Embed Size (px)

Citation preview

KDDI CORPORATION

Financial Results of the Fiscal Year Ended March 2010

April 23, 2010

Ubiquitous Solution Company

1

The figures included in the following brief, including the business performance target and the target for the number of subscribers are all projected data based on the information currently available to the KDDI Group, and are subject to variable factors such as economic conditions, a competitive environment and the future prospects for newly introduced services.Accordingly, please be advised that the actual results of business performance or of the number of subscribers may differ substantially from the projections described here.

2

1.1.1. Financial Results Highlights for FY2010.31. Financial Results Highlights for FY2010.3Consolidated basis

Operating revenues declined by 1.6% yoy. Operating income rose by 0.1% yoy. Posted ¥61.1B extraordinary loss including business restructuring expenses for streamlining NW and impairment loss etc.

Mobile BusinessOperating revenues declined by 2.5% yoy. Operating income declined by 3.5% yoy.No. of “au” subs at end-March was 31.87M with a cumulative share at 28.4%.Handset sales were 10.20 million units, average sales commission was ¥36,000.

Fixed-line BusinessOperating revenues declined 1.1% yoy. Operating income recovered by ¥12.3B, to ¥44.2B.At end-March, no. of fixed access lines was 5.94M. Within this, no. of FTTH subs rose to 1.51M.Profitability achieved for the fiscal year by CTCNote1, consolidated subsidiary providing FTTH services etc. in Chubu region.

KDDI’s Equity Participation in J:COMAssumed Liberty Global, Inc. (LGI) Group’s stake in J:COM by acquiring LGI Group’s entire stake in three intermediary holding companiesNote2 for ¥361.7B.

Increase year-end dividend per share from ¥5,500, to ¥6,500, giving full-year dividendper share of ¥13,000.

1

2

3

4

5

Note1: Chubu Telecommunications Co., Inc. Note2: Liberty Global Japan Ⅱ, LLC / Liberty Jupiter, LLC / Liberty Japan LLC

3

1.1.2. Full2. Full--year Outlook for FY2011.3 (1)year Outlook for FY2011.3 (1)

On a consolidated basis, both operating revenues and operating income are forecasted tokeep the same level as FY2010.3.- Mobile Business

Decrease due to decrease in voice ARPU caused by customer shift to “Simple course”and increase in cost due to reorganization of 800MHz band.

- Fixed-line BusinessAchieve profitability through reduction of NW cost etc. and improvement of profitabilityof FTTH business etc.

FY2010.3 Result → FY2011.3 Forecast (Change)

Note: All figures are on a consolidated basis except those where business segments are referred.

1

Operating revenues ¥3,442.1B → ¥3,440.0B (▲ ¥2.1B / - 0.1% yoy)¥1.1B yoy)

yoy))

¥53.7B¥54.2B

¥400)0.93M)0.40M)0.54M)0.53M)

Operating income ¥443.9B → ¥445.0B (+ / + 0.3%Mobile Business ¥483.7B → ¥430.0B (▲ / -11.1%Fixed-line Business ▲¥44.2B → ¥10.0B (+ / -

Key performance index- “au” ARPU ¥5,410 → ¥ 5,010 (▲- “au” total subs 31.87M → 32.80M (+- “au” handset no. of unit sold 10.20M → 10.60M (+- Fixed-access lines total subs 5.94M → 6.48M (+- FTTH total subs 1.51M → 2.04M (+

4

1.1.2. Full2. Full--year Outlook for FY2011.3 (year Outlook for FY2011.3 (22))

CAPEX peaked out in FY2009.3. Forecast for FY2011.3 at ¥490.0B, decrease by ¥28.0B yoy.

Main new facts included in the basis of the outlook and the effect amount- Increased number of overseas companies included in the scope of consolidation

Operating revenues: ¥50.0B / Operating income: ¥3.0B

- Equity participation in J:COM (became KDDI Group affiliate)Effect on equity in gain of affiliates: ▲¥3.0BNote1 (same effect on ordinary income)

Breakdown: Amortization of goodwill: ¥11.0B(goodwill equivalent: ¥290.0BNote2 / depreciation 20 years)

Equity in gain of affiliates : ¥8.0BNote3

2

3

Note1: Plan to recognize from 2Q. Note2: Estimate as of Apr. 23, 2010. Note3: Calculation by KDDI based on business results forecasts for the year ending Dec. 31, 2010, which J:COM released

on Jan. 28, 2010.

5

1.1.33. FY2011.3 Challenges. FY2011.3 Challenges1

2

3

4

Amid dramatic change in markets and earnings structures, advance business restructuringfor sustainable growth.

Mobile BusinessAchieve fundamental improvement in profitability as voice ARPU decreases with customer shift to “Simple course”.Promote transfer to tri-band compatible handsets in preparation for reorganization of the 800MHz band.Step up initiatives for new areas (smart phones / data cards etc.) and enhance data ARPU.Strengthen infrastructure for mobile Broadband era.

Fixed-line BusinessAchieve profitability on operating income basis.Expand FTTH customer base even further.

Growing / new areasExpand businesses not dependent on telecommunications traffic (content/media business).Expand overseas businesses through development of data center business globally andentry into emerging countries’ business etc.Strengthen management foundations of WiMAX business / financial business and promotedevelopment of new businesses.Build partnership with J:COM and J:COM’s existing shareholders and realize synergies.

6

2. Consolidated Financial Results2. Consolidated Financial ResultsOperating revenues

(Billions of yen)

0.0

100.0

200.0

300.0

400.0

500.0

FY2009.3 FY2010.3 FY2011.3(E)

yoy +0.1%

Operating income(Billions of yen)

+0.3%

0.0

1,000.0

2,000.0

3,000.0

4,000.0

FY2009.3 FY2010.3 FY2011.3(E)

yoy -1.6% -0.1%

(Billions of yen)

FY2009.3yoy yoy

Operating revenues 3,497.5 3,442.1 -1.6% 3,440.0 -0.1%Operating income 443.2 443.9 0.1% 445.0 0.3% Operating margin 12.7% 12.9% - 12.9% -Ordinary income 440.5 422.9 -4.0% 420.0 -0.7%Net income 222.7 212.8 -4.5% 240.0 12.8%Free Cash Flow -63.2 -184.4 - 230.0 -EBITDA 904.0 927.3 2.6% 910.0 -1.9% EBITDA margin 25.8% 26.9% - 26.5% -

FY2010.3 FY2011.3(E)

7

3. Mobile Business3. Mobile BusinessOperating revenues

0.0

100.0

200.0

300.0

400.0

500.0

600.0

FY2009.3 FY2010.3 FY2011.3(E)

yoy -3.5%

(Billions of yen) Operating income(Billions of yen)

0.0

1,000.0

2,000.0

3,000.0

4,000.0

FY2009.3 FY2010.3 FY2011.3(E)

-11.1%

yoy -2.5% -4.0%

(Billions of yen)

(' 000)Total Subs 30,843 31,872 32,800 of module-type 923 1,085 1,300

WIN(EV-DO) 22,722 26,174 29,9001X 7,805 5,451 -cdmaOne 316 247 -

FY2011.3(E)FY2010.3FY2009.3FY2009.3yoy yoy

Operating revenues 2,719.2 2,650.1 -2.5% 2,545.0 -4.0%Operating income 501.5 483.7 -3.5% 430.0 -11.1% Operating margin 18.4% 18.3% - 16.9% -Ordinary income 509.1 490.6 -3.6% 415.0 -15.4%Net income 273.1 293.2 7.3% 235.0 -19.8%Free Cash Flow 180.0 276.5 53.6% 235.0 -15.0%EBITDA 821.9 826.8 0.6% 765.0 -7.5% EBITDA margin 30.2% 31.2% - 30.1% -

FY2011.3(E)FY2010.3

Note

Note: For FY2011.3 (E), equity-method investment income/loss, that used to be out of segment, is allocated to each segment.

8

(Ref.) Mobile Business Operating income(Ref.) Mobile Business Operating income

300.0

350.0

400.0

450.0

500.0

0FY2009.3 FY2010.3 FY2011.3

501.5483.7

430.0(a)

(b)

(c)

-95.4 -5.7

+60.0

+23.3

(d)

(a)

(b)

+17.0

-114.9

(c)

+62.0

-17.8(d)

-17.7B -53.7B

(E)

(a)Revenues from telecommunication business(b)NW-related expensesNote

(c)Sales commissions (d)Others

Operating income

(Billions of yen)

Cases of increases and decreases(FY2009.3 to FY2011.3 estimate)

Note: Depreciation + noncurrent assets retirement cost + communication facility fee (including access charge for services).

9

4. Fixed4. Fixed--line Businessline Business

-80.0

-60.0

-40.0

-20.0

0.0

20.0

FY2009.3 FY2010.3 FY2011.3(E)0.0

200.0

400.0

600.0

800.0

1,000.0

FY2009.3 FY2010.3 FY2011.3(E)

Subs (' 000)

ADSL 1,224 1,031 840 FTTH 1,099 1,513 2,040 Metal-plus 3,130 2,852 2,570 Cable-plus phone 604 960 1,280 CATV 722 972 1,040

5,342 5,944 6,480

FY2011.3(E)FY2010.3FY2009.3

Fixed access lines

FY2009.3yoy yoy

Operating revenues 848.7 839.2 -1.1% 940.0 12.0%Operating income -56.6 -44.2 - 10.0 - Operating margin -6.7% -5.3% - 1.1% -Ordinary income -61.6 -56.8 - 0.0 -Net income -43.1 -68.4 - 0.0 -Free Cash Flow -40.7 -75.7 - 0.0 -EBITDA 82.3 94.7 15.0% 140.0 47.9% EBITDA margin 9.7% 11.3% - 14.9% -

FY2010.3 FY2011.3(E)

yoy -1.1%

Operating incomeOperating revenues(Billions of yen)(Billions of yen)

*Yoy comparisons are not available as figures are negative.

(Billions of yen)

Note2: CATV subs include number of households with at least one contract via broadcasting, internet, or telephone.Note3: Fixed access lines are FTTH, direct-revenue telephony (Metal-plus, Cable-plus phone) and CATV subs and the number excludes crossover subs.Note4: For FY2011.3 (E), equity-method investment income/loss, that used to be out of segment, is allocated to each segment.

Note1 : Including ADSL one (ADSL used over Metal-plus).

Note1

Note2

Note3

+12.0%

Note4

10

(Ref.)(Ref.) FixedFixed--line Business Operating incomeline Business Operating income

-100.0

-80.0

-60.0

-40.0

-20.0

0.0

-56.6

-44.2

10.0(Billions of yen)

Note: CTC, JCN and overseas subsidiaries

+12.3B +54.2B

(a)

-28.6

(b)

(c)+27.6+9.4

+4.0

(d)

(a)

+18.9

(c)+27.4

+11.7

-3.8(d)

FY2009.3 FY2010.3 FY2011.3(E)

Profitable in FY2011.3

(a)Non-consolidated operating revenues(b)Non-consolidated operating expenses(c)Group company earningsNote (d)Others

Operating income

(b)

Inclusive of ¥19.5B effectfrom network cost etc.

reduction

Cases of increases and decreases(FY2009.3 to FY2011.3 estimate)

11

5. Capital Expenditures5. Capital Expenditures

55.0

98.1

127.0

42.5

83.6

0.0

50.0

100.0

150.0

200.0

FY2009.3 FY2010.3 FY2011.3(E)

106.6 74.2

119.2

360.0

3.31.42.9 0.1

200.1204.3

96.8

0.0

100.0

200.0

300.0

400.0

500.0

FY2009.3 FY2010.3 FY2011.3(E)

Fixed-line capexMobile capex

(Billions of yen)

New 800MHz2GHz800MHz EV-DO800MHz 1X

Common Equip.

OthersFTTH

(Billions of yen)

(Billions of yen)

yoy yoyCapex (Cash basis) Consolidated 575.1 518.0 -9.9% 490.0 -5.4%

Mobile 432.1 376.8 -12.8% 360.0 -4.5%Fixed-line 140.6 138.7 -1.4% 127.0 -8.4%

FY2010.3 FY2011.3(E)FY2009.3

Note: Excludes ¥207.1B cost for buy-back of 4 buildings in FY2009.3.

12

6. Free Cash Flows6. Free Cash FlowsCreate stable operating cash flows of approx. ¥600.0B every fiscal year.Expect free cash flows of ¥230.0B for FY2011.3.

-12.5 -63.2-184.4

230.0296.5139.6

-1,000.0

-800.0

-600.0

-400.0

-200.0

0.0

200.0

400.0

600.0

800.0

1,000.0

FY2006.3 FY2007.3 FY2008.3 FY2009.3 FY2010.3 FY2011.3

- 1, 000

- 800

- 600

- 400

- 200

0

200

400

600

800

1, 000

Cash Flow Benchmarks

(E)

4 Buildings buy-back related etc. Equity participation in J:COM etc.

Effect of period-end holiday

Capex

CF fromoperating activities

Other CF(investment etc.)

FCF

EBITDA

(equity participationetc.)

(Billions of yen)

13

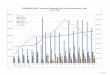

7. Shareholder Returns7. Shareholder ReturnsIncreased dividend ¥2,000 for FY2010.3 (increased for 8 consecutive periods).

Policy of steadily increase consolidated payout ratio to 25%–30% range while considering investment for sustainable growth remains.

895895

8951,200

1,200

2,4002,400

1,000

3,500

3,500

4,500

4,500

5,000

5,000

5,500

5,500

5,500

5,500

1,000

6,500

6,500

6,500

FY2002.3 FY2003.3 FY2004.3 FY2005.3 FY2006.3 FY2007.3 FY2008.3 FY2009.3 FY2010.3 FY2011.3

Year-end DividendCommemorative DividendInterim Dividend

(yen)

( - )(17.5%)

(16.8%)

(21.2%)(20.8%)

(22.0%)

Dividend per Share

(22.4%)

1,790 2,0953,600

6,9008,000

11,0009,500

(21.5%)10,500

(E)

(27.2%)

13,000

Note: ( ) refers to payout ratio, which shows on non-consolidated basis until FY2006.3 and on a consolidated basis from FY2007.3. FY2002.3 posted net loss.

(24.1%)

13,000

(E)

14

Segment Discussions & StrategiesSegment Discussions & Strategies

Mobile BusinessMobile Business

Fixed-line BusinessFixed-line Business

Growth / new areasGrowth / new areas

15

1.1.1. Net Additions1. Net Additions

Full-year / FY2010.3Full-year / FY2009.3

(Share) (Share)

Full-year / FY2009.3 Full-year / FY2010.3

Total Sub Basis Mobile Internet Sub Basis

504k subs / 10.6% 1,030k subs / 21.9% 678k subs / 27.1% 784k subs / 38.2%

Net additions of subs in FY2010.3 was 1,030k with a share of 21.9%. Net additions of mobile Internet subs in FY2010.3 was 784k with a share of 38.2%.

MobileBusiness

FY2009.3 FY2010.3 FY2009.3 FY2010.3

-40%

-20%

0%

20%

40%

60%

80%

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

KDDINTT DOCOMOSOFTBANK MOBILEEMOBILE

-40%

-20%

0%

20%

40%

60%

80%

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

KDDINTT DOCOMOSOFTBANK MOBILEEMOBILE

Source: Telecommunications Carriers Association website

16

1.2. Churn Rate1.2. Churn Rate MobileBusiness

0.87%0.77%

0.65%

0.85%

0.67%0.72%0.64%

0.75%

0.0%

0.5%

1.0%

1.5%

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

<0.72%><0.76%>

FY2009.3

Full-year

Churn rate in FY2010.3 was 0.72%, down 0.04 points yoy.

FY2010.3 FY2011.3(E)

<0.69%>

Down 0.04 points yoy

Note: Churn rate is calculated for ordinary handsets which exclude module-type terminals.

17

1.3. Sales Commissions1.3. Sales Commissions MobileBusiness

Average sales commissions for FY2010.3 was ¥36,000, down ¥3,000 yoy.

010,00020,00030,00040,00050,000

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

FY2009.3 FY2010.3

Average Commissions per Unit ** New purchases & upgrade models

(yen)

FY2009.3 FY2010.3 FY2011.31Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q (E)

129.0 104.0 79.0 114.0 90.0 112.0 71.0 93.0

45,000 38,000 32,000 41,000 41,000 44,000 30,000 30,000

2,860 2,700 2,450 2,800 2,210 2,560 2,330 3,100

36,000

10,200

365.0Total sales commissions

29,000

Number of units sold

Average commissions / unit

10,810 10,600

303.0425.0

39,000(Billions of yen)

(yen)

(‘000 units)

18

1.4. 1.4. AARPURPU MobileBusiness

ARPU in FY2010.3 was ¥5,410, down 6.7% yoy.

2,190 2,210 2,220 2,220 2,250 2,270 2,260 2,270 2,320

3,710 3,730 3,650 3,280 2,6902,7303,3303,350 3,210

148150142138135140139136

020406080

100120140160

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q0

2,000

4,000

6,000

8,000

FY2009.3

FY2011.3(E)

Total

Voice

Data

MOU

5,010

5,900 5,940 5,870 5,500

FY2010.3

5,600

Total ARPU

5,600 5,470

yoyTotal ▲ ¥390 (▲ 6.7%)

of Voice ▲ ¥440 (▲12.3%)

of Data + ¥50 (+ 2.3%)

5,000

Full-year FY2009.3 FY2010.3 FY2011.3(E)

¥5,410¥3,150¥2,260

¥5,010¥2,690¥2,320

Total ARPUof Voiceof Data

¥5,800¥3,590¥2,210

Note: The portion of FY2009.3 4Q and FY2010.3 4Q are decreases due to the settlement of access charges among carriers.

(mins.) (yen)

19

1.1.55.. ““ SSimple Course imple Course ”” MobileBusiness

12.52M subscriptions at end-March, making cumulative take-up ratio 41%Note.

Among customers who selected “Simple course,” installment payment rate was 42% in FY2010.3.

58%

7%4%

31%

Payment MethodNo. of Subs and Take-up Ratio

(24 times)

(18 times)

(12 times)

(FY2010.3)

0

5

10

15

20

25

30

3/'09 6/'09 9/'09 12/'09 3/'10 3/'11

(Million subs)

Note: Module-type and pre-paid contract are out of scope of take-up ratio calculation.

(E)

take-up raaio:41%

take-up ratio: 68%Lump sumpayment

Lump sumpayment

Installmentpayment

Installmentpayment

20

2.2. ReorganizationReorganization of 800MHz Bandof 800MHz Band MobileBusiness

20.67 million tri-band (new 800MHz / current 800MHz / 2GHz) compatible handsetsas of end-March.Promote transfer to tri-band compatible handsets in preparation for reorganizationof the 800MHz band in Jul. 2012.

0

10

20

30

3/'09 3/'10 3/'11

Tri-band Compatible Handset Contract Measure to Promote Transfer

Attracting to stores by sending DM.Waiving charges for handset upgradeprocessing.Providing handsets at affordable prices etc. (Use mid-range / low-end handsets)

Target non-tri-band-compatible handsets users by…

(E)

(Million subs)

52%

67%

86%

Effect on FY2011.3

Expected cost: approx. ¥80.0B

Note: %s show tri-band compatible handset contract ratio. Module-type contract is out of scope of calculation.

21

3. Smart Phones3. Smart Phones MobileBusiness

New Android MarketTM

E-mail(@ezweb.ne.jp)

Based on open platform handsets, use operator packs to customize functions standardin Japan and seek “ease of use” while aiming to reduce handset procurement cost.Plan to introduce models likely to be used as primary handset from second release onward.

UI suited to Japanese mobile usersCustomize standard AndroidTM UI for Japan

Card-type menu, control functions for applications running etc.

Functions standard in JapanNote1

Infraredcommunication

Decoration mail

“1-seg”

Also compatible with au services

Planned, from late Sept.“au one Navi Walk”

Roll out in Japanese apps. market

Note1: Not applicable to IS02 (release scheduled in late Jun.) Note: “Android” and “Android market” are registered trademarks of Google Inc.

22

4. Applications Market4. Applications Market MobileBusiness

Android MarketTM

Note1: as of end-Mar. 2010

For smart phones incorporating AndroidTM, in addition to Android MarketTM, construct easy-to-understand applications market suited to Japan and encourage data usage.

Secure

Danger-ous Low (Compatibility in Japan) High

Japanese compatible(approx. 3%)

Total: approx. 30,000

applicationsNote1

Recommendedapps.

Generalapps.

Expand recommended functionsAgency function for collecting charges

(au simple settlement)Security check functions

(Create confidence through recommended applications)

Advance adaptation of applications to Japanese language

Note2: Planned release from late Aug. 2010.

Based on proactive search by userPrompt model: users download after accepting security risks disclosed

(Security level)

23

5. Promote Increased Data Usage (1)5. Promote Increased Data Usage (1) MobileBusiness

Promote spread of EZ News EX as content suited to targeting customers in their 40s and above.For customers that use data infrequently, use au shops to encourage data usage.

0%

10%

20%

30%

40%

50%EZ News EX "au one" top page

EZ News EX Readers by Age Group

Members surpass 500k,Members surpass 500k,eight months after service beginseight months after service begins

Targeting customers in their 40s and

above

10s 20s 30s 40s 50s-

Expand EZ News EX Services

“Ultra-fast Bulletin Mail” and“Professional BaseballBulletins” started from March

Further expand content to increase

percentage of readers

Promotion at au Shops

Showcase content at au shop outlets.Consider using digital signage etc. to showcase / sell content.

24

5. Promote Increased Data Usage (2)5. Promote Increased Data Usage (2) MobileBusiness

0

100

200

300

400

500

600

1 月 2 月

StandardSimple

Business EZ

For Adult

Instead of standard efforts to attract customers to the general portal site “au one,”establish new entrances suited to different lifestyles, and encourage content usage among mid-level-usage customers and enhance data ARPU.

Expansion of Portal for Each Segment

Change in data ARPU before/after “au one for adults”

usage (50s and above)

Up more than ¥350

Before usageThree-month average

After usageThree-month average

(1) Target period: Oct. 2009 – Dec. 2009(2) Target customers: Individual users receiving

services at Feb. 28, 2010(3) Calculation of average value in three months

before and after month in which customer first accessed “au one for adults” over three times.

(Statistical parameters)

25

6. Strengthening Infrastructure6. Strengthening Infrastructure MobileBusiness

DataTrans-missionMarket

MobilePhoneMarket

CDMA OFDMA3G/3.5G 3.9G

Wi-Fi

CDMA2000 1x

2009 2010 2011 2012~

WiMAX (OFDMA : TDD)

EV-DO Rev. 0/Rev. A Multi-carrier Rev. A

LTE(OFDMA : FDD)

~2008

Wi-FiPurpose

-

Realize max. of 9.3Mbps (downstream) by converting current Rev.A system to multicarrier, strengthen competitiveness.Exploit Wi-Fi and Femtocell, promote development of data usage indoors and improvement of connection quality.

FY2011.3 measures

Exploit to expand data services

FemtocellExpand au areaDevelop into major access point offuture mobile BB era

Increase Wi-Fi compatible handsets

Plan to begin providing this summer

26

((RerRer.) Competitiveness in the Mobile Broadband Era MobileBusiness.) Competitiveness in the Mobile Broadband Era

Wi-Fi / Femtocell etc.

BBroadcast FFixed MMobile

USB Dongle

Data card

Data traffic peak: Centers on late night home usage

Fixed broadband system has significant importance as the backhaul for the mobile communication as well as for FTTH service.For femtocell, which is at center of attention, needs fixed broadband system.

Fixed AccessFTTHADSL

Broadcasting & Internet

CATV 3G MobileEV-DO Rev.A

Multi-carrier Rev. A

New Gen. RANsMobile WiMAX

LTEBB Access

IP Backbone

KDDI Powered Ethernet

The Internet Cloud

27

1. Fixed Access Lines1. Fixed Access Lines Fixed-lineBusiness

At end-March, number of fixed access lines was 5.94M.FTTH subs in FY2010.3 was 414k, up 71% yoy.

722 882 896 913 972 1,040604 697 778 871 960 1,280

3,130 3,065 3,000 2,927 2,852 2,570

1,099 1,211 1,319 1,426 1,5132,040

0

2,000

4,000

6,000

8,000

3/'09 6/'09 9/'09 12/'09 3/'10 3/'11

FTTHMetal-plusCable-plus phoneCATV

(E)

(5,342)(5,587) (5,700) (5,813) (5,944)

34 28 3548

80 8261

8226

2223

26

23

262830

2

0

20

40

60

80

100

120

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

OCTCTCKDDI

5951

58

74

FY2009.3

112

FY2010.3

108 107

86

(6,480)

414242

Note2

Fixed Access Lines Note1 FTTH Net Additions(‘000 subs) (‘000 subs)

Note2: Okinawa Cellular Telephone Company. Subs of OkinawaTelecommunication Network Co., Inc. included.

Note1: ( ) shows total subs of access lines excluding crossover subs.

28

2.2. FTTHFTTH Fixed-lineBusiness

Introduction of “Giga Value Plan”FY2009.3

FY2010.3

FY2011.3

Expansion of detached houses areaFor low-rise condominiums introduction of 1Gbps serviceOCT launched FTTH service

Enhancement of products

Expansion of Service area

Customerbase

expansion

As of end-Mar. 2010.

For detached houses:For condominiums: nationwide

(970GC*)

Existing service area

* In Okinawa, using NW of Okinawa Telecommunication Network Co., Inc.

In FY2011.3, work to further expand FTTH customer base, aim for full-year net increase of 0.53M and 2.04M cumulative subs at end-March 2011.

“au HIKARI”

“Commuf@-hikari”

“Hikarifuru” “au HIKARI Chura”

29

1. Content/Media Business1. Content/Media Business Growth/new areas

Sales of Content/Media Business

0.0

20.0

40.0

60.0

80.0

100.0

FY2005.3 FY2006.3 FY2007.3 FY2008.3 FY2009.3 FY2010.3 FY2011.3

Collaborative content & othersE-commerceAdvertisingContent-fee collection

(E)

Note: The accounting method for advertising sales changed in FY2008.3 and FY2009.3.

11.317.5

27.235.9

44.7

58.6

72.1

(Billions of yen)

FY2010.3 content/media revenues increased 31% yoy, to ¥58.6B. Focus on developing various business models not dependent on telecommunications traffic and expand business fields of entire Group.

30

2. Overseas Business2. Overseas Business Growth/new areas

Expand existing ICT businesses, develop WiMAX businesses and DC businesses in developing countries’ growth markets. Enter the mobile phone businesses targeting immigrants in U.S., expand business domain overseas.

Expanding Existing ICT Businesses

Streng-thening

SI

Streng-thening

SI

・Between Japan and U.S.: Unity

・Asia: SJC

Expand-ingNW

Expand-ingNW

Increas-ingDC

Increas-ingDC

・U.K.: London (Docklands West)・Singapore・Vietnam: Hanoi・South Africa: Cape Town, Johannesburg

Entry into mobile Entry into mobile phone businesses phone businesses targeting immigrants targeting immigrants in U.S. (MVNO)in U.S. (MVNO)

Entry into fixed Entry into fixed WiMAX business WiMAX business in Bangladeshin Bangladesh

Entry into growth markets

Development of ICT businesses in developing countries

Services for immigrants from developing countries

Developed nations BRICs etc. Developing countries

・Strengthening in Asia

Making DMX con-solidated subsidiary

OverseasBases

25 countries55 cities83 locations

31

3. 3. WiMAXWiMAX Growth/new areas

0

10

20

9/'09 12/'09 3/'10 3/'110

100

200

300

400

500

600

No. of base stations(left axes)

(’000 stations) (‘000 subs)Base stations and subs

Subs(rightaxes)

(E)

1,000

UQ Communications Inc., an affiliate of KDDI, develop mobile WiMAX services aiming to realize true mobile broadband society.

AreaCoverage

Base stations at Mar. 31: 7,013→Covering all 47 pref. capitals and

major cities nationwideDevelopment of repeaters→Strengthening indoor connectivity

Handsets

WiMAX-embedded PCs: 9 manufacturers, 31 models

→Embedded-as-standard models increasingMobile Wi-Fi gateway:

4 manufacturers, 4 models

MVNO

Concluded wholesale contracts: 39 companies→Number of electronics retail stores carrying

MVNO increasing

Subs.Subs. at Mar. 31: 150,300→Accompanying area expansion,

currently accelerating

Current situation

Expand areacoverage

Realize interna-tional roaming

Spread WiMAX PCs

Expand sales channels

FY2011.3 initiatives

31

32

44. . Financial BusinessFinancial Business Growth/new areas

Expand services of affiliate Jibun Bank Corporation and increase no. of accounts.

To develop a mobile-based new-concept general insurance business, Aioi Insurance Co., Ltd., and KDDI jointly invested to establish a preparatory company (Feb. 2010).

754853

179

343

495641

0

200

400

600

800

1,000

9/'08 3/'09 9/'09 3/'10

(‘000 accounts)

“Jibun Bank”Expand

financial products for individuals

Compatibilitywith various

Internet settlements

Surpassed900k

accounts

Fastest approach to 1 millionaccounts among Internet banks

(less than 2 years since operations began)

Entry into General Insurance Business

Establishment of preparatory company

(Company name) Mobile General Insurance Planning Co., Ltd.

(Capital) ¥300M (KDDI stake: 33.4%)

Concept

Combine mobile content and nonlife insurance etc., provide optimal insurance suited to au mobile phones and services used(example)

× sports insurance

EC / auction × shopping insurance

33

5.5. Alliance with J:COM (1)Alliance with J:COM (1) Growth/new areas

Started the talk about business alliance between KDDI and J:COM going forward.Build partnership with J:COM and J:COM’s existing shareholders and realize synergies.

2nd largest telecomoperator in Japan

Establish strategic partnership

Holds JCN, the 2nd largestMSONote in Japan, as aconsolidated subsidiary

Largest MSONote in Japan

Value ofAlliance

By converging KDDI’s telecommunications business (mobile/fixed-line) resource and J:COM’s CATV business resource,offer attractive FMBC service and enhance customer satisfaction,as well as enhance both companies’ enterprise value by the synergies given.

Note: Multiple System Operator

34

5.5. Alliance with J:COM (2)Alliance with J:COM (2) Growth/new areas

Telecom Business/Product

Collaboration WG

Business collaboration among fixed-line telephone, mobile/wireless communication and ISP.Sales channel collaboration.

Establish Alliance Study Committee where concrete plans for collaboration between KDDI and J:COM are studied. By setting up working groups (WG) for every category of issues, aim to speed up the study for the collaboration plans.

Alliance Study Committee and Possible Themes to be Studied

Media BusinessWG

Utilization of J:COM content business by KDDI.Collaboration in mobile/multimedia broadcasting.

CATV BusinessWG

Joint marketing and sales collaboration by J:COMand JCN.

Technology/Infrastructure WG

Development of equipment or products utilizing technology development resource of KDDI, such asnext generation set-top box (STB) for CATV etc.Effective investment by both companies, networkconsolidation, for example.

35