Embed Size (px)

Citation preview

Financial andFinancial andCost-Volume-Profit ModelsCost-Volume-Profit Models

Chapter 12Chapter 12

Financial ModelingQuantitative simulation of relations among

various factors

Allows the organization to assess “what if” scenarios to support

Decision making

Forecasting

Cost-Volume-Profit ModelsIllustrates the relationship between sales

volume, costs and revenues

Based on variable (direct) costing

Sales – variable costs = contribution margin

Each additional unit sold “contributes” that amount to the bottom line

Breakeven point is reached when total contribution equals total fixed costs

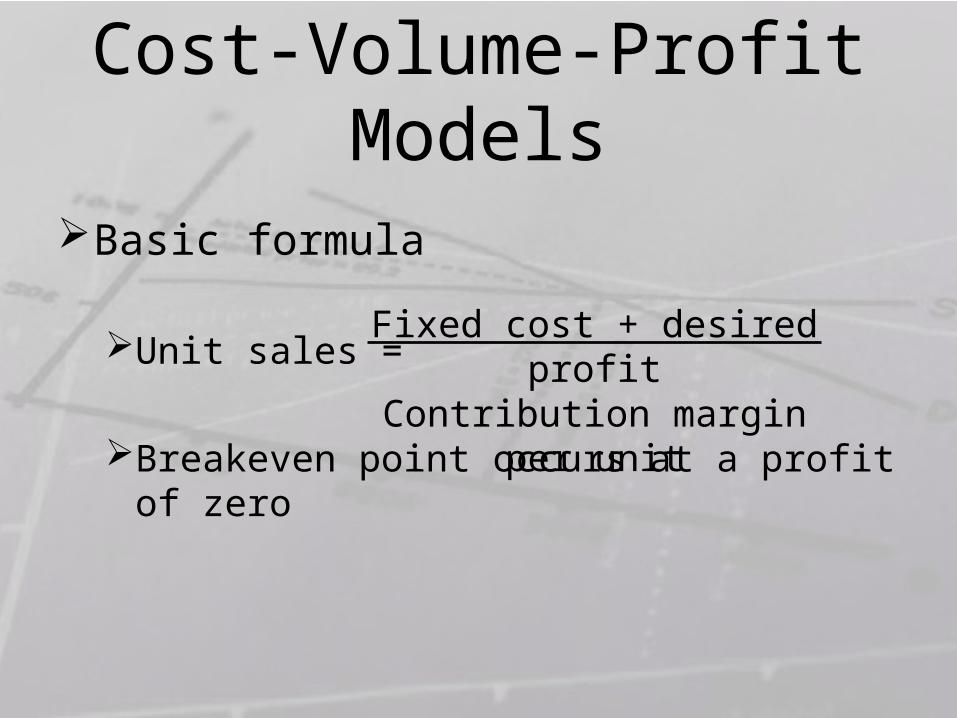

Cost-Volume-Profit Models

Basic formula

Unit sales =

Breakeven point occurs at a profit of zero

Fixed cost + desired profitContribution margin per unit

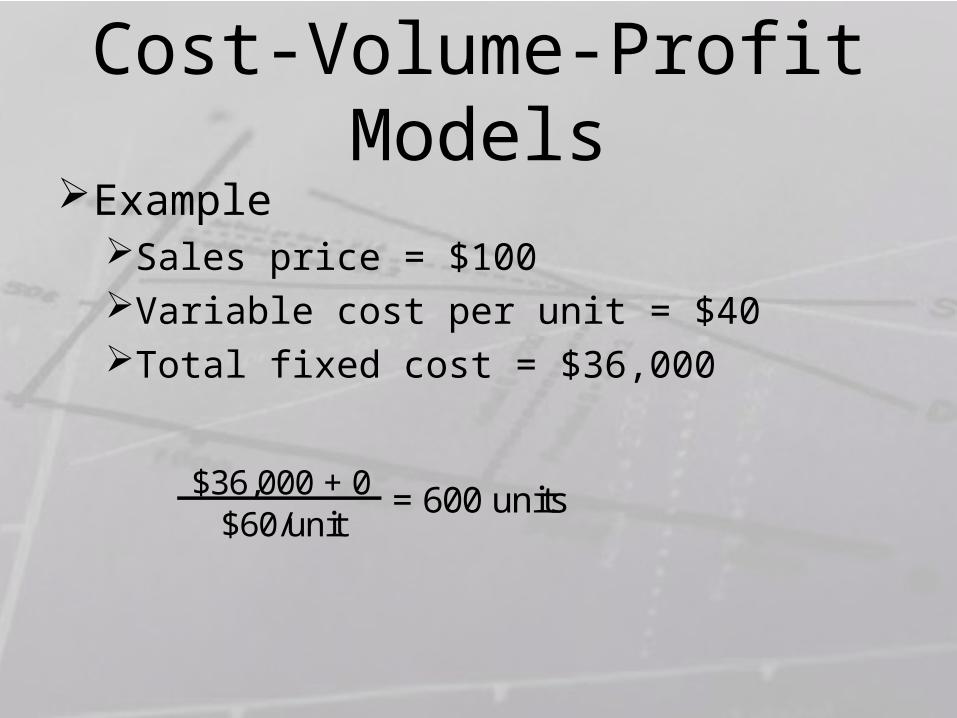

Cost-Volume-Profit ModelsExample

Sales price = $100Variable cost per unit = $40Total fixed cost = $36,000

= 600 units$36,000 + 0$60/unit

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

$180,000

010

020

030

040

050

060

070

080

090

01,

000

1,10

01,

200

1,30

01,

400

1,50

01,

600

Unit sales

Re

ve

nu

e a

nd

co

sts

Fixed cost Total cost Revenue

Variable cost

Profit

Loss

Breakevenpoint

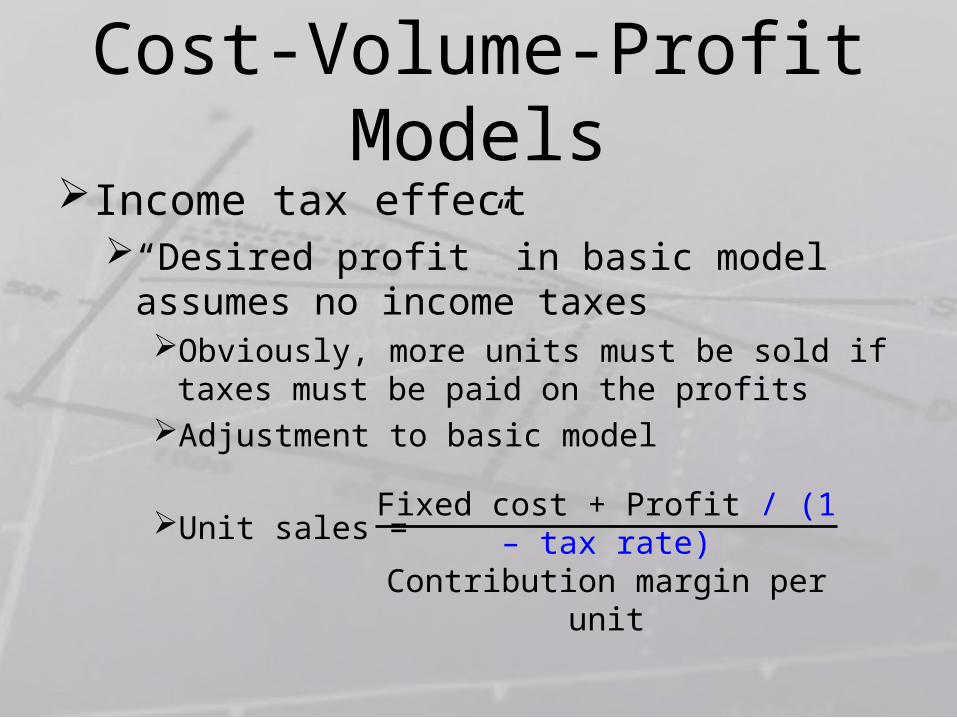

Cost-Volume-Profit ModelsIncome tax effect

“Desired profit” in basic model assumes no income taxesObviously, more units must be sold if taxes must

be paid on the profitsAdjustment to basic model

Unit sales = Fixed cost + Profit / (1 – tax rate)

Contribution margin per unit

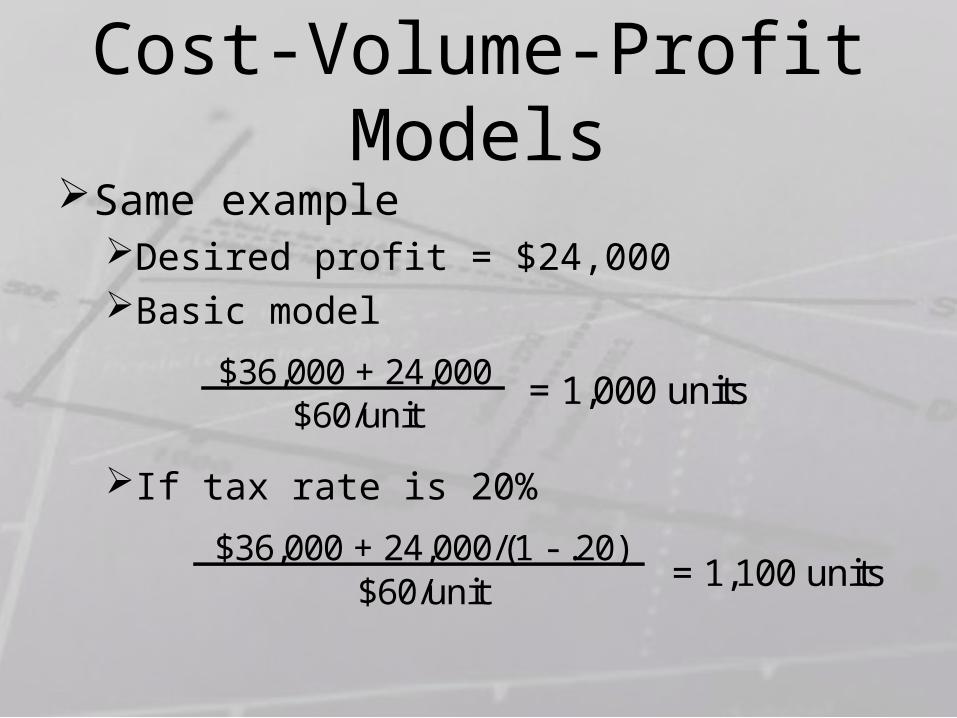

Cost-Volume-Profit ModelsSame example

Desired profit = $24,000Basic model

If tax rate is 20%

$36,000 + 24,000$60/unit

= 1,000 units

$36,000 + 24,000/(1 - .20)$60/unit = 1,100 units

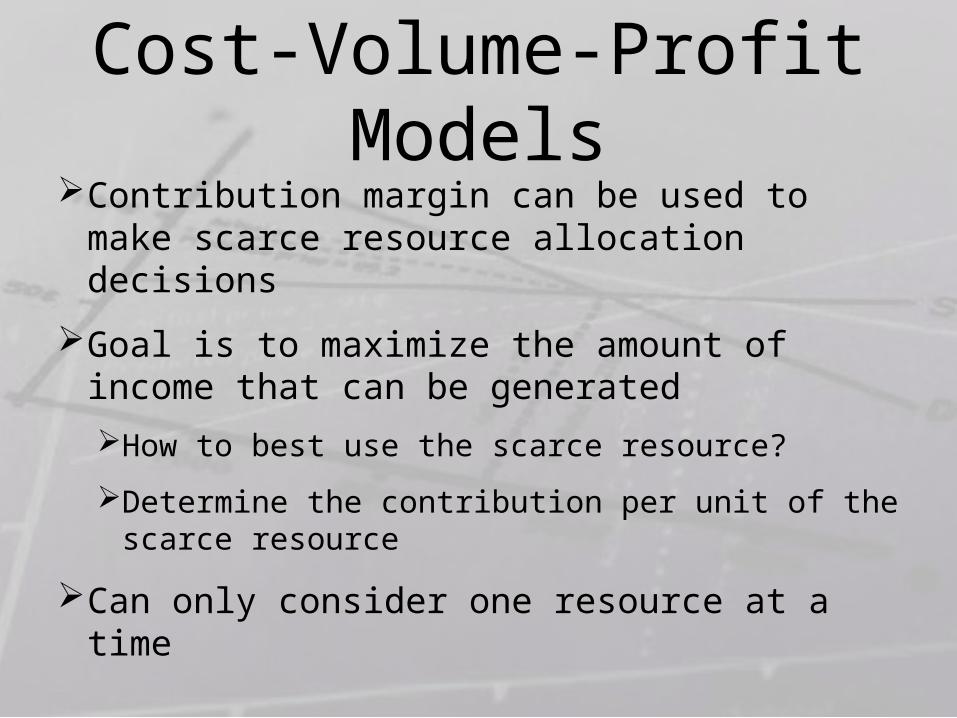

Cost-Volume-Profit ModelsContribution margin can be used to make

scarce resource allocation decisions

Goal is to maximize the amount of income that can be generated

How to best use the scarce resource?

Determine the contribution per unit of the scarce resource

Can only consider one resource at a time

Product A Product B Product C Product DSales price 100$ 210$ 380$ 450$ Variable cost/unit 72 90 200 210 Contribution margin 28$ 120$ 180$ 240$ Units of scarce resources required for each unit of product 2 5 6 12 Contribution margin per unit of scarce resource 14$ 24$ 30$ 20$

What is the best use of 300 units of the resource?

Cost-Volume-Profit ModelsMultiple product situations

Basic model assumes only one productMultiple product situation replaces the

contribution margin per unit with the weighted average contribution marginBased on the normal relative sales volumes of the

products

Resulting “units to sell” is then divided among the products in their original proportions

Cost-Volume-Profit ModelsExample

ProductSelling price

Var.cost per unit

CM per unit

Relative sales

Weighted CM per unit

Folders 1.00$ 0.40$ 0.60$ 60% 0.36$ Binders 5.00 2.20 2.80 30% 0.84 Portfolios 20.00 12.00 8.00 10% 0.80

2.00$

Fixed cost 100,000$

Desired profit 10,000$

Cost-Volume-Profit Models

$100,000 + 10,000$2.00/unit

= 55,000 units

ProductRelative

salesTotal sales

Units of product

CM per unit Total CM

Folders 60% 55,000 33,000 0.60$ 19,800$ Binders 30% 55,000 16,500 2.80 46,200 Portfolios 10% 55,000 5,500 8.00 44,000

110,000$

Cost-Volume-Profit ModelsOperating leverage

Companies with relatively low variable costs per unit, but high fixed costs, experience greater swings in profitability with volume changes than do companies with high variable costs and low fixed costs

Operating leverage is a multiplier

%∆ in sales * operating leverage = %∆ in income

Cost-Volume-Profit Models

Operating leverage =Contribution marginOperating income

Company A Company BSales 1,000,000$ 1,000,000$ Variable costs 300,000 600,000 Contribution margin 700,000$ 400,000$ Fixed costs 600,000 300,000 Operating income 100,000$ 100,000$

Operating leverage 7.00 4.00

Cost-Volume-Profit ModelsA 10% increase in sales will result in a

70% increase in Company A’s income, but only a 40% increase in Company B’s

Company A Company BSales 1,100,000$ 1,100,000$ Variable costs 330,000 660,000 Contribution margin 770,000$ 440,000$ Fixed costs 600,000 300,000 Operating income 170,000$ 140,000$

New operating leverage 4.53 3.14

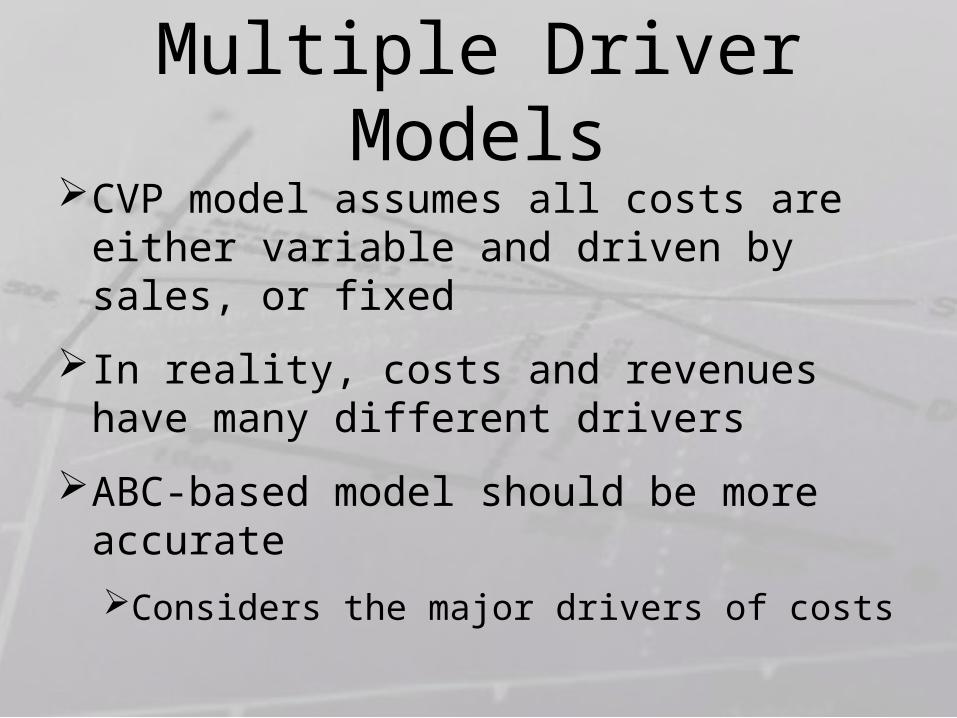

Multiple Driver ModelsCVP model assumes all costs are either

variable and driven by sales, or fixed

In reality, costs and revenues have many different drivers

ABC-based model should be more accurate

Considers the major drivers of costs

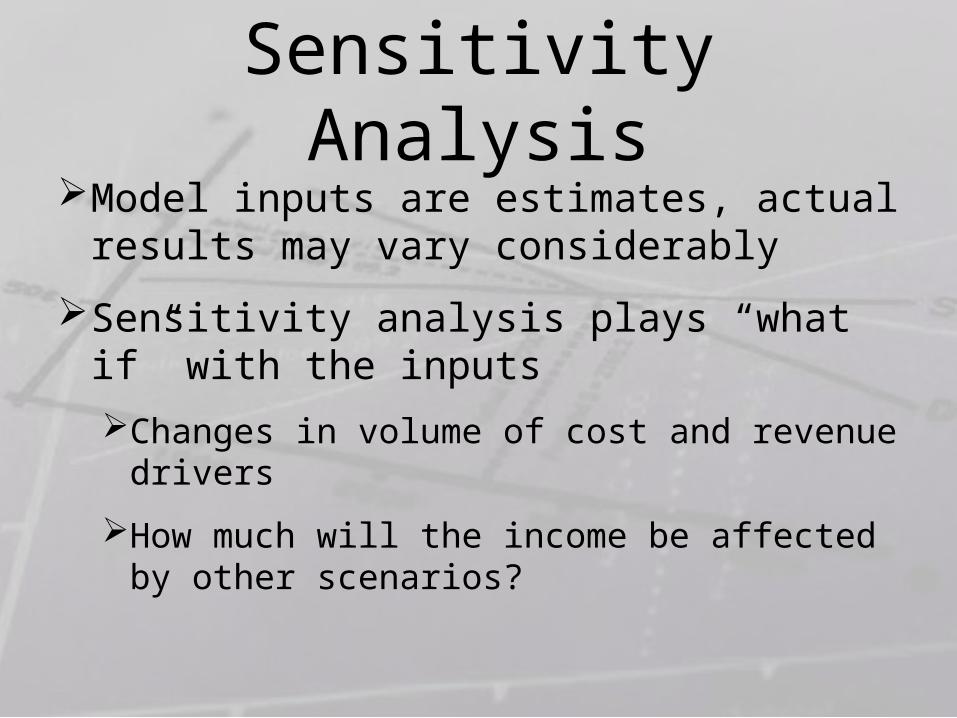

Sensitivity AnalysisModel inputs are estimates, actual results

may vary considerably

Sensitivity analysis plays “what if” with the inputs

Changes in volume of cost and revenue drivers

How much will the income be affected by other scenarios?

Theory of ConstraintsIdentification and best use of bottlenecks

Bottleneck is anything that prevents the company from producing and selling more

Process: machine capacity, available labor

Policy: no weekend or overtime work

Resource: shortage of materials

Market: not enough demand for product

Theory of Constraints

Product AProcess 1 Process 2 Process 3 Process 4

Product B Capacity: Capacity: Capacity: Capacity:12/hour 4/hour 6/hour 5/hour

Product C

Theory of ConstraintsStep 1: Identify appropriate value measure

Usually throughput

Step 2: Identify bottlenecks

Work piling up, unused capacity, etc.

Step 3: Optimize the bottleneck

What will produce the greatest value?

Theory of ConstraintsStep 4: Adjust process to bottleneck’s needs

Produce only what is needed by the bottleneck

Step 5: Alleviate the bottleneck

Add capacity, demand, etc.

Step 6: Repeat steps 1-5

Eliminating one bottleneck creates another

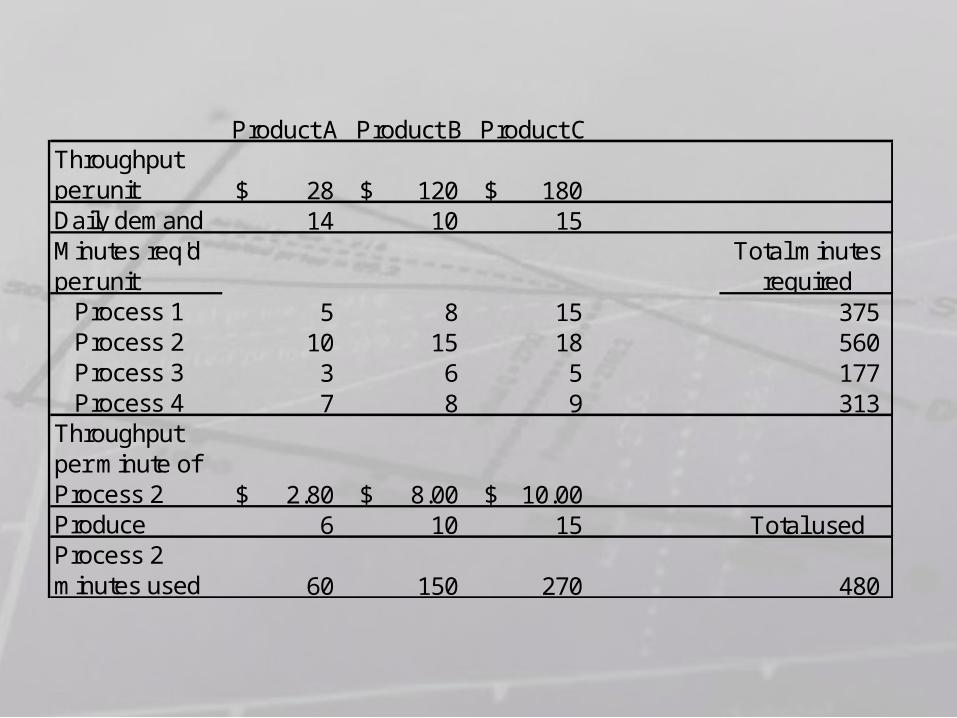

Product A Product B Product CThroughput per unit 28$ 120$ 180$ Daily demand 14 10 15 Minutes req'd per unit

Total minutes required

Process 1 5 8 15 375 Process 2 10 15 18 560 Process 3 3 6 5 177 Process 4 7 8 9 313 Throughput per minute of Process 2 2.80$ 8.00$ 10.00$ Produce 6 10 15 Total usedProcess 2 minutes used 60 150 270 480