Embed Size (px)

Citation preview

Annual results 2012

Financial performance George Quinn, Group CFO

Business update Michel M. Liès, Group CEO

Today’s agenda

2

Annual results 2012

Financial performance George Quinn, Group CFO

3

Annual results 2012

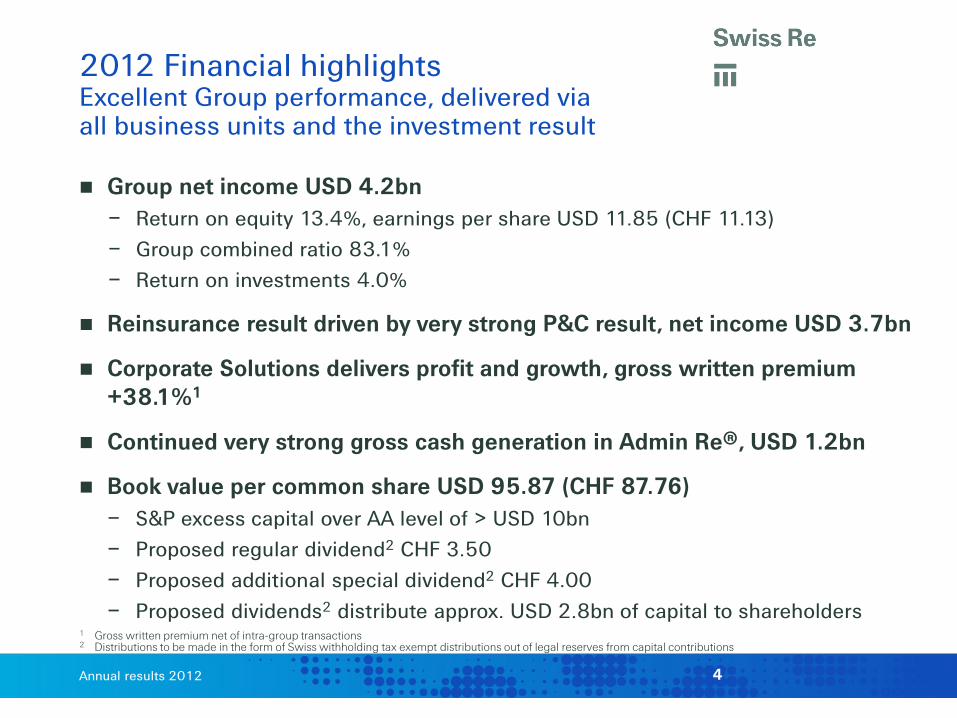

Group net income USD 4.2bn – Return on equity 13.4%, earnings per share USD 11.85 (CHF 11.13) – Group combined ratio 83.1% – Return on investments 4.0%

Reinsurance result driven by very strong P&C result, net income USD 3.7bn

Corporate Solutions delivers profit and growth, gross written premium +38.1%1

Continued very strong gross cash generation in Admin Re®, USD 1.2bn

Book value per common share USD 95.87 (CHF 87.76) – S&P excess capital over AA level of > USD 10bn

– Proposed regular dividend2 CHF 3.50 – Proposed additional special dividend2 CHF 4.00 – Proposed dividends2 distribute approx. USD 2.8bn of capital to shareholders

1 Gross written premium net of intra-group transactions 2 Distributions to be made in the form of Swiss withholding tax exempt distributions out of legal reserves from capital contributions

2012 Financial highlights Excellent Group performance, delivered via all business units and the investment result

4

Annual results 2012

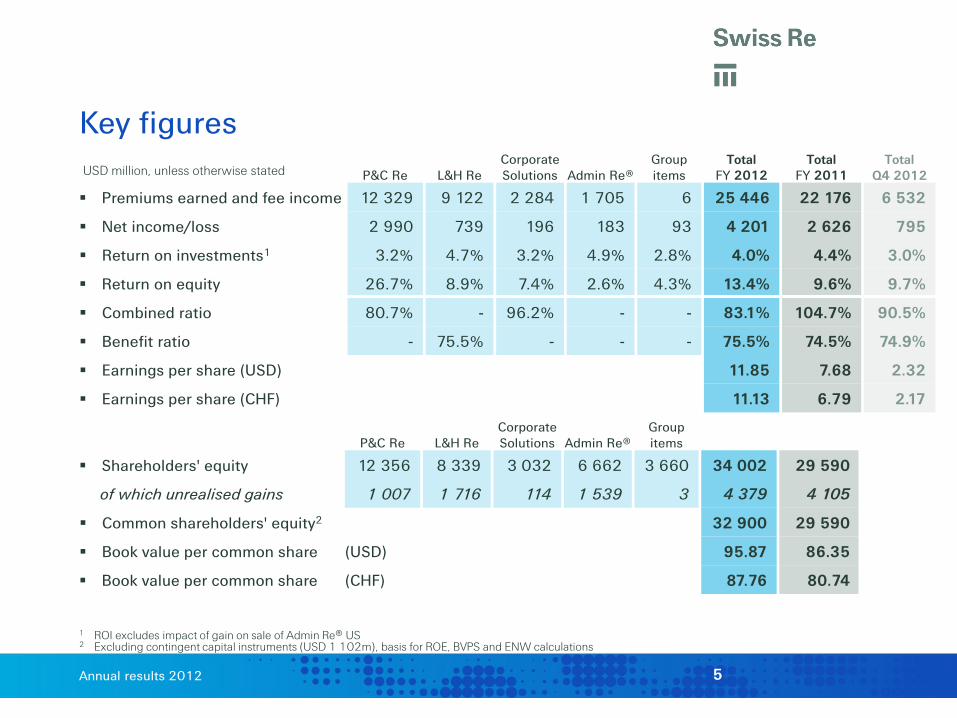

USD million, unless otherwise stated P&C Re L&H Re Corporate Solutions Admin Re®

Group items

Total FY 2012

Total FY 2011

Total Q4 2012

Premiums earned and fee income 12 329 9 122 2 284 1 705 6 25 446 22 176 6 532

Net income/loss 2 990 739 196 183 93 4 201 2 626 795

Return on investments1 3.2% 4.7% 3.2% 4.9% 2.8% 4.0% 4.4% 3.0%

Return on equity 26.7% 8.9% 7.4% 2.6% 4.3% 13.4% 9.6% 9.7%

Combined ratio 80.7% - 96.2% - - 83.1% 104.7% 90.5%

Benefit ratio - 75.5% - - - 75.5% 74.5% 74.9%

Earnings per share (USD) 11.85 7.68 2.32

Earnings per share (CHF) 11.13 6.79 2.17

Key figures

P&C Re L&H Re Corporate Solutions Admin Re®

Group items

Shareholders' equity 12 356 8 339 3 032 6 662 3 660 34 002 29 590

of which unrealised gains 1 007 1 716 114 1 539 3 4 379 4 105

Common shareholders' equity2 32 900 29 590

Book value per common share (USD) 95.87 86.35

Book value per common share (CHF) 87.76 80.74

1 ROI excludes impact of gain on sale of Admin Re® US 2 Excluding contingent capital instruments (USD 1 102m), basis for ROE, BVPS and ENW calculations

5

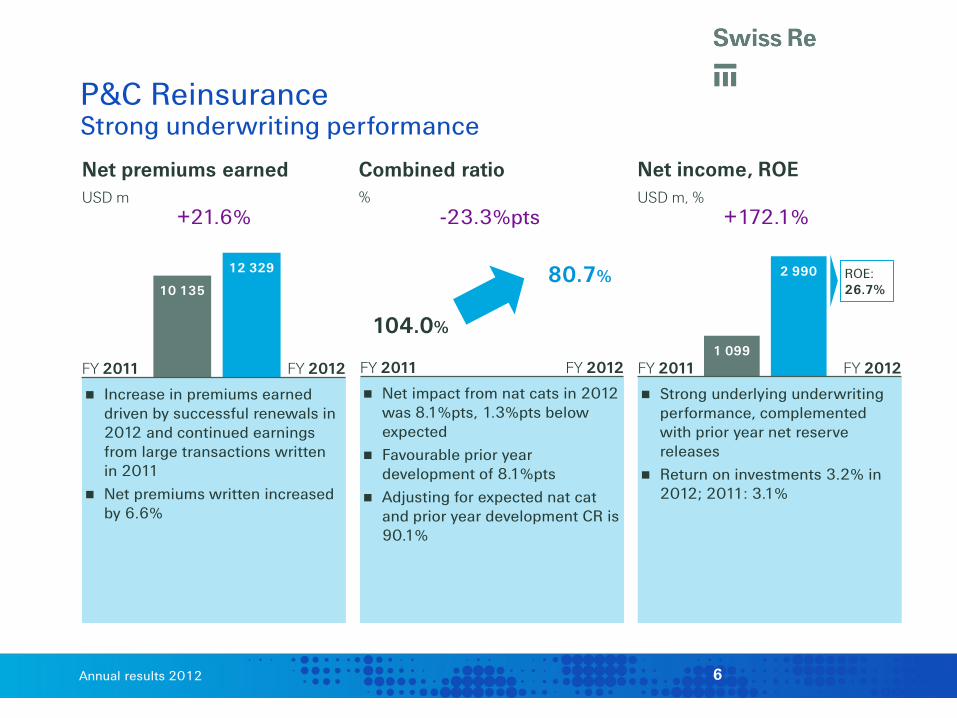

Annual results 2012

1 099

2 990 10 135

12 329

Net premiums earned USD m

Net income, ROE USD m, %

+21.6%

ROE: 26.7%

Combined ratio %

80.7%

104.0%

-23.3%pts +172.1%

P&C Reinsurance Strong underwriting performance

FY 2011 FY 2012

Increase in premiums earned driven by successful renewals in 2012 and continued earnings from large transactions written in 2011

Net premiums written increased by 6.6%

FY 2011 FY 2012

Net impact from nat cats in 2012 was 8.1%pts, 1.3%pts below expected

Favourable prior year development of 8.1%pts

Adjusting for expected nat cat and prior year development CR is 90.1%

FY 2011 FY 2012

Strong underlying underwriting performance, complemented with prior year net reserve releases

Return on investments 3.2% in 2012; 2011: 3.1%

6

Annual results 2012

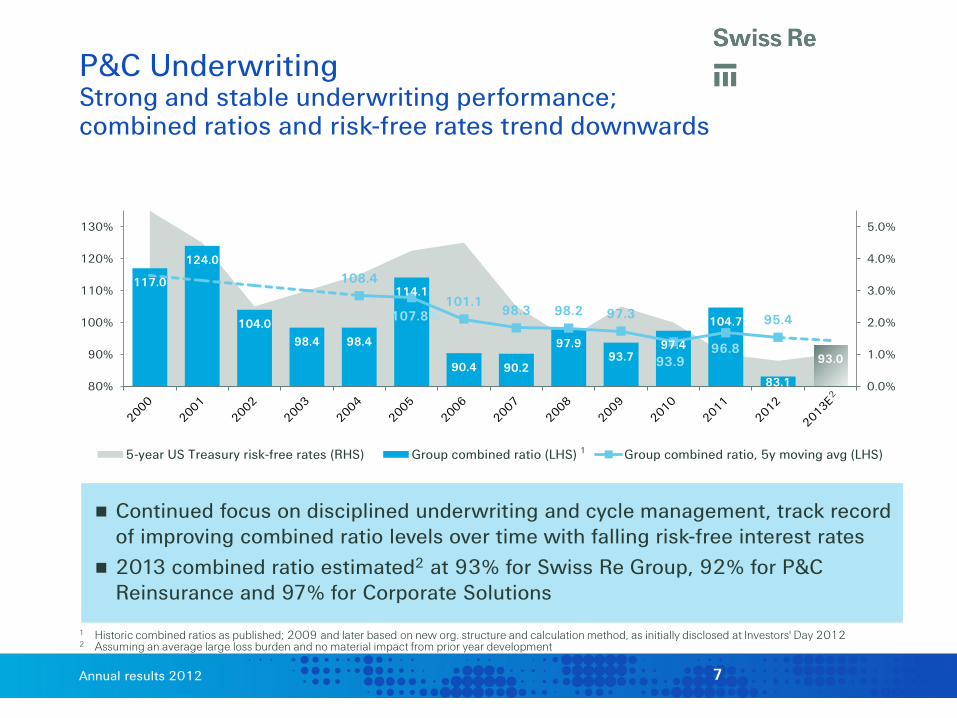

Continued focus on disciplined underwriting and cycle management, track record of improving combined ratio levels over time with falling risk-free interest rates

2013 combined ratio estimated2 at 93% for Swiss Re Group, 92% for P&C Reinsurance and 97% for Corporate Solutions

P&C Underwriting Strong and stable underwriting performance; combined ratios and risk-free rates trend downwards

1 Historic combined ratios as published; 2009 and later based on new org. structure and calculation method, as initially disclosed at Investors' Day 2012 2 Assuming an average large loss burden and no material impact from prior year development

117.0

124.0

104.0

98.4 98.4

114.1

90.4 90.2

97.9 93.7

97.4

104.7

83.1

93.0

108.4

107.8% 101.1

98.3 98.2 97.3

93.9 96.8

95.4

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

80%

90%

100%

110%

120%

130%

5-year US Treasury risk-free rates (RHS) Group combined ratio (LHS) Group combined ratio, 5y moving avg (LHS)1

7

Annual results 2012

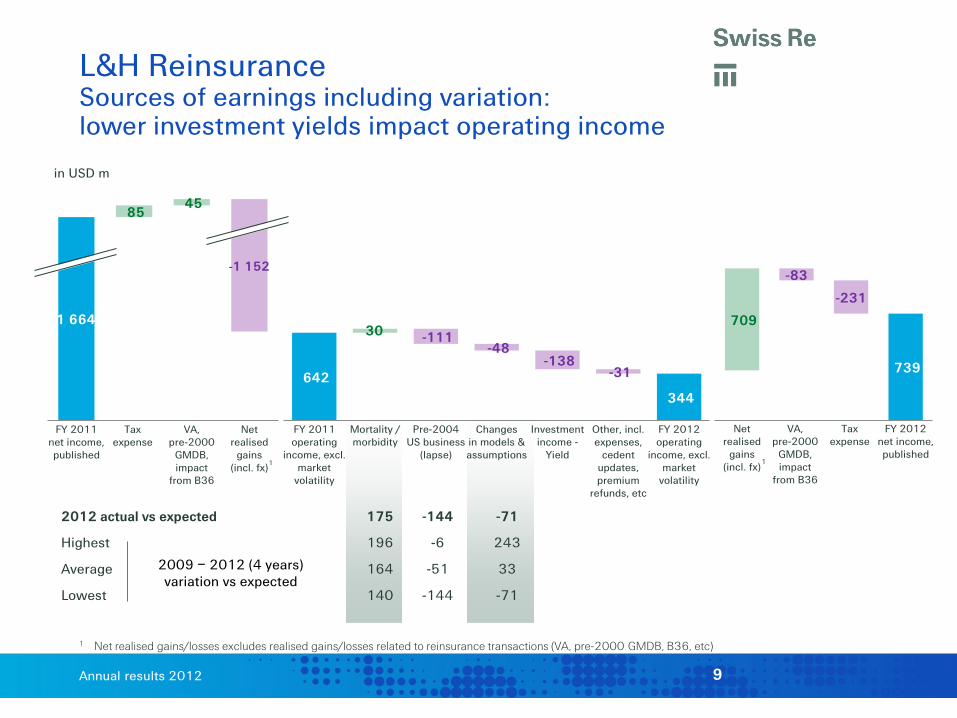

1 664

739

9 948 10 488

Operating revenues USD m

Net income, ROE USD m, %

Benefit ratio1

% +5.4% +1.0%pts

75.5%

74.5%

1 Benefit ratio excludes the impact of VA & pre-2000 GMDB from all periods presented 2 Net realised gains excludes realised gains/losses related to reinsurance transactions (VA, pre-2000 GMDB, B36, etc) of USD -147m, largely contained in the VA,

pre-2000 GMDB, B36 result of USD -83m

ROE: 8.9%

-55.6%

FY 2011 FY 2012

Favourable mortality largely offset by unfavourable morbidity

Adverse results of pre-2004 US business, USD 144m loss; 2011: USD 33m loss

Higher benefit ratio partly due to change in business mix, particularly increase in weighting of new health business

FY 2011 FY 2012 The increase in premium and fee

income is driven by new health business in Europe and Asia and new longevity business in Europe

Premiums earned and fee income increased by 9%; Life grew 3% and Health 23%

Lower investment income due to lower investment yields

FY 2011 FY 2012

Net realised gains (incl. fx)2 of USD 709m significantly lower than in 2011: USD 1 152m

Net inv. income USD 1 365m in 2012; 2011: USD 1 544m

Return on investments 4.7% Exceptional 2011 tax rate (4.9%)

not repeated in 2012 (22.9%)

L&H Reinsurance Lower investment return and unfavourable impact of pre-2004 US business

8

Annual results 2012

2012 actual vs expected 175 -144 -71

Highest 196 -6 243

Average 164 -51 33

Lowest 140 -144 -71

L&H Reinsurance Sources of earnings including variation: lower investment yields impact operating income

1 Net realised gains/losses excludes realised gains/losses related to reinsurance transactions (VA, pre-2000 GMDB, B36, etc)

1 664

-1 152

85 45

FY 2011net income,published

Taxexpense

VA,pre-2000

GMDB,impact

from B36

Netrealised

gains(incl. fx)

-83

-231

709

739

Netrealised

gains(incl. fx)

VA,pre-2000

GMDB,impact

from B36

Taxexpense

FY 2012net income,published

in USD m

-111 -48

-138 -31

30

642 344

FY 2011operating

income, excl.market

volatility

Mortality /morbidity

Pre-2004US business

(lapse)

Changesin models &assumptions

Investmentincome -

Yield

Other, incl.expenses,

cedentupdates,premium

refunds, etc

FY 2012operating

income, excl.market

volatility

1 1

2009 – 2012 (4 years) variation vs expected

9

Annual results 2012

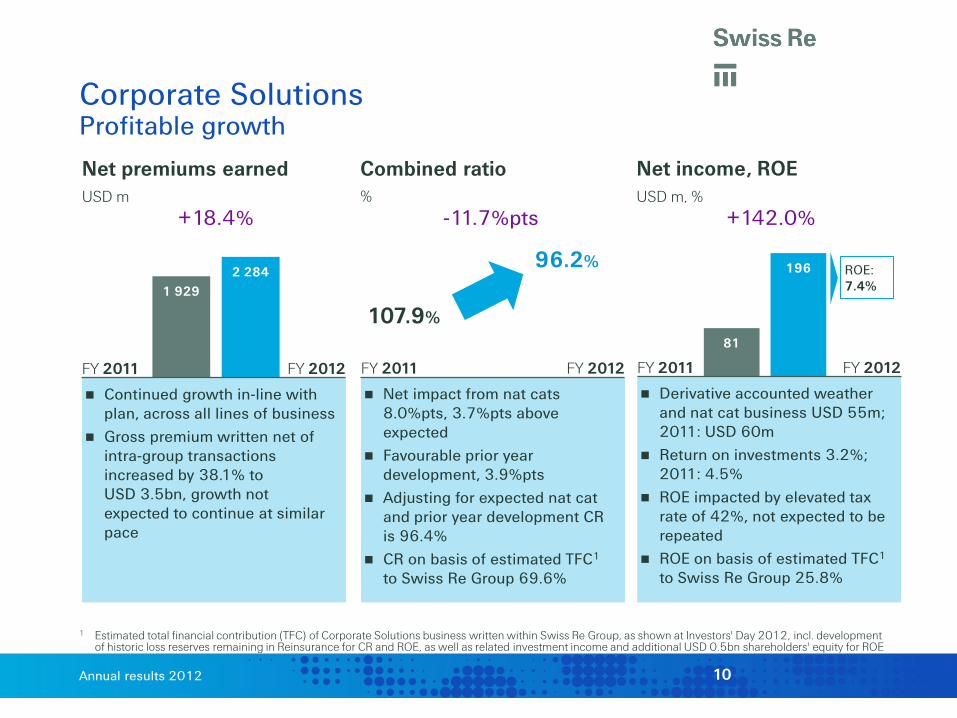

81

196

1 929 2 284

Net premiums earned USD m

Combined ratio %

Net income, ROE USD m, %

Corporate Solutions Profitable growth

1 Estimated total financial contribution (TFC) of Corporate Solutions business written within Swiss Re Group, as shown at Investors' Day 2012, incl. development of historic loss reserves remaining in Reinsurance for CR and ROE, as well as related investment income and additional USD 0.5bn shareholders' equity for ROE

FY 2011 FY 2012

Net impact from nat cats 8.0%pts, 3.7%pts above expected

Favourable prior year development, 3.9%pts

Adjusting for expected nat cat and prior year development CR is 96.4%

CR on basis of estimated TFC1 to Swiss Re Group 69.6%

FY 2011 FY 2012

Derivative accounted weather and nat cat business USD 55m; 2011: USD 60m

Return on investments 3.2%; 2011: 4.5%

ROE impacted by elevated tax rate of 42%, not expected to be repeated

ROE on basis of estimated TFC1

to Swiss Re Group 25.8%

FY 2011 FY 2012

Continued growth in-line with plan, across all lines of business

Gross premium written net of intra-group transactions increased by 38.1% to USD 3.5bn, growth not expected to continue at similar pace

+18.4%

96.2%

107.9%

-11.7%pts

ROE: 7.4%

+142.0%

10

Annual results 2012

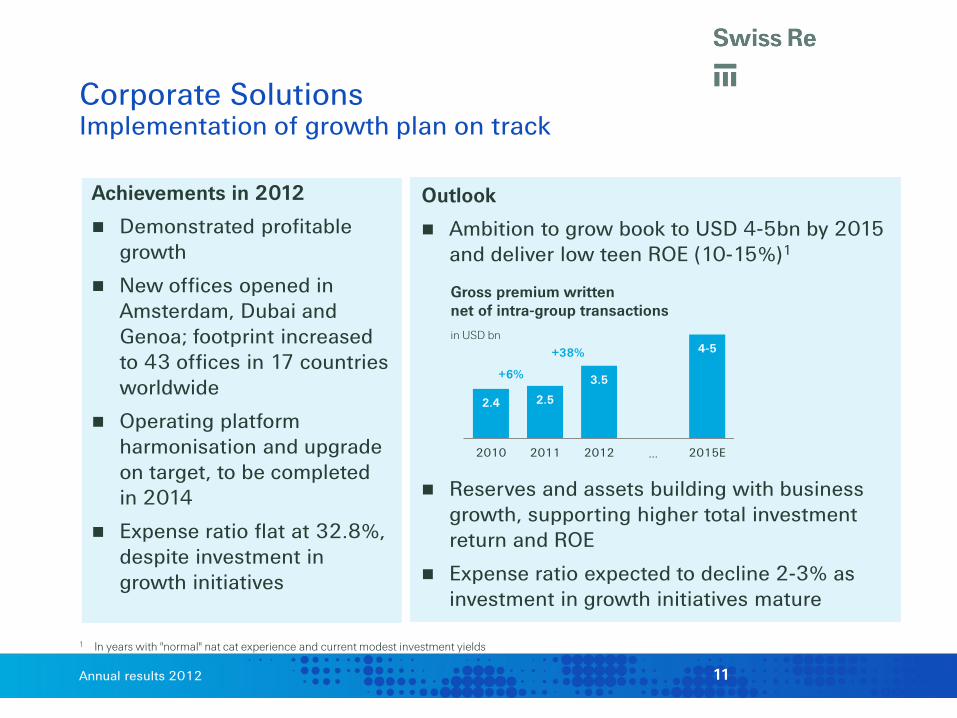

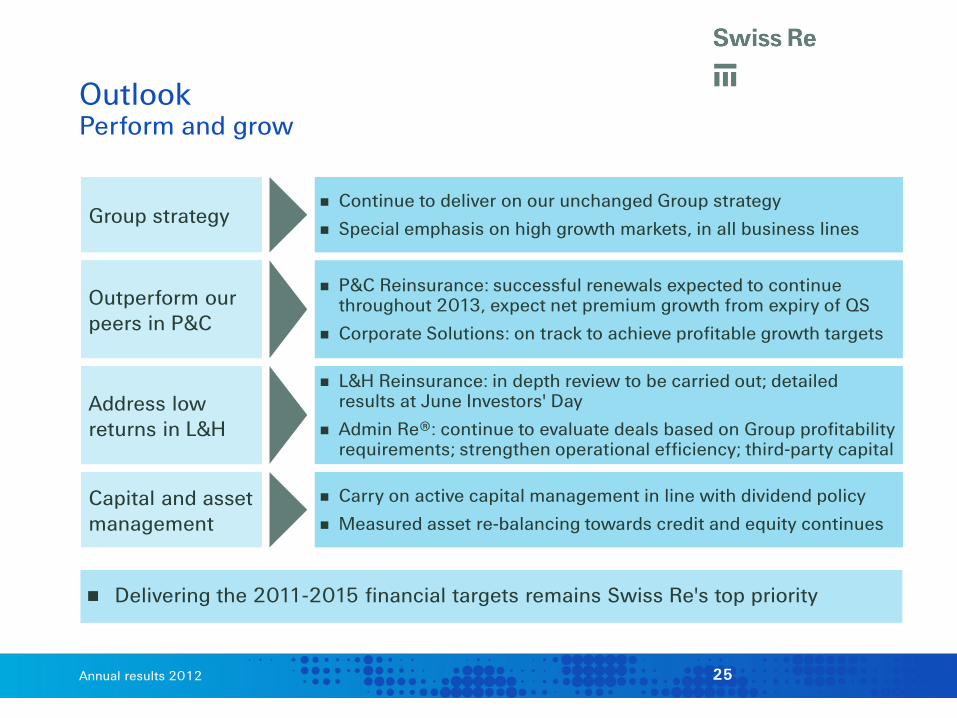

Outlook

Ambition to grow book to USD 4-5bn by 2015 and deliver low teen ROE (10-15%)1

Reserves and assets building with business growth, supporting higher total investment return and ROE

Expense ratio expected to decline 2-3% as investment in growth initiatives mature

Gross premium written net of intra-group transactions in USD bn

2.4 2.5

3.5

4-5

2010 2011 2012 … 2015E

Corporate Solutions Implementation of growth plan on track

1 In years with "normal" nat cat experience and current modest investment yields

+6%

+38%

Achievements in 2012

Demonstrated profitable growth

New offices opened in Amsterdam, Dubai and Genoa; footprint increased to 43 offices in 17 countries worldwide

Operating platform harmonisation and upgrade on target, to be completed in 2014

Expense ratio flat at 32.8%, despite investment in growth initiatives

11

Annual results 2012

Return on investments %

Net income, ROE USD m, %

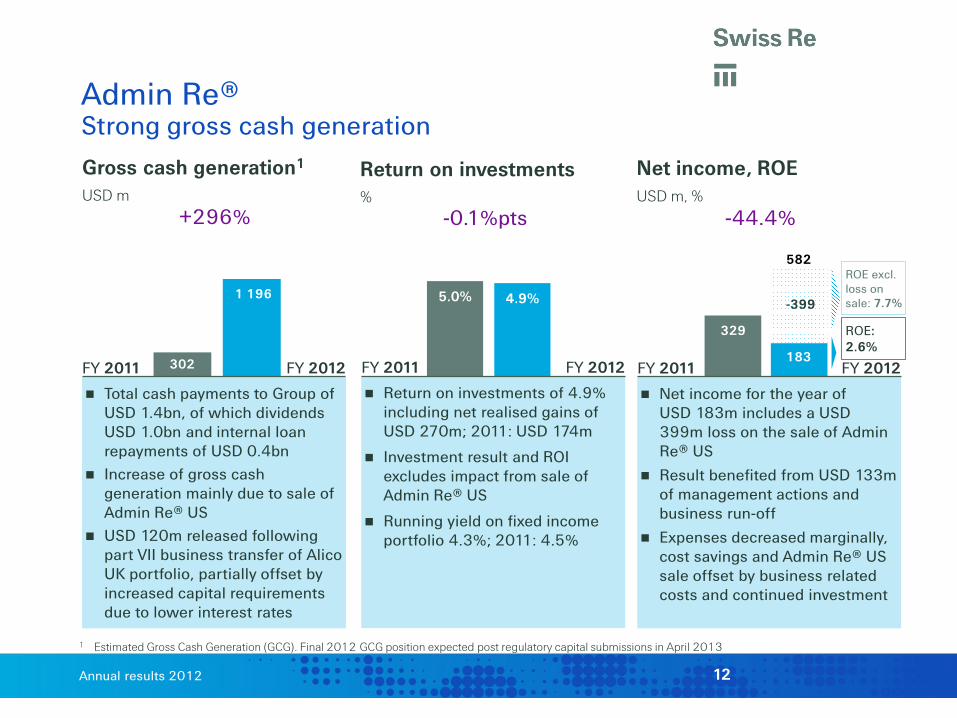

1 Estimated Gross Cash Generation (GCG). Final 2012 GCG position expected post regulatory capital submissions in April 2013

329

183

582

Gross cash generation1

USD m

5.0% 4.9% -399

ROE: 2.6%

ROE excl. loss on sale: 7.7%

Admin Re® Strong gross cash generation

-44.4% -0.1%pts +296%

302

1 196

FY 2011

FY 2012

Total cash payments to Group of USD 1.4bn, of which dividends USD 1.0bn and internal loan repayments of USD 0.4bn

Increase of gross cash generation mainly due to sale of Admin Re® US

USD 120m released following part VII business transfer of Alico UK portfolio, partially offset by increased capital requirements due to lower interest rates

FY 2011

FY 2012

Net income for the year of USD 183m includes a USD 399m loss on the sale of Admin Re® US

Result benefited from USD 133m of management actions and business run-off

Expenses decreased marginally, cost savings and Admin Re® US sale offset by business related costs and continued investment

12

FY 2011

FY 2012

Return on investments of 4.9% including net realised gains of USD 270m; 2011: USD 174m

Investment result and ROI excludes impact from sale of Admin Re® US

Running yield on fixed income portfolio 4.3%; 2011: 4.5%

Annual results 2012

1 050

50 - 140 100 - 150

~2 400 -

~2 500

GCG generated since1 Jan 2012

Revised base case2013-2016E

Operational efficiency& cost management

Active portfoliomanagement

Aspirational2012-2016E

(incl. mgt actions)

Admin Re® gross cash generation Increased forecast 2012-2016

USD m

GCG generated in the year included USD 198m from operational efficiency and cost management, previously within aspirational actions. Aspirational GCG range increased by USD 200m to USD 2.4bn - 2.5bn, due to additional portfolio steering related management actions driven by a change in strategic asset allocation in the UK

Estimated dividends of USD 2.0bn over 2012 - 2016, including USD 0.9bn paid in Q3 2012 following the completion of the sale of Admin Re® US

Future GCG will not be linear and may be negative in particular quarters e.g. due to new deals. Gross cash generation targets will continue to be re-forecast on an annual basis

1 250

Base case 2012 – 2016E

650 Sale of Admin Re® US

As at April 2012 Investors' Day

1 900

998

198

1 196

Base

Mgt. stretch

~2 250

13

Annual results 2012

8.7%

5.4% 4.4% 4.0%

FY 2011

FY 2012

ROI at 4.0%, driven by net investment income from fixed income and realised gains of USD 1 532m; 2011: USD 1 700m

ROI excluding fx of 4.2% in 2012 and 3.7% in 2011

Fixed income running yield of 3.2% for FY 2012 (Q4 2012: 3.1%), compared to 3.6% in FY 2011

123.9 122.8

Group investment result Consistent and strong performance

Total return %

Return on investments %

Avg. invested assets1

USD bn, basis for ROI calculation -0.4%pts -0.9%

1 2011 average assets calculated based on annual average due to new segmental structure

-3.3%pts

FY 2011 FY 2012

Impairments of USD 162m; minimal exposure to peripheral EU government debt USD 19m

Measured re-balancing into corporate bonds: USD 4.1bn and equities USD 0.8bn

Duration largely matched, DV01 USD +0.9m

FY 2011

FY 2012

Total return for FY 2012 impacted by mark-to-market gains from low interest rates, tighter credit spreads and a rise in equity markets

14

Annual results 2012

29 590

-1 134

-363

4 201

332 274

1 102

32 900

34 002

25 000

26 000

27 000

28 000

29 000

30 000

31 000

32 000

33 000

34 000

Shareholders'equity

31 Dec 2011

Net incomeattributable to

commonshareholders

Dividends Other Foreigncurrency

translationadjustments

Net change inunrealised

gains/losses

Commonshareholders'

equity31 Dec 2012

Contingentcapital

instruments

Shareholders'equity

31 Dec 2012

Shareholders' equity 2012 Increase driven by strong net earnings

USD m

1

1 Basis for ROE, BVPS and ENW calculations

Gov bonds -1.4 Corp bonds 0.5 Sec products 0.5 Equities and others 0.7 Tax 0.0 Total 0.3

15

Annual results 2012

31 December 2012, USD millions unless otherwise stated

P&C Reinsurance

L&H Reinsurance Reinsurance

Corporate Solutions Admin Re® Group items

Total Swiss Re

Group

US GAAP shareholders' equity 12 356 8 339 20 695 3 032 6 662 3 660 34 0021

SST Ratio2

SST green zone threshold: 100% 202% 207%

S&P excess capital over AA level3 Internal goal: meet AA requirements

> 3bn > 10bn

Group and Business Unit capitalisation Capital adequacy remains very strong

All Business Units continue to benefit from diversification within their Business Units (in particular, Reinsurance between P&C Re and L&H Re)

All Business Units meet their respective standalone capital and liquidity requirements

1 Total is after consolidation 2 SST 2/2012, as filed with FINMA at the end of October, based on a projection for mid-2012 to mid-2013. Impact of sale of Admin Re® US and July 2012 EUR 500m hybrid issuance not yet apparent in SST 2/2012, but will be in SST 1/2013 3 Note: Before taking into account the proposed 2012 regular and special dividend (distributions to be made in the form of Swiss withholding tax exempt

distributions out of legal reserves from capital contributions) or expiry of 20% P&C quota share

16

Annual results 2012

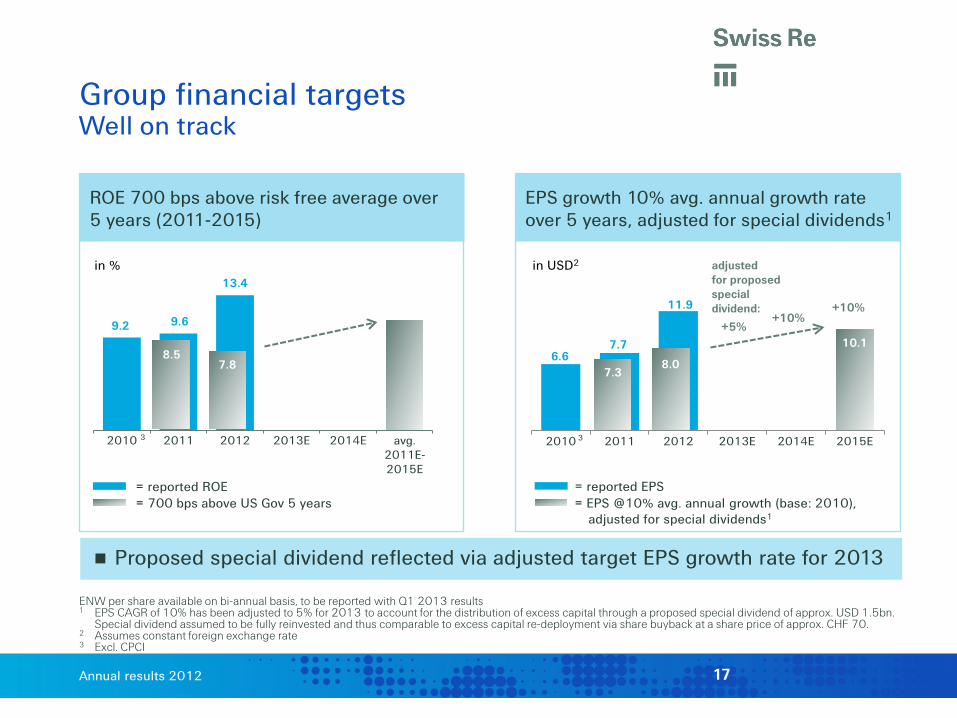

Group financial targets Well on track

ENW per share available on bi-annual basis, to be reported with Q1 2013 results 1 EPS CAGR of 10% has been adjusted to 5% for 2013 to account for the distribution of excess capital through a proposed special dividend of approx. USD 1.5bn.

Special dividend assumed to be fully reinvested and thus comparable to excess capital re-deployment via share buyback at a share price of approx. CHF 70. 2 Assumes constant foreign exchange rate 3 Excl. CPCI

Proposed special dividend reflected via adjusted target EPS growth rate for 2013

= EPS @10% avg. annual growth (base: 2010), adjusted for special dividends1

= reported EPS

in % in USD2

= reported ROE = 700 bps above US Gov 5 years

7.8

9.2 9.6

13.4

2010 2011 2012 2013E 2014E avg.2011E-2015E

3

7.8 8.5 6.6

7.7

11.9

10.1

2010 2011 2012 2013E 2014E 2015E

8.0 7.3

+10% +10%

adjusted for proposed special dividend:

+5%

3

ROE 700 bps above risk free average over 5 years (2011-2015)

EPS growth 10% avg. annual growth rate over 5 years, adjusted for special dividends1

17

Annual results 2012

Business update Michel M. Liès, Group CEO

18

Annual results 2012

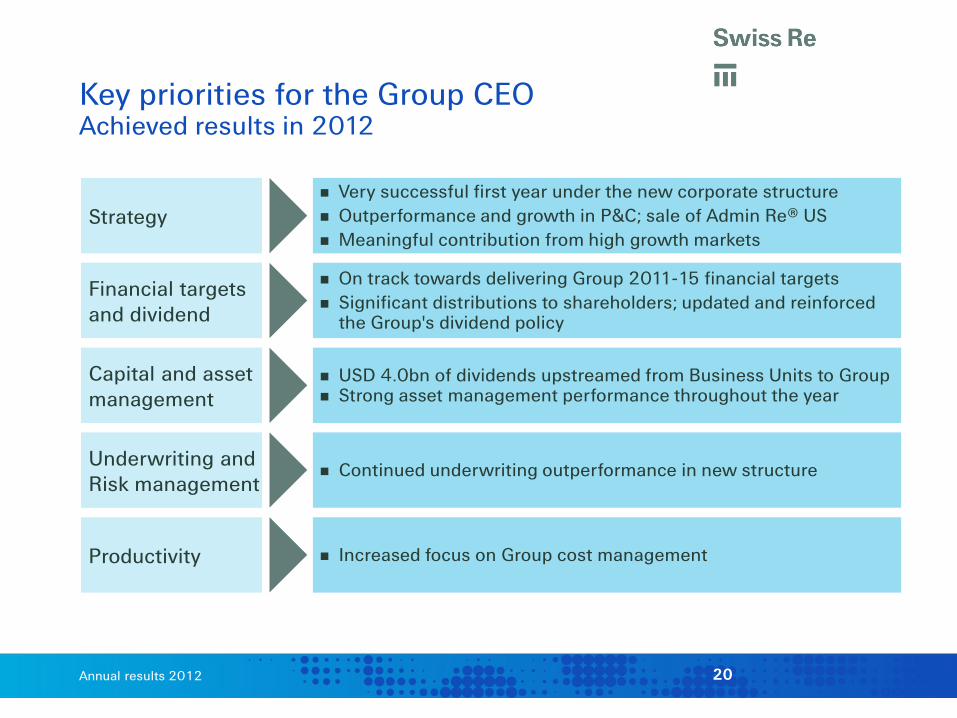

Key priorities for the Group CEO As announced at Investors' Day 17 April 2012

Define the Group strategy and control implementation

Delivery on 2011-15 financial targets is the top priority Adhere to Swiss Re's dividend policy, ensure attractive payouts

(Re)deploy capital based on contribution to our targets Oversee asset allocation from the Group's perspective

Control cost and efficiency in new corporate structure

Underwriting and Risk management

Maintain underwriting as Swiss Re's core strength Set and steer Group risk tolerance (e.g. limits, liquidity)

Capital and asset management

Financial targets and dividend

Strategy

Productivity

19

Annual results 2012

Key priorities for the Group CEO Achieved results in 2012

Very successful first year under the new corporate structure Outperformance and growth in P&C; sale of Admin Re® US Meaningful contribution from high growth markets

On track towards delivering Group 2011-15 financial targets Significant distributions to shareholders; updated and reinforced

the Group's dividend policy

USD 4.0bn of dividends upstreamed from Business Units to Group Strong asset management performance throughout the year

Increased focus on Group cost management

Underwriting and Risk management

Continued underwriting outperformance in new structure

Capital and asset management

Financial targets and dividend

Strategy

Productivity

20

Annual results 2012

100%

111%

Up for renewal1 Jan 2013

Growth Estimatedoutcome

P&C Re: January 2013 treaty renewals Successful renewals leading to profitable growth

Gross premium volume1

USD 9.3bn

USD 8.4bn

January renewals: 11% top line growth driven by structured solutions and solvency relief transactions in Europe and the Americas

11%

1 Note: Volume is shown on a gross basis, hence the impact from the P&C quota share is not visible 2 USD 2.9bn multi-year transactions written in January 2012 are not up for renewal in January 2013

USD 0.9bn

High growth markets (HGM)

– Lower solvency-related cessions in China led to reduction in premium volumes

– Outside of China, HGM premium grew to approx. USD 0.7bn

– Strongest growth rates achieved in emerging Asia (67%) ex China, Africa (48%) and Latin America (35%)

2

21

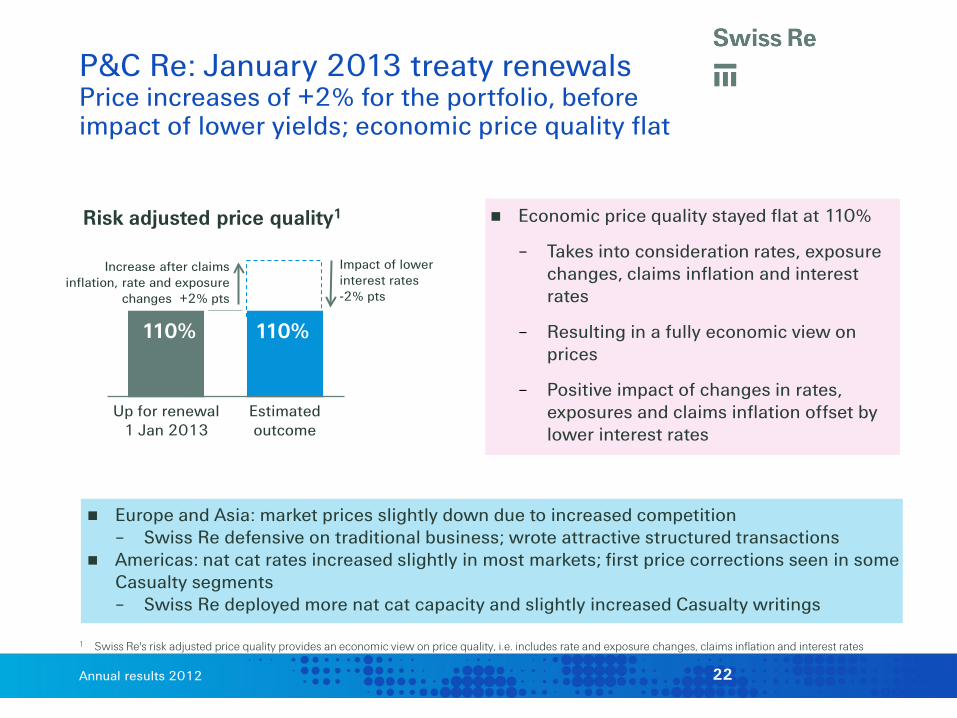

Annual results 2012

110% 110%

Up for renewal1 Jan 2013

Estimatedoutcome

P&C Re: January 2013 treaty renewals Price increases of +2% for the portfolio, before impact of lower yields; economic price quality flat

Europe and Asia: market prices slightly down due to increased competition – Swiss Re defensive on traditional business; wrote attractive structured transactions

Americas: nat cat rates increased slightly in most markets; first price corrections seen in some Casualty segments – Swiss Re deployed more nat cat capacity and slightly increased Casualty writings

Risk adjusted price quality1

1 Swiss Re's risk adjusted price quality provides an economic view on price quality, i.e. includes rate and exposure changes, claims inflation and interest rates

Economic price quality stayed flat at 110%

– Takes into consideration rates, exposure changes, claims inflation and interest rates

– Resulting in a fully economic view on prices

– Positive impact of changes in rates, exposures and claims inflation offset by lower interest rates

Impact of lower interest rates -2% pts

Increase after claims inflation, rate and exposure

changes +2% pts

22

Annual results 2012

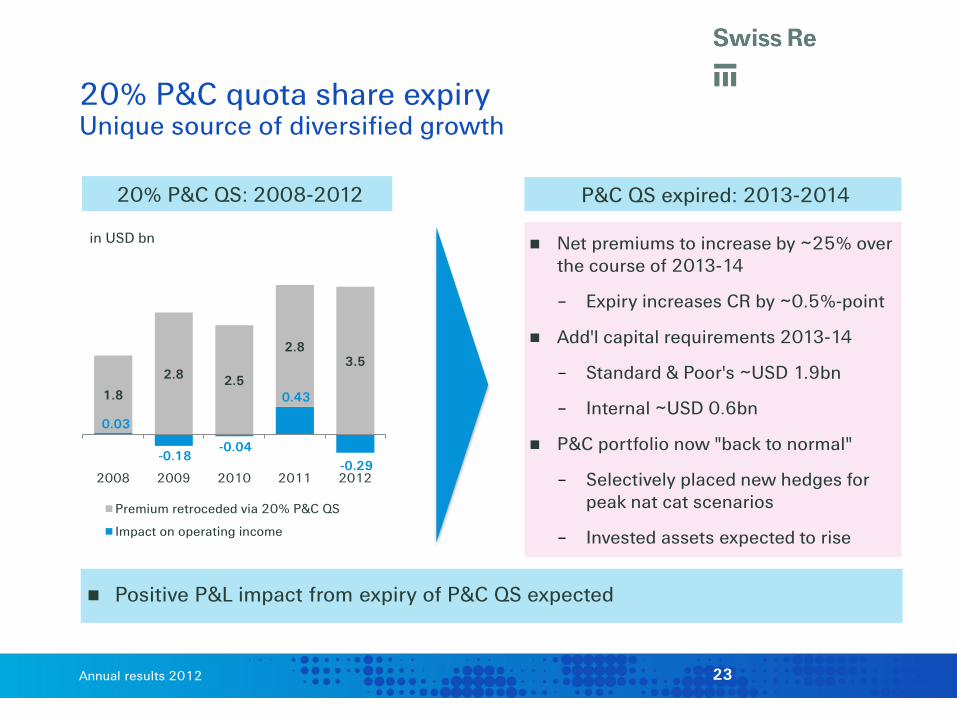

20% P&C quota share expiry Unique source of diversified growth

in USD bn

Positive P&L impact from expiry of P&C QS expected

Net premiums to increase by ~25% over the course of 2013-14

– Expiry increases CR by ~0.5%-point

Add'l capital requirements 2013-14

– Standard & Poor's ~USD 1.9bn

– Internal ~USD 0.6bn

P&C portfolio now "back to normal"

– Selectively placed new hedges for peak nat cat scenarios

– Invested assets expected to rise

20% P&C QS: 2008-2012 P&C QS expired: 2013-2014

0.03

-0.18 -0.04

0.43

-0.29

1.8

2.8 2.5

2.8 3.5

2008 2009 2010 2011 2012

Premium retroceded via 20% P&C QS

Impact on operating income

23

Annual results 2012

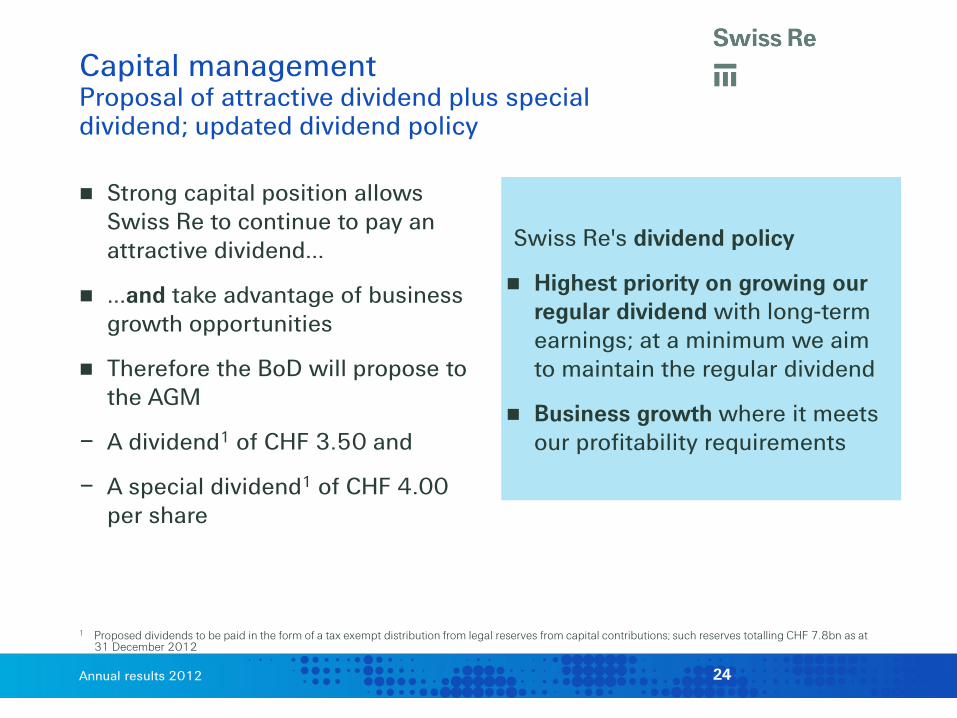

Strong capital position allows Swiss Re to continue to pay an attractive dividend…

…and take advantage of business growth opportunities

Therefore the BoD will propose to the AGM

– A dividend1 of CHF 3.50 and

– A special dividend1 of CHF 4.00 per share

Swiss Re's dividend policy

Highest priority on growing our regular dividend with long-term earnings; at a minimum we aim to maintain the regular dividend

Business growth where it meets our profitability requirements

Capital management Proposal of attractive dividend plus special dividend; updated dividend policy

1 Proposed dividends to be paid in the form of a tax exempt distribution from legal reserves from capital contributions; such reserves totalling CHF 7.8bn as at 31 December 2012

24

Annual results 2012

Outlook Perform and grow

Address low returns in L&H

L&H Reinsurance: in depth review to be carried out; detailed results at June Investors' Day

Admin Re®: continue to evaluate deals based on Group profitability requirements; strengthen operational efficiency; third-party capital

P&C Reinsurance: successful renewals expected to continue throughout 2013, expect net premium growth from expiry of QS

Corporate Solutions: on track to achieve profitable growth targets

Outperform our peers in P&C

Continue to deliver on our unchanged Group strategy

Special emphasis on high growth markets, in all business lines Group strategy

Delivering the 2011-2015 financial targets remains Swiss Re's top priority

Carry on active capital management in line with dividend policy

Measured asset re-balancing towards credit and equity continues Capital and asset management

25

Annual results 2012

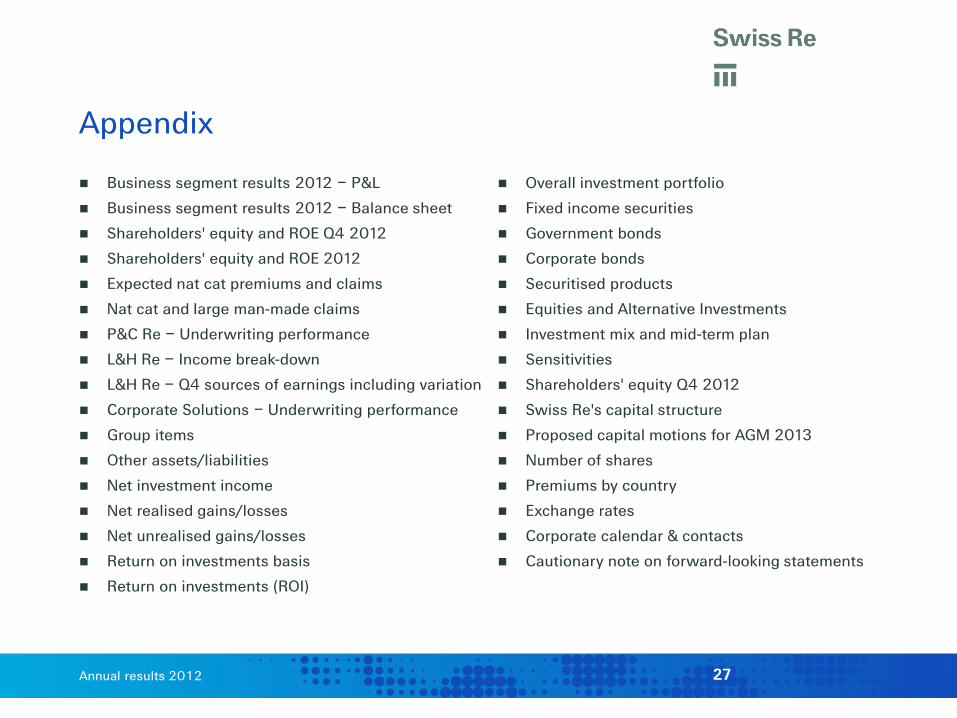

Appendix

26

Annual results 2012

Appendix

Business segment results 2012 – P&L

Business segment results 2012 – Balance sheet

Shareholders' equity and ROE Q4 2012

Shareholders' equity and ROE 2012

Expected nat cat premiums and claims

Nat cat and large man-made claims

P&C Re – Underwriting performance

L&H Re – Income break-down

L&H Re – Q4 sources of earnings including variation

Corporate Solutions – Underwriting performance

Group items

Other assets/liabilities

Net investment income

Net realised gains/losses

Net unrealised gains/losses

Return on investments basis

Return on investments (ROI)

Overall investment portfolio

Fixed income securities

Government bonds

Corporate bonds

Securitised products

Equities and Alternative Investments

Investment mix and mid-term plan

Sensitivities

Shareholders' equity Q4 2012

Swiss Re's capital structure

Proposed capital motions for AGM 2013

Number of shares

Premiums by country

Exchange rates

Corporate calendar & contacts

Cautionary note on forward-looking statements

27

Annual results 2012

USD millions Re-

insurance P&C Re L&H Re Corporate Solutions

Admin Re®

Group items

Consoli-dation

Total FY 2012

Total FY 2011

Total Q4 2012

Revenues Premiums earned 21 379 12 329 9 050 2 284 992 6 - 24 661 21 300 6 390 Fee income from policyholders 72 - 72 - 713 - - 785 876 142 Net investment income/loss – non participating 2 816

1 451

1 365

109

1 548

18 -18

4 473 4 626 1 010

Net realised investment gains/losses – non participating 821

259

562

142

-89

73 -

947 1 634 54

Net investment result – unit-linked and with-profit 222

-

222

-

2 348

- -

2 570 -403 618

Other revenues 96 95 1 1 3 385 -297 188 50 4 Total revenues 25 406 14 134 11 272 2 536 5 515 482 -315 33 624 28 083 8 218 Expenses Claims and claim adjustment expenses -6 306 -6 306 - -1 448 - -14 5 -7 763 -8 810 -2 263 Life and health benefits -6 787 - -6 787 - -2 086 - -5 -8 878 -8 414 -2 221 Return credited to policyholders -271 - -271 - -2 688 - - -2 959 -61 -776 Acquisition costs -4 103 -2 316 -1 787 -300 -142 -3 - -4 548 -4 021 -1 083 Other expenses -2 158 -1 325 -833 -449 -457 -403 250 -3 217 -3 051 -867 Interest expenses -697 -111 -586 - -53 -51 65 -736 -851 -182 Total expenses -20 322 -10 058 -10 264 -2 197 -5 426 -471 -315 -28 101 -25 208 -7 392 Income before income tax expenses 5 084 4 076 1 008 339 89 11 - 5 523 2 875 826 Income tax expense/benefit -1 165 -934 -231 -143 101 82 - -1 125 -77 -13 Net income/loss before attribution of non-controlling interests 3 919

3 142

777

196

190

93 -

4 398 2 798 813

Income attributable to non-controlling interests -134

-134

-

-

-7

- -

-141 -172 -1

Net income/loss after attribution of non-controlling interests 3 785

3 008

777

196

183

93 -

4 257 2 626 812

Interest on contingent capital instruments -56 -18 -38 - - - - -56 0 -17 Net income/loss attributable to common shareholders 3 729

2 990

739

196

183

93 -

4 201 2 626 795

Business segment results 2012 Profit and loss statement

28

Annual results 2012

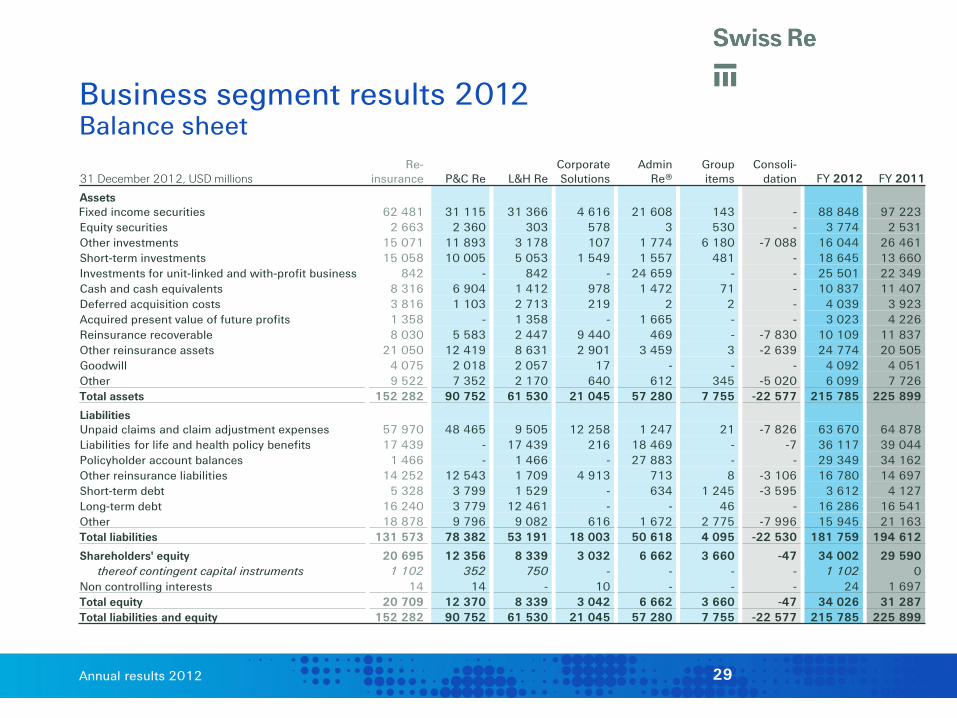

31 December 2012, USD millions Re-

insurance P&C Re L&H Re Corporate Solutions

Admin Re®

Group items

Consoli-dation

FY 2012

FY 2011

Assets

Fixed income securities 62 481 31 115 31 366 4 616 21 608 143 - 88 848 97 223 Equity securities 2 663 2 360 303 578 3 530 - 3 774 2 531 Other investments 15 071 11 893 3 178 107 1 774 6 180 -7 088 16 044 26 461 Short-term investments 15 058 10 005 5 053 1 549 1 557 481 - 18 645 13 660 Investments for unit-linked and with-profit business 842 - 842 - 24 659 - - 25 501 22 349 Cash and cash equivalents 8 316 6 904 1 412 978 1 472 71 - 10 837 11 407 Deferred acquisition costs 3 816 1 103 2 713 219 2 2 - 4 039 3 923 Acquired present value of future profits 1 358 - 1 358 - 1 665 - - 3 023 4 226 Reinsurance recoverable 8 030 5 583 2 447 9 440 469 - -7 830 10 109 11 837 Other reinsurance assets 21 050 12 419 8 631 2 901 3 459 3 -2 639 24 774 20 505 Goodwill 4 075 2 018 2 057 17 - - - 4 092 4 051 Other 9 522 7 352 2 170 640 612 345 -5 020 6 099 7 726 Total assets 152 282 90 752 61 530 21 045 57 280 7 755 -22 577 215 785 225 899

Liabilities Unpaid claims and claim adjustment expenses

64 878 57 970 48 465 9 505 12 258 1 247 21 -7 826 63 670

Liabilities for life and health policy benefits 17 439 - 17 439 216 18 469 - -7 36 117 39 044 Policyholder account balances 1 466 - 1 466 - 27 883 - - 29 349 34 162 Other reinsurance liabilities 14 252 12 543 1 709 4 913 713 8 -3 106 16 780 14 697 Short-term debt 5 328 3 799 1 529 - 634 1 245 -3 595 3 612 4 127 Long-term debt 16 240 3 779 12 461 - - 46 - 16 286 16 541 Other 18 878 9 796 9 082 616 1 672 2 775 -7 996 15 945 21 163 Total liabilities 131 573 78 382 53 191 18 003 50 618 4 095 -22 530 181 759 194 612

Shareholders' equity 20 695 12 356 8 339 3 032 6 662 3 660 -47 34 002 29 590 thereof contingent capital instruments 1 102 352 750 - - - - 1 102 0

Non controlling interests 14 14 - 10 - - - 24 1 697 Total equity 20 709 12 370 8 339 3 042 6 662 3 660 -47 34 026 31 287 Total liabilities and equity 152 282 90 752 61 530 21 045 57 280 7 755 -22 577 215 785 225 899

Business segment results 2012 Balance sheet

29

Annual results 2012

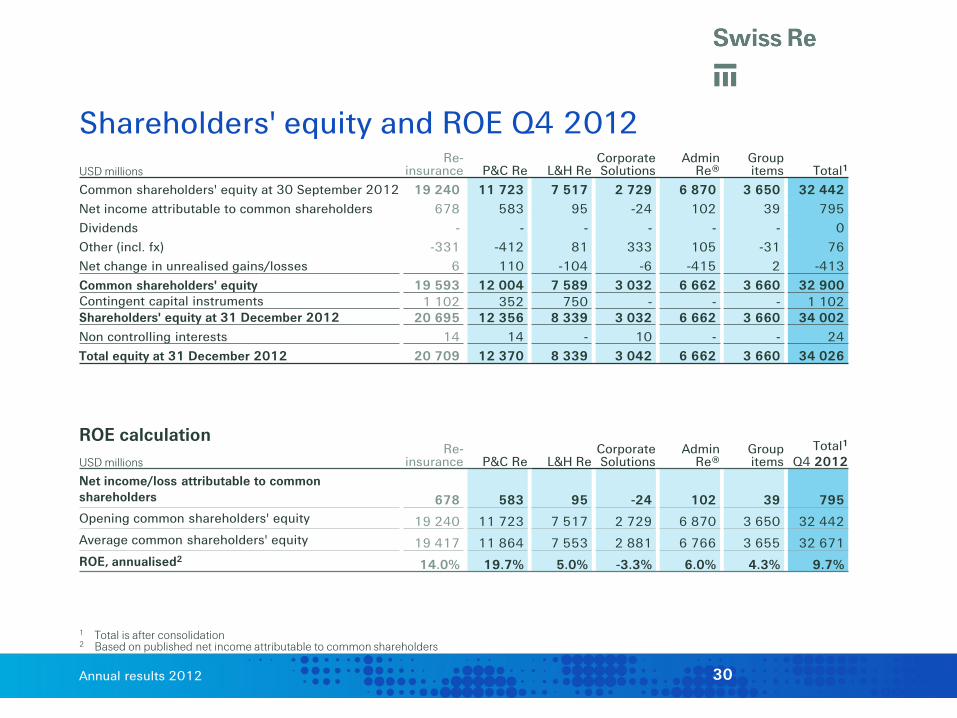

Shareholders' equity and ROE Q4 2012

ROE calculation USD millions

Re-

insurance

P&C Re L&H Re Corporate Solutions

Admin

Re® Group items

Total1 Q4 2012

Net income/loss attributable to common shareholders 678 583 95 -24 102 39 795 Opening common shareholders' equity 19 240 11 723 7 517 2 729 6 870 3 650 32 442 Average common shareholders' equity 19 417 11 864 7 553 2 881 6 766 3 655 32 671 ROE, annualised2 14.0% 19.7% 5.0% -3.3% 6.0% 4.3% 9.7%

1 Total is after consolidation 2 Based on published net income attributable to common shareholders

USD millions Re-

insurance P&C Re L&H Re Corporate Solutions

Admin Re®

Group items

Total1

Common shareholders' equity at 30 September 2012 19 240 11 723 7 517 2 729 6 870 3 650 32 442 Net income attributable to common shareholders 678 583 95 -24 102 39 795 Dividends - - - - - - 0 Other (incl. fx) -331 -412 81 333 105 -31 76 Net change in unrealised gains/losses 6 110 -104 -6 -415 2 -413 Common shareholders' equity 19 593 12 004 7 589 3 032 6 662 3 660 32 900 Contingent capital instruments 1 102 352 750 - - - 1 102 Shareholders' equity at 31 December 2012 20 695 12 356 8 339 3 032 6 662 3 660 34 002 Non controlling interests 14 14 - 10 - - 24 Total equity at 31 December 2012 20 709 12 370 8 339 3 042 6 662 3 660 34 026

30

Annual results 2012

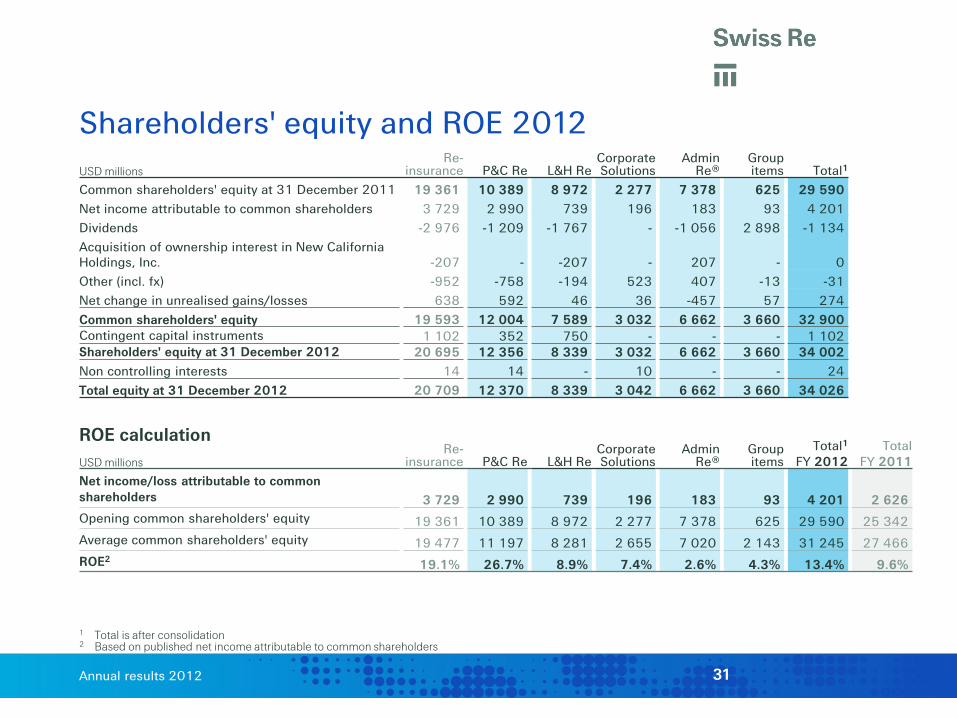

Shareholders' equity and ROE 2012

ROE calculation USD millions

Re-

insurance

P&C Re L&H Re Corporate Solutions

Admin

Re® Group items

Total1 FY 2012

Total FY 2011

Net income/loss attributable to common shareholders 3 729 2 990 739 196 183 93 4 201 2 626 Opening common shareholders' equity 19 361 10 389 8 972 2 277 7 378 625 29 590 25 342 Average common shareholders' equity 19 477 11 197 8 281 2 655 7 020 2 143 31 245 27 466 ROE2 19.1% 26.7% 8.9% 7.4% 2.6% 4.3% 13.4% 9.6%

1 Total is after consolidation 2 Based on published net income attributable to common shareholders

USD millions Re-

insurance P&C Re L&H Re Corporate Solutions

Admin Re®

Group items

Total1

Common shareholders' equity at 31 December 2011 19 361 10 389 8 972 2 277 7 378 625 29 590 Net income attributable to common shareholders 3 729 2 990 739 196 183 93 4 201 Dividends -2 976 -1 209 -1 767 - -1 056 2 898 -1 134 Acquisition of ownership interest in New California Holdings, Inc. -207 - -207 - 207 - 0 Other (incl. fx) -952 -758 -194 523 407 -13 -31 Net change in unrealised gains/losses 638 592 46 36 -457 57 274 Common shareholders' equity 19 593 12 004 7 589 3 032 6 662 3 660 32 900 Contingent capital instruments 1 102 352 750 - - - 1 102 Shareholders' equity at 31 December 2012 20 695 12 356 8 339 3 032 6 662 3 660 34 002 Non controlling interests 14 14 - 10 - - 24 Total equity at 31 December 2012 20 709 12 370 8 339 3 042 6 662 3 660 34 026

31

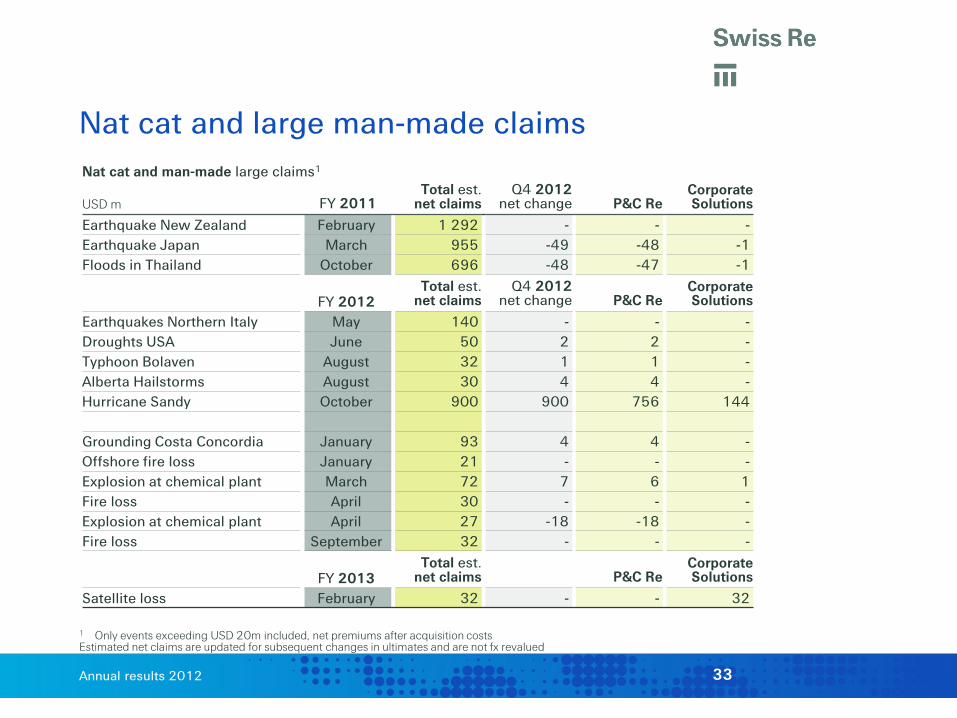

Annual results 2012

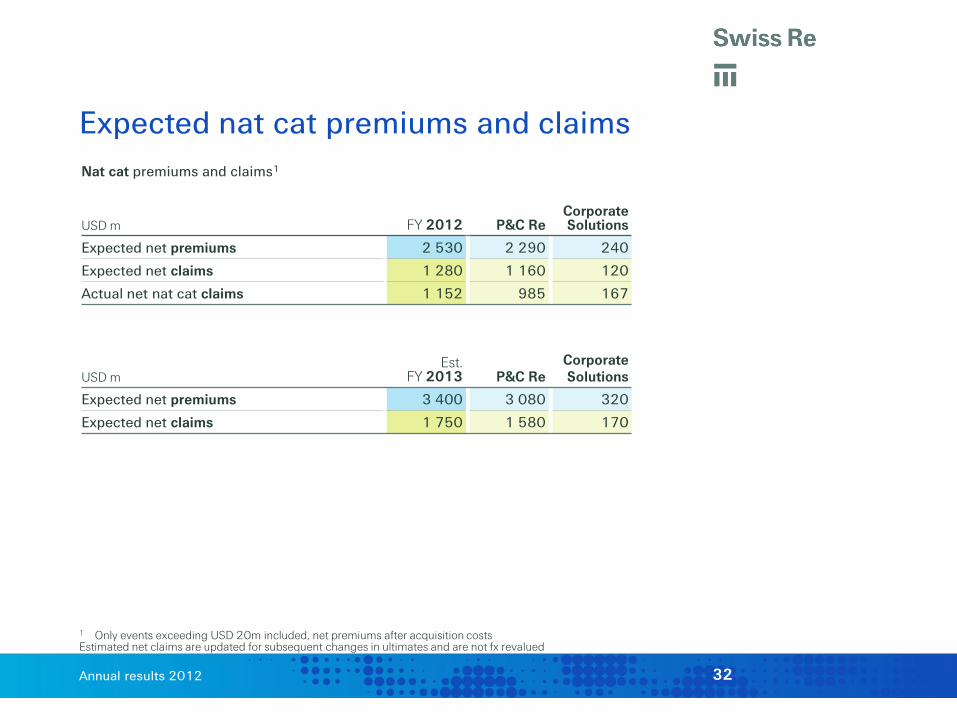

1 Only events exceeding USD 20m included, net premiums after acquisition costs Estimated net claims are updated for subsequent changes in ultimates and are not fx revalued

Expected nat cat premiums and claims Nat cat premiums and claims1

P&C Re Corporate Solutions USD m FY 2012

Expected net premiums 2 530

2 290 240

Expected net claims 1 280 1 160 120

Actual net nat cat claims 1 152 985 167

USD m Est.

FY 2013 P&C Re Corporate Solutions

Expected net premiums 3 400 3 080 320

Expected net claims 1 750 1 580 170

32

Annual results 2012

1 Only events exceeding USD 20m included, net premiums after acquisition costs Estimated net claims are updated for subsequent changes in ultimates and are not fx revalued

Nat cat and large man-made claims Nat cat and man-made large claims1

USD m FY 2011 Total est.

net claims Q4 2012

net change P&C Re Corporate Solutions

Earthquake New Zealand February 1 292 - - - Earthquake Japan March 955 -49 -48 -1 Floods in Thailand October 696 -48 -47 -1

FY 2012

Total est. net claims

Q4 2012 net change P&C Re

Corporate Solutions

Earthquakes Northern Italy May 140 - - - Droughts USA June 50 2 2 - Typhoon Bolaven August 32 1 1 - Alberta Hailstorms August 30 4 4 - Hurricane Sandy October 900 900 756 144

Grounding Costa Concordia January 93 4 4 - Offshore fire loss January 21 - - - Explosion at chemical plant March 72 7 6 1 Fire loss April 30 - - - Explosion at chemical plant April 27 -18 -18 - Fire loss September 32 - - -

FY 2013

Total est. net claims P&C Re

Corporate Solutions

Satellite loss February 32 - - 32

33

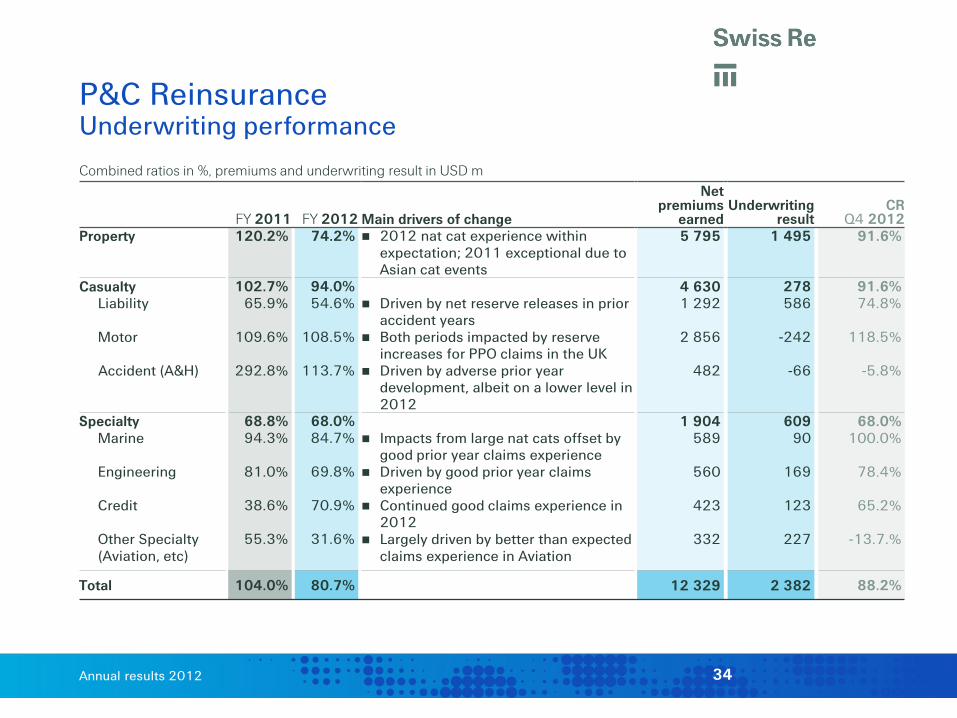

Annual results 2012

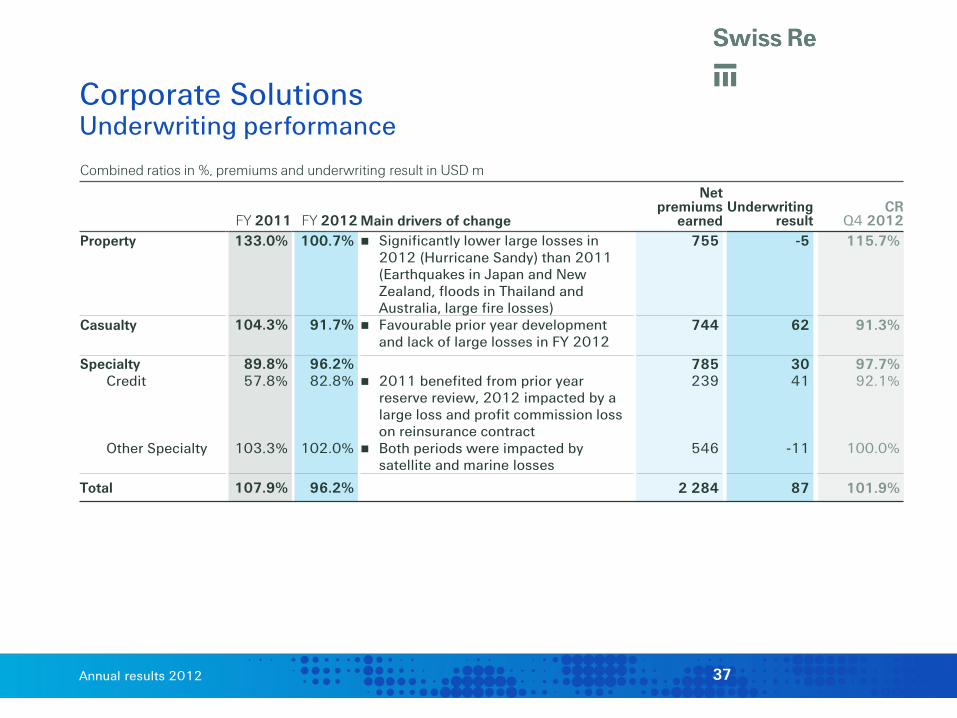

Combined ratios in %, premiums and underwriting result in USD m

FY 2011 FY 2012 Main drivers of change

Net premiums

earned Underwriting

result CR

Q4 2012 Property 120.2% 74.2% 2012 nat cat experience within

expectation; 2011 exceptional due to Asian cat events

5 795 1 495 91.6%

Casualty Liability Motor Accident (A&H)

102.7% 65.9%

109.6%

292.8%

94.0% 54.6%

108.5%

113.7%

Driven by net reserve releases in prior

accident years Both periods impacted by reserve

increases for PPO claims in the UK Driven by adverse prior year

development, albeit on a lower level in 2012

4 630 1 292

2 856

482

278 586

-242

-66

91.6% 74.8%

118.5%

-5.8%

Specialty Marine

Engineering Credit Other Specialty (Aviation, etc)

68.8% 94.3%

81.0%

38.6%

55.3%

68.0% 84.7%

69.8%

70.9%

31.6%

Impacts from large nat cats offset by

good prior year claims experience Driven by good prior year claims

experience Continued good claims experience in

2012 Largely driven by better than expected

claims experience in Aviation

1 904 589

560

423

332

609 90

169

123

227

68.0% 100.0%

78.4%

65.2%

-13.7.%

Total 104.0% 80.7% 12 329 2 382 88.2%

P&C Reinsurance Underwriting performance

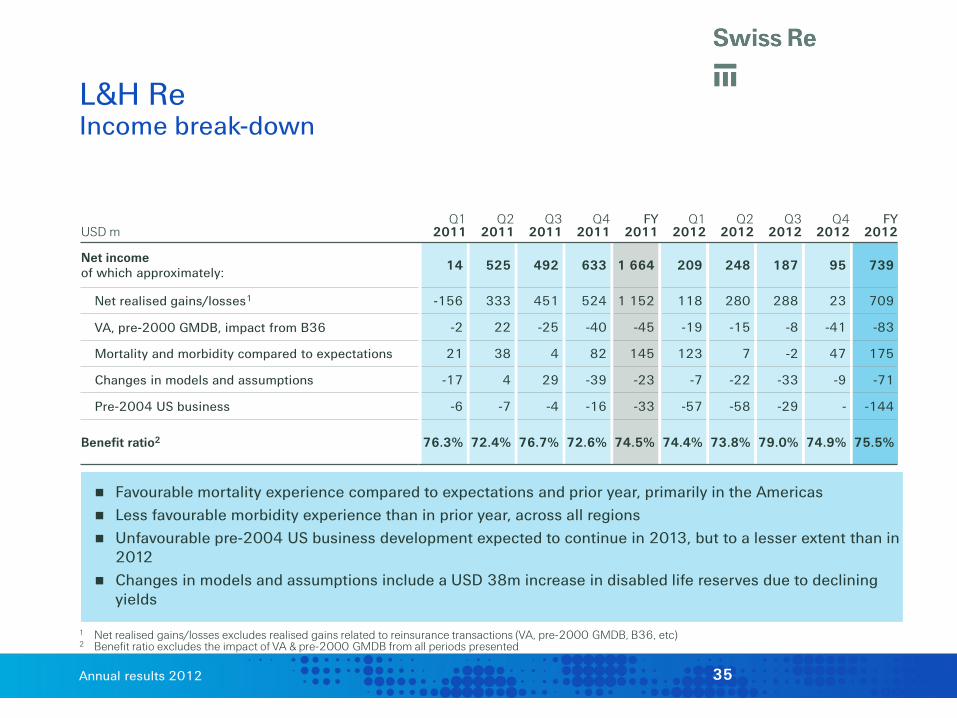

34

Annual results 2012

L&H Re Income break-down

1 Net realised gains/losses excludes realised gains related to reinsurance transactions (VA, pre-2000 GMDB, B36, etc) 2 Benefit ratio excludes the impact of VA & pre-2000 GMDB from all periods presented

Favourable mortality experience compared to expectations and prior year, primarily in the Americas Less favourable morbidity experience than in prior year, across all regions Unfavourable pre-2004 US business development expected to continue in 2013, but to a lesser extent than in

2012 Changes in models and assumptions include a USD 38m increase in disabled life reserves due to declining

yields

USD m Q1

2011 Q2

2011 Q3

2011 Q4

2011 FY

2011 Q1

2012 Q2

2012 Q3

2012 Q4

2012 FY

2012

Net income of which approximately: 14 525 492 633 1 664 209 248 187 95 739

Net realised gains/losses1 -156 333 451 524 1 152 118 280 288 23 709

VA, pre-2000 GMDB, impact from B36 -2 22 -25 -40 -45 -19 -15 -8 -41 -83

Mortality and morbidity compared to expectations 21 38 4 82 145 123 7 -2 47 175

Changes in models and assumptions -17 4 29 -39 -23 -7 -22 -33 -9 -71

Pre-2004 US business -6 -7 -4 -16 -33 -57 -58 -29 - -144

Benefit ratio2 76.3% 72.4% 76.7% 72.6% 74.5% 74.4% 73.8% 79.0% 74.9% 75.5%

35

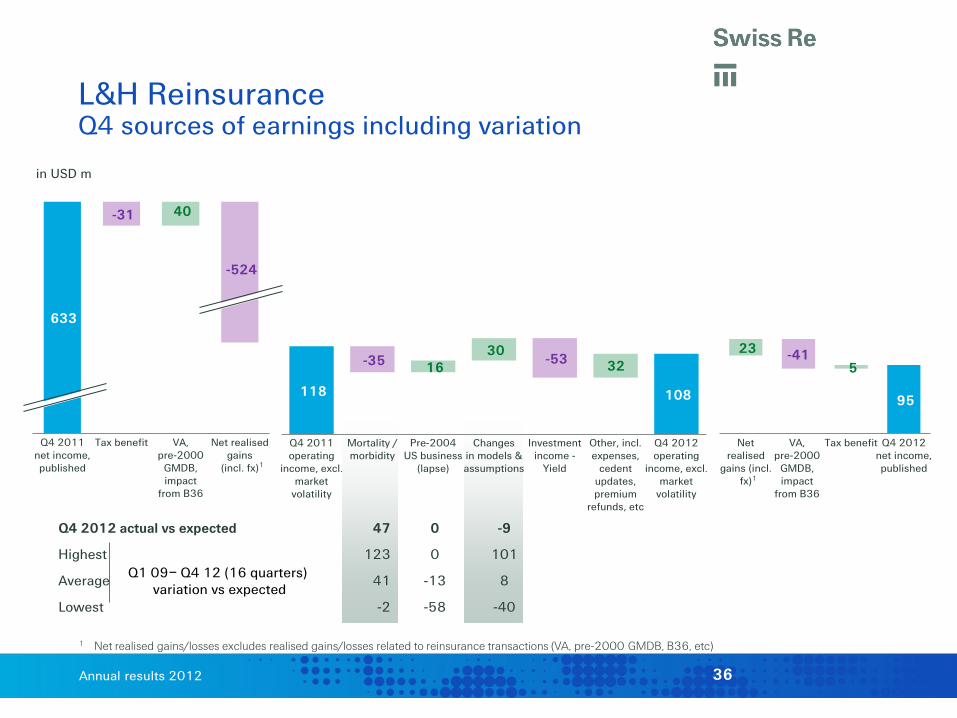

Annual results 2012

Q4 2012 actual vs expected 47 0 -9

Highest 123 0 101

Average 41 -13 8

Lowest -2 -58 -40

L&H Reinsurance Q4 sources of earnings including variation

1 Net realised gains/losses excludes realised gains/losses related to reinsurance transactions (VA, pre-2000 GMDB, B36, etc)

633

-31

-524

40

Q4 2011net income,published

Tax benefit VA,pre-2000

GMDB,impact

from B36

Net realisedgains

(incl. fx)

36

-41 23 5

95

Netrealised

gains (incl.fx)

VA,pre-2000

GMDB,impact

from B36

Tax benefit Q4 2012net income,published

in USD m

-35 -53 16

30 32

118 108

Q4 2011operating

income, excl.market

volatility

Mortality /morbidity

Pre-2004US business

(lapse)

Changesin models &assumptions

Investmentincome -

Yield

Other, incl.expenses,

cedentupdates,premium

refunds, etc

Q4 2012operating

income, excl.market

volatility

1

Q1 09– Q4 12 (16 quarters) variation vs expected

1

Annual results 2012

Corporate Solutions Underwriting performance

Combined ratios in %, premiums and underwriting result in USD m

FY 2011 FY 2012 Main drivers of change

Net premiums

earned Underwriting

result CR

Q4 2012 Property 133.0% 100.7% Significantly lower large losses in

2012 (Hurricane Sandy) than 2011 (Earthquakes in Japan and New Zealand, floods in Thailand and Australia, large fire losses)

755 -5 115.7%

Casualty 104.3% 91.7% Favourable prior year development and lack of large losses in FY 2012

744 62 91.3%

Specialty Credit Other Specialty

89.8% 57.8%

103.3%

96.2% 82.8%

102.0%

2011 benefited from prior year

reserve review, 2012 impacted by a large loss and profit commission loss on reinsurance contract

Both periods were impacted by satellite and marine losses

785 239

546

30 41

-11

97.7% 92.1%

100.0%

Total 107.9% 96.2% 2 284 87 101.9%

37

Annual results 2012

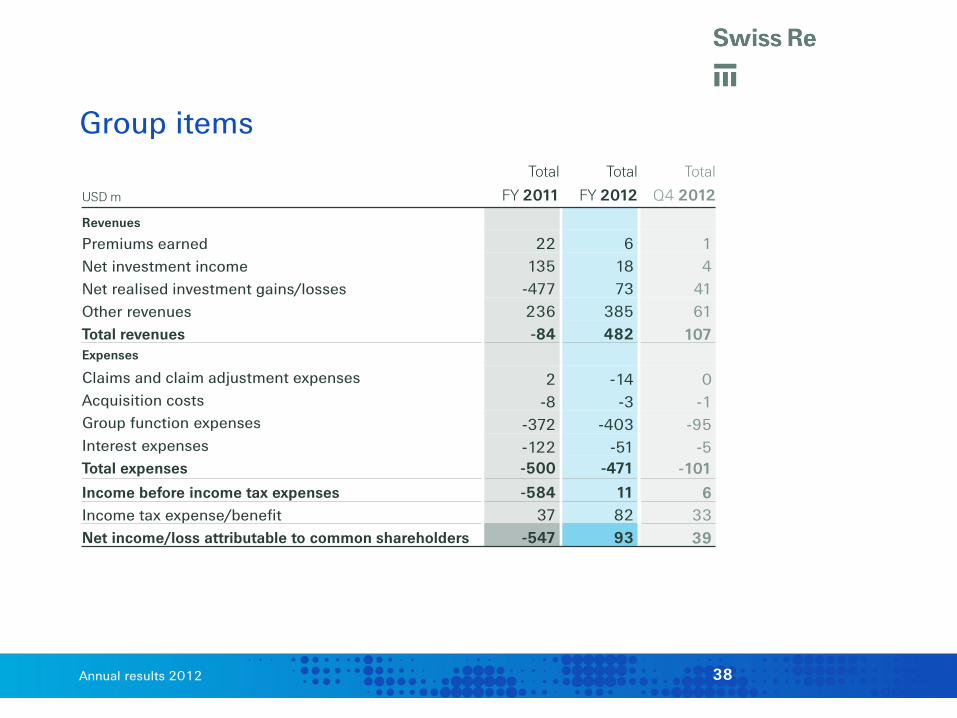

Group items

USD m

Total

FY 2011

Total

FY 2012

Total

Q4 2012

Revenues

Premiums earned 22 6 1 Net investment income 135 18 4 Net realised investment gains/losses -477 73 41 Other revenues 236 385 61 Total revenues -84 482 107 Expenses

Claims and claim adjustment expenses 2 -14 0 Acquisition costs -8 -3 -1 Group function expenses -372 -403 -95 Interest expenses -122 -51 -5 Total expenses -500 -471 -101

Income before income tax expenses -584 11 6 Income tax expense/benefit 37 82 33 Net income/loss attributable to common shareholders -547 93 39

38

Annual results 2012

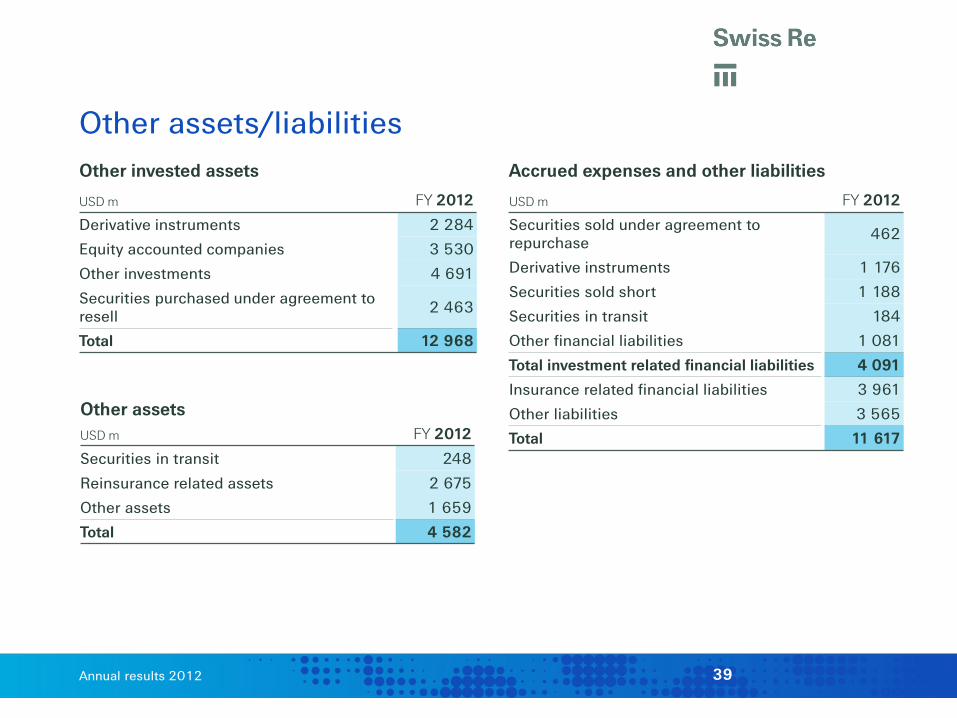

Other assets/liabilities Other invested assets

USD m FY 2012

Derivative instruments 2 284

Equity accounted companies 3 530

Other investments 4 691

Securities purchased under agreement to resell 2 463

Total 12 968

Accrued expenses and other liabilities

USD m FY 2012

Securities sold under agreement to repurchase 462

Derivative instruments 1 176

Securities sold short 1 188

Securities in transit 184

Other financial liabilities 1 081

Total investment related financial liabilities 4 091

Insurance related financial liabilities 3 961

Other liabilities 3 565

Total 11 617

Other assets USD m FY 2012

Securities in transit 248

Reinsurance related assets 2 675

Other assets 1 659

Total 4 582

39

Annual results 2012

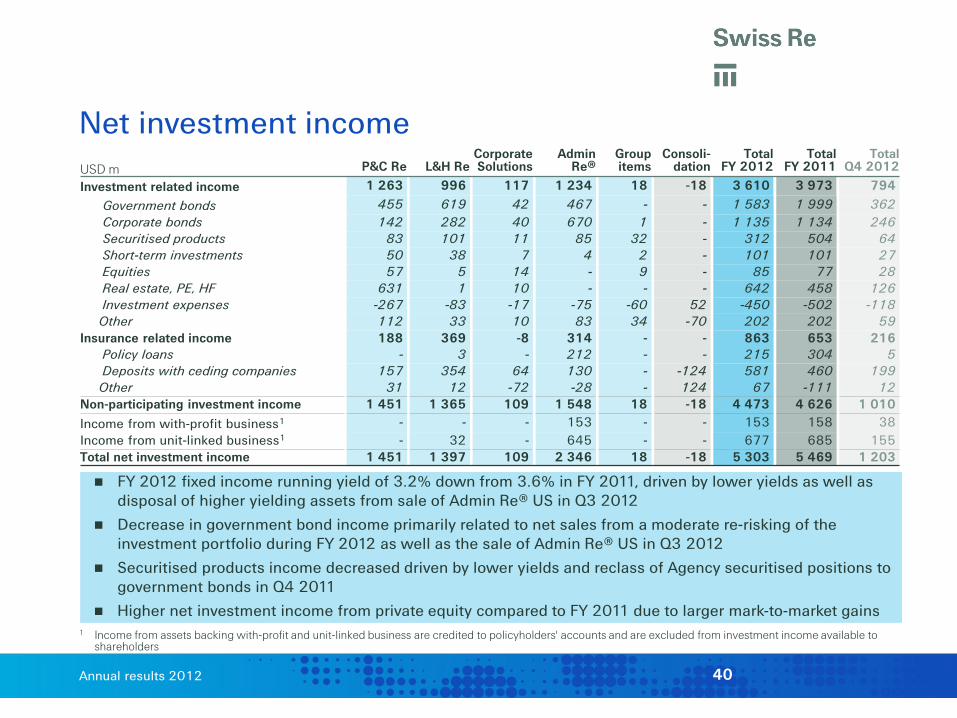

Net investment income

FY 2012 fixed income running yield of 3.2% down from 3.6% in FY 2011, driven by lower yields as well as disposal of higher yielding assets from sale of Admin Re® US in Q3 2012

Decrease in government bond income primarily related to net sales from a moderate re-risking of the investment portfolio during FY 2012 as well as the sale of Admin Re® US in Q3 2012

Securitised products income decreased driven by lower yields and reclass of Agency securitised positions to government bonds in Q4 2011

Higher net investment income from private equity compared to FY 2011 due to larger mark-to-market gains 1 Income from assets backing with-profit and unit-linked business are credited to policyholders' accounts and are excluded from investment income available to

shareholders

USD m P&C Re L&H Re Corporate Solutions

Admin Re®

Group items

Consoli-dation

Total FY 2012

Total FY 2011

Total Q4 2012

Investment related income 1 263 996 117 1 234 18 -18 3 610 3 973 794

Government bonds 455 619 42 467 - - 1 583 1 999 362 Corporate bonds 142 282 40 670 1 - 1 135 1 134 246 Securitised products 83 101 11 85 32 - 312 504 64

Short-term investments 50 38 7 4 2 - 101 101 27 Equities 57 5 14 - 9 - 85 77 28 Real estate, PE, HF 631 1 10 - - - 642 458 126 Investment expenses -267 -83 -17 -75 -60 52 -450 -502 -118 Other 112 33 10 83 34 -70 202 202 59

Insurance related income 188 369 -8 314 - - 863 653 216 Policy loans - 3 - 212 - - 215 304 5 Deposits with ceding companies 157 354 64 130 - -124 581 460 199 Other 31 12 -72 -28 - 124 67 -111 12

Non-participating investment income 1 451 1 365 109 1 548 18 -18 4 473 4 626 1 010 Income from with-profit business1 - - - 153 - - 153 158 38 Income from unit-linked business1 - 32 - 645 - - 677 685 155 Total net investment income 1 451 1 397 109 2 346 18 -18 5 303 5 469 1 203

40

Annual results 2012

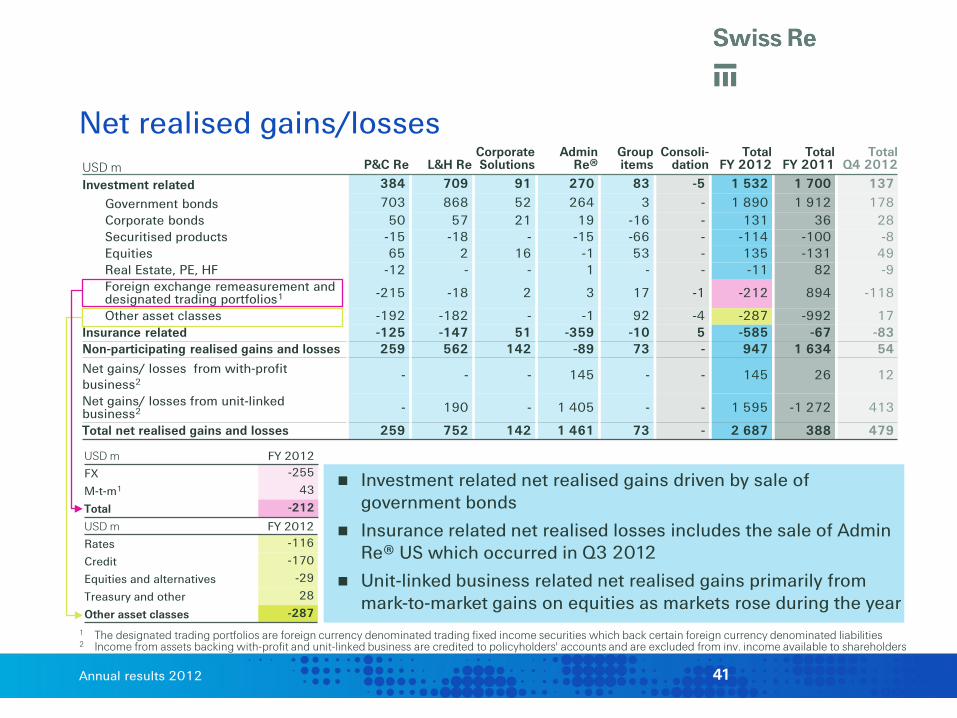

Net realised gains/losses

Investment related net realised gains driven by sale of government bonds

Insurance related net realised losses includes the sale of Admin Re® US which occurred in Q3 2012

Unit-linked business related net realised gains primarily from mark-to-market gains on equities as markets rose during the year

USD m P&C Re L&H Re Corporate Solutions

Admin Re®

Group items

Consoli-dation

Total FY 2012

Total FY 2011

Total Q4 2012

Investment related 384 709 91 270 83 -5 1 532 1 700 137

Government bonds 703 868 52 264 3 - 1 890 1 912 178 Corporate bonds 50 57 21 19 -16 - 131 36 28 Securitised products -15 -18 - -15 -66 - -114 -100 -8 Equities 65 2 16 -1 53 - 135 -131 49 Real Estate, PE, HF -12 - - 1 - - -11 82 -9 Foreign exchange remeasurement and designated trading portfolios1 -215 -18 2 3 17 -1 -212 894 -118

Other asset classes -192 -182 - -1 92 -4 -287 -992 17 Insurance related -125 -147 51 -359 -10 5 -585 -67 -83 Non-participating realised gains and losses 259 562 142 -89 73 - 947 1 634 54 Net gains/ losses from with-profit business2

- - - 145 - - 145 26 12

Net gains/ losses from unit-linked business2 - 190 - 1 405 - - 1 595 -1 272 413

Total net realised gains and losses 259 752 142 1 461 73 - 2 687 388 479

USD m FY 2012 Rates -116

Credit -170

Equities and alternatives -29

Treasury and other 28

Other asset classes -287

USD m FY 2012 FX -255

M-t-m1 43

Total -212

1 The designated trading portfolios are foreign currency denominated trading fixed income securities which back certain foreign currency denominated liabilities 2 Income from assets backing with-profit and unit-linked business are credited to policyholders' accounts and are excluded from inv. income available to shareholders

41

Annual results 2012

USD m P&C Re L&H Re Corporate Solutions

Admin Re®1 Group items

Total FY 2012

Total FY 2011

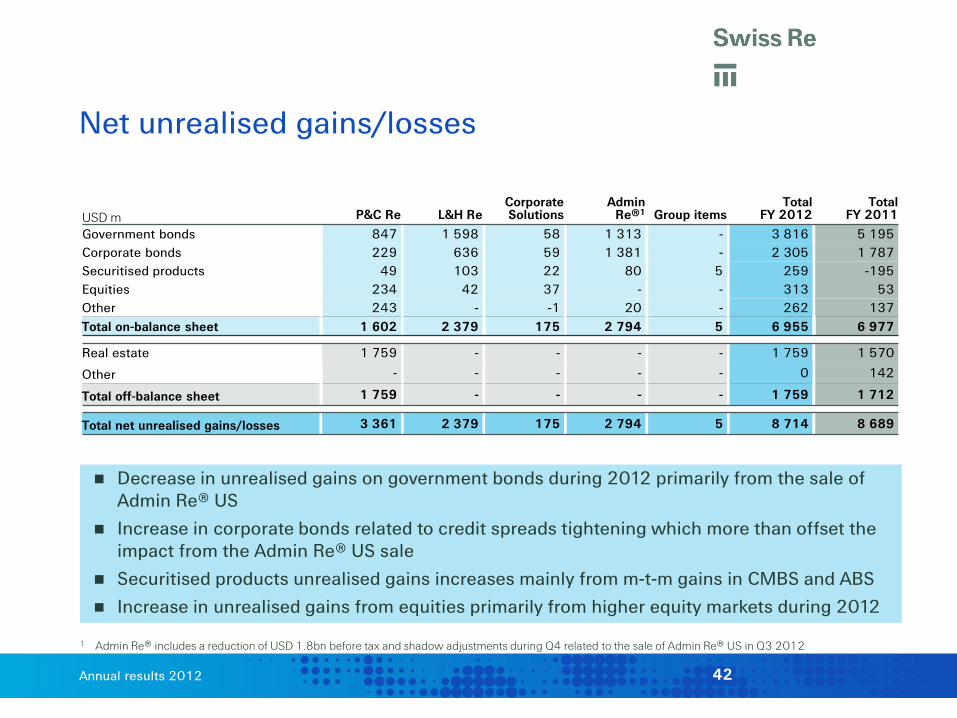

Government bonds 847 1 598 58 1 313 - 3 816 5 195 Corporate bonds 229 636 59 1 381 - 2 305 1 787 Securitised products 49 103 22 80 5 259 -195 Equities 234 42 37 - - 313 53 Other 243 - -1 20 - 262 137 Total on-balance sheet 1 602 2 379 175 2 794 5 6 955 6 977

Real estate 1 759 - - - - 1 759 1 570

Other - - - - - 0 142

Total off-balance sheet 1 759 - - - - 1 759 1 712

Total net unrealised gains/losses 3 361 2 379 175 2 794 5 8 714 8 689

Net unrealised gains/losses

Decrease in unrealised gains on government bonds during 2012 primarily from the sale of Admin Re® US

Increase in corporate bonds related to credit spreads tightening which more than offset the impact from the Admin Re® US sale

Securitised products unrealised gains increases mainly from m-t-m gains in CMBS and ABS

Increase in unrealised gains from equities primarily from higher equity markets during 2012

1 Admin Re® includes a reduction of USD 1.8bn before tax and shadow adjustments during Q4 related to the sale of Admin Re® US in Q3 2012

42

Annual results 2012

Return on investments basis

USD bn FY 20111 FY 2012 Where to find?

Total investment portfolio 173.6 163.7 Slide 45

Unit-linked investments With-profit business

-19.7 -3.3

-22.7 -3.6

Slide 45 Slide 45

Total (excl. unit-linked and with-profit) 150.6 137.4 Slide 45

Cash and cash equivalents Policy loans Other – insurance related Securities in transit Subtract investment related financial liabilities Minority interest in private equity Other assets backing insurance

-10.8 -3.7 -1.5

+1.4 -10.0

-1.3 -0.8

-10.0 -0.3 -1.3

+0.2 -4.1 -0.0 -0.7

Slide 45 Slide 45 Slide 45 Slide 39 Slide 39 n/a Various items (including cat bonds)

Total 123.9 121.2

Investments included in the RoI calculation

1 Return on investments calculation methodology has changed: The scope now includes the Group's entire investment portfolio (incl. Asset Mgmt, Treasury and former Legacy)

43

Annual results 2012

Return on investments (ROI)

USD m P&C Re L&H Re Corporate Solutions

Admin Re®2

Group items

Consoli-dation

Total FY 2012

Total FY 2011

Total Q4 2012

Net investment income 1 263 996 117 1 234 18 -18 3 610 3 973 794 Net realised gains/losses (incl. fx) 384 709 91 270 83 -5 1 532 1 700 137 Other revenue 67 - - -1 - -47 19 24 -4 Investment operating income 1 714 1 705 208 1 503 101 -70 5 161 5 697 927 Less minority interest income -133 - - - - - -133 -159 -1 Less income from cash / interest income -46 -19 -4 -2 - 1 -70 -72 -20

Basis for ROI 1 535 1 686 204 1 501 101 -69 4 958 5 466 906 Average investment assets at avg. fx rates1

47 250 35 919 6 372 30 879 3 659 -1 297 122 782 123 880 119 370

Return on investments2, 3 3.2% 4.7% 3.2% 4.9% 2.8% n/a 4.0% 4.4% 3.0%

1 Average assets calculation based on monthly average 2 Return on investments does not include recycled gains from the sale of Admin Re® US 3 Published FY 2011 RoI 5.1%. Return on investments calculation methodology has changed: The scope now includes the Group's entire investment portfolio

(incl. Asset Mgmt, Treasury and former Legacy)

44

Annual results 2012

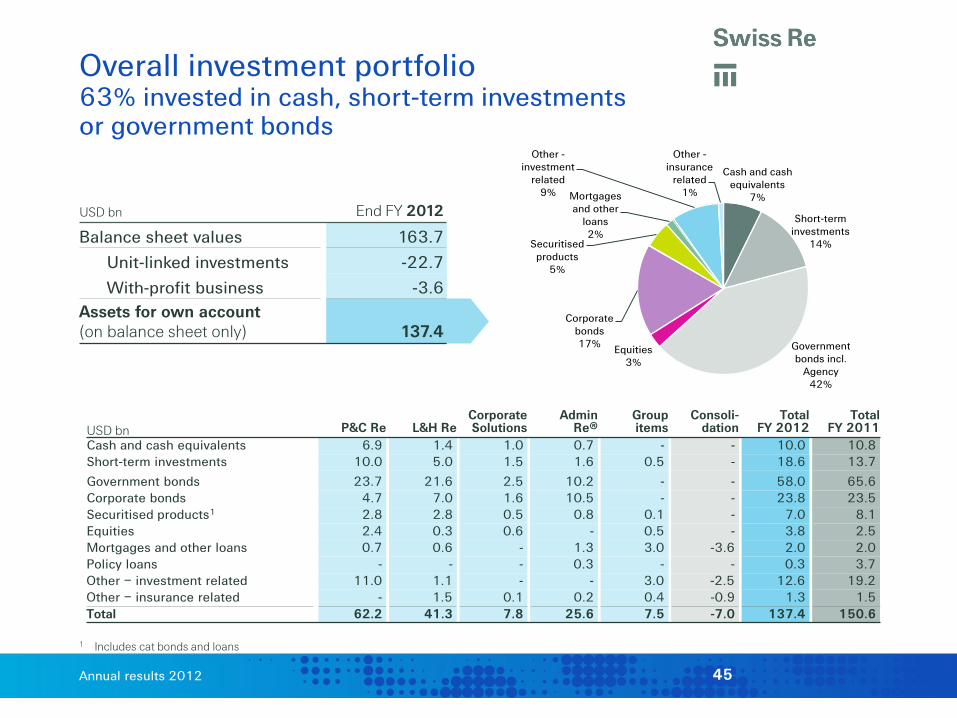

Overall investment portfolio 63% invested in cash, short-term investments or government bonds

Cash and cash equivalents

7%

Short-term investments

14%

Government bonds incl.

Agency 42%

Equities 3%

Corporate bonds 17%

Securitised products

5%

Mortgages and other

loans 2%

Other - investment

related 9%

Other - insurance

related 1%

USD bn End FY 2012

Balance sheet values 163.7

Unit-linked investments -22.7

With-profit business -3.6 Assets for own account (on balance sheet only) 137.4

USD bn P&C Re L&H Re Corporate Solutions

Admin Re®

Group items

Consoli-dation

Total FY 2012

Total FY 2011

Cash and cash equivalents 6.9 1.4 1.0 0.7 - - 10.0 10.8 Short-term investments 10.0 5.0 1.5 1.6 0.5 - 18.6 13.7

Government bonds 23.7 21.6 2.5 10.2 - - 58.0 65.6 Corporate bonds 4.7 7.0 1.6 10.5 - - 23.8 23.5 Securitised products1 2.8 2.8 0.5 0.8 0.1 - 7.0 8.1 Equities 2.4 0.3 0.6 - 0.5 - 3.8 2.5 Mortgages and other loans 0.7 0.6 - 1.3 3.0 -3.6 2.0 2.0 Policy loans - - - 0.3 - - 0.3 3.7 Other – investment related 11.0 1.1 - - 3.0 -2.5 12.6 19.2 Other – insurance related - 1.5 0.1 0.2 0.4 -0.9 1.3 1.5 Total 62.2 41.3 7.8 25.6 7.5 -7.0 137.4 150.6

1 Includes cat bonds and loans

45

Annual results 2012

23.5 23.8

End FY 2011 End FY 2012

Fixed income securities

Government bonds1 Corporate bonds2 Securitised products3

USD bn End FY 2011 End FY 2012 Balance sheet values 101.3 93.5 Unit-linked investments -2.4 -2.6 With-profit business -1.7 -2.1 Balance sheet values (excl. unit-linked and with-profit business) 97.2 88.8

Mark-to-market gains and fx partially offset by net sales and maturities of USD 1.4bn (driven by sale of Admin Re® US of USD 5.5bn and net purchases of USD 4.1bn from moderate re-risking)

65.6 58.0

End FY 2011 End FY 2012

7.6 6.7

End FY 2011 End FY 2012

1 Includes Agency securitised products 2 Includes Pfandbriefe / covered bonds 3 Includes invested assets and off balance sheet investment exposures, excludes cat bonds and loans

Net sales and maturities of USD 9.6bn (driven by sale of Admin Re® US of USD 4.8bn) partially offset by mark-to-market gains and fx

Net sales and maturities of USD 1.8bn (driven by sale of Admin Re® US of USD 1.1bn) partially offset by mark-to market gains and fx

46

Annual results 2012

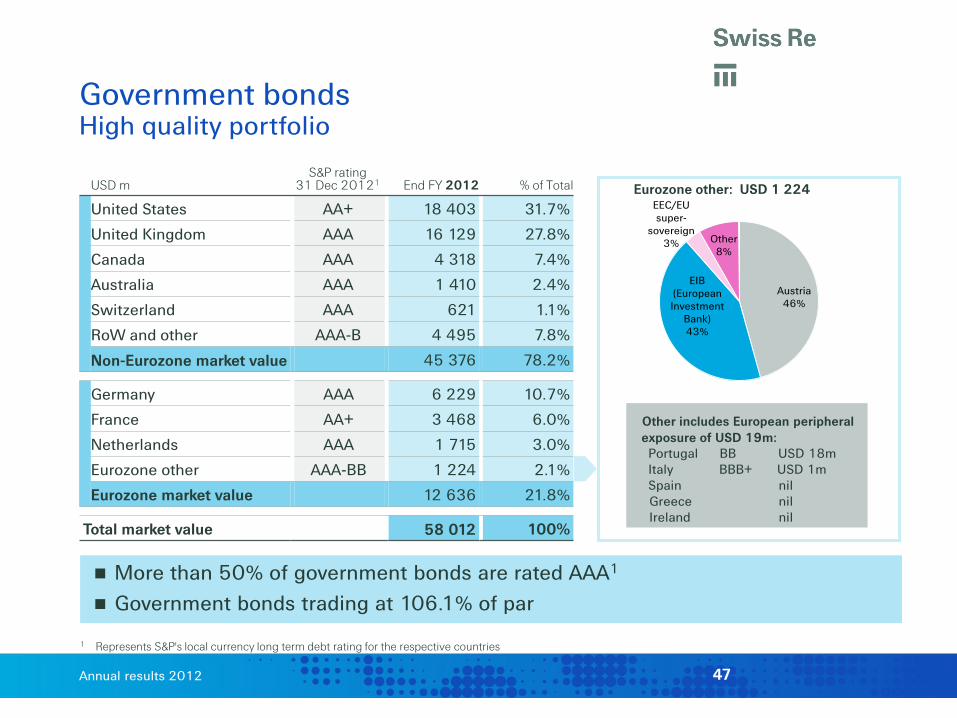

Austria 46%

EIB (European Investment

Bank) 43%

EEC/EU super-

sovereign 3% Other

8%

Eurozone other: USD 1 224

Government bonds High quality portfolio

More than 50% of government bonds are rated AAA1

Government bonds trading at 106.1% of par

USD m S&P rating

31 Dec 20121 End FY 2012 % of Total

United States AA+ 18 403 31.7%

United Kingdom AAA 16 129 27.8%

Canada AAA 4 318 7.4%

Australia AAA 1 410 2.4%

Switzerland AAA 621 1.1%

RoW and other AAA-B 4 495 7.8%

Non-Eurozone market value 45 376 78.2%

Germany AAA 6 229 10.7%

France AA+ 3 468 6.0%

Netherlands AAA 1 715 3.0%

Eurozone other AAA-BB 1 224 2.1%

Eurozone market value 12 636 21.8%

Total market value 58 012 100%

1 Represents S&P's local currency long term debt rating for the respective countries

Other includes European peripheral exposure of USD 19m: Portugal BB USD 18m Italy BBB+ USD 1m Spain nil Greece nil Ireland nil

47

Annual results 2012

Corporate bonds Moderate re-risking while maintaining high quality

1 Hedging is presented on a notional basis; however, when viewed on an economic risk basis, hedging may have a different impact on the portfolio

USD m End FY 2012

% of Total

Resources 2 754 11.6%

Basic industries 1 155 4.8%

Cyclical consumer goods 643 2.7%

Cyclical services 2 812 11.8%

Energy, utilities & mining 2 320 9.7%

Financials 9 271 38.9%

General industries 942 4.0%

Information technologies 348 1.5%

Non-cyclical consumer goods 1 890 7.9%

Non-cyclical services 1 699 7.1%

Total 23 834 100%

8% 7%

34%

45%

6%

AAA

AA

A

BBB

<BBB

End FY 2012

Pfandbriefe / covered bonds

19%

Banks 47%

Specialty 13%

Insurance 13%

Real Estate, other 8%

Total 100%

52%

17% 5%

5%

4%

6%

3%

2% 6%

United States

United Kingdom

Australia

Canada

Switzerland

Netherlands

Sweden

France

Other

Includes USD 5.5bn reduction from sale of Admin Re® US, which was partially offset by net purchases from re-risking of USD 4.1bn

Hedge notional1 decreased by USD 2.9bn to USD 0.2bn Sensitivity - CR01 is the sensitivity of Swiss Re’s investment portfolio per basis point move in credit spreads.

As at 31 December 2012 the net impact would be a decrease of USD 16.7m for each basis point credit spreads widen

48

Annual results 2012

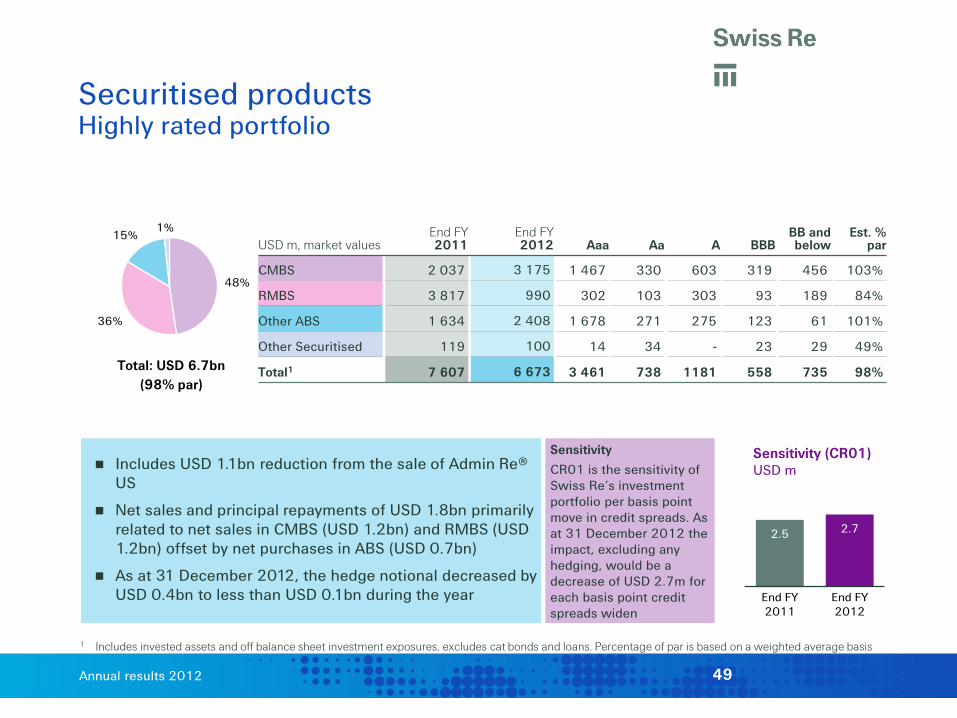

48%

36%

15% 1%

Securitised products Highly rated portfolio

1 Includes invested assets and off balance sheet investment exposures, excludes cat bonds and loans. Percentage of par is based on a weighted average basis

Includes USD 1.1bn reduction from the sale of Admin Re® US

Net sales and principal repayments of USD 1.8bn primarily related to net sales in CMBS (USD 1.2bn) and RMBS (USD 1.2bn) offset by net purchases in ABS (USD 0.7bn)

As at 31 December 2012, the hedge notional decreased by USD 0.4bn to less than USD 0.1bn during the year

USD m, market values End FY 2011

End FY 2012 Aaa Aa A BBB

BB and below

Est. % par

CMBS 2 037 3 175 1 467 330 603 319 456 103%

RMBS 3 817 990 302 103 303 93 189 84%

Other ABS 1 634 2 408 1 678 271 275 123 61 101%

Other Securitised 119 100 14 34 - 23 29 49%

Total1 7 607 6 673 3 461 738 1181 558 735 98% Total: USD 6.7bn (98% par)

2.5 2.7

End FY2011

End FY2012

Sensitivity (CR01) USD m

Sensitivity

CR01 is the sensitivity of Swiss Re’s investment portfolio per basis point move in credit spreads. As at 31 December 2012 the impact, excluding any hedging, would be a decrease of USD 2.7m for each basis point credit spreads widen

49

Annual results 2012

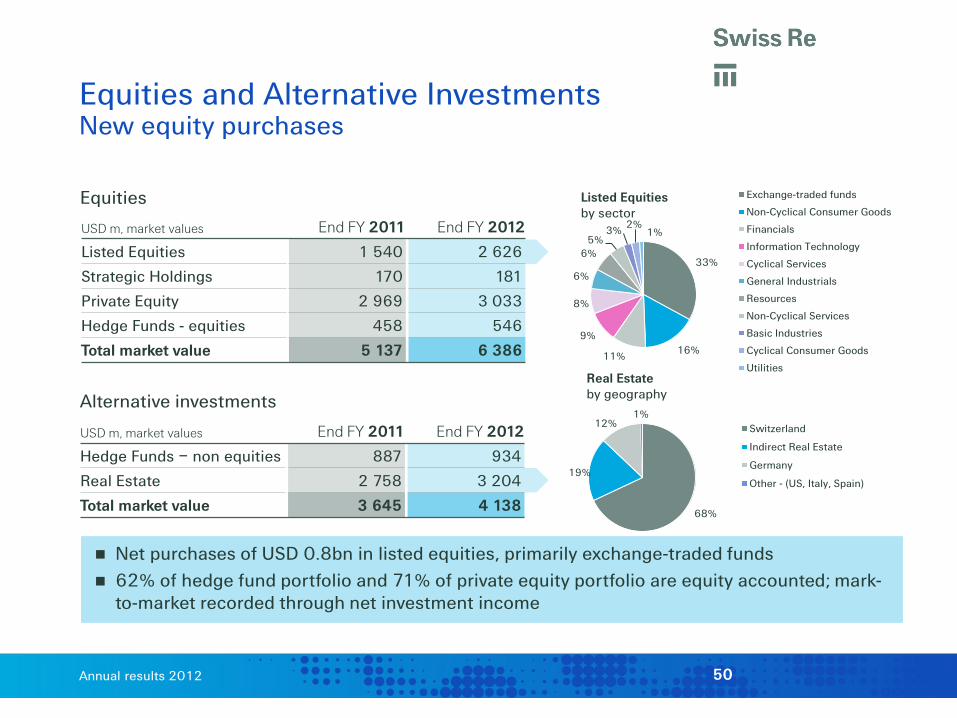

Equities and Alternative Investments New equity purchases

USD m, market values End FY 2011 End FY 2012

Listed Equities 1 540 2 626

Strategic Holdings 170 181

Private Equity 2 969 3 033

Hedge Funds - equities 458 546

Total market value 5 137 6 386

USD m, market values End FY 2011 End FY 2012

Hedge Funds – non equities 887 934

Real Estate 2 758 3 204

Total market value 3 645 4 138

Equities

Alternative investments

Net purchases of USD 0.8bn in listed equities, primarily exchange-traded funds 62% of hedge fund portfolio and 71% of private equity portfolio are equity accounted; mark-

to-market recorded through net investment income

33%

16% 11%

9%

8%

6%

6% 5%

3% 2% 1%

Listed Equities by sector

Exchange-traded funds

Non-Cyclical Consumer Goods

Financials

Information Technology

Cyclical Services

General Industrials

Resources

Non-Cyclical Services

Basic Industries

Cyclical Consumer Goods

Utilities

68%

19%

12% 1%

Real Estate by geography

Switzerland

Indirect Real Estate

Germany

Other - (US, Italy, Spain)

50

Annual results 2012

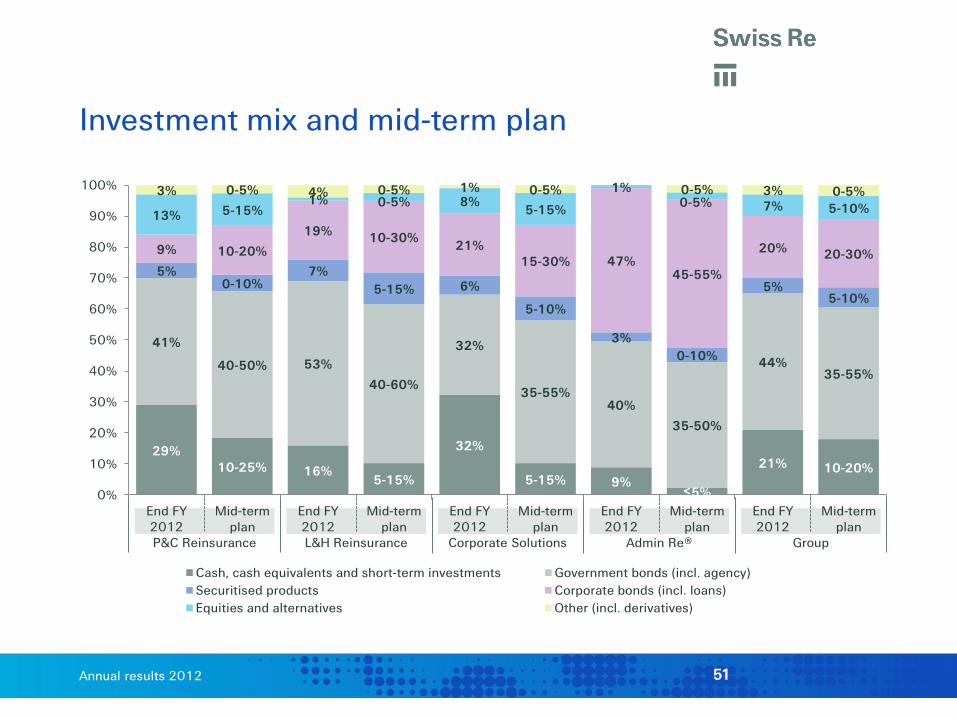

P&C Reinsurance L&H Reinsurance Corporate Solutions Admin Re® Group

Investment mix and mid-term plan

51

29% 10-25% 16%

5-15%

32%

5-15% 9% ≤5%

21% 10-20%

41%

40-50% 53%

40-60%

32%

35-55% 40%

35-50%

44% 35-55%

5% 0-10%

7% 5-15% 6%

5-10%

3% 0-10%

5% 5-10%

9% 10-20%

19% 10-30% 21% 15-30% 47%

45-55%

20% 20-30%

13% 5-15% 1% 0-5% 8%

5-15%

1% 0-5% 7% 5-10%

3% 0-5% 4% 0-5% 1% 0-5% 0-5% 3% 0-5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

End FY2012

Mid-termplan

End FY2012

Mid-termplan

End FY2012

Mid-termplan

End FY2012

Mid-termplan

End FY2012

Mid-termplan

Cash, cash equivalents and short-term investments Government bonds (incl. agency)Securitised products Corporate bonds (incl. loans)Equities and alternatives Other (incl. derivatives)

Annual results 2012

USD m Scenario

Estimated impact on shareholders’

equity

Estimated impact on economic available

capital

Listed equity investments Fall in market values of 25% -657 -657

Private equity investments1 Fall in market values of 25% -804 -804

Hedge Funds investments Fall in market values of 25% -370 -370

Government bonds Rise in interest rates of 100 bps -5 268 -79

Corporate bonds Increase in spreads of 100 bps -1 672

net: -1 670 -1 672

net: -1 670

Securitised products Increase in spreads of 100 bps -265

net: -262 -265

net: -262

Sensitivities

1 Includes strategic holdings Net is net of hedging impact All sensitivities are assumed to take effect on 31 December 2012 and no management actions are included in this analysis. Results are pre-tax and estimated as mutually exclusive events and reflect the estimated impact on the Group of given economic outcomes

52

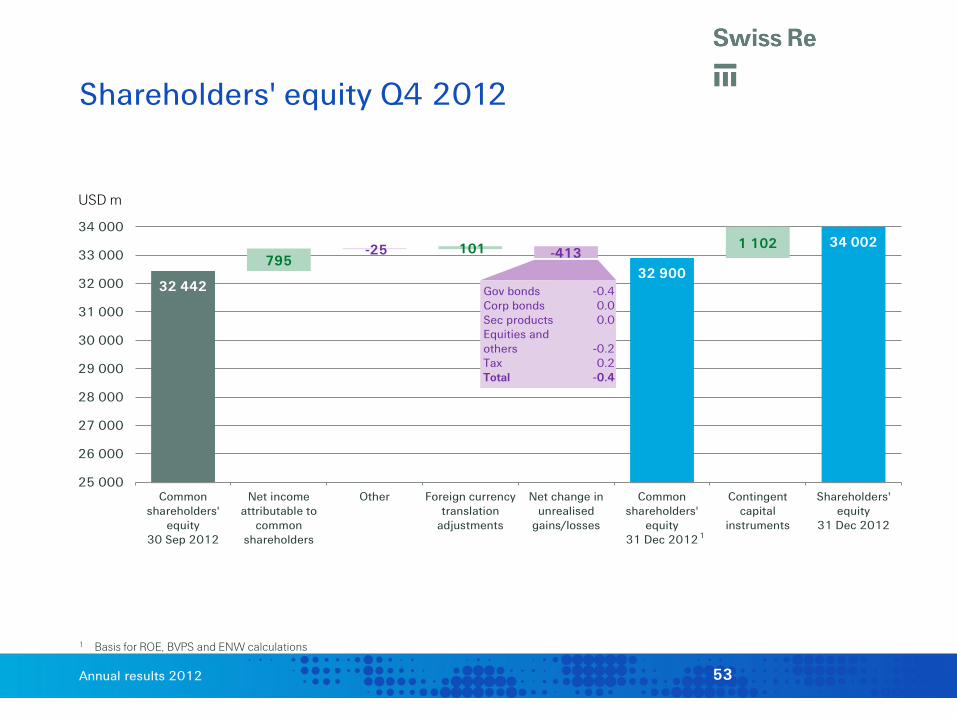

Annual results 2012

32 442

-25 -413 795 101 1 102

32 900

34 002

25 000

26 000

27 000

28 000

29 000

30 000

31 000

32 000

33 000

34 000

Commonshareholders'

equity30 Sep 2012

Net incomeattributable to

commonshareholders

Other Foreign currencytranslation

adjustments

Net change inunrealised

gains/losses

Commonshareholders'

equity31 Dec 2012

Contingentcapital

instruments

Shareholders'equity

31 Dec 2012

USD m

1

1 Basis for ROE, BVPS and ENW calculations

Shareholders' equity Q4 2012

Gov bonds -0.4 Corp bonds 0.0 Sec products 0.0 Equities and others -0.2 Tax 0.2 Total -0.4

53

Annual results 2012

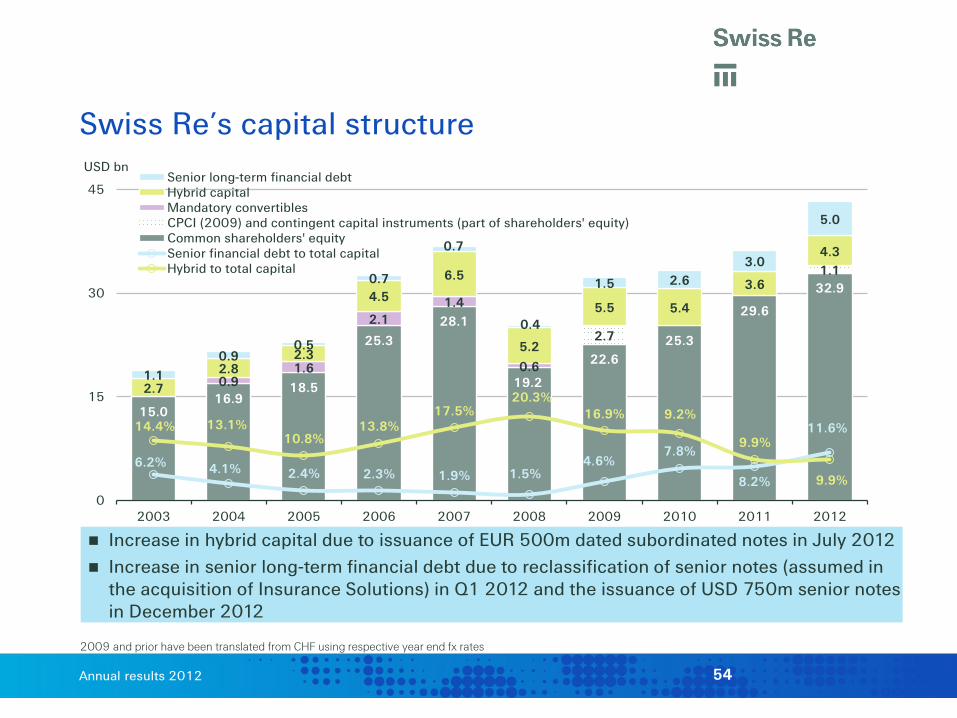

Swiss Re’s capital structure USD bn

2009 and prior have been translated from CHF using respective year end fx rates

15.0 16.9

18.5

25.3 28.1

19.2

22.6 25.3

29.6

32.9

2.7

1.1

0.9 1.6

2.1 1.4

0.6

2.7

2.8 2.3

4.5

6.5

5.2

5.5 5.4

3.6

4.3

1.1 0.9

0.5

0.7

0.7

0.4

1.5 2.6 3.0

5.0

6.2% 4.1% 2.4% 2.3% 1.9% 1.5% 4.6%

7.8%

8.2%

11.6% 14.4% 13.1% 10.8%

13.8% 17.5%

20.3% 16.9% 9.2%

9.9%

9.9%

0%

25%

50%

75%

0

15

30

45

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Senior long-term financial debtHybrid capitalMandatory convertiblesCPCI (2009) and contingent capital instruments (part of shareholders' equity)Common shareholders' equitySenior financial debt to total capitalHybrid to total capital

Increase in hybrid capital due to issuance of EUR 500m dated subordinated notes in July 2012 Increase in senior long-term financial debt due to reclassification of senior notes (assumed in

the acquisition of Insurance Solutions) in Q1 2012 and the issuance of USD 750m senior notes in December 2012

54

Annual results 2012

Increase regular dividend to CHF 3.50 per share and pay out a special dividend of CHF 4.00 per share

– Both dividends to be paid in the form of withholding tax exempt distributions of legal reserves from capital contributions; such reserves totalling CHF 7.8bn as at 31 December 2012 (as confirmed by the Swiss Federal Tax Authority)

Authorised capital – Renew existing authorised capital (up to 85 million shares with a sublimit of 35 million

shares where Board of Directors may limit or withdraw subscription rights of existing shareholders); new proposed expiry date 10 April 2015

– Cancel authorised capital for the exchange of shares

Conditional capital – No changes in conditional capital for equity-linked financing instruments of up to 50 million

shares

– Adjust the limit of total shares issued from authorised and conditional capital without subscription rights of existing shareholders from 74.14 million to 74 million shares for formal reasons, with alignment of the expiry date of the limitation provision with the expiry date of the authorised capital (10 April 2015)

Proposed capital motions for AGM 2013

55

Annual results 2012

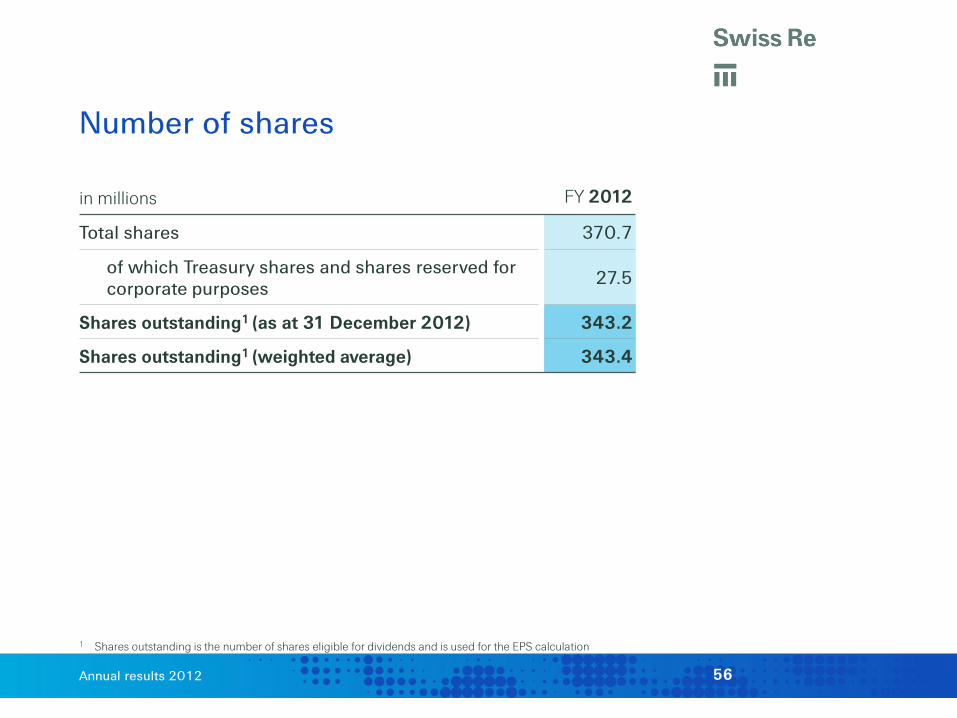

Number of shares

1 Shares outstanding is the number of shares eligible for dividends and is used for the EPS calculation

in millions FY 2012

Total shares 370.7

of which Treasury shares and shares reserved for corporate purposes 27.5

Shares outstanding1 (as at 31 December 2012) 343.2

Shares outstanding1 (weighted average) 343.4

56

Annual results 2012

Premiums by country

USD m Life&Health Non-Life Total

FY 2012 USA

4 554 6 743 11 297 UK 1 598 1 907 3 505 France 198 2 151 2 349 China 92 2 009 2 101 Australia 1 020 885 1 905 Canada 927 544 1 471 Germany 191 1 076 1 267 Japan 207 1 023 1 230 Ireland 701 70 771 Netherlands 106 413 519 Switzerland 73 374 447 Italy 122 305 427 Spain 31 391 422 Bermuda 0 341 341 South Africa 141 142 283 Republic of Korea 57 203 260 Israel 141 86 227 Mexico 23 191 214 India 30 148 178 Other 704 2 590 3 294 Total 10 916 21 592 32 508 1 Country split based on the country where the premium was generated or an approximation thereof

2012 Gross premiums written and fees assessed against policyholders by country1

57

Annual results 2012

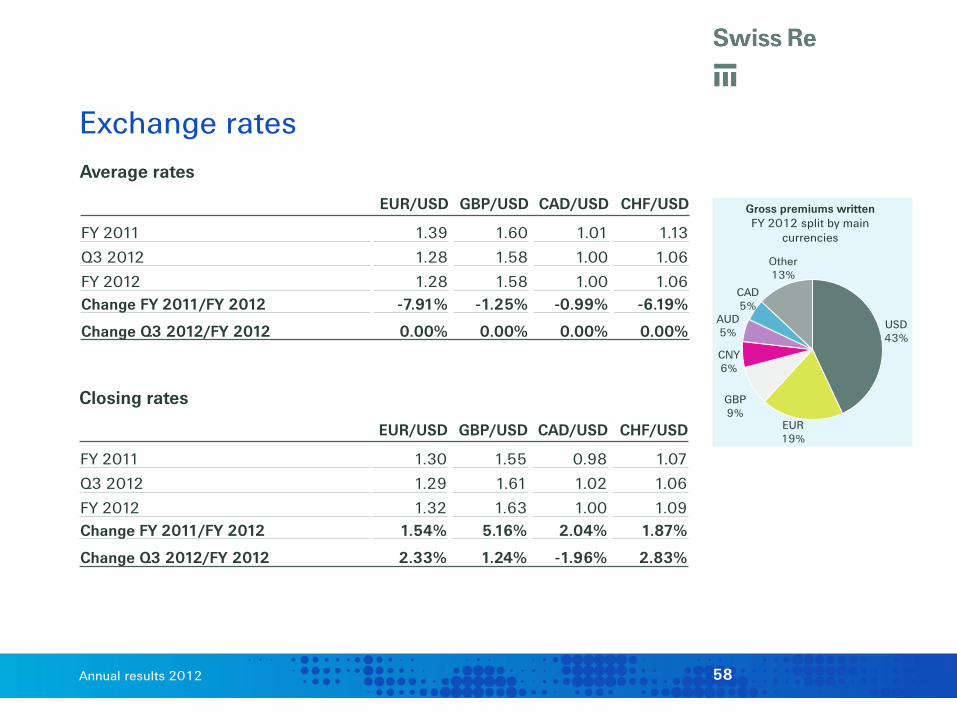

Exchange rates

Closing rates

EUR/USD GBP/USD CAD/USD CHF/USD

FY 2011 1.30 1.55 0.98 1.07

Q3 2012 1.29 1.61 1.02 1.06

FY 2012 1.32 1.63 1.00 1.09 Change FY 2011/FY 2012 1.54% 5.16% 2.04% 1.87%

Change Q3 2012/FY 2012 2.33% 1.24% -1.96% 2.83%

Average rates

EUR/USD GBP/USD CAD/USD CHF/USD

FY 2011 1.39 1.60 1.01 1.13

Q3 2012 1.28 1.58 1.00 1.06

FY 2012 1.28 1.58 1.00 1.06 Change FY 2011/FY 2012 -7.91% -1.25% -0.99% -6.19%

Change Q3 2012/FY 2012 0.00% 0.00% 0.00% 0.00% USD 43%

EUR 19%

GBP 9%

CNY 6%

AUD 5%

CAD 5%

Other 13%

Gross premiums written FY 2012 split by main

currencies

58

Annual results 2012

Investor Relations contacts Hotline E-mail +41 43 285 4444 [email protected] Eric Schuh Ross Walker Chris Menth +41 43 285 4708 +41 43 285 2243 +41 43 285 3878

Simone Lieberherr Simone Fessler +41 43 285 4190 +41 43 285 7299

Corporate calendar 15 March 2013 Publication of Annual Report 2012 and EVM 2012 18 March 2013 AGM Briefing Call Conference call 10 April 2013 149th Annual General Meeting Zurich 02 May 2013 First Quarter 2013 results Conference call 24 June 2013 Investors' Day Zurich 08 August 2013 Second Quarter 2013 results Conference call 07 November 2013 Third Quarter 2013 results Conference call

Corporate calendar & contacts

59

Annual results 2012

Cautionary note on forward-looking statements Certain statements and illustrations contained herein are forward-looking. These statements (including as to plans objectives, targets and trends) and illustrations provide current expectations of future events based on certain assumptions and include any statement that does not directly relate to a historical fact or current fact. Forward-looking statements typically are identified by words or phrases such as “anticipate“, “assume“, “believe“, “continue“, “estimate“, “expect“, “foresee“, “intend“, “may increase“ and “may fluctuate“ and similar expressions or by future or conditional verbs such as “will“, “should“, “would“ and “could“. These forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause Swiss Re’s actual results of operations, financial condition, solvency ratios, liquidity position or prospects to be materially different from any future results of operations, financial condition, solvency ratios, liquidity position or prospects expressed or implied by such statements or cause Swiss Re to not achieve its published targets. Such factors include, among others:

further instability affecting the global financial system and developments related thereto, including as a result of concerns over, or adverse developments relating to, sovereign debt of euro area countries;

further deterioration in global economic conditions; Swiss Re’s ability to maintain sufficient liquidity and access to capital markets,

including sufficient liquidity to cover potential recapture of reinsurance agreements, early calls of debt or debt-like arrangements and collateral calls due to actual or perceived deterioration of Swiss Re’s financial strength or otherwise;

the effect of market conditions, including the global equity and credit markets, and the level and volatility of equity prices, interest rates, credit spreads, currency values and other market indices, on Swiss Re’s investment assets;

changes in Swiss Re’s investment result as a result of changes in its investment policy or the changed composition of its investment assets, and the impact of the timing of any such changes relative to changes in market conditions;

uncertainties in valuing credit default swaps and other credit-related instruments; possible inability to realise amounts on sales of securities on Swiss Re’s balance

sheet equivalent to their mark-to-market values recorded for accounting purposes; the outcome of tax audits, the ability to realise tax loss carryforwards and the

ability to realise deferred tax assets (including by reason of the mix of earnings in a jurisdiction or deemed change of control), which could negatively impact future earnings;

the possibility that Swiss Re’s hedging arrangements may not be effective; the lowering or loss of one of the financial strength or other ratings of one or more

Swiss Re companies, and developments adversely affecting Swiss Re’s ability to achieve improved ratings;

the cyclicality of the reinsurance industry; uncertainties in estimating reserves; uncertainties in estimating future claims for purposes of financial reporting,

particularly with respect to large natural catastrophes, as significant uncertainties may be involved in estimating losses from such events and preliminary estimates may be subject to change as new information becomes available;

the frequency, severity and development of insured claim events; acts of terrorism and acts of war; mortality, morbidity and longevity experience; policy renewal and lapse rates; extraordinary events affecting Swiss Re’s clients and other counterparties, such

as bankruptcies, liquidations and other credit-related events; current, pending and future legislation and regulation affecting Swiss Re or its

ceding companies, and the interpretations of legislation or regulations by regulators;

legal actions or regulatory investigations or actions, including those in respect of industry requirements or business conduct rules of general applicability;

changes in accounting standards; significant investments, acquisitions or dispositions, and any delays,

unexpected costs or other issues experienced in connection with any such transactions;

changing levels of competition; and operational factors, including the efficacy of risk management and other internal

procedures in managing the foregoing risks.

These factors are not exhaustive. Swiss Re operates in a continually changing environment and new risks emerge continually. Readers are cautioned not to place undue reliance on forward-looking statements. Swiss Re undertakes no obligation to publicly revise or update any forward-looking statements, whether as a result of new information, future events or otherwise. This communication is not intended to be a recommendation to buy, sell or hold securities and does not constitute an offer for the sale of, or the solicitation of an offer to buy, securities in any jurisdiction, including the United States. Any such offer will only be made by means of a prospectus or offering memorandum, and in compliance with applicable securities laws.

60