Embed Size (px)

Citation preview

Seite 1

Financial Crises and Coordination

Preliminaries

lectures: Thursday 12:15 – 13:45, H 2033

Exercise class by Christian Basteck: Thursday 8:30-10 a.m., H 2033start: Thursday, 19.4.12

Office hour Heinemann: Tuesday 2 – 3 p.m., H 5107 or by appointment (e-mail)

Final Exam during the term break, 16.7.12, 10:00, room H 0107

Exercises, slides, and some of the additional literature is available at thewebsite of the Chair of Macroeconomics:

http://www.macroeconomics.tu-berlin.de/

Some books from reading list are available at the Library (Wiwidok, Semesterapparat)

Summer term 2012

Seite 2

Literature

General reading

Allen, Franklin, and Douglas Gale (2009): Understanding Financial Crises, Oxford Univ. Press.

Kindleberger, Charles P., and Robert Z. Aliber (2005) Manias, Panics, and Crashes: A History of Financial Crises, 5th edition, Palgrave Macmillan.

Reinhart, Carmen, and Kenneth Rogoff (2009): This Time is Different, Princeton Univ. Press.

Aschinger, Gerhard (2001), Währungs- und Finanzkrisen, Vahlen, München.

Specialized reading for various parts of the course:

see course website

http://www.macroeconomics.tu-berlin.de/menue/teaching_-_lehre/financial_crises_and_coordination/

Seite 3

Aims of the course

Understanding causes and mechanisms of banking and currency crises, their resolution, and means of prevention Typical phases of financial crises Credit expansion Bubbles The role of speculation Information asymmetries, herding, and contagion, Speculative attacks, bursting bubbles, bank runs: reversal of capital

flows Coordination of traders / creditors Self fulfilling prophecies and behavioral theories of equilibrium

selection The effects of transparency Moral Hazard issues and banking regulation

Seite 4

Contents

Part I. Characteristics and Origins of Financial Crises

1. Introduction

2. Phases of financial crises

3. Exchange rates

4. The role of speculation

5. Efficiency of financial markets

6. Bubbles in the overlapping generations model

7. The subprime crisis 2007-2009 / Euro crisis 2010-2012?

Part II. Theories of Financial Crises

8. Currency crises

9. Banking crises

10. Connection between banking and currency crises

Seite 5

Part III. Coordination Games

11. Equilibrium selection

12. Theory of global games

13. Experimental evidence on coordination games

14. The role of information and transparency

Part IV. Moral Hazard and Banking Regulation

15. Moral hazard in banking

16. Banking regulation

Contents

Seite 6

1. Introduction

What is a crisis?

Currency crisis: strong unexpected devaluation in short time

In countries with fixed exchange rate a currency crisis is easy to identify. It usually goes along with a breakdown of the currency regime.

Banking crisis: Illiquidity of one or several important financial intermediaries (banks, insurance companies, hedgefonds etc.)

Asset market crises: rapid decline of asset prices (stocks, real estate)

Frequency: since 1980 we had on average 2-3 currency crises and 1-2 banking crises per year

Some of the most important recent crises:

Japan 1990s, East Asia 1997/98, LTCM 1998, dot.com bubble 2000, Argentina 2001, subprime crisis 2007-09

Seite 7

Bordo et al. (2001)

Seite 8

Average frequency of crises (% per annum per country)

Bordo et al. (2001)

Seite 9

Bordo et al. (2001)

Average frequency of crises (% per annum per country)

Seite 10

Seite 11

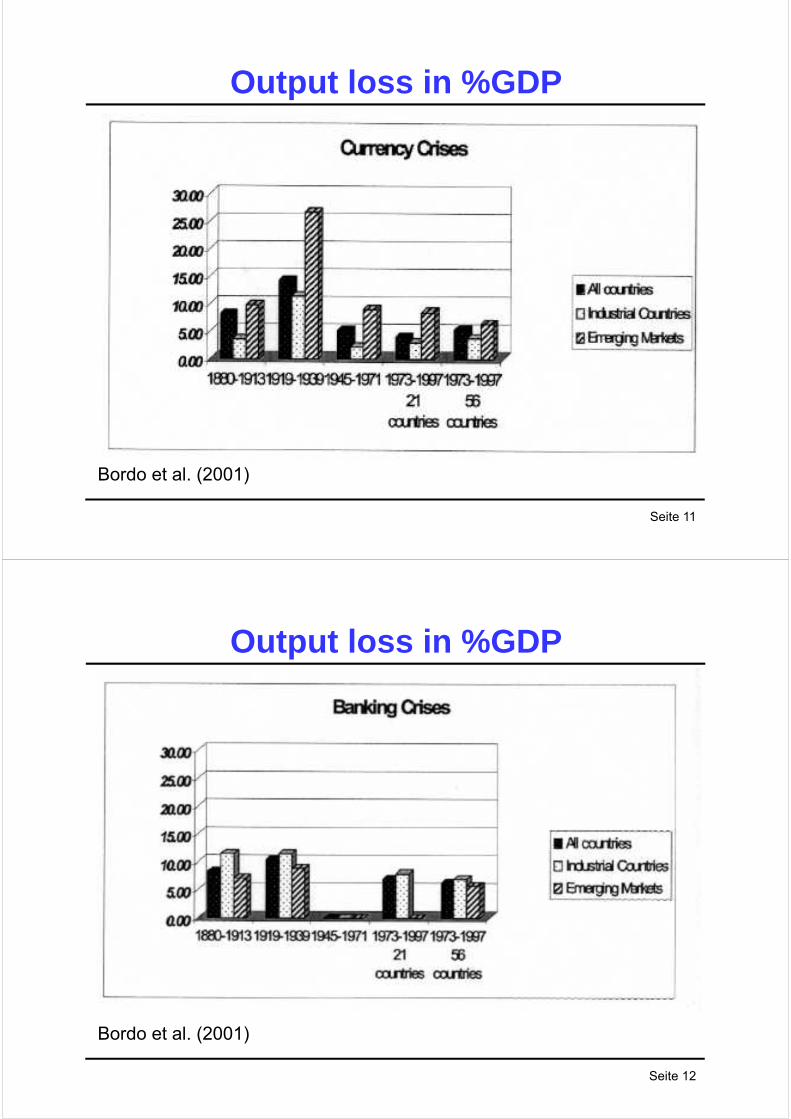

Output loss in %GDP

Bordo et al. (2001)

Seite 12

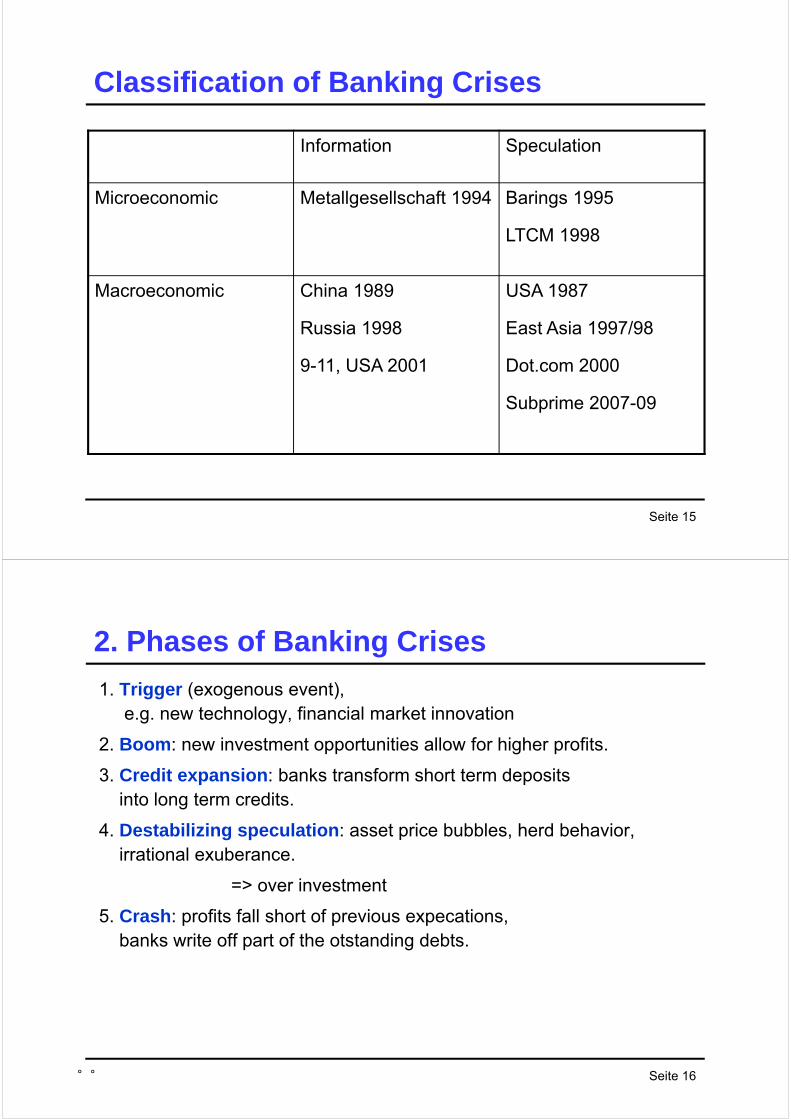

Output loss in %GDP

Bordo et al. (2001)

Seite 13

Output loss in %GDP

Bordo et al. (2001)

Seite 14

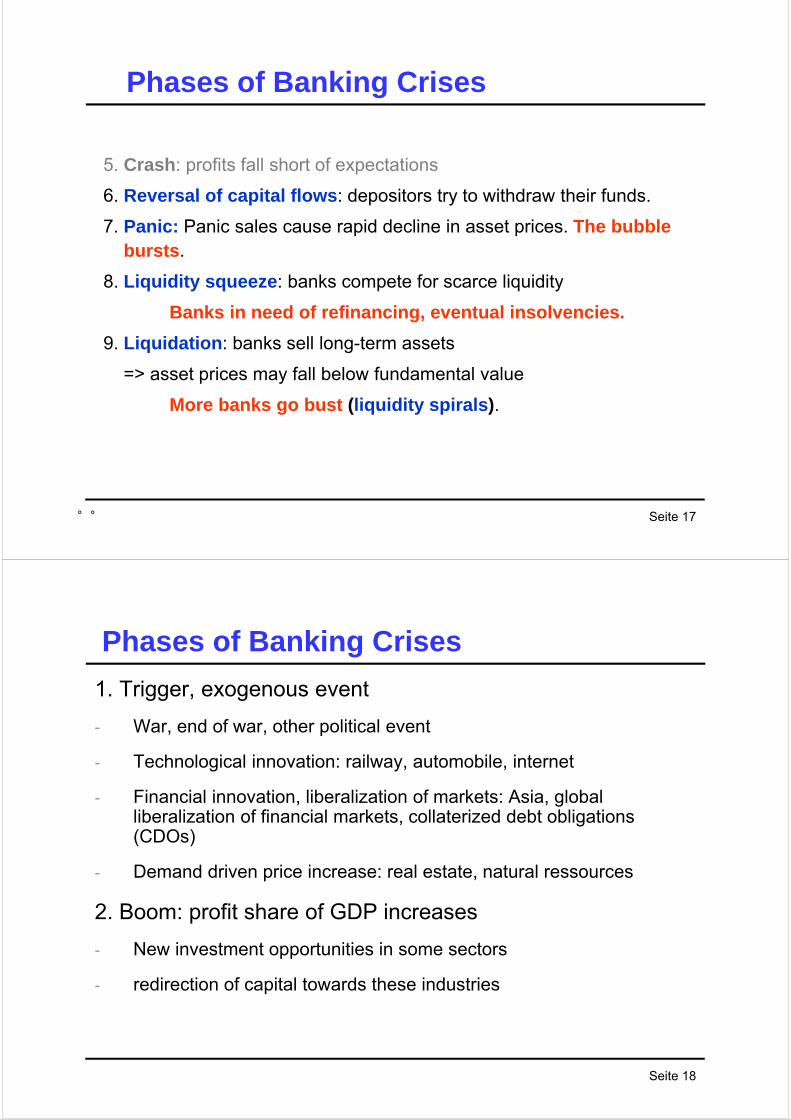

Classification of Banking Crises- Microeconomic crisis: a single institute in distress

- Macroeconomic crisis: concerns a whole economy (also systemic crisis)

Microeconomic crises may grow by contagion towards a macroeconomic crisis (systemic risk)

Classification by causes:

- Information: crisis triggered by information that calls for a reevaluation of assets (fundamental values).→ no market failure, stabilizing speculation

- Speculation: Speculation leads to unsustainable asset prices. → market failure: destabilizing speculation

Speculative bubbles may burst after minor reevaluations caused by information of secondary importance.

Seite 15

Classification of Banking Crises

Information Speculation

Microeconomic Metallgesellschaft 1994 Barings 1995

LTCM 1998

Macroeconomic China 1989

Russia 1998

9-11, USA 2001

USA 1987

East Asia 1997/98

Dot.com 2000

Subprime 2007-09

Seite 16

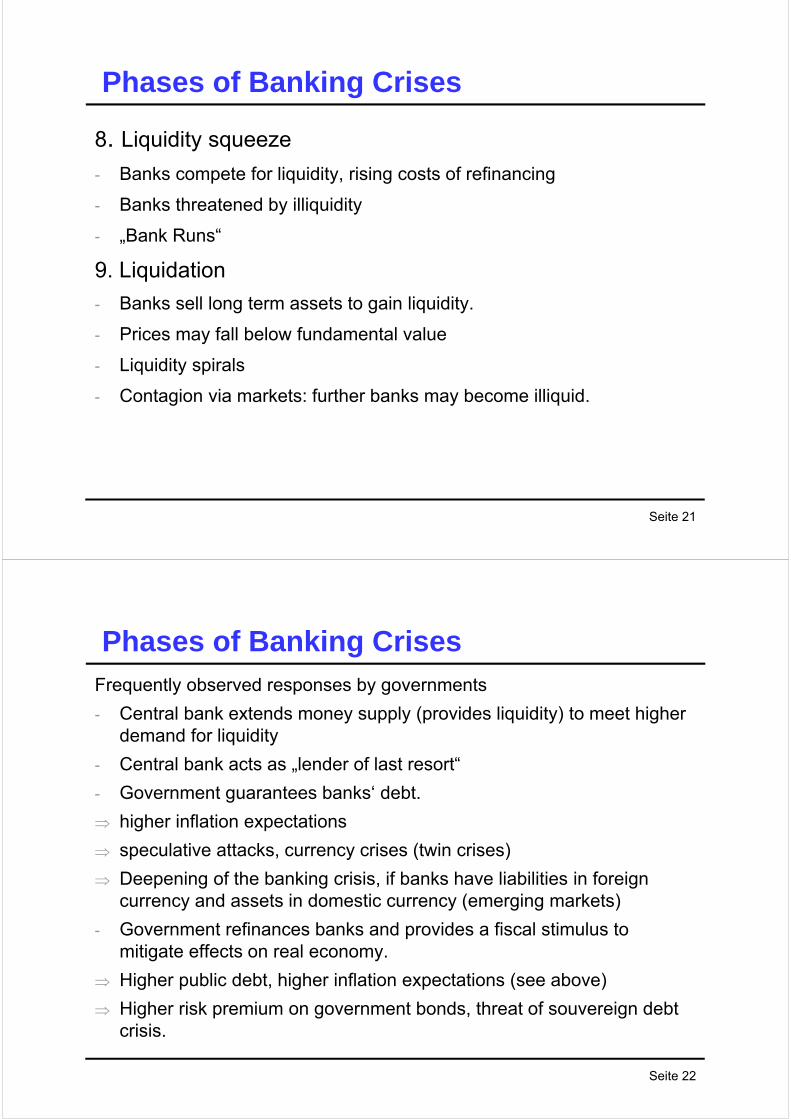

2. Phases of Banking Crises

1. Trigger (exogenous event), e.g. new technology, financial market innovation

2. Boom: new investment opportunities allow for higher profits.

3. Credit expansion: banks transform short term depositsinto long term credits.

4. Destabilizing speculation: asset price bubbles, herd behavior, irrational exuberance.

=> over investment

5. Crash: profits fall short of previous expecations, banks write off part of the otstanding debts.

Seite 17

Phases of Banking Crises

5. Crash: profits fall short of expectations

6. Reversal of capital flows: depositors try to withdraw their funds.

7. Panic: Panic sales cause rapid decline in asset prices. The bubble bursts.

8. Liquidity squeeze: banks compete for scarce liquidity

Banks in need of refinancing, eventual insolvencies.

9. Liquidation: banks sell long-term assets

=> asset prices may fall below fundamental value

More banks go bust (liquidity spirals).

Seite 18

Phases of Banking Crises

1. Trigger, exogenous event

- War, end of war, other political event

- Technological innovation: railway, automobile, internet

- Financial innovation, liberalization of markets: Asia, global liberalization of financial markets, collaterized debt obligations (CDOs)

- Demand driven price increase: real estate, natural ressources

2. Boom: profit share of GDP increases

- New investment opportunities in some sectors

- redirection of capital towards these industries

Seite 19

Phases of Banking Crises

3. Credit expansion

- Financial innovations that substitute moneay: bills of eschange, clearinghouses, predated cheques, Eurodollar („offshore banking“)

- Raising the collateral value of real estate or stocks.

- Ponzi-Games: „call money“

- Term transformation: financing long term investment by short term credit.

4. Destabilizing speculation

- Price bubbles

- Herd behaviour: „rational herding“

- irrational exuberance

- Over investment → „Tobin‘s q“

Seite 20

Phases of Banking Crises

5. Crash

- Information about limits to price bubbles in the near future

- Realized returns lower than expected

- Change in financial conditions (rising interest rate, regulation)

- Stop in the inflow of funds

6. Reversal of capital flow

- Threat of illiquidity of financial intermediaries

- Depositors try to withdraw their funds

7. Panic

- Panic sales trigger a collapse of asset prices. The bubble bursts

- Contagion due to information spillovers

Seite 21

Phases of Banking Crises

8. Liquidity squeeze

- Banks compete for liquidity, rising costs of refinancing

- Banks threatened by illiquidity

- „Bank Runs“

9. Liquidation

- Banks sell long term assets to gain liquidity.

- Prices may fall below fundamental value

- Liquidity spirals

- Contagion via markets: further banks may become illiquid.

Seite 22

Phases of Banking CrisesFrequently observed responses by governments

- Central bank extends money supply (provides liquidity) to meet higher demand for liquidity

- Central bank acts as „lender of last resort“

- Government guarantees banks‘ debt.

higher inflation expectations

speculative attacks, currency crises (twin crises)

Deepening of the banking crisis, if banks have liabilities in foreign currency and assets in domestic currency (emerging markets)

- Government refinances banks and provides a fiscal stimulus to mitigate effects on real economy.

Higher public debt, higher inflation expectations (see above)

Higher risk premium on government bonds, threat of souvereign debt crisis.

Seite 23

3. Exchange rates

What determines exchange rates?

Advantages and disadvantages of different currencyregimes

How does the impact of policy measures depend on thecurrency regime? Mundell Fleming Model

Theoriy of optimum currency areas (Mundell)

Why do we observe high volatility exchange rates? Dornbusch Overshooting Modell

Why are regimes with fixed exchange rates vulnerable forspeculative attacks? Krugman, Obstfeld, Morris / Shin

Seite 24

Exchange rates – equilibrium concepts:current account balance (equilibrium in flows)Export and import adjust slowly (if domestic currency is undervalued imports are expensive, exports are cheap current account balance becomes positive inflow of foreign currency excess demand for domestic currency on FX market appreciation of domestic currency).slow process, compounded by transaction costs current accounts and trade flows affect exchange rates only in the long run.

Capital market equilibrium (equilibrium in stocks)demand and supply of assets must be equal. Large stocks small relative changes of portfolios have strong price

effects. In the short run, exchange rate movements are dominated

by capital markets.

Seite 25

Purchasing power parity (PPP)

What determines trend of exchange rates in the long run?

Absolute purchasing power parity:

All tradable goods should have the same price everywhere (law of one price)

Relative price: ε = E P*/ P = 1

If ε >1: domestic goods are cheaper than foreign goods

Consequence: Increase in exports / decrease in imports => no stationary equilibrium

Seite 26

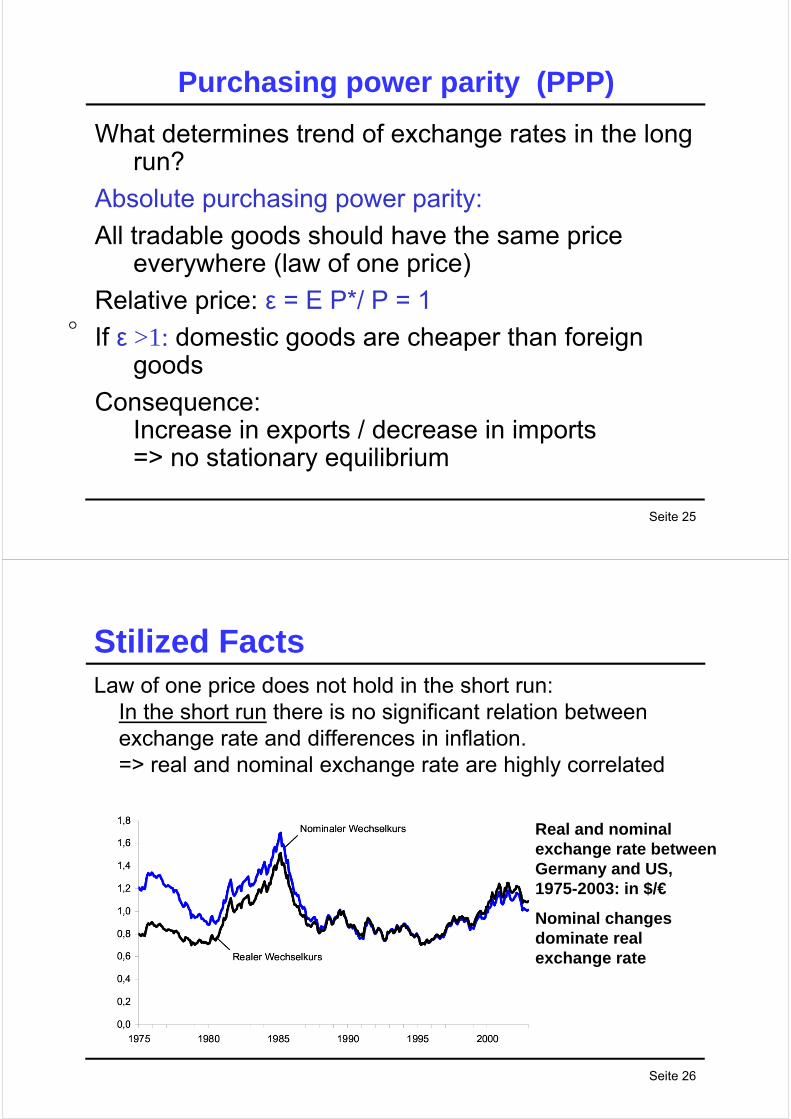

Stilized FactsLaw of one price does not hold in the short run:

In the short run there is no significant relation between exchange rate and differences in inflation. => real and nominal exchange rate are highly correlated

Real and nominal exchange rate between Germany and US, 1975-2003: in $/€

Nominal changes dominate real exchange rate

Seite 27

Interest rate parity

Swaps, Hedging and Speculation

Exchange rate as a future-oriented price for assets –central idea: differences between interest rates are equal to expected change of exchange rate

Covered and uncovered interest rate parity:

Distinguish exchange rate at fututes market Ft and expected rate at spot market E(St+1)

1) Covered interest rate parity (CIP):

no arbitrage by risk free transactions at FX market: (swaps as risk free arbitrage)

2) Uncovered interest rate parity (UIP):

equilibrium between expected effective returns without securitization

Seite 28

Covered interest rate parityAnnual return on X € investment:

Effective return must be the same on all markets, if exchange rate risks are covered

Eurobond X

$-bondX / St

Buy $ at spot market rate St

1+i*

Return:

X (1+i)

1+i

Sell $ at future market rate Ft

Return in €:X (1+i*) Ft / St

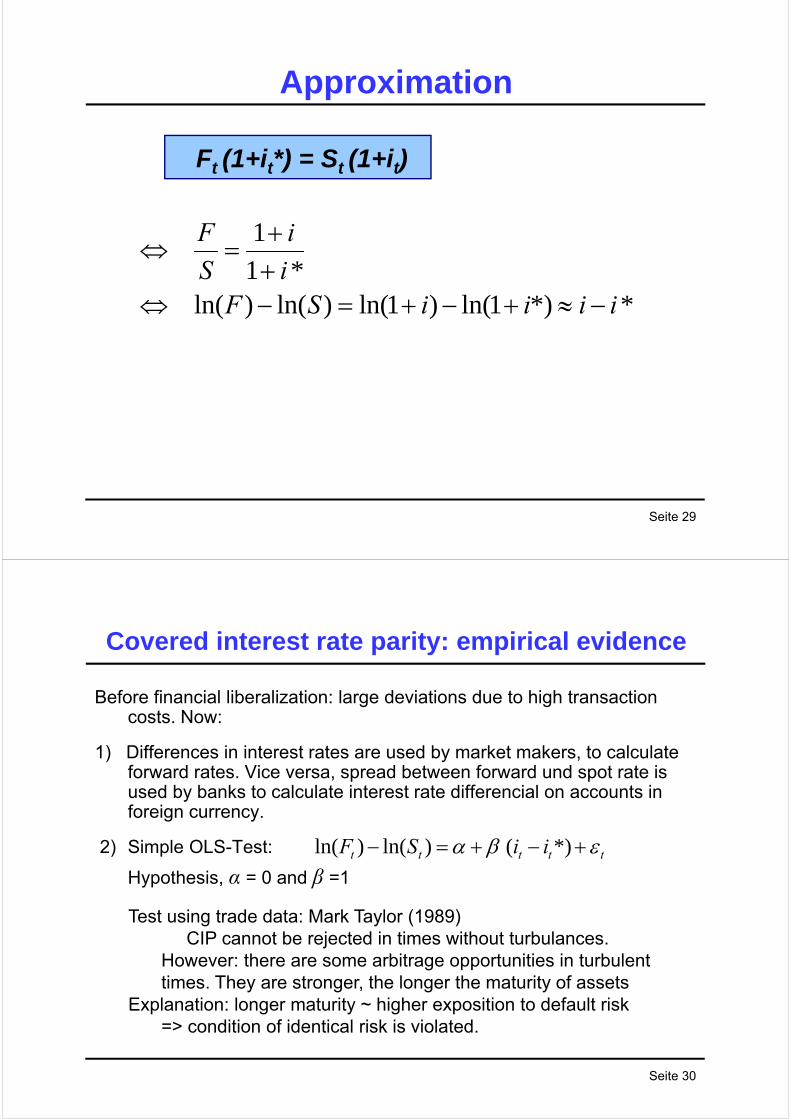

Ft (1+it*) = St (1+it)CIP (covered interest parity):

Seite 29

Approximation

**)1ln()1ln()ln()ln(*1

1

iiiiSFi

i

S

F

Ft (1+it*) = St (1+it)

Seite 30

Covered interest rate parity: empirical evidence

Before financial liberalization: large deviations due to high transaction costs. Now:

1) Differences in interest rates are used by market makers, to calculate forward rates. Vice versa, spread between forward und spot rate is used by banks to calculate interest rate differencial on accounts in foreign currency.

2) Simple OLS-Test:

Hypothesis, α = 0 and β =1ttttt iiSF *)()ln()ln(

Test using trade data: Mark Taylor (1989) CIP cannot be rejected in times without turbulances.

However: there are some arbitrage opportunities in turbulent times. They are stronger, the longer the maturity of assets

Explanation: longer maturity ~ higher exposition to default risk => condition of identical risk is violated.

Seite 31

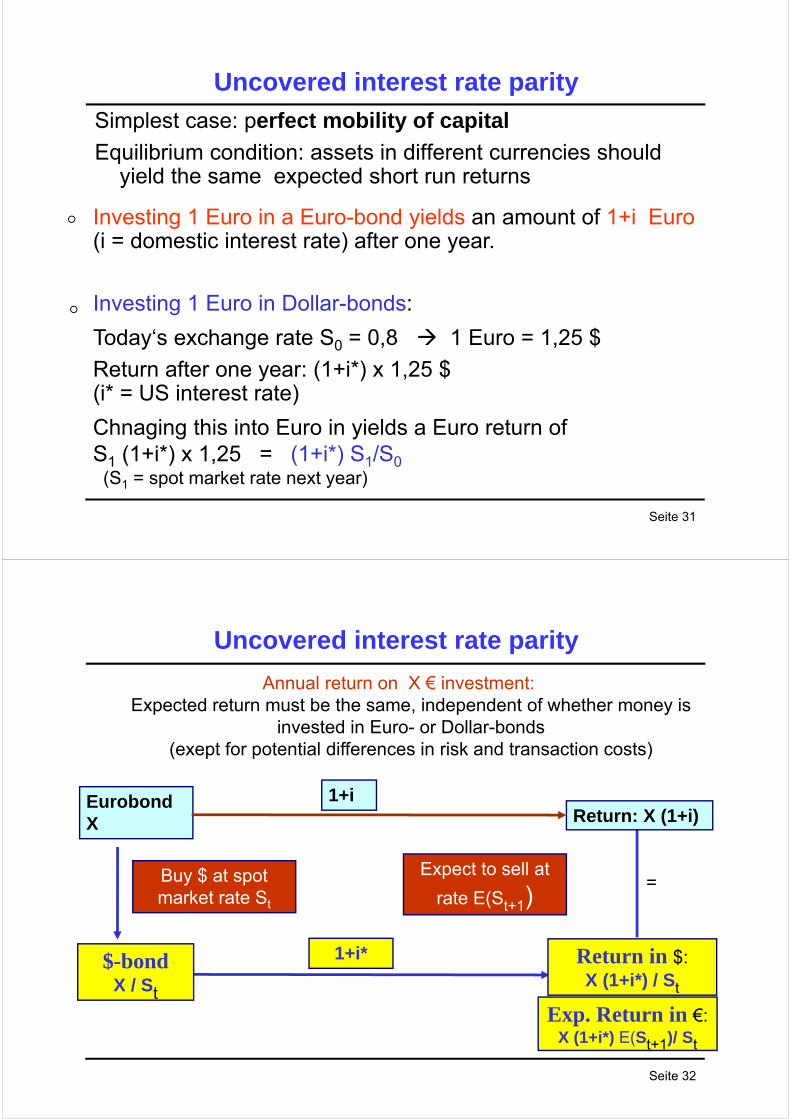

Uncovered interest rate parity

Simplest case: perfect mobility of capital

Equilibrium condition: assets in different currencies should yield the same expected short run returns

Investing 1 Euro in a Euro-bond yields an amount of 1+i Euro(i = domestic interest rate) after one year.

Investing 1 Euro in Dollar-bonds:

Today‘s exchange rate S0 = 0,8 1 Euro = 1,25 $

Return after one year: (1+i*) x 1,25 $(i* = US interest rate)

Chnaging this into Euro in yields a Euro return of S1 (1+i*) x 1,25 = (1+i*) S1/S0(S1 = spot market rate next year)

Seite 32

Uncovered interest rate parity

Eurobond X

$-bondX / St

Buy $ at spot market rate St

1+i*

Return: X (1+i)

Return in $:X (1+i*) / St

Exp. Return in €:X (1+i*) E(St+1)/ St

Expect to sell at

rate E(St+1)

Annual return on X € investment:Expected return must be the same, independent of whether money is

invested in Euro- or Dollar-bonds(exept for potential differences in risk and transaction costs)

1+i

=

Seite 33

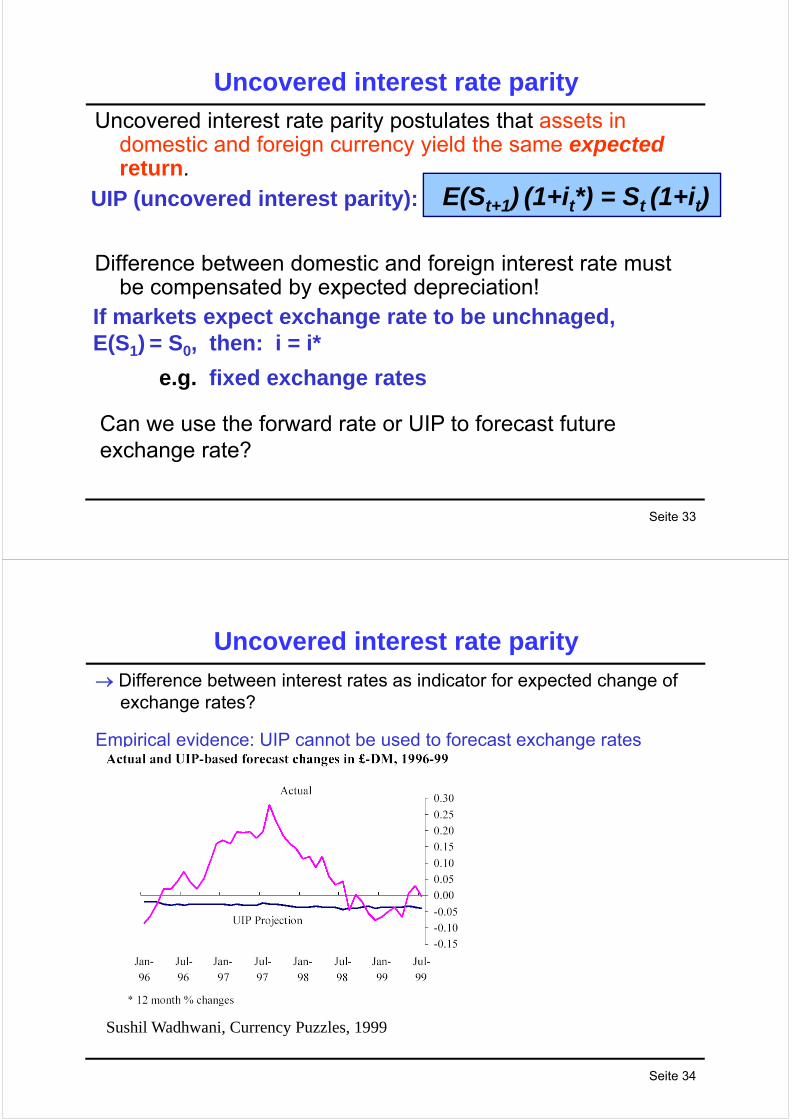

Uncovered interest rate parity

Uncovered interest rate parity postulates that assets in domestic and foreign currency yield the same expectedreturn.

Difference between domestic and foreign interest rate must be compensated by expected depreciation!

If markets expect exchange rate to be unchnaged, E(S1) = S0, then: i = i*

e.g. fixed exchange rates

E(St+1) (1+it*) = St (1+it)UIP (uncovered interest parity):

Can we use the forward rate or UIP to forecast future exchange rate?

Seite 34

Uncovered interest rate parity

Difference between interest rates as indicator for expected change of exchange rates?

Empirical evidence: UIP cannot be used to forecast exchange rates

Sushil Wadhwani, Currency Puzzles, 1999

Seite 35

Uncovered interest rate parity – empirical evidence

Empirical evidence: hypothesis of UIP is rejected by all studies

Problem: expected exchange rate cannot be observed

For rational expectation, the error term should be uncorrelated with all information that is already available at the time when expectations are formed.

Thus, UIP implies:

Consistent OLS-estimator

Hypothesis, α = 0 and β =1.

1*

1 ttttt iiss

1t*ttt1t )ii(ss

)s(Es 1t1t1t

Seite 36

Uncovered interest rate parity – empirical evidence

UIP is always rejected: spreads can explain only a small part of movements in the exchange rate. Even the predicted direction of adjustments is often misleading.

Empirical tests: ß is significantly different from 1 (in most cases ß is even negative). Also, significant difference of α from 0.

Actual changes seem to be driven by unexpected news: ln(s) follows a random walk, while interest rate differential is autocorrelated over time.

Possible reasons for rejecting UIP?

Random Walk Puzzle: Predictions of exchange rate by theoretical models are not better than a random walk.

Seite 37

Uncovered interest rate parity – empirical evidence

1) varying risk premium or other fundamentals (but: why is it systematic?)

2) Indeterminacy of fundamentalsPeso problem: Expectations about a depreciation do not need to realizein the period under investigation. A positive probability for a currencycrisis justifies a higher interest rate, even when the crisis never occurs.

3) Speculation? (Ir-) rational bubbles?Market participants have incomplete informationen and need to deriveinformation from price movements Herd behavior; noise traders (behavioral finance); rational bubbles

4) Monetary authorities set interest rates to work against undesiredchanges in the exchange rates – simultaneity bias (McCallum)

Possible reasons for rejecting UIP

Seite 38

Carry Trades

An investor borrows a currency with a low interestrate, converts it on the spot market to buy bonds in a currency with a high interst rate.

Example: interest rate in Japan 1%, in US 4%. Trader borrows 100,000 Yen = 1,000 $ and buysUS govt. bonds. One year later, he gets 1,040 $. Ifexchange rate is still 100:1, he gets 104,000 Yen, pays back 101,000 Yen and has a profit of 3,000 Yen.

Carry trades speculate on violations of UIP!