Embed Size (px)

Citation preview

Financial Statements and Federal Single Audit

Report

Public Utility District No. 1 of Skagit

County

For the period January 1, 2015 through December 31, 2016

Published October 9, 2017

Report No. 1020031

Insurance Building, P.O. Box 40021 Olympia, Washington 98504-0021 (360) 902-0370 [email protected]

October 9, 2017

Board of Commissioners

Public Utility District No. 1 of Skagit County

Mount Vernon, Washington

Report on Financial Statements and Federal Single Audit

Please find attached our report on Public Utility District No. 1 of Skagit County’s financial

statements and compliance with federal laws and regulations.

We are issuing this report in order to provide information on the District’s financial condition.

Sincerely,

Pat McCarthy

State Auditor

Olympia, WA

Office of the Washington State Auditor

Pat McCarthy

TABLE OF CONTENTS

Schedule Of Findings And Questioned Costs ................................................................................. 4

Schedule Of Audit Findings And Responses .................................................................................. 6

Summary Schedule Of Prior Audit Findings .................................................................................. 9

Independent Auditor’s Report On Internal Control Over Financial Reporting And On

Compliance And Other Matters Based On An Audit Of Financial Statements Performed In

Accordance With Government Auditing Standards ..................................................................... 10

Independent Auditor’s Report On Compliance For Each Major Federal Program And Report

On Internal Control Over Compliance In Accordance With The Uniform Guidance .................. 13

Independent Auditor’s Report On Financial Statements .............................................................. 16

Financial Section ........................................................................................................................... 19

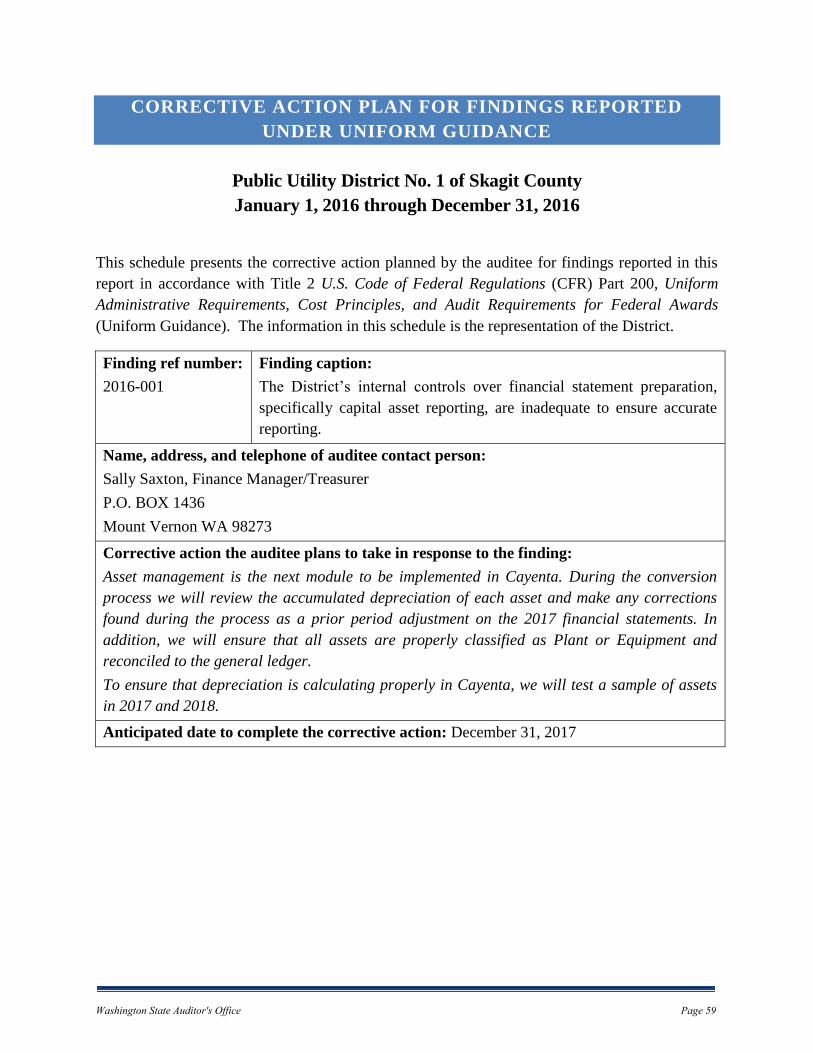

Corrective Action Plan For Findings Reported Under Uniform Guidance .................................. 59

About The State Auditor’s Office ................................................................................................. 60

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 3

SCHEDULE OF FINDINGS AND QUESTIONED COSTS

Public Utility District No. 1 of Skagit County

January 1, 2016 through December 31, 2016

SECTION I – SUMMARY OF AUDITOR’S RESULTS

The results of our audit of Public Utility District No. 1 of Skagit County are summarized below

in accordance with Title 2 U.S. Code of Federal Regulations (CFR) Part 200, Uniform

Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards

(Uniform Guidance).

Financial Statements

We issued an unmodified opinion on the fair presentation of the basic financial statements in

accordance with accounting principles generally accepted in the United States of America

(GAAP).

Internal Control over Financial Reporting:

Significant Deficiencies: We identified deficiencies in the design or operation of internal

control over financial reporting that we consider to be significant deficiencies.

Material Weaknesses: We identified no deficiencies that we consider to be material

weaknesses.

We noted no instances of noncompliance that were material to the financial statements of the

District.

Federal Awards

Internal Control over Major Programs:

Significant Deficiencies: We reported no deficiencies in the design or operation of

internal control over major federal programs that we consider to be significant

deficiencies.

Material Weaknesses: We identified no deficiencies that we consider to be material

weaknesses.

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 4

We issued an unmodified opinion on the District’s compliance with requirements applicable to

its major federal program.

We reported no findings that are required to be disclosed in accordance with 2 CFR 200.516(a).

Identification of Major Federal Programs:

The following program was selected as a major program in our audit of compliance in

accordance with the Uniform Guidance.

CFDA No. Program or Cluster Title

66.468 Capitalization Grants for Drinking Water State Revolving Funds

The dollar threshold used to distinguish between Type A and Type B programs, as prescribed by

the Uniform Guidance, was $750,000.

The District did not qualify as a low-risk auditee under the Uniform Guidance.

SECTION II – FINANCIAL STATEMENT FINDINGS

See finding 2016-001.

SECTION III – FEDERAL AWARD FINDINGS AND QUESTIONED

COSTS

None reported.

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 5

SCHEDULE OF AUDIT FINDINGS AND RESPONSES

Skagit County Public Utility District No. 1

January 1, 2016 through December 31, 2016

2016-001 The District’s internal controls over capital asset reporting were

inadequate to ensure accurate reporting.

Background

District commissioners, state and federal agencies, and the public rely on the

information included in the financial statements and report to make decisions.

District management is responsible for designing and following internal controls

that provide reasonable assurance regarding the reliability of financial reporting.

Our audit identified a deficiency in internal controls over financial reporting that

hindered the District’s ability to produce reliable financial statements.

Description of Condition

The Budgeting, Accounting and Reporting System (BARS) Manual outlines the

requirements for capital asset records.

The District did not have a process in place to ensure that capital asset balances,

including depreciation expense and accumulated depreciation, reported on the

financial statements are accurate and properly supported.

This deficiency in internal controls over financial reporting represents a

significant deficiency.

Cause of Condition

The District has experienced significant turnover in the accounting positions that

oversee capital asset reporting, causing a loss of knowledge of historical

transactions.

In addition, several concerns have been noted internally regarding the District’s

previous financial system, specifically the limitations on capital asset tracking and

reporting.

Effect of Condition

During our testing of capital asset depreciation calculations, significant variances

were noted for the majority of selected assets. Audit work determined that the

reported Accumulated Depreciation was under-reported by $5,492,840. The

District was unable to explain the reasoning for any differences.

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 6

In addition, the District was unable to provide a detailed listing of Plant capital

assets separate from all asset categories, to support the balance reported on the

financial statements.

Recommendation

We recommend the District develop a process to ensure capital asset amounts are

accurately presented in the financial statements and properly supported.

District’s Response

We appreciate the work performed by the Washington State Auditor’s Office. The

District has been transitioning to a new financial system and the next module to

be implemented is asset management; which should be completed in 2017.

The majority of the issue noted in the current audit can be traced back to

reclassifications of assets in 2010 and 2012. We were able to find documentation

that supported the District’s decision in 201 that determined it would be more

efficient to combine similar assets. In 2012, the District changed the service life of

a group of assets. In both circumstances, the information was not updated

correctly resulting in depreciation not calculating in one instance and not

properly in the other; this was a result of data entry error, not a system error or

limitation.

The implementation of the new asset management module will require the District

to convert and reconcile data for all asset classifications, which will result in

better information for all users of the financial statements.

We look forward to reviewing our process with the State Auditor during the 2017

financial statement audit.

Auditor’s Remarks

We appreciate the District’s commitment to resolving the issues identified above.

We will review the corrective action taken during our next audit. We thank the

District for its cooperation and assistance during the audit.

Applicable Laws and Regulations

RCW 43.09.200 Local government accounting – Uniform system of accounting

Budgeting Accounting and Reporting System (BARS) Manual – Accounting,

Accounting Principles and General Procedures, Internal Control (3.1.3)

Government Auditing Standards, December 2011 Revision, paragraph 4.23

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 7

The American Institute of Certified Public Accounts defines significant

deficiencies and material weaknesses in its Codification of Statements on Audit

Standards section 115

Budgeting Accounting and Reporting System (BARS) Manual – Accounting,

Capital Assets, Capital Asset Management System Requirements (3.3.9)

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 8

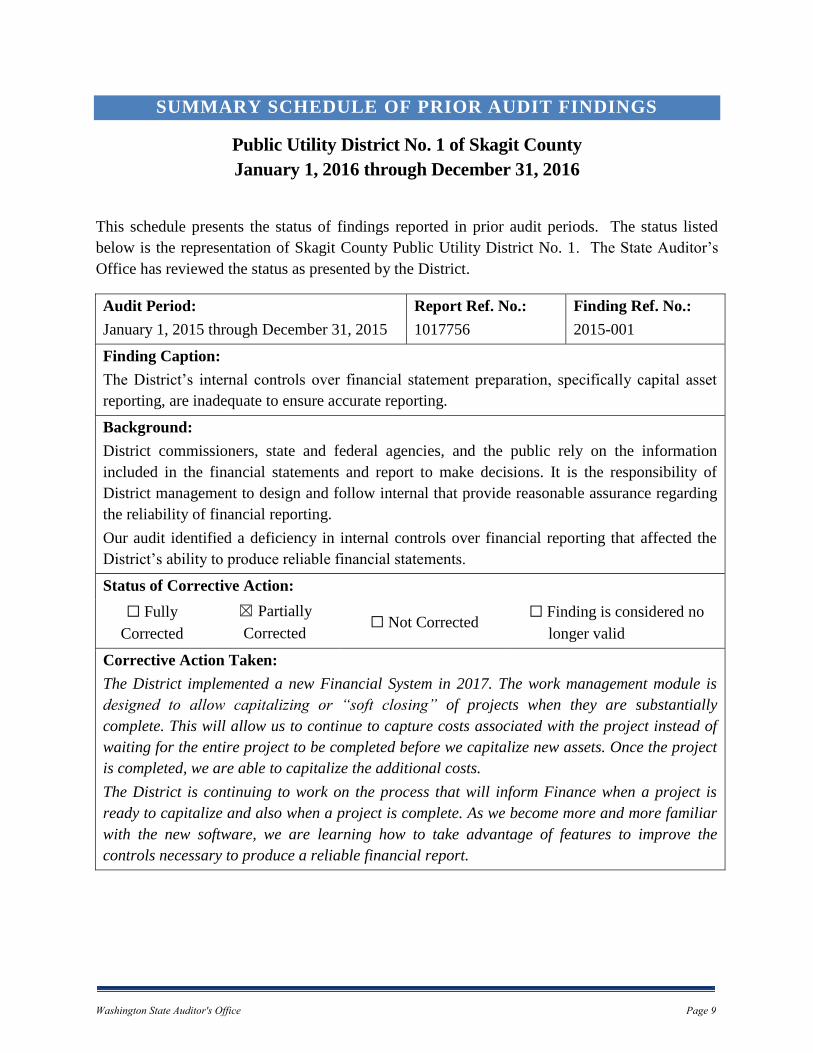

SUMMARY SCHEDULE OF PRIOR AUDIT FINDINGS

Public Utility District No. 1 of Skagit County

January 1, 2016 through December 31, 2016

This schedule presents the status of findings reported in prior audit periods. The status listed

below is the representation of Skagit County Public Utility District No. 1. The State Auditor’s

Office has reviewed the status as presented by the District.

Audit Period:

January 1, 2015 through December 31, 2015

Report Ref. No.:

1017756

Finding Ref. No.:

2015-001

Finding Caption:

The District’s internal controls over financial statement preparation, specifically capital asset

reporting, are inadequate to ensure accurate reporting.

Background:

District commissioners, state and federal agencies, and the public rely on the information

included in the financial statements and report to make decisions. It is the responsibility of

District management to design and follow internal that provide reasonable assurance regarding

the reliability of financial reporting.

Our audit identified a deficiency in internal controls over financial reporting that affected the

District’s ability to produce reliable financial statements.

Status of Corrective Action:

☐ Fully

Corrected

☒ Partially

Corrected ☐ Not Corrected

☐ Finding is considered no

longer valid

Corrective Action Taken:

The District implemented a new Financial System in 2017. The work management module is

designed to allow capitalizing or “soft closing” of projects when they are substantially

complete. This will allow us to continue to capture costs associated with the project instead of

waiting for the entire project to be completed before we capitalize new assets. Once the project

is completed, we are able to capitalize the additional costs.

The District is continuing to work on the process that will inform Finance when a project is

ready to capitalize and also when a project is complete. As we become more and more familiar

with the new software, we are learning how to take advantage of features to improve the

controls necessary to produce a reliable financial report.

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 9

INDEPENDENT AUDITOR’S REPORT ON INTERNAL CONTROL

OVER FINANCIAL REPORTING AND ON COMPLIANCE AND

OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL

STATEMENTS PERFORMED IN ACCORDANCE WITH

GOVERNMENT AUDITING STANDARDS

Public Utility District No. 1 of Skagit County

January 1, 2015 through December 31, 2016

Board of Commissioners

Public Utility District No. 1 of Skagit County

Mount Vernon, Washington

We have audited, in accordance with auditing standards generally accepted in the United States

of America and the standards applicable to financial audits contained in Government Auditing

Standards, issued by the Comptroller General of the United States, the financial statements of

Public Utility District No. 1 of Skagit County, Washington, as of and for the years ended

December 31, 2016 and 2015, and the related notes to the financial statements, which

collectively comprise the District’s basic financial statements, and have issued our report thereon

dated September 29, 2017.

INTERNAL CONTROL OVER FINANCIAL REPORTING

In planning and performing our audits of the financial statements, we considered the District’s

internal control over financial reporting (internal control) to determine the audit procedures that

are appropriate in the circumstances for the purpose of expressing our opinion on the financial

statements, but not for the purpose of expressing an opinion on the effectiveness of the District’s

internal control. Accordingly, we do not express an opinion on the effectiveness of the District’s

internal control.

A deficiency in internal control exists when the design or operation of a control does not allow

management or employees, in the normal course of performing their assigned functions, to

prevent, or detect and correct, misstatements on a timely basis. A material weakness is a

deficiency, or a combination of deficiencies, in internal control such that there is a reasonable

possibility that a material misstatement of District's financial statements will not be prevented, or

detected and corrected on a timely basis. A significant deficiency is a deficiency, or a

combination of deficiencies, in internal control that is less severe than a material weakness, yet

important enough to merit attention by those charged with governance.

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 10

Our consideration of internal control was for the limited purpose described in the first paragraph

of this section and was not designed to identify all deficiencies in internal control that might be

material weaknesses or significant deficiencies and therefore, material weaknesses or significant

deficiencies may exist that were not identified. Given these limitations, during our audit we did

not identify any deficiencies in internal control that we consider to be material weaknesses. We

did identify certain deficiencies in internal control, described in the accompanying Schedule of

Audit Findings and Responses as Finding 2016-001 that we consider to be significant

deficiencies.

COMPLIANCE AND OTHER MATTERS

As part of obtaining reasonable assurance about whether the District’s financial statements are

free from material misstatement, we performed tests of the District’s compliance with certain

provisions of laws, regulations, contracts and grant agreements, noncompliance with which could

have a direct and material effect on the determination of financial statement amounts. However,

providing an opinion on compliance with those provisions was not an objective of our audit, and

accordingly, we do not express such an opinion.

The results of our tests disclosed no instances of noncompliance or other matters that are

required to be reported under Government Auditing Standards.

DISTRICT’S RESPONSE TO FINDINGS

The District’s response to the findings identified in our audit is described in the accompanying

Schedule of Audit Findings and Responses. The District’s response was not subjected to the

auditing procedures applied in the audit of the financial statements and, accordingly, we express

no opinion on the response.

PURPOSE OF THIS REPORT

The purpose of this report is solely to describe the scope of our testing of internal control and

compliance and the results of that testing, and not to provide an opinion on the effectiveness of

the District’s internal control or on compliance. This report is an integral part of an audit

performed in accordance with Government Auditing Standards in considering the District’s

internal control and compliance. Accordingly, this communication is not suitable for any other

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 11

purpose. However, this report is a matter of public record and its distribution is not limited. It

also serves to disseminate information to the public as a reporting tool to help citizens assess

government operations.

Pat McCarthy

State Auditor

Olympia, WA

September 29, 2017

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 12

INDEPENDENT AUDITOR’S REPORT ON COMPLIANCE FOR

EACH MAJOR FEDERAL PROGRAM AND REPORT ON

INTERNAL CONTROL OVER COMPLIANCE IN ACCORDANCE

WITH THE UNIFORM GUIDANCE

Public Utility District No. 1 of Skagit County

January 1, 2016 through December 31, 2016

Board of Commissioners

Public Utility District No. 1 of Skagit County

Mount Vernon, Washington

REPORT ON COMPLIANCE FOR EACH MAJOR FEDERAL

PROGRAM

We have audited the compliance of Public Utility District No. 1 of Skagit County, Skagit County, Washington, with the types of compliance requirements described in the U.S. Office of

Management and Budget (OMB) Compliance Supplement that could have a direct and material

effect on each of the District’s major federal programs for the year ended December 31, 2016.

The District’s major federal programs are identified in the accompanying Schedule of Findings

and Questioned Costs.

Management’s Responsibility

Management is responsible for compliance with federal statutes, regulations, and the terms and

conditions of its federal awards applicable to its federal programs.

Auditor’s Responsibility

Our responsibility is to express an opinion on compliance for each of the District’s major federal

programs based on our audit of the types of compliance requirements referred to above. We

conducted our audit of compliance in accordance with auditing standards generally accepted in

the United States of America; the standards applicable to financial audits contained in

Government Auditing Standards, issued by the Comptroller General of the United States; and the

audit requirements of Title 2 U.S. Code of Federal Regulations Part 200, Uniform Administrative

Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform

Guidance). Those standards and the Uniform Guidance require that we plan and perform the

audit to obtain reasonable assurance about whether noncompliance with the types of compliance

requirements referred to above that could have a direct and material effect on a major federal

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 13

program occurred. An audit includes examining, on a test basis, evidence about the District’s

compliance with those requirements and performing such other procedures as we considered

necessary in the circumstances.

We believe that our audit provides a reasonable basis for our opinion on compliance for each

major federal program. Our audit does not provide a legal determination on the District’s

compliance.

Opinion on Each Major Federal Program

In our opinion, the District complied, in all material respects, with the types of compliance

requirements referred to above that could have a direct and material effect on each of its major

federal programs for the year ended December 31, 2016.

REPORT ON INTERNAL CONTROL OVER COMPLIANCE

Management of the District is responsible for establishing and maintaining effective internal

control over compliance with the types of compliance requirements referred to above. In

planning and performing our audit of compliance, we considered the District’s internal control

over compliance with the types of requirements that could have a direct and material effect on

each major federal program in order to determine the auditing procedures that are appropriate in

the circumstances for the purpose of expressing an opinion on compliance for each major federal

program and to test and report on internal control over compliance in accordance with the

Uniform Guidance, but not for the purpose of expressing an opinion on the effectiveness of

internal control over compliance. Accordingly, we do not express an opinion on the

effectiveness of the District's internal control over compliance.

A deficiency in internal control over compliance exists when the design or operation of a control

over compliance does not allow management or employees, in the normal course of performing

their assigned functions, to prevent, or detect and correct, noncompliance with a type of

compliance requirement of a federal program on a timely basis. A material weakness in internal

control over compliance is a deficiency, or combination of deficiencies, in internal control over

compliance, such that there is a reasonable possibility that material noncompliance with a type of

compliance requirement of a federal program will not be prevented, or detected and corrected, on

a timely basis. A significant deficiency in internal control over compliance is a deficiency, or a

combination of deficiencies, in internal control over compliance with a type of compliance

requirement of a federal program that is less severe than a material weakness in internal control

over compliance, yet important enough to merit attention by those charged with governance.

Our consideration of internal control over compliance was for the limited purpose described in

the first paragraph of this section and was not designed to identify all deficiencies in internal

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 14

control that might be material weaknesses or significant deficiencies. We did not identify any

deficiencies in internal control over compliance that we consider to be material weaknesses.

However, material weaknesses may exist that have not been identified.

Purpose of this Report

The purpose of this report on internal control over compliance is solely to describe the scope of

our testing of internal control over compliance and the results of that testing based on the

requirements of the Uniform Guidance. Accordingly, this report is not suitable for any other

purpose. However, this report is a matter of public record and its distribution is not limited. It

also serves to disseminate information to the public as a reporting tool to help citizens assess

government operations.

Pat McCarthy

State Auditor

Olympia, WA

September 29, 2017

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 15

INDEPENDENT AUDITOR’S REPORT ON

FINANCIAL STATEMENTS

Public Utility District No. 1 of Skagit County

January 1, 2015 through December 31, 2016

Board of Commissioners

Public Utility District No. 1 of Skagit County

Mount Vernon, Washington

REPORT ON THE FINANCIAL STATEMENTS

We have audited the accompanying financial statements of Public Utility District No. 1 of Skagit

County, Washington, as of and for the years ended December 31, 2016 and 2015, and the related

notes to the financial statements, which collectively comprise the District’s basic financial

statements as listed on page 19.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements

in accordance with accounting principles generally accepted in the United States of America; this

includes the design, implementation, and maintenance of internal control relevant to the

preparation and fair presentation of financial statements that are free from material misstatement,

whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express opinions on these financial statements based on our audits. We

conducted our audits in accordance with auditing standards generally accepted in the United

States of America and the standards applicable to financial audits contained in Government

Auditing Standards, issued by the Comptroller General of the United States. Those standards

require that we plan and perform the audit to obtain reasonable assurance about whether the

financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and

disclosures in the financial statements. The procedures selected depend on the auditor’s

judgment, including the assessment of the risks of material misstatement of the financial

statements, whether due to fraud or error. In making those risk assessments, the auditor

considers internal control relevant to the District’s preparation and fair presentation of the

financial statements in order to design audit procedures that are appropriate in the circumstances,

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 16

but not for the purpose of expressing an opinion on the effectiveness of the District’s internal

control. Accordingly, we express no such opinion. An audit also includes evaluating the

appropriateness of accounting policies used and the reasonableness of significant accounting

estimates made by management, as well as evaluating the overall presentation of the financial

statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a

basis for our audit opinions.

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects,

the financial position of Public Utility District No. 1 of Skagit County, as of December 31, 2016

and 2015, and the changes in financial position and cash flows thereof for the years then ended in

accordance with accounting principles generally accepted in the United States of America.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the

management’s discussion and analysis and required supplementary information listed on page 19

be presented to supplement the basic financial statements. Such information, although not a part

of the basic financial statements, is required by the Governmental Accounting Standards Board

who considers it to be an essential part of financial reporting for placing the basic financial

statements in an appropriate operational, economic or historical context. We have applied

certain limited procedures to the required supplementary information in accordance with auditing

standards generally accepted in the United States of America, which consisted of inquiries of

management about the methods of preparing the information and comparing the information for

consistency with management’s responses to our inquiries, the basic financial statements, and

other knowledge we obtained during our audit of the basic financial statements. We do not

express an opinion or provide any assurance on the information because the limited procedures

do not provide us with sufficient evidence to express an opinion or provide any assurance.

Supplementary and Other Information

Our audits were conducted for the purpose of forming opinions on the financial statements that

collectively comprise the District’s basic financial statements. The accompanying Schedule of

Expenditures of Federal Awards is presented for purposes of additional analysis as required by

Title 2 U.S. Code of Federal Regulations (CFR) Part 200, Uniform Administrative Requirements,

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 17

Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance). This

schedule is not a required part of the basic financial statements. Such information is the

responsibility of management and was derived from and relates directly to the underlying

accounting and other records used to prepare the basic financial statements. The information has

been subjected to the auditing procedures applied in the audit of the basic financial statements

and certain additional procedures, including comparing and reconciling such information directly

to the underlying accounting and other records used to prepare the basic financial statements or

to the basic financial statements themselves, and other additional procedures in accordance with

auditing standards generally accepted in the United States of America. In our opinion, the

information is fairly stated, in all material respects, in relation to the basic financial statements

taken as a whole.

OTHER REPORTING REQUIRED BY GOVERNMENT AUDITING

STANDARDS

In accordance with Government Auditing Standards, we have also issued our report dated

September 29, 2017 on our consideration of the District’s internal control over financial

reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts

and grant agreements and other matters. The purpose of that report is to describe the scope of

our testing of internal control over financial reporting and compliance and the results of that

testing, and not to provide an opinion on internal control over financial reporting or on

compliance. That report is an integral part of an audit performed in accordance with Government

Auditing Standards in considering the District’s internal control over financial reporting and

compliance.

Pat McCarthy

State Auditor

Olympia, WA

September 29, 2017

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 18

FINANCIAL SECTION

Public Utility District No. 1 of Skagit County

January 1, 2015 through December 31, 2016

REQUIRED SUPPLEMENTARY INFORMATION

Management’s Discussion and Analysis – 2016 and 2015

BASIC FINANCIAL STATEMENTS

Comparative Statement of Net Position – 2016 and 2015

Comparative Statement of Revenues, Expenses and Changes in Net Position – 2016 and

2015

Comparative Statement of Cash Flows – 2016 and 2015

Notes to Financial Statements – 2016 and 2015

REQUIRED SUPPLEMENTARY INFORMATION

OPEB Schedule of Funding Progress – 2016

OPEB Schedule of Employer Contributions – 2016

Schedule of Proportionate Share of Net Pension Liability – PERS 1, PERS 2/3 – 2016

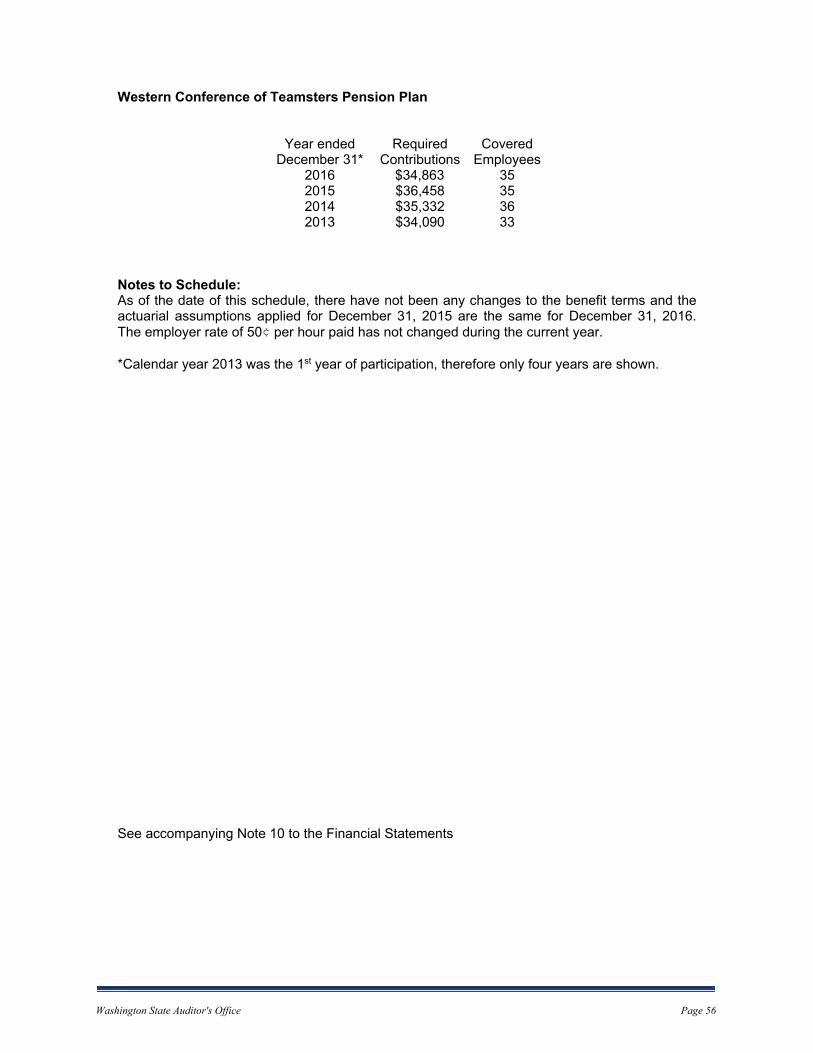

Schedule of Employer Contributions – PERS 1, PERS 2/3 – 2016

Schedule of Employer Contributions – Western Conference of Teamsters Pension Plan –

2016

SUPPLEMENTARY AND OTHER INFORMATION

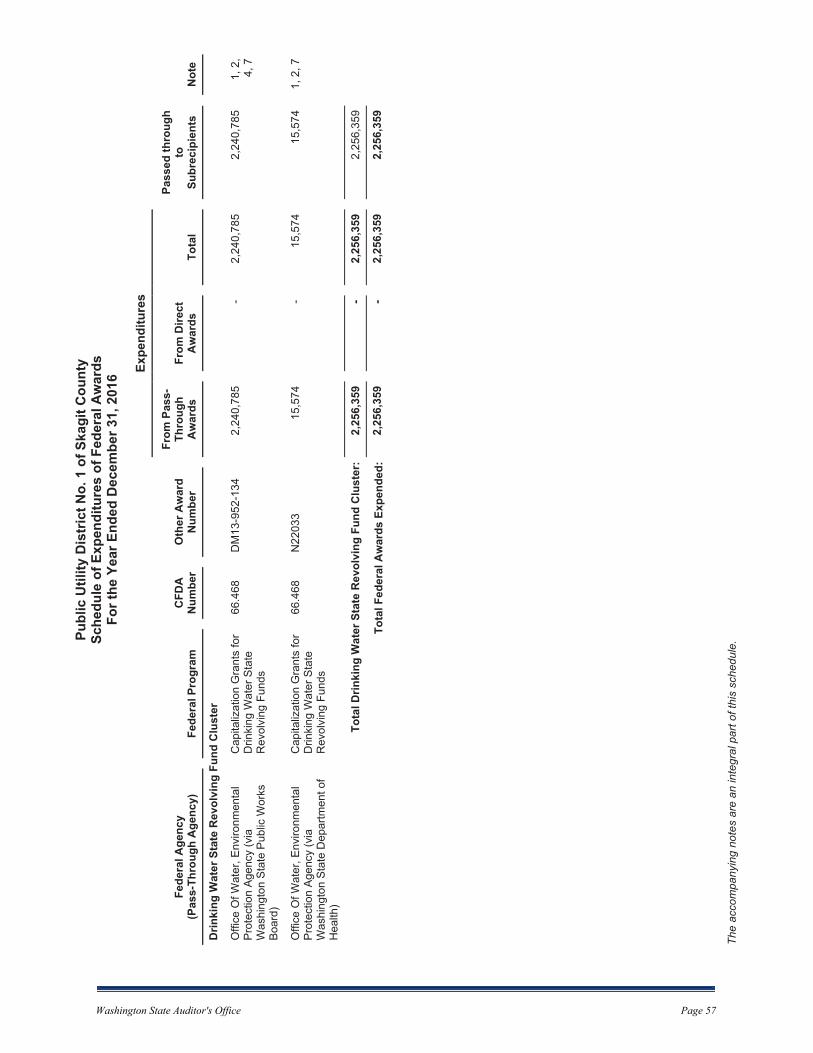

Schedule of Expenditures of Federal Awards – 2016

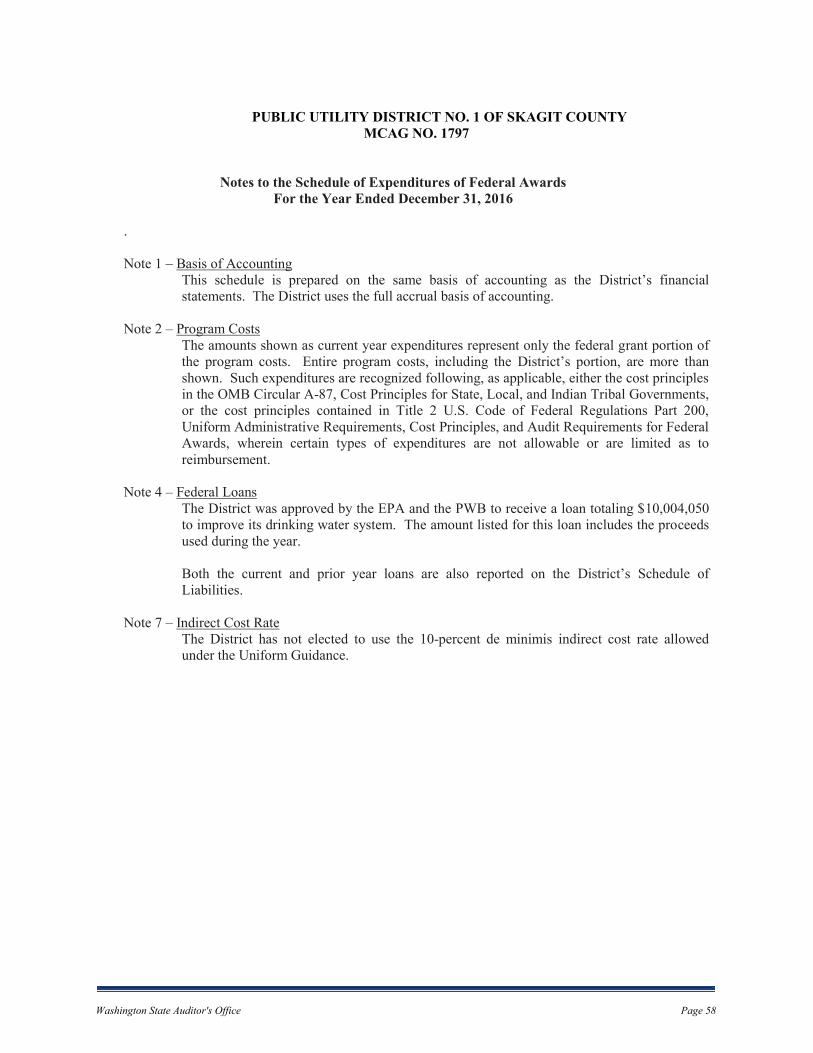

Notes to the Schedule of Expenditures of Federal Awards – 2016

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 19

PUBLIC UTILITY DISTRICT NO. 1 OF SKAGIT COUNTY

MANAGEMENT DISCUSSION AND ANALYSIS For the Years Ended December 31, 2016 and 2015

MANAGEMENT’S DISCUSSION AND ANALYSIS The Management Discussion and Analysis of Public Utility District No. 1 of Skagit County (the District) provides an overview and analysis of the District’s financial activities for the year ended December 31, 2016 with comparative data for 2015 and 2014. This information is designed to be used in conjunction with the financial statements and accompanying notes. OVERVIEW OF THE FINANCIAL STATEMENTS Basic Financial Statements The District accounts for its financial activity within a single enterprise fund. The activities of the District are comprised of treating and distributing water, as well as the sale of wholesale telecommunication services. The District also has voter-approved authority for sewer, although the District does not have sewer operations at this time. The basic financial statements of the District are designed to provide readers with a broad overview of the District’s finances similar to statements of a private-sector business. They are prepared using the accrual basis of accounting in accordance with generally accepted accounting principles. Under this basis of accounting, revenues are recognized in the period in which they are earned and expenses are recognized in the period in which they are incurred, regardless of the timing of related cash flows. These statements offer short-term and long-term financial statement information about District activities. The basic financial statements are comprised of: The Comparative Statement of Net Position: The District presents its statement of net position using the balance sheet format. The statement provides information on all of the District’s assets, deferred outflows, liabilities, deferred inflows, and net position at year end. The net position section is separated into three categories; net investment in capital assets; restricted net positon; and unrestricted net position. Investment in capital assets reflects the District’s investment in capital assets (land, plant, and equipment) less any remaining related debt. Restricted assets represent resources that are subject to external restrictions on how the funds may be used. Restrictions placed on these assets generally relate to constraints derived from grants, loans, or other debt. Unrestricted assets may be used to meet the District’s ongoing obligations. The Comparative Statement of Revenues, Expenses, and Changes in Net Position: This statement provides information on the District’s current and prior year revenues and expenses. Revenues are classified by major source and expenses are classified by function. Revenues and expenses are classed as operating or non-operating based upon the nature of the transaction. The Comparative Statement of Cash Flows: This statement provides relevant information about the District’s cash receipts and cash payments for operations as well as funds provided and used by investing and financing activities during the year. Notes to the Financial Statements: The notes to the financial statements are presented at the end of the basic financial statements and provide additional information that is essential to a full understanding of the data provided in the basic financial statements

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 20

FINANCIAL ANALYSIS

The following analysis provides a three-year comparison of key financial information:

Capital Assets The increase in capital assets and construction in progress are the results of the completion of a few large multi-year pipeline replacement projects that transferred the related costs from the construction in progress to the capital asset and projects that moved from the design phase to construction phase. The following is a summary of the major projects completed in 2016:

Discovery, Peterson to Gailee & Gull Dr, Gailee to Maple Crest Dr Ball Road East (500’) Mann Road LUD #31 Bulk Water Filling stations at Bow Hill Rd and Old Highway 99 The conversion of the Accounting, Customer Service, and Work Management systems. Security systems put into place at the Water Treatment Plant Various developer projects and annual pipe replacement and upsizing projects

2016 2015 Change 2014Assets

Current and other assets 21,757,650$ 15,920,843$ 36.66% 14,971,953$

Capital assets 162,110,153 153,002,914 5.95% 150,906,976

Total assets 183,867,803 168,923,757 8.85% 165,878,929

Deferred outflow of resources 1,136,027 562,579 101.93% 246,758

Liabilities

Current and other liabilities 6,292,782$ 4,832,521$ 30.22% 4,497,961$

Long-term liabilities 30,532,776 22,548,622 35.41% 23,146,066

Total liabilities 36,825,558 27,381,143 34.49% 27,644,027

Deferred inflow of resources 105,213 713,799 -85.26% 1,572,800

Net Position

Net investment in capital assets 136,557,964$ 134,107,401$ 1.83% 130,113,953$

Restricted 6,496,763 221,904 2827.74% 396,075

Unrestricted 5,018,332 7,062,089 -28.94% 6,398,832

Total net position 148,073,059 141,391,394 4.73% 136,908,860

Condensed Comparative Statement of Net Position

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 21

The following is a summary of the major projects that completed design work and construction started in 2016:

Josh Wilson Road, Higgins Airport Way to Walker Road Pipeline and Fiber and Old Highway 99 to Tina’s Coma Reservoir Fiber

Chemical Feed System for the Water Treatment Plant N 30th Street Transmission Line and Digby Road Pipeline, Phase I N 30th Street Transmission Line and Digby Road Pipeline, Phase II E Division Street Tank and Booster Pump Station Warehouse storage building on campus

The District’s 2017 capital budget includes plans for investing an additional $19.878 million of new and existing funds into capital improvements. This plan includes:

I-5 crossing at Conway Replacing the raw water PS Pump at the Skagit River Diversion Purchase of 250 acres around the Gilligan Creek watershed Mundt Creek Intake Improvements Judy WTP to Mount Vernon Transmission Line-Phase 2 Annual plant replacement and upsizing of infrastructure

See Note 3 for more information regarding capital asset activity.

Long-term Liabilities The increase in long-term liabilities is attributed to a 2016 Revenue bond issue of $6.3 million to fund the Judy WTP to Mount Vernon transmission Line – Phase II project and draws of $2.4 million against a Drinking Water loan to fund the E Division Street Tank, Booster Pump Station and Piping project. The District will be receiving $4.2 million in 2017 from an additional bond issue. See note 6 for more information regarding outstanding debt. Net Position The restricted portion of total net position, represent resources that are subject to external restrictions on how the funds may be used. The 2016 Revenue Bond issue was relatively unspent by the end of 2016; these unspent funds are reflected as restricted for capital projects. The decrease in unrestricted net position is a result of an aggressive pipe replacement program that is funded by water revenues.

Changes in the District’s net position can be determined by reviewing the following condensed Statement of Revenues, Expenses, and Changes in Net Position.

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 22

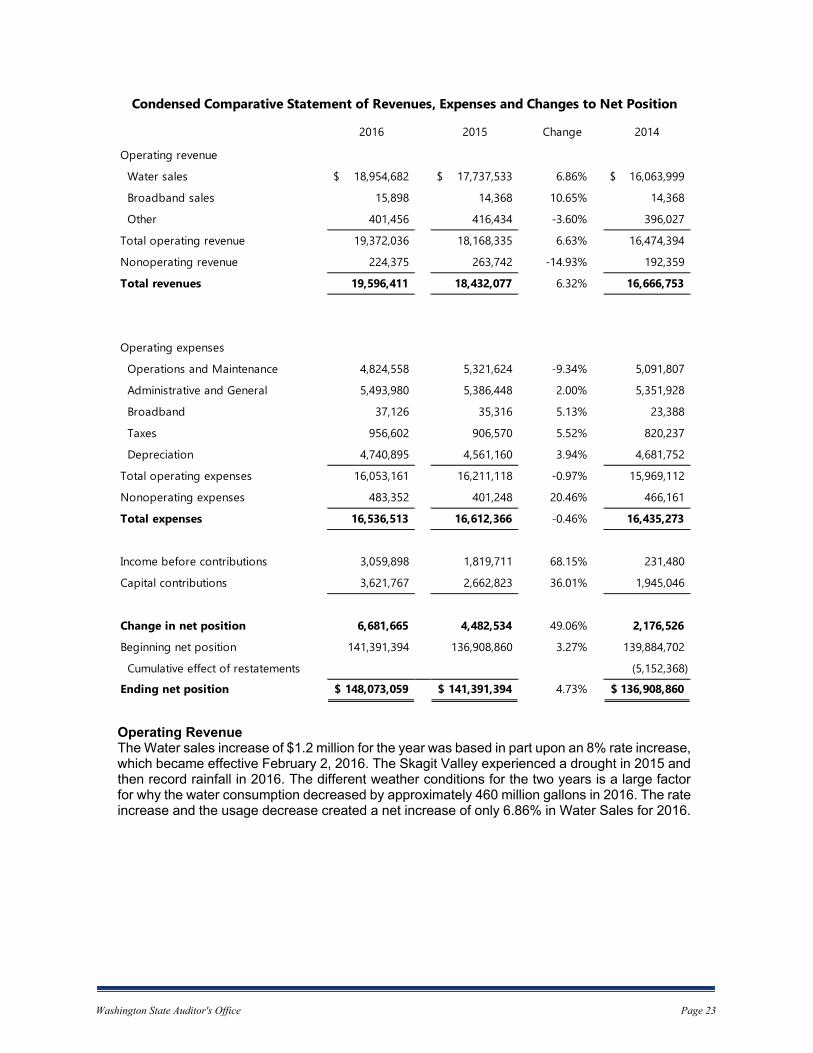

Operating Revenue The Water sales increase of $1.2 million for the year was based in part upon an 8% rate increase, which became effective February 2, 2016. The Skagit Valley experienced a drought in 2015 and then record rainfall in 2016. The different weather conditions for the two years is a large factor for why the water consumption decreased by approximately 460 million gallons in 2016. The rate increase and the usage decrease created a net increase of only 6.86% in Water Sales for 2016.

2016 2015 Change 2014

Operating revenue

Water sales 18,954,682$ 17,737,533$ 6.86% 16,063,999$

Broadband sales 15,898 14,368 10.65% 14,368

Other 401,456 416,434 -3.60% 396,027

Total operating revenue 19,372,036 18,168,335 6.63% 16,474,394

Nonoperating revenue 224,375 263,742 -14.93% 192,359

Total revenues 19,596,411 18,432,077 6.32% 16,666,753

Operating expenses

Operations and Maintenance 4,824,558 5,321,624 -9.34% 5,091,807

Administrative and General 5,493,980 5,386,448 2.00% 5,351,928

Broadband 37,126 35,316 5.13% 23,388

Taxes 956,602 906,570 5.52% 820,237

Depreciation 4,740,895 4,561,160 3.94% 4,681,752

Total operating expenses 16,053,161 16,211,118 -0.97% 15,969,112

Nonoperating expenses 483,352 401,248 20.46% 466,161

Total expenses 16,536,513 16,612,366 -0.46% 16,435,273

Income before contributions 3,059,898 1,819,711 68.15% 231,480

Capital contributions 3,621,767 2,662,823 36.01% 1,945,046

Change in net position 6,681,665 4,482,534 49.06% 2,176,526

Beginning net position 141,391,394 136,908,860 3.27% 139,884,702

Cumulative effect of restatements (5,152,368)

Ending net position 148,073,059$ 141,391,394$ 4.73% 136,908,860$

Condensed Comparative Statement of Revenues, Expenses and Changes to Net Position

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 23

Operating Expenses Operating expenses decreased by .97% for 2016 The District did experience higher legal costs due to personnel issues, increased cost in water purchased through the City of Anacortes due to a new agreement, but that was offset by unfilled budgeted positions and updating the rate our equipment is charged to capital projects. Change in Net Position At the end of 2016, the District’s total net position increased by $6,681,665. Two major components of that increase were an operating income of $3,318,875 and capital contributions of $3,621,767. ECONOMIC FACTORS AND NEXT YEAR’S BUDGET AND RATES The District’s annual budget, as approved by the Board of Commissioners, outlines its plan for operations, maintenance, and growth, in order to provide quality potable water to the District’s customers for the present and foreseeable future. In considering the District’s budget for the 2017 year, the Board of Commissioners and management used the following estimates:

Revenue from water sales and charges are expected to increase as a result of a rate increase of 8.5%.

Capital contributions are expected to be $2,935,000. This amount includes $600,000 in fees approved to fund pipe replacement.

Operating expenses, excluding depreciation and OPEB, are expected to increase approximately 2.7% in 2017. Unfilled positions, repairs to the Skagit River Diversion and Water Treatment Plant, and contracting out our billing process are some of the contributors to the increase.

REQUESTS FOR INFORMATION The basic financial statements, notes and management discussion and analysis are designed to provide a general overview of the District’s finances. If you have any questions about the report or need additional financial information, contact the District Treasurer at: Public Utility District No. 1 of Skagit County Attention: Treasurer Post Office Box 1436 Mount Vernon, Washington 98273-1436

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 24

The notes to the financial statements are an integral part of this statement.

ASSETS

CURRENT ASSETS 2016 2015Cash and cash equivalents 4,272,905$ 6,023,464$ Restricted assets

Cash and cash equibalents 136,677 160,100 Receivables - 39,931

Customer accounts receivable, net 2,689,844 2,104,224 Accounts receivable, other 894,177 103,182 Materials inventory 1,507,917 1,647,025 Prepaid insurance 227,461 26,073 Other current assets 170,613 167,578

Total current assets 9,899,594 10,271,577

NON-CURRENT ASSETSInvestments 3,640,759 2,757,237 Restricted assets

Cash and cash equibalents 6,184,616 - Investments 309,220 217,061

Assessment receivable 948,322 879,191 Preconstruction costs 767,753 1,781,775 Other non-current assets 7,386 14,002 Capital assets not being depreciated

Non-operating property 29,521 29,521 Land and land rights 579,821 579,821 Earthen impounding reservoir 12,375,489 12,375,489 Construction in progress 6,070,441 7,666,801

Capital assets net of accumulated depreciationPlant 135,419,800 125,632,784 Equipment 7,635,081 6,718,498

Total non-current assets 173,968,209 158,652,180

Total assets 183,867,803 168,923,757

DEFERRED OUTFLOWS OF RESOURCESDeferred outflows related to pensions 1,136,027 562,579

Total deferred outflows of resources 1,136,027 562,579

TOTAL ASSETS AND DEFERRED OUTFLOWS OF RESOURCES 185,003,830$ 169,486,336$

PUBLIC UTILITY DISTRICT NO. 1 OF SKAGIT COUNTY

COMPARATIVE STATEMENTS OF NET POSITION

DECEMBER 31, 2016 AND 2015

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 25

The notes to the financial statements are an integral part of this statement.

LIABILITIES

CURRENT LIABILITIES 2016 2015Accounts payable 2,387,401$ 1,311,165$ Taxes payable 147,250 118,339 Customer deposits 168,854 165,688 Restricted liabilities

Debt interest 133,750 155,257 Accrued interest on debt 53,857 39,311 Bonds and loans payable 2,934,307 2,647,223 Other current liabilities 467,363 395,538

Total current liabilities 6,292,782 4,832,521

NON-CURRENT LIABILITIESOther post-employment benefits 1,285,524 1,018,703 Compensated absences 551,183 484,280 Long-term debt, revenue bonds 10,197,203 5,234,958 Long-term debt, loans 12,420,679 11,027,334

Net Pension Liability 6,078,187 4,783,347

Total non-current liabilities 30,532,776 22,548,622

Total liabilities 36,825,558 27,381,143

DEFERRED INFLOWS OF RESOURCESDeferred inflows related to pensions 105,213 713,799

Total deferred inflows of resources 105,213 713,799

NET POSITIONNet investment in capital assets 136,557,964 134,107,401Restricted for

Debt service 312,147 221,904Capital projects 6,184,616 0

Unrestricted 5,018,332 7,062,089

Total net position 148,073,059 141,391,394

TOTAL LIABILITIES, DEFERRED INFLOWS OF RESOURCES AND NET POSITION 185,003,830$ 169,486,336$

COMPARATIVE STATEMENT OF NET POSITION

PUBLIC UTILITY DISTRICT NO. 1 OF SKAGIT COUNTY

DECEMBER 31, 2016 AND 2015

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 26

The notes to the financial statements are an integral part of this statement.

OPERATING REVENUESWater sales 2016 2015

Residential and multiple 13,355,049$ 12,597,211$ Commercial, industrial and farms 4,554,616 4,122,563 Government 559,800 505,485 Resale 89,261 96,143 Irrigation 395,956 416,131

Broadband sales 15,898 14,368 Other sales 401,456 416,434

Total operating revenues 19,372,036 18,168,335

OPERATING EXPENSESSupply 787,604 735,439 Treatment 1,713,345 1,718,875 Transmission and distribution 2,323,609 2,867,310 Broadband 37,126 35,316 Customer accounts 1,255,267 1,109,612 Administrative and general 4,238,713 4,276,836 Utility taxes 956,602 906,570 Depreciation and amortization 4,740,895 4,561,160

Total operating expenses 16,053,161 16,211,118

Operating income (loss) 3,318,875 1,957,217

NON-OPERATING REVENUES (EXPENSES)Interest income 47,461 7,947 LUD interest and penalty income 36,768 44,442 Interest and related charges (466,909) (384,027) Federal rebates on revenue bonds 66,151 66,009 Gain (loss) on capital asset disposition 42,684 104,394 Other non-operating revenues 31,311 40,950 Other non-operating expenses (16,443) (17,221)

Total non-operating revenues (expenses) (258,977) (137,506)

Income before capital contributions 3,059,898 1,819,711

CAPITAL CONTRIBUTIONSNon-donated plant 123,850 269,388 Donated plant 880,379 513,224 System development fees 1,341,132 1,216,991 Services 367,340 248,944 Pipe replacement 591,860 374,345 Local utility districts 269,796 - Capital grants 47,410 39,931

Total capital contributions 3,621,767 2,662,823

Change in net position 6,681,665 4,482,534

TOTAL NET POSITION - beginning of year 141,391,394 136,908,860

TOTAL NET POSITION - end of year 148,073,059$ 141,391,394$

PUBLIC UTILITY DISTRICT NO. 1 OF SKAGIT COUNTY

FOR YEARS ENDED DECEMBER 31, 2016 AND 2015

COMPARATIVE STATEMENTS OF REVENUES, EXPENSES, AND CHANGES IN FUND NET POSITION

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 27

The notes to the financial statements are an integral part of this statement.

2016 2015

CASH FLOWS FROM OPERATING ACTIVITIES

Cash received from customers 18,775,082$ 18,099,325$

Cash payments to suppliers for goods and services (1,306,515) (3,550,238)

Cash payments to employees for services (7,659,247) (7,878,316)

Cash payments for taxes (927,691) (860,433)

Other cash receipts or (payments) 10,465 32,431

Net cash provided (used) by operating activities 8,892,094 5,842,769

CASH FLOWS FROM NON-CAPITAL FINANCING ACTIVITIES

Cash received from non-capital grants - -

Net cash provided (used) for non-capital financing actitivies - -

CASH FLOWS FROM CAPITAL AND RELATED FINANCING ACTIVITIES

Acquisition and construction of capital assets (12,002,306) (5,853,356)

Proceeds from sale of capital assets 48,537 128,999

Principal paid on captial debt (2,647,222) (2,607,223)

Interest paid on capital debt (486,651) (429,829)

Federal interest rebates 66,151 66,009

Bond issues and Loan proceeds 8,730,218 627,336

Grant proceeds 87,341 -

Proceeds from customers for capital purposes 2,656,623 2,372,741

Net cash provided (used) for capital and related financing activities (3,547,309) (5,695,323)

CASH FLOWS FROM INVESTING ACTIVITIES

Purchase of investment securities (998,118) (2,990,203)

Proceeds from sale or maturity of investment securities - 2,000,000

Investment income proceeds 63,967 12,689

Net cash provided (used) for investing activities (934,151) (977,514)

Net increase (decrease) in cash and cash equivalents 4,410,634 (830,068)

CASH AND CASH EQUIVALENTS AT BEGINNING OF YEAR 6,183,564 7,013,632

CASH AND CASH EQUIVALENTS AT END OF YEAR 10,594,198$ 6,183,564$

PUBLIC UTILITY DISTRICT NO. 1 OF SKAGIT COUNTY

COMPARATIVE STATEMENTS OF CASH FLOWS

FOR YEARS ENDED DECEMBER 31, 2016 AND 2015

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 28

The notes to the financial statements are an integral part of this statement.

2016 2015

RECONCILIATION OF OPERATING INCOME TO NET CASH

PROVIDED BY (USED IN) OPERATING ACTIVITIES

Net operating income (loss) 3,318,875$ 1,957,217$

Adjustments to reconcile operating income to net cash

provided by (used in) operating activities

Depreciation and amortization 4,740,895 4,561,160

Other Income (Expenses) 10,465 32,431

Change in assets and liabilities

Accounts receivable (585,396) (66,359)

Inventory 139,108 (272,944)

Other current assets (201,388) 44,820

Preliminary expenses (72,571) (939,320)

Accounts payable 113,370 8,559

Accrued taxes 1,161,915 241,966

Other postemployment benefits 266,821 275,239

Net cash provided by operating activities 8,892,094$ 5,842,769$

During the year 2016, plant assets of $228,157 were donated to the District.

During the year 2015, plant assets of $497,725 were donated to the District.

FOR YEARS ENDED DECEMBER 31, 2016 AND 2015

PUBLIC UTILITY DISTRICT NO. 1 OF SKAGIT COUNTY

COMPARATIVE STATEMENT OF CASH FLOWS

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 29

PUBLIC UTILITY DISTRICT NO. 1 OF SKAGIT COUNTY

NOTES TO FINANCIAL STATEMENTS For the Years Ended December 31, 2016 and 2015

These notes are an integral part of the accompanying financial statements. NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES The accounting policies of the District conform to generally accepted accounting principles (GAAP) as applicable to proprietary funds of governments. The Governmental Accounting Standards Board (GASB) is the accepted standard setting body for establishing governmental accounting and financial reporting principles. The significant accounting policies are described below. Reporting Entity Public Utility District No. 1 of Skagit County (the District) is a municipal corporation governed by an elected three-person Commission, authorized under Title 54 RCW. The District is a special purpose government that provides water supply and distribution services. In addition, the District provides wholesale telecommunication services. As required by generally accepted accounting principles, management has considered all potential component units in defining the reporting entity. The District has no component units. Basis of Accounting and Presentation The accounting records of the District are maintained in accordance with methods prescribed by the State Auditor under the authority of Chapter 43.09 RCW and are based on the Uniform System of Accounts for Class A and B Water Utilities as prescribed by the National Association of Regulatory Utility Commissioners. The District uses the full-accrual basis of accounting where revenues are recognized when earned and expenses are recognized when incurred. Capital asset purchases and construction are capitalized and unbilled utility service receivables are recorded at year end. Operating revenues are defined as related to the sale of water to customers and to other services that are usually provided under standard rate schedules or by contractual arrangements. Operating expenses are defined as related to the operations and maintenance of treating and distributing water, customer service activities and general administration. Non-operating revenues and expenses are all revenues and expenses not meeting these definitions, such as financing and investing activities. Cash and Cash Equivalents For purposes of the statement of cash flows, the District considers all highly liquid investments (including restricted assets) with a maturity of three months or less to be cash equivalents. Balances in the Local Government Investment Pool (LGIP) are considered cash equivalents as they can be converted into cash within one business day.

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 30

Investments See Note 2 – Deposits and Investments Receivables The District maintains receivable for its billing for water service, property improvement assessments, and other miscellaneous billings. It is the District’s policy to write off accounts as uncollectible after 90 days, at which time they are turned over to collection. Any subsequently collected accounts reduce bad debt expense. Inventories Inventories are valued at average weighted cost, which approximates the market value. Restricted Assets and Liabilities In accordance with bond resolutions and other agreements, separate reserve accounts have been established for restricted or limited-use resources. The assets held in these funds are restricted for specific uses, including construction, debt service, and other reserve requirements. The restricted assets of the District are composed of the following: 2016 2015 Cash and Investments – Debt Service $ 445,897 $ 377,162

Cash and Investments – Construction $ 6,184,616 $ 0

Capital Assets Capital assets are defined by the District as assets with individual costs of more than $5,000 and an estimated useful life in excess of two years. The cost of maintenance and repairs is charged to expense as incurred, while the cost of replacements and improvements is capitalized. Utility plant and other capital assets are recorded at the original cost where the historical cost is known. Where historical cost is not known, assets are recorded at fair market value, as determined by Engineer’s estimate. Donations by developers and customers are recorded at the contract price and donor cost. An allowance for funds used during construction is capitalized as part of the cost of utility plant. This procedure is intended to remove the cost of financing construction activity from the statement of revenues, expenses and changes in net position and to treat such cost in the same manner as construction labor and material costs. Capital assets are depreciated using the straight-line method over the following estimated useful lives: Water Mains (Transmission, distribution, and supply) 70 years Structures and improvements 50 years Services 40 years Intakes, wells, reservoirs, standpipes, and hydrants 30 years

Pumping equipment 20 years Meters 15 years General plant, furniture, tools, lab, and other equipment 10 years Transportation and power-operated equipment 6.67 years

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 31

Depreciation is recorded the year following acquisition or construction. When a capital asset is retired, or otherwise disposed of, the original cost is removed from the capital asset account and from accumulated depreciation Preconstruction costs incurred for proposed projects are deferred pending construction of the project. Costs relating to projects ultimately constructed are reclassified to utility plant. If the projects are abandoned, the costs are expensed. See Note 3 – Capital Assets Compensated Absences The District maintains a Personal Leave Plan (PLP) for vacation, sick and family leave purposes; accruing based upon an employee’s length of service. Personal Leave may be carried forward from year-to-year to a maximum accumulation of 800 hours. Any accumulated Personal Leave balance is paid to the employee at retirement, termination of employment or death. The exception is for employees retiring from the PERS 1 Retirement System. These employees may be paid a maximum of 240 hours compensated leave at retirement. The District records PLP as a component of payroll labor load as earned with a liability representing earned leave balances not yet taken. The District maintains a Supplemental Leave Bank which originated from a former sick leave plan at the change to the Personal Leave Plan. The old sick leave is non-accruing and no portion is payable at termination of employment. It is used solely to supplement short-term disability for those eligible. Pensions For purposes of measuring the net pension liability, deferred outflows of resources and deferred inflows of resources related to pensions, and pension expense, information about the fiduciary net position of all state sponsored pension plans and additions to/deductions from those plans’ fiduciary net position have been determined on the same basis as they are reported by the Washington State Department of Retirement Systems. For this purpose, benefit payments (including refunds of employee contributions) are recognized when due and payable in accordance with the benefit terms. Investments are reported at fair value. See Note 10 – Pension Plans. Use of Estimates The preparation of the financial statements, in conformity with Generally Accepted Accounting Principles (GAAP), requires management to make estimates and assumptions that affect amounts reported in the financial statements. Estimates may be included in the disclosure of contingent assets and liabilities at the date of the financial statements, and in the reported amounts of revenues and expenses during the reporting period. Actual results could differ from these estimates. Financial Statement Reclassifications Certain prior year amounts have been reclassified to conform to the current year presentation. NOTE 2 – DEPOSITS AND INVESTMENTS Deposits The District’s deposits are entirely covered by the Federal Depository Insurance Corporation (FDIC) or by collateral held in a multiple financial institution collateral pool administered by the

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 32

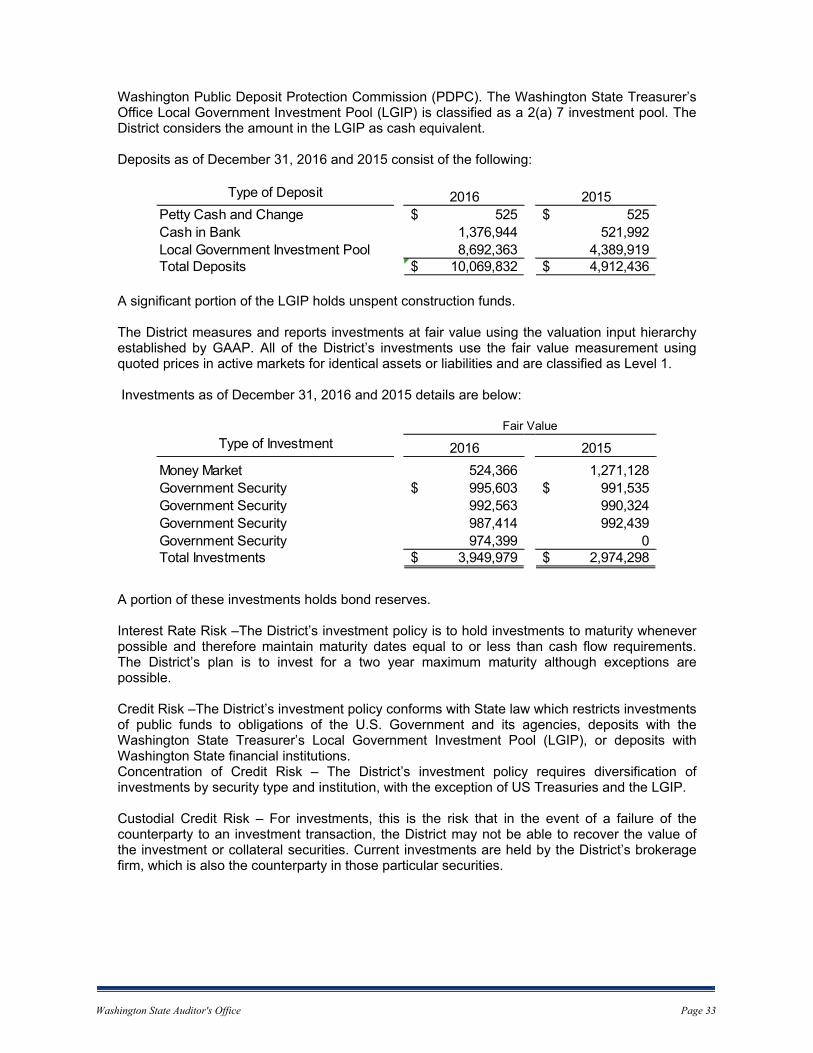

Washington Public Deposit Protection Commission (PDPC). The Washington State Treasurer’s Office Local Government Investment Pool (LGIP) is classified as a 2(a) 7 investment pool. The District considers the amount in the LGIP as cash equivalent. Deposits as of December 31, 2016 and 2015 consist of the following:

A significant portion of the LGIP holds unspent construction funds. The District measures and reports investments at fair value using the valuation input hierarchy established by GAAP. All of the District’s investments use the fair value measurement using quoted prices in active markets for identical assets or liabilities and are classified as Level 1. Investments as of December 31, 2016 and 2015 details are below:

A portion of these investments holds bond reserves. Interest Rate Risk –The District’s investment policy is to hold investments to maturity whenever possible and therefore maintain maturity dates equal to or less than cash flow requirements. The District’s plan is to invest for a two year maximum maturity although exceptions are possible. Credit Risk –The District’s investment policy conforms with State law which restricts investments of public funds to obligations of the U.S. Government and its agencies, deposits with the Washington State Treasurer’s Local Government Investment Pool (LGIP), or deposits with Washington State financial institutions. Concentration of Credit Risk – The District’s investment policy requires diversification of investments by security type and institution, with the exception of US Treasuries and the LGIP. Custodial Credit Risk – For investments, this is the risk that in the event of a failure of the counterparty to an investment transaction, the District may not be able to recover the value of the investment or collateral securities. Current investments are held by the District’s brokerage firm, which is also the counterparty in those particular securities.

Type of Deposit 2016 2015Petty Cash and Change 525$ 525$ Cash in Bank 1,376,944 521,992Local Government Investment Pool 8,692,363 4,389,919Total Deposits 10,069,832$ 4,912,436$

Type of Investment 2016 2015

Money Market 524,366 1,271,128Government Security 995,603$ 991,535$ Government Security 992,563 990,324Government Security 987,414 992,439Government Security 974,399 0Total Investments 3,949,979$ 2,974,298$

Fair Value

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 33

NOTE 3 – CAPITAL ASSETS Utility plant activity for the year ended December 31, 2016 was as follows:

Interest incurred by the District during the current year is $479,691. Of this amount, $46,027 was included as part of the capitalized value. Utility plant activity for the year ended December 31, 2015 was as follows:

Interest incurred by the District during 2015 was $416,172. Of this amount, $41,663 was included as part of the capitalized value.

Balance Increase Decrease Ending Balance

Utility plant not being depreciated:Non-operating property 29,521$ -$ -$ 29,521$

Land and land rights 579,821 - - 579,821

Earthen impounding reservoir 12,375,489 - - 12,375,489

Construction in progress 7,666,801 13,493,217 (15,089,577) 6,070,441

Total utility plant not being depreciated 20,651,632 13,493,217 (15,089,577) 19,055,272

Utility plant being depreciated:Plant 188,835,639 14,407,359 (440,484) 202,802,514

Equipment 9,743,322 1,042,989 - 10,786,311

Total utility plant being depreciated 198,578,961 15,450,348 (440,484) 213,588,825

Accumulated depreciation for:Plant (63,202,855) (4,587,382) 434,631 (67,355,606)

Equipment (3,024,824) (153,514) - (3,178,338)

Total accumulated depreciation (66,227,679) (4,740,896) 434,631 (70,533,944)

Total utility plant being depreciated, net 132,351,282 10,709,452 (5,853) 143,054,881

TOTAL UTILITY PLANT, NET 153,002,914$ 24,202,669$ (15,095,430)$ 162,110,153$

Beginning Balance Increase Decrease Ending Balance

Utility plant not being depreciated:Non-operating property 29,521$ -$ -$ 29,521$

Land and land rights 585,877 - (6,056) 579,821

Earthen impounding reservoir 12,375,489 - - 12,375,489

Construction in progress 8,076,635 6,183,979 (6,593,813) 7,666,801

Total utility plant not being depreciated 21,067,522 6,183,979 (6,599,869) 20,651,632

Utility plant being depreciated:Plant 182,414,049 6,868,830 (447,240) 188,835,639

Equipment 9,818,451 222,708 (297,837) 9,743,322

Total utility plant being depreciated 192,232,500 7,091,538 (745,077) 198,578,961

Accumulated depreciation for:Plant (59,331,753) (4,351,976) 480,874 (63,202,855)

Equipment (3,061,294) (209,184) 245,654 (3,024,824)

Total accumulated depreciation (62,393,047) (4,561,160) 726,528 (66,227,679)

Total utility plant being depreciated, net 129,839,453 2,530,378 (18,549) 132,351,282

TOTAL UTILITY PLANT, NET 150,906,975$ 8,714,357$ (6,618,418)$ 153,002,914$

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 34

NOTE 4 – CONSTRUCTION IN PROGRESS The District had active construction projects as of December 31, 2016 in the amount of $6,070,441; these are listed as Construction in Progress on the Statement of Net Position. As of December 31, 2016, the District’s commitments with contractors are as follows:

The District had active construction projects as of December 31, 2015 in the amount of $7,666,801; these are listed as Construction in Progress on the Statement of Net Position. As of December 31, 2015, the District’s commitments with contractors are as follows:

NOTE 5 – LEASE COMMITMENTS The District has no capital or operating lessee commitments as of December 31, 2016. NOTE 6 – LONG-TERM DEBT AND LIABILITIES Long-Term Debts The District issues revenue bonds and has loans obtained through State and Federal programs to finance the acquisition of property or equipment or construction of utility plant improvements or replacements of the existing water infrastructure. The bonds are repaid using the water revenue of the District.

Spent RemainingProject to Date CommitmentJosh Wilson Road, Higgins Airport Way to Walker Road Pipeline and Fiber 1,183,749 369,840Chemical Feed System at the Water Treatment Plant 5,899 599,531N 30th Street Transmission Line & Digby Pipeline, Phase I 763,590 64,640N 30th Street Transmission Line & Digby Pipeline, Phase II 2,295,554 110,897E Division Street Tank and Booster Pump Station 283,733 7,624,988Warehouse 0 89,248

ProjectSpent to

DateRemaining

CommitmentGilligan Road Culvert Replacement 4,062 1,197

Old Day Creek Road "A" Street to Transmission Line 903,810 43,662Judy WTP to SW Transmission Line Phase 1 931,099 44,981

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 35

Long-term debts as of December 31, 2016, are as follows:

The annual requirements for all debts outstanding as of December 31, 2016, are as follows:

Description Maturity RangeStated Interest

RateOriginal Amount

Amount of Installment

Water Revenue Refunding Bond, 2008 2009 - 2018 3.5% - 4.25% 7,205,000 805,000

Water Revenue Bond, 2009A 2009 - 2016 2.75% - 4.0% 1,335,000 220,000

Water Revenue Bonds, 2009B (Taxable Build America Bonds)

2017 - 20294.159% - 5.824%

Original3,660,000 0

Water Revenue Bond, 2016 2017 - 2036 2.65% - 10% 6,300,000 0

Bond Premiums2008, 2009 Issuances

N/A 275,712 25,671

Drinking Water State Revolving FundLoan #01-65101-026

2008 - 2022 1.50% 77,520 5,168

Drinking Water State Revolving FundLoan #01-65101-027

2005 - 2022 1.50% 1,758,480 110,538

Drinking Water State Revolving FundLoan #01-65120-028

2005 - 2021 1.50% 1,803,360 106,520

Drinking Water State Revolving FundLoan #01-65120-036

2005 - 2021 1.50% 64,619 4,069

Drinking Water State Revolving FundLoan #01-65120-037

2004 - 2021 1.50% 704,070 39,728

Drinking Water State Revolving FundLoan #DM13-952-134

2018 - 2042 1.50% 3,057,555 0

Public Works BoardLoan# PW-02-691-047

2004 - 2022 0.50% 10,000,000 562,494

Public Works BoardLoan# PW-01-691-057

2003 - 2021 0.50% 10,000,000 542,424

Public Works BoardLoan# PC12-951-059

2013 - 2031 0.25% 3,342,154 176,282

Public Works BoardLoan# PR13-951-106

2015 - 2018 1.00% 300,000 75,000

Totals 2,672,894

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 36

Long-term debts as of December 31, 2015 are as follows:

The annual requirements for all debts outstanding as of December 31, 2015, are as follows:

Description Maturity RangeStated Interest

RateOriginal Amount

Amount of Installment

Water Revenue Refunding Bond, 2008 2009 - 2018 3.5% - 4.25% 7,205,000 805,000

Water Revenue Bond, 2009A 2009 - 2016 2.75% - 4.0% 1,335,000 220,000

Water Revenue Bonds, 2009B (Taxable Build America Bonds)

2017 - 20294.159% - 5.824%

Original3,660,000 0

Bond Premiums2008, 2009 Issuances

N/A 275,712 31,817

Drinking Water State Revolving FundLoan #01-65101-026

2008 - 2022 1.50% 77,520 5,168

Drinking Water State Revolving FundLoan #01-65101-027

2005 - 2022 1.50% 1,758,480 110,538

Drinking Water State Revolving FundLoan #01-65120-028

2005 - 2021 1.50% 1,803,360 106,520

Drinking Water State Revolving FundLoan #01-65120-036

2005 - 2021 1.50% 64,619 4,069

Drinking Water State Revolving FundLoan #01-65120-037

2004 - 2021 1.50% 704,070 39,728

Drinking Water State Revolving FundLoan #DM13-952-134

2018 - 2042 1.50% 700,194 0

Public Works BoardLoan# PW-02-691-047

2004 - 2022 0.50% 10,000,000 562,494

Public Works BoardLoan# PW-01-691-057

2003 - 2021 0.50% 10,000,000 542,424

Public Works BoardLoan# PC12-951-059

2013 - 2031 0.25% 3,342,154 176,282

Public Works BoardLoan# PR13-951-106

2015 - 2018 1.00% 300,000 75,000

Totals 2,679,040

Year Ending Debt ServiceDec 31st Principal Interest Total

2016 2,647,222 381,453 3,028,6752017 2,934,307 497,004 3,431,3112018 2,785,811 434,526 3,220,3372019 2,071,665 388,404 2,460,0692020 2,088,114 360,666 2,448,780

2021-2025 5,891,162 1,350,551 7,241,7132026-2030 3,958,362 671,553 4,629,9152031-2035 2,173,130 228,109 2,401,2392036-2040 546,434 21,733 568,1672041-2042 58,350 1,313 59,663

Totals 25,154,557 4,335,312 29,489,869

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 37

At December 31, 2016, and December 31, 2015, the District had $1,447,664 and $1,159,652, respectively, available in debt service funds to service the revenue bonds. Restricted assets contained $312,147 in 2016 and $221,905 in 2015 which were comprised of sinking funds and reserves as required by bond indentures. In 2015, the District contracted with the Washington State Department of Commerce for a Drinking Water State Revolving Fund loan to finance the construction of the Division Street Tank and Booster Pump Station and Piping. The loan amount is for $10,004,050, in 2016 $3,015,568 in draws were made, and in 2015 $700,194 in draws were made. In 2016, the District contracted with the Washington State Department of Ecology for a Clean Water State Revolving Fund loan to finance the acquisition of approximately 250 acres of watershed land around the Gilligan Creek intake to protect public water supply source. This loan is for $1,590,000 with 25% loan forgiveness. No draws have been made against this loan. In 2016, the District issued $6,300,000 of revenue bonds with additional issues of $4,200,000 planned in 2017 to provide funding for the Judy Water Treatment Plant to Mount Vernon transmission line project and various other projects. The District spends bond proceeds within the allowable period of time to avoid a negative arbitrage position. Changes in Long-term Liabilities During the year ended December 31, 2016, the following changes occurred in long-term liabilities:

Beginning Balance

Ending Balance

Description 1/1/2016 Additions Reductions 12/31/2016Revenue Bonds Payable

Revenue Refunding Bonds 2,325,000 805,000 1,520,000 840,000Revenue Bonds 3,880,000 6,300,000 220,000 9,960,000 472,083Unamortized Bond Premium 54,958 25,671 29,287 19,525

Total Revenue Bonds Payable 6,259,958 6,300,000 1,050,671 11,509,287 1,331,608

Long-term Debt PayableDrinking Water Revolving Fund Loans 2,412,033 3,015,568 266,022 5,161,579 266,022Public Works Trust Fund Loans 10,237,525 1,356,201 8,881,324 1,356,201

Total Long-term Debt Payable 12,649,558 3,015,568 1,622,223 14,042,903 1,622,223

Other Long-term LiabilitiesCompensated Absences 820,061 647,953 579,285 888,729 337,547Net Pension Liabilities 4,783,347 1,294,840 6,078,187Other Post-employment Benefits (OPEB) 1,018,703 266,821 1,285,524

Total Other Long-term Liabilities 6,622,111 2,209,614 579,285 8,252,440 337,547

Total Long-term Liabilities 25,531,627 11,525,182 3,252,179 33,804,630 3,291,378

Due within one Year

Washington State Auditor's Office

___________________________________________________________________________________________________________________

Page 38

During the year ended December 31, 2015, the following changes occurred in long-term liabilities:

NOTE 7 – SPECIAL ASSESSMENTS The District receives annual installments on outstanding special assessments, which have remaining terms ranging from 1 to 20 years. Outstanding assessments receivable consist of current and delinquent assessments and related interest and penalties. As of December 31, 2016, $33,538 of special assessments was delinquent, and as of December 31, 2015, $40,619 was delinquent. There is minimal risk to collecting special assessment amounts since a lien is formed on each individual property. NOTE 8 – TELECOMMUNICATION SERVICES In 2009, the District started providing wholesale telecommunications services to Internet Service Providers. Revenue from the telecommunication activity is included in Broadband Sales in the Comparative Statement of Revenue, Expenses and Changes in Net Position. Telecommunication activities for 2016 and 2015 are as follows:

Beginning Balance

Ending Balance

Due within one Year

Description 1/1/2015 Additions Reductions 12/31/2015Revenue Bonds Payable

Revenue Refunding Bonds 3,100,000 775,000 2,325,000 805,000Revenue Bonds 4,090,000 210,000 3,880,000 220,000Unamortized Bond Premium 86,775 31,817 54,958 25,671

Total Revenue Bonds Payable 7,276,775 0 1,016,817 6,259,958 1,050,671

Long-term Debt PayableDrinking Water Revolving Fund Loans 1,977,860 700,194 266,021 2,412,033 266,022Public Works Trust Fund Loans 11,593,728 1,356,203 10,237,525 1,356,200

Total Long-term Debt Payable 13,571,588 700,194 1,622,224 12,649,558 1,622,222

Other Long-term LiabilitiesCompensated Absences 810,133 566,395 556,467 820,061 335,782Net Pension Liabilities 3,706,562 1,076,785 4,783,347Other Post-employment Benefits (OPEB) 743,464 275,239 1,018,703

Total Other Long-term Liabilities 5,260,159 1,918,419 556,467 1,838,764 5,119,129