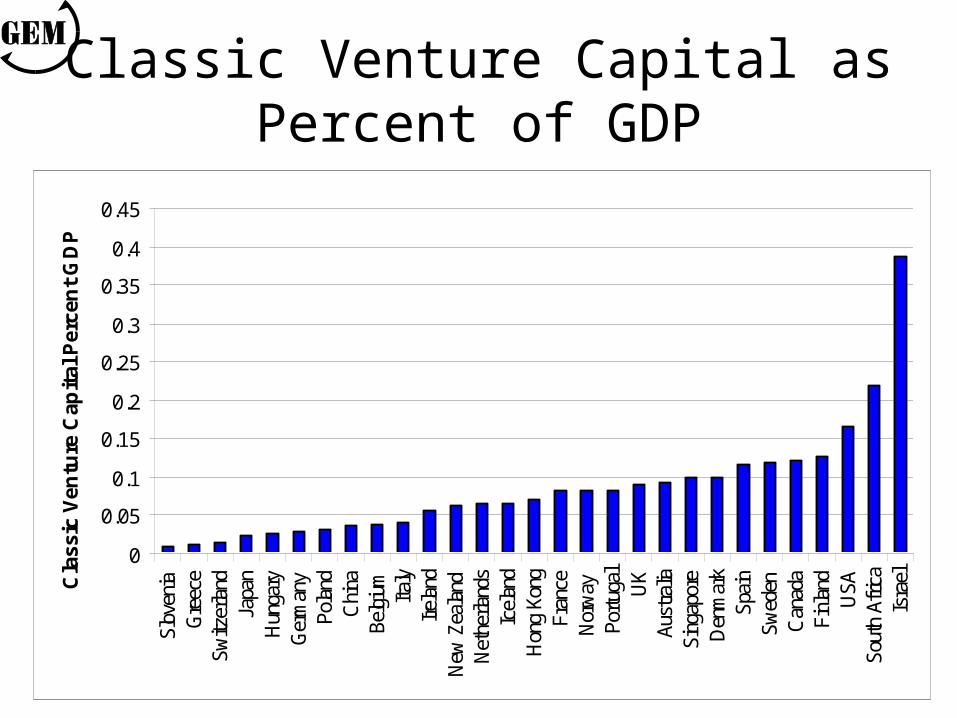

Classic Venture Capital asPercent of GDP

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

Slov

enia

Gre

ece

Switz

erla

ndJa

pan

Hun

gary

Ger

man

yPo

land

Chi

naBe

lgiu

mIta

lyIre

land

New

Zea

land

Net

herla

nds

Icel

and

Hon

g Ko

ngFr

ance

Nor

way

Portu

gal

UK

Aust

ralia

Sing

apor

eD

enm

ark

Spai

nSw

eden

Can

ada

Finl

and

USA

Sout

h Af

rica

Isra

elCla

ssic

Ven

ture

Cap

ital

Per

cen

t G

DP

Other GEM nations

$11.1 billion 38%

USA$18.07 billion 62%

Amount of Classic Venture Capital USA and Other GEM nations

USA2,22719%

Other GEM nations

9,269 81%

Number of Companies Receiving Classic Venture Capital

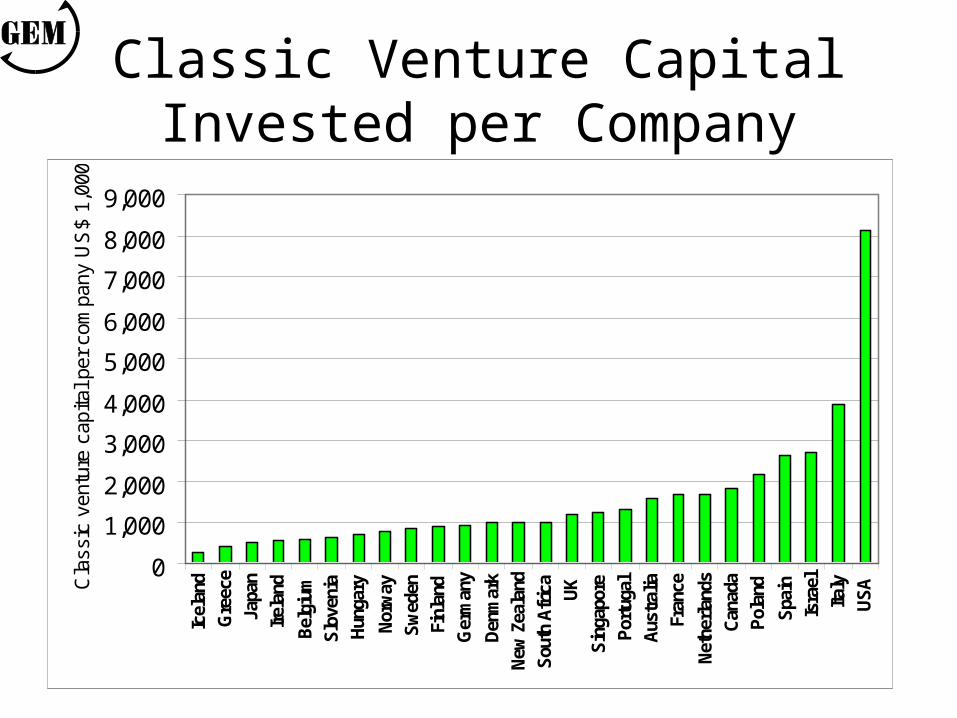

Classic Venture Capital Invested per Company

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000Ic

elan

d

Gre

ece

Japa

n

Irel

and

Bel

gium

Slo

veni

a

Hun

gary

Nor

way

Sw

eden

Finl

and

Ger

man

y

Den

mar

k

New

Zea

land

Sou

th A

fric

a

UK

Sin

gapo

re

Por

tuga

l

Aus

tral

ia

Fran

ce

Net

herl

ands

Can

ada

Pol

and

Spa

in

Isra

el

Italy

US

ACla

ssic

ven

ture

cap

ital p

er c

ompa

ny U

S$

1,00

0

Classic Venture Capital Invested per Company

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000Ic

elan

d

Gre

ece

Japa

n

Irel

and

Bel

gium

Slo

veni

a

Hun

gary

Nor

way

Sw

eden

Finl

and

Ger

man

y

Den

mar

k

New

Zea

land

Sou

th A

fric

a

UK

Sin

gapo

re

Por

tuga

l

Aus

tral

ia

Fran

ce

Net

herl

ands

Can

ada

Pol

and

Spa

in

Isra

el

Italy

US

ACla

ssic

ven

ture

cap

ital p

er c

ompa

ny U

S$

1,00

0

0

1

2

3

4

5

6

7

Biotechnology ComputerSoftware &Hardware

Communications

Cla

ssic

ven

ture

cap

ital,

US

$ bi

llion

Other GEM nations

USA

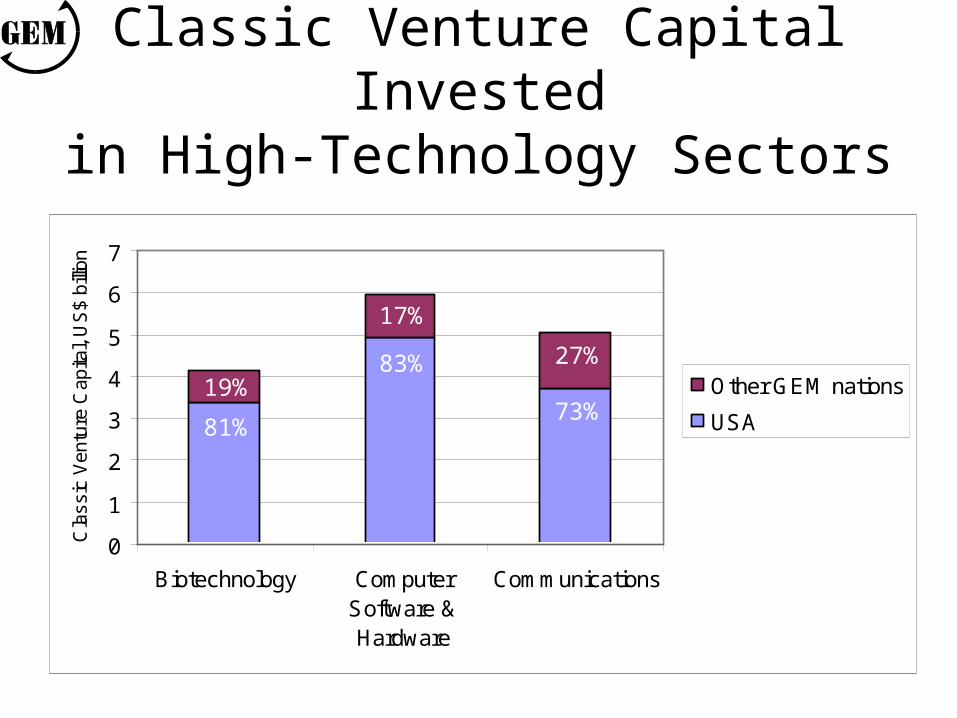

Classic Venture Capital Investedin High-Technology Sectors

0

1

2

3

4

5

6

7

Biotechnology ComputerSoftware &Hardware

Communications

Cla

ssic

Ven

ture

Cap

ital,

US

$ bi

llion

Other GEM nations

USA81%

83%

73%

Classic Venture Capital Investedin High-Technology Sectors

19%

17%

27%

Trend in Domestic Investment of Classic Venture Capital 1999-2003

$0

$20,000,000

$40,000,000

$60,000,000

$80,000,000

$100,000,000

$120,000,000

1999 2000 2001 2002 2003

Denmark

Ireland

Finland

Norway

Belgium

Sweden

Australia

Spain

Italy

Israel

Japan

France

Germany

UK

Canada

USA

USA82%

USA83%

USA77%

USA70%

Ven

ture

Cap

ital

Inv

estm

ent (

1,00

0)

USA66%

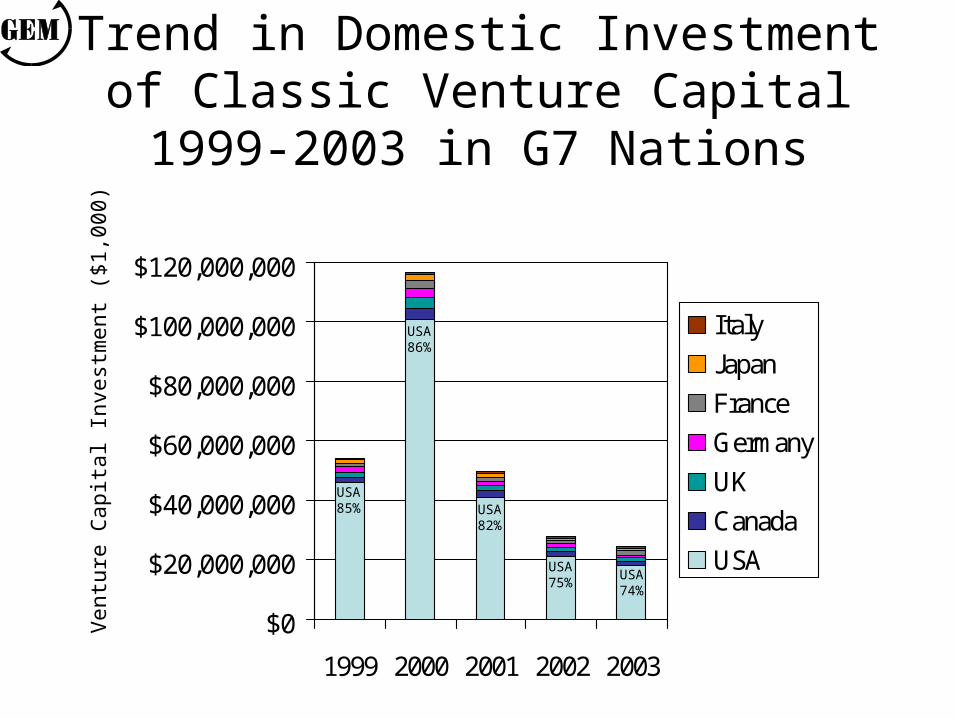

Trend in Domestic Investment of Classic Venture Capital 1999-2003 in G7 Nations

$0

$20,000,000

$40,000,000

$60,000,000

$80,000,000

$100,000,000

$120,000,000

1999 2000 2001 2002 2003

Italy

Japan

France

Germany

UK

Canada

USA

USA85%

USA86%

USA82%

USA75%

Ven

ture

Cap

ital

Inv

estm

ent (

$1,0

00)

USA74%

Implications & Recommendations

• Self-financing and informal investment are far and away the most important sources of startup financing.

• If self-financing and informal investment dried up,

entrepreneurship would wither and die.

• On the other hand, if classic venture capital dried up, entrepreneurship in general would continue to flourish.

• Classic venture capital is primarily an accelerant in the commercialization of new products and services. It seldom funds revolutionary research.

• Get your initial financing from yourselves, family, friends, work colleagues, and strangers (4Fs).

• Don’t even think about classic venture capital at the seed-stage. The odds on raising venture capital for a seed-stage company are worse than the odds on becoming a professional athlete!

Entrepreneurs:

Policy Makers:

• Give entrepreneurs and informal investors a tax break and other incentives.

• Let classic venture capital take care of itself. Just treat classic venture capital as an asset class from the point of view of investors and pension funds.

Educators & Trainers:

• Pay much, much more attention to self-funding and informal investment as sources of startup capital.

• Pay much less attention to classic venture capital as a source of startup capital.

• Put much less emphasis on business plans and business plan competitions that target venture capital.

Researchers

• Conduct far fewer studies of classic venture capital and public stock markets as sources of financing for entrepreneurs.

• Conduct far more studies of funding by informal investors and self-funding by entrepreneurs themselves.

Founding and Supporting InstitutionsBabson College and London Business School