Embed Size (px)

Citation preview

FINANCIAL MANAGEMENT SYSTEMS MANUAL - DRAFT

FEBRUARY 2005

WATER SERVICES TRUST FUNDWATER SERVICES TRUST FUND

PWC

FINANCIAL MANAGEMENT SYSTEMS MANUAL - DRAFT

FEBRUARY 2005

WATER SERVICES TRUST FUNDWATER SERVICES TRUST FUND

PWC

MMIINNIISSTTRRYY OOFF WWAATTEERR AANNDD IIRRRRIIGGAATTIIOONN

TABLE OF CONTENTS

Page

1 Introduction .................................................................................................................1

1.1 Background.........................................................................................................1 1.2 Purpose of the Financial Management Systems Manual (FMSM) ............1 1.3 Structure of the Financial Management Systems Manual ..........................1

2 Financial Regulations and Policies......................................................................5 2.1 Financial regulations .........................................................................................5 2.2 Objectives of the accounting and reporting systems ...................................5 2.3 Significant accounting policies .........................................................................5 2.4 Policies ................................................................................................................5

3 Reporting, Structure of Accounts and Analysis Codes..................................8 3.1 Purpose...............................................................................................................8 3.2 Reports and data analysis requirements .......................................................8 3.3 Chart of accounts .............................................................................................11

4 Systems – to be inserted once Financial Management System is selected......................................................................................................................13

5 Budget Preparation Procedures..........................................................................14 5.1 Budget preparation procedures.....................................................................14 5.2 Annual estimates .............................................................................................14 5.3 Data Flow Diagram ..........................................................................................16

6 Cash Management...................................................................................................20 6.1 Purpose.............................................................................................................20 6.2 Receipt of money and recording of funds....................................................20 6.3 Payment procedures .......................................................................................20 6.4 Authorisation of payment for goods, works and services ..........................21 6.5 Bank and banking arrangements ..................................................................21 6.6 Cash flow forecast and investment of excess funds ..................................22 6.7 Data Flow Diagram (DFD) and Data Processing Instructions (DPI) ........23

7 Petty Cash Control Procedures...........................................................................28 7.1 Purpose.............................................................................................................28 7.2 Policy .................................................................................................................28 7.3 Description ........................................................................................................28

8 Travel and Activity Imprests.................................................................................34 8.1 Purpose.............................................................................................................34 8.2 Policy .................................................................................................................34 8.3 In country- out of station allowance ..............................................................34 8.4 Out of country subsistence allowance..........................................................34 8.5 Application for travels and activities imprests .............................................34

9 Payroll Procedures..................................................................................................39 9.1 Purpose.............................................................................................................39

9.2 Policy .................................................................................................................39 9.3 Description ........................................................................................................40

10 Fixed Assets System..............................................................................................43 10.1 Purpose.............................................................................................................43 10.2 Policy .................................................................................................................43 10.3 Data Flow Diagram (DFD)..............................................................................45

11 WSTF Accounting and Reporting Procedures................................................50 11.1 WSTF accounting policies ..............................................................................50 11.2 Reporting and data analysis requirements ..................................................50 11.3 Reports from benefic iaries and preparation of consolidated reports .......53 11.4 Project auditing arrangements .......................................................................53

APPENDIX 1: Structure of Accounts............................................................................54 APPENDIX 2: Accounting Forms ..................................................................................58 APPENDIX 3: Reporting Forms .....................................................................................71

PricewaterhouseCoopers Water Services Trust Fund 1 Financial Management Manual (Draft)

List of Abbreviations and Acronyms CB Cas h Book CBO Community Based Organisation CEO Chief Executive Officer CV Curriculum Vitae FMSM Financial Management Systems Manual GoK Government of Kenya GRN Goods Received Note LPO Local Purchase Order MTEF Medium Term Expenditure Framework MWI Ministry of Water and Irrigation NGO Non-Governmental Organisation PCV Petty Cash Voucher PS Permanent Secretary PV Payment Voucher WSTF Water Services Trust Fund

PricewaterhouseCoopers Water Services Trust Fund 1 Financial Management Manual (Draft)

1 Introduction

1.1 Background The Water Services Trust Fund (WSTF) was set up under The Water Act 2002 as a mechanism for financing the provision of water and sanitation services to inadequately served areas. WSTF will manage funds received from the Government of Kenya (GoK), donations, grants and bequests from sources as outlined in the Act.

The objectives for which the Trust Fund was formed are:

• Providing financing and other support towards capital investment costs of providing water services to communities without adequate water services; Capacity building activities and projects which enable communities to plan, implement, manage, operate and sustain water services; The creation of awareness and dissemination of information regarding community management of water services; and Active community participation in the implementation and management of water services.

• Providing a mechanism for managing funding systems whose objective is to fund activities within the Water sector generally as may from time to time be assigned to it to manage.

1.2 Purpose of the Financial Management Systems Manual (FMSM) The p urpose of this manual is to provide a comprehensive documentation of the WSTF’s accounting and reporting procedures. It will be used as follows:

• as a training resource for staff either new or redeployed to the WSTF

• as reference material by existing staff in performance of financial management tasks

• by management and trustees of the WSTF in ensuring compliance with WSTF financial management policies and procedures

• by auditors, consultants and development partners who want to understand and/or evaluate WSTF’s financial management systems

1.3 Structure of the Financial Management Systems Manual The Financial Management Systems Manual (FMSM) is organised under three main sections as follows:

l The introduction

l Procedures and documentation

l Appendices

1.3.1 Procedures documentation

The procedures are grouped into a number of sections. In each section the following is provided:

PricewaterhouseCoopers Water Services Trust Fund 2 Financial Management Manual (Draft)

l Purpose of the procedure and significant policy statements (where applicable)

l Description of the procedure

l Data flow diagrams and detailed instructions for the procedure

1.3.2 Appendices

The appendices to the Financial Management Systems Manual include:

l Accounts Structure

l Accounting forms

l Sample of Financial Reporting Forms

1.3.3 Flowchart Symbols Used

Connector

Process

Document

Decision

Computer Interface

Printer

File

PricewaterhouseCoopers Water Services Trust Fund 3 Financial Management Manual (Draft)

1.3.4 How to use the manual

The manual is organised in sections of specific relevance to minimise the need for reference. For example, staff concerned with imprests may need only to read that section, while the finance staff may need to read the whole manual.

1.3.5 How to maintain the manual

The Finance Manager will be directly responsible for the update of this FMSM. However, all users may initiate improvement and changes. The FM will be responsible for ensuring that:

l Amendments to the manual are properly authorised and controlled

l The manual is kept up to date

l Sufficient copies are appropriately distributed in a timely manner.

l A change to the procedures manual could be prompted by:

− A change to existing procedures

− A deletion of existing procedure

− Addition of new or previously omitted procedure.

1.3.6 Distribution of the manual

A record of the holders of the manual showing the holder and the number of the manual shall be maintained.

1.3.7 Financial management and reporting

The principal sources of funding to WSTF are the Government of Kenya (GOK), development partners and other funding agencies and individuals. These sources have varying reporting requirements, all of which have to be met if maximum co-operation from all stakeholders is to be sustained.

To achieve this reporting WSTF has developed financial management systems manual to capture transactions at all levels. The accounting system is central and flexible enough to meet GOK and other development partners accounting and reporting requirements.

For the efficient conduct of the affairs of the WSTF the finance function will be organised as shown below:

PricewaterhouseCoopers Water Services Trust Fund 4 Financial Management Manual (Draft)

Basic organogram of the finance function

The Finance Department headed by a Finance Manager supported by accountants provides regular financial management skills support to implementing bodies. It is responsible for financial reporting and finance mobilization strategies.

The Finance Department also supports the implementing institutions in their strategy formulation, planning and budgeting. It is also be responsible for all the WSTF financial operations and management and cash flow forecasts that will be used for request for disbursement from development partners and other contributors to WSTF.

Finance Manager

Assistant Accountant /

Cashier

Procurement Officer

Internal Auditor

CEO

Financial Accountant

Management Accountant

PricewaterhouseCoopers Water Services Trust Fund 5 Financial Management Manual (Draft)

2 Financial Regulations and Policies

2.1 Financial regulations The FMSM addresses the following GoK regulations:

i. WSTF will be guided by the Trustees Act of the Laws of Kenya

ii. WSTF will strictly adhere to the requirements of the Public Audit Act, 2003 and the Exchequer and Audit Act (CAP, 412), Laws of Kenya;

iii. The Financial Year of the Fund shall be the period of twelve months commencing 1 st July to 30th June of the following year;

2.2 Objectives of the accounting and reporting systems The objectives of WSTF FMSM procedures are to:

• Provide accurate, complete, reliable and timely financial information to management to facilitate informed and timely decision-making

• Ensure effective control and security, and efficient utilisation of resources

• Provide reports to the GoK, donors and other stakeholders in accordance with agreed content, format and reporting period

2.3 Significant accounting policies WSTF will observe accounting practices acceptable to the Government of Kenya and where appropriate, specific accounting policies and reporting requirements as set out in the Memorandum of Understanding between the Trustees and the Donors.

It is a going concern that will report its activities and financial transactions over specified periods on the basis of generally accepted accounting practices. These will be modified as appropriate to address the requirements of the GoK and development partners.

2.4 Policies 2.4.1 Historical cost

Transactions shall be recorded at historical cost i.e. the exchange price on the date of the transaction.

PricewaterhouseCoopers Water Services Trust Fund 6 Financial Management Manual (Draft)

2.4.2 Modified accrual accounting

Under the accrual concept revenue is recognized when earned and expenditure when incurred. WSTF will apply this principle as follows:

Revenue recognition

Revenue is recognized when funds are received both from the Government, other donors and other sources.

Expenditure recognition

Expenses will be recognised when incurred even though payment may not have been made.

2.4.3 Consistency

Consistent accounting methods will be applied and changes made will be reported and the effect on reported results disclosed in accordance with Generally Accepted Accounting Principles (GAAP).

2.4.4 Foreign currency transactions

The accounts of WSTF will be maintained in Kenya Shillings. Transactions denominated in foreign currency will be converted into Kenya Shillings as follows:

• transactions, including grants and donations received, which are expressed or denominated in a foreign currency will be converted into Kenya Shillings at the market exchange rate prevailing at the date of each transaction,

• foreign currency assets and liabilities will be converted into Kenya Shillings at the exchange rates prevailing at the balance sheet date, and

• exchange differences arising from the conversion of foreign currency balances will be dealt with through the income and expenditure statement.

2.4.5 Reporting in foreign currencies

Financial statements may be translated into a relevant foreign currency for donors who require such reports.

PricewaterhouseCoopers Water Services Trust Fund 7 Financial Management Manual (Draft)

In this case:

• transactions and balances which are denominated in foreign currency or expressed in foreign currency shall be shown in the relevant foreign currency.

• all other income and expenditure in Kenya Shillings should be translated into the relevant foreign currency using the average exchange rate obtained from the exchange of the foreign currency during the period, and

• all assets and liabilities will be translated into the relevant foreign currency at the exchange rate prevailing as at the balance sheet date or reporting period.

2.4.6 Fixed Assets

Fixed assets are defined as all tangible assets with a life of three years or more and having a minimum value of Kshs 50,000 either individually or collectively. This may be reviewed and revised by Management as necessary. Fixed Assets will be capitalised, inventoried and controlled individually by assigning tag numbers and maintaining a detailed register combined with periodical physical checks.

2.4.7 Depreciation

The straight-line depreciation method will be used. This will allocate the cost of the depreciable asset uniformly over its expected useful life. The annual depreciation will be based on the full acquisition cost of the depreciable asset, net of its salvage value, as applicable. The rate will apply from the year of acquisition until it is disposed of/written off or until it is fully depreciated, whichever occurs first.

A set of office furniture purchased at a single point in time should be considered an asset for depreciation, even if individual items cost less than the minimum value for categorisation as an asset.

2.4.8 Stocks and stores (inventories)

Stocks will be valued at the lower of cost or net realisable value. Cost will comprise expenditure incurred in the ac quisition of these items.

Items in the stores will be tagged and their usage controlled through the use of store movement cards.

2.4.9 Funds disbursed to Projects

Funds disbursed to various water projects will be recorded as payments in WSTF accounting records. These payments will however need to be fully accounted for and supported with expenditure and project reports.

PricewaterhouseCoopers Water Services Trust Fund 8 Financial Management Manual (Draft)

3 Reporting, Structure of Accounts and Analysis Codes

3.1 Purpose The purpose of the structure of accounts or a chart of accounts and analysis codes is to provide a framework for capturing and grouping data in a manner that will facilitate generation of the required reports. Its design depends on:

• The reporting requirements of the organization

• The accounting software on which the systems are based.

Below are the main procedures in the maintenance of the structure of accounts.

3.2 Reports and data analysis requirements

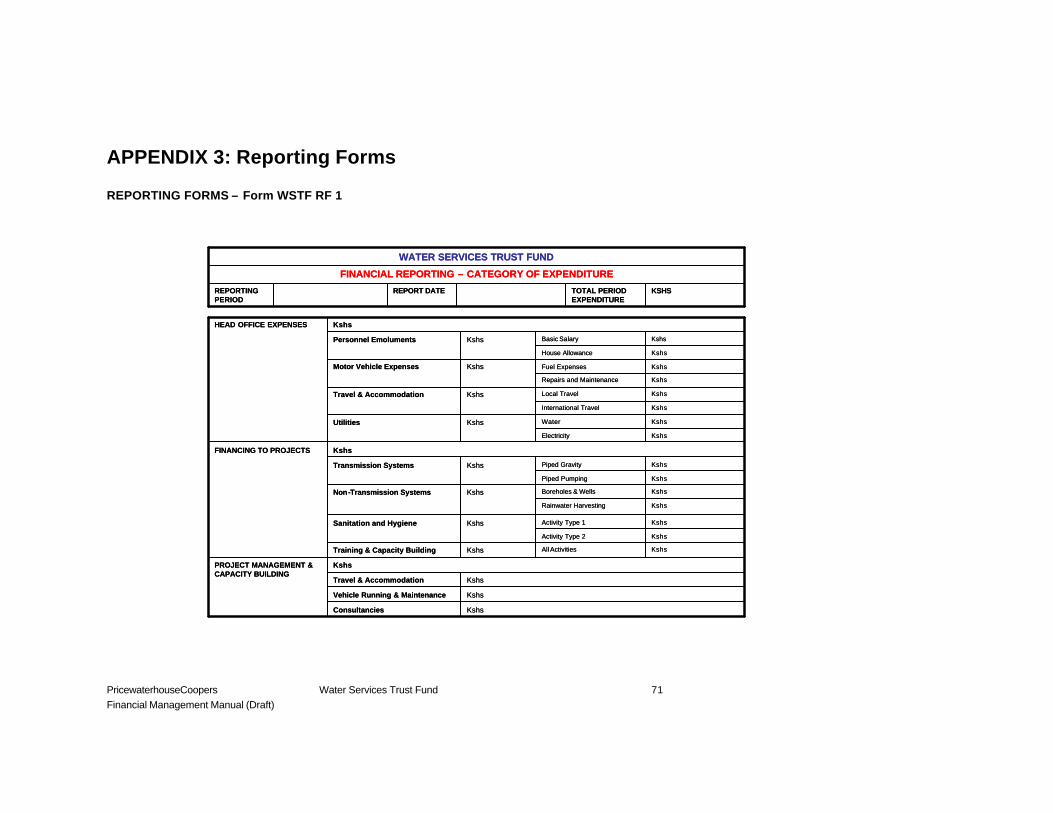

Formats of the required financial reports and management reports are provided in Appendix 3. To efficiently produce these reports, the accounting transactions need to be analysed in a number of ways, including:

• Expenditure categories and sub-categories

• Components and activities

• Source of funds

• Geographical location of projects

• Time frame – date and periods

• Cost centres

• Specific technology applied in water supply interventions

These dimensions of analysis are captured by a combination of both account and analysis codes. Brief descriptions of these dimensions are provided below.

3.2.1 Dimension 1: Expenditure categories and sub-categories

The expenditure categories for the WSTF will follow categories that will assist management control expenditure. The main groups are as follows:

PricewaterhouseCoopers Water Services Trust Fund 9 Financial Management Manual (Draft)

The following will be the 3 main expenditure categories, from which other sub -categories may follow:

• Office Expenses

• Disbursements to Projects

• Project Management and Capacity Building Expenses

Office Expenses:

These would include those costs specifically incurred at the head office or any other WSTF offices and arising from office operations. A number of these expenditure sub-categories would include:

• Personnel emoluments • Motor Vehicle Expenses • Travel and Accommodation • Utilities • Telephone and Postal Expenses • Insurance (Non -Motor) • Board Expenses • Office Running Expenses • Staff Training Costs • Staff Expenses • Consultancies • Advoca cy and Advertising • Printing and Stationery • Bank Charges

Disbursements to Projects

These are those funds disbursed to projects which have been approved based on procedures outlined in the WSTF Operations Manual. Projects receiving funds will then be grouped into the following sub-categories based on the nature of the intervention:

• Water Supply Systems – including piped-gravity and piped-pumping schemes, open ducts, boreholes, shallow wells, rain water harvesting (rain water catchment), dams, pans etc

• Sanitation and Hygiene Promotion

• Training and Capacity Building

PricewaterhouseCoopers Water Services Trust Fund 10 Financial Management Manual (Draft)

Project Management and Capacity Building

This category includes expenses incurred in supervision and co -ordination of implementation of projects which are ongoing at project sites. As the funded projects are envisioned to be demand driven, these expenses will be those incurred in backstopping by technical staff from the head office and would include:

• Travel and Accommodation

• Vehicle running and maintenance costs

• Printing, photocopy and stationery

• Consultancy services for 3 r d parties to carry out the supervision and co-ordination activities where deemed appropriate by WSTF management

3.2.2 Dimension 2: Components and activities

WSTF was formed for the purpose of providing financing and other support towards the capital investment costs of providing water services to communities without adequate water services and to provide a mechanism for managing funding systems whose objective is to fund activities within the water sector.

The key components and priority areas that WSTF will be engaged in seeking to fulfil the above objectives will include;

• Promotion of Water Supply Systems • Promotion of Sanitation and Hygiene • Training and Capacity Building The accounting system will have the ability to generate reports showing expenditure per component and priority area.

3.2.3 Dimension 3: Source of funds

Data may be analysed by the funding source at the transaction entry level to facilitate reporting by financier. Financiers include GOK and other donors or funding agencies.

3.2.4 Dimension 4: Geographic location of projects

Reports produced should enable management assess expenditure by geographic areas and by number of beneficiaries in those locations. Geographic locations may refer to Administrative Regions following from the various Water Service Boards or to Climatic Regions, with areas classified as either, Arid and Semi-Arid Lands (ASAL), High, Medium or Low potential. This will help management identify the cost per beneficiary served in different geographic locations.

PricewaterhouseCoopers Water Services Trust Fund 11 Financial Management Manual (Draft)

3.2.5 Dim ension 5: Timeframe

Management reporting will be on a quarterly basis. Data will be analysed by date at the transaction entry level to facilitate generation of reports for various periods, including daily, weekly, monthly etc.

3.2.6 Dimension 6: WSTF units and cost centres

Data will be analyzed by WSTF Units and Cost Centres, which include:

• Finance & Resource Mobilization Department • Technical Appraisal Department – Nairobi , Central, Coast and Northern • Technical Appraisal Department – Lake Victoria North, Lake Victoria South, Rift Valley • Field Co-ordination Department • Administration and Human Resources Department • Sanitation and Hygiene • Institutional Development • CEO

The heads of different departments will be the budget holders for their respective departments / cost centres.

3.3 Chart of accounts The design of a chart of accounts normally depends on:

• The reporting requirements

• Data analysis and reporting compatibility of the accounting software on which it is based.

To meet the identified reporting requirements, the project accounting software will have a strong data analysis capability and a flexible report generator.

Based on the reporting requirements and operations of the WSTF, the account code will have segments as outlined below. A more detailed illustration of the Accounts Structure is provided in Appendix 1 .

The first segment will identify the Account Type as follows:

100000 for income accounts 200000 for expenditure accounts 300000 for assets 400000 for liabilities 500000 for capital accounts 600000 clearing account

PricewaterhouseCoopers Water Services Trust Fund 12 Financial Management Manual (Draft)

The second segment will identify the Primary Expenditure Groups as follows:

10000 for Office Expenses 20000 for Funds Disbursed to Projects 30000 for Project Management and Capacity Building

The third segment will be the Cost Centre. These would include

1000 Finance & Resource Mobilization Department 2000 Technical Appraisal Department – Nairobi, Central, Coast and Northern 3000 Technical Appraisal Department – Lake Victoria North, Lake Victoria South, Rift Valley 4000 Field Co-ordination Department 5000 Administration and Human Resources Department 6000 Sanitation and Hygiene Department 7000 CEO

The fourth segment will identify the priority intervention areas. These include:

100 Ground Water Distribution 200 Surface Water Distribution 300 Rainwater Harvesting 400 Transmission Systems 500 Point Sources 600 Promotion of Sanitation and Hygiene 700 Training and Capacity Building

The fifth segment is the main account code. For Instance:

10 Printing, photocopy and stationery 20 Travel and accommodation 30 Vehicle running and maintenance costs

PricewaterhouseCoopers Water Services Trust Fund 13 Financial Management Manual (Draft)

4 Systems – to be inserted once Financial Management System is selected

PricewaterhouseCoopers Water Services Trust Fund 14 Financial Management Manual (Draft)

5 Budget Preparation Procedures

5.1 Budget preparation procedures WSTF has a role in the wider budget process through the influence of resource allocation to key priority areas and activities carried out by various stakeholders. WSTF will prepare its annual and quarterly budgets in accordance with the requirements of Government of Kenya. The Government of Kenya budget is prepared in the three-year rolling Medium Term Expenditure Framework (MTEF). The MTEF provides a link between budgetary allocations and specific measures /activities geared towards fulfilling the overall objective or theme of the budget.

5.2 Annual estimates

As outlined in section 3.2.1, WSTF will have 3 key types of expenditure, Offices Expenses; Funds Disbursed to Projects and Project Management and Capacity Building Expenses.

Head Office Expenses which will include personnel emoluments and office operation costs will be categorised as recurrent expenditure while funds disbursed to projects, project management and capacity building expenses will be categorised as development expenditure. Annual estimates for the WSTF will then be prepared in accordance with Treasury circulars.

5.2.1 Recurrent expenditure estimates for WSTF

These will be prepared by the various cost centre heads in consultation with the WSTF Finance and Resource Mobilisation Department. These estimates will be reviewed and approved by the CEO and Trustees and will then be forwarded to the Ministry of Water and Irrigation. These estimates will be prepared in line with the guidelines of the State Corporations Act CAP 446 and The Report of the Inter-Ministerial Task Force on The Delinking of the Water State Corporations of August 2004.

The submissions are scrutinised in line with the recurrent ceiling of the ministry and the resource envelope to the Trust Fund. Monitoring and Evaluation of the annual budget shall be done to rationalize further the available resources for different activities. It also acts as a remedy / check to over-expenditures and under-expenditures in the budgeting process.

5.2.2 Development expenditure estimates for WSTF

WSTF will prepare annual development expenditure budgets guided by the objectives it sets out in its Strategic Plans which will typically be based on a time frame of 3 to 5 years. Based on the identified priority technologies to be employed per geographic area, the intended number of people to be served and costs per beneficiary per identified technology to be applied per geographic area, annual development expenditure estimates may then be generated. The development expenditure budgets prepared in this way will assist the WSTF in resource planning.

PricewaterhouseCoopers Water Services Trust Fund 15 Financial Management Manual (Draft)

For control purposes and expense rationalisation, Project Management and Capacity Building expenses will be computed as a percentage of funds to be disbursed to projects. Depending on the geographical location of the project and technology applied for water supply and sanitation delivery this percentage will vary. WSTF will develop rates following an outline as per the table below to assist it in budgeting.

Region Ground Water

Distribution

Surface Water

Distribution

Rainwater

Harvesting

Transmission

Systems

Point

Sources

Sanitation

and Hygiene

Training

and Cap

Bldg

Central

Coast

L. Victoria N

L. Victoria S

Nairobi

Northern

Rift Valley

It is also recognised that WSTF may receive funds in an ad-hoc manner not necessarily following its calendar year. As this is likely to be a key method of funds receipt, WSTF budget preparation processes should be flexible enough to adapt accordingly and assist management with human and financial resource planning.

Funds will typically be received in two ways: Funds allocated to specific projects; funds received and placed in the WSTF expenditure pool. Besides affecting human resource planning for monitoring, evaluation and technical support, specifically funded projects are not expected to have a major impact on the WSTF annual budgeting process.

Actual funding for disbursement to projects received for the year may differ from that projected based on firm commitments earlier received. The grading of project funding applications should be flexible enough to ensure that funding is then disbursed based on a rational system taking into account the ranking given to the application and geographic location of the project such as to fairly allocate funds to more projects if the funds actually received are higher than the commitments made and to fairly exclude projects if the funds received are less than the commitments made.

Development expenditure estimates will be prepared by activity and type as per the necessary work plans received from the various p rojects. These must be approved by the respective water Service Boards otherwise the Trustees will approve the projects where the Water Service Boards are not yet operational.

PricewaterhouseCoopers Water Services Trust Fund 16 Financial Management Manual (Draft)

5.3 Data Flow Diagram The procedures are provided in detail below.

Heads of Departments

Heads of Departments

Finance Manager

• Finance Manager• CEO• Trustees

1. Staff within the various departments contribute towards the generation of annual expenditure estimates based on their annual work plans

2. The department / cost centre heads submit their expenditure estimates to the finance manager

3. Finance manager to consolidate expenditure estimates from the various departments

4. Finance manager to forward the consolidated organisational -wide expenditure estimate to the CEO and Trustees for review and approval

1.

2.

3.

4.

ResponsibilityProcedure StepsProcess Flow

WSTF Budgeting Preparation Procedures – Recurrent Expenditure

Heads of Departments

Heads of Departments

Finance Manager

• Finance Manager• CEO• Trustees

1. Staff within the various departments contribute towards the generation of annual expenditure estimates based on their annual work plans

2. The department / cost centre heads submit their expenditure estimates to the finance manager

3. Finance manager to consolidate expenditure estimates from the various departments

4. Finance manager to forward the consolidated organisational -wide expenditure estimate to the CEO and Trustees for review and approval

1.

2.

3.

4.

ResponsibilityProcedure StepsProcess Flow

WSTF Budgeting Preparation Procedures – Recurrent Expenditure

Departments / Cost Centres to prepare work plans for the year in consultation with Finance Manager

Annual Work plans and expenditure estimates submitted to the Finance Manager

Finance manager to consolidate the various work plans and expenditure estimates

Consolidated organisational-wide annual recurrent expenditure estimate

To 5

Organisation-wide expenditure estimates forwarded to CEO and Trustees for review and approval

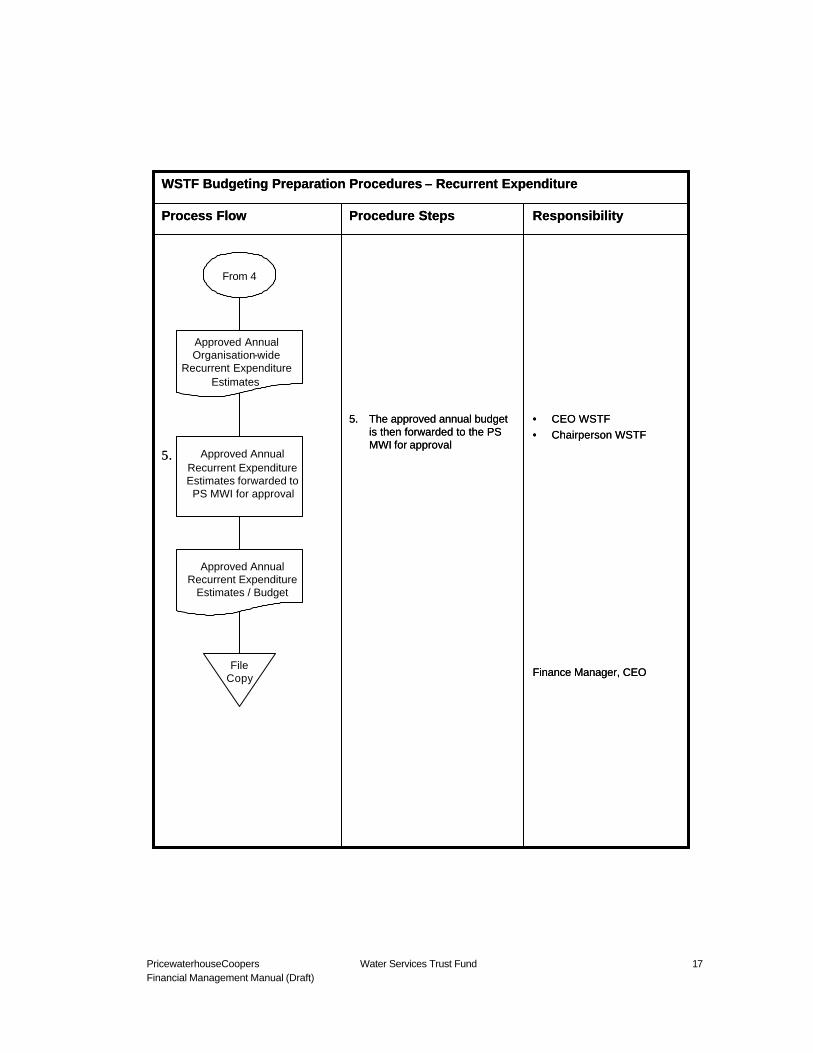

PricewaterhouseCoopers Water Services Trust Fund 17 Financial Management Manual (Draft)

• CEO WSTF• Chairperson WSTF

Finance Manager, CEO

5. The approved annual budget is then forwarded to the PS MWI for approval

5.

ResponsibilityProcedure StepsProcess Flow

WSTF Budgeting Preparation Procedures – Recurrent Expenditure

• CEO WSTF• Chairperson WSTF

Finance Manager, CEO

5. The approved annual budget is then forwarded to the PS MWI for approval

5.

ResponsibilityProcedure StepsProcess Flow

WSTF Budgeting Preparation Procedures – Recurrent Expenditure

Approved Annual Organisation-wide

Recurrent Expenditure Estimates

Approved Annual Recurrent Expenditure Estimates forwarded to PS MWI for approval

Approved Annual Recurrent Expenditure

Estimates / Budget

File Copy

From 4

PricewaterhouseCoopers Water Services Trust Fund 18 Financial Management Manual (Draft)

Department Heads,Finance Manager

Department Heads,Finance Manager

Department Heads,Finance Manager

Finance Manager

CEO

CEO

1. The total number of the target population for the year is identified from the objectives outlined in the Strategic Plan.

2. The target population is divided into geographic areas based both on administrative regions and climatic conditions.

3. A per capita service cost rate is applied to the targeted population per geographic location. A percentage rate for project management and capacity building is also applied based on the value of projects selected for a geographic area.

4. A 1st Draft Development Expenditure Budget is developed

5. The 1st draft budget is circulated to the CEO and all department heads, discussed and agreed upon by the WSTF management team

6. The 1st draft budget is forwarded to the trustees for review and approval

1.

2.

3.

4.

5.

6.

ResponsibilityProcedure StepsProcess Flow

WSTF Budgeting Preparation Procedures – Development Expenditure

Department Heads,Finance Manager

Department Heads,Finance Manager

Department Heads,Finance Manager

Finance Manager

CEO

CEO

1. The total number of the target population for the year is identified from the objectives outlined in the Strategic Plan.

2. The target population is divided into geographic areas based both on administrative regions and climatic conditions.

3. A per capita service cost rate is applied to the targeted population per geographic location. A percentage rate for project management and capacity building is also applied based on the value of projects selected for a geographic area.

4. A 1st Draft Development Expenditure Budget is developed

5. The 1st draft budget is circulated to the CEO and all department heads, discussed and agreed upon by the WSTF management team

6. The 1st draft budget is forwarded to the trustees for review and approval

1.

2.

3.

4.

5.

6.

ResponsibilityProcedure StepsProcess Flow

WSTF Budgeting Preparation Procedures – Development Expenditure

WSTF Strategic Plan

Total No. of Target Population Identified

Target Population divided into

Geographic Regions

Per Capita Service Cost Rates applied to

Target Population

1st Draft Development Expenditure

Budget Developed

1st Draft Development Expenditure

Budget

1st draft circulated and

discussed

1st draft forwarded to trustees for review and

approval

To 7

PricewaterhouseCoopers Water Services Trust Fund 19 Financial Management Manual (Draft)

Trustees

PS MWI

WSTF

7. The approved draft expenditure budget is forwarded to the PS MWI for review and approval

8. The PS MWI reviews and approves the draft development expenditure budget and may propose adjustments to be made

9. The final development expenditure budget is prepared and adopted

7.

8.

9.

ResponsibilityProcedure StepsProcess Flow

WSTF Budgeting Preparation Procedures – Development Expenditure

Trustees

PS MWI

WSTF

7. The approved draft expenditure budget is forwarded to the PS MWI for review and approval

8. The PS MWI reviews and approves the draft development expenditure budget and may propose adjustments to be made

9. The final development expenditure budget is prepared and adopted

7.

8.

9.

ResponsibilityProcedure StepsProcess Flow

WSTF Budgeting Preparation Procedures – Development Expenditure

From 6

Approved draft budget forwarded

to PS MWI

PS MWI reviews and approves draft budget or proposes adjustments

Final Development Expenditure Budget

Prepared

Development Expenditure

Budget

PricewaterhouseCoopers Water Services Trust Fund 20 Financial Management Manual (Draft)

6 Cash Management

6.1 Purpose The purpose of the cash management system is to ensure that:

• All cash received is promptly and accurately accounted for and banked intact

• All payments are properly verified and approved before payment is made

• All vouchers and supporting documentation are properly stamped “paid” immediately after payment is done

• There is adequate segregation of responsibilities

• All cash transactions are properly captured by the General Ledger system

• Bank and cash reconciliations are done on a timely basis

• Cash requirements are forecast and surplus funds may be invested.

6.2 Receipt of money and recording of funds

Funds are received in the following ways:

• Direct transfers into WSTF accounts from the donors and other funding agencies. • Cheque /cash receipts from GoK and donors. • In the case of direct bank transfers, WSTF will receive a deposit advice from the bank to confirm

receipt of the funds. The bank advice will be used to raise a receipt. • When cash/cheque is received, an official receipt will be raised in triplicate immediately.

6.3 Payment procedures Payments will be made to:

• Contracted Parties implementing relevant projects • Suppliers of goods and services • Staff carrying out WSTF activities in form of imprests • Staff as salaries • Replenish petty cash

PricewaterhouseCoopers Water Services Trust Fund 21 Financial Management Manual (Draft)

For all purchase/service and payment orders there shall be two authorised signatories. The Finance department will prepare payments upon the receipt of approved purchase orders, invoices and other supporting documents.

All cheques will be supported by a payment voucher and will be entered into a register before they are released. The register will show the name of the payee, the am ount, the cheque number and the date of collection (or despatch by registered mail and courier). All cancelled cheques will be stamped "VOID" and recorded in the cheque register with the word ‘CANCELLED’ in the payee space.

6.4 Authorisation of payment for goods, works and services

Official purchase orders shall be issued for all goods, works and services required in accordance with the WSTF procurement regulations. These regulations will be based on best practice, public procurement regulations and project donor procurement guidelines. For specific procurements being funded by a specific Development Partner, the WSTF procurement regulations and practices will allow GoK and /or development partners procedures to take precedence over any conflicting provisions in the WSTF regulations.

Local Purchase/Service Orders shall be in a form approved by the Finance Manager in liaison with the Administration and Human Resources Manager as well as the Procurement Officer.

The Procurement Officer shall control the printing and issue of such forms. The orders and copies thereof shall contain such information as the Procurement Officer in consultation with the Finance Manager and Administration and Human Resources Manager, require from time to time to ensure that there is an a dequate record of WSTF’s liability.

The Local Purchase/Service Order will be signed by two authorised officials as follows:

Finance Manager & CEO Kshs.5,000 – Kshs.1 Million Selected Trustee and CEO Over Kshs.1 Million Authorisation for payment levels and signatories are as follows:

Finance Manager Up to Kshs. 200,000 CEO Up to Kshs. 5,000,000 Trustees’ resolution Over Kshs. 5 million

6.5 Bank and banking arrangements The CEO on behalf of the Fund shall make all bank and banking arrangements with reputable banks only as approved by the trustees.

The cheque signatories will fall under two categories as follows:

Category A Finance Manager

PricewaterhouseCoopers Water Services Trust Fund 22 Financial Management Manual (Draft)

CEO Category B WSTF Chairperson Two designated trustees All cheques must have 2 signatories with both Category A and B bei ng mandatory. Cheques shall only be ordered by any of the two signatories per mandate. The Finance Manager will make adequate arrangements for their custody.

Cheques in current use shall be entered in the register of accountable documen ts to be kept by the Finance Manager.

Bank reconciliations will be prepared not later than 10 working days after the previous end of month by the Accountant. The Finance Manager will ensure the reconciliation of all bank account balances to the cashbooks is done. Each bank reconciliation will be prepared by a designated accountant and reviewed by the Finance Manager (Evidence of the date of preparation and review must be indicated on each reconciliation). The WSTF CEO will randomly review the bank reconciliations from time to time.

6.5.1 Insurance

All cash in transit and petty cash held in the WSTF offices shall be insured against any form of loss. The level of insurance shall depend on the security measures put in place to minimise theft or any other form of loss.

Fidelity guarantee must be taken in respect of pecuniary loss as a result of infidelity of employees occupying declared positions in finance.

6.6 Cash flow forecast and investment of excess funds Cash flow projections will be prepared and the cash position reviewed in making cash management decisions. Surplus funds will be invested, according to the approved investment policy, while ensuring WSTF is liquid enough to make payments for its obligations in a timely manner.

The Finance Manager will be responsible for the preparation of cash projections (Weekly, monthly, quarterly) and any envisaged excess funds/cash will be invested in short term (Maximum 90 days) liquid and secure securities e.g. Government securities like Treasury Bills or similar investments. WSTF’s bankers will act as agents and/or advisors once investment decisions are taken by the Fund.

PricewaterhouseCoopers Water Services Trust Fund 23 Financial Management Manual (Draft)

6.7 Data Flow Diagram (DFD) and Data Processing Instructions (DPI) The procedures are provided in detail below.

Finance Manager (FM)

Cashier

Cashier

Cashier

Accountant

Accountant

Accountant

1. Receive cheque or bank deposit advice, ensure it has been registered in the incoming mail register, and forward it to the Cashier.

2. Receive cash/cheque or bank deposit advice and raise an official receipt in triplicate. Send one copy to source of funds to acknowledge receipt. File a copy in the bank fi le and leave third as the book copy.

3. Bank cheques and cash received immediately, and not later than the end of the business day following the date of receipt.

4. Code the Official Receipt using the chart of Accounts and analysis codes.

5. Review Coding and approve for entry to Cashbook.

6. Update the Cashbook.

7. File official receipts and bank pay- in-slips, and vouchers in serial number order.

1.

2.

3.

4.

5.

6.

7.

ResponsibilityProcedure StepsProcess Flow

Receipt and Recording of Funds

WSTF Cash Management Procedures

Finance Manager (FM)

Cashier

Cashier

Cashier

Accountant

Accountant

Accountant

1. Receive cheque or bank deposit advice, ensure it has been registered in the incoming mail register, and forward it to the Cashier.

2. Receive cash/cheque or bank deposit advice and raise an official receipt in triplicate. Send one copy to source of funds to acknowledge receipt. File a copy in the bank fi le and leave third as the book copy.

3. Bank cheques and cash received immediately, and not later than the end of the business day following the date of receipt.

4. Code the Official Receipt using the chart of Accounts and analysis codes.

5. Review Coding and approve for entry to Cashbook.

6. Update the Cashbook.

7. File official receipts and bank pay- in-slips, and vouchers in serial number order.

1.

2.

3.

4.

5.

6.

7.

ResponsibilityProcedure StepsProcess Flow

Receipt and Recording of Funds

WSTF Cash Management Procedures

Funds Advice

Receive Chq /Advice

Raise receipt

Receipt

File

Pay -in Slips

Bank Funds

Assign Codes

Approve

Record

File

Funds from donors

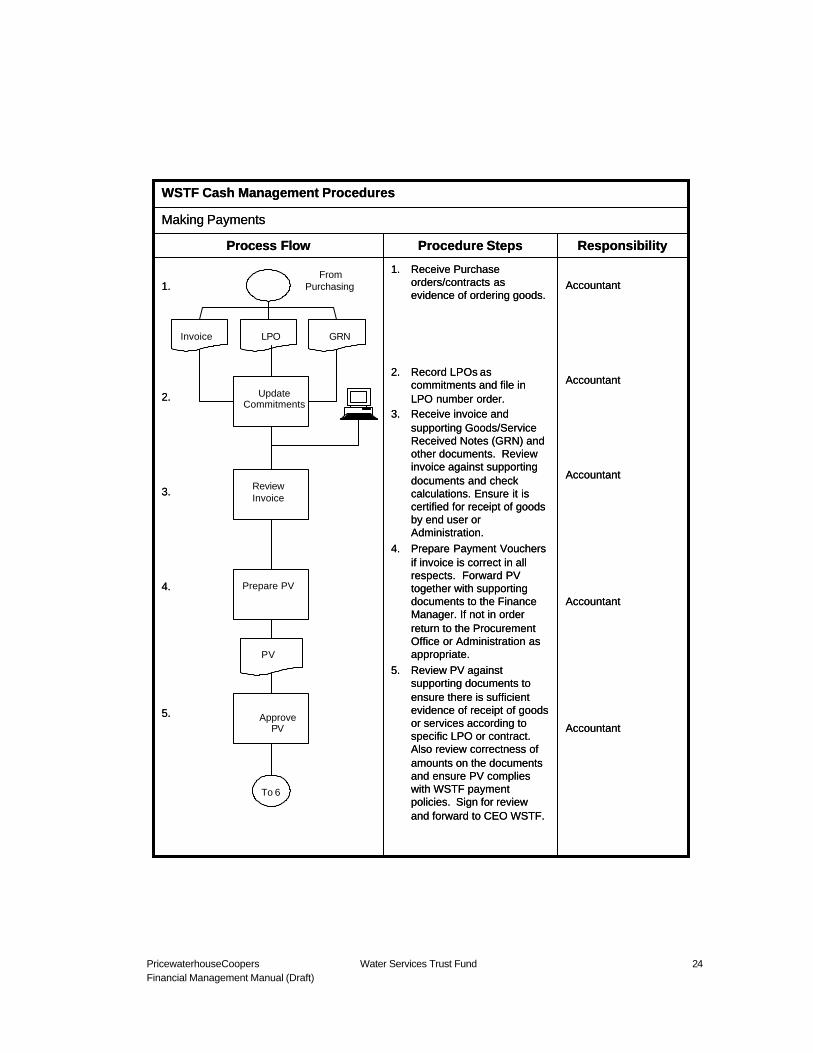

PricewaterhouseCoopers Water Services Trust Fund 24 Financial Management Manual (Draft)

Accountant

Accountant

Accountant

Accountant

Accountant

1. Receive Purchase orders/contracts as evidence of ordering goods.

2. Record LPOs as commitments and file in LPO number order.

3. Receive invoice and supporting Goods/Service Received Notes (GRN) and other documents. Review invoice against supporting documents and check calculations. Ensure it is certified for receipt of goods by end user or Administration.

4. Prepare Payment Vouchers if invoice is correct in all respects. Forward PV together with supporting documents to the Finance Manager. If not in order return to the Procurement Office or Administration as appropriate.

5. Review PV against supporting documents to ensure there is sufficient evidence of receipt of goods or services according to specific LPO or contract. Also review correctness of amounts on the documents and ensure PV complies with WSTF payment policies. Sign for review and forward to CEO WSTF.

1.

2.

3.

4.

5.

ResponsibilityProcedure StepsProcess Flow

Making Payments

WSTF Cash Management Procedures

Accountant

Accountant

Accountant

Accountant

Accountant

1. Receive Purchase orders/contracts as evidence of ordering goods.

2. Record LPOs as commitments and file in LPO number order.

3. Receive invoice and supporting Goods/Service Received Notes (GRN) and other documents. Review invoice against supporting documents and check calculations. Ensure it is certified for receipt of goods by end user or Administration.

4. Prepare Payment Vouchers if invoice is correct in all respects. Forward PV together with supporting documents to the Finance Manager. If not in order return to the Procurement Office or Administration as appropriate.

5. Review PV against supporting documents to ensure there is sufficient evidence of receipt of goods or services according to specific LPO or contract. Also review correctness of amounts on the documents and ensure PV complies with WSTF payment policies. Sign for review and forward to CEO WSTF.

1.

2.

3.

4.

5.

ResponsibilityProcedure StepsProcess Flow

Making Payments

WSTF Cash Management Procedures

Invoice LPO GRN

Update Commitments

Review Invoice

Prepare PV

PV

Approve PV

To 6

From Purchasing

PricewaterhouseCoopers Water Services Trust Fund 25 Financial Management Manual (Draft)

Finance Manager

Cashier

Cheque Signatories

Accountant

Cashier

Accountant

Accountant

6. Sign PV to authorise payment and forward it together with supporting documents to the Cashier.

7. Prepare cheque and submit to the signatories.

8. Sign cheques and forward for recording and despatch.

9. Record details of signed cheques in the Cheque Despatch Register. Ensure that all cancelled Cheque are stamped ‘VOID’ and recorded in the Register with word ‘CANCELLED’ on the payee field. Ensure persons collecting Cheques enter their name, signature and identification numbers on the Register. Use Registered mail or Courier service for deliveries outside Nairobi.

10. Stamp the PV, invoices and supporting documents ‘PAID’. Record the payment in the Cash Book.

11. Review Cashbook journal and update General Ledger.

12. File PVs, supporting journal print out and documents in PV order number

6.

7.

8.

9.

10.

11.

12.

WSTF Cash Management Procedures

Finance Manager

Cashier

Cheque Signatories

Accountant

Cashier

Accountant

Accountant

6. Sign PV to authorise payment and forward it together with supporting documents to the Cashier.

7. Prepare cheque and submit to the signatories.

8. Sign cheques and forward for recording and despatch.

9. Record details of signed cheques in the Cheque Despatch Register. Ensure that all cancelled Cheque are stamped ‘VOID’ and recorded in the Register with word ‘CANCELLED’ on the payee field. Ensure persons collecting Cheques enter their name, signature and identification numbers on the Register. Use Registered mail or Courier service for deliveries outside Nairobi.

10. Stamp the PV, invoices and supporting documents ‘PAID’. Record the payment in the Cash Book.

11. Review Cashbook journal and update General Ledger.

12. File PVs, supporting journal print out and documents in PV order number

6.

7.

8.

9.

10.

11.

12.

WSTF Cash Management Procedures

From 5

Authorise Payment

Prepare Cheque

Sign Cheque

Stamp PV

Record Cheque

Update CB and GL

File

Cheque

PricewaterhouseCoopers Water Services Trust Fund 26 Financial Management Manual (Draft)

Finance Manager

Accountant

Accountant

Accountant

Finance Manager

Accountant

Accountant

1. Receive monthly bank statements from the bank.

2. Agree the balance to the cashbook balance

3. Identify the reconciling items.

4. Prepare adjusting journals for the identified reconciling items.

5. Review the reconciliation and sign off

6. Process the journals in the accounts and adjust the cash book.

7. File copy of the reconciliation

1.

2.

3.

4.

5.

6.

7.

ResponsibilityProcedure StepsProcess Flow

Bank reconciliation procedures

WSTF Cash Management Procedures

Finance Manager

Accountant

Accountant

Accountant

Finance Manager

Accountant

Accountant

1. Receive monthly bank statements from the bank.

2. Agree the balance to the cashbook balance

3. Identify the reconciling items.

4. Prepare adjusting journals for the identified reconciling items.

5. Review the reconciliation and sign off

6. Process the journals in the accounts and adjust the cash book.

7. File copy of the reconciliation

1.

2.

3.

4.

5.

6.

7.

ResponsibilityProcedure StepsProcess Flow

Bank reconciliation procedures

WSTF Cash Management Procedures

Receive Statement

Agree to Cashbook

Identify reconciling

items

Prepare adjusting journals

Sign Off

Process account

File

Print-out

PricewaterhouseCoopers Water Services Trust Fund 27 Financial Management Manual (Draft)

Heads of Departments

Finance Manager

Finance Manager

Finance Manager

Finance Manager

CEO and Trustees

Finance Manager

Finance Manager

Monthly:1. With assistance from

Finance, allocate planned expenditure to the approximate month of payment. In doing this consider timing of activity and payment policy.

2. Generate cash requirements forecast analysed by activity and expense type.

3. Prepare a projected cash inflow analysed by source of funds and discuss with CEO

4. Obtain approval of cash flow forecast from the CEO and transfer funds to operating accounts as appropriate.

5. Seek authority to invest surplus funds in accordance to WSTF’s surplus funds investment policy

6. Approve investment of funds in deposit accounts.

7. Prepare advice for funds transfer; obtain approval from cheque signatories and forward transfer advice to the Bank.

8. File copy of the forecast

1.

2.

3.

4.

5.

6.

7.

8.

ResponsibilityProcedure StepsProcess Flow

Review of Cash position and Preparation of Cash Forecasts

WSTF Cash Management Procedures

Heads of Departments

Finance Manager

Finance Manager

Finance Manager

Finance Manager

CEO and Trustees

Finance Manager

Finance Manager

Monthly:1. With assistance from

Finance, allocate planned expenditure to the approximate month of payment. In doing this consider timing of activity and payment policy.

2. Generate cash requirements forecast analysed by activity and expense type.

3. Prepare a projected cash inflow analysed by source of funds and discuss with CEO

4. Obtain approval of cash flow forecast from the CEO and transfer funds to operating accounts as appropriate.

5. Seek authority to invest surplus funds in accordance to WSTF’s surplus funds investment policy

6. Approve investment of funds in deposit accounts.

7. Prepare advice for funds transfer; obtain approval from cheque signatories and forward transfer advice to the Bank.

8. File copy of the forecast

1.

2.

3.

4.

5.

6.

7.

8.

ResponsibilityProcedure StepsProcess Flow

Review of Cash position and Preparation of Cash Forecasts

WSTF Cash Management Procedures

Payments timing

estimate

Generate Cash Requirement

Forecast

Project Cash-flow

Obtain approval

Surplus?

Seek approval

Approve investment

Process transfer

File To Bank

Bank advice

File

Bank statement

Forecast

From bank

NO

YES

PricewaterhouseCoopers Water Services Trust Fund 28 Financial Management Manual (Draft)

7 Petty Cash Control Procedures

7.1 Purpose The purpose of the petty cash system is to ensure:

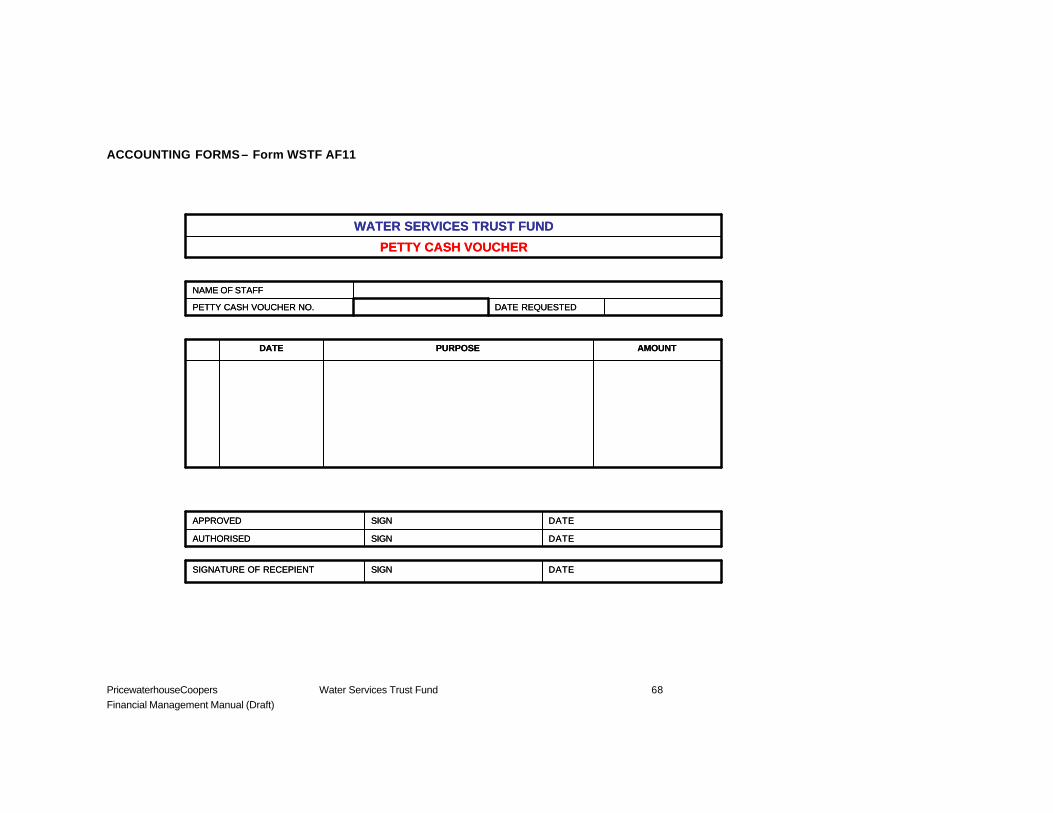

• The maintenance of sufficient amount of float to meet small cash needs • Safe custody of petty cash funds • Adequate controls over a petty cash held and petty cash payments made • Prompt and accurate processing, issuance, recording and accounting for petty cash.

7.2 Policy WSTF will maintain a petty cash float to meet small office expenses.

WSTF management will agree the float amount which will be monitored and revised, with approval of the CEO, when considered necessary.

Any payments in excess of Kshs 5,000 will be made by Cheque.

7.3 Description The Cashier will maintain an initial float of Kshs 50,000 for meeting small office expenses, and any other cash withdrawn for specific purposes has to be surrendered to the Cashier for proper accounting before the money is paid out. Petty cash will not be used for workshops, travel, per diems, allowances, fuel or salary advances.

Travel allowance and workshop imprest procedures are provided in Section 8. Funds for these activities will be advanced and accounted for using an Imprest Application Form and an Imprest Accounting Form.

Petty cash shall be securely locked up in a safe. The Cashier should ensure adequate security measures are in place while transporting petty cash from the bank and when accessing the safe to make payments.

The Finance Manager will conduct surprise petty cash counts to ensure petty cash is safe, used as intended and accounted for correctly. The count sheet shall be counter signed by both the Cashier and the person conducting the count and dated. Any discrepancies noted shall be reported immediately to the Finance Manager and WSTF CEO.

7.3.1 Request and payment of petty cash

Requests for petty cash will be made using a Petty Cash Voucher (PCV). Employees requiring petty cash will complete the form and obtain approval from the respective Head of Department. Heads of

PricewaterhouseCoopers Water Services Trust Fund 29 Financial Management Manual (Draft)

Departments requiring petty cash will complete the form and obtain approval from the Finance Manager or CEO.

Once approved by the Finance Manager or Accountant, the PCV will be presented to the Cashier for payment. The recipient of petty cash will sign the PCV on receipt of the funds. The Cashier will retain the PCV in the petty cash box until the funds are accounted for with supporting documents.

7.3.2 Accounting for expenditure

Petty cash advances will be accounted for immediately after incurring expenditure. This should take place on the same day the petty cash a dvance is taken. Only in exceptional cases should petty cash be accounted other than on the day of disbursement. The petty cash holder will summarise the expenses, attach all the receipts and submit them to the Cashier. Any difference between the advance and the expenditure will be reflected on the PCV and surrendered to the Cashier. If more than the approved advance is spent, the person who authorised the expenditure will be required to approve the additional payment to the Petty Cash holder.

Un-surrendered petty cash should be recovered from the staff salary in the same month it was paid out.

7.3.3 Petty cash replenishment

The petty cash float will be replenished with the amount spent every time the balance falls below 25% of the float. The CEO, WSTF will appro ve any revision to this percentage. A properly analysed Petty Cash Replenishment Request Form will be completed to account for the float. This will be adequately supported by PCVs and expenditure receipts.

A payment voucher will be raised for the replenishment. The petty cash replenishment cheque should be reconciled to the petty cash expenditure. Any discrepancies noted should be investigated immediately and corrective action taken.

7.3.4 Cash reconciliation procedures

This will be prepared on a daily basis by the Cashier and supervised by the Accountant who will ensure that it agrees to the daily balances.

7.3.5 Data flow Diagram (DFD)

The procedures are illustrated below.

PricewaterhouseCoopers Water Services Trust Fund 30 Financial Management Manual (Draft)

Petty Cash Applicant

Finance Manager orAccountant

Petty Cash Applicant

Cashier

1. Fill in a Petty Cash Voucher (PCV) for the required amount of petty cash and forward to the to Section Head to approve.

2. Review PCV and ensure that:

• it is reasonable and/or adequately supported by valid documentation

• the purpose of the request (the activity, expenditure type and details) is clearly stated

• activity is within the approved work-plan and budget approved.

Approve petty cash voucher and forward to the Cashier.

3. Receive cash from the Cashier and sign for receipt

4. Hold PCV in petty cash box until funds are accounted for

1.

2.

3.

4.

ResponsibilityProcedure StepsProcess Flow

Request and Payment of Petty Cash

WSTF: PETTY CASH CONTROL

Petty Cash Applicant

Finance Manager orAccountant

Petty Cash Applicant

Cashier

1. Fill in a Petty Cash Voucher (PCV) for the required amount of petty cash and forward to the to Section Head to approve.

2. Review PCV and ensure that:

• it is reasonable and/or adequately supported by valid documentation

• the purpose of the request (the activity, expenditure type and details) is clearly stated

• activity is within the approved work-plan and budget approved.

Approve petty cash voucher and forward to the Cashier.

3. Receive cash from the Cashier and sign for receipt

4. Hold PCV in petty cash box until funds are accounted for

1.

2.

3.

4.

ResponsibilityProcedure StepsProcess Flow

Request and Payment of Petty Cash

WSTF: PETTY CASH CONTROL

Prepare PCV

PCV

Approve PCV

Receive Cash

Hold

PricewaterhouseCoopers Water Services Trust Fund 31 Financial Management Manual (Draft)

Petty Cash Holder

Cashier

Accountant

Cashier

Cashier

Cashier

1. Support expenditure incurred with original receipts and sign each receipt at the back. Return the documents together with all unused cash to the Cashier immediately on return to office.

2. Attach all the original receipts to the PCV and ensure that relevant expenditure details (Activity, expense type and source of funds) are indicated. Indicate expenditure amount on the PCV and calculate difference between advance and expenditure.

3. Verify Petty cash expenditure.

4. Where there is a balance of unused petty cash, receive it and sign the PCV. Where the Holder spends more than advanced, pay balance after the person who authorised the advance approves the extra spending. Ensure the recipient signs the PCV for the additional payment.

5. Record petty cash expenditure in the Petty Cash Book.

6. File the petty cash vouchers sequentially in a box file

1.

2.

3.

4.

5.

6.

ResponsibilityProcedure StepsProcess Flow

Accounting for Petty Cash

WSTF: PETTY CASH CONTROL

Petty Cash Holder

Cashier

Accountant

Cashier

Cashier

Cashier

1. Support expenditure incurred with original receipts and sign each receipt at the back. Return the documents together with all unused cash to the Cashier immediately on return to office.

2. Attach all the original receipts to the PCV and ensure that relevant expenditure details (Activity, expense type and source of funds) are indicated. Indicate expenditure amount on the PCV and calculate difference between advance and expenditure.

3. Verify Petty cash expenditure.

4. Where there is a balance of unused petty cash, receive it and sign the PCV. Where the Holder spends more than advanced, pay balance after the person who authorised the advance approves the extra spending. Ensure the recipient signs the PCV for the additional payment.

5. Record petty cash expenditure in the Petty Cash Book.

6. File the petty cash vouchers sequentially in a box file

1.

2.

3.

4.

5.

6.

ResponsibilityProcedure StepsProcess Flow

Accounting for Petty Cash

WSTF: PETTY CASH CONTROL

Expense receipts

Submit expense receipts

Attach expense receipts

Verify expenses

Receive cash

differences

Update petty cash book

File

File

PCV

PCV

File

PricewaterhouseCoopers Water Services Trust Fund 32 Financial Management Manual (Draft)

Cashier

Cashier

Accountant

Finance Manager

Accountant

Finance Manager

Accountant

1. Count the cash at close of business

2. Agree to petty cash book

3. Identify all the reconciling items

4. If misuse of petty cash noted then disciplinary action should be taken.

5. Where normal reconciling items pass adjusting journals

6. Review the reconciliation and sign off

7. Process the account with any adjustments and file the reconciliation together with cash count results

1.

2.

3.

4.5.

6.

7.

ResponsibilityProcedure StepsProcess Flow

Daily Cash Reconciliation

WSTF: PETTY CASH CONTROL

Cashier

Cashier

Accountant

Finance Manager

Accountant

Finance Manager

Accountant

1. Count the cash at close of business

2. Agree to petty cash book

3. Identify all the reconciling items

4. If misuse of petty cash noted then disciplinary action should be taken.

5. Where normal reconciling items pass adjusting journals

6. Review the reconciliation and sign off

7. Process the account with any adjustments and file the reconciliation together with cash count results

1.

2.

3.

4.5.

6.

7.

ResponsibilityProcedure StepsProcess Flow

Daily Cash Reconciliation

WSTF: PETTY CASH CONTROL

Count cash

Agree to petty cash book

Identify reconciling

itemsSerious?

YES

NO

Pass adjusting journal

Sign off

Process account

File

Take Action

PricewaterhouseCoopers Water Services Trust Fund 33 Financial Management Manual (Draft)

Cashier

Accountant

Finance Manager

Cashier

Cheque Signatories

Cashier

Accountant

Accountant

Accountant

1. Prepare an expenditure report, the Petty Cash Replenishment Request (PCRR) detailing total expenditure each time the balance reaches replenishment level (25% Float).

2. Prepare a Payment Voucher for replenishment of petty cash. Attach the PCRR and supporting expenditure documents, and forward to the Finance Manager.

3. Check the PCRR to the original receipts. Review the payment voucher and ensure that the reimbursement amount equals the total of the expenditure receipts. Approve the replenishment

4. Raise Cheque for Replenishment and forward to cheque signatories.

5. Sign Petty Cash replenishment Cheque.

6. Replenish the float.

7. Update the General Ledger with petty cash expenditure as follows:

Dr Expense (various)Cr. Petty Cash.

8. Update the Cash book with the float replenishment payment by:

Dr. Petty cash Cr. Bank-main cashbook

9. File vouchers in PV Number order

1.

2.

3.

4.

5.

6.

7.

8.

9.

ResponsibilityProcedure StepsProcess Flow

Replenishment of Petty Cash

WSTF: PETTY CASH CONTROL

Cashier

Accountant

Finance Manager

Cashier

Cheque Signatories

Cashier

Accountant

Accountant

Accountant

1. Prepare an expenditure report, the Petty Cash Replenishment Request (PCRR) detailing total expenditure each time the balance reaches replenishment level (25% Float).

2. Prepare a Payment Voucher for replenishment of petty cash. Attach the PCRR and supporting expenditure documents, and forward to the Finance Manager.

3. Check the PCRR to the original receipts. Review the payment voucher and ensure that the reimbursement amount equals the total of the expenditure receipts. Approve the replenishment

4. Raise Cheque for Replenishment and forward to cheque signatories.

5. Sign Petty Cash replenishment Cheque.

6. Replenish the float.

7. Update the General Ledger with petty cash expenditure as follows:

Dr Expense (various)Cr. Petty Cash.

8. Update the Cash book with the float replenishment payment by:

Dr. Petty cash Cr. Bank-main cashbook

9. File vouchers in PV Number order

1.

2.

3.

4.

5.

6.

7.

8.

9.

ResponsibilityProcedure StepsProcess Flow

Replenishment of Petty Cash

WSTF: PETTY CASH CONTROL

Prepare PCRR

PCRR

Prepare PV

PV

Review PCRR/ PV

Raise Cheque

Cheque

Sign Cheque

Replenish float

Update GL

Update CB and PCB

File

PricewaterhouseCoopers Water Services Trust Fund 34 Financial Management Manual (Draft)

8 Travel and Activity Imprests

8.1 Purpose The purpose of the imprest system is to ensure that:

• Imprest is issued for approved activities and expenditure types • Proper approval systems are adhered to in making imprests payments • Reasonable amounts are paid out as imprests • Imprest is promptly and fully accounted for with appropriate supporting documents • Travel and other activities requiring imprests are adequately planned for in advance.

8.2 Policy WSTF will pay for travel and reasonable living expenses for employees on official business in accordance with guidelines and rates set out in the Terms and Conditions of Service. These details will be elaborated in a personnel policies and procedures manual, but in summary the expenses will be claimed as detailed in the sections that follow.

8.3 In country- out of station allowance Officers travelling on duty within Kenya and away from their duty station will be paid a per diem / Daily Subsistence Allowance (a flat accommodation allowance per night) at rates guided by government circulars to be issued from time to time.

Officers travelling on duty but not spending a night away from their duty station will be eligible for lunch and dinner allowance at rates also to be guided by government circulars issued from time to time.

Fuel and other incidental vehicle running costs will be based on the official expenditure receipts.

8.4 Out of country subsistence allowance This allowance will be paid as per agreed rates determined by the WSTF Management. All out of country travel allowances will be approved by the Chairperson of WSTF or by the Vice-Chairperson in the absence of the Chairperson.

8.5 Application for travels and activities imprests The respective budget holders for approved activities will review and approve local travel and activity imprest applications. All out of country activities must also be approved by the Chairperson of WSTF or by the Vice-Chairperson in the absence of the Chairperson.

PricewaterhouseCoopers Water Services Trust Fund 35 Financial Management Manual (Draft)

The approved application shall be submitted to the Finance department at least one week (5 working days) before the date on which funds are required. Once an imprest is issued, it will immediately be posted to an interim staff imprest account of the individual taking the imprest.

8.6 Accounting for imprests

Imprests must be accounted for within 48 hours of return to office from activity in the field. No further advances will be made until previous ones are fully accounted for. An Expenditure Form will be completed in accounting for the imprest. The form is designed to facilitate analysis of the spending by activity and expenditure type, e.g. per diem, stationery, transport etc.

The imprest holder will obtain approval either from the Budget Holder or the CEO, WSTF before submitting the form to Finance Department.

Any amounts not spent will be surrendered to the Cashier when accounting for the imprest, and an official receipt issued. Similarly, officers who spend more than the amount advanced will be refunded the excess amount spent after they have accounted for the advance. The excess amount must be approved by the Department Head or CEO.

8.7 Unsurrendered imprest

Imprests that remain unaccounted for beyond the required period of return to office will be recovered from the employee’s salary in such amounts and over such period as the Finance Manager in consultation with the CEO, WSTF may consider appropriate.

8.8 Data Flow Diagram (DFD)

A diagram illustrating the sequence of processes identified above is illustrated below:

PricewaterhouseCoopers Water Services Trust Fund 36 Financial Management Manual (Draft)

Applicant

Head of Department

Head of Department

Administration

Accountant

Accountant

Accountant

1. Complete and sign an Imprest Application Form (IAF) either for travel on WSTF assignment /conferences/ meetings or to undertake activities which are included in the approved work plan and budget for the period.

2. Review the IAF to confirm activity is within our work plan and budget for the period. Also check reasonableness of rates and quantities used. Approve, if satisfied and forward the IAF to the CEO.

3. Review IAF and if satisfied, authorise travel or activity. (CEO and Chairperson of WSTF may approve out of country applications)

4. If ticket or other procurement required, observe appropriate procurement procedures. Forward documents for payment to Finance.

5. Observe payment procedures to process payments.

6. Record the advance payment in the cash book. Also update the Imprest Ledger to reflect the debit on the imprest holder’s account.

Dr. Imprest Holder (specific)Cr. Bank/Cash.

7. File Documents.

1.

2.

3.

4.

5.

6.

7.

ResponsibilityProcedure StepsProcess Flow

Travel and Activity Imprest Application

WSTF: IMPRESTS – TRAVEL AND ACTIVITY

Applicant

Head of Department

Head of Department

Administration

Accountant

Accountant

Accountant

1. Complete and sign an Imprest Application Form (IAF) either for travel on WSTF assignment /conferences/ meetings or to undertake activities which are included in the approved work plan and budget for the period.

2. Review the IAF to confirm activity is within our work plan and budget for the period. Also check reasonableness of rates and quantities used. Approve, if satisfied and forward the IAF to the CEO.

3. Review IAF and if satisfied, authorise travel or activity. (CEO and Chairperson of WSTF may approve out of country applications)

4. If ticket or other procurement required, observe appropriate procurement procedures. Forward documents for payment to Finance.

5. Observe payment procedures to process payments.

6. Record the advance payment in the cash book. Also update the Imprest Ledger to reflect the debit on the imprest holder’s account.

Dr. Imprest Holder (specific)Cr. Bank/Cash.

7. File Documents.

1.

2.

3.

4.

5.

6.

7.

ResponsibilityProcedure StepsProcess Flow

Travel and Activity Imprest Application

WSTF: IMPRESTS – TRAVEL AND ACTIVITY

Complete IAF

IAF

Review and approve

Review and sign IAF

Ticket purchase

To purchase of ticket

To payment procedures

Record imprestadvance

File

PricewaterhouseCoopers Water Services Trust Fund 37 Financial Management Manual (Draft)

Advance Holder

Head of Department

Accountant

Accountant

Accountant

Accountant

1. To account for travel/activity imprest, fill in a Personal Expenditure Form (PEF) within 14 days of returning to office, to account for the imprest. Where a flat per diem is used, show the number of nights actually spent and rate applied. For fuel and other activities attach supporting expenditure documentation and forward to the Head of Department.

2. Review expenditure report to ensure that all expenditure items are supported by valid receipts/vouchers. Approve and forward to the Finance Section.

3. If there is a difference between imprest and expenditure observe payment procedure to make additional payment and receiving procedure to record funds surrendered.

4. Ensure expenditure is assigned to the correct account codes and correctly analysed by activity codes, cost centre and financier codes.

5. Record the expenditure to debit the expense accounts and credit staff imprest account

Dr. Expense (various)Cr. Imprest Holder. Also record cash

balance paid or received Back as appropriate.

6. File documents.

1.

2.

3.

4.

5.

6.

ResponsibilityProcedure StepsProcess Flow

Accounting for Imprests

WSTF: IMPRESTS – TRAVEL AND ACTIVITY

Advance Holder

Head of Department

Accountant

Accountant

Accountant

Accountant

1. To account for travel/activity imprest, fill in a Personal Expenditure Form (PEF) within 14 days of returning to office, to account for the imprest. Where a flat per diem is used, show the number of nights actually spent and rate applied. For fuel and other activities attach supporting expenditure documentation and forward to the Head of Department.

2. Review expenditure report to ensure that all expenditure items are supported by valid receipts/vouchers. Approve and forward to the Finance Section.

3. If there is a difference between imprest and expenditure observe payment procedure to make additional payment and receiving procedure to record funds surrendered.

4. Ensure expenditure is assigned to the correct account codes and correctly analysed by activity codes, cost centre and financier codes.

5. Record the expenditure to debit the expense accounts and credit staff imprest account

Dr. Expense (various)Cr. Imprest Holder. Also record cash

balance paid or received Back as appropriate.

6. File documents.

1.

2.

3.

4.

5.

6.

ResponsibilityProcedure StepsProcess Flow

Accounting for Imprests

WSTF: IMPRESTS – TRAVEL AND ACTIVITY

Complete PEF

PEF

Review PEF

Imprest = Expense ?

YES

NOTo payment

Analyse expenditure

Record

File