Embed Size (px)

Citation preview

Research report

Financial trends for UK-based INGOs An analysis of Bond members’ income between 2006/07 and 2013/14

Financial trends for UK-based INGOs

Foreword 1

Executive summary 2

1. Introduction 4

2. Methodology 5

3. Income in 2013/14 8

4. Trends in total income over time 12

5. Trends in income by source 16

6. Trends in income by size of organisation 24

7. Other financial trends 29

8. Non-financial operational data 32

9. Conclusion 38

Appendix: A comparison with the wider international sector 39

Contents

About Bond

Bond is the civil society network for global change. We bring people together to make the international development sector more effective. bond.org.uk

Acknowledgements

This report was authored by David Kane from NCVO, and Graham MacKay and Kathy Peach from Bond. Particular thanks to Jo Edwards from Mango and Siham Bortcosh for their comments on earlier drafts.

Financial trends for UK-based INGOs, April 2016 Published by Bond, Society Building, 8 All Saints Street, London N1 9RL, UK Registered Charity No. 1068839 Company Registration No. 3395681 (England and Wales) © Bond, 2016

Design: TRUE www.truedesign.co.uk

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License, https://creativecommons.org/licenses/by-nc/4.0

Financial trends for UK-based INGOs 1

ForewordThis research into the financial profiles of UK-based international NGOs comes at an important time. We know many agencies are considering how they can ensure their continued relevance and financial sustainability in a rapidly changing world.

As the first large scale market analysis of income trends for UK agencies working in international development, this report aims to provide useful insights for senior leaders as they make decisions about how best to resource their organisations’ work.

The analysis looks at 362 organisations for the period 2006/7 to 2013/14, the most up to date information available. On the face of it, the overall picture for Bond members looks healthy – although this study exposes different patterns according to organisational size, with both winners and losers.

The data on which this report is based cannot, however, reflect events of recent months or changes on the horizon that may well disrupt the trajectory.

Organisations in receipt of Programme Partnership Agreements (PPAs) funded by DFID know that this particular funding vehicle comes to an end in December 2016. Meanwhile, voluntary sector and government donors are beginning to turn towards more direct funding of NGOs in the global south, thereby bypassing the traditional intermediary role played by international NGOs.

Our data shows that public support for aid and development appears relatively steady, but we are yet to see the full effect of changes in fundraising regulation and practice, and of current political and public debates about aid. And while contracting has been an important source of income growth for some agencies, we know the majority are struggling to recover anywhere near their full costs – something highlighted in our recent benchmarking study, Cost recovery: what it means for CSOs.

In such an uncertain context, no NGO can afford to be complacent about its funding. A key headline for all NGOs must surely be the need to look afresh at whether they have the right business model for their purpose and role into the future. Those with a clear value proposition and a vigilant awareness of the evolving external environment will be best equipped to face the challenge of securing resources to achieve their development goals.

I hope you find the report interesting and useful.

Sarah MistryDirector of Effectiveness and Learning, Bond

Financial trends for UK-based INGOs 2

Bond worked with NCVO to carry out this research between November 2015 and March 2016 using data for 362 of its member organisations that is publicly available from the Charity Commission.

1. Big fall: income halved or more between 2008/09 and 2013/14; Little fall: income fell by one-fifth or more between 2008/9 and 2013/14; Ticking along: income in 2013/14 was within 20% of the income in 2008/9; Little rise: income rose by one-fifth or more between 2008/9 and 2013/14; Big rise: income doubled or more between 2008/9 and 2013/14.

The aim of this research is to develop a better understanding of the income profiles of UK-based international non-governmental organisations (INGOs), generate insight into their financial sustainability, and identify any trends associated with growth or decline in income. This report provides background intelligence for Bond’s work supporting INGOs to develop future-fit business models.

Unlike charities in the UK domestic sector, UK-based INGOs experienced sustained growth in income between 2006/07 and 2013/14

Bond members experienced a period of sustained growth in income between 2006/07 and 2013/14, with a strong recovery following a brief spell of turbulence after the 2008 financial crisis. The trend in income for Bond members diverges significantly from the UK charity sector as a whole, whose income has not recovered from the peak of 2007/08. During the period, 44% of Bond members have experienced either a little rise or a big rise in income, with a further 19% ticking along. Just 13% of Bond members have experienced either a big fall or little fall in income.1

Executive summary

Income from government has replaced individual donations as the largest overall source of income

Income from government (UK, overseas and multilateral donors) has increased by 165% over the last eight years to nearly £1.3 billion, or 39% of total income in 2013/14, replacing income from individuals as the largest overall income source. Much of this growth has come from contracts, which now make up 25% of total income for Bond members. Income from individuals also grew (by 23%) and still remains highly important as the source for £1.2 billion of income (37% of total income). Income from voluntary organisations (chiefly grants from foundations) has also grown, reaching nearly £630m in 2013/14, or 19% of total income.

Large INGOs are doing best – picking up the majority of income growth from most sources

The largest INGOs (organisations represented in the >£40m income segment) appear to have experienced the highest growth in income and increased their market share of most income streams – government contracts, government grants, voluntary sector income, individual donations, and earned charitable income. Although overall income for this segment is going up, it is still very uneven with some organisations growing considerably and others less so.

Financial trends for UK-based INGOs 3

Small INGOs are faring worst, with declining income across all sources

Smaller agencies (those with income <£2m) appear to have declining income across the board, and have lost market share in all areas. No other segment of the Bond membership has experienced such negative trends across all income sources, and it raises questions about potential avenues of growth or, perhaps even survival, for organisations in this group.

Earned charitable and corporate income is a particular growth area for INGOs in the £2-5m and £5-20m segments

Organisations in the £2-5m segment increased their income from corporate sources nine-fold in the eight years (from a low base), while the £5-20m group increased their income from corporates by 73%. However, there is a large degree of variation from the average over the period, showing this to be an unpredictable source of income and growth. It has also grown modestly over the eight years, by 54%. The other significant growth area for these two segments (as well as for organisations in the larger income categories) was earned charitable income from individuals (fees for services or goods). Could these trends suggest perhaps an increasingly commercial mindset among Bond’s mid-size members?

INGOs in the £20m-£40m income segment are specialising in government contracts

Organisations in the £20-40m segment have doubled their market share in government contracts (to 15%) over the period, with government contracts responsible for more than 50% of the income for these organisations (and total income from government accounting for more than 60%) in 2013/14. There is a trend for both government grants and contracts to go disproportionately to larger organisations, with those over £20m now holding 83% market share of government contracts as smaller organisations lost out during the period.

Financial trends for UK-based INGOs 4

1. IntroductionThe international development landscape is changing. Urbanisation, technological advances, and the diversification of development actors are just some of the trends that will require international non-governmental organisations (INGOs) to fundamentally rethink their purpose, their role, and how they fund their work.

As a network for international development organisations, Bond has a responsibility to help its members innovate and adapt so that they can keep meeting the changing needs of poor and marginalised communities around the world. Our futures and innovation programme, of which this research is a part, aims to help organisations to prepare for the future.

Ensuring financial sustainability has always been an important task for senior leadership teams and boards. But as traditional sources of financing for INGOs appear to be coming under pressure, including from recent public fundraising scandals and political shifts in the allocation of overseas development assistance (ODA), it has never been more challenging. The ability to develop new, future-facing business models will be a critical test for the sector’s senior leaders over the coming years – one that Bond will support its members to rise to.

Understanding current income profiles for INGOs, their vulnerability to disruption in funding, and the trends associated with growth or decline in income is important grounding for any discussion of long-term sustainability and future business models. This report hopes to provide a snapshot of the present situation for UK-based INGOs, and an analysis of the trends over the last eight years.

Bond, with NCVO, carried out this research between November 2015 and March 2016 using data for 362 of its members that was publicly available from the Charity Commission.

The data analysis is divided into six main sections:

• Section 3 provides an overview of income for Bond’s members in 2013/14

• Section 4 covers trends in total income between 2006/7 and 2013/14

• Section 5 examines the trends in different income sources

• Section 6 looks at how the income profiles of different sized Bond members has changed between 2006/7 and 2013/14

• Section 7 covers other financial trends, including fundraising ratios, reserves and assets

• Section 8 brings together non-financial information on the size and scope of the Bond membership.

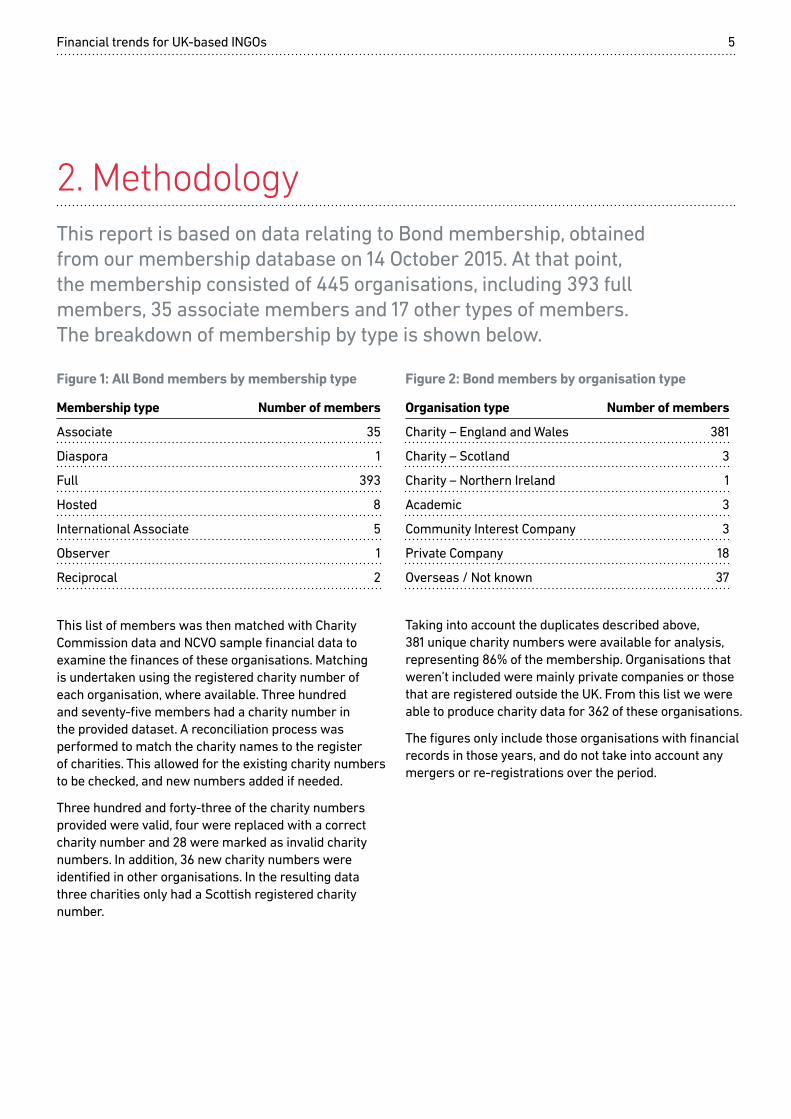

Taking into account the duplicates described above, 381 unique charity numbers were available for analysis, representing 86% of the membership. Organisations that weren’t included were mainly private companies or those that are registered outside the UK. From this list we were able to produce charity data for 362 of these organisations.

The figures only include those organisations with financial records in those years, and do not take into account any mergers or re-registrations over the period.

Figure 1: All Bond members by membership type

Membership type Number of members

Associate 35

Diaspora 1

Full 393

Hosted 8

International Associate 5

Observer 1

Reciprocal 2

Figure 2: Bond members by organisation type

Organisation type Number of members

Charity – England and Wales 381

Charity – Scotland 3

Charity – Northern Ireland 1

Academic 3

Community Interest Company 3

Private Company 18

Overseas / Not known 37

Financial trends for UK-based INGOs 5

2. MethodologyThis report is based on data relating to Bond membership, obtained from our membership database on 14 October 2015. At that point, the membership consisted of 445 organisations, including 393 full members, 35 associate members and 17 other types of members. The breakdown of membership by type is shown below.

This list of members was then matched with Charity Commission data and NCVO sample financial data to examine the finances of these organisations. Matching is undertaken using the registered charity number of each organisation, where available. Three hundred and seventy-five members had a charity number in the provided dataset. A reconciliation process was performed to match the charity names to the register of charities. This allowed for the existing charity numbers to be checked, and new numbers added if needed.

Three hundred and forty-three of the charity numbers provided were valid, four were replaced with a correct charity number and 28 were marked as invalid charity numbers. In addition, 36 new charity numbers were identified in other organisations. In the resulting data three charities only had a Scottish registered charity number.

Financial trends for UK-based INGOs 6

2.1 Exclusions

Additional criteria was applied to the data from section 3.3 onwards to present a more typical picture of changes in income for UK-based INGOs, who currently make up the majority of Bond’s membership.

The following organisations were excluded from the trend analysis and analysis of income sources:

• British Council and Save the Children International (outliers, whose large size heavily skewed overall results);

• Disasters Emergency Committee (as much of their income would be passed on to others and so would be double counted);

• A number of large foundations and trusts (including Comic Relief);

• Large national UK charities (such as Leonard Cheshire Disability and RNLI) that only do a small amount of international work (as unfortunately the data source does not allow for their international activities to be separated out from the rest of their data).

Where appropriate, these excluded organisations have been presented in charts for comparison purposes.

2.2 Categorising Bond members

For the purpose of analysing trends among Bond members of different sizes we segmented the data into the following categories from section 3 onwards.

• Organisations with income of less than £100k

• Organisations with income between £100-£500k

• Organisations with income between £500k-£2m

• Organisations with income between £2m and £5m

• Organisations with income between £5m and £20m

• Organisations with income between £20m and £40m

• Organisations with income over £40m.

From section 5 onwards, we reduced the number of categories analysed to five; grouping together the three smaller organisation segments into one category of >£2m income. This was done to aggregate the spend for the smaller organisations so we could compare more easily between segments. But it also means we may have lost some of the subtlety in the trends.

2.3 Financial values in real terms

When looking at trends in income, we have revised all the figures to reflect real terms amounts related to the last year in the study. Therefore 2013/14 is unchanged and the 2006/07 figures are revised upwards to reflect their 2013/14 cash value. We believe this gives a more representative view of the trends.

Financial trends for UK-based INGOs 7

2.4 Glossary of income sources and types

• Individuals – including the general public, high net worth donors and legacies.

• Government – including UK central government departments, local authorities, or other government bodies, as well as overseas governments and supranational and international bodies such as the EU, UN and World Bank.

• Voluntary sector – including grants from foundations and earned income from other voluntary organisations.

• Corporate – including grants from businesses and any contracts with businesses to provide a service.

• National Lottery – including grants from any of the UK’s national lottery distribution bodies, notably the Big Lottery Fund. Unless presented separately, this income source is included within the voluntary sector income analysis.

• Earned income – received in return for selling goods or services.

• Earned charitable income – generated when fees are paid for a charity to deliver goods or services that further the charity’s objectives (in this report we specifically look at earned charitable income from individuals, which would consist of fees for services such training, rent of rooms, research etc.

• Earned fundraising income – generated specifically to raise funds for the charity, for example, from the selling of donated goods, or admission fees for fundraising events.

• Investment – received as a return on investment assets, for example, property, stocks and shares or other similar assets.

• Donations – income given freely by individuals, for which they receive no material benefit. This is sometimes also known as voluntary income. Donations are usually unrestricted.

• Grants –awards provided by a funder for certain type of activities, they can be unrestricted but increasingly tend to be restricted to the purposes specified.

• Contracts – fees for provision of a specific service. This report specifically looks at trends in contracts from governments.

Financial trends for UK-based INGOs 8

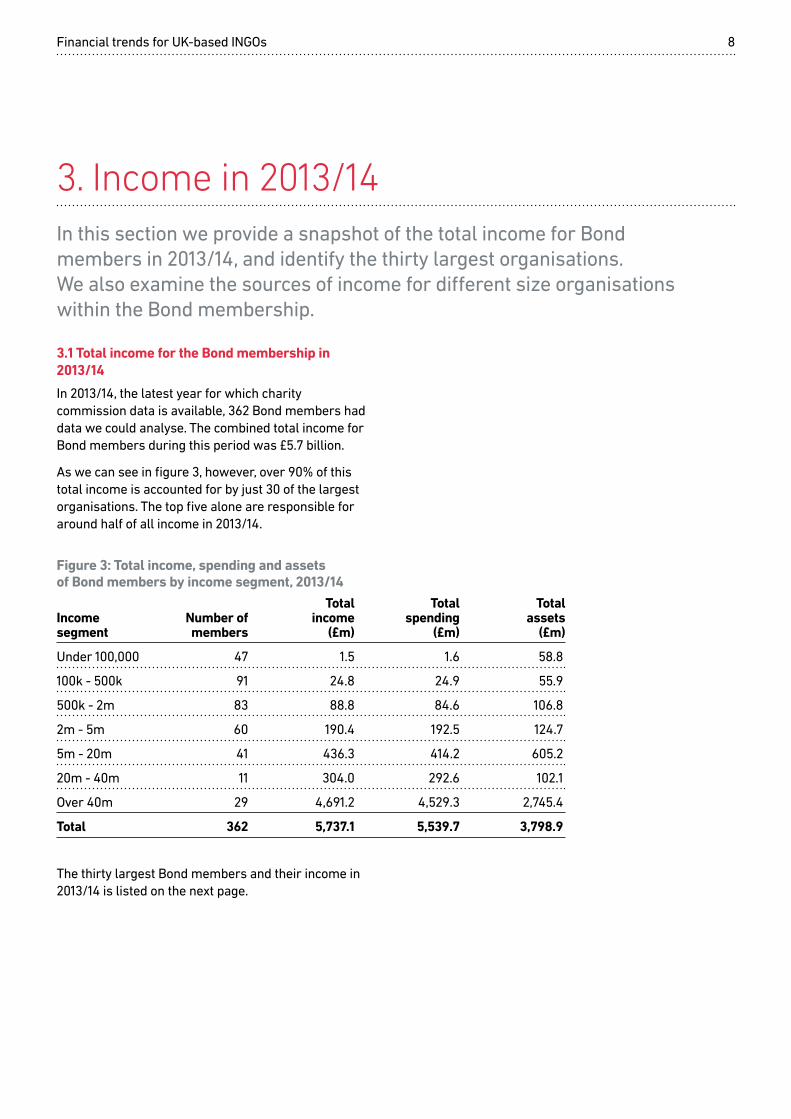

3.1 Total income for the Bond membership in 2013/14

In 2013/14, the latest year for which charity commission data is available, 362 Bond members had data we could analyse. The combined total income for Bond members during this period was £5.7 billion.

As we can see in figure 3, however, over 90% of this total income is accounted for by just 30 of the largest organisations. The top five alone are responsible for around half of all income in 2013/14.

3. Income in 2013/14In this section we provide a snapshot of the total income for Bond members in 2013/14, and identify the thirty largest organisations. We also examine the sources of income for different size organisations within the Bond membership.

Figure 3: Total income, spending and assets of Bond members by income segment, 2013/14 Total Total Total Income Number of income spending assets segment members (£m) (£m) (£m)

Under 100,000 47 1.5 1.6 58.8

100k - 500k 91 24.8 24.9 55.9

500k - 2m 83 88.8 84.6 106.8

2m - 5m 60 190.4 192.5 124.7

5m - 20m 41 436.3 414.2 605.2

20m - 40m 11 304.0 292.6 102.1

Over 40m 29 4,691.2 4,529.3 2,745.4

Total 362 5,737.1 5,539.7 3,798.9

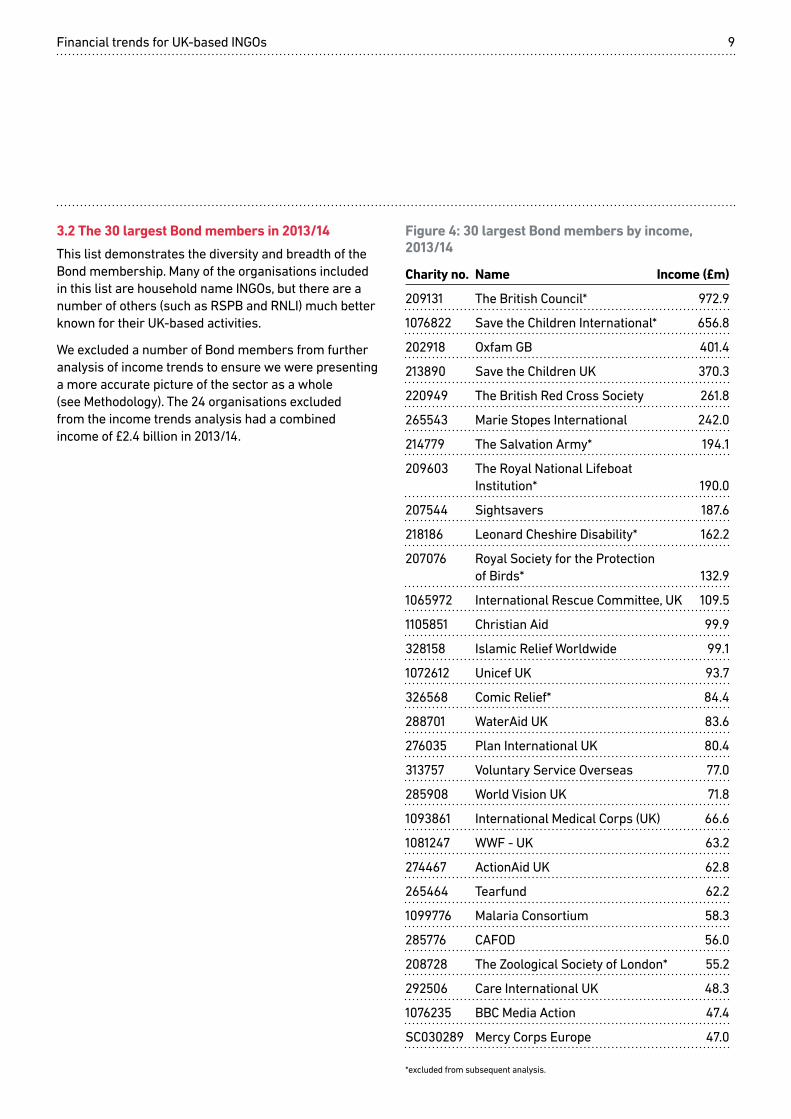

The thirty largest Bond members and their income in 2013/14 is listed on the next page.

Figure 4: 30 largest Bond members by income, 2013/14

Charity no. Name Income (£m)

209131 The British Council* 972.9

1076822 Save the Children International* 656.8

202918 Oxfam GB 401.4

213890 Save the Children UK 370.3

220949 The British Red Cross Society 261.8

265543 Marie Stopes International 242.0

214779 The Salvation Army* 194.1

209603 The Royal National Lifeboat Institution* 190.0

207544 Sightsavers 187.6

218186 Leonard Cheshire Disability* 162.2

207076 Royal Society for the Protection of Birds* 132.9

1065972 International Rescue Committee, UK 109.5

1105851 Christian Aid 99.9

328158 Islamic Relief Worldwide 99.1

1072612 Unicef UK 93.7

326568 Comic Relief* 84.4

288701 WaterAid UK 83.6

276035 Plan International UK 80.4

313757 Voluntary Service Overseas 77.0

285908 World Vision UK 71.8

1093861 International Medical Corps (UK) 66.6

1081247 WWF - UK 63.2

274467 ActionAid UK 62.8

265464 Tearfund 62.2

1099776 Malaria Consortium 58.3

285776 CAFOD 56.0

208728 The Zoological Society of London* 55.2

292506 Care International UK 48.3

1076235 BBC Media Action 47.4

SC030289 Mercy Corps Europe 47.0

Financial trends for UK-based INGOs 9

3.2 The 30 largest Bond members in 2013/14

This list demonstrates the diversity and breadth of the Bond membership. Many of the organisations included in this list are household name INGOs, but there are a number of others (such as RSPB and RNLI) much better known for their UK-based activities.

We excluded a number of Bond members from further analysis of income trends to ensure we were presenting a more accurate picture of the sector as a whole (see Methodology). The 24 organisations excluded from the income trends analysis had a combined income of £2.4 billion in 2013/14.

*excluded from subsequent analysis.

Financial trends for UK-based INGOs 10

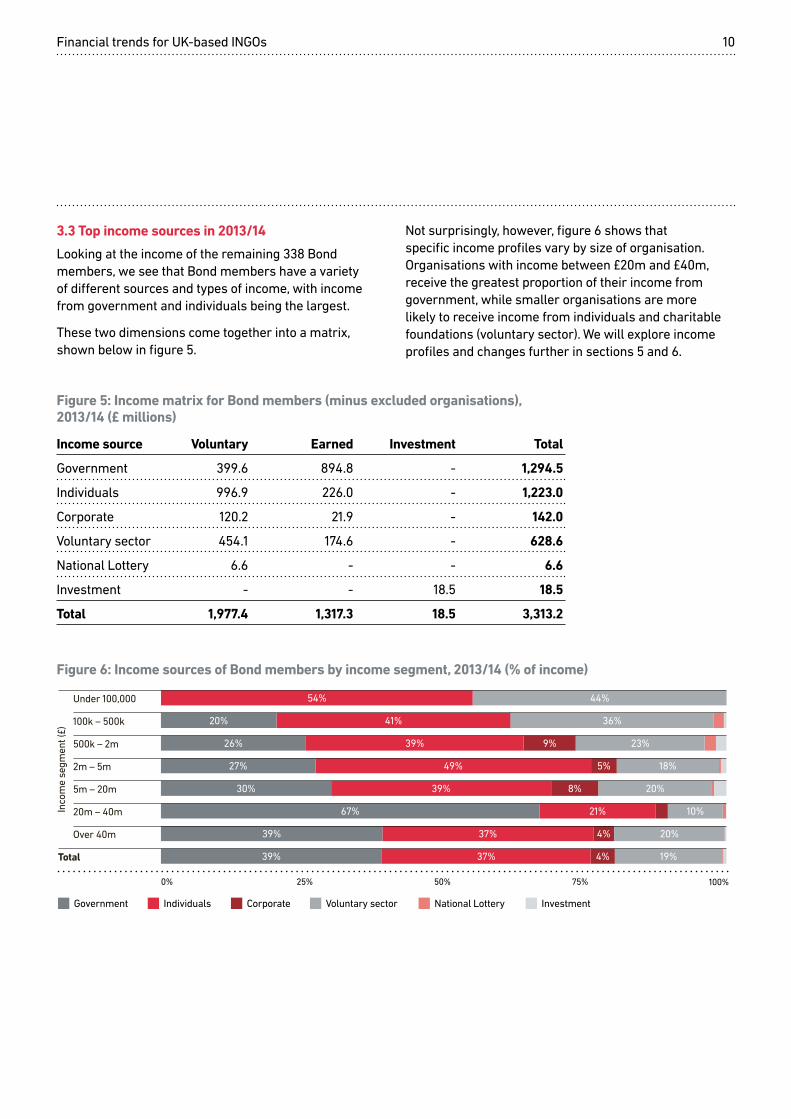

3.3 Top income sources in 2013/14

Looking at the income of the remaining 338 Bond members, we see that Bond members have a variety of different sources and types of income, with income from government and individuals being the largest.

These two dimensions come together into a matrix, shown below in figure 5.

Not surprisingly, however, figure 6 shows that specific income profiles vary by size of organisation. Organisations with income between £20m and £40m, receive the greatest proportion of their income from government, while smaller organisations are more likely to receive income from individuals and charitable foundations (voluntary sector). We will explore income profiles and changes further in sections 5 and 6.

Figure 5: Income matrix for Bond members (minus excluded organisations), 2013/14 (£ millions)

Income source Voluntary Earned Investment Total

Government 399.6 894.8 - 1,294.5

Individuals 996.9 226.0 - 1,223.0

Corporate 120.2 21.9 - 142.0

Voluntary sector 454.1 174.6 - 628.6

National Lottery 6.6 - - 6.6

Investment - - 18.5 18.5

Total 1,977.4 1,317.3 18.5 3,313.2

Figure 6: Income sources of Bond members by income segment, 2013/14 (% of income)

100%50%25% 75%0%

Government Individuals Corporate Voluntary sector National Lottery Investment

20%

26%

27%

30%

67%

39%

39%

54%

41%

39% 9%

49% 5%

39%

21% £24.5m

37% 4% £884.8m £464.0m

37% 4% £628.6m

Under 100,000

100k – 500k

500k – 2m

2m – 5m

5m – 20m

20m – 40m

Over 40m

Total

Inco

me

segm

ent (

£)

44%

36%

23%

18%

20%8%

10%

20%

19%

Financial trends for UK-based INGOs 11

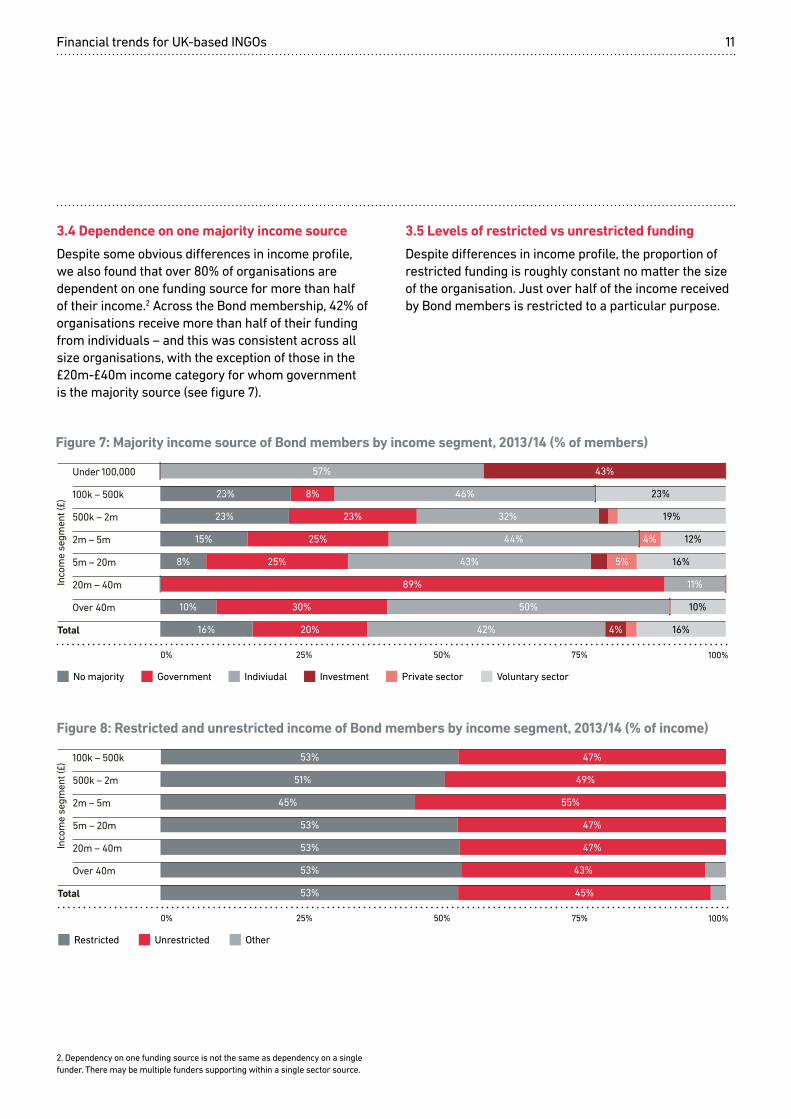

3.4 Dependence on one majority income source

Despite some obvious differences in income profile, we also found that over 80% of organisations are dependent on one funding source for more than half of their income.2 Across the Bond membership, 42% of organisations receive more than half of their funding from individuals – and this was consistent across all size organisations, with the exception of those in the £20m-£40m income category for whom government is the majority source (see figure 7).

2. Dependency on one funding source is not the same as dependency on a single funder. There may be multiple funders supporting within a single sector source.

3.5 Levels of restricted vs unrestricted funding

Despite differences in income profile, the proportion of restricted funding is roughly constant no matter the size of the organisation. Just over half of the income received by Bond members is restricted to a particular purpose.

Figure 7: Majority income source of Bond members by income segment, 2013/14 (% of members)

100%50%25% 75%0%

No majority Government Indiviudal Investment Private sector Voluntary sector

23% 8% 46% 23%

23% 23% 32% 19%

15% 25% 44% 4% 12%

25% 43% 5% 16%8%

89% 11%

30% 50% 10%10%

16% 20% 16%42% 4%

57% 43%Under 100,000

100k – 500k

500k – 2m

2m – 5m

5m – 20m

20m – 40m

Over 40m

Total

Inco

me

segm

ent (

£)

Figure 8: Restricted and unrestricted income of Bond members by income segment, 2013/14 (% of income)

100%50%25% 75%0%

53%

51%

45%

53%

53%

53%

53%

49%

55%

47%

47%

43%

45%

100k – 500k

500k – 2m

2m – 5m

5m – 20m

20m – 40m

Over 40m

Total

Restricted Unrestricted Other

Inco

me

segm

ent (

£)

47%

Figure 9: Total income of Bond members in cash and real terms between 1996/97 and 2013/14 (£ millions)

Bond members cash terms

Bond members real terms

Excluded members real terms

500

1,000

0

1,500

2,000

2,500

3,000

97/98 99/00 01/02 03/04 05/06 07/08 09/10 11/12 13/14

Excluded members cash terms

Financial trends for UK-based INGOs 12

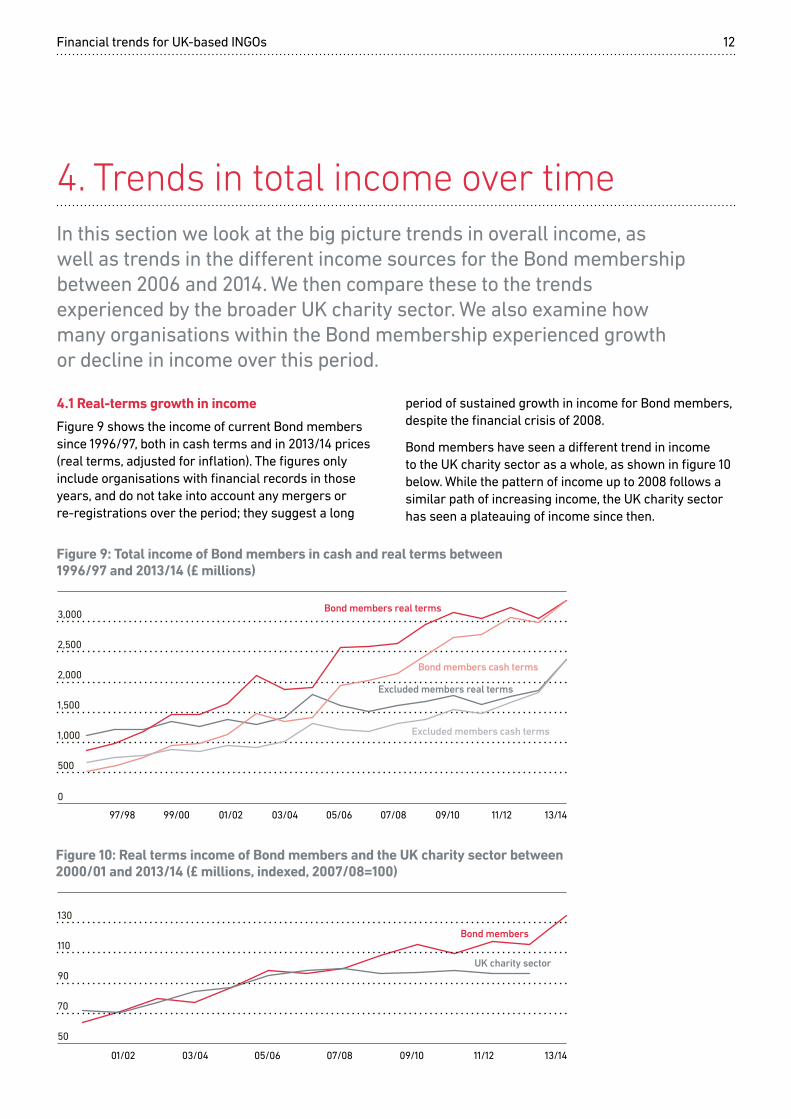

4.1 Real-terms growth in income

Figure 9 shows the income of current Bond members since 1996/97, both in cash terms and in 2013/14 prices (real terms, adjusted for inflation). The figures only include organisations with financial records in those years, and do not take into account any mergers or re-registrations over the period; they suggest a long

4. Trends in total income over time In this section we look at the big picture trends in overall income, as well as trends in the different income sources for the Bond membership between 2006 and 2014. We then compare these to the trends experienced by the broader UK charity sector. We also examine how many organisations within the Bond membership experienced growth or decline in income over this period.

period of sustained growth in income for Bond members, despite the financial crisis of 2008.

Bond members have seen a different trend in income to the UK charity sector as a whole, as shown in figure 10 below. While the pattern of income up to 2008 follows a similar path of increasing income, the UK charity sector has seen a plateauing of income since then.

Figure 10: Real terms income of Bond members and the UK charity sector between 2000/01 and 2013/14 (£ millions, indexed, 2007/08=100)

01/02 03/04 05/06 07/08 09/10 11/12 13/14

UK charity sector

Bond members

70

90

50

110

130

Figure 11: Income sources of Bond members between 2006/07 and 2013/14 (£ millions, 2013/14 prices)

Government

Individuals

Voluntary sector

Corporate

InvestmentNational Lottery

200

400

0

600

800

1,000

1,200

06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

Figure 12: Income sources of UK charity sector between 2006/07 and 2012/13 (£ millions, 2013/14 prices)

Government

Individuals

Voluntary sectorInvestmentCorporateNational Lottery

06/07 07/08 08/09 09/10 10/11 11/12 12/13

3,000

6,000

0

9,000

12,000

15,000

18,000

Financial trends for UK-based INGOs 13

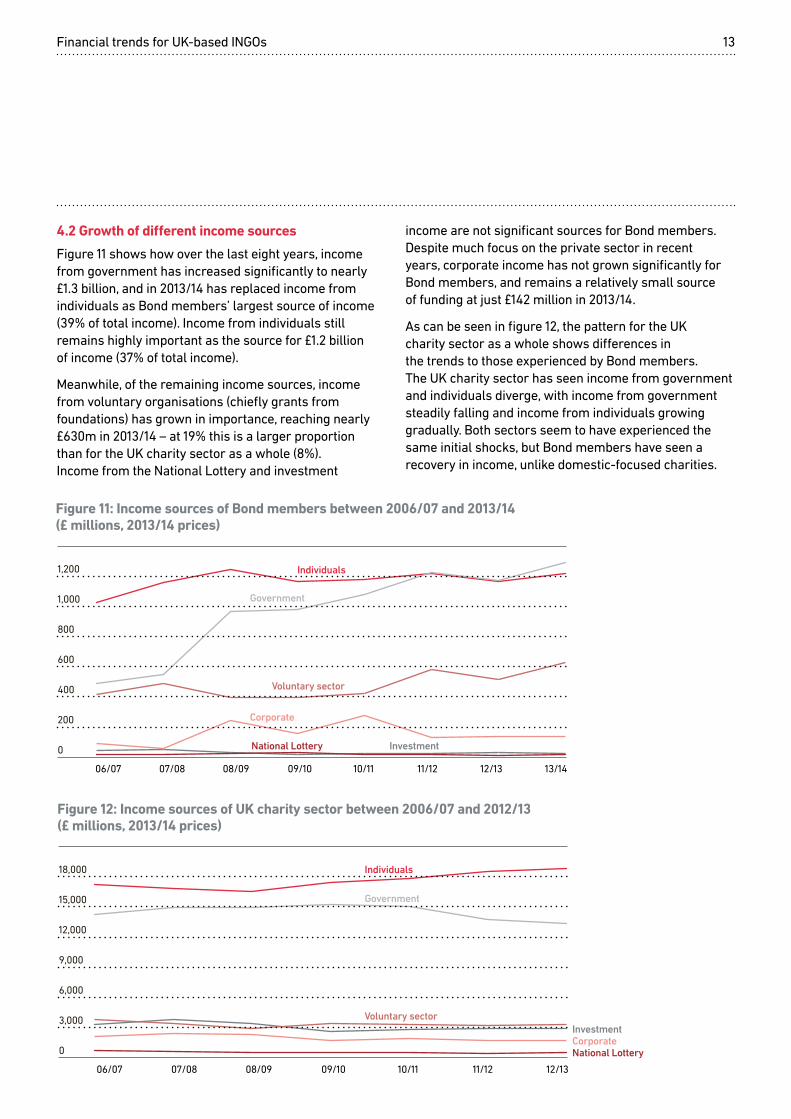

4.2 Growth of different income sources

Figure 11 shows how over the last eight years, income from government has increased significantly to nearly £1.3 billion, and in 2013/14 has replaced income from individuals as Bond members’ largest source of income (39% of total income). Income from individuals still remains highly important as the source for £1.2 billion of income (37% of total income).

Meanwhile, of the remaining income sources, income from voluntary organisations (chiefly grants from foundations) has grown in importance, reaching nearly £630m in 2013/14 – at 19% this is a larger proportion than for the UK charity sector as a whole (8%). Income from the National Lottery and investment

income are not significant sources for Bond members. Despite much focus on the private sector in recent years, corporate income has not grown significantly for Bond members, and remains a relatively small source of funding at just £142 million in 2013/14.

As can be seen in figure 12, the pattern for the UK charity sector as a whole shows differences in the trends to those experienced by Bond members. The UK charity sector has seen income from government and individuals diverge, with income from government steadily falling and income from individuals growing gradually. Both sectors seem to have experienced the same initial shocks, but Bond members have seen a recovery in income, unlike domestic-focused charities.

Financial trends for UK-based INGOs 14

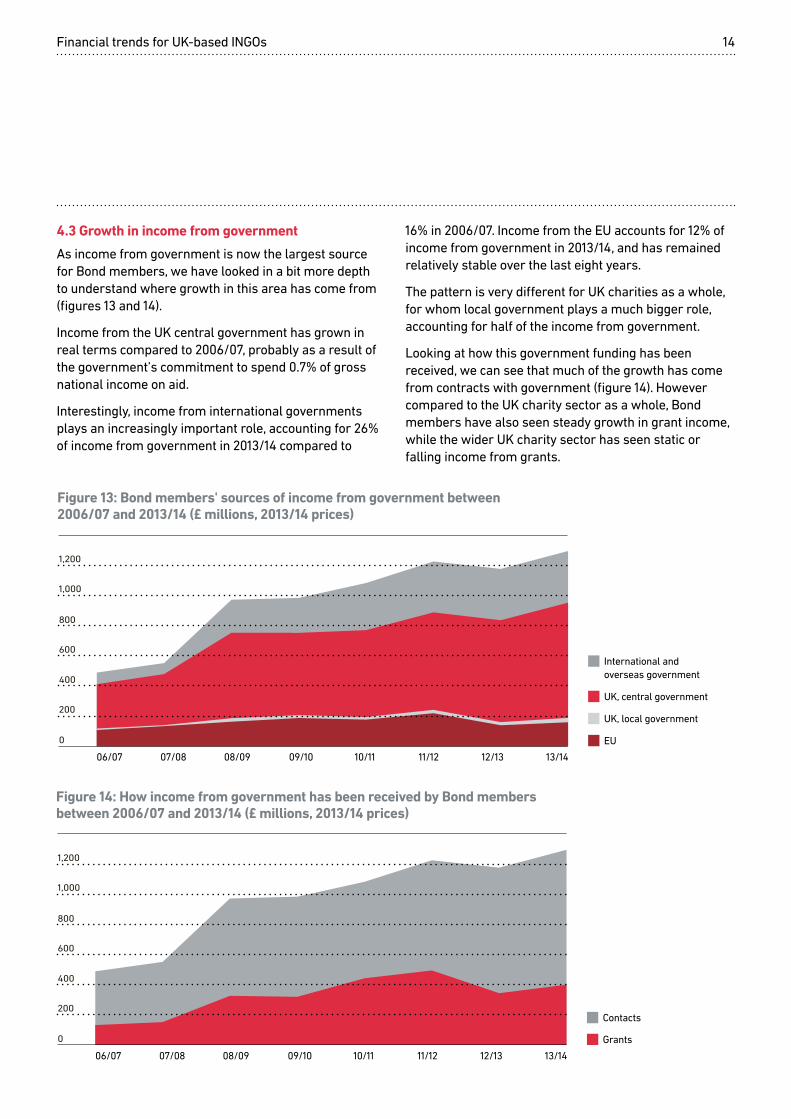

4.3 Growth in income from government

As income from government is now the largest source for Bond members, we have looked in a bit more depth to understand where growth in this area has come from (figures 13 and 14).

Income from the UK central government has grown in real terms compared to 2006/07, probably as a result of the government’s commitment to spend 0.7% of gross national income on aid.

Interestingly, income from international governments plays an increasingly important role, accounting for 26% of income from government in 2013/14 compared to

Figure 13: Bond members' sources of income from government between 2006/07 and 2013/14 (£ millions, 2013/14 prices)

06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

International and overseas government

UK, central government

UK, local government

EU0

400

800

1,000

200

600

1,200

16% in 2006/07. Income from the EU accounts for 12% of income from government in 2013/14, and has remained relatively stable over the last eight years.

The pattern is very different for UK charities as a whole, for whom local government plays a much bigger role, accounting for half of the income from government.

Looking at how this government funding has been received, we can see that much of the growth has come from contracts with government (figure 14). However compared to the UK charity sector as a whole, Bond members have also seen steady growth in grant income, while the wider UK charity sector has seen static or falling income from grants.

Figure 14: How income from government has been received by Bond members between 2006/07 and 2013/14 (£ millions, 2013/14 prices)

06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

0

400

800

1,000

200

600

1,200

Grants

Contacts

Financial trends for UK-based INGOs 15

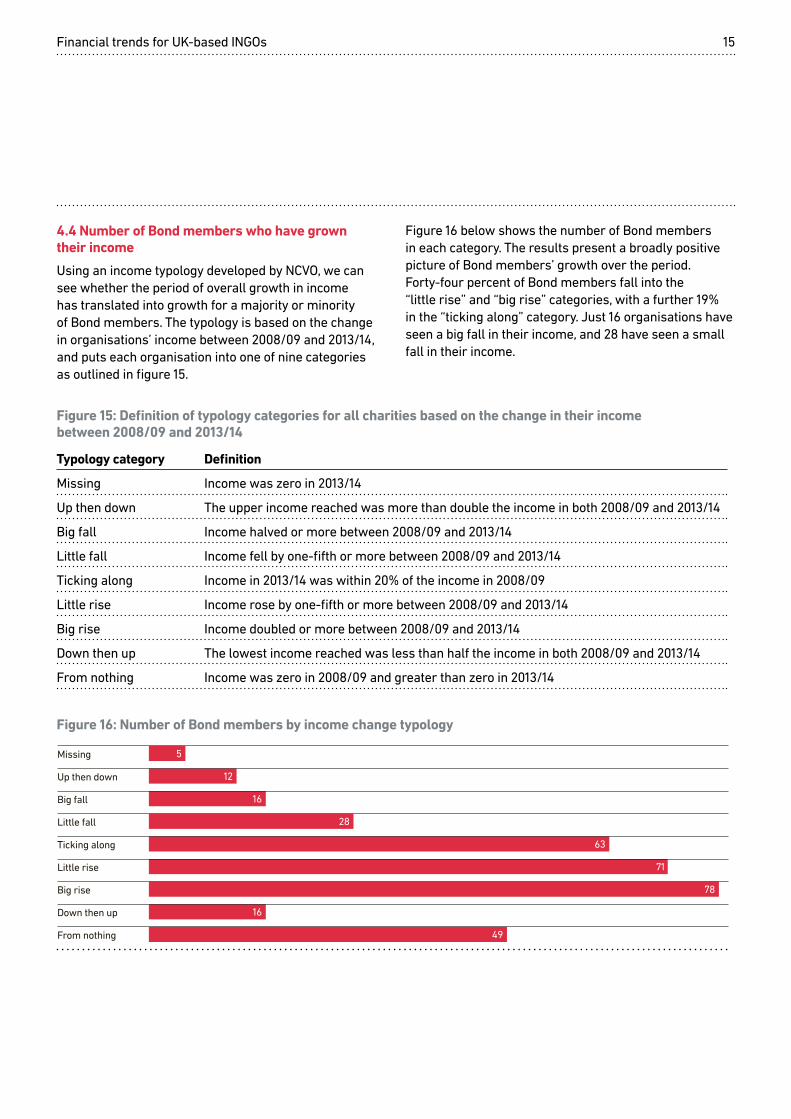

Figure 16 below shows the number of Bond members in each category. The results present a broadly positive picture of Bond members’ growth over the period. Forty-four percent of Bond members fall into the “little rise” and “big rise” categories, with a further 19% in the “ticking along” category. Just 16 organisations have seen a big fall in their income, and 28 have seen a small fall in their income.

4.4 Number of Bond members who have grown their income

Using an income typology developed by NCVO, we can see whether the period of overall growth in income has translated into growth for a majority or minority of Bond members. The typology is based on the change in organisations’ income between 2008/09 and 2013/14, and puts each organisation into one of nine categories as outlined in figure 15.

Figure 15: Definition of typology categories for all charities based on the change in their income between 2008/09 and 2013/14

Typology category Definition

Missing Income was zero in 2013/14

Up then down The upper income reached was more than double the income in both 2008/09 and 2013/14

Big fall Income halved or more between 2008/09 and 2013/14

Little fall Income fell by one-fifth or more between 2008/09 and 2013/14

Ticking along Income in 2013/14 was within 20% of the income in 2008/09

Little rise Income rose by one-fifth or more between 2008/09 and 2013/14

Big rise Income doubled or more between 2008/09 and 2013/14

Down then up The lowest income reached was less than half the income in both 2008/09 and 2013/14

From nothing Income was zero in 2008/09 and greater than zero in 2013/14

Figure 16: Number of Bond members by income change typology

5

12

16

28

63

71

78

16

49

Missing

Up then down

Big fall

Little fall

Ticking along

Little rise

Big rise

Down then up

From nothing

5

12

16

28

63

71

78

16

49

Figure 16: Bond members by income growth typology

Missing

Up then down

Big fall

Little fall

Ticking along

Little rise

Big rise

Down then up

From nothing

Financial trends for UK-based INGOs 16

We have segmented the Bond membership into the following categories for this analysis:

• Organisations with income under £2m

• Organisations with income between £2m and £5m

• Organisations with income between £5m and £20m

• Organisations with income between £20m and £40m

• Organisations with income over £40m.

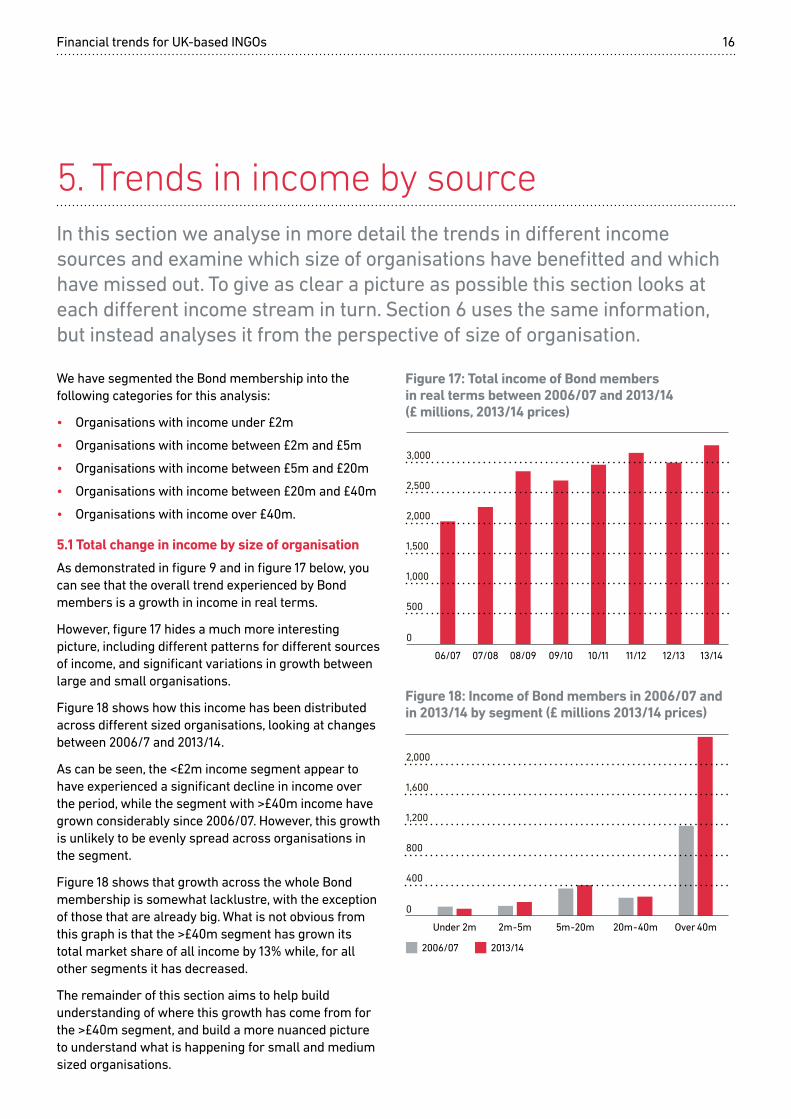

5.1 Total change in income by size of organisation

As demonstrated in figure 9 and in figure 17 below, you can see that the overall trend experienced by Bond members is a growth in income in real terms.

However, figure 17 hides a much more interesting picture, including different patterns for different sources of income, and significant variations in growth between large and small organisations.

Figure 18 shows how this income has been distributed across different sized organisations, looking at changes between 2006/7 and 2013/14.

As can be seen, the <£2m income segment appear to have experienced a significant decline in income over the period, while the segment with >£40m income have grown considerably since 2006/07. However, this growth is unlikely to be evenly spread across organisations in the segment.

Figure 18 shows that growth across the whole Bond membership is somewhat lacklustre, with the exception of those that are already big. What is not obvious from this graph is that the >£40m segment has grown its total market share of all income by 13% while, for all other segments it has decreased.

The remainder of this section aims to help build understanding of where this growth has come from for the >£40m segment, and build a more nuanced picture to understand what is happening for small and medium sized organisations.

5. Trends in income by sourceIn this section we analyse in more detail the trends in different income sources and examine which size of organisations have benefitted and which have missed out. To give as clear a picture as possible this section looks at each different income stream in turn. Section 6 uses the same information, but instead analyses it from the perspective of size of organisation.

Figure 17: Total income of Bond members in real terms between 2006/07 and 2013/14 (£ millions, 2013/14 prices)

500

1,000

0

1,500

2,000

2,500

3,000

06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

Figure 18: Income of Bond members in 2006/07 and in 2013/14 by segment (£ millions 2013/14 prices)

2006/07 2013/14

400

800

0

1,200

1,600

2,000

Under 2m 2m-5m 5m-20m 20m-40m Over 40m

Financial trends for UK-based INGOs 17

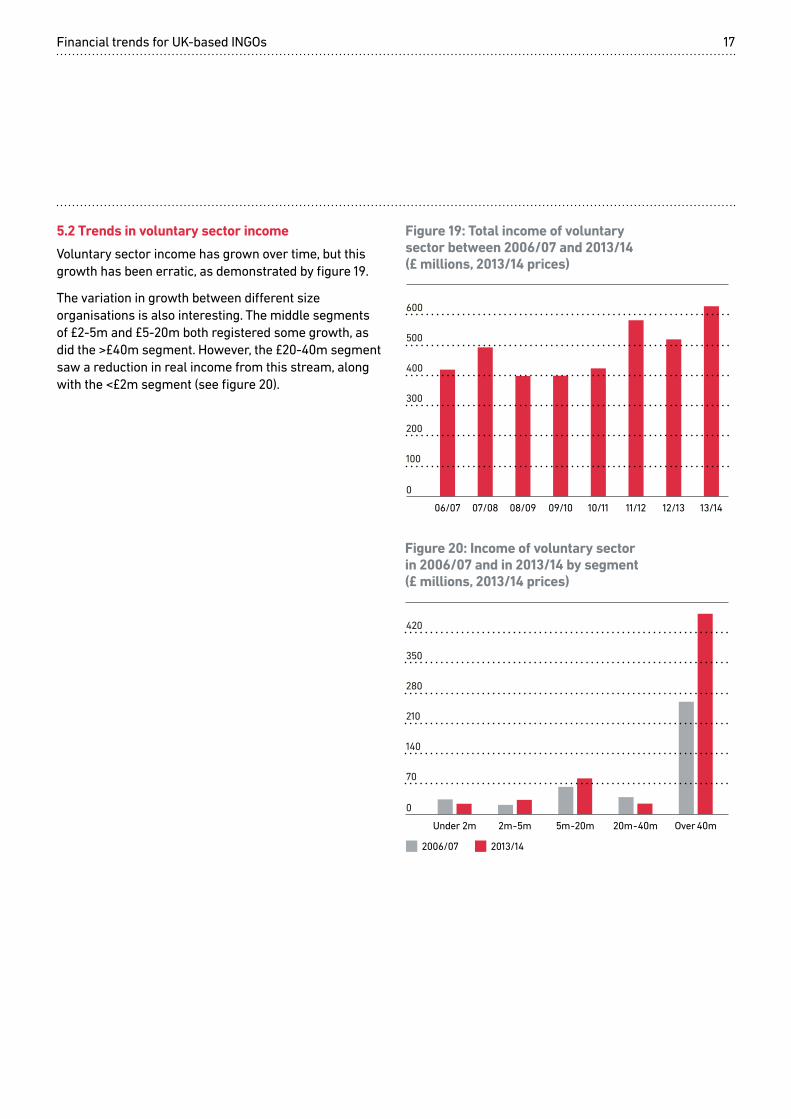

5.2 Trends in voluntary sector income

Voluntary sector income has grown over time, but this growth has been erratic, as demonstrated by figure 19.

The variation in growth between different size organisations is also interesting. The middle segments of £2-5m and £5-20m both registered some growth, as did the >£40m segment. However, the £20-40m segment saw a reduction in real income from this stream, along with the <£2m segment (see figure 20).

Figure 19: Total income of voluntary sector between 2006/07 and 2013/14 (£ millions, 2013/14 prices)

100

200

0

300

400

500

600

06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

2006/07 2013/14

70

140

0

210

280

350

420

Under 2m 2m-5m 5m-20m 20m-40m Over 40m

Figure 20: Income of voluntary sector in 2006/07 and in 2013/14 by segment (£ millions, 2013/14 prices)

Financial trends for UK-based INGOs 18

Figure 22: Corporate income in 2006/07 and in 2013/14 by segment (£ millions, 2013/14 prices)

2006/07 2013/14

14

28

0

42

56

70

84

Under 2m 2m-5m 5m-20m 20m-40m Over 40m

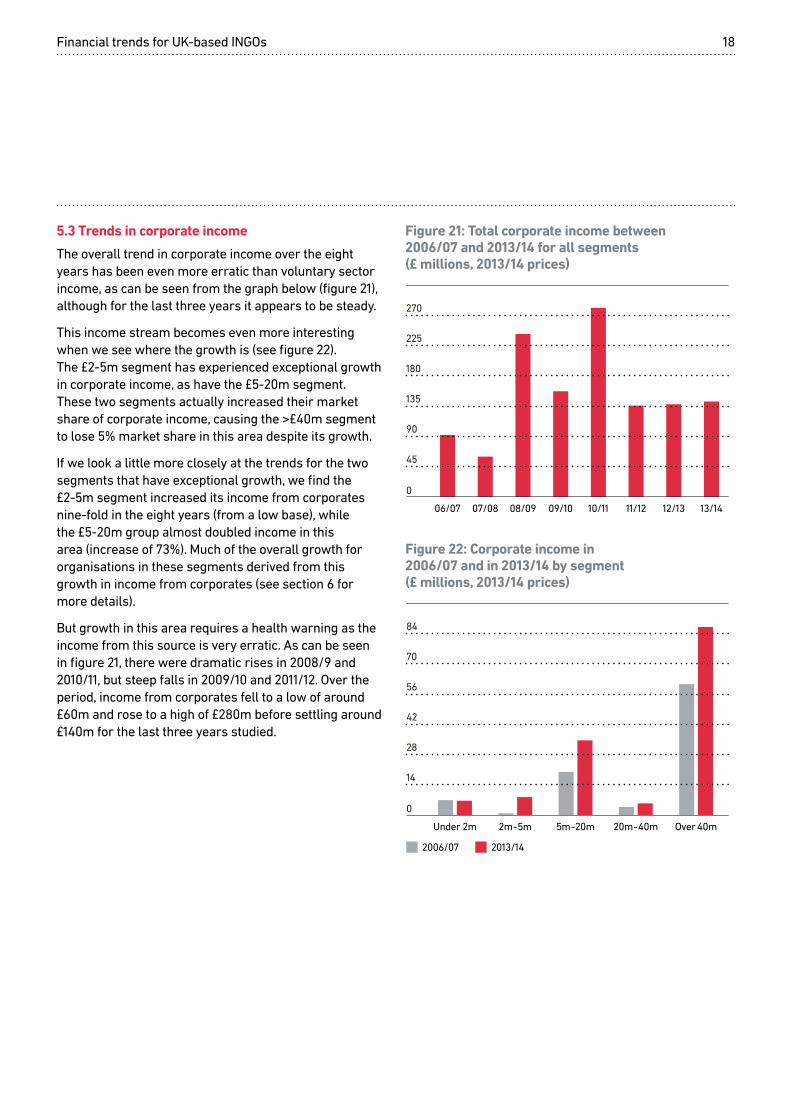

5.3 Trends in corporate income

The overall trend in corporate income over the eight years has been even more erratic than voluntary sector income, as can be seen from the graph below (figure 21), although for the last three years it appears to be steady.

This income stream becomes even more interesting when we see where the growth is (see figure 22). The £2-5m segment has experienced exceptional growth in corporate income, as have the £5-20m segment. These two segments actually increased their market share of corporate income, causing the >£40m segment to lose 5% market share in this area despite its growth.

If we look a little more closely at the trends for the two segments that have exceptional growth, we find the £2-5m segment increased its income from corporates nine-fold in the eight years (from a low base), while the £5-20m group almost doubled income in this area (increase of 73%). Much of the overall growth for organisations in these segments derived from this growth in income from corporates (see section 6 for more details).

But growth in this area requires a health warning as the income from this source is very erratic. As can be seen in figure 21, there were dramatic rises in 2008/9 and 2010/11, but steep falls in 2009/10 and 2011/12. Over the period, income from corporates fell to a low of around £60m and rose to a high of £280m before settling around £140m for the last three years studied.

Figure 21: Total corporate income between 2006/07 and 2013/14 for all segments (£ millions, 2013/14 prices)

45

90

0

135

180

225

270

06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

Financial trends for UK-based INGOs 19

5.4 Trends in government grants

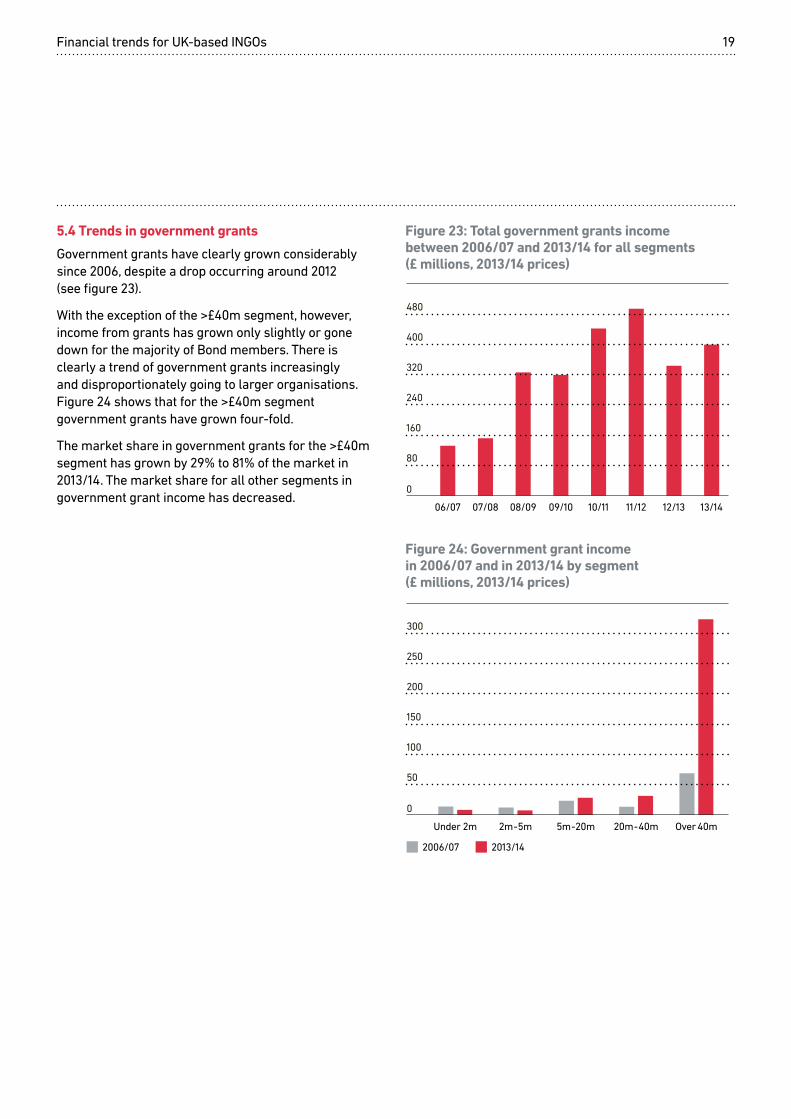

Government grants have clearly grown considerably since 2006, despite a drop occurring around 2012 (see figure 23).

With the exception of the >£40m segment, however, income from grants has grown only slightly or gone down for the majority of Bond members. There is clearly a trend of government grants increasingly and disproportionately going to larger organisations. Figure 24 shows that for the >£40m segment government grants have grown four-fold.

The market share in government grants for the >£40m segment has grown by 29% to 81% of the market in 2013/14. The market share for all other segments in government grant income has decreased.

Figure 23: Total government grants income between 2006/07 and 2013/14 for all segments (£ millions, 2013/14 prices)

80

160

0

240

320

400

480

06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

2006/07 2013/14

50

100

0

150

200

250

300

Under 2m 2m-5m 5m-20m 20m-40m Over 40m

Figure 24: Government grant income in 2006/07 and in 2013/14 by segment (£ millions, 2013/14 prices)

Financial trends for UK-based INGOs 20

5.5 Trends in government contracts

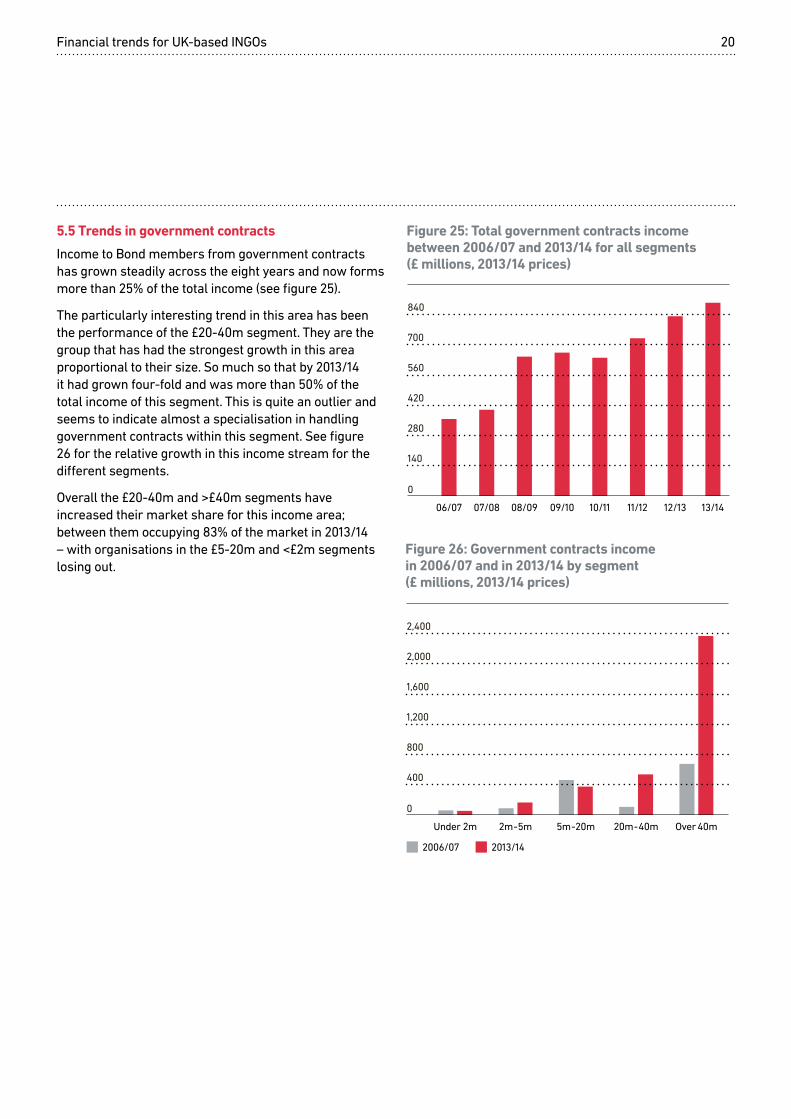

Income to Bond members from government contracts has grown steadily across the eight years and now forms more than 25% of the total income (see figure 25).

The particularly interesting trend in this area has been the performance of the £20-40m segment. They are the group that has had the strongest growth in this area proportional to their size. So much so that by 2013/14 it had grown four-fold and was more than 50% of the total income of this segment. This is quite an outlier and seems to indicate almost a specialisation in handling government contracts within this segment. See figure 26 for the relative growth in this income stream for the different segments.

Overall the £20-40m and >£40m segments have increased their market share for this income area; between them occupying 83% of the market in 2013/14 – with organisations in the £5-20m and <£2m segments losing out.

Figure 25: Total government contracts income between 2006/07 and 2013/14 for all segments (£ millions, 2013/14 prices)

140

280

0

420

560

700

840

06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

2006/07 2013/14

400

800

0

1,200

1,600

2,000

2,400

Under 2m 2m-5m 5m-20m 20m-40m Over 40m

Figure 26: Government contracts income in 2006/07 and in 2013/14 by segment (£ millions, 2013/14 prices)

Financial trends for UK-based INGOs 21

5.6 Trends in earned fundraising income from individuals

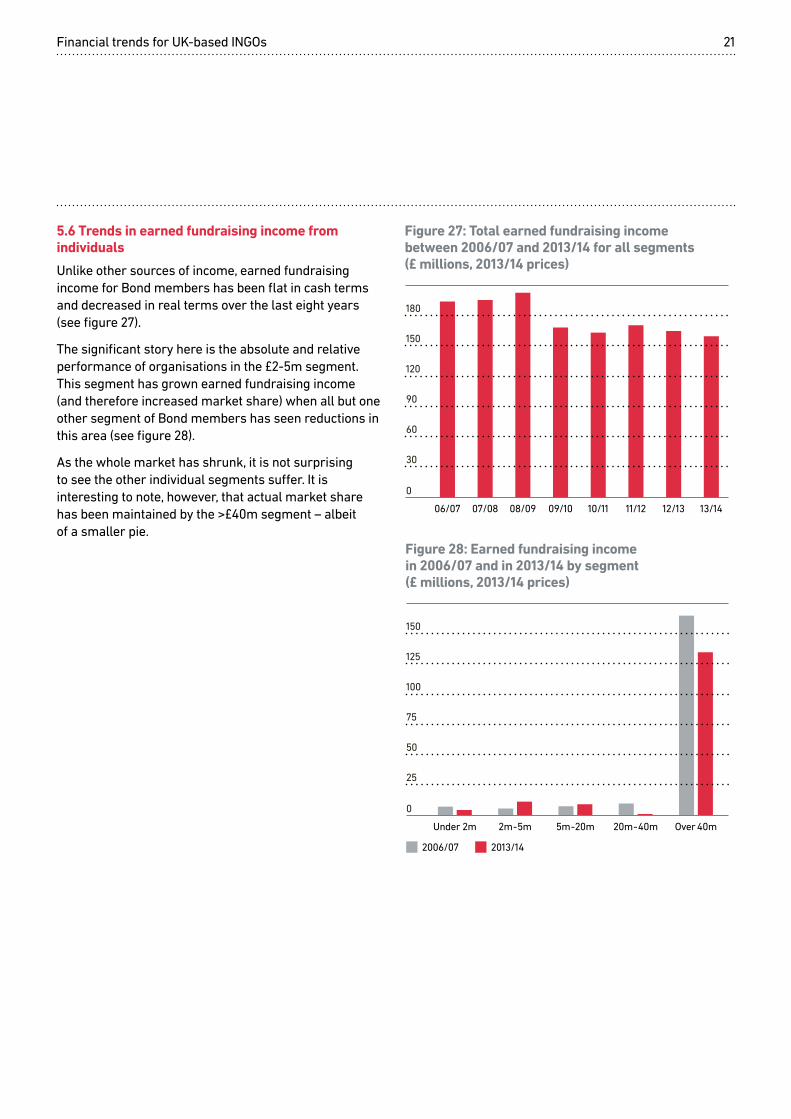

Unlike other sources of income, earned fundraising income for Bond members has been flat in cash terms and decreased in real terms over the last eight years (see figure 27).

The significant story here is the absolute and relative performance of organisations in the £2-5m segment. This segment has grown earned fundraising income (and therefore increased market share) when all but one other segment of Bond members has seen reductions in this area (see figure 28).

As the whole market has shrunk, it is not surprising to see the other individual segments suffer. It is interesting to note, however, that actual market share has been maintained by the >£40m segment – albeit of a smaller pie.

Figure 27: Total earned fundraising income between 2006/07 and 2013/14 for all segments (£ millions, 2013/14 prices)

30

60

0

90

120

150

180

06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

Figure 28: Earned fundraising income in 2006/07 and in 2013/14 by segment (£ millions, 2013/14 prices)

2006/07 2013/14

25

50

0

75

100

125

150

Under 2m 2m-5m 5m-20m 20m-40m Over 40m

Financial trends for UK-based INGOs 22

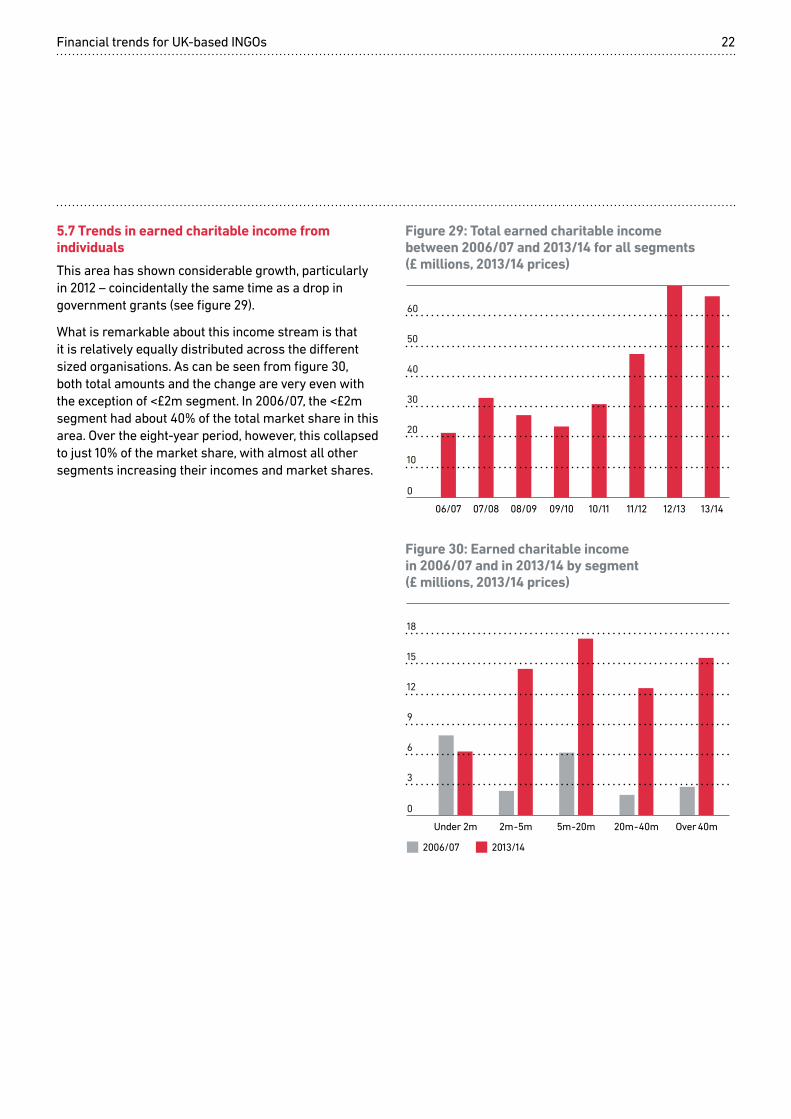

5.7 Trends in earned charitable income from individuals

This area has shown considerable growth, particularly in 2012 – coincidentally the same time as a drop in government grants (see figure 29).

What is remarkable about this income stream is that it is relatively equally distributed across the different sized organisations. As can be seen from figure 30, both total amounts and the change are very even with the exception of <£2m segment. In 2006/07, the <£2m segment had about 40% of the total market share in this area. Over the eight-year period, however, this collapsed to just 10% of the market share, with almost all other segments increasing their incomes and market shares.

10

20

0

30

40

50

60

06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

Figure 29: Total earned charitable income between 2006/07 and 2013/14 for all segments (£ millions, 2013/14 prices)

Figure 30: Earned charitable income in 2006/07 and in 2013/14 by segment (£ millions, 2013/14 prices)

2006/07 2013/14

3

6

0

9

12

15

18

Under 2m 2m-5m 5m-20m 20m-40m Over 40m

Financial trends for UK-based INGOs 23

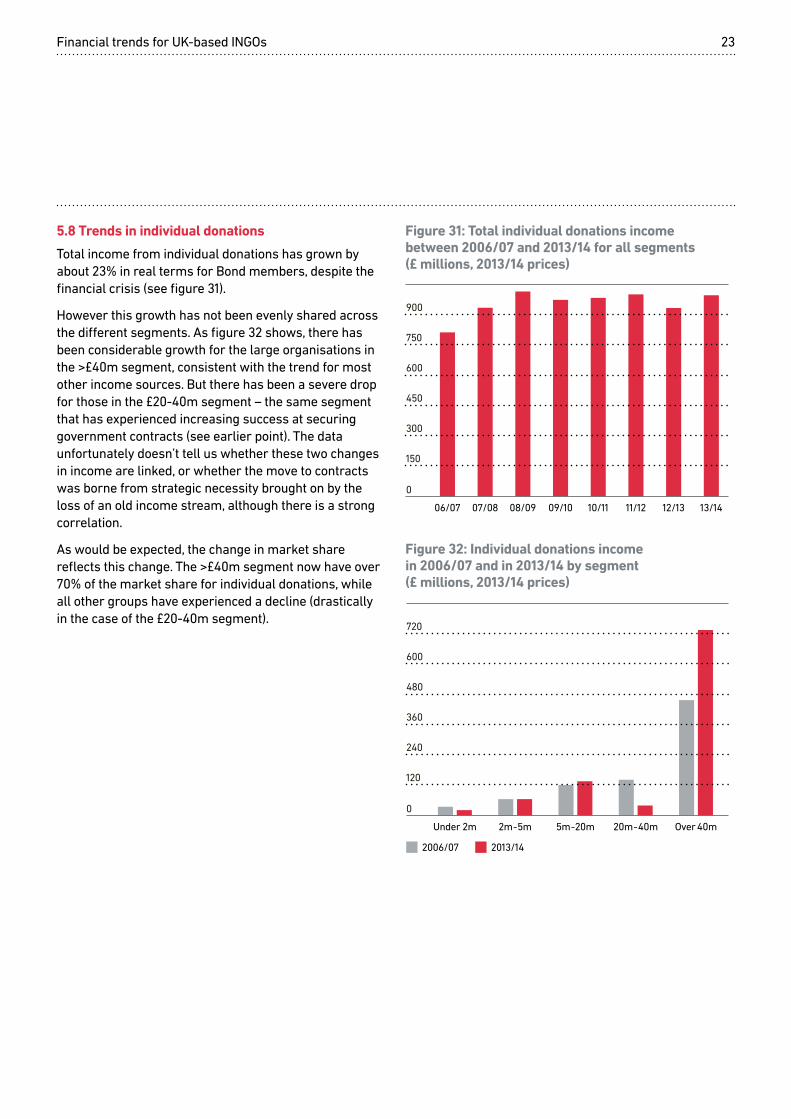

5.8 Trends in individual donations

Total income from individual donations has grown by about 23% in real terms for Bond members, despite the financial crisis (see figure 31).

However this growth has not been evenly shared across the different segments. As figure 32 shows, there has been considerable growth for the large organisations in the >£40m segment, consistent with the trend for most other income sources. But there has been a severe drop for those in the £20-40m segment – the same segment that has experienced increasing success at securing government contracts (see earlier point). The data unfortunately doesn’t tell us whether these two changes in income are linked, or whether the move to contracts was borne from strategic necessity brought on by the loss of an old income stream, although there is a strong correlation.

As would be expected, the change in market share reflects this change. The >£40m segment now have over 70% of the market share for individual donations, while all other groups have experienced a decline (drastically in the case of the £20-40m segment).

Figure 31: Total individual donations income between 2006/07 and 2013/14 for all segments (£ millions, 2013/14 prices)

150

300

0

450

600

750

900

06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

Figure 32: Individual donations income in 2006/07 and in 2013/14 by segment (£ millions, 2013/14 prices)

120

240

0

360

480

600

720

2006/07 2013/14

Under 2m 2m-5m 5m-20m 20m-40m Over 40m

Voluntary sector

Corporate income

Government grants

Government contracts

Individual donations

Earned charitable income

Earned fundraising income

300 5 10 15 20 25

Financial trends for UK-based INGOs 24

6.1 Trends for organisations in the <£2m income segment

Figure 33 shows that small organisations with an income of less than £2m, tend to rely on income from the voluntary sector and from individual donations.

6. Trends in income by size of organisation In this section we examine the changes in income source since 2006/07 from the perspective of each different segment of the Bond membership, as categorised according to their total income in 2013/14. As we look at the different segments we can see that there is very uneven income growth and some quite radically different trends are emerging.

Figure 33: Income in 2013/14 by source, <£2m segment (£ millions)

Figure 34: Percentage change in all income sources between 2006/07 and 2013/14, >£0-2m segment

Voluntary sector

Corporate income

Government grants

Government contracts

Individual donations

Earned charitable income

Earned fundraising income

Overall

0-40% -30% -20% -10%

What is interesting for this segment is the trend over time. Figure 34 shows the percentage change over the period for the segment. It is brutally obvious that income from all sources has shrunk. No other segment of the Bond membership has experienced such negative trends across the board.

Financial trends for UK-based INGOs 25

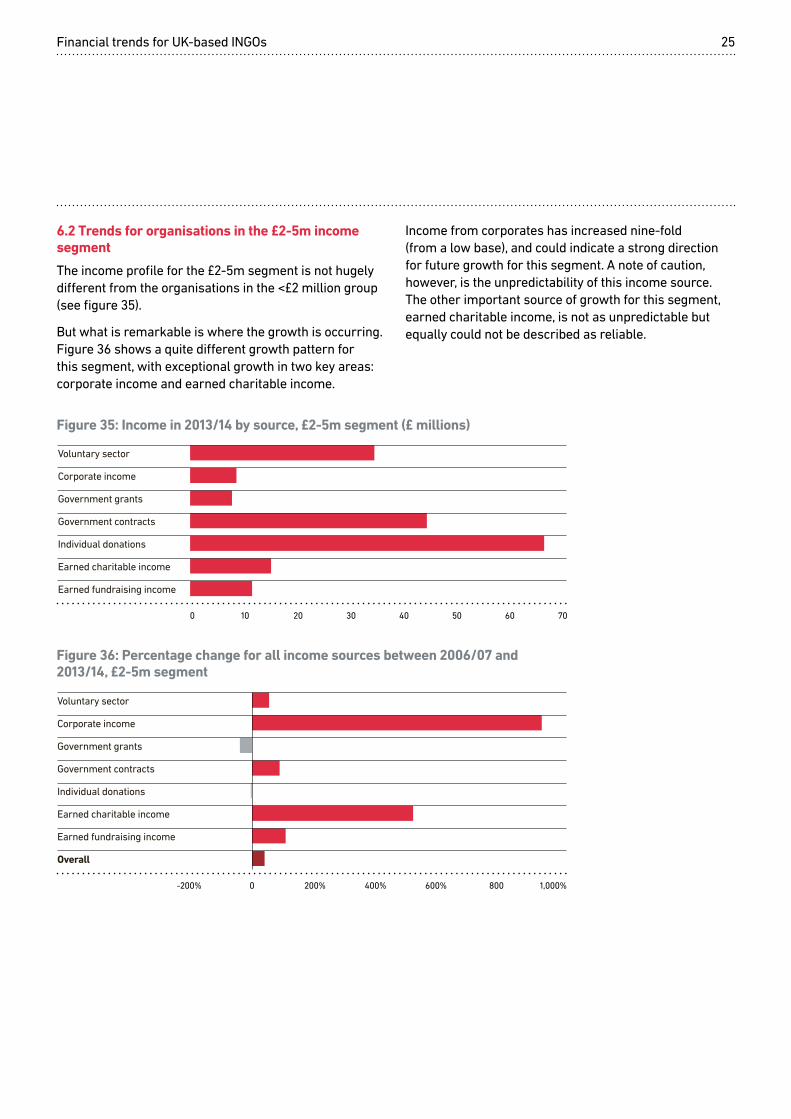

Income from corporates has increased nine-fold (from a low base), and could indicate a strong direction for future growth for this segment. A note of caution, however, is the unpredictability of this income source. The other important source of growth for this segment, earned charitable income, is not as unpredictable but equally could not be described as reliable.

6.2 Trends for organisations in the £2-5m income segment

The income profile for the £2-5m segment is not hugely different from the organisations in the <£2 million group (see figure 35).

But what is remarkable is where the growth is occurring. Figure 36 shows a quite different growth pattern for this segment, with exceptional growth in two key areas: corporate income and earned charitable income.

Voluntary sector

Corporate income

Government grants

Government contracts

Individual donations

Earned charitable income

Earned fundraising income

Overall

Figure 36

1,000%-200% 0 200% 400% 600% 800

Figure 36: Percentage change for all income sources between 2006/07 and 2013/14, £2-5m segment

Figure 35: Income in 2013/14 by source, £2-5m segment (£ millions)

Voluntary sector

Corporate income

Government grants

Government contracts

Individual donations

Earned charitable income

Earned fundraising income

70600 10 20 30 40 50

Financial trends for UK-based INGOs 26

Figure 38 shows that over the eight-year period, income from government contracts has decreased, with a loss of more than 20% market share. Indeed, this segment has lost market share (despite seeing growth) in all income streams apart from corporates and earned fundraising income. In real terms the growth of this segment has effectively been just 1.5% for each year (12.5% in total for the eight sampled years).

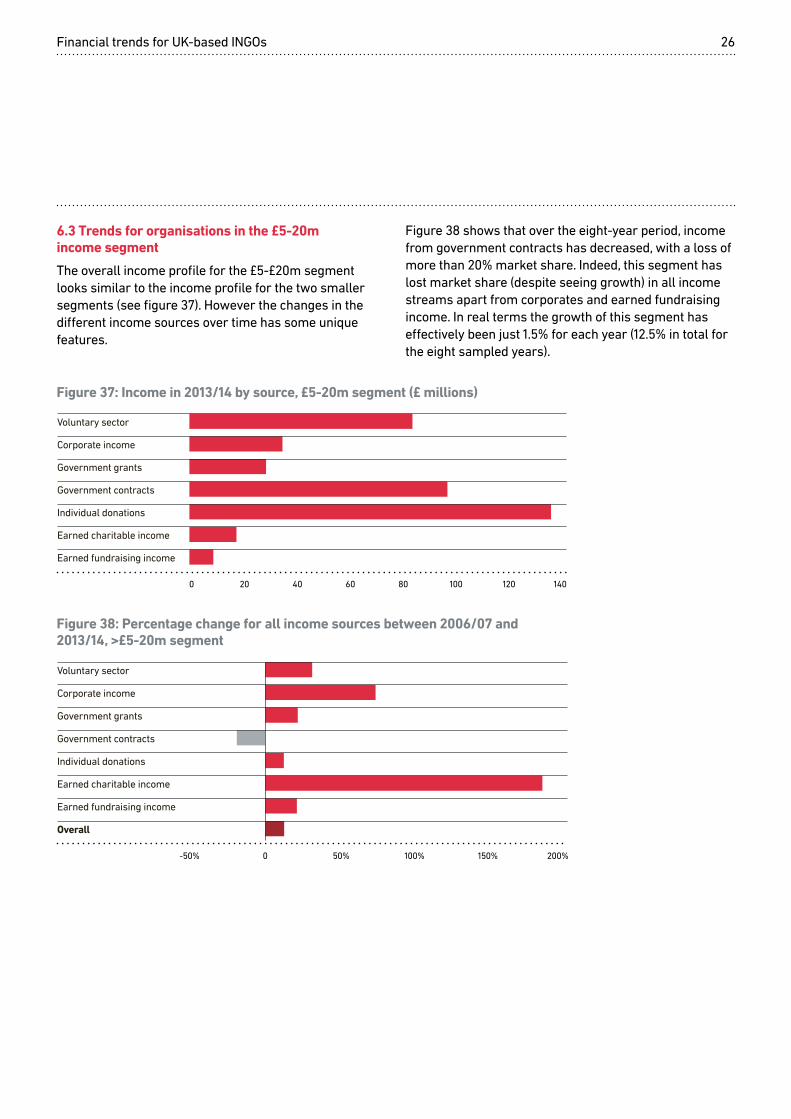

6.3 Trends for organisations in the £5-20m income segment

The overall income profile for the £5-£20m segment looks similar to the income profile for the two smaller segments (see figure 37). However the changes in the different income sources over time has some unique features.

Figure 37: Income in 2013/14 by source, £5-20m segment (£ millions)

Voluntary sector

Corporate income

Government grants

Government contracts

Individual donations

Earned charitable income

Earned fundraising income

1401200 20 40 60 80 100

Figure 38: Percentage change for all income sources between 2006/07 and 2013/14, >£5-20m segment

Voluntary sector

Corporate income

Government grants

Government contracts

Individual donations

Earned charitable income

Earned fundraising income

Overall

200%-50% 0 50% 100% 150%

Financial trends for UK-based INGOs 27

among this segment, this appears part of a deliberate strategy to succeed in these areas. This growth appears to have followed a sharp reduction of income from individual donations, making this segment now highly dependent on government funding, with grants and contracts from government together making up more than two thirds of total income.

The result is that organisations in this segment could increasingly look like government contractors. To survive, they will need to be managing their overheads very tightly and be good at negotiating favourable terms.

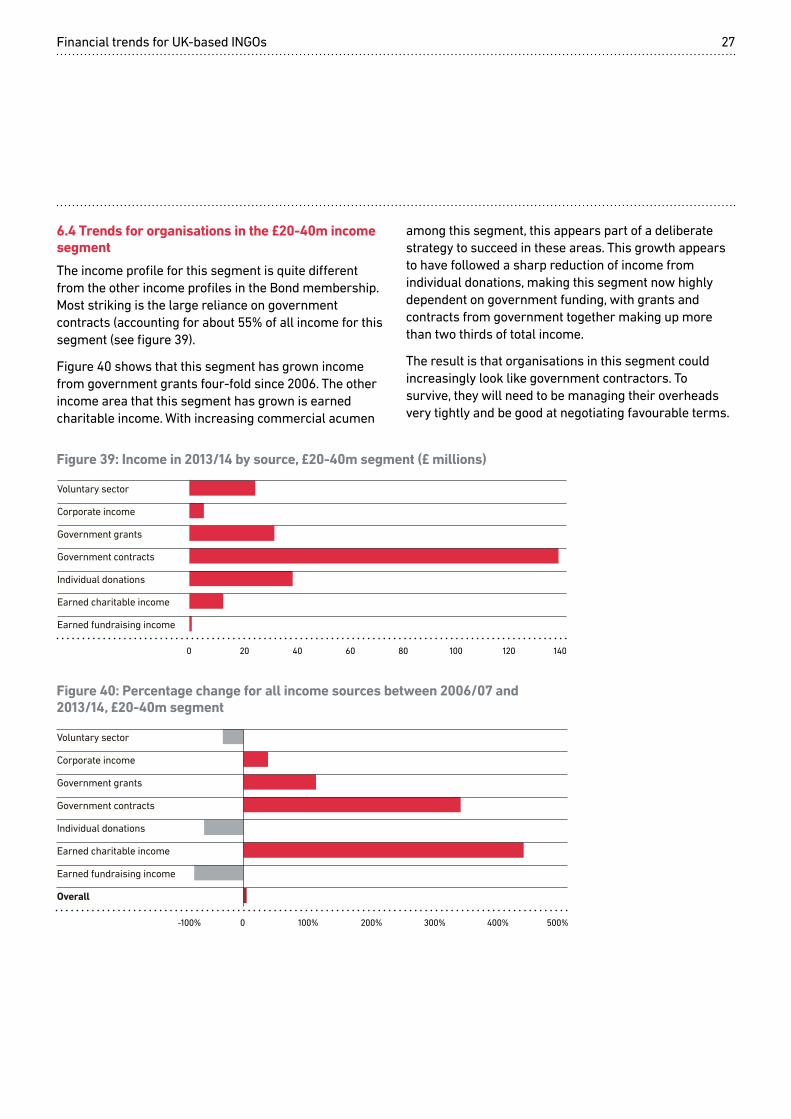

6.4 Trends for organisations in the £20-40m income segment

The income profile for this segment is quite different from the other income profiles in the Bond membership. Most striking is the large reliance on government contracts (accounting for about 55% of all income for this segment (see figure 39).

Figure 40 shows that this segment has grown income from government grants four-fold since 2006. The other income area that this segment has grown is earned charitable income. With increasing commercial acumen

Figure 39: Income in 2013/14 by source, £20-40m segment (£ millions)

Voluntary sector

Corporate income

Government grants

Government contracts

Individual donations

Earned charitable income

Earned fundraising income

1401200 20 40 60 80 100

Figure 40: Percentage change for all income sources between 2006/07 and 2013/14, £20-40m segment

Voluntary sector

Corporate income

Government grants

Government contracts

Individual donations

Earned charitable income

Earned fundraising income

Overall

500%-100% 0 100% 200% 300% 400%

Financial trends for UK-based INGOs 28

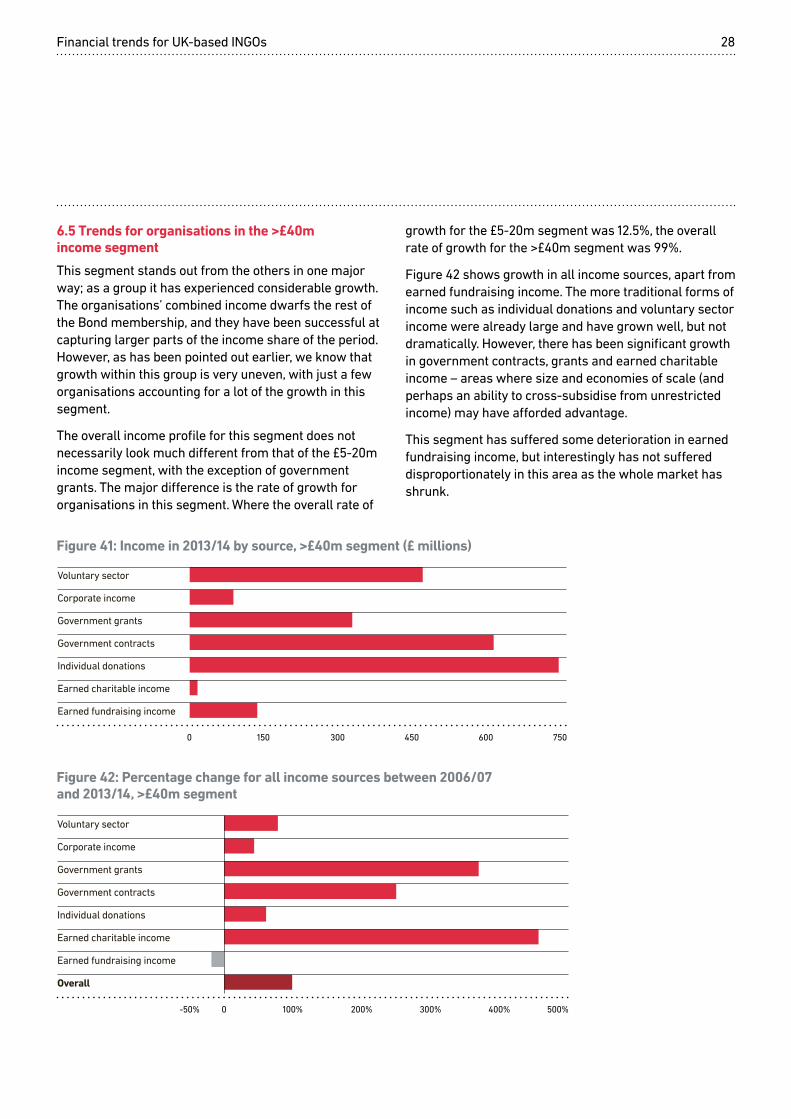

growth for the £5-20m segment was 12.5%, the overall rate of growth for the >£40m segment was 99%.

Figure 42 shows growth in all income sources, apart from earned fundraising income. The more traditional forms of income such as individual donations and voluntary sector income were already large and have grown well, but not dramatically. However, there has been significant growth in government contracts, grants and earned charitable income – areas where size and economies of scale (and perhaps an ability to cross-subsidise from unrestricted income) may have afforded advantage.

This segment has suffered some deterioration in earned fundraising income, but interestingly has not suffered disproportionately in this area as the whole market has shrunk.

6.5 Trends for organisations in the >£40m income segment

This segment stands out from the others in one major way; as a group it has experienced considerable growth. The organisations’ combined income dwarfs the rest of the Bond membership, and they have been successful at capturing larger parts of the income share of the period. However, as has been pointed out earlier, we know that growth within this group is very uneven, with just a few organisations accounting for a lot of the growth in this segment.

The overall income profile for this segment does not necessarily look much different from that of the £5-20m income segment, with the exception of government grants. The major difference is the rate of growth for organisations in this segment. Where the overall rate of

Figure 41: Income in 2013/14 by source, >£40m segment (£ millions)

Voluntary sector

Corporate income

Government grants

Government contracts

Individual donations

Earned charitable income

Earned fundraising income

7500 150 300 450 600

Voluntary sector

Corporate income

Government grants

Government contracts

Individual donations

Earned charitable income

Earned fundraising income

Overall

500%-50% 0 100% 200% 300% 400%

Figure 42: Percentage change for all income sources between 2006/07 and 2013/14, >£40m segment

Financial trends for UK-based INGOs 29

7.1 Fundraising ratios

With the exception of 2007/08, which may be an anomalous year, Bond members have a higher fundraising ratio than UK charities as a whole. This fundraising ratio, which measures the income achieved for every pound spent on generating funds, was £6.97 in 2013/14 for Bond members, compared to £4.70 for UK charities. This ratio is higher than the steady level of around £5, which held between 2008/09 and 2012/13.

7. Other financial trends This section provides information on other important financial trends for Bond members, including fundraising ratios, levels of reserves and net assets.

7.2 Reserves

An organisation’s reserves represent the proportion of their assets that can be readily accessed in the event of a cash flow problem, for example, to meet redundancy costs if an organisation is forced to close. Reserves can be expressed in terms of the months of expenditure that they would cover. According to NCVO’s annual UK Civil Society Almanac, the average amount of reserves held by UK operating charities (excluding grant-making foundations with large assets) is seven months.

Bond members’ reserves are smaller than this on average, representing less than three months of expenditure in 2013/14. This level has fallen since 2008/09 when it was over three months.

Figure 43: Income generated per £ spent between 2007/08 and 2013/14 (£)

07/08 08/09 09/10 10/11 11/12 12/13 13/14

All charities

Bond members

3

4

5

6

7

8

Figure 44: Level of reserves between 2006/07 and 2013/14 (months of expenditure)

06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

2.5

3

2

3.5

4

Financial trends for UK-based INGOs 30

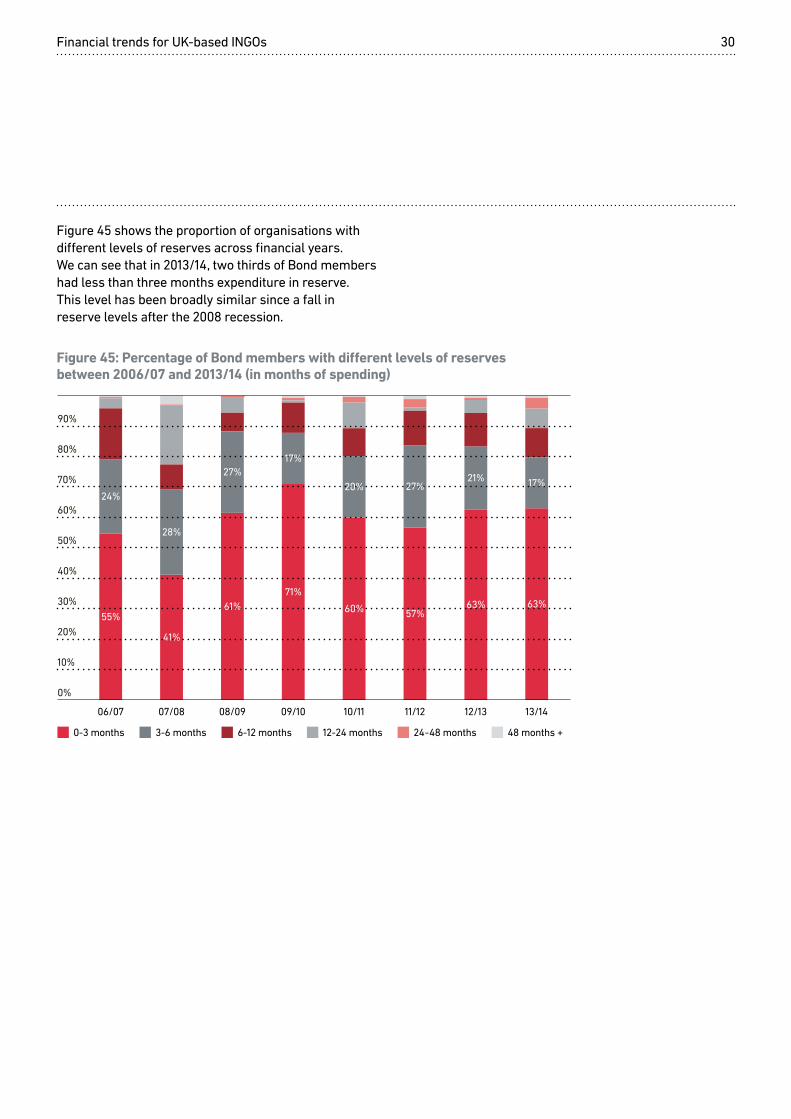

Figure 45 shows the proportion of organisations with different levels of reserves across financial years. We can see that in 2013/14, two thirds of Bond members had less than three months expenditure in reserve. This level has been broadly similar since a fall in reserve levels after the 2008 recession.

Figure 45: Percentage of Bond members with different levels of reserves between 2006/07 and 2013/14 (in months of spending)

06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

10%

20%

0%

30%

40%

50%

60%

70%

80%

90%

0-3 months 3-6 months 6-12 months 12-24 months 24-48 months 48 months +

17%

20% 27%21% 17%

27%

28%

24%

71%

60% 57%63% 63%61%

41%

55%

Financial trends for UK-based INGOs 31

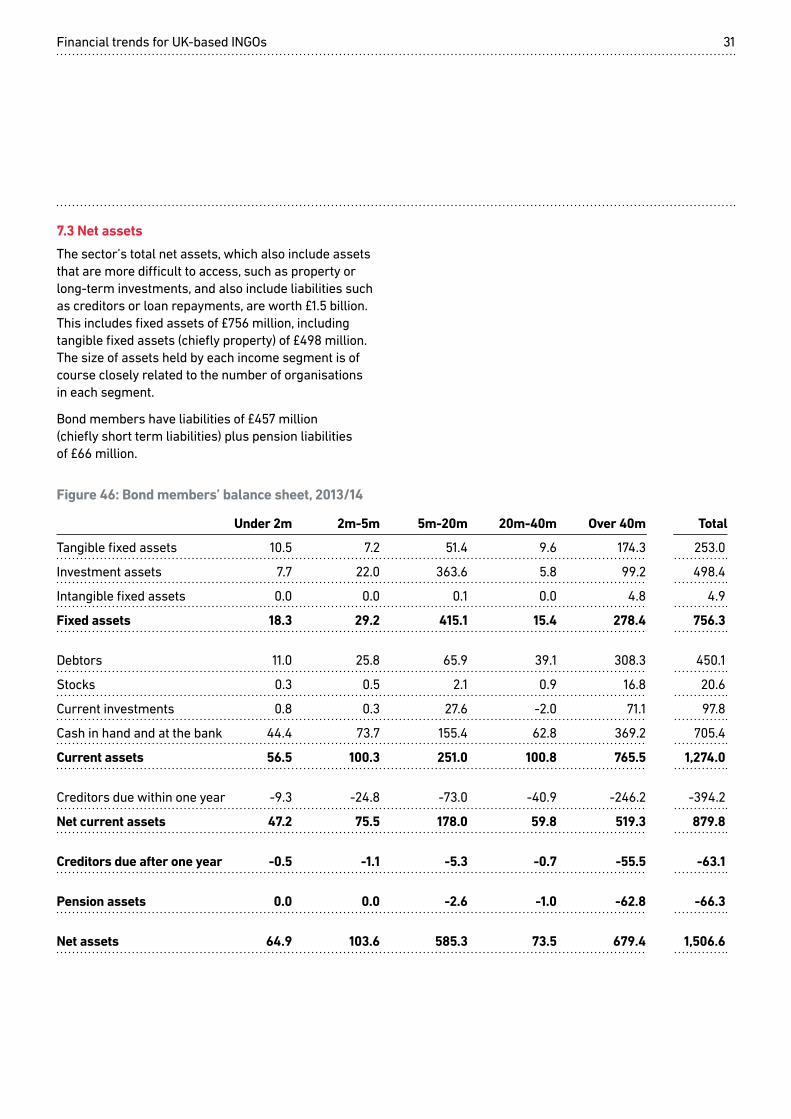

7.3 Net assets

The sector’s total net assets, which also include assets that are more difficult to access, such as property or long-term investments, and also include liabilities such as creditors or loan repayments, are worth £1.5 billion. This includes fixed assets of £756 million, including tangible fixed assets (chiefly property) of £498 million. The size of assets held by each income segment is of course closely related to the number of organisations in each segment.

Bond members have liabilities of £457 million (chiefly short term liabilities) plus pension liabilities of £66 million.

Figure 46: Bond members’ balance sheet, 2013/14

Under 2m 2m-5m 5m-20m 20m-40m Over 40m Total

Tangible fixed assets 10.5 7.2 51.4 9.6 174.3 253.0

Investment assets 7.7 22.0 363.6 5.8 99.2 498.4

Intangible fixed assets 0.0 0.0 0.1 0.0 4.8 4.9

Fixed assets 18.3 29.2 415.1 15.4 278.4 756.3

Debtors 11.0 25.8 65.9 39.1 308.3 450.1

Stocks 0.3 0.5 2.1 0.9 16.8 20.6

Current investments 0.8 0.3 27.6 -2.0 71.1 97.8

Cash in hand and at the bank 44.4 73.7 155.4 62.8 369.2 705.4

Current assets 56.5 100.3 251.0 100.8 765.5 1,274.0

Creditors due within one year -9.3 -24.8 -73.0 -40.9 -246.2 -394.2

Net current assets 47.2 75.5 178.0 59.8 519.3 879.8

Creditors due after one year -0.5 -1.1 -5.3 -0.7 -55.5 -63.1

Pension assets 0.0 0.0 -2.6 -1.0 -62.8 -66.3

Net assets 64.9 103.6 585.3 73.5 679.4 1,506.6

Financial trends for UK-based INGOs 32

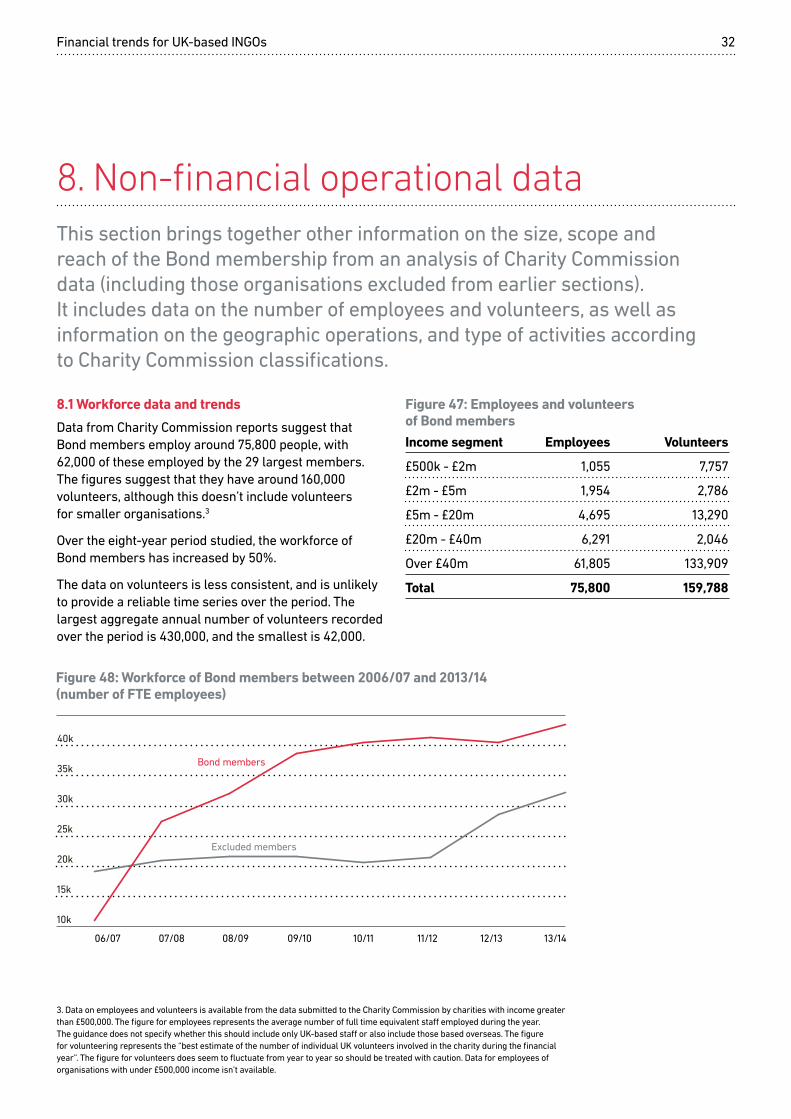

8.1 Workforce data and trends

Data from Charity Commission reports suggest that Bond members employ around 75,800 people, with 62,000 of these employed by the 29 largest members. The figures suggest that they have around 160,000 volunteers, although this doesn’t include volunteers for smaller organisations.3

Over the eight-year period studied, the workforce of Bond members has increased by 50%.

The data on volunteers is less consistent, and is unlikely to provide a reliable time series over the period. The largest aggregate annual number of volunteers recorded over the period is 430,000, and the smallest is 42,000.

8. Non-financial operational dataThis section brings together other information on the size, scope and reach of the Bond membership from an analysis of Charity Commission data (including those organisations excluded from earlier sections). It includes data on the number of employees and volunteers, as well as information on the geographic operations, and type of activities according to Charity Commission classifications.

Figure 47: Employees and volunteers of Bond membersIncome segment Employees Volunteers

£500k - £2m 1,055 7,757

£2m - £5m 1,954 2,786

£5m - £20m 4,695 13,290

£20m - £40m 6,291 2,046

Over £40m 61,805 133,909

Total 75,800 159,788

3. Data on employees and volunteers is available from the data submitted to the Charity Commission by charities with income greater than £500,000. The figure for employees represents the average number of full time equivalent staff employed during the year. The guidance does not specify whether this should include only UK-based staff or also include those based overseas. The figure for volunteering represents the “best estimate of the number of individual UK volunteers involved in the charity during the financial year”. The figure for volunteers does seem to fluctuate from year to year so should be treated with caution. Data for employees of organisations with under £500,000 income isn’t available.

Figure 48: Workforce of Bond members between 2006/07 and 2013/14 (number of FTE employees)

06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

15k

20k

10k

25k

30k

35k

40k

Excluded members

Bond members

Financial trends for UK-based INGOs 33

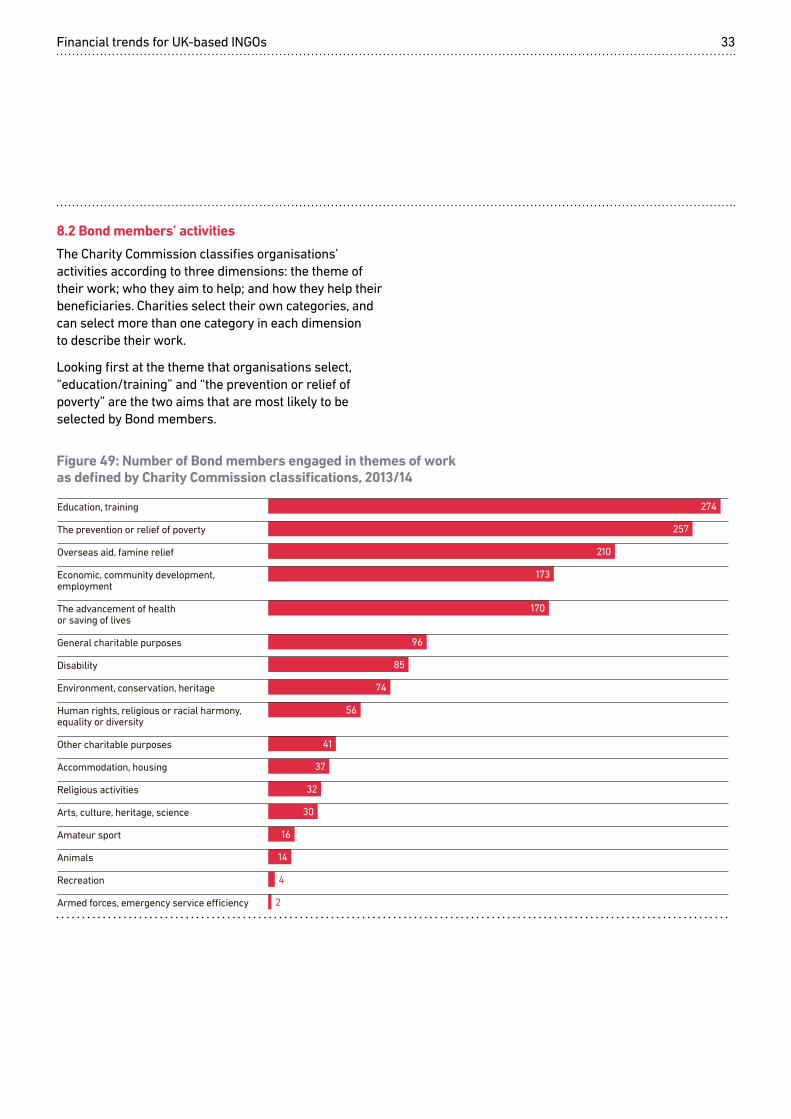

8.2 Bond members’ activities

The Charity Commission classifies organisations’ activities according to three dimensions: the theme of their work; who they aim to help; and how they help their beneficiaries. Charities select their own categories, and can select more than one category in each dimension to describe their work.

Looking first at the theme that organisations select, “education/training” and “the prevention or relief of poverty” are the two aims that are most likely to be selected by Bond members.

Figure 49: Number of Bond members engaged in themes of work as defined by Charity Commission classifications, 2013/14

Education, training

The prevention or relief of poverty

Overseas aid, famine relief

Economic, community development, employment

The advancement of health or saving of lives

General charitable purposes

Disability

Environment, conservation, heritage

Human rights, religious or racial harmony, equality or diversity

Other charitable purposes

Accommodation, housing

Religious activities

Arts, culture, heritage, science

Amateur sport

Animals

Recreation

Armed forces, emergency service e�ciency

274

257

210

173

170

96

85

74

56

41

37

32

30

16

14

4

2

Financial trends for UK-based INGOs 34

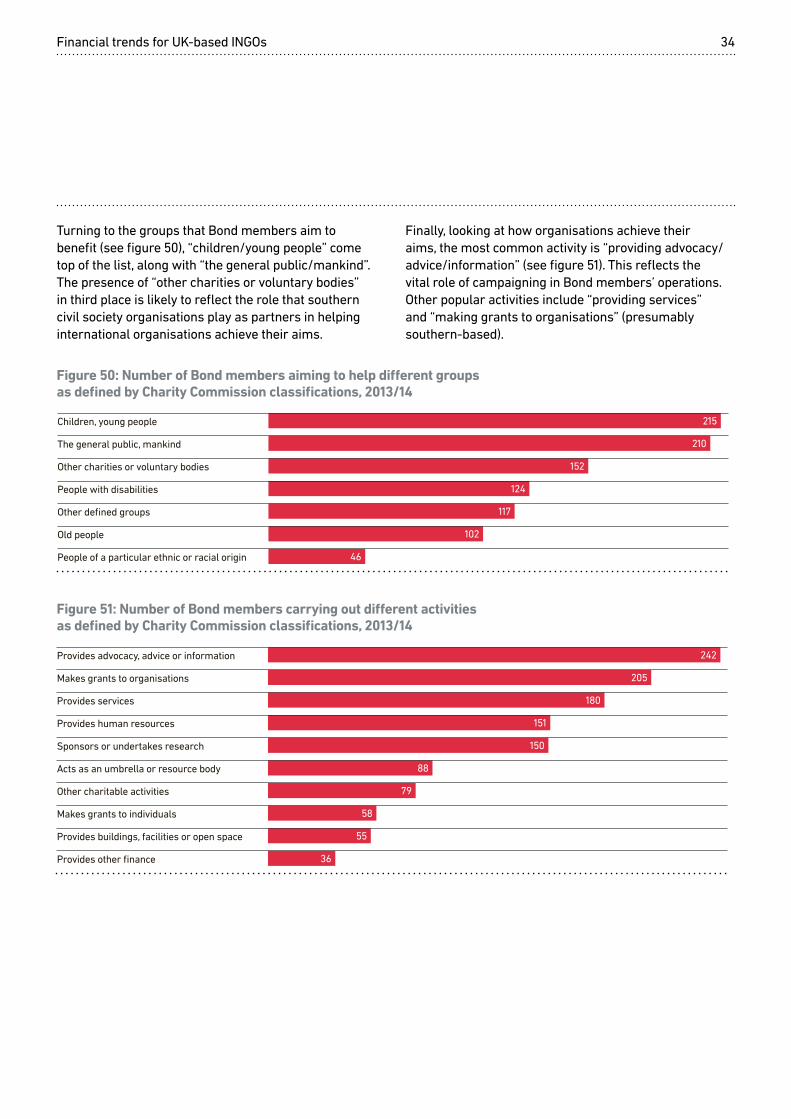

Turning to the groups that Bond members aim to benefit (see figure 50), “children/young people” come top of the list, along with “the general public/mankind”. The presence of “other charities or voluntary bodies” in third place is likely to reflect the role that southern civil society organisations play as partners in helping international organisations achieve their aims.

Figure 50: Number of Bond members aiming to help different groups as defined by Charity Commission classifications, 2013/14

Children, young people

The general public, mankind

Other charities or voluntary bodies

People with disabilities

Other defined groups

Old people

People of a particular ethnic or racial origin

215

210

152

124

117

102

46

Figure 51: Number of Bond members carrying out different activities as defined by Charity Commission classifications, 2013/14

Provides advocacy, advice or information

Makes grants to organisations

Provides services

Provides human resources

Sponsors or undertakes research

Acts as an umbrella or resource body

Other charitable activities

Makes grants to individuals

Provides buildings, facilities or open space

Provides other finance

242

205

180

151

150

88

79

58

55

36

Finally, looking at how organisations achieve their aims, the most common activity is “providing advocacy/advice/information” (see figure 51). This reflects the vital role of campaigning in Bond members’ operations. Other popular activities include “providing services” and “making grants to organisations” (presumably southern-based).

Financial trends for UK-based INGOs 35

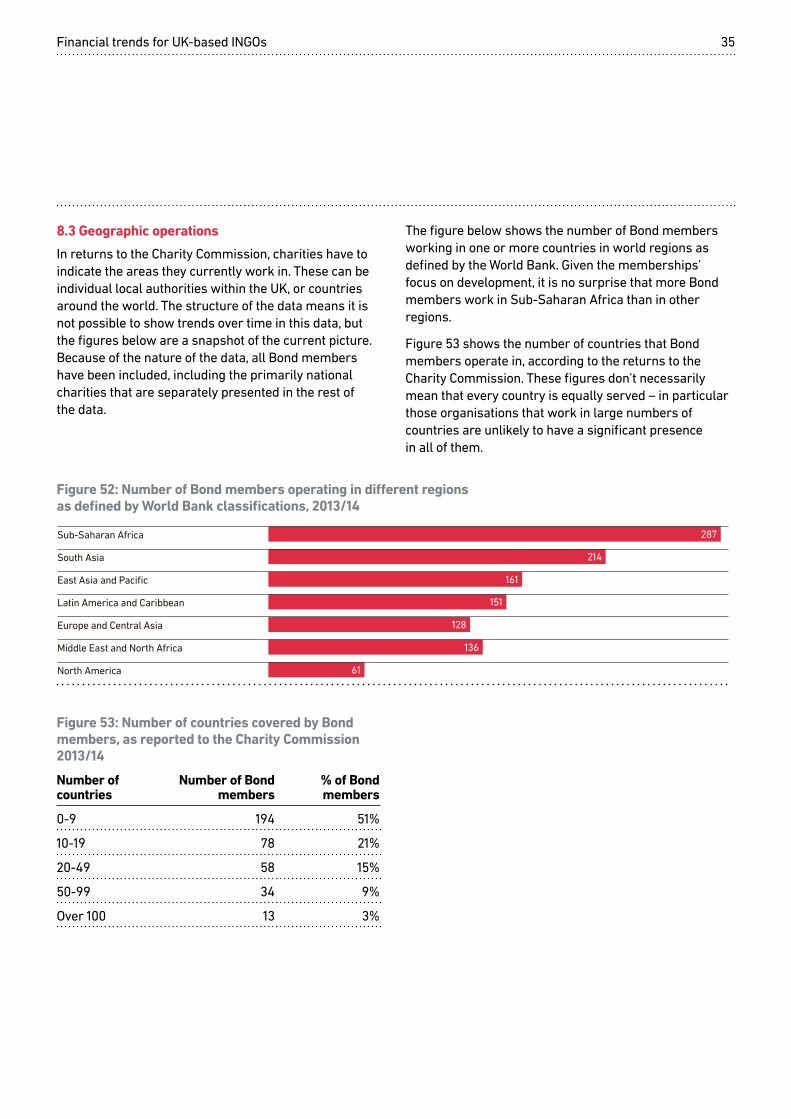

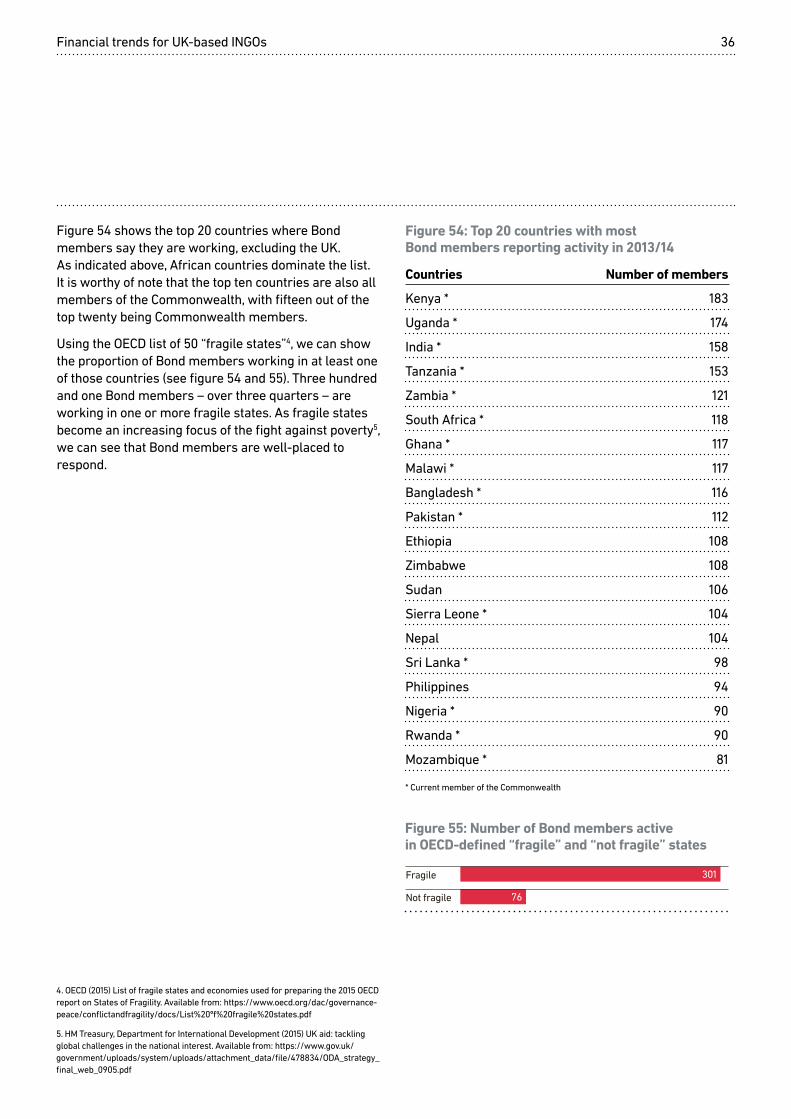

Figure 53: Number of countries covered by Bond members, as reported to the Charity Commission 2013/14

Number of Number of Bond % of Bond countries members members

0-9 194 51%

10-19 78 21%

20-49 58 15%

50-99 34 9%

Over 100 13 3%

8.3 Geographic operations

In returns to the Charity Commission, charities have to indicate the areas they currently work in. These can be individual local authorities within the UK, or countries around the world. The structure of the data means it is not possible to show trends over time in this data, but the figures below are a snapshot of the current picture. Because of the nature of the data, all Bond members have been included, including the primarily national charities that are separately presented in the rest of the data.

Figure 52: Number of Bond members operating in different regions as defined by World Bank classifications, 2013/14

Sub-Saharan Africa

South Asia

East Asia and Pacific

Latin America and Caribbean

Europe and Central Asia

Middle East and North Africa

North America

287

214

161

151

128

136

61

The figure below shows the number of Bond members working in one or more countries in world regions as defined by the World Bank. Given the memberships’ focus on development, it is no surprise that more Bond members work in Sub-Saharan Africa than in other regions.

Figure 53 shows the number of countries that Bond members operate in, according to the returns to the Charity Commission. These figures don’t necessarily mean that every country is equally served – in particular those organisations that work in large numbers of countries are unlikely to have a significant presence in all of them.

Financial trends for UK-based INGOs 36

Figure 54: Top 20 countries with most Bond members reporting activity in 2013/14

Countries Number of members

Kenya * 183

Uganda * 174

India * 158

Tanzania * 153

Zambia * 121

South Africa * 118

Ghana * 117

Malawi * 117

Bangladesh * 116

Pakistan * 112

Ethiopia 108

Zimbabwe 108

Sudan 106

Sierra Leone * 104

Nepal 104

Sri Lanka * 98

Philippines 94

Nigeria * 90

Rwanda * 90

Mozambique * 81

* Current member of the Commonwealth

Figure 54 shows the top 20 countries where Bond members say they are working, excluding the UK. As indicated above, African countries dominate the list. It is worthy of note that the top ten countries are also all members of the Commonwealth, with fifteen out of the top twenty being Commonwealth members.

Using the OECD list of 50 “fragile states”4, we can show the proportion of Bond members working in at least one of those countries (see figure 54 and 55). Three hundred and one Bond members – over three quarters – are working in one or more fragile states. As fragile states become an increasing focus of the fight against poverty5, we can see that Bond members are well-placed to respond.

Figure 55: Number of Bond members active in OECD-defined “fragile” and “not fragile” states

301

76

Fragile

Not fragile

4. OECD (2015) List of fragile states and economies used for preparing the 2015 OECD report on States of Fragility. Available from: https://www.oecd.org/dac/governance-peace/conflictandfragility/docs/List%20of%20fragile%20states.pdf

5. HM Treasury, Department for International Development (2015) UK aid: tackling global challenges in the national interest. Available from: https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/478834/ODA_strategy_final_web_0905.pdf

Financial trends for UK-based INGOs 37

Code Country Number of members

AF Afghanistan 72

BD Bangladesh 116

BA Bosnia & Herzegovina 40

BI Burundi 52

CM Cameroon 58

CF Central African Republic 42

TD Chad 43

KM Comoros 11

CD Congo (D. R.) 76

CG Congo, Rep. of 34

CI Cote d'Ivoire 48

EG Egypt 53

ER Eritrea 29

ET Ethiopia 108

GN Guinea 35

GW Guinea Bissau 22

HT Haiti 67

IQ Iraq 51

KE Kenya 183

KI Kiribati 14

XK Kosovo 25

LR Liberia 70

LY Libya 26

MG Madagascar 40

MW Malawi 117

Code Country Number of members

ML Mali 59

MH Marshall Islands 8

MR Mauritania 31

FM Micronesia 9

MM Myanmar 77

NP Nepal 104

NE Niger 54

NG Nigeria 90

KP North Korea 18

PK Pakistan 112

RW Rwanda 90

SL Sierra Leone 104

SB Solomon Islands 23

SO Somalia 70

SS South Sudan 0

LK Sri Lanka 98

SD Sudan 106

SY Syria 56

TL Timor-Leste 28

TG Togo 38

TV Tuvalu 10

UG Uganda 174

PS West Bank & Gaza 67

YE Yemen 41

ZW Zimbabwe 108

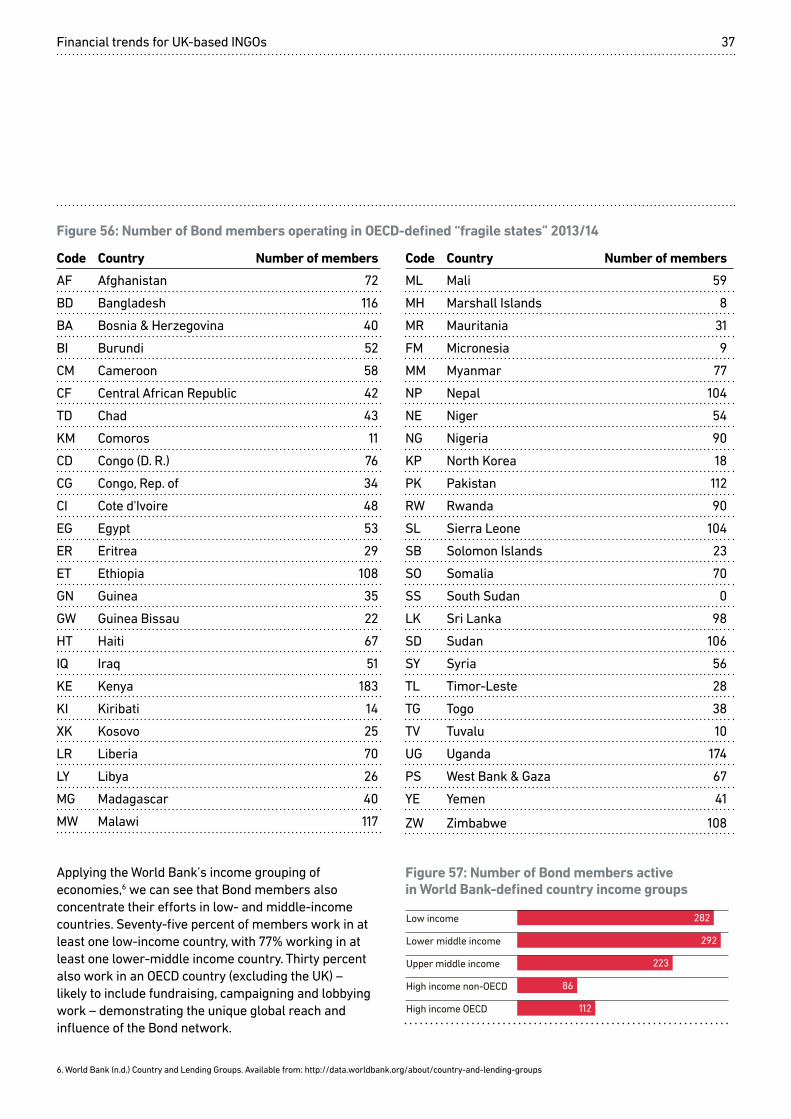

Figure 56: Number of Bond members operating in OECD-defined “fragile states” 2013/14

Applying the World Bank’s income grouping of economies,6 we can see that Bond members also concentrate their efforts in low- and middle-income countries. Seventy-five percent of members work in at least one low-income country, with 77% working in at least one lower-middle income country. Thirty percent also work in an OECD country (excluding the UK) – likely to include fundraising, campaigning and lobbying work – demonstrating the unique global reach and influence of the Bond network.

Figure 57: Number of Bond members active in World Bank-defined country income groups

282

292

Low income

Lower middle income

Upper middle income

High income non-OECD

High income OECD

223

86

112

6. World Bank (n.d.) Country and Lending Groups. Available from: http://data.worldbank.org/about/country-and-lending-groups

Financial trends for UK-based INGOs 38

9. ConclusionThis research found the Bond membership has experienced a period of sustained growth in income over the eight years studied, largely as a result of an increase in income from UK central government and overseas governments (particularly in the form of contracts).

Income from government is now the single largest income source for Bond members. Income from individuals and the voluntary sector also grew in the period, albeit much more modestly, while income from the corporate sector did not increase substantially and remains a relatively small source of funding.

Despite the overall picture of income growth, however, the distribution of income across the Bond membership was highly uneven – with lacklustre growth in all segments apart from the largest organsations. The segment of organisations with an income of >£40m appears to be doing best and increasing their market share of most income streams – including government contracts and grants, voluntary sector income, individual donations and earned charitable income. However, we know that this hides considerable differences in growth within this segment. Nevertheless, the opportunities for market share for this segment still appear considerable.

The small INGO segments meanwhile, have faced declining income across the board with a loss of market share in all areas. For those in the mid-range segments (£2-5m, £5-20m and £20-40m incomes), we are perhaps beginning to see some interesting specialisation and a more commercial focus, with noteworthy growth in corporate income (£2-5m and £5-20m segments), earned income and government contracts (£20m-£40m).

Financial trends for UK-based INGOs 39

As may be expected, Bond members are concentrated in both of these categories. However, the nature of these classification systems, and the wide variety of activities that organisations perform, means that there is not an exact one-to-one correlation.

When looking at the area of benefit, 81% of bond members say they work overseas, with the remaining 19% working both nationally and overseas.

The results for ICNPO are more mixed. Just under half of Bond’s members are classified into the “international” category (45%), but the mixed nature of many of Bond’s members means that over half are included in other categories – including social services (13%), grant-making foundations (7%) and religion (7%).

However, it is clear that Bond members represent the most substantial part of the UK’s international development sector. The combined income of Bond members in 2012/13 – £4.7 billion – was greater than the income of all organisations classified as international in the ICNPO category in that year. And the 45% of Bond members that are in that category had an income of £3.1 billion, suggesting that nearly 90% of the economic activity of these international organisations is contained in Bond members.

In this section, we have made comparisons between the Bond membership and the wider international sector.

Appendix: A comparison with the wider international sector

To define this we have used category 9100 from the International Classification of Non-Profit Organisations (ICNPO), as applied to the register of charities in England and Wales. However, the nature of classification systems like this one means that it doesn’t necessarily align with how the Bond and its network views the international development sector.

In particular, the category covers all organisations whose main work is carried out overseas, a wider definition than “international development”. It could include, for example, the funding of universities in developed countries.

We also draw on organisations’ classification of the scope of their benefit. This is a free-text field, but has been classified into the following categories: local (within the UK); national (within the UK); overseas; and national and overseas.

Data on these organisations is drawn from the UK Civil Society Almanac, published by NCVO, and from the database.

Data from the latest Almanac identifies 5,344 organisations in the UK in 2012/13 classified into the “international” ICNPO category, representing 3.3% of all organisations. These organisations have combined income of £3.6 billion and spending of £3.6 billion, as well as holding assets worth £2.2 billion.

Income from individuals represents 39% of these organisations’ income, while government provides 30%. Both of these figures are slightly lower than the average for all UK charity sector organisations (46% and 33% respectively). International organisations have a much higher proportion of their funding from the voluntary sector – 25% compared to 8% for the sector as a whole – reflecting the importance of grant-making foundations in their funding mix.

Separately, the Almanac finds that 9,092 organisations operate overseas, with a further 5,000 saying that they operate nationally and overseas. These represent 6% and 3% of the total sector respectively – 78% of the UK charity sector say they operate at a local level (within the UK).

Overlap between Bond members and other international organisations

Bondmembership

Areaof benefitoverseas

ICNPOinternational

130 22

81

131

Bond Society Building 8 All Saints Street London N1 9RL, UK

+44 (0)20 7837 8344 bond.org.uk

Registered Charity No. 1068839 Company registration No. 3395681 (England and Wales)