Embed Size (px)

Citation preview

Israel Economic Review Vol. 14, No. 1 (2016), 75-95

FINANCIAL LITERACY AND RETIREMENT PLANNING:

EVIDENCE FROM ISRAEL

ADI MEIR* , YEVGENY MUGERMAN

** ORLY SADE

***

Abstract

Increasing life expectancy together with reforms in the retirement savings

market and changes in the job market pose significant challenges for Israelis,

who today find themselves confronted with the need to carefully plan for

future retirement. Financial literacy is critical to retirement planning,

particularly in wake of the increasingly wide array of long-term financial

products, schemes and services marketed to individual investors. Our research

focuses on financial literacy as it relates to financial planning for retirement

(“retirement literacy”). It surveys and documents two aspects of financial

literacy: financial knowledge and financial decision-making behavior.

The findings indicate that the activities of searching for financial

information and monitoring household expenses are positively correlated with

retirement literacy, even after controlling for various demographic and

behavioral variables. Surprisingly, no significant correlation was found

between retirement literacy and financial knowledge or numeracy skills, when

controlling for other variables. Financial literacy regarding retirement savings

increases with an individual’s tendency to meticulously check bills and

periodic account statements, while financial expertise does not necessarily

translate into higher levels of retirement literacy.

1. INTRODUCTION

Financial decision making is an integral part of daily life. Most of these decisions are made

without consulting trained financial advisors. Accordingly, our ability to make financial

decisions often depends on the ability to comprehend financial theories and terminology

and integrate them into the decision-making process. Financial literacy is the term used to

describe the combination of economic and theoretical knowledge employed in financial

decision making. The academic literature does not currently provide a universally accepted

* Israel Gerontological Data Center, Hebrew University of Jerusalem, [email protected]

** The School of Business Administration, Hebrew University of Jerusalem, [email protected]

*** The School of Business Administration, Hebrew University of Jerusalem, [email protected]

ISRAEL ECONOMIC REVIEW76

definition of financial literacy.1 The most commonly used definition is that adopted by the

OECD: “A combination of awareness, knowledge, skill, attitude and behavior necessary to

make sound financial decisions and ultimately achieve individual financial wellbeing.”2

The OECD definition incorporates both cognitive and behavioral aspects of financial

literacy: (1) familiarity with financial concepts; (2) awareness and engagement in financial

decision-making; (3) financial skill; (4) optimal decision-making tailored to individual

needs.

Some financial decisions have far-reaching implications for the individual and society,

and chief among these are decisions pertaining to retirement planning. Recent demographic

and socio-economic developments, including the increase in life expectancy, the

restructuring of the capital market and changes in career trajectory, have rendered

retirement planning more critical in past years. At the same time, decisions regarding

retirement planning have become increasingly more complex, given reforms undertaken in

the regulation of retirement and other long-term savings schemes. These reforms have

enhanced the individual’s control and right to choose (between alternative complex

products, which include tax and other incentives) and have reduced government

responsibility to underwrite the livelihood of its citizens after retirement.

The composition and level of retirement savings affects the lives of individuals after

retirement. Difficulties encountered in financing retirement may cause some to become a

burden on their families and community, as well as on the public welfare system. Our

research is designed to map the aspects of financial literacy and involvement in retirement

planning related to knowledge. Unlike previous studies, it examines the various

components of “retirement literacy”, which will be defined in-depth below, through a

survey developed by the Israel Gerontological Data Center at the Hebrew University of

Jerusalem specifically for this study. Our research is unique in its focus on adults

approaching retirement age. It examines various aspects of individual financial literacy: the

tendency to track bank accounts and household bills, financial knowledge, the tendency to

seek out information, and numeracy skills. In addition, it examines factors related

specifically to an individual’s “retirement literacy”: the tendency to monitor long-term

savings accounts, one’s awareness of allocations to retirement, and active engagement in

the long-term savings management. Our findings indicate that demographic variables such

as age and income level explain the level of retirement literacy estimated in the study, while

general financial knowledge has little bearing on retirement literacy. The “tendency to

check accounts and bills” was found to be the variable most highly correlated with

retirement literacy, after controlling for demographic and behavioral variables. Does this

variable point solely to a personality trait or is it generated from greater access to

1 For a discussion of the various approaches used to define financial literacy, see Hung, Parker, and

Yoong (2009), "Defining and Measuring Financial Literacy" RAND Labor and Population Working Paper. 2 OECD (2011), "Measuring Financial Literacy: Questionnaire and Guidance Notes for Conducting an

Internationally Comparable Survey of Financial Literacy", p.3.

77 FINANCIAL LITERACY AND RETIREMENT PLANNING: EVIDENCE FROM ISRAEL

information? Additional research on this subject could have important implications for how

to face the challenge of improving financial literacy regarding retirement planning.

2. REVIEW OF THE LITERATURE

a. Pension Reforms

Given the increase in life expectancy and market volatility, many governments worldwide

have implemented structural reforms in financial markets and retirement savings systems in

recent years. Overall, governments have tended to reduce their role in providing retirement

income, while increasing an individual’s freedom of choice in managing retirement savings.

These reforms were recommended by the World Bank, and have been implemented in

countries such as Australia (Gerrans et al., 2010), Sweden (Almenberg and Save-

Soderbergh, 2011), England (U.K. Department of Work & Pensions, 2012), Poland (Zijlstra

et al., 2010), Russia (Williamson et al., 2006), and countries in South America (Calvo and

Williamson, 2008). According to Holzmann et al. (2012), 29 countries implemented

pension reforms between the years 1998 and 2008.

The economic behavior of individuals saving for retirement has become increasingly

significant with the implementation of these reforms, multiplying several-fold in the wake

of rising life expectancy. Individuals today must provide for themselves for many years

after retirement. Retirement financing is contingent on setting aside funds for years prior to

retirement. Recognizing this, Israel, like many other countries, has made retirement savings

mandatory. According to a survey conducted by the Central Bureau of Statistics (2012a),

approximately half of all adults twenty years and older currently have a pension fund.

Defined benefit pension funds, which guaranteed fixed retirement income regardless of

the sum deposited by the individual, prevailed in vast sectors of the Israeli economy in the

past. Over the past decade, however, these funds have been curtailed, are no longer

available to new employees, and have been replaced with defined contribution funds, for

which retirement income is contingent on accrued savings. The Bachar reform instituted in

2005 transferred the choice of pension plan or retirement savings scheme solely to the

individual employee. In addition, as of 2008, both employers and employees are required

(by law) to allocate certain percentages of all salaries to a pension or retirement savings

scheme. As a result of these measures, all employees must make decisions regarding

retirement planning. At the same time, there has been a decline in job security in Israel and

worldwide. Individuals tend to pursue more than one career over the course of a lifetime,

and the longevity of each career is typically shorter than in the past (Kirpal, 2011). As a

result, retirement management has become increasingly complex, and the demands on

individuals to acquire financial knowledge have increased.

ISRAEL ECONOMIC REVIEW78

b. Financial Literacy

Broadly defined, the issue of financial literacy developed to address the need to measure the

ability of various economic entities, particularly individuals, to make financial decisions.

As we mentioned in the introduction to this paper, the academic literature includes diverse

definitions of the term. In this study, we focus on the following aspects of financial literacy

in general: engagement, as evidenced in the tendency to check bank statements and bills,

financial knowledge, proactivity in seeking out financial information, and numeracy skills.

In addition, we focus on various aspects related specifically to an individual’s “retirement

literacy”: the tendency to check long-term savings account statements, assessment of an

individual’s knowledge regarding retirement income, and the level of activism regarding

long-term savings management.

Understanding the findings of our survey is important, since it is not clear if the

possession of financial knowledge necessarily leads to better retirement planning and

management. Does familiarity with the various financial concepts lead to more active long-

term savings management? Does the enhancement of general financial knowledge through

financial education programs in schools and other frameworks make the consumers of

savings schemes more sophisticated?

To the best of our knowledge, until our study, academic research on financial literacy

has not been carried out in Israel. The academic literature abroad focuses primarily on the

possession of theoretical financial knowledge as the heart and often the sole essence of

financial literacy. Financial literacy is measured in terms of financial knowledge (based on

a limited number of recurring questions) and is correlated with an individual’s demographic

profile. First and foremost, extensive and accurate familiarity with economic and financial

concepts has been found among more highly educated individuals (Van Rooij et al., 2011;

Lusardi and Mitchell, 2011a). Another variable found to have a clear and strong correlation

with financial knowledge and the familiarity with economic concepts is gender. The

tendency for men to possess greater knowledge and command of economic and financial

concepts than women is well documented (Van Rooij et al., 2011). Men tend to be more

involved in retirement planning (Lusardi and Mitchell 2011a) and tend to have better

numeracy skills than women (Banks and Oldfield, 2007). This is despite the fact that

retirement planning is particularly relevant for women, since they have a longer life

expectancy.

In addition, it has been found that greater financial literacy is associated with greater

individual and household wealth (Gustman et al., 2010; Banks and Oldfield, 2007; Van

Rooij et al., 2012). The evidence regarding the direction of causality of the correlation

between wealth and literacy is mixed (Gustman et al., 2010; Bernheim et al. 2001; Van

Rooij et al., 2012).

Several studies have examined the level of financial literacy as a function of age. Based

on these studies one would expect to find that individuals facing retirement would possess

considerable financial literacy. Research conducted in the United States and Europe

79 FINANCIAL LITERACY AND RETIREMENT PLANNING: EVIDENCE FROM ISRAEL

indicate that financial literacy increases during middle age, but then recedes (Van Rooij et

al., 2011; Lusardi and Mitchell, 2011b; Lusardi, 2008). One can understand that there is a

surge in the financial knowledge acquired prior to retirement, and a subsequent reduction

after retirement.

The findings of research conducted on the general population indicate that financial

literacy can improve income levels after retirement. There is a strong correlation between

financial literacy and retirement planning. Similarly, it has been found that the planning of

retirement savings, or even the mere consideration of retirement, doubles the total amount

individuals put aside for retirement (Van Rooij et al., 2012; Lusardi and Beeler, 2007;

Gustman et al., 2010; Lusardi, 2008) and hence, those who think about retirement in

advance tend to have twice the savings of those who do not.

The evidence regarding the impact of financial education on the quality of financial

decision-making is mixed (see for example, Mugerman, Sade and Shayo, 2014). At the

same time, however, most studies conducted on financial education programs for

employees at the work place point to these having a significantly positive effect on

decisions about savings (see for example, Bernheim and Garrett, 2003).

3. METHODOLOGY AND DATA

a. Sample

In this study we use unique data compiled from a survey developed by the Israel

Gerontological Data Center at the Hebrew University of Jerusalem to collect insights into

decision-making regarding investments in long-term savings schemes. The survey was

distributed by email to a random sample of 501 Israelis, drawn from a database of persons

registered on the iPanel online survey site. The sample group comprised Jewish men and

women between the ages of 46 and 613, natives of Israel or who immigrated to Israel prior

to 1990, randomly distributed in terms of place of residence, age and gender. Immigrants to

Israel post-1990 and non-Jews were not included in the study, since they tend to have

relatively fewer monetary resources for retirement (Semyonov and Lewin Epstein, 2011).

The use of an online sample was selected after running a telephone pilot, which did not

succeed, the complexity of the questions and the unwillingness of the respondents to reply

to the entire survey.4 This method of data collection is accepted practice in financial literacy

research (Lusardi, 2008).

3 At the time of the study, retirement age in Israel was 67 for men and 62 for women, such that the

population surveyed is primarily pre-retirement. 4

iPanel sent respondents e-mail invitations to take part in the survey. For completing the survey, the

respondents received compensation equivalent to three shekels. After 510 people completed the survey, it

was closed to new respondents. Of the 510 respondents, nine (1.8%) were disqualified for the following

reasons: three didn’t answer the majority of the survey questions, five did not answer at least 2/3 of the

ISRAEL ECONOMIC REVIEW80

The sample (Table 1) is divided almost equally between men and women, comprises

primarily secular (70.4% of the sample group), native Israelis (80% of the sample group).

The sample group is more highly educated than the general population of the designated

age group. An overwhelming majority of the respondents (85%) completed degrees at

institutions of higher education. Almost all of the respondents (94.9% of the sample group)

reported being in reasonable health or better, while 47.2% defined their household income

as above average. At the same time, however, the majority of respondents (57.8%) reported

having trouble making ends meet.

b. Research Tools

The survey composed for this research represents five content domains (indicators)

associated with financial literacy: searching financial information, monitoring accounts and

household bills, economic knowledge, numeracy skills, and retirement savings literacy.

Description of financial literacy variables

A score was calculated for each respondent for each one of the five indicators only if he/she

answered at least 75% of the question for that indicator. The search for financial

information (Search) indicator represents the number of different sources the respondent

searched for financial information, of the four sources indicated in the survey. Economic

knowledge (Knowledge) is measured according to the number of correct answers given by

a respondent to eight questions testing his/her familiarity with economic concepts, such as

the relation between risk and return, etc. The monitoring of bank accounts and household

bills (Check) indicator was derived by taking the average of three questions pertaining to

the frequency with which respondents check bank account statements and household bills.

It is important to bear in mind that the bills in question relate to household expenses, such

as water and electricity, and not to pension or retirement savings accounts. The scale of

responses is: 1-No; 2-Yes, every few months; 3-Yes, once or twice a month; 4-Yes, once a

week or more. The questions comprising these three indicators were compiled from existing

questionnaires found in the general financial literacy literature (Beal and Delpachitra, 2003,

Lusardi and Mitchell, 2011a; Van Rooij et al., 2011; Moore, 2003; Social Research Centre,

2008; Hilgert et al.,2003).

Numeracy skills (Numeracy) are measured by a respondent’s success (on a scale of 0 to 4)

on a questionnaire taken from the Survey of Health, Aging and Retirement in Europe

(SHARE), in which open-ended arithmetic problems are given.

���������������������������������������� ���������������������������������������� ���������������������������������������� ����������������������������

demographic questions, including the question regarding education, and one gave unreasonable and

contradictory responses on one of the scales.

81 FINANCIAL LITERACY AND RETIREMENT PLANNING: EVIDENCE FROM ISRAEL

Table 1

Demographic data and behavioral variables

Percentage of Respondents

Gender

Women 49.3%

Men 50.7%

Native Israelis 80.0%

Finance background (working or worked in finance) 17.4%

Household income relative to Israeli average (82%)

Well below average 13.9%

Slightly below average 15.1%

Average 23.8%

Slightly above average 30.9%

Well above average 16.3%

Ability to cover household needs (92%)

Great difficulty 13.0%

Barely 44.8%

Fairly easily 26.1%

Easily 16.1%

Health

Very bad 0.2%

Bad 4.9%

Reasonable 19.9%

Good 40.7%

Very good 34.3%

Education

No secondary school 1.2%

Partial secondary 3.4%

Graduated secondary 20.4%

Post-secondary diploma 25.3%

Bachelor's degree 30.9%

Master's degree and above 18.8%

Financial decision making at home

Self (alone or with another) 83.5%

Third party 16.5%

Asset ownership

Bank account 99.2%

Pension/retirement savings scheme (94.6%) 92.0%

Stocks and Bonds (91.6%) 37.5%

Other securities (90.2%) 17.9%

The rate of response is specified for each question eliciting less than a 95% response rate.

ISRAEL ECONOMIC REVIEW82

Pension literacy (Lit Pension) is measured as follows. Individuals lacking a pension plan

receive a negative score, -1; those with pension plans receive a score starting at 0, accruing

points for each one of the following: if the respondent checked the balance of savings in the

last three months; if the respondent is aware of the income he/she will receive after

retirement; if the respondent considered changing savings schemes or the asset

management/insurance company responsible for managing his/her retirement savings fund.

The pension literacy of those with pension plans (Lit_Pension_h) is measured in a similar

manner, but respondents without pension plans did not receive any score. The series of

questions pertaining to pension literacy were compiled specially for this survey.

Control Variables

In our survey, we examined the following potential contributory factors to financial

literacy: the tendency to compare prices and the motivation behind saving (questions drawn

from the questionnaire developed by Israel’s Central Bureau of Statistics), the respondent’s

self-assessment of his/her financial knowledge, the willingness of respondents to participate

in financial education programs, risk adversity (question drawn from the US Health and

Retirement Study (HRS)), and personal disposition (based on the LOT-R scale of

optimistic/pessimistic life orientation). In addition, we collected demographic, economic

and health data for each member of the sample group.

Age represents the age reported by the respondent.

Gender: Men received the value 1, while women constituted the comparison group.

Immigration to Israel (Aliya): Immigrants received the value 1, while native Israelis

constituted the comparison group. Only individuals who immigrated prior to 1990 were

sampled.

Education (Educ) was measured by the question regarding the name of the highest

educational institution completed by the respondent. The educational institutions were

divided into seven levels, based on criteria developed by UNESCO’s International Standard

Classification of Education (ISCED) (UNESCO, 2011): 0 – no primary schooling; 1 –

primary or middle school; 2 – partial secondary education; 3 – completed secondary school

(high school/yeshiva); 4 – post-secondary diploma program; 5 – bachelor’s degree; 6-

master’s degree and up. For the regression we compressed these categories into four

dummy variables as follows: educ1 (base group) – respondents who did not complete

secondary school receive the value 1; educ2 – secondary school graduates receive the value

1; educ3 – college graduates with bachelor’s degree receive the value 1; educ4 – college

graduates with advanced academic degrees receive the value 1.

Income is measured as household income relative to average income in Israel, on a scale of

1 to 5, 1 being “well below average” and 5 being “well above average”. For regression

83 FINANCIAL LITERACY AND RETIREMENT PLANNING: EVIDENCE FROM ISRAEL

purposes we employed three dummy variables: income1 (base group) – respondents in

lower-than-average income brackets receive the value 1; income2 – respondents in average

income bracket receive the value 1; income3 – respondents in higher-than-average income

brackets receive the value 1.

Money manager (Manage): Each respondent indicated who in the household makes

decisions regarding the avenues of investment and the financial vendors through which

investments are made. Each respondent reporting that he/she is the primary decision maker,

or that decisions are jointly made are assigned the value 1, meaning that he/she participates

in decision-making. Respondents reporting that a third party was the primary decision-

maker are assigned the value 0.

Securities (Stocks): Respondents directly investing (i.e. not through managed funds) in

stocks, bonds or other securities investments receive the value 1; others receive the value 0.

Health: Health is measured by the respondent’s subjective assessment of his/her health on a

scale from 1 to 5: 1 – very bad; 2 – bad; 3 – reasonably good; 4 –good; 5 – very good. The

responses were divided into two categories on the basis of the median: 0- from very bad to

reasonably good; 1- good or very good.

Attitude towards risk (Risky): The attitude towards risk is measured by the respondent’s

preference between a job which pays a secure steady salary and a job with a 50% chance of

double salary and a 50% chance that the salary will be cut by one-third. Those choosing the

first option were defined as “risk averse” and assigned the value 0; those choosing the

second option were assigned the value 1.

4. FINDINGS

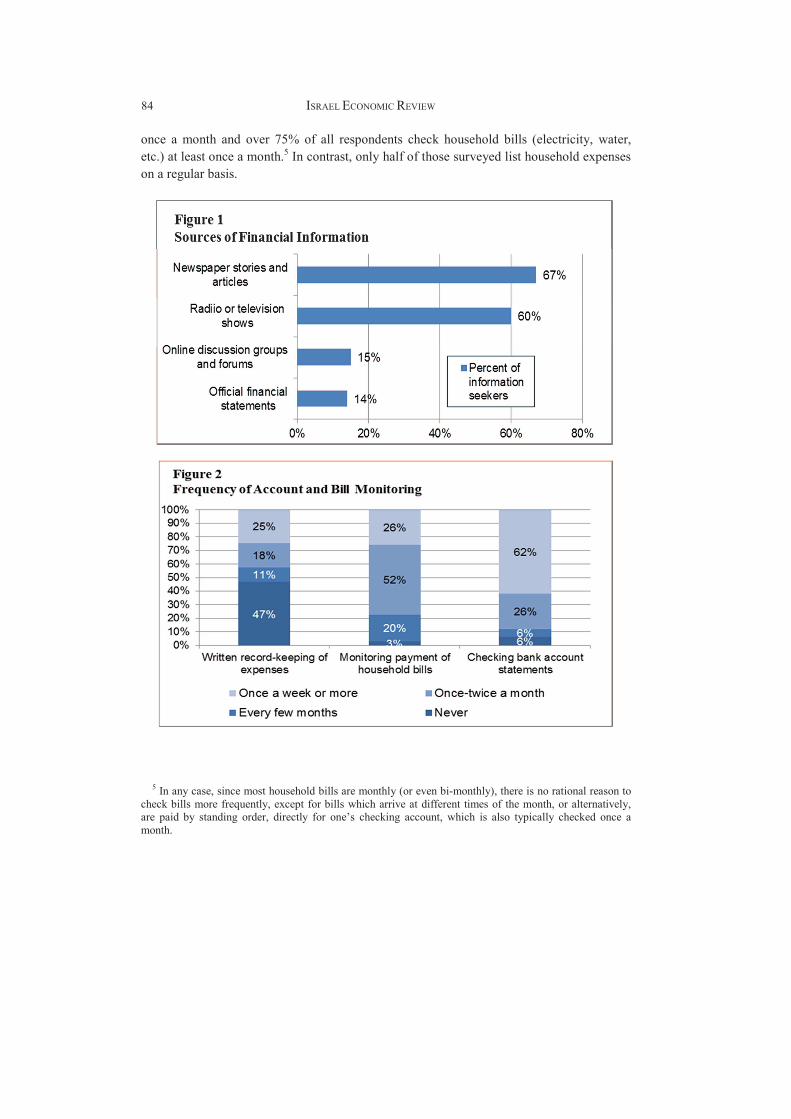

Our findings for the various financial literacy indicators are presented in Figures 1–5. For

the “search financial information” indicator (Figure 1), we find that the most frequently

consulted sources of information are newspaper stories and articles (67% of the sample

group) and radio and television programs (60% of the sample group). The search for

information online and through reviewing financial statements is considerably less

prevalent. Generally speaking, on average, respondents tend to rely on more than one

source of information (1.6 sources on average) when seeking financial information. A

financial literacy survey conducted by Israel’s Central Bureau of Statistics (CBS) among

1,200 individuals aged 20 and older in January–May 2012, also found that the media—

newspaper stories and articles and radio and television programs—constituted the most

popular source for seeking financial information, albeit at a lower rate. The far less frequent

use of online discussion groups and forums also appeared on the CBS survey (Israel Central

Bureau of Statistics, 2012a).Regarding the monitoring accounts and bills indicator (Figure

2), we found that 88% of those surveyed check their checking account statements at least

ISRAEL ECONOMIC REVIEW���

once a month and over 75% of all respondents check household bills (electricity, water,

etc.) at least once a month.5 In contrast, only half of those surveyed list household expenses

on a regular basis.

5�In any case, since most household bills are monthly (or even bi-monthly), there is no rational reason to

check bills more frequently, except for bills which arrive at different times of the month, or alternatively,

are paid by standing order, directly for one’s checking account, which is also typically checked once a

month.

���FINANCIAL LITERACY AND RETIREMENT PLANNING: EVIDENCE FROM ISRAEL

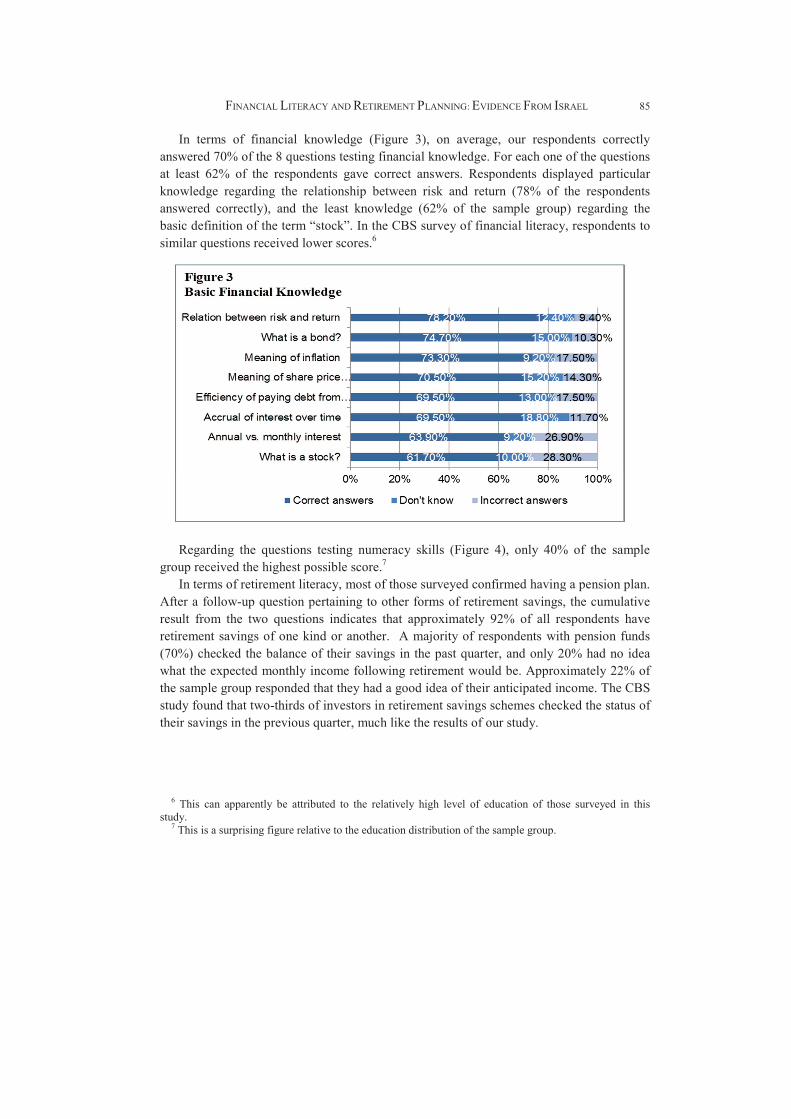

In terms of financial knowledge (Figure 3), on average, our respondents correctly

answered 70% of the 8 questions testing financial knowledge. For each one of the questions

at least 62% of the respondents gave correct answers. Respondents displayed particular

knowledge regarding the relationship between risk and return (78% of the respondents

answered correctly), and the least knowledge (62% of the sample group) regarding the

basic definition of the term “stock”. In the CBS survey of financial literacy, respondents to

similar questions received lower scores.�6

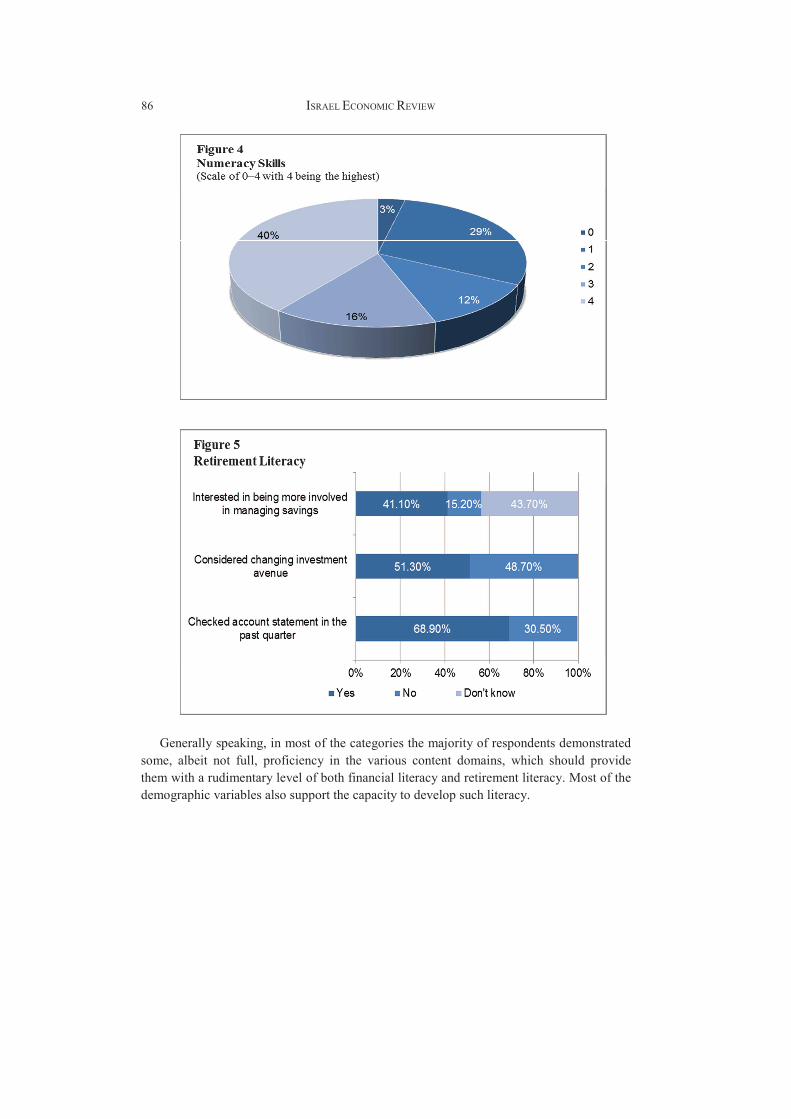

Regarding the questions testing numeracy skills (Figure 4), only 40% of the sample

group received the highest possible score.�7

In terms of retirement literacy, most of those surveyed confirmed having a pension plan.

After a follow-up question pertaining to other forms of retirement savings, the cumulative

result from the two questions indicates that approximately 92% of all respondents have

retirement savings of one kind or another. A majority of respondents with pension funds

(70%) checked the balance of their savings in the past quarter, and only 20% had no idea

what the expected monthly income following retirement would be. Approximately 22% of

the sample group responded that they had a good idea of their anticipated income. The CBS

study found that two-thirds of investors in retirement savings schemes checked the status of

their savings in the previous quarter, much like the results of our study.

6 This can apparently be attributed to the relatively high level of education of those surveyed in this

study. 7�This is a surprising figure relative to the education distribution of the sample group.

ISRAEL ECONOMIC REVIEW���

Generally speaking, in most of the categories the majority of respondents demonstrated

some, albeit not full, proficiency in the various content domains, which should provide

them with a rudimentary level of both financial literacy and retirement literacy. Most of the

demographic variables also support the capacity to develop such literacy.

87 FINANCIAL LITERACY AND RETIREMENT PLANNING: EVIDENCE FROM ISRAEL

We compiled a number of regressions to test the factors affecting financial literacy in

general and retirement literacy in particular, by testing demographic and behavioral

variables against the impact of the various indicators discussed above.

We examined the following models:

(1)

(2)

(3)

������� � �� ��� � ������� � ���� � ����� � ������� � �������� � �

!���"� � �� ��� � ������� � ���� � ����� � ������� � �������� � �

#�������� � �� ��� � ������� � ���� � ����� � ������� � �������� ��

)4(

(5)

$��%������ � �� ��� � ������� � ���� � ����� � ������� � �������� � �

&��'()*�+) �� �� ��� � ������� � ���� � ����� � ������� � �������� ��

)6( &��,-��.���,�� � �� ��� � ������� � ���� � ����� � ������� � �������� ��

i = 1,2……..,501 (i, representing the member of the sample group).

Regressions (1)–(6) test the impact of demographic variables (age, gender, education,

immigration status, health and income) on each one of the indicators appearing in the

questionnaire. Through these regressions, it is possible to assess whether and how these

indicators affect the level of financial literacy and retirement literacy of various segments of

the population. Equation (1) examines how the demographic variables affect the tendency

to seek out financial information. Equation (2) tests these variables against the respondents’

tendency to monitor accounts and household expenses. Equation (3) examines how they

relate to numeracy skills, while Equation (4) tests them against familiarity with basic

financial concepts. Equations (5) and (6) examine the impact demographic variables have

on retirement literacy, while Equation (6) relates solely to the population group which

actually holds pension plans.

Following this, we ran the same regressions, adding a number of controlled behavioral

variables: attitude to risk, investments in securities and involvement in financial decision

making. These additional variables are designed to represent a pattern of financial conduct.

We expected to find that financial literacy is less prevalent among risk-averse individuals

and more prevalent among those more actively engaged in investments, i.e., those holding

direct securities investments and those making household financial decisions, since these

activities necessitate comprehension of financial concepts.

After testing the interrelationships between the respondents’ demographic and

behavioral variables and their financial literacy, we endeavored to focus on the factors

contributing to retirement literacy in both the entire sample group and particularly among

those actually saving in pension funds. Accordingly, we examined the correlation between

ISRAEL ECONOMIC REVIEW88

each one of the financial literacy indicators and retirement literacy in general, and each

indicator and retirement literacy specifically among pension-holders, as follows:

)7( &��,-��.���� � ��������� � !���"� � #�������� � $��%������� ��

)8( &��,-��.���,�� � ��������� � !���"� � #�������� � $��%������� ��

We subsequently ran the same tests on Regressions (7) and (8), adding the demographic

factors outlined in Equations (1)–(6) as dependent variables. In addition, we conducted the

tests on Equations (7) and (8), including both the demographic and behavioral variables.

Table 2

Impact of demographic variables on financial literacy

Search Check Numeracy Knowledge Lit_pension Lit_pension_h

(1) (2) (3) (4) (5) (6)

Age 0.022** 0.006 -0.019 0.016 0.053*** 0.032***

(0.010) (0.007) (0.012) (0.018) (0.014) (0.010)

Gender 0.506*** 0.038 0.528*** 1.353*** 0.275** 0.139

(0.098) (0.069) (0.120) (0.171) (0.136) (0.095)

Educ2 0.859*** 0.178 0.251 0.362 -0.013 0.381

(0.251) (0.173) (0.304) (0.433) (0.345) (0.245)

Educ3 1.079*** 0.198 0.712** 1.314 *** 0.433 0.610***

(0.237) (0.163) (0.287) (0.408) (0.325) (0.228)

Educ4 1.013*** 0.093 0.872*** 1.886*** 0.655* 0.693***

(0.254) (0.176) (0.309) (0.441) (0.351) (0.244)

Aliya -0.264** 0.108 -0.062 -0.269 0.013 0.101

(0.122) (0.084) (0.147) (0.210) (0.167) (0.118)

Health -0.239** 0.007 -0.04 0.175 0.269* 0.127

(0.111) (0.008) (0.135) (0.193) (0.154) (0.111)

Income2 0.26** 0.051 -0.036 0.221 0.515*** 0.380***

(0.131) (0.092) (0.160) (0.228) (0.183) (0.132)

Income3 0.182* 0.103 0.107 0.382** 0.849*** 0.305***

(0.110) (0.077) (0.135) (0.192) (0.153) (0.108)

Observations 491 495 501 501 498 344

R2 0.133 0.015 0.087 0.209 0.134 0.108

Each one of the columns represents a specified OLS regression. The dependent variable is indicated

in the column title. Colum (1) examines how the designated demographic variables affect the

tendency to seek financial information. Column (2) examines this with respect to the tendency to

check accounts and bills. Column (3) examines the same with respect to numeracy skills. Column (4)

examines this with respect to financial knowledge. Columns (5) and (6) examine the impact of the

demographic variables with respect to retirement literacy, where column (6) relates solely to

respondents that are actually pension fund holders. Standard errors are in parentheses: * = 10%

significance level; ** = 5% significance level; *** = 1% significance level.

89 FINANCIAL LITERACY AND RETIREMENT PLANNING: EVIDENCE FROM ISRAEL

The results of the regressions on Equations (1)–(6) render a number of significant

findings (see Table 2). First, there is a significant positive correlation between the age of

the respondent and his/her retirement literacy, such that literacy increases with age. In other

words, the closer one gets to retirement age, the more one demonstrates proficiency and

involvement in one’s retirement savings. In addition, we show a positive correlation

between gender (male) and numeracy skills, the search for financial information and

financial expertise. Gender was not found to be significantly associated with account and

bill monitoring or with retirement literacy among those with pension plans. In other words,

despite that fact that men apparently have a better “tool box” to work with, they do not use

it more effectively than women to track the relevant data or to generate a higher level of

retirement literacy. We also found a positive correlation between education and financial

literacy, as there is a significant positive associative correlation between respondents with

advanced academic degrees and numeracy skills, basic financial knowledge and retirement

literacy among pension holders. As is the case with gender, no associative correlation was

observed between education levels and the frequency of checking bank statements and

household bills. In addition, the health and immigration status variables were not found to

be correlated with any of the financial literacy indicators, other than searching information.

Finally, there is a positive correlation between income level and retirement literacy, which

is reflected in the sample as a whole and in the subset of respondents with pension funds.

After adding the behavioral variables to the regressions (see Table 3), no substantial

changes in the significance of the correlations between the demographic variables and the

various types of literacy occurred, with the exception of the significance of age and

education in the retirement literacy regression. The statistical significance of the correlation

between age and primary education and retirement literacy decreased when controlled for

behavioral variables.

Among the behavioral variables a significant positive correlation was found between

engaging in direct securities investments and most of the financial literacy indicators

(except numeracy skills). It is reasonable to assume that a command of the skills required

for retirement literacy is also required for securities investments, particularly those skills

related to basic financial knowledge and information tracking. In addition, among those

participating in household financial decision-making, retirement literacy was found to be

positively associated with financial expertise and a general tendency to monitor accounts

and bills and to a lesser degree with numeracy skills. This is quite logical, at least as far as

it pertains to the association with monitoring of household expenses. We also found that

there is a negative correlation between risk aversion and the literacy indicators.In re-

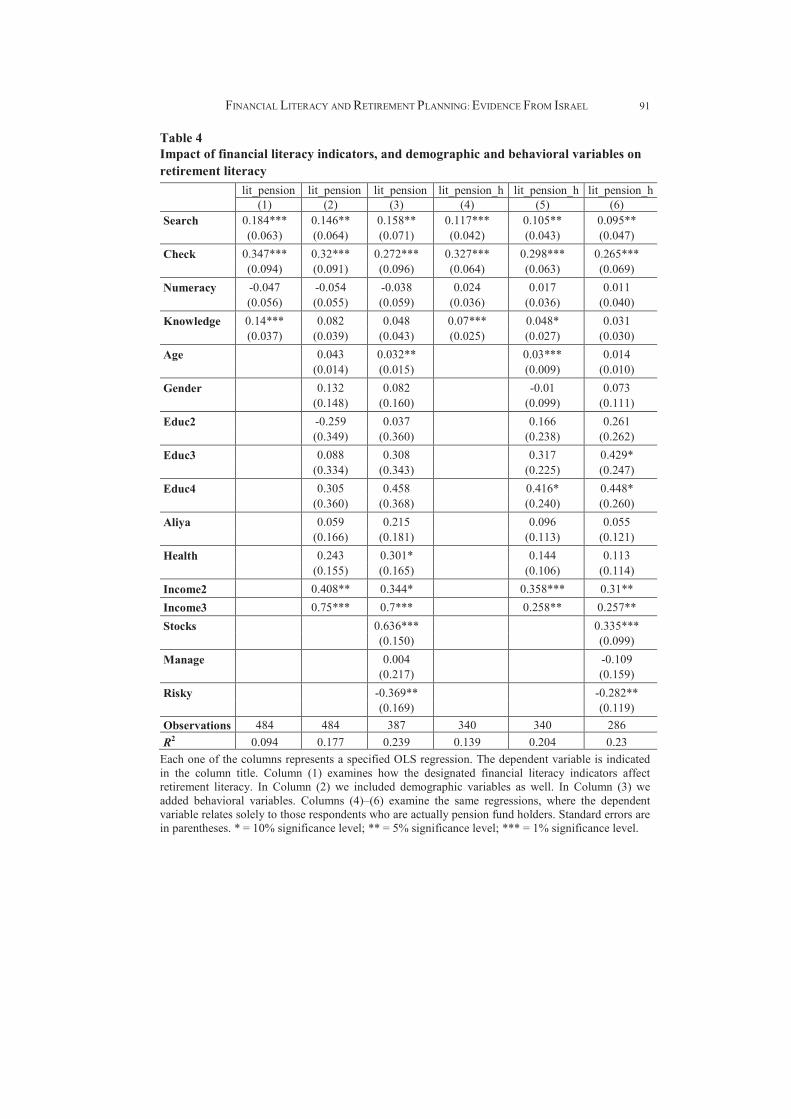

examining the factors related to retirement literacy (Equations (7) and (8)), we found a

significant positive associative correlation between three indicators of financial literacy—

the search for financial information, the monitoring of accounts and household bills and

financial knowledge—and retirement literacy in both the entire sample group and in the

subset of respondents holding pension funds (Table 4). These findings support our

ISRAEL ECONOMIC REVIEW90

assumptions regarding the importance of these factors to retirement literacy. Numeracy

skills were not found to be significant. When we add the demographic variables to these

regressions, the correlations between the various financial literacy indicators and the two

indicators of retirement literacy are weaker, but nonetheless preserved (Table 4).

Table 3

Impact of demographic and behavioral variables on financial literacy

Search Check Numeracy Knowledge Lit_pension Lit_pension_h

(1) (2) (3) (4) (5) (6)

Age 0.020* 0.006 -0.015 0.014 0.038** 0.014

(0.011) (0.008) (0.013) (0.018) (0.015) (0.011)

Gender 0.395*** -0.073 0.586*** 1.162*** 0.13 0.148

(0.110) (0.080) (0.134) (0.182) (0.150) (0.107)

Educ2 0.873*** 0.324* -0.016 0.189 0.32 0.479*

(0.263) (0.189) (0.317) (0.430) (0.352) (0.267)

Educ3 0.935*** 0.385** 0.404 0.804** 0.618* 0.715***

(0.248) (0.178) (0.299) (0.406) (0.332) (0.249)

Educ4 0.929*** 0.235 0.734** 1.445*** 0.754** 0.707***

(0.265) (0.192) (0.321) (0.214) (0.356) (0.263)

Aliya -0.394*** 0.02 -0.128 -0.416* 0.111 0.027

(0.133) (0.096) (0.161) (0.219) (0.179) (0.125)

Health -0.265** -0.092 0.14 0.351* 0.288* 0.08

(0.119) (0.088) (0.146) (0.198) (0.163) (0.119)

Income2 0.168 0.016 0.06 0.027 0.385** 0.315**

(0.142) (0.104) (0.174) (0.236) (0.195) (0.144)

Income3 0.131 0.092 0.18 0.12 0.753*** 0.267**

(0.119) (0.088) (0.146) (0.198) (0.162) (0.115)

Stocks 0.333*** 0.113 -0.313** 0.413** 0.792*** 0.394***

(0.107) (0.079) (0.132) (0.179) (0.146) (0.100)

Manage 0.317** 0.262** 0.377* 1.007*** 0.155 -0.012

(0.158) (0.115) (0.193) (0.261) (0.214) (0.162)

Risky 0.219* -0.119 0.201 0.368* -0.315* -0.269**

(0.124) (0.091) (0.153) (0.207) (0.170) (0.123)

Observations 392 395 399 399 397 289

R2 0.175 0.049 0.14 0.263 0.208 0.156

Each one of the columns represents a specified OLS regression. The dependent variable is indicated in

the column title. Column (1) examines how the designated demographic and behavioral variables

affect the tendency to seek financial information. Column (2) examines the same with respect to the

tendency to check accounts and bills. Column (3) examines this with respect to numeracy skills.

Column (4) examines this with respect to financial knowledge. Columns (5) and (6) examine the

impact of these variables with respect to retirement literacy, where column (6) relates solely to

respondents that are actually pension fund holders. Standard errors are in parentheses: * = 10%

significance level; ** = 5% significance level; *** = 1% significance level.

91 FINANCIAL LITERACY AND RETIREMENT PLANNING: EVIDENCE FROM ISRAEL

Table 4

Impact of financial literacy indicators, and demographic and behavioral variables on

retirement literacy

lit_pension lit_pension lit_pension lit_pension_h lit_pension_h lit_pension_h

(1) (2) (3) (4) (5) (6)

Search 0.184*** 0.146** 0.158** 0.117*** 0.105** 0.095**

(0.063) (0.064) (0.071) (0.042) (0.043) (0.047)

Check 0.347*** 0.32*** 0.272*** 0.327*** 0.298*** 0.265***

(0.094) (0.091) (0.096) (0.064) (0.063) (0.069)

Numeracy -0.047 -0.054 -0.038 0.024 0.017 0.011

(0.056) (0.055) (0.059) (0.036) (0.036) (0.040)

Knowledge 0.14*** 0.082 0.048 0.07*** 0.048* 0.031

(0.037) (0.039) (0.043) (0.025) (0.027) (0.030)

Age 0.043 0.032** 0.03*** 0.014

(0.014) (0.015) (0.009) (0.010)

Gender 0.132 0.082 -0.01 0.073

(0.148) (0.160) (0.099) (0.111)

Educ2 -0.259 0.037 0.166 0.261

(0.349) (0.360) (0.238) (0.262)

Educ3 0.088 0.308 0.317 0.429*

(0.334) (0.343) (0.225) (0.247)

Educ4 0.305 0.458 0.416* 0.448*

(0.360) (0.368) (0.240) (0.260)

Aliya 0.059 0.215 0.096 0.055

(0.166) (0.181) (0.113) (0.121)

Health 0.243 0.301* 0.144 0.113

(0.155) (0.165) (0.106) (0.114)

Income2 0.408** 0.344* 0.358*** 0.31**

Income3 0.75*** 0.7*** 0.258** 0.257**

Stocks 0.636*** 0.335***

(0.150) (0.099)

Manage 0.004 -0.109

(0.217) (0.159)

Risky -0.369** -0.282**

(0.169) (0.119)

Observations 484 484 387 340 340 286

R2 0.094 0.177 0.239 0.139 0.204 0.23

Each one of the columns represents a specified OLS regression. The dependent variable is indicated

in the column title. Column (1) examines how the designated financial literacy indicators affect

retirement literacy. In Column (2) we included demographic variables as well. In Column (3) we

added behavioral variables. Columns (4)–(6) examine the same regressions, where the dependent

variable relates solely to those respondents who are actually pension fund holders. Standard errors are

in parentheses. * = 10% significance level; ** = 5% significance level; *** = 1% significance level.

ISRAEL ECONOMIC REVIEW92

Our findings do not allow us to determine whether the positive correlation between

searching financial information and household bill monitoring on the one hand and

retirement literacy on the other indicates that accessibility to such information alone

contributes to financial literacy. Alternatively, it is possible that these variables coincide

with personality trait variables on which we have no data. Our findings do point, however,

to the need to examine this subject in depth .

The demographic variables presented in Table 4 demonstrate a correlation similar to

that documented in Tables 2 and 3, except for the education variable, which was found to

be statistically significant in the initial tests, but disappeared as an explanation of retirement

literacy in the regressions that include the various literacy variables as well. We believe that

the strong correlation between education and the financial literacy indicators, as reflected in

Tables 1 and 2, accounts for this.

With the addition of the behavioral variables to Equations (7) and (8), the associative

correlations between the variables found in the original equations become weaker or

disappear. The most surprising result is the lack of correlation between financial expertise,

an indicator of financial literacy, and retirement literacy. In other words, account and

household bill monitoring and financial information seeking are more strongly correlated

with retirement literacy than either familiarity with financial concepts or numeracy skills.

5. CONCLUSIONS

Vast changes have been made over the years in the Israeli government’s long-term

retirement savings policy. Salaried workers transitioned from the world of defined-benefit

pension plans, which gave them a relatively generous monthly income, (often without any

contribution from the worker), to the world of defined contribution, in which their post-

retirement economic well-being depended solely on the retirement savings accrued prior to

retirement. In light of this new reality, financial literacy, and particularly financial literacy

for retirement planning, has become increasingly important to Israeli citizens. The

government has undertaken a number of measures to encourage the public to save for

retirement, including tax incentives totaling billions of shekels each year and compulsory

deposits in retirement savings schemes.

Our research, which focuses on financial knowledge and conduct, maps demographic

and behavioral variables and the correlations between them and financial literacy,

particularly as it applies to retirement planning. We found a correlation between retirement

literacy and the following financial literacy indicators: the search for financial information,

the tendency to check bank statements and household bills, and the possession of financial

knowledge. When controlling for the background variables, the correlation between

financial knowledgeability and retirement literacy surprisingly disappears. The

disappearance of this correlation indicates that financial knowledge neither leads to a

command of the pension characteristics nor to awareness of total savings. In addition, the

93 FINANCIAL LITERACY AND RETIREMENT PLANNING: EVIDENCE FROM ISRAEL

correlation between retirement literacy and information seeking weakens and only the

“household bill tracking” effect remains stable.

The enhancement of retirement literacy must be undertaken in a manner which enables

meticulous long-term planning of an individual’s future livelihood. Our findings underscore

the fact that, in addition to the improvement of the public’s general financial literacy

through programs initiated by various agencies, there is a need for in-depth examination of

other ways of enhancing public accessibility to information—for example by explaining

available information, such as the information included on the monthly salary slip or by the

introduction of “smart” salary slips with embedded links to relevant information.

It should be remembered that personality traits or certain behavioral factors, which were

not examined by us in the questionnaire, may cause certain individuals to be more involved

in monitoring their bank accounts and household bills, conduct which is positively

correlated with retirement literacy. To prove the existence of a causal relationship between

the tendency to check accounts and bills, or information accessibility, and retirement

literacy requires additional research. Such a study can examine, in a controlled manner,

the impact of improving the accessibility of financial information on retirement literacy. It

is possible, for example, to employ existing tools, such as salary slips and pension

statements, and make them more accessible, or even consider combining the two so that the

data relevant to retirement is reflected on the monthly salary slip. We intend to examine this

issue in future research.

ISRAEL ECONOMIC REVIEW94

REFERENCES

Almenberg, J. and J. Save-Soderbergh (2011), "Financial Literacy and Retirement Planning

in Sweden", Journal of Pension Economics and Finance ,10 (4), pp. 585–598.

Banks, J. and Z. Oldfield (2007), "Understanding Pensions: Cognitive Function, Numerical

Ability and Retirement Saving," Fiscal Studies, 28 (2), pp.143–170.

Beal, D. and S. Delpachitra (2003), Financial Literacy Among Australian University

Students. Economic Papers, 22 (1), pp. 65–78.

Bernheim, B., D. Garrett and D. Maki (2001), "Education and Saving: The Long-Term

Effects of High School Financial Curriculum Mandates", Journal of Public Economics,

80 (3), pp. 435–465.

Bernheim, B. and D. Garrett (2003), "The Effects of Financial Education in the Workplace:

Evidence from A Survey of Households", Journal of Public Economics, 87, pp. 1487–

1519.

Calvo, E. and J. Williamson (2008), "Old-Age Pension Reform and Modernization

Pathways: Lessons for China from Latin America," Journal of Aging Studies, 22 (1),

pp. 74–87.

Gerrans, P., M. Clark-Murphy and C. Speelman (2010), "Asset Allocation and Age Effects

in Retirement Savings Choices", Accounting & Finance, 50 (2), pp. 301–319.

Gustman, A., T. Steinmeier and N. Tabatabai (2010), "Financial Knowledge and Financial

Literacy at the Household Level", NBER Working Paper No.16500, Cambridge, Mass:

National Bureau of Economic Research.

Hilgert, M., J. Hogarth and S. Beverly (2003), "Household Financial Management: The

Connection Between Knowledge and Behavior", Federal Reserve Bulletin (July), pp.

309–322.

Holzmann, R., E. Palmer and D. Robalino (2012), "The Economics of Reverse Funds in

NDC Schemes: Role, Means, and Size to Manage Shocks", in R. Holzmann, E. Palmer

and D. Robalino (eds), Nonfinancial Defined Contribution Pension Schemes in a

Changing Pension World, Vol. 2 - Gender, Politics, and Financial Stability.

Israel Central Bureau of Statistics (2012a). "Knowledge, Opinion and Behavior in Financial

Issues- Financial Literacy Survey", Jerusalem: Central Bureau of Statistics.

Israel Central Bureau of Statistics (2012b). "The Financial Situation of Israelis and How

They Manage It - Financial Literacy Survey", Jerusalem: Central Bureau of Statistics.

Kirpal, S. (2011), "Labour-Market Flexibility and Individual Careers: A Comparative

Study", Technical and Vocational Education and Training, Series 13, Springer.

Lusardi, A. (2008), "Financial Literacy: An Essential Tool for Informed Consumer

Choice?", NBER Working Paper Series No. 14084, Cambridge, Mass.: National

Bureau of Economic Research.

Lusardi, A. and J. Beeler (2007), "Savings Between Cohorts: The Role of Planning", in B.

Madrian, O. Mitchell, and B. Soldo (eds), Refining Retirement: How Will Boomers

Fare? Oxford University Press, Oxford, pp. 271–295.

95 FINANCIAL LITERACY AND RETIREMENT PLANNING: EVIDENCE FROM ISRAEL

Lusardi, A. and O. Mitchell (2007), "Financial Literacy and Retirement Preparedness:

Evidence and Implications for Financial Education," Business Economics, 42 (1), pp.

35–44.

Lusardi, A. and O. Mitchell (2011a), "Financial Literacy and Planning: Implications for

Retirement Wellbeing", NBER Working Paper No. 17078, Cambridge, Mass: National

Bureau of Economic Research.

Lusardi, A. and O. Mitchell (2011b), "Financial Literacy Around the World: An

Overview", Journal of Pension Economics and Finance, 10 (4), pp. 497–508.

Moore, D. (2003), "Survey of Financial Literacy in Washington State: Knowledge,

Behavior, Attitudes, and Experiences", Washington State University, Social and

Economic Sciences Research Center, Pullman, WA.

Mugerman, Y., O. Sade and M. Shayo (2014), "Long-Term Savings Decisions: Financial

Reform, Peer Effects and Ethnicity", Journal of Economic Behavior and Organization,

106, pp. 235–253.

Semyonov, M. and N. Lewin-Epstein (2011), "Wealth Inequality: Ethnic Disparities in

Israeli Society", Social Forces, 89 (3), pp. 935–959.

Social Research Centre (2008), "ANZ Third Survey of Adult Financial Literacy in

Australia".

U.K. Department of Work & Pensions (2012), 5, Accessed 06/11/2012.

http://www.dwp.gov.uk/policy/pensions-reform/

UNESCO (2011), "ISCED: International Standard Classification of Education", UNESCO

Institute for Statistics.

Van Rooij, M., A. Lusardi and R.J.M. Alessie (2011), "Financial Literacy and Stock

Market Participation", Journal of Financial Economics, 101 (2), pp. 449–472.

Van Rooij, M., A. Lusardi and R. Alessie (2012), "Financial Literacy, Retirement Planning

and Household Wealth", The Economic Journal, 122 (560), pp. 449–478.

Williamson J., S. Howling and M. Maroto (2006), "The Political Economy of Pension

Reform in Russia: Why Partial Privatization?", Journal of Aging Studies, 20 (2), pp.

165–175.

Zijlstra G., J. van Haastregt, J. van Eijk, L. de Witte, T. Ambergen and G. Kempen (2010),

"Mediating Effects of Psychosocial Factors on Concerns About Falling and Daily

Activity in a Multicomponent Cognitive Behavioral Group Intervention," Aging &

Mental Health, 15 (1), pp. 68–77.