Embed Size (px)

Citation preview

FINANCIAL MANAGEMENT FRAMEWORK

HANDBOOK

Authorised by: The Treasurer

Issue date: 25 June 1998

Chapter 1: About this handbook

Chapter 2: Revenue Cycle

Chapter 3: Expenditure Cycle

Chapter 4: Asset and liabilities cycle - property, plant and equipment

Chapter 5: Asset and liabilities cycle - inventory

Chapter 6: Asset and liabilities cycle - cash

Chapter 7: Asset and liabilities cycle - other assets

Chapter 8: Asset and liabilities cycle - liabilities

Chapter 9: Financial reporting

Chapter 10: Planning and analysis

Chapter 11: Human resources

Chapter 12: Control Checklist Appendix

Chapter 13: Glossary of terms

Chapter 1: About this handbook

Introduction

The Financial Management Handbook has been developed by the Department of Treasury and Finance to assist the staff of agencies with the implementation of the principles set out in the Financial Management Framework. The Financial Management Framework has been issued by the Treasurer as a contribution towards financial management improvement across the public sector. The Financial Management Framework sets out broad principles which are central to good financial management in any organisation and this handbook is intended to provide examples of the controls and procedures which can be employed by agency managers and staff who may have responsibility for ensuring that the principles set out in the framework are adhered to. The procedures set out in the handbook are not mandatory, nor are they exhaustive. They are intended to provide a reference which can be used when developing internal policies or when assessing the adequacy of existing controls and practices. Each agency will need to assess the applicability of the suggested procedures or controls given its own unique environment, and to adapt and supplement the material in the handbook to ensure its relevance. Structure of the chapters

The structure of this document is based on the functions of financial management as per the Financial Management Framework (FMF) and includes a typical agency's accounting cycles:

• Revenue Cycle; • Expenditure Cycle; • Asset and Liability Cycle;

o property, plant and equipment o inventory o cash o other assets o liabilities

• Financial Reporting; • Planning and Analysis; • Human Resources; and • Control Checklists

Structure of the procedures

The procedures are generally control based, however the accounting cycles (ie Revenue, Expenditure and Asset and Liability Cycles) include both accounting and period and year end procedures. The procedures have been prepared in accordance with fundamental principles in financial management and suggested best practices referred to in the Financial Management Framework. The procedures are not exhaustive, nor will they be applicable to all agencies. However they will assist Chief Executives in developing systems, processes and procedures in their agencies. As discussed previously the development of agency procedures will need to be tailored to reflect the special characteristics of each agency. As the focus of this handbook is largely on generic type procedures, further emphasis is required by agencies in addressing many of the requirements which are unique to each agency's own environment. To best achieve this, agencies will need to refer to the FMF, which clearly sets out the fundamental principles and key performance objectives of all the related finance functions. These principles are extremely useful in ensuring that all procedures are developed in the most efficient and effective manner. Included in this document are examples of accounting entries, including a flowchart and a commentary on each entry, as well as a checklist for Chief Executives to assess the adequacy of the establishment and maintenance of control procedures. The checklist is not exhaustive and is merely intended to provide agencies with guidance in assessing internal controls. Chief Executives may choose to apply other processes to assess the adequacy of internal control, however those that choose to adopt the approach in this document will need to tailor its contents to reflect the circumstances of their operation.

Chapter 2: Revenue Cycle

Overview of revenue cycle

The revenue generated by an agency must be effectively managed, accurately recorded and the transactions efficiently processed to ensure revenue is maximised and non collections minimised. The following procedures which support the prescribed elements in the Financial Management Framework represent some effective management practices that, if properly implemented, will assist in minimising the risk of error or fraud. Further procedures on Cash Management are covered in Chapter 6: Asset and liabilities cycle - cash. Accounting based procedures for revenue cycle

The following accounting based procedures will ensure revenue transactions are accurately recorded and processed on a timely basis. See examples of accounting entries, flowcharts and commentary provided for each type of revenue in the section Accounting entries for revenue. A checklist is available in Chapter 12: Control Checklist Appendix.

Revenues from goods and services

1. Revenue arising from the provision of goods and services should be recognised when:

o an agreement exists with one or more external entities supporting the provision of goods; and

o all acts of performance necessary to establish a valid claim against the external parties have been completed.

2. Revenue from the sale of goods and services should be recorded at the time the goods and services are provided to the customer. In the case of a cash sale, the revenue should be recognised immediately.

3. Revenue is to be recognised at the time the amounts are earned ( gains control), not when the amounts are received. However, due to the uncertainty of amounts to be received, some revenue items will be recorded on a cash basis. These include amounts received for items such as licence and accreditation fees, fines and penalties.

4. At the time the goods and services are provided any cash received should be recorded in the cashbook (or equivalent) and in the general ledger as revenue.

At the same time an invoice should be raised and any amounts owing to the agency should be recorded in the debtor's sub-ledger and the general ledger as revenue. The subsequent cash receipt should be recorded against accounts receivable in the cashbook and the debtor's sub-ledger.

Revenue from licence and accreditation fees

Revenue received for licence and accreditation fees, where the period of accreditation is greater than 1 reporting period, should be recognised in their entirety in the reporting period when the agency gains control of the revenue. Revenue from appropriations

All revenue received from Recurrent and Capital Appropriations should be accounted for when agencies gain control of the amounts appropriated for its use. This usually occurs when amounts have been received. Revenue from doubtful debts

A provision for doubtful debts should be raised against a receivable as soon as the agency becomes aware that its recovery is doubtful. This should be done after careful analysis of the aged debtor listing, or upon information received (for example, details from an accounting firm advising that a debtor is in liquidation). Accounting entries for revenue

Accounting entries for sale of goods and materials

Primary entries for sale of goods and materials

Entry and description Account category

Movement

PAE1 DR—Bank Deposit Account Asset Increase CR—Revenue - Sale of Goods (To record any cash received at the time of sale.)

Revenue Increase

PAE2 DR—Accounts Receivable - General Asset Increase CR—Revenue - Sale of Goods (To record amount owing to the Agency for

Revenue Increase

the goods provided.)

Secondary entries for sale of goods and materials

Entry and description Account category

Movement

SAE1 DR—Bank - Deposit Account Asset Increase CR—Accounts Receivable - General (To record subsequent receipts.)

Asset Decrease

Commentary on sale of goods and materials As noted in the procedures, revenue should be recognised, accounts receivable recognised and customers billed (ie. invoices) as soon as practicable after goods and services have been provided. Where services are provided over a period of time it is recommended that progress bills are raised to reflect that portion of revenue earned to date, rather than billing upon completion. This amounts to good debtor management and an overall better control over the agency's Cash Management Practice. For more information refer to the flowchart Revenues - Sales of Goods and Materials. Fees for service income

Primary entries for fees for service income

Entry and description Account category

Movement

PAE1 DR—Accounts receivable - General Asset Increase CR—Revenue - Fees for service (To recognise revenue once the services have been provided, normally upon invoice.)

Revenue Increase

PAE2 DR—Bank - Deposit Account Asset Increase CR—Deferred Revenue (To recognise moneys received in advance for services which have not yet been provided.)

Liability Increase

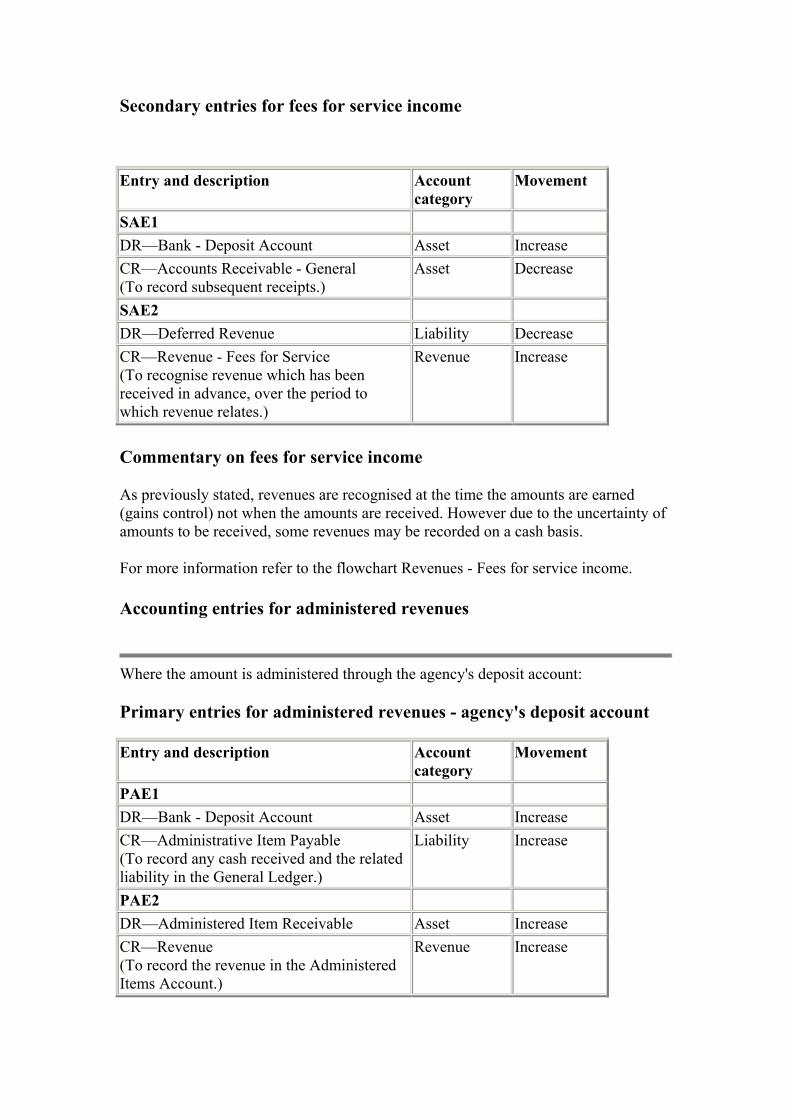

Secondary entries for fees for service income

Entry and description Account category

Movement

SAE1 DR—Bank - Deposit Account Asset Increase CR—Accounts Receivable - General (To record subsequent receipts.)

Asset Decrease

SAE2 DR—Deferred Revenue Liability Decrease CR—Revenue - Fees for Service (To recognise revenue which has been received in advance, over the period to which revenue relates.)

Revenue Increase

Commentary on fees for service income As previously stated, revenues are recognised at the time the amounts are earned (gains control) not when the amounts are received. However due to the uncertainty of amounts to be received, some revenues may be recorded on a cash basis. For more information refer to the flowchart Revenues - Fees for service income. Accounting entries for administered revenues

Where the amount is administered through the agency's deposit account: Primary entries for administered revenues - agency's deposit account

Entry and description Account category

Movement

PAE1 DR—Bank - Deposit Account Asset Increase CR—Administrative Item Payable (To record any cash received and the related liability in the General Ledger.)

Liability Increase

PAE2 DR—Administered Item Receivable Asset Increase CR—Revenue (To record the revenue in the Administered Items Account.)

Revenue Increase

Where the amount is paid directly into the Consolidated Account: Primary entries for administered revenues - Consolidated Account

Entry and description Account category

Movement

PAE1 DR—Consolidated Account Revenue Offset Revenue Decrease CR—Revenue (To record any cash received and the negative revenue offset in the Administered Items Account.)

Revenue Increase

Where the amount is paid into a specific administered deposit account: Primary entries for administered revenues - specific administered deposit account

Entry and description Account category

Movement

PAE1 DR—Cash Asset Increase CR—Revenue (To record any cash received and the related revenue in the Administered Items Account.)

Revenue Increase

Commentary on administered revenues Administered revenue arises from responsibilities or activities undertaken by agencies which are not attributable to the agency. This revenue may be credited direct to a separate Treasury line (eg. revenue for the sale of Crown Land and property, fines and penalties and private plated vehicle contributions) or credited to the agencies' own Deposit Account for eventual payment to the relevant party/parties. Agencies do not have control over administered revenue and merely act as a collection agency for Treasury or as an intermediary between recipients and the relevant government appropriators/agencies. Information about administered items is relevant to an assessment of each agency's performance. Normally administered expenses will be separated in the general ledger by the use of unique objects and/or the use of separate business/cost centres. This separation enables easier reporting of administered activities both on a monthly and yearly basis.

Accounting entries for appropriations

Primary entries for appropriations

Entry and description Account category

Movement

PAE1 DR—Bank - Deposit Account Asset Increase CR—Capital Appropriations (To record Treasury funding relating to capital items.)

Revenue Increase

PAE2 DR—Bank - Deposit Account Asset Increase CR—Recurrent Appropriations (To record Treasury funding relating to recurrent items.)

Revenue Increase

Commentary on appropriations Recurrent and capital appropriations will be recorded on a cash basis only as this is when agencies gain control of the funds. The differentiation between Capital and Recurrent Appropriations is based on the source of funding and does not necessarily indicate how the funds will be recorded by each agency. For instance Capital Appropriations may include an amount in respect of maintenance on capital items, which would in fact be expensed and included in the Operating Statement. Capital Appropriations that are used to purchase Capital items (eg Land and Buildings, Plant and Equipment) would be included in the Statement of Financial Position as an asset. Accounting entries for donations and grants

Primary entries for donations and grants

Entry and description Account category

Movement

PAE1 DR—Bank - Deposit Account Asset Increase CR—Revenue - Donations & Industry Contributions (To record the contribution of monetary resources.)

Revenue Increase

PAE2 DR—Property, Plant & Equipment Asset Increase

CR—Revenue - Donations & Industry Contributions (To record the contribution of non monetary resources such as property, plant and equipment, for instance.)

Revenue Increase

PAE3 DR—Operating Expenses Expense Increase CR—Revenue - Donations & Industry Contributions (To record the contribution of non monetary resources such as donated goods and services, for instance.)

Revenue Increase

Commentary on donations and grants Donations and grants are non reciprocal in the sense that the transferor and transferee do not directly sacrifice and receive approximately equal value. Donors may impose restrictions in respect of the manner or timing of the agency to use the contributed assets effectively, however this restriction does not of itself create a present obligation to make a reciprocal transfer of economic benefits. Grants can also be received with restrictions on the purpose for which it may be used. This is particularly evident with the many grants received from the Commonwealth Government. It could be argued that whilst the purpose for which it was received remains undischarged, a liability exists. The grant is not classified as a liability as it does not give the grantor a right to directly receive benefits from the grantee and hence does not have a present obligation to make future sacrifice of economic benefits to the grantor. Donations, industry contributions and grants from other agencies include grants in the form of donations, prize funds, bequests, gifts and the provisions of free services (only recognised if the agency would have purchased the service if it had not been donated). Donations may include non-monetary items such as property , plant and equipment. Non-monetary contributions are to be recorded at their 'fair value'. Fair Value is to be interpreted as the amount for which an asset could be exchanged between a knowledgeable willing buyer and a knowledgeable willing seller in an arm's length exchange. In practice, the non monetary contributions would be valued based on current market rates ie. what the agency would have to pay had the donation not been made. Further details on grants and donations are contained in Accounting Policy Statement No. 11, Contributions. This policy statement also details the required disclosure requirements

Accounting entries for accounts receivable doubtful debt provisions

Primary entries for accounts receivable doubtful debt provisions

Entry and description Account category

Movement

PAE1 DR—Doubtful Debts Expense Expense Increase CR—provision for Doubtful Debts (To recognise amounts against receivables to reflect the portion which the agency may not recover.)

Asset Offset Increase

PAE2 DR—provision for Doubtful Debts Asset Offset Decrease CR—Accounts Receivable - General (To write off amount recorded as owing to the agency for goods provided.)

Asset Decrease

PAE3 DR—Doubtful Debts Expense Expense Increase CR—Provision for Doubtful Debts (To revise the provision for doubtful debts to reflect the portion which the agency may not recover following the write off of a debt which was previously included in the provision.)

Asset Offset Increase

Secondary entries for accounts receivable doubtful debt provisions

Entry and description Account category

Movement

SAE1 DR—Accounts Receivable - General Asset Increase CR—Revenue (To recognise revenue once the services have been provided, normally upon invoice)

Revenue Increase

Commentary on accounts receivable doubtful debt provisions A provision for doubtful debts should be raised against a receivable as soon as the agency becomes aware that its recovery is doubtful. This occurs after the lapse of time, careful analysis of the aged debtors listing, or upon information received (for example details from an accounting firm advising a debtor is in liquidation).

Once a debt which had earlier been provided against becomes clearly irrecoverable, it is written off against the statement of financial position provision and not recorded as an expense in the operating statement. The doubtful debt provision may then require adjustment to reflect the portion of receivables which agencies estimate may not be recovered. Agency specific procedures need to be established to ensure debts are written off with appropriate approval by management. There is a degree of judgment required to determine when a provision should be raised against a receivable and later, when that receivable should be written off. When calculating a provision, agencies should take account of all the available evidence about the condition of its receivables. Some examples are:

• historical trend of debt write-offs; • aged profile of receivables at the end of the accounting period; • the repayment history of the individual borrowers; • the borrowers' financial position; • information which is available in the public domain eg. media stories/reports,

analyst reports, etc; • analysis of the geographical location; • analysis of the class of customers; and • analysis of the specific cost centres which originally raised the invoice.

The monitoring of debtors in determining which are likely to be classified as doubtful needs to be performed continuously throughout the financial year and not only considered as an end of financial year activity. Effective credit control over debtors by management ensures that debtors pay their accounts in full and on time. If effective credit control exists, then the likelihood of bad debts diminishes. For more information refer to the flowchart Revenues - Fees for service income. Control based procedures for revenue

The control based procedures minimise the risk of error or fraud and therefore ensure the effective management of revenue. See the checklist in Chapter 12: Control Checklist Appendix. Accounts Receivable

Only orders for accounts receivable that qualify for goods and services under policy guidelines should be processed. The accounts receivable authorisation systems should therefore provide accurate and timely information regarding approved credit limits, current balances due, and aged balances of receivables. Purchase orders should be accurately and expeditiously processed by:

• Prenumbering order forms and periodically following up on those not processed within a reasonable timeframe.

• Accounts receivable order information being verified with appropriate customer service representatives.

To ensure all goods and services are accurately billed in the proper period:

• Standard contract terms should be used and non standard contract terms should be communicated to the accounts receivable section.

• Goods and services should be identified in the correct reporting period by means of a prenumbered and properly dated document.

• The date of the physical performance of services or delivery of goods should be checked against the invoice date.

To ensure invoices for all authorised supply of services are accurately recorded:

• Service or dispatch documents and sales invoices should be prenumbered and accounted for.

• Delivery information should be matched with invoice details. • Accounts receivable invoices or statements should be periodically mailed and

any disputes or inquiries investigated by individuals independent of the invoicing function.

• The number of debtor complaints regarding improper invoices or statements should be monitored.

To ensure proper control over moneys received:

• Ensure security over mail collection, cashiering, terminal access, handover arrangements and cash in transit.

• Two officers should be involved in the opening of mail, with all cash received being recorded in a cashbook in each person's presence.

• Ensure immediate stamping of all cheques received with "not negotiable". • Maintain a post dated cheque register. • Establish a policy against encashment of cheques or giving 'change' on

cheques received. • Bank moneys received promptly. • Reconcile banking amounts with agency records.

Authorisations

To ensure authorised credits and only such credits are accurately recorded:

• Credit memos should be authorised by individuals independent of the accounts receivable function.

• All correspondence authorising credits should be reviewed for proper authorisation and all credit memos prenumbered and accounted for.

Customers

In order to handle customer inquiries expeditiously and efficiently:

• Accurate and timely information should be provided to customers upon request.

• Staff should be provided with initial and periodic customer service training and training on agency services available.

• Customer service representatives should receive training and guidance to understand the agency's objectives, obligations to the community, and the requirements of individual customers.

All arrangements for the provision of credit (other than by way of credit cards) by agencies to purchasers of goods and services should be authorised and should only be provided to credit worthy customers. This can be done by:

• Establishing and maintaining adequate procedures for pursuing unpaid demands for payment.

• The use of credit limits and credit reference checks. • The maintenance of a bad debtors' database. • The effective management of the use of progress payments.

Segregation of duties for revenue

Where practicable the following functions within the revenue cycle should be segregated:

• provision of goods and services; • invoicing; and • cash processing, debtors and general ledger.

Where practicable the following tasks should be segregated:

• cash collection and deposit preparation; • recording of cash receipts; • general ledger inquiries; and • bank reconciliation approval.

Access restrictions

Managers should ensure that there are adequate physical controls over access to computer equipment, such as by locking terminal room doors, and also controls within programs, such as user passwords which require a specified level of user authorisation for each application. Document controls

Where applicable the following documents should be received, approved and processed with controls to ensure that the revenue details are consistent throughout:

• orders; • shipping dockets/notifications of services provided; • invoices; • remittances; and • cheques received.

Data entry and processing

Processing controls such as batch totals, programmed balancing controls, data transmission controls, and cut-off controls should be in place. Controls over the operation of the system, for instance proper period end cut-off procedures, must be communicated throughout all levels of the agency. Edit and validation checks should be incorporated into systems programs to facilitate the identification and correction of data entered which does not meet pre-determined criteria. Management review

The various components of the Revenue Cycle should be reviewed by management to substantiate the receipt of all revenue. This can be achieved by:

• Comparing actual results on revenue and debtor balances to budgeted amounts and investigating any significant variance.

• Analysing reports on such areas as revenues and associated costs by division, outstanding debtors, credit notes issued, as well as any individually significant revenues or debtor balances.

• Investigating any unusual reconciling items between the debtor's subledger and the general ledger control account.

• Ensuring that the determination of the revenue amounts were adequately authorised by an appropriate person.

Period and year end requirements for revenue

• This covers the period and year end requirements for debtors, any adjustments and reports.

Debtors sub-ledger for revenue

The sub-ledger should be reconciled to the general ledger at period end. Any reconciling amounts should be investigated and corrected.

Debtors accrual for revenue

Where an accounting department cannot process all the revenue amounts for a certain financial period an accrual should be recorded in the debtors control account and the appropriate revenue account. This entry should then be reversed in the following financial period. Period end adjustments for revenue

Any adjustments that are necessary should be made at the end of a financial period in respect of revenue and debtors. These may include:

• Recording any revenues identified during the reconciliation of the bank, including any adjustment for dishonoured cheques.

• Adjusting the provision for doubtful debts to reflect current debtor balances and collection trends.

Period and end year reporting for revenue

Reports generated by the Revenue Cycle should include:

• financial and non financial reports; • sales-related and cash related reports; and • daily, weekly and monthly reports.

Specifically some of these key reports include:

• Monthly statement of outstanding sales invoices for a customer. • Open order reports listing those sales orders that are not completely shipped

and billed. • Accounts receivable ageing schedule identifying overdue amounts by time

period and those accounts that are urgently in need of collection.

A detailed analysis of the age and size of current debtor balances should be performed at the end of each financial year. Overdue balances should be reviewed to determine its probability of collection.

Chapter 3: Expenditure Cycle

Overview of expenditure cycle

The expenditure incurred by an agency must be effectively managed, accurately recorded and the transactions efficiently processed. The agency's Chief Executive must ensure this occurs through the appropriate delegation of responsibility for expenditure transactions to accountable officers. The following procedures which support the prescribed elements in the Financial Management Framework, represent some effective management practices that if properly implemented will assist in the minimisation of risk of error or fraud. Accounting based procedures for expenditure

The following procedures will ensure that purchases of goods and services are accurately accounted for. See examples of accounting entries, flowcharts and commentary provided for each type of expenditure in the section Accounting entries for expenditure. A checklist is available in Chapter 12: Control Checklist Appendix.

Non employee expenses and creditors, and goods and services

Upon receipt of an invoice for goods which have been received or services which have been provided, an expense should be recorded in the general ledger and a liability in the creditors sub-ledger. Expenses should be recognised at the time goods are delivered or when services are provided. All goods purchased below the value of an agencies capitalisation threshold should be expensed at the time of purchase. (Agencies should refer to the Accounting Policy Statements for details on the current capitalisation threshold used for whole of Government reporting). Administered expenses

Administered expenses should be recorded separately. These expenses should not be shown in the Operating Statement, but instead disclosed in a Statement of Administered Items and should be maintained separately on the general ledger.

Trust expenses

Trusts (including statutory funds or other entities) controlled by agencies should be included with other controlled expenses. Trusts administered by agencies which it does not control but are controlled by the SA Government are to be included with other administered items. Trusts administered by agencies which are not controlled by either the agency or the SA Government must only be disclosed as a note to the financial statements. Trust expenses should be recognised at the time when goods or services are provided. However some trust expenses may take the form of a court judgment or claim for payment. In this instance the expense will be recognised in the financial period in which the payment is made. Operating lease expenditure

Expenses associated with operating leases should be recorded as they fall due. Employee expenses

To ensure employee expenses are properly recorded employee expenses should be recorded in the period in which they accrue. To properly record employee entitlements all employee entitlements should be recorded in the period in which the employees have earned them. Leave and other employee entitlements

Accurate provisions for employee entitlements should be recognised as liabilities in the Statement of Financial Position.

Accounting entries for expenditure

Accounting entries for non employee expenses and creditors, and goods and services

Primary entries for non employee expenses and creditors, and goods and services

Entry and description Account category

Movement

PAE1 DR—Operating Expenses Expense Increase CR—Creditors - General (To record the acquisition of goods and/or services.)

Liability Increase

Secondary entries for non employee expenses and creditors, and goods and services

Entry and description Account category

Movement

SAE1 DR— Liability Decrease CR—Bank - Deposit Account (To record subsequent payments made.)

Asset Decrease

SAE2 DR—Operating Expenses Expense Increase CR—Creditors - Accrual (To accrue for goods and/or services provided in the accounting period but which have not been recorded.)

Liability Increase

SAE3 DR—Creditors - Accrual Liability Decrease CR—Operating Expenses (To reverse the accrual of goods and/or services provided in the previous accounting period.)

Expense Decrease

Accounting entries PAE1 and SAE1 are processed when the actual invoice is processed for the goods and/or services previously accrued. The net result is an expense being recorded in the period in which the goods and/or services were

provided to the agency. The credit to Operating Expenses from SAE3 nets off with the debit to Operating Expenses from PAE1. Commentary on non employee expenses and creditors, and goods and services The purchase of goods includes for example computer related items, supplies of plant equipment, furniture and fittings. All purchased goods below each agency's capitalisation threshold should be expensed. Further details on capitalisation thresholds, including aggregate and network assets is contained in the Asset and Liability Cycle of this Handbook. The acquisition of services includes for example, travel, transportation, property leasing, utilities and many general operating expenses such as advertising. The acquisition of services differs from that of goods because a purchase order is often not prepared for services, nor is there a delivery docket. Alternative documentation is often required. It is important that correct objects are used in classifying the operating expenses. This will assist in managers receiving meaningful reports accurately detailing account code allocations. For more information refer to the flowchart Non Employee Expenses - Purchase Goods and/or Services. Accounting entries for operating lease expenditure

Primary entries for operating lease expenditure

Entry and description Account category

Movement

PAE1 DR—Operating Lease Expenditure Expense Increase CR—Creditors - General (To record periodic operating lease expenditure incurred.)

Liability Increase

Secondary entries for operating lease expenditure

Entry and description Account category

Movement

SAE1 DR—Creditors - General Liability Decrease CR—Bank - Deposit Account Asset Decrease

Commentary on operating lease expenditure Where the effect of the lease is not to gain effective ownership control of an asset but merely to obtain the use of an asset for less than its life, an operating lease exists. A finance lease on the other hand is based on the understanding that the lessee will make periodic lease payments with the aim of controlling the asset for a substantial majority of the assets useful life. This changes the substance of the lease from a rental agreement to a purchase. In these cases the appropriate accounting treatment would be to capitalise the entire cost of the lease as an asset and the capital amount repayable as a liability in accordance with the provisions of AAS 17, Accounting for Leases. The treatment of finance leases is dealt with specifically in Finance leases in Chapter 7: Asset and liabilities cycle - other assets. For more information refer to the flowchart Non Employee Expenses - Operating Lease Expenditure. Accounting entries for administered expenses

Primary entries for administered expenses paid through the agency's deposit account

Entry and description Account category

Movement

PAE1 DR—Administered Item payable Liability Decrease CR—Bank - Deposit Account (To record any cash paid and the related reduction in liabilities in the General Ledger.)

Asset Decrease

PAE2 DR—Expense Expense Increase CR—Administered Item Receivable (To record an expense in the Administered Items Account.)

Asset Decrease

Primary entries for administered expenses paid from the Consolidated Account for Special Acts or Ministerial Other payments

Entry and description Account category

Movement

PAE1 DR—Expense Expense Increase

CR—Appropriation (To record appropriation received and an expense in the Administered Items Account.)

Revenue Increase

Primary entries for administered expenses paid from a specific administered deposit account

Entry and description Account category

Movement

PAE1 DR—Expense Revenue Increase CR—Cash (To record cash paid and the related expense in the Administered Items Account.)

Asset Decrease

Commentary on administered expenses Administered expenses arise from responsibilities or activities undertaken by agencies which are not attributable to the agency. These expenses may be paid via a separate Treasury line (eg. certain salaries and expenses) or from the agency's Deposit Account. In certain circumstances, agencies initially receive the funds (administered revenue) prior to the eventual payment to the relevant party/parties. Administered expenses may also include refunds of amounts which were previously recorded as administered revenue. Information about administered items is relevant to an assessment of the agency's performance. Normally administered expenses will be separated in the general ledger by the use of unique objects and/or the use of separate business/cost centres. This separation enables easier reporting of administered activities both on a monthly and yearly basis. Where administered items include amounts paid from Consolidated Account for Special Acts or Ministerial Other payments, the payment timing will exactly match the timing of appropriation for that payment and both should be recorded simultaneously. Accounting entries for trust expenses

The accounting entries are identical to that of other non-employee expenses except the trust expense accounts used will probably be a unique object pertaining to the trust activity of the agency. Commentary on trust expenses Trust expenses arise from funds which agencies hold in the capacity as trustee.

Depending on who controls the funds governs where the expenses will be recorded. Beneficiaries of trusts include other government agencies, Treasury and Finance, individuals who may have suffered pecuniary loss, and other individuals who have a valid claim against the Trust. Normally trust expenses will be separated in the general ledger by the use of unique objects and/or the use of separate business/cost centres. This separation allows for easier reporting of trust activities both on a monthly and yearly basis. For more information refer to the flowchart Payments - On Account. Accounting entries for Employee related expenses - salaries and wages

Primary entries for employee related expenses - salaries and wages

Entry and description Account category

Movement

PAE1 DR—Salaries and Wages Expense Expense Increase CR—Creditors - Government Entities & Other

Liability Increase

CR—Bank - Deposit Account (To record the salary and wages expense corresponding to a pay period. The creditor amount includes withholding for employee contributed superannuation, tax and other miscellaneous deductions which are to be remitted at a later date.) NB. Some Agencies may use employee related clearing accounts instead of the Creditors account.

Asset Decrease

PAE2 DR—Payroll Tax Expense Expense Increase DR—Employer Contributed Superannuation Expense Increase DR—Other Employee On-Costs Expense Increase CR—Creditors - Government Entities & Other

Liability Increase

CR—Bank - Deposit Account (To record employee on-costs and employer contributed superannuation corresponding to a pay period. The creditor amounts are to be remitted at a later date.)

Asset Decrease

Secondary entries for employee related expenses - salaries and wages

Entry and description Account category

Movement

SAE1 DR—Creditors - Government Entities & Other

Liability Decrease

CR—Bank - Deposit Account (To record subsequent remittances for deductions withheld at the end of the pay period, for instance employee contributed superannuation.)

Asset Decrease

If an agency uses employee related clearing accounts instead of the Creditors account, then the debit as shown in SAE1 will clear the balance owing in the clearing account to the creditor.

Entry and description Account category

Movement

SAE2 DR—Salaries and Wages Expense Expense Increase CR—Accrued Salaries and Wages (To accrue for salaries and wages unpaid at the end of a financial period.)

Liability Increase

SAE3 DR—Accrued Salaries and Wages Liability Decrease CR—Salaries and Wages Expense (To reverse the accrual of wages and salaries from the previous accounting period.)

Expense Decrease

Accounting entry PAE1 is processed from the relevant payroll system (eg. Concept) which will then overlap the period in which the accrued entry was made for wages and salaries. The net result is an expense being recorded in the period in which the employee provided service to the agency. The credit to Salaries and Wages from SAE3 will not totally net off with the debit to Salaries and Wages from PAE1. Commentary on employee related expenses - salaries and wages Salaries and wages may also include for example commissions, performance bonuses, living away from home allowances, overtime, penalties, termination pay, and accrued salaries and wages. For more information refer to the flowchart Employee Related Expenses - Salaries and Wages.

Accounting entries for annual leave

Primary entries for annual leave

Entry and description Account category

Movement

PAE1 DR—Salaries and Wages Expense Expense Increase CR—Bank - Deposit Account (To record annual leave taken during service and paid that period.)

Asset Decrease

In some agency's owing to the quality of their payroll system, an entry may be made directly to annual leave expense account based on their pro rata entitlement and then paid out of employee provisions once it is taken.

Entry and description Account category

Movement

PAE2 DR—Annual Leave Expense Expense Increase CR—Salaries and Wages Expense (To record at the end of each financial period, the transfer from payroll system to the general ledger, the amount of annual leave paid during service.)

Expense Decrease

PAE3 DR—Annual Leave Expense Expense Increase CR—Bank - Deposit Account (To record the payment of annual leave on termination.)

Asset Decrease

PAE4 DR—Annual Leave Expense Expense Increase CR—Annual Leave Provision (To adjust the accrual for annual leave owing at the end of the financial year (this provision should not be reversed in the following financial year.)

Liability Increase

Commentary on annual leave For most agency's, annual leave is initially charged to salaries and wages expense because it is paid through the normal payroll system and is not separately identifiable due to the quality of existing ledger systems. When an employee takes leave, Entry

PAE1 would be included in the normal salaries and wages entry Employee Related Expense - Salaries. Annual Leave paid on termination would be recorded separately from the normal payroll entries. Because the amount of annual leave paid in a financial year is required to be separately disclosed in the notes to the financial statements, it will be necessary to determine and reclassify the amount of annual paid leave entitlement which has been included in the year's salaries and wages expense. This reclassification should normally be done at the end of each financial period. Employment on-costs relating to the annual leave provision are also raised at the end of the reporting period. Further details relating to annual leave are contained in Accounting Policy Statement No. 9, Employee Entitlements and AAS 30, Accounting for Employee Entitlements. For more information refer to the flowchart Employee Related Expenses - Annual Leave. Accounting entries for sick leave

Non vesting sick leave is charged as part of the salaries and wages expense (refer Employee Related Expenses - salaries and wages) when it is paid. Provided that sick leave taken in future periods is not greater than the benefits accrued, no further accounting treatment or reclassification is required. Primary entries for sick leave – vesting

Entry and description Account category

Movement

PAE1 DR—Salaries and Wages Expense Expense Increase CR—Bank - Deposit Account (To record sick leave taken during service and paid that period.)

Asset Decrease

PAE2 DR—Sick Leave Expense (Vesting) Expense Increase CR—Salaries and Wages Expense (To record at the end of each financial period, the transfer from payroll system to the general ledger, the amount of sick leave paid during service.)

Expense Decrease

PAE3 DR—Sick Leave Expense (Vesting) Expense Increase CR—Bank - Deposit Account (To record the payment of sick leave on termination.)

Asset Decrease

PAE4 DR—Sick Leave Expense (Vesting) Expense Increase CR—Sick Leave Expense (Vesting) (To adjust the accrual for vesting sick leave provision at the end of the financial year.)

Expense Increase

Commentary on sick leave The key consideration in determining the liability for sick leave at reporting date is whether the sick leave is vesting or non-vesting. Most SA Government employees are subject to non vesting sick leave entitlements. In simple terms, the accounting treatment is such that where, on average, non-vesting sick leave taken is less than total entitlement then there is no liability. In order to calculate this liability for non-vesting sick leave, Agencies should produce reports each financial year from the relevant human resources system detailing sick leave taken for the current financial year, together with sick leave accrued for the financial year. This report could also be used by management for agency best practice comparisons regarding the percentage of sick leave taken versus sick leave accrued. Further details relating to sick leave are contained Accounting Policy Statement No. 9, Employee Entitlements and AAS 30, Accounting for Employee Entitlements. Accounting entries for long service leave

Primary entries for long service leave

Entry and description Account category

Movement

PAE1 DR—Salaries and Wages Expense Expense Increase CR—Bank - Deposit Account (To record long service leave (LSL) taken during service and paid in that period.)

Asset Decrease

Where the payroll systems permit, an entry shall be made directly to LSL expense account based on their pro rata entitlement, and a debit is raised against the provision once it is taken.

Entry and description Account category

Movement

PAE2 DR—Long Service Leave Expense Expense Increase CR—Salaries and Wages Expense (To record at the end of each financial period, the transfer from payroll system to

Expense Decrease

the general ledger, the amount of LSL paid during service.) PAE3 DR—Long Service Leave Expense Expense Increase CR—Bank - Deposit Account (To record the payment of LSL on termination.)

Asset Decrease

PAE4 DR—Long Service Leave Expense Expense Increase CR—Long Service Leave Provision (To adjust the accrual for long service leave owing at the end of the financial year (this provision should not be reversed in the following financial year.)

Liability Increase

Commentary on long service leave Employees accrue long service leave on an annual basis after the completion of ten years effective service by the Government, however pro-rata leave can be taken after seven years. This long service leave may either be taken during service, or paid out on termination. Any leave taken is to be taken into account. Each agency will recognise an expense for the financial year equal to the movement in the liability for long service leave throughout the period, adjusted for leave taken/paid, and transfers of employees to/from the agency. To simplify the estimation of long service leave liability for each agency, each agency should take into account, as a benchmark, an actuarial assessment prepared by the Department of Treasury and Finance based on a significant sample of employees throughout the South Australian public sector. This benchmark is the number of years of service which produces a value equal to the actuarially calculated net present value. The liability for long service leave is calculated by multiplying the pro-rata entitlement for each employee whose service years exceed the benchmark by the remuneration rate current at the reporting date. Each agency should review the benchmark annually to ensure an adequate reflection of its long service leave liability is maintained. It should also have the Auditor General confirm its appropriateness prior to adoption. Employment on-costs relating to the long service leave provision are also raised at the end of the reporting period. Further details relating to long service leave are contained in Accounting Policy Statement No. 9, Employee Entitlements and AAS 30, Accounting for Employee Entitlements. For more information refer to the flowchart Employee Related Expenses - Long Service Leave.

Accounting entries for superannuation

Primary entries for superannuation

Entry and description Account category

Movement

PAE1 DR—Superannuation Expense Expense Increase CR—Unfunded Super Revenue (Treasury to record the amount of expense and unfunded revenue relating to superannuation. This entry is a Treasury responsibility and is not to be undertaken by the Agency.)

Liability Increase

PAE2 DR—Salaries and Wages Expense Expense Increase DR—Superannuation Expense Expense Increase CR—Superannuation Clearing Liability Increase CR—Bank - Deposit Account (To record salary and wages and the employer contributed superannuation corresponding to a pay period.)

Asset Decrease

Secondary entries for superannuation

Entry and description Account category

Movement

SAE1 DR—Superannuation Clearing Liability Decrease CR—Bank - Deposit Account (To record subsequent employer contributed superannuation remittances.)

Asset Decrease

Commentary on superannuation All SA Government employees are covered by some forms of superannuation scheme operated by the Government, statutory authorities or other public sector organisations. These schemes include member and employer contributions to voluntary schemes and employer contributions to the State Superannuation Benefits Scheme, in lieu of Commonwealth mandated Superannuation Guarantee arrangement, for employees who are not members of the voluntary schemes. For more information refer to the flowchart Employee Related Expenses - Superannuation.

Accounting entries for employee related liabilities, salaries and wages

Primary entries for employee related liabilities, salaries and wages

Entry and description Account category

Movement

PAE1 DR—Salaries and Wages Expense Expense Increase CR—Accrued Salaries and Wages (To accrue for salaries and wages unpaid at the end of the financial period. This entry should be reversed in the following period.)

Liability Increase

Secondary entries for employee related liabilities, salaries and wages

Entry and description Account category

Movement

SAE1 DR—Salaries and Wages Expense Expense Increase CR—Creditors Liability Increase CR—Bank - Deposit Account (To record salary and wages corresponding to a pay period. The creditor amount includes withholding for superannuation, tax and other miscellaneous deductions which are to be remitted at a later date.)

Asset Decrease

SAE2 DR—Salaries and Wages Expense Expense Increase CR—Creditors - Government Entities (To record as on-costs an agency's contributions owing in respect of its employees.)

Liability Increase

SAE3 DR—Creditors - Government Entities Liability Decrease CR—Bank - Deposit Account (To record subsequent remittances of amounts withheld and/or on-costs.)

Asset Decrease

For more information refer to the flowchart Employee Related Liabilities - Salaries and Wages.

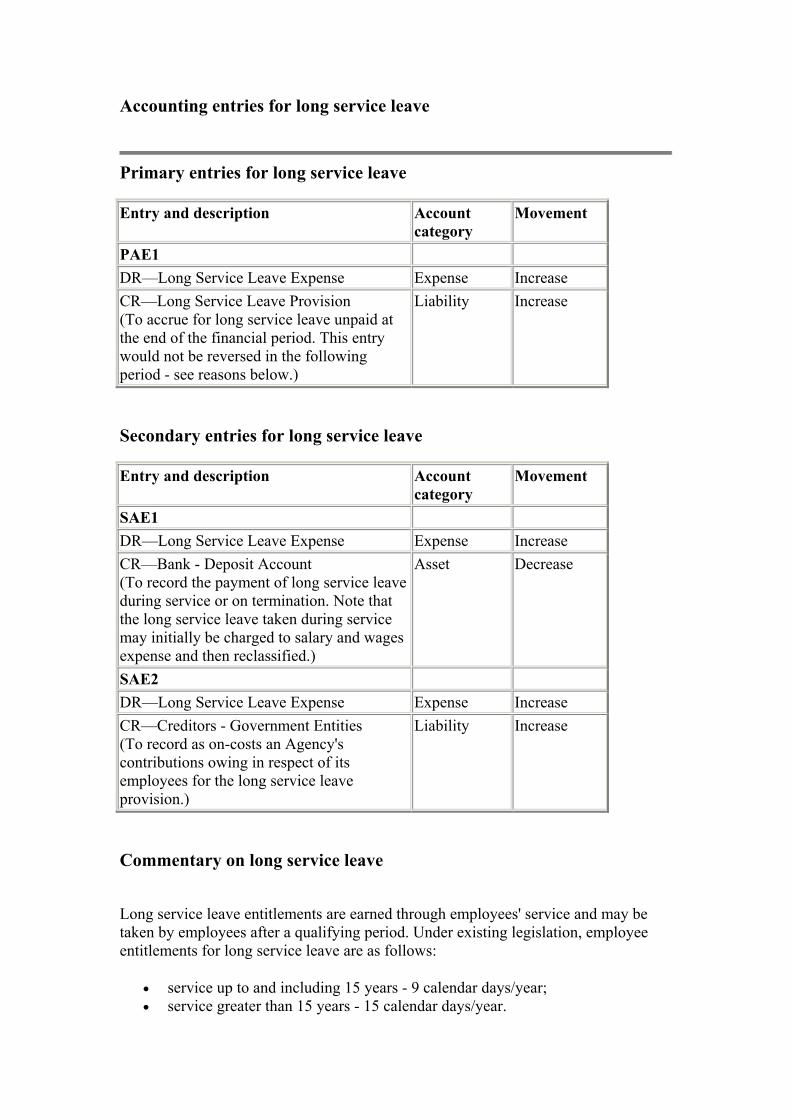

Accounting entries for long service leave

Primary entries for long service leave

Entry and description Account category

Movement

PAE1 DR—Long Service Leave Expense Expense Increase CR—Long Service Leave Provision (To accrue for long service leave unpaid at the end of the financial period. This entry would not be reversed in the following period - see reasons below.)

Liability Increase

Secondary entries for long service leave

Entry and description Account category

Movement

SAE1 DR—Long Service Leave Expense Expense Increase CR—Bank - Deposit Account (To record the payment of long service leave during service or on termination. Note that the long service leave taken during service may initially be charged to salary and wages expense and then reclassified.)

Asset Decrease

SAE2 DR—Long Service Leave Expense Expense Increase CR—Creditors - Government Entities (To record as on-costs an Agency's contributions owing in respect of its employees for the long service leave provision.)

Liability Increase

Commentary on long service leave

Long service leave entitlements are earned through employees' service and may be taken by employees after a qualifying period. Under existing legislation, employee entitlements for long service leave are as follows:

• service up to and including 15 years - 9 calendar days/year; • service greater than 15 years - 15 calendar days/year.

Employees accrue long service leave on an annual basis after the completion of ten years effective service by the Government, however pro-rata leave can be taken after seven years. This long service leave may either be taken during service, or paid out on termination. Any leave taken is to be taken into account. At the end of the financial year it is necessary to record the accurate provision for long service leave entitlements owing to all employees and related on-costs. The recording of this provision will also serve to correct the amount of the year's long service leave expense and on-costs so that it represents entitlement earned during the years and not entitlement paid. The provision for long service leave from the previous year should be left in the records until the current financial year end. This provides the following benefits:

• maintaining a liability in the statement of financial position which approximates the amount of long service leave owing at any point during the financial year; and

• prevents drastic fluctuations in the long service leave expense that would result from a full provision being put through in the last financial period of the year and then reversed in the first period of the following financial year.

The provision must take into account employees' service year dates, including part completed years to ensure that the correct liability is taken into account. If the actuarial assessment calculated benchmark changes, additional entries will be required to reflect the change (either upward or downward movement) in the long service leave provision as shown in accounting entry PAE1. In applying the benchmark, agencies should consider whether its experience of employee retention is sufficiently different to that of most other agencies to render use of the benchmark and short-cut method unreliable in estimating its long service leave liability. Agencies should ensure that the leave liability calculated using the short-cut benchmark method is not materially different from an estimate determined by using the present value basis of measurement and detailed group-based estimates (long hand method). Further details relating to the measurement of long service leave liabilities are contained in AAS 30, Accounting for Employee Entitlements. For more information refer to the flowchart Employee Related Liabilities - Long Service Leave. Control based procedures for expenditure

This outlines the key internal controls recommended for the Expenditure Cycle. The procedures provide a guide to the types of controls that are necessary to ensure effective control in a standard organisation. In some situations the controls listed will not be able to be implemented in a cost effective manner or more stringent controls may be required. In these cases alternate action should be taken. To ensure purchases are completely and accurately recorded, before recording purchases, the invoice should be matched to the appropriate control documentation (eg purchase order and goods received note) and ensure that all documents have been

duly authorised. Expenses should be recorded when the acquitted invoice is received, and unrecorded liabilities at period end should be accrued. Controls should include:

• Prenumbering and accounting for purchase orders, receiving reports and other similar documentation.

• Matching invoice, receiving order and purchase order information and following through on missing or inconsistent information.

To ensure appropriate payment of invoices:

• Reductions in liabilities should be recorded as soon as payments are made. • Before payments are released, ensure sufficient authorisation has been

attained. • All payments should be made in accordance with the due date of payment.

To ensure proper control over cheque runs:

• Ensure cancellation of all incorrect cheques. • Ensure authorised signatures on all cheques. • Cheques should be posted immediately after they are produced. • Reconcile each cheque run with system report.

Use of credit cards

The use of credit cards should be restricted to authorised cardholders. The following controls should also be established:

• Regular reviews should be made of cardholders to ensure that a card is still necessary and that transaction and monthly spending limits are appropriate.

• Complete prohibition of the use of cards for private expenditure. • Ensure each card account is reconciled monthly and appropriate supporting

documentation is received for each transaction. • Discrepancies should be followed up immediately. • Cards should be kept securely at all times.

Appropriate authorisations

Appropriate delegations authorities for expenditure should be established and documented within the department. These should be reviewed, updated and distributed regularly and approved by the Chief Executive.

Segregation of duties for expenditure

The following functions should be performed by separate sections within each accounting department:

• purchasing; • receiving; and • invoice processing, creditor, and general ledger maintenance.

The following functions should be performed by separate sections within the payroll function:

• timekeeping; and • personnel, payroll processing, payments and general ledger maintenance.

Within the section performing the invoice processing, creditor, and general ledger maintenance, the following tasks should be performed by different officers where practicable:

• disbursement preparation; • disbursement approval; • recording of cash disbursements; and • general ledger entries.

Vendor controls To monitor vendors:

• Investigate and periodically update records regarding vendor capabilities in service delivery, quality, capacity, price, leadtime requirements, customer satisfaction, and financial and management stability.

• Monitor frequency of credit claims and returns. • Monitor problems relating to materials out of stock or incorrectly supplied. • Develop data on alternate vendors and periodically evaluate vendor selection

decisions. • When calling for tenders, except where the estimated amount of a purchase is

$5,000 or less, all offers should be received in writing. At least three representative offers should be sought wherever possible.

• Specify procedures for vendors to notify of potential problems in supplying in line with contracted terms.

Accurately record receipt of goods

To accurately record receipt of goods:

• Maintain procedures for promptly updating payables and stores records.

• Periodically verify that prenumbered receiving documents have been entered in the information system.

• Maintain purchase order information so that unfulfilled orders can be identified to determine orders that are overdue.

• Compare goods or services received with those ordered and investigate those not properly ordered.

• Ensure transfer documentation accompanies all transfers of materials.

Security and access restrictions

Controls should exist to restrict access to computer programs and computer data records. These will include:

• Controls built into the software such as password access controls, which will restrict staff access to programs and data appropriate for their position and function.

• Physical controls over access of staff and the public to computer terminals, including locking doors with access to computer terminals and requiring identification to be displayed by staff while in an area with computer access.

• Similar physical controls should be applied regarding access to all non computerised financial and personnel records, such as purchase orders and accounts payable files.

Document controls

The following reports should be prepared and analysed:

• purchases by supplier; • outstanding creditors • cash discounts taken; • individual significant purchases; and • creditor balances.

Data entry and processing

To ensure control over data entry the computer system should have validation checks incorporated into its application programs to identify and/or correct any data entered which does not meet pre-determined criteria. To ensure control over data processing, controls need to be in place to ensure entries are completed in the proper financial period. To assist in this process computer application programs should include the use of batch totals, programmed balancing controls, data transmission controls, and cut-off controls. Computer applications should be set up to distinguish certain transactions as inaccurate or unacceptable, based on pre determined criteria. For example, an account

coding for a cash disbursement may be identified as inappropriate. These may be the result of:

• A numerical entry utilising a check digit being inappropriate. • An account or creditor code being used that does not exist on the system. • Amounts outside specified criteria for that account being entered.

Computer applications can be set up to treat the transaction in three possible ways:

• Accept the transaction but note it as an exception. • Transfer the transaction to a suspense account. • Reject the transaction entirely.

Computer applications should automatically produce reports detailing any transaction dealt with in any of the three ways described above. These transactions should be promptly addressed and corrected. Payroll controls

To ensure proper control over the payroll cycle:

• Review and approve initial pay and any subsequent additions and changes. • Periodically verify payroll database information eg bone fide reports. • Review and approve initial deductions/benefits elections. • Use standard forms for making adjustments to payroll records.

Regular management reviews

In order to maintain effective control the following reviews should be regularly performed:

• Reports should be developed to compare actual results (on expenses and creditor levels) to budgeted amounts. Any significant variances should be investigated.

• Any significant or unusual reconciling items between the creditors subledger and the general ledger should be investigated.

• Adequate supporting documentation should be provided with cheques and payroll authorisation for review by the authorised cheques signatories.

• Comparing actual employee related expenses to budgeted amounts and investigating any significant variances.

• Analysing reports on such areas as average employee costs by department, new hires and terminations, sick and annual leave taken, overtime payments, and individually significant compensation and benefit payments.

• Any significant or unusual reconciling items between the payroll system and the general ledger control account should be investigated.

Period and year end requirements for expenditure

Period end adjustments for expenditure

To ensure appropriate reconciliations are conducted.

• All bank accounts should be reconciled. • The creditor's subledger should be reconciled with the general ledger at the

end of each month. All reconciling amounts should be investigated and corrected.

To ensure control over void (or stale) cheques, those written that have remained unpresented for longer than 15 months should be removed from the unpresented cheques listing and credited back to the account from which the payment was allocated. Accurate records should be maintained to allow claims of such funds by creditors to be verified at a later date.

Chapter 4: Asset and liabilities cycle - property, plant and equipment

Accounting based procedures for property, plant and equipment

• Chief Executives must ensure that assets are effectively and efficiently managed by developing and implementing policies to identify, acquire, accurately value, manage and dispose of assets. The following procedures which support the prescribed elements within the Assets and Liability section of the Financial Management Framework, represent some effective management practices that if properly implemented will assist in the minimisation of risk of error or fraud. See examples of accounting entries, flowcharts and commentary provided for each type of asset and liability in the section Accounting entries for property, plant and equipment. A checklist is available in Chapter 12: Control Checklist Appendix. Acquisitions

Assets should be recognised in accordance with Accounting Policy Statement No. 2, which suggests an asset threshold of $10,000. A capitalisation threshold lower than this amount can be adopted by agencies if the total value of the assets below this threshold represents a significant percentage of the total value of the agency's assets. At the time the purchase requisition or other initial documentation is processed for an asset, it should be determined whether the expenditure relates to acquisition, an enhancement, or maintenance. When the goods or services have been received the asset should be recorded in the asset register and the liability in the creditors subledger. Construction

If the asset is in the process of being constructed, the asset value should be transferred to the fixed asset register from the general ledger's work-in-progress at the completion of the construction project. During construction the project costs may be recorded in the work-in-progress ledger until the project is completed.

Disposals

The disposal of an asset should be recorded at the time of disposal (that is, at the time the asset is no longer used in operations). If cash proceeds are received for the disposal of the asset, the cash is recorded in the cashbook and in the general ledger. The balance of accumulated depreciation as well as the item of plant and equipment should be removed in the fixed asset register. The gain/loss on disposal should be recorded in the general ledger. For further details refer Fast Help, Fixed Assets, Asset Administration, Asset Retirements. Revaluations

Assets should be revalued in accordance with Accounting Policy Statement No. 3, Revaluation of Non Current Assets. All physical non-current assets should be revalued at intervals not exceeding three years. Classes of assets may be progressively revalued on a systematic basis provided that all assets within a class are revalued at least every three years. Prior to performing the revaluation in either Masterpiece or Accpac, the depreciation run process should be up to date. This will ensure that where the amount relating to accumulated depreciation is to be cleared, it is done so in full for that asset. Further details are contained in the Fast Help, Fixed Assets, Asset Administration, Revaluations. Transfers

Transfers of property, plant and equipment should be recorded as soon as practicable after the transfer has occurred. Transferred assets which have been received should be recorded in the Asset Register with a corresponding credit to the revenue account. Depreciation should be calculated for the newly transferred asset. Depreciation

The depreciable amount of a depreciable asset should be progressively recognised in the Operating Statement by means of depreciation charges calculated using the method which most accurately reflects the pattern of consumption of the asset over its useful life. Depreciation should be charged commencing in the financial period a depreciable asset is first put to use or held ready for use.

A depreciation expense which has been calculated and accumulated in the fixed asset register should be recorded in the general ledger Accounting entries for property, plant and equipment Accounting entries for additions and acquisitions

Primary entries for additions and acquisitions

Entry and description Account category

Movement

PAE1 DR—Property, Plant and Equipment Asset Increase CR—Creditors - General (To record a good or service received in respect of a Property, Plant and Equipment acquisition.)

Liability Increase

NB. Some agencies may use a fixed asset clearing account to assist in the recording and reconciliation of property, plant and equipment. The end result of the transfer to the general ledger from the fixed asset system (which clears any fixed asset clearing accounts) is the above accounting entry. Secondary entries for additions and acquisitions

Entry and description Account category

Movement

SAE1 DR—Creditors - General Liability Decrease CR—Bank - Deposit Account (To record subsequent payments made.)

Asset Decrease

Commentary on additions and acquisitions There are many classifications relating to expenditure on Property, Plant and Equipment which must be understood before it may be properly recorded. Firstly, the nature of expenditure is either capital (acquisitions and enhancements), or an expense (maintenance). Secondly, capital expenditure may be classified as either an acquisition or an enhancement and may be for either purchased or constructed assets. The original estimated useful life of an asset assumes that there will be periodic maintenance performed to maintain its service potential. Although most expenditure immediately improves the condition of the related asset, it should only be capitalised if it significantly increases the service potential from that of the original estimate.

Expenditure which forms part of the normal, routine maintenance so that it merely enables the asset to see out its expected useful life is considered to be an expense. Further details on the distinction between maintenance and capital expenditure is contained in Accounting Policy Statement No. 10, Maintenance, Repairs and Overhauls. Capital expenditure, both for constructed and purchased assets, may be either acquisitions or enhancements. Acquisitions relate to separately identifiable assets, ie the purchase of new assets or additional distinct components for existing assets. A component is distinct to an existing asset if it has a significantly different useful life, or if it may be used or transferred independently of the existing asset. For more information refer to the flowchart Additions - Acquisitions. Accounting entries for enhancements

Primary entries for enhancements

Entry and description Account category

Movement

PAE1 DR—Property, Plant and Equipment Asset Increase CR—Creditors - General (To record a good or service received in respect of a Property, Plant and Equipment enhancement.)

Liability Increase

NB. Some agencies may use a fixed asset clearing account to assist in the recording and reconciliation of property, plant and equipment. The end result of the interface to the general ledger from the fixed asset system (which clears any fixed asset clearing accounts) is the above accounting entry. Secondary entries for enhancements

Entry and description Account category

Movement

SAE1 DR—Creditors - General Liability Decrease CR—Bank - Deposit Account (To record subsequent payments made.)

Asset Decrease

Commentary on enhancements Again, the nature of expenditure for assets is split between acquisitions (including construction asset projects), enhancements and expenses (maintenance). In outlining the difference between capital expenditure and maintenance, the original estimated useful life of an asset assumes that there will be periodic maintenance performed to maintain its service potential. Although most expenditure immediately improves the condition of the related asset, it should only be capitalised if it significantly increases the service potential from the original estimate. Expenditure which forms part of the normal, routine maintenance so that it merely enables the asset to see out its expected useful life is considered to be an expense. Further details on the distinction between maintenance and capital expenditure is contained in Accounting Policy Statement No. 10, Maintenance, Repairs and Overhauls. Capital expenditure, both for constructed and purchased assets, may be either acquisitions or enhancements. Acquisitions relate to separately identifiable assets, ie the purchase of new assets or additional distinct components for existing assets. A component is distinct to an existing asset if it has a significantly different useful life, or if it may be used or transferred independently of the existing asset. An enhancement on the other hand would increase the existing asset's cost (and therefore its carrying amount) in the fixed asset register, and would be amortised over its remaining useful life. Note that if the remaining useful life was significantly different from the original asset then the expenditure would be an acquisition, and not an enhancement. Enhancements to existing assets could include the following:

• resurfacing of a road; • memory upgrade to a computer system; • engine overhaul to a plane; • additional office work stations built; and • building extensions.

For more information refer to the flowchart Additions - Enhancements. Accounting entries for construction

Primary entries for construction

Entry and description Account category

Movement

PAE1 DR—Work in Progress Asset Increase

CR—Creditors - General (To record a good or service received in respect of a capital work in progress project.)

Liability Increase

PAE2 DR—Property, Plant and Equipment Asset Increase CR—Work in Progress (To transfer the value of the construction project to the Property, Plant and Equipment accounts upon completion.)

Asset Decrease

NB. Some agencies may charge work in progress to individual objects such as consultancies, contractors, consumables, etc. Upon completion of the capital work in progress project, balances are transferred to the general ledger from the fixed asset system as per PAE2 above, except that the credit goes to the relevant individual object. At the end of each reporting period, these agencies need to determine the value of work in progress accumulated and make the necessary general ledger entries. Secondary entries for construction

Entry and description Account category

Movement

SAE1 DR—Creditors - General Liability Decrease CR—Bank - Deposit Account (To record subsequent payments made.)

Asset Decrease

Commentary on construction Again, the nature of expenditure for assets is split between acquisitions (including construction asset projects), enhancements and expenses (maintenance). In outlining the difference between asset acquisitions and construction acquisitions (work in progress), the key question to ask is "Is the asset complete and ready and able for use by the agency?" If the answer is no, then the asset is not a completed asset and hence should be recorded as work in progress in both the general ledger and the fixed asset register until ready for use. The cost to be recorded is the purchase consideration and includes costs incidental to the construction project (eg. freight, installation, design costs, duties, project management costs, etc.). Essentially, only costs which are necessary and directly attributable to a specific item within construction activity may be capitalised. Some start up costs such as training would not be capitalised as they were not necessarily incurred in preparing the item for its intended use. The CA Masterpiece Fixed Assets module has a capability to record construction in progress assets, including the facility to capture budget, commitment and actual amounts against capital projects. Further details are contained in FAST Help - Fixed Assets, Periodic Processing, Summary Assets Roll-up. Construction assets (work in progress) could include the following:

• construction of a new road; • construction of a boardwalk; and • construction of new premises.

For more information refer to the flowchart Additions - Construction. Accounting entries for disposals

Primary entries for disposals

Entry and description Account category

Movement

PAE1 DR—Bank - Deposit Account Asset Increase CR—Asset Disposal Clearing Account (To record the proceeds upon sale of the item of property, plant and equipment—where cash proceeds received.)

Clearing Account

Increase

PAE2 DR—Accumulated Depreciation Asset Offset Decrease CR—Asset Disposal Clearing Account (To eliminate the balance of accumulated depreciation for the item of property, plant and equipment disposed by transferring it to the Disposal account.)

Clearing Account

Increase

PAE3 DR—Asset Disposal Clearing Account Clearing

Account Decrease

CR—Property, Plant and Equipment (To eliminate the balance of the item of property, plant and equipment disposed by transferring it to the Disposal account.)

Asset Decrease

PAE4 DR—Asset Disposal Clearing Account Clearing

Account Decrease

CR—Gain/(Loss) on Disposal (To account for the gain/loss on disposal of the item of Property, Plant and Equipment.)

Revenue Increase

Commentary on disposals The gain/loss on the disposal of the asset is normally calculated automatically by either the ACCPAC or Masterpiece fixed asset module upon processing of the asset disposal. Further details are contained in FAST Help - Fixed Assets, Asset Administration, Asset Retirements. If the item of Property, Plant and Equipment has no sale proceeds (ie. scrapped,