Embed Size (px)

Citation preview

FINANCIAL PERFORMANCE OF INDIAN PHARMACEUTICAL INDUSTRY

Mr. U. Shaji

Ph.D. Research Scholar,

Department of Commerce, Bharathiar University, Coimbatore-641046.

Email:[email protected]

Dr. G. Ganesan

Professor and Head, School of Commerce, Bharathiar University, Coimbatore-641046

ABSTRACT

With the de-licensing of pharmaceutical industry and complemented by scientific

talent and research capabilities and Intellectual Property Protection Regime, Indian

pharmaceutical industry in all set to take on new challenges in the international market.

Indian pharmaceutical industry has played a key role in promoting and sustaining

development in the vital field of medicines. Financial analysts often assess firm's

production and productivity performance, profitability performance, liquidity

performance, working capital performance, fixed assets performance, fund flow

performance and social performance. The financial performance analysis identifies the

financial strengths and weaknesses of the firm by properly establishing relationships

between the items of the balance sheet and profit and loss account. Thus, the present

paper is of crucial importance to measure the firm’s liquidity, profitability, and other

indicators that the business is conducted in a rational and normal way; ensuring enough

returns to the shareholders to maintain at least its market value. In this context

researcher has undertaken an analysis of financial performance of pharmaceutical

companies to understand how management of finance plays a crucial role in the

growth. The present study covers two public sector drug & pharmaceutical enterprises

listed on BSE. The study has been undertaken for the period of twelve years from

199899 to 200910. In order to analyze financial performance in terms of liquidity,

solvency, profitability and financial efficiency, various accounting ratios have been

used. Statistical measures i.e., linear multiple regression analysis and test of hypothesis –

t test has been used.

Keywords: De-licensing, Pharmaceutical Industry, Scientific Talent, Research,

Capabilities, Intellecutal, Property, Regime, Productivity, Fixed Assets Performace,

Market Value, Liquidity, Solvency, Financial Efficiency,

Namex International Journal of Management Research 68 Vol. 2, Issue No. 1, Jan-June 2012

Financial Performance Of Indian Pharmaceutical Industry

1. Introduction

The Indian pharmaceutical industry is

one of the world’s largest, ranking 4th

in terms of volume and 13th in terms

of value in the global

pharmaceutical market. In 2005,

domestic pharmaceutical sales were

US$4.5 billion, growing at CAGR

of 8.59%. The Indian pharmaceutical

industry is characterized by a multitude

of manufacturers (over 20,000

registered, as of 2003). These are

predominantly small manufacturers,

focusing on either Active

Pharmaceutical Ingredients (APIs) or

formulations. Until the advent of

product patents in January 2005, only

process patents were applicable in

India, which effectively made it a low

cost, generic market. As a result,

manufacturing expertise and

efficiency were the only requirements

to participate in this industry, creating

low barriers of entry.

As a result, the leading Indian

pharmaceutical companies have

become some of the most efficient

manufacturing units in the world. In

fact, India has the highest number of US

FDA (Food and Drug Administration)

certified manufacturing facilities

outside the United States. There are an

increasing number of opportunities with

large Indian manufacturers & contract

manufacturing organizations for the

increasingly costconscious

multinationals.

One of the major factors that have

increased the confidence of foreign

multinationals looking for local

opportunities in India is the adoption of

a new product patent regime in January

2005. This will facilitate concurrent

global phase II and III clinical trials. A

new patent regime has changed the

dynamics of the Indian pharmaceuticals

industry in other respects, too. Several

leading domestic producers have begun

to conduct original research into new

chemical entities (NCEs) and novel

drug delivery systems. However, these

companies are likely to license most of

these drug candidates to Western

pharmaceutical companies, because few

Indian companies can afford the high

costs and failure rates associated with

developing an NCE. In this context,

several Indian firms have already

entered into research partnerships with

multinationals. Some pharmaceutical

MNCs like AstraZeneca have opened

their own captive research centers in

India to take advantage of the low costs

as well as availability of high quality

intellectual work force.

The present study covers two public

sector drug & pharmaceutical

enterprises listed on BSE. The sample

of the companies has been selected on a

convenient basis and the necessary data

have been obtained from CMIE

database and public enterprises survey.

The researcher selects Karnataka

Antibiotics & Pharmaceuticals Ltd.

(KAPL) and Rajasthan Drugs &

Pharmaceuticals Ltd. (RDPL).

2. Statement of the Problem

Financial performance analysis is the

process of determining the operating

and financial characteristics of a firm

from accounting and financial

statements. The ability of an

Namex International Journal of Management Research 69 Vol. 2, Issue No. 1, Jan-June 2012

Financial Performance Of Indian Pharmaceutical Industry

organization to analyze its financial

position is essential for improving its

competitive position in the

marketplace. Through a careful

analysis of its financial performance,

the organization can identify

opportunities to improve performance

of the department, unit or organizational

level. In this context an attempt has

been made an analysis of financial

performance of pharmaceutical

companies to understand how

management of finance plays a crucial

role in the growth.

3. Objectives of the study

The main objectives of the present work

are to make a study on the overall

financial performance of selected public

sector drug & pharmaceutical

enterprises in India.

4. Methodology

The study has been undertaken for the

period of twelve years from 199899 to

200910. In order to analyze financial

performance in terms of liquidity,

solvency, profitability and financial

efficiency, various accounting ratios

have been used. Various statistical

measures have been used i.e., Mean.,

S.D., C.V., linear multiple regression

analysis and test of hypothesis – t test.

In this context an attempt has been

made an analysis of financial

performance of pharmaceutical

companies to understand how

management of finance plays a crucial

role in the growth.

5. Research Hypotheses

Keeping the above objectives in mind,

the following null and alternative

hypotheses have been formulated and

tested during the study period:

Hypotheses of the Study :

1. When return on investment

increases, liquid ratio remains

same.

2. When return on investment

increases, net profit to total asset

ratio remains same.

3. When return on investment

increases, debt to net worth ratio

remains same.

4. When return on investment

increases, debt equity ratio

remains same.

5. When debt equity ratio

increases, interest coverage ratio

remains same.

6. When net profit to total asset

ratio increases, debt equity ratio

remains same.

7. When return on investment ratio

increases, total liability to total

asset ratio remains same.

Namex International Journal of Management Research 70 Vol. 2, Issue No. 1, Jan-June 2012

Financial Performance Of Indian Pharmaceutical Industry

Financial

Performance

Liquidity

Solvency

Efficiency

Financial Stability

Overall

Profitability

Net Profit

Return on

Investment

Profitability Financial Performance

Indicators

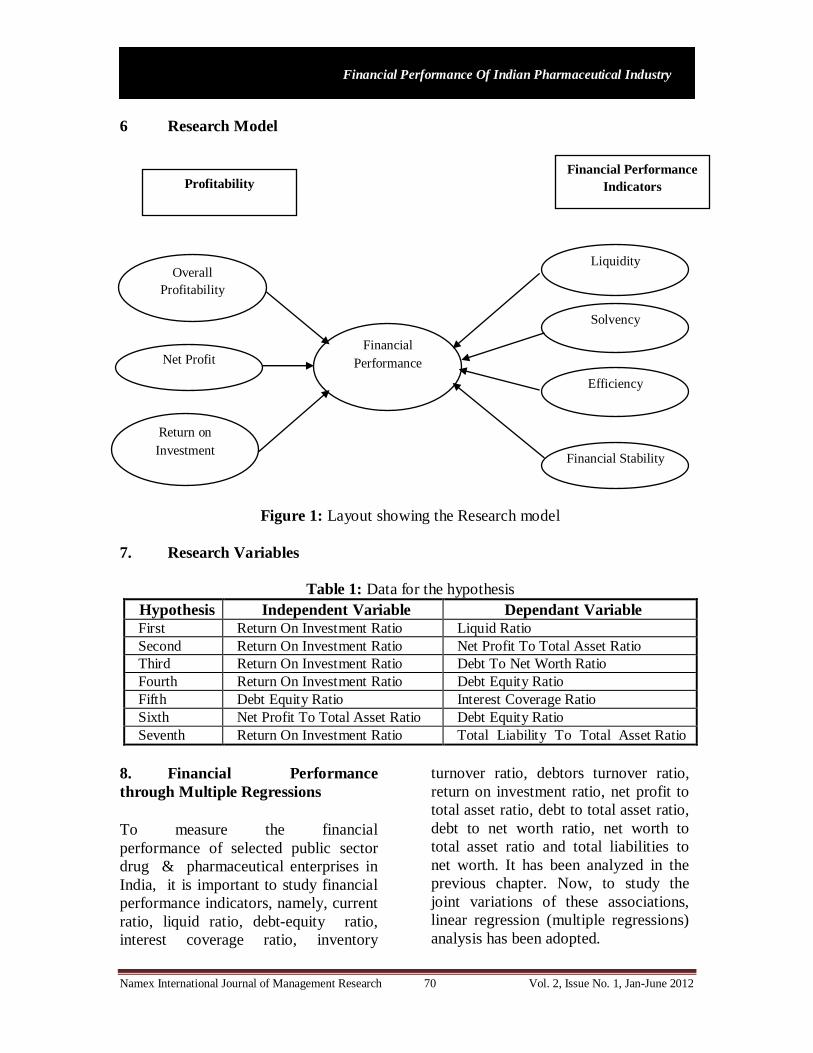

6 Research Model

Figure 1: Layout showing the Research model

7. Research Variables

Table 1: Data for the hypothesis

Hypothesis Independent Variable Dependant Variable First Return On Investment Ratio Liquid Ratio

Second Return On Investment Ratio Net Profit To Total Asset Ratio

Third Return On Investment Ratio Debt To Net Worth Ratio

Fourth Return On Investment Ratio Debt Equity Ratio

Fifth Debt Equity Ratio Interest Coverage Ratio

Sixth Net Profit To Total Asset Ratio Debt Equity Ratio

Seventh Return On Investment Ratio Total Liability To Total Asset Ratio

8. Financial Performance

through Multiple Regressions

To measure the financial

performance of selected public sector

drug & pharmaceutical enterprises in

India, it is important to study financial

performance indicators, namely, current

ratio, liquid ratio, debtequity ratio,

interest coverage ratio, inventory

turnover ratio, debtors turnover ratio,

return on investment ratio, net profit to

total asset ratio, debt to total asset ratio,

debt to net worth ratio, net worth to

total asset ratio and total liabilities to

net worth. It has been analyzed in the

previous chapter. Now, to study the

joint variations of these associations,

linear regression (multiple regressions)

analysis has been adopted.

Namex International Journal of Management Research 71 Vol. 2, Issue No. 1, Jan-June 2012

Financial Performance Of Indian Pharmaceutical Industry

In this section an attempt has been made

to examine composite impact of

financial performance indicators on

profitability through the sophisticated

statistical techniques. Accordingly,

multiple regression techniques have

been applied to study the joint

influence of the selected ratios

indicating company's financial position

and performance on the profitability and

the regression coefficients have been

tested with the help of the most popular

‘t’ test. In this study, CR, LR, DER,

ICR, ITR, DTR, NPTAR, DTAR,

DNWR, NWTAR and TLTWR have

been taken as the explanatory variables

and ROIR has been used as the

dependent variable. The regression

model used in this analysis is

ROIR = £ + ß1CR + ß2 LR + ß3 DER + ß4 ICR + ß5 ITR + ß6DTR + ß7NPTAR

+ ß8 DTAR + ß9 DNWR + ß10 NWTAR + ß11 TLTWR

where £, ß1, ß2, ß3, ß4, ß5, ß6, ß7, ß8, ß9, ß10 and ß11 are the parameters of the ROIR

line.

How different financial performance

indicators adopted in the analysis have

played role in attaining the

profitability is one of the objects of the

present study?

9. Joint Impact of Performance

Indicators on Profitability of KAPL

Multiple regression analysis of KAPL

has been tabulated in Table 8. Table 8

proves the potency of relationship

between the dependent variable, ROIR

and all the independent variables taken

together and the impact of these

independent variables on the

profitability. It was observed that

increase in CR by one unit, the ROIR

increased by 34.713 units that was

statistically significant at 1 per cent

level. For one unit increase in LR, the

profitability of the company increased

by 18.264 units, which was

statistically significant at 1 per cent

level. However, when DER increased

by one unit, the ROIR of the company

decreased by 8.365 units though the

influence of DER on ROIR was very

significant. For one unit increase in

ICR, the profitability of the company

decreased by 0.370 units. Again, two

important indicators of efficiency, ITR

and DTR, increased by one unit, ROIR

decreased by 3.827 units and 1.902

units respectively which was

statistically at 1 per cent level. It was

observed that increase in NPTAR by

one unit, the ROIR decreased by

335.934 units that was statistically

significant at 1 per cent level. For one

unit increase in DTAR, the

profitability of the company decreased

by 203.388 units, which was

statistically significant at 1 per cent

level. However, when DNWR

increased by one unit, the ROIR of the

company decreased by 4.244 units

though the influence of DNWR on

ROIR was very noteworthy. For one

unit increase in NWTAR, the

profitability of the company decreased

by 114.374 units. However, when

TLTWR increased by one unit, the

ROIR of the company decreased by

0.674 units though the influence of

TLTWR on ROIR was very significant.

Namex International Journal of Management Research 72 Vol. 2, Issue No. 1, Jan-June 2012

Financial Performance Of Indian Pharmaceutical Industry

Table 2: Multiple Regression Analysis of KAPL Coefficients (a)

Variables/Model

Unstandardized

Coefficients Standardized Coefficients

t value Sig.

B Std. Error Beta

Constant

CR

LR

DER

ICR

ITR

DTR NPTAR

DTAR

DNWR

NWTAR

TLTWR

59.948

34.713

18.264

8.365

0.370

3.827

1.902 335.934

203.388

4.244

114.374

0.674

0.00

0.00

0.00

0.00

0.00

0.00

0.00 0.00

0.00

0.00

0.00

0.00

2.604

0.844

0.290

1.240

1.376

0.539 1.355

2.604

1.929

3.336

0.156

-

-

-

-

-

-

- -

-

-

-

-

-

-

-

-

-

-

- -

-

-

-

-

a. Dependent Variable: ROIR

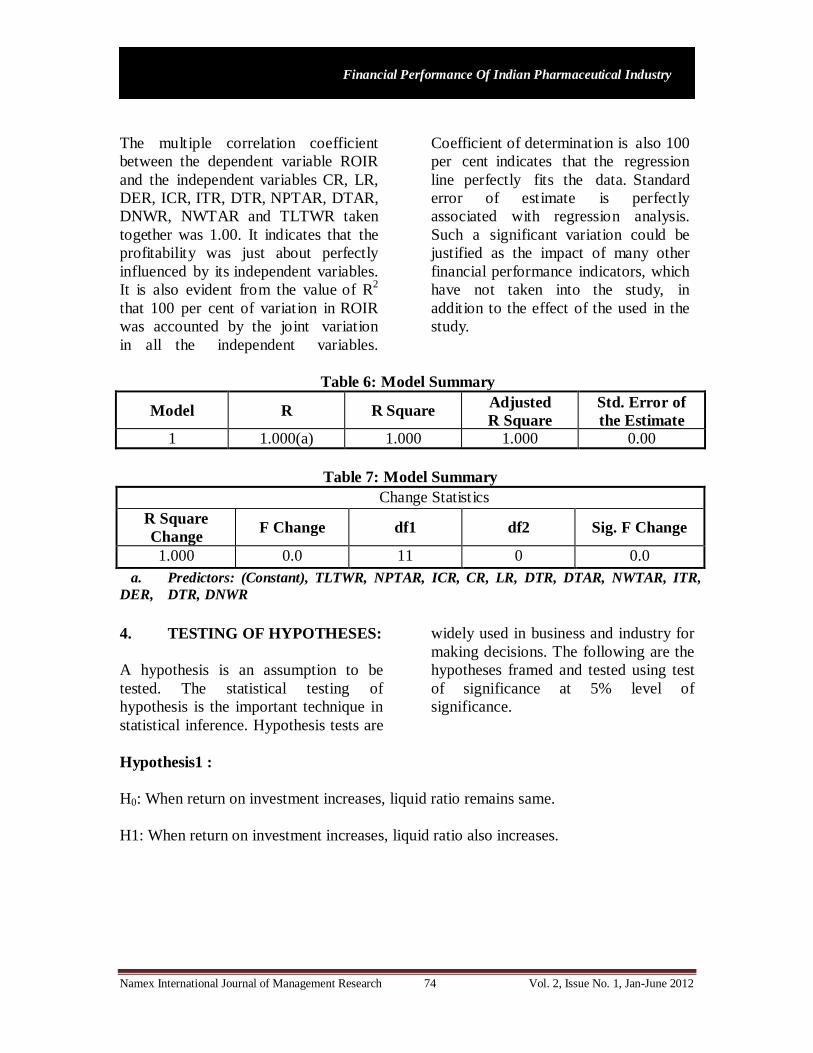

The multiple correlation coefficient

between the dependent variable ROIR

and the independent variables CR, LR,

DER, ICR, ITR, DTR, NPTAR, DTAR,

DNWR, NWTAR and TLTWR taken

together was 1.00. It indicates that the

profitability was just about perfectly

influenced by its independent variables. It

is also evident from the value of R2 that

100 per cent of variation in ROIR was

accounted by the joint variation in all

the independent variables. Coefficient

of determination is also 100 per cent

indicates that the regression line

perfectly fits the data. Standard error of

estimate is perfectly associated with

regression analysis. Such a significant

variation could be justified as the impact

of many other financial performance

indicators, which have not taken into the

study, in addition to the effect of the used

in the study.

Table 3: Model Summary

Model R R Square Adjusted R

Square

Std. Error of

the Estimate 1 1.000(a) 1.000 1.000 0.00

Table 4: Model Summary

Change Statistics

R Square

Change F Change df1 df2 Sig. F Change

1.000 0.00 11 0 0.00

a. Predictors: (Constant), TLTWR, DNWR, ICR, DTR, LR, ITR, DER,

NPTAR, NWTAR, DTAR, CR

Namex International Journal of Management Research 73 Vol. 2, Issue No. 1, Jan-June 2012

Financial Performance Of Indian Pharmaceutical Industry

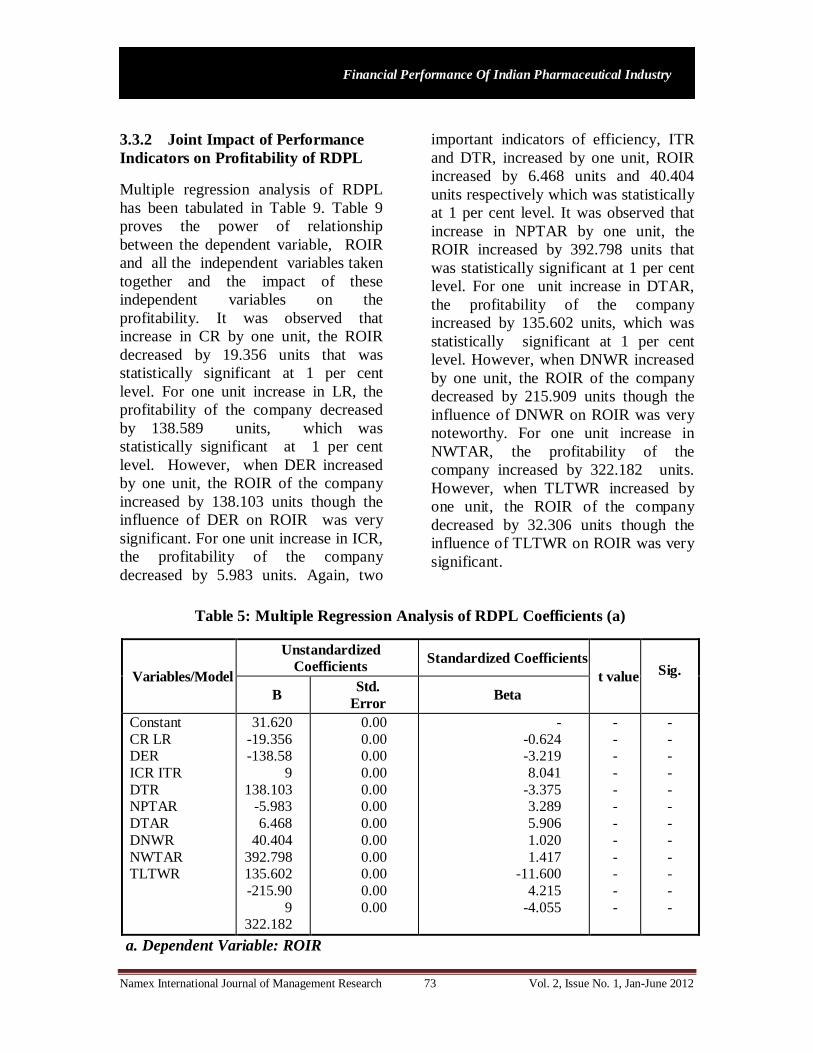

3.3.2 Joint Impact of Performance

Indicators on Profitability of RDPL

Multiple regression analysis of RDPL

has been tabulated in Table 9. Table 9

proves the power of relationship

between the dependent variable, ROIR

and all the independent variables taken

together and the impact of these

independent variables on the

profitability. It was observed that

increase in CR by one unit, the ROIR

decreased by 19.356 units that was

statistically significant at 1 per cent

level. For one unit increase in LR, the

profitability of the company decreased

by 138.589 units, which was

statistically significant at 1 per cent

level. However, when DER increased

by one unit, the ROIR of the company

increased by 138.103 units though the

influence of DER on ROIR was very

significant. For one unit increase in ICR,

the profitability of the company

decreased by 5.983 units. Again, two

important indicators of efficiency, ITR

and DTR, increased by one unit, ROIR

increased by 6.468 units and 40.404

units respectively which was statistically

at 1 per cent level. It was observed that

increase in NPTAR by one unit, the

ROIR increased by 392.798 units that

was statistically significant at 1 per cent

level. For one unit increase in DTAR,

the profitability of the company

increased by 135.602 units, which was

statistically significant at 1 per cent

level. However, when DNWR increased

by one unit, the ROIR of the company

decreased by 215.909 units though the

influence of DNWR on ROIR was very

noteworthy. For one unit increase in

NWTAR, the profitability of the

company increased by 322.182 units.

However, when TLTWR increased by

one unit, the ROIR of the company

decreased by 32.306 units though the

influence of TLTWR on ROIR was very

significant.

Table 5: Multiple Regression Analysis of RDPL Coefficients (a)

Variables/Model

Unstandardized

Coefficients Standardized Coefficients

t value Sig.

B Std.

Error Beta

Constant

CR LR DER

ICR ITR

DTR NPTAR

DTAR

DNWR

NWTAR TLTWR

31.620

19.356 138.58

9

138.103 5.983

6.468

40.404

392.798 135.602

215.90

9 322.182

32.306

0.00

0.00 0.00

0.00

0.00 0.00

0.00

0.00

0.00 0.00

0.00

0.00

0.624 3.219

8.041

3.375 3.289

5.906

1.020

1.417 11.600

4.215

4.055

-

- -

-

- -

-

-

- -

-

-

-

- -

-

- -

-

-

- -

-

-

a. Dependent Variable: ROIR

Namex International Journal of Management Research 74 Vol. 2, Issue No. 1, Jan-June 2012

Financial Performance Of Indian Pharmaceutical Industry

The multiple correlation coefficient

between the dependent variable ROIR

and the independent variables CR, LR,

DER, ICR, ITR, DTR, NPTAR, DTAR,

DNWR, NWTAR and TLTWR taken

together was 1.00. It indicates that the

profitability was just about perfectly

influenced by its independent variables.

It is also evident from the value of R2

that 100 per cent of variation in ROIR

was accounted by the joint variation

in all the independent variables.

Coefficient of determination is also 100

per cent indicates that the regression

line perfectly fits the data. Standard

error of estimate is perfectly

associated with regression analysis.

Such a significant variation could be

justified as the impact of many other

financial performance indicators, which

have not taken into the study, in

addition to the effect of the used in the

study.

Table 6: Model Summary

Model R R Square Adjusted

R Square

Std. Error of

the Estimate

1 1.000(a) 1.000 1.000 0.00

Table 7: Model Summary

Change Statistics

R Square

Change F Change df1 df2 Sig. F Change

1.000 0.0 11 0 0.0

a. Predictors: (Constant), TLTWR, NPTAR, ICR, CR, LR, DTR, DTAR, NWTAR, ITR,

DER, DTR, DNWR

4. TESTING OF HYPOTHESES:

A hypothesis is an assumption to be

tested. The statistical testing of

hypothesis is the important technique in

statistical inference. Hypothesis tests are

widely used in business and industry for

making decisions. The following are the

hypotheses framed and tested using test

of significance at 5% level of

significance.

Hypothesis 1 :

H0: When return on investment increases, liquid ratio remains same.

H1: When return on investment increases, liquid ratio also increases.

Namex International Journal of Management Research 75 Vol. 2, Issue No. 1, Jan-June 2012

Financial Performance Of Indian Pharmaceutical Industry

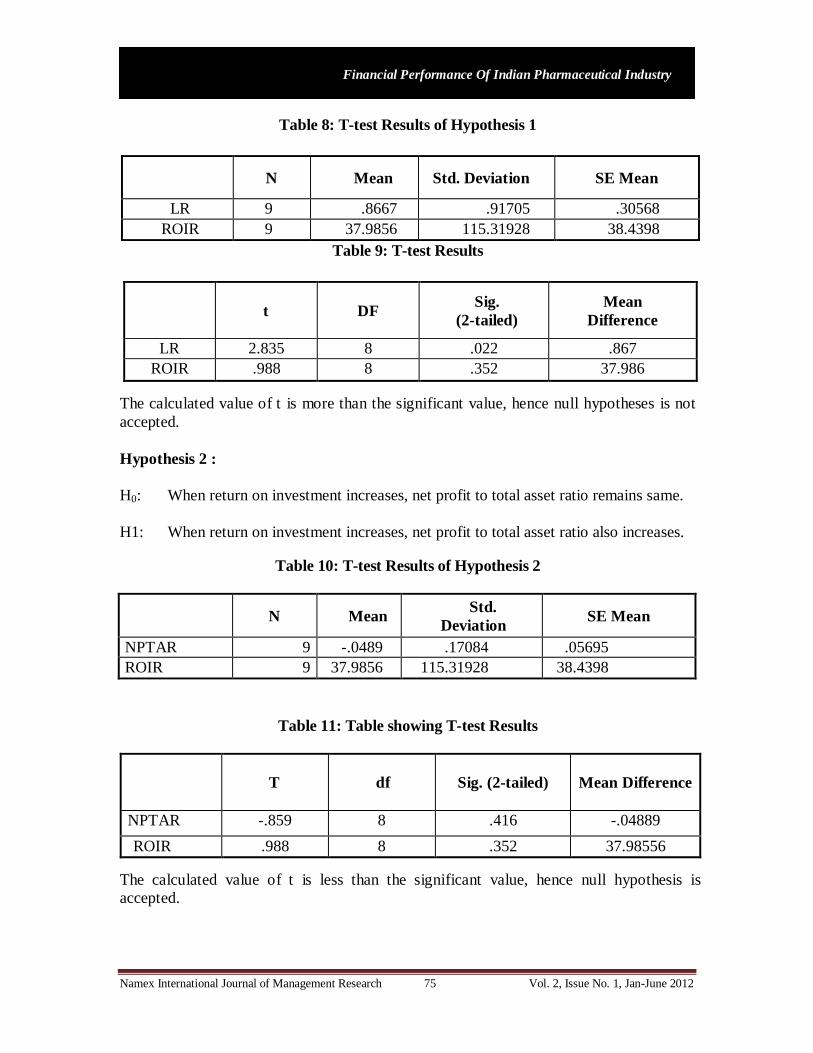

Table 8: Ttest Results of Hypothesis 1

N Mean Std. Deviation SE Mean

LR 9 .8667 .91705 .30568

ROIR 9 37.9856 115.31928 38.4398

Table 9: Ttest Results

t DF Sig.

(2tailed)

Mean

Difference

LR 2.835 8 .022 .867

ROIR .988 8 .352 37.986

The calculated value of t is more than the significant value, hence null hypotheses is not

accepted.

Hypothesis 2 :

H0: When return on investment increases, net profit to total asset ratio remains same.

H1: When return on investment increases, net profit to total asset ratio also increases.

Table 10: Ttest Results of Hypothesis 2

N Mean Std.

Deviation SE Mean

NPTAR 9 .0489 .17084 .05695

ROIR 9 37.9856 115.31928 38.4398

Table 11: Table showing Ttest Results

T df Sig. (2tailed) Mean Difference

NPTAR .859 8 .416 .04889

ROIR .988 8 .352 37.98556

The calculated value of t is less than the significant value, hence null hypothesis is

accepted.

Namex International Journal of Management Research 76 Vol. 2, Issue No. 1, Jan-June 2012

Financial Performance Of Indian Pharmaceutical Industry

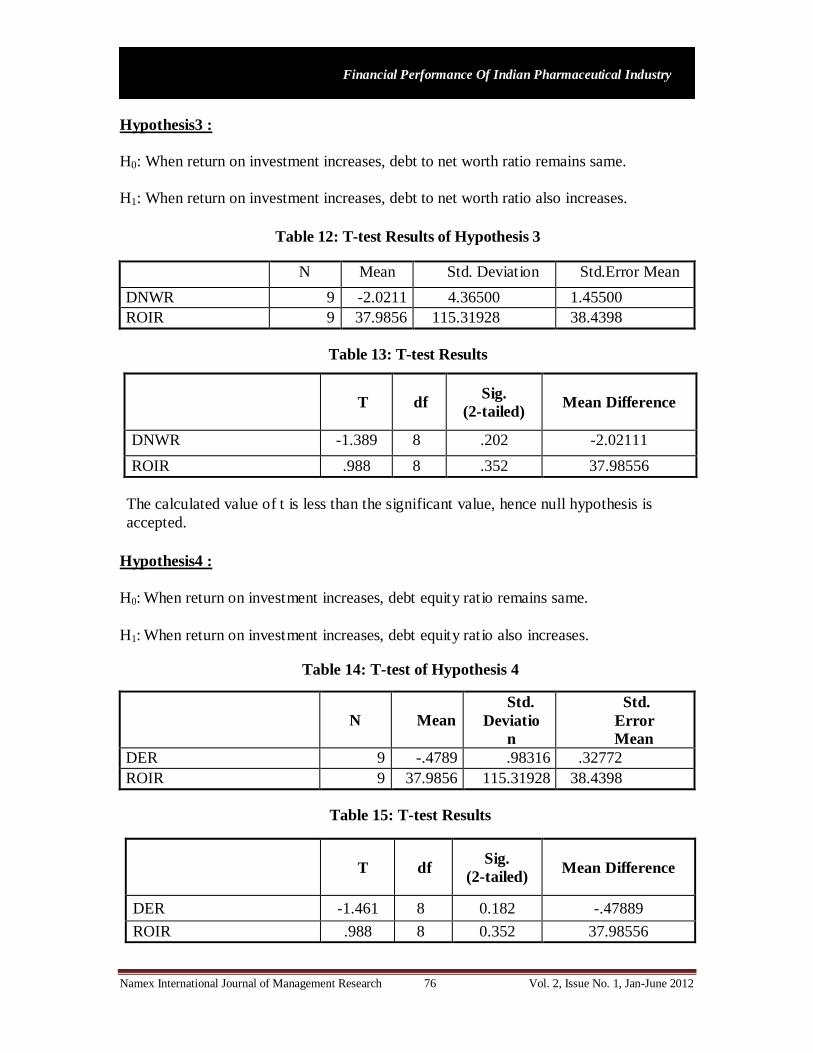

Hypothesis 3 :

H0: When return on investment increases, debt to net worth ratio remains same.

H1: When return on investment increases, debt to net worth ratio also increases.

Table 12: Ttest Results of Hypothesis 3

N Mean Std. Deviation Std.Error Mean

DNWR 9 2.0211 4.36500 1.45500

ROIR 9 37.9856 115.31928 38.4398

Table 13: Ttest Results

T df Sig.

(2tailed) Mean Difference

DNWR 1.389 8 .202 2.02111

ROIR .988 8 .352 37.98556

The calculated value of t is less than the significant value, hence null hypothesis is

accepted.

Hypothesis 4 :

H0: When return on investment increases, debt equity ratio remains same.

H1: When return on investment increases, debt equity ratio also increases.

Table 14: Ttest of Hypothesis 4

N Mean

Std.

Deviatio

n

Std.

Error

Mean

DER 9 .4789 .98316 .32772

ROIR 9 37.9856 115.31928 38.4398

Table 15: Ttest Results

T df Sig.

(2tailed) Mean Difference

DER 1.461 8 0.182 .47889

ROIR .988 8 0.352 37.98556

Namex International Journal of Management Research 77 Vol. 2, Issue No. 1, Jan-June 2012

Financial Performance Of Indian Pharmaceutical Industry

The calculated value of t is less than the significant value, hence null hypothesis is

accepted.

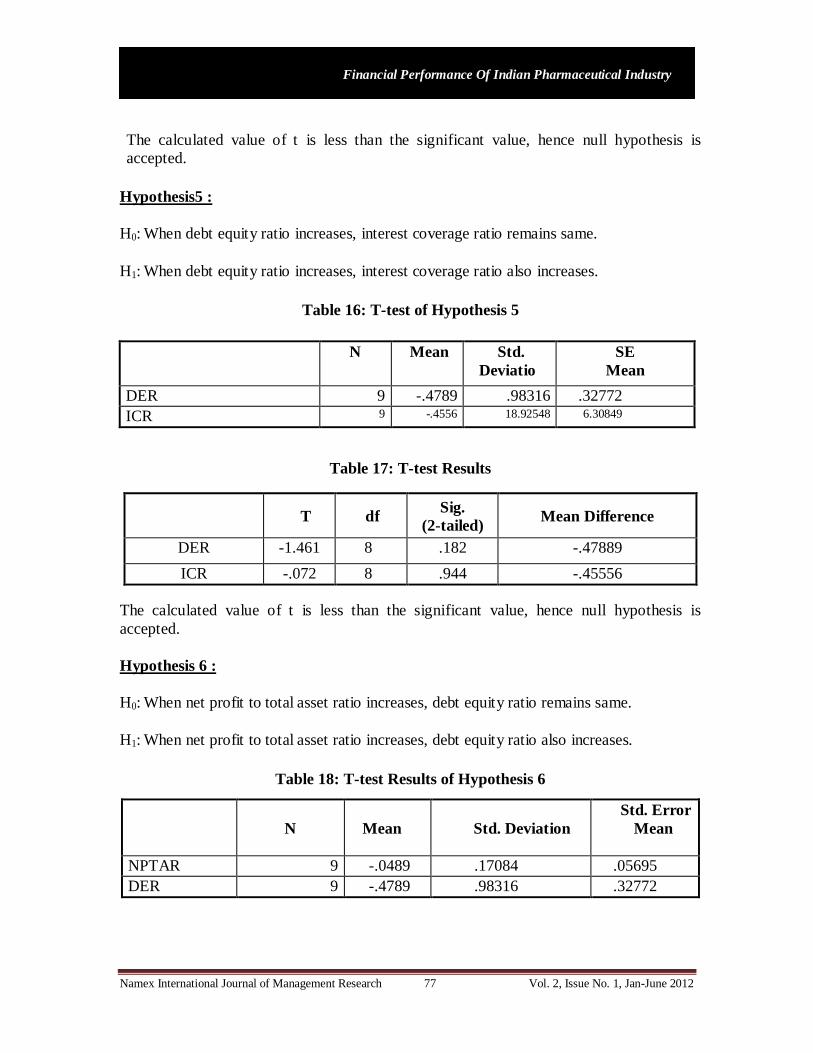

Hypothesis 5 :

H0: When debt equity ratio increases, interest coverage ratio remains same.

H1: When debt equity ratio increases, interest coverage ratio also increases.

Table 16: Ttest of Hypothesis 5

N Mean Std.

Deviatio

n

SE

Mean

DER 9 .4789 .98316 .32772

ICR 9 .4556 18.92548 6.30849

Table 17: Ttest Results

T df Sig.

(2tailed) Mean Difference

DER 1.461 8 .182 .47889

ICR .072 8 .944 .45556

The calculated value of t is less than the significant value, hence null hypothesis is

accepted.

Hypothesis 6 :

H0: When net profit to total asset ratio increases, debt equity ratio remains same.

H1: When net profit to total asset ratio increases, debt equity ratio also increases.

Table 18: Ttest Results of Hypothesis 6

N

Mean

Std. Deviation

Std. Error

Mean

NPTAR 9 .0489 .17084 .05695

DER 9 .4789 .98316 .32772

Namex International Journal of Management Research 78 Vol. 2, Issue No. 1, Jan-June 2012

Financial Performance Of Indian Pharmaceutical Industry

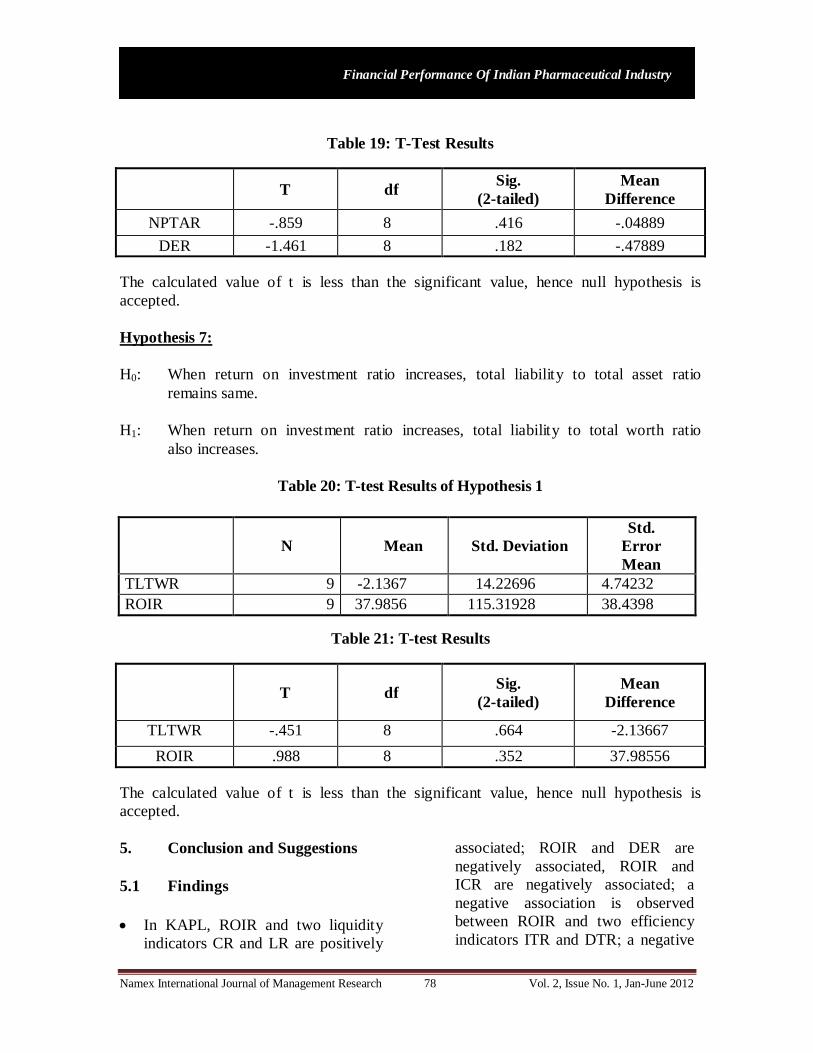

Table 19: TTest Results

T df Sig.

(2tailed)

Mean

Difference

NPTAR .859 8 .416 .04889

DER 1.461 8 .182 .47889

The calculated value of t is less than the significant value, hence null hypothesis is

accepted.

Hypothesis 7:

H0: When return on investment ratio increases, total liability to total asset ratio

remains same.

H1: When return on investment ratio increases, total liability to total worth ratio

also increases.

Table 20: Ttest Results of Hypothesis 1

N Mean Std. Deviation

Std.

Error

Mean

TLTWR 9 2.1367 14.22696 4.74232

ROIR 9 37.9856 115.31928 38.4398

Table 21: Ttest Results

T df Sig.

(2tailed)

Mean

Difference

TLTWR .451 8 .664 2.13667

ROIR .988 8 .352 37.98556

The calculated value of t is less than the significant value, hence null hypothesis is

accepted.

5. Conclusion and Suggestions

5.1 Findings

In KAPL, ROIR and two liquidity

indicators CR and LR are positively

associated; ROIR and DER are

negatively associated, ROIR and

ICR are negatively associated; a

negative association is observed

between ROIR and two efficiency

indicators ITR and DTR; a negative

Namex International Journal of Management Research 79 Vol. 2, Issue No. 1, Jan-June 2012

Financial Performance Of Indian Pharmaceutical Industry

association between ROIR and

NPTAR is seen; a negative

association between DTAR and

DNWR with ROIR is observed;

ROIR is negatively associated with

NWTAR and a negative

association is clearly seen between

ROIR and TWTAR. All the

performance indicators and

profitability are just about

correlated. The coefficient of

determination is almost 100 per cent.

In RDPL, ROIR and two liquidity

indicators CR and LR are negatively

associated; ROIR and DER are

positively associated, ROIR and

ICR are negatively associated; a

positive association is observed

between ROIR and two efficiency

indicators ITR and DTR; a positive

association between ROIR and

NPTAR is seen; a positive and

negative association between

DTAR and DNWR with ROIR is

observed; ROIR is positively

associated with NWTAR and a

negative association is clearly seen

between ROIR and TWTAR. All

the performance indicators and

profitability are just about

correlated. The coefficient of

determination is almost 100 per cent.

5.2 Suggestions

For solving the problems of

debtors’ management in case of

RDPL, an effective professional

coordination between sales,

production and finance departments

is called for. Prompt billing, timely

reminders to defaulting customers

and immediate action should be

ensured. The investment in loans

and advances should be minimized

to the extent possible.

To improve the financial position

of KAPL and RDPL, equity

oriented dependability have to be

reduced properly.

To improve the financial stability of

both the companies under the study,

proper mixture of stake in the

business between the owners and

the creditors have to be made in

which significant pressure on future

cash flows can be avoid.

Higher degree of multiple

correlations implies the presence

of explained variables (liquidity,

solvency, efficiency and financial

stability) that have lead to lower

profitability over and above poor

financial position and performance,

are in action. To remove such

problems, accurate liquidity

management, correct solvency or

leverage management and

appropriate wealth management is

highly needed.

As far as selected enterprises are

concerned, the management of the

companies should contemplate its

efforts in maximizing assets and

minimizing liabilities, so that the

company's financial position could

be improved.

Conclusions of the Study

From the study of the financial

performance of the select

pharmaceutical it can be concluded that

the liquidity position was strong in

Namex International Journal of Management Research 80 Vol. 2, Issue No. 1, Jan-June 2012

Financial Performance Of Indian Pharmaceutical Industry

case of KAPL and RDPL thereby

reflecting the ability of the companies

to pay shortterm obligations on due

dates.Longterm solvency in case of

KAPL and RDPL in all years which

shows that companies relied more on

external funds in terms of longterm

borrowings thereby providing a lower

degree of protection to the

creditors.Debtors’ turnover ratio of

RDPL needs to be improved as the

solvency of the firm depends upon the

sales income generated from the use of

various assets.Financial stability ratios

in the vein of debt to total asset ratio,

debt to net worth ratio, net worth to

total asset ratio and total liabilities to

total worth ratio in case of both the

selected companies have showed a

downward trend and consequently the

financial stability of selected

pharmaceutical companies have been

decreasing at an intense rate.The

Indian pharmaceutical industry will

witness an increase in the market share.

The sector is poised not only to take

new challenge but to sustain the

growth momentum of the past decade.

6. Limitations of the Study

Study exclusively depends on the

published financial data, so it is

subject to all limitations that are

inherent in the condensed published

financial statements.

The drug & pharmaceutical

enterprises selected have been taken

from CMIE database. The study

covers a period of only twelve years

from 1999 to 2010. The data

collected is only for ten companies

and this might not be true

representation of the population.

This is a major limitation of the

research.

7. References

1. Biswanath, S.R. (2008), “A Case

Study: Financial Performance of

Pharmaceutical Companies”, Oxford

University Press, New Delhi.

2. Chaudhuri, Sudip (2005), “The

WTO and India’s Pharmaceuticals

Industry: Patent Protection TRIPS

and Developing Countries”, Oxford

University Press, New Delhi, p.65.

3. Clark, Andrew (1995), “Global

Healthcare: Indian Pharmaceutical

Sector”, Barings Securities: London

Felker.

4. Erich A. Helfert (2002), “Techniques

of Financial Analysis”,

McGrawHill/Irwin, USA.

5. Kambhampati, U. S. (1996)

Industrial Concentration and

Performance; A Study of the

Structure, Conduct and Performance

of Indian Industry, (New Delhi:

Oxford University Press), New

Delhi, 89.

6. Kothari C.R. (2003), “Research

Methodology – Methods &

Techniques, Wishawa Prakashan,

New Delhi.

7. Abhinav Agrawal, Kamal Dua,

Vaibhav Garg, U.V.S. Sara and

Akash Taneja (2006), “Challenges

and Opportunities for the Indian

Pharma Industry”, Health

Administrator, Vol: XX Number

1&2.

8. Aggarwal, Aradhana (2008),

“Strategic Approach to

Strengthening the International

Competitiveness in Knowledge

Based Industries: The Indian

Pharmaceutical Industry.” RISDP,

Namex International Journal of Management Research 81 Vol. 2, Issue No. 1, Jan-June 2012

Financial Performance Of Indian Pharmaceutical Industry

New Delhi.

9. Agarwal Sumit, H. Michele, Oberoi

Arjun (2010), “Unlocking the Value

in Big Pharma”, The McKinsey

Quarterly, 2010 Number 2.

10. Altman, E. (1968), “Financial

Ratios, Discriminant Analysis and

the Prediction of Corporate

Bankruptcy”, Journal of Finance.

11. Chen, Q. (1999), “Evidence

Analysis on Financial Distress of

Listing Companies”, Accounting

Research.

12. Chaudhuri, Sudip (2005), “The

WTO and India’s Pharmaceuticals

Industry: Patent

Protection TRIPS and Developing

Countries”, Oxford University Press,

New Delhi.

13. Deakin, E.B. (1972), “A

Discriminant Analysis of

Predictors of Business Failure”,

Journal of Accounting Research,

March.

14. Mishra, P. (2006) Mergers

Acquisition Market Structure and

Industry Performance: Experience

of Indian Pharmaceutical Industry,

Review of Development and

Change, 11(2).

15. Mishra, P. (2008)

ConcentrationMarkup Relationship

in Indian Manufacturing Sector,

Economic and Political Weekly,

43(39).

16. Ohlson, James A. (1980),

“Financial ratios and the

probabilities prediction of

bankruptcy”, Journal of Accounting

Research, Vol. 18.