Embed Size (px)

Citation preview

1

Financial Development Convergence

Berrak Bahadir and Neven Valev

September, 2013

Abstract

We show that credit levels relative to GDP and other measures for financial development tend to converge across countries over time. The results are obtained using a broad sample of countries over many years and controlling for the quality of country-level institutions, the efficiency of financial institutions, and a range of macroeconomic variables. While we find evidence for convergence in the broad sample, we show that it levels off when countries reach a medium level of financial development. At high levels of financial development, convergence slows down even more and becomes negligible.

JEL Codes: G01, E22

Key Words: Financial Development, Convergence, Institutions

Contacts: Bahadir, University of Georgia ([email protected]); Valev, Georgia State University ([email protected]).

2

Financial Development Convergence

I. Introduction The last several decades have witnessed massive financial liberalization in emerging

markets. For the financial markets, the objective has been to foster financial development by

inviting international know-how and to reduce the “knowledge gap” (Goldberg, 2007) in finance

between developed and developing countries. The objective for the real economy has been to

provide funding for capital investment and to stimulate economic growth, thus helping emerging

markets reach the standard of living achieved in developed economies (Aghion et.al. 2005).

While the benefits of financial development are well established, to date there is little

systematic evidence indicating whether the financial development in developing countries is

catching up with the levels achieved by advanced countries. Bridging the financial development

gap is likely to help reduce the income gap between countries. If there is divergence, then the

gap between developed and emerging countries will keep growing, with important ramifications

not only for the financial sector but also for the real economy. In this paper, we investigate

whether such convergence has occurred using a broad sample of countries with a primary focus

on credit markets. Our findings suggest that:

• there is an underlying process of financial development convergence but it ceases as

countries reach higher levels of financial development;

• the convergence cannot be attributed to improvements in the country-level institutions or

in the efficiency of financial institutions;

• it is most likely driven by expanding the financial sector to reach new customers in

underdeveloped countries; as the gains from such investment wear off with diminishing

returns, convergence slows down.

3

There is an important difference between studying the determinants of financial

development and studying financial development convergence. Financial markets have evolved

substantially in advanced economies during the last several decades reflecting significant

improvements in financial sector know-how. The question for emerging markets then is not only

whether its citizens can access more financial services over time but whether they take full

advantage of the available international finance know-how. To answer that question, we must

look at the differences between countries over time, and not only at the growth of financial

services within one country over time. Similar to the economic growth literature, where the goal

is to know if incomes increase and, separately, if they increase relative to advanced countries, in

the financial development literature the objective is to know: 1) whether the access to financial

services increases over time and 2) whether the increase in a particular country outpaces or lags

behind the development in the leader countries. The literature has addressed the former question

on the determinants of financial development but has paid less attention to the latter question on

financial development convergence.

We can highlight the process of convergence with a couple of examples. In 2011 credit to

the private sector was 135 percent of GDP in Germany and two times smaller (66 percent) in

neighboring Poland. However, in 2000 the difference was even greater: credit in Poland (34

percent) was four times smaller than in Germany (146 percent). Going further east, in 2000

credit in Belarus was almost eight times smaller than in Germany (19 percent); by 2011 it was

only four times smaller (34 percent). We investigate whether a similar process can be observed

across other countries as well.

Our analysis extends the literature on the determinants of financial development, e.g. La

Porta et al. (1997, 1998); Djankov et al. (2007); and Beck et al. (2003). Similar to that literature,

4

we are interested in the factors that explain the differences in financial development across

countries. However, we analyze whether we observe financial development convergence or

divergence across countries. Our focus is on the changes in the country differences over time.

We also contribute to several recent papers on financial system convergence. Antzoulatos et al.

(2011) find evidence for non-convergence in a sample of thirty eight industrial and developing

countries during 1990 – 2005 whereas Veysov and Stolbov (2011) report convergence. Bruno et

al. (2012) find mixed evidence for convergences looking at household financial assets in the

OECD countries. Our contribution to these papers is threefold. First, we approach the question

with the entire financial structure database (Beck and Demirgüç-Kunt, 2009) using all countries

and years for which data are available. Second, we investigate financial development

convergence at different levels of economic and financial development. Third, we explore

whether the process of convergence can be attributed to institutional changes on the country level

or to changes in the efficiency of operation of financial institutions. These estimations are

important as institutions are the primary factor for financial development (La Porta et al. 1997)

while the efficiency of financial institutions reflects know-how and innovation.

The rest of the paper is structured as follows. In section II we discuss whether or not we

should expect convergence. Then, we present the data in Section III and the empirical results in

section IV. The paper concludes with final remarks in section V.

II. Should we expect financial development convergence?

Looking at the global economy, private credit as percent of GDP had doubled in the three

decades before the financial crisis of 2008. It increased from 87.7 percent of GDP in 1975, to

113.8 percent in 1985, 145.9 percent in 1995, and reached 162 percent in 2005. The growth has

5

been faster in some countries and slower (or nonexistent) in others but, nonetheless, the general

trend has been upward and quite steep.

Available time series do not tell us how much of that growth can be attributed to larger

loans to existing borrowers or to a larger number of borrowers. A recent project by the World

Bank (Demirgüç-Kunt and Klapper, 2012) has started collecting such data but it would be some

time before time series are accumulated. Nonetheless, the initial survey from 2011 shows that

over 30 percent of households in the U.S., UK, Sweden, Netherlands, Belgium, Denmark, and

other developed countries have mortgages while the percent of households with mortgages is less

than 10 percent in most of the rest of the world. In fact, less than 5 percent of households in

many countries in Africa, Latin America, and the former communist bloc have outstanding

mortgages. Given these numbers and that much of the growth in credit has come from growth in

household credit (Beck et al., 2012; Büyükkarabacak and Valev, 2010; Greenwood and

Scharfstein, 2012), we can conjecture that an increase in the number of borrowers can explain

much of the credit growth.

The increase in the number of borrowers can be attributed to several potential factors.

First, institutions that are important to the financial system could have improved over time

allowing banks to go down-market. Many emerging markets have made efforts to adopt

institutions that promote financial development. More efficient bankruptcy procedures, better

financial transparency rules, and stronger regulation and supervision of the financial system

could help expand the supply of external financing to households and firms. As we pointed out

earlier, the literature, e.g. La Porta et al. (1997, 1998), identifies institutions as the primary

determinant of financial development.

6

Second, financial liberalization has spread financial sector know-how to emerging

markets. The branches of international banks bring expertise in risk management, credit

evaluation, and other areas that facilitate the development of the financial sector. In some

emerging markets, such as the Ukraine, more than half of the entire financial system is foreign

owned. In some developing countries, mobile technology has played a vital role in expanding

financial services to rural areas. All of those could increase the efficiency of operation of the

financial system, bringing down the costs and allowing financial institutions to reach new

customers.

Third, financial liberalization and the general move towards market-based economies

around the world have opened the playing field for capital investment in financial services.

Domestic and international banks have invested in new branches in urban and rural areas

reducing the geographic distance to their customers. According to Demirgüç-Kunt and Leora

Klapper (2012), geographic distance to financial institutions is a major deterrent to the use of

financial services. Respectively, reducing the distances can help bring more households and

firms into the formal financial system even if institutions and technological know-how remain

the same. A few numbers from the IMF’s Financial Access Survey could illustrate that point.

The number of bank branches per 100,000 adults in middle income countries increased from 8.1

in 2004 to 12.2 in 2010. At the same time, the number of bank branches in the high income

countries decreased from 31.6 per 100,000 adults to 23.1.1

1 The data set begins in 2004 and cannot be used in our analysis as the series is too short. Moreover, there are limited data for low income countries.

The number of ATM’s per 1000

adults increased by about 50 percent in the high income countries (from 68.6 to 90.1). In middle

income countries, their number tripled from 10.1 to 29.0.

7

Fourth, the general growth of income across countries has pushed more households and

firms above a threshold level of income and savings that allow them to start using financial

services. Similar to the levels of credit, global GDP per capita in constant 2000 dollars has nearly

doubled from 3,594 dollars in 1975 to 5,700 dollars in 2005. Higher and more stable incomes

along with real estate and other assets that could serve as collateral allow new customers to

increase their demand for financial services and the financial system to provide them.

If the factors discussed above have played a more important role in less developed

countries compared to developed countries, then we should observe convergence in terms of

credit availability. If they have benefited primarily the already developed countries, then we

should observe divergence. As a parallel, the economic growth literature (Pritchettt, 1997;

Durlauf, 1996) finds that incomes per capita do not exhibit convergence on a worldwide scale. In

fact, looking at the most and the least advanced economies, income levels tend to diverge over

time. There are two reasons for that. First, new technologies are not readily adopted in countries

with poor education, institutions, and infrastructure. Thus, while new ideas raise the standard of

living in rich countries, they have had less impact on incomes in poor countries. Second, as

Romer (1986) shows, investment in new capital could have decreasing returns on a firm level but

it could exhibit increasing returns on a societal level if firms benefit from other firms’ investment

in new knowledge. Thus, rich countries get richer over time, benefiting from a virtuous cycle,

while poor countries are stuck in a vicious cycles or low investment and low productivity.

The same forces could be at play in the financial system. New financial sector

technologies may not be suitable in institutionally weak countries and financial innovations may

not take hold. Also, countries with weak institutions may find it difficult to invest the necessary

resources to improve their institutions. Thus, a financially underdeveloped economy may remain

8

such while the financial sectors in developed countries continue to innovate and expand.

However, it could also be the case that convergence occurs despite institutional differences. The

financial system could be adding new firms and households as customers at a more rapid rate in

the less developed countries simply because the starting base is smaller. In that environment,

capital investment in new bank branches and introducing new assets have a bigger impact in

terms of new customer generation compared to advanced economies where a higher percent of

the private sector is already “banked”. Then, we could observe convergence while holding

constant the quality of institutions and financial innovation.

The discussion suggests that, along with other controls, our models exploring financial

development convergence should incorporate: 1) measures for the quality of country-level

institutions; 2) measures of the efficiency of financial institutions, and 3) income levels. We want

to know if there is evidence for convergence even after controlling for institutions, bank

operating efficiency, and rising incomes. If such evidence is present, we could attribute the

process of convergence to capital investment in financial services.

Whether convergence is a byproduct of the improvements in the county-level institutions

or it results from additional investments in the financial sector has important implications. At

some point, the financial institutions have succeeded in reaching most potential customers and

there are fewer opportunities to reach new ones by simply opening another bank branch in a part

of town without any. In essence, the diminishing returns to capital investment slow down the

growth. From that point on, further convergence would be possible only if country-level

institutions improve and financial institutions innovate.

9

III. Data and methodology

We explore the convergence of several measures for financial development from the

Financial Structure Database (Beck and Demirgüç-Kunt, 2009). Our primary focus is on credit to

the private sector (CREDIT) as a percent of GDP since that variable has been used most

extensively in the literature to study financial development (Beck et al., 2007; Djankov et al.,

2007). It measures the level of firm and household credit by deposit money banks and other

financial institutions as a percent of GDP. We also report estimations with BANK CREDIT

which is the amount of credit extended by deposit money banks to the private sector as percent

of GDP; and LIQUID LIABILITIES, defined as the ratio of liquid liabilities to GDP. Summary

statistics and correlations are presented in the Appendix. Since we are interested in the rate of

growth of these variables, we also report summary statistics for the average annual rates of

change during the sample period.

We transformed the annual data into five-year periods: 1965-1969, 1970-1974, .., 2005-

2009. The objective was to preserve the time variation on the country level while at the same

time smooth out the annual variations. It is a method that has been used extensively in the

literature (Beck et al., 2000). For completeness, in unreported regressions we also use the annual

data panel and a cross section database with the country averages for the entire period, and

obtained qualitatively similar results. The estimation results are available on request.

We start our estimations with a simple empirical formulation for convergence:

( 1 )

10

where is the growth of financial development in country i during a five-year period t. is

the level of financial development in the first year of that same time period.2

Equation (1) estimates unconditional convergence as it does not control for any country

characteristics. Building on that, we add a vector of control variables :

We are interested in

the coefficient estimate for : implies convergence of the level of financial development

in the sense that financial development grows more rapidly in countries/periods with a lower

initial level of financial development; implies that differences in financial development

across countries persist over time; and provides evidence for divergence, i.e. finance

expands more rapidly in countries that are already more financially developed.

( 2 )

The base control set includes the level of real GDP PER CAPITA, INFLATION,

GOVERNMENT spending, and TRADE openness. Favorable macroeconomic conditions affect

credit growth by increasing the borrowing capacity of households and decreasing the default

rates likelihood. Thus, we expect an increase in the real growth of GDP to increase the credit

growth (Levine, 2005). High inflation is associated with high nominal interest rates and may also

be viewed as a proxy for poor macroeconomic management. Also, because the real profits of

banks may become harder to predict during periods of high inflation, banks may find it more

difficult to assess credit quality at these times. Huybens and Smith (1999) theoretically and Boyd

et al. (2001) empirically study the effects of inflation on financial development and conclude that

economies with higher inflation rates are likely to have smaller banks and equity markets. An

increase in government spending is likely to crowd out private borrowing and is negatively

associated with private credit growth. Finally, following Huang and Temple (2005) we include

2 We also experimented using the average level of financial development from the preceding five year period and obtained similar results.

11

trade openness, as the ratio of exports plus imports to GDP. We expect to see a positive

correlation between trade openness and private credit growth as international trade requires

financing and the exposure to international competitions stimulates the demand for capital

investment and innovation.

All variables are entered in logs and are timed at the beginning of the five year period to

reduce endogeneity issues. Alternatively, we used the average values from the preceding five-

year period as well as the average values during the contemporaneous period. The results are

similar and available upon request. All the models are estimated with generalized least squares

allowing for autocorrelation within countries as well as heterogeneous standard errors across

countries. For robustness we also estimate the models with fixed effects and robust standard

errors.

Next, we add institution variables to equation (2):

( 3 )

We start with the rule of law measure from the International Country Risk Guide (ICRG)

as well as a composite ICRG variable that averages three of the ICRG indexes: rule of law,

corruption, and bureaucratic efficiency. The advantage of the ICRG variables is that they are

collected on an annual basis and have some time variation. The disadvantage is that the series

start in 1984 reducing our sample size substantially. Then we add countries’ legal origin as it has

been identified as an important predictor of financial development (La Porta et al., 1997).

Finally, we add the religious composition of the population: CATHOLIC and MUSLIM, leaving

PROTESTANT as the omitted category, as the literature (Stulz and Williamson, 2003) has

identified the religious composition of the population as an important and exogenous predictor of

financial development. Specifically, countries with predominantly protestant population exhibit

12

higher levels of financial development. We are interested in whether there is evidence for

convergence after we control for institutions.

Then, we add several measures for the efficiency of financial institutions to the baseline

equation (2):

( 4 )

Specifically, we introduce the NET INTEREST MARGIN which is defined as the accounting

value of bank's net interest revenue as a share of its interest-bearing (total earning) assets; COST

is the total costs as a share of total income of all commercial banks; and RETRUN ON ASSETS

is the average return on assets (Net Income/Total Assets). Similar to equation (3), we are

interested in whether the evidence for convergence, i.e. the coefficient estimate for , is affected

by the inclusion of these variables.3

Next, we estimate equation (2) for different groups of countries based on their levels of

economic and financial development. And, finally, we follow Aghion et al. (2005) and estimate

an alternative version of equation (2) where we explain the growth of financial development

relative to the U.S. where the U.S. is taken as the frontier of development:

(3)

Here, we ask whether financial development grows faster in countries that are further away from

the U.S. in terms of financial development.

3 Unfortunately, we could not incorporate the share of foreign owned banks or other market structure variables in the analysis as their time and country coverage is limited.

13

IV. Results

Table 1 shows the results of estimating equation (1) using the various measures for

financial development. Recall that in those estimations, we do not include any control variables

but we allow for country-specific effects, heterogeneity across countries, and serial correlation

within countries over time. Looking across the three columns of results we see evidence for

convergence for all financial variables with a level of statistical significance falling below 1%

percent. Table 2 adds a range of macroeconomic control variables to the model. We still observe

statistically significant evidence for financial development convergence across the different

measures. Of the control variables, initial income per capita is positive and statistically

significant in all of the models whereas government spending has a negative and statistically

significant effect in two of the three regressions. Trade openness has a positive and statically

significant on the broader financial development measures – financial system credit and liquid

liabilities. Higher inflation reduces the growth of bank credit and liquid liabilities.

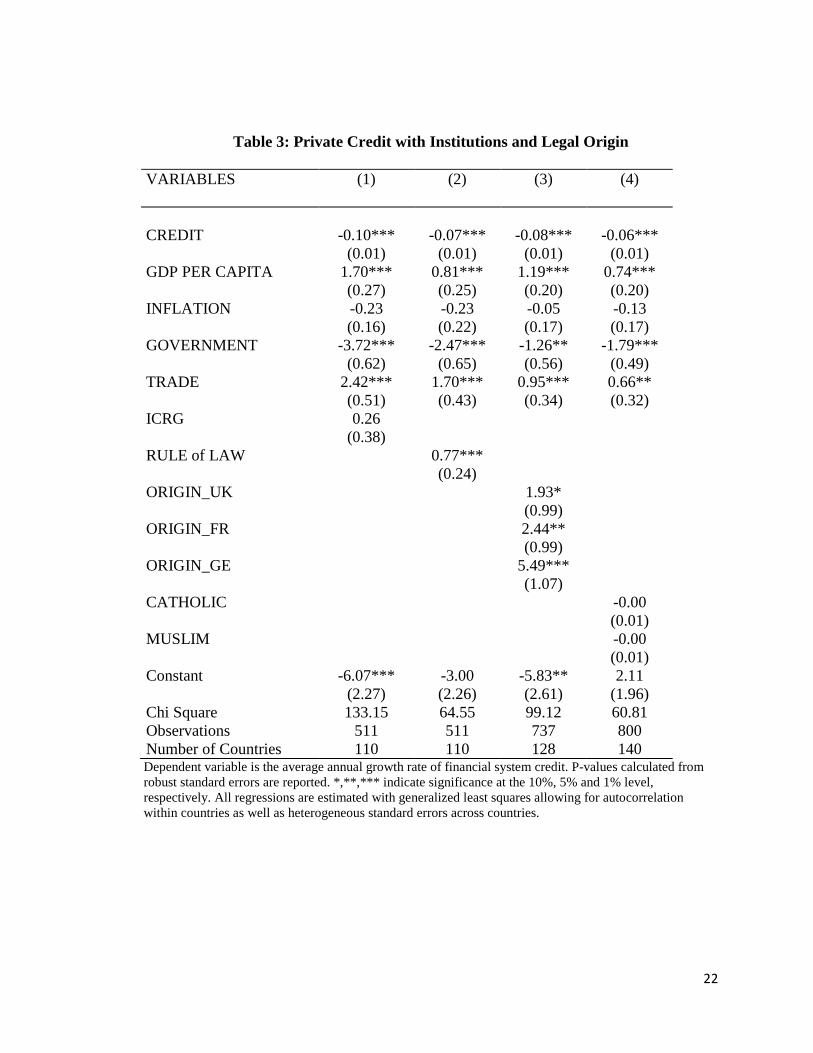

Next, in Table 3 we estimate equation (3) and add various measures for institutions to the

model specification. We focus on financial system credit as that variable is the most widely used

financial development measure in the literature. First, we introduce the ICRG variables, then we

add legal origin, and finally the variables for religious composition. Notice that the initial level

of financial development remains negative and statistically significant across all estimations. The

second column of results suggests that stronger rule of law is associated with more rapid growth

in financial system credit. The third column provides evidence that legal origin also matters. The

British, French, and German legal origins are associated with more rapid credit growth compared

to the omitted Scandinavian legal origin.4

4 There are no countries with Socialist legal origin in the sample.

14

Note that the rank order of the three legal origin variables in terms of coefficient size

suggests that the German legal system is associated with the most rapid credit growth, followed

by the French legal system, and then the British legal system. This runs counter to the results

reported in the earlier literature where the British legal system is associated with the highest level

of financial development. However, here we study the change of financial development. Thus,

the reported coefficient estimates on the legal origin variables provide additional evidence for

convergence: credit grows more rapidly in countries whose legal origin is, in principle,

associated with a lower level of financial development. Interestingly, these results also suggest

that institutions, while a major factor for financial development as identified in the literature do

not restrict completely the convergence of credit levels across countries. In other words, credit

levels converge over time despite differences in institutions across countries. Unlike legal origin,

there is no evidence that religious composition affects the growth of credit. Still, the evidence for

convergence remains statistically significant after controlling for religious composition.

The sizes of the estimated coefficients on the initial credit level, i.e. the estimate of in

Table 3 range between -0.1 and -0.06. If we take the -0.1 estimate, an increase in initial credit of

10 percentage points, e.g. an increase in the credit to GDP ratio from 50 percent to 60 percent, is

associated with a decline in the growth of credit by about 1, i.e. by one percentage point. That is

an economically sizable effect given that the average annual growth rate of credit in the sample

is 4.93 percent. For example, controlling for other factors, as credit in Turkey increased from 14

to 38 percent between 1990-2010, the rate of growth of credit slowed down by 2.4 percentage

points.

In Table 4 we add the four variables that measure the efficiency of financial institutions.

The return on assets is the only variable with statistical significance and has a positive effect on

15

credit growth. More importantly, looking across all the estimations, the evidence for credit

convergence remains similar after the inclusion of the efficiency variables. It seems that

convergence is not a byproduct of an increased efficiency of operation of the financial

institutions.

Next, Table 5 shows estimates from estimating split samples according to the level of

economic development of a country. We use the World Bank categorization to identify four

income groups: low, lower middle, upper middle, and high income. The coefficient estimate on

initial credit is negative and statistically significant in all four samples but its size differs. The

most economically important evidence for convergence is observed in the low income countries

and the slowest convergence is observed in the high income group of countries. The evidence for

the middle income countries is mixed, with a stronger effects for upper middle income countries,

but overall they fall in-between the low and the high income groups in terms of the size of the

coefficient on initial credit.

Table 6 repeats that exercise with groups of countries split according to their average

level of financial development during the sample period. Following Rioja and Valev (2004), we

run estimations for three groups: low, middle, and high level of financial development. The

results suggest a similar pattern to what we observe in Table 5. Convergence is most rapid in

countries with low financial development, followed by the middle group. Convergence is

markedly slower among countries with a high level of financial development.

Next, we report two sets of robustness tests. In Table 7 we estimate the benchmark results

with the ICRG variables, fixed country-specific effects and robust standard errors. As before,

initial credit is negative and statistically significant and the control variables have similar effects.

Then, in Table 8 we follow Aghion et al. (2005) and estimate the benchmark models but taking

16

the U.S. as a frontier county. Here we explore the convergence to the level of financial system

credit in the U.S. The results confirm our earlier findings of a negative and statistical significant

effect of initial credit levels on the subsequent growth in credit.

V. Conclusion

We present evidence that the financial system credit to GDP ratio of different countries,

and other measures of financial development, converge over time. Countries with a lower initial

level of financial development experience more rapid growth of financial development. We

observe convergence for different measures of financial development, with various control sets,

and estimation techniques. Most importantly, convergence is present even after we control for

the quality of institutions. Institutions have been identified as the most important fundamental

determinant of financial development. We find, however, that the levels of financial

development across countries become more similar over time despite the persistent differences in

institutions.

Our analysis has centered on credit variables, leaving aside the question whether stock

markets also exhibit convergence. There are reasons to expect different dynamics. The threshold

level of institutions and economic development that allow stock markets to develop may be

higher for stock markets than for bank credit. Also, while lending to firms and households is

primarily a local activity, stock market activity is concentrated in several large financial centers.

Therefore, our conjecture is that we would not observe similar convergence for stock markets but

we leave that question for future research.

Similarly, we leave to future research to explore the convergence of other aspects of

financial development. While widely used in the literature and available for many countries and

17

years, the credit level is not a perfect measure of financial development. We want to know

whether new credit reaches more firms and households or it services mostly existing customers;

whether it goes mostly to households or firms; what are its uses; etc. Hopefully, future data sets

would allow us to explore the dynamics of these and other aspects of financial development.

18

References

Aghion, Philippe, Peter Howitt, and David Mayer-Foulkes. "The effect of financial development on convergence: Theory and evidence". The Quarterly Journal of Economics, 120 (1) (2005): 173-222. Antzoulatos, Angelos A., Ekaterini Panopoulou, and Chris Tsoumas. "Do Financial Systems Converge?." Review of International Economics 19.1 (2011): 122-136. Beck, Thorsten, Asli Demirgüç-Kunt, and Ross Levine. "Law, endowments, and finance." Journal of Financial Economics 70.2 (2003): 137-181. Beck, Thorsten, Asli Demirguc-Kunt, and Ross Levine. “Finance, inequality, and the poor." Journal of Economic Growth 12 (2007), 27-49.

Beck, T., Buyukkarabacak, B., Rioja, F., & Valev, N. (2012). Who gets the credit? And does it matter? Household vs. firm lending across countries. BE Journal of Macroeconomics, 12(1). Beck, Thorsten and Asli Demirgüç-Kunt. "Financial institutions and markets across countries and over time-data and analysis." World Bank Policy Research Working Paper Series, Vol (2009). Boyd, John H., Ross Levine, and Bruce D. Smith. "The impact of inflation on financial sector performance." Journal of Monetary Economics 47.2 (2001): 221-248. Bruno, Giuseppe, Riccardo De Bonis, and Andrea Silvestrini. "Do financial systems converge? New evidence from financial assets in OECD countries." Journal of Comparative Economics (2011). Büyükkarabacak, Berrak, and Neven T. Valev. "The role of household and business credit in banking crises." Journal of Banking & Finance 34.6 (2010): 1247-1256. Demirgüç-Kunt, Asli, and Leora Klapper. "Measuring Financial Inclusion: The Global Findex Database." World Bank Policy Research Working Paper 6025 (2012). Djankov, Simeon, Caralee McLiesh, and Andrei Shleifer. "Private credit in 129 countries." Journal of Financial Economics 84.2 (2007): 299-329. Durlauf, Steven N. "On the convergence and divergence of growth rates." The Economic Journal 106.437 (1996): 1016-1018. Goldberg, Linda S. "Financial sector FDI and host countries: New and old lessons" FRBNY Economic Policy Review, March, (2007).

19

Greenwood, Robin, and David Scharfstein. "The Growth of Modern Finance." Available at SSRN 2162179 (2012). Huang, Yongfu, and Jonathan Temple. "Does external trade promote financial development?" CEPR discussion paper no. 5150 (2005) Huybens, Elisabeth, and Bruce D. Smith. "Inflation, financial markets and long-run real activity." Journal of Monetary Economics 43.2 (1999): 283-315. Levine, Ross. "Finance and growth: Theory and evidence." Handbook of Economic Growth 1 (2005): 865-934. La Porta, Rafeal, Lopez de Silanes, Florencio, Shleifer, Andrei, and Vishny, Robert. (1997) “Legal determinants of external finance.” Journal of Finance, 52, 1131-1150. La Porta, Rafeal., López de Silanes, Florencio., Shleifer, Andrei., & Vishny, Robert. (1998) “Law and finance.” Journal of Political Economy, 106, 1113-1155. Pritchett, Lant (1997) “Divergence, big time." The Journal of Economic Perspectives 11.3 (1997): 3-17. Rioja, Felix, and Neven Valev. "Does one size fit all?: a reexamination of the finance and growth relationship." Journal of Development Economics 74.2 (2004): 429-447. Romer, Paul M. "Increasing returns and long-run growth." The Journal of Political Economy (1986): 1002-1037. Veysov, Alexander, and Mikhail Stolbov. "Do financial systems converge? A Comprehensive panel data approach and new evidence from a dataset for 102 countries." (2011).

Stulz, Rene M., and Rohan Williamson. "Culture, openness, and finance." Journal of Financial Economics 70.3 (2003): 313-349.

20

Table 1: Unconditional Convergence

(1) (2) (3) VARIABLES Fin System

Credit Bank Credit

Liquid Liabilities

CREDIT -0.029*** (0.00) BANK CREDIT -0.024*** (0.00) LIQUID LIABILITIES -0.021*** (0.01) Constant 4.05*** 4.14*** 3.35*** (0.21) (0.19) (0.27) Chi Square 64.87 59.02 24.91 Observations 842 840 809 Number of countries 143 143 140 Dependent variables are the average annual growth rate of financial system credit, bank credit and liquid liabilities. P-values calculated from robust standard errors are reported. *,**,*** indicate significance at the 10%, 5% and 1% level, respectively. All regressions are estimated with generalized least squares allowing for autocorrelation within countries as well as heterogeneous standard errors across countries.

21

Table 2: Baseline Regressions for all FD variables

(1) (2) (3) VARIABLES Fin System

Credit Bank Credit

Liquid Liabilities

CREDIT -0.05*** (0.01) BANK CREDIT -0.05*** (0.01) LIQUID LIABILITIES -0.05*** (0.01) GDP PER CAPITA 0.61*** 0.55*** 0.27** (0.16) (0.15) (0.13) INFLATION -0.13 -0.36** -0.28** (0.17) (0.17) (0.13) GOVERNMENT -1.25*** -0.58 -1.72*** (0.49) (0.46) (0.50) TRADE 0.60** 0.34 1.13*** (0.28) (0.27) (0.26) Constant 1.50 1.61 2.93* (1.66) (1.58) (1.54) Chi Square 48.51 45.12 63.94 Observations 802 800 770 Number of Countries 141 141 138 Dependent variables are the average annual growth rate of financial system credit, Bank credit and liquid liabilities. P-values calculated from robust standard errors are reported. *,**,*** indicate significance at the 10%, 5% and 1% level, respectively. All regressions are estimated with generalized least squares allowing for autocorrelation within countries as well as heterogeneous standard errors across countries.

22

Table 3: Private Credit with Institutions and Legal Origin

VARIABLES (1) (2) (3) (4) CREDIT -0.10*** -0.07*** -0.08*** -0.06*** (0.01) (0.01) (0.01) (0.01) GDP PER CAPITA 1.70*** 0.81*** 1.19*** 0.74*** (0.27) (0.25) (0.20) (0.20) INFLATION -0.23 -0.23 -0.05 -0.13 (0.16) (0.22) (0.17) (0.17) GOVERNMENT -3.72*** -2.47*** -1.26** -1.79*** (0.62) (0.65) (0.56) (0.49) TRADE 2.42*** 1.70*** 0.95*** 0.66** (0.51) (0.43) (0.34) (0.32) ICRG 0.26 (0.38) RULE of LAW 0.77*** (0.24) ORIGIN_UK 1.93* (0.99) ORIGIN_FR 2.44** (0.99) ORIGIN_GE 5.49*** (1.07) CATHOLIC -0.00 (0.01) MUSLIM -0.00 (0.01) Constant -6.07*** -3.00 -5.83** 2.11 (2.27) (2.26) (2.61) (1.96) Chi Square 133.15 64.55 99.12 60.81 Observations 511 511 737 800 Number of Countries 110 110 128 140 Dependent variable is the average annual growth rate of financial system credit. P-values calculated from robust standard errors are reported. *,**,*** indicate significance at the 10%, 5% and 1% level, respectively. All regressions are estimated with generalized least squares allowing for autocorrelation within countries as well as heterogeneous standard errors across countries.

23

Table 4: Testing the diminishing returns hypothesis – main effects

VARIABLES (1) (2) (3) (4) CREDIT -0.08*** -0.09*** -0.08*** -0.08*** (0.01) (0.01) (0.01) (0.01) GDP PER CAPITA 0.73*** 0.58** 0.62*** 0.73*** (0.21) (0.24) (0.15) (0.16) INFLATION -0.43 -0.40 -0.35 -0.33 (0.30) (0.38) (0.27) (0.29) GOVERNMENT -0.50 0.27 -0.41 -0.34 (0.50) (0.71) (0.38) (0.44) TRADE 1.05* 1.36** 1.05** 1.31*** (0.56) (0.56) (0.41) (0.38) OVERHEAD 9.79 (15.55) INTEREST MARGIN -12.84 (13.96) COST -0.72 (1.42) RETURN ON ASSETS 45.02*** (12.72) Constant -0.18 -0.95 0.83 -2.22 (2.13) (2.47) (1.75) (1.89) Chi Squared 51.93 71.96 55.83 119.08 Observations 310 301 314 315 Number of Countries 107 104 109 109 Dependent variable is the average annual growth rate financial system credit. P-values calculated from robust standard errors are reported. *,**,*** indicate significance at the 10%, 5% and 1% level, respectively. All regressions are estimated with generalized least squares allowing for autocorrelation within countries as well as heterogeneous standard errors across countries.

24

Table 5: Private Credit Convergence for Different Income Levels

(1) (2) (3) (4) VARIABLES Low Lower Middle Upper Middle High CREDIT -0.39*** -0.06*** -0.18*** -0.04*** (0.10) (0.02) (0.02) (0.01) GDP PER CAPITA -0.13 -0.59 3.08*** 0.34 (2.14) (0.69) (0.83) (0.49) INFLATION -1.57** 0.39 -0.51 -0.05 (0.62) (0.37) (0.32) (0.25) GOVERNMENT 1.64 -1.31 -4.68*** -0.24 (1.82) (1.05) (1.46) (0.74) TRADE -1.81 2.34*** 3.22*** 0.88*** (1.90) (0.89) (0.88) (0.31) Constant 15.09 1.21 -15.04* -1.19 (11.38) (4.35) (8.90) (5.00) Chi Square 27.42 20.40 75.15 25.99 Observations 122 216 189 275 Number of Countries 27 35 34 45

Dependent variable is the average annual growth rate of financial system credit. P-values calculated from robust standard errors are reported. *,**,*** indicate significance at the 10%, 5% and 1% level, respectively. All regressions are estimated with generalized least squares allowing for autocorrelation within countries as well as heterogeneous standard errors across countries.

25

Table 6: Private Credit Convergence for Different Financial Development Levels

(1) (2) (3) (4) (5) (6) VARIABLES Low Middle High Low Middle High CREDIT -0.86*** -0.23*** -0.02** -1.40*** -0.73*** -0.13*** (0.11) (0.04) (0.01) (0.25) (0.13) (0.03) CREDIT*CREDIT 0.04*** 0.01*** 0.00*** (0.01) (0.00) (0.00) GDP PER CAPITA 5.52*** 2.00*** 0.26 1.01*** 1.93*** 0.11 (1.74) (0.49) (0.30) (0.37) (0.48) (0.27) INFLATION -0.09 -0.41 -0.17 -1.32*** -0.31 -0.32 (0.46) (0.33) (0.25) (0.45) (0.33) (0.23) GOVERNMENT 1.65 -0.08 0.63 -1.25 0.40 1.28* (2.03) (1.17) (0.81) (1.08) (1.17) (0.76) TRADE 2.30 1.60* 0.21 -0.12 1.62* 0.19 (1.92) (0.87) (0.34) (0.94) (0.88) (0.30) Constant -33.35*** -10.80*** -1.34 13.43*** -4.63 2.18 (12.57) (3.81) (4.33) (3.32) (4.27) (3.85) Chi Squared 72.76 46.88 6.49 72.76 46.88 6.49 Observations 216 295 291 216 295 291 Number of Countries 47 48 46 47 48 46

Dependent variable is the average annual growth rate of financial system credit. P-values calculated from robust standard errors are reported. *,**,*** indicate significance at the 10%, 5% and 1% level, respectively. All regressions are estimated with generalized least squares allowing for autocorrelation within countries as well as heterogeneous standard errors across countries.

26

Table 7: Robustness Test: Fixed Effects and Robust Standard Errors

VARIABLES (1) (2) (3) CREDIT -0.17*** -0.18*** -0.19*** (0.04) (0.04) (0.04) GDP PER CAPITA 8.61*** 12.78*** 12.64*** (2.17) (3.63) (3.67) INFLATION -0.31 0.12 0.10 (0.61) (0.76) (0.78) GOVERNMNENT -4.32** -7.18*** -6.69*** (1.98) (2.48) (2.47) TRADE 2.48 3.63 3.45 (1.87) (2.69) (2.72) ICRG 0.17 (1.12) RULE of LAW 1.26* (0.65) Constant -54.22*** -85.78*** -89.27*** (14.77) (27.55) (27.76) Chi Squared 6.23 5.87 6.66 Observations 808 516 516 R-squared 0.10 0.13 0.14 Number of Countries 147 115 115

Dependent variable is the average annual growth rate of financial system credit. P-values are calculated from robust standard errors are reported. *,**,*** indicate significance at the 10%, 5% and 1% level, respectively. All regressions are estimated with fixed effects and robust standard error.

27

Table 8: Convergence relative to the Frontier (USA)

VARIABLES (1) (2) (3) (4) (5) CREDIT -0.06*** -0.06*** -0.06*** -0.03*** -0.05*** (0.01) (0.01) (0.01) (0.00) (0.01) GDP PER CAPITA 1.22*** 1.07*** 0.98*** 0.61*** 0.92*** (0.24) (0.29) (0.28) (0.17) (0.21) INFLATION 0.54*** 0.74*** 0.75*** 0.36** 0.47** (0.21) (0.23) (0.24) (0.18) (0.19) GOVERNMENT -1.09 0.23 0.04 0.41 -0.52 (0.81) (0.79) (0.80) (0.57) (0.68) TRADE -0.56 0.78 0.69 -0.40 -0.51 (0.44) (0.50) (0.50) (0.26) (0.33) ICRG 0.44 (0.40) RULE of LAW 0.51* (0.28) ORIGIN_UK 0.65 (0.65) ORIGIN_FR 0.50 (0.69) ORIGIN_GE 1.92** (0.81) CATHOLIC -0.00 (0.01) MUSLIM -0.01 (0.01) Constant -8.91*** -19.62*** -18.50*** -7.27*** -7.10*** (3.12) (3.25) (3.29) (2.43) (2.65) Chi Squared 83.45 97.07 91.29 60.76 78.73 Observations 804 512 512 739 802 Number of Countries 141 110 110 128 140

Dependent variable is the average annual growth rate of financial system credit. P-values calculated from robust standard errors are reported. *,**,*** indicate significance at the 10%, 5% and 1% level, respectively. All regressions are estimated with generalized least squares allowing for autocorrelation within countries as well as heterogeneous standard errors across countries.

28

Summary Statistic Bank Credit to

GDP Fin. System Credit to

GDP Liquid Liabilities to

GDP Credit

Growth Bank Credit

Growth LL

Growth GDP per

Inflation Government Trade Openness

ICRG RULE of LAW

Mean 37.42 40.73 57.33 4.9326 5.0328 2.9650 6541. 51.5714 15.8004 73.6444 2.9149 3.6616

Standard Deviation 35.75 38.28 35.29 14.3181 14.5072 6.6262 10431 703.1084 6.3926 46.6972 1.1595 1.4665

Minimum 0.83 0.84 1.21 -17.6568 -17.6568 -19.9553 58.4599 -9.0736 0.0000 0.0000 0.0000 0.0000

Maximum 261.45 265.90 115.2917 292.2205 292.2205 73.8810 105147 23773 69.5428 421.5666 5.3333 6.0000

Correlation

Bank Credit 1

Fin. System Credit 0.9033 1

Value Traded 0.5601 0.6208

Turnover 0.4095 0.4608

Liquid Liabilities 0.7447 0.6678 1

Credit Gr. -0.0003 -0.0165 -0.1497 1

Bank Credit Gr. 0.0089 -0.0297 -0.1511 0.9604 1

Value Traded Gr. -0.0851 -0.0894 -0.0517 -0.0271 -0.0228

Turnover Gr. -0.044 -0.0255 -0.0467 -0.0605 -0.06

Liq. Liab. Gr. 0.0267 -0.0012 -0.0117 0.5572 0.5394 1

GDP pc 0.657 0.7072 0.5898 -0.1037 -0.0923 -0.0971 1

Inflation -0.3465 -0.3515 -0.2867 -0.0226 -0.0337 0.004 -0.3054 1

Gov. Spending 0.3443 0.3501 0.1738 0.0352 0.0501 -0.0136 0.4592 -0.2508 1

Trade Open. 0.2711 0.2184 0.4147 0.0044 0.0038 0.0011 0.153 -0.1461 0.0043 1

ICRG 0.6019 0.6217 0.45 -0.1046 -0.1013 -0.0968 0.7884 -0.259 0.5387 0.1502 1

Rule of RULE of LAW 0.5546 0.5438 0.4304 0.0237 0.0369 -0.0038 0.6887 -0.255 0.5098 0.1925 0.8826 1