Embed Size (px)

Citation preview

Financial Accounting, 5eFinancial Accounting, 5e

Prepared byKurt M. Hull, MBA CPA

California State University, Los Angeles

John Wiley & Sons, Inc.

Weygandt, Kieso, & Kimmel

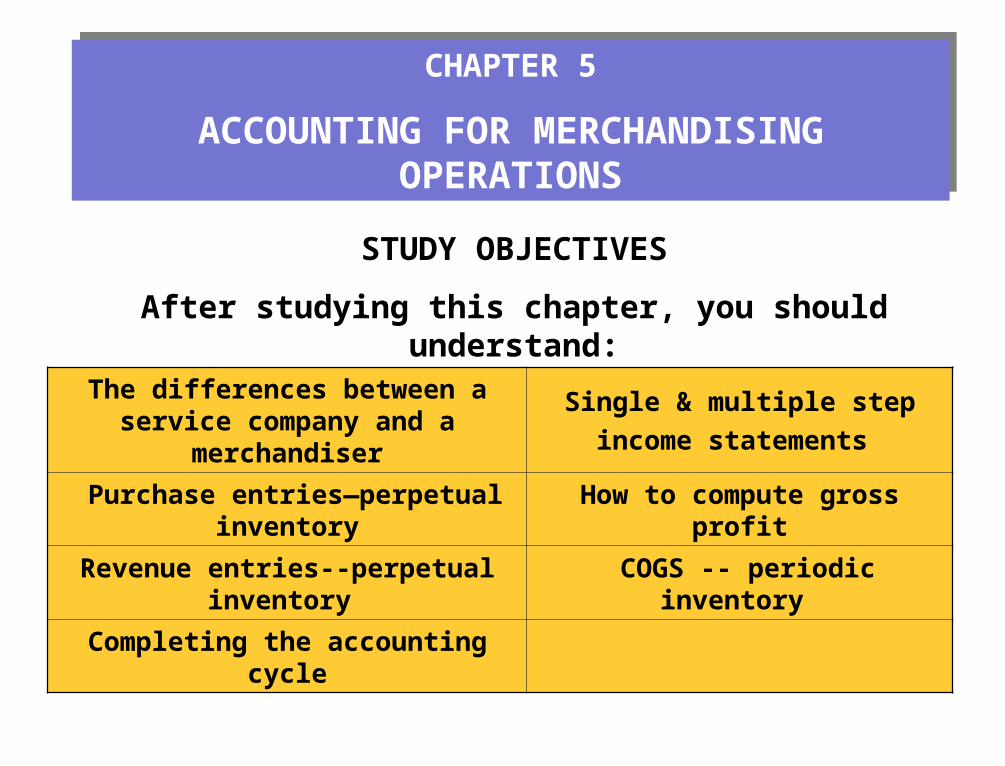

STUDY OBJECTIVES

After studying this chapter, you should understand:

CHAPTER 5

ACCOUNTING FOR MERCHANDISING OPERATIONS

CHAPTER 5

ACCOUNTING FOR MERCHANDISING OPERATIONS

The differences between a service company and a merchandiser

Single & multiple step

income statements

Purchase entries—perpetual inventory How to compute gross profit

Revenue entries--perpetual inventory COGS -- periodic inventory

Completing the accounting cycle

STUDY OBJECTIVE 1

MERCHANDISER VS. SERVICE COMPANY

STUDY OBJECTIVE 1

MERCHANDISER VS. SERVICE COMPANY

-

A service companyprovides a serviceto earn a profit.

No COGS

A merchandiserbuys and sells goods

to earn a profit.

Wholesalers/Retailers

COGS

Sales Revenue

Cost ofGoods Sold

Gross Profit

Operating Expenses

Net Income(Loss)

Less

Equals

Less

Equals

INCOME MEASUREMENT

MERCHANDISER

INCOME MEASUREMENT

MERCHANDISER

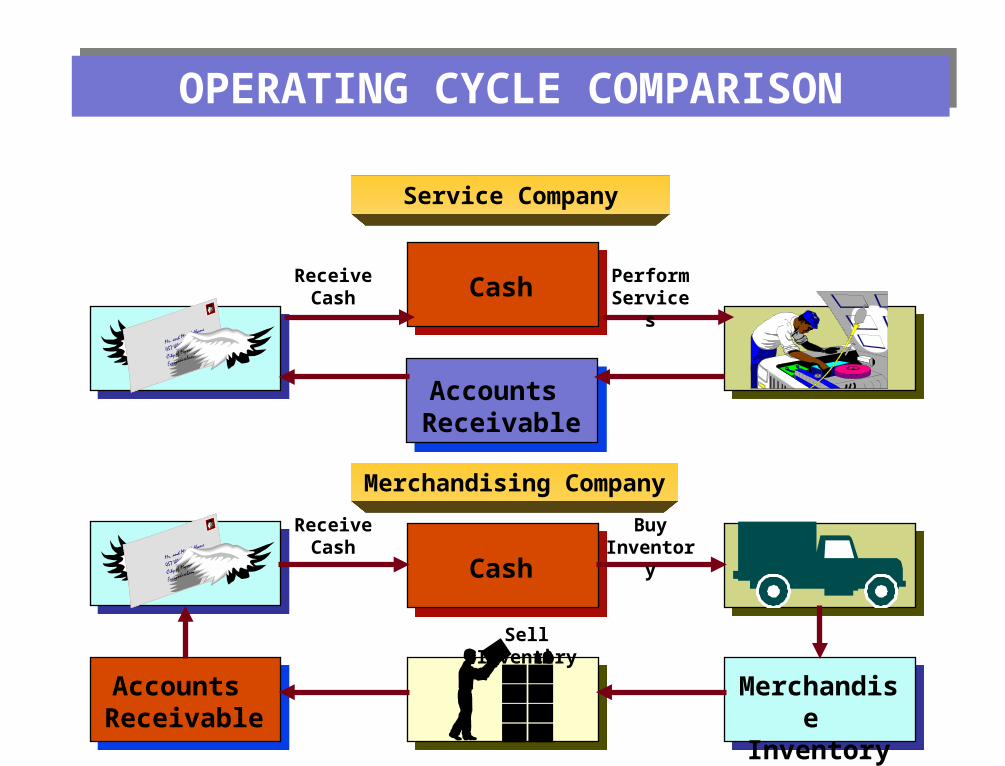

Accounts Receivable

Cash

Cash

Service Company

Merchandising Company

Accounts Receivable

Merchandise Inventory

Receive Cash

Perform Services

Receive Cash

Buy Inventory

Sell Inventory

OPERATING CYCLE COMPARISONOPERATING CYCLE COMPARISON

INVENTORY SYSTEMSINVENTORY SYSTEMS

PERPETUAL INVENTORY

Inventory purchased

Record purchase

Item sold

Record revenue & COGS

End of period

No entry

Inventory purchased

Record purchase

Item sold

Record revenue only

End of period

Computeand record

COGS

PERIODIC INVENTORY

SOLD

SOLD

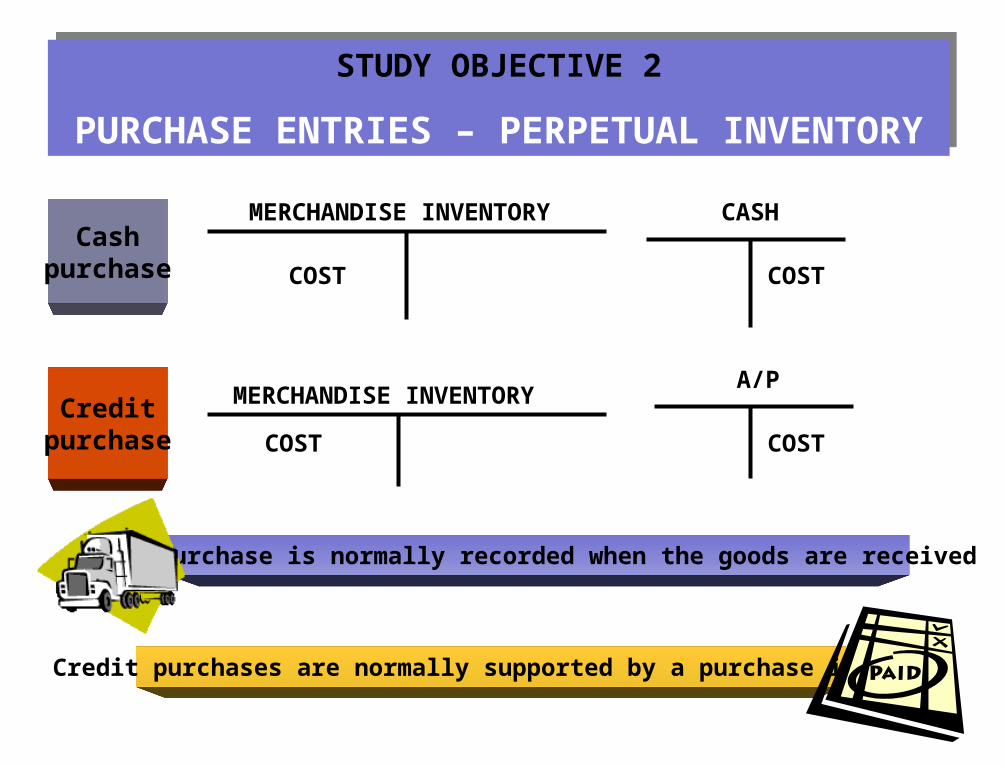

STUDY OBJECTIVE 2

PURCHASE ENTRIES – PERPETUAL INVENTORY

STUDY OBJECTIVE 2

PURCHASE ENTRIES – PERPETUAL INVENTORY

MERCHANDISE INVENTORY CASH

COST COST

MERCHANDISE INVENTORYA/P

COST COST

Cashpurchase

Creditpurchase

The purchase is normally recorded when the goods are received

Credit purchases are normally supported by a purchase invoice

3800 3800

STUDY OBJECTIVE 2

PURCHASE ENTRIES – PERPETUAL INVENTORY

STUDY OBJECTIVE 2

PURCHASE ENTRIES – PERPETUAL INVENTORY

3800 3 800

Cashpurchase

Creditpurchase

FOB SHIPPING POINT FOB DESTINATION

Title transfers to buyer at sellers shipping dock

Buyer pays freight costs

Title transfers to buyer at buyers receiving dock

Seller pays freight costs

SHIPPING TERMS – FREE ON BOARDSHIPPING TERMS – FREE ON BOARD

Freight costs are part of the cost of inventory purchased.Freight costs are part of the cost of inventory purchased.

GENERAL JOURNALDate Account Titles and Explanation Dr. Cr.

May 6 Merchandise Inventory Cash

(To record payment of freight, terms FOB shipping point)

150150

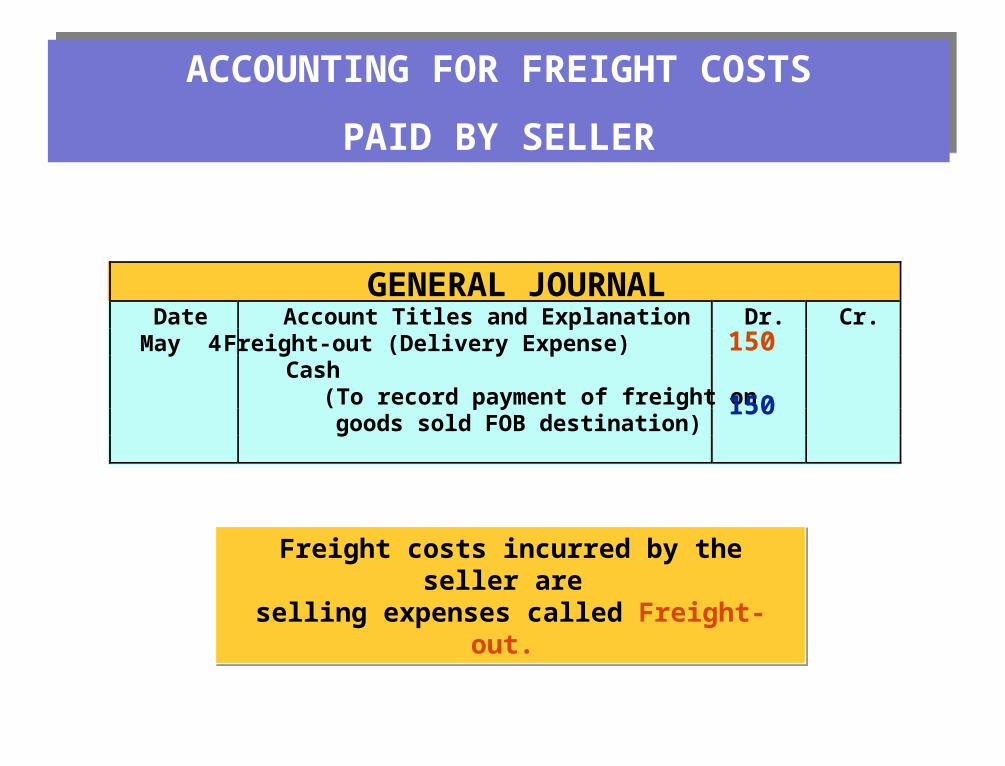

ACCOUNTING FOR FREIGHT COSTS

PAID BY BUYER

ACCOUNTING FOR FREIGHT COSTS

PAID BY BUYER

Freight costs incurred by the seller are selling expenses called Freight-out.

Freight costs incurred by the seller are selling expenses called Freight-out.

GENERAL JOURNALDate Account Titles and Explanation Dr. Cr.

May 4 Freight-out (Delivery Expense) Cash

(To record payment of freight on goods sold FOB destination)

150150

ACCOUNTING FOR FREIGHT COSTS

PAID BY SELLER

ACCOUNTING FOR FREIGHT COSTS

PAID BY SELLER

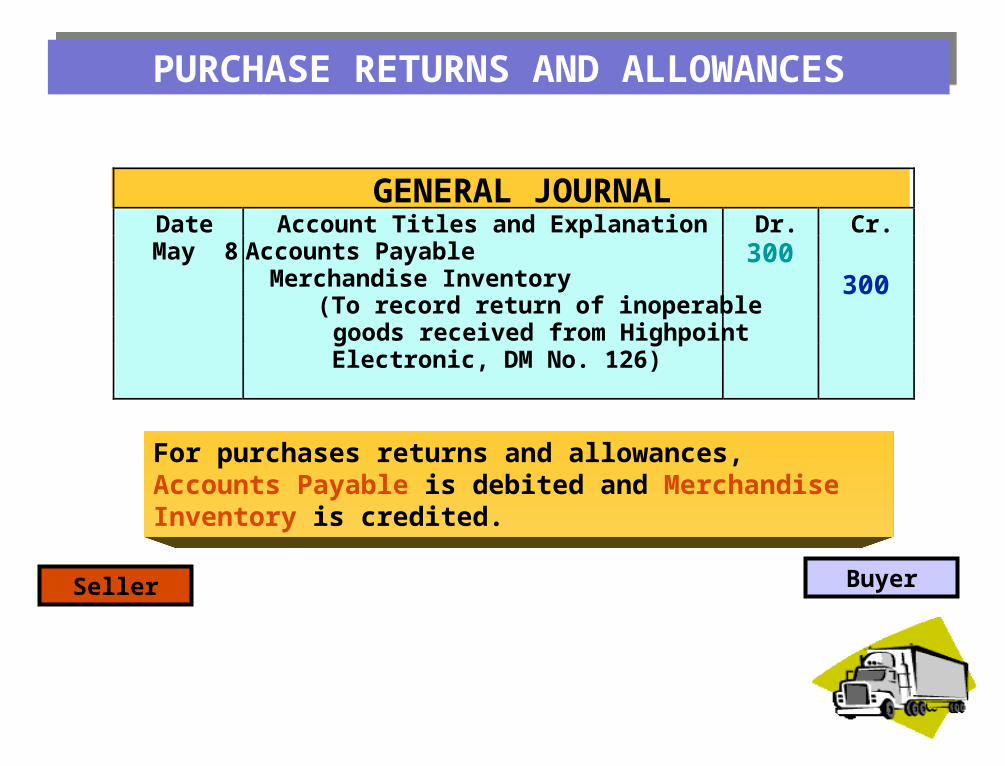

For purchases returns and allowances, Accounts Payable is debited and Merchandise Inventory is credited.

GENERAL JOURNALDate Account Titles and Explanation Dr. Cr.

May 8 Accounts Payable Merchandise Inventory (To record return of inoperable goods received from Highpoint Electronic, DM No. 126)

300300

PURCHASE RETURNS AND ALLOWANCESPURCHASE RETURNS AND ALLOWANCES

Seller Buyer

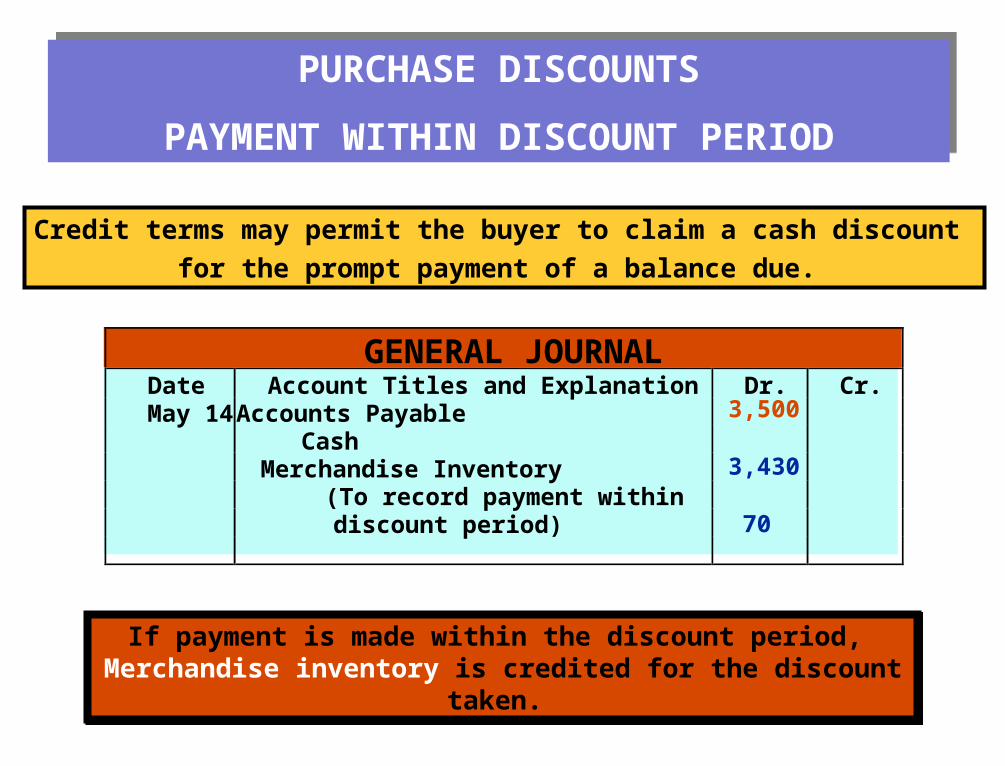

If payment is made within the discount period, Merchandise inventory is credited for the discount taken.

If payment is made within the discount period, Merchandise inventory is credited for the discount taken.

GENERAL JOURNALDate Account Titles and Explanation Dr. Cr.

May 14 Accounts Payable Cash Merchandise Inventory (To record payment within discount period)

3,5003,430 70

Credit terms may permit the buyer to claim a cash discount

for the prompt payment of a balance due.

PURCHASE DISCOUNTS

PAYMENT WITHIN DISCOUNT PERIOD

PURCHASE DISCOUNTS

PAYMENT WITHIN DISCOUNT PERIOD

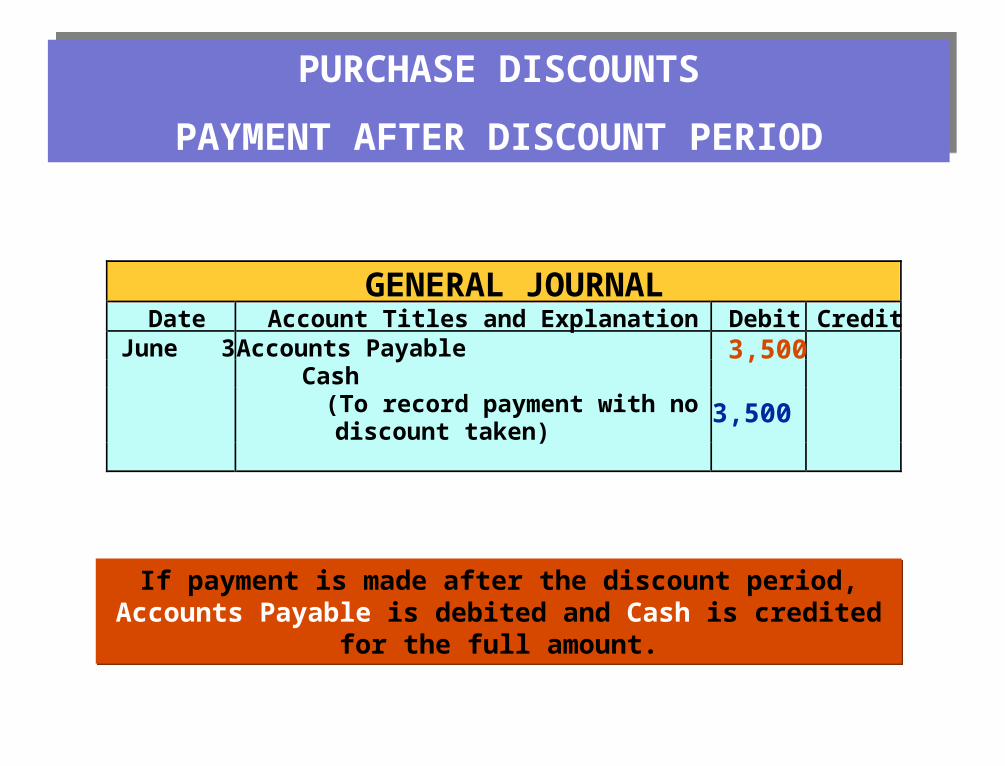

If payment is made after the discount period, Accounts Payable is debited and Cash is credited for the full amount.

If payment is made after the discount period, Accounts Payable is debited and Cash is credited for the full amount.

GENERAL JOURNALDate Account Titles and Explanation Debit Credit

June 3 Accounts Payable Cash (To record payment with no discount taken)

3,5003,500

PURCHASE DISCOUNTS

PAYMENT AFTER DISCOUNT PERIOD

PURCHASE DISCOUNTS

PAYMENT AFTER DISCOUNT PERIOD

STUDY OBJECTIVE 3

REVENUE ENTRIES – PERPETUAL INVENTORY

STUDY OBJECTIVE 3

REVENUE ENTRIES – PERPETUAL INVENTORY

Revenues are reported when earned in accordance with the revenue recognition principle.

All sales should be supported by a

cash register tape or sales invoice.

In a merchandising company,

revenues are earned

when the goods are

transferred from seller to buyer.

For cash sales, simply replace the debit to accounts receivable with a debit to cash.

GENERAL JOURNALDate Account Titles and Explanation Dr. Cr.

May 4 Accounts Receivable Sales (To record credit sales to Chelsea Video per invoice #731)

4 Cost of Goods Sold Merchandise Inventory (To record cost of merchandise sold on invoice #731 to Chelsea Video)

3,8003,800

2,4002,400

REVENUE ENTRIES – PERPETUAL INVENTORYREVENUE ENTRIES – PERPETUAL INVENTORY

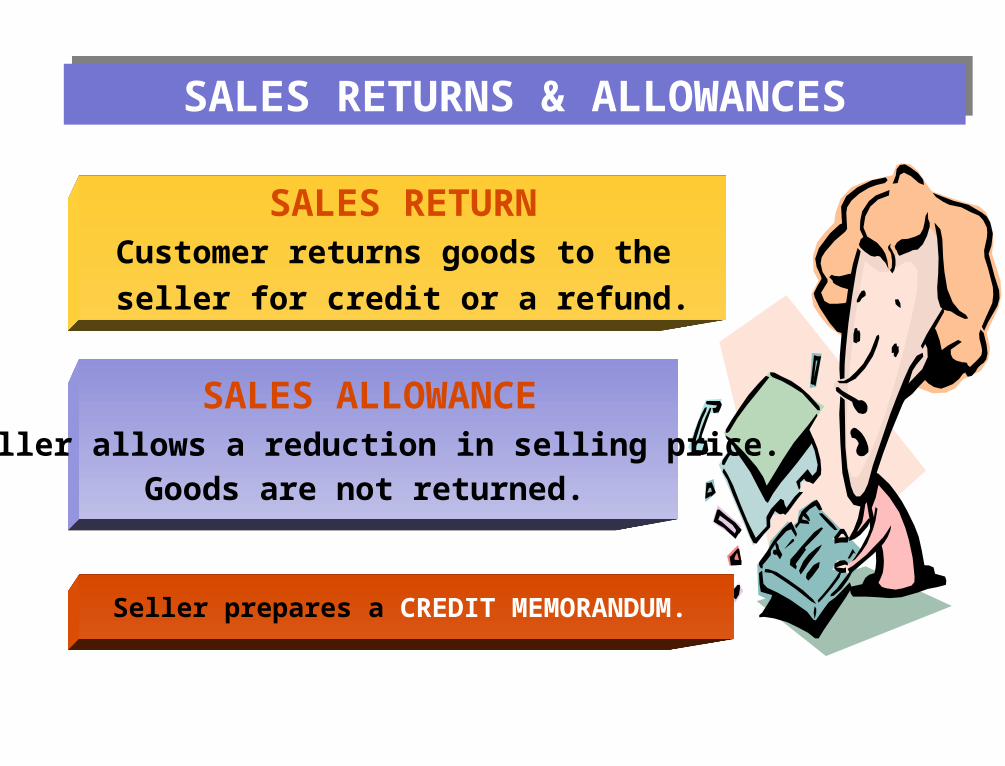

SALES RETURNS & ALLOWANCESSALES RETURNS & ALLOWANCES

SALES RETURNCustomer returns goods to the

seller for credit or a refund.

SALES ALLOWANCE

Seller allows a reduction in selling price.

Goods are not returned.

Seller prepares a CREDIT MEMORANDUM.

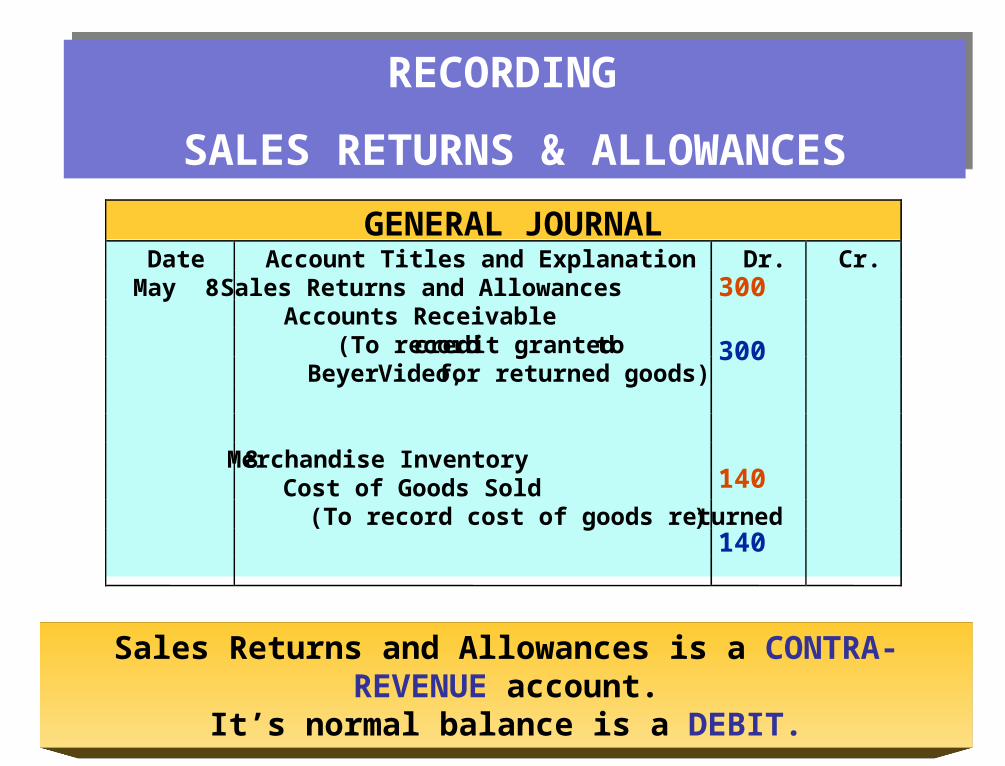

Sales Returns and Allowances is a CONTRA-REVENUE account.It’s normal balance is a DEBIT.

GENERAL JOURNAL

Date Account Titles and Explanation Dr. Cr. May 8 Sales Returns and Allowances Accounts Receivable (To record credit granted to Beyer Video, for returned goods) 8 Merchandise Inventory Cost of Goods Sold (To record cost of goods returned)

300300

140140

RECORDING

SALES RETURNS & ALLOWANCES

RECORDING

SALES RETURNS & ALLOWANCES

2/10, n/30 A 2% discount may be taken if payment is made within 10 days of the invoice date.

1/10 EOM A 1% discount is available if payment is made by the 10th of the next month.

SALES DISCOUNTSSALES DISCOUNTS

Seller offers customer a cash discount

for prompt payment of balance due.

Credit terms indicate the discount percent, Discount period, and final due date.

Sales discounts is a CONTRA-REVENUE ACCOUNT. It’s normal balance is a DEBIT.

GENERAL JOURNALDate Account Titles and Explanation Dr. Cr.

May 14 CashSales Discounts Accounts Receivable (To record collection within 2/10,

n/30 discount period from Beyer Video)

3,430 70

3,500

RECORDING

SALES DISCOUNTS

RECORDING

SALES DISCOUNTS

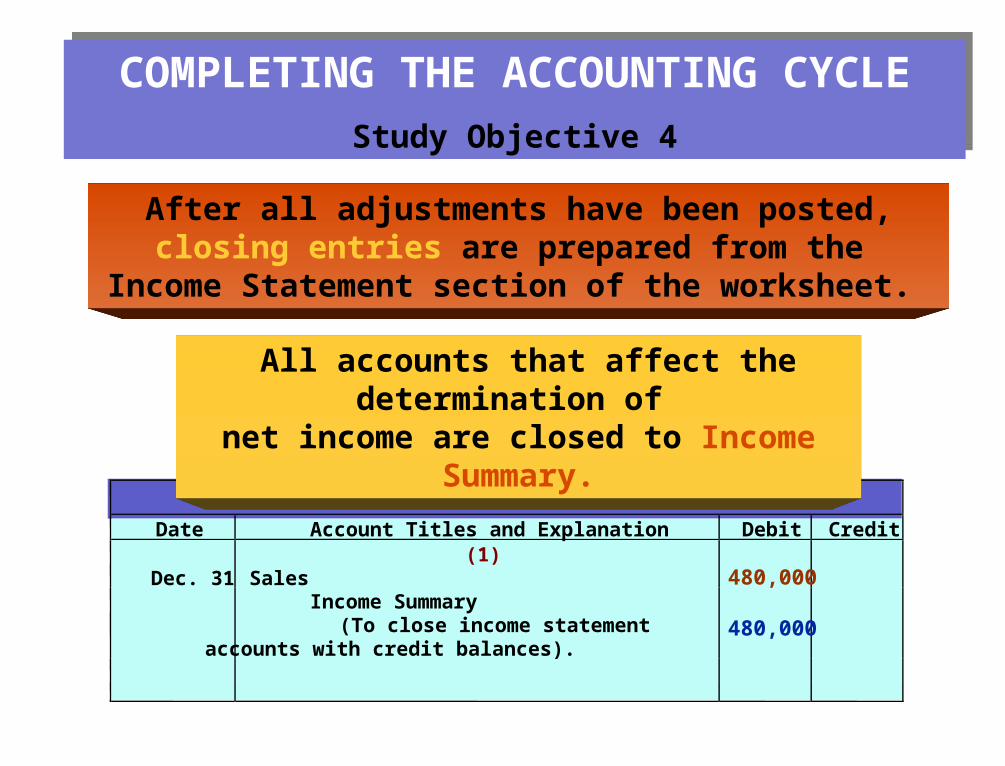

After all adjustments have been posted, closing entries are prepared from the

Income Statement section of the worksheet.

GENERAL JOURNAL

Date Account Titles and Explanation Debit Credit (1) Dec. 31 Sales Income Summary (To close income statement

accounts with credit balances).

480,000480,000

COMPLETING THE ACCOUNTING CYCLE

Study Objective 4

COMPLETING THE ACCOUNTING CYCLE

Study Objective 4

All accounts that affect the determination of net income are closed to Income Summary.

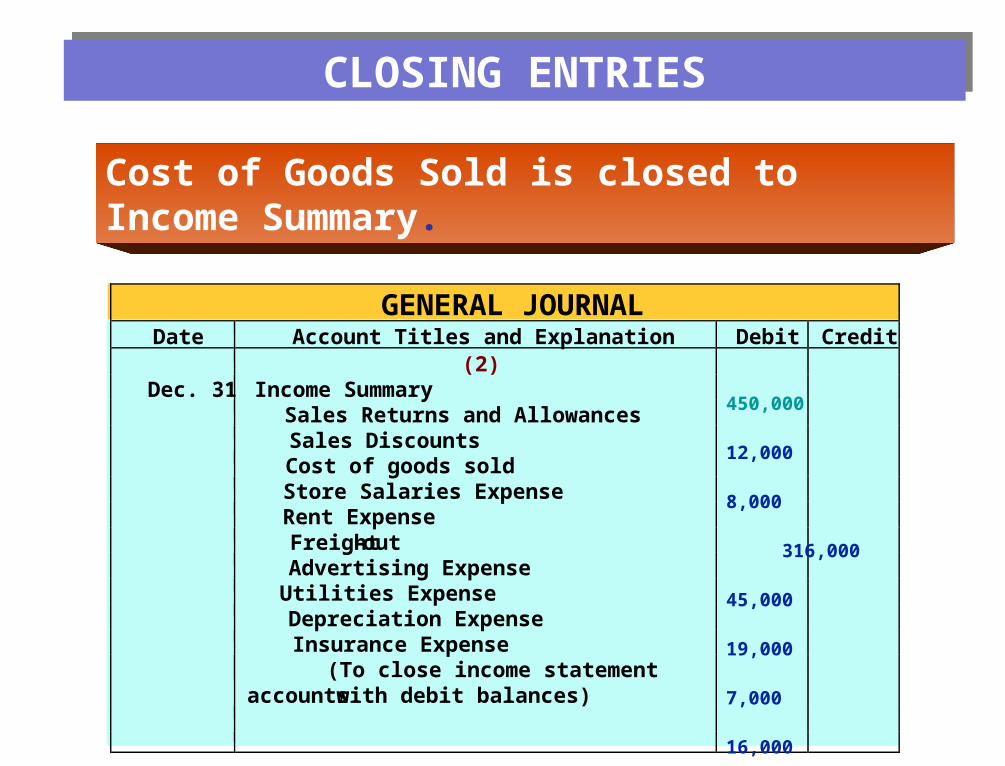

Cost of Goods Sold is closed to Income Summary.

GENERAL JOURNAL

Date Account Titles and Explanation Debit Credit (2) Dec. 31 Income Summary Sales Returns and Allowances Sales Discounts Cost of goods sold Store Salaries Expense Rent Expense Freight -out Advertising Expense Utilities Expense Depreciation Expense Insurance Expense (To close income statement

accounts with debit balances)

450,00012,000 8,000

316,00045,00019,000 7,00016,00017,000 8,000 2,000

CLOSING ENTRIESCLOSING ENTRIES

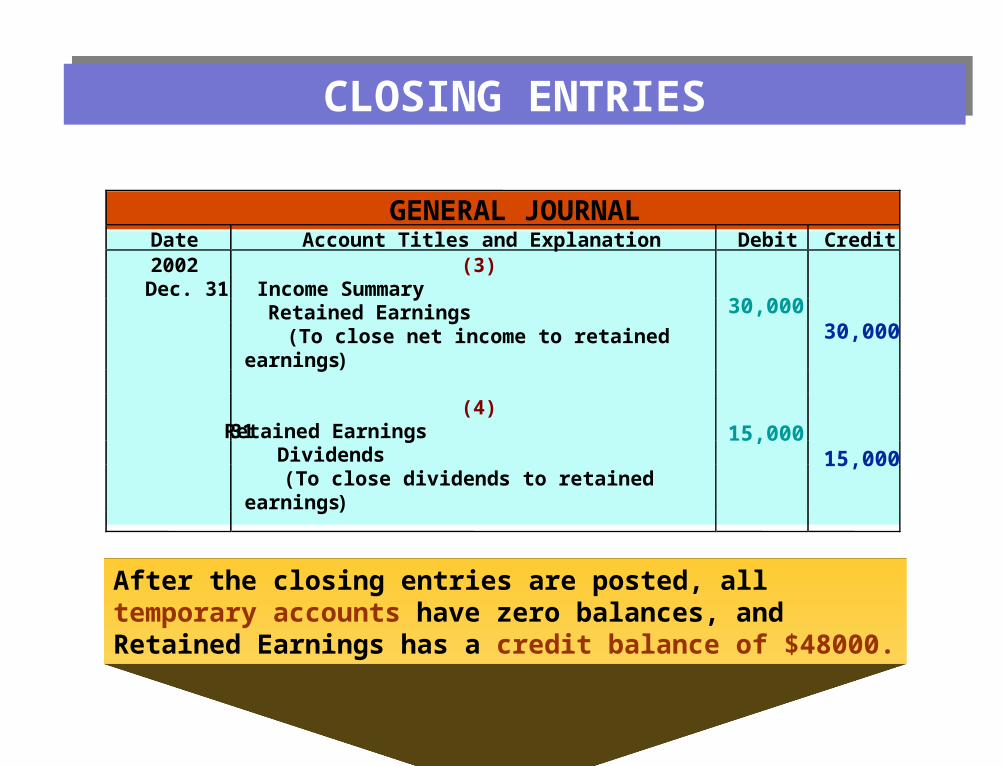

After the closing entries are posted, all temporary accounts have zero balances, and Retained Earnings has a credit balance of $48000.

GENERAL JOURNAL

Date Account Titles and Explanation Debit Credit 2002 (3) Dec. 31 Income Summary Retained Earnings (To close net income to retained

earnings )

(4) 31 Retained Earnings Dividends (To close dividends to retained

earnings )

30,00030,000

15,00015,000

CLOSING ENTRIESCLOSING ENTRIES

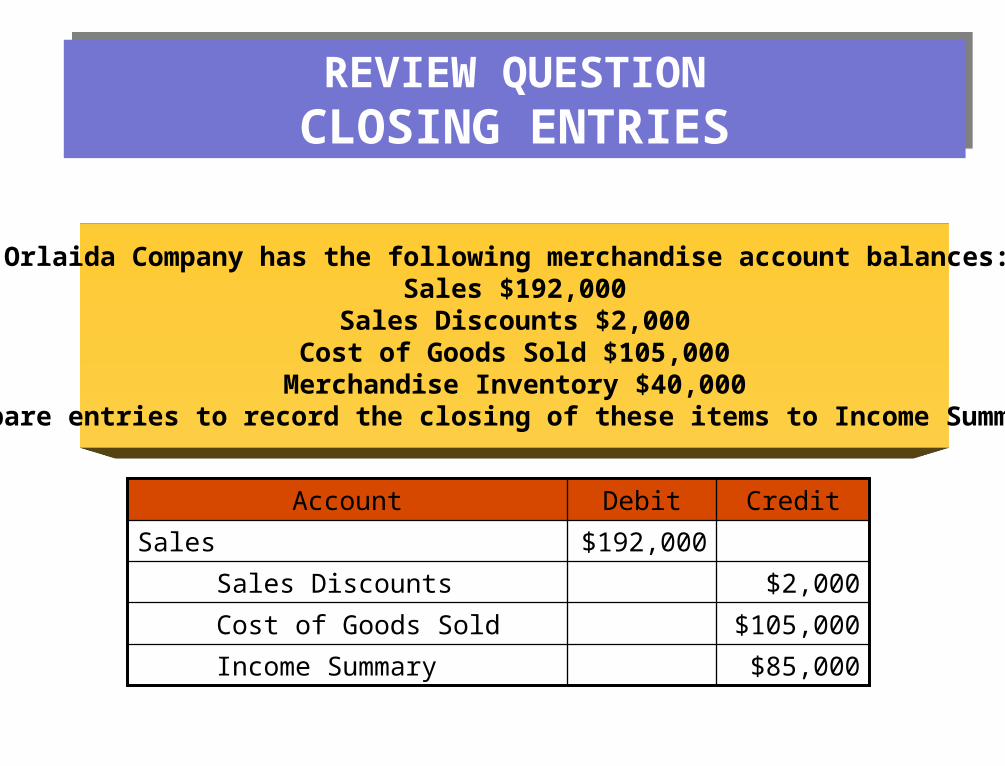

REVIEW QUESTIONCLOSING ENTRIESREVIEW QUESTION

CLOSING ENTRIES

Orlaida Company has the following merchandise account balances: Sales $192,000

Sales Discounts $2,000Cost of Goods Sold $105,000

Merchandise Inventory $40,000Prepare entries to record the closing of these items to Income Summary.

$85,000 Income Summary

$105,000 Cost of Goods Sold

$2,000 Sales Discounts

$192,000Sales

CreditDebitAccount

STUDY OBJECTIVE 5

MULTIPLE - STEP INCOME STATEMENT

STUDY OBJECTIVE 5

MULTIPLE - STEP INCOME STATEMENT

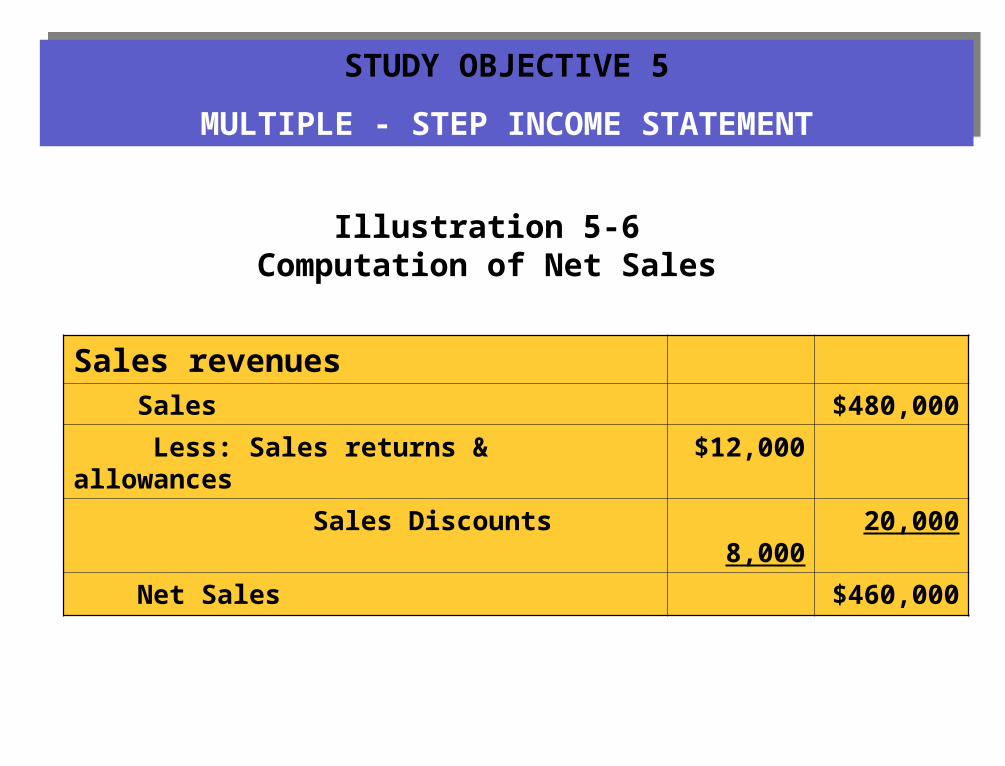

Sales revenues Sales $480,000

Less: Sales returns & allowances $12,000

Sales Discounts 8,000 20,000

Net Sales $460,000

Illustration 5-6Computation of Net Sales

STUDY OBJECTIVES 5 & 6

MULTIPLE - STEP INCOME STATEMENT

STUDY OBJECTIVES 5 & 6

MULTIPLE - STEP INCOME STATEMENT

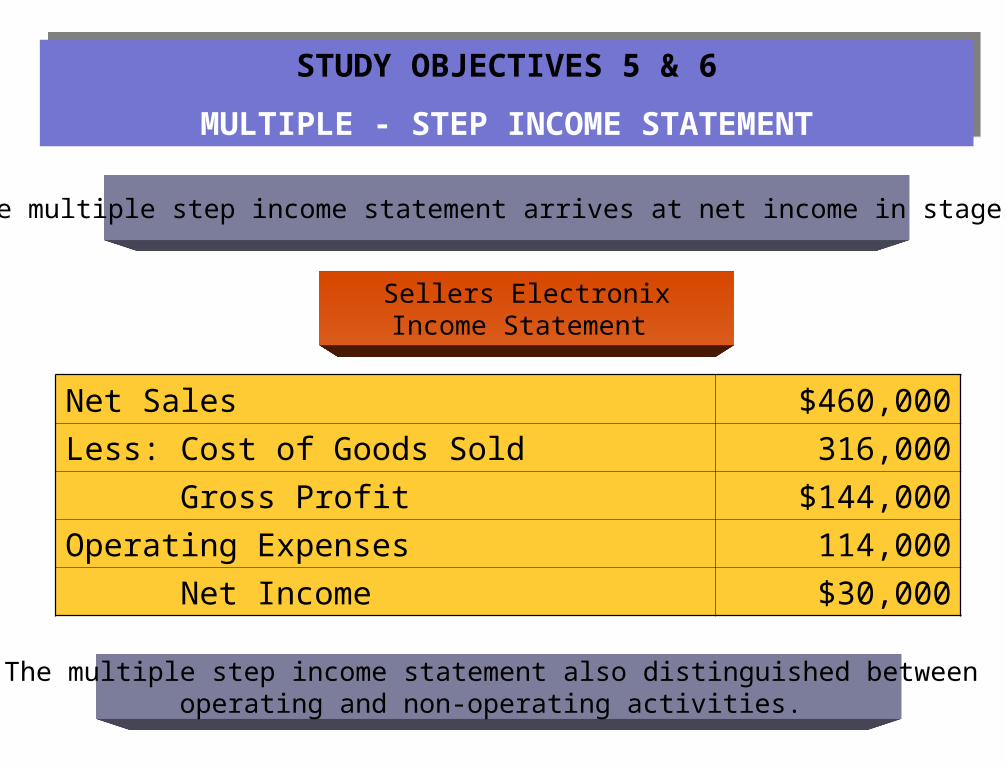

Net Sales $460,000

Less: Cost of Goods Sold 316,000

Gross Profit $144,000

Operating Expenses 114,000

Net Income $30,000

The multiple step income statement arrives at net income in stages.

Sellers ElectronixIncome Statement

The multiple step income statement also distinguished between operating and non-operating activities.

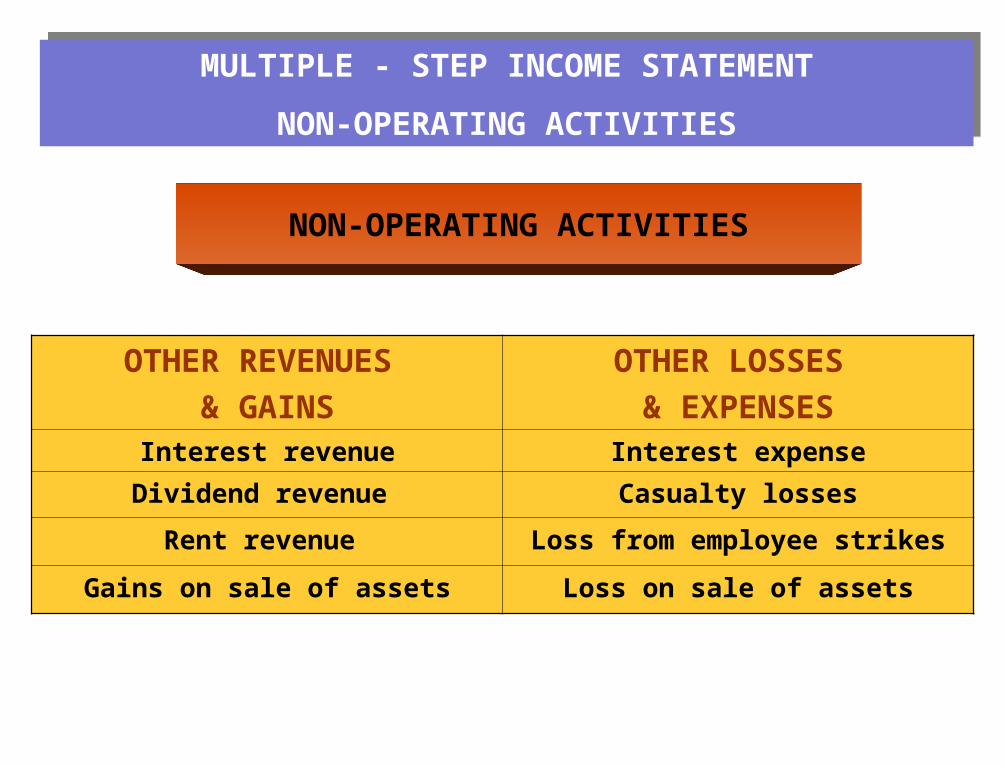

MULTIPLE - STEP INCOME STATEMENT

NON-OPERATING ACTIVITIES

MULTIPLE - STEP INCOME STATEMENT

NON-OPERATING ACTIVITIES

OTHER REVENUES

& GAINS

OTHER LOSSES

& EXPENSESInterest revenue Interest expense

Dividend revenue Casualty losses

Rent revenue Loss from employee strikes

Gains on sale of assets Loss on sale of assets

NON-OPERATING ACTIVITIES

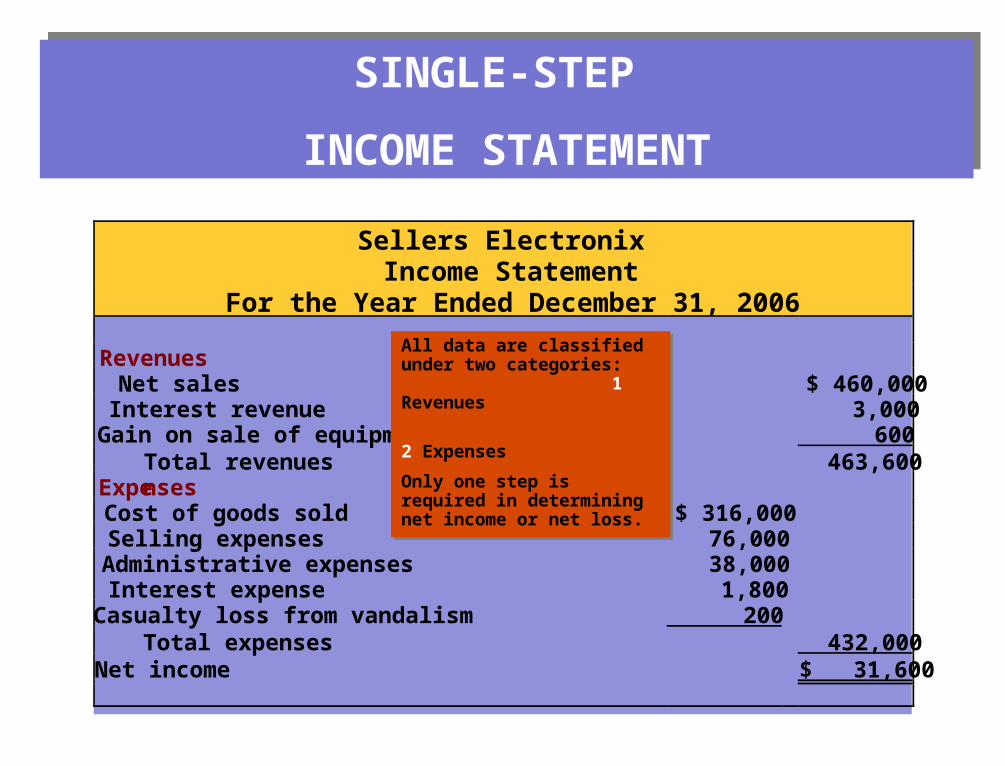

Sellers Electronix Income Statement For the Year Ended December 31, 2006

Revenues Net sales $ 460,000 Interest revenue 3,000 Gain on sale of equipment 600 Total revenues 463,600 Expenses Cost of goods sold $ 316,000 Selling expenses 76,000 Administrative expenses 38,000 Interest expense 1,800 Casualty loss from vandalism 200 Total expenses 432,000 Net income $ 31,600

All data are classified under two categories: 1 Revenues

2 Expenses

Only one step is required in determining net income or net loss.

All data are classified under two categories: 1 Revenues

2 Expenses

Only one step is required in determining net income or net loss.

SINGLE-STEP

INCOME STATEMENT

SINGLE-STEP

INCOME STATEMENT

STUDY OBJECTIVES 7

COST OF GOODS SOLD—PERIODIC INVENTORY

STUDY OBJECTIVES 7

COST OF GOODS SOLD—PERIODIC INVENTORY

Cost of Goods Sold

Inventory, January 1 $36,000

Purchases $325,000

Less: Purchase returns & allowances

$10,400

Purchase discounts 6,800 17,200

Net purchases 307,800

Add: Freight-in 12,200

Cost of Goods Purchased 320,000

Cost of Goods Available for Sale 356,000

Inventory, December 31 40,000

Cost of Goods Sold 316,000

Sellers ElectronixCost of Goods Sold

For the year ended December 31, 2006

COPYRIGHTCOPYRIGHT

Copyright © 2006 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written consent of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein.

Copyright © 2006 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written consent of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein.

CHAPTER 5 ACCOUNTING FOR MERCHANDISING OPERATIONS

CHAPTER 5 ACCOUNTING FOR MERCHANDISING OPERATIONS